property sciences amc - staff and fee appraiserstoday+5... · property sciences amc - staff and fee...

TRANSCRIPT

IN THIS ISSUEManaging multiple appraisal deadlines to increase productivity . . . . . . . . . . . . . . . . . .Page 6Howto use the 1004MC to address uneasonable reconsideration requests . . . . . . . . . . .Page 9

Property Sciences AMC - staff and fee appraisers

May 2013–©Appraisal Today–PAGE 1

VOLUME 21 • ISSUE 5 • May 2013

Many AMCs were started byappraisers who had a non-

AMC appraisal business using bothstaff and independent contractorappraisers. This has not changedmuch over time, including the recentboom in the AMC business. My arti-cle in the April 2013 issue, "A briefAMC history from 1967 to now -from 5% to over 80% of theappraisals!". discussed AMCs in the1990s. Many were started by apprais-ers back then, similar to today'sAMCs.

Most of the over 400 AMCs startedsince HVCC were started by apprais-ers.

Property Sciences is one of the fewlong time appraisal companies thatshifted to AMC work. It has been inbusiness for almost 30 years and sur-vived two significant appraisal reces-sions. I have included information onhow they survived.

I have known Paul Chandler, MAI,the founder and CEO of PropertySciences since soon after I started myappraisal business in 1986. Paul start-ed his business in 1984. We bothstarted our businesses doing commer-cial appraisals and shifted to bothcommercial and residential due to theappraisal boom that started in 1986.

Paul is one of the few appraiserswho successfully shifted his business

strategy when the residentialappraisal business changed over time,responding to the booms and busts ofthat market.

In stark contrast, the commercialappraisal side of his business haschanged little over time, similar tomine. Steady volume, not manychanges in reports, no AMCs, etc.

A brief history of Property SciencesThe company was founded in

1984. The founder, Paul Chandler,graduated from University ofCalifornia Berkeley in 1981, with aB.S. in business administration,(emphasis in finance). He receivedhis MBA (emphasis in real estate) in1989 and his MAI designation in1989.

In 1980, while still in college, hestarted working for Corinthian RealEstate. He was a site locator for S&Lbranch offices. The second year ther,he began to work for Corinthian'sparent company, Market InsightCorporation, consulting on marketanalysis, acquisitions, and S&Lbranch locations for S&L expansion.

In 1984, he started working forGolden Coin Savings. He was a VicePresident of Real Estate, working onresidential developments. At that timeS&Ls were allowed to do develop-ment loans. This was later stoppedwhen many went out of business dueto bad development loans, resultingin FIRREA regulations, which alsorequired appraiser licensing.

He started his appraisal business in1984, doing commercial appraisals.In 1986 he expanded into residentialappraisals. There were very fewappraisers left after the 18% mort-gage rates from 1981 to 1985. At thattime, most appraisers were staffappraisers for lenders. Almost allwere laid off. Some were able to dojobs such as tellers at bank branchesto keep employed.

Paul had two very experiencedappraisers who helped him when hefirst started his business and when hebegan doing more residential work,since he was a commercial appraiser.I also had two appraisers who helpedme with lender residential appraisals,as I had never seen a Fannie Mae

www.appraisaltoday.com

PAGE 2–©Appraisal Today–May 2013

form. Chief appraisers at severallenders were also very helpful, espe-cially regarding what could, andcould not, be included on the formsdue to banking regulations (i.e., fairlending).

I left an assessor's office and got anMBA in 1980. From 1980 to 1985 Iworked in corporate real estate for abiotech company. I had planned onreturning to appraising, but therewere very few appraisal jobs andthey paid much less than non-appraisal real estate jobs.

I got bored with the corporate lifeafter awhile and really missed work-ing in the field. In 1985 I decided tostart my own appraisal business andworked part-time for another apprais-er for about 6 months.

In January, 1986, when I startedmy business, there was no appraiserlicensing. Lenders gave you workbased on your experience, education,and work samples. You interacteddirectly with the local appraisaldepartments of national lenders suchas Bank of America and locallenders.

When I started my business, simi-lar to Paul, I did commercialappraisals. But, I was able to get asmuch residential work as I wanted,so I shifted to mostly residential. Istill do both residential and commer-cial appraisals.

Paul has always focused on lenderwork and does some non-lender com-mercial appraisals. He also has donea lot of training for both residentialand commercial appraisers. All of hisformer trainees say their training wasvery good. Of course, after HVCChe did not have any residentialtrainees as they could no longer signappraisals.

Paul Chandler - life beyondappraising

When I visited the PropertyScience office, I noticed classic base-ball photos and old Hollywood movieposters on the walls instead of theusual blank white walls found inmost offices, including mine.

Paul is a sports fan, with seasontickets to the Oakland A's baseballteam. He is a golfer and tennis player.He collects piggy banks from oldS&Ls and classic movie posters.

He loves to travel and went toThailand last month, with his wife of30 years.

He has one child, a 18 year olddaughter. No, she does not want to bean appraiser (now). But, I havenoticed that some children join thefamily business after a few years ofso-so jobs following college gradua-tion.

Transition to appraisal managementIn the late 1990s when the Internet

was starting to take off, Chandlerworked with eloan (one of the firstonline mortgage origination compa-nies). He hired software programmersand helped establish their appraisalpolicies, including an electronicappraisal interface and set up anAMC for eloan to order appraisals.After a few years, he quit working foreloan and dropped the AMC work.

In 2008, anticipating HVCC, herealized that mortgage bankers need-ed someone to do their appraisals. Heset up the first HVCC compliantmortgage appraisal portal for origina-tors using five software programmers.Within five months of HVCC imple-mentation in 5/09, 7 out of 10 mort-gage bankers were using his software,Accelerated Mortgage Connection,AMCTrak.

Afer the AMC business took off, hehired more residential staff appraisersand expanded to a national AMCusing independent contractors.

Residential review business - startedin the early 2000s

In the early 2000s, the appraisalreview market was very strong withlots of business. Three of the largestreview companies were purchased byFidelity, including two in California.

Chandler saw an opportunity andshifted his residential business focusfrom appraisals to reviews. PerChandler, he had the largest share ofreviews in the California review mar-ket.

Handling the ups and downs of theappraisal business

There was a very significant crashin the appraisal business in 1994. Iwent from 7 employees to myself anda part time assistant.

At the peak, Chandler had 6 officesand 115 people working for him. In1993-1994, Inc magazine namedProperty Sciences one of the "FastestGrowing Companies in America".Within 12 months, he downsized by50% and kept his Los Angeles office,which a partner later bought out.

The next crash started in 2008,with the subprime mess. He laid offmost of his appraisers, with about 6-7appraisers remaining.

By shifting to AMC work post-HVCC, he started hiring staffappraisers and greatly expanded hisuse of independent contractors on anational basis. Staff appraisers are onthe West Coast. He now has 107employees, including 72 licensed/cer-tified appraisers.

He has a southern California officein Glendale and recently started aFlorida division. Why Florida? A bigmortgage market. He is already inCalifornia, the biggest market in thecountry.

