real estate terms & concepts jerry rioux, ccrh board member [email protected]

TRANSCRIPT

Real Estate Terms & Concepts

Jerry Rioux, CCRH Board Member

http://www.angelfire.com/jazz/jrioux/

Workshop Outline

Part I - Terms & Concepts

Part II - Financing

Part III - Purchase Process

Part I

Terms & Concepts

What Is Real Estate?

Land Affixed to the Land Appurtenant to Land Immovable by Law

Real Estate = Bundle of Rights

Old English Concept of Ownership The Right to Possess, Enjoy, Control

and Dispose of Real Estate The Individual “Rights” May be Bought

and Sold or Rented Separately

Title & Estates

Title = Ownership of Real Estate Estate = Character of Interest Fee Simple Less Than Fee Estate Life Estate

Real Estate Legal Descriptions

Lot, Block and Tracks

Metes and Bounds

Section and Township

Deeds

Legal Documents that Convey (Transfer) the Title to Real Estate

Usually Recorded against the Property in the County Recorder’s Office

Examples of Deeds

Warranty Deed Grant Deed Quitclaim Deed Tax Deed Trust Deed (or Deed of Trust) Deed of Reconveyance

Encumbrances

Things that Burden the Title to Property Claims of Others to Property Non-Monitory Encumbrances Monitory Encumbrances

Non-Monitory Encumbrances

C C & Rs Easements Encroachments Mineral Rights Leases Regulatory Agreements Public Rights of Way

Covenants, Conditions and Restrictions (C C & Rs) Private Land Use Controls

– Lot Size, Set-Backs...– Home Size, Architectural Style…– Parking, Pets…

Public Deed Restrictions– Price & Occupancy Controls

Covenants, Conditions and Restrictions (C C & Rs) Judicial Enforcement Invalid

– Racial & Religious Covenants Unenforceable

– Restrictions the Cause Waste Can Be Released by Beneficiary

Monitory Encumbrances

aka Liens Loans, Taxes & Assessments Voluntary or Involuntary General or Specific “Blanket Encumbrances” Cover

Multiple Parcels

Lien Priorities

Based on Recording Dates or Subordination Agreement

Legal Description (lot split) C C & Rs Property Taxes 1st Mortgage 2nd Mortgage

Real Estate Contracts

Real Estate Purchase Agreement Land Contract (Contract for Deed) Option Lease Option First Right of Refusal

Valid Real Estate Contracts

In Writing Capable Parties Mutual Consent Lawful Object Sufficient Consideration

Purchase Contract

Consideration Purchase Price Timing Financing & Other Terms Contingencies

Contingencies

Financing Appraisal Clear Title Due Diligence

Option to Purchase

Right to Purchase Consideration Time Limits for Performing Extension Fees Purchase Price or Formula No Obligation to Buy

First Right of Refusal

Right to Buy When Offered for Sale Match Price or Formula Limited Time to Perform No Obligation to Buy

Title Insurance Companies

Title Plants - duplicates county records Organizes Records by Parcel Provides Title Reports Records Documents Issues Title Insurance

Title Reports

Preliminary (not Title) Reports Lists Ownership Interests and

Encumbrances Encumbrances are “Exceptions”

to the Title Buyers want Exceptions Removed

Types of Insurance

Title Insurance – CLTA & ALTA

Mortgage Insurance– PMI & MMI

Hazard Insurance– also Flood & Earthquake

Escrow

Independent 3rd Party who Processes Real Estate Sales Transactions

Acts Only When All Conditions Are Met Divides or Allocates Costs as Agreed Can Handled by

– Title Insurance Companies– Private Escrow Companies– Real Estate Brokers

Closing Costs - Recurring

Property Taxes Insurance Interest HOA Dues Assessments

Closing Costs - Non-Recurring

Escrow Fees Title Insurance Transfer Fees Recording Fees Doc Prep Fees Loan Fees & Points Home Warrantee

Part II

Financing

Single Family Financing

Value of Collateral Payment Ratios Buyer’s Credit Worthiness Stability of Buyer’s Income

Loan to Value Ratio (LTV)

Loan Amount divided by Property Value $160,000 / $200,000 = 80% 97% and 100% are Possible over 80% needs Mortgage Insurance

Payment Ratio (Housing)

PITI– Principal– Interest – Taxes – Insurance

divided by Gross Income 28%, 32%, 40%...

