publication carbone 4 infrastructures - climate

TRANSCRIPT

INFRASTRUCTURE:A KEY ASSET CATEGORY FOR THE CLIMATE

What exactly do we mean by ‘ infrastructure’?

Why does the success of the energy transitiondepend on such assets?

To what extent should climate risks be betterincorporated into infrastructure portfoliomanagement?

What follows is a general overview that Carbone4 has put together of this asset category and theissues that link it to climate change.

Carbone 454 rue de Clichy 75009 PARIS [email protected]+33 (0)1 76 21 10 00www.carbone4.com

Finance divisionJune 2019

Sylvain BorieSenior Consultant

Juliette DecqManager

Contact :[email protected]

2 www.carbone4.com

TABLE OF CONTENTS

INTRODUCTION

KEY MESSAGES

3

4

1 A NEW AND VERY DYNAMIC ASSET CATEGORY

5

2 INFRASTRUCTURE: ASSETS AT THE HEART OF CLIMATE CHANGE-RELATED ISSUES

9

3 WHAT CAN INVESTORS AND MANAGERS DO?

15

CONCLUSION 16

INTRODUCTION

www.carbone4.com3

Infrastructure is a very hot topic at themoment; from the privatisation ofAéroport de Paris to the €20bn 10-yearhigh-speed broadband plan, notforgetting record capital campaigns fromFrench firm Ardian and Swedish firm EQT,there is certainly no shortage ofopportunity, or of enthusiasm concerninginvestors.

Something else that has been in the newsrecently is the tragic collapse of thebridge in Genoa - a reminder of thecritical importance of maintaining currentinfrastructure in good condition as vitalorgans that help keep our economy alive.

Infrastructure also plays a key role in theissues associated with the climatetransition. It might enable our economyto develop, but infrastructure also resultsin the generation of emissions thatcontribute to climate imbalance, whichcan in turn lead to such physical assetsbeing exposed to increased risks.

Conversely, an ambitious emissionsreduction policy could disrupt the long-term stable and predictable returns onwhich the success of this asset categoryrelies upon.

How should infrastructure investors andmanagers be interpreting all of thesechallenges and opportunities?

It might enable our economy to develop, but infrastructure also results in the generation of emissions that contribute to climate imbalance, which can in turn lead to such physical assets being exposed to increased risks.

4

KEY TAKEAWAYSSUMMARY

TWO MAJOR CHALLENGES FOR INFRASTRUCTURE INVESTORS & MANAGERS

Infrastructure plays a special role in the fightagainst climate change and there are twopriorities that infrastructure investors andmanagers must address:à Immediately embark upon an investmentpath that makes it possible to stay within theParis Agreement carbon budget. This is whatis known as a 2°C/1.5°C compatiblepathway.à Integrating climate risk managementpractices, whether transitional or physical.

RISK MANAGEMENT: INCORPORATING CLIMATE CHANGE INTO THE INVESTMENT PROCESS AS A WHOLE

Infrastructure portfolios are exposed to ahigh risk of stranded assets as a result ofboth the climate transition and acceleratedclimate change consequences.

The strategy adopted by investors and assetmanagers must be implemented on anumber of levels if these risks are to beminimised as much as possible:

- When defining the investment strategyand choosing new assets

- Throughout the entire period for which theasset is held in order to encourage itstransformation towards a low-carboneconomy and achieve the following:

• a level of climate performance that iscompatible with the Paris Agreement(focusing notably on the 3 main pillars,namely sobriety, energy efficiency andthe integration of low-carbon energysources)

• a level of resilience that is compatiblewith the climate conditions of the future(concrete designed to withstandheatwaves, resilience to increasingly badweather, etc.).

