process costing key topics: –cost flows in mass production –steps in preparing process cost...

TRANSCRIPT

Process Costing

Key Topics:–Cost flows in mass production–Steps in preparing process cost reports (FIFO and weighted average)

•Equivalent units•Applying costs

–Spoilage in process costing– Uses, Uncertainties, and limitations

Chapter 6

Process Costing

Process product-costing systems are used for costing inventories or services when they are mass-produced, identical units.

These products differ from the custom-made or unique goods that are assigned costs under a job costing system

Chapter 6

Mass Production

Many goods are produced using a continuous process.

Examples:

Chapter 6

Overview of Process Costing Systems

Chapter 6

Steps for Preparing a Process Costing Report:

1. Summarize total costs to account for.2. Summarize total physical and equivalent

units.3. Compute cost per equivalent unit.4. Account for cost of units completed and cost

of ending WIP.

Chapter 6

What Are Equivalent Units, and How Do They Relate to the Production Process?

Equivalent Units:• Measure the resources used in partially completed units

relative to the resources needed to complete the units.

Equivalent Units Depend on the Pattern of Cost Flow:Direct Materials:* Added at the beginning of the process* Added during the processConversion Costs:* Incurred uniformly throughout the process* Incurred non-uniformly

Chapter 6

How Is the Weighted Average Method Used in Process Costing?

Weighted Average Method:Costs from beginning WIP (performed last period) are averaged with costs incurred during the current period and then allocated to all units completed and ending WIP.

Chapter 6

Summaries of Physical Units and Total Costs for Weighted Average Calculations

(Assuming direct materials are added at the beginning of the process)