Payment Ratio (Overall)

PITI plus Other Recurring Debt divided by Gross Income 36%, 40%, 45%...

Market Rate Home Buyer

First Mortgage $160,000

Cash Down Payment 45,000

Purchase Price $200,000

Buyer's Closing Costs 5,000

Total Acquisition Costs $205,000

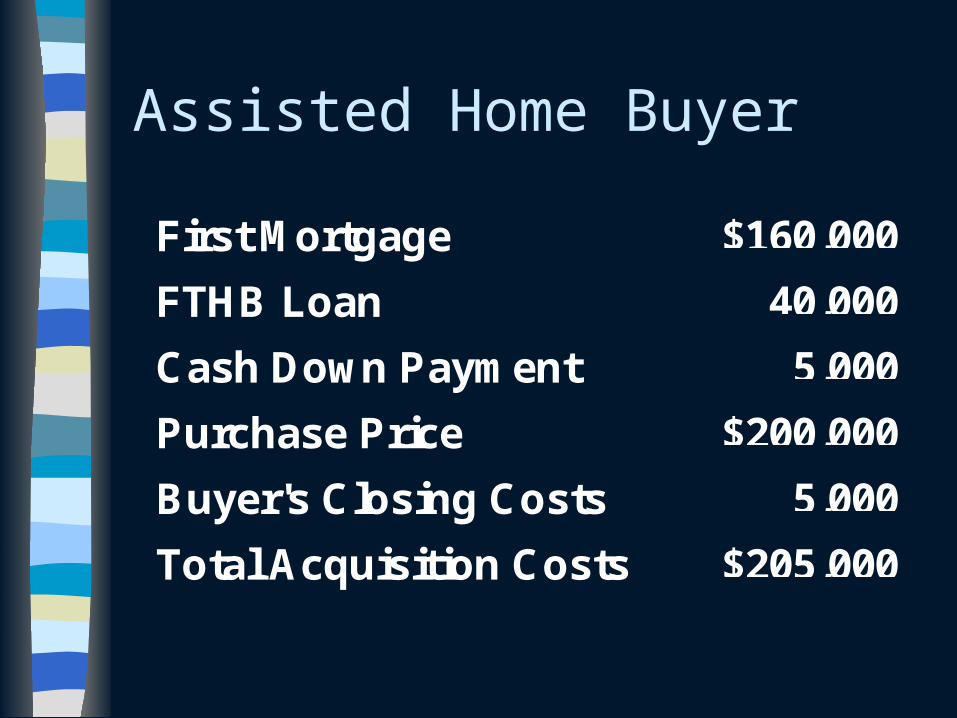

Assisted Home Buyer

First Mortgage $160,000

FTHB Loan 40,000

Cash Down Payment 5,000

Purchase Price $200,000

