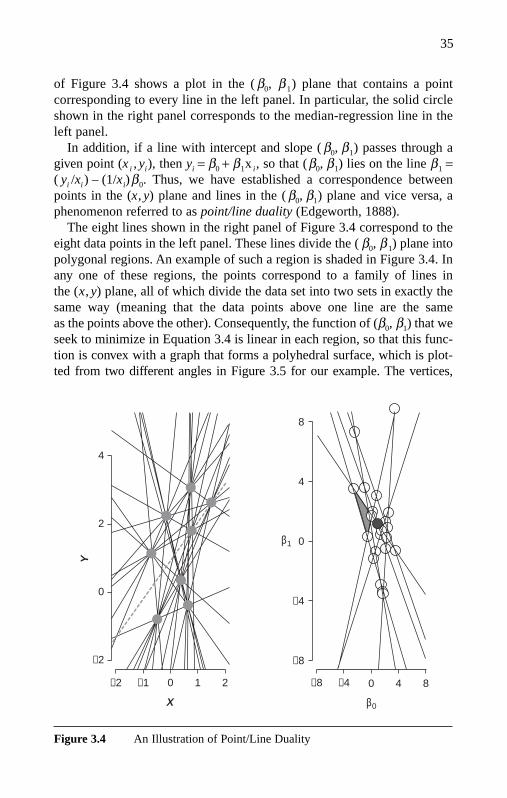

quantitative applications in the social sciences · pdf filequantitative applications in the...

TRANSCRIPT

Quantitative Applications in the Social Sciences

A S AG E P U B L I C AT I O N S S E R I E S

1. Analysis of Variance, 2nd Edition Iversen/Norpoth

2. Operations Research Methods Nagel/Neef3. Causal Modeling, 2nd Edition Asher4. Tests of Significance Henkel5. Cohort Analysis, 2nd Edition Glenn6. Canonical Analysis and Factor

Comparison Levine7. Analysis of Nominal Data, 2nd Edition

Reynolds 8. Analysis of Ordinal Data

Hildebrand/Laing/Rosenthal 9. Time Series Analysis, 2nd Edition Ostrom

10. Ecological Inference Langbein/Lichtman 11. Multidimensional Scaling Kruskal/Wish 12. Analysis of Covariance Wildt/Ahtola 13. Introduction to Factor Analysis

Kim/Mueller 14. Factor Analysis Kim/Mueller 15. Multiple Indicators Sullivan/Feldman 16. Exploratory Data Analysis Hartwig/Dearing 17. Reliability and Validity Assessment

Carmines/Zeller 18. Analyzing Panel Data Markus 19. Discriminant Analysis Klecka 20. Log-Linear Models Knoke/Burke21. Interrupted Time Series Analysis

McDowall/McCleary/Meidinger/Hay22. Applied Regression Lewis-Beck 23. Research Designs Spector 24. Unidimensional Scaling McIver/Carmines 25. Magnitude Scaling Lodge26. Multiattribute Evaluation

Edwards/Newman27. Dynamic Modeling

Huckfeldt/Kohfeld/Likens 28. Network Analysis Knoke/Kuklinski 29. Interpreting and Using Regression Achen 30. Test Item Bias Osterlind31. Mobility Tables Hout 32. Measures of Association Liebetrau33. Confirmatory Factor Analysis Long 34. Covariance Structure Models Long 35. Introduction to Survey Sampling Kalton36. Achievement Testing Bejar 37. Nonrecursive Causal Models Berry38. Matrix Algebra Namboodiri 39. Introduction to Applied Demography

Rives/Serow 40. Microcomputer Methods for Social

Scientists, 2nd Edition Schrodt41. Game Theory Zagare 42. Using Published Data Jacob 43. Bayesian Statistical Inference Iversen 44. Cluster Analysis Aldenderfer/Blashfield45. Linear Probability, Logit, and Probit Models

Aldrich/Nelson

46. Event History Analysis Allison 47. Canonical Correlation Analysis Thompson 48. Models for Innovation Diffusion Mahajan/

Peterson 49. Basic Content Analysis, 2nd Edition

Weber 50. Multiple Regression in Practice Berry/

Feldman 51. Stochastic Parameter Regression Models

Newbold/Bos 52. Using Microcomputers in Research

Madron/Tate/Brookshire 53. Secondary Analysis of Survey Data

Kiecolt/Nathan 54. Multivariate Analysis of Variance

Bray/Maxwell 55. The Logic of Causal Order Davis 56. Introduction to Linear Goal Programming

Ignizio 57. Understanding Regression Analysis

Schroeder/Sjoquist/Stephan 58. Randomized Response Fox/Tracy59. Meta-Analysis Wolf 60. Linear Programming Feiring 61. Multiple Comparisons Klockars/Sax62. Information Theory Krippendorff 63. Survey Questions Converse/Presser 64. Latent Class Analysis McCutcheon 65. Three-Way Scaling and Clustering

Arabie/Carroll/DeSarbo66. Q Methodology McKeown/Thomas 67. Analyzing Decision Making Louviere 68. Rasch Models for Measurement Andrich 69. Principal Components Analysis Dunteman 70. Pooled Time Series Analysis Sayrs 71. Analyzing Complex Survey Data,

2nd Edition Lee/Forthofer72. Interaction Effects in Multiple Regression,

2nd Edition Jaccard/Turrisi73. Understanding Significance Testing Mohr 74. Experimental Design and Analysis Brown/

Melamed 75. Metric Scaling Weller/Romney 76. Longitudinal Research, 2nd Edition

Menard 77. Expert Systems Benfer/Brent/Furbee 78. Data Theory and Dimensional Analysis

Jacoby 79. Regression Diagnostics Fox 80. Computer-Assisted Interviewing Saris 81. Contextual Analysis Iversen 82. Summated Rating Scale Construction

Spector 83. Central Tendency and Variability Weisberg 84. ANOVA: Repeated Measures Girden 85. Processing Data Bourque/Clark 86. Logit Modeling DeMaris

FM-Hao.qxd 3/13/2007 11:20 AM Page i

87. Analytic Mapping and GeographicDatabases Garson/Biggs

88. Working With Archival DataElder/Pavalko/Clipp

89. Multiple Comparison ProceduresToothaker

90. Nonparametric Statistics Gibbons 91. Nonparametric Measures of Association

Gibbons 92. Understanding Regression Assumptions

Berry 93. Regression With Dummy Variables Hardy 94. Loglinear Models With Latent Variables

Hagenaars95. Bootstrapping Mooney/Duval 96. Maximum Likelihood Estimation Eliason 97. Ordinal Log-Linear Models Ishii-Kuntz 98. Random Factors in ANOVA Jackson/

Brashers 99. Univariate Tests for Time Series Models

Cromwell/Labys/Terraza 100. Multivariate Tests for Time Series Models

Cromwell/Hannan/Labys/Terraza 101. Interpreting Probability Models: Logit,

Probit, and Other Generalized LinearModels Liao

102. Typologies and Taxonomies Bailey103. Data Analysis: An Introduction

Lewis-Beck104. Multiple Attribute Decision Making

Yoon/Hwang105. Causal Analysis With Panel Data Finkel106. Applied Logistic Regression Analysis,

2nd Edition Menard107. Chaos and Catastrophe Theories Brown108. Basic Math for Social Scientists:

Concepts Hagle 109. Basic Math for Social Scientists:

Problems and Solutions Hagle110. Calculus Iversen111. Regression Models: Censored, Sample

Selected, or Truncated Data Breen112. Tree Models of Similarity and Association

James E. Corter113. Computational Modeling Taber/Timpone114. LISREL Approaches to Interaction Effects

in Multiple Regression Jaccard/Wan115. Analyzing Repeated Surveys Firebaugh116. Monte Carlo Simulation Mooney117. Statistical Graphics for Univariate and

Bivariate Data Jacoby118. Interaction Effects in Factorial Analysis

of Variance Jaccard

119. Odds Ratios in the Analysis ofContingency Tables Rudas

120. Statistical Graphics for VisualizingMultivariate Data Jacoby

121. Applied Correspondence AnalysisClausen

122. Game Theory Topics Fink/Gates/Humes123. Social Choice: Theory and Research

Johnson124. Neural Networks Abdi/Valentin/Edelman 125. Relating Statistics and Experimental

Design: An Introduction Levin 126. Latent Class Scaling Analysis Dayton 127. Sorting Data: Collection and Analysis

Coxon 128. Analyzing Documentary Accounts

Hodson 129. Effect Size for ANOVA Designs

Cortina/Nouri 130. Nonparametric Simple Regression:

Smoothing Scatterplots Fox 131. Multiple and Generalized Nonparametric

Regression Fox 132. Logistic Regression: A Primer Pampel 133. Translating Questionnaires and Other

Research Instruments: Problems andSolutions Behling/Law

134. Generalized Linear Models: A UnitedApproach Gill

135. Interaction Effects in Logistic RegressionJaccard

136. Missing Data Allison 137. Spline Regression Models Marsh/Cormier 138. Logit and Probit: Ordered and

Multinomial Models Borooah 139. Correlation: Parametric and

Nonparametric MeasuresChen/Popovich

140. Confidence Intervals Smithson 141. Internet Data Collection Best/Krueger142. Probability Theory Rudas 143. Multilevel Modeling Luke 144. Polytomous Item Response Theory

Models Ostini/Nering 145. An Introduction to Generalized Linear

Models Dunteman/Ho 146. Logistic Regression Models for Ordinal

Response Variables O’Connell 147. Fuzzy Set Theory: Applications in the

Social Sciences Smithson/Verkuilen 148. Multiple Time Series Models

Brandt/Williams149. Quantile Regression Hao/Naiman

Quantitative Applications in the Social Sciences

A S AG E P U B L I C AT I O N S S E R I E S

FM-Hao.qxd 3/13/2007 11:20 AM Page ii

Series/Number 07–149

QUANTILE REGRESSION

LINGXIN HAOThe Johns Hopkins University

DANIEL Q. NAIMANThe Johns Hopkins University

FM-Hao.qxd 3/13/2007 11:20 AM Page iii

Copyright © 2007 by Sage Publications, Inc.