Chapter 6

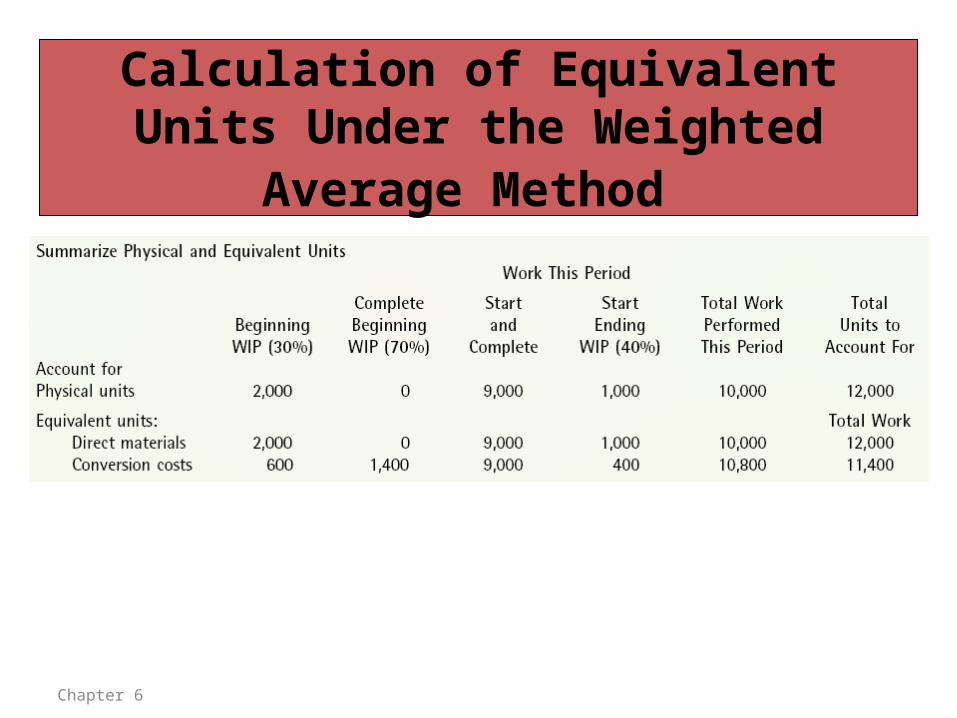

Calculation of Equivalent Units Under the Weighted Average Method

Chapter 6

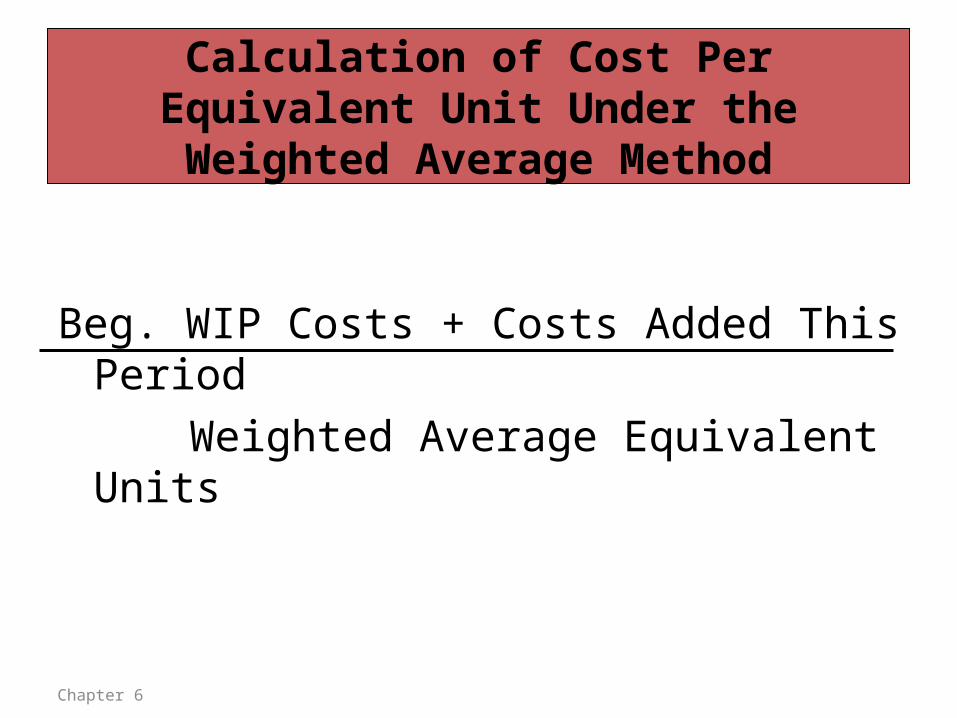

Calculation of Cost Per Equivalent Unit Under the Weighted Average Method

Beg. WIP Costs + Costs Added This PeriodWeighted Average Equivalent Units

Chapter 6

Equivalent Unit Costs

Weighted Average:Direct materials = $6,000+$30,500 =$3.0417 12,000Conversion costs=$4,200+$76,680=$7.0947 11,400Total cost per equivalent unit = $10.1364

