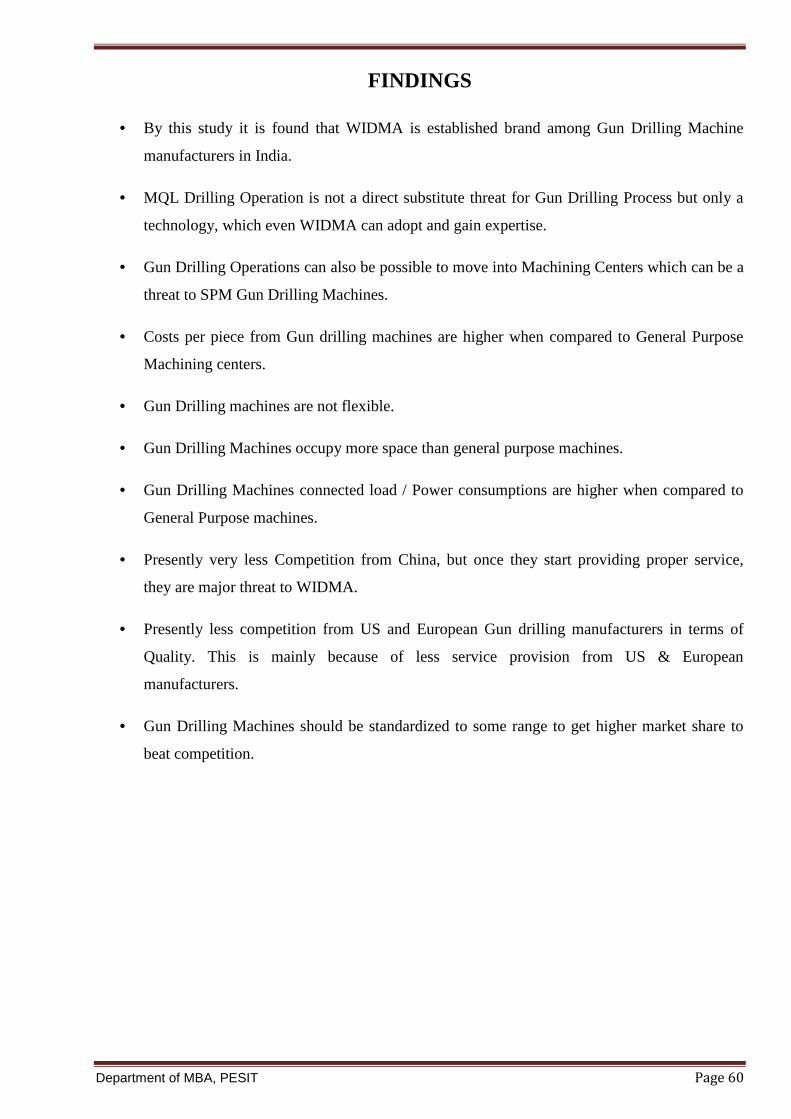

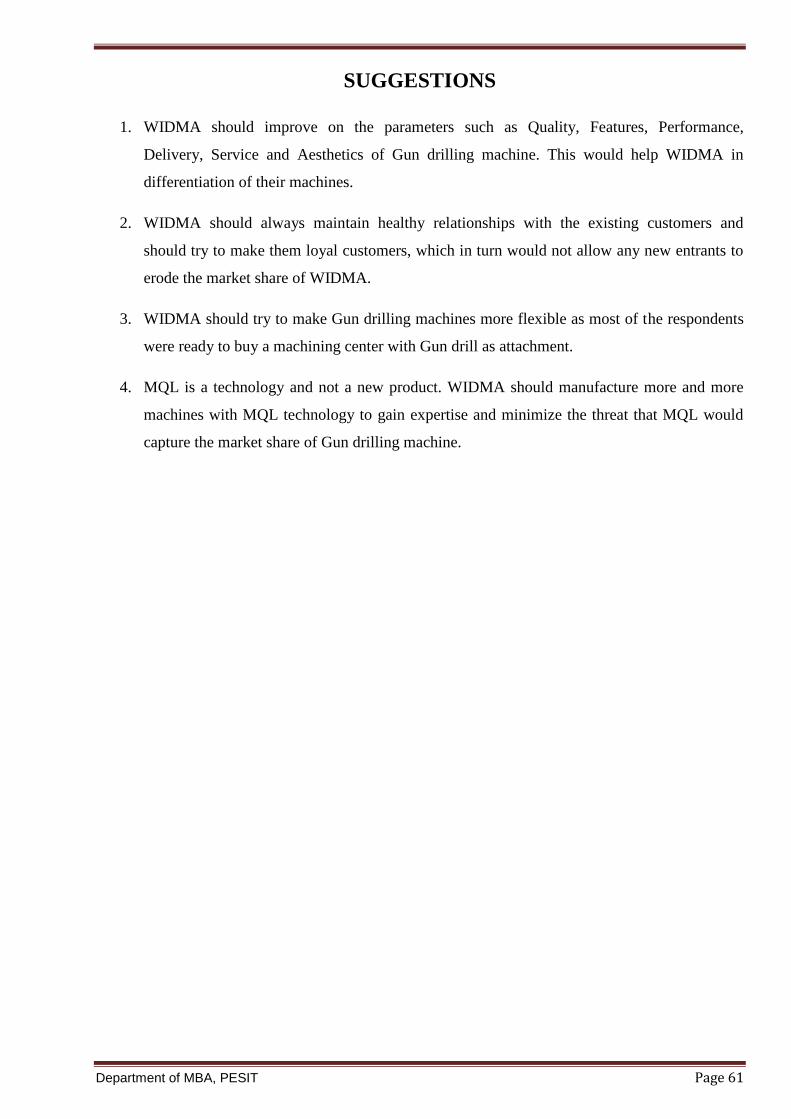

project report-porters five force analysis of gdm

DESCRIPTION

five force porters analysisTRANSCRIPT

Department of MBA, PESIT Page 1

EXECUTIVE SUMMARY

The research titled “PORTER’S FIVE FORCE MODEL ANALYSIS OF WIDMA GUN DRILLING

MACHINE” is undertaken to analyze the threats from substitutes as well as new entrants and

competition among the Gun Drilling Machine manufacturers. This study also analyses the bargaining

power of customer and the vendor.

To accomplish the task, a survey was carried out among the users and non-users of WIDMA gun

drilling machine with a sample size of 65 respondents based on convenience sampling. This was

done by means of online questionnaire which was sent to the respondents by email. The data so

collected was analysed by both percentages and statistical method.

The survey was conducted using the online market research website, in which questionnaire was

prepared as per the requirement. This website was even used to send the questionnaire to the selected

respondents and also remind the respondent about the survey, so that they can respond whenever

they were free.

This study gives a bird’s eye view of the WIDMA Gun drilling machine and important concepts

which are related to the performance and future prospect of the machine among the users and non-

users.

This report will help Kennametal - Machining Solution Group to evaluate their product. This will act

as a tool for the company to know their opportunities and threats in the market. This report will also

help the company to take right decision and steps for its better sales and service and also make

strategies to face the competition by other players in the industry.

Department of MBA, PESIT Page 2

INDUSTRY PROFILE

OVERVIEW

India ranks 17th in production and 12th in the consumption of machine tools in the world. The country

is set to become a key player in the global machine tools industry and is likely to see substantial high

end machine tool manufacturing, even as China keeps its lead in lower end volumes. Several firms

have entered the Indian machine tools sector, or announced plans for joint ventures or wholly owned

subsidiaries in India.

Machine tools – a strategic industry, forms the backbone of many if not most of the major sectors of

industrial activity in a country in the traditional manufacturing context. Therefore, a country such as

India which is on the threshold of becoming a major global industrial and economic power must have

a strong, well-developed, robust and modern machine tool industry to support and assist its

manufacturing sector.

In India, the machine tool industry supports the strategic development and growth of the automotive,

the white and brown goods, the capital goods industries as well as strategic sectors such as defense,

railways, aerospace, etc. Machine tools also contribute to the vibrancy of small and medium scale

manufacturing industries, in particular, the millions of job shops in the country.

In India, the Rs.17 billion machine tool industry supports more than Rs. 2,000 billion manufacturing

sector in the country. The Indian machine tool industry predominantly comprises manufacturers from

the small and medium-sized enterprises. There are about 150 major manufacturers in the organised

sector. About three-quarters of total machine tool production in the country comes out of ISO

certified companies that are involved in manufacturing of metalworking machine tools,

manufacturing solutions, accessories, and cutting tools & tooling systems.

Historical Backdrop

This sector has had a long history of growth in India, beginning in the 1940s. From early 1950s to

mid-1970s, the machine tools industry evolved under an umbrella of protection in which the growth

was based on import substitution. The Government of India set up the Hindustan Machine Tools

(HMT), which provided a nucleus for development of technological capabilities and skills. It also

spearheaded sprouting of several ancillary units in the private sector by providing support and thus

became local suppliers of components, etc.

Department of MBA, PESIT Page 3

During the 1950s to mid-1960s, this sector bolstered in confidence and began to absorb imported

technology and manufacture machine tools to specifications given by foreign collaborators. It also

initiated developmental work directed to modifying machine tools and developing variants of

machines for which design had been acquired by the purchase of licenses.

In the 1980s, the industry developed further and was able to acquire know-how in machine tool

technology in order to reproduce and even develop new machine tools, particularly special purpose

machine tools (SPMs). The national expertise developed over the years provided the needed human

resources to initiate creative modified versions of existing machine tools manufactured under license,

thereby further paving the way towards self-reliance through aggressive R&D in India.

As a result of the various initiations, output of the Indian machine tool industry, witnessed a steep

rise from Rs. 290 million in 1970-71 to Rs. 1,185 million a decade later. And by the time of the

economic liberalisation in 1990-91, turnover of the industry touched a new high of Rs. 4,135 million.

Indian machine tool industry was among the first industry sectors to be thrown open to global

competition in the economic reforms of the early Nineties. That, however, did not deter the industry,

to face the onslaught challenges – and towards this direction improved features of their machines,

enhanced productivity, increased reliability and performances, and embraced TQM practices. Efforts

of domestic machine tool manufacturers made a paradigm shift that led to a manifold increase in

performance.

The spurt in the country’s manufacturing activity since 2003-04 led to increased potential for Indian

machine tools, which got a boost from the automotive sector. The booming automotive and auto

ancillary industry in India is currently driving growth and the competitiveness of the Indian machine

tool industry. Domestic manufacturers are fulfilling stringent tolerances, and process capability

requirements of the highly demanding auto industries. The focuses of several Indian manufacturers

currently provide machine tools with integrated Total Productive Maintenance (TPM) features. This

has increased the potential and improved the competitiveness of Indian-built machine tools.

The strength of the Indian machine tool industry was galvanised by Indian Machine Tool

Manufacturers’ Association (IMTMA) – the apex industry body of machine tool and manufacturing

solutions, which currently represents over 80 per cent of the machine tool industry in India. With a

membership of over 350 small, medium and large companies, IMTMA is the single point of contact

for the machine tool industry in India.

While the Indian machine tool industry takes determined steps to support its users and customer

through a range of value-adding initiatives, along with a greater emphasis on R&D activities.

Department of MBA, PESIT Page 4

Simultaneously it has initiated steps to develop mechanisms to protect and provide market

exclusivity, in domestic and international markets, for locally developed innovations and/or new and

improved product and processes.

Industry Strengths

The machine tool industry in India is recognised for:

• Capability to manufacture low-cost, highly productive manufacturing solutions, especially

customised products, for Indian and overseas users – in the range of turning centers, machining

centers, and grinding machines.

• Consistent attempt to transform the industry to become more productive, more efficient, and, above

all, much more cost competitive. Products offered by the Indian machine tool industry today are

priced much lower than earlier.

• Strong emphasise towards improvement of quality. Over 75 per cent of the total production of the

industry comes from ISO certified and CE accredited manufacturers.

• Engineering expertise on design, CAD, documentation, testing and evaluation. Most machine tools

manufactured in India are indigenously designed.

• Pool of skilled workforce specialising in assembly, design, and software development, as well as in

efforts to further strengthen their design and innovative skills.

• Forging backward integration with sub-suppliers and vendors for greater standardisation of

components and assemblies.

• Proactive efforts to reach out to customers through process of interactive dialogues – at the industry

and at the individual company levels.

• Special focus on increasing reach of the industry to other potential overseas markets. The machine

tool industry is making special forays to establish presence in key machine tool markets – through

joint participation in overseas fairs, as well as establishment of exclusive machine tool show centers.

As a result, Indian machine tools are today well accepted in China, Germany, Italy, France and North

America.

Department of MBA, PESIT Page 5

Core Competency

The Indian machine tool industry manufactures almost the complete range of metal-cutting and

metal-forming machine tools. Customised in nature, the products from India comprise conventional

machine tools as well as computer numerically controlled (CNC) machines. There are other variants

offered by Indian manufacturers too, including special purpose machines, robotics, handling systems,

and TPM-friendly machines.

One of the significant developments in machine tool industry in recent times has been the Computer

Numerically Controlled (CNC) machines. Emergence of CNC machine tools and its dominance over

the last few years in the overall product segment stemmed from its value-added features, such as

enhanced productivity, higher precision, increased reliability, better finishing, and improved

aesthetics and design. Achievement of higher growth and increased share of CNC machines in the

overall output surmises the commitment of Indian machine tool manufacturers to providing

competitive manufacturing solutions, now at cost effective prices.

In terms of key product segments, high growth areas for the Indian machine tool industry include

turning centers, machining centers, grinding machines, and cell manufacturing, amongst others. The

other emerging demand is for total manufacturing solutions, whereby users seek to economise on

manufacturing cost and time.

