prospective value appraisal report

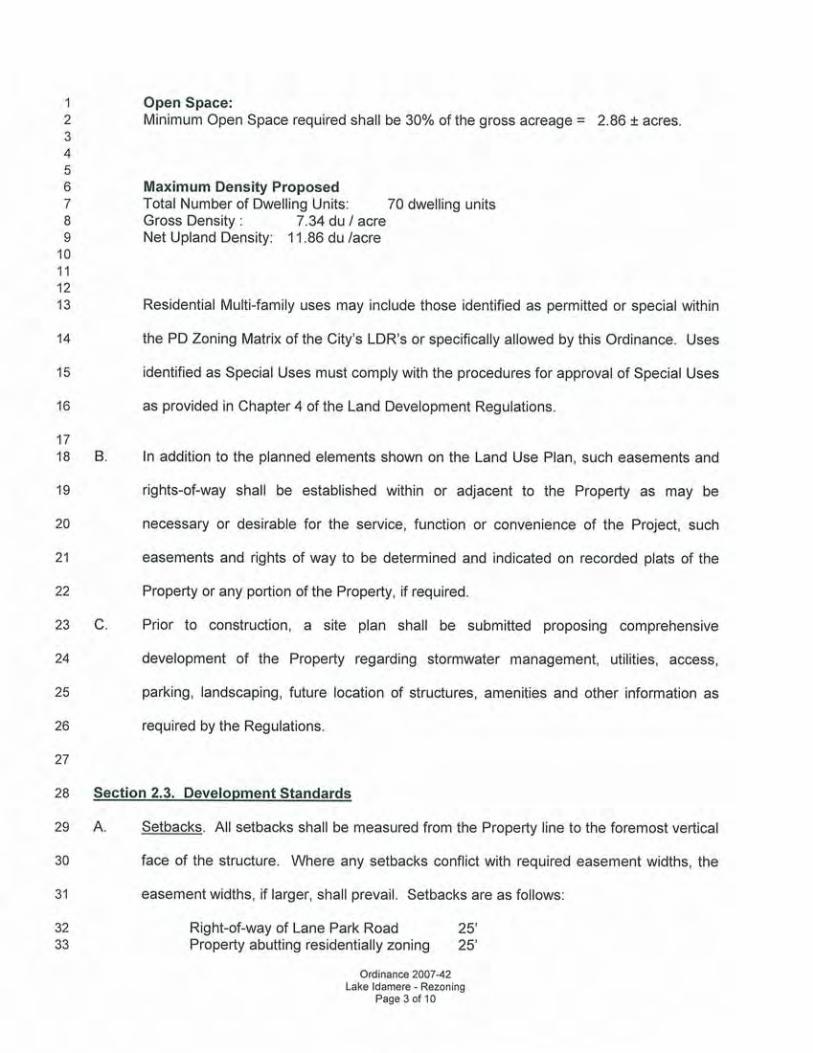

TRANSCRIPT

Prospective Value Appraisal Report

9.54 Acres Previously Proposed for Development as Lake Idamere Townhomes South Side of Lane Park Cutoff, East of US Highway 19

In the Municipality of Tavares, Lake County, Florida 32778

MAY 26, 2017

FOR

Fairwinds Credit Union Mr. Aaron Gozan, Special Assets Officer

135 W. Central Boulevard, Suite 120

Orlando, Florida 32801

Valbridge Property Advisors | Beaumont Matthes and Church

603 Hillcrest Street Orlando, Florida 32803 (407) 839-3626 phone (407) 839-3453 fax Valbridge Job No.: FL02-17-157-000 valbridge.com

603 Hillcrest Street

Orlando, Florida 32803

407-839-3626 phone

407-839-3453 fax

valbridge.com

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc.

May 26, 2017

Mr. Aaron Gozan, Special Assets Officer

Fairwinds Credit Union

135 W. Central Boulevard, Suite 120

Orlando, Florida 32801

RE: Appraisal Report of the 9.54 acres previously proposed for development as Lake Idamere

Townhomes, located at the south side of Lane Park Cutoff, east of US Highway 19, in the

municipality of Tavares, Lake County, Florida 32778

Dear Mr. Gozan:

In accordance with your request, we have prepared a real property appraisal of the above-referenced

property. This appraisal report sets forth the pertinent data gathered, the techniques employed, and the

reasoning leading to our value opinions. The purpose of the appraisal was to provide an opinion of the

prospective market value of the fee simple estate of the subject property described herein, as of May 31,

2017.

The intended use of the report is in making decisions regarding the disposal of the obligation secured by

the property, by the intended user, Fairwinds Credit Union. This appraisal report was prepared for the

sole use and benefit of Fairwinds Credit Union. There are no other intended uses and/or users of this

report.

We developed our analyses, opinions, and conclusions and prepared this report in conformity with

Standards Rule 2-2(a) the Uniform Standards of Professional Appraisal Practice (USPAP) of the Appraisal

Foundation; the Financial Institutions Reform, Recovery, and Enforcement Act (FIRREA); the Interagency

Appraisal and Evaluation Guidelines; the Code of Professional Ethics and Standards of Professional

Appraisal Practice of the Appraisal Institute; and the requirements of our client as we understand them.

The acceptance of this appraisal assignment and the completion of the appraisal report submitted

herewith are subject to the General Assumptions and Limiting Conditions contained in the report. The

findings and conclusions are further contingent upon the following extraordinary assumptions and/or

hypothetical conditions which might have affected the assignment results:

Extraordinary Assumptions: Per the client’s request, the date of value of this appraisal is May 31, 2017. The date of our

inspection was May 20, 2017. Therefore, the opinion of value contained herein is a Prospective

Value. This report is subject to the Extraordinary Assumption that there will be no substantive

changes to the legal, physical or economic issues pertaining to the subject property between the

date of our inspection and the date of value.

This appraisal is subject to a study reflecting no gopher tortoise issues on the subject property, an

Extraordinary Assumption.

Hypothetical Conditions: None

Fairwinds Credit Union

May 26, 2017

Page 2

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc.

Based on the analysis contained in the following report, our value conclusion involving the subject

property is summarized as follows:

Date Of Inspection May 20, 2017

Date Of Report May 30, 2017

Date Of Value May 31, 2017

Market Value $460,000*

*Prospective

This letter of transmittal must be accompanied by all sections of this report as outlined in the Table of

Contents, in order for the value opinions set forth above to be valid.

Respectfully submitted,

Valbridge Property Advisors | Beaumont, Matthes & Church, Inc.

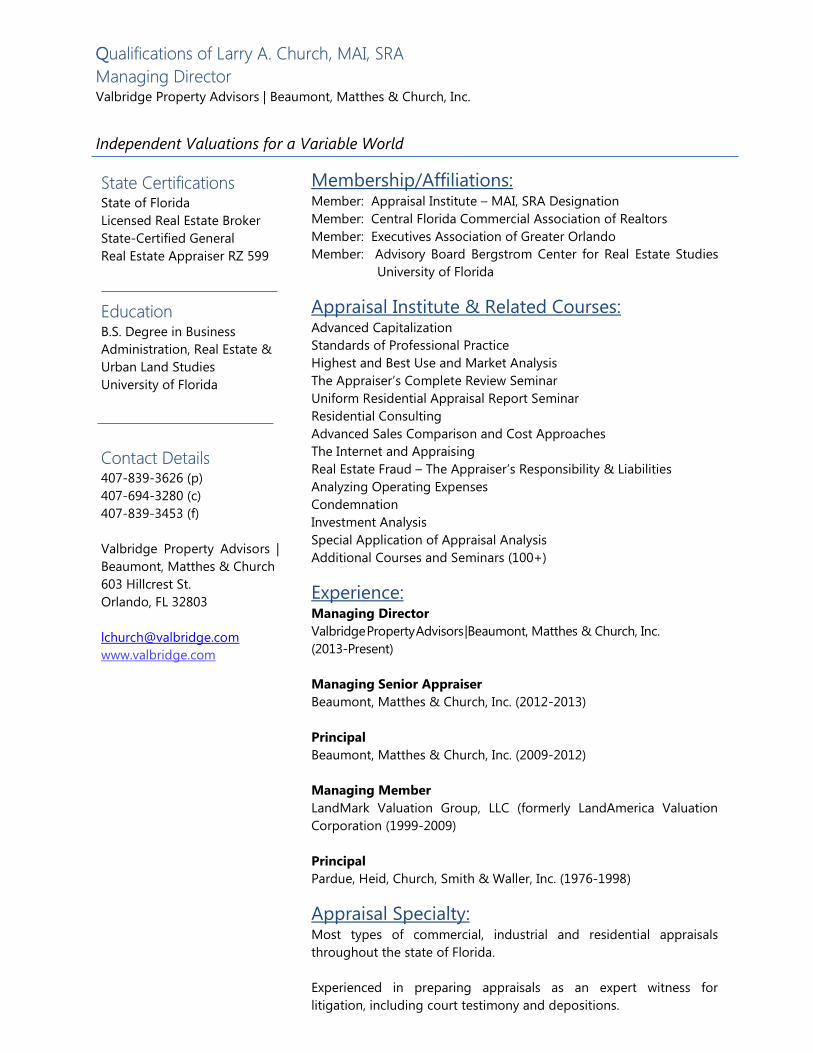

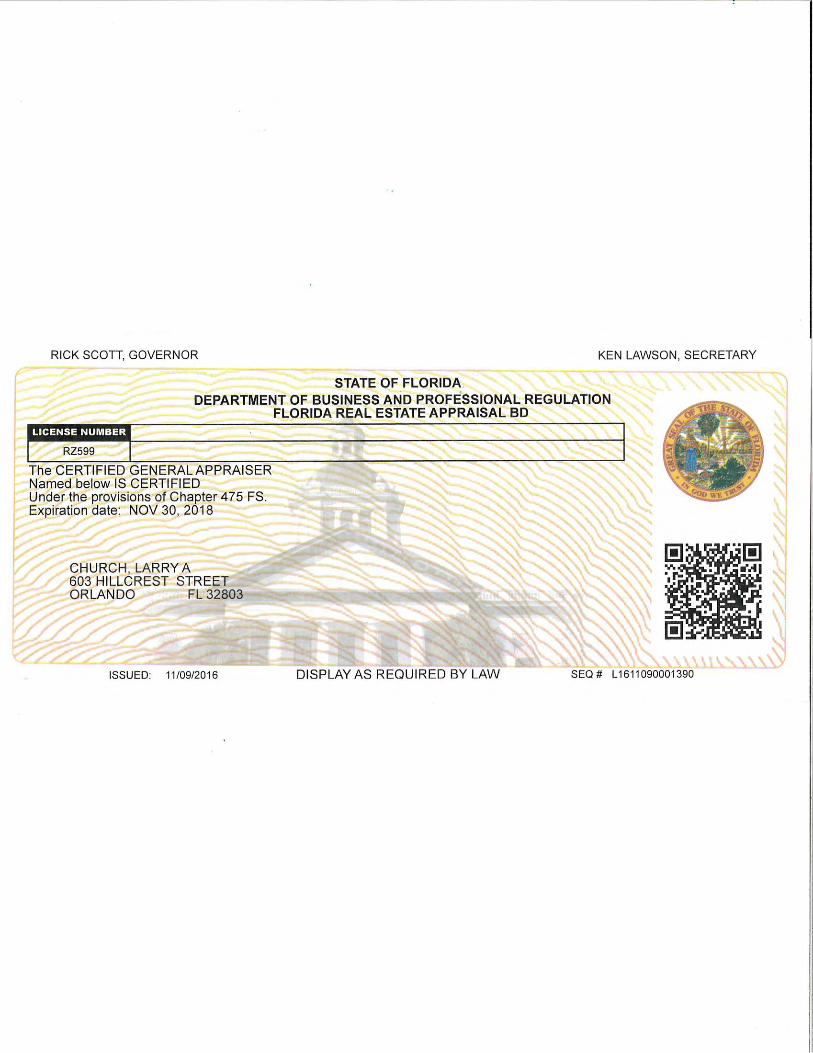

Larry Church, MAI, SRA Michael D. Dabby

Managing Director Director, Senior Land and Subdivision Specialist

State-Certified General State-Certified General

Real Estate Appraiser RZ 599 Real Estate Appraiser RZ 1590

[email protected] [email protected]

407-839-3626 (Ext 204) 407-839-3626 (Ext 216)

ROCHELLE HOLDINGS II, LLC (TAVARES)

TABLE OF CONTENTS

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 i

Table of Contents

Table of Contents .................................................................................................................................................................................. i

Summary of Salient Facts and Conclusions ............................................................................................................................... 1

Introduction ............................................................................................................................................................................................ 2

Neighborhood Description .............................................................................................................................................................. 6

Site Description .................................................................................................................................................................................. 14

Assessment & Tax Data .................................................................................................................................................................. 34

Highest & Best Use ........................................................................................................................................................................... 35

Appraisal Methodology & Land Valuation.............................................................................................................................. 37

General Assumptions & Limiting Conditions ......................................................................................................................... 46

Certification.......................................................................................................................................................................................... 51

Addenda ................................................................................................................................................................................................ 53

ROCHELLE HOLDINGS II, LLC (TAVARES)

SUMMARY OF SALIENT FACTS AND CONCLUSIONS

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 1

Summary of Salient Facts and Conclusions

Location: South side of Lane Park Cutoff, east of US Highway 19, in the municipality of

Tavares, Lake County, Florida 32778.

