prnhx new horizons fund prjix new horizons …individual.troweprice.com/gcfiles/pdf/arnhf.pdfproof...

TRANSCRIPT

Proof #4

December 31, 2017

PRNHX

PRJIX

ANNUALREPORT

New Horizons Fund

New Horizons Fund– I Class

T. Rowe PRICe

The fund invests in small-cap, emerging growth companies that are early in their corporate life cycles.

Proof #4

REPORTS ON THE WEB

Sign up for our Email Program, and you can begin to receive updated fund reports and prospectuses online rather than through the mail. Log in to your account at troweprice.com for more information.

HIGHLIGHTS

• Mostmajorstockindexesfinishedtheyearnearrecordlevelsamidexpectationsthatthenewtaxlawwouldliftcorporateearningsandaddtoeconomicgrowthin2018.

• TheNewHorizonsFundposteda31.49%returninthe12-monthreportingperiod,outperformingitsbenchmarkandLipperpeergroupindex.

• Inthisletter,weanalyzethekeydriversofthefund’sperformanceoverthepasteightyearsanddiscusshowourinvestmentprocesscanbeimprovedtodrivefutureperformance.

• Thecurrentenvironmentisseeminglyidealforequities,withsolidandimprovinggrowthpairedwithfiscalstimulusthatisencouraginginvestorstoacceptahigherlevelofrisk.Evenso,weareawarethatwearelateinthecycleandthatvaluationsarehighrelativetotraditionalmetrics.

T. Rowe Price New Horizons Fund

TheviewsandopinionsinthisreportwerecurrentasofDecember31,2017.They are not guarantees of performance or investment results andshouldnotbe takenas investmentadvice. Investmentdecisionsreflectavarietyof factors,and themanagers reserve the right tochange theirviews about individual stocks, sectors, and the markets at any time.As a result, the views expressed should not be relied upon as a fore-castof the fund’s future investment intent.Thereport iscertifiedunderthe Sarbanes-Oxley Act, which requiresmutual funds and other publiccompanies to affirm that, to the best of their knowledge, the informa-tionintheirfinancialreportsisfairlyandaccuratelystatedinallmaterialrespects.

Proof #4

T. Rowe Price New Horizons Fund

Manager’s Letter

1

Fellow Shareholders

Your fund solidly outperformed its benchmark and peer group and returned more

than 31% in the 12-month reporting period. Our performance is the result of our

philosophy and investment process throughout the years. In this letter, we will

seek to further illustrate our innovative approach to investing in private companies

and how we engage our early-stage growth companies in building a durable and

sustainable business.

PERfORmaNcE REvIEW

The New Horizons Fund returned 31.49% for the year ended December 31, 2017, outperforming the 22.17% return of its bench-mark, the Russell 2000 Growth Index, as a result of stock selection.

The fund also outpaced the Lipper Small-Cap Growth Funds Index, which generated a 24.77% return. (Performance for the I Class shares will vary due to its different fee structure and other factors.) The New Horizons Fund was in the top 2% of its Lipper small-cap growth funds peer group for the trailing 5- and 10-year periods ended December 31, 2017.

Based on cumulative total return, Lipper ranked the New Horizons Fund 66 of 558, 46 of 502, 6 of 457, and 1 of 342 small-cap growth funds for the 1-, 3-, 5-, and 10-year periods ended December 31, 2017, respectively. (Results may vary for other periods. Past performance cannot guarantee future results.)

TotalReturnPeriodsEnded12/31/17 6Months 12Months

NewHorizonsFund 11.60% 31.49%

NewHorizonsFund–IClass 11.68 31.67

Russell2000GrowthIndex 11.09 22.17

Russell2000Index 9.20 14.65

S&P500Index 11.42 21.83

S&PMidCap400Index 9.68 16.24

LipperSmall-CapGrowthFundsIndex 12.43 24.77

Performance Comparison

Proof #4

2

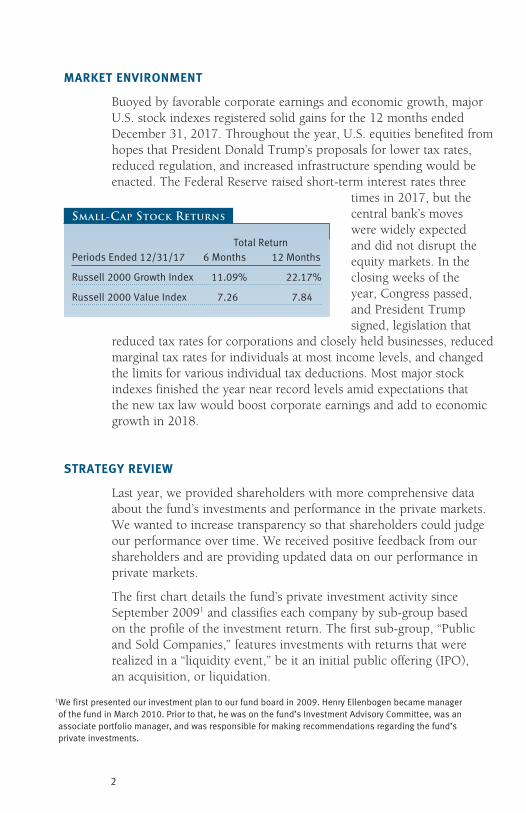

maRkET ENvIRONmENT

Buoyed by favorable corporate earnings and economic growth, major U.S. stock indexes registered solid gains for the 12 months ended December 31, 2017. Throughout the year, U.S. equities benefited from hopes that President Donald Trump’s proposals for lower tax rates, reduced regulation, and increased infrastructure spending would be enacted. The Federal Reserve raised short-term interest rates three

times in 2017, but the central bank’s moves were widely expected and did not disrupt the equity markets. In the closing weeks of the year, Congress passed, and President Trump signed, legislation that

reduced tax rates for corporations and closely held businesses, reduced marginal tax rates for individuals at most income levels, and changed the limits for various individual tax deductions. Most major stock indexes finished the year near record levels amid expectations that the new tax law would boost corporate earnings and add to economic growth in 2018.

STRaTEGy REvIEW

Last year, we provided shareholders with more comprehensive data about the fund’s investments and performance in the private markets. We wanted to increase transparency so that shareholders could judge our performance over time. We received positive feedback from our shareholders and are providing updated data on our performance in private markets.

The first chart details the fund’s private investment activity since September 20091 and classifies each company by sub-group based on the profile of the investment return. The first sub-group, “Public and Sold Companies,” features investments with returns that were realized in a “liquidity event,” be it an initial public offering (IPO), an acquisition, or liquidation.

1Wefirstpresentedourinvestmentplantoourfundboardin2009.HenryEllenbogenbecamemanagerofthefundinMarch2010.Priortothat,hewasonthefund’sInvestmentAdvisoryCommittee,wasanassociateportfoliomanager,andwasresponsibleformakingrecommendationsregardingthefund’sprivateinvestments.

