compare standard to fifo costing oaug cost management sig june 18, 2013

TRANSCRIPT

Compare Standard to FIFO Costing

OAUG Cost Management SIGJune 18, 2013

2

Contents -

Presenter Introduction What is EBS Discrete FIFO Costing? EBS Standard and FIFO: A Comparison FIFO Cost - Implementation Considerations Change from Standard to FIFO Cost Org Question and Answer

3

Presenter Introduction - Dave Sweas, CPA

Senior Solution Architect - MarketSphere Consulting, LLC EBS functional experience: Since 1995 (Industry, Big 5, middle

market consultancies) EBS Concentration: Core Financials, Discrete Cost, Project

Mfg., OPM Cost/SLA, Cost Management SLA Industry experience: General Accountant, FA, AP, Budgets,

Cost Accounting Manager, Plant Controller, Supply Chain Cost Analyst, Profitability Analyst

Advisory approach to implementation Core strength: Converting “ERP/EBS-speak” into accountant-

friendly language

4

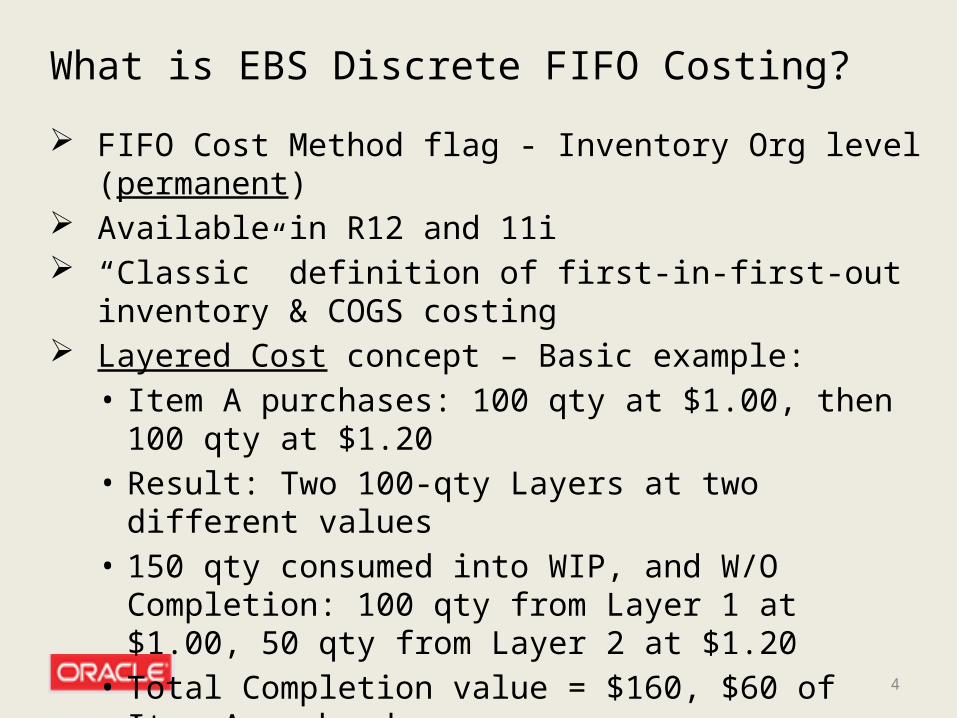

What is EBS Discrete FIFO Costing? FIFO Cost Method flag - Inventory Org level (permanent) Available in R12 and 11i “Classic” definition of first-in-first-out inventory & COGS costing Layered Cost concept – Basic example:

• Item A purchases: 100 qty at $1.00, then 100 qty at $1.20 • Result: Two 100-qty Layers at two different values• 150 qty consumed into WIP, and W/O Completion: 100 qty

from Layer 1 at $1.00, 50 qty from Layer 2 at $1.20• Total Completion value = $160, $60 of Item A on-hand

5

What is EBS Discrete FIFO Costing? Applies to all items within a FIFO Org Costing method only; not automatically tied to

physical flow of goods Seeded Cost Types: “FIFO” and “FIFO Rates” Key inquiries and reports: Layered Cost Transaction Detail,

Layered Cost Elemental Report, Item Cost History, MADS / MADD detail (the latter is same report as in Std Cost Org)