Current Owner: Rochelle Holdings II, LLC

Parcel ID #s: 05-20-26-0201-000-37700 and 06-20-26-0004-000-05700

Land Area/Property Type: The subject property consists of 9.54 gross acres of vacant land. We estimate

approximately 5.50 acres are net developable.

Improvements: The site is vacant with no improvements of contributory value.

Future Land Use/

Zoning: FLU: MED (Medium Density Residential –up to 12 dwelling units per acre

Zoning: PD (expired Lake Idamere Townhomes, previously proposed as a 70 unit

subdivision.)

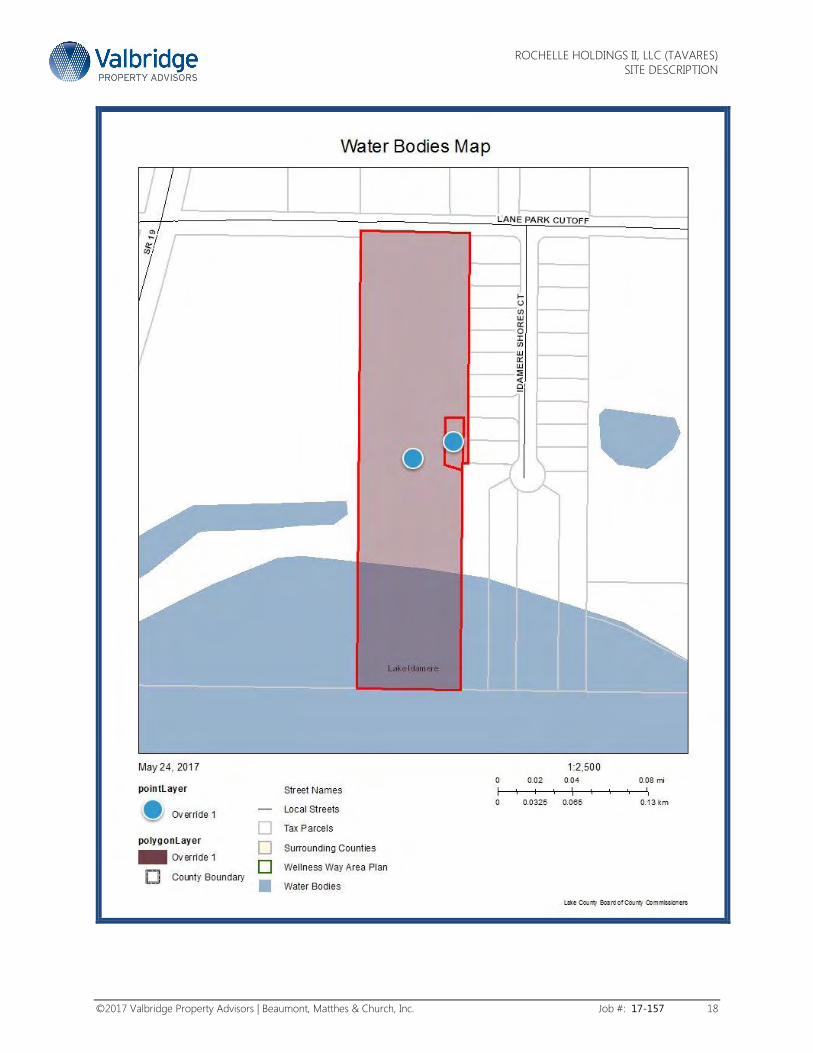

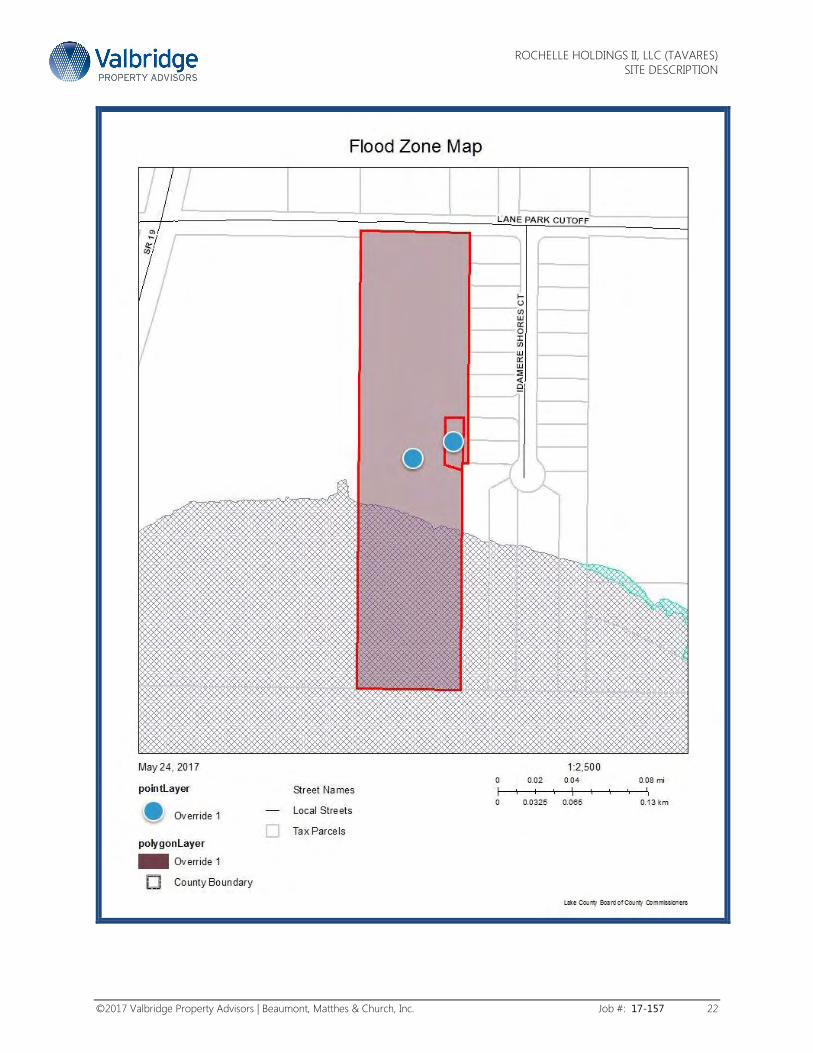

Flood Zone: The developable area of the site is entirely within Flood Zone “X” - “areas

determined to be outside the 0.2% annual chance floodplain.”

Highest and

Best Use (as vacant): Future development of approximately 66 multifamily units.

Property Rights

Appraised: Fee simple interest

Date of Inspection: May 20, 2017

Date of Report: May 26, 2017

Opinion of Value: $460,000 (Prospective)

Estimated Marketing

Period: As-Is - 12 months

Comments: This appraisal is subject to the “Assumptions and Limiting Conditions” which are

considered usual for this type of assignment.

Per the client’s request, the date of value of this appraisal is May 31, 2017. The date of our

inspection was May 20, 2017. Therefore, the opinion of value contained herein is a Prospective

Value. This report is subject to the Extraordinary Assumption that there will be no substantive

changes to the legal, physical or economic issues pertaining to the subject property between the

date of our inspection and the date of value.

This appraisal is subject to a study reflecting no gopher tortoise issues on the subject property, an

Extraordinary Assumption.

ROCHELLE HOLDINGS II, LLC (TAVARES)

INTRODUCTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 2

Introduction

Location The subject property is located along the south side of Lane Park Cutoff, east of US Highway 19, in the

municipality of Tavares, Lake County, Florida 32778. The site is located within 2010 Census Tract Number

310. The subject property is vacant unimproved land with no improvements of contributory value.

Client, Intended Use and Users of the Appraisal The client in this assignment is Fairwinds Credit Union. This appraisal report was prepared for the

intended use and benefit of Fairwinds Credit Union. The intended use of this report is in making decisions

regarding the disposal of the obligation secured by the property. There are no other intended uses

and/or users of this report. The appraisers are not responsible for unauthorized use of this report.

Real Estate Identification The property consists of two (2) entire tax parcels - 05-20-26-0201-000-37700 and 06-20-26-0004-000-

05700.

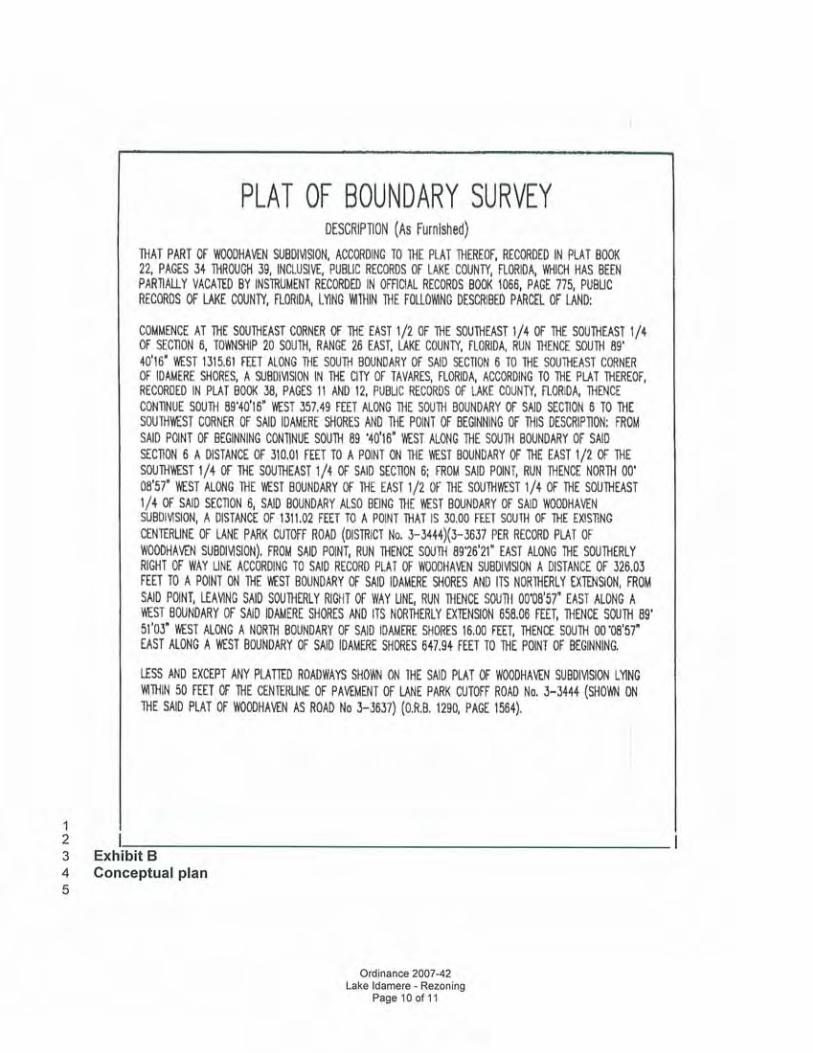

Legal Description The legal description per the accompanying survey, last deed of conveyance and title policy is as follows:

ROCHELLE HOLDINGS II, LLC (TAVARES)

INTRODUCTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 3

Real Property Interest Appraised We have appraised the fee simple estate interest in the subject property.

Types of Value We have developed an opinion of the following types of value for the subject property.

VALUATION SCENARIOS

Prospective, as of May 31, 2017

Definition of Market Value Market value is defined as:

The most probable price that a property should bring in a competitive and open market under all

conditions requisite to a fair sale, the buyer and seller each acting prudently and knowledgeably, and

assuming the price is not affected by undue stimulus. Implicit in this definition is the consummation of a

sale as of a specified date and the passing of title from seller to buyer under conditions whereby:

Buyer and seller are typically motivated;

Both parties are well informed or well advised, and acting in what they

consider their own best interests;

A reasonable time is allowed for exposure in the open market;

Payment is made in terms of cash in U.S. dollars or in terms of financial

arrangements comparable thereto; and

The price represents the normal consideration for the property sold

unaffected by special or creative financing or sales concessions granted by

anyone associated with the sale.

(Source: Interagency Appraisal and Evaluation Guidelines, December 10, 2010, Federal Register, Volume 75 Number 237, Page 77472).

Effective Date of Value The effective date of value is May 31, 2017. The date the date of inspection was May 20, 2017.

Date of Report The date of this report is May 26, 2017, the date of the letter of transmittal.

Scope of Work The scope of work for this original report includes 1) the extent to which the subject property is identified,

2) the extent to which the subject property is inspected, 3) the type and extent of data researched, 4) the

type and extent of analysis applied, and the type of appraisal report prepared. These items are discussed

as follows:

Extent to Which the Property Is Identified

Legal Characteristics - The subject was identified by the client by tax parcel numbers. The client also

provided the zoning radiance for the subject property and a previously proposed conceptual plan.

Future Land Use, Zoning and similar data was provided by City of Tavares personnel and website.

ROCHELLE HOLDINGS II, LLC (TAVARES)

INTRODUCTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 4

Physical Characteristics - Resources include physical inspection, survey/conceptual plans, various public

sources and maps (tax, aerial. topo, flood, wetlands) and a variety of other private sources. Many of these

maps, photographs etc. are provided herein.

