received aug 31 2015 - sec.gov | home · john buono in the oip vs. john buono in the...

TRANSCRIPT

UNITED STATES OF AMERICA Before the

RECEIVED

AUG 31 2015 SECURITIES AND EXCHANGE COMMISSION

OFFICE OF THE SECRETARY

ADMINISTRATIVE PROCEEDING File No. 3-16293

In the Matter of

LAURIE BEBO, and JOHN BUONO, CPA

Res ondents.

RESPONDENT LAURIE BEBO'S REPLY TO THE DIVISION OF ENFORCEMENT'S POST-HEARING BRIEF

Mark A. Cameli [email protected] Ryan S. Stippich [email protected] Reinhart Boemer Van Deuren s.c. 1000 North Water Street Milwaukee, WI 53202 (414) 298-1000 Attorneys for Laurie A. Bebo

TABLE OF CONTENTS

INTRODUCTION ........................................................................................................................... 1

I. The Division of Enforcement's Post-Hearing Brief Willfully Ignores All of The Evidence That Undermines Its Case .................................................................................... 3

A. The Division does not even mention ALC's disclosure process, including the existence of ALC's Disclosure Committee, or explain how a fraud claim can exist when dozens of others, inside and outside of ALC, knew the Lease covenants were met using the employee leasing program and never recommended ALC change its disclosure ..................................................... .4

B. The Division ignores the fact that Grant Thornton's engagement partners discussed the inclusion of employees in the covenant calculations with the Audit Committee in 2009, 2010, and 2011 .............................................................. 9

C. The Division fails to acknowledge Milbank's investigation and conclusions that the use of employees in the covenant calculations was not concealed from the Board and Ventas could not deny that an agreement was reached ............................................................................................................ 12

D. In attempting to try a breach of contract case as Ventas' proxy, the Division fails to acknowledge that Ventas itself never pursued litigation related to the occupancy covenants or attempted to remove ALC from the properties ................................................................................................................ 14

II. Instead of Developing a Theory Based on the Actual Facts of the Case and the Evidence Elicited at the Hearing, the Division Continues to Pursue Its Predetermined Narrative, Supporting Its Case with "Facts" that Do Not Exist.. ............... 17

A. Much like its Pre-Hearing Brief, the Division's Post-Hearing Brief fills its predetermined narrative with broad assertions lacking evidentiary support ......... 19

B. Despite evidence to the contrary, the Division sticks to its predetermined narrative, asserting "facts" that do not exist or lack critical context.. .................... 23

1. The existence of an agreement with Ventas regarding the employee leasing program .......................................................................................... 23

2. Knowledge of the inclusion of employees,,fn the covenant calculations ............................................. "": ................................................ 28

(a) The Board was aware of the inclusion of employees in the covenant calculations ..................................................................... 28

32565777 1

(b) Ms. Bebo did not seek to conceal the employee leasing program from others, including Grant Thornton and Ventas ........ 34

3. The employee leasing process ................................................................... 39

4. The sale of ALC and the valuation of the Cara Vita Facilities .................. .46

III. In Contrast to the Consistent Testimony of Ms. Bebo, Many of the Division's Witnesses Lack Credibility ................................................................................................ 48

A. Laurie Bebo ............................................................................................................ 50

1. Many instances of the Division's "impeachment" were improper and did not constitute impeachment at all .................................................. 50

2. Ms. Bebo was consistent and credible over the course of thirty hours of hearing and forty-two hours of investigative testimony .............. 60

·B. John Buono ............................................................................................................ 62

1. John Buono in the OIP vs. John Buono in the Division's Post-Hearing Brief ............................................................................................. 62

2. Mr. Buono tried to help the Division, and undermined his own credibility ................................................................................................... 64

3. The Division has used Mr. Buono's newfound memories to advance inconsistent theories ..................................................................... 66

4. When Mr. Buono did not attempt to rewrite his story, he was credible, and his testimony was ignored by the Division .......................... 68

IV. The Division Has Failed To Establish Any Violation Of The Securities Laws ................ 70

32565777

A. The Division's Post-Hearing Brief sets forth no cognizable legal theory to support its securities fraud claim ........................................................................... 70

1.

2.

3.

The Division concedes that the challenged statements are statements of opinion rather than statements of fact, but fails to address the appropriate legal standard for evaluating its claims ................ 71

Omnicare's omission test does not apply, but if it did, Ms. Bebo has demonstrated that there was no omi§.sion and no duty to disclose the manner in which ALC waimeeting the covenants ................ 72

The few cases cited by the Division in its "legal analysis" provide no support for its fraud claim ..................................................................... 74

ii

4. The Division presented no credible evidence to support a finding of materiality .............................................................................................. 78

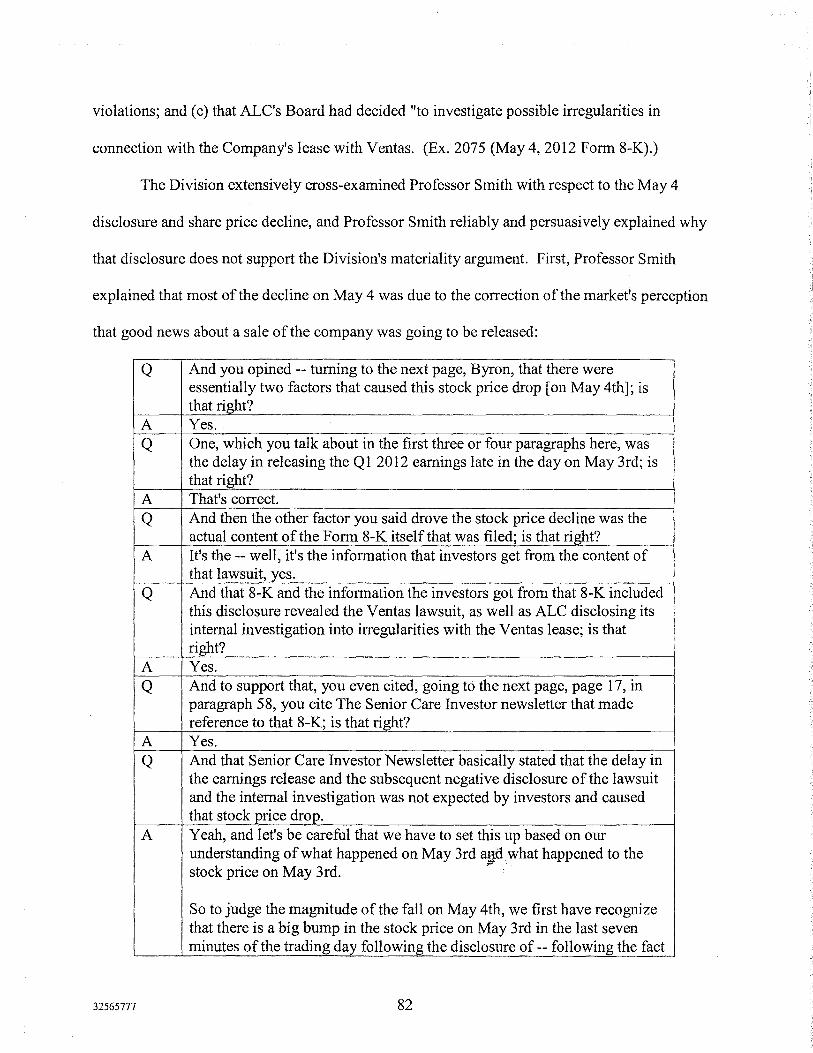

5. Professor Smith's unrebutted report and testimony is the best evidence on the issue of materiality, and conclusively establishes that the alleged misstatements were not material ...................................... 81

6. The Division's resort to so-called "scheme" liability cannot save its fraud claim ................................................................................................. 87

7. The Division failed to prove Ms.Bebo was reckless with respect to ALC's disclosures, much less that she did not subjectively believe the company was in compliance with the Lease ........................................ 89

B. There Is No Basis For The Division's Misleading The Auditors Claim ................ 92

C. The Division has failed to establish that Ms. Bebo violated the Exchange Act's books and records and internal controls provisions ...................................... 94

V. The Division has failed to establish that its requested remedies are available or appropriate here ................................................................................................................. 96

A. Disgorgement is not appropriate because Ms. Bebo did not obtain any "ill-gotten gains." ......................................................................................................... 96

B. Monetary penalties are not warranted in this case ............................................... 101

C. The Division's request for an officer and director bar should likewise be rejected ................................................................................................................. 105

D. Ms. Bebo should not be punished for contesting the Division's allegations ........ I 06

32565777 iii

TABLE OF AUTHORITIES

Cases

Asiana Airlines v. FAA, 134 F.3d 393 (D.C. Cir. 1998) ................................................................................................ 104

Aviva Partners, LLC v. Exide Techs., 2007 WL 789083 (D.N.J. Mar. 13, 2007) ................................................................................. 76

Dura Auto. Sys. of Ind., Inc. v. CTS Corp., 285 F.3d 609 (7th Cir. 2002) .................................................................................................... 79

Fail-Safe, L.L.C. v. A.O. Smith Corp., 744 F. Supp. 2d 870 (E.D. Wis. 2010) ...................................................................................... 79

Griffin v. Oceanic Contractors, Inc., 458 U.S. 564, 575 (1982) ........................................................................................................ 104

Herman & MacLean v. Huddleston, 459 U.S. 375 (1983) .................................................................................................................. 73

In re Almost Family, Inc. Sec. Litig., 2012 WL 443461 (W.D. Ky. Feb. 10, 2012) ............................................................................ 87

In re Credit Suisse First Bos. Corp., 431F.3d36 (1st Cir. 2005) ................................................................................................. 90, 92

In re Francis V. Lorenzo, Release No. 9762, 2015 WL 1927763 (Apr. 29, 2015) ............................................................ 88

In re John P. Flannery, Release No. 3981, 2014 WL 7145625 (Dec. 15, 2014) ............................................................ 88

In re Robert W Armstrong, Release No. 2264, 2005 WL 1498425 (June 24, 2005) ...................................................... 88, 89

In re Suprema Specialties, Inc. Sec. Litig., 334 F. Supp. 2d 637 (D.N.J. 2004) ........................................................................................... 76

In re Williams Sec. Litig., 339 F. Supp. 2d 1206 (N.D. Okla. 2003) .................................................................................. 77

In the Matter of Timbervest, LLC, Initial Decision Release No. 658, 2014 WL 4090371 (Aug. 20, 2014) .................................. 100

Loeffel Steel Prods., Inc. v. Delta Brands, Inc., 387 F. Supp. 2d 794 (N.D. Ill. 2005) ........................................................................................ 79

Meyer v. Greene, ·0' 710 F.3d 1189 (11th Cir. 2013) .......................................... }:: ................................................... 87

MHC Mutual Conversion Fund, L.P. v. Sandler O'Neill & Partners, L.P., 761F.3d1109 ................................................................................................................. 9, 71, 72

In re D VL Inc. Sec. Litig., 2010 WL 3522086 (E.D. Pa. Sept. 3, 2010) ............................................................................. 77

32565777 iv

Omnicare, Inc. v. Laborers Dist. Council Constr. Indus. Pension Fund, 135 S. Ct. 1318 (2015) ........................................................................................................ 72, 73

