quality control for major operational risk areas

TRANSCRIPT

Moderator:

Mark Atencio, Executive Consultant, Lyons McCloskey, LLC

Panelists:

Jennifer Greear, Vice President, Wells Fargo Home Mortgage

Wade Mjelde, VP, Servicing QC Division, Tena Companies, Inc

Jim Shankle, Managing Director, CrossCheck Compliance

Quality Control for Major Operational Risk Areas

February 27, 2019

Panel Discussion

• Benefits to a Successful Quality Control Program

• Regulatory Environment

• Servicing Quality Control Requirements

• Customer Handling and Response: Customer Complaint Response Program

• Regulatory and Operational Coverage Areas

• Transactional Testing: The Servicing File

• Common Industry Gross Defects by Area

• Remediation: Fixing Areas of Weakness

• Quality Control Efficiencies

• Q&A

Benefits to a Successful Quality Control Program

• Meeting complex and changing state and federal laws

• Achieving regulatory and investor expectation and successful external exams

• Staying on top of variations in investor rules driving repurchases or indemnifications

• Reducing investor fees and penalties

• Increased rating agencies ratings

• Maintaining or improving reputation risk

• Minimizing costs and improve operations

• Eliminating regulatory fines and restrictions

• Opportunity to train staff

Regulatory Environment

Regulatory Environment – CFPB

• White House administration want to roll back regulations on the whole, Dodd-Frank

regulations in particular.

• President wants Congress to make financial regulatory reform a priority and to eliminate or

severely diminish role/authority/reach of CFPB.

• In May 2018, President Trump signed S. 2155, Economic Growth, Regulatory Relief, and

Consumer Protection Act (EGRRCPA)

• CFPB philosophy and priorities:

• Acting Director Mulvaney Memo to staff

• CFPB will no longer “push the envelope” of the law to send a message to regulated entities.

• December 2018: Director Kathy Kraninger

• We aim to make consumer financial markets work for consumers, responsible providers,

and the economy as a whole:

Empower, Enforce, Educate

Regulatory Environment – CFPB Assessing 2014 Effective Servicing Rules

• The Bureau’s 2013 RESPA Mortgage Servicing Rule took effect on Jan. 10, 2014, and

this report publishes the findings of the Bureau’s assessment of the Rule.

• In general, these rules gave borrowers new consumer protections related to

mortgage loan servicing to help consumers who were having trouble making their

mortgage payments.

• The issuance of this report is not the end of the review for the Bureau. They note:

• The Bureau uses lessons drawn from the assessments to inform our approach to

future assessments and future rulemakings.

• The Bureau anticipates that continued interaction with stakeholders will help

inform our future assessments as well as future policy decisions.

CFPB Released Report: Assessing our Rules – January 11, 2019

Regulatory Environment – CFPB

CFPB’s broad review of their policies and operations issued Requests for Information

(RFIs) seeking comment:

• 2/21/18 RFI - Bureau External Engagements

• 3/1/18 Regarding Bureau Public Reporting Practices of Consumer Complaint Information

• 3/7/18 Regarding Bureau Rulemaking Processes

• 3/9/18 Proper and appropriate functions to best protect consumers

• 90 days – Opportunity for public to submit feedback and suggest ways to improve outcomes.

• The Bureau is analyzing more than 86,000 comments received in response to its “Call for Evidence”

initiative seeking feedback on Bureau operations and regulations.

• Following consideration of these various initiatives, the Bureau expects to refine its rulemaking

priorities no later than the Spring 2019 Agenda and will publish an updated statement of priorities at

that time.

Regulatory Environment – US Treasury Report July 2018

Treasury outlined recommended changes to the regulations for mortgage lending and servicing.

Servicing recommendations included:

• Federally supported mortgage programs explore standardizing the most effective features of a

successful loss mitigation program across the federal footprint.

• HUD continue to review FHA servicing practices with the intention to increase certainty and reduce

needlessly costly and burdensome regulatory requirements.