Economic Characteristics - Economic and neighborhood data and characteristics are based on

observation, demographics, review of other sources inducing but not limited to Residential Market

Reports and others as presented and referred. Market data is cultivated from various sources, including

market participants, data sources such as CoStar COMPS, MLS, Lake County Property Appraiser’s website,

Residential Market Reports, appraisers’ files, interviews with market participants and public records, as

well as a comparison to properties with similar locational and physical characteristics.

Extent to Which the Property Is Inspected

We inspected the subject on May 31, 2017. The extent of the inspection was limited observing the subject

property from the adjacent right-of-way along the north side of the subject property with various maps in

hand. Due to the overgrown nature of the vegetation, we were unable to inspect the interior of the site.

We also inspected the subject property from the southerly terminus of a public road in the adjacent

subdivision to the east of the subject.

Type and Extent of the Data Researched

We researched and analyzed: 1) market area data, 2) property-specific, market-analysis data, 3) zoning

and land-use data, and 4) current market data on comparable listings and sales in the competitive or

similar market area(s).

Type and Extent of Analysis Applied

We observed surrounding land use trends, condition of neighborhood improvements, demand for the

subject property, and relative legal limitations in concluding a highest and best use. We then developed

an as-is opinion of the market value on the highest and best use conclusion, relying on the Sales

Comparison Approach. The Cost and Income Approaches were not utilized since they are not generally

applicable to vacant land.

Type of Appraisal and Report Option

This is an Appraisal Report as defined by Uniform Standards of Professional Appraisal Practice under

Standards Rule 2-2(a).

Competency Provision Each of the appraisers has provided valuation and consultation services on numerous types of vacant

lands and developments in the Central Florida market over the past 30+ years. Therefore, the appraisers

have adequate knowledge and experience in accepting and completing this assignment. The reader is

referred to the appraisers’ qualifications for additional evidence of this competency.

Use Of Real Estate As Of The Effective Date Of Value The subject property was not put to any economic use as of the date of valuation.

Ownership and Sales History According to the records researched, the subject property has been owned by Rochelle Holdings II, LLC

since 2006. To the best of our knowledge the subject property has not been marketed for sale in the past

three years.

ROCHELLE HOLDINGS II, LLC (TAVARES)

INTRODUCTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 5

Extraordinary Assumptions An extraordinary assumption, as defined by the Uniform Standards of Professional Appraisal Practice is

“an assumption, directly related to a specific assignment, which, if found to be false could alter the

appraisers’ opinions or conclusions. Extraordinary assumptions presume as fact otherwise uncertain

information about physical, legal or economic characteristics of the subject property; or about conditions

external to the subject property, such as market conditions or trends or about the integrity of the data

used in the analysis.”

Per the client’s request, the date of value of this appraisal is May 31, 2017. The date of our

inspection was May 20, 2017. Therefore, the opinion of value contained herein is a Prospective

Value. This report is subject to the Extraordinary Assumption that there will be no substantive

changes to the legal, physical or economic issues pertaining to the subject property between the

date of our inspection and the date of value.

This appraisal is subject to a study reflecting no gopher tortoise issues on the subject property, an

Extraordinary Assumption.

This appraisal is not subject to any other Extraordinary Assumptions.

Hypothetical Conditions A hypothetical condition is defined by the Uniform Standards of Professional Appraisal Practice as “that

which is contrary to what exists, but is supposed for the purpose of analysis. Hypothetical conditions

assume conditions contrary to known facts about physical, legal, or economic characteristics of the

subject property; or about conditions external to the property, such as market conditions or trends; or

about the integrity of data used in an analysis.”

This appraisal is not subject to any Hypothetical Conditions.

ROCHELLE HOLDINGS II, LLC (TAVARES)

NEIGHBORHOOD DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 6

Neighborhood Description

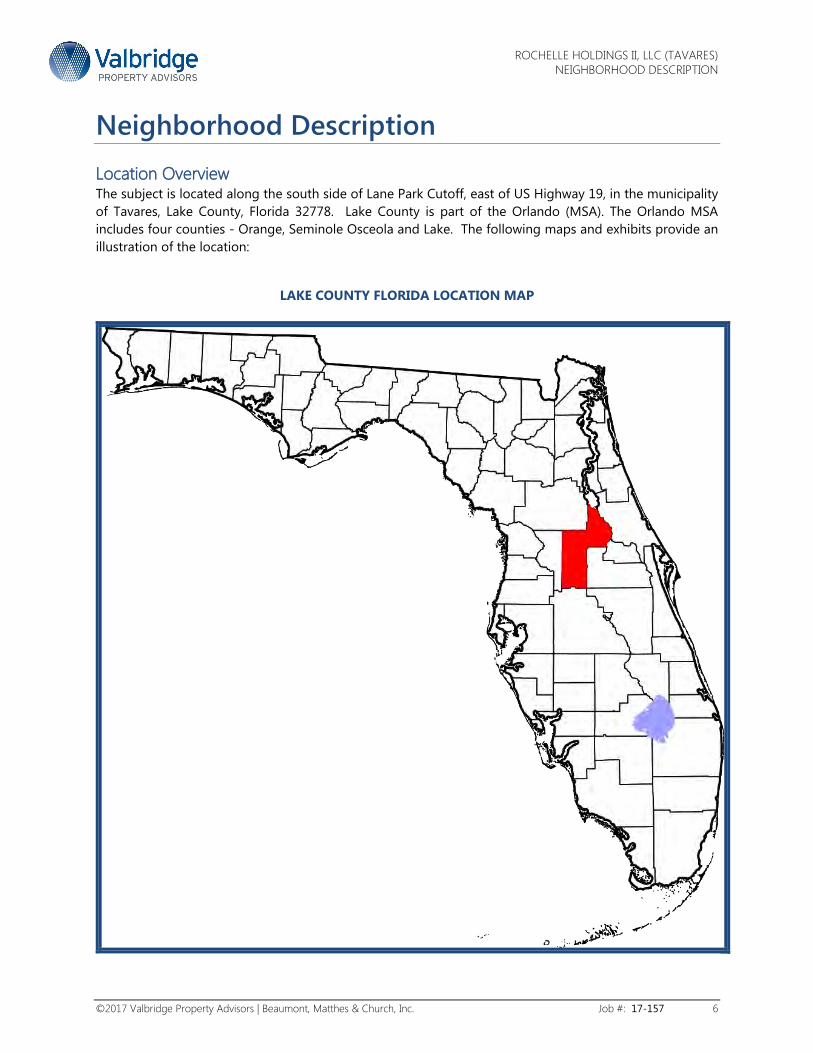

Location Overview The subject is located along the south side of Lane Park Cutoff, east of US Highway 19, in the municipality

of Tavares, Lake County, Florida 32778. Lake County is part of the Orlando (MSA). The Orlando MSA

includes four counties - Orange, Seminole Osceola and Lake. The following maps and exhibits provide an

illustration of the location:

LAKE COUNTY FLORIDA LOCATION MAP

ROCHELLE HOLDINGS II, LLC (TAVARES)

NEIGHBORHOOD DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 7

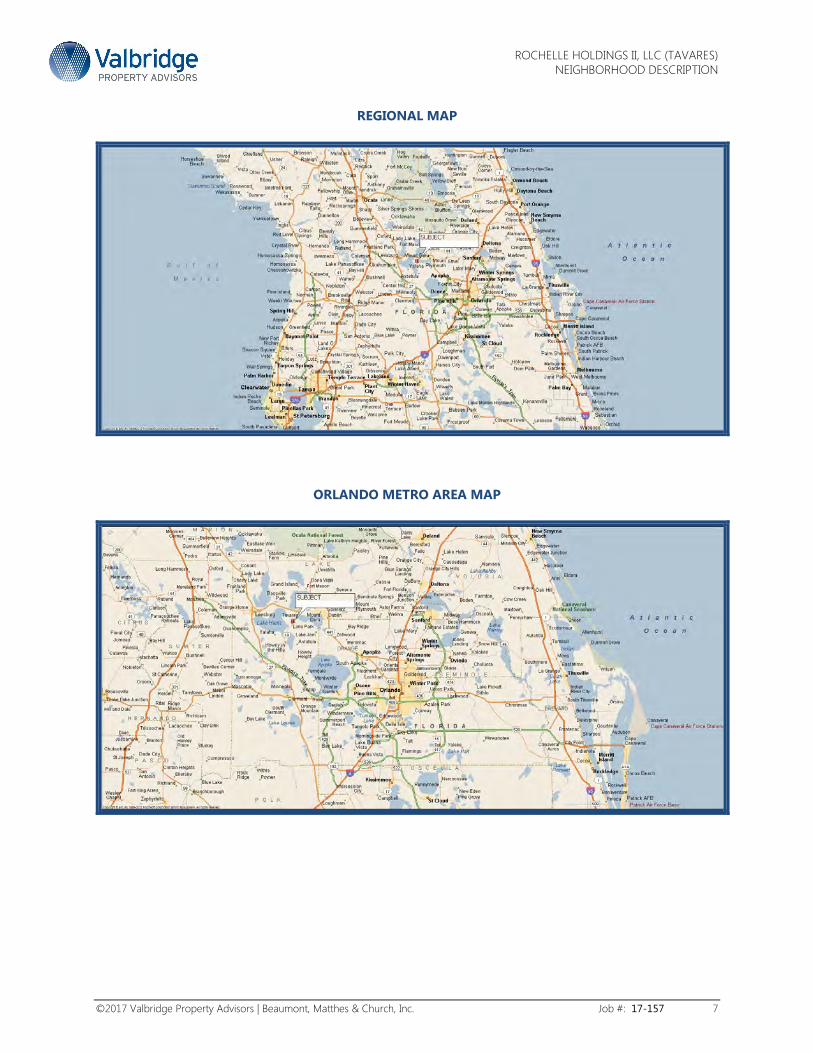

REGIONAL MAP

ORLANDO METRO AREA MAP

ROCHELLE HOLDINGS II, LLC (TAVARES)

NEIGHBORHOOD DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 8

LAKE COUNTY MAP

ROCHELLE HOLDINGS II, LLC (TAVARES)

NEIGHBORHOOD DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 9

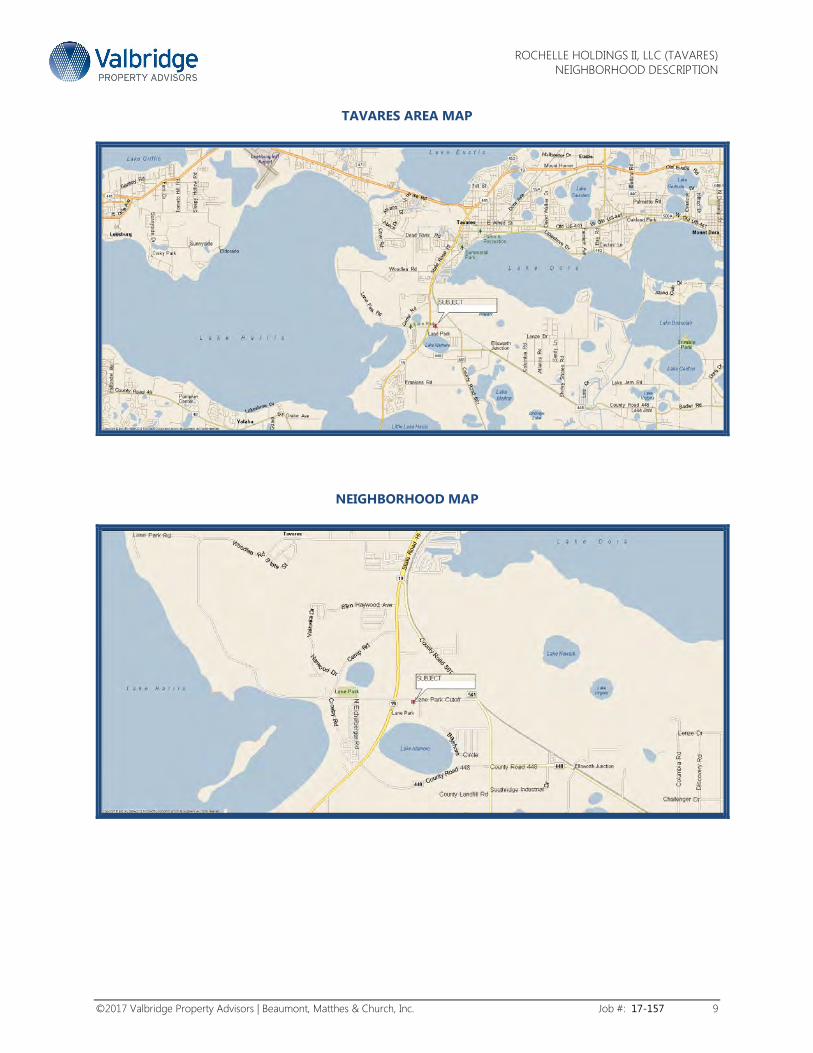

TAVARES AREA MAP

NEIGHBORHOOD MAP

ROCHELLE HOLDINGS II, LLC (TAVARES)

NEIGHBORHOOD DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 10

Neighborhood Description The subject property is located along the south side of Lane Park Cutoff, east of US Highway 19, in the

municipality of Tavares, Lake County, Florida 32778. This places the subject property on the north shore

of Lake Idamere.