Current Scenario

The auto sector accounts for 60% of machine tool demand in the country. Auto Component

Manufacturers Association (ACMA) estimates India will sell 2.7 million cars, 12.5 million two

wheelers and 0.5 million commercial vehicles (CVs) in 2010-11. This will grow exponentially to 10

million cars, 30 million two wheelers and 2.2 million CVs by 2020. This means that auto component

manufacturers will have to invest $2 billion every year, and machine tool operators in the country

will have to ramp up capacity by 7-8 times to meet that demand.

The local machine tool players do not have the financial wherewithal to make such levels of

investments. Around 60% of the sector consists of small unorganized players. The remaining 40%

includes bigger organized players like HMT, Kennametal (MSG), Premier and Ace Micromatic. The

current size of the machine tool industry stands at Rs 9,000 crore and IMTMA forecasts this to

increase to Rs 23,000 cr. by 2020.

Department of MBA, PESIT Page 6

COMPANY PROFILE

A. BACKGROUND AND INCEPTION OF THE COMPANY

Innovation, perseverance and close attention to customer needs have characterized Kennametal since

its founding. In 1938, after years of research, metallurgist Philip M. McKenna created a tungsten-

titanium carbide alloy for cutting tools that provided a productivity breakthrough in the machining of

steel. "Kennametal®" tools cut faster and lasted longer, and thereby facilitated metalworking in

products from automobiles to airliners to machinery. With his invention, Philip started the McKenna

Metals Company in Latrobe, Pennsylvania. Later renamed Kennametal, the corporation has become

a world leader in the metalworking industry and remains headquartered in Latrobe.

Kennametal developed an international presence from the start. Philip sold early patent rights to

British industrialists who later also began Kennametal of Canada. Exports through the company's

first five years totaled more than $2.5 million, and by 1955 Kennametal had representation in 19

countries. The company's overseas manufacturing started in 1957 with a joint venture in Italy. A

joint venture in the United Kingdom and a German sales subsidiary soon followed. Between 1972

and 1981, foreign sales grew from 17 to 34 percent of the total.

McKenna Metal's first full-year sales, with a staff of 12 employees, totaled some $30,000. But World

War II saw American heavy industry shift into high gear. Kennametal's annual sales approached $10

million and employment was nearly 900 as the company's tools were used extensively in the war-

time economy.

In 1993, Kennametal acquired Hertel AG, a tooling systems manufacturer headquartered in Fürth,

Germany, with operations throughout Europe and worldwide. This enabled the corporation to

compete more effectively in Western Europe, gain better access to emerging markets in Eastern

Europe, and offer additional product lines in Asia Pacific. The Asia Pacific effort was further

expanded to include manufacturing joint ventures for mining tools in China and a metalworking tool

manufacturing plant in Shanghai. In 2002, Kennametal acquired Widia, a leading manufacturer and

marketer of metalworking tools in Europe and India which was incorporated in India in the year

1964.

Department of MBA, PESIT Page 7

A Technological Leader

Kennametal was founded on the strength of a technological breakthrough, and a list of highlights

demonstrates that it has continued to lead its industry in innovation.

In 1946, the company introduced the Kendex line of mechanically held, index able insert

systems that accelerated tool changing and increased machining precision.

Kennametal's unique, patented Thermite process for producing impact-resistant macro

crystalline tungsten carbide today remains the best way to produce extremely tough tool

materials for demanding applications such as mining.

In 1964, Kennametal introduced tungsten-carbide-tipped Ken grip tire studs. Although studs

clearly contributed to safe winter travel, they became controversial amid speculation about

their role in road deterioration. After legislation limited the use of carbide studs, Kennametal

left the business in 1977.

Leader in the development of silicon-nitride based "Sialon" ceramics for the machining of

exotic aerospace materials.

First to develop cobalt-enriched substrates for coated inserts was first to commercially

introduce physical-vapor-deposition (PVD) coated cemented carbide cutting tools and

created the first commercially viable diamond-coated carbide inserts.

Leader in the development of quick-change tooling systems that today lead the world in

versatility, speed and accuracy.

Kennametal maintains its technological leadership through its $30-million Technology Center at its

world and North America headquarters in Latrobe, Pennsylvania, and complementary facilities in

various locations around the globe. The facilities are dedicated to rapid development of products

engineered to meet specific customer requirements.

Department of MBA, PESIT Page 8

B. NATURE OF THE BUSINESS CARRIED

Kennametal India Ltd carries out its business strategically in three segments:

I. Metalworking Solutions & Services Group (MSSG)

II. Advanced Materials Solutions Group (AMSG)

III. Machining Solution Group (MSG)

I. Metalworking Solutions & Services Group (MSSG) segment:

In the MSSG segment, the company provides consumable metal cutting tools and tooling systems to

manufacturing companies in a range of industries throughout the world. Metal cutting operations

include turning, boring, threading, grooving, milling, and drilling. Its tooling systems consist of a

steel tool holder and cutting tools, such as index able inserts and drills made from cemented tungsten

carbides, ceramics, cermet’s or other hard materials. The company also provides solutions to its

customers’ metal cutting needs through engineering services. Engineering services include field sales

engineers identifying products and engineering product designs to serve customer needs.

The company serves various industries that cut and shape metal parts, including manufacturers of

automobiles, trucks, aerospace components, farm equipment, oil and gas drilling and processing

equipment, railroad, marine and power generation equipment, light and heavy machinery, appliances,

factory equipment, and metal components, as well as job shops and maintenance operations.

KENNAMETAL is the only major machine tool supplier in the country which offers both machine

and tooling solutions. It produces Special Purpose Machines which are customized products. It also

produces tool and cutter grinding machines. All the machines are designed with TPM and safety

measures.

II. Advanced Materials Solutions Group (AMSG) segment:

In the AMSG segment, the company’s principal business lines include the production and sale of

cemented tungsten carbide products used in mining, highway construction, and engineered

applications requiring wear and corrosion resistance, including compacts and other similar

applications. Additionally, the company manufactures and markets engineered components with a

proprietary metal cladding technology, as well as other hard materials that likewise provide wear

resistance and life extension of the target component. These products include radial bearings used for

directional drilling for oil and gas; extruder barrels used by plastics manufacturers, turbine blades,

burner tips and tubing used in power generation applications, food processors and numerous other

Department of MBA, PESIT Page 9

engineered components to service various industrial markets. It also provides metallurgical powders

to manufacturers of cemented tungsten carbide products, intermetallic composite ceramic powders

and parts used in the metalized film industry. The company also provides application-specific

component design services and on-site application support services. It provides its customers with

engineered component process technology and materials that focus on component deburring,

polishing, and producing controlled radii.

The company’s mining and construction tools include products fabricated from steel parts tipped

with cemented carbide, as well as wear resistant products made from steels and other hard materials.

Mining tools, used primarily in the coal industry, include long wall shearer and continuous miner

drums, blocks, conical bits, drills, pinning rods, augers, cladded products, wear pins, and a range of

mining tool accessories. Highway construction cutting tools include carbide-tipped bits for ditching,

trenching and road planning, grader blades for site preparation and routine roadbed control and

snowplow blades and shoes for winter road plowing. The company produces these products for mine

operators and suppliers, highway construction companies, municipal governments and manufacturers

of mining equipment.

The company's customers use engineered products in manufacturing or other operations where

extremes of abrasion, corrosion or impact require combinations of hardness or other toughness

afforded by cemented tungsten carbides, ceramics or other hard materials.

III Machining Solution Group (MSG) Segment:

In the MSG segment, the company’s principal business lines include the production and sale of

Special Purpose Machines (SPM) used mostly in Automobile industry. For over two and a half

decades, MSG has been leading the special purpose machine tool industry in India, elevating it to the

best global standards. MSG has state of the art manufacturing plant, they partner with customers

spanning diverse industries across the country and overseas. They count on MSG for high

performance, world class total machining solutions to manufacture their most critical components.

The Machining Solution group of Kennametal India provides end-to-end metal cutting solutions and

not just stand-alone machines. They offer customers an unmatched advantage by leveraging their

close association with world-renowned tooling brands and their access to a global application

database, besides their ability to design customized machines and tooling.

Department of MBA, PESIT Page 10

C. VISION, MISSION AND QUALITY POLICY

Vision:

The vision statement of Kennametal is as given below:

“To be recognized as a premier, customer-driven enterprise that delivers our promise of exceptional

value, growth and productivity solutions to our customers, consistent returns for shareholders, and

rewarding careers to employees”.

Mission:

“Kennametal delivers productivity to customers seeking peak performance in demanding

environments by providing innovative custom and standard wear-resistant solutions, enabled through

our advanced materials sciences, application knowledge, and commitment to a sustainable

environment.”

Quality Policy:

Promise of Kennametal: “Engineering your competitive edge”.

OPPERATIONAL EXCELLENCE: Kennametal’s systematic process of reducing and eliminating

waste in all its processes.

STRATEGIC PLANNING: Consistent development of long-term business strategy in alignment

with the company’s vision, key values, and ambitions.

INNOVATION: Stage-gated product development process for rapidly bringing world-leading new

products to market.

CUSTOMER EXCELLENCE: A process to continuously deliver the best economic value to

increase their customer’s competitiveness.

TALENT DEVELOPMENT: Kennametal’s process to manage and develop their workforce to be

highly competitive and performance driven.

PORTFOLIO MANAGEMENT: Guides an extremely disciplined approach to the identification,

closing, and integration of acquisition candidates and portfolio management of existing businesses.

Department of MBA, PESIT Page 11

D. PRODUCTS/ SERVICES PROFILE

There are five important products of MSG under the brand name WIDMA of Kennametal.

They are

1. Special Purpose Machine

The WIDMA range of Special Purpose Machines offer solutions covering all machining

operations: turning, milling and drilling including special operations like fine boring,

deep hole drilling, facing and centering etc. All WIDMA machines are designed to

maximize productivity, reduce cycle time and achieve optimal cost per component.

2. WIDMA Flex series

The WIDMA Flex family of machines is specially designed to help industry optimize

manufacturing. They are built on the Lean concept. It combines the versatility of a General

Purpose Machine with the productivity of a Special Purpose Machine. WIDMA Flex is

eminently adaptable to different applications. Standard Flex module, customized work

holding and various combinations of additional axes ensure high productivity.

Department of MBA, PESIT Page 12

3. Fixtures/ Tooling

To address the complex challenges in machining, one needs to have rich insights

into all the three major areas involved – The Machine, the Tooling and the Fixtures

– and how they interact. WIDMA manufactures this comprehensive and intensive

expertise to give its customers the most optimal integrated machining solutions for

their machining needs.

4. Ecogrind

The best choice for a wide variety of tools. Dedicated to the manufacturing and

regrinding of round tools in one setup. They are designed with well balanced &

optimum axes configuration, superior rigidity and adequate power. They ensure high

productivity and impeccable precision.

Department of MBA, PESIT Page 13

5. Special Vertical Turning Machines

Over 100 installations ,these uniquely designed machines answer the long-standing question

- “How can one maximize productivity and combine operations in a single set-up without

compromising on component quality?” From turning to more demanding turn-milling and

complex 5-face machining, the range covers all applications, are designed for rigidity and

optimization. They segment leading capacities, adequate spindle power and superior

precision, all within a compact footprint .They have FEA optimized design and machine

grade cast iron construction for vibration free long working life even in the most demanding

conditions.

The Services provided by Kennametal are:

• Wear Assessment

• Solution Design & Engineering

• Cladding Fabrication & Application

• Installation Support

• Ongoing Wear Monitoring & Consultation

Department of MBA, PESIT Page 14

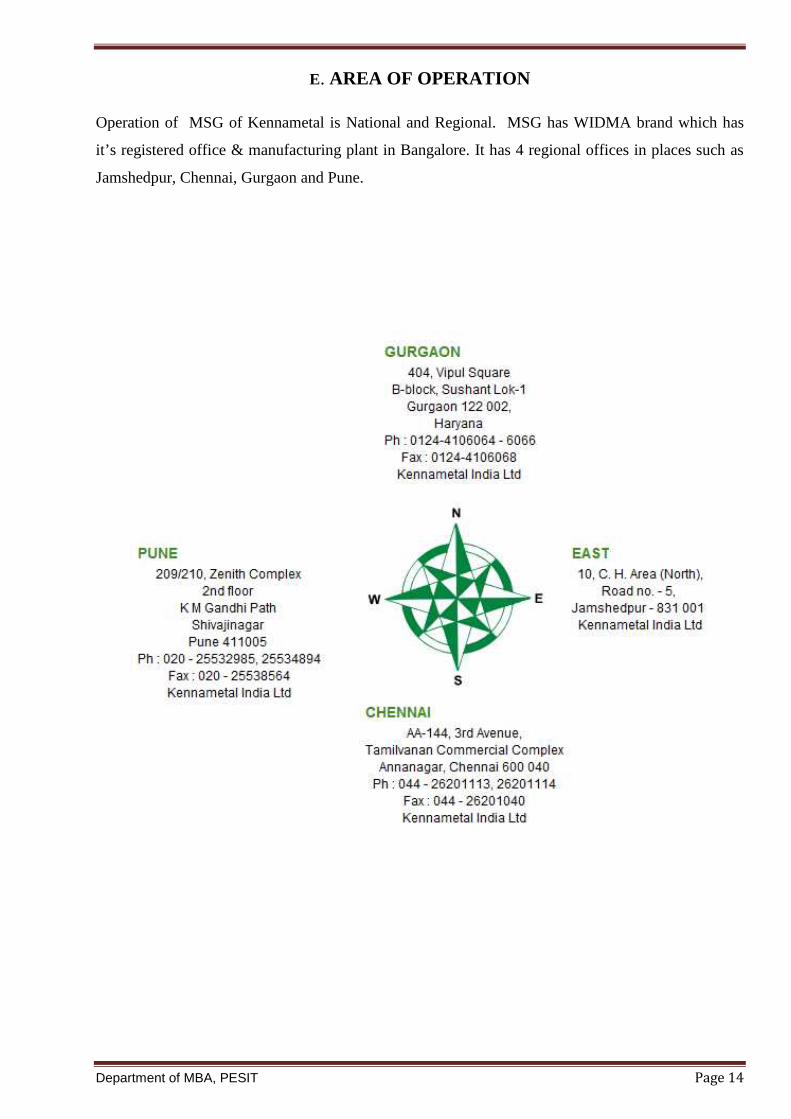

E. AREA OF OPERATION

Operation of MSG of Kennametal is National and Regional. MSG has WIDMA brand which has

it’s registered office & manufacturing plant in Bangalore. It has 4 regional offices in places such as

Jamshedpur, Chennai, Gurgaon and Pune.