2°C COMPATIBLE PORTFOLIO: FINDING THE RIGHT BALANCE

Identifying a 2°C/1.5°C compatible pathwayis not the same as a portfolio consisting of100% renewable production assets. Whilstthe latter are, of course, vital to the successof the energy transition, the other issue hererelates to investment in energy efficiencyand the accelerated transformation of assetsthat are currently highly carbon-dependent,such as motorways, buildings and airports.

This being the case, airports and motorways,for example, could be included in these ‘2°Ccompatible’ infrastructure portfoliosprovided that their individual climateperformance and their weighting within theportfolio (as a % of the euros invested) arecompatible with the carbon budget,meaning that they limit global warming to+1.5 or 2°C. It is very unlikely, for example,that a portfolio with 30% airport investments(as a % of the euros invested by the fund) willbe compatible with the carbon budget andthe 2°C global warming limit.

5

Utilities : distribution andtreatment of waste and water

Energy : production, transport and distribution of electricity, gas or oil, renewable or not.

Telecommunications : servers, optical fibre, communication towers

Transport : ports, highways, airports, bridges, rail network, tunnels, parking…

Social : hospitals, schools, stadiums, public buildings (courthouse…)

1A NEW AND VERY DYNAMIC ASSET CATEGORY

INFRASTRUCTURE: VITAL ASSETS AND SERVICES ON WHICH A SOCIETY’S ECONOMIC PRODUCTIVITY DEPENDS

The term ‘infrastructure’, which firstappeared in the late 1880s, refers to thebasic physical systems on which a businessor country is built. These systems, whichhave a long lifespan and require significantinvestment, are vital to a country’sproductive activity.

Infrastructure tends to require significant investment and is vital to a country’s economic development and prosperity

THE DIFFERENT TYPES OF INFRASTRUCTURE

Whilst there is no truly exhaustive commonlist of assets that might be considered asinfrastructure, certain assets areunanimously considered to fall into theinfrastructure category, and these can bedivided into 5 sub-categories (seediagram)

The definition of infrastructure can be usedbroadly. Some classification systems mightalso include ore and metal productionassets, whilst others will include defenceand security-related assets or evenagricultural land.

THE GROWING PRESENCE OF PRIVATE INVESTMENTS

Traditionally the domain of publicauthorities, it is becoming increasinglycommon these days for infrastructureprojects to be funded by private sources.

There is, in fact, a growing need forinfrastructure funding, and this needcannot be met using public resourcesalone. This need has resulted in thedevelopment of the famous Public-PrivatePartnerships (PPP) and concession systemsor public companies over the course ofrecent decades.Industrial players are generally interested inthis type of contract because it providesthem with access to captive markets (forexample, thanks to a PPP agreement for astadium, a player in the building andpublic works industry would be able tobuild the stadium themselves).

THE 5 MAJOR SUB-CATEGORIES OF INFRASTRUCTURE

INFRASTRUCTURE: AN ASSET CATEGORY IN ITS OWN RIGHT

Just like bonds, infrastructureoffers predictable long-term returns. It is also conducive to leveraging capital investment and private equity and shares a distinctive feature with property in terms of investing in physical assets.

Institutional investors, however, are alsointerested in this type of asset because itgives them access to recurring long-termcash flows, not to mention a good level ofdiversification, which is why infrastructureemerged as an asset category, initially inAustralia, in the 1990s, and more recently inEurope.

Infrastructure is a ‘hybrid’ category as itcombines some of the characteristics ofdifferent asset categories. Just like bonds,for example, infrastructure offerspredictable long-term returns. It is alsoconducive to leveraging capitalinvestment and private equity and shares adistinctive feature with property in terms ofinvesting in physical assets.

According to Vincent Levita, “infrastructurefunds provide not only a competitivefunding solution for such projects but alsothe characteristics that many institutionalinvestors are looking for and are no longerable to find in traditional asset categories,or even, really, in alternative assetcategories.