Tavares is within Central Lake County approximately 25 driving miles northwest of the Orlando Central

Business District (CBD) via the fastest route and is the seat of Lake County government. 5

Lake County - In the 1980’s Lake County was the last of the four counties to be included in the Orlando

MSA, which also includes Orange Seminole and Osceola counties. It is the north-westerly-most of the

four counties. Lake County has evolved from a primarily agricultural/citrus area to a suburban/commuter

area with a large and growing retiree population as well as commuters to the regional employment

centers which are primarily in the other three counties. In the most recent decade was among the fastest

growing counties in Central Florida. The growth occurred primarily in the Clermont area and to a lesser

degree in the Leesburg/Mt. Dora/Tavares area - generally those locations with a good road network to

Orlando. It ranks third in total population of the four counties and still retains considerable agricultural

activities and pursuits.

Tavares – The municipality of Tavares is located north of Clermont, east of Leesburg, west of Mt. Dora

and south of Eustis. The Tavares Seaplane Base is a city-owned, public-use facility located on Lake Dora.

The base is popular and gives rise to the city's nickname, "America's Seaplane City".

Tavares is the county seat of Lake County. Although not the largest city in the county, it is home to the

usual county seat government offices, as well as various city offices. Along with Eustis, Leesburg and Mt.

Dora, this part of the county has experienced significant growth over the past two decades. And although

growth is partly a result of the expanding urbanized Orlando area, much of the growth is a result of

relocating northern retirees. Tavares’s population is rapidly increasing (from approximately 9,700 in 200,

to 13,951 in 2010 to an estimated 15,430 in 2015. The median age is approximately 56 years.

Consequently, there has also been a burgeoning medical community in the area. We note that the

developed area of this part of Lake County is generally along the US Highway 441 corridor. This corridor

provides most of the retail commercial needs and services to the growth area.

A neighborhood is defined in terms of common characteristics, trends, and groupings of similar or

complementary land uses. The subject property is in the southwest quadrant of Tavares. The

neighborhood/corridor may be considered the SR 19 corridor south and west of CR 561 and north of the

bridge between Lake Harris and Little Lake Harris. Much of this area is vacant land (former citrus groves,

with some relatively recent single family residential development occurring. There is also a county landfill

in the area off CR 561. SR 19 also includes some commercial development particularly north of Lane Park

Cutoff. Lane Park Cutoff consists primarily of vacant land. Development includes a manufactured housing

subdivision, Lake County Technical College, Institute of Public Safety, a fire station, the Big House, a

community center and sports training facility. The area along CR 561, including the easterly end of Lane

Park Cutoff is industrially oriented.

Demographic data for one, three and five mile rings around the subject is provided in the Exhibit section

of this appraisal report. The most pertinent data is the one mile radius. The data reflects an older

population of very modest means. Growth is not projected to be rapid. Due to the recent growth of the

area and the relatively sparse existing residential development, we do not consider the demographics to

provide much insight into the character of the neighborhood.

ROCHELLE HOLDINGS II, LLC (TAVARES)

NEIGHBORHOOD DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 11

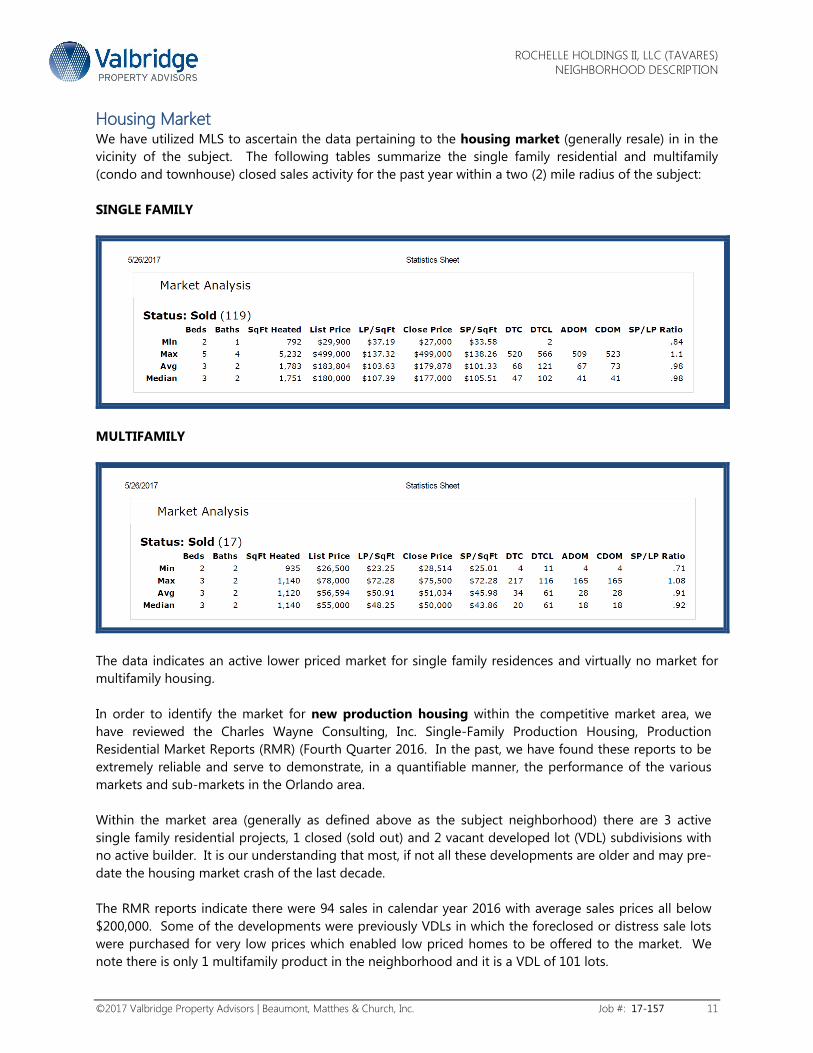

Housing Market We have utilized MLS to ascertain the data pertaining to the housing market (generally resale) in in the

vicinity of the subject. The following tables summarize the single family residential and multifamily

(condo and townhouse) closed sales activity for the past year within a two (2) mile radius of the subject:

SINGLE FAMILY

MULTIFAMILY

The data indicates an active lower priced market for single family residences and virtually no market for

multifamily housing.

In order to identify the market for new production housing within the competitive market area, we

have reviewed the Charles Wayne Consulting, Inc. Single-Family Production Housing, Production

Residential Market Reports (RMR) (Fourth Quarter 2016. In the past, we have found these reports to be

extremely reliable and serve to demonstrate, in a quantifiable manner, the performance of the various

markets and sub-markets in the Orlando area.

Within the market area (generally as defined above as the subject neighborhood) there are 3 active

single family residential projects, 1 closed (sold out) and 2 vacant developed lot (VDL) subdivisions with

no active builder. It is our understanding that most, if not all these developments are older and may pre-

date the housing market crash of the last decade.

The RMR reports indicate there were 94 sales in calendar year 2016 with average sales prices all below

$200,000. Some of the developments were previously VDLs in which the foreclosed or distress sale lots

were purchased for very low prices which enabled low priced homes to be offered to the market. We

note there is only 1 multifamily product in the neighborhood and it is a VDL of 101 lots.

ROCHELLE HOLDINGS II, LLC (TAVARES)

NEIGHBORHOOD DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 12

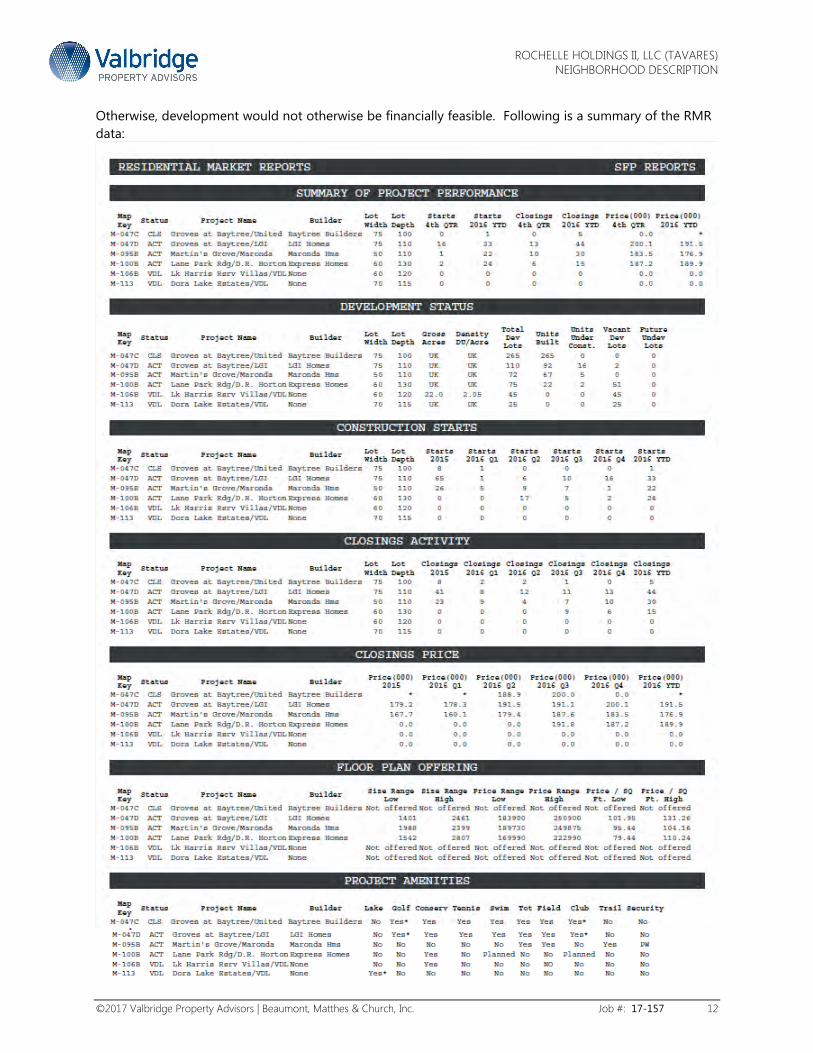

Otherwise, development would not otherwise be financially feasible. Following is a summary of the RMR

data:

ROCHELLE HOLDINGS II, LLC (TAVARES)

NEIGHBORHOOD DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 13

The market data indicates that there is active market for low/entry priced single family residences in the

market. The data also indicates no discernable market for multifamily for-sale housing. Owing to the

lack of a nearby definable or active growing employment center, we do not anticipate rental apartment

feasibility.

We are aware of several recent sales of land with subdivision infrastructure in place for single family

housing. These sales were for less than $30,000 per lot. Based on our knowledge of development costs,

we note these sales are for less than the cost of development. We also note new housing on those lots

and those in the vicinity of the subject reflect prices that are nominally higher than the existing housing.

We conclude that development, either for single family residences of multifamily is not currently

financially feasible.

Summary - The subject neighborhood is in transition from a slightly outlying, in the path of growth,

formerly agricultural area to suburban density single family residential housing with neighborhood and

community commercial support facilities. The housing market in the neighborhood is for low/entry priced

single family residences. However, development is not currently financially feasible. With the growth of

the area and region and likely absorption of the excess VDL inventory, we anticipate future development

to be feasible in, say, five (5) years.