Department of MBA, PESIT Page 15

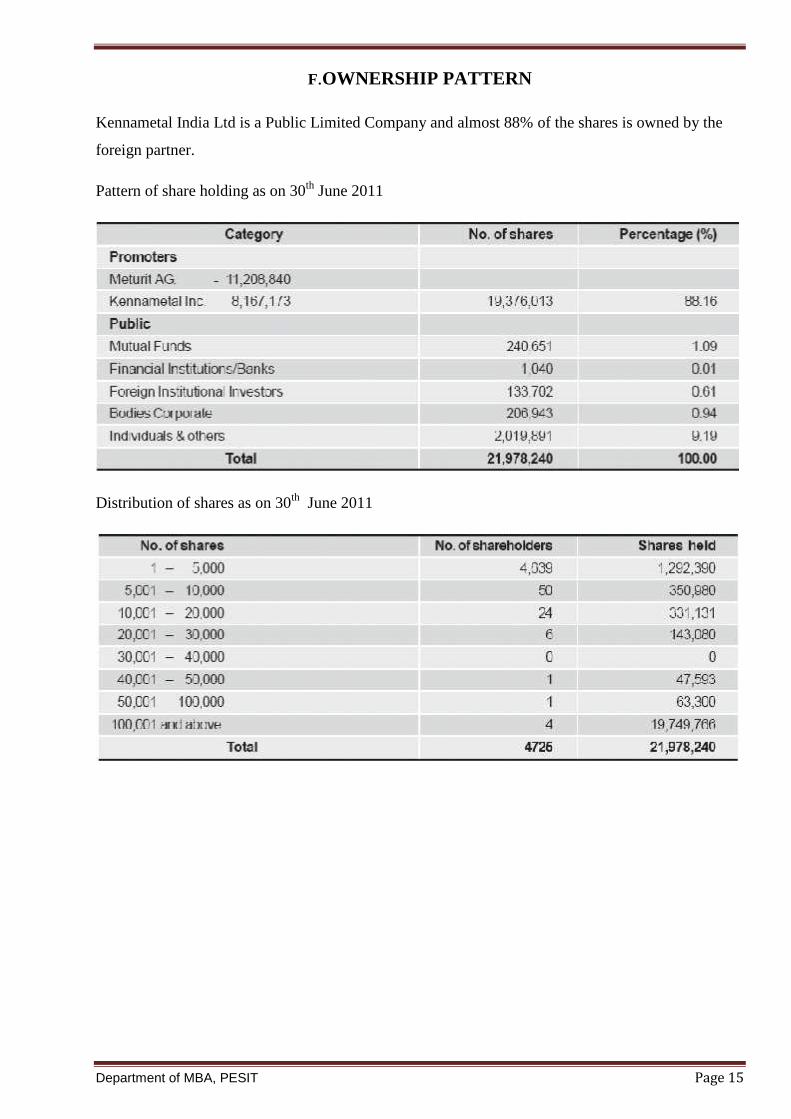

F.OWNERSHIP PATTERN

Kennametal India Ltd is a Public Limited Company and almost 88% of the shares is owned by the

foreign partner.

Pattern of share holding as on 30th June 2011

Distribution of shares as on 30th June 2011

Department of MBA, PESIT Page 16

G.INFRASTRUCTURAL FACILITIES

Machining Solution Group (MSG) - Kennametal India is an organization headquaterd at Bengaluru

of India. The Infrastructural Facilities available here are as follows.

MSG division of Kennametal India is equipped with large machine assembly area located in

Bengaluru.

MSG- Kennametal India has Kennametal Knowledge Center which conducts various

education/training courses to meet the training needs of the Industries.

MSG- Kennametal India has a Sales department, Supply Chain Department, Project

Management department and a dedicated Design center.

In addition to this it has a very good office infrastructure and IT infrastructure, Canteen

facility etc.

It also provides transportation facility to its employees.

Department of MBA, PESIT Page 17

H. ACHIEVEMENTS AND AWARDS

Some of the awards won by MSG of Kennametal India are as follows:

1. FI foundation award winner

For 6 Axis CNC Tool and cutter grainding machine WGS 6

2.IMTEX-92

For VALVE SEAT Generating and VALVE guide reaming machine

Kennametal India Ltd - Second best in Medium Scale Category in EHS Awards 2010

Customer Awards:

1. Honda Award

For Machine tools 2003-2004

2. Honda Award

For machinery 2004-2005

3. Honda Award

For QCDDM (Machinery) 2006-2007

4.FIE foundation award for best machine design.

4. Honda Award

For QCDDM (Machinery) 2010-2011

Department of MBA, PESIT Page 18

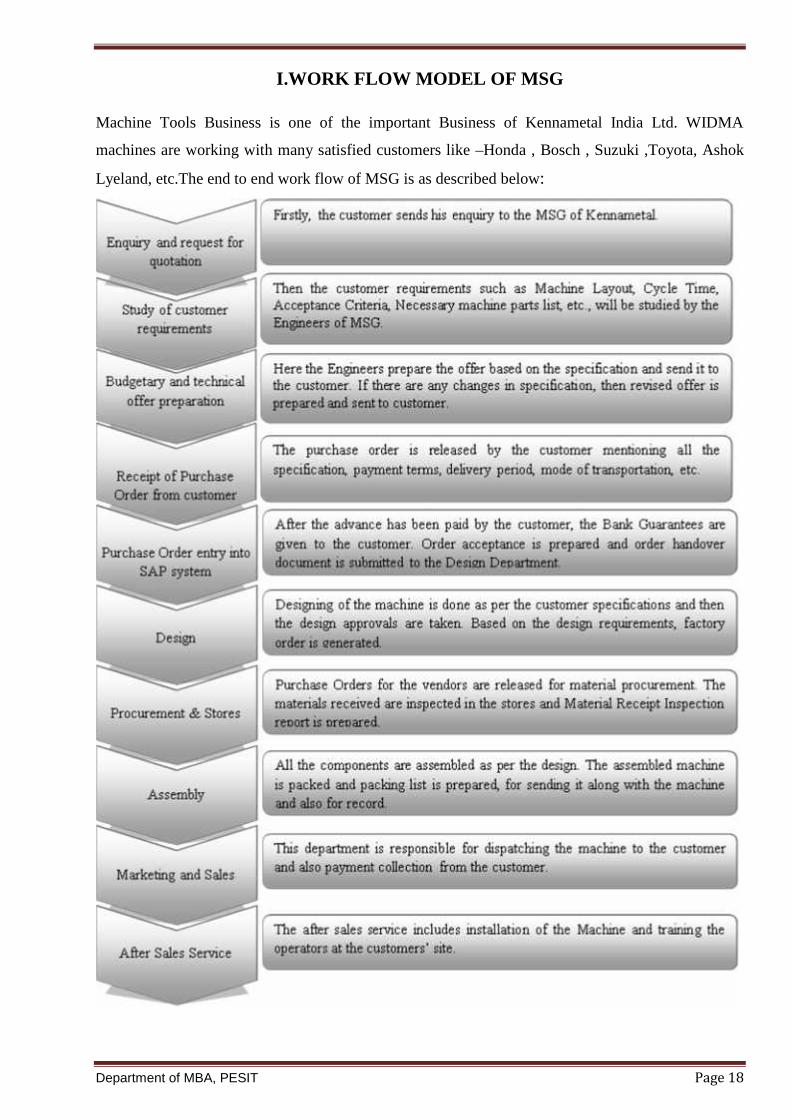

I.WORK FLOW MODEL OF MSG

Machine Tools Business is one of the important Business of Kennametal India Ltd. WIDMA

machines are working with many satisfied customers like –Honda , Bosch , Suzuki ,Toyota, Ashok

Lyeland, etc.The end to end work flow of MSG is as described below:

Department of MBA, PESIT Page 19

J. FUTURE GROWTH AND PROSPECTS

MSG- Kennametal India Limited has good infrastructure facility located in Bengaluru, which has

helped the company improve the quality of its products and has aggressive investment plan to

enhance capacity to meet increasing demand.

Department of MBA, PESIT Page 20

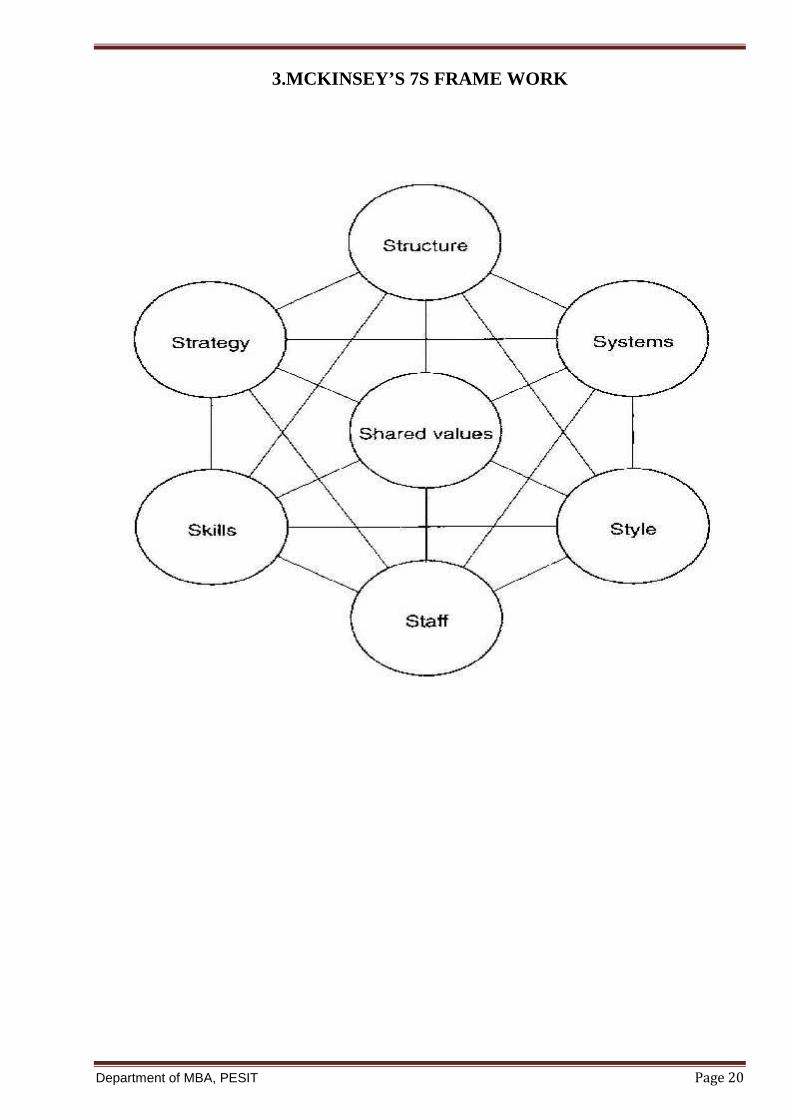

3.MCKINSEY’S 7S FRAME WORK

Department of MBA, PESIT Page 21

a. Shared Values of Kennametal:

The values of Kennametal is as shown in the below figure.

a.1 People

Kennametal’s talented global workforce is their number-one competitive advantage. It

aspires to be the employer of choice for the best people.Their sustainability programs,

designed to provide a safe and rewarding workplace,reflect the company’s commitment to

the highest levels of employee safety.

Kennametal’s comittment is to provide their people with the components of a great place

to work,such as:

• A safe work environment

• Career opportunities

• Opportunities to learn and grow

• Competitive Compensation

a.2 Environment

At the beginning of fiscal year 2008, Kennametal developed and launched the Protecting

Our Planet initiative. This program is designed to foster, recognize, and reward employee

achievement in the areas of energy and water conservation, waste reduction, and materials

recycling. It reflects Kennametal’s dedication to lead by example in protecting our planet

not just for this generation, but for many still to come.

Department of MBA, PESIT Page 22

They annually present Environmental Health and Safety Excellence awards to:

• Reward and recognize extraordinary efforts in EHS throughout the organization.

• Promote EHS awareness and involvement among all employees.

• Share best practices among all sites.

• Inspire EHS greatness throughout Kennametal.

The environmental initiatives are an integral part of their sustainability strategy, driving

business value while creating a better environment.

a.3 Innovation

At Kennametal, innovation is defined as the process of delivering ever increasing

business value to its customers. Innovation at Kennametal is not a function, it is a

business process that is customer driven and owned by all functions collectively.

The key metric of an innovative company such as Kennametal is the percentage of its

revenue generated from new product sales. An innovative company must be continually

bringing new products to market, and having them perform more successfully than the

products they replace.

a.4 Customer

As customers drive toward more sustainable productivity, they look to Kennametal for

innovative solutions that help them achieve their goals. In fact, in 2009 it began a total

reorganization of their company, making it more customer centric and market focused.

Helping customers meet their overall goals is clearly an objective of Kennametal’s

sustainability program. They focus on products that provide customers with lower fuel

costs, reduced packaging requirements, lower transportation costs, and improved product

performance.

a.5 Performance

Kennametal’s FY 2011 financial performance demonstrates the company’s ability to

operate effectively and profitably in a challenging global environment, and to be a top-tier

financial performer.