All rights reserved. No part of this book may be reproduced or utilized in any form or by anymeans, electronic or mechanical, including photocopying, recording, or by any informationstorage and retrieval system, without permission in writing from the publisher.

For information:

Sage Publications, Inc.2455 Teller RoadThousand Oaks, California 91320E-mail: [email protected]

Sage Publications Ltd.1 Oliver’s Yard55 City RoadLondon EC1Y 1SPUnited Kingdom

Sage Publications India Pvt. Ltd.B 1/l 1 Mohan Cooperative Industrial AreaMathura Road, New Delhi 110 044India

Sage Publications Asia-Pacific Pte. Ltd.33 Pekin Street #02-01Far East SquareSingapore 048763

Printed in the United States of America.

Library of Congress Cataloging-in-Publication Data

Hao, Lingxin, 1949–Quantile regression / Lingxin Hao, Daniel Q. Naiman.

p. cm.—(Quantitative applications in the social sciences; 149)Includes bibliographical references and index.ISBN 978-1-4129-2628-7 (pbk.)

1. Social sciences—Statistical methods. 2. Regression analysis.I. Naiman, Daniel Q. II. Title.HA31.3.H36 2007519.5′36—dc22

2006035964

This book is printed on acid-free paper.

07 08 09 10 11 10 9 8 7 6 5 4 3 2 1

Acquisitions Editor: Lisa Cuevas ShawAssociate Editor: Sean ConnellyEditorial Assistant: Karen GreeneProduction Editor: Melanie BirdsallCopy Editor: Kevin BeckTypesetter: C&M Digitals (P) Ltd.Proofreader: Cheryl RivardIndexer: Sheila BodellCover Designer: Candice HarmanMarketing Manager: Stephanie Adams

FM-Hao.qxd 3/13/2007 11:20 AM Page iv

CONTENTS

Series Editor’s Introduction vii

Acknowledgments ix

1. Introduction 1

2. Quantiles and Quantile Functions 7

CDFs, Quantiles, and Quantile Functions 7Sampling Distribution of a Sample Quantile 11Quantile-Based Measures of Location and Shape 12Quantile as a Solution to a Certain Minimization Problem 14Properties of Quantiles 19Summary 20Note 20Chapter 2 Appendix: A Proof: Median and Quantiles

as Solutions to a Minimization Problem 21

3. Quantile-Regression Model and Estimation 22

Linear-Regression Modeling and Its Shortcomings 22Conditional-Median and Quantile-Regression Models 29QR Estimation 33Transformation and Equivariance 38Summary 42Notes 42

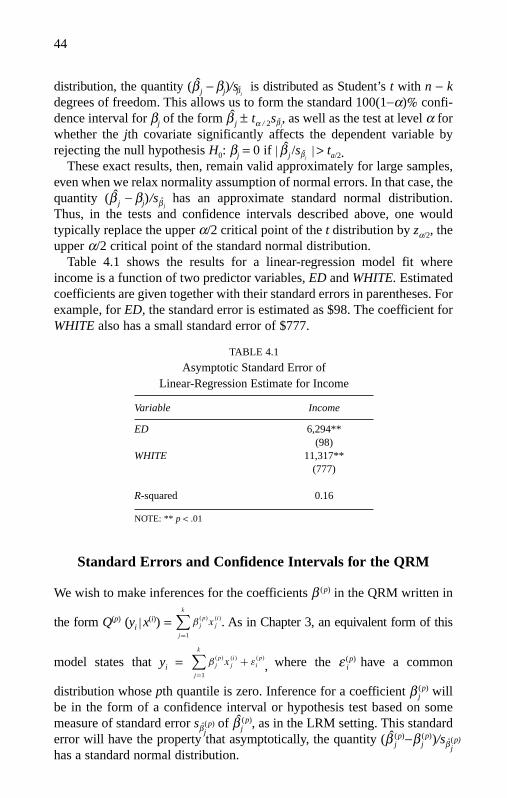

4. Quantile-Regression Inference 43

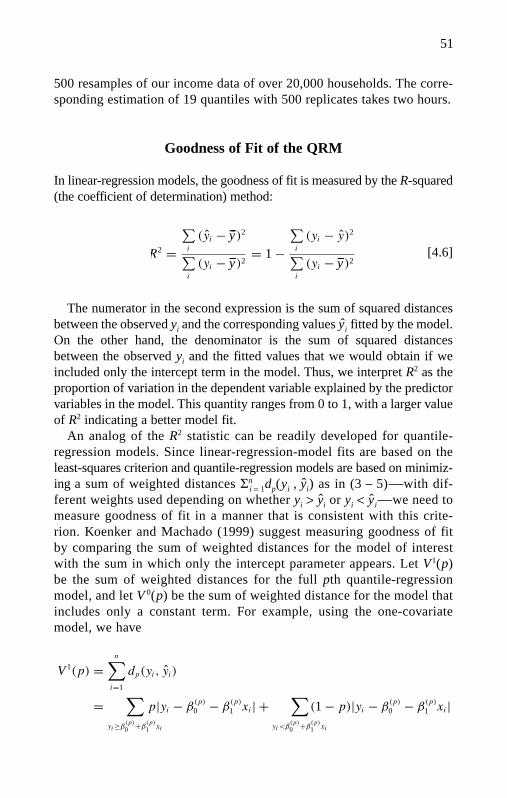

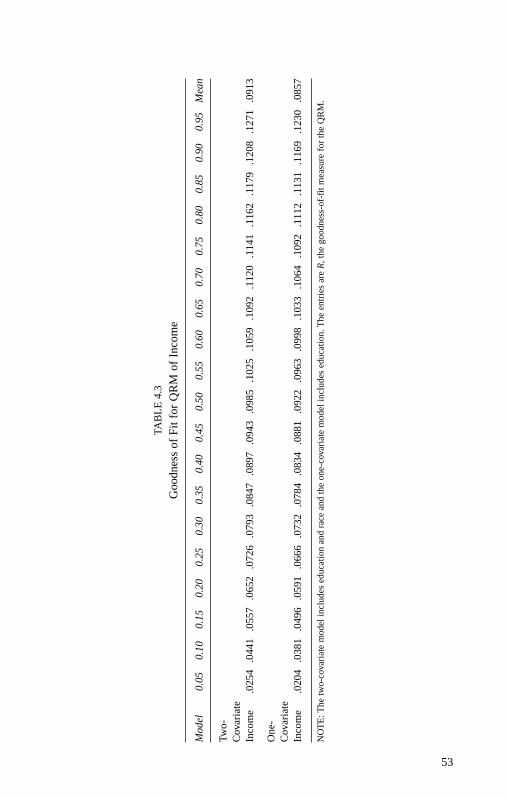

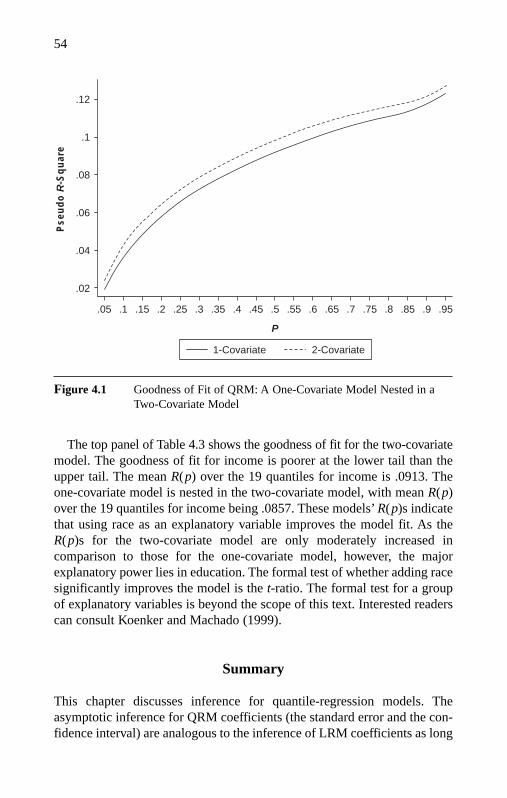

Standard Errors and Confidence Intervals for the LRM 43Standard Errors and Confidence Intervals for the QRM 44The Bootstrap Method for the QRM 47Goodness of Fit of the QRM 51Summary 54Note 55

FM-Hao.qxd 3/13/2007 11:20 AM Page v

5. Interpretation of Quantile-Regression Estimates 55

Reference and Comparison 56Conditional Means Versus Conditional Medians 56Interpretation of Other Individual Conditional Quantiles 59Tests for Equivalence of Coefficients Across Quantiles 60Using the QRM Results to Interpret Shape Shifts 63Summary 76Notes 76

6. Interpretation of Monotone-Transformed QRM 77

Location Shifts on the Log Scale 78From Log Scale Back to Raw Scale 78Graphical View of Log-Scale Coefficients 86Shape-Shift Measures From Log-Scale Fits 88Summary 91Notes 91

7. Application to Income Inequality in 1991 and 2001 92

Observed Income Disparity 92Descriptive Statistics 96Notes on Survey Income Data 97Goodness of Fit 97Conditional-Mean Versus Conditional-Median Regression 98Graphical View of QRM Estimates From Income and

Log-Income Equations 100Quantile Regressions at Noncentral Positions:

Effects in Absolute Terms 105Assessing a Covariate’s Effect on Location and Shape Shifts 107Summary 112

Appendix: Stata Codes 113

References 121

Index 123

About the Authors 126

FM-Hao.qxd 3/13/2007 11:20 AM Page vi

vii

SERIES EDITOR’S INTRODUCTION

The classical linear-regression model has been part and parcel of aquantitative social scientist’s methodology for at least four decades. TheQuantitative Applications in the Social Sciences series has covered the topicwell, with at least the following numbers focused centrally on the classicallinear regression: Nos. 22, 29, 50, 57, 79, 92, and 93. There are manymore treatments in the series of various extensions of the linear regression,such as logit, probit, event history, generalized linear, and generalized non-parametric models as well as linear-regression models of censored, sample-selected, truncated, and missing data, as well as many other related methods,including analysis of variance, analysis of covariance, causal modeling,log-linear modeling, multiple comparisons, and time-series analysis.