Pension Tr. Fund for Operating Eng'rs v. Assisted Living Concepts, Inc., 2013 WL 3154116 (E.D. Wis. June 21, 2013) .............................................................. 74, 75, 76

Podany v. Robertson Stephens, Inc., 318 F. Supp. 2d 146 (S.D.N.Y. 2004) ....................................................................................... 90

SEC v. Better Life Club of Am., Inc., 995 F. Supp. 167 (D.D.C. 1998) ............................................................................................... 96

SEC v. Black, 2009 WL 1181480 (N.D. Ill. Apr. 30, 2009) .................................................................... 99, 100

SEC v. Cohen, 2007 WL 1192438 (E.D. Mo. Apr. 19, 2007) ..................................................................... 97, 99

SEC v. Conaway, 2009 WL 902063 (E.D. Mich. Mar. 31, 2009) ............................................................... 100, 101

SEC v. Conaway, 695 F. Supp. 2d 534 (E.D. Mich. 2010) .................................................................................. 101

SEC v. Espuelas, 905 F. Supp. 2d 507 (S.D.N.Y. 2012) ....................................................................................... 93

SEC v. First City Fin. Corp., 890 F.2d 1215 (D.C. Cir. 1989) ................................................................................................ 96

SEC v. Ingoldsby, 1990 WL 120731 (D. Mass. May 15, 1990) ........................................................................... 107

SEC v. Jones, 476 F. Supp. 2d 374 (S.D.N.Y. 2007) ....................................................................................... 96

SEC v. Resnick, 604 F. Supp. 2d 773 (D. Md. 2009) .................................................................................... 96, 98

SECv. Todd, 2007 WL 1574756 (S.D. Cal. May 30, 2007) ........................................................................... 99

SECv. Todd, 642 F.3d 1207 (9th Cir. 2011) .................................................................................................. 93

SEC v. Johnson, 595 F. Supp. 2d 40 (D.D.C. 2009) .......................................................................................... 106

Target Mkt. Publ'g, Inc. v. ADVO, Inc., 136 F.3d 1139 (7th Cir. 1998) .................................................. ,. .............................................. 79

;J'

Tellabs, Inc. v. Makar Issues & Rights, Ltd., 551 U.S. 308 (2007) .................................................................................................................. 90

United States v. Reyes, 577 F.3d 1069 (9th Cir. 2009) .................................................................................................. 95

32565777 v

Victory Records, Inc. v. Virgin Records Am., Inc., 2011WL382743 (N.D. Ill. Feb. 3, 2011) ................................................................................ 79

Zaluski v. United American Healthcare Corp., 527 F.3d 564 (6th Cir. 2008) .................................................................................................... 73

Statutes

15 u.s.c. § 78j(b) ······································································································· 72, 73, 75, 88

15 U.S.C. § 78u-2(b)(3) .............................................................................................................. 102

Exchange Act§ 13(b)(2)(A) ......................................................................................................... 94

Exchange Act§ 13(b)(2)(B) ................................................................................................... 94, 95

Exchange Act§ 13(b)(5) ......................................................................................................... 94, 96

Other Authorities

SEC Release Notice No. 17500, 1981WL36385 (Jan. 29, 1981) ............................................... 95

Securities Act of 1933 ............................................................................................................. 72, 73

Tom C.W. Lin, Reasonable Investor(s), 95 B. U. L. Rev. 461, 466-68 (2015) ........................................................................................ 80

Rules

Federal Rule of Evidence 408 ............................................................................................... 75, 104

Federal Rules of Evidence 608(b) ................................................................................................. 50

Regulations

17 C.F.R. § 201.1004 .................................................................................................................. 102

17 C.F.R. § 240.1 Ob-5(a) .............................................................................................................. 88

17 C.F.R. § 240.lOb-5, Rule lOb-5 ......................................................................................... 87, 88

32565777 VI

Respondent Laurie A. Bebo, by and through her counsel, Reinhart Boemer

Van Deuren s.c., hereby respectfully submits this Reply to the Division of Enforcement's Post-

Hearing Brief and requests that the Court conclude that the claims set forth in the December 3,

2014 Order Instituting Proceedings ("OIP") filed by the Securities and Exchange Commission's

("SEC's" or the "Commission's") Division of Enforcement (the "Division") be dismissed in their

entirety.

INTRODUCTION

The Division's Post-Hearing Brief accentuates rather than dispels the fundamental legal

and factual flaws in its case. Reading the first thirty-nine pages of "facts" in the Division's brief,

one could scarcely tell that this is a securities fraud case involving alleged disclosure fraud.

Indeed, a discussion of ALC's Commission filings is limited to three short paragraphs. The

remainder is spent attempting, and failing, to prove a breach of contract action that ALC's

counter-party-Ventas-never asserted. And the great weight of the evidence at the hearing

further demonstrated that, by its inaction with respect to covenant violations, Ventas never would

have invoked the remedies under the Lease for a financial covenant default.

The Division's failure to discuss or deal with the undisputed facts related to ALC's

deliberative process with respect to the opinion asserted in its Commission filings that it was in

compliance with "certain operating and occupancy covenants" is telling of its inability to meet

the burden of proving a securities fraud claim here. That is because it is undisputed that dozens

of people between 2009 and 2012, who had roles in evaluating or approving ALC's periodic

filings and the challenged statement at issue here, were aware of the basic fact that ALC was

meeting the financial covenants through the use of rooms that the; Company paid for employees

to use. This included people internal at ALC, at Grant Thornton, at Quarles & Brady, and at

32565777 1

Milbank. None of them ever suggested that ALC needed to disclose the manner in which it was

meeting the Lease covenants or its disclosure misrepresented compliance.

Given the Division's position that the employee leasing arrangement was inherently

impermissible and had to be disclosed, this basic fact dooms the Division's claim, particularly

when the applicable legal standard requires it to prove not only that the challenged opinion was

not just objectively wrong, but unreasonable. The reasonableness of ALC's disclosure is

confirmed by Ms. Bebo's expert, the SEC's former Director of Corporate Finance, that additional

disclosures about the manner in which ALC was meeting the covenants was not required. The

Division never mentions Mr. Martin's opinion in its brief.

Moreover, the Division has utterly failed to address its inability to prove materiality.

Again, the basic facts established at the hearing were that ALC's investors did not think it was

important to know about how ALC was meeting the Lease covenants. The Division has no

answer for Professor Smith's well-founded and unrebutted opinion that demonstrates this

conclusively. Instead, the Division effectively acknowledges the appropriateness of his analysis

but stakes out a position unsupported by any evidence-that the share price decline on May 4,

2012 was related in any way to disclosure of financial covenant allegations. The Division's

scienter claim fares no better, as it is premised upon applying an improper standard and more

unsupported assertions and false narratives.

To remedy the obvious deficiencies in its case, the Division continues to resort to

mischaracterizations of the evidence and the record. Reasonable parties may differ about the

significance and meaning of evidence, and such advocacy is a 90re component of the adversarial

process. Fundamental to the Respondent's objection to the government's prosecution and, most

recently, its Post-Hearing Brief is the Division's mischaracterization of material evidence,

32565777 2

omission of evidence, reliance on "half-truths," and even statements that are contradicted by the

Division's own evidence and witnesses.

This is not proper advocacy and it is an impermissible tactic for any party to employ. But

it is especially troubling when it is advanced by the government-an institution particularly

duty-bound to the integrity of the evidence it proffers and the arguments it makes. (See

Respondent Laurie Bebo's Post-Hearing Brief at 6, n.4.)1 Abandoning these principles in a zeal

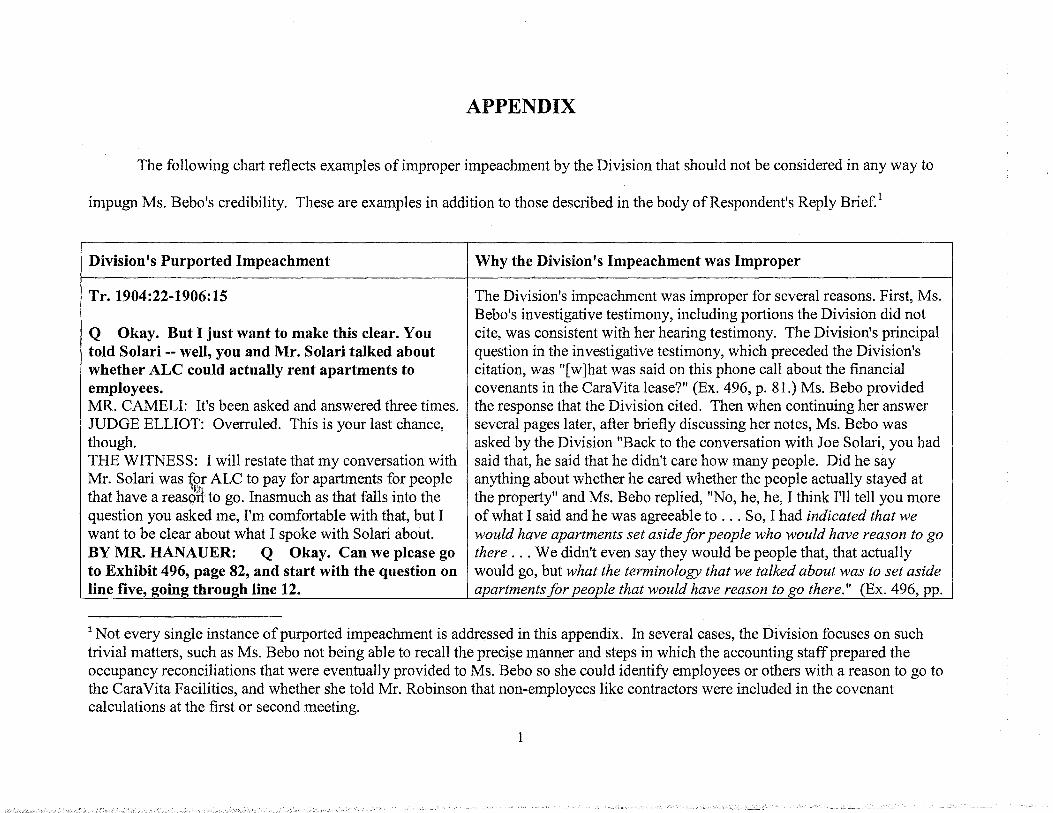

to "win," Respondent has been forced to devote inordinate resources to simply identify and

correct the Division's misstated "facts." For example, the Appendix and portions of this Brief

alone required over fifty pages devoted entirely to providing record cites disproving the

government's claimed "impeachment" of Ms. Bebo.

As set forth below and with greater detail, the Division's Post-Hearing Brief willfully

ignores the evidence that undermines its case as well as the void of evidence that prevents it from

meeting its burden of proof. Likewise, the Division has not established, as a matter oflaw, any

violation of securities laws. Finally, should this Court somehow find liability for any violation,

the Division's requested remedies contravene the legal standards and record evidence presented.