TotalReturnPeriodsEnded12/31/17 6Months 12Months

Russell2000GrowthIndex 11.09% 22.17%

Russell2000ValueIndex 7.26 7.84

Small-Cap Stock Returns

Proof #4

3

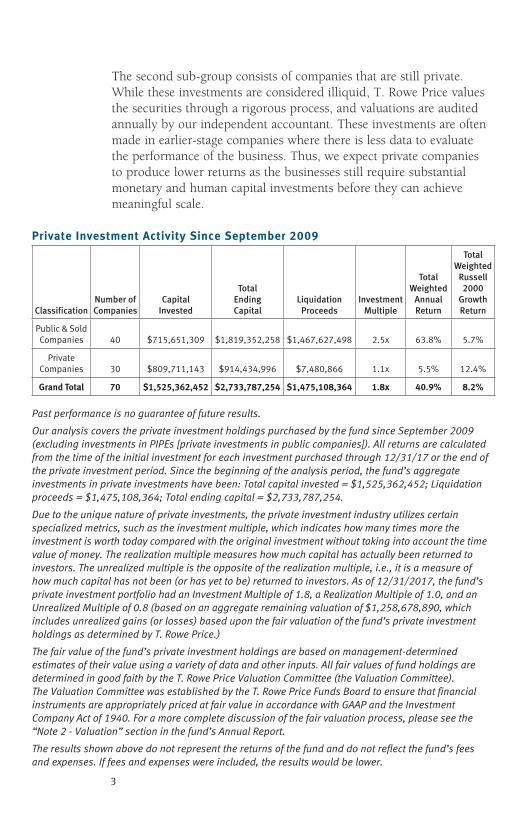

The second sub-group consists of companies that are still private. While these investments are considered illiquid, T. Rowe Price values the securities through a rigorous process, and valuations are audited annually by our independent accountant. These investments are often made in earlier-stage companies where there is less data to evaluate the performance of the business. Thus, we expect private companies to produce lower returns as the businesses still require substantial monetary and human capital investments before they can achieve meaningful scale.

Private Investment activity Since September 2009

ClassificationNumber of Companies

Capital Invested

Total Ending Capital

Liquidation Proceeds

Investment Multiple

Total Weighted

Annual Return

Total Weighted

Russell 2000

Growth Return

Public&SoldCompanies 40 $715,651,309 $1,819,352,258 $1,467,627,498 2.5x 63.8% 5.7%

PrivateCompanies 30 $809,711,143 $914,434,996 $7,480,866 1.1x 5.5% 12.4%

Grand Total 70 $1,525,362,452 $2,733,787,254 $1,475,108,364 1.8x 40.9% 8.2%

Past performance is no guarantee of future results.

Our analysis covers the private investment holdings purchased by the fund since September 2009 (excluding investments in PIPEs [private investments in public companies]). All returns are calculated from the time of the initial investment for each investment purchased through 12/31/17 or the end of the private investment period. Since the beginning of the analysis period, the fund’s aggregate investments in private investments have been: Total capital invested = $1,525,362,452; Liquidation proceeds = $1,475,108,364; Total ending capital = $2,733,787,254.

Due to the unique nature of private investments, the private investment industry utilizes certain specialized metrics, such as the investment multiple, which indicates how many times more the investment is worth today compared with the original investment without taking into account the time value of money. The realization multiple measures how much capital has actually been returned to investors. The unrealized multiple is the opposite of the realization multiple, i.e., it is a measure of how much capital has not been (or has yet to be) returned to investors. As of 12/31/2017, the fund’s private investment portfolio had an Investment Multiple of 1.8, a Realization Multiple of 1.0, and an Unrealized Multiple of 0.8 (based on an aggregate remaining valuation of $1,258,678,890, which includes unrealized gains (or losses) based upon the fair valuation of the fund’s private investment holdings as determined by T. Rowe Price.)

The fair value of the fund’s private investment holdings are based on management-determined estimates of their value using a variety of data and other inputs. All fair values of fund holdings are determined in good faith by the T. Rowe Price Valuation Committee (the Valuation Committee). The Valuation Committee was established by the T. Rowe Price Funds Board to ensure that financial instruments are appropriately priced at fair value in accordance with GAAP and the Investment Company Act of 1940. For a more complete discussion of the fair valuation process, please see the “Note 2 - Valuation” section in the fund’s Annual Report.

The results shown above do not represent the returns of the fund and do not reflect the fund’s fees and expenses. If fees and expenses were included, the results would be lower.

Proof #4

4

“Total Weighted Annual Return” represents the annualized returns of our private security holdings by evaluating the cash flows of the securities over the periods indicated: taking into account any drawdowns, distributions, income, or dividends; the timing of our investments; and the investment’s final value (if any). This is equivalent to a money-weighted daily internal rate of return (IRR).

“Total Weighted Russell 2000 Growth Return” represents the results of the Russell 2000 Growth Index adjusted to mirror the capital inflows and outflows of our private investments (money-weighted daily IRR). The adjustment is intended to make the comparison between our private investment activities and the Index more meaningful.

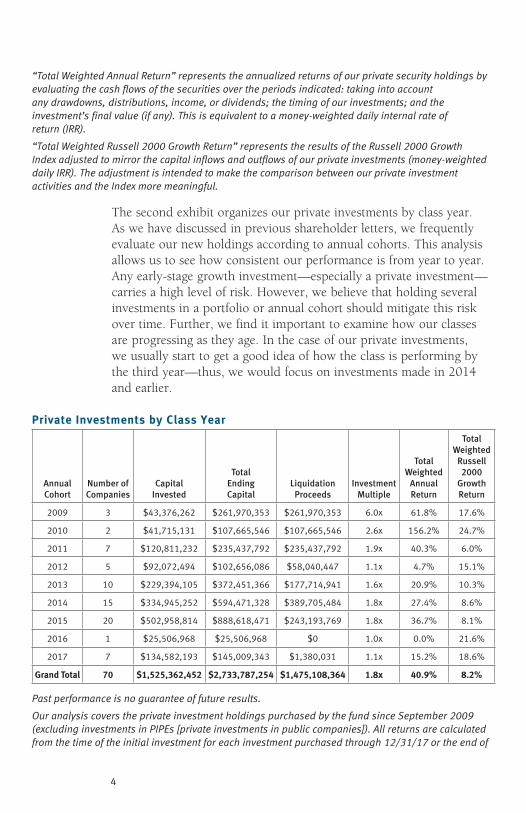

The second exhibit organizes our private investments by class year. As we have discussed in previous shareholder letters, we frequently evaluate our new holdings according to annual cohorts. This analysis allows us to see how consistent our performance is from year to year. Any early-stage growth investment—especially a private investment—carries a high level of risk. However, we believe that holding several investments in a portfolio or annual cohort should mitigate this risk over time. Further, we find it important to examine how our classes are progressing as they age. In the case of our private investments, we usually start to get a good idea of how the class is performing by the third year—thus, we would focus on investments made in 2014 and earlier.