The central aim of the classical regression is to estimate the meansof a response variable conditional on the values of the explanatory vari-ables. This works well when regression assumptions are met, but notwhen conditions are nonstandard. (For a thorough discussion of linear-regression assumptions, see No. 92, Understanding Regression Assump-tions, by William Berry.) Two of them are the normality assumption and thehomoscedasticity assumption. These two crucial assumptions may not besatisfied by some common social-science data. For example, (conditional)income distributions are seldom normal, and the dispersion of the annualcompensations of chief executive officers tends to increase with firm size,an indication of heteroscedasticity. This is where quantile regression canhelp because it relaxes these assumptions. In addition, quantile regressionoffers the researcher a view—unobtainable through the classical regression—of the effect of explanatory variables on the (central and noncentral) loca-tion, scale, and shape of the distribution of the response variable.

The idea of quantile regression is not new, and in fact goes back to 1760,when the itinerant Croatian Jesuit Rudjer Josip Boscovich—a man whowore many hats including those of a physicist, an astronomer, a diplomat, aphilosopher, a poet, and a mathematician—went to London for computa-tional advice for his nascent method of median regression. However, thecomputational difficulty for such regression analysis posed a huge chal-lenge until recent years. With today’s fast computers and wide availability ofstatistical software packages such as R, SAS, and Stata that implementthe quantile-regression procedure, fitting a quantile-regression model todata has become easy. However, we have so far had no introduction inthe series to the method to explain what quantile regression is all about.

FM-Hao.qxd 3/13/2007 11:20 AM Page vii

Hao and Naiman’s Quantile Regression is a truly welcome addition tothe series. They present the concept of quantiles and quantile functions,specify the quantile-regression model, discuss its estimation and infer-ence, and demonstrate the interpretation of quantile-regression estimates—transformed and not—with clear examples. They also provide a completeexample of applying quantile regression to the analysis of income inequal-ity in the United States in 1991 and 2001, to help fix the ideas and proce-dures. This book, then, fills a gap in the series and will help make quantileregression more accessible to many social scientists.

—Tim F. LiaoSeries Editor

viii

FM-Hao.qxd 3/13/2007 11:20 AM Page viii

ACKNOWLEDGMENTS

Lingxin first became interested in using quantile regression to study race,immigration, and wealth stratification after learning of Buchinsky’s work(1994), which applied quantile regression to wage inequality. This interestled to frequent discussions about methodological and mathematical issuesrelated to quantile regression with Dan, who had first learned about the sub-ject as a graduate student under Steve Portnoy at the University of Illinois.In the course of our conversations, we agreed that an empirically orientedintroduction to quantile regression would be vital to the social-scienceresearch community. Particularly, it would provide easier access to neces-sary tools for social scientists who seek to uncover the impact of socialfactors on not only the mean but also the shape of a response distribution.

We gratefully acknowledge our colleagues in the Departments of Sociologyand Applied Mathematics and Statistics at The Johns Hopkins Universityfor their enthusiastic encouragement and support. In addition, we are grate-ful for the aid that we received from the Acheson J. Duncan Fund for theAdvancement of Research in Statistics. Our gratitude further extends toadditional support from the attendees of seminars at various universitiesand from the Sage QASS editor, Dr. Tim F. Liao. Upon the completion ofthe book, we wish to acknowledge the excellent research and editorialassistance from Xue Mary Lin, Sahan Savas Karatasli, Julie J. H. Kim, andCaitlin Cross-Barnet. The two anonymous reviewers of the manuscript alsoprovided us with extremely helpful comments and beneficial suggestions,which led to a much-improved version of this book. Finally, we dedicatethis book to our respective parents, who continue to inspire us.

ix

FM-Hao.qxd 3/13/2007 11:20 AM Page ix

FM-Hao.qxd 3/13/2007 11:20 AM Page x

QUANTILE REGRESSION

Lingxin HaoThe Johns Hopkins University

Daniel Q. NaimanThe Johns Hopkins University

1. INTRODUCTION

The purpose of regression analysis is to expose the relationship between aresponse variable and predictor variables. In real applications, the responsevariable cannot be predicted exactly from the predictor variables. Instead,the response for a fixed value of each predictor variable is a random vari-able. For this reason, we often summarize the behavior of the response forfixed values of the predictors using measures of central tendency. Typicalmeasures of central tendency are the average value (mean), the middle value(median), or the most likely value (mode).

Traditional regression analysis is focused on the mean; that is, wesummarize the relationship between the response variable and predictorvariables by describing the mean of the response for each fixed value ofthe predictors, using a function we refer to as the conditional mean of theresponse. The idea of modeling and fitting the conditional-mean function isat the core of a broad family of regression-modeling approaches, includingthe familiar simple linear-regression model, multiple regression, modelswith heteroscedastic errors using weighted least squares, and nonlinear-regression models.

Conditional-mean models have certain attractive properties. Under idealconditions, they are capable of providing a complete and parsimoniousdescription of the relationship between the covariates and the response dis-tribution. In addition, using conditional-mean models leads to estimators(least squares and maximum likelihood) that possess attractive statisticalproperties, are easy to calculate, and are straightforward to interpret. Such

1

01-Hao.qxd 3/13/2007 3:28 PM Page 1

models have been generalized in various ways to allow for heteroscedasticerrors so that given the predictors, modeling of the conditional mean andconditional scale of the response can be carried out simultaneously.

Conditional-mean modeling has been applied widely in the social sci-ences, particularly in the past half century, and regression modeling of therelationship between a continuous response and covariates via least squaresand its generalization is now seen as an essential tool. More recently, mod-els for binary response data, such as logistic and probit models and Poissonregression models for count data, have become increasingly popular in social-science research. These approaches fit naturally within the conditional-mean modeling framework. While quantitative social-science researchershave applied advanced methods to relax some basic modeling assumptionsunder the conditional-mean framework, this framework itself is seldomquestioned.

The conditional-mean framework has inherent limitations. First, whensummarizing the response for fixed values of predictor variables, theconditional-mean model cannot be readily extended to noncentral locations,which is precisely where the interests of social-science research oftenreside. For instance, studies of economic inequality and mobility haveintrinsic interest in the poor (lower tail) and the rich (upper tail). Educationalresearchers seek to understand and reduce group gaps at preestablishedachievement levels (e.g., the three criterion-referenced levels: basic, pro-ficient, and advanced). Thus, the focus on the central location has longdistracted researchers from using appropriate and relevant techniques toaddress research questions regarding noncentral locations on the responsedistribution. Using conditional-mean models to address these questions maybe inefficient or even miss the point of the research altogether.

Second, the model assumptions are not always met in the real world.In particular, the homoscedasticity assumption frequently fails, andfocusing exclusively on central tendencies can fail to capture informa-tive trends in the response distribution. Also, heavy-tailed distributionscommonly occur in social phenomena, leading to a preponderance ofoutliers. The conditional mean can then become an inappropriate andmisleading measure of central location because it is heavily influencedby outliers.

Third, the focal point of central location has long steered researchers’attention away from the properties of the whole distribution. It is quite natural to go beyond location and scale effects of predictor variables on theresponse and ask how changes in the predictor variables affect the underlyingshape of the distribution of the response. For example, much social-scienceresearch focuses on social stratification and inequality, areas that require

2

01-Hao.qxd 3/13/2007 3:28 PM Page 2

close examination of the properties of a distribution. The central location,the scale, the skewness, and other higher-order properties—not central loca-tion alone—characterize a distribution. Thus, conditional-mean models are inherently ill equipped to characterize the relationship between a responsedistribution and predictor variables. Examples of inequality topics include economic inequality in wages, income, and wealth; educational inequality inacademic achievement; health inequality in height, weight, incidence of dis-ease, drug addiction, treatment, and life expectancy; and inequality in well-being induced by social policies. These topics have often been studied underthe conditional-mean framework, while other, more relevant distributionalproperties have been ignored.

An alternative to conditional-mean modeling has roots that can be tracedto the mid-18th century. This approach can be referred to as conditional-median modeling, or simply median regression. It addresses some of theissues mentioned above regarding the choice of a measure of central ten-dency. The method replaces least-squares estimation with least-absolute-distance estimation. While the least-squares method is simple to implementwithout high-powered computing capabilities, least-absolute-distance esti-mation demands significantly greater computing power. It was not until thelate 1970s, when computing technology was combined with algorithmicdevelopments such as linear programming, that median-regression model-ing via least-absolute-distance estimation became practical.

The median-regression model can be used to achieve the same goal as conditional-mean-regression modeling: to represent the relationshipbetween the central location of the response and a set of covariates. However,when the distribution is highly skewed, the mean can be challenging tointerpret while the median remains highly informative. As a consequence,conditional-median modeling has the potential to be more useful.

The median is a special quantile, one that describes the central loca-tion of a distribution. Conditional-median regression is a special case ofquantile regression in which the conditional .5th quantile is modeledas a function of covariates. More generally, other quantiles can be usedto describe noncentral positions of a distribution. The quantile notiongeneralizes specific terms like quartile, quintile, decile, and percentile.The pth quantile denotes that value of the response below which theproportion of the population is p. Thus, quantiles can specify any positionof a distribution. For example, 2.5% of the population lies below the.025th quantile.

Koenker and Bassett (1978) introduced quantile regression, which mod-els conditional quantiles as functions of predictors. The quantile-regressionmodel is a natural extension of the linear-regression model. While the

3

01-Hao.qxd 3/13/2007 3:28 PM Page 3

linear-regression model specifies the change in the conditional mean of thedependent variable associated with a change in the covariates, the quantile-regression model specifies changes in the conditional quantile. Since anyquantile can be used, it is possible to model any predetermined position ofthe distribution. Thus, researchers can choose positions that are tailored totheir specific inquiries. Poverty studies concern the low-income population;for example, the bottom 11.3% of the population lived in poverty in 2000(U.S. Census Bureau, 2001). Tax-policy studies concern the rich, forexample, the top 4% of the population (Shapiro & Friedman, 2001).Conditional-quantile models offer the flexibility to focus on these popula-tion segments whereas conditional-mean models do not.