May 2013–©Appraisal Today–PAGE 3

Commercial vs. residentialThe number of commercial

appraisers remained fairly constantthrough the booms and busts.Property Sciences currently has 11commercial appraisers. They wereable to shift from origination to assetmanagement. There was also non-lender work available.

Use of technologyAlthough Paul is not a computer

programmer, he has developed andused technology. He developed theappraisal policies around the firstonline mortgage origination platformfor e-loan in the late 1990s, includingan electronic appraisal interface.

In the late 1990s he developed C-loan, an online commercial lenderdirectory for mortgage bankers andbrokers. He sold the business in 2001to another directory that wanted toexpand from residential into com-mercial lending.

A key component for AMCs' suc-cess is software that can handle man-aging the appraisal orders. Some oldAMCs use old "legacy" systems.Newer ones use online applicationsdeveloped by software companies,such as etrac and a la mode.

Property Sciences developed itsown appraisal management softwareto track and manage appraisal ordersbefore HVCC started, which isunusual for a small to mid-size AMC.It also has online software, developedearlier, to interface with its clients(AMCtrac).

AMC sub-contracting - "cascading"Many of the large AMCs subcon-

tract their overflow to mid-sizeAMCs. That is one of the reasonsthat appraiser fees are low. I call it"cascading". Big AMC A subcon-tracts to Mid size AMC B, who thensubcontracts to mid-size or smallAMC C. Each one of these needs tomake money.

Property Sciences does not partici-pate in sub-contracting. It does not

subcontract to other AMCs.

Number of appraisals from eachstate varies

Property Sciences has concentratedon California appraisals for manyyears, so much of its business is inCalifornia. In 2007, it expandednationally. When you are a nationalAMC you agree to accept appraisalsfrom all over the country. For exam-ple, a credit union in San Franciscomay need an appraisal for a memberwho moved to Illinois.

How many appraisals and reviewsper year?

About 8,500 appraisal orders permonth. Typical for a mid-size AMC.

Of the 8,500 orders:- Full appraisals: 86%- Reviews: 14%

How are orders assigned?Staff appraisers are typically given

first priority, just like any otherappraisal company or AMC.

Each order is manually assigned.Property Sciences conducts prelimi-nary research on each property that isto be appraised, so that any uniquefactors that may increase complexityare considered and addressed withthe appraiser during the qualificationprocess and the best appraisal firm isutilized.

Do they broadcast orders?They prefer to use appraisers that

have worked for them before, justlike any other type of business.

Property Sciences does not blast orblindly broadcast orders for the low-est fee quote or for first-come/first-serve assignment.

If they receive an order in an areawhere they don't have appraisers theyhave used before or a super-rushorder, they broadcast the order toappraisers on their panel in that area.

How many appraisals are reviewedby appraisers?

All appraisals are reviewed byProperty Science staff appraisers.This is unusual. Most AMCs onlyhave the difficult appraisals or "prob-lem" appraisals reviewed by apprais-ers.

How many licensed appraisers arethere and what do they do?

72 (70%) of the 103 total employ-ees are licensed/certified appraisers.This is an unusually high number ofappraisers for the company's size.

Breakdown:- Commercial appraisers: 11- Staff appraisers (production): 30- QC (reviewers): 28 (1 appraiser forevery 321 orders, or 16 reviews perday). - Other appraisers: 11 managers

For an appraiser, this means youcan talk with an appraiser, a signifi-cant plus. Most AMCs have muchfewer appraisers per number oforders.

How are appraisals checked andreviewed?

Lender's information is automati-cally pulled into the system from thelender online interface. - Rules check: Rules engine (ACIHotspot), similar to forms softwarereviews- Stage 2: Real Estate Analyst (recentcollege graduates): Verify basic data (match publicrecords, check MLS) and check criteria: i.e., ½ mile for compsfrom MLS- Stage 3 and 4: QC licensed apprais-er, reads reports, minimum of 10years of experience. These are theonly people who can call appraisers.

More details (information sent to aprospective lender client):

1. Report scrubbing technologyruns hundreds of automated QC rulesthat instantly check the report forerrors, inconsistencies, and potentialviolations. Rules results are populat-

How are cash flow problemshandled?

Residential lending is notoriouslyvolatile. Labor cost is very, very highfor any appraisal business. AMCstake in orders, but their clients don'tpay them when they place the orders.If they don't have cash reserves, theycan run out of money waiting for thelenders to pay them. AMCs have topay their staff appraisers first. If theydon't have the cash, fee appraisershave to wait.

Property Sciences has been throughtwo major appraisal recessions andsurvived. That experience of manag-ing cash flow is very valuable.

What are the advantages of shiftingstaff appraisers between QC andproduction?

One of the big advantages to hav-ing staff appraisers is shifting thembetween QC and production. Forexample, business picks way up.Appraisers can shift from productionto QC. Fee appraisers can be usedmore for production. Or, businessslows down and and QC appraiserscan shift to production appraisers.Fee appraisers will have less work.

For lenders, one of the biggestproblems is QC "bottlenecks" as thereare not enough QC reviewers andappraisals get stalled. The ability toshift production appraisers to QChelps resolve this problem.

What does this mean for feeappraisers? Less work for some, butalso less risk of not getting paid.

PAGE 4–©Appraisal Today–May 2013

ed into an internal QC checklist forreview by the Real Estate Analystteam, who conduct a first pass manu-al quality control review of eachreport.

2. Preliminary QC Review processincludes automated rules results veri-fication and the compilation of prop-erty and market specific publicrecords and MLS data, where indi-vidual property information as wellas general market recent sales andlistings activity through publicrecords, MLS, and other data sourcesare gathered and compiled for furtheranalysis and validation by a seniorlevel professional.

3. Senior QC Review. Each reportthen undergoes a line-by-line manualreview by one of the senior QC pro-cessionals, selected based primarilyon geographic competency, volumecapacity, and property or client-spe-cific specialization They averageover 10 years of appraisal, qualitycontrol, and/or collateral due dili-gence experience.

How are conditions fromunderwriters handled?

They are first screened to see ifthey are reasonable and make sense.Those that do not pass the screeningare sent to the appraisers.

What about underwriter requests?After the appraisals are ready to

do, they are sent to the lender clientand reviewed by one of their under-writers.

Unfortunately, underwriters workwith the specific requirements oftheir employers. They are notappraisers and have little or noappraisal training.

Many don't understand appraisals.Asking them to read appraisals look-ing for answers to their questionsdoes not work well. Spending a lot oftime looking for answers and maybe,or maybe not, understanding theanswers is a real hassle.

Do they have appraiser "tiers"?They have a "core" groups of about

10-15% of the 8,800 appraisers ontheir list.

They prefer to use appraisers theyhave used in the past and have estab-lished a relationship with.

How are fees determined?They don't have set fees.

Appraisers set their own fees.

What about background checks?They do not require them for fee

appraisers. They do them only forstaff appraisers.