Buyer's Closing Costs 5,000

Total Acquisition Costs $205,000

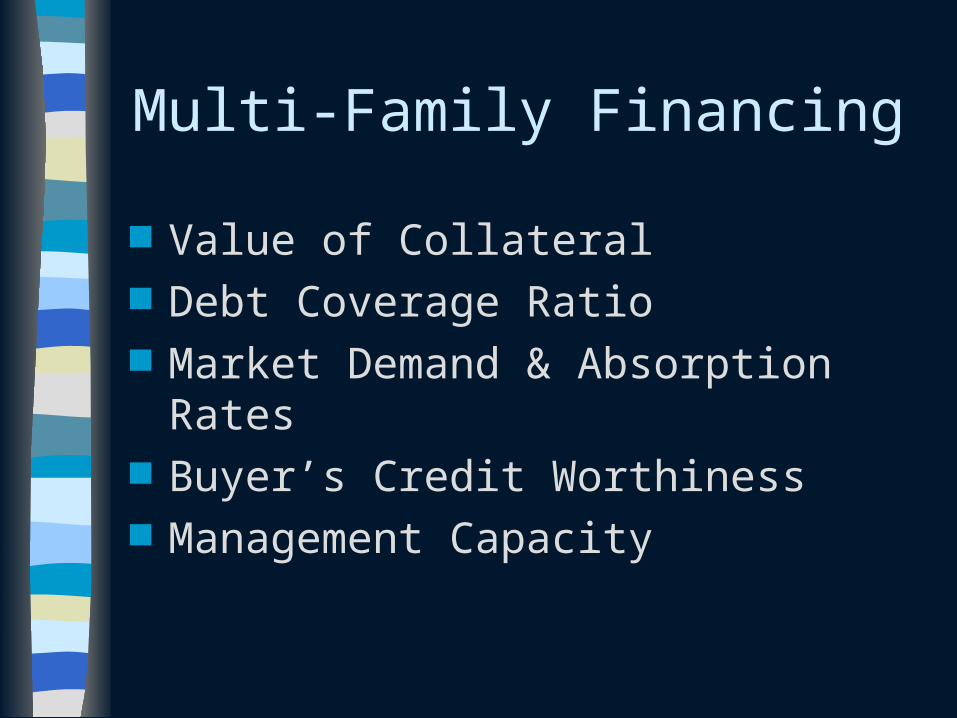

Multi-Family Financing

Value of Collateral Debt Coverage Ratio Market Demand & Absorption Rates Buyer’s Credit Worthiness Management Capacity

Proforma or Pro Forma

Jargon for Budget Project Financial Performance Development Pro Forma Operating Pro Forma Development & Operating together