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 14

Site Description

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 15

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 16

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 17

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 18

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 19

SOILS KEY

8 9 17 38 39 45 99

Candler sand,

0 to 5 percent

slopes

Candler sand,

5 TO 12

percent

slopes

Arents Placid sand,

frequently

ponded, 0 to

2 percent

slopes

Seffner sand Tavares sand,

0 to 5 percent

slopes

Water

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 20

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 21

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 22

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 23

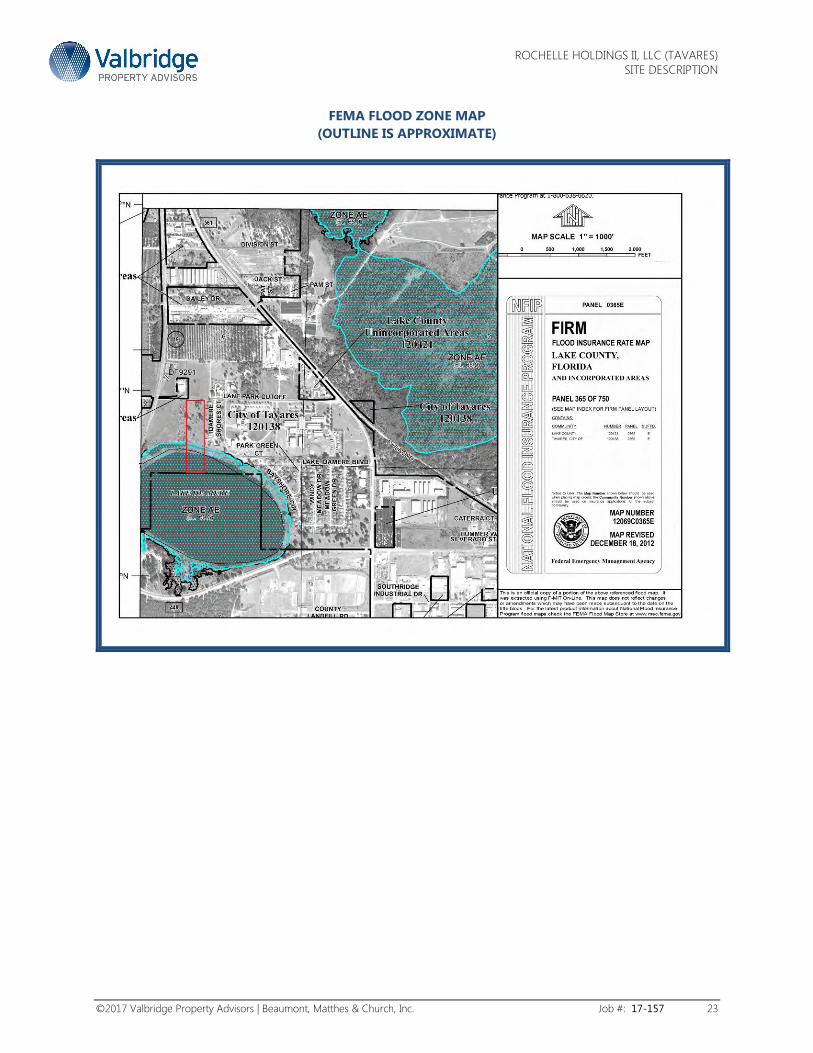

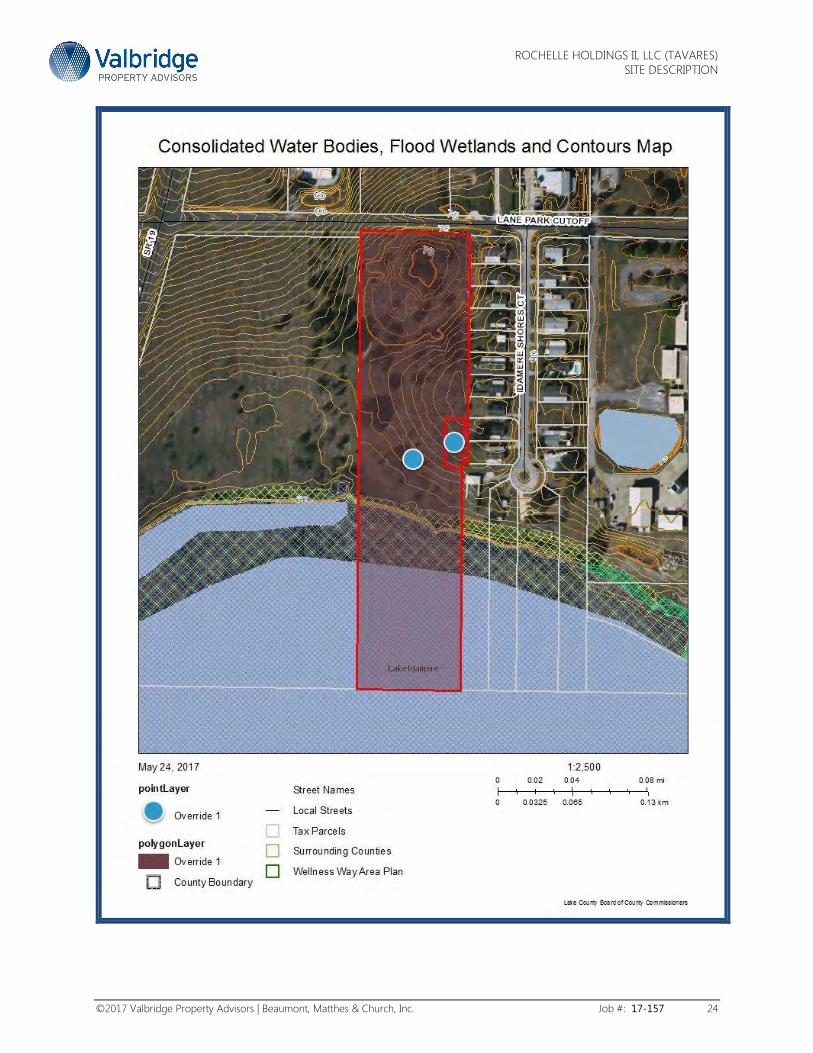

FEMA FLOOD ZONE MAP

(OUTLINE IS APPROXIMATE)

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 24

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 25

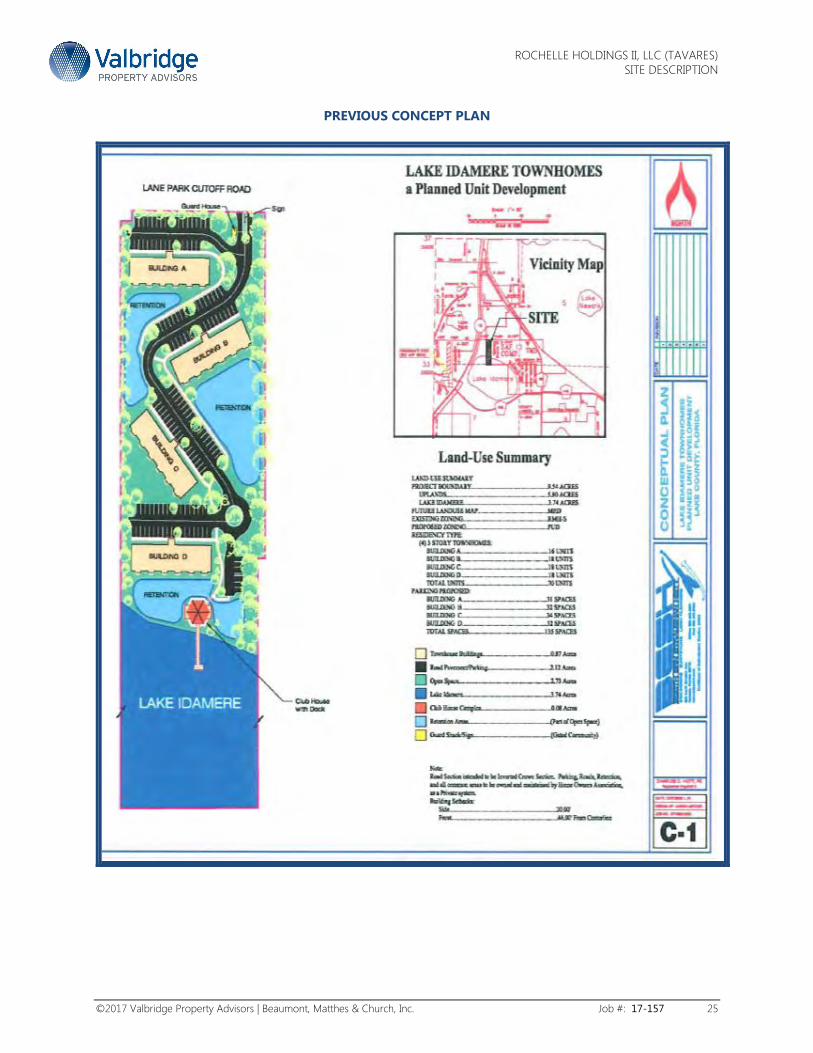

PREVIOUS CONCEPT PLAN

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 26

SUBJECT PHOTOGRAPHS

View west along Lane Park Cutoff from vicinity of northwest corner of subject

(subject not visible)

View east along Lane Park Cutoff from vicinity of northwest corner of subject

(subject on right)

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 27

View south along subject’s west property line from vicinity of northwest corner of subject

(subject on left)

View of subject property frontage easterly from vicinity of northwest corner of subject

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 28

View east along Lane Park Cutoff from vicinity of northeast corner of subject

(subject not visible)

View west along Lane Park Cutoff from vicinity of northeast corner of subject

(subject on left)

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 29

View south along subject’s west property line from vicinity of northeast corner of subject

(subject on right)

View of subject property frontage westerly from vicinity of northeast corner of subject

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 30

General Data Location: The subject property is located along the south side of Lane Park

Cutoff, east of US Highway 19, in the municipality of Tavares,

Lake County, Florida 32778.

Current Owner: Rochelle Holdings II, LLC

Parcel ID #: 05-20-26-0201-000-37700 and 06-20-26-0004-000-05700

Gross Land Area 9.54 acres per survey

Overall Configuration Slightly irregular/Mostly rectangular

Approximate Overall Dimensions Frontage (north) – 326’

Depth (west) – 1,311.02

Access Lane Park Cutoff, a two-lane paved, undivided local road; no medians

Wetlands Wetlands and water bodies cover the southerly 40%+ of the site;

See maps

Contours/Topography The highest elevations are approximately 80’ above mean sea level at

the northwest corner of the site. The lowest elevation is

approximately 70’ at or adjacent to the shore of Lake Idamere and

the adjacent wetlands. See maps.

Soils See map and narrative

Flood Per FEMA Map 12069C0365E, revised December 18, 2012 (and the

Lake County GIS maps), most of the site is within unshaded Flood

Zone “X” (areas determined to be outside the 0.02% annual chance

floodplain”). The southerly extreme of the site (within and adjacent

to Lake Idamere) is within Flood Zone “AE” - (Special Flood Hazard

Areas (SFHAs) subject to Inundation by the 1% Annual Chance Flood

–Base Flood Elevations determined” (100 year floodplain) – See

maps (the base flood elevation is 69.3’ at or near that area indicated

as a water body on the accompanying map.)

Utilities (City of Tavares) Potable Water - 12” line along south side of Lane Park Cutoff

Sewer - 6” force main along south side of Lane Park Cutoff (will

require lift station)

Drainage Must be provided on-site;

Hazardous or Toxic Materials See narrative

Other Environmental Considerations See narrative – See Extraordinary Assumptions

Easements/Encumbrances See narrative

Improvements None noted

Estimated Upland Area 5.5 acres

NOTE: The survey has the following comment:

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 31

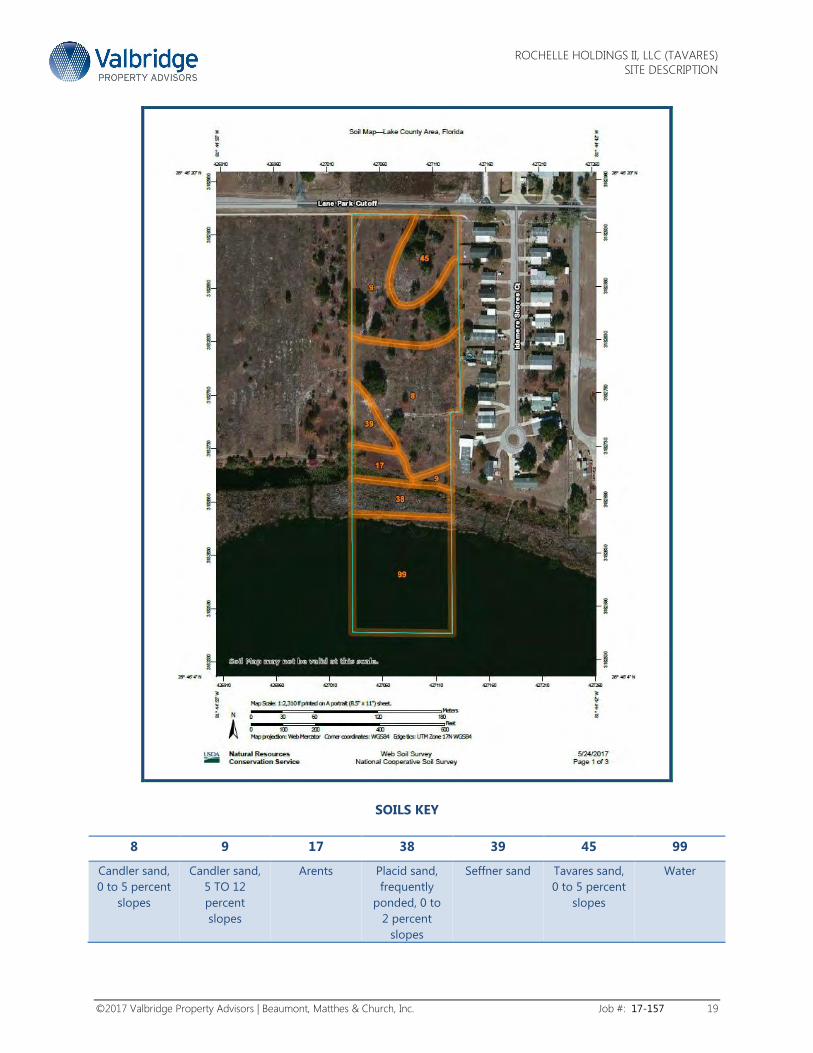

Other Site Conditions Soils: Soil maps for the subject property indicate a variety of soils. The

upland soils are situated in the northern portion of the site while

the hydric soils are situated to the south and north of Lake

Idamere. The reader is referred to Item 20 of the “General

Assumptions and Limiting Conditions.” Where applicable, an

inspection of the site and indicates no unusual soil or subsoil

conditions, which would result in reduced load-bearing capacity,

atypical drainage conditions, or other conditions which would

result in excessive site preparation costs. However, we assume

no responsibility for hidden or unapparent conditions beyond

the area of our expertise as appraisers.

Environmental Issues: The appraisers are not experts in determining the presence or

absence of hazardous or toxic substances, defined as all

hazardous or toxic materials, waste, pollutants or contaminants,

including but not limited to asbestos, PCB, UFFI,

perchloroethylene, or other raw material or chemicals used in

construction or otherwise present on the property. The

appraisers are not experts in determining the presence or

absence of endangered or protected species.