See next section for Standard to FIFO comparison

6

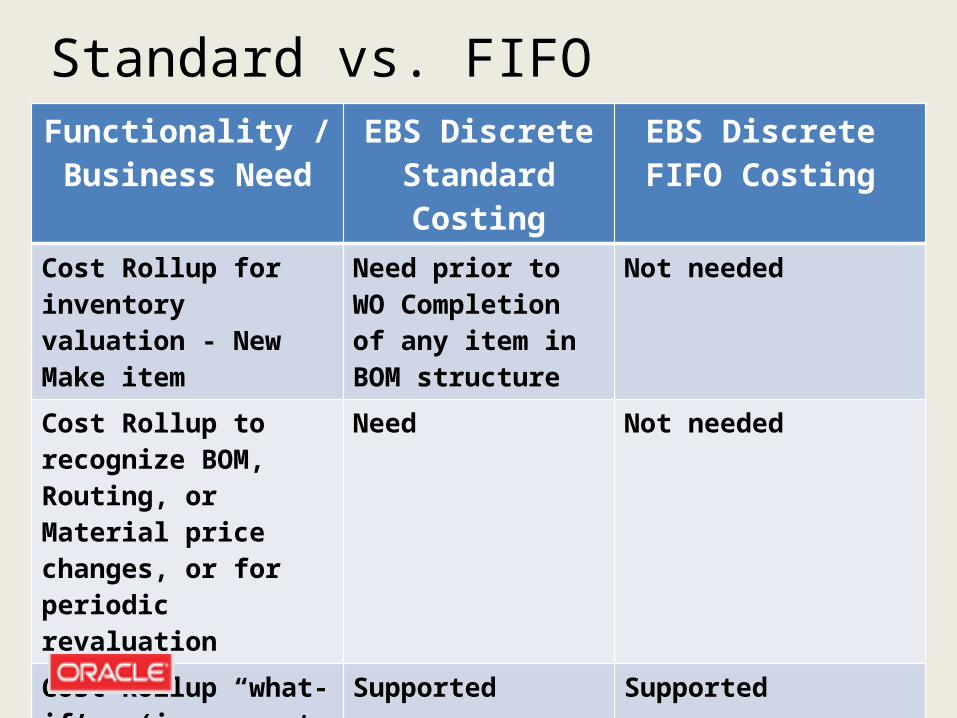

EBS Standard and FIFO: A Comparison

7

Functionality / Business Need

EBS Discrete Standard Costing

EBS Discrete FIFO Costing

Cost Rollup for inventory valuation - New Make item

Need prior to WO Completion of any item in BOM structure

Not needed

Cost Rollup to recognize BOM, Routing, or Material price changes, or for periodic revaluation

Need Not needed

Cost Rollup “what-if’s” (in separate Cost Types)