Indeed, infrastructure funds offer thefollowing benefits:

• a long-term duration and investmenthorizon,

• a real return (with an IRR of between 10and 20%) and inflation protection (theservices that end-users pay for ofteninclude clauses relating to the level ofinflation),

• diversification and a weak correlationwith financial markets,

• an illiquidity premium with a relativelylow capital risk.”

INFRASTRUCTURE AS AN ASSET CATEGORY: A BROAD DEFINITION...

All assets that fall within the broaderdefinition of infrastructure (a physical assetwith a clearly defined purpose thatgenerates stable cash flows based onprice and volume projections that can bemade based on a natural or statutorymonopoly with strong barriers to entry andlittle potential direct competition) can beincluded in an infrastructure portfolio.

This being the case, it is perfectly possibleto see fleets of vehicles, load sheddingunits and even agricultural assetsfeaturing alongside traditional assets inportfolios since such assets are managedas infrastructure.

6

… BUT A VERY STABLE SECTORAL ALLOCATION OF INVESTMENT

In practice, however, infrastructure funds primarily invest in the sort of shared infrastructure defined above (Source: Preqin Infrastructure Online):

7

61%

9%

18%

9%

2%1%

EnergyTransportSocialUtilitiesTelecommunicationsOther

Number of deals per asset type in 2017

EXPONENTIAL GROWTH...

Investor’s appetite is demonstrated by the fact that the amounts generated by infrastructurefunds increased fourfold in the space of 10 years, from $100bn in 2007 to $418bn in 2017, withthe volume of assets under private management doubling over the same period.

Furthermore, this trend is gaining momentum, notably in Europe and particularly in France,where infrastructure funds are breaking capital campaign records on a regular basis. Theamount of capital raised by French funds, for example, tripled between 2017 and 2018 (€4.2bnas opposed to €12.1bn), meaning that the sector has some $23bn in dry powder (amounts thathave been raised but not yet invested by asset managers) that will be invested over the comingyears.French players are therefore establishing themselves as true global leaders.

The Ardian fund caused something ofa sensation in late January 2019 byraising Europe’s largest infrastructurefund, valued at €6 billion. The lastvehicle, created in 2016, failed toexceed 2.65 billion.American fund GIP and Canadian firmBrookfield, meanwhile, are about toraise funds valued at over $20 billion.

The fact that the sector is attracting such enthusiasm, in comparison with France’scommitments to neutrality, is forcing the sector to assess and consequently reduce anyaspects that might have a negative impact on climate change. The huge volume of drypowder available and the intense competition surrounding assets to acquire, however,tends to push prices up, thus making it all the more important to have a well-honed businessmodel and strict and thorough transition and physical risk management practices in orderto avoid a loss resulting from any political, economical or climate-related surprises in themedium term.

... THAT REQUIRES A MORE DISCIPLINED APPROACH TO CLIMATE RISKS

French players are establishing themselves as true global leaders.

x 4.2

x 2.1

In infrastructure:

In other asset categories:

Growth in the amounts invested by unlisted portfolio managers over the

2007-2017 period:

/

8

9

2INFRASTRUCTURE: ASSETS AT THE HEART OF CLIMATE CHANGE-RELATED ISSUES

HEADING TOWARDS ANUNPRECEDENTED CLIMATE CRISIS

It is essential, first and foremost, that webear in mind the unprecedented scaleand nature of the anthropogenicclimate change we are facing today.

In fact, we would have to go back 3million years to find an atmosphericconcentration of CO2 as high as it istoday (Potsdam Institute for ClimateImpact Research).The anthropogenic phenomenon we arecurrently witnessing as a result ofgreenhouse gas emissions generated byhuman activity (caused primarily byburning oil, coal and gas) is therefore notonly very intense but also developingvery rapidly.

The last deglaciation of the Earth, whichcaused sea levels to rise over 100m anddisplaced ecosystems by some 20degrees of latitude, was, in fact, theresult of a natural warming of "only" 5°Cover the course of 5,000 to 10,000 years.We could now be witnessing a warmingof a similar magnitude, this time over thecourse of just a century or two...