• FHA consider administrative changes to how penalties are assessed across FHA’s multi-part

foreclosure timeline to allow for greater flexibility for servicers to miss intermediate deadlines while

adhering to the broader resolution timeline, as well as to better align with federal loss mitigation

requirements now in place through the Bureau.

US Treasury July 2018

Regulatory Environment – US Treasury Report July 2018

Servicing recommendations continued:

• FHA explore changes to its property conveyance framework to reduce costs and increase efficiencies

by addressing frequent and costly delays associated with the current process.

• FHA continue to make appropriate use of, and consider expanding, programs which reduce the need

for foreclosed properties to be conveyed to HUD, such as Note Sales and FHA’s Claim Without

Conveyance of Title.

• Foreclosure State Law Challenges

• States pursue the establishment of a model foreclosure law, or make any modifications they

deem appropriate to an existing model law, and amend their foreclosure statutes based on that

model law.

US Treasury July 2018

Regulatory Environment – What to do

• Regulatory environment today is changing but could be hostile depending on servicing

results

• More Information for Mortgage Regulatory Environment:

Justin Wiseman, MBA

Associate Vice President

Managing Regulatory Counsel

202-557-2854

Servicers are still facing enforcement from a number of other directions

(state regulators, state AGs, private litigation)

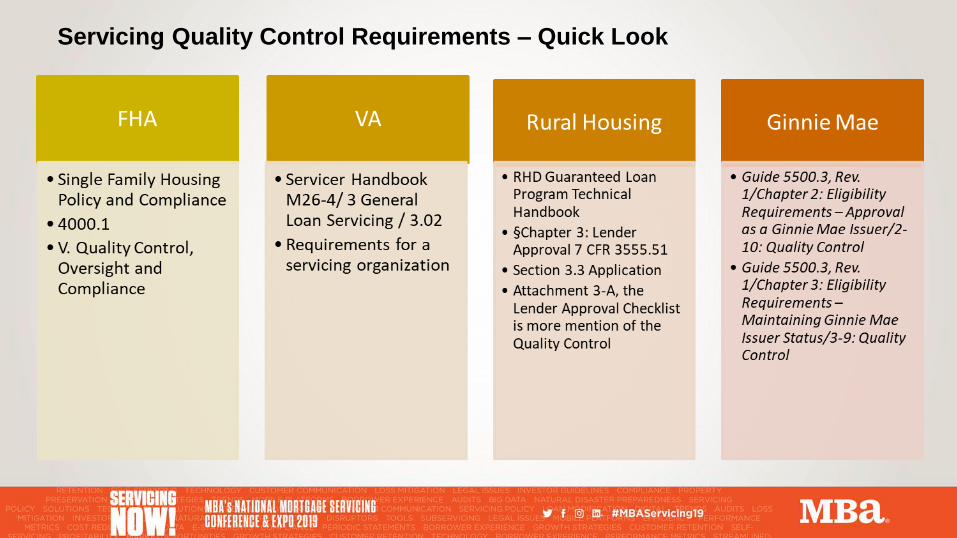

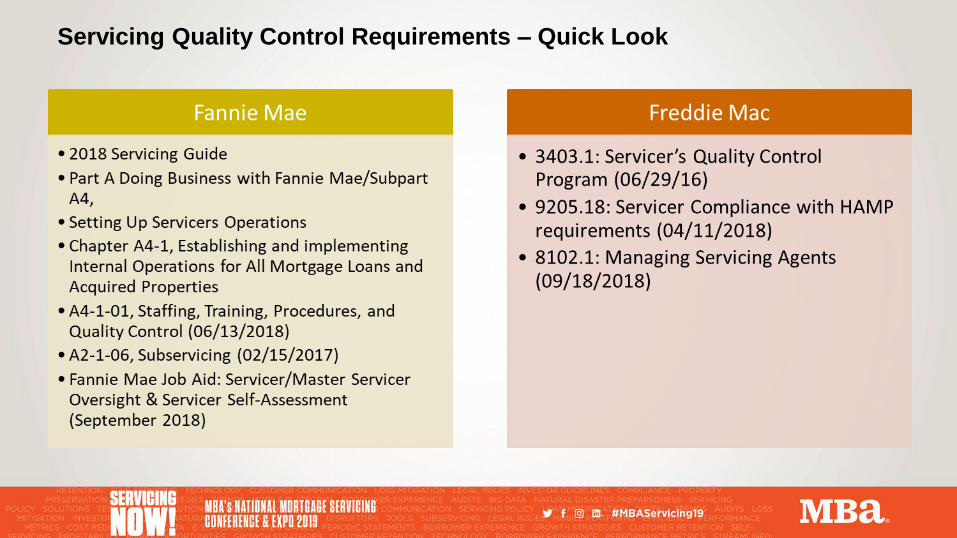

Servicing Quality Control Requirements

Servicing Quality Control Requirements – Quick Look

Servicing Quality Control Requirements – Quick Look

Servicing Quality Control Requirements – Quick Look

Customer Handling and ResponseCustomer Complaint Response Program

CFPB Assessing 2014 Effective Servicing Rules

Assessing our rules: RESPA Mortgage Servicing Rule 1/11/19

CFPB Released Report: Assessing our Rules – January 11, 2019