Private Investments by class year

Annual Cohort

Number of Companies

Capital Invested

Total Ending Capital

Liquidation Proceeds

Investment Multiple

Total Weighted

Annual Return

Total Weighted

Russell 2000

Growth Return

2009 3 $43,376,262 $261,970,353 $261,970,353 6.0x 61.8% 17.6%

2010 2 $41,715,131 $107,665,546 $107,665,546 2.6x 156.2% 24.7%

2011 7 $120,811,232 $235,437,792 $235,437,792 1.9x 40.3% 6.0%

2012 5 $92,072,494 $102,656,086 $58,040,447 1.1x 4.7% 15.1%

2013 10 $229,394,105 $372,451,366 $177,714,941 1.6x 20.9% 10.3%

2014 15 $334,945,252 $594,471,328 $389,705,484 1.8x 27.4% 8.6%

2015 20 $502,958,814 $888,618,471 $243,193,769 1.8x 36.7% 8.1%

2016 1 $25,506,968 $25,506,968 $0 1.0x 0.0% 21.6%

2017 7 $134,582,193 $145,009,343 $1,380,031 1.1x 15.2% 18.6%

Grand Total 70 $1,525,362,452 $2,733,787,254 $1,475,108,364 1.8x 40.9% 8.2%

Past performance is no guarantee of future results.

Our analysis covers the private investment holdings purchased by the fund since September 2009 (excluding investments in PIPEs [private investments in public companies]). All returns are calculated from the time of the initial investment for each investment purchased through 12/31/17 or the end of

Proof #4

5

the private investment period. Since the beginning of the analysis period, the fund’s aggregate investments in private investments have been: Total capital invested = $1,525,362,452; Liquidation proceeds = $1,475,108,364; Total ending capital = $2,733,787,254.

Due to the unique nature of private investments, the private investment industry utilizes certain specialized metrics, such as the investment multiple, which indicates how many times more the investment is worth today compared with the original investment without taking into account the time value of money. The realization multiple measures how much capital has actually been returned to investors. The unrealized multiple is the opposite of the realization multiple, i.e., it is a measure of how much capital has not been (or has yet to be) returned to investors. As of 12/31/2017, the fund’s private investment portfolio had an Investment Multiple of 1.8, a Realization Multiple of 1.0, and an Unrealized Multiple of 0.8 (based on an aggregate remaining valuation of $1,258,678,890, which includes unrealized gains (or losses) based upon the fair valuation of the fund’s private investment holdings as determined by T. Rowe Price.)

The fair value of the fund’s private investment holdings are based on management-determined estimates of their value using a variety of data and other inputs. All fair values of fund holdings are determined in good faith by the T. Rowe Price Valuation Committee (the “Valuation Committee”). The Valuation Committee was established by the T. Rowe Price Funds Board to ensure that financial instruments are appropriately priced at fair value in accordance with GAAP and the Investment Company Act of 1940. For a more complete discussion of the fair valuation process, please see the “Note 2 - Valuation” section in the fund’s Annual Report.

The results shown above do not represent the returns of the fund and do not reflect the fund’s fees and expenses. If fees and expenses were included, the results would be lower.

“Total Weighted Annual Return” represents the annualized returns of our private security holdings by evaluating the cash flows of the securities over the periods indicated: taking into account any drawdowns, distributions, income, or dividends; the timing of our investments; and the investment’s final value (if any). This is equivalent to a money-weighted daily internal rate of return (IRR).

“Total Weighted Russell 2000 Growth Return” represents the results of the Russell 2000 Growth Index adjusted to mirror the capital inflows and outflows of our private investments (money-weighted daily IRR). The adjustment is intended to make the comparison between our private investment activities and the Index more meaningful.

As we have stated in the past, we view our private investing as an extension of our early-stage growth investing discipline and not as a distinct practice. In past shareholder letters, we discussed our Act I and Act II framework for early-stage growth investing. Our goal is to buy shares in our successful early-stage growth companies as their stock price is rising, but in our view, has not yet peaked. We call this “dollar cost averaging up.” One of the principal reasons we invest in private companies is to encourage them to think about scale in people, processes, or systems. Often, our best contribution is introducing companies to outside executives who understand the concept of scale. We have seen a number of situations in which companies decided to add these executives to their boards. Chewy, one of the fund’s leading performers in 2017, is a good example of this in practice. After our initial 2014 investment in Chewy, we introduced the company’s chief executive to an entrepreneur who had been directly involved with two

Proof #4

6

successful companies in which our fund had invested. The company later decided to bring him on as chairman. We believe this move contributed to Chewy’s success scaling its business and teams, which resulted in its $3.35 billion acquisition by PetSmart in mid-2017. (Please refer to the fund’s portfolio of investments for a complete list of holdings and the amount each represents in the portfolio.)

In 2017, three of the top 10 contributors to the fund’s performance were private investments, including CarGurus (class of 2015), GrubHub (class of 2014), and Atlassian (class of 2014). Of note, we generated substantially more value for shareholders by holding Atlassian and GrubHub as public companies than as private investments. We believe this is consistent with our philosophy of holding on to our winners.

When looking at the top contributors to the fund’s outperformance (alpha) versus the Russell 2000 Growth Index benchmark over the trailing five-year period, we found that the top 10 securities were responsible for 86% of our total alpha generation over the past five years, and the top 20 contributed 130%—meaning that the results of this group were partially offset by the performance of other holdings. The takeaway from the fund’s performance is clear—wealth creation is concentrated among a select few winners over long periods.

The study “Do Stocks Outperform Treasury Bills” by Hendrik Bessembinder of Arizona State University2 supports this notion, finding that the entire gain in the U.S. stock market since 19263 was attributable to fewer than the best-performing 4% of listed stocks and the average stock matched the return on the one-month Treasury bill. The idea of letting your winners run is more of an empirical fact than a heuristic for investing—the mathematical reality is that selling a scarce winner dramatically increases the probability that proceeds are deployed in lower-quality, lower-expected-return assets over time.

2Bessembinder,Hendrik,“DoStocksOutperformTreasuryBills”ArizonaStateUniversity(2017)p.20.3BasedontheCenterforResearchinSecurityPricesmonthlystockreturndatabase,whichcontainsallcommonlistedstocksontheNYSE,AMEX,andNASDAQexchangesfrom1926-2015.

Proof #4

7

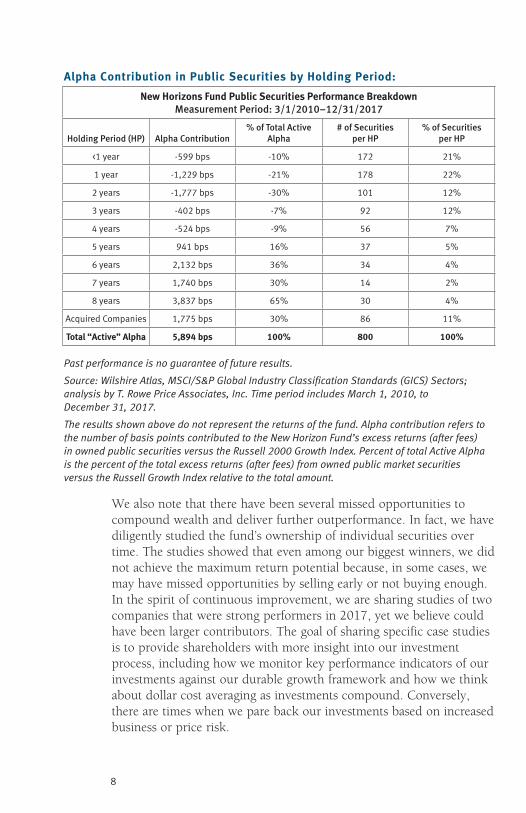

Next, we provide an analysis of the fund’s performance to quantify the importance of compounding returns since I began managing the fund. The chart delineates the performance of the individual public companies owned by the fund from March 1, 2010, to December 31, 2017, based on the length of our holding period for each investment. The maximum holding period is eight years, commensurate with my tenure as portfolio manager. Companies that were acquired are represented in the acquired company’s cohort as the holding periods were influenced by the sale rather than our decision to exit at that time.