We are certainly dealing with a brutalphenomenon, one that is the first of itskind in the history of humanity and theconsequences of which will wreakabsolute havoc for human society.

TARGETING INVESTMENT AND MANAGING CLIMATE RISKS

Investors must take on board two majorchallenges:

- guiding investment in order to make apositive contribution to the energytransition

- protecting themselves against climaterisks, both transition-related (thoseassociated with the regulatory, technicaland market developments we will see aswe move towards a low-carboneconomy) and physical (thoseassociated with the accumulatedconsequences of climate change, suchas global warming, changes in theprecipitation pattern, heat waves, risingsea levels, etc.)

This dual challenge applies to all assetcategories. The challenges are, however,all the more significant whereinfrastructure is concerned owing to itsvery long lifespan and to the fact that therevenue it generates depends very muchon its physical integrity.

The challenges are all the more significant where infrastructure is concerned owing to its lifespan and the fact that the revenue it generates depends on its physical integrity.

“EXISTING INFRASTRUCTURE ACCOUNTS FOR 95% OF THE CARBON BUDGET AVAILABLE IF WE ARE TO REMAIN WITHIN A LIMIT OF 2°C” (International Energy Agency)

This observation leads to an extremelyrestrictive conclusion for the sector, namelythat introducing new carbon-dependentinfrastructure today would automaticallydestroy our chances of meeting the 2°Ctarget outlined in the Paris Agreement.

With this in mind, meeting thecorresponding targets for fighting climatechange represents three consequenceswhere infrastructure managers andinvestors are concerned:

CONSEQUENCE #1: Those assets thatdepend the most on greenhouse gasemissions will have to close prior toreaching their anticipated date ofeconomic maturity.

Whilst we may have a few years before weexceed the 2°C threshold for globalwarming, the residual lifespan and activitylevel of existing infrastructure means that itsemissions potential accounts for all of theemissions that we can still afford togenerate (i.e. the carbon budget).

If new infrastructure were to result in thisbudget being exceeded, this would meanthat achieving the objectives set by theParis Agreement would necessarily result inthe emergence of stranded economicassets (assets that are prematurelydecommissioned as a result of the fightagainst climate change).Sticking to the budget will inevitably resultin the closure of certain existinginfrastructure assets if new projects that willgenerate their own emissions are to becreated.

The example of the French coal-firedpower stations that are set to close by 2022whilst others have recently been renovatedwith the aim of keeping them running until2030 is an effective illustration of thisphenomenon, which is likely to bemagnified in the future.

CONSEQUENCE #2: Existing assets will haveto significantly improve their carbonperformance or change their businessmodels.

Indeed, existing assets have an emissionspotential attributed to them, but it ispossible to change business models(switching from a basic model to a cutting-edge production model for a carbonasset), accelerate renovation and increasethe scale thereof, and even decarbonisethe use of existing infrastructure wherepossible (e.g. reducing the emissions pervehicle for a motorway).

Taking such factors into account in theinvestment strategy will also have animpact on negotiations regarding theacquisition of new assets.

CONSEQUENCE #3: It is important to investin assets that contribute to the energytransition (renewables, energy efficiency,transition infrastructure, etc.)

Responsibility on the part of infrastructureproject sponsors is therefore critical sinceall new assets that spring up will generatetheir own emissions for many years tocome. With this in mind, compatibility withefforts to limit global warming to 2°C mustplay a central role when it comes toselecting investments.

The fact that the current ‘business as usual’state of the world is not, by definition,compatible with this 2°C limitation meansthat we need to completely rethink currentmethods and ways of thinking in this sector.

10

The New Climate Economy claimed, in2015, that an additional $1,000 billionof investment each year is necessaryin order to finance the energyefficiency and low-carboninfrastructure and annual divestmentin fossil fuels of up to $400bn everyyear is needed.