Development Pro Forma

Land $1,300,000

Permits & Fees 225,000

Off Site Improvements 175,000

Construction Costs 4,000,000

Overhead & Profit 100,000

Total Development Costs $5,800,000

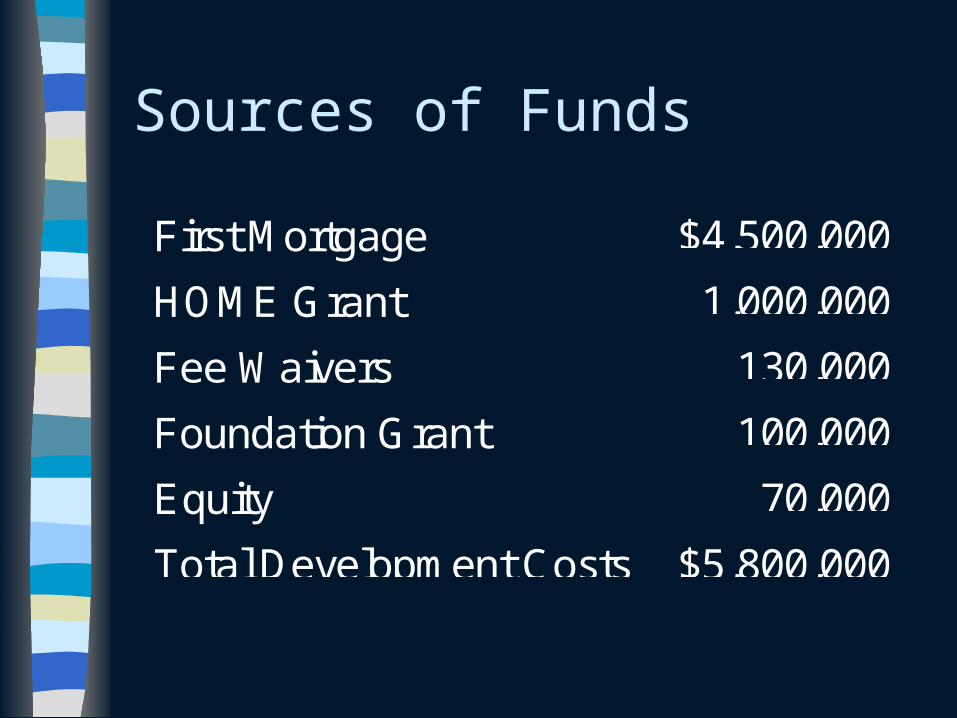

Sources of Funds

First Mortgage $4,500,000

HOME Grant 1,000,000

Fee Waivers 130,000

Foundation Grant 100,000

Equity 70,000

Total Development Costs $5,800,000

Operating Pro Forma

Rent $1,000,000

Management Costs - 230,000

Maintenance Costs - 180,000

Taxes & Insurance - 30,000

Replacement Reserves - 10,000

Net Operating Income $550,000

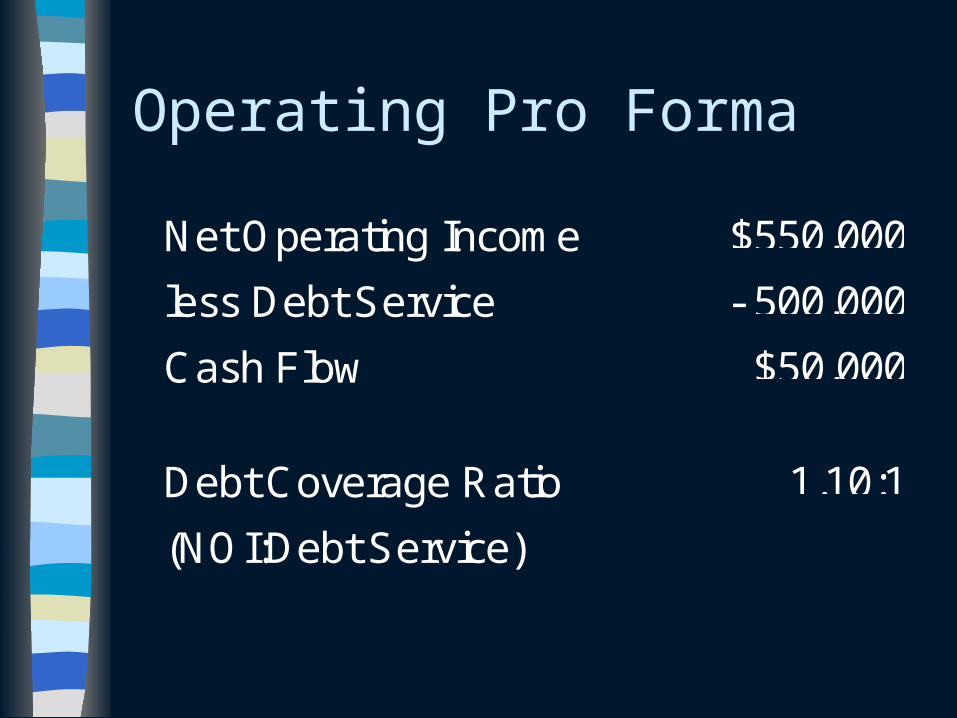

Operating Pro Forma

Net Operating Income $550,000

less Debt Service - 500,000

Cash Flow $50,000

Debt Coverage Ratio 1.10:1

(NOI:Debt Service)