Consumer mortgage delinquency:

• Servicers respond more quickly with retention alternatives

• Effective Quality Control measures implemented to reinforce requirements, good behavior and identify process gaps or deficiencies

CFPB Released Data – Mortgage Complaints

A snapshot of mortgage complaints – January 2019• Between November 1, 2016 and October 31, 2018, approximately 11 percent of complaints

were about mortgages.

• Most mortgage complaints were about

• Trouble during payment process (42 percent)

• Struggling to pay mortgage (36 percent).

• Compared to the monthly average during the past 24 months, people submitted 18 percent fewer

mortgage complaints in October 2018.

• There were 15 percent fewer mortgage complaints from August 2018 to October 2018

compared to August 2017 to October 2017.

CFPB Released Data – January 2019

• Ensures borrower is provided a swift response that clearly addresses the issue(s)

• Provides the servicer valuable feedback as to root cause of complaints; are issues

systemic?

• Serves as a preventive control in addressing common issues prior to regulatory

inquiries/intervention

Benefits of an Effective Complaint Management Program

Best Practices for Implementing Complaint Management Program

• Establishing a consistent definition of what represents a “complaint” vs. an inquiry

• Ensuring that all channels in which complaints are received adhere to same definition

Front lines

Call centers

Written complaints

Social media

Third-parties engaged by the servicer

• Requiring that the narrative describing the complaint is clear and not subject to interpretation

Best Practices for Implementing Complaint Management Program

• Maintaining a central depository of complaint data

• Requiring consistent documentation that supports the issue and ultimate resolution

• Ensuring that abbreviations or specific terminology used within the servicing

operations are defined

• Creating sufficient data fields to allow for capturing and sorting complaint data