THE FIGHT TO AVOID STRANDED ASSETS

As previously mentioned, complying with theParis Agreement whilst at the same timehaving an emissions potential that exceedsthe carbon budget available will unavoidablylead to the emergence of stranded assets.That said, if emissions are not limited, thelatter will inevitably emerge as consequencesof a rapid rate of global warming, which willin turn lead to increasing levels of damagewhere physical assets, such as networks,ports, power stations, etc., included ininfrastructure asset portfolios are concerned.

Stranded assets can therefore come aboutas a result of both transition risks andphysical risks.

Ultimately, whilst some assets will ‘suddenly’need to be shut down, a very large numberof assets will experience a loss in value orprofitability as a result of climate risks. Whatwe are dealing with here is a continuum ofrisk with financial consequences that will varyin severity depending on the asset inquestion.

Whilst naturally greenfield project sponsorsare concerned by how to achieve climatetargets, brownfield managers are, in fact,equally concerned.

Indeed, one of the roles that brownfieldinvestors play within the financialecosystem is to enable other players, andnotably project sponsors, to sell assets witha view to freeing up cash that can then beinvested in new developments.

Taking into account changes in the costsand revenues associated with complyingwith the Paris Agreement, brownfieldinvestors will naturally increase theirrequirements when it comes to purchasingcarbon-dependent assets.

If a clear indication of this is detected,project sponsors may be less inclined todevelop carbon-intensive assets if theyknow that they will have difficulty sellingthem at the desired price.

This being the case, the solution will requireaction for all stakeholders involved.Investors must therefore adopt aresponsible approach to climate changeas part of their mandates, which should, atthe very least, include analysing thecompatibility of the investment strategywith limiting global warming to 2°C.

A RESPONSIBILITY SHARED BY ALL OF THE PLAYERS INVOLVED

Staying within the carbon budget will clearly result in theemergence of stranded assets where fossil fuel reservesand assets that depend on them (shopping centres,motorways, ports, etc.) are concerned

Carbon budget v. Fossil fuel reserves(source: CRO Forum – The heat is on)

The wait-and-see approach which involves not committing to taking any outrightaction to reduce emissions for fear that it might affect the profitability of certainassets is a short-term vision. Indeed, the latter results in a certain irreversibledeterioration in the profitability of other assets in the long term owing to theincreased presence of physical risks.