Since multiple quantiles can be modeled, it is possible to achieve amore complete understanding of how the response distribution is affectedby predictors, including information about shape change. A set of equallyspaced conditional quantiles (e.g., every 5% or 1% of the population) cancharacterize the shape of the conditional distribution in addition to itscentral location. The ability to model shape change provides a significantmethodological leap forward in social research on inequality. Traditionally,inequality studies are non-model based; approaches include the Lorenzcurve, the Gini coefficient, Theil’s measure of entropy, the coefficient ofvariation, and the standard deviation of the log-transformed distribution. Inanother book for the Sage QASS series, we will develop conditional Lorenzand Gini coefficients, as well as other inequality measures based on quantile-regression models.

Quantile-regression models can be easily fit by minimizing a generalizedmeasure of distance using algorithms based on linear programming. As aresult, quantile regression is now a practical tool for researchers. Softwarepackages familiar to social scientists offer readily accessed commands forfitting quantile-regression models.

A decade and a half after Koenker and Bassett first introduced quantileregression, empirical applications of quantile regression started to growrapidly. Empirical researchers took advantage of quantile regression’sability to examine the impact of predictor variables on the response dis-tribution. Two of the earliest empirical papers by economists (Buchinsky,1994; Chamberlain, 1994) provided practical examples of how to applyquantile regression to the study of wages. Quantile regression allowedthem to examine the entire conditional distribution of wages and deter-mine if the returns to schooling, and experience and the effects of unionmembership differed across wage quantiles. The use of quantile regres-sion to analyze wages increased and expanded to address additional top-ics such as changes in wage distribution (Machado & Mata, 2005; Melly,

4

01-Hao.qxd 3/13/2007 3:28 PM Page 4

2005), wage distributions within specific industries (Budd & McCall,2001), wage gaps between whites and minorities (Chay & Honore, 1998)and between men and women (Fortin & Lemieux, 1998), educationalattainment and wage inequality (Lemieux, 2006), and the intergenerationaltransfer of earnings (Eide & Showalter, 1999). The use of quantile regres-sion also expanded to address the quality of schooling (Bedi & Edwards,2002; Eide, Showalter, & Sims, 2002) and demographics’ impact oninfant birth weight (Abreveya, 2001). Quantile regression also spread toother fields, notably sociology (Hao, 2005, 2006a, 2006b), ecology andenvironmental sciences (Cade, Terrell, & Schroeder, 1999; Scharf,Juanes, & Sutherland, 1989), and medicine and public health (Austin et al., 2005; Wei et al., 2006).

This book aims to introduce the quantile-regression model to a broadaudience of social scientists who are interested in modeling both the loca-tion and shape of the distribution they wish to study. It is also written forreaders who are concerned about the sensitivity of linear-regression modelsto skewed distributions and outliers. The book builds on the basic literatureof Koenker and his colleagues (e.g., Koenker, 1994; Koenker, 2005;Koenker & Bassett, 1978; Koenker & d’Orey, 1987; Koenker & Hallock,2001; Koenker & Machado, 1999) and makes two further contributions. Wedevelop conditional-quantile-based shape-shift measures based on quantile-regression estimates. These measures provide direct answers to researchquestions about a covariate’s impact on the shape of the response distribu-tion. In addition, inequality research often uses log transformation of right-skewed responses to create a better model fit even though “inequality” inthis case refers to raw-scale distributions. Therefore, we develop methods toobtain a covariate’s effect on the location and shape of conditional-quantilefunctions in absolute terms from log-scale coefficients.

Drawn from our own research experience, this book is oriented towardthose involved with empirical research. We take a didactic approach, usinglanguage and procedures familiar to social scientists. These include clearlydefined terms, simplified equations, illustrative graphs, tables and graphsbased on empirical data, and computational codes using statistical softwarepopular among social scientists. Throughout the book, we draw examplesfrom our own research on household income distribution. In order to pro-vide a gentle introduction to quantile regression, we use simplified modelspecifications wherein the conditional-quantile functions for the raw or logresponses are linear and additive in the covariates. As in linear regression,the methodology we present is easily adapted to more complex model spec-ifications, including, for example, interaction terms and polynomial or splinefunctions of covariates.

5

01-Hao.qxd 3/13/2007 3:28 PM Page 5

Quantile-regression modeling provides a natural complement to model-ing approaches dealt with extensively in the QASS series: UnderstandingRegression Assumptions (Berry, 1993), Understanding Regression Analysis(Schroeder, 1986), and Multiple Regression in Practice (Berry & Feldman,1985). Other books in the series can be used as references to some of thetechniques discussed in this book, e.g., Bootstrapping (Mooney, 1993) andLinear Programming (Feiring, 1986).

The book is organized as follows. Chapter 2 defines quantiles and quantilefunctions in two ways—using the cumulative distribution function and solv-ing a minimization problem. It also develops quantile-based measures oflocation and shape of a distribution in comparison with distributional moments(e.g., mean, standard deviation). Chapter 3 introduces the basics of thequantile-regression model (QRM) in comparison with the linearregres-sion model, including the model setup, the estimator, and properties. Thenumerous quantile-regression equations with quantile-specific parametersare a unique feature of the quantile-regression model. We describe howquantile-regression fits are obtained by making use of the minimum dis-tance principle. The QRM possesses properties such as monotonic equivari-ance and robustness to distributional assumptions, which produce flexible,nonsensitive estimates, properties that are absent in the linear-regressionmodel. Chapter 4 discusses inferences for the quantile-regression model. Inaddition to introducing the asymptotic inference for quantile-regressioncoefficients, the chapter emphasizes the utility and feasibility of the boot-strap method. In addition, this chapter briefly discusses goodness of fit forquantile-regression models, analogous to that for linear-regression models.Chapter 5 develops various ways to interpret estimates from the quantile-regression model. Going beyond the traditional examination of the effectof a covariate on specific conditional quantiles, such as the median or off-central quantiles, Chapter 5 focuses on a distributional interpretation. Itillustrates graphical interpretations of quantile-regression estimates andquantitative measures of shape changes from quantile-regression estimates,including location shifts, scale shifts, and skewness shifts. Chapter 6 con-siders issues related to monotonically transformed response variables. Wedevelop two ways to obtain a covariate’s effect on the location and shapeof conditional-quantile functions in absolute terms from log-scale coeffi-cients. Chapter 7 presents a systematic application of the techniques intro-duced and developed in the book. This chapter analyzes the sources of thepersistent and widening income inequality in the United States between1991 and 2001. Finally, the Appendix provides Stata codes for performingthe analytic tasks described in Chapter 7.

6

01-Hao.qxd 3/13/2007 3:28 PM Page 6

2. QUANTILES AND QUANTILE FUNCTIONS

Describing and comparing the distributional attributes of populations isessential to social science. The simplest and most familiar measures used todescribe a distribution are the mean for the central location and the standarddeviation for the dispersion. However, restricting attention to the mean andstandard deviation alone leads us to ignore other important properties thatoffer more insight into the distribution. For many researchers, attributes ofinterest often have skewed distributions, for which the mean and standarddeviation are not necessarily the best measures of location and shape. To characterize the location and shape of asymmetric distributions, thischapter introduces quantiles, quantile functions, and their properties byway of the cumulative distribution function (cdf). It also develops quantile-based measures of location and shape of a distribution and, finally, rede-fines a quantile as a solution to a certain minimization problem.

CDFs, Quantiles, and Quantile Functions

To describe the distribution of a random variable Y, we can use its cumulativedistribution function (cdf). The cdf is the function FY that gives, for eachvalue of y, the proportion of the population for which Y ≤ y. Figure 2.1 showsthe cdf for the standard normal distribution. The cdf can be used to calculatethe proportion of the population for any range of values of y. We see in Figure2.1 that FY(0) = .5 and FY (1.28) = .9. The cdf can be used to calculate all otherprobabilities involving Y. In particular: P[Y > y] = 1 − Fy (y) (e.g., in Figure 2.1,P[Y > 1.28] = 1 − Fy (1.28) = 1 − 0.9 = 0.1) and P[a < Y ≤ b] = FY (b) − FY (a)(e.g., in Figure 2.1, P[0 ≤ Y ≤ 1.28] = FY (1.28) − FY (0) = 0.40)). The twomost important properties of a cdf are monotonicity (i.e., F ( y1) ≤ F(y2 )whenever y1 ≤ y2) and its behavior at infinity limy→−∞ F(y) = 0 andlimy→+∞ F (y) = 1. For a continuous random variable Y, we can also representits distribution using a probability density function fy defined as the functionwith the property that P[a ≤ Y ≤ b] = ∫b

y = a fY dy for all choices of a and b.Returning to the issue of the inadequacy of location and spread for fully

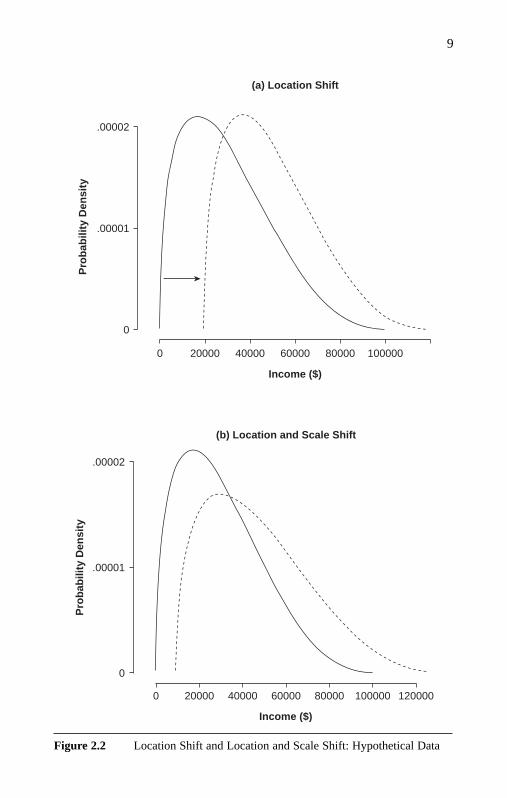

describing a distribution, suppose we are told that the mean householdincome for whites (W) exceeds that of blacks (B) by $20,500. This could bedescribed simply by a shift in the location of the distribution while retain-ing the shape (see the corresponding density functions in Figure 2.2a),so that the relationship between the distributions is expressed byFB(y) = F W(y − 20,500). The difference in distributions may consist of achange in both location and scale (see the corresponding density functionsin Figure 2.2b), so that the relationship between the distributions takes thegeneral form FB(y) = F W(ay − c) for constants a and c (a > 0). This is the

7

02-Hao.qxd 3/13/2007 4:29 PM Page 7

case when both the mean and the variance of y differ between populationsW and B. Knowledge of measures of location and scale, for example, themean and standard deviation, or alternatively the median and interquartilerange, enables us to compare the attribute Y between the two distributions.