I. The Division of Enforcement's Post-Hearing Brief Willfully Ignores All of The Evidence That Undermines Its Case.

Notably absent from the Division's campaign to paint Ms. Bebo as a liar and a fraudster,

are the inconvenient facts that corroborate her testimony and support her defense. The Division's

Post-Hearing Brief does not discuss Grant Thornton's presentations to the Audit Committee

regarding the inclusion of employees in the covenant calculations in 2009-2011, Milbank's

investigation and conclusions regarding the employee leasing program, Mr. Solari's inability to

1 Ms. Bebo's initial Post-Hearing Brief will be cited throughout as "Resp't Br. at_." The Division of Enforcement's Post-Hearing Brief will be cited throughout as "Div. Br. at_." Citations to the record and other defined tenns utilized in the same manner as in Ms. Bebo's Post-Hearing Brief.

32565777 3

recall the substance of his important call with Ms. Bebo, Ventas' lack of action in response to

"learning" about the inclusion of employees in the covenant calculations, or even the existence of

ALC's Disclosure Committee or how the company evaluated (and approved) its disclosures. The

Division's inability to explain or otherwise address all of that evidence reveals the inherent

weakness of its case.

A. The Division does not even mention ALC's disclosure process, including the existence of ALC's Disclosure Committee, or explain how a fraud claim can exist when dozens of others, inside and outside of ALC, knew the Lease covenants were met using the employee leasing program and never recommended ALC change its disclosure.

In a case in which the Division pursues charges of disclosure fraud, it is baffling when its

post-hearing brief never once mentions the existence of a disclosure committee or the process by

which the company prepared and evaluated its disclosures. But, here, because ALC's Disclosure

Committee not only knew about the inclusion of employees in the covenant calculations, but

repeatedly approved the disclosure related to it (as did all other relevant parties), this evidence

does not support the Division's theory of the case, so it has simply been ignored.

The Division has not addressed who prepared the "boilerplate" statements at issue here,

why they were prepared, or the relative importance (or lack thereof) of the statement in ALC's

financial reporting process. (Smith, Tr. 3631 (describing the statement at issue here, based on

his extensive research, as "boilerplate language that's in a lot of 10-Ks of firms that have

financial covenants").) That is no doubt because the alleged false statement was specifically

reviewed and approved by Mr. Fonstad in the days immediately following the agreement with

Ventas approving the use of room rentals related to employees~jn the covenant calculations. And }fM

;/'

it was reviewed and approved by many other senior executives with critical roles in ALC's

financial reporting process-including the CFO, director of financial reporting, and internal

32565777 4

auditor-all with knowledge of all of the pertinent facts of ALC's covenant compliance

practices.

As noted in Ms. Bebo's Post-Hearing Brief, ALC had "extensive" policies and procedures

for meeting its financial and SEC reporting obligations besides the Disclosure Committee.

(Ex. 1655; Lucey, Tr. 3684-93.) Within those procedures, the Disclosure Committee's function

was to assist ALC in its disclosure obligations to investors. (Ex. 1919, p. 3; Fonstad,

Tr. 1567-68.) Specifically, the Disclosure Committee was tasked with identifying and reviewing

potential disclosure matters and making recommendations to the senior officers, like Ms. Bebo,

who were not members of the Committee. (Ex. 1919, p. 3; Fonstad, Tr. 1567-68; Buono,

Tr. 2445.)

ALC's Disclosure Committee--chaired by Eric Fonstad and Mary Zak Kowalczyk,

consecutively-was not only aware of the employee leasing program, but reviewed and

approved the disclosures related to compliance with the Ventas Lease covenants on a regular

basis. The Disclosure Committee knew about the employee leasing program from the outset.

On February 13, 2009-only eight days after Ms. Bebo forwarded to Mr. Fonstad a copy of her

e-mail to Mr. Solari and his response-the ALC Disclosure Committee met to discuss the

disclosures in ALC's 2008 annual report on Form 10-K. (Ex. 124.) During that meeting, the

minutes indicate Mr. Buono reported that "Ventas lease covenants continue to be monitored and

correspondence between ALC and Ventas has occurred whereby the covenant calculations have

been clarified as to census." (Ex. 124, p. 3.) At every subsequent meeting in 2009 following the

February 13, 2009 meeting described above, the Disclosure Conpnittee discussed this same topic ;f'

in connection with the disclosure in ALC's SEC filings regarding compliance with the Lease, and

32565777 5

that same or similar language was included in the minutes. (See Resp't Br. at 119 (citing

exhibits).)

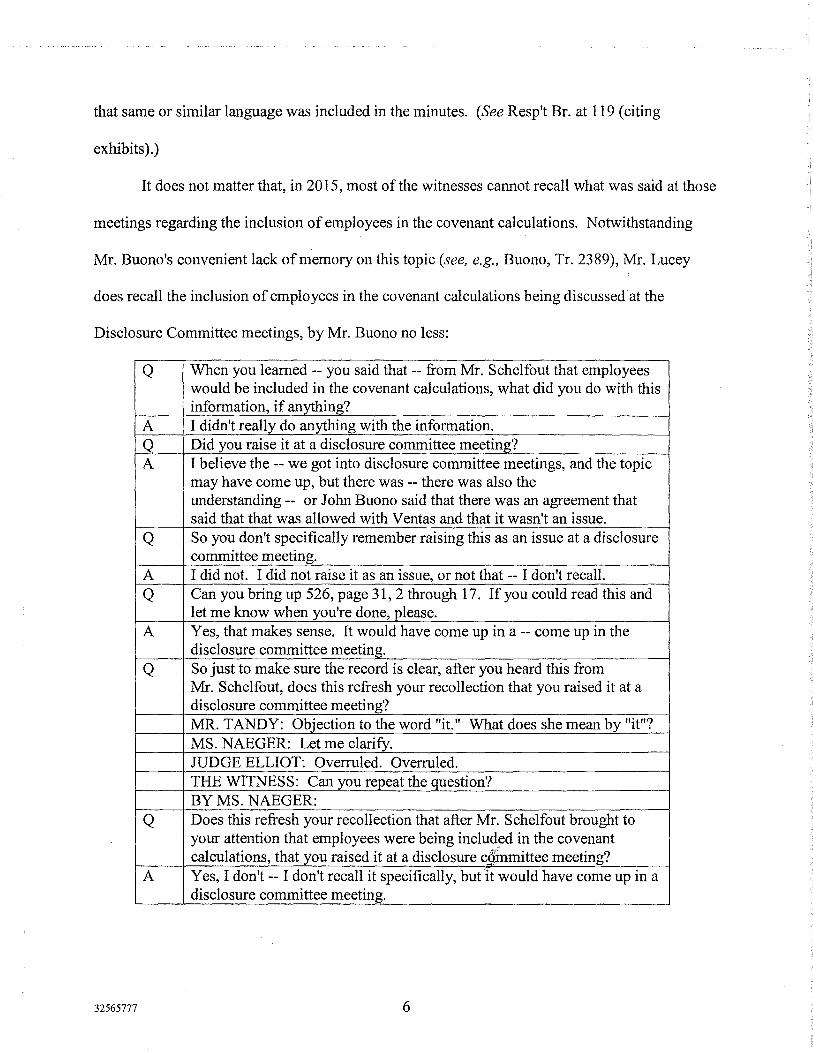

It does not matter that, in 2015, most of the witnesses cannot recall what was said at those

meetings regarding the inclusion of employees in the covenant calculations. Notwithstanding

Mr. Buono's convenient lack of memory on this topic (see, e.g., Buono, Tr. 2389), Mr. Lucey

does recall the inclusion of employees in the covenant calculations being discussed at the

Disclosure Committee meetings, by Mr. Buono no less:

Q When you learned -- you said that -- from Mr. Schelfout that employees would be included in the covenant calculations, what did you do with this information, if anything?

A I didn't really do anything with the information.

Q Did you raise it at a disclosure committee meeting? A I believe the -- we got into disclosure committee meetings, and the topic

may have come up, but there was -- there was also the understanding -- or John Buono said that there was an agreement that said that that was allowed with Ventas and that it wasn't an issue.

Q So you don't specifically remember raising this as an issue at a disclosure committee meeting.

A I did not. I did not raise it as an issue, or not that -- I don't recall. Q Can you bring up 526, page 31, 2 through 17. If you could read this and

let me know when you're done, please. A Yes, that makes sense. It would have come up in a -- come up in the

disclosure committee meeting.

Q So just to make sure the record is clear, after you heard this from Mr. Schelfout, does this refresh your recollection that you raised it at a disclosure committee meeting? MR. TANDY: Objection to the word "it." What does she mean by "it"? MS. NAEGER: Let me clarify. JUDGE ELLIOT: Overruled. Overruled. THE WITNESS: Can you repeat the question? BY MS. NAEGER:

Q Does this refresh your recollection that after Mr. Schelfout brought to your attention that employees were being includ,ed in the covenant calculations, that you raised it at a disclosure committee meeting?

A Yes, I don't -- I don't recall it specifically, but it would have come up in a disclosure committee meeting.

32565777 6

(Lucey, Tr. 3699-3700.) And the truth is, no one has any other rational explanation for what that

language-"correspondence between ALC and Ventas has occurred whereby the covenant

calculations have been clarified as to census"--could possibly mean or refer to, if not the Solari

email and the agreement reached with Ventas. In fact, Mr. Hokeness, who drafted the minutes,

testified that he was referring to the inclusion of employees in the occupancy covenant

calculations when he wrote "the covenant calculations have been clarified as to census."

(Hokeness, Tr. 3089-90.) And as Mr. Buono candidly admits, why else would ALC have

discussed the matter with Ventas in the first place if not for the purpose of compliance with the

covenants? (See Buono, Tr. 2492-96.)

But the vetting of the disclosures did not end with the Disclosure Committee, or with one

repeated conversation about the employee leasing program. In addition to review, analysis and

comment by the Disclosure Committee, which included ALC's in-house counsel, ALC also

provided copies of the draft filings to its external auditors, Grant Thornton, for review and

comment. (Koeppel, Tr. 3359-60.) And the disclosure at issue was vetted yet again in late 2011

after ALC received a comment letter from the SEC. No one-not the Disclosure Committee, the

Audit Committee, ALC's attorneys, nor ALC's auditors-suggested a different disclosure at any

point during that time. (See, e.g., Lucey, Tr. 3711; Koeppel, Tr. 3359-60; see Resp't Br. at 120

(citing testimony).) Of course, as outlined elsewhere in this Brief and in Ms. Bebo's Post

Hearing Brief, each of these groups of people was told that ALC was including employees in the

covenant calculations.

And although the Division disputes whether Ms. Bebo ~_;cussed the employee leasing

practice with lawyers at Quarles & Brady in connection with the comment letter response, it is

undisputed that in April 2012 securities counsel and litigation counsel at Quarles & Brady were

32565777 7

provided information (again) about the material facts surrounding ALC's use of employee

leasing to meet the Lease covenants. This included, for example, the fact that ALC was

including rooms for "70 to 90 employee/staff/other" in the occupancy covenants and revenue

derived from those rooms through intercompany transfers in the coverage ratio covenants.