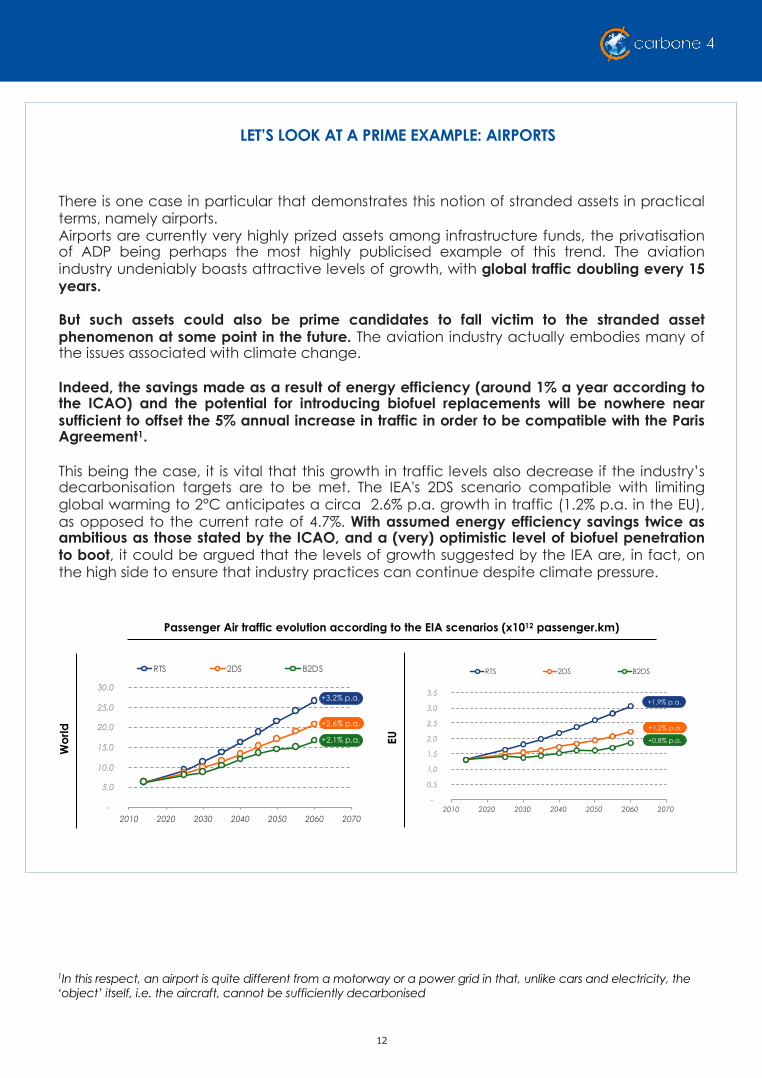

There is one case in particular that demonstrates this notion of stranded assets in practicalterms, namely airports.Airports are currently very highly prized assets among infrastructure funds, the privatisationof ADP being perhaps the most highly publicised example of this trend. The aviationindustry undeniably boasts attractive levels of growth, with global traffic doubling every 15years.

But such assets could also be prime candidates to fall victim to the stranded assetphenomenon at some point in the future. The aviation industry actually embodies many ofthe issues associated with climate change.

Indeed, the savings made as a result of energy efficiency (around 1% a year according tothe ICAO) and the potential for introducing biofuel replacements will be nowhere nearsufficient to offset the 5% annual increase in traffic in order to be compatible with the ParisAgreement1.

This being the case, it is vital that this growth in traffic levels also decrease if the industry’sdecarbonisation targets are to be met. The IEA's 2DS scenario compatible with limitingglobal warming to 2°C anticipates a circa 2.6% p.a. growth in traffic (1.2% p.a. in the EU),as opposed to the current rate of 4.7%. With assumed energy efficiency savings twice asambitious as those stated by the ICAO, and a (very) optimistic level of biofuel penetrationto boot, it could be argued that the levels of growth suggested by the IEA are, in fact, onthe high side to ensure that industry practices can continue despite climate pressure.

1In this respect, an airport is quite different from a motorway or a power grid in that, unlike cars and electricity, the ‘object’ itself, i.e. the aircraft, cannot be sufficiently decarbonised

LET’S LOOK AT A PRIME EXAMPLE: AIRPORTS

12

Passenger Air traffic evolution according to the EIA scenarios (x1012 passenger.km)

-

5,0

10,0

15,0

20,0

25,0

30,0

2010 2020 2030 2040 2050 2060 2070

RTS 2DS B2DS

+3,2% p.a.

+2,6% p.a.

+2,1% p.a.

Wo

rld

EU

-

0,5

1,0

1,5

2,0

2,5

3,0

3,5

2010 2020 2030 2040 2050 2060 2070

RTS 2DS B2DS

+1,9% p.a.

+1,2% p.a.

+0,8% p.a.

Consumers who are sensitive to environmental issues have indeed taken the matter onboard, with various initiatives, such as the flygskam (or ‘shame of flying’) initiative inSweden, springing up in the most advanced of countries. The aforementioned initiative,which condemns choosing to fly over taking the train, is undoubtedly linked to the 5% dropin the number of flights taken with Sweden’s domestic airlines over the course of a year. It ishighly likely that this type of initiative could be extended, in some form or other, to othercountries.