We offer a few observations based on these data. First, we prune our holdings over time as we observe our companies develop and, as a result, we expect to own significantly fewer companies over the longer term. Second, as companies transition from early-stage growth to an Act II or prove themselves to be a durable growth company, we let compounding work in our favor by purchasing more stock at higher prices. Thus, we anticipate that our outperformance will be concentrated in holdings that we believe are worth owning for many years. Consistent with the academic literature cited above, we believe the best approach is to let compounding drive the best companies over time. For example, only 115 securities were held for a period of five years or more. This group of 115 securities contributed 147% of the fund’s excess return, after fees and versus its benchmark, generated in public securities over the period. We also note that there were 44 securities owned for seven years or more, and those contributed 95% of the fund’s excess return from public stock selection versus the benchmark.

Proof #4

8

alpha contribution in Public Securities by Holding Period:

New Horizons fund Public Securities Performance Breakdown Measurement Period: 3/1/2010–12/31/2017

Holding Period (HP) Alpha Contribution% of Total Active

Alpha# of Securities

per HP% of Securities

per HP

<1year -599bps -10% 172 21%

1year -1,229bps -21% 178 22%

2years -1,777bps -30% 101 12%

3years -402bps -7% 92 12%

4years -524bps -9% 56 7%

5years 941bps 16% 37 5%

6years 2,132bps 36% 34 4%

7years 1,740bps 30% 14 2%

8years 3,837bps 65% 30 4%

AcquiredCompanies 1,775bps 30% 86 11%

Total “active” alpha 5,894 bps 100% 800 100%

Past performance is no guarantee of future results.

Source: Wilshire Atlas, MSCI/S&P Global Industry Classification Standards (GICS) Sectors; analysis by T. Rowe Price Associates, Inc. Time period includes March 1, 2010, to December 31, 2017.

The results shown above do not represent the returns of the fund. Alpha contribution refers to the number of basis points contributed to the New Horizon Fund’s excess returns (after fees) in owned public securities versus the Russell 2000 Growth Index. Percent of total Active Alpha is the percent of the total excess returns (after fees) from owned public market securities versus the Russell Growth Index relative to the total amount.

We also note that there have been several missed opportunities to compound wealth and deliver further outperformance. In fact, we have diligently studied the fund’s ownership of individual securities over time. The studies showed that even among our biggest winners, we did not achieve the maximum return potential because, in some cases, we may have missed opportunities by selling early or not buying enough. In the spirit of continuous improvement, we are sharing studies of two companies that were strong performers in 2017, yet we believe could have been larger contributors. The goal of sharing specific case studies is to provide shareholders with more insight into our investment process, including how we monitor key performance indicators of our investments against our durable growth framework and how we think about dollar cost averaging as investments compound. Conversely, there are times when we pare back our investments based on increased business or price risk.

Proof #4

9

Vail Resorts was the top holding at the end of 2017 as well as a top contributor to the fund’s performance for the period ended December 31, 2017. We initiated our position in Vail Resorts between 2010 and 2012 believing that Vail offered a unique investment opportunity that could benefit from a cyclical recovery in skier visits. The company had introduced an attractive season pass program that was allowing it to gain local and regional market share. By 2014, the stock had nearly doubled, and we opted to sell about 10% of our position, following an unexpectedly strong earnings report and an announcement that Vail would acquire Park City Mountain Resort. It is easy to be critical of those stock sales with the benefit of hindsight. First, the 2014 fiscal year results showed that season pass sales had stabilized Vail’s financial performance despite a historically weak ski season in Tahoe, where Vail has two ski resorts. Second, the acquisition of Park City expanded Vail’s ski network, which made the season pass even more attractive to customers.

Over the following year, we did further due diligence. Our work showed that when Vail reported its results for 2015—the first year Park City was included in the network—season pass sales growth accelerated. Furthermore, the company gained more scale against its fixed costs to improve margins, increase the customer experience, and improve return on invested capital for shareholders. Following this bottom-up analysis, the fund increased its position in Vail by about 15% at an average cost of $125, or more than triple our historical average purchase price, and separately acquired about a 10% ownership stake in Whistler Blackcomb. We believed that Vail could pay a substantial premium to Whistler’s prevailing share price and still generate an attractive return for shareholders. Vail acquired Whistler Blackcomb in 2016 for cash and stock, which further increased our ownership stake in Vail by about 17%.

Fortunately, we didn’t miss the opportunity to create value through dollar cost averaging up with this stock. We learned two valuable lessons from the Vail acquisition. First, we need to anticipate events and potential outcomes. Second, we should recognize that changes and improvements can be nonlinear, especially when buying into a network. As to the first point, we weren’t well prepared to analyze the Park City acquisition but sharpened our focus in anticipation of Vail’s purchase of Whistler. Regarding the second point, we learned that when a company has taken steps to improve its network and monetize assets in new ways, its durability can improve.

Proof #4

10

The fund initially invested in GrubHub through a private placement in mid-2013 before its IPO in late 2014. GrubHub was a top 15 position at the end of 2017, and it was a top five contributor to the fund’s performance over the past year.

We invested in GrubHub because we expected the food delivery market was poised for strong growth over the next several years and was also essential for growth in the restaurant market. While restaurants were facing numerous headwinds—including flat or declining same-store sales growth in 2018 and rising labor costs—we believed that online food ordering and delivery would be an area of continued strong secular growth. What was occurring in the broader food delivery market was akin to what happened to the pizza industry in the 1980s. Over the next decade, pizza delivery increased tenfold.

Following the IPO, the fund materially increased its position in GrubHub. We expected that the company would perform well in a large market with strong secular tailwinds, that the service would become more attractive to customers after it added more restaurants, and that there would be significant margin improvement as the business grew over time. In 2015, GrubHub invested in its Act II as the company recognized the need to offer delivery services and more restaurant selection for its customers. Under its legacy business model, GrubHub had focused on connecting customers and restaurants but not the delivery element. GrubHub invested about $20 million in 2015 to build out local delivery networks in major cities. But the company’s ability to create such a network from scratch was far from certain given the number of well-funded companies already aggressively competing in this space. As a result, GrubHub’s stock price remained under pressure.

Our challenge was to balance our fundamental conviction that the food delivery space was poised for rapid growth with our assessment of GrubHub’s ability to successfully transition to its Act II. In early 2017, we gained conviction that GrubHub had navigated this transition. As a result, we materially increased our investment, and subsequently, GrubHub further added value by acquiring marketplace competitors that were unable to make the transition to delivery.

This example demonstrates the need for early-stage growth companies to continuously invest in the business. The market is typically skeptical of these investment periods in which there is greater uncertainty about the potential outcomes. While we remain positive about our GrubHub investment thesis, we must continue to track our assumptions and be able to dispassionately process new information when making the next investment decision.