As distributions become less symmetrical, more complex summarymeasures are needed. Consideration of quantiles and quantile functionsleads to a rich collection of summary measures. Continuing the discussionof a cdf, F, for some population attribute, the pth quantile of this distribu-tion, denoted by Q (p)(F) (or simply Q (p) when it is clear what distribution isbeing discussed), is the value of the inverse of the cdf at p, that is, a valueof y such that F (y) = p. Thus, the proportion of the population with anattribute below Q (p) is p. For example, in the standard normal case (seeFigure 2.1), F(1.28) = .9, so Q(.9) = 1.28, that is, the proportion of the pop-ulation with the attribute below 1.28 is .9 or 90%.

Analogous to the population cdf, we consider the empirical or sample cdfassociated with a sample. For a sample consisting of values y1, y2, . . . , yn,the empirical cdf gives the proportion of the sample values that is less thanor equal to any given y. More formally, the empirical cdf F is defined by

F(y) = the proportion of sample values less than or equal to y.

As an example, consider a sample consisting of 20 households withincomes of $3,000, $3,500, $4,000, $4,300, $4,600, $5,000, $5,000, $5,000,$8,000, $9,000, $10,000, $11,000, $12,000, $15,000, $17,000, $20,000,

8

.0−3 −2 −1 0 1 2 3

.2

.4

.6

.8

.9

1

.5F(y

)

Y

Q(.9)

Figure 2.1 The CDF for the Standard Normal Distribution

02-Hao.qxd 3/13/2007 4:29 PM Page 8

9

Pro

bab

ility

Den

sity

Income ($)

(a) Location Shift

.00001

.00002

0

0 20000 40000 60000 80000 100000

Figure 2.2 Location Shift and Location and Scale Shift: Hypothetical Data

Pro

bab

ility

Den

sity

Income ($)

.00001

.00002

0

0 20000 40000 60000 80000 100000 120000

(b) Location and Scale Shift

02-Hao.qxd 3/13/2007 4:29 PM Page 9

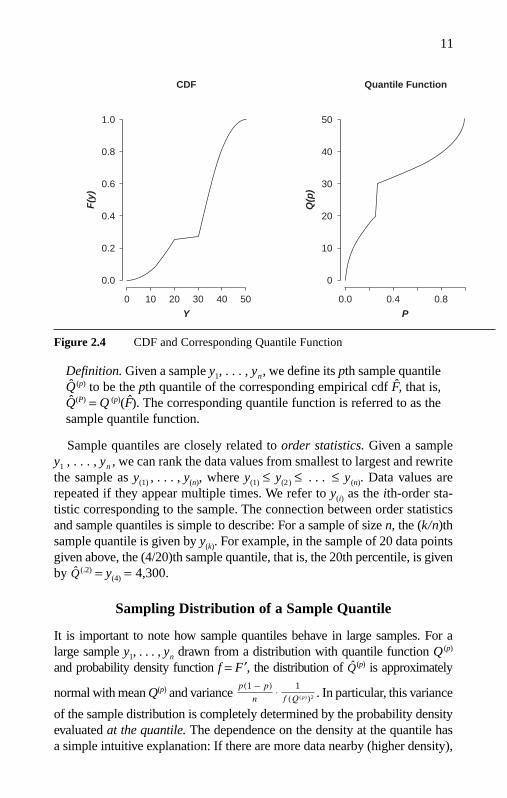

$32,000, $38,000, $56,000, and $84,000. Since there are eight householdswith incomes at or below $5,000, we have F(5,000) = 8/20. A plot of theempirical cdf is shown in Figure 2.3, which consists of one jump and severalflat parts. For example, there is a jump of size 3/20 at 5,000, indicating thatthe value of 5,000 appears three times in the sample. There are also flat partssuch as the portion between 56,000 and 84,000, indicating that there are nosample values in the interior of this interval. Since the empirical cdf can beflat, there are values having multiple inverses. For example, in Figure 2.3there appears to be a continuum of choices for Q (.975) between 56,000 and84,000. Thus, we need to exercise some care when we introduce quantilesand quantile functions for a general distribution with the following definition:

Definition. The pth quantile Q (p) of a cdf F is the minimum of the setof values y such that F (y) ≥ p. The function Q (p) (as a function of p) isreferred to as the quantile function of F.

Figure 2.4 shows an example of a quantile function and the correspond-ing cdf. Observe that the quantile function is a monotonic nondecreasingfunction that is continuous from below.

As a special case we can talk about sample quantiles, which can be usedto estimate quantiles of a sampled distribution.

10

flat for incomes between$56,000 and $84,000

jump of size3/20 at $5,000

20000 40000 60000 80000 1000000

0.2

0.4

0.6

0.8

1.0

Fre

qu

ency

Income ($)

Figure 2.3 CDF With Jumps and Flat Parts

02-Hao.qxd 3/13/2007 4:29 PM Page 10

Definition. Given a sample y1, . . . , yn, we define its pth sample quantileQ (p) to be the pth quantile of the corresponding empirical cdf F, that is,Q(P) = Q (p)(F). The corresponding quantile function is referred to as thesample quantile function.

Sample quantiles are closely related to order statistics. Given a sampley1 , . . . , yn , we can rank the data values from smallest to largest and rewritethe sample as y(1) , . . . , y(n), where y(1) ≤ y(2) ≤ . . . ≤ y(n). Data values arerepeated if they appear multiple times. We refer to y(i) as the ith-order sta-tistic corresponding to the sample. The connection between order statisticsand sample quantiles is simple to describe: For a sample of size n, the (k/n)thsample quantile is given by y(k). For example, in the sample of 20 data pointsgiven above, the (4/20)th sample quantile, that is, the 20th percentile, is givenby Q (.2) = y(4) = 4,300.

Sampling Distribution of a Sample Quantile

It is important to note how sample quantiles behave in large samples. For alarge sample y1, . . . , yn drawn from a distribution with quantile function Q (p)

and probability density function f = F′, the distribution of Q(p) is approximately

normal with mean Q(p) and variance . In particular, this variance

of the sample distribution is completely determined by the probability densityevaluated at the quantile. The dependence on the density at the quantile hasa simple intuitive explanation: If there are more data nearby (higher density),

p(1 − p)

n· 1

f (Q(p))2

11

0 10 20 30 40 50

Y

0.0

0.2

0.4

0.6

0.8

1.0

F(y

)

PQ

(p)

0.0 0.4 0.8

0

10

20

30

40

50

CDF Quantile Function

Figure 2.4 CDF and Corresponding Quantile Function

02-Hao.qxd 3/13/2007 4:29 PM Page 11

the sample quantile is less variable; conversely, if there are fewer data nearby(low density), the sample quantile is more variable.

To estimate the quantile sampling variability, we make use of the varianceapproximation above, which requires a way of estimating the unknownprobability density function. A standard approach to this estimation is illus-trated in Figure 2.5, where the slope of the tangent line to the function Q(p)

at the point p is the derivative of the quantile function with respect to p, or

equivalently, the inverse density function: = 1/f(Q(p)). This term can be

approximated by the difference quotient , which is the slope

of the secant line through the points (p − h, Q(p − h)) and (p + h, Q(p + h)) forsome small value of h.

Quantile-Based Measures of Location and Shape

Social scientists are familiar with the quantile-based measure of centrallocation; namely, instead of the mean (the first moment of a density func-tion), the median (i.e., the .5th quantile) has been used to indicate the

1

2h(Q(p+h) − Q(p−h))

d

dpQ(p)

12

Q(p0+h)

Q(p0+h) − Q(p0−h)

Q(p0−h)

p0−h p0+hp0

Q(p0)

secantline tangent

line

Q(p)

P

2h

Figure 2.5 Illustrating How to Estimate the Slope of a Quantile Function

NOTE: The derivative of the function Q(p) at the point p0 (the slope of the tangent line) is approximated bythe slope of the secant line, which is (Q(p

0+ h) − Q(p

0− h))/2h.

02-Hao.qxd 3/13/2007 4:29 PM Page 12

center of a skewed distribution. Using quantile-based location allows oneto investigate more general notions of location beyond just the center of adistribution. Specifically, we can examine a location at the lower tail (e.g.,the .1th quantile) or a location at the upper tail (e.g., the .9th quantile) forresearch questions regarding specific subpopulations.

Two basic properties describe the shape of a distribution: scale and skew-ness. Traditionally, scale is measured by the standard deviation, which is basedon the second moment of a distribution involving a quadratic function of thedeviations of data points from the mean. This measure is easy to interpret fora symmetric distribution, but when the distribution becomes highly asymmet-ric, its interpretation tends to break down. It is also misleading for heavy-taileddistributions. Since many of the distributions used to describe social phenom-ena are skewed or heavy-tailed, using the standard deviation to characterizetheir scales becomes problematic. To capture the spread of a distribution with-out relying on the standard deviation, we measure spread using the followingquantile-based scale measure (QSC) at a selected p:

QSC (p) = Q(1 − p) − Q(p) for p < .5. [2.1]

We can obtain the spread for the middle 95% of the population betweenQ (.025) and Q (.975), or the middle 50% of the population between Q (.25) andQ (.75) (the conventional interquartile range), or the spread of any desirablemiddle 100(1 − 2p)% of the population.

The QSC measure not only offers a direct and straightforward measure ofscale but also facilitates the development of a rich class of model-based scale-shift measures (developed in Chapter 5). In contrast, a model-based approachthat separates out a predictor’s effect in terms of a change in scale as measuredby the standard deviation limits the possible patterns that could be discovered.

A second measure of a distributional shape is skewness. This property isthe focus of much inequality research. Skewness is measured using a cubicfunction of data points’ deviations from the mean. When the data are sym-metrically distributed about the sample mean, the value of skewness is zero.A negative value indicates left skewness and a positive value indicates rightskewness. Skewness can be interpreted as saying that there is an imbalancebetween the spread below and above the median.