(Resp't Br. at 149-50 (citing evidence); Lucey, Tr. 3719-21; Ex. 3683.) There is no evidence that

Quarles & Brady recommended that ALC modify its disclosures to include an explanation about

how it was meeting the occupancy and coverage ratio covenants.2 Indeed, draft press releases

about the Ventas lawsuit and 10-Qs prepared with Quarles' assistance in early May (prior to the

whistleblower letter) contained no additional disclosures with respect to how ALC was meeting

the financial covenants. (Id.; see also Bxs. 1070, 1070A, p. 2 (May 1, 2012 Quarles 8-K draft

stating: "The Notices or the failure by the Company to meet certain covenants in the Ventas

Lease with regard to occupancy and financial thresholds could result in Ventas invoking

remedies available to it under the Ventas Lease ... ").)

Similarly, as discussed in more detail below, lawyers at Milbank conducted an extensive

investigation of the issues this Court is reviewing-whether disclosures in ALC's periodic filings

were mis-stated with respect to compliance with the financial covenants. (See infra at 12-14;

Resp't Br. at 158-61.) Milbank concluded that ALC's filings were not mis-stated because the

determination it was in compliance with the covenants through the understanding reached with

Mr. Solari on the phone and confirmed through the February 4 e-mail was reasonable. (Id.)

Milbank reported its findings to Grant Thornton, who reached the same conclusion, given it

issued a clean opinion on ALC's internal controls for 2012 and did not recommend any re-

statement of ALC's financials. (Id.)

2 They did want to confirm that the employee-related occupancy and intercompany revenue reported to Ventas was excluded from the statistics in the 10-Q, which Mr. Lucey confirmed. (Resp't Br. at 149-50 (citing evidence); Lucey, Tr. 3719-21; Ex. 3683.)

32565777 8

In a case where the operative standard is not whether ALC was correct in reaching its

judgment that it was in compliance (though it was correct), but is whether that judgment was

reasonable, this evidence-all of which is ignored by the Division-is highly probative and

should dispose of the Division's fraud claim. See MHC Mutual Conversion Fund, L.P. v.

Sandler O'Neill & Partners, L.P., 761 F.3d 1109, 1118 (dismissing complaint because there is

"no authority suggesting that an issuer's opinion about the market prospects for securities held by

a company lacks a reasonable basis when multiple and independent expert analysts who study

the company's portfolio reach the same view").

B. The Division ignores the fact that Grant Thornton's engagement partners discussed the inclusion of employees in the covenant calculations with the Audit Committee in 2009, 2010, and 2011.

The evidence the Division will never be able to reconcile with its flawed theory that the

Board did not know about the employee leasing program until March 2012-and therefore

chooses to ignore-is the testimony of Jeff Robinson and Melissa Koeppel. In 2009, 2010, and

2011, the Grant Thornton engagement partners discussed the fact that ALC was including

employees in the covenant calculations with the Audit Committee while the other Board

members were present. No one was surprised. (See Resp't Br. at 123-26 (citing testimony).)

Mr. Robinson also informed the Board that ALC would fail the covenants without the inclusion

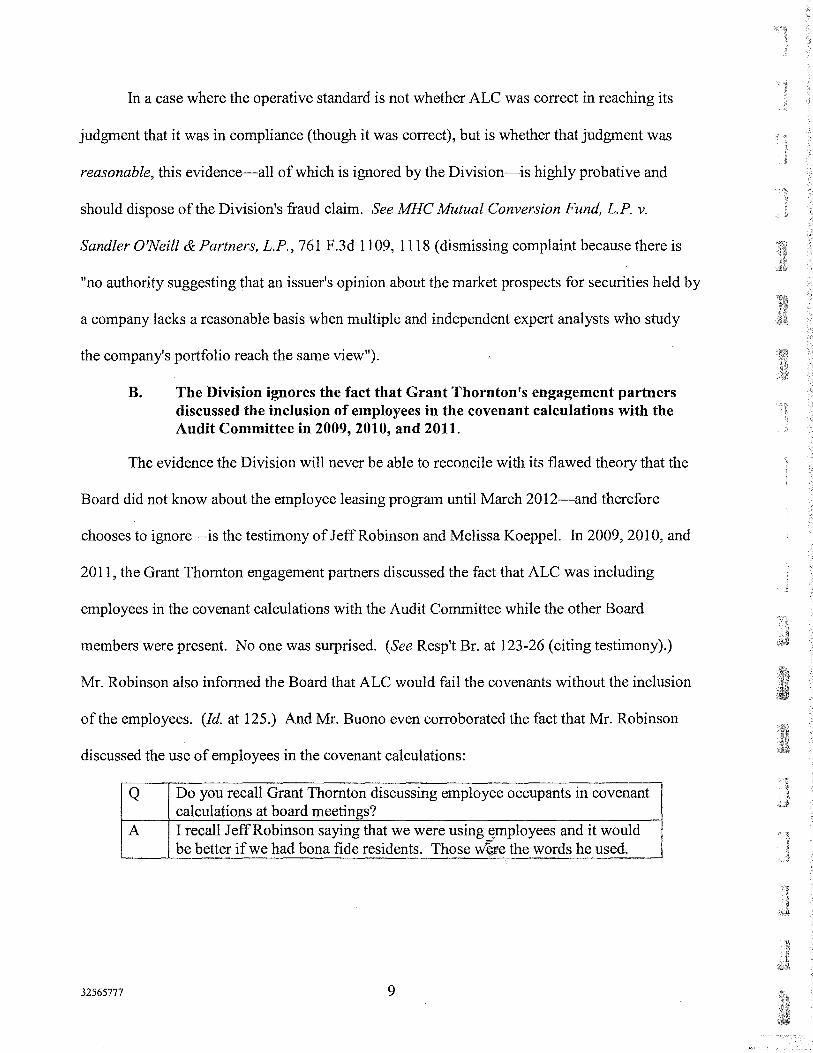

of the employees. (Id. at 125.) And Mr. Buono even corroborated the fact that Mr. Robinson

discussed the use of employees in the covenant calculations:

Q Do you recall Grant Thornton discussing employee occupants in covenant calculations at board meetings?

A I recall Jeff Robinson saying that we were using ~mployees and it would be better if we had bona fide residents. Those w~e the words he used.

32565777 9

(Buono, Tr. 2778.)3

Instead, the Division asserts that Ms. Koeppel and Mr. Robinson "dispute [Ms.] Bebo's

account that [Ms.] Bebo disclosed to the board that ALC was including employees in the

covenant calculations." (Div. Br. at 44.) This statement is troubling for at least two reasons:

(1) it is false; and (2) it ignores the fact that Ms. Koeppel and Mr. Robinson themselves

discussed the issue with the Board, during the Audit Committee meetings. Nowhere in the

testimony cited by the Division-3329:18-3330: 11, 3366:5-3368:17, 3430:11-3431 :6, 3496:4-

3497 :24--does either witness dispute that Ms. Bebo disclosed to the Board that ALC was

including employees in the covenant calculations. The testimony cited by the Division does not

mention anything about what Ms. Bebo did or did not present to the Board. And, in fact, the

cited testimony shows that Ms. Koeppel and Mr. Robinson did have discussions with the Board

on this topic. In attempting to shore up a false statement, the Division included a citation to

some of the very testimony it otherwise ignores:

Q Prior to March 2012, what, if any, discussions did you have with the board about ALC including employees in the covenant calculations?

A Are you asking about conversations with the board as a whole? Q Yeah, let's -- let's talk about just, yeah, at board meetings -- board or audit

committee meetings. A So we actually had a conversation with the audit committee during the

3 The Division's attempt to "rehabilitate" Mr. Buono, and get him back on board with their theory of the case, was nonsensical and demonstrates, yet again, how the Division was more interested in having Mr. Buono stay on script than having his testimony be credible or make sense:

BY MR. HANAUER: Q And do you remember making a statement about what Mr. Robinson said to the board

about something along the lines of not making any money off employees? A Yes. Q When he made that statement, did he say anything abounhe covenant calculations? A No. ~~

(Buono, Tr. 2784.) Mr. Buono did not say that Mr. Robinson said ALC was not making any money off employees. In response to a question about "employee occupants in covenant calculations," Mr. Buono testified that Mr. Robinson said ALC was "using employees and it would be better if we had bona fide residents." The meaning of Mr. Buono's testimony was clear, and the Division's leading suggestion to Mr. Buono that the covenant calculations were not discussed is beyond the pale.

32565777 10

closing of the first quarter review of 2011 regarding the existence of the practice of utilizing employees to fulfill the covenant calculations with those leases. That was an audit committee meeting. There were other members of the board that were in attendance at that audit committee meeting, as frequently happened.

Q Do you know whether all of the other board members were in attendance? A I don't remember if all of them were in attendance. Q And what -- what do you remember about that discussion with the audit

committee? A What I remember about the conversation was that we -- again, as I

mentioned, we did inform them that the company was utilizing these -- you know, the employee count for purposes of meeting the covenants and that it was our understanding that this was in accordance with an agreement that management had with Ventas.

(Robinson, Tr. 3430-31.) And the very next questions and answers in Mr. Robinson's

testimony-which the Division did not cite-indicate that the Board did not ask any questions or

appear surprised to hear about the utilization of employees to fulfill the covenant calculations:

Q At that time, did any of the board members ask you any questions about that?

A Not to my recollection. Q What, if any, impression did you get with respect to whether they knew

about this subject matter already? A The impression -- the impression I received in that meeting was that there

didn't seem to be any surprises when we told them that. So it confirmed my belief that they had been previously informed by our -- that they had been informed by our previous audit teams on this topic.

(Robinson, Tr. 3431.) Ms. Koeppel said the same thing in the two questions and answers

immediately following the testimony cited by the Division:

Q And did you get any questions from the board members about that? A No. Q What do you recall, if anything, about their reaction to your presentation

about this issue? A You know, that they were engaged in the convers1i.tion. You know, their

body language didn't express any surprise. In tafK:ing with them across the table, they seemed to kind of acknowledge it, and then we moved on to other subjects.

32565777 11

(Koeppel, Tr. 3330.) This testimony is far from disputing the fact that Ms. Bebo disclosed the

matter to the Board. To the contrary, it suggests that the Board was well aware of the practice

before Grant Thornton mentioned it because Ms. Bebo discussed it in detail with the Board, as

she testified at the hearing.

C. The Division fails to acknowledge Milbank's investigation and conclusions that the use of employees in the covenant calculations was not concealed from the Board and Ventas could not deny that an agreement was reached.

Despite the considerable evidence to the contrary, the Division continues to insist that

ALC's Board did not learn that employees were being included in the covenant calculations until

March 2012. In doing so, the Division ignores considerable evidence undermining its theory,

including the fact the Board hired Milbank to conduct an internal investigation into the employee

leasing program, which concluded the opposite. That is, Milbank quickly reached the conclusion

that allegations that it was concealed from the Board were incorrect. (See Ex. 3460, p. 2 (Grant

Thornton notes of call with Milbank: "Based on their initial discussions, they believe the

consideration that this practice was concealed from the Board is incorrect."); see also Robinson,

Tr. 3461-62 (confirming Milbank relayed that conclusion).)

And upon completing its investigation, Milbank came to a number of conclusions that are

in stark contrast to the picture that the Division is trying to paint of a clueless Board and an

impossible story of an agreement with Ventas:

• "No one including those spoken to at Ventas could testify that the Bebo employee leasing inclusion was not accurate." (Robinson, Tr. 3482; Ex. 1879, p. 5 (Milbank's conclusions reported to Grant Thornton).)