What about work samples?They do not require work samples.

They prefer to see how the appraiserperforms on the first few orders.

How are lender's specialrequirements communicated to theappraiser?

In the letter of engagement.Requirements of the lender request-ing the appraisal are included, notpages and pages of requirements ofall the AMCs lenders.

How many clients are there?Property Sciences has about 20

"core" accounts with about 30 othersmall lenders.

What ordering and managingsoftware do they use?

They use proprietary software:PSManager for tracking the orderfrom beginning to end within theAMC, and AMCTrak online interfacethat connects appraisers, AMCs,lcients and other business partners.

May 2013–©Appraisal Today–PAGE 5

What about exclusionary/watchlists?

AMCs need to keep close track oflender's "black" lists. If they use anappraiser on a lenders blacklist, theywill have to pay another appraiser todo the appraisal and their client willhave to wait.

Property Sciences uses a formalcommittee. If the committee votes tono longer accept work from theappraiser, a letter is sent to theappraiser providing 30 days torespond. There are different levels ofactions:- Placement on exclusionary list- Letter of concern- Senior review always required- No action required

How are lender requirementscommunicated to the feeappraisers?

Their engagement letters sent toappraisers are specific to eachlender's requirements, rather thanusing long "generic" engagement let-ters that combine requirements ofmany AMCs. Their software is set upto easily accomplish this.

When are fee appraisers paid?Twice per month via their choice

of check or direct deposit, betweennet 7 and net 22 days from theappraiser's order completion.

How do appraisers apply for thepanel?

Go to www.propsci.com and clickon Approval Packets. They do notrequire work samples, although theweb site refers to them.

How does Property Sciences comparewith other AMCs?

This is my second AMC profile.The first one, in the January 2013issue profiled Axis which has a simi-lar monthly volume and is similar insome ways and different in others.Check out their profile and compare itwith Property Sciences.

Should you work for PropertySciences?

Just like deciding for any AMC,what is important to you?- High fees- AMC reviews done by appraisers- Timely payment of fees- Give you work regularly, not once ayear- Low risk of payment problems- Fewer stupid condition- Don't want to work for the bigAMCs- Don't like broadcast orders

Contact information:www.propsci.com395 Taylor Blvd, Suite 250Pleasant Hill, CA 94523Phone: (925) 246-7300

PAGE 6–©Appraisal Today–May 2013

gridded listings. More lenders aredemanding the cost approach, partic-ularly in FHA appraisals.

Appraisal management companiesand lenders have risen to new heightsin techniques for prodding appraisersto meet deadlines. Some even sendout monthly performance reports, sortof report cards on whether appraisersplay well with others or at least sendin reports on-time. With each gain inoffice productivity, clients seem todemand still shorter report turn-around times.

The incessant faxes, e-mails, andfollow-up phone calls tracking reportprogress are becoming serious inter-ruptions in report production.

The stress of managing multiplereports takes its toll on appraisersability to maintain confidence andmake sound decisions under stress.

While technology now dominatesour discussions and that which weread in the trade magazines, apprais-ers must not overlook real and lastingproductivity gains found in manage-ment techniques and principles. Someof these skills appraisers apply every-day. Other techniques are not new,but deserve even more emphasis.

Step 1. Set goals and prioritiesManagement guru Tom Peters once

said, "Effective visions prepare forthe future, but honor the past."Whether it is a formal business planor simply a list of goals and direc-tions, it is difficult to imagine pro-ceeding in today's business environ-ment without an overall plan for thefuture.

Experts on time management allagree setting out future goals anddirections is the number one essentialof management and collectively allinsist these must be in writing andreviewed constantly. Without a road

By Doug Smith, SRA

Editor's comment: fees are up, butScope Creep is making appraisalstake longer to complete. Efficient useof your time to complete moreappraisals is very critical now. Noone knows how long this boom willlast. I took a one-day business timemanagement seminar many yearsago. I still use the techniques Ilearned every day.

As appraisers adjust to the shift incompanies ordering appraisals,

orders are flowing again. However,these new companies have hugeexpectations not only in turn times,but for the amount of information inreports.

Appraisers, both residential andcommercial have in the last fewyears embraced technology, newsoftware, Internet communicationand Web based data research toimprove productivity.

Appraisers as well as appraisalsoftware companies labored mightilyand continue to work to keep up withthe UAD changeover and makeeverything having to do with UADwork efficiently. While theseimprovements reduce report prepara-tion time, improve delivery to clientsand make research more efficient,appraisers increasingly struggle tomeet deadlines and manage multipleorders.

Increasing expansion of scope ofwork and requests for updates

Appraisers comparing the com-plexity of appraisals point out thoselenders are expanding the scope ofwork of assignments.

More is required within reportsincluding the 1004MC and additional

map, appraisers will likely neverrealize the goal of effectively manag-ing multiple reports and meetingdeadlines.

A corollary to setting out writtengoals and directions is using a priori-tizing system.

The key to this system is sortingout deadlines in terms of long term,short term or immediate. The nextstep is to weigh the deadlines interms of return or impact.

For appraisers, defining and weigh-ing the payoff or consequence frommeeting deadlines is probably thegreatest hurdle. Often, the client whois the squeaky wheel gets theresponse.

The word triage is commonlythought of as applying the assign-ment of degrees of urgency to decidethe order of treatment of wounds, ill-nesses on the battlefield.

While on some days appraisersmay feel they are on a battlefieldmanaging multiple casualties, theword triage, in its first definition, ismore meaningful to the managementof report preparation. The first pre-ferred definition of triage is, "the actof sorting according to quality."

Clients represent differing qualitiesand, therefore, deserve greater or lesspriority in terms of their contributionto the long-term health of theappraisal firm. For some appraisers,clients are not always seen to have along-term effect with only a one-timeneed.

However, each client must be eval-uated in terms of their possible influ-ence for referring other clients. Anynew client deserves careful evalua-tion in terms of quality and thepotential they might have in a long-term relationship. I

In any prioritizing system, the first

Managing multiple appraisal deadlines to increase your productivity

May 2013–©Appraisal Today–PAGE 7

rule is to be aware of qualitative dif-ferences among clients.

Step 2. Rank priorities - Mind yourA, B, C's

The second step in a system of pri-oritizing is ranking priorities.

There are several well-known sys-tems for weighting individual priori-ties. Alan Lakein, in his book firstpublished in 1974, "How to GetControl of Your Time and Your Life"suggested an A, B, C system forassigning importance to items.

More recently Steven Covey,author of "The 7 Habits of HighlyEffective People" promotes a systemhe describes as the four quadrants.The upper left quadrant being thoseitems that are urgent and important;the upper right quadrant being thoseitems that are important, but not yeturgent. The lower left quadrant is thedangerous trap for appraisers; thoseitems that are urgent, yet not impor-tant. Finally he labels the time wast-ing items in the lower right as thoseitems not important and not urgent.Covey emphasizes addressing thoseitems in the upper right quadrant thatare important, but not yet urgent.Assigning priorities depends on indi-vidual preference.