Use of Excel very common in servicing industry

Expanding data fields captured has evolved recently

Presentation Appendix has Common Servicer Data Fields for Complaints

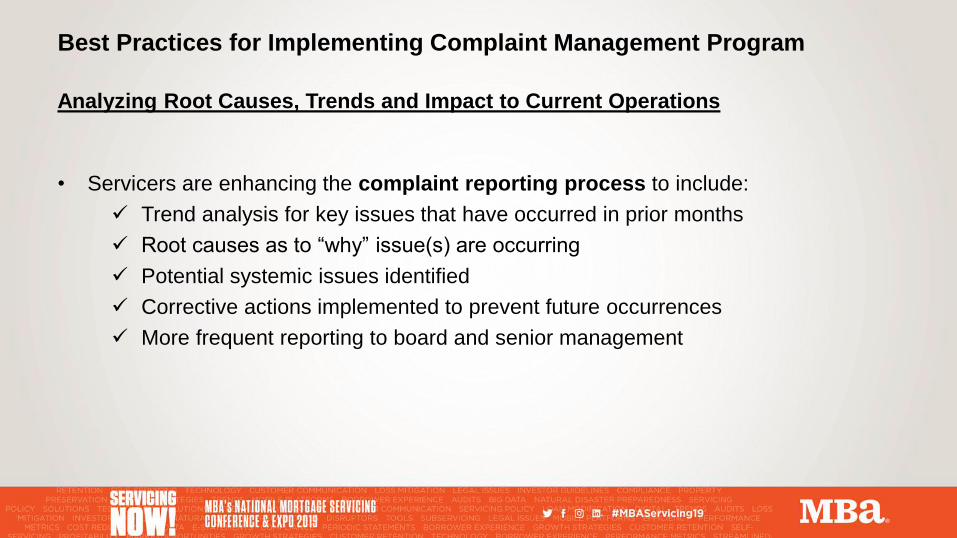

Best Practices for Implementing Complaint Management Program

Analyzing Root Causes, Trends and Impact to Current Operations

• Servicers are enhancing the complaint reporting process to include:

Trend analysis for key issues that have occurred in prior months

Root causes as to “why” issue(s) are occurring

Potential systemic issues identified

Corrective actions implemented to prevent future occurrences

More frequent reporting to board and senior management

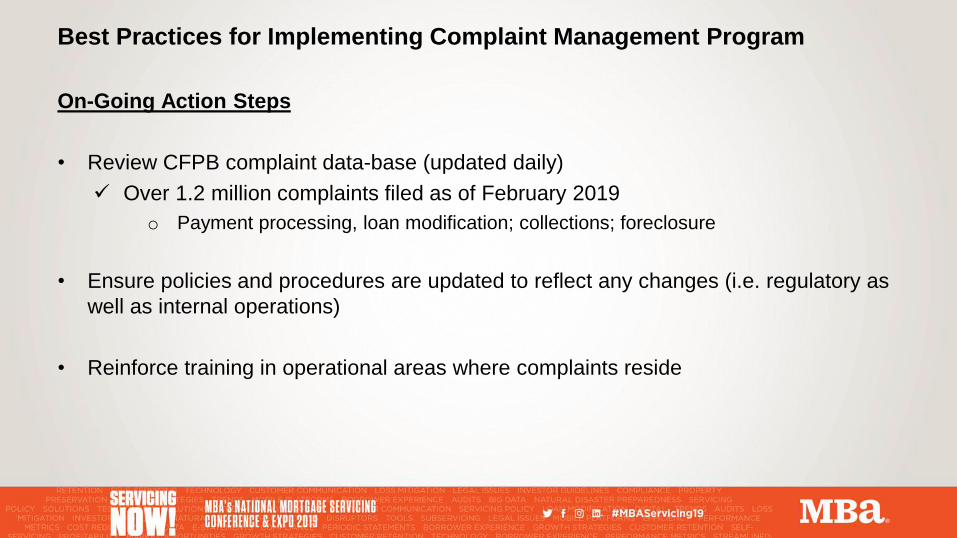

Best Practices for Implementing Complaint Management Program

On-Going Action Steps

• Review CFPB complaint data-base (updated daily)

Over 1.2 million complaints filed as of February 2019

o Payment processing, loan modification; collections; foreclosure

• Ensure policies and procedures are updated to reflect any changes (i.e. regulatory as

well as internal operations)