Department of MBA, PESIT Page 23

Kennametal delivered improved overall performance in spite of uncertain market

conditions. This was the result of careful planning and execution. Over the past few years,

Kennametal’s management team has consistently demonstrated both of these capabilities,

while redefining their business and positioning the company to perform in a sustainable

manner in virtually any operating environment.

a.6 Integrity

Kennametal is diligent in communicating the values of integrity throughout the entire

organization. The Kennametal Code of Conduct serves as the compass and bearings for

the company’s strong commitment to integrity, always doing the right thing, and doing

what they say they will do, every time.

b. Staff:

There are more than 500 employees who are working dedicatedly to meet the goals of the

organization. Customer Satisfaction and the organizational values are the motivators for

the employees of Kennametal. The organizational culture is such that there is no

difference between the employer and the employee. All the employees of the organization

are treated equally.

c. Strategy:

The Strategies of Kennametal India are as follows:

c.1 WIN THE CUSTOMER:

Earn a reputation as the most knowledgeable and easiest to do business with. Develop and

retain customers, and deliver enhanced productivity solutions. Become the recognized leaders in

customer loyalty, know-how and satisfaction, and increase our penetration into core markets and

existing customers.

Department of MBA, PESIT Page 24

c.2 ADVANCE WITH TECHNOLOGY:

Deliver market-leading advances, innovations and customer delivery systems that will

enhance our global competitiveness. Achieve product line renewal at an unparalleled pace. Make

today’s technological upgrades tomorrow’s tools for maintaining our advantage.

c.3 COMMIT TO EXCELLENCE:

Consistently deliver quality products and service solutions, on-time, and at record industry

lead times. Maximize Lean processing to achieve top-tier performance and companywide

financial excellence.

c.4 GROW FOR PROFIT:

Build and maintain a balanced portfolio of Products, Markets and Geographies- the “Thirds,”

and consistently grow our enterprise at twice the market rate. Achieve organic, inorganic and

emerging market growth with the focus on profitability and shareholder return.

c.5 ENSURE MISSION READINESS:

Acquire, train and manage talent for the challenges ahead, and be seen as the employer of

choice for the best people. Develop a flexible, effective and ever-ready team that can deliver

the best solutions faster and more accurately, and exceed customer expectations.

Department of MBA, PESIT Page 25

d. Structure:

Kennametal India Ltd follows product organization structure approach. Activities are

divided on the basis of individual product lines. The marketing, production, finance are

contained within each department. The organization also have a centralized finance and

Human Resource function. The organization structure is as shown.

Organization Structure of MSG - Kennametal India

Managing Director

Kennametal India Ltd.

Head - Finance,Legal

Head - HumanResource

Head - MetalForming

Head - MetalWorkingBusiness

Head- MachiningSolution Group

(MSG)

Special PurposeMachine

Flex series Fixtures /Tooling

Special VerticalTurning Machines

Ecogrind

DesignMarketing& Sales

Assembly After SalesService

SCM

Department of MBA, PESIT Page 26

e. Systems:

The following are the systems that are present in Kennametal for smooth working of the

organization.

ISO 9001 Certified system

ERP-SAP system for order booking and other process

Auto-CAD and other computer aided tools systems for designing of machines.

f. Style:

Kennametal is an Organization following a lean structure.

The managers follow the method of Management by Objectives in order to achieve the

organizational goals. Every morning a small meeting with the manager and subordinates

is done and all the activities for the day will be planned. The managers here acts as

leaders and not just as managers. They are not autocratic.

g. Skills :

Skills are the capabilities of the staff within the organisation. MSG- Kennametal India is

the largest manufacturer of Special Purpose Machines in India.The manufactures a entire

range of machines for 2- wheeler and 4- wheeler vehicles.The company’s skill lies in

product design, mechanical engineering, electrical engineering, quality engineering &

production engineering.

Department of MBA, PESIT Page 27

4 .SWOT ANALYSIS

Strengths

1. Existence in market since long time.

2. Large customer base.

3. Qualified & well trained employees.

4. Diversified product portfolio.

5. Good infrastructure.

Weekness

1. Less focus on SME’s.

2. Availability of flexible capacity is less to meet the unexpected demands.

3. Deteriorating delivery commitments.

Opportunities

1. Good scope for selling the SPMs in international market.

2. Very few SPM manufacturers in the country, can focus on customers of non-

automobile sector.

3. Can focus on number of SME’s.

4. Very few domestic competitors

Threats

1. Too much dependancy on automobile sector for selling of SPMs.

2. Entry of low cost Chinese SPMs into Indian market.

Department of MBA, PESIT Page 28

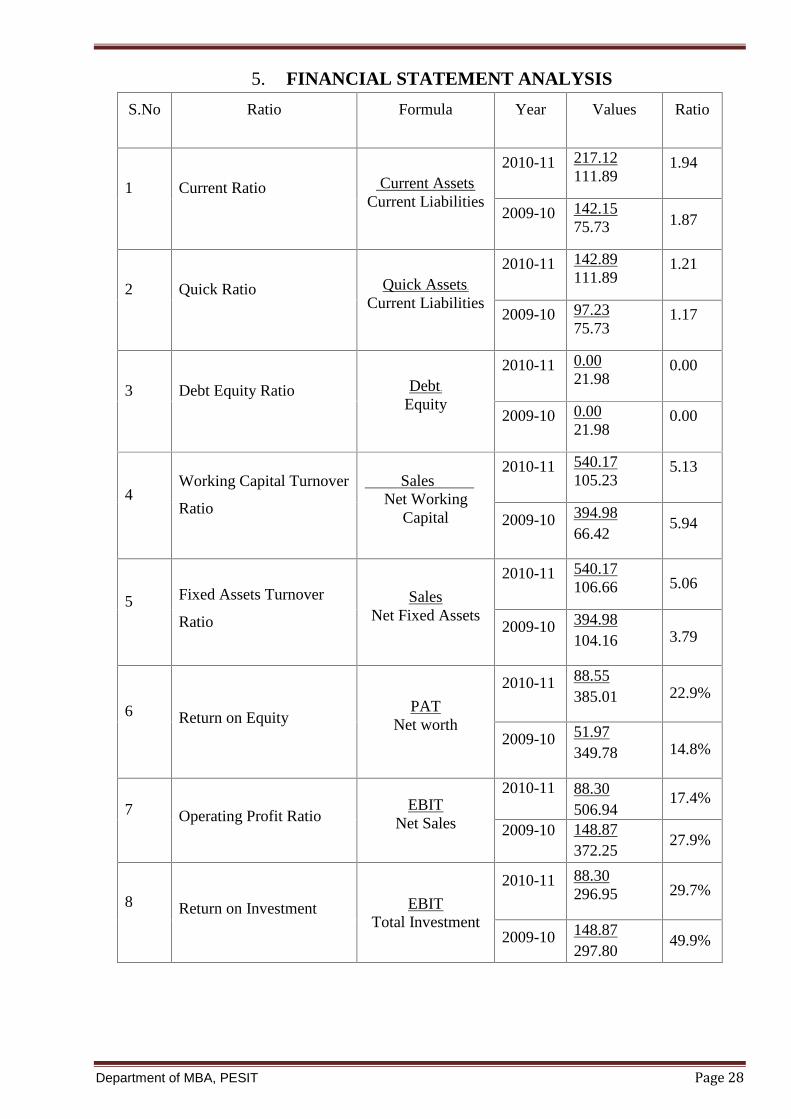

5. FINANCIAL STATEMENT ANALYSIS

S.No Ratio Formula Year Values Ratio

1 Current Ratio Current Assets.

Current Liabilities

2010-11 217.12111.89

1.94

2009-10 142.1575.73 1.87

2 Quick Ratio Quick Assets.

Current Liabilities

2010-11 142.89111.89

1.21

2009-10 97.2375.73

1.17

3 Debt Equity Ratio Debt.

Equity

2010-11 0.0021.98

0.00

2009-10 0.0021.98

0.00

4Working Capital Turnover

Ratio

Sales .

Net WorkingCapital

2010-11 540.17105.23

5.13

2009-10 394.9866.42

5.94

5 Fixed Assets Turnover

Ratio

Sales.

Net Fixed Assets

2010-11 540.17106.66 5.06

2009-10 394.98104.16 3.79

6 Return on EquityPAT.

Net worth

2010-11 88.55385.01 22.9%

2009-10 51.97349.78 14.8%

7 Operating Profit RatioEBIT.

Net Sales

2010-11 88.30506.94

17.4%

2009-10 148.87372.25

27.9%

8 Return on Investment EBIT.

Total Investment

2010-11 88.30296.95 29.7%

2009-10 148.87297.80

49.9%

Department of MBA, PESIT Page 29

Department of MBA, PESIT Page 30

6. LEARNING EXPERIENCE

It was a great opportunity for me to do my internship in such an esteemed organization. The

organization culture is very good and it does create an homely atmoshphere and thus motivates to

learn.

I had a great experience learning in this Organization. “Learning by doing” was the strategy adopted

throughout ten weeks of duration of the project. Every minute in the organization taught new things

that would be a basement in my career.

This was a good platform for me to learn about the day to day management in an organization. The

ten weeks stay in the organization also helped me in improving my over all personality.

I learned how to apply theory into practicle application. This was done by applying theoretical

knowledge of Porter’s five force model into practical application.

I gained the knowledge of organisation structure which affects the daily operations, decision making

and flow of information.

Department of MBA, PESIT Page 31

PART – B

INDTRODUCTION TO THE RESEARCH

Statement of the problem

Kennametal – Machining Solution Group is a Market Leader in Gun Drilling Machines

Manufacturing and wanted to up keep this marker leadership position in next five years.

Presently it feels that the competition, new technology and new entrant from foreign countries may

erode the market share. So Kennametal Machining Solution Group wanted to know what would

make KIL –MSG to up keep the market leadership position in Gun Drilling Machine Manufacturing.

Purpose of the study:

The Indian machine tool industry is seeing entry of many foreign brands who are experts in Special

Purpose Machine manufacturing. Also there is stiff competition when it comes to the manufacture of

Gun Drilling Machine. The following below mentioned are the points which this study would be

focusing on:

A sound knowledge of consumer buying behaviour will help the marketer extract every bit of

competitive advantage in terms of available substitute’s knowledge, about the new entrants

trying to enter Indian machine tool industry for the manufacture of Gun Drilling Machine and

information about the competitors’ products and services.

Through this study, an attempt has been made to identify the key factors (if any) that might

lead to increased bargaining power of customer, Threats from substitutes as well new entrants

and competitors performance.

Department of MBA, PESIT Page 32

Objectives of the study

WIDMA will produce Gun Drilling Machine for Next 5 to 7 Years.

MQL Drilling Operation is direct substitute threat for Gun Drilling Process.

Gun Drilling Operations can also be possible to move into Machining Centers which can be a

threat to SPM Gun Drilling Machines.

Cost Per Piece will be higher when compared to General Purpose Machining centers

Expecting Heavy Competition from China in terms of Cost.

Expecting Heavy Competition from US and Europe in terms of Quality.

Gun Drilling Machines should be standardized to some range to get higher market share to

beat competition.

Scope of the study

1) To analyse the bargaining power of the customer.

2) To identify the potential threats or substitutes which would replace Gun drilling machine in

future.

3) To identify the threats from new entrants into the industry, which would lead to decrease in

market share of WIDMA gun drilling machines.

4) To analyse the bargaining power of the vendor / supplier.

5) To analyse the level of competition among the manufacturers of Gun drilling machine.

Department of MBA, PESIT Page 33

Methodology of the study

For doing the survey a structured and disguised type of questionnaire was prepared which was based

on the Porter’s Five Force Industry Analysis Narrowed Down only to Machine Tool Industry – Gun

Drilling Machines.

The Research will collect data, analyze and interpret from all the Porters five forces specified in the

Model

– Bargaining power of Customer

– Threat of New Entrant

– Threat of New Product and Technology Development

– Bargaining Power of Vendor.

Bargaining power of Customer

Bargaining power of customer is mainly to determine how much the customer power affects the

profitability of the business. This act as a base for pricing strategy.

In bargaining power of Customer, the study will cover the following parameters

Buyer concentration to firm concentration ratio

As the number of buyers increases relative to the number of competitors the negotiating power of

anyone buyer decreases. Conversely as the number of buyers reduces relative to the number of

competitors the power of the buyer increases

Differentiation of output

If the Product Provides significant Differentiation in Customer output product then Seller has higher

bargaining power

Bargaining leverage, particularly in industries with high fixed costs

The products represent a relatively large expense for your customers. Customers may not price shop

for a quart of oil, but they will price shop if purchasing a new vehicle.

Buyer volume

Buyers who buy only a few of your products each year are less likely to shop around for price on

those items.

Department of MBA, PESIT Page 34

Buyer switching costs relative to firm switching costs

A switching cost is a cost that your customer would incur if they ceased buying from you and

commenced buying from one of your competitors. Higher the cost lesser the bargaining power

These costs could be anything from the cost for legal to prepare and review of new contracts, the cost

of stocking spare parts specific to your competitors’ products, the cost of adopting a new ordering

system, the cost of retraining employees, or there maybe intangible costs such as increased risk (the

unknon).

Buyer information availability

Customers have access to and are able to evaluate market information. You have less room for

negotiation if buyers know market demand, prices, and your costs.

Ability to backward integrate

Customers could possibly make your product themselves, to meet their needs.

Availability of existing substitute products

A substitute is a different product or service that can be used instead of your industries products or

services. A substitute is not a competitor’s version of your product. Substitutes are typically

products/services that are not in your industry. Availability of such product reduces the sellers

bargaining power.