We have checked available resources to ascertain the likelihood

of the presence of selected endangered or protected species in

the vicinity of the subject property. This includes, but is limited

to eagle nests, sand skinks and gopher tortoises.

The Florida Fish and Wildlife Commission map indicates no active

eagle nests within the regulated distance from the subject

property. The subject property does not meet the geographical

criteria for the presence of sand skinks; however, due to the

vagaries of scale, this may be subject to interpretation.

According to the on-line Web Soil Survey provided by the USDA,

Natural Resources Conservation Services, the soil found on the

site ranges from “unrated” to “highly unsuitable” as gopher

tortoise habitat. The “highly suitable” rating and “less suitable”

soils are non-hydric and found in the northerly portion of the

site, and are the most suitable for development.

This is not a comprehensive investigation and we

recommend retaining competent specialized professionals to

ascertain the possible presence of environmental issues

including but not limited to endangered or protected species

and impacts on development.

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 32

Soils and Sub-Soils – A summary description of the soil types

may be found in the Addenda. We assume no responsibility for

hidden or unapparent conditions beyond the area of our

expertise as appraisers (see “Assumptions and Limiting

Conditions”.)

This appraisal is subject to a study reflecting no gopher

tortoise issues on the subject property, an Extraordinary

Assumption.

We also recommend retaining competent specialized

professionals to ascertain the site’s surface and soil

conditions and impacts on development.

Easements and Encumbrances: The title policy provided to us did not indicate the presence of

any easements or encumbrances which would impact the utility

subject property.

Site Improvements Off-Site Improvements: Sidewalk on the south side of Lane Park Cutoff

On-Site Improvements: None

Building Improvements None

ROCHELLE HOLDINGS II, LLC (TAVARES)

SITE DESCRIPTION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 33

Future Land Use/Zoning The subject property is located in the municipality of Tavares. In 2007 the City has designated the Future

Land Use (FLU) of the subject property as MED - Medium Density Residential, which allows up to 12 units

per acre.

The highest intensity permissible zonings in the MED FLU include RMF-2 and RMF-3. Permissible uses in

these zoning districts include citrus groves, single family dwelling, two-family dwelling, duplexes,

townhomes, multifamily dwellings (3 or more attached dwelling units), guest apartments , boarding and

rooming houses, group home/community residential home (max. of 6 residents), adult activity center,

private docks and boathouses, child care centers, and home owners association/park business office.

Some of these uses have restrictions.

Concurrent with the designation, the City re-zoned the property to PD - Planned Development. A copy of

the rezoning ordinance may be found in the Addenda of this report. The ordinance details the allowable

use of 70 units (adult-age restricted) based on 5.9 acres at 12 units per upland acre as well as various

development standards including setbacks, impervious surface area, building height, etc.

Per Mike Fitzgerald, Development Coordinator at the City of Tavares, the PD has expired. He informed us

that it would be likely to be well received by the City if the PD were re-instituted, which would entail

meeting the updated development codes. This could include both single and multifamily residential uses

at densities not to exceed 12 units per upland acre. The accompanying is a concept plan provided to the

City for consideration with the PD zoning application.

Based on our estimate of 5.5 upland acres, the maximum number that could be developed on the

subject property is 66 units.

Concurrency and Impact Fees Concurrency issues are evaluated at the time of development submittals.

ROCHELLE HOLDINGS II, LLC (TAVARES)

NEW HOUSING MARKET DATA

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 34

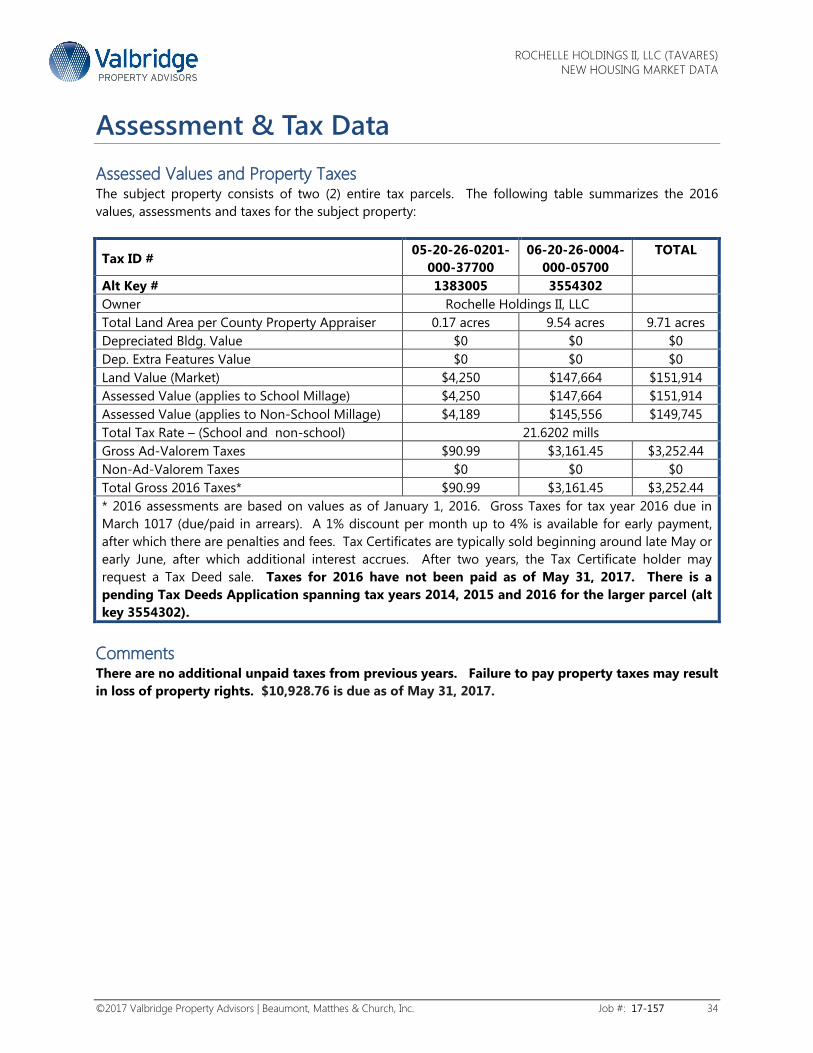

Assessment & Tax Data

Assessed Values and Property Taxes The subject property consists of two (2) entire tax parcels. The following table summarizes the 2016

values, assessments and taxes for the subject property:

Tax ID # 05-20-26-0201-

000-37700

06-20-26-0004-

000-05700

TOTAL

Alt Key # 1383005 3554302

Owner Rochelle Holdings II, LLC

Total Land Area per County Property Appraiser 0.17 acres 9.54 acres 9.71 acres

Depreciated Bldg. Value $0 $0 $0

Dep. Extra Features Value $0 $0 $0

Land Value (Market) $4,250 $147,664 $151,914

Assessed Value (applies to School Millage) $4,250 $147,664 $151,914

Assessed Value (applies to Non-School Millage) $4,189 $145,556 $149,745

Total Tax Rate – (School and non-school) 21.6202 mills

Gross Ad-Valorem Taxes $90.99 $3,161.45 $3,252.44

Non-Ad-Valorem Taxes $0 $0 $0

Total Gross 2016 Taxes* $90.99 $3,161.45 $3,252.44

* 2016 assessments are based on values as of January 1, 2016. Gross Taxes for tax year 2016 due in

March 1017 (due/paid in arrears). A 1% discount per month up to 4% is available for early payment,

after which there are penalties and fees. Tax Certificates are typically sold beginning around late May or

early June, after which additional interest accrues. After two years, the Tax Certificate holder may

request a Tax Deed sale. Taxes for 2016 have not been paid as of May 31, 2017. There is a

pending Tax Deeds Application spanning tax years 2014, 2015 and 2016 for the larger parcel (alt

key 3554302).

Comments There are no additional unpaid taxes from previous years. Failure to pay property taxes may result

in loss of property rights. $10,928.76 is due as of May 31, 2017.

ROCHELLE HOLDINGS II, LLC (TAVARES)

HIGHEST AND BEST USE

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 35

Highest & Best Use

Highest and best use may be defined as that reasonable and probable use that supports the highest

present value as of the date of appraisal. The estimate of highest and best use is determined from a

group of alternative potential uses. The highest and best use is legally permissible, physically possible,

financially feasible and maximally productive.

The highest and best use analysis first determines the highest and best use of the subject as though

vacant. This analysis results in the conclusion of what would be the "ideal" improvement to the subject

land. The existing improvements, if any, are then compared to this "ideal" improvement in order to

conclude the highest and best use as improved. The subject consists of vacant, unimproved land.

Therefore, an analysis of the highest and best use as vacant is applicable.

Highest and Best Use As Vacant Based on a review of the legally permissible, physically possible, financially feasible and maximally

productive uses, and the date provided in this report, the highest and best use of the subject property is

for speculative holding for future, multifamily development of approximately 66 units.

Highest and Best Use As Improved Not applicable

Most Probable Buyer/User As of the date of value, the potential buyer of the subject property (in its entirety) is most likely to be

speculator or developer builder of multifamily product.

Exposure and Marketing Periods Exposure time is the estimated length of time the property interest being appraised would have been

offered on the market prior to the hypothetical consummation of a sale at market value on the effective

date of appraisal; a retrospective opinion based on an analysis of past events assuming a competitive and

open market. Exposure time is always presumed to occur prior to the effective date of the appraisal.

The reasonable marketing time is an opinion of the amount of time it might take to sell a real property

interest at the concluded market value level during the period immediately after the effective date of an

appraisal.

The subject property is located in an area that has longer, but relatively short term opportunities for

development. This bodes well for speculative investment.

Based on statistical information about days on market, escrow length, and marketing times gathered

through national investor surveys, sales verification, and interviews of market participants, exposure time

was estimated at 12 months at the value reported herein. Marketing time is also projected at 12 months

to account for what we see as increasing risk to commercial real estate values because of the Fed’s

repeated insistence they intend to increase interest rates in the near future. We estimate a substantial

portion of commercial real estate value appreciation over the past two years is due directly to lower

interest rates and the “search for yield” as sovereign bond rates decline and/or dip into negative territory.

ROCHELLE HOLDINGS II, LLC (TAVARES)

HIGHEST AND BEST USE

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 36

As is demonstrated by the bond market each time higher interest rates are mentioned, there is an often

violent drop in bond values due to their greater liquidity. Due to the real estate market’s much lower

liquidity level, such periodic “mood swings” are not as evident, but the sentiment is clear; increasing

interest rates will ultimately result in a decline in the underlying asset value of any investment. Since

interest rates can barely go any lower, it is possible the real estate market is in the terminal stage of an

uptrend caused by declining interest rates. Thus, values may begin to trend lower over the coming years.

ROCHELLE HOLDINGS II, LLC (TAVARES)

APPRAISAL METHODOLOGY & LAND VALUATION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 37

Appraisal Methodology & Land Valuation

Three Approaches to Value There are three traditional approaches normally employed by appraisers in the development of an

opinion of market value. These three approaches analyze data from three market perspectives. The

approaches are the Cost Approach, the Income Approach and the Sales Comparison Approach.

The subject property consists of vacant land, the highest and best use of which is for imminent

development of approximately 91 single family residential lots. The Sales Comparison Approach is the

only applicable approach for land such as the subject property, which effectively has no current income or

approved development plan.

The Sales Comparison Approach is the process for comparing prices paid for properties having a

satisfactory degree of similarity to the subject property, adjusted for differences in time, location and

physical characteristics. This approach is based upon the principle of substitution, which implies that a

prudent purchaser would not pay more to buy a property than it would cost to buy a comparable

substitute property in a similar location.

Methodology An opinion of the value of vacant land is most often developed using the Sales Comparison Approach.

This approach is based on the premise that a buyer would pay no more for a specific property than the

cost of obtaining a property with the same utility. In the sales comparison approach, the opinion of

market value is based on sales of properties having a highest and best use similar to that of the subject

property. The highest and best use of the subject property is speculation for future development of

approximately 66 multifamily units.