Proof #4

11

PORTfOLIO REvIEW

Our top contributor in 2017 was CBOE Global Markets, which operates the largest U.S. options exchange. CBOE’s acquisition of BATS Global Markets brought CBOE’s culture of innovation and proprietary products, including volatility and S&P 500 contracts, under the same roof with BATS’ strong technology culture. After thorough due diligence following the acquisition, we came to believe the combination of CBOE and BATS was a unique acquisition that increased value above the combination of two platforms. Our experience is that the best deals happen when the acquisition renders the whole company more valuable. We felt the BATS product and technology skills would improve the combined company. In late 2017, the market recognized this powerful combination and rewarded the stock throughout the year.

Burlington Stores was a meaningful contributor to the fund’s performance. The off-price retailer is in the early innings of refining its business model by improving its systems and store base. We believe Burlington is on the right side of a powerful secular trend as traffic and available inventory flows migrate from department stores and traditional retailers to the off-price channel. There are clear threats from Amazon and other e-commerce retailers, but the Burlington business model should prove to be relatively insulated given lower order costs, fast inventory turnover, and average selling prices that are lower than those of similar products at Amazon. We believe Burlington can sustain its current pace of new-store growth. Burlington is also positioned to benefit from the continued wave of bankruptcies and store closures across the brick-and-mortar retail space, which will allow Burlington to negotiate lower rents and improved terms.

O’Reilly Automotive was a detractor from performance as the auto parts retailer endured a challenging year. The first three quarters of 2017 were mixed due to execution issues, a broad industry slowdown, and concerns over irrational competition and heightened terminal value risk regarding the secular shift online. The disruption created by online retailers became more apparent across the industry as comparable same-store sales growth decelerated. Despite this secular backdrop, we remain positive on the company’s superior service culture, the inventory required to meet customer demands, the need for immediate delivery in the commercial business-to-business market, and the positive financial characteristics of the business. We continue to monitor our thesis for this company, and for all of our holdings, as new information becomes available.

Proof #4

12

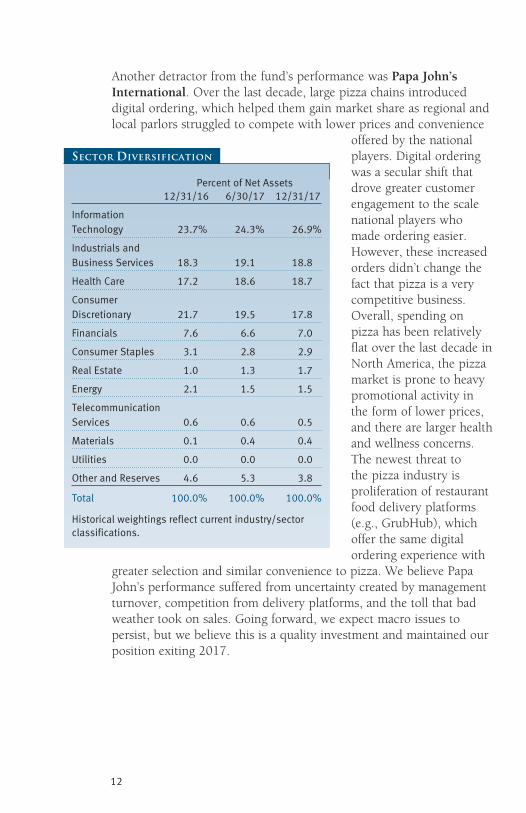

Another detractor from the fund’s performance was Papa John’s International. Over the last decade, large pizza chains introduced digital ordering, which helped them gain market share as regional and local parlors struggled to compete with lower prices and convenience

offered by the national players. Digital ordering was a secular shift that drove greater customer engagement to the scale national players who made ordering easier. However, these increased orders didn’t change the fact that pizza is a very competitive business. Overall, spending on pizza has been relatively flat over the last decade in North America, the pizza market is prone to heavy promotional activity in the form of lower prices, and there are larger health and wellness concerns. The newest threat to the pizza industry is proliferation of restaurant food delivery platforms (e.g., GrubHub), which offer the same digital ordering experience with

greater selection and similar convenience to pizza. We believe Papa John’s performance suffered from uncertainty created by management turnover, competition from delivery platforms, and the toll that bad weather took on sales. Going forward, we expect macro issues to persist, but we believe this is a quality investment and maintained our position exiting 2017.

PercentofNetAssets 12/31/16 6/30/17 12/31/17

InformationTechnology 23.7% 24.3% 26.9%

IndustrialsandBusinessServices 18.3 19.1 18.8

HealthCare 17.2 18.6 18.7

ConsumerDiscretionary 21.7 19.5 17.8

Financials 7.6 6.6 7.0

ConsumerStaples 3.1 2.8 2.9

RealEstate 1.0 1.3 1.7

Energy 2.1 1.5 1.5

TelecommunicationServices 0.6 0.6 0.5

Materials 0.1 0.4 0.4

Utilities 0.0 0.0 0.0

OtherandReserves 4.6 5.3 3.8

Total 100.0% 100.0% 100.0%

Historicalweightingsreflectcurrentindustry/sectorclassifications.

Sector Diversification

Proof #4

13

OuTLOOk

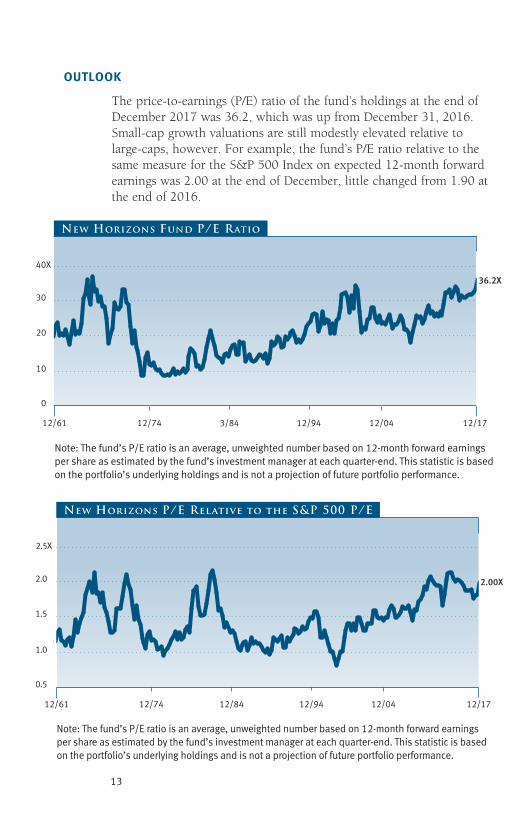

The price-to-earnings (P/E) ratio of the fund’s holdings at the end of December 2017 was 36.2, which was up from December 31, 2016. Small-cap growth valuations are still modestly elevated relative to large-caps, however. For example, the fund’s P/E ratio relative to the same measure for the S&P 500 Index on expected 12-month forward earnings was 2.00 at the end of December, little changed from 1.90 at the end of 2016.

12/61 12/1712/74 3/84 12/94 12/04

20

10

0

30

40X

New Horizons Fund P/E Ratio

Note: The fund’s P/E ratio is an average, unweighted number based on 12-month forward earnings per share as estimated by the fund’s investment manager at each quarter-end. This statistic is based on the portfolio’s underlying holdings and is not a projection of future portfolio performance.