Supported Supported

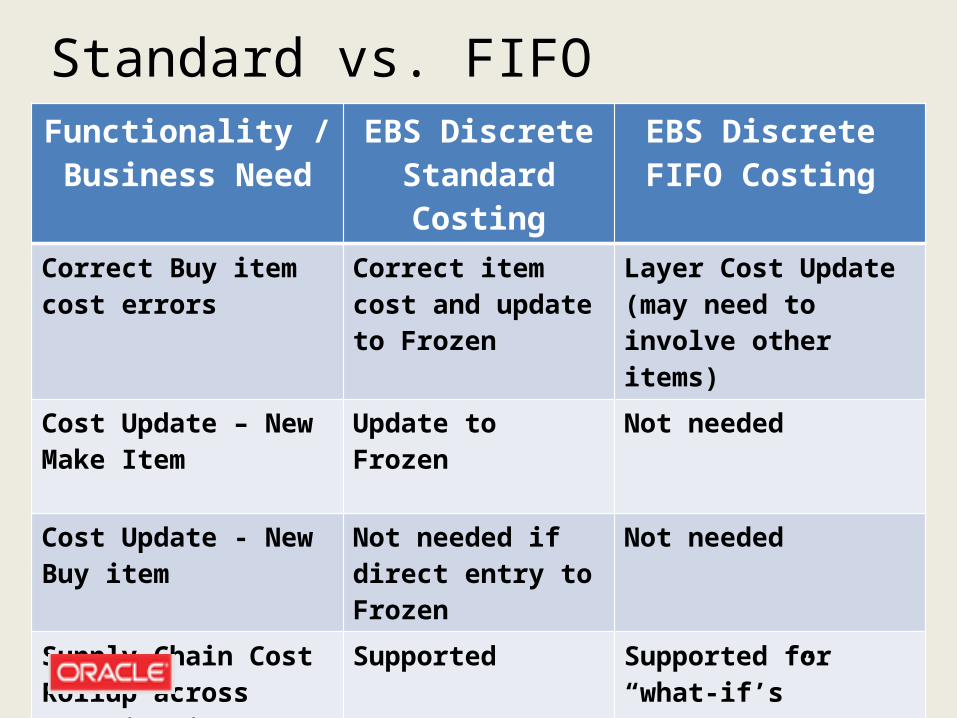

Correct Make item cost errors

Cost Rollup Layer Cost Update (may need to involve other items)

Standard vs. FIFO

8

Functionality / Business Need

EBS Discrete Standard Costing

EBS Discrete FIFO Costing

Correct Buy item cost errors

Correct item cost and update to Frozen

Layer Cost Update (may need to involve other items)

Cost Update – New Make Item

Update to Frozen Not needed

Cost Update - New Buy item

Not needed if direct entry to Frozen

Not needed

Supply Chain Cost Rollup across Organizations

Supported Supported for “what-if’s”

Standard vs. FIFO

9

Functionality / Business Need

EBS Discrete Standard Costing

EBS Discrete FIFO Costing

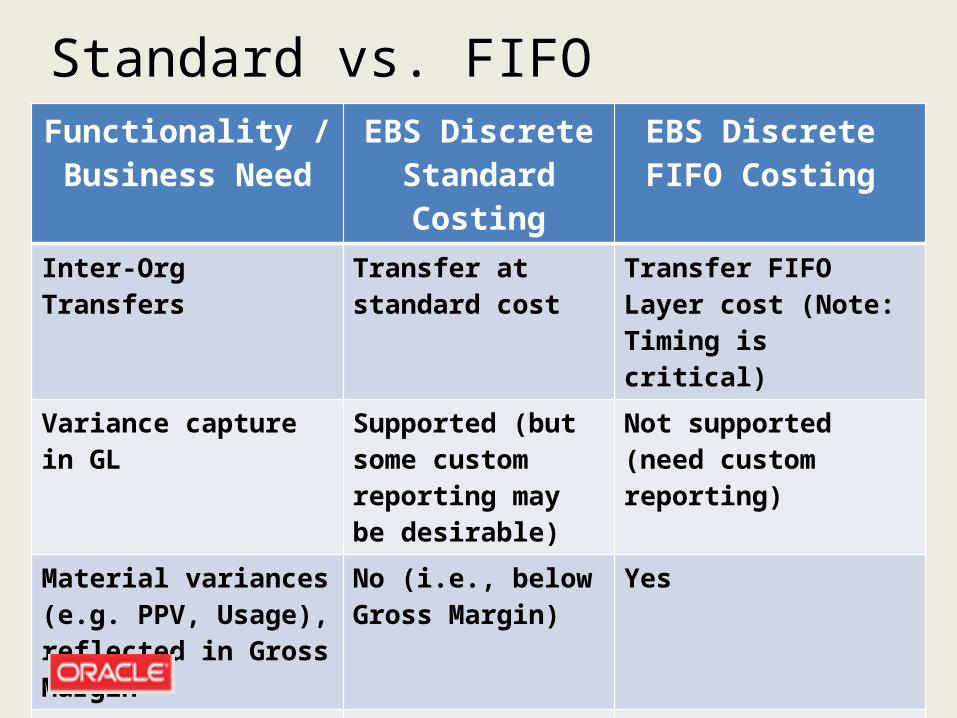

Inter-Org Transfers Transfer at standard cost

Transfer FIFO Layer cost (Note: Timing is critical)

Variance capture in GL Supported (but some custom reporting may be desirable)

Not supported (need custom reporting)

Material variances (e.g. PPV, Usage), reflected in Gross Margin

No (i.e., below Gross Margin)