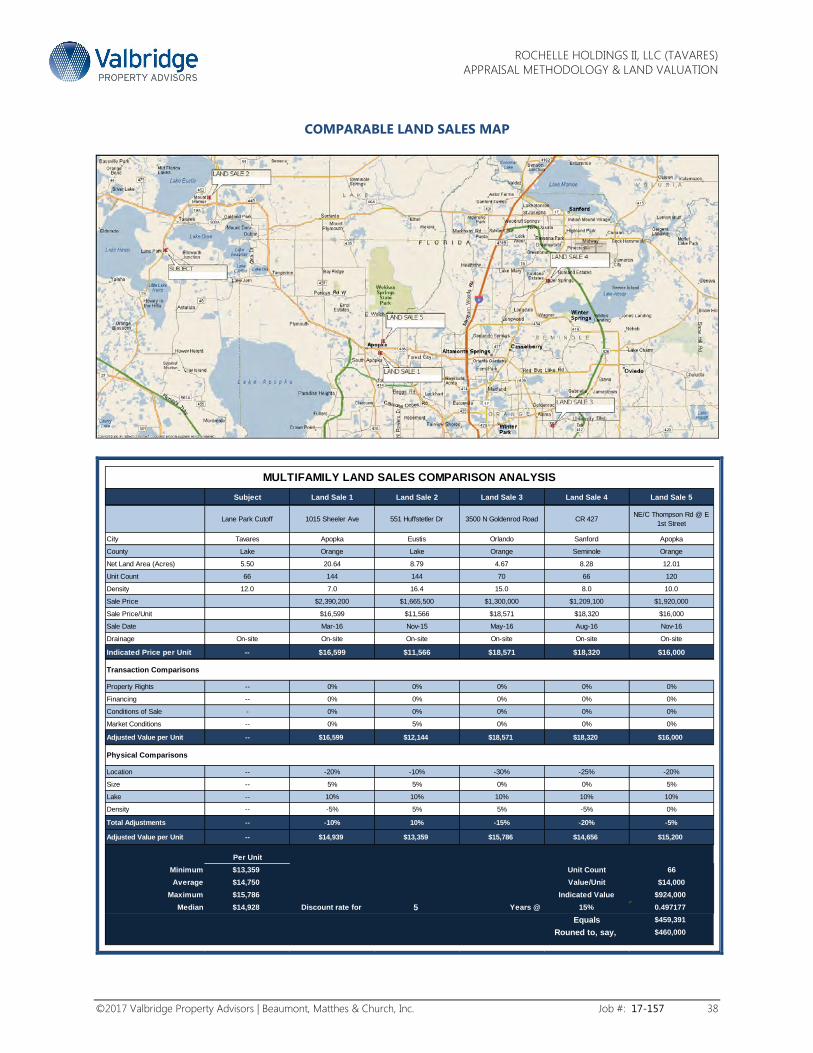

Land Valuation Analysis We searched for recent sales having a similar highest and best use in and around the subject

neighborhood and other similar areas of the region, including, Orange, Seminole, Osceola and Lake

Counties.

The comparable sales are geographically identified and summarized on the accompanying map and chart

on the following pages. Each comparable is written up in detail, followed by a brief narrative discussion of

the comparables as they relate to the subject in developing our final opinion of value.

We have analyzed the sales on the basis of price per proposed unit, a common unit of comparison for

residential land. The sales range in price from $11,556 to $18,571 per unit.

Adjustments were considered for Transaction differences (property rights conveyed, terms of financing,

unusual conditions and market conditions) and Physical differences (location, size and drainage.)

ROCHELLE HOLDINGS II, LLC (TAVARES)

APPRAISAL METHODOLOGY & LAND VALUATION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 38

COMPARABLE LAND SALES MAP

Subject Land Sale 1 Land Sale 2 Land Sale 3 Land Sale 4 Land Sale 5

Lane Park Cutoff 1015 Sheeler Ave 551 Huffstetler Dr 3500 N Goldenrod Road CR 427NE/C Thompson Rd @ E

1st Street

City Tavares Apopka Eustis Orlando Sanford Apopka

County Lake Orange Lake Orange Seminole Orange

Net Land Area (Acres) 5.50 20.64 8.79 4.67 8.28 12.01

Unit Count 66 144 144 70 66 120

Density 12.0 7.0 16.4 15.0 8.0 10.0

Sale Price $2,390,200 $1,665,500 $1,300,000 $1,209,100 $1,920,000

Sale Price/Unit $16,599 $11,566 $18,571 $18,320 $16,000

Sale Date Mar-16 Nov-15 May-16 Aug-16 Nov-16

Drainage On-site On-site On-site On-site On-site On-site

Indicated Price per Unit -- $16,599 $11,566 $18,571 $18,320 $16,000

Property Rights -- 0% 0% 0% 0% 0%

Financing -- 0% 0% 0% 0% 0%

Conditions of Sale - 0% 0% 0% 0% 0%

Market Conditions -- 0% 5% 0% 0% 0%

Adjusted Value per Unit -- $16,599 $12,144 $18,571 $18,320 $16,000

Physical Comparisons

Location -- -20% -10% -30% -25% -20%

Size -- 5% 5% 0% 0% 5%

Lake -- 10% 10% 10% 10% 10%

Density -- -5% 5% 5% -5% 0%

Total Adjustments -- -10% 10% -15% -20% -5%

Adjusted Value per Unit -- $14,939 $13,359 $15,786 $14,656 $15,200

Per Unit

Minimum $13,359 Unit Count 66

Average $14,750 Value/Unit $14,000

Maximum $15,786 Indicated Value $924,000

Median $14,928 Discount rate for 5 Years @ 15% 0.497177

Equals $459,391

Rouned to, say, $460,000

MULTIFAMILY LAND SALES COMPARISON ANALYSIS

Transaction Comparisons

ROCHELLE HOLDINGS II, LLC (TAVARES)

APPRAISAL METHODOLOGY & LAND VALUATION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 39

LAND SALE 1

Transaction

Property ID 4826 Sale Date 03-28-2016

Name Ambergate Townhouses Adjusted Sale

Price

$2,390,200

Address 1015 Sheeler Avenue Price per Acre $115,804

City Apopka Sale Status Closed

State Florida Sale Conditions Arms Length

Seller Sheeler Road Capital, LLC Rights Conveyed Fee Simple

Buyer Park Square Enterprises, LLC Days on Market

Book/Page 2016-0157236 Confirmed With Steve Rosser

Legal Description Lengthy

Site

Land Acres 20.64 Topography Generally level

Land Sq Ft 899,078 Zoning PD

Frontage In Flood Plain? No

Utilities All to site Environ. Issues?

Improvements and Ratios

Gross Density 7.0 Adj $/ Lot $16,599

Remarks

This seller previously secured entitlements for 159 townhouse units and revised approvals to 144 units per the buyer's

needs. The property was under contract for approximately one year and closing was upon securing all permits. There is

a gas easement encumbering the site which, along with the irregular configuration, modestly adversely impacted the

density yield. The townhouse lots are believed to be 22' wide. This sale represents a price of $16,599 per unit.

ROCHELLE HOLDINGS II, LLC (TAVARES)

APPRAISAL METHODOLOGY & LAND VALUATION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 40

LAND SALE 2

Transaction

Property ID 3815 Sale Date 11-20-2015

Name HTG Valencia Adjusted Sale

Price

$1,665,500

Address 551 Huffstetler Drive Price per Acre $189,477

City Eustis Sale Status Closed

State Florida Sale Conditions Arm's Length

Seller Ann Huffstetler Rou, Individually

& as Trustee

Rights Conveyed Fee Simple

Buyer HTG Valencia, LLC Days on Market

Book/Page 4708/1959 Confirmed With CoStar and Public Records

Legal Description Lengthy - Part of S 22, T 19S, R26E, Lake County

Site

Land Acres 8.79 Topography Generally level

Land Sq Ft 382,892 Zoning MCR

Frontage Along both Huffstetler Dr and

Dillard Rd

In Flood Plain? No

Shape Rectangular Encumbrances No known easements or

encroachments that have an

adverse/negative effect on the site

Utilities To site Environ. Issues?

Improvements and Ratios

Proposed Units 144 $/Proposed Unit $11,566

Gross Density 16.38 $/ Lot

Proposed Bldgs. Current Use Vacant

Remarks

The site is being developed with 144 apartment units, resulting in a density of 16.4 units per acre. This sale reflects a

price of $11,566 per unit.

ROCHELLE HOLDINGS II, LLC (TAVARES)

APPRAISAL METHODOLOGY & LAND VALUATION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 41

LAND SALE 3

Transaction

Property ID 5175 Sale Date 05-05-2016

Name Goldenrod Pointe Apartments Adjusted Sale

Price

$1,300,000

Address 3500 N Goldenrod Rd Price per Acre $278,432

City Winter Park Sale Status Closed

State Florida Sale Conditions Arms Length

Seller Goldenrod Baptist Church, Inc. Rights Conveyed Fee Simple

Buyer Goldenrod Pointe Partners, Ltd. Days on Market

Book/Page 2016-0231558 Confirmed With

Legal Description S 1/2 of SE 1/4 of SE 1/4 of NW 1/4 of Section 11, Township 22 South, Range 30 East, Less and

Except the East 500 feet, Orange County, Florida

Site

Land Acres 4.67 Topography Generally level

Land Sq Ft 203,382 Zoning R-3

Shape Rectangular Encumbrances

Utilities To site Environ. Issues?

Improvements and Ratios

Proposed Units 70 Adj $/Proposed

Unit

$18,571

Gross Density 14.99 Adj $/ Lot

Remarks

The property was improved with a church and ancillary facilities which provided no contributory value. This sale

reflects a net area of 4.303 acres, or a density of 16.3 units per net acre. The sale reflects a price of $18,571 per unit.

This is an income restricted development.

ROCHELLE HOLDINGS II, LLC (TAVARES)

APPRAISAL METHODOLOGY & LAND VALUATION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 42

LAND SALE 4

Transaction

Property ID 3966 Sale Date 08-26-2016

Name Windsor Square Townhomes Adjusted Sale

Price

$1,209,100

Address Thomas Stable Road and. Ronald

Reagan Boulevard (CR 427)

Price per Acre $146,113

City Sanford Sale Status Closed

State Florida Sale Conditions Arm's Length

Seller Sydney Levy Rights Conveyed Fee Simple

Buyer Park Square Enterprises, LLC Days on Market

Book/Page 8756/1328 Confirmed With Meera Bhutta/Rep of Grantee

Legal Description Lengthy

Site

Land Acres 8.28 Topography Gently sloping

Land Sq Ft 360,463 Zoning PD

Frontage Approx. 485 feet along CR 427 In Flood Plain? No

Shape Generally Rectangular Encumbrances No are no known easements or

encroachments that have an

adverse/negative effect on the site.

Utilities All available Environ. Issues?

Improvements and Ratios

Proposed GBA 135,526 $/Proposed SF $8.92

Proposed Units 66 $/Proposed Unit $18,320

Gross Density 7.98 Adj $/ Lot

Proposed Bldgs. 14 Current Use Vacant

Remarks

The property had not off-site improvements. The buyer was responsible for road improvements. This sale reflects a

price of $18,320 per unit

ROCHELLE HOLDINGS II, LLC (TAVARES)

APPRAISAL METHODOLOGY & LAND VALUATION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 43

LAND SALE 5

Transaction

Property ID 5176 Sale Date 11-29-2016

Name Wellington Apartments Adjusted Sale

Price

$1,920,000

Address 25 N Thompson Road Price per Acre $159,867

City Apopka Sale Status Closed

State Florida Sale Conditions Arms Length

Seller Thompson Road LLC Rights Conveyed Fee Simple

Buyer Wellington Park Apartments, Ltd. Days on Market

Book/Page 2016-0624390 Confirmed With

Legal Description Lengthy, retained in files

Site

Land Acres 12.01 Topography Generally level

Land Sq Ft 523,156 Zoning PD

Frontage In Flood Plain? No

Shape Rectangular Encumbrances

Improvements and Ratios

Proposed Units 120 Adj $/Proposed

Unit

$16,000

Gross Density 9.99 Adj $/ Lot

Remarks

The property had old nursery related improvements which provided no contributory value. This sale reflects a price of

$16,000 per dwelling unit.

ROCHELLE HOLDINGS II, LLC (TAVARES)

APPRAISAL METHODOLOGY & LAND VALUATION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 44

Transaction Adjustments All sales were conveyances of the fee simple interest and cash or cash equivalent transactions. No

adjustments were necessary for these characteristics. The sales occurred between November 2015 and

November 2016. The effective date of this appraisal is May 31, 2017. The apartment market has been

improving, particularly during the early part of this period for which an upward adjustment of 5% was

applied to November 2015 sale. The adjusted prices range from $12,144 to $18,571 per unit.

Physical Adjustments Location - Adjustments were applied based on relative market desirability and exposure for the highest

and best uses. This includes relative market activity, prices, absorption, etc.

Size - Smaller parcels typically command higher unit prices due to generally shorter holding time or

sellout and associated lower holding costs as well as more buyers in the market at lower absolute prices.

Adjustments were applied accordingly.

Lake - The subject property has frontage on Lake Idamere, a view amenity which can provide premium

prices or rents. None of the comparables have exposure on a view amenity and for which a 10%

adjustment was applied to each sale.

Density - The subject property would have a density of 12 units per acre. The comparables’ densities

range from 7.0 to 16.4 units per acre. Higher densities are less desirable than lower densities from

marketability and finished product price perspective, for which adjustments were applied accordingly.

Summary and Value Conclusion The comparables reflect adjusted unit values of $14,939, $13,359, $15,786, $14,656 and $15,200 per unit,

respectively. The overall indicated range is $13,359 to $15,786 per unit, with a mean and median of

$14,750 and $14,928 per unit, respectively. Sale 2 is the only sale in Lake County and is geographically the

nearest. It also required the least absolute value adjustments. Therefore, we have placed higher reliance

on this sale and secondary reliance on the other sales and mean and median indicators and conclude on a

value of $14,000 per unit.

Multiplying $14,000 per unit by an estimated 66 units, results in a value indication of $924,000. We note

this value is an indicator of value as if ready for current development. However, we estimate the market

maturity (feasibility for development) of the site is five years into the future. In order to reflect this

characteristic, it is necessary to discount this as a future value to ascertain the current value.

Based on our experience, we estimate a 15% discount rate is appropriate to induce a speculator to invest

in the subject property. The multiplication factor for 5 years at 15% is 0.49177. Multiplying the above

developed value of $924,000 by this factor, result in a current, as-is value indicator of $$459,391, rounded

to, say $460,000.