36.2X

12/61 12/1712/74 12/84 12/94 12/04

1.5

1.0

0.5

2.0

2.5X

New Horizons P/E Relative to the S&P 500 P/E

Note: The fund’s P/E ratio is an average, unweighted number based on 12-month forward earnings per share as estimated by the fund’s investment manager at each quarter-end. This statistic is based on the portfolio’s underlying holdings and is not a projection of future portfolio performance.

2.00X

Proof #4

14

Market leadership is likely to narrow as the bull market ages. As always, unforeseen risks, such as geopolitical turmoil, also pose challenges. Global macroeconomic events, including commodity price volatility, could affect performance, and the escalation of tensions with North Korea is a particular risk. We are also on the lookout for a regulatory attack on leading technology and Internet firms, which could have unintended consequences and result in increased concerns with regard to inflation. As such, we will closely monitor global economic and political conditions and be cautious around new bouts of risk taking. Nevertheless, we remain confident in our ability to find and hold smaller companies that can compound wealth by becoming durable and sustainable businesses, even through the downturns and valuation adjustments that are part of every market cycle.

Thank you for investing with T. Rowe Price.

Respectfully submitted,

Henry EllenbogenPresident of the fund and chairman of its Investment Advisory Committee

January 25, 2018

The committee chairman has day-to-day responsibility for managing the portfolio and works with committee members in developing and executing the fund’s investment program.

Proof #4

15

T. Rowe Price New Horizons Fund

Risks of Investing

Aswithallstockandbondmutualfunds,eachfund’ssharepricecanfallbecauseofweaknessinthestockorbondmarkets,aparticularindustry,orspecificholdings.Stockmarketscandeclineformanyreasons,includingadversepoliticaloreconomicdevelopments,changesininvestorpsychology,orheavyinstitutionalselling.Theprospectsforanindustryorcompanymaydeterioratebecauseofavarietyoffactors,includingdisappointingearningsorchangesinthecompetitiveenvironment.Inaddition,theinvestmentmanager’sassessmentofcompaniesheldinafundmayproveincorrect,resultinginlossesorpoorperformanceeveninrisingmarkets.

Investinginsmallcompaniesinvolvesgreaterriskthaniscustomarilyassociatedwithlargercompanies.Stocksofsmallcompaniesaresubjecttomoreabruptorerraticpricemovementsthanlarger-companystocks.Smallcompaniesoftenhavelimitedproductlines,markets,orfinancialresources,andtheirmanagementsmaylackdepthandexperience.Suchcompaniesseldompaysignificantdividendsthatcouldcushionreturnsinafallingmarket.

Glossary

alpha:Excessreturnabovethatofthebenchmark.

Dollar cost averaging:Aninvestmenttechniqueofbuyingafixeddollaramountofaparticularinvestmentonaregularschedule,regardlessoftheshareprice.

Initial public offering:Thefirstsaleofstocktothepublicbyaformerlyprivatecompany.

Lipper indexes:Fundbenchmarksthatconsistofasmallnumber(10to30)ofthelargestmutualfundsinaparticularcategoryastrackedbyLipperInc.

Price/book ratio:Avaluationmeasurethatcomparesastock’smarketpricewithitsbookvalue;i.e.,thecompany’snetworthdividedbythenumberofoutstandingshares.

Price/earnings (P/E) ratio:Avaluationmeasurecalculatedbydividingthepriceofastockbyitscurrentorprojectedearningspershare.Theratioisameasureofhowmuchinvestorsarewillingtopayforthecompany’searnings.

Russell 2000 Growth Index:Anindexthattrackstheperformanceofsmall-capstockswithhigherprice-to-bookratiosandhigherforecastgrowthvalues.

Russell 2000 Index:Anunmanagedindexthattracksthestocksof2,000smallU.S.companies.

Proof #4

16

T. Rowe Price New Horizons Fund

Glossary (continued)

Russell 2000 value Index:Anindexthattrackstheperformanceofsmall-capstockswithlowerprice-to-bookratiosandlowerforecastgrowthvalues.

S&P 500 Index:Anunmanagedindexthattracksthestocksof500primarilylarge-capU.S.companies.

S&P midcap 400 Index:Anunmanagedindexthattrackstheperformanceof400U.S.mid-capcompanies.

Note:RussellInvestmentGroupisthesourceandownerofthetrademarks,servicemarks,andcopyrightsrelatedtotheRussellindexes.Russell®isatrademarkofRussellInvestmentGroup.

Proof #4

17

T. Rowe Price New Horizons Fund

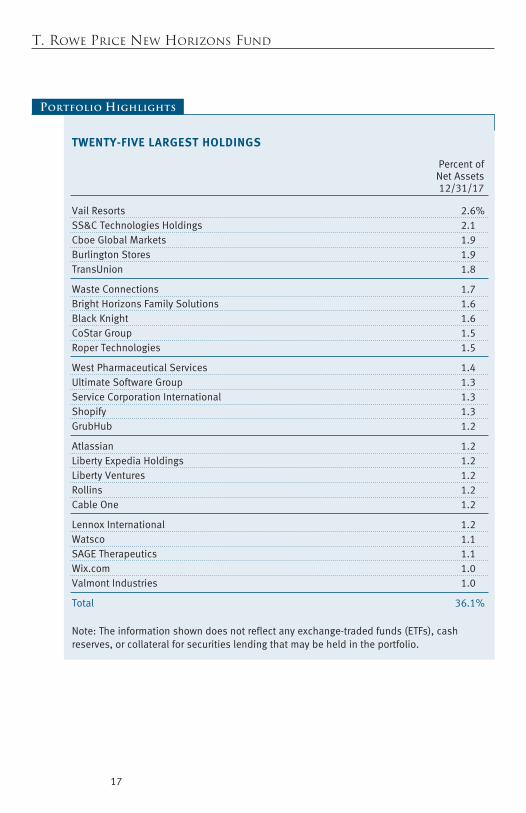

TWENTy-fIvE LaRGEST HOLDINGS

Percentof NetAssets 12/31/17

VailResorts 2.6%SS&CTechnologiesHoldings 2.1CboeGlobalMarkets 1.9BurlingtonStores 1.9TransUnion 1.8

WasteConnections 1.7BrightHorizonsFamilySolutions 1.6BlackKnight 1.6CoStarGroup 1.5RoperTechnologies 1.5

WestPharmaceuticalServices 1.4UltimateSoftwareGroup 1.3ServiceCorporationInternational 1.3Shopify 1.3GrubHub 1.2

Atlassian 1.2LibertyExpediaHoldings 1.2LibertyVentures 1.2Rollins 1.2CableOne 1.2

LennoxInternational 1.2Watsco 1.1SAGETherapeutics 1.1Wix.com 1.0ValmontIndustries 1.0

Total 36.1%

Note:Theinformationshowndoesnotreflectanyexchange-tradedfunds(ETFs),cashreserves,orcollateralforsecuritieslendingthatmaybeheldintheportfolio.