Buyer price sensitivity

Is the ratio of reduction in sales with respect to unit price increase? More the price sensitive less the

bargain power the seller has.

Differential advantage (uniqueness) of industry products

Your product is not unique and can be purchased from other suppliers. If your brand is homogenous

or similar to all of the others, buyers will base their decision mainly on price. In this case the seller

has less bargaining power

Buyer profitability

Buyer profitability – are your customers profitable and likely to remain profitable? The more

profitable your customers are the less likely they are to be concerned with the amount you charge.

Department of MBA, PESIT Page 35

Decision Maker Incentives.

The decision maker within your customers business may be receiving incentives from your

competitors such as free tickets. However they are equally likely to be given incentives, to negotiate,

by their employer.

The presence of incentives influences the decision, with part of the decision based on something

other than merit.

New Entrant

You may have the market cornered with your product, but your success may inspire others to enter

the business and challenge your position. The threat of new entrants is the possibility that new firms

will enter the industry. New entrants bring a desire to gain market share and often have significant

resources. Their presence may force prices down and put pressure on profits.

In New Entrant the study will cover the following parameters.

The existence of barriers to entry (patents, rights, etc.)

Processes are not protected by regulations or patents. In contrast, when licenses and permits are

required to do business, such as with the liquor industry, existing firms enjoy some protection from

new entrants.

Economies of product differences

If Product differentiation is easily achievable and can be done economically then the chance of new

entrant into the market is more.

Brand equity

Customers have little brand loyalty. Without strong brand loyalty, a potential competitor has to spend

little to overcome the advertising and service programs of existing firms and New Firms is more

likely to enter the industry.

Switching costs

In situations where customers do not face significant one-time costs from switching suppliers, it is

more attractive for new firms to enter the industry and lure the customers away from their previous

suppliers.

Department of MBA, PESIT Page 36

Capital requirements

Start-up costs are low for new businesses entering the industry. The less commitment needed in

advertising, research and development, and capital assets, the greater the chance of new entrants to

the industry

Access to distribution

You will have developed methods to distribute your products to your customers, the harder it is for

new entrants to replicate this distribution system the less likely new entrants are to enter and remain

in the industry.

Customer loyalty to established brands

If customer loyalty is very less among the established brands then chance of new entrant is more

likely

Absolute cost

Do you have a good location, long term arrangements for access to raw materials or unique

production or distribution system that makes it hard for anyone to compete with you then chance of

new entrant is less.

Industry profitability;

The more profitable the industry the more attractive it will be to new competitors

Department of MBA, PESIT Page 37

Threat of Substitute

New Product and Technology Development (Substitute)

Products from one business can be replaced by products from another. If you produce a commodity

product that is undifferentiated, customers can easily switch away from your product to a

competitor’s product with few consequences. In contrast, there may be a distinct penalty for

switching if your product is unique or essential for your customer’s business. Substitute products are

those that can fulfill a similar need to the one your product fills.

In this the study will cover the following parameters

Buyer propensity to substitute

Refers to your customers loyalty to your product or service .How do your customers react to

substitutes, do they trial them or are they loyal to your industry?

It would also pay to identify the things that need to change for your customers to change their

propensity to trial substitute products.

Relative price performance of substitute

Refers to the cost effectiveness of the substitute products, (Total supply chain costs)

Alternative products that provide overall savings to your customers, without impacting the quality of

your customer’s products or services are more likely to be viewed favorably for adoption.

Buyer switching costs

In situations where customers do not face significant one-time costs from switching to substitute

then, it is more attractive for firms to use the substitute product.

Perceived level of product differentiation

It is the substitute perceived as a product differentiator.

Number of substitute products available in the market

If more number of substitutes are available, then the chance of switch to substitute is more likely.

Department of MBA, PESIT Page 38

Bargaining Power of Vendors

Any business requires inputs—labour, parts, raw materials, and services. The cost of your inputs can

have a significant effect on your company’s profitability. Whether the strength of Suppliers

represents a weak or a strong force hinges on the amount of bargaining power they can exert and,

ultimately, on how they can influence the terms and conditions of Transactions in their favor.

Suppliers would prefer to sell to you at the highest price possible or provide you with no more

services than necessary. If the force is weak, then you may be able to negotiate a favorable business

deal for yourself. Conversely, if the force is strong, then you are in a weak position and may have to

pay a higher price or accept a lower level of quality or service.

In this the study will cover the following parameters

Supplier switching costs relative to firm switching costs

If the switch cost of supplier from one firm to another is higher than the Bargaining power of vendor

is less.

Degree of differentiation of inputs

If the input from the vendor is different from other vendor then the vendor has higher bargaining

power

Impact of inputs on cost or differentiation

If the input from the vendor makes significant differentiation in product then the vendor has higher

bargaining power

Presence of substitute inputs

Refers to an alternative product or service that is not in your supplier's industry. If it is available then

the vendor has less power to bargain

Strength of distribution channel

If the Distribution channel of the vendor is very strong and the availability is very quick then the

vendor has significant bargain power.

Supplier concentration to firm concentration ratio

Refers to the ratio of suppliers to buyers in your industry

Department of MBA, PESIT Page 39

Decision on data collection method

Bargaining Power of Buyer

Buyer concentration to firm concentration ratio

Data Type: Secondary Data

Data Source: - Historical Database, Internet and Data Collection Agency.

Attribute:-

1) No. of buyers available in the market (Customers who buy’s SPM Gun Drilling machine)

2) No. of SPM Gun Drilling Machine Sellers in the Market.

Differentiation of output

Data Type: - Primary

Data Source: - Directly From the Buyers Sample

Attribute: -

How The Buyer Feels about the WIDMA Gun Drilling Machines Features, Service and Quality.

Bargaining leverage, particularly in industries with high fixed costs

Data Type: - Secondary

Data Source: - Historical Database, Internet and Information Bureaus

Attribute:- What is the cost of Gun Drilling Machine primarily to find out whether gun drilling

machines has high fixed cost or not.

Buyer volume

Data Type: Secondary

Data Source: - Historical data.

Attribute:-Customer wise Gun Drilling Machine sales in one year, frequency of purchase and number

of machines purchased by the customer.

Department of MBA, PESIT Page 40

Buyer switching costs relative to firm switching costs

Data Type: - Primary

Data Source: - Group Discussion & Buyer

Attribute:-

Collects switching cost of Buyer incase if he switches from WIDMA to another Supplier like Admin

Cost, ordering cost, training cost and increased Risk.

Buyer information availability

Data Type: - Primary & Secondary

Data Source: - Customer & Group Discussion

Attribute:-

How Buyer Get to Know about the competitors & Substitute Product

Ability to backward integrate

Data Type: - Primary

Data Source: - Group Discussion

Attribute:-

Whether customer has a chance and will go for backward integration

Availability of existing substitute products

Data Type: - Secondary & Primary

Data Source: - Historical data, Internet, Information Bureau and Customer

Attribute:-

List of Substitute available to customer which serves customer Gun Drilling requirement

Buyer price sensitivity

Data Type: - Secondary & Primary

Data Source: - Historical Customer Budget Data, Group Discussion, Customer

Attribute: - At what price customer stops buying.

Department of MBA, PESIT Page 41

Impact of output on the cost of Differentiation

Data Type: - Primary

Data source: - Customer

Attribute:-

Does the WIDMA Gun Drilling Machines provide Differentiation to customer product?

Decision Maker Incentives.

Data type: - Primary

Data Source: - Internal Sales Team

Attribute: -

Availability of Decision Maker Incentives System with competitor and how much this impacts the

sales conversion

New Entrant

The existence of barriers to entry (patents, rights, etc.)

Data Type: Secondary & Primary

Data Source: Historical Data, Information Bureaus, Internet and Internal Team

Attribute:-

Existence of Patent, Govt. Policy for Foreign Entrant & Domestic Entrant, Capital Requirement for

Startup, Economy of Scale based on the Capex.

Brand equity

Data Type: Primary

Data Source: Customer

Attribute: - Brand Equity

What is the Relative Market Share?

What is the Relative Price?

What is the Durability?

Department of MBA, PESIT Page 42

Switching costs or sunk costs

Data Collection plan already exist in bargaining power of Customer

Capital requirements

Data Collection Plan already exists in Entry Barrier.

Access to distribution

Data Type: - Secondary

Data Source: - Historical Data, Internet

Attribute:-

How much access the New Entrant has in terms of Sales and after sales service distribution

Customer loyalty to established brands

Data Type: - Primary

Data Source: - Secondary

Attribute:-

Which Brand the customer willing to buy next time when the customer buys next time?

Which Brand the customer willing to refer to another colleague or friend from another company

when they want to buy the product?

Industry profitability

Data Type: - Secondary

Data Source: Historical Data

Attribute: PAT

Department of MBA, PESIT Page 43

New Product and Technology Development

Buyer propensity to substitute

Already exist in bargaining power of Buyer

Relative price performance of substitute

Data Type: Primary & Secondary

Data Source: Historical Data, Internet, Information Bureaus

Attribute:

Overall cost saving to customer when they use the substitute (without affecting the quality of the

output product)

Buyer switching costs

Data type: - Primary

Data Source: Customer

Attribute:-

Cost if they incur while changing to substitute product (Legal Cost, Spare inventory, risk perceived)

Perceived level of product differentiation

Data type: - Secondary

Data Source: Internet, information Bureaus

Attribute:-

What is the Difference between Substitute and the Current Product offering in terms of cost, quality

of output, ease of operation and service availability?

Number of substitute products available in the market

Data type: Secondary

Data Source: Internet, Information Bureaus

Attribute:-

List of Substitute Product Available

Department of MBA, PESIT Page 44

Bargaining Power of Vendors

Degree of differentiation of inputs

Data Type: - Primary

Data Source: Internal SCM Team

Attribute: -

Supplier Product or service is unique supplier product attribute restricts from buying from others

Impact of inputs on cost or differentiation

Data type: - Primary

Data source: - Internal Design & SCM Team

Attribute:-

Whether the supplier input reduces the cost or product differentiation.

Presence of substitute inputs

Data Type: - Primary

Data Source: - Internal SCM Team

Attribute:-

Is there any Substitute available for the Supplier input?

Supplier concentration to firm concentration ratio

Data Type: - Primary

Data Source: Internal SCM Team

Attribute: -

Firm Concentration Ratio and Supplier Concentration Ratio

Importance of Volume to the supplier

Data Type: - Primary

Attribute: - What is the Importance of Production Volume to the supplier?

Department of MBA, PESIT Page 45

DATA COLLECTION

As the users of Gun drilling machine are situated in different parts of India, the area of study was all

over India. Convenience sampling method was used as this technique helped in sending the

questionnaire to the respondents who have used / not used WIDMA Gun drilling machine. Data was

analysed by using Microsoft Excel.

SAMPLING METHOD: Convenience Sampling

SAMPLE SIZE : The sample size has been fixed to 65 respondents.

The respondents responded through online survey questionnaire

(Survey monkey)

SAMPLING PLAN : Online questionnaire

COVERAGE : All over India

DURATION : 8 Weeks

DATA SOURCES :

PRIMARY DATA

Primary data is the data collected specifically for the study currently undertaken. The

procedure followed and the collection of primary data is by structured online questionnaire,

which consisted of multiple choice questions, open end and close ended questions.

SECONDARY DATA

Data which is useful in solving the current problem, which was collected for different

purpose. It includes the information collected from the Organisation website / database,

Journals, Articles and prior research report.

RESEARCH INSTRUMENT: Online Questionnaire

TYPES OF QUESTIONS : Multiple choice questions, Ranking type questions,

Dichotomous questions, Open ended and close ended

questions.

Department of MBA, PESIT Page 46

LIMITATIONS OF THE STUDY

The study is limited to only Gun drilling machine users.

The findings are based on the information given by the respondents.

It is assumed that the respondents understood the questions in the questionnaire as

they were supposed to, the chances of misunderstanding were remote but it cannot be

ruled out.

The study was focused mainly on the middle level managers and not on the end user /

operator of the machine.

The competitive rivalry analysis is not included in the scope of this study and is being

done by third party to have an un-biased result.