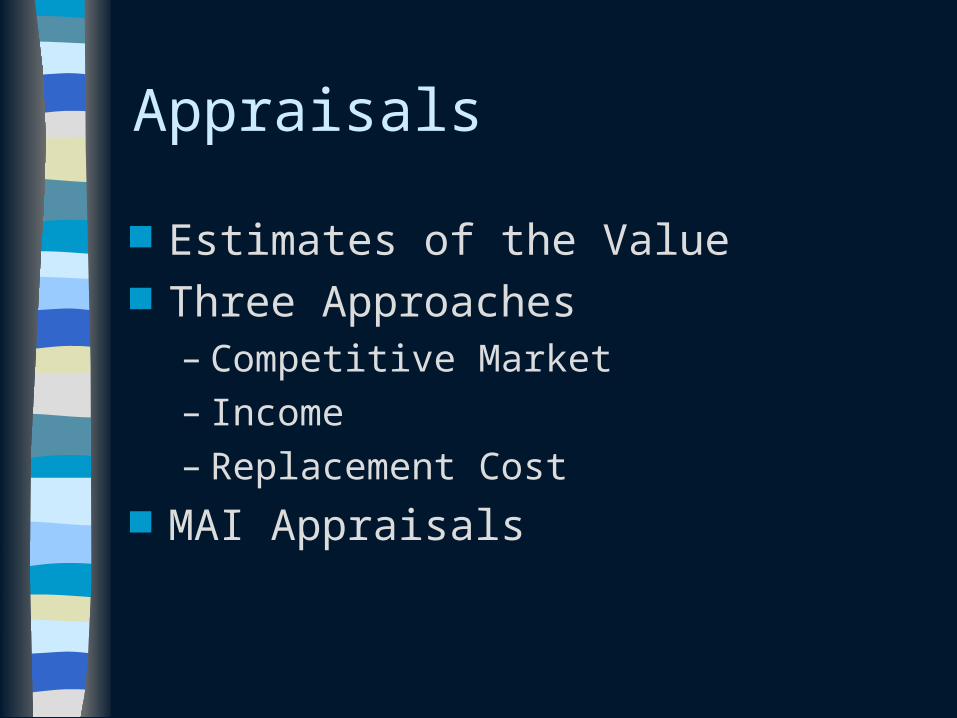

Appraisals

Estimates of the Value Three Approaches

– Competitive Market– Income– Replacement Cost

MAI Appraisals

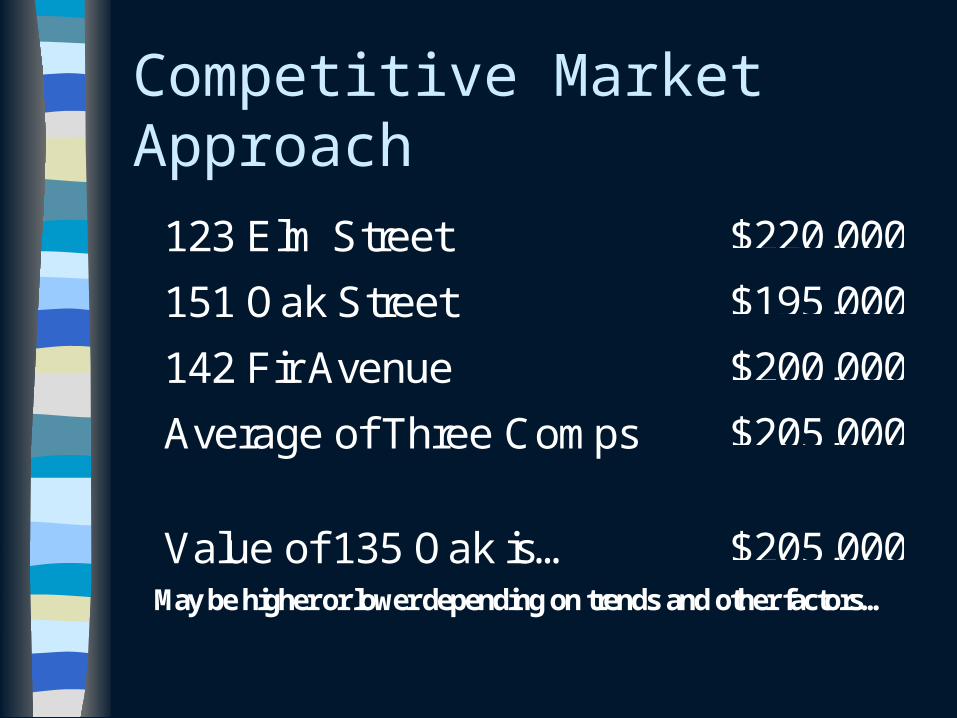

Competitive Market Approach

123 Elm Street $220,000

151 Oak Street $195,000

142 Fir Avenue $200,000

Average of Three Comps $205,000

Value of 135 Oak is… $205,000May be higher or lower depending on trends and other factors…