Portfolio Highlights

Proof #4

18

T. Rowe Price New Horizons Fund

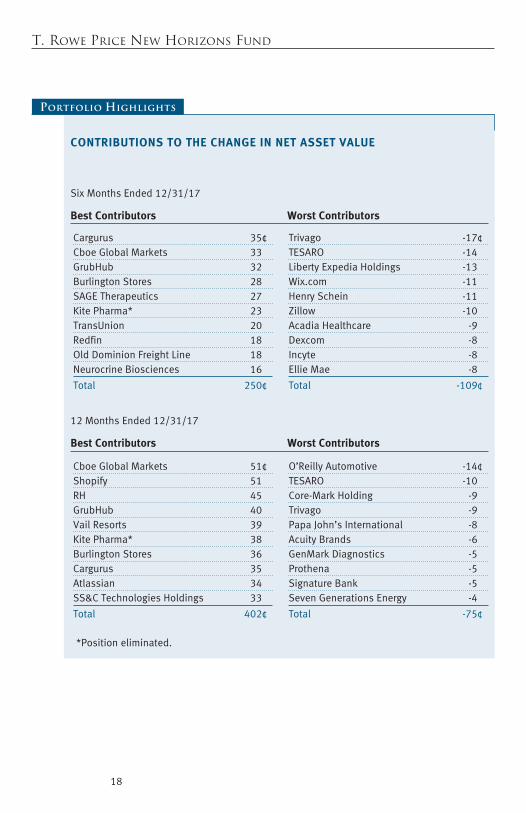

cONTRIBuTIONS TO THE cHaNGE IN NET aSSET vaLuE

SixMonthsEnded12/31/17

Best contributors Worst contributors

Cargurus 35¢CboeGlobalMarkets 33GrubHub 32BurlingtonStores 28SAGETherapeutics 27KitePharma* 23TransUnion 20Redfin 18OldDominionFreightLine 18NeurocrineBiosciences 16

Total 250¢

Trivago -17¢TESARO -14LibertyExpediaHoldings -13Wix.com -11HenrySchein -11Zillow -10AcadiaHealthcare -9Dexcom -8Incyte -8EllieMae -8

Total -109¢

12MonthsEnded12/31/17

Best contributors Worst contributors

CboeGlobalMarkets 51¢Shopify 51RH 45GrubHub 40VailResorts 39KitePharma* 38BurlingtonStores 36Cargurus 35Atlassian 34SS&CTechnologiesHoldings 33

Total 402¢

O’ReillyAutomotive -14¢TESARO -10Core-MarkHolding -9Trivago -9PapaJohn’sInternational -8AcuityBrands -6GenMarkDiagnostics -5Prothena -5SignatureBank -5SevenGenerationsEnergy -4

Total -75¢

*Positioneliminated.

Portfolio Highlights

Proof #4

19

T. Rowe Price New Horizons Fund

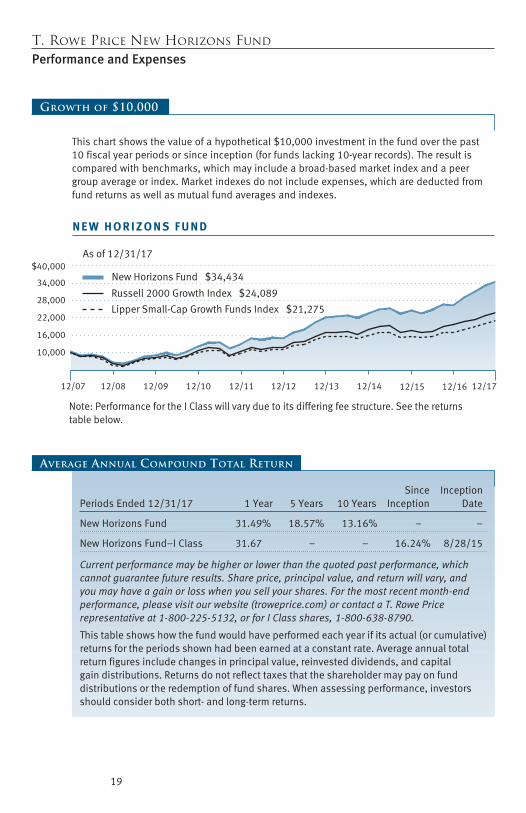

Performance and Expenses

Russell 2000 Growth Index $24,089

New Horizons Fund $34,434

As of 12/31/17

12/07 12/1312/1212/1112/1012/0912/08 12/1712/14

N E W H O R I Z O N S F U N D

Lipper Small-Cap Growth Funds Index $21,275

10,000

16,000

22,000

28,000

34,000

$40,000

12/15 12/16

Note: Performance for the I Class will vary due to its differing fee structure. See the returnstable below.

Growth of $10,000

Thischartshowsthevalueofahypothetical$10,000investmentinthefundoverthepast10fiscalyearperiodsorsinceinception(forfundslacking10-yearrecords).Theresultiscomparedwithbenchmarks,whichmayincludeabroad-basedmarketindexandapeergroupaverageorindex.Marketindexesdonotincludeexpenses,whicharedeductedfromfundreturnsaswellasmutualfundaveragesandindexes.

Since InceptionPeriodsEnded12/31/17 1Year 5Years 10Years Inception Date

NewHorizonsFund 31.49% 18.57% 13.16% – –

NewHorizonsFund–IClass 31.67 – – 16.24% 8/28/15

Current performance may be higher or lower than the quoted past performance, which cannot guarantee future results. Share price, principal value, and return will vary, and you may have a gain or loss when you sell your shares. For the most recent month-end performance, please visit our website (troweprice.com) or contact a T. Rowe Price representative at 1-800-225-5132, or for I Class shares, 1-800-638-8790.

Thistableshowshowthefundwouldhaveperformedeachyearifitsactual(orcumulative)returnsfortheperiodsshownhadbeenearnedataconstantrate.Averageannualtotalreturnfiguresincludechangesinprincipalvalue,reinvesteddividends,andcapitalgaindistributions.Returnsdonotreflecttaxesthattheshareholdermaypayonfunddistributionsortheredemptionoffundshares.Whenassessingperformance,investorsshouldconsiderbothshort-andlong-termreturns.

Average Annual Compound Total Return

Proof #4

20

T. Rowe Price New Horizons Fund

Fund Expense Example

Asamutualfundshareholder,youmayincurtwotypesofcosts:(1)transactioncosts,suchasredemptionfeesorsalesloads,and(2)ongoingcosts,includingmanagementfees,distributionandservice(12b-1)fees,andotherfundexpenses.Thefollowingexampleisintendedtohelpyouunderstandyourongoingcosts(indollars)ofinvestinginthefundandtocomparethesecostswiththeongoingcostsofinvestinginothermutualfunds.Theexampleisbasedonaninvestmentof$1,000investedatthebeginningofthemostrecentsix-monthperiodandheldfortheentireperiod.

Pleasenotethatthefundhastwoshareclasses:Theoriginalshareclass(InvestorClass)chargesnodistributionandservice(12b-1)fee,andtheIClasssharesarealsoavailabletoinstitutionallyorientedclientsandimposeno12b-1oradministrativefeepayment.Eachshareclassispresentedseparatelyinthetable.

actual ExpensesThefirstlineofthefollowingtable(Actual)providesinformationaboutactualaccountvaluesandexpensesbasedonthefund’sactualreturns.Youmayusetheinformationonthisline,togetherwithyouraccountbalance,toestimatetheexpensesthatyoupaidovertheperiod.Simplydivideyouraccountvalueby$1,000(forexample,an$8,600accountvaluedividedby$1,000=8.6),thenmultiplytheresultbythenumberonthefirstlineundertheheading“ExpensesPaidDuringPeriod”toestimatetheexpensesyoupaidonyouraccountduringthisperiod.