• Reinforce training in operational areas where complaints reside

Regulatory and Operational

Coverage Areas

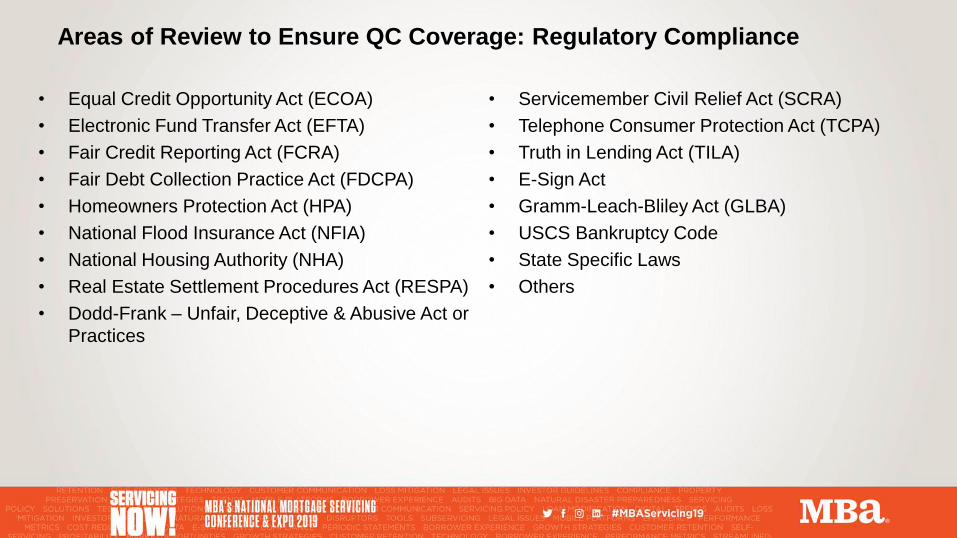

Areas of Review to Ensure QC Coverage: Regulatory Compliance

• Equal Credit Opportunity Act (ECOA)

• Electronic Fund Transfer Act (EFTA)

• Fair Credit Reporting Act (FCRA)

• Fair Debt Collection Practice Act (FDCPA)

• Homeowners Protection Act (HPA)

• National Flood Insurance Act (NFIA)

• National Housing Authority (NHA)

• Real Estate Settlement Procedures Act (RESPA)

• Dodd-Frank – Unfair, Deceptive & Abusive Act or

Practices

• Servicemember Civil Relief Act (SCRA)

• Telephone Consumer Protection Act (TCPA)

• Truth in Lending Act (TILA)

• E-Sign Act

• Gramm-Leach-Bliley Act (GLBA)

• USCS Bankruptcy Code

• State Specific Laws

• Others

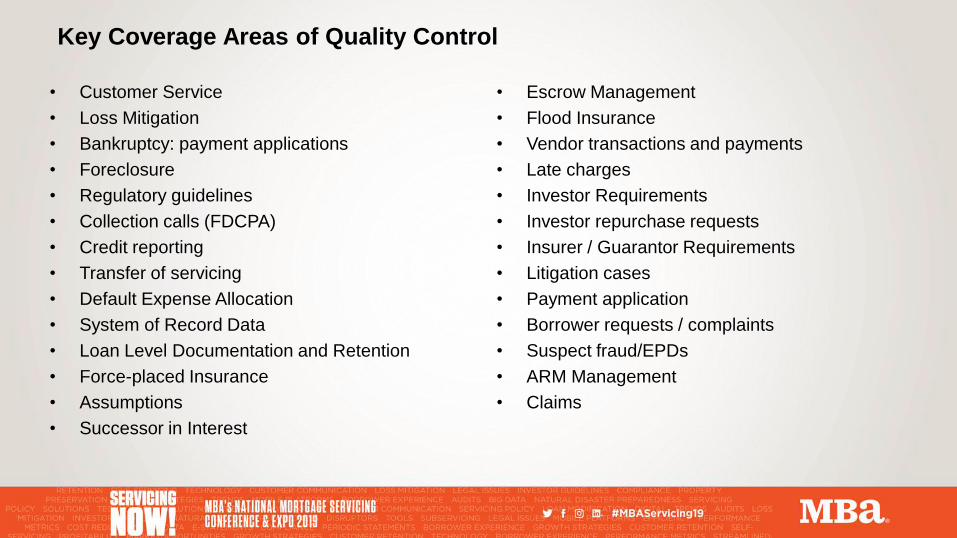

Key Coverage Areas of Quality Control

• Customer Service

• Loss Mitigation

• Bankruptcy: payment applications

• Foreclosure

• Regulatory guidelines

• Collection calls (FDCPA)