Department of MBA, PESIT Page 47

ANALYSIS, DESIGN AND INTERPRETATION

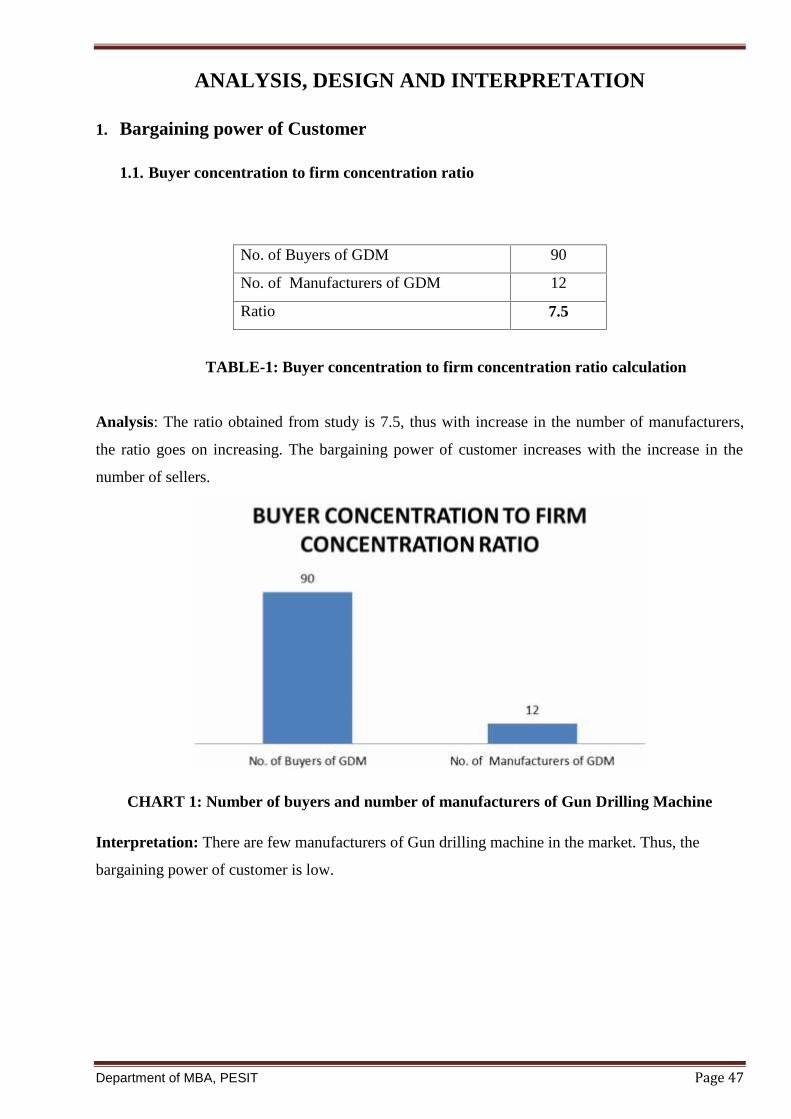

1. Bargaining power of Customer

1.1. Buyer concentration to firm concentration ratio

No. of Buyers of GDM 90

No. of Manufacturers of GDM 12

Ratio 7.5

TABLE-1: Buyer concentration to firm concentration ratio calculation

Analysis: The ratio obtained from study is 7.5, thus with increase in the number of manufacturers,

the ratio goes on increasing. The bargaining power of customer increases with the increase in the

number of sellers.

CHART 1: Number of buyers and number of manufacturers of Gun Drilling Machine

Interpretation: There are few manufacturers of Gun drilling machine in the market. Thus, the

bargaining power of customer is low.

Department of MBA, PESIT Page 48

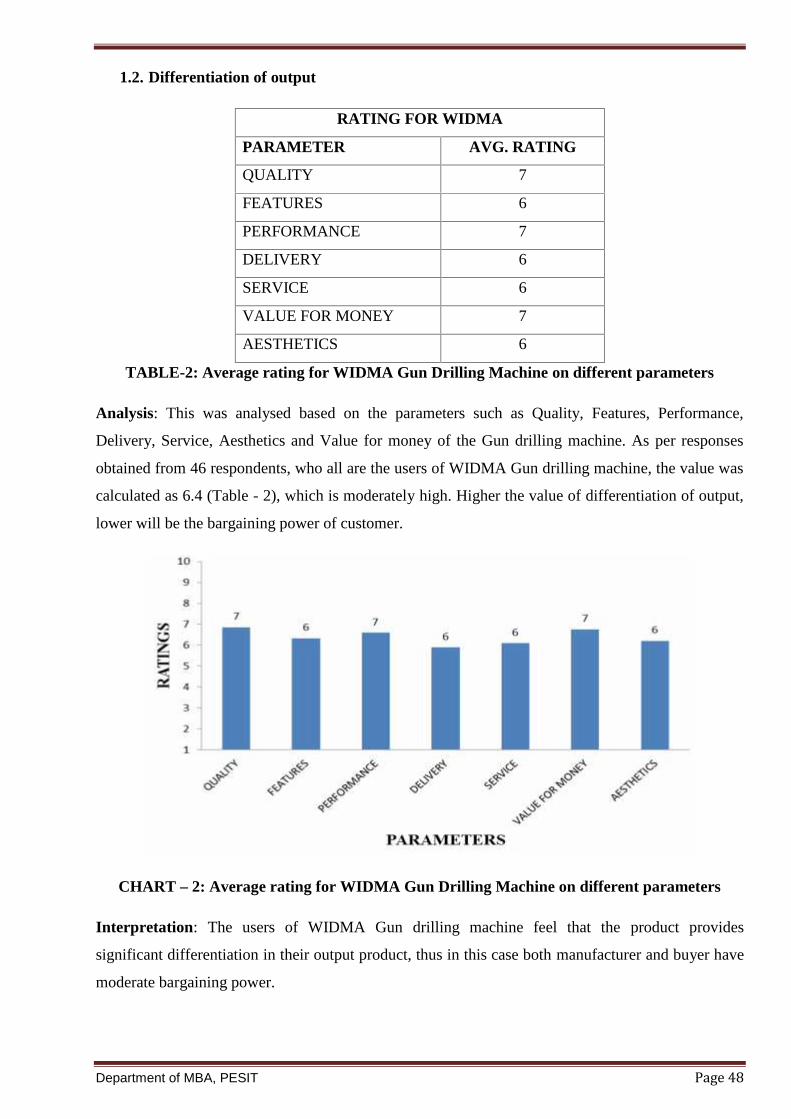

1.2. Differentiation of output

RATING FOR WIDMA

PARAMETER AVG. RATING

QUALITY 7

FEATURES 6

PERFORMANCE 7

DELIVERY 6

SERVICE 6

VALUE FOR MONEY 7

AESTHETICS 6

TABLE-2: Average rating for WIDMA Gun Drilling Machine on different parameters

Analysis: This was analysed based on the parameters such as Quality, Features, Performance,

Delivery, Service, Aesthetics and Value for money of the Gun drilling machine. As per responses

obtained from 46 respondents, who all are the users of WIDMA Gun drilling machine, the value was

calculated as 6.4 (Table - 2), which is moderately high. Higher the value of differentiation of output,

lower will be the bargaining power of customer.

CHART – 2: Average rating for WIDMA Gun Drilling Machine on different parameters

Interpretation: The users of WIDMA Gun drilling machine feel that the product provides

significant differentiation in their output product, thus in this case both manufacturer and buyer have

moderate bargaining power.

Department of MBA, PESIT Page 49

1.3. Bargaining leverage, particularly in industries with high fixed costs

Analysis: The product represents a relatively large expense for the buyer. This is because the

machines have high fixed costs. Thus, the buyer will definitely negotiate with the manufacturer of

the machine and would take longer time to make purchase decision. As a result of which the

bargaining leverage is quite high. Thus, with more number of manufacturers, the bargaining leverage

also increases.

Interpretation: From the study it can be interpreted that there are many manufacturers of Gun

drilling machine. Thus, the bargaining power of customer is high.

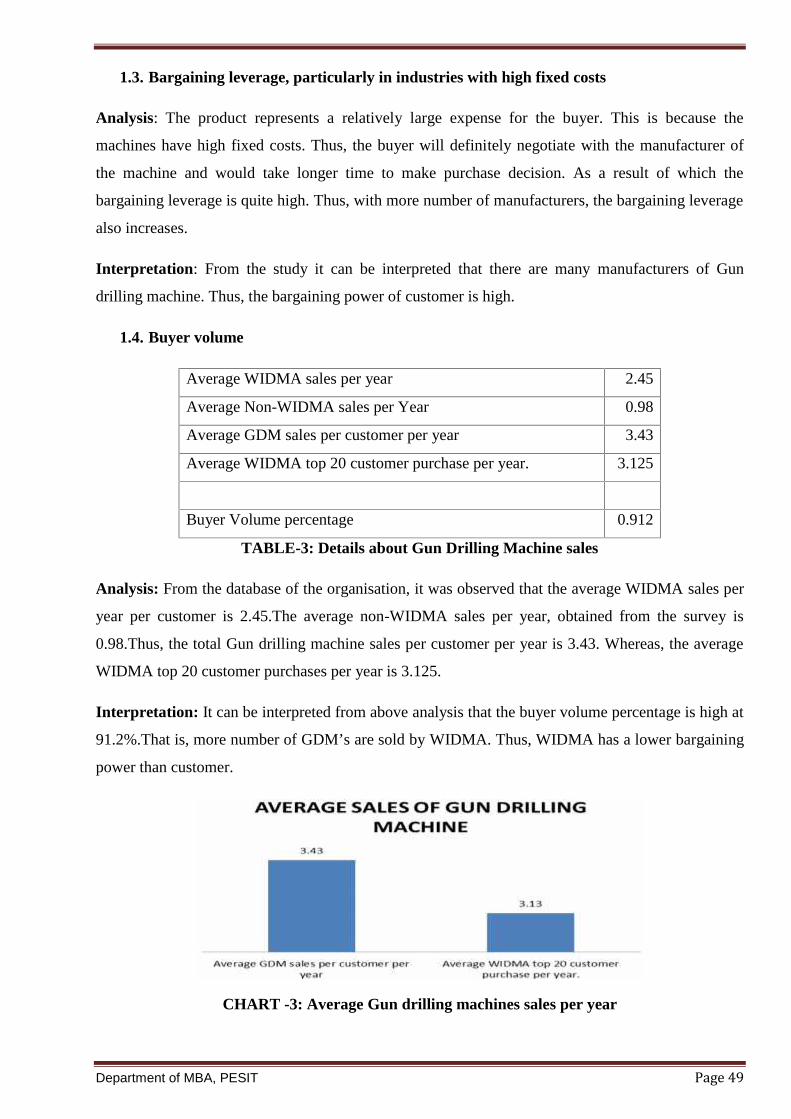

1.4. Buyer volume

Average WIDMA sales per year 2.45

Average Non-WIDMA sales per Year 0.98

Average GDM sales per customer per year 3.43

Average WIDMA top 20 customer purchase per year. 3.125

Buyer Volume percentage 0.912

TABLE-3: Details about Gun Drilling Machine sales

Analysis: From the database of the organisation, it was observed that the average WIDMA sales per

year per customer is 2.45.The average non-WIDMA sales per year, obtained from the survey is

0.98.Thus, the total Gun drilling machine sales per customer per year is 3.43. Whereas, the average

WIDMA top 20 customer purchases per year is 3.125.

Interpretation: It can be interpreted from above analysis that the buyer volume percentage is high at

91.2%.That is, more number of GDM’s are sold by WIDMA. Thus, WIDMA has a lower bargaining

power than customer.

CHART -3: Average Gun drilling machines sales per year

Department of MBA, PESIT Page 50

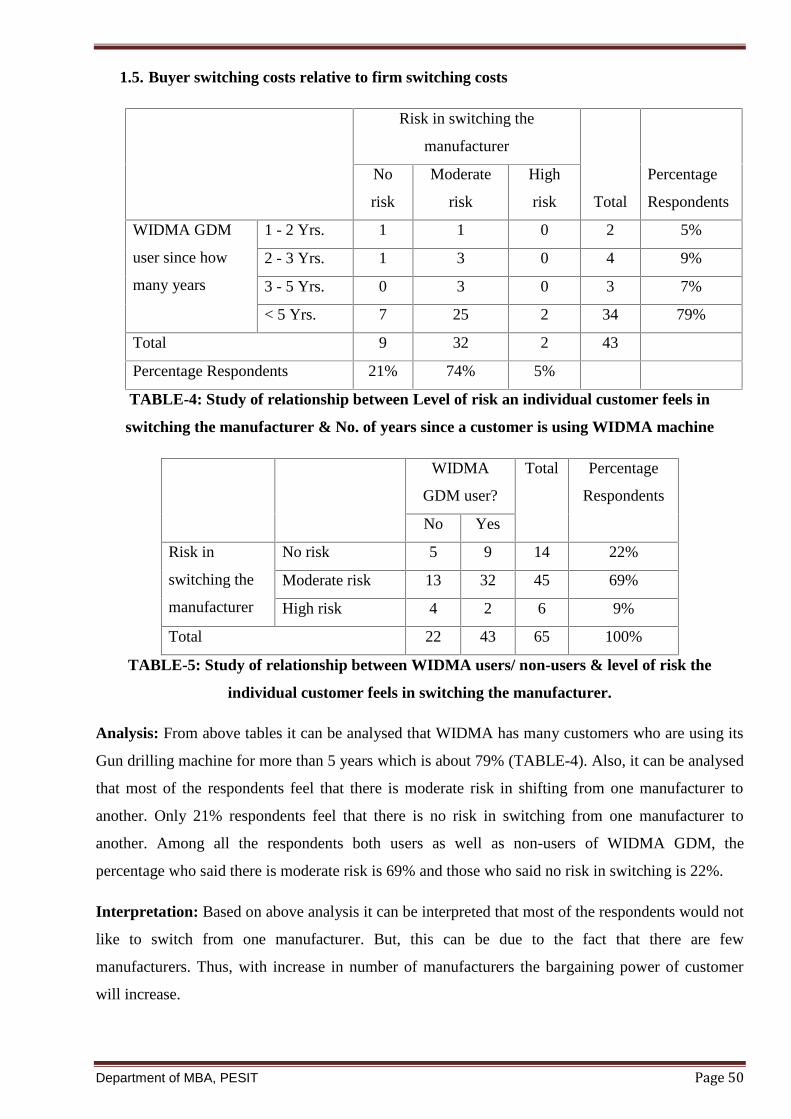

1.5. Buyer switching costs relative to firm switching costs

Risk in switching the

manufacturer

Total

Percentage

Respondents

No

risk

Moderate

risk

High

risk

WIDMA GDM

user since how

many years

1 - 2 Yrs. 1 1 0 2 5%

2 - 3 Yrs. 1 3 0 4 9%

3 - 5 Yrs. 0 3 0 3 7%

< 5 Yrs. 7 25 2 34 79%

Total 9 32 2 43

Percentage Respondents 21% 74% 5%

TABLE-4: Study of relationship between Level of risk an individual customer feels in

switching the manufacturer & No. of years since a customer is using WIDMA machine

WIDMA

GDM user?

Total Percentage

Respondents

No Yes

Risk in

switching the

manufacturer

No risk 5 9 14 22%

Moderate risk 13 32 45 69%

High risk 4 2 6 9%

Total 22 43 65 100%

TABLE-5: Study of relationship between WIDMA users/ non-users & level of risk the

individual customer feels in switching the manufacturer.