However, the essential step is rank-ing those priorities. In this step,appraisers have an advantage becauseprioritizing is an everyday skillhoned as part of the appraisal processcomparing one property with another.Once a set of priorities is set out,ranking is accomplished by compar-ing the first priority, to the secondand then comparing the more urgentof those first two on the list to thethird working down.

With priorties in place, the nextstep is to view the greater timeframe, not just the day, but also theweek and the month. Some benefitfrom keeping a time log in the shortterm to diagnose activities that maycontribute to inefficiency and theresultant stress. Keeping a time log

over time is not practical and is bet-ter used from time to time as a diag-nostic tool.

Step 3. Follow your calendarThe goal of every appraiser is to

have a high impact week. In highimpact management of time leadingto greater productivity there is onecommonality above all others andthat is the diligent use of a portablepersonal planner.

There are many systems, Franklin,Day Timer and Filo-Fax to mention afew. More and more appraisers arereporting good use being made of acloud based program calledEvernote. Evernote is particularlyuseful for offices with more than oneperson. Evernote sets up multiplenotebooks that can be accessed byothers in the office.

For those who are comfortablewith Microsoft Outlook, the calendarprogram is fully capable of keepingtrack of work in progress andappointments.

There are a myriad of PDA orga-nizers for smart phones and tablets. Isubmit, however, that if the appraiserdoes not now use a personal planner,making the leap to a palm type orga-nizer may not result in meaningfulmanagement of time. Like the draw-ing programs, if an appraiser can'tdraw a house on paper, they neverwill do it well with a drawing pro-gram.

The personal planner keeps pro-jects and deadlines in view at alltimes. Appraisers are out of theiroffices frequently, inspecting andcollecting information, thereforeportability of the daily planner isessential. Lastly, the personal planneras a constant companion keepsappraisers from losing tract of thesmall items, requests and those ideasthat come out of no where.

I learned one lasting lesson in timemanagement seminar that has stayedwith me. It is "When you think it-inkit."

When in doubt, throw it outThe handling of information both in

written form and on computers is somuch a part of appraising, efficienthandling is essential to meeting dead-lines.

B.C. Forbes famously said, "Next tothe dog, the wastebasket is your bestfriend." Simply put, working effi-ciently means getting rid of the clutterboth past and present. Steps for han-dling information or paper workinclude:• Dispose of it: throw it away• Send it on to someone else for han-dling-delegate• Do something with it• File it; archive it• Read it or handle it later

If there is any delay in handling theinformation, proper office manage-ment demands a tickler file or calen-dar file system.

One of the remarkable tips I gotfrom an experienced office managerwas the use of a stand up sloping filedivider. Appraisal files in process arenearby, visible and within easy reach.

I found this to be superior to a filedrawer system where reports maybecome "out of sight, out of mind."

Again, systems are individually dri-ven. Some appraisers use a log sys-tem independent of each individualfiles to track the progress of files.Others log progress on the files them-selves.

Office management and handlingmay seem to be so much commonsense. But, I have benefitted greatlyby having an experienced office man-ager review my office procedures,location of file drawers and work-space arrangement.

Of course, the best advice was"clean up this place." Out went theold phone books, out of date maga-zines and useless clutter that apprais-ers are likely to keep. Have an outsideexpert review your system and objec-tively critique the appraisal office asan office workplace.

Knowing when to say noAppraisers face too many requests

for their time. Having a system inplace is not enough. Sometimes theability to meet deadlines and handlemultiple projects requires an apprais-er to say no.

The typical preliminary clientrequest is predicated on three ques-tions, 1. Can you do an appraisal in a cer-tain area? Answered affirmatively,the next two questions are: 2. How much is the appraisal?3. What is your turnaround time?

Appraisers have a number of stockanswers to turnaround. Any othercommercial enterprise, when askedthese questions, qualifies the cus-tomer. Appraisers can do this by ask-ing, "What is the range of yourrequired turnaround time." In otherwords, begin the process of establish-ing just what is expected. Repeatclients sometimes have set deadlinesand turnaround times. In some casesthese may be negotiated.

The second question about price isalso a qualification measure. Asking,what is the expected cost in this areaof reports received is a polite way ofestablishing the price point of thepotential client. If the client is trulyshopping and reluctant to discusstheir fees, they are most likely actingon the lowest bid. They also areprobably not a good fit in theappraiser's business plan.

How to say noBut at that point, how best to say

no? The simplest way is to prepare the

listener for the turn down and say soearly in the conversation. "I wouldreally like to help you with thisassignment, but I can't."

Some appraisers leave the dooropen by stating when they haveopening in the future. For commer-cial appraisers, lead-time is greaterand this is a realistic approach.

In today's market, however, for the

residential appraiser, saying youdon't have an opening in two weeksdodges the issue. It is better to sayno up front and invite a subsequentorder than to state an impossiblecompletion time.

In client communication, there aretwo word commonly misused. Thesewords are "can" and "how." Thequestion "can I help you?" implies ayes or no answer. "How may I helpyou?" seeks information.

In your discussion with clientsconcentrate on how you may help. Inthe same way, when an appraisersays no, explain why and offer alter-native solutions.

Saying no requires preparation.When the request comes in, apprais-ers must know where they are inreport production to effectivelyaccept or decline an order.

Lastly, probably no business enter-prise can be over-marketed, but inthe law of supply and demandappraisers must be discerning in allmatters of accepting or rejectingpotential business or clients. Thelong-term health of the appraiser'sbusiness depends on it.

SummaryTo effectively manage multiple

appraisal deadlines, working from aset of clear goals and prioritizingworkflow allows the appraiser tofocus.

Proper planning in the form ofadherence to the use of a portablepersonal planner eliminates procrasti-nation, neglect and confusion.

Having a system in place to handleinformation and paper work gives theappraiser control over workflow.

Finally, practicing effective com-munication with potential clients andbeing able to say no builds both per-sonal power and strength in theappraisal firm.

Concentrating, then, on the man-agement aspects of productivity canpay great dividends, increase produc-tivity, reduce the constant sense ofurgency and make appraising a lessstressful enterprise.

Where to get more informationThere are many books, online arti-

cles, audio recordings, etc. For me,taking a live seminar on businesstime management worked best. Theyall have the same basic concepts dis-cussed above. Google your locationfor any live seminars. Google thetopic for online articles. Go to ama-zon.com and look at the books,video, and audio resources.

About the authorDoug Smith has an appraisal prac-

tice in Missoula, Montana, and is acertified general appraiser doing bothresidential and commercial apprais-ing with a specialty in hotel apprais-ing and feasibility studies.

He has an MBA from theUniversity of Montana and the SRAdesignation from the AppraisalInstitute. He can be contacted [email protected].

PAGE 8–©Appraisal Today–May 2013

May 2013–©Appraisal Today–PAGE 9

By Denis DeSaix, SRA

Stakeholders in the residentialmortgage finance process can ini-

tiate a request for reconsideration ofvalue. Typically, that reconsiderationincludes some data that the stake-holder suggests the appraiser consid-er and, after consideration, mayresult in a modification of the valueopinion.