Yes

PO price maintenance impact

Inaccuracies fall through as PPV, no effect on Assembly costs

Inaccuracies affect related Assembly costs

Standard vs. FIFO

10

Functionality / Business Need

EBS Discrete Standard Costing

EBS Discrete FIFO Costing

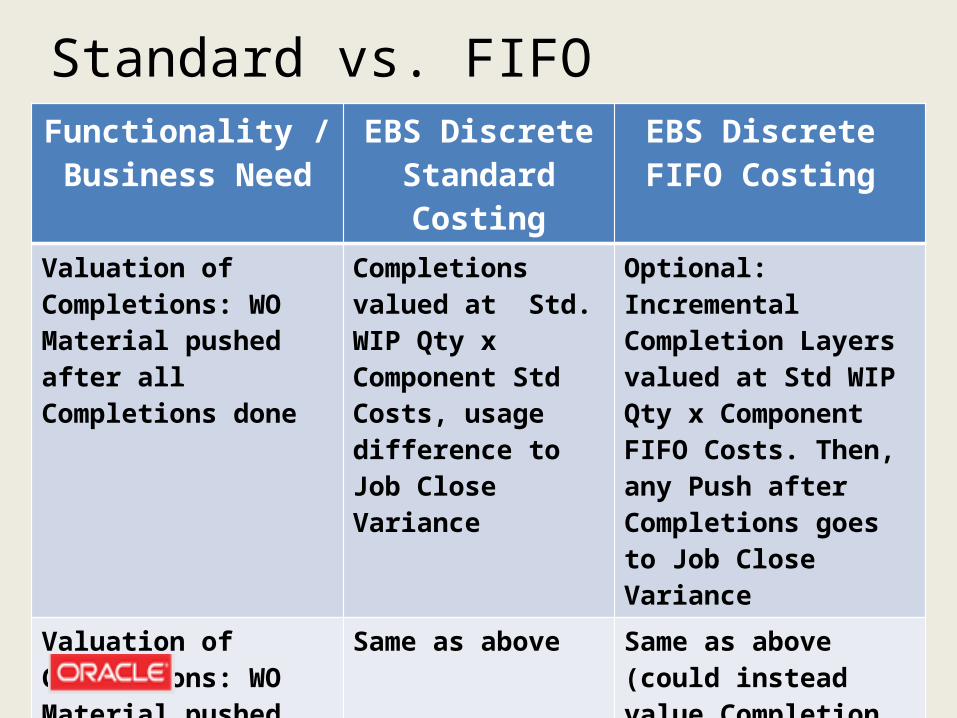

Valuation of Completions: WO Material pushed after all Completions done

Completions valued at Std. WIP Qty x Component Std Costs, usage difference to Job Close Variance

Optional: Incremental Completion Layers valued at Std WIP Qty x Component FIFO Costs. Then, any Push after Completions goes to Job Close Variance

Valuation of Completions: WO Material pushed during Completions

Same as above Same as above (could instead value Completion at value of Material push)

Valuation of Completions: WO Material backflush

Completions valued at Std. WIP Qty x Component Std Costs

Completions valued at Std. WIP Qty x Component FIFO Costs

Standard vs. FIFO

11

Functionality / Business Need

EBS Discrete Standard Costing

EBS Discrete FIFO Costing

Manual labor charge after incremental Completion (Resource Charge Type = Manual)

Inv valuation = Std Qty x Std Resource Rate, diff vs. std to Job Close Variance

Inv valuation = $0 for Layer built from that Completion, labor $$ to Job Close Variance

Labor charge when Resource Charge Type = WIP Move

Inv valuation = Routing Qty x Resource Rate

Same way as Standard

BS inventory valuation (GAAP, / L-C-M, IFRS, etc.)

Need separate FIFO reserve

Accepted (Note: Get up-front auditor verification)

Periodic inventory valuation at actual cost (via Cost Mass Edit)

Supported (via Cost Mass Edit and rollup at BOM and Rtg qtys)