• Milbank informed Grant Thornton that the integritx,,-0f the CEO and CFO, among others, was not in question, and Milbank was not m a position to conclude that any representations made in the past were false. (Ex. 19i8, p. 2; Ex. 3455, p. 2.)

• "S[enior] management open [and] transparent to auditors on this topic -- which units were set aside for which employees. Both Bebo [and] Buono were open [and]

32565777 12

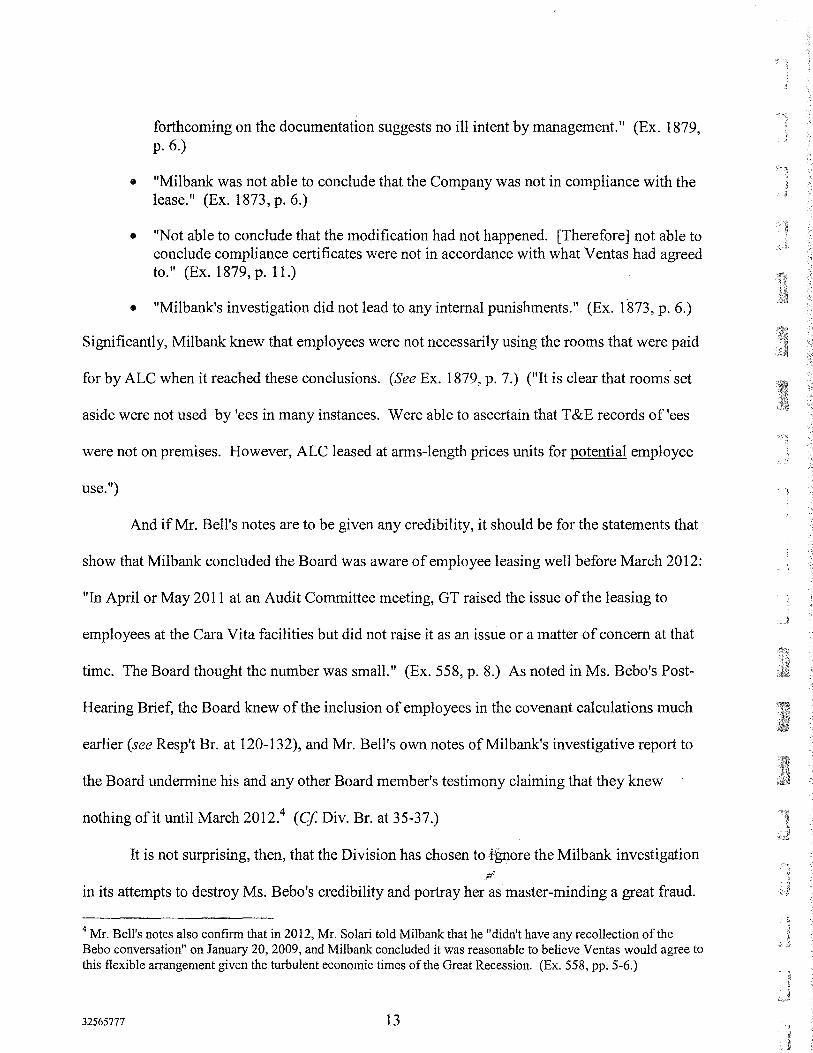

forthcoming on the documentation suggests no ill intent by management." (Ex. 1879, p. 6.)

• "Milbank was not able to conclude that the Company was not in compliance with the lease." (Ex. 1873, p. 6.)

• "Not able to conclude that the modification had not happened. [Therefore] not able to conclude compliance certificates were not in accordance with what Ventas had agreed to." (Ex. 1879, p. 11.)

• "Milbank's investigation did not lead to any internal punishments." (Ex. 1873, p. 6.)

Significantly, Milbank knew that employees were not necessarily using the rooms that were paid

for by ALC when it reached these conclusions. (See Ex. 1879, p. 7.) ("It is clear that rooms set

aside were not used by 'ees in many instances. Were able to ascertain that T &E records of 'ees

were not on premises. However, ALC leased at arms-length prices units for potential employee

use.")

And if Mr. Bell's notes are to be given any credibility, it should be for the statements that

show that Milbank concluded the Board was aware of employee leasing well before March 2012:

"In April or May 2011 at an Audit Committee meeting, GT raised the issue of the leasing to

employees at the Cara Vita facilities but did not raise it as an issue or a matter of concern at that

time. The Board thought the number was small." (Ex. 558, p. 8.) As noted in Ms. Bebo's Post-

Hearing Brief, the Board knew of the inclusion of employees in the covenant calculations much

earlier (see Resp't Br. at 120-132), and Mr. Bell's own notes ofMilbank's investigative report to

the Board undermine his and any other Board member's testimony claiming that they knew

nothing of it until March 2012.4 (Cf Div. Br. at 35-37.)

It is not surprising, then, that the Division has chosen to t1wore the Milbank investigation

in its attempts to destroy Ms. Bebo's credibility and portray her as.master-minding a great fraud.

4 Mr. Bell's notes also confirm that in 2012, Mr. Solari told Milbank that he "didn't have any recollection of the Bebo conversation" on January 20, 2009, and Milbank concluded it was reasonable to believe Ventas would agree to this flexible arrangement given the turbulent economic times of the Great Recession. (Ex. 558, pp. 5-6.)

32565777 13

Because it is not possible to reconcile the Division's claims that no member of the Board was

aware that ALC was including employees in the covenant calculations before March 2012 (and

that there was no agreement with Ventas at all) with the conclusions reached by Milbank after its .

investigation in 2012, when all of the witnesses' memories were presumably "fresher" than they

are in 2015. Importantly, the Milbank review confirms the reasonableness of Ms. Bebo's view

that ALC was in compliance with the Lease covenants, negating any inference of falsity and

sci enter.

D. In attempting to try a breach of contract case as Ventas' proxy, the Division fails to acknowledge that Ventas itself never pursued litigation related to the occupancy covenants or attempted to remove ALC from the properties.

In attempting to try a breach of contract case to prove up its allegations of disclosure

fraud, the Division again fails to acknowledge relevant and material evidence-Ventas itself

never pursued, and never would have pursued, any action based upon the asserted breach of the

occupancy covenant. As noted in Ms. Bebo's Post-Hearing Brief, on April 26, 2012, a few

weeks after receiving several notices that state regulators were taking actions against the licenses

of two Cara Vita Facilities, Ventas filed a lawsuit against ALC in federal district court asserting a

breach of the Lease due to the regulatory issues. (Resp't Br. at 147; Ex. 2075.) In April and

May, ALC and Ventas began discussing a potential negotiated resolution of the disputed event of

default and the lawsuit. After some internal debate, on April 27, ALC sent a settlement proposal

including specific language for a release with respect to the use of rentals to employees in the

covenant calculations. (Exs. 1535, 1535A, p. 2.)

On May 9, 2012 Ventas sent another default notice to ALC asserting a host of new

alleged breaches of the Lease. (Ex. 355; Doman, Tr. 347-50.)"''A number of the allegations

related to the licensing issues and a fire at one of the Facilities. (Id.) Ventas also asserted,

however, that ALC "may have failed to comply" with the occupancy and coverage ratio

32565777 14

covenants when it submitted "fraudulent information" including employees as bona fide third

party rentals. (Ex. 355, p. 5.) But when it filed a motion to amend its complaint against ALC the

very next day, there was no allegation to be found related to the occupancy and coverage ratio

covenants. (See Ex. 1194 (first amended complaint); Ex. 2076, p. 2 (ALC's 8-K describing the

letter and amended complaint allegations); Div. Br. at 18 n.5.)

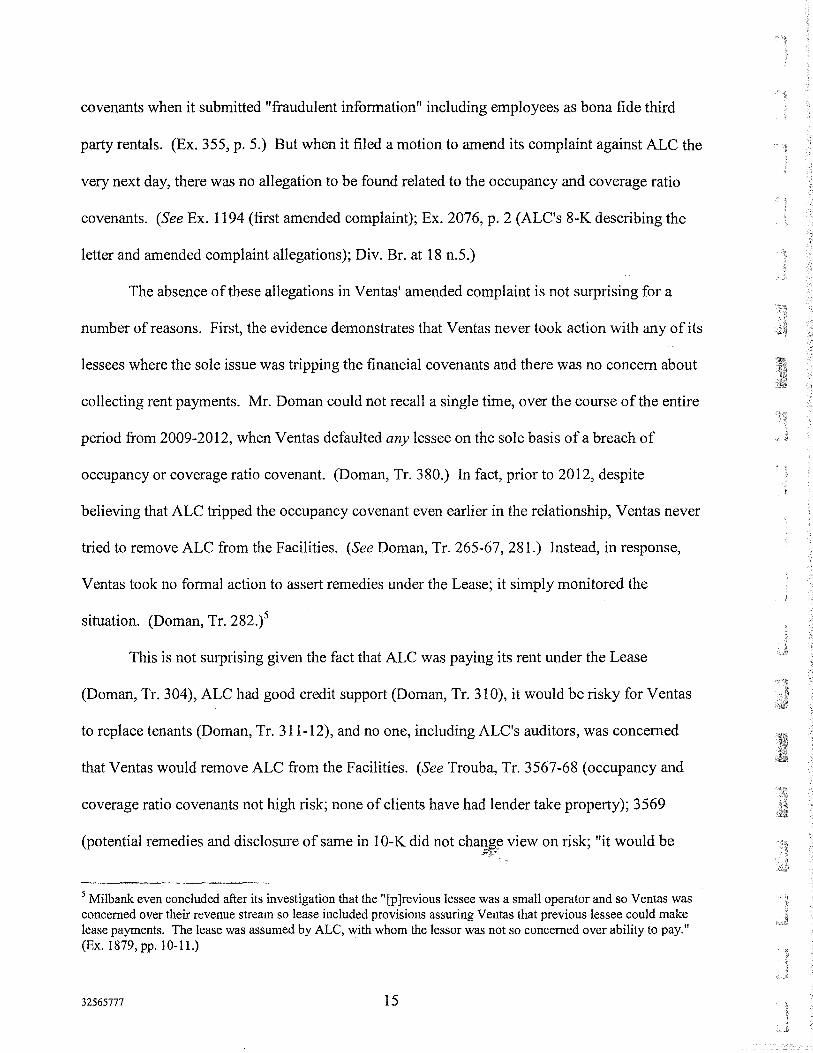

The absence of these allegations in Ventas' amended complaint is not surprising for a

number of reasons. First, the evidence demonstrates that Ventas never took action with any of its

lessees where the sole issue was tripping the financial covenants and there was no concern about

collecting rent payments. Mr. Doman could not recall a single time, over the course of the entire

period from 2009-2012, when Ventas defaulted any lessee on the sole basis of a breach of

occupancy or coverage ratio covenant. (Doman, Tr. 380.) In fact, prior to 2012, despite

believing that ALC tripped the occupancy covenant even earlier in the relationship, Ventas never

tried to remove ALC from the Facilities. (See Doman, Tr. 265-67, 281.) Instead, in response,