The request for reconsideration is alegitimate component in the mort-gage lending process:• Reconsideration requests arespecifically cited in Dodd-Frank asnot being an infringement onAppraiser Independence• FHA (for example) requires that itsfee panel appraisers evaluate recon-siderations as part of the engagementand to do so at no additional charge• The GSEs have no prohibition onreconsiderations• Many clients have reconsiderationlanguage as part of their engage-ment-agreements

An underlying premise of thereconsideration is that the new datagiven to the appraiser be appropriate.Not all stakeholders have the where-withal to evaluate what constitutesappropriate (vs. inappropriate), andnot all stakeholders are objective intheir reconsideration-data selection.

On the other hand, some requestsare legitimate; both in the data selec-tion and in the motivation for provid-ing it, and those instances warrantthe full attention of the appraiser.

A challenge that many appraisersface is: A. How to quickly and efficientlyscreen the reconsideration data todetermine its appropriateness, and B. If found inappropriate, how toaddress that issue to the client in a

manner that is impartial, objective,and independent, and maintains apositive, business-like rapport andrelationship between the appraiserand client?

One relatively simple and impartialmethod is to rely upon the appraisal'smarket analysis and 1004MC form-driven analysis to be the primaryevaluation process to determine theappropriateness of new data providedin the reconsideration request.

Indeed, this is the initial test theappraiser uses to determine whatsales are comparables; it shouldtherefore be the credible test to deter-mine the appropriateness of any newdata.

Step 1: Market Analysis - definingthe market

The first step is for the appraiser todefine the subject's neighborhoodand competitive market area.

The Dictionary of Real EstateAppraisal (4th ed.) defines the term"neighborhood" as: "A group of com-plementary land uses; a congruousgrouping of inhabitants, buildings, orbusiness enterprises."

The subject's competitive market iswhere it competes against other, sim-ilar properties for the same buyerpool. The Dictionary of Real EstateAppraisal defines "CompetitiveMarket" as: "The geographic or loca-tional delineation of the market for aspecific category of real estate, i.e.,the area in which alternative, similarproperties effectively compete withthe subject property in the minds ofprobable, potential purchasers andusers.

As a rule, the competitive marketwill be equal to or larger than theneighborhood. Defining the marketin this manner provides two ratio-nales for comparable selection:

1. In general, homes in the immediateneighborhood would be more similarto the subject than those in the larger,competitive market; and2. As a rule, homes within the com-petitive market are better substitutesvs. homes outside of the competitivemarket.

By definition, a comparable for thesubject will be in the competitivemarket area.

Defining the neighborhood pro-vides a rationale for the appraiser toargue that a home in the neighbor-hood may be superior to a home out-side of the neighborhood (but insideof the competitive market); alterna-tively, if the appraiser excludeshomes within the neighborhood, thenthe appraiser should be able to sup-port that rationale as well.

Nevertheless, the data consideredas comparables are those propertiesthat are within the competitive mar-ket; data outside of this defined area,by definition, is not relevant unless itis necessary to go to a "competingmarket". In most cases, if appropriatedata exists in the primary market,there is no reason to go to a compet-ing market.

The two definitions can be used aspart of the regular template in anappraisers report. For each assign-ment, the subject-specific boundariesare identified and described. Anexample is included below:

Defining the market area - Anexample from an appraisal report

The Dictionary of Real EstateAppraisal (4th ed.) defines the term"neighborhood" as:A group of complementary land uses;a congruous grouping of inhabitants,buildings, or business enterprises.The subject's neighborhood is there-fore identified by the following

How to use the 1004MC to address unreasonablereconsideration requests

PAGE 10–©Appraisal Today–May 2013

boundaries: Bernal Av (SE), FoothillRd (SW), W. Las Positas Dr (NW),and the 680 Frwy (NE).

The subject's competitive market iswhere it competes against other, simi-lar properties for the same buyerpool. "Competitive Market" isdefined as: The geographic or loca-tional delineation of the market for aspecific category of real estate, i.e.,the area in which alternative, similarproperties effectively compete withthe subject property in the minds ofprobable, potential purchasers andusers.

The subject's competitive market isidentified by the following bound-aries: Foothill Rd (SW), CastlewoodDr/Sunol Blvd/Sycamore Rd (SW),open space (E), Vineyard Ave (N),1st/Bernal Av (N & NW), and the 680Frwy (NE).

Adequately defining the subjectNeighborhood and CompetitiveMarket is the first filter to use forscreening reconsideration data.

Step 2: The 1004MC AnalysisThe 1004MC analysis is designed

to provide the client with a summaryof the properties within the subject'scompetitive market that directly com-pete with the subject.

In other words, these homes arethose properties that the appraiser hasdetermined are the likely/best substi-tutes a likely buyer (the market)would consider when evaluating thesubject in a purchase-decision.

The search parameters for likelysubstitutes are typically based on thesignificant elements of comparison.For example, such parameters may beCondition• GLA• Location• Bed/Bath Count• Lot Size• Any other special amenity

Data is initially searched usingthese parameters.

Appraisers should add an addi-tional filter screen to this initialsearch to identify and eliminateoutliers. Outliers can skew the data(a low sale due to a significant condi-tion impairments, etc.).

With additional screening, theappraiser can be confident that thesearch has resulted in those propertiesthat are most similar to the subjectand that are located within the com-petitive market area.

Assuming the appraiser has con-structed a reasonable market-screenfor the subject, the results are all theproperties that should be used forcomparable selection.

Many MLS systems provide a for-mat report that is similar to the1004MC grids. In addition to the gridsummary, they also provide a list ofthe data considered in the analysis.

An example of an MLS-print out ofa single-screen form is presented onthe previous page.

This is the data that the appraiserhas determined are the most relevantand appropriate comparables to con-sider. If there are sufficient datapoints within this sample, thenreliance on the primary competitivemarket for comparable selection isestablished. If the data sample is notsufficient, then additional searchesmay be necessary in competing mar-kets.

Note: the 1004MC is designed toprovide the client with informationon the subject's competitive marketonly. The 1004MC search parame-ters should not be artificiallyexpanded if there are few sales.Indeed, one purpose of the analysis isto support the decision to go outsideto competing markets if necessary.

Therefore, the 1004MC resultsshould only include those found inthe identified competitive market. Ifthe appraiser uses sales from a com-peting market, these should not beincluded in the 1004MC results.

The final component is to providecommentary in the 1004MC adden-

dum regarding the comparable searchprocess. An example of such a com-ment is included below.