For background purposes, we should also add that kerosene is not currently taxed - aprivilege that is difficult to sustain if you are claiming to be serious about wanting to limitclimate change, and it is safe to say that the future of the aviation industry in thistransitioning world will not be as bright as its recent past. Le Monde echoed the EuropeanCommission’s discussions concerning the taxation of kerosene last May, indicating thatthings could be about to change.

LET’S LOOK AT A PRIME EXAMPLE: AIRPORTS

13

the flygskam or ‘shame of flying’ initiative has already resulted in a 5% drop in the number of flights taken with Sweden’s domestic airlines in a year.

Current frequence and intensity exposure to heatwaves

Source : Climat: Notes créées à partir de l’étude de l’évolution de Tmax et du nombrede jours de vagues de chaleur, sur la période1960-1999. Notation : Carbone 4 à partir des sorties de trois modèles (GFDL, CNRM et IPSL). Aéroports : MIT/Partow

© 2018 Carbone 4

AIRPORT EXPOSURE TO HEAT WAVES

A recent study by Carbone 4 explored theimpact of heat waves on airport activity(bearing in mind that these are not theonly physical risks to which such assets areexposed (see extract below)).Of course, heat waves are not the onlyclimate hazards that we need to look outfor, either, with 25% of the world’s busiestairports actually located less than 10mabove sea level and traffic at Osakaairport having been disrupted for anumber of days in September 2018 owingto a rise in the level of the Pacific Ocean.

LET’S LOOK AT A PRIME EXAMPLE: AIRPORTS

14

Kansai International Airport flooded following Typhoon Jebi (source:

ladepeche.fr)This general picture obviously varies somewhat depending on the location of the airportand the volume of traffic it handles, but an infrastructure fund manager looking to limittheir exposure to climate risks would have to pay particular attention to the threats towhich airports are exposed in the medium term.

Maintaining the status quo, however, would not necessarily be any better. Indeed, if we donot succeed in decarbonising the world, the physical risks to which airports are exposedwill be substantial.

15

OUTLINE AN INVESTMENT PATH THAT IS COMPATIBLE WITH THE PARIS AGREEMENT

3WHAT CAN INVESTORS AND MANAGERS DO?

It is vital that climate-related risks be taken into account at every stage of the managementprocess in order to minimise exposure to such risks. This primarily requires a goodunderstanding of the issues at hand (notably through appropriate training), which is still rarelythe case, and for technical resources devoted specifically to such matters to be incorporated.It also requires proven portfolio decarbonisation management methods corresponding to theproblem at hand.

In order to one day achieve a portfoliothat is compatible with a 2°C pathway atglobal level the following steps must betaken:

à systematically perform a transition riskanalysis and a physical risk analysis foreach asset in the portfolio;

à do the same for any potential newinvestments;

à For new investments, select only assetswhose use is not affected by a 2°Ccompatible pathway (which requiresglobal emissions to be cut by two-thirds in30 years) and that are not at risk due to thephysical consequences of future changesin the geographical areas in which theyare located;

THE CLIMATE CHECK-LIST

à examine and outline in detail how thecarbon dependency of the assets alreadyin the portfolio and intended to beretained can be reduced;

à determine whether, in the case of theassets in question, this dependency can besufficiently altered (which, unfortunately,will often not be the case);

à take the appropriate measures identifiedto reduce carbon dependency in thosecases in which this is possible (byencouraging a decrease in its usage byincreasingly low-emission vehicles in thecase of a motorway, or by increasing theproportion of biogas in a gas distributionnetwork, for example).