Income Approach

Net Operating Income $550,000

Capitalization Rate 11.0%

Indicated Value $5,000,000

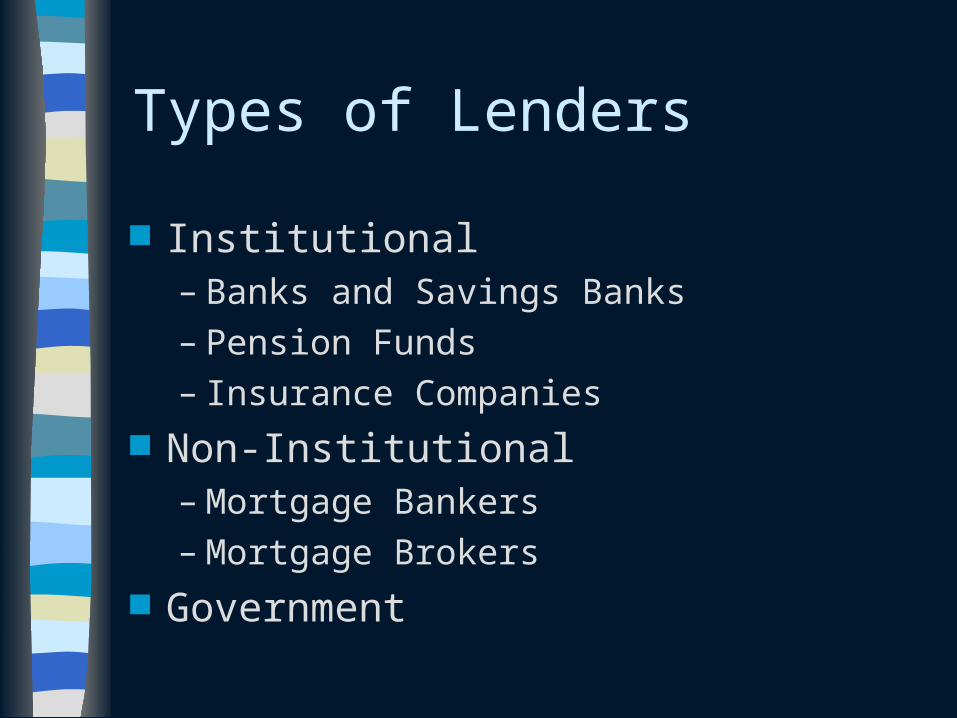

Types of Lenders

Institutional – Banks and Savings Banks– Pension Funds– Insurance Companies

Non-Institutional – Mortgage Bankers– Mortgage Brokers

Government

S&L Concept

Intermediation– Accept lots of small short-term deposits

to make 30-year home loans Disintermediation

– Depositors withdraw money faster than it is collected from Borrowers

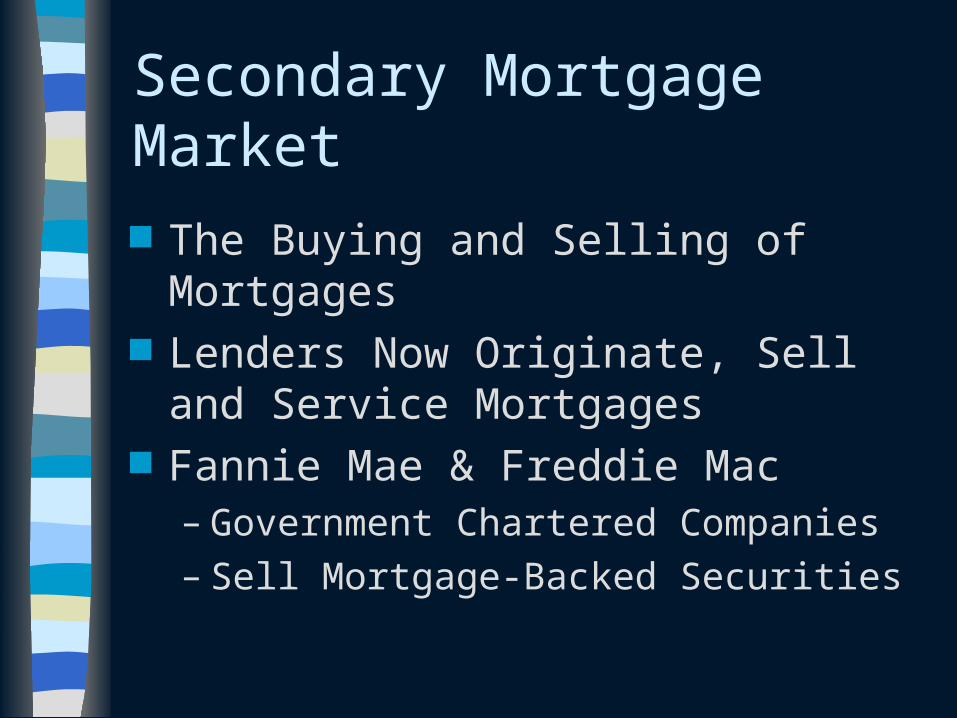

Secondary Mortgage Market

The Buying and Selling of Mortgages Lenders Now Originate, Sell and

Service Mortgages Fannie Mae & Freddie Mac

– Government Chartered Companies – Sell Mortgage-Backed Securities

Types of Loans

Amortized Loan Fixed Rate & Adjustable Loans Balloon Payment Loan Straight Note Insured & Guaranteed Loans

Typical Loan Documents

Promissory Note Deed of Trust Regulatory Agreement

– (assisted housing only)

Promissory Note

Agreement to Repay the Loan– Amount Borrowed– Interest Rate– Repayment Terms– Other Conditions

Between Lender & Borrower

Straight Note

Frequently used for interim financing and seller carry back loans

monthly payments of interest only balloon payment of principal due on specific date or occurance

Straight Note (example)

Borrow agrees to pay Lender $200,000 plus interest at the rate of 12% per annum. Borrow shall make monthly payments of interest only in the amount of $2,000 on the first of each month beginning June 1, 2001. The principal balance shall be due and payable in full on May 1, 2006.

Dated: May 1, 2001 Signed: Borrower

Deed of Trust

Pledge of Real Estate as Collateral for Repayment of the Loan Amount