Note that the citation includes:• A reference to the defined competi-tive market areaThe significant elements of compari-son that were used as a primaryscreen• The fact that outliers were excludedon a second screenThese are the sales most similar tothe subject and these are the salesconsidered by the appraiser. This isconsistent with the following certifi-cation in the GSE reporting form:

Evaluating the reconsideration dataThe prior process is part of the nor-

mal procedure in developing andreporting an opinion of market valuefor a residential mortgage loan.Appraisers complete these steps, andappraisers can use this process toscreen the reconsideration data. Insummary, the steps are:1. Define the competitive market andthe subject's neighborhood (these maybe the same geographic area, but thecompetitive market will typically beat least as large as the neighborhood).2. Define the significant elements ofcomparison (GLA, condition, etc.)that are used to select the best substi-tutes for the subject within its definedcompetitive market.3. Analyze the area (defined in Step1) with the first screening filter(defined in Step 2) and review theresults.4. Complete a second screening of thedata and exclude the outliers.5. The resulting data collected fromthe two-step process becomes thedata used in the 1004MC analysis.6. In the report, include a summary ofall the data analyzed (most MLS sys-tems or 3rd party 1004mc productsare capable of this task) in the1004MC. These represent all thedata points considered relevant forthe assignment.

May 2013–©Appraisal Today–PAGE 11

Sample response to data outside ofthe competitive market area

"I have received your request for areconsideration and have reviewedthe data you provided me. I note thesales are all located outside of thesubject's competitive market area asdefined in the report. Please beadvised that the GSE guidelines andsigned-certification with the reportstates "I selected and used compara-ble sales that are locationally, physi-cally, and functionally the most simi-lar to the subject property." The salesand comparables analyzed in the1004MC are consistent with that cer-tification; the data supplied with thereconsideration is not. I thereforehave not reconsidered the originalanalysis or opinion of market value.Thank you."

PLEASE SEE THE LAST PAGE OFTHIS NEWSLETTER FORSAMPLE 1004MC

Sample response to data thatexceeds the elements of comparisonparameters

"I have received your request for areconsideration and have reviewedthe data you provided me. I note thatthe sales provided all exceed theparameters used in the 1004MC.

in the 1004MC search. If this is thecase, it is up to the appraiser to stateif there is a reason to re-analyze thevalue and give the offered data pointssome consideration in the analysis, orto state that it has already been con-sidered, but is not superior to thecomparables selected for comparisonpurposes within the grid.D. The appraiser missed a data pointand it does fit the parameters (thishappens); in this case, a reconsidera-tion process is warranted (and thatmay result in a change of the valueopinion).

Response to the clientAs discussed, unwarranted recon-

sideration requests can be burden-some, waste time and resources, andgenerally impair the appraiser's pro-ductivity. If an appraiser follows theprocess outlined in this article, manyunwarranted responses can be dealtwith quickly, efficiently, and in amanner that maintains a proper busi-ness rapport with the client.

Below are some response examples.

7. It is important to include the searchparameter in the report (the space isavailable to include this in the1004MC form itself). This is neces-sary to communicate to the clientwhat elements are necessary (size-range, condition, bed/bath count, etc.)for a sale to be considered a compara-ble.

The final step is to evaluate thereconsideration data with the originalprocess outlined above. The data sup-plied with the reconsideration requestis either part of the original data setanalyzed or it is not part of that set.There can only be four reasons whynew data provided by the client hasnot already been considered:A. It is not within the defined com-petitive market area; if there is suffi-cient data within the competitive mar-ket area to consider, there is no needto consider outside data; regardless ifit is in a competing market or not. Itis not necessary and can be arguednot appropriate to consider.B. It does not fall within the identi-fied elements of comparison. It is notappropriate to consider because it isnot a comparable (as defined by theappraiser in the original report by pro-viding the parameter criteria).C. It is included in the data contained

Text for image above:Cite sources for above information:MLS subject’s defined competitve market area, detached homes, GLA - 1,1650, outliers excluded----------------------------------------------------------------------------------------------------------------------------------Text for image below: Certification 7:I selected and used comparable sales that are locationally, physically, and funtionally the mostsimilar to the subject property.

Appraisal TodayISSN 1066–3900

Appraisal Today is published 12 times per year by Real Estate Communication Resources.

Subscription rate: $99 per year, $169 - 2 yearsPublisher

Ann O'Rourke, MAI, SRA, [email protected]

Subscriber ServicesTheresa Lua

M,T,W 7AM to noonFriday 7AM to 9 AM (Pacific time)[email protected] (24 x 7)

CirculationHancock Mailing Service

Editorial and Subscription Offices2033 Clement Ave., Suite 105

Alameda, CA 94501 Phone: 1-800-839-0227Fax: 1–800–839–0014

Email: [email protected]

Appraisal Today is sold with the understanding that the publisher,editors, and others associated with the publication are not engagedin rendering accounting, legal, or other professional services. Itdoes not attempt to offer specific solutions to individual problems.Questions about specific issues should be referred to the appropri-ate professional for analysis. ©2013 by Real Estate Communication Resources. All rightsreserved. The contents of this publication may not be reproducedeither whole or in part without consent.

PAGE 12–©Appraisal Today–May 2013

Those parameters (the significant ele-ments of comparison) are necessaryin order to be compliant with the fol-lowing GSE guidelines and thesigned-certification that states, "Iselected and used comparable salesthat are locationally, physically, andfunctionally the most similar to thesubject property." The sales and com-parables analyzed in the 1004MC areconsistent with that certification; thedata supplied with the reconsidera-tion is not. For example, the sale on123 Main St you provided is 40%larger in GLA vs. the subject; thecomparables used in the grid are allwithin 20% of the subject's size andshare the same buyer pool. I thereforehave not reconsidered the originalanalysis or opinion of market value.Thank you."

Sample response to data that isincluded in the 1004MC Analysis,but not used in the grid

"I have received your request for a

MBA Loan Volume Application Index – 11/11 to 4/13

Market Index Base = 100 in 1990

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

1600.0

Nov-11

Dec-11

Jan-12

Feb-12

Mar-12

Apr-12

May-12

Jun-12

Jul-12

Aug-12

Sep-12

Oct-12

Nov-12

Dec-12

Jan-13

Feb-13

reconsideration and have reviewed thedata you provided me. I did considerthe sales you have provided and theyare included in the "summary of sales"attachment for the 1004MC analysis.However, I did not consider it superiorto the sales used in the grid due to X,Y, and Z reasons. While the sales youprovided are sufficiently similar to thesubject to be considered and evaluat-ed, they are not superior in similarityto the subject as are the comparablesused in the grid. Please be advisedthat the GSE guidelines and signed-certification with the report states "Iselected and used comparable salesthat are locationally, physically, andfunctionally the most similar to thesubject property." The comparablesthat were selected and used in thesales grid are the most similar to thesubject based on my analysis. Thedata you have supplied was previouslyconsidered, and upon a re-review, areagain considered inferior to the com-parables in the grid. Therefore, I havenot reconsidered the original analysisor opinion of market value. Thankyou."

SummaryReconsiderations of value are

part of the residential mortgagelending and appraisal process. Theyare allowed by law (Dodd-Frank),regulation, GSE process, andrequired by many clients in theirengagement-agreements.

Reconsiderations that involveappropriate data serve a legitimatepurpose.