Chapter 6

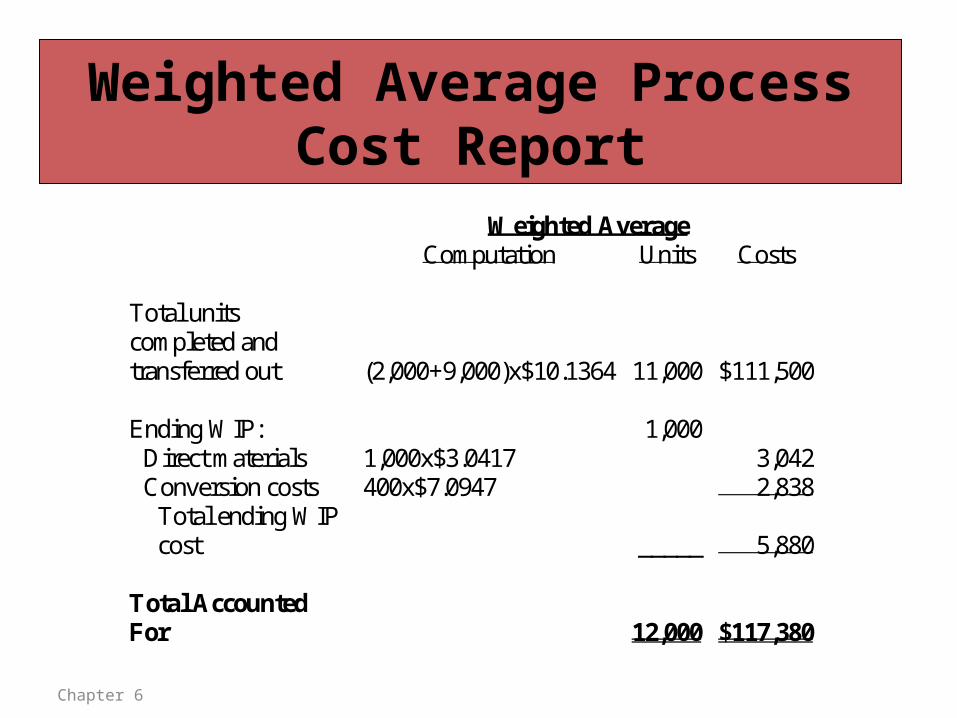

Weighted Average Process Cost Report

Weighted Average Computation Units Costs

Total units completed and transferred out

(2,000+9,000)x$10.1364 11,000 $111,500

Ending WIP: 1,000

Direct materials 1,000x$3.0417 3,042 Conversion costs 400x$7.0947 2,838

Total ending WIP cost

_____ 5,880

Total Accounted For

12,000 $117,380

Chapter 6

Summaries of Physical Units and Total Costs for FIFO Calculations

(Assuming direct materials are added at the beginning of the process)

Chapter 6

Calculation of Equivalent Units Under the FIFO Method

Chapter 6

First-in, First-out (FIFO) Method

The current period’s costs are used to allocate cost to work performed this period

Chapter 6

Calculation of Cost Per Equivalent Unit

Chapter 6

Current Period Cost

Equivalent Units for Work Performed this Period

Equivalent Units Costs

FIFO:Direct materials = $30,500 = $3.05 10,000Conversion costs=76,680 = $7.10 10,800Total cost per equivalent unit = $10.15

Chapter 6

FIFO Process Cost Report First-in, First-Out

Computation Units Costs Beginning WIP 2,000 $ 10,200 Costs to complete beginning WIP:

Direct materials 0x$3.05 0 Conversion costs 1,400x$7.10 9,940

Total costs added this period _____ 9,940 Total cost of beginning WIP transferred out

2,000 20,140

New units started, completed, and transferred out

9,000x$10.15 9,000 91,350

Total units completed and transferred out 11,000 111,490 Ending WIP: 1,000

Direct materials 1,000x$3.05 3,050 Conversion costs 400x$7.10 2,840

Total ending WIP cost _____ 5,890 Total Accounted For 12,000 $117,380

Chapter 6

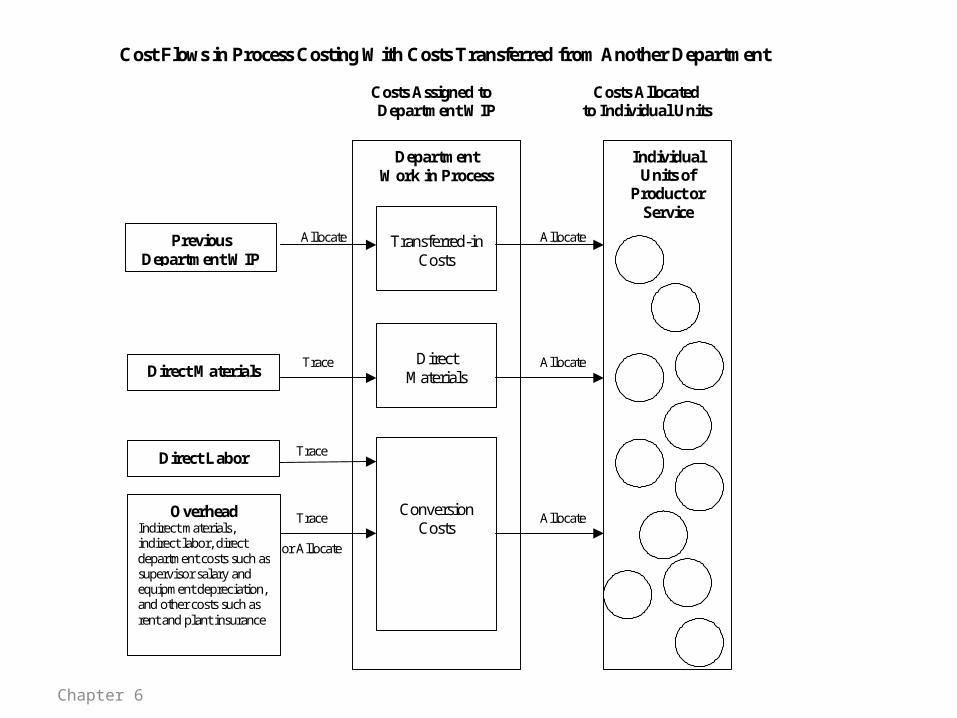

How Is Process Costing Performed for Multiple Production Departments

Transferred-in Costs:• Costs of processing performed in a previous

department

• Transferred-in costs are pooled separately from other costs

Chapter 6

Chapter 6

Cost Flows in Process Costing With Costs Transferred from Another Department Costs Assigned to Costs Allocated Department WIP to Individual Units Allocate Allocate Trace Allocate Trace Trace Allocate or Allocate