Not needed

Standard vs. FIFO

12

Functionality / Business Need

EBS Discrete Standard Costing

EBS Discrete FIFO Costing

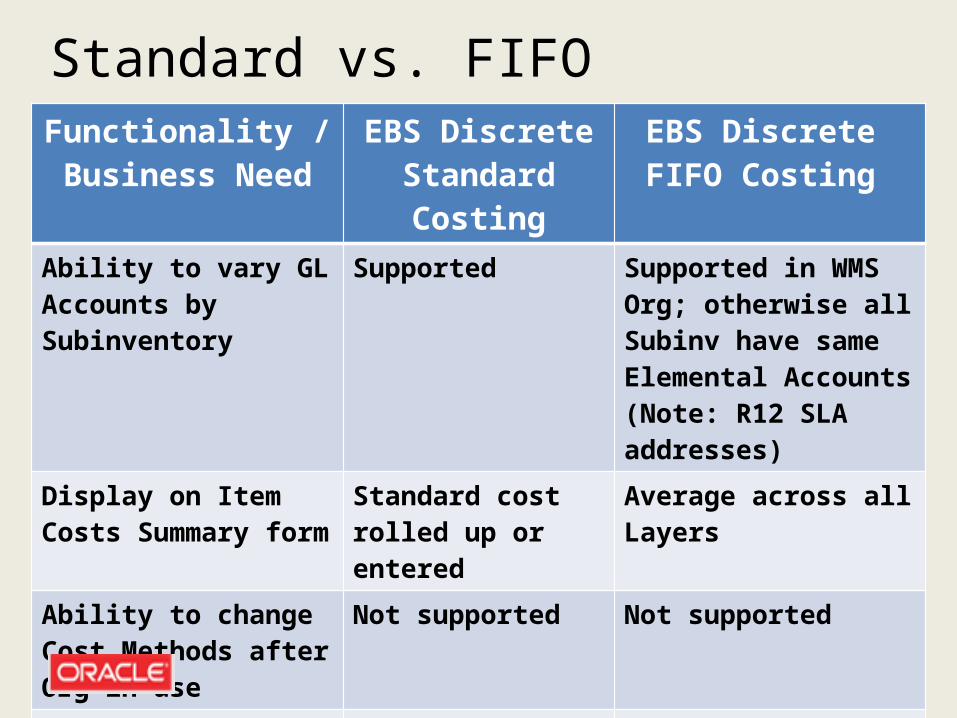

Ability to vary GL Accounts by Subinventory

Supported Supported in WMS Org; otherwise all Subinv have same Elemental Accounts (Note: R12 SLA addresses)

Display on Item Costs Summary form

Standard cost rolled up or entered

Average across all Layers

Ability to change Cost Methods after Org in use

Not supported Not supported

MOH absorption, MOH Defaults (e.g. MOH based on % of Material cost)

Supported Supported

Standard vs. FIFO

13

Functionality / Business Need

EBS Discrete Standard Costing

EBS Discrete FIFO Costing

Outside Processing - Inventory valuation

Supported (inventory valuation at Std qty x Std Resource Rate)

Supported (inventory Layer valuation at WO OSP qty x PO price)

Cost Copy – Items, Resources, OH)

Supported Supported (including from FIFO and FIFO Rates Cost Types)

COGS Recognition Deferred COGS debit upon ship, run three Concurrent Requests to move $$ to COGS