Reconsiderations that involveinappropriate data can be time con-suming to respond to and take upvaluable resources.

The existing appraisal develop-ment and communication process,if used to its potential, can assistthe appraiser in addressing in aquick, easy, and impartial mannermany inappropriate requests.

Adequately and appropriatelydefining the subject's neighborhoodand competitive market allows theappraiser to exclude reconsiderationdata quickly and easily due to loca-tion.

PAGE 13–©Appraisal Today–February 2013

Adequately and appropriatelydefining the significant elements ofcomparison in the comparable selec-tion process (and reporting them inthe 1004MC) allows the appraiser toexclude reconsideration data quicklyand easily due to the dissimilaritiesin physical or functional attributesthat drive market-participant deci-sions.

Screening the 1004MC a secondtime to eliminate outliers ensures thatthe final data set are those compara-bles that are most similar to the sub-ject and meet the requirement ofCertification #7: I selected and usedcomparable sales that are locational-ly, physically, and functionally themost similar to the subject property.

Once the above is done, then it iseasy and simple to address unwar-ranted requests in a manner that isnon-confrontational, professional,and consistent with the appraiser'srole as being an impartial, objective,and independent valuation expert thatthe client and all stakeholders canrely upon to produce credible assign-ment results.

About the authorFor lots more info, see the April

issue of Appraosal Today, whichprofled Denis. A very interestingstory!!

Denis DeSaix is a CertifiedResidential Appraiser with over 18years of real property valuation andconsulting experience. Mr. DeSaix'sareas of expertise include complexresidential and commercialproperties, mortgage and forensicreview work for attorneys andlenders, and estate and portfoliovaluation for accountants and thegeneral public.

Mr. DeSaix has been qualified asan expert witness for litigation andhas testified on valuation issues incourt. Mr. DeSaix earned hisBachelor of Science degree inFinance and graduated with honorsfrom the University of Phoenix, is amember of the Appraisal Institute ®(non-designated member), and is cur-rently on a dual-track candidacy forhis SRA and MAI designations. Mr.DeSaix is a proud veteran of theUnited States Marine Corps.

Contact information: www.metro-calappraisal.com

Search Criteria:Class=RE,LL,MH,RI,LR,MU,BO,IS,IL,CL

Market Conditions Addendum Report(Fannie Mae Form 1004MC)

(Freddie Mac Form 71)Date Run: 3/20/2013

Base/List Date/Current: 3/19/2013Inventory Analysis Prior 7 - 12 Months Prior 4 - 6 Months Current - 3 Months

Total # of Comparable Sales (Settled) 7 6 3

Absorption Rate (Total Sales/Months) 1.17 2 1

Total # of Comparable Active Listings 4 1 1

Months of Housing Supply (Total Listings/Ab.Rate) 3.43 0.50 1

Median Sale & ListPrice, DOM, Sale/List% Prior 7 - 12 Months Prior 4 - 6 Months Current - 3 Months

Median Comparable Sale Price $394,000.00 $420,000.00 $451,000.00

Median Comparable Sales Days on Market 14 15 6

Median Comparable List Price $391,500.00 $409,475.00 $459,000.00

Median Comparable Listings Days on Market 15 12 6

Median Sale Price as % of List Price 101.38% 100.63% 100.00%

MLS Number Status Address List Date Sold Date DOM List Price Sold Price %Sold/List