Recorded Against Property Parties to a Trust Deed

– Borrower (Trustor)– Lender (Beneficiary)– Trustee (Holder of Title)

Typical Loan Conditions

Late Payment Fees Agreements to Maintain Property, Pay

Property Taxes & Carry Insurance Agreements to Perform Other Things Acceleration Clause (Due on Default) Alienation Clause (Due on Sale)

Part III

Purchase Process

Real Estate Purchase Process

Identify Needs Search for Property Gain Site Control Conduct Due Diligence Secure Financing Secure Everything Else Close Escrow

Identify Needs

Desired Location Desired Characteristics Desired Cost Land w/ Zoning & Services Building of Adequate Size on Bus Line

Search for Property

Local Real Estate Brokers Talk with Planning Departments Public/Private Records Research Drive Around Target Areas Contact Property Owners Directly

Gain Site Control

Purchase Contract Option Lease Partner or Joint Venture Disposition & Development Agreement

from Redevelopment Agency

Conduct Due Diligence

Review Title & Clear Exceptions Verify Zoning, Utilities, etc. Conduct Studies

– Environmental Studies/Reviews– Structural Studies– Termite/Pests– Soils Studies

Secure Financing

Loan Commitments Loan Guarantees Grants & Subsidies Make Sure Property Qualifies Make Sure Management Qualifies

Secure Everything Else

Re-Zone, Use Permit, Subdivision Map and/or Development Approvals

Project Design Review Construction/Rehab Plans & Specs Bids from Contractors

Close Escrow

Bring it All Together Satisfy Conditions Exchange Promises Exchange Money Exchange Title

Develop the Property

Whether New Construction, Major Rehab or Less, the Real Work Begins Now...