Analysis: From above tables it can be analysed that WIDMA has many customers who are using its

Gun drilling machine for more than 5 years which is about 79% (TABLE-4). Also, it can be analysed

that most of the respondents feel that there is moderate risk in shifting from one manufacturer to

another. Only 21% respondents feel that there is no risk in switching from one manufacturer to

another. Among all the respondents both users as well as non-users of WIDMA GDM, the

percentage who said there is moderate risk is 69% and those who said no risk in switching is 22%.

Interpretation: Based on above analysis it can be interpreted that most of the respondents would not

like to switch from one manufacturer. But, this can be due to the fact that there are few

manufacturers. Thus, with increase in number of manufacturers the bargaining power of customer

will increase.

Department of MBA, PESIT Page 51

1.6. Ability to backward integrate

Analysis: From TABLE-4 it can be analysed that there are more respondents who are using WIDMA

Gun drilling machine for more than 5 years which is about 79%.

Interpretation: Thus it can be interpreted that the ability to backward integrate among the users of

the Gun drilling machine is very low. Also, expertise is required in terms of designing and

manufacturing of the Gun drilling machine. Thus, bargaining power of customer is low in this case.

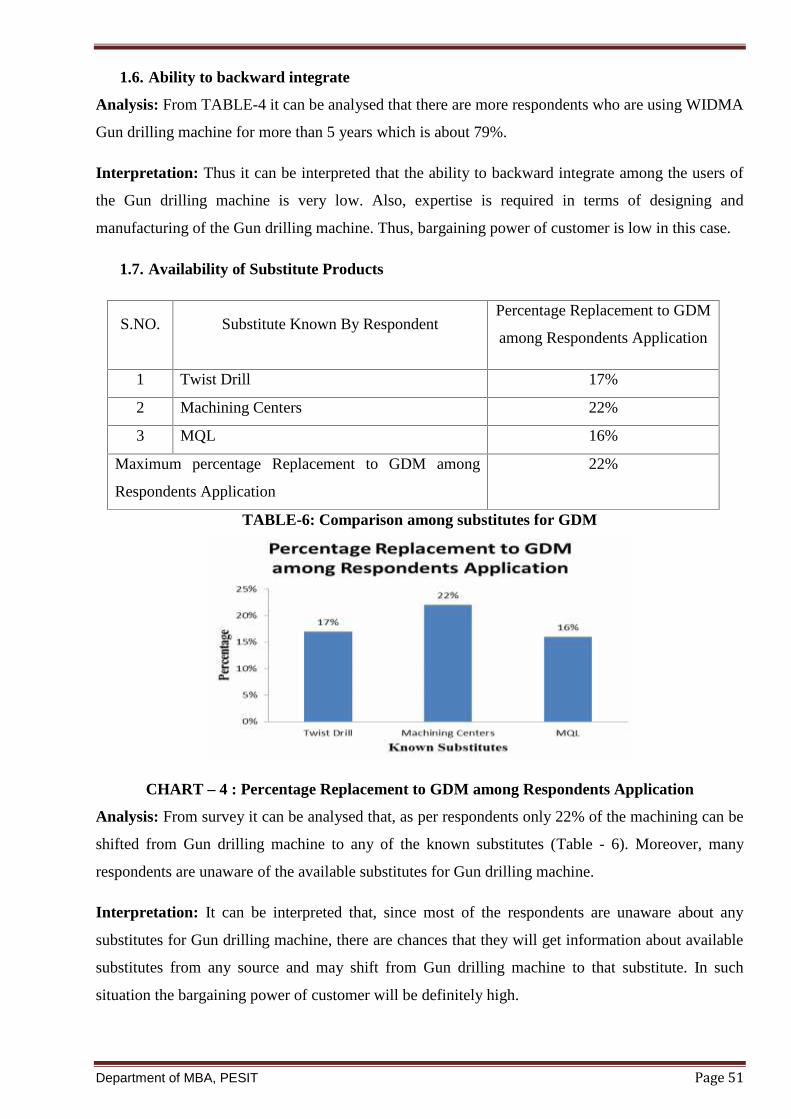

1.7. Availability of Substitute Products

S.NO. Substitute Known By RespondentPercentage Replacement to GDM

among Respondents Application

1 Twist Drill 17%

2 Machining Centers 22%

3 MQL 16%

Maximum percentage Replacement to GDM among

Respondents Application

22%

TABLE-6: Comparison among substitutes for GDM

CHART – 4 : Percentage Replacement to GDM among Respondents Application

Analysis: From survey it can be analysed that, as per respondents only 22% of the machining can be

shifted from Gun drilling machine to any of the known substitutes (Table - 6). Moreover, many

respondents are unaware of the available substitutes for Gun drilling machine.

Interpretation: It can be interpreted that, since most of the respondents are unaware about any

substitutes for Gun drilling machine, there are chances that they will get information about available

substitutes from any source and may shift from Gun drilling machine to that substitute. In such

situation the bargaining power of customer will be definitely high.

Department of MBA, PESIT Page 52

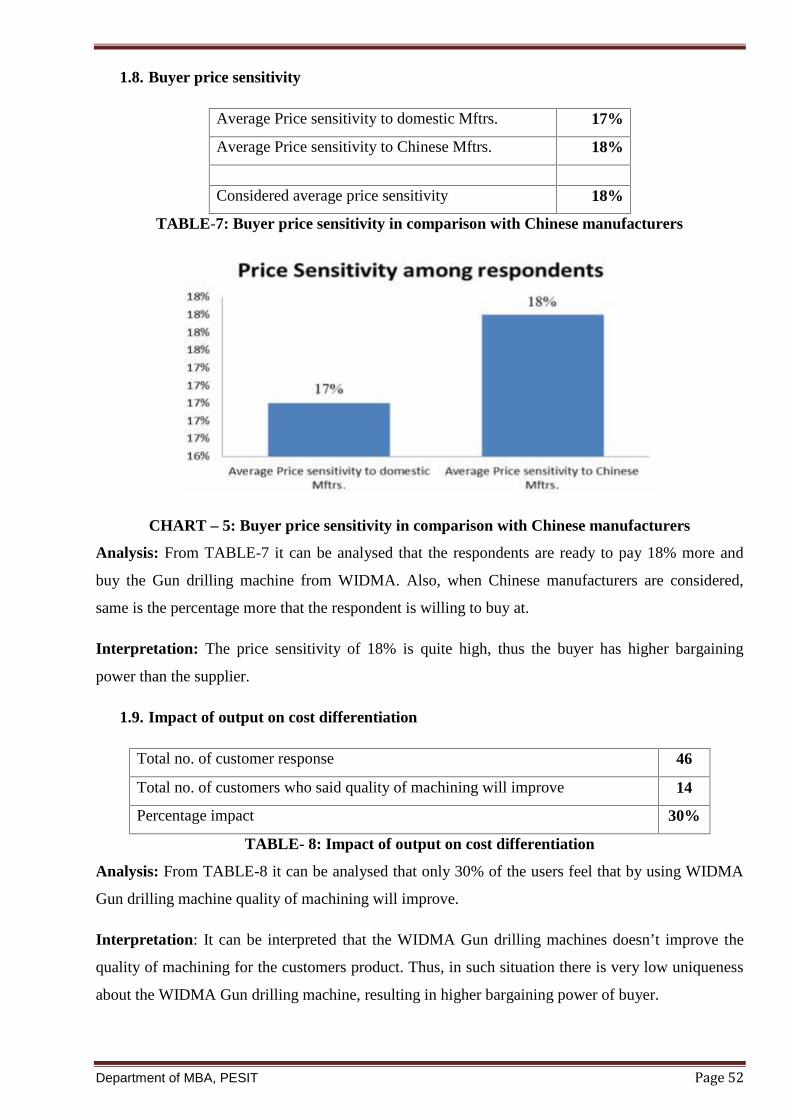

1.8. Buyer price sensitivity

Average Price sensitivity to domestic Mftrs. 17%

Average Price sensitivity to Chinese Mftrs. 18%

Considered average price sensitivity 18%

TABLE-7: Buyer price sensitivity in comparison with Chinese manufacturers

CHART – 5: Buyer price sensitivity in comparison with Chinese manufacturers

Analysis: From TABLE-7 it can be analysed that the respondents are ready to pay 18% more and

buy the Gun drilling machine from WIDMA. Also, when Chinese manufacturers are considered,

same is the percentage more that the respondent is willing to buy at.

Interpretation: The price sensitivity of 18% is quite high, thus the buyer has higher bargaining

power than the supplier.

1.9. Impact of output on cost differentiation

Total no. of customer response 46

Total no. of customers who said quality of machining will improve 14

Percentage impact 30%

TABLE- 8: Impact of output on cost differentiation

Analysis: From TABLE-8 it can be analysed that only 30% of the users feel that by using WIDMA

Gun drilling machine quality of machining will improve.

Interpretation: It can be interpreted that the WIDMA Gun drilling machines doesn’t improve the

quality of machining for the customers product. Thus, in such situation there is very low uniqueness

about the WIDMA Gun drilling machine, resulting in higher bargaining power of buyer.

Department of MBA, PESIT Page 53

2. Threat from New Entrants

2.1 The existence of barriers to entry (patents, rights, etc.)

Analysis: When it comes to machine tool industry, there is 100% FDI allowed. Also the import duty

rate of 25% is quite low for an International manufacturer to enter Indian market and sell his

machines. Also, secondary data available through IMTMA & other government websites, it can be

analysed that there are neither entry barriers in the form of Government regulations nor any patents

for the technology related to Gun drilling machine.

Interpretation: Thus, it can be interpreted that any new or foreign manufacturer can enter machine

tool industry in India to manufacture and sell the Gun drilling machine. In such case the threat from

new entrants is very high.

2.2 Brand equity

WIDMA Competitor -1 Competitor -2

Relative Market share 0.4 Relative Market share 0.3Relative Market

share0.2

Relative Price 1.18 Relative Price 1.2 Relative Price 1.05

Durability 0.9 Durability 0.9 Durability 0.9

Brand Equity 42% Brand Equity 32% Brand Equity 19%

TABLE-9: Brand Equity analysis among competitors

Analysis: Assuming the relative market share of WIDMA to be 40% and similarly assuming the

market share of local competitors 1 and 2 to be 30 and 20% respectively, it can be analysed that the

available brand equity to enter the industry for new company is only 6% (100-(42+32+19)).

Interpretation: Thus, for a new entrant very less percent of market share is available to enter the

industry. In such situation the threat from the new entrants is very low.

Note: The relative market share is assumed because the actual data is not available and finding the

market share is out of the scope of this study. The same is being done by the third party.

Department of MBA, PESIT Page 54

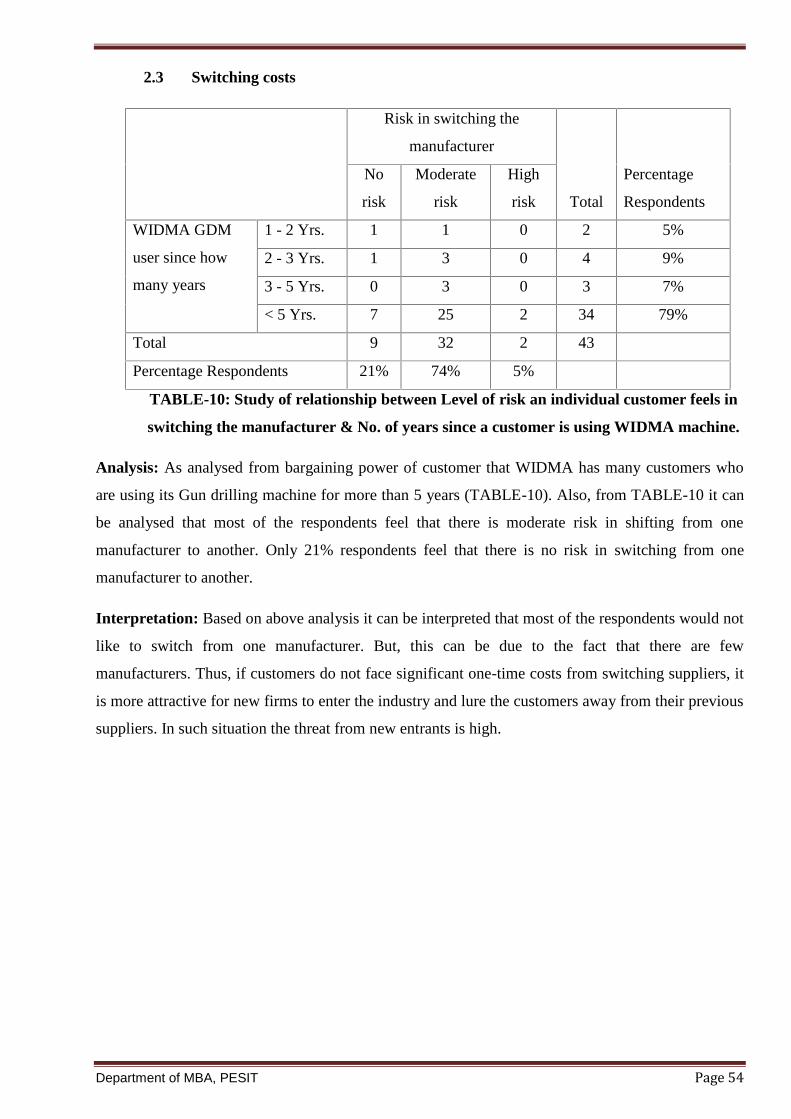

2.3 Switching costs

Risk in switching the

manufacturer

Total

Percentage

Respondents

No

risk

Moderate

risk

High

risk

WIDMA GDM

user since how

many years

1 - 2 Yrs. 1 1 0 2 5%

2 - 3 Yrs. 1 3 0 4 9%

3 - 5 Yrs. 0 3 0 3 7%

< 5 Yrs. 7 25 2 34 79%

Total 9 32 2 43

Percentage Respondents 21% 74% 5%

TABLE-10: Study of relationship between Level of risk an individual customer feels in

switching the manufacturer & No. of years since a customer is using WIDMA machine.