40572978 Withdrawn 4485 Juneberry 4/22/2012 28 $459,000

40607164 Active 4491 SILVERBERRY CT 3/15/2013 5 $459,000

40605481 Pending 5095 Murchio Drive 3/1/2013 6 $425,000

40586155 Pending 1208 Pinecrest Dr 7/19/2012 0 $425,000

40605688 Pending 4359 BLENHEIM WAY 3/4/2013 7 $447,500

40606409 Pending 4413 Marsh Elder Ct 3/10/2013 7 $469,000

40602319 Pending 1372 SAINT CATHERINE CT 2/1/2013 15 $469,990

40572809 Sold 4453 BIRCH BARK RD 5/4/2012 5/30/2012 5 $349,000 $351,000 100.57%

40576330 Sold 5198 Garaventa Dr 6/1/2012 9/4/2012 34 $369,900 $375,000 101.38%

40574372 Sold 4339 FALLBROOK RD 4/26/2012 6/29/2012 29 $376,000 $397,000 105.59%

40568028 Sold 4344 CHELSEA WAY 3/30/2012 5/8/2012 5 $380,000 $400,000 105.26%

40585891 Sold 5101 Garaventa Dr 8/8/2012 11/1/2012 23 $385,000 $385,000 100.00%

40577599 Sold 1393 MOSSY CT 6/10/2012 7/26/2012 14 $385,000 $394,000 102.34%

40598044 Sold 4399 N Canoe Birch Court 12/11/2012 12/30/2012 6 $389,000 $451,000 115.94%

40590994 Sold 4403 SUGAR MAPLE CT 9/28/2012 11/5/2012 8 $390,000 $440,000 112.82%

40570450 Sold 1227 BLUEJAY CT 4/18/2012 6/14/2012 7 $399,000 $400,000 100.25%

40590973 Sold 5342 Lightwood Drive 9/17/2012 11/16/2012 23 $399,950 $405,000 101.26%

40580789 Sold 4485 Juneberry Ct. 7/8/2012 8/16/2012 17 $409,900 $390,000 95.15%

40597145 Sold 1417 Parkland Dr. 11/30/2012 1/16/2013 16 $419,000 $410,000 97.85%

40593453 Sold 5025 St Garrett 10/19/2012 11/28/2012 2 $429,000 $435,000 101.40%

40596608 Sold 4414 SPOONWOOD CT 7/21/2012 11/16/2012 86 $450,000 $435,000 96.67%

40600100 Sold 4483 STONE CANYON CT 1/11/2013 3/1/2013 5 $465,000 $465,000 100.00%

40577241 Sold 4985 Murchio Drive 6/8/2012 9/20/2012 6 $398,000 $398,000 100.00%

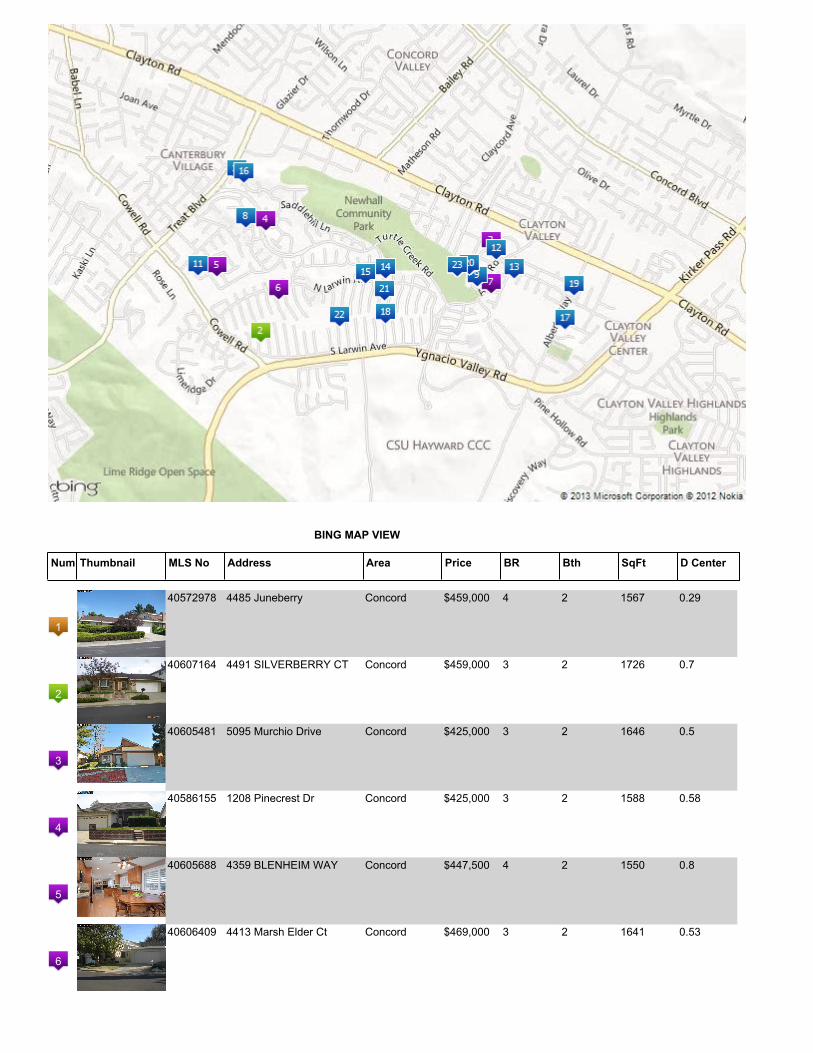

BING MAP VIEW

Num Thumbnail MLS No Address Area Price BR Bth SqFt D Center

1

40572978 4485 Juneberry Concord $459,000 4 2 1567 0.29

2

40607164 4491 SILVERBERRY CT Concord $459,000 3 2 1726 0.7

3

40605481 5095 Murchio Drive Concord $425,000 3 2 1646 0.5

4

40586155 1208 Pinecrest Dr Concord $425,000 3 2 1588 0.58

5

40605688 4359 BLENHEIM WAY Concord $447,500 4 2 1550 0.8

6

40606409 4413 Marsh Elder Ct Concord $469,000 3 2 1641 0.53

7

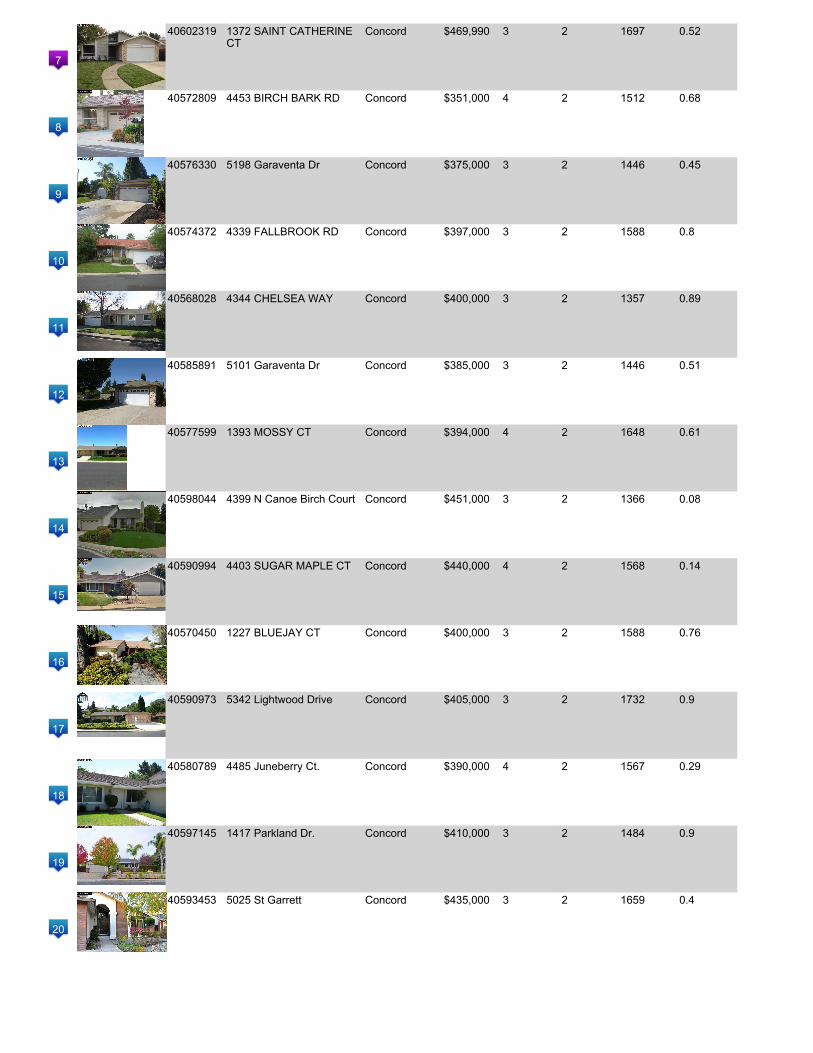

40602319 1372 SAINT CATHERINECT

Concord $469,990 3 2 1697 0.52

8

40572809 4453 BIRCH BARK RD Concord $351,000 4 2 1512 0.68

9

40576330 5198 Garaventa Dr Concord $375,000 3 2 1446 0.45

10

40574372 4339 FALLBROOK RD Concord $397,000 3 2 1588 0.8

11

40568028 4344 CHELSEA WAY Concord $400,000 3 2 1357 0.89

12

40585891 5101 Garaventa Dr Concord $385,000 3 2 1446 0.51

13

40577599 1393 MOSSY CT Concord $394,000 4 2 1648 0.61

14

40598044 4399 N Canoe Birch Court Concord $451,000 3 2 1366 0.08

15

40590994 4403 SUGAR MAPLE CT Concord $440,000 4 2 1568 0.14

16

40570450 1227 BLUEJAY CT Concord $400,000 3 2 1588 0.76

17

40590973 5342 Lightwood Drive Concord $405,000 3 2 1732 0.9

18

40580789 4485 Juneberry Ct. Concord $390,000 4 2 1567 0.29

19

40597145 1417 Parkland Dr. Concord $410,000 3 2 1484 0.9

20

40593453 5025 St Garrett Concord $435,000 3 2 1659 0.4

21

40596608 4414 SPOONWOOD CT Concord $435,000 4 2 1607 0.18

22

40600100 4483 STONE CANYON CT Concord $465,000 3 2 1367 0.38

23

40577241 4985 Murchio Drive Concord $398,000 3 2 1697 0.34

© 2013 BEAR, CCAR, EBRD. This information is deemed reliable, but not verified or guaranteed.