• Credit reporting

• Transfer of servicing

• Default Expense Allocation

• System of Record Data

• Loan Level Documentation and Retention

• Force-placed Insurance

• Assumptions

• Successor in Interest

• Escrow Management

• Flood Insurance

• Vendor transactions and payments

• Late charges

• Investor Requirements

• Investor repurchase requests

• Insurer / Guarantor Requirements

• Litigation cases

• Payment application

• Borrower requests / complaints

• Suspect fraud/EPDs

• ARM Management

• Claims

Transactional Testing: The Servicing File

Transactional Testing: The Servicing File

Impact: Gross versus Net Variance

• Good file preparation

• Uniform standards and triggers

• Consistently document and tell the story

• Align interpretations across teams

• Use the best source for the servicing information

• Servicing information may not be in one system

• For example, sometimes foreclosure information initiates in vendor systems

• Consistently document file indexing and stacking order

• Automate as much as possible

• Document manual steps in a procedure

• Ongoing file sampling, findings reporting and remediation ensure ongoing quality

• Monthly/quarterly sampling to ensure that standards are consistently followed and controls are working

• Strategic testing and design to minimize rework

Presentation Appendix has Transactional Testing Key File Ingredients

Common Industry Gross Defects by Area

Gross Defect by Area of Review at TENA

• Driver of High Gross

Defect

• Missing

Documents /

Lack of Access

• Largest Driver of

Inefficiency

• Multiple Touches

• Large Differences in

Net Defect Total

Remediation: Fixing Areas of Weakness

Successful Remediation

• Determine the full scope of the problem

• Who was effected: Current, former or

potential customers

• What was the impact to the Consumers?

• Financial, confusion or UDAAP

• Where are the process gaps or

deficiencies?

• Internal, Vendor or both

• Systems, technology, human

• Develop remediation Plan(s); more than

one may be required

• Plan to address impacted consumers

and systemic issue

• Include detailed project plan

• Key completion milestones

• Material dependencies on vendors

• Action: Work the plan

• Monitor the Remediation

• Ensure the planned changes will

achieve the desired outcome

• Make adjustments as necessary

• Document when and why

• Update Policy and Procedures

• Include a training plan for all staff impacted

by the changes

• Provide periodic updates to executive

oversight and subsequent reporting

Quality Control Efficiencies

Quality Control Efficiencies: Key Attributes

• Independent and strong leadership with excellent

communication skills

• Effective internal rollout of industry changes

• Developed policies and procedures

• Well developed sampling selection

• Statistical Sampling vs Fixed Statistical Sample

• Defect rates for sampling based on testing history

• Targeted testing based on high defect areas

• Accurate data

• Identify and eliminate audit challenges

• System access

• Missing documents

• Define testing period

• Regulatory monitory management up-to-date

• Audit staff sufficiently trained to test to rules and

regulations

• Automation of testing elements

• Overlap in testing areas

• Testing script design

• Measure and track results: Company,

Department, Team and Employee

• Develop and track quality metrics on the Quality

Control team

• Effective follow-up and action planning with

business units

• Use feedback as a training method for staff

• Admit issues and fix them – ‘clean up your spill’

Quality Control Efficiencies: Considerations

• Quality Control results in operations’ performance goals

• Automated Software Systems

• Quality Interfaces

• Enterprise Risk Management

• Compliance, regulatory and investor requirements

• Servicing Systems

• Policy and Procedures

• Decision to Outsource

• Interim – new products

• Niche products

• Mock audits

• Cost efficiency

• Decision to Offshore

• Specific functions

Questions

Thank You!

Moderator:

Mark Atencio, Executive Consultant, Lyons McCloskey, LLC

lyonsmccloskey.com

[email protected] 602-228-4974

Panelists:

Jennifer Greear, Vice President, Wells Fargo Home Mortgage

wellsfargo.com/mortgage/

[email protected] 515-398-1540

Wade Mjelde, VP, Servicing QC Division, Tena Companies, Inc

Tenaco.com

[email protected] 651-379-6283

Jim Shankle, Managing Director, CrossCheck Compliance

crosscheckcompliance.com

[email protected] 312-346-4600

Appendix

Best Practices for Implementing Complaint Management Program

Common Data Fields Captured by Servicers

Best Practices for Implementing Complaint Management Program

Common Data Fields Captured by Servicers

• Date complaint received

• Channel complaint received

• Servicing issue identified in the complaint (payment processing; collections; loan modification, etc.)