Ventas took no formal action to assert remedies under the Lease; it simply monitored the

situation. (Doman, Tr. 282.)5

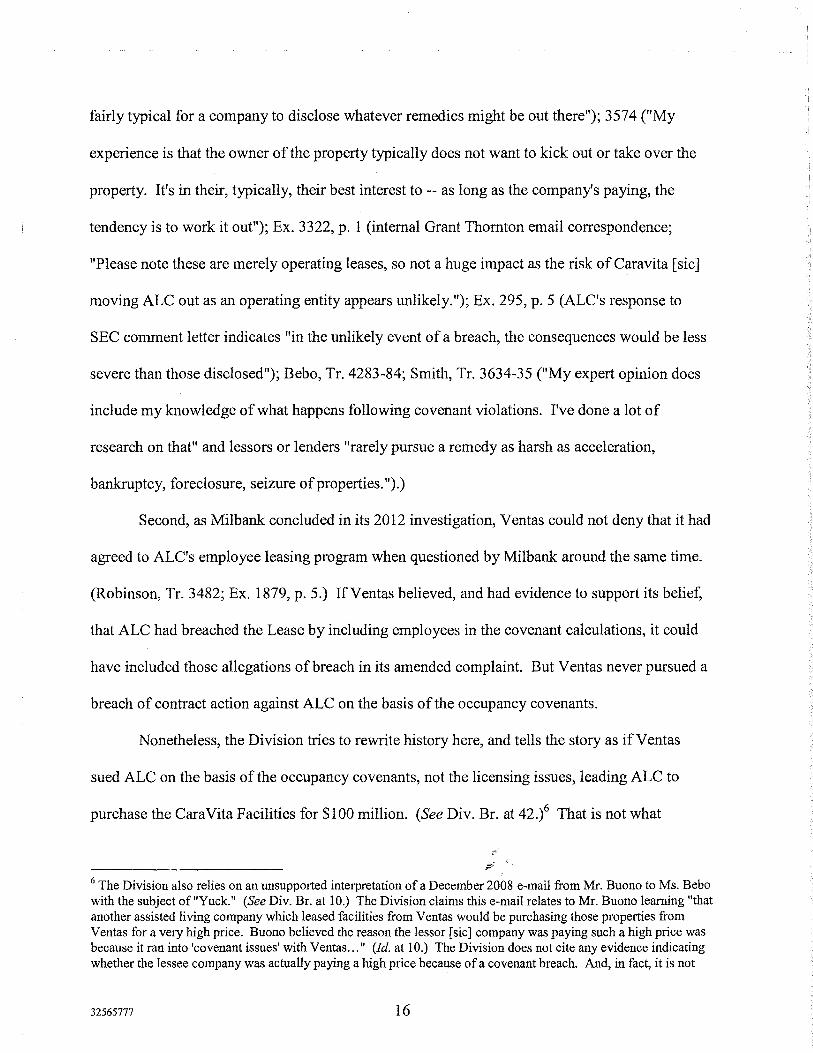

This is not surprising given the fact that ALC was paying its rent under the Lease

(Doman, Tr. 304), ALC had good credit support (Doman, Tr. 310), it would be risky for Ventas

to replace tenants (Doman, Tr. 311-12), and no one, including ALC's auditors, was concerned

that Ventas would remove ALC from the Facilities. (See Trouba, Tr. 3567-68 (occupancy and

coverage ratio covenants not high risk; none of clients have had lender take property); 3569

(potential remedies and disclosure of same in 10-K did not cha~e view on risk; "it would be ~:;:;?"

5 Milbank even concluded after its investigation that the "[p ]revious lessee was a small operator and so Ventas was concerned over their revenue stream so lease included provisions assuring Ventas that previous lessee could make lease payments. The lease was assumed by ALC, with whom the lessor was not so concerned over ability to pay." (Ex.1879,pp.10-ll.)

32565777 15

fairly typical for a company to disclose whatever remedies might be out there"); 3574 ("My

experience is that the owner of the property typically does not want to kick out or take over the

property. It's in their, typically, their best interest to -- as long as the company's paying, the

tendency is to work it out"); Ex. 3322, p. 1 (internal Grant Thornton email correspondence;

"Please note these are merely operating leases, so not a huge impact as the risk of Caravita [sic]

moving ALC out as an operating entity appears unlikely."); Ex. 295, p. 5 (ALC's response to

SEC comment letter indicates "in the unlikely event of a breach, the consequences would be less

severe than those disclosed"); Bebo, Tr. 4283-84; Smith, Tr. 3634-35 ("My expert opinion does

include my knowledge of what happens following covenant violations. I've done a lot of

research on that" and lessors or lenders "rarely pursue a remedy as harsh as acceleration,

bankruptcy, foreclosure, seizure of properties.").)

Second, as Milbank concluded in its 2012 investigation, Ventas could not deny that it had

agreed to ALC's employee leasing program when questioned by Milbank around the same time.

(Robinson, Tr. 3482; Ex. 1879, p. 5.) If Ventas believed, and had evidence to support its belief,

that ALC had breached the Lease by including employees in the covenant calculations, it could

have included those allegations of breach in its amended complaint. But Ventas never pursued a

breach of contract action against ALC on the basis of the occupancy covenants.

Nonetheless, the Division tries to rewrite history here, and tells the story as if Ventas

sued ALC on the basis of the occupancy covenants, not the licensing issues, leading ALC to

purchase the Cara Vita Facilities for $100 million. (See Div. Br. at 42.)6 That is not what

6 The Division also relies on an unsupported interpretation of a December 2008 e-mail from Mr. Buono to Ms. Bebo with the subject of"Yuck." (See Div. Br. at 10.) The Division claims this e-mail relates to Mr. Buono learning "that another assisted living company which leased facilities from Ventas would be purchasing those properties from Ventas for a very high price. Buono believed the reason the lessor [sic] company was paying such a high price was because it ran into 'covenant issues' with Ventas ... " (Id. at 10.) The Division does not cite any evidence indicating whether the lessee company was actually paying a high price because of a covenant breach. And, in fact, it is not

32565777 16

happened, as the documentary evidence makes clear. And we know now that if anything

motivated the purchase, it was the flexibility ownership afforded with respect to licensing,

avoiding regulatory pitfalls, and building expansions to the well-performing properties. (Resp't

Br. at 152-56.) Notwithstanding the reality of the situation, and the lack of action by Ventas (as

predicted by ALC and Ms. Bebo), the Division is attempting to try an alleged breach of contract

case now, when Ventas chose not to do so then, and is taking an even larger leap converting that

breach of contract case into a claim of securities fraud.

II. Instead of Developing a Theory Based on the Actual Facts of the Case and the Evidence Elicited at the Hearing, the Division Continues to Pursue Its Predetermined Narrative, Supporting Its Case with "Facts" that Do Not Exist.

As it did in its Pre-hearing Brief and in the OIP, the Division continues to pursue its

predetermined narrative, instead of dealing directly with the evidence that exists. And because

the Division now has the benefit of knowing the full scope of the evidence and testimony

admitted at the hearing, its single-minded adherence to this predetermined narrative is

particularly troubling. The Division resorts to bold statements, without regard to their ultimate

veracity, and using evidence out of context in an attempt to mold the facts around its theory of

the case.

In doing so, the Division also advances theories that are inconsistent and illogical. For

example, the Division asserts that ALC's Board of Directors was particularly concerned about

compliance with the Lease covenants, yet was unaware that ALC began including employees to

satisfy the covenant calculations. How could this same Board become comfortable with ALC's

covenant compliance in 2009, without, as the Division represe~s, any concrete explanation of

the increase in occupancy at the Facilities during the worst real estate recession in recent history?

true. (Bebo, Tr. 1863-64.) Instead, the Court heard testimony that Mr. Buono did not have background or knowledge on these properties and his view on the purchase of these properties changed. (Id.)

32565777 17

The Division would have the Court believe that Board members were at once "hypersensitive" to

the issue, and also totally disengaged, going so far as to put forth the incredible testimony that

members of the Audit Committee of a public company never reviewed the detailed financial

information about ALC provided to Board members in advance of the Board meetings.

The Division fails to explain this paradox; notably absent from the Division's theory is

any explanation for why these Board members who "cared about ALC's compliance with the

covenants," who allegedly discussed "the effect non-compliance would have on ALC's stock

price," and who "repeatedly inquired at board meetings about ALC's compliance with the

financial covenants" could have reasonably believed ALC would meet the covenants during the

Great Recession without the employee leasing program. (See Div. Br. at 13, 49.) The more

logical conclusion, based on the Division's own theory of the facts, is that the Board initially was

concerned about failing the Ventas Lease covenants and then became less concerned after they

agreed that ALC should participate in the employee leasing program. This is particularly true

given the testimony of Ms. Bucholtz and others that poor occupancy at, and financial

performance of, the Cara Vita Facilities was a repeated item of discussion at Board meetings.

(See Bucholtz, Tr. 2956-57.) The reality is that no evidence exists of alternative explanations for

meeting the financial covenants and the Board did not express any concern for several years,

because they knew that the employee leasing program was in effect.

Similarly, according to the Division, Ventas was both on high-alert for a covenant breach

in February 2009, but also would not have been able to determine from the February 4, 2009

e-mail that ALC would be including rentals related to employ~s in the covenant calculations.

Nor is there any explanation for the Division's inconsistent positions with respect to Mr. Buono's

testimony about the agreement with Mr. Solari, as described in more detail below. (See infra

32565777 18

Section III.B.3.) On the one hand the Division asserts, through Mr. Buono, that there was no

agreement, and on the other hand the Division asserts Mr. Buono purportedly expressed concern

about whether ALC was complying with the agreement.

These inconsistent and contradictory theories and constant loose play with, and in some

instances misrepresentations about, the factual record permeate and undermine the reliability of

the Division's entire case. The Court must reject the Division's attempts to use "facts" that do not

exist and others that do, but only when taken out of context. The Division must establish its case

on the basis of facts and evidence that actually exist, not the "facts" the Division would like to

exist to fit its predetermined narrative.

A. Much like its Pre-Hearing Brief, the Division's Post-Hearing Brief fills its predetermined narrative with broad assertions lacking evidentiary support.

The Division makes several broad claims using the same or similar language as was used

in the Division's Pre-hearing Brief or the OIP that are unsupported by the evidence actually

elicited at the hearing. For example, the Division maintains that Ventas did not agree to the

employee leasing practice, and that Ventas, ALC's Board, and ALC's attorneys did not know

about the inclusion of employees in the covenant calculations until early 2012. (See Div. Br.

at 1, 2, 3, 12, 16, 35, 36, 37, 38, 40, 41, 43, 45, 50, 54.) To do so, the Division makes several

broad, unsupported statements, such as:

• "Indeed, no document exists corroborating Bebo's story of what was disclosed to, or approved by, Ventas, the attorneys, the board, and the auditors. And her story of an agreement with Ventas and full disclosure of ALC's covenant practices was refuted by every percipient witness who testified . ... Simply put, Bebo lied to Ventas, lied to ALC's board, lied to Grap.t Thornton, and lied to the Court." (Id. at 3 (emphasis added).)