Same as Standard

R12 Cost Management-SLA – Setups and Create Accounting

Feature Feature

Standard vs. FIFO

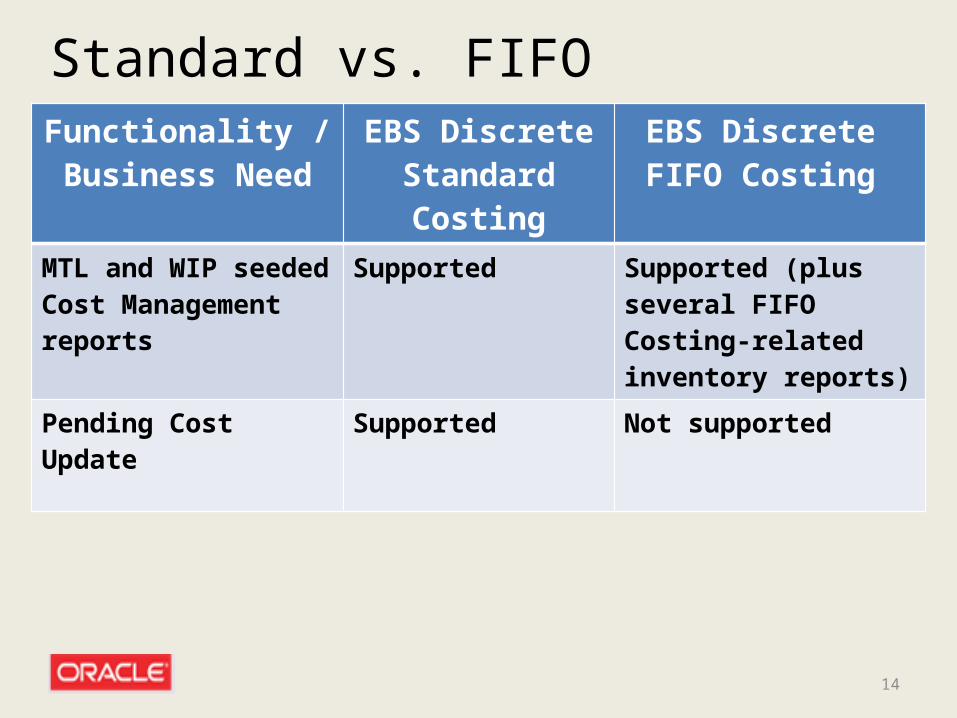

14

Functionality / Business Need

EBS Discrete Standard Costing

EBS Discrete FIFO Costing

MTL and WIP seeded Cost Management reports

Supported Supported (plus several FIFO Costing-related inventory reports)

Pending Cost Update Supported Not supported

Standard vs. FIFO

15

FIFO Cost - Implementation Considerations

16

Current Landscape – Discrete Manufacturers

Fluctuating raw material prices, escalation in recent years Material cost avg. 65-80% of COGS value Competitive - Hold line on pricing --“margin squeeze” Need for improved GM/contribution margin info greater than

ever PPV – Often largest variance vs. standard; difficult to

meaningfully allocate to COGS Limitations of EBS period-end actual costing model Accounting departments- Expectation with ERP: “Do more

with same / fewer resources” Lean concepts being driven firm-wide

17

FIFO Cost Org: Key Factors to Consider

Discrete Org Cost Methods are permanent Overall PO price maintenance – Critical BOM / Routing maintenance up-to-date? Cost Rollups (what-if’s, new products, etc.) can

be run in a FIFO Org In general: The fewer the raw material SKU’s and

greater the price fluctuations, the better the fit In general: The more backflush, the better the fit

18

FIFO Cost Org: Key Factors to Consider

Process automation - Cost accounting (FIFO = no Rollup for new products, eliminates revaluation)

The more Resources = WIP Move, better the fit Variance capture in GL needed? Variances for

management reporting purposes only? Conduct cost method requirements workshop, all

parties involved Beware of “accepting the past” (challenge long-

time accounting processes)

19

FIFO Cost Org: Key Factors to Consider

Focus on COGS valuation (less so on inventory valuation):•COGS – Analysis •Inventory - Reporting

FIFO costing may not be acceptable for some industries

Consult internal / external auditors first: e.g., GAAP- & IFRS-compliance, prior year restatement considerations, relevancy of physical flow of goods