16

CONCLUSION

THE NEED TO ACT QUICKLY

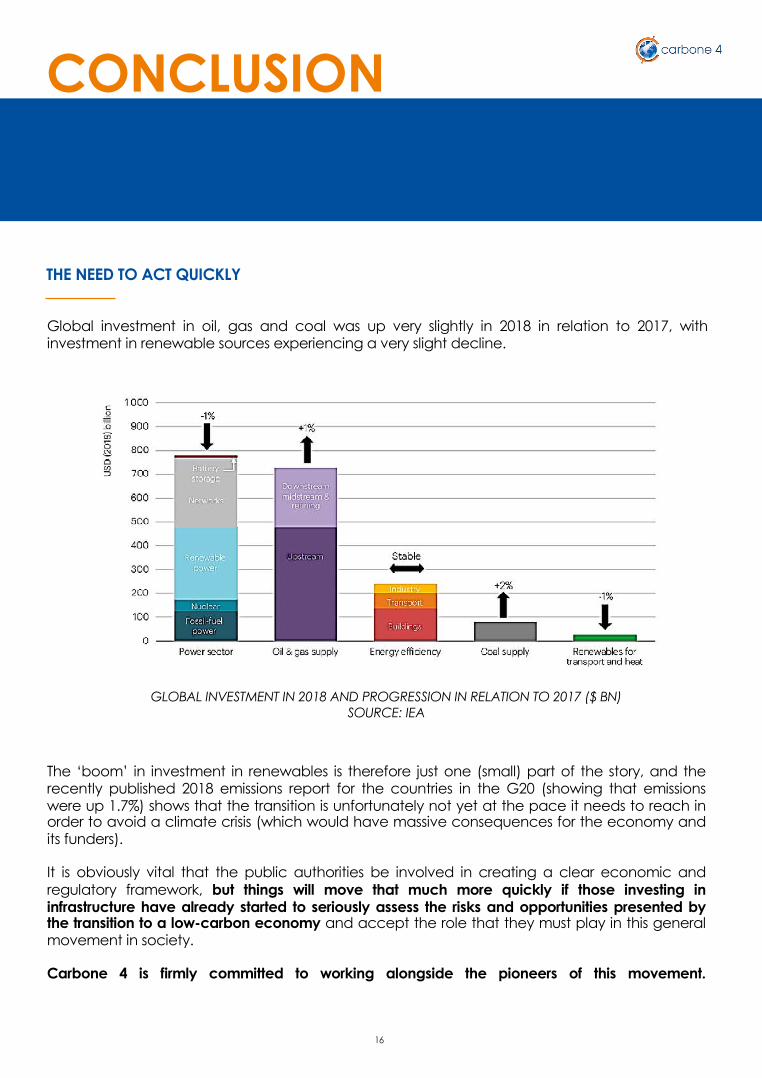

Global investment in oil, gas and coal was up very slightly in 2018 in relation to 2017, withinvestment in renewable sources experiencing a very slight decline.

The ‘boom’ in investment in renewables is therefore just one (small) part of the story, and therecently published 2018 emissions report for the countries in the G20 (showing that emissionswere up 1.7%) shows that the transition is unfortunately not yet at the pace it needs to reach inorder to avoid a climate crisis (which would have massive consequences for the economy andits funders).

It is obviously vital that the public authorities be involved in creating a clear economic andregulatory framework, but things will move that much more quickly if those investing ininfrastructure have already started to seriously assess the risks and opportunities presented bythe transition to a low-carbon economy and accept the role that they must play in this generalmovement in society.

Carbone 4 is firmly committed to working alongside the pioneers of this movement.

GLOBAL INVESTMENT IN 2018 AND PROGRESSION IN RELATION TO 2017 ($ BN)SOURCE: IEA

Carbone 4 is the leading independent consulting firm specialized in low carbon strategyand climate change adaptation.Driven by strong values of commitment, integrity and boldness, the Carbone 4 team ismade up of 35 passionate and expert employees.Our common goal since 2007: to guide our clients in understanding the emerging world.Constantly paying attention to weak signals, we use a systemic vision of the energy-climate constraint, while keeping in mind that the vital technical transformation needs tocome with a change of mindset.With a great attention to details and creativity, we work to turn our customers into leadersof the climate challenge.