"

• "The heart ofBebo's defense is her claim that Ventas agreed to the inclusion of employees in the covenant calculations, and that she fully disclosed the practice to various attorneys, auditors, and ALC's board. Notably, there is no documentary

32565777 19

evidence to support Bebo. And more importantly, each of the percipient witnesses refuted Bebo's version of the events." (Id. at 43 (emphasis added)/

• "Further, every percipient witness other than Bebo testified Bebo concealed key aspects of ALC's covenant calculation practices from Ventas and ALC's board, attorneys, and auditors." (Id. at 50 (emphasis added).)

• "(E]ach of the eleven witnesses other than Bebo who attended board meetings -- Bell, Buono, Buntain, Fonstad, Hennigar, Hokeness, Koeppel, Rhinelander, Roadman, Robinson and Zak -- all dispute Bebo's account that Bebo disclosed to the board that ALC was including employees in the covenant calculations. These eleven witnesses further refute Bebo's claim that she, or anyone, told the board the numbers of employees being included in the calculations, that ALC was including employees who did not stay at the Ventas facilities, and that the applicable criteria for employees' inclusion was whether they had a 'reason to go."'(ld. at 45 (emphasis added).)8

To make these statements the Division has ignored or misconstrued evidence in the record to

suits its needs, or used clever wording to make damning claims that ring hollow.

In anticipation of the Division maintaining these positions in its Post-Hearing Brief,

Ms. Bebo addressed many of these statements in her own Post-Hearing Brief. (See, e.g., Resp't

Br. at 8-26.) As made clear there, contrary to the Division's assertions here, there are many

7 The Division's decision to fit the evidence into its predetermined narrative, without regard to what testimony was actually elicited at the hearing, is evidenced by the similarity between the statements that the Division made before and after the hearing. (Div. Br. at 19 ("The heart ofBebo's defense is her self-serving claim that Ventas agreed to the inclusion of employees in the covenant calculations and that she fully disclosed the practice to various attorneys, auditors, and ALC's board. Notably, there is no documentary evidence to support Bebo. And more importantly, each of the percipient witnesses will testifj; that Bebo is not telling the truth.") (emphasis added); see also id. at 2 ("Beyond Bebo's story not making any sense, not a single percipient witness or document will corroborate Bebo's alibis. To the Contrary, the three individuals Bebo claims were witnesses to her purported agreement with Ventas will all deny that an agreement existed to include any employees in the covenant calculations"; "Again no document exists corroborating Bebo's account of what she disclosed to, or was approved by, Ventas, the attorneys, the board, and auditors.") (emphasis added).) 8 Notwithstanding the lack of support for the assertions here about Ms. Koeppel and Mr. Robinson (see supra pp. 10-12), to make this statement the Division also ignores other testimo11¥ from these very same witnesses that undermines the credibility of the testimony cited by the Division. For examp1e, Mr. Buono testified about a meeting he attended with Ms. Bebo, during which Mr. Rhinelander gave them approval to pursue the employee leasing program. (Buono, Tr. 2393-96.) And Mr. Buntain testified that "they" (meaning management, including Ms. Bebo) "justified their use of employees" while discussing ALC's proposed response to the SEC comment letter at the Board meeting. (Resp't Br. at 127-28; Buntain, Tr. 1452-54.) This is yet another example of how the Division has overstated its case.

32565777 20

documents and "percipient" witnesses supporting Ms. Bebo's defense. (See id.) In the chart on

pages 8 through 26 alone, Ms. Bebo's Post-Hearing Brief, has cited at least:

• 42 different pieces of testimony, from witnesses other than Ms. Bebo, to support her claims that (1) the employee leasing agreement existed between ALC and Ventas, (2) that Ventas, the Board, auditors, and ALC's internal counsel were knowledgeable of the practice, including many, if not all, of its details; and (3) these parties approved the practice, as well as

• 55 exhibits-documents that the Division contends do not exist or support Ms. Bebo's defense.

In light of this, the Division's argument must be that there is no support for Ms. Bebo's position

because no single piece of evidence clearly and comprehensively shows that ALC had an

agreement with Ventas that was widely known and implemented. Of course, the Division's

theory of the case is not neatly tied up in one single piece of evidence either.

What the Division's broad statements fail to account for is the considerable evidence,

viewed individually or collectively, that directly supports Ms. Bebo's testimony that there was an

agreement with Ventas and that the manner by which ALC was meeting the covenants was well-

known both inside and outside of ALC:

• Mr. Solari has no memory of the key telephone conference on January 20, 2009 and cannot dispute Ms. Bebo's detailed memory of the call. He received the confirming e-mail and admits neither he nor Ventas ever expressed concern, objected, or otherwise responded to the e-mail confirming the agreement. (Resp't Br.at 76-81.)

• Mr. Buono, ALC's CFO, participated on the call and from 2009 until the Division told Mr. Buono that Ms. Bebo had "thrown him under the bus," understood that Ventas had agreed to the employee leasing arrangement, reassured others inside and outside of ALC about the nature and sufficiency of the agreement, represented to auditors after Ms. Bebo left ALC that the employee leasing arrangement did not involve "irregularities" much less fraud, and otherwise took no actions contrary to his belief that an agreement existed. (See, e.g., infra pp. 63-64; Resp't Br. at 104-105, 161 (citing evidence).) ;:'

• Every percipient witness to testify about the call with Mr. Solari confirmed that ALC's general counsel, Mr. Fonstad, was present in Ms. Bebo's office for it, including Mr. Buono (through impeachment of prior statements), Ms. Bebo, Ms. Bucholtz, and Ms. Zaffke. (Id. at 75.)

32565777 21

• Ms. Bebo's February 4, 2009 e-mail exists confirming the employee leasing discussion occurred, which was reviewed by several Ventas executives, none of whom ever raised a concern or objection to the disclosure of ALC's room rentals related to employees. (Id. at 84-91.)

• Mr. Fonstad, who participated on the call, helped draft the follow up e-mail to Ventas confirming the agreement, told Mr. Buono that employee leasing was okay or kosher, chaired quarterly disclosure committee meetings where the employee leasing arrangement was repeatedly discussed, and continued to be involved in approving ALC's disclosure about the Ventas Lease. (Id. at 83-84, 118-20.)

• Grant Thornton was aware of the employee leasing program and the engagement partners testified that they informed the Board about the employee leasing program, specifically telling the Board that employees were included in the covenant calculations. (Id. at 123-26, 133-34.) Additionally, Grant Thornton knew that occupancy reconciliation reports were not meant to track the length of individuals' actual overnight stays at the properties, since they were receiving lists of occupants where individuals were listed as staying at multiple properties at the same time. (Id. at 103-08.)

• The Board knew about employee leasing arrangement as evidenced by e-mails, John Buono's testimony, Grant Thornton's testimony, and the Board members' testimony. (Resp't Br. at 120-32.)

• Although it is disputed whether Quarles & Brady knew pertinent facts about the employee leasing arrangement with Ventas prior to 2012, it is undisputed that Quarles & Brady knew in April 2012 that ALC was meeting the financial covenants through the use of70-90 units that ALC paid for through intercompany transfers for employees to stay at the Facilities. At that time, Quarles did not recommend that ALC modify its disclosure regarding how it was meeting the financial covenants. (Id. at 149-50.)

• At no point did Ventas add a claim with regard to employee leasing to its already filed lawsuit, despite knowing that the practice occurred. (Id. at 147-49.)

• Milbank, a reputable law firm, spent a significant amount of time investigating the employee leasing issue and concluded that: (1) Milbank was "not able to determine that units for employee use to calculate minimum occupancy was done without the knowledge and approval of Ventas" (Robinson, Tr. 3479; Ex. 1879, p. 3); (2) "the consideration that this practice was concealed from the Board is incorrect" (Ex. 3460, p. 2; Robinson, Tr. 3461-62); and (3) Solari and V ~)ltas could not refute the existence of an agreement. (Robinson, Tr. 3480; Ex. 1879, p-: 4 ("Ventas' counsel reached out to Solari .... He was unable to deny the Bebo repres-entation of his approval."); Robinson, Tr. 3482; Ex. 1879 ("February 4th, 2009 e-mails could lead to ALC leases -- employees for use. However, ALC leased from lessor for use by potential employees when traveling to the unit. Employees were not actually at the premises, but potentially could have been at the premises.").)

32565777 22

• The Division presented no logical theory of what Ms. Bebo's motive would be to risk her livelihood by committing securities fraud. (Resp't Br. at 206-07.)

In sum, the Division can only make these broad statements based on its deliberate

disregard of the evidence actually presented at the hearing. The Division has no explanation for

any of these facts that contradict its predetermined narrative, many of them undisputed. But the

inaccuracies in the Division's Post-Hearing Brief do not stop at these general statements; the

Division's Post-Hearing Brief repeatedly misstates the record and evidence presented.

B. Despite evidence to the contrary, the Division sticks to its predetermined narrative, asserting "facts" that do not exist or lack critical context.

The Division's theory of the case depends in large part on there being no agreement

between Ventas and ALC regarding the rental of rooms for employees, and all of the relevant

parties being unaware of ALC's inclusion of employees in the covenant calculations. Because

these "facts" are so crucial to the Division's case, it continues to assert them, in a series of

unsupported or incomplete statements.

1. The existence of an agreement with Ventas regarding the employee leasing program.

In its attempt to disprove that any agreement existed between ALC and Ventas regarding

the inclusion of employees in the covenant calculations, the Division does not acknowledge the

true nature of ALC's general counsel's participation at the inception of the employee leasing

program and misconstrues what really happened on and after the January 20, 2009 phone call

with Mr. Solari. The Division outlines the "facts" only as they fit its predetermined narrative.

False Narrative EJ:planation

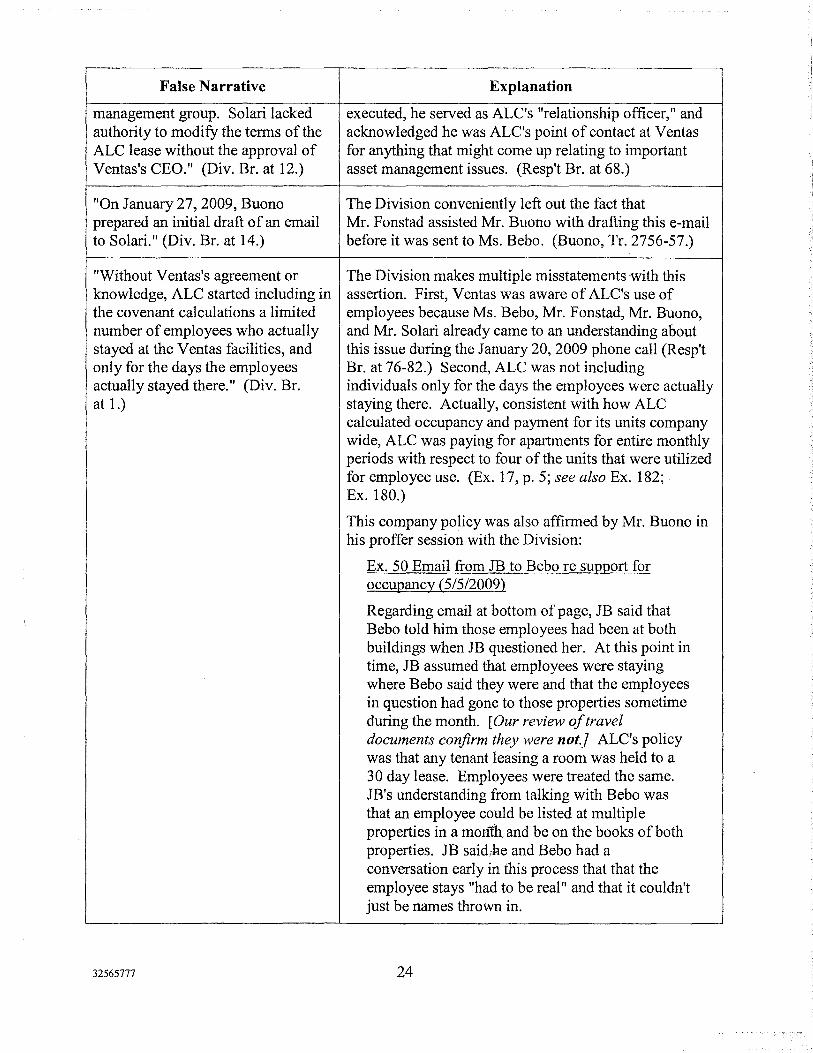

"Solari's responsibilities at Ventas Mr. Solari was principally responsible on Ventas' part for dealt with Acquisitions as opposed negotiating the terms of the Lease with ALC, so he to Management of Ventas's certainly had authority to modify the terms of the Lease. properties, which was the At a minimum he had apparent authority. Moreover, responsibility of the asset Mr. Solari acknowledged that even after the Lease was