Although skewness has long been used to describe the nonnormality of adistribution, the fact that it is based on higher moments of the distributionis confining. We seek more flexible methods for linking properties likeskewness to covariates. In contrast to moment-based measures, samplequantiles can be used to describe the nonnormality of a distribution in ahost of ways. The simple connection between quantiles and the shape of adistribution enables further development of methods for modeling shapechanges (this method is developed in Chapter 5).

13

02-Hao.qxd 3/13/2007 4:29 PM Page 13

Uneven upper and lower spreads can be expressed using the quantilefunction. Figure 2.6 describes two quantile functions for a normal distribu-tion and a right-skewed distribution. The quantile function for the normaldistribution is symmetric around the .5th quantile (the median). For exam-ple, Figure 2.6a shows that the slope of the quantile function at the .1thquantile is the same as the slope at the .9th quantile. This is true for all othercorresponding lower and upper quantiles. By contrast, the quantile functionfor a skewed distribution is asymmetric around the median. For instance,Figure 2.6b shows that the slope of the quantile function at the .1th quan-tile is very different from the slope at the .9th quantile.

Let the upper spread refer to the spread above the median and the lowerspread refer to the spread below the median. The upper spread and thelower spread are equal for a symmetric distribution. On the other hand, thelower spread is much shorter than the upper spread in a right-skewed dis-tribution. We quantify the measure of quantile-based skewness (QSK) as aratio of the upper spread to the lower spread minus one:

QSK(p) = (Q (1−p) − Q (.5))/(Q (.5) − Q (p) ) − 1 for p < 0.5. [2.2]

The quantity QSK (p) is recentered using subtraction of one, so that it takesthe value zero for a symmetric distribution. A value greater than zero indi-cates right-skewness and a value less than 0 indicates left-skewness.

Table 2.1 shows 9 quantiles of the symmetric and right-skewed distributionin Figure 2.6b, their upper and lower spreads, and the QSK (p) at four differentvalues of p. The QSK (p)s are 0 for the symmetric example, while they rangefrom 0.3 to 1.1 for the right-skewed distribution. This definition of QSK (p) issimple and straightforward and has the potential to be extended to measurethe skewness shift caused by a covariate (see Chapter 5).

So far we have defined quantiles in terms of the cdf and have developedquantile-based shape measures. Readers interested in an alternative defini-tion of quantiles that will facilitate the understanding of the quantile-regression estimator (in the next chapter) are advised to continue on to thenext section. Others may wish to skip to the Summary Section.

Quantile as a Solution to a Certain Minimization Problem

A quantile can also be considered as a solution to a certain minimizationproblem. We introduce this redefinition because of its implication for thequantile-regression estimator to be discussed in the next chapter. We startwith the median, the .5th quantile.

To motivate the minimization problem, we first consider the familiar mean,µ, of the y distribution. We can measure how far a given data point of Y is fromthe value µ using the squared deviation (Y − µ)2, and then how far Y is from µ,

14

02-Hao.qxd 3/13/2007 4:29 PM Page 14

15

P

0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

Q

6

5

4

5.5

4.5

(a) Normal

6

5.5

5

4.5

4

Q

P

0 .1 .2 .3 .4 .5 .6 .7 .8 .9 1

(b) Right-Skewed

Figure 2.6 Normal Versus Skewed Quantile Functions

02-Hao.qxd 3/13/2007 4:29 PM Page 15

on average, by the mean squared deviation E[(Y − µ)2]. One way to think abouthow to define the center of a distribution is to ask for the point µ at which theaverage squared deviation from Y is minimized. Therefore, we can write

E [(Y − µ)2] = E [Y2] − 2E [Y]µ + µ2

= (µ − E [Y])2 + (E [Y2] − (E [Y])2).= (µ − E [Y])2 + Var (Y) [2.3]

Because the second term Var(Y) is constant, we minimize Equation 2.3by minimizing the first term (µ − Ε[Y])2. Taking µ = Ε[Y] makes the firstterm zero and minimizes Equation 2.3 because any other values of µ makethe first term positive and cause Equation 2.3 to depart from the minimum.

Similarly, the sample mean for a sample of size n can also be viewed asthe solution to a minimization problem. We seek the point µ that minimizes

the average squared distance

[2.4]

where y− denotes the sample mean, and s2y the sample variance. The solution

to this minimization problem is to take the value of µ that makes the firstterm as small as possible, that is, we take µ = y− .

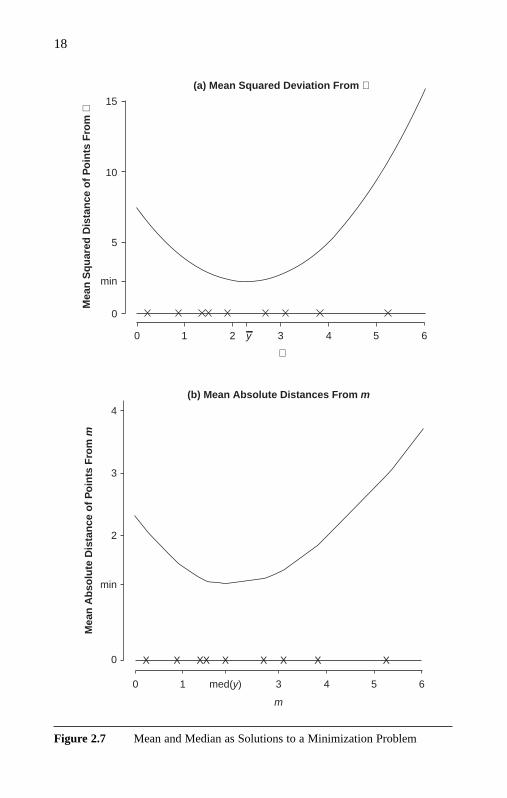

For concreteness, consider a sample of the following nine values: 0.23,0.87, 1.36, 1.49, 1.89, 2.69, 3.10, 3.82, and 5.25. A plot of the mean squared

1

n

n∑i=1

(yi − µ)2 = 1

n

n∑i=1

(µ − y---)2 + 1

n

n∑i=1

(yi − y---)2 = (µ − y---)2 + s2y,

1

n

n∑i=1

(yi − µ)2 :

16

TABLE 2.1Quantile-Based Skewness Measure

Symmetric Right-Skewed

Lower or Lower or Proportion of Upper Upper Population Quantile Spread QSK Quantile Spread QSK

0.1 100 110 0 130 60 1.70.2 150 60 0 150 40 1.30.3 180 30 0 165 25 1.00.4 200 10 0 175 15 0.30.5 210 — — 190 — —0.6 220 10 — 210 20 —0.7 240 30 — 240 50 —0.8 270 60 — 280 90 —0.9 320 110 — 350 160 —

02-Hao.qxd 3/13/2007 4:29 PM Page 16

distance of sample points from a given point µ is shown in Figure 2.7a.Note that the function to minimize is convex, with a smooth parabolic form.

The median m has a similar minimizing property. Instead of using squareddistance, we can measure how far Y is from m by the absolute distance|Y − m|and measure the average distance in the population from m by the meanabsolute distance E|Y − m|. Again we can solve for the value m by minimizingE|Y − m|. As we shall see, the function of |Y − m| is convex, so that the mini-mization solution is to find a point where the derivative with respect to m is zeroor where the two directional derivatives disagree in sign. The solution is themedian of the distribution. (A proof appears in the Appendix of this chapter.)

Similarly, we can work on the sample level. We define the mean absolute

distance from m to the sample points by . A plot of this function

is given in Figure 2.7b for the same sample of nine points above. Comparedwith the function plotted in Figure 2.7a (the mean squared deviation), Figure2.7b remains convex and parabolic in appearance. However, rather than beingsmooth, the function in Figure 2.7b is piecewise linear, with the slope changingprecisely at each sample point. The minimum value of the function shownin this figure coincides with the median sample value of 1.89. This is a specialcase of a more general phenomenon. For any sample, the function defined

by f (m) is the sum of V-shaped functions fi(m) = |yi − m|/n

(see Figure 2.8 for the function fi corresponding to the data point withyi = 1.49). The function fi takes a minimum value of zero when m = yi has aderivative of −1/n for m < yi and 1/n for m > yi . While the function is not dif-ferentiable at m = yi, it does have a directional derivative there of −1/n in thenegative direction and 1/n in the positive direction. Being the sum of thesefunctions, the directional derivative of f at m is (r − s)/n in the negative direc-tion and (s − r) /n in the positive direction, where s is the number of datapoints to the right of m and r is the number of data points to the left of m. Itfollows that the minimum of f occurs when m has the same number of datapoints to its left and right, that is, when m is a sample median.

This representation of the median generalizes to the other quantiles as fol-lows. For any p∈(0,1), the distance from Y to a given q is measured by theabsolute distance, but we apply a different weight depending on whether Y is tothe left or to the right of q. Thus, we define the distance from Y to a given q as:

[2.5]

We look for the value q that minimizes the mean distance from Y:E [dp(Y,q)]. The minimum occurs when q is the pth quantile (see Appendix

dp(Y, q) ={(1 − p)|Y − q| Y < q

p|Y − q| Y ≥ q.

= 1

n

n∑i=1

|yi − m|

1

n

n∑i=1

|yi − m|

17

{

02-Hao.qxd 3/13/2007 4:29 PM Page 17

18

15

(a) Mean Squared Deviation From µ

10

5

0

min

0 1 2 3 4 5 6

Mea

n S

qu

ared

Dis

tan

ce o

f P

oin

ts F

rom

µ

µ

y

4

3

2

0

min

0 1 3

m

4 5 6med(y)

Mea

n A

bso

lute

Dis

tan

ce o

f P

oin

ts F

rom

m

X X XX X X X X X

(b) Mean Absolute Distances From m

Figure 2.7 Mean and Median as Solutions to a Minimization Problem

02-Hao.qxd 3/13/2007 4:29 PM Page 18

of this chapter). Similarly, the pth sample quantile is the value of q that min-imizes the average (weighted) distance:

Properties of Quantiles

One basic property of quantiles is monotone equivariance property. It statesthat if we apply a monotone transformation h (for example, the exponentialor logarithmic function) to a random variable, the quantiles are obtained byapplying the same transformation to the quantile function. In other words,if q is the pth quantile of Y, then h(q) is the pth quantile of h(Y). An analogousstatement can be made for sample quantiles. For example, for the sampledata, since we know that the 20th percentile is 4,300, if we make a log

1

n

n∑i=1

dp(yi, q) = 1 − p

n

∑yi<q

|yi − q| + p

n

∑yi>q

|yi − q|.