Direct Materials

Overhead Indirect materials, indirect labor, direct department costs such as supervisor salary and equipment depreciation, and other costs such as rent and plant insurance

Direct Labor

Individual Units of

Product or Service

Department Work in Process

Direct

Materials

Conversion Costs

Transferred-in

Costs Previous

Department WIP

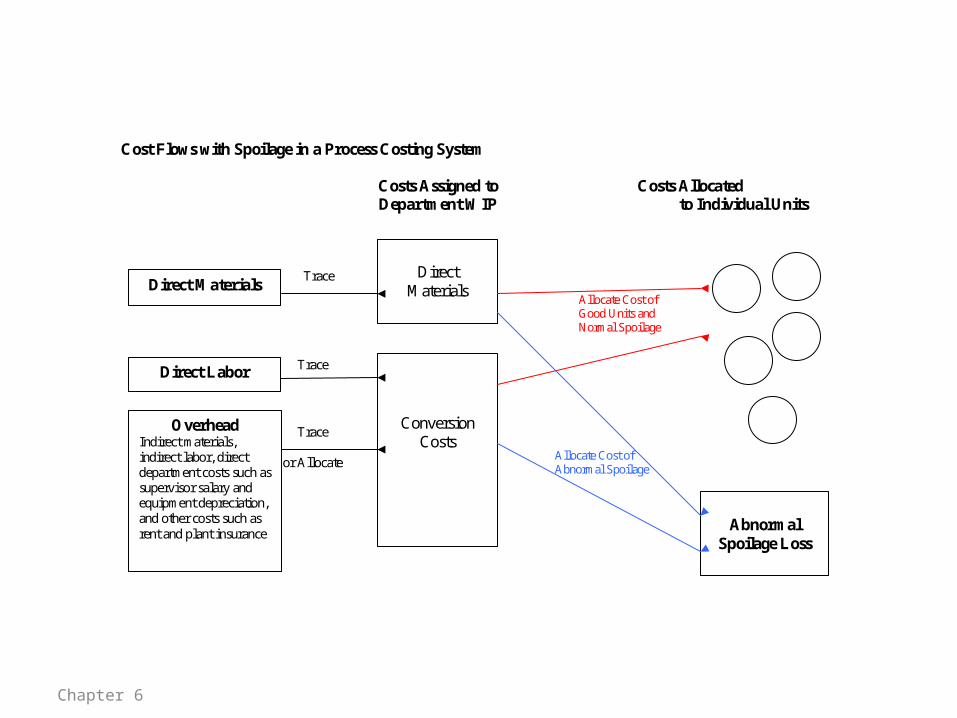

How Are Spoilage Costs Handled in Process Costing?

Normal Spoilage:Defective units that arise as part of regular operations

Abnormal Spoilage:Spoilage that is not part of everyday operations

Chapter 6

Chapter 6

Cost Flows with Spoilage in a Process Costing System Costs Assigned to Costs Allocated Department WIP to Individual Units Trace Trace Trace or Allocate

Direct Materials

Overhead Indirect materials, indirect labor, direct department costs such as supervisor salary and equipment depreciation, and other costs such as rent and plant insurance

Direct Labor

Direct

Materials

Conversion Costs

Abnormal

Spoilage Loss

Allocate Cost of Good Units and Normal Spoilage

Allocate Cost of Abnormal Spoilage

Use Process Cost Information to:

• Measure costs of products mass-produced products• Assign costs to inventory and cost of goods sold for

financial statements and income tax returns• Monitor operations and costs• Develop estimates of future costs for decision

making• Analyze the costs and benefits of quality

improvements• Identify potential areas for process improvements

Chapter 6

Uncertainties and Measurement Errors in Process Costing

Actual cost flows might not be known:* When are direct materials added?* When are conversion costs incurred?* How complete are the units in ending work in process?* What amount of spoilage is normal?

Chapter 6