ROCHELLE HOLDINGS II, LLC (TAVARES)

APPRAISAL METHODOLOGY & LAND VALUATION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 45

Therefore, as a result of our investigation into those matters that affect market value, and by virtue of our

experience and training, we have formed the opinion that the prospective market value of the fee simple

estate of the subject property, as of May 31, 2017, will be:

FOUR HUNDRED SIXTY THOUSAND DOLLARS

($460,000)

Your attention is directed to the "Assumptions and Limiting Conditions," which are considered usual for

this type of assignment.

Per the client’s request, the date of value of this appraisal is May 31, 2017. The date of our

inspection was May 20, 2017. Therefore, the opinion of value contained herein is a Prospective

Value. This report is subject to the Extraordinary Assumption that there will be no substantive

changes to the legal, physical or economic issues pertaining to the subject property between the

date of our inspection and the date of value.

This appraisal is subject to a study reflecting no gopher tortoise issues on the subject property, an

Extraordinary Assumption.

ROCHELLE HOLDINGS II, LLC (TAVARES)

GENERAL ASSUMPTIONS AND LIMITING CONDITONS

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 46

General Assumptions & Limiting Conditions

This appraisal is subject to the following limiting conditions:

1. The legal description – if furnished us – is assumed to be correct.

2. No responsibility is assumed for legal matters, questions of survey or title, soil or subsoil

conditions, engineering, availability or capacity of utilities, or other similar technical matters. The

appraisal does not constitute a survey of the property appraised. All existing liens and

encumbrances have been disregarded and the property is appraised as though free and clear,

under responsible ownership and competent management unless otherwise noted.

3. Unless otherwise noted, the appraisal will value the property as though free of contamination.

Valbridge Property Advisors | Beaumont Matthes & Church, Inc. will conduct no hazardous

materials or contamination inspection of any kind. It is recommended that the client hire an

expert if the presence of hazardous materials or contamination poses any concern.

4. The stamps and/or consideration placed on deeds used to indicate sales are in correct

relationship to the actual dollar amount of the transaction.

5. Unless otherwise noted, it is assumed there are no encroachments, zoning violations or

restrictions existing in the subject property.

6. The appraiser is not required to give testimony or attendance in court by reason of this appraisal,

unless previous arrangements have been made.

7. Unless expressly specified in the engagement letter, the fee for this appraisal does not include the

attendance or giving of testimony by Appraiser at any court, regulatory or other proceedings, or

any conferences or other work in preparation for such proceeding. If any partner or employee of

Valbridge Property Advisors | Beaumont Matthes & Church, Inc. is asked or required to appear

and/or testify at any deposition, trial, or other proceeding about the preparation, conclusions or

any other aspect of this assignment, client shall compensate Appraiser for the time spent by the

partner or employee in appearing and/or testifying and in preparing to testify according to the

Appraiser’s then current hourly rate plus reimbursement of expenses.

8. The values for land and/or improvements, as contained in this report, are constituent parts of the

total value reported and neither is (or are) to be used in making a summation appraisal of a

combination of values created by another appraiser. Either is invalidated if so used.

9. The dates of value to which the opinions expressed in this report apply are set forth in this report.

We assume no responsibility for economic or physical factors occurring at some point at a later

date, which may affect the opinions stated herein. The forecasts, projections, or operating

estimates contained herein are based on current market conditions and anticipated short-term

supply and demand factors and are subject to change with future conditions.

ROCHELLE HOLDINGS II, LLC (TAVARES)

GENERAL ASSUMPTIONS AND LIMITING CONDITONS

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 47

10. The sketches, maps, plats and exhibits in this report are included to assist the reader in visualizing

the property. The appraiser has made no survey of the property and assumed no responsibility in

connection with such matters.

11. The information, estimates and opinions which were obtained from sources outside of this office,

are considered reliable. However, no liability for them can be assumed by the appraiser.

12. Possession of this report, or a copy thereof, does not carry with it the right of publication. Neither

all, nor any part of the content of the report, or copy thereof (including conclusions as to property

value, the identity of the appraisers, professional designations, reference to any professional

appraisal organization or the firm with which the appraisers are connected), shall be disseminated

to the public through advertising, public relations, news, sales, or other media without prior

written consent and approval.

13. No claim is intended to be expressed for matters of expertise which would require specialized

investigation or knowledge beyond that ordinarily employed by real estate appraisers. We claim

no expertise in areas such as, but not limited to, legal, survey, structural, environmental, pest

control, mechanical, etc.

14. This appraisal was prepared for the sole and exclusive use of the client for the function outlined

herein. Any party who is not the client or intended user identified in the appraisal or engagement

letter is not entitled to rely upon the contents of the appraisal without express written consent of

Valbridge Property Advisors | Beaumont Matthes & Church, Inc. and Client. Client shall not

include partners, affiliates, or relatives of the party addressed herein. The appraiser assumes no

obligation, liability or accountability to any third party.

15. Distribution of this report is at the sole discretion of the client, but no third-party not previously

listed as an intended user on the face of the appraisal or the engagement letter may rely upon

the contents of the appraisal. In no event shall client give a third-party a partial copy of the

appraisal report. We will make do distribution of the report without the specific direction of the

client.

16. This appraisal shall be used only for the function outlined herein, unless expressly authorized by

Valbridge Property Advisors | Beaumont Matthes & Church, Inc.

17. This appraisal shall be considered in its entirety. No part thereof shall be used separately or out of

context.

18. Unless otherwise noted in the body of this report, this appraisal assumes that the subject property

does not fall within the areas where mandatory flood insurance is effective. Unless otherwise

noted, we have not completed nor have we contracted to have completed an investigation to

identify and/or quantify the presence of non-tidal wetland conditions on the subject property.

Because the appraiser is not a surveyor, he or she makes no guarantees, express or implied,

regarding this determination.

ROCHELLE HOLDINGS II, LLC (TAVARES)

GENERAL ASSUMPTIONS AND LIMITING CONDITONS

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 48

19. If the appraisal is for mortgage loan purposes: 1) we assume satisfactory completion of

improvements if construction is not complete, 2) no consideration has been given for rent loss

during rent-up unless noted in the body of this report, and 3) occupancy at levels consistent with

our “Income & Expense Projection” are anticipated.

20. It is assumed that there are no hidden or unapparent conditions of the property, subsoil, or

structures which would render it more or less valuable. No responsibility is assumed for such

conditions or for engineering which may be required to discover them.

21. Our inspection included an observation of the land and improvements thereon only. It was not

possible to observe conditions beneath the soil or hidden structural components within the

improvements. We inspected the buildings involved, and reported damage (if any) by termites,

dry rot, wet rot, or other infestations as a matter of information, and no guarantee of the amount

or degree of damage (if any) is implied. Condition of heating, cooling, ventilation, electrical and

plumbing equipment is considered to be commensurate with the condition of the balance of the

improvements unless otherwise stated.

22. This appraisal does not guarantee compliance with building code and life safety code

requirements of the local jurisdiction. It is assumed that all required licenses, consents, certificates

of occupancy or other legislative or administrative authority from any local, state or national

governmental or private entity or organization have been or can be obtained or renewed for any

use on which the value conclusion contained in this report is based unless specifically stated to

the contrary.

23. When possible, we have relied upon building measurements provided by the client, owner, or

associated agents of these parties. In the absence of a detailed rent roll, reliable public records, or

“as-built” plans provided to us, we have relied upon our own measurements of the subject

improvements. We follow typical appraisal industry methods; however, we recognize that some

factors may limit our ability to obtain accurate measurements including, but not limited to,

property access on the day of inspection, basements, fenced/gated areas, grade elevations,

greenery/shrubbery, uneven surfaces, multiple story structures, obtuse or acute wall angles,

immobile obstructions, etc. Professional building area measurements of the quality, level of detail,

or accuracy of professional measurement services are beyond the scope of this appraisal

assignment.

24. We have attempted to reconcile sources of data discovered or provided during the appraisal

process, including assessment department data. Ultimately, the measurements that are deemed

by us to be the most accurate and/or reliable are used within this report. While the measurements

and any accompanying sketches are considered to be reasonably accurate and reliable, we cannot

guarantee their accuracy. Should the client desire a greater level of measuring detail, they are

urged to retain the measurement services of a qualified professional (space planner, architect or

building engineer). We reserve the right to use an alternative source of building size and amend

the analysis, narrative and concluded values (at additional cost) should this alternative

measurement source reflect or reveal substantial differences with the measurements used within

the report.

ROCHELLE HOLDINGS II, LLC (TAVARES)

GENERAL ASSUMPTIONS AND LIMITING CONDITONS

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 49

25. In the absence of being provided with a detailed land survey, we have used assessment

department data to ascertain the physical dimensions and acreage of the property. Should a

survey prove this information to be inaccurate, we reserve the right to amend this appraisal (at

additional cost) if substantial differences are discovered.

26. If only preliminary plans and specifications were available for use in the preparation of this

appraisal, then this appraisal is subject to a review of the final plans and specifications when

available (at additional cost) and we reserve the right to amend this appraisal if substantial

differences are discovered.

27. Unless otherwise stated in this report, the value conclusion is predicated on the assumption that

the property is free of contamination, environmental impairment or hazardous materials. Unless

otherwise stated, the existence of hazardous material was not observed by the appraiser and the

appraiser has no knowledge of the existence of such materials on or in the property. The

appraiser, however, is not qualified to detect such substances. The presence of substances such as

asbestos, urea-formaldehyde foam insulation or other potentially hazardous materials may affect

the value of the property. No responsibility is assumed for any such conditions, or for any

expertise or engineering knowledge required for discovery. The client is urged to retain an expert

in this field, if desired.

28. The Americans with Disabilities Act (“ADA”) became effective January 26, 1992. We have not made

a specific compliance survey of the property to determine if it is in conformity with the various

requirements of the ADA. It is possible that a compliance survey of the property, together with an

analysis of the requirements of the ADA, could reveal that the property is not in compliance with

one or more of the requirements of the Act. If so, this could have a negative effect on the value of

the property. Since we have no direct evidence relating to this issue, we did not consider possible

noncompliance with the requirements of ADA in developing an opinion of value.

29. This appraisal applies to the land and building improvements only. The value of trade fixtures,

furnishings, and other equipment, or subsurface rights (minerals, gas, and oil) were not

considered in this appraisal unless specifically stated to the contrary.

30. No changes in any federal, state or local laws, regulations or codes (including, without limitation,

the Internal Revenue Code) are anticipated, unless specifically stated to the contrary.

31. Any income and expense estimates contained in the appraisal report are used only for the

purpose of estimating value and do not constitute prediction of future operating results.

Furthermore, it is inevitable that some assumptions will not materialize and that unanticipated

events may occur that will likely affect actual performance.

32. Any estimate of insurable value, if included within the scope of work and presented herein, is

based upon figures developed consistent with industry practices. However, actual local and

regional construction costs may vary significantly from our estimate and individual insurance

policies and underwriters have varied specifications, exclusions, and non-insurable items. As such,

we strongly recommend that the Client obtain estimates from professionals experienced in

establishing insurance coverage. This analysis should not be relied upon to determine insurance

coverage and we make no warranties regarding the accuracy of this estimate.

ROCHELLE HOLDINGS II, LLC (TAVARES)

GENERAL ASSUMPTIONS AND LIMITING CONDITONS

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 50

33. The data gathered in the course of this assignment (except data furnished by the Client) shall

remain the property of the Appraiser. The appraiser will not violate the confidential nature of the

appraiser-client relationship by improperly disclosing any confidential information furnished to

the appraiser. Notwithstanding the foregoing, the Appraiser is authorized by the client to disclose

all or any portion of the appraisal and related appraisal data to appropriate representatives of the

Appraisal Instituted is such disclose is required to enable the appraiser to comply with the Bylaws

and Regulations of such Institute now or hereafter in effect.

34. The value opinion(s) provided herein is subject to any and all predications set forth in this report.

35. The Valbridge Property Advisors office responsible for the preparation of this report is

independently owned and operated by Beaumont Matthes & Church, Inc., a Florida corporation.

Neither Valbridge Property Advisors, Inc., nor any of its affiliates has been engaged to provide this

report. Valbridge Property Advisors, Inc., the parent company, does not provide valuation services,

and has taken no part in the preparation of this report.

36. This report and any associated work files may be subject to evaluation by Valbridge Property

Advisors, Inc., or its affiliates, for quality control purposes.

37. Acceptance and/or use of this appraisal report constitutes acceptance of the foregoing general

assumptions and limiting conditions.

ROCHELLE HOLDINGS II, LLC (TAVARES)

CERTIFICATION

©2017 Valbridge Property Advisors | Beaumont, Matthes & Church, Inc. Job #: 17-157 51

Certification

We certify that, to the best of our knowledge and belief:

1. The statements of fact contained in this report are true and correct.

2. The reported analyses, opinions, and conclusions are limited only by the reported assumptions

and limiting conditions and are our personal, impartial, and unbiased professional analyses,

opinions, and conclusions.

3. We have no present or prospective interest in the property that is the subject of this report and

no personal interest with respect to the parties involved.

4. We have no bias with respect to the property that is the subject of this report or to the parties

involved with this assignment.

5. Our engagement in this assignment was not contingent upon developing or reporting

predetermined results.

6. Our compensation for completing this assignment is not contingent upon the development or