• Summary of borrower complaint received

Written complaint received from borrower

Summary of complaint received by call center (can be recorded call from borrower)

Narrative prepared by servicing personnel

Regulatory agency

Best Practices for Implementing Complaint Management Program

Common Data Fields Captured by Servicers (continued)

• “Tags” to identify categories of borrowers (service member; loss mitigation; FCL; BK, etc.)

• Response Status

In-process

Closed with explanation

Closed with monetary relief

Closed with non-monetary relief

• Date of response to borrower

Best Practices for Implementing Complaint Management Program

Common Data Fields Captured by Servicers (continued)

• Was response timely?

If not, why?

• Borrower satisfied with response?

If not, document follow-up or escalation process, if applicable

• Complaint risk rating

Develop standardized rating definitions and action steps for escalating complaints

Common ratings assigned are high, moderate and low

Best Practices for Implementing Complaint Management Program

Common Data Fields Captured by Servicers (continued)

• Consider risk ranking all complaints as high risk for the following:

Source of complaint is regulatory agency (regardless of severity of allegation)

Complaint alleges potential fair lending violation

Complaint, as described could be interpreted as UDAAP

Per the servicer’s policy, complaint is required to be escalated to board and/or

legal

Transactional Testing: The Servicing File

Key File Ingredients

Transactional Testing: Key File Ingredients

• Mortgage or Deed of Trust • Social media postings to which servicer has responded

• Default Notices

• Note • Servicer responses with dates • Bankruptcy Documentation

• Closing Disclosure or HUD-1 Settlement Statement

• Electronic data related to the borrowers’ account (all systems)

• Loss Mitigation Offers and Documentation

• Home Equity disclosure documents at time of application

• All information and documents related to errors, complaints and loss mitigation

• Adverse Action Notices

• Annual Statements • Collection notices, comments, notes • Borrower Appeal Notices

• All communications from and to borrower including phone calls, recordings, emails, social media postings, etc., including, but not limited to, the following:

• Notices, letters and statements provided by servicer and/or vendors on behalf of servicer including, but not limited to, the following:

• Payment information change notices (e.g. address changes for making payments)

• Complaint notices • Monthly statement • Foreclosure Documents including internal referral notes

•Presidential letters • Escrow Analyses • Disposition Notification to Borrower

• Mortgage account monetary transaction history including payments and disbursements

• Notices of deficiency or shortage • Charge Off notifications

Transactional Testing: Key File Ingredients

• Privacy Notices • Borrower notification of acquisition, assignment or transfer

• Refund statements

• Notices, letters and statements provided by servicer and/or vendors related to servicing transfers (in and out) including, but not limited to, the following:

• Hazard, Flood, Windstorm, Other, and optional Insurance notifications

• All notices, correspondence, notes, recorded calls related to private mortgage insurance cancellation including, but not limited to, the following:

• New loan onboarding file • Biweekly program notifications • Borrower requests:

• Servicing transfer disclosure • Biweekly payment plan application with payment history, if applicable, from prior servicer

• Servicer responses

• Correspondence to and from borrower • Employee Roster at time of acquisition or transfer

• Notification of cancellation

• Previous servicer notes • Military orders and duty records • Loan modification documentation

• Servicer notes • Evidence of SCRA compliance • Origination file documentation related to high risk loans

• Hello/Goodbye Letters • Notices related to home equity plans • Annual disclosures

• ARM disclosure documents including, but not limited to, the following

• Force Placed Insurance Letters and Reminder notices

• Deficiency Judgment notifications

Transactional Testing: Key File Ingredients

• Initial Rate change disclosure • Flood Notices • Charge Off notes

• Rate change disclosures • Collection Letters • Claim documentation

• Rate adjustments and payment change disclosures

• Delinquency notices • Affinity product offering solicitations

• Validation of debt letter • Notices of deferred interest • Acknowledgement Notices

• Dispute requests from borrower • Borrower Payoff Requests • Credit reporting history

• Previous servicer correspondence (notes, call activity, etc.) related to transfer

• Borrower Payoff Statements • Servicing file creation date

• Previous servicer loan file • Loss mitigation documentation from previous servicer

• Loss mitigation documentation from previous servicer