19

0.4

0.3

0.2

0.1

0.0

0 1 2 3 4 5yi

µ

Fi(

m)

Figure 2.8 V-Shaped Function Used to Describe the Median as the Solutionto a Minimization Problem

02-Hao.qxd 3/13/2007 4:29 PM Page 19

transformation of the data, the 20th percentile for the resulting data will belog (4,300) = 8.37.

Another basic property of sample quantiles relates to their insensitivityto the influence of outliers. This feature, which has an analog in quantileregression, helps make quantiles and quantile-based procedures useful inmany contexts. Given a sample of data x1, . . . , xn with sample median m,we can modify the sample by changing a data value xi that is above themedian to some other value above the median. Similarly, we can change adata value that is below the median to some other value below the median.Such modifications to the sample have no effect on the sample median.1 Ananalogous property holds for the pth sample quantile as well.

We contrast this with the situation for the sample mean: Changing anysample value xi to some other value xi + ∆ changes the sample mean by ∆/n.Thus, the influence of individual data points is bounded for sample quan-tiles and is unbounded for the sample mean.

Summary

This chapter introduces the notions of quantile and quantile function. Wedefine quantiles and quantile functions by way of the cumulative distribu-tion function. We develop quantile-based measures of location and shape ofa distribution and highlight their utility by comparing them with conven-tional distribution moments. We also redefine quantiles as a solution to aminimization problem, preparing the reader for a better understanding ofthe quantile regression estimator. With these preparations, we proceed tothe next chapter on the quantile-regression model and its estimator.

Note

1. To be precise, this assumes that the sample size is odd. If the samplesize is even, then the sample median is defined as the average of the (n/2)thand (n/2 + 1)th order statistics, and the statement holds if we modify a datavalue above (or below) the (n/2 + 1)th (or (n/2)th) order statistic, keepingit above (or below) that value.

20

02-Hao.qxd 3/13/2007 4:29 PM Page 20

Chapter 2 Appendix

A Proof: Median and Quantiles as Solutions to a Minimization Problem

To make things simple, we assume that the cdf F has a probability densityfunction f. To see why median can be defined as a minimization problem,we can write

[A.1]

As Figure 2.7b shows, Equation A.1 is a convex function. Differentiatingwith respect to m and setting the partial derivative to zero will lead to thesolution for the minimum. The partial derivative of the first term is:

and the partial derivative of the second term is:

∂

∂m

+∞∫y=m

(y − m)f (y)dy = −+∞∫

y=m

f (y)dy = −(1 − F(m)).

∂

∂m

m∫y=−∞

(m − y)f (y)dy = (m − y)f (y)|y=m +m∫

y=−∞

∂

∂m(m − y)f (y)dy

=m∫

y=−∞

f (y)dy = F(m)

E|Y − m| =∫ +∞

−∞|y − m|f (y)dy

=m∫

y=−∞

|y − m|f (y)dy++∞∫

y=m

|y − m|f (y)dy

=m∫

y=−∞

(m − y)f (y)dy++∞∫

y=m

(y − m)f (y)dy.

21

03-Hao.qxd 3/13/2007 5:24 PM Page 21

Combining these two partial derivatives leads to:

[A.2]

By setting 2F(m) − 1 = 0, we solve for the value of F(m) = 1/2, that is,the median, to satisfy the minimization problem.

Repeating the above argument for quantiles, the partial derivative forquantiles corresponding to Equation A.2 is:

[A.3]

We set the partial derivative F(q) − p = 0 and solve for the value ofF(q) = p that satisfies the minimization problem.

3. QUANTILE-REGRESSION MODEL AND ESTIMATION

The quantile functions described in Chapter 2 are adequate for describ-ing and comparing univariate distributions. However, when we model therelationship between a response variable and a number of independentvariables, it becomes necessary to introduce a regression-type model for the quantile function, the quantile-regression model (QRM). Given a set ofcovariates, the linear-regression model (LRM) specifies the conditional-mean function whereas the QRM specifies the conditional-quantile func-tion. Using the LRM as a point of reference, this chapter introduces theQRM and its estimation. It makes comparisons between the basic modelsetup for the LRM and that for the QRM, a least-squares estimation forthe LRM and an analogous estimation approach for the QRM, and theproperties of the two types of models. We illustrate our basic points usingempirical examples from analyses of household income.1

Linear-Regression Modeling and Its Shortcomings

The LRM is a standard statistical method widely used in social-scienceresearch, but it focuses on modeling the conditional mean of a responsevariable without accounting for the full conditional distributional propertiesof the response variable. In contrast, the QRM facilitates analysis of the full

∂

∂qE[dp(Y, q)] = (1 − p)F(q) − p(1 − F(q)) = F(q) − p.

∂

∂m

∫ +∞

−∞|y − m|f (y)dy = F(m) − (1 − F(m)) = 2F(m) − 1.

22

03-Hao.qxd 3/13/2007 5:24 PM Page 22

23

conditional distributional properties of the response variable. The QRM andLRM are similar in certain respects, as both models deal with a continuousresponse variable that is linear in unknown parameters, but the QRM andLRM model different quantities and rely on different assumptions abouterror terms. To better understand these similarities and differences, we layout the LRM as a starting point, and then introduce the QRM. To aid theexplication, we focus on the single covariate case. While extending to morethan one covariate necessarily introduces additional complexity, the ideasremain essentially the same.

Let y be a continuous response variable depending on x. In our empiricalexample, the dependent variable is household income. For x, we use aninterval variable, ED (the household head’s years of schooling), or alterna-tively a dummy variable, BLACK (the head’s race, 1 for black and 0 forwhite). We consider data consisting of pairs (xi ,yi) for i = 1, . . . , n basedon a sample of micro units (households in our example).

By LRM, we mean the standard linear-regression model

yi = β0 + β1x i + ε i , [3.1]

where εi is identically, independently, and normally distributed with meanzero and unknown variance σ 2. As a consequence of the mean zeroassumption, we see that the function β 0 + β 1x being fitted to the data corre-sponds to the conditional mean of y given x (denoted by E [ y ⎢x]), which isinterpreted as the average in the population of y values corresponding to afixed value of the covariate x.

For example, when we fit the linear-regression Equation 3.1 usingyears of schooling as the covariate, we obtain the prediction equationy = –23127 + 5633ED, so that plugging in selected numbers of years of schooling leads to the following values of conditional means forincome.

ED 9 12 16E ( y | ED) $27,570 $44,469 $67,001

Assuming a perfect fit, we would interpret these values as the averageincome for people with a given number of years of schooling. For example,the average income for people with nine years of schooling is $27,570.

Analogously, when we take the covariate to be BLACK, the fitted regres-sion equation takes the form y = 53466 – 18268BLACK, and plugging in thevalues of this covariate yields the following values.

03-Hao.qxd 3/13/2007 5:24 PM Page 23

Again assuming the fitted model to be a reflection of what happens at thepopulation level, we would interpret these values as averages in subpopulations,for example, the average income is $53,466 for whites and $35,198 for blacks.

Thus, we see that a fundamental aspect of linear-regression models isthat they attempt to describe how the location of the conditional distribu-tion behaves by utilizing the mean of a distribution to represent its centraltendency. Another key feature of the LRM is that it invokes a homoscedas-ticity assumption; that is, the conditional variance, Var (y|x ), is assumed tobe a constant σ 2 for all values of the covariate. When homoscedasticityfails, it is possible to modify LRM by allowing for simultaneous modelingof the conditional mean and the conditional scale. For example, one canmodify the model in Equation 3.1 to allow for modeling the conditionalscale: yi = β0 + β1x i + e γε i, where γ is an additional unknown parameterand we can write Var (y|x) = σ 2e γ.

Thus, utilizing LRM reveals important aspects of the relationshipbetween covariates and a response variable, and can be adapted to performthe task of modeling what is arguably the most important form of shapechange for a conditional distribution: scale change. However, the estimationof conditional scale is not always readily available in statistical software.In addition, linear-regression models impose significant constraints on themodeler, and it is challenging to use LRM to model more complex condi-tional shape shifts.

To illustrate the kind of shape shift that is difficult to model using LRM,imagine a somewhat extreme situation in which, for some population ofinterest, we have a response variable y and a covariate x with the propertythat the conditional distribution of y has the probability density of the formshown in Figure 3.1 for each given value of x = 1,2,3. The three probabil-ity density functions in this figure have the same mean and standard devia-tion. Since the conditional mean and scale for the response variable y donot vary with x, there is no information to be gleaned by fitting a linear-regression model to samples from these populations. In order to understandhow the covariate affects the response variable, a new tool is required.Quantile regression is an appropriate tool for accomplishing this task.

A third distinctive feature of the LRM is its normality assumption.Because the LRM ensures that the ordinary least squares provide the bestpossible fit for the data, we use the LRM without making the normalityassumption for purely descriptive purposes. However, in social-scienceresearch, the LRM is used primarily to test whether an explanatory variable

24

BLACK 0 1E ( y | BLACK) $53,466 $35,198

03-Hao.qxd 3/13/2007 5:24 PM Page 24

significantly affects the dependent variable. Hypothesis testing goes beyondparameter estimation and requires determination of the sampling variabil-ity of estimators. Calculated p-values rely on the normality assumption oron large-sample approximation. Violation of these conditions may causebiases in p-values, thus leading to invalid hypothesis testing.

A related assumption made in the LRM is that the regression model usedis appropriate for all data, which we call the one-model assumption.Outliers (cases that do not follow the relationship for the majority of thedata) in the LRM tend to have undue influence on the fitted regression line.The usual practice used in the LRM is to identify outliers and eliminatethem. Both the notion of outliers and the practice of eliminating outliersundermine much social-science research, particularly studies on socialstratification and inequality, as outliers and their relative positions to thoseof the majority are important aspects of inquiry. In terms of modeling, onewould simultaneously need to model the relationship for the majority casesand for the outlier cases, a task the LRM cannot accomplish.