Analysis: As analysed from bargaining power of customer that WIDMA has many customers who

are using its Gun drilling machine for more than 5 years (TABLE-10). Also, from TABLE-10 it can

be analysed that most of the respondents feel that there is moderate risk in shifting from one

manufacturer to another. Only 21% respondents feel that there is no risk in switching from one

manufacturer to another.

Interpretation: Based on above analysis it can be interpreted that most of the respondents would not

like to switch from one manufacturer. But, this can be due to the fact that there are few

manufacturers. Thus, if customers do not face significant one-time costs from switching suppliers, it

is more attractive for new firms to enter the industry and lure the customers away from their previous

suppliers. In such situation the threat from new entrants is high.

Department of MBA, PESIT Page 55

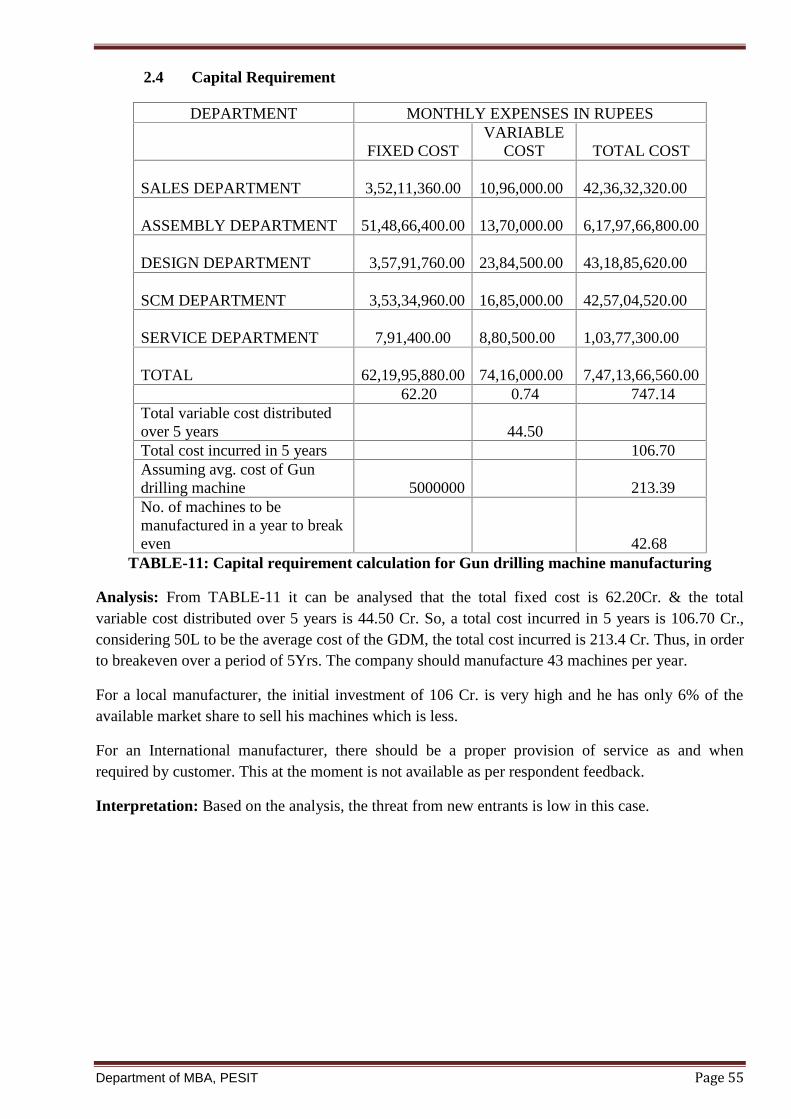

2.4 Capital Requirement

DEPARTMENT MONTHLY EXPENSES IN RUPEES

FIXED COSTVARIABLE

COST TOTAL COST

SALES DEPARTMENT 3,52,11,360.00 10,96,000.00 42,36,32,320.00

ASSEMBLY DEPARTMENT 51,48,66,400.00 13,70,000.00 6,17,97,66,800.00

DESIGN DEPARTMENT 3,57,91,760.00 23,84,500.00 43,18,85,620.00

SCM DEPARTMENT 3,53,34,960.00 16,85,000.00 42,57,04,520.00

SERVICE DEPARTMENT 7,91,400.00 8,80,500.00 1,03,77,300.00

TOTAL 62,19,95,880.00 74,16,000.00 7,47,13,66,560.0062.20 0.74 747.14

Total variable cost distributedover 5 years 44.50Total cost incurred in 5 years 106.70Assuming avg. cost of Gundrilling machine 5000000 213.39No. of machines to bemanufactured in a year to breakeven 42.68

TABLE-11: Capital requirement calculation for Gun drilling machine manufacturing

Analysis: From TABLE-11 it can be analysed that the total fixed cost is 62.20Cr. & the totalvariable cost distributed over 5 years is 44.50 Cr. So, a total cost incurred in 5 years is 106.70 Cr.,considering 50L to be the average cost of the GDM, the total cost incurred is 213.4 Cr. Thus, in orderto breakeven over a period of 5Yrs. The company should manufacture 43 machines per year.

For a local manufacturer, the initial investment of 106 Cr. is very high and he has only 6% of theavailable market share to sell his machines which is less.

For an International manufacturer, there should be a proper provision of service as and whenrequired by customer. This at the moment is not available as per respondent feedback.

Interpretation: Based on the analysis, the threat from new entrants is low in this case.

Department of MBA, PESIT Page 56

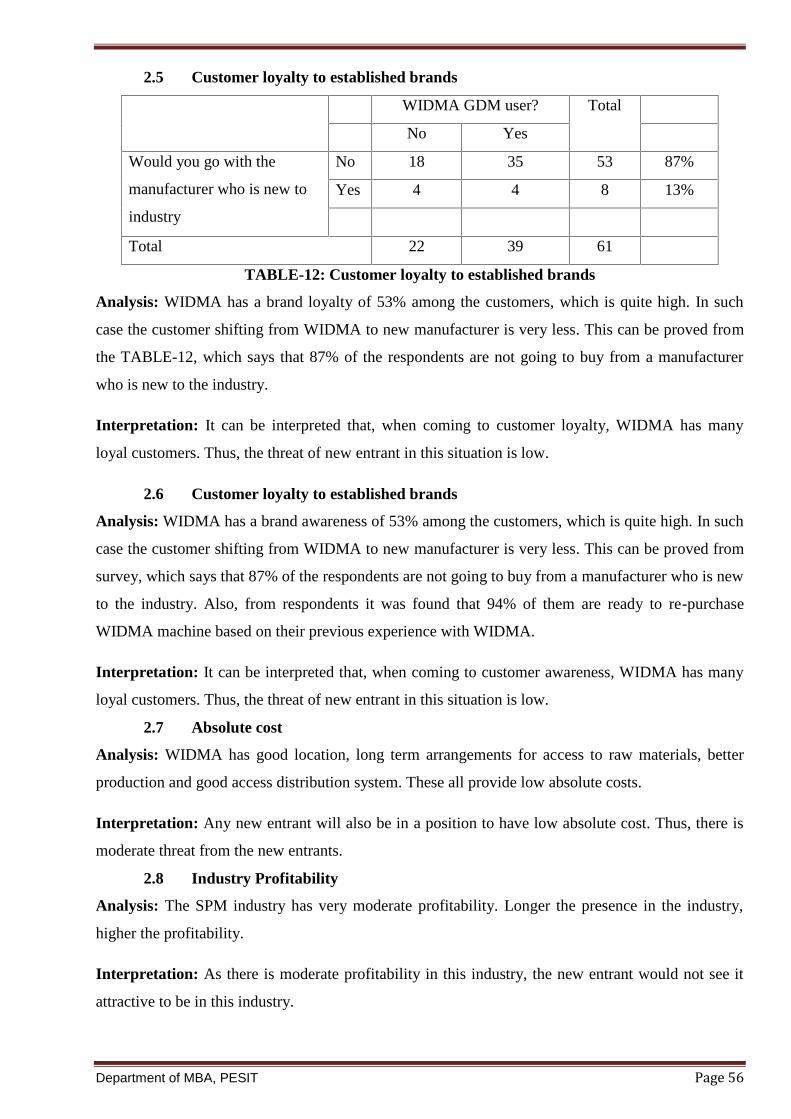

2.5 Customer loyalty to established brands

WIDMA GDM user? Total

No Yes

Would you go with the

manufacturer who is new to

industry

No 18 35 53 87%

Yes 4 4 8 13%

Total 22 39 61

TABLE-12: Customer loyalty to established brands

Analysis: WIDMA has a brand loyalty of 53% among the customers, which is quite high. In such

case the customer shifting from WIDMA to new manufacturer is very less. This can be proved from

the TABLE-12, which says that 87% of the respondents are not going to buy from a manufacturer

who is new to the industry.

Interpretation: It can be interpreted that, when coming to customer loyalty, WIDMA has many

loyal customers. Thus, the threat of new entrant in this situation is low.

2.6 Customer loyalty to established brands

Analysis: WIDMA has a brand awareness of 53% among the customers, which is quite high. In such

case the customer shifting from WIDMA to new manufacturer is very less. This can be proved from

survey, which says that 87% of the respondents are not going to buy from a manufacturer who is new

to the industry. Also, from respondents it was found that 94% of them are ready to re-purchase

WIDMA machine based on their previous experience with WIDMA.

Interpretation: It can be interpreted that, when coming to customer awareness, WIDMA has many

loyal customers. Thus, the threat of new entrant in this situation is low.

2.7 Absolute cost

Analysis: WIDMA has good location, long term arrangements for access to raw materials, better

production and good access distribution system. These all provide low absolute costs.

Interpretation: Any new entrant will also be in a position to have low absolute cost. Thus, there is

moderate threat from the new entrants.

2.8 Industry Profitability

Analysis: The SPM industry has very moderate profitability. Longer the presence in the industry,

higher the profitability.

Interpretation: As there is moderate profitability in this industry, the new entrant would not see it

attractive to be in this industry.

Department of MBA, PESIT Page 57

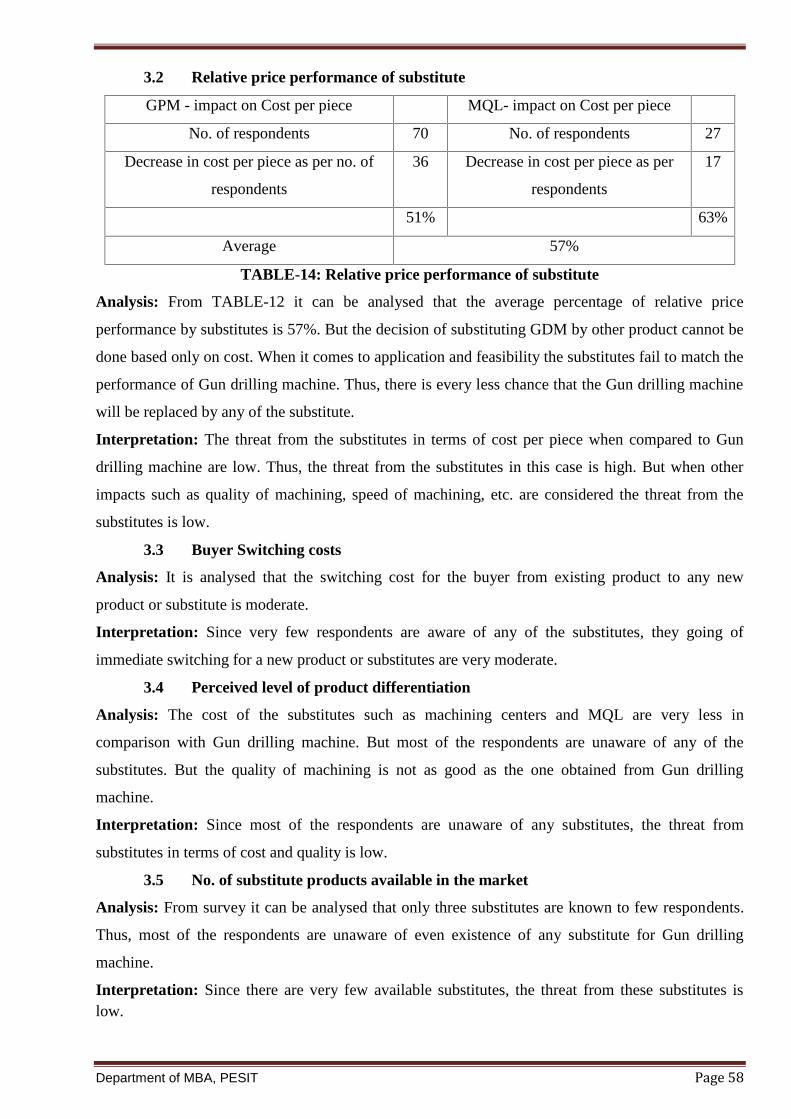

3. Threat of New product or Substitutes

3.1 Buyer Propensity to substitute

Percentage replacement by MQL 16%

Percentage replacement by Machining centers 22%

Percentage replacement by Twist Drill 17%

Max.% Replacement to GDM among customer application 22%

TABLE-13: Buyer propensity to substitute products

CHART – 6: Percentage replacement by substitutes

Analysis: From survey it can be analysed that, as per respondents only 22% of the machining can be

shifted from Gun drilling machine to any of the known substitutes (TABLE-13). Moreover, many