20

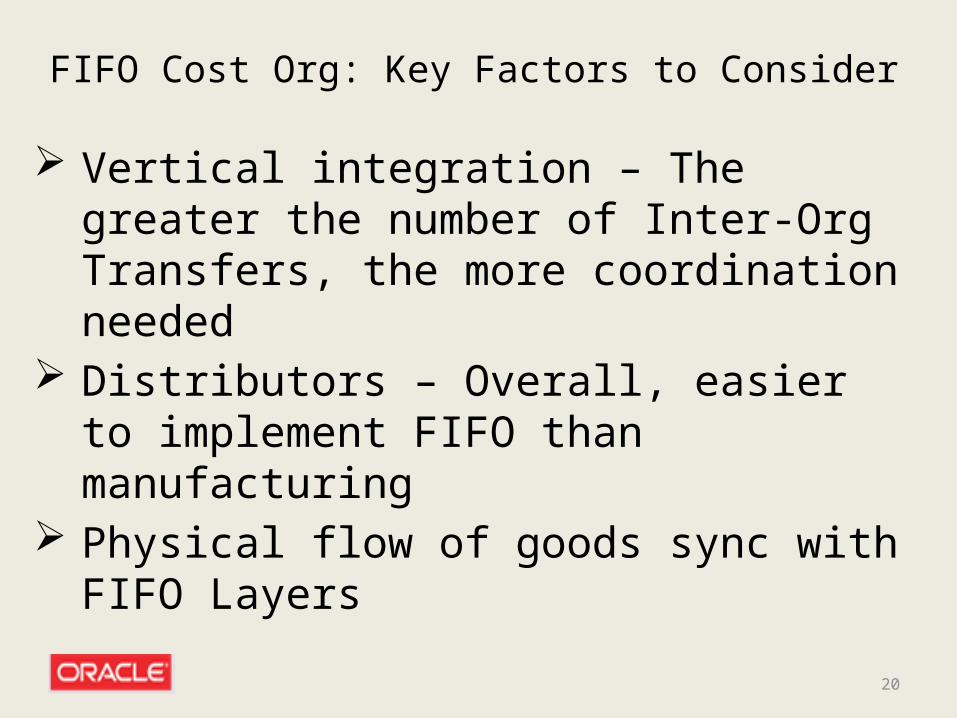

FIFO Cost Org: Key Factors to Consider

Vertical integration – The greater the number of Inter-Org Transfers, the more coordination needed

Distributors – Overall, easier to implement FIFO than manufacturing

Physical flow of goods sync with FIFO Layers

21

FIFO Costing and Physical Flow of Goods EBS FIFO Layers are consumed without regard to Lots,

Serial Numbers, etc. or other physical flow Within normal range of inventory turns, in a discrete

manufacturing environment the difference tends to be acceptable:• All factors (variances) considered, generally more

comprehensive COGS valuation than standard costing

• Other factors (low number of raw materials, back-flush vs. push) can offset need to match Material flow with Cost Layer consumption

22

Change from Standard to FIFO Cost Org

23

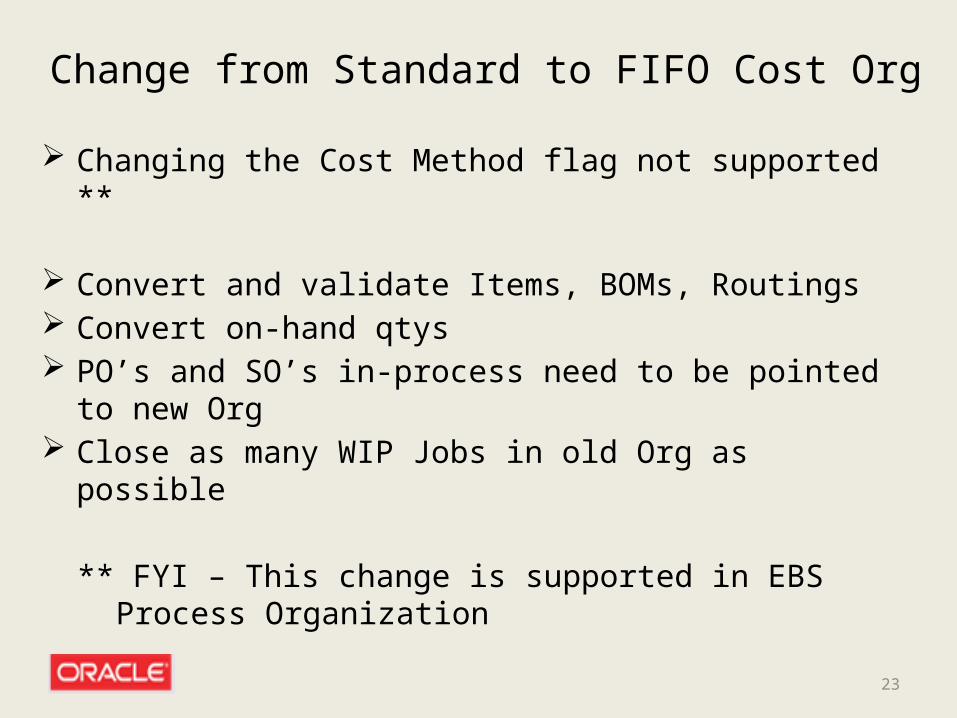

Change from Standard to FIFO Cost Org

Changing the Cost Method flag not supported **

Convert and validate Items, BOMs, Routings Convert on-hand qtys PO’s and SO’s in-process need to be pointed to new

Org Close as many WIP Jobs in old Org as possible

** FYI – This change is supported in EBS Process Organization

Question & Answer

24