25

0.5 1.0 1.5

1.5

1.0

0.5

0.0

2.0 2.5

Y

x = 3

x = 1x = 2

Figure 3.1 Conditional Distributions With the Same Mean and StandardDeviation but Different Skewness

03-Hao.qxd 3/13/2007 8:28 PM Page 25

All of the features just mentioned are exemplified in our householdincome data: the inadequacy of the conditional mean from a distributionalpoint of view and violations of the homoscedasticity assumption, the nor-mality assumption, and the one-model assumption. Figure 3.2 shows thedistributions of income by education groups and racial groups. The locationshifts among the three education groups and between blacks and whites areobvious, and their shape shifts are substantial. Therefore, the conditionalmean from the LRM fails to capture the shape shifts caused by changes inthe covariate (education or race). In addition, since the spreads differ sub-stantially among the education groups and between the two racial groups,the homoscedasticity assumption is violated, and the standard errors arenot estimated precisely. All box graphs in Figure 3.2 are right-skewed.Conditional-mean and conditional-scale models are not able to detect thesekinds of shape changes.

By examining residual plots, we have identified seven outliers, includingthree cases with 18 years of schooling having an income of more than$505,215 and four cases with 20 years of schooling having an income ofmore than $471,572. When we add a dummy variable indicating member-ship in this outlier class to the regression model of income on education, wefind that these cases contribute an additional $483,544 to the intercept.

These results show that the LRM approach can be inadequate for a vari-ety of reasons, including heteroscedasticity and outlier assumptions and thefailure to detect multiple forms of shape shifts. These inadequacies are notrestricted to the study of household income but also appear when othermeasures are considered. Therefore, it is desirable to have an alternativeapproach that is built to handle heteroscedasticity and outliers and detectvarious forms of shape changes.

As pointed out above, the conditional mean fails to identify shape shifts.The conditional-mean models also do not always correctly model centrallocation shifts if the response distribution is asymmetric. For a symmetricdistribution, the mean and median coincide, but the mean of a skewed dis-tribution is no longer the same as the median (the .5th quantile). Table 3.1shows a set of brief statistics describing the household income distribution.The right-skewness of the distribution makes the mean considerably largerthan the median for both the total sample and for education and racialgroups (see the first two rows of Table 3.1). When the mean and the medianof a distribution do not coincide, the median may be more appropriate tocapture the central tendency of the distribution. The location shifts amongthe three education groups and between blacks and whites are considerablysmaller when we examine the median rather than the mean. This differenceraises concerns about using the conditional mean as an appropriate measurefor modeling the location shift of asymmetric distributions.

26

03-Hao.qxd 3/13/2007 5:24 PM Page 26

27

600

(a) Education Groups

500

400

300

200

100

0

$100

0

9 years of schooling 12 years of schooling 16 years of schooling

600

500

400

300

200

100

0

$100

0

White Black

(b) Race Groups

Figure 3.2 Box Graphs of Household Income

03-Hao.qxd 3/13/2007 5:24 PM Page 27

28

TAB

LE

3.1

Hou

seho

ld I

ncom

e D

istr

ibut

ion:

Tota

l,E

duca

tion

Gro

ups,

and

Rac

ial G

roup

s

Tota

lE

D =

9E

D =

12E

D =

16W

HIT

EB

LA

CK

Mea

n50

,334

27,8

4140

,233

71,8

3353

,466

35,1

98

Qua

ntil

eM

edia

n (.

50th

Qua

ntile

)39

,165

22,1

4632

,803

60,5

4541

,997

26,7

63.1

0th

Qua

ntile

11,0

228,

001

10,5

1021

,654

12,4

866,

837

.25t

h Q

uant

ile20

,940

12,3

2918

,730

36,8

0223

,198

13,4

12.7

5th

Qua

ntile

65,7

9336

,850

53,0

7590

,448

69,6

8047

,798

.90t

h Q

uant

ile98

,313

54,3

7077

,506

130,

981

102,

981

73,0

30

Qua

ntil

e-B

ased

Sca

le(Q

.75−

Q.2

5)44

,853

24,5

2134

,344

53,6

4646

,482

34,3

86(Q

.90−

Q.1

0)87

,291

46,3

6966

,996

109,

327

90,4

9566

,193

Qua

ntil

e-B

ased

Ske

wne

ss(Q

.75−

Q.5

0) −1

(Q.5

0−Q

.25)

.46

.50

.44

.26

.47

.58

(Q.9

0−Q

.50)

−1(Q

.50−

Q.1

0)1.

101.

281.

01.8

11.

071.

32

03-Hao.qxd 3/13/2007 5:24 PM Page 28

Conditional-Median and Quantile-Regression Models

With a skewed distribution, the median may become the more appropriatemeasure of central tendency; therefore, conditional-median regression,rather than conditional-mean regression, should be considered for thepurpose of modeling location shifts. Conditional-median regression wasproposed by Boscovich in the mid-18th century and was subsequentlyinvestigated by Laplace and Edgeworth. The median-regression modeladdresses the problematic conditional-mean estimates of the LRM. Medianregression estimates the effect of a covariate on the conditional median, soit represents the central location even when the distribution is skewed.

To model both location shifts and shape shifts, Koenker and Bassett (1978)proposed a more general form than the median-regression model, the quan-tile-regression model (QRM). The QRM estimates the potential differentialeffect of a covariate on various quantiles in the conditional distribution, forexample, a sequence of 19 equally distanced quantiles from the .05th quan-tile to the .95th quantile. With the median and the off-median quantiles, these19 fitted regression lines capture the location shift (the line for the median),as well as scale and more complex shape shifts (the lines for off-medianquantiles). In this way, the QRM estimates the differential effect of a covari-ate on the full distribution and accommodates heteroscedasticity.

Following Koenker and Bassett (1978), the QRM corresponding to theLRM in Equation 3.1 can be expressed as:

yi = β (p)0 + β (p)

1 xi + ε (p)i , [3.2]

where 0 < p < 1 indicates the proportion of the population havingscores below the quantile at p. Recall that for LRM, the conditional meanof yi given x i is E (yi|xi ) = β0 + β 1x i, and this is equivalent to requiringthat the error term ε i have zero expectation. In contrast, for the corre-sponding QRM, we specify that the pth conditional quantile given xi isQ (p)( yi|xi) = β (p)

0 + β (p)1 xi. Thus, the conditional pth quantile is determined

by the quantile-specific parameters, β (p)0 and β (p)

1 , and a specific value of thecovariate xi. As for the LRM, the QRM can be formulated equivalently witha statement about the error terms εi. Since the term β (p)

0 +β (p)1 x i is a constant,

we have Q (p)( yi|xi) = β (p)0 + β (p)

1 xi + Q(p)(εi ) = β (p)0 + β (p)

1 xi, so an equivalentformulation of QRM requires that the pth quantile of the error termbe zero.

It is important to note that for different values of the quantile p ofinterest, the error terms ε ( p)

i for fixed i are related. In fact, replacingp by q in Equation 3.2 gives yi = β (q)

0 + β (q)1 x i + ε (q)

i , which leads toε (p)

i – ε (q)i = (β (q)

0 – β (p)0 ) + xi( β (q)

1 – β (p)1 ), so that the two error terms differ by

29

03-Hao.qxd 3/13/2007 5:24 PM Page 29

a constant given x i. In other words, the distributions of ε (p)i and ε (q)

i are shiftsof one another. An important special case of QRM to consider is one inwhich the ε (p)

i for i = 1, . . . , n are independent and identically distributed;we refer to this as the i.i.d. case. In this situation, the qth quantile of ε (p)

i isa constant cp,q depending on p and q and not on i. Using Equation 3.2, wecan express the qth conditional-quantile function as Q(q)( yi|xi ) =Q(p)( yi|xi ) + cp,q.

2 We conclude that in the i.i.d. case, the conditional-quan-tile functions are simple shifts of one another, with the slopes β 1

(p) taking acommon value β1. In other words, the i.i.d. assumption says that there areno shape shifts in the response variable.

Equation 3.2 dictates that unlike the LRM in Equation 3.1, whichhas only one conditional mean expressed by one equation, the QRM canhave numerous conditional quantiles. Thus, numerous equations can beexpressed in the form of Equation 3.2.3 For example, if the QRM specifies19 quantiles, the 19 equations yield 19 coefficients for x i , one at each of the19 conditional quantiles ( β 1

.05, β 1.10, . . . , β 1

.95). The quantiles do not have tobe equidistant, but in practice, having them at equal intervals makes themeasier to interpret.

Fitting Equation 3.2 in our example yields estimates for the 19 condi-tional quantiles of income given education or race (see Tables 3.2 and 3.3).The coefficient for education grows monotonically from $1,019 at the .05thquantile to $8,385 at the .95th quantile. Similarly, the black effect is weakerat the lower quantiles than at the higher quantiles.

The selected conditional quantiles on 12 years of schooling are:

30

p .05 .50 .95E ( yi | EDi = 12) $7,976 $36,727 $111,268

and the selected conditional quantiles on blacks are:

p .05 .50 .95E ( yi | BLACKi = 1) $5,432 $26,764 $91,761

These results are very different from the conditional mean of the LRM.The conditional quantiles describe a conditional distribution, which can beused to summarize the location and shape shifts. Interpreting QRM esti-mates is a topic of Chapters 5 and 6.

Using a random sample of 1,000 households from the total sample andthe fitted line based on the LRM, the left panel of Figure 3.3 presentsthe scatterplot of household income against the head of household’s yearsof schooling. The single regression line indicates mean shifts, for example,a mean shift of $ 22,532 from 12 years of schooling to 16 years of schooling

03-Hao.qxd 3/13/2007 5:24 PM Page 30

31

TAB

LE

3.2

Qua

ntile

-Reg

ress

ion

Est

imat

es f

or H

ouse

hold

Inc

ome

on E

duca

tion

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

(12)

(13)

(14)

(15)

(16)

(17)

(18)

(19)

ED

1,01

91,

617

2,02

32,

434

2,75

03,

107

3,39

73,

657

3,94

84,

208

4,41

84,

676

4,90