32565777 23

False Narrative Explanation

management group. Solari lacked executed, he served as ALC's "relationship officer," and authority to modify the terms of the acknowledged he was ALC's point of contact at Ventas ALC lease without the approval of for anything that might come up relating to important Ventas's CEO." (Div. Br. at 12.) asset management issues. (Resp't Br. at 68.)

"On January 27, 2009, Buono The Division conveniently left out the fact that prepared an initial draft of an email Mr. Fonstad assisted Mr. Buono with drafting this e-mail to Solari." (Div. Br. at 14.) before it was sent to Ms. Bebo. (Buono, Tr. 2756-57.)

"Without Ventas's agreement or The Division makes multiple misstatements with this knowledge, ALC started including in assertion. First, Ventas was aware of ALC's use of the covenant calculations a limited employees because Ms. Bebo, Mr. Fonstad, Mr. Buono, number of employees who actually and Mr. Solari already came to an understanding about stayed at the Ventas facilities, and this issue during the January 20, 2009 phone call (Resp't only for the days the employees Br. at 76-82.) Second, ALC was not including actually stayed there." (Div. Br. individuals only for the days the employees were actually at 1.) staying there. Actually, consistent with how ALC

calculated occupancy and payment for its units company wide, ALC was paying for apartments for entire monthly periods with respect to four of the units that were utilized for employee use. (Ex. 17, p. 5; see also Ex. 182; Ex. 180.)

This company policy was also affirmed by Mr. Buono in his proffer session with the Division:

Ex. 50 Email from JB to Bebo re suggort for occupancy (5/5/2009)

Regarding email at bottom of page, JB said that Bebo told him those employees had been at both buildings when JB questioned her. At this point in time, JB assumed that employees were staying where Bebo said they were and that the employees in question had gone to those properties sometime during the month. [Our review of travel documents confirm they were not.] ALC's policy was that any tenant leasing a room was held to a 30 day lease. Employees were treated the same. JB's understanding from talking with Bebo was that an employee could be listed at multiple properties in a momh.and be on the books of both properties. JB said,Jle and Bebo had a conversation early in this process that that the employee stays "had to be real" and that it couldn't just be names thrown in.

32565777 24

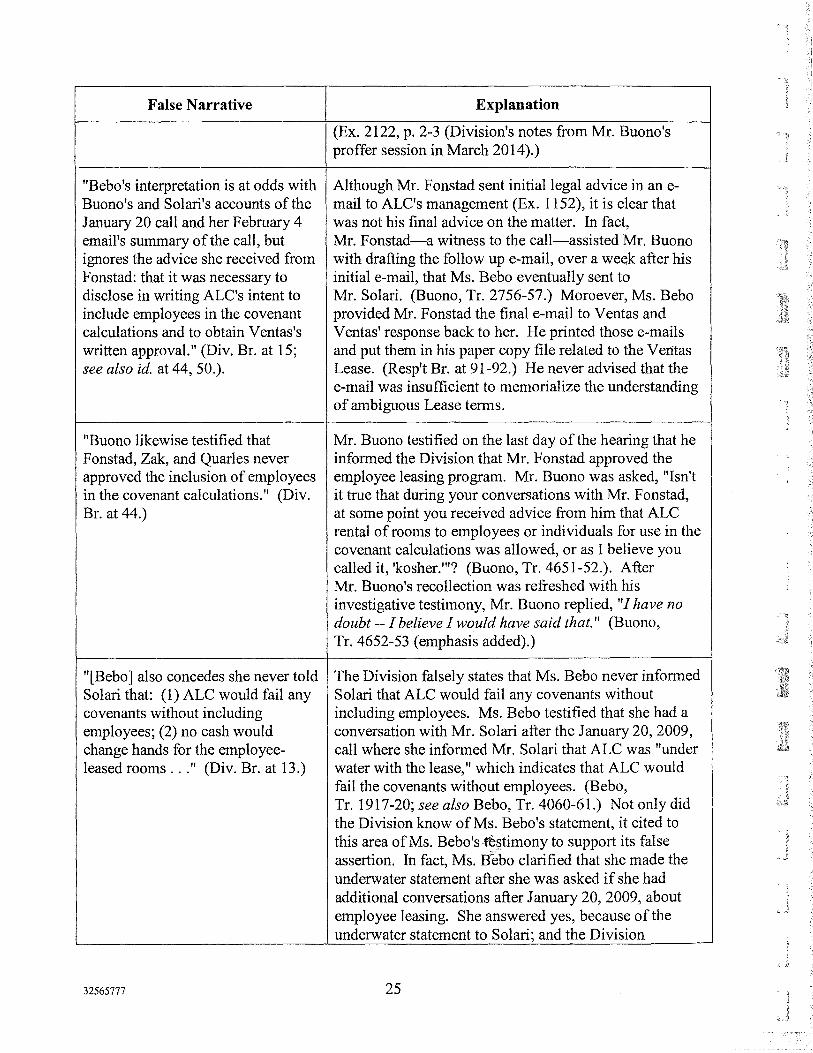

False Narrative Explanation

(Ex. 2122, p. 2-3 (Division's notes from Mr. Buono's proffer session in March 2014).)

"Bebo's interpretation is at odds with Although Mr. Fonstad sent initial legal advice inane-Buono's and Solari's accounts of the mail to ALC's management (Ex. 1152), it is clear that January 20 call and her February 4 was not his final advice on the matter. In fact, email's summary of the call, but Mr. Fonstad-a witness to the call-assisted Mr. Buono ignores the advice she received from with drafting the follow up e-mail, over a week after his Fonstad: that it was necessary to initial e-mail, that Ms. Bebo eventually sent to disclose in writing ALC's intent to Mr. Solari. (Buono, Tr. 2756-57.) Moroever, Ms. Bebo include employees in the covenant provided Mr. Fonstad the final e-mail to Ventas and calculations and to obtain Ventas's Ventas' response back to her. He printed those e-mails written approval." (Div. Br. at 15; and put them in his paper copy file related to the Ventas see also id. at 44, 50.). Lease. (Resp't Br. at 91-92.) He never advised that the

e-mail was insufficient to memorialize the understanding of ambiguous Lease terms.

"Buono likewise testified that Mr. Buono testified on the last day of the hearing that he Fonstad, Zak, and Quarles never informed the Division that Mr. Fonstad approved the approved the inclusion of employees employee leasing program. Mr. Buono was asked, "Isn't in the covenant calculations. 11 (Div. it true that during your conversations with Mr. Fonstad, Br. at 44.) at some point you received advice from him that ALC

rental of rooms to employees or individuals for use in the covenant calculations was allowed, or as I believe you called it, 'kosher."'? (Buono, Tr. 4651-52.). After Mr. Buono's recollection was refreshed with his investigative testimony, Mr. Buono replied, "I have no doubt -- I believe I would have said that. 11 (Buono, Tr. 4652-53 (emphasis added).)

"[Bebo] also concedes she never told The Division falsely states that Ms. Bebo never informed Solari that: (1) ALC would fail any Solari that ALC would fail any covenants without covenants without including including employees. Ms. Bebo testified that she had a employees; (2) no cash would conversation with Mr. Solari after the January 20, 2009, change hands for the employee- call where she informed Mr. Solari that ALC was "under leased rooms ... " (Div. Br. at 13.) water with the lease," which indicates that ALC would

fail the covenants without employees. (Bebo, Tr. 1917-20; see also Bebo, Tr. 4060-61.) Not only did the Division know of Ms. Bebo's statement, it cited to this area of Ms. Bebo'stt!§timony to support its false assertion. In fact, Ms. gebo clarified that she made the underwater statement after she was asked if she had additional conversations after January 20, 2009, about employee leasing. She answered yes, because of the underwater statement to Solari; and the Division

32565777 25

False Narrative Explanation

"impeached" her with her prior statement that she did not recall additional conversations. (Bebo, Tr. 1917-20). Finally, to the extent the Division is only referencing Ms. Bebo's statements during the January 20, 2009, conversation, then the Division intentionally omitted a later statement by Ms. Bebo with regard to this issue.

"Buono testified consistently with Solari's professed belief (speculation) that no agreement Solari .... Buono confirmed no about employee leasing was reached and his canned covenants were discussed, and that response to this effect is contradicted by his prior Solari did not agree to anything." statements relayed to Milbank, which the Division (Div. Br. at 13.) The Division made chooses to ignore. (Robinson, Tr. 3480; Ex. 1879, p. 4 additional statements that Solari and ("Ventas' counsel reached out to Joe Solari, a Ventas Buono confirmed that Solari did not liaison to ALC, terminated in 4/2009 due to downsizing agree to the employee leasing after he received the February 4th, 2009 e-mail on program. (Id. at 12-13, 43.) employee leasing arrangements. This was the person

who had the reported arrangement. He was unable to deny the Bebo representation of his approval.").) Additionally, the next section of this brief addresses the absurdity of the Division's statements that Buono confirmed that Solari did not agree to employee leasing.

"Ventas never responded to this The Division chooses not to acknowledge or explain the proposal [the February 4, 2009 implications of the undisputed fact that Ms. Bebo's e-mail e-mail to Joe Solari], and Bebo was reviewed by several Ventas executives and officials. agreed that prior to April 2012, ALC (Ex. 1343.) Also, the Division ignored Ms. Bebo's did not inform Ventas that ALC was comment to Mr. Solari that ALC was underwater and that including employees in the covenant it did not help that ALC was paying for rooms (Bebo, calculations. According to Bebo, Tr. 1917-20; see also Bebo, Tr. 4060-61), which is not Ventas's silence confirmed its refuted by the any of the Division's citations to the agreement that ALC could include in record. (See Div. Br. at 14). the calculations .... " (Div. Br. at 14 (citation omitted).)