Hypothetical Example for comparison PurposesTheinformationonthesecondlineofthetable(Hypothetical)isbasedonhypotheticalaccountvaluesandexpensesderivedfromthefund’sactualexpenseratioandanassumed5%peryearrateofreturnbeforeexpenses(notthefund’sactualreturn).Youmaycomparetheongoingcostsofinvestinginthefundwithotherfundsbycontrastingthis5%hypotheticalexampleandthe5%hypotheticalexamplesthatappearintheshareholderreportsoftheotherfunds.Thehypotheticalaccountvaluesandexpensesmaynotbeusedtoestimatetheactualendingaccountbalanceorexpensesyoupaidfortheperiod.

NewHorizonsFund 0.79%

NewHorizonsFund–IClass 0.65

Theexpenseratioshownisasofthefund’sfiscalyearended12/31/16.Thisnumbermayvaryfromtheexpenseratioshownelsewhereinthisreportbecauseitisbasedonadifferenttimeperiodand,ifapplicable,includesacquiredfundfeesandexpensesbutdoesnotincludefeeorexpensewaivers.

Expense Ratio

Proof #4

21

T. Rowe Price New Horizons Fund

Fund Expense Example (continued)

Note:T.RowePricechargesanannualaccountservicefeeof$20,generallyforaccountswithlessthan$10,000.ThefeeiswaivedforanyinvestorwhoseT.RowePricemutualfundaccountstotal$50,000ormore;accountselectingtoreceiveelectronicdeliveryofaccountstatements,transactionconfirmations,prospectuses,andshareholderreports;oraccountsofaninvestorwhoisaT.RowePricePersonalServicesorEnhancedPersonalServicesclient(enrollmentintheseprogramsgenerallyrequiresT.RowePriceassetsofatleast$250,000).Thisfeeisnotincludedintheaccompanyingtable.Ifyouaresubjecttothefee,keepitinmindwhenyouareestimatingtheongoingexpensesofinvestinginthefundandwhencomparingtheexpensesofthisfundwithotherfunds.

Youshouldalsobeawarethattheexpensesshowninthetablehighlightonlyyourongoingcostsanddonotreflectanytransactioncosts,suchasredemptionfeesorsalesloads.Therefore,thesecondlineofthetableisusefulincomparingongoingcostsonlyandwillnothelpyoudeterminetherelativetotalcostsofowningdifferentfunds.Totheextentafundchargestransactioncosts,however,thetotalcostofowningthatfundishigher.

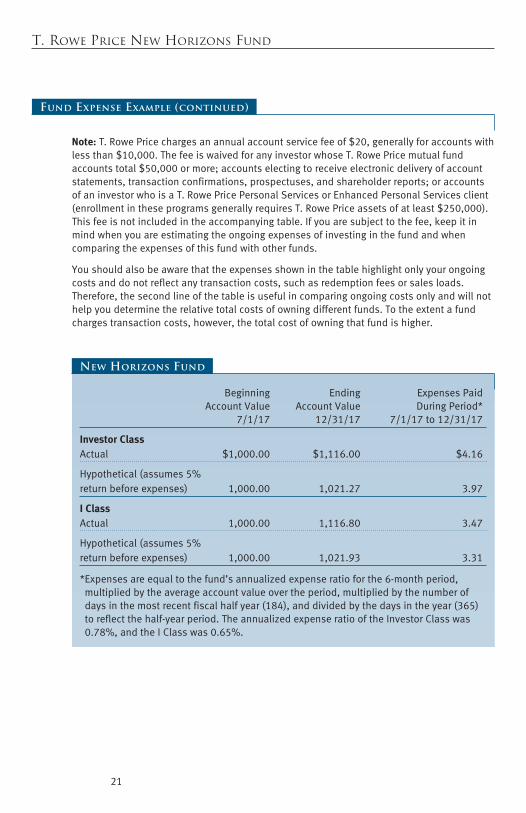

Beginning Ending ExpensesPaid AccountValue AccountValue DuringPeriod* 7/1/17 12/31/17 7/1/17to12/31/17

Investor classActual $1,000.00 $1,116.00 $4.16

Hypothetical(assumes5%returnbeforeexpenses) 1,000.00 1,021.27 3.97

I classActual 1,000.00 1,116.80 3.47

Hypothetical(assumes5%returnbeforeexpenses) 1,000.00 1,021.93 3.31

*Expensesareequaltothefund’sannualizedexpenseratioforthe6-monthperiod,multipliedbytheaverageaccountvalueovertheperiod,multipliedbythenumberofdaysinthemostrecentfiscalhalfyear(184),anddividedbythedaysintheyear(365)toreflectthehalf-yearperiod.TheannualizedexpenseratiooftheInvestorClasswas0.78%,andtheIClasswas0.65%.

New Horizons Fund

Proof #4

22

T. Rowe Price New Horizons Fund

Financial Highlights For a share outstanding throughout each period

The accompanying notes are an integral part of these financial statements.

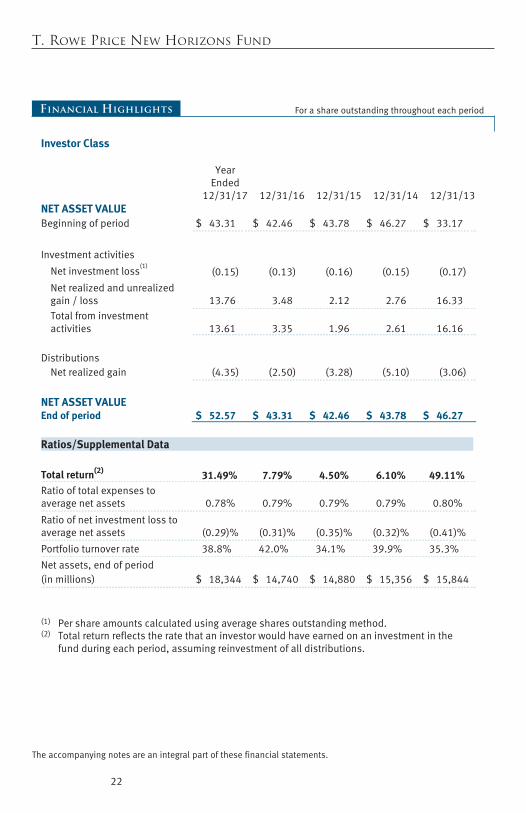

Investor Class

Year Ended

12/31/17

12/31/16

12/31/15

12/31/14

12/31/13

NET ASSET VALUE

Beginning of period

$ 43.31

$ 42.46

$ 43.78

$ 46.27

$ 33.17

Investment activities

Net investment loss(1)

(0.15)

(0.13)

(0.16)

(0.15)

(0.17)

Net realized and unrealized gain / loss

13.76

3.48

2.12

2.76

16.33

Total from investment activities

13.61

3.35

1.96

2.61

16.16

Distributions

Net realized gain

(4.35)

(2.50)

(3.28)

(5.10)

(3.06)

NET ASSET VALUE

End of period $ 52.57 $ 43.31 $ 42.46 $ 43.78 $ 46.27

Ratios/Supplemental Data Total return(2) 31.49% 7.79% 4.50% 6.10% 49.11%

Ratio of total expenses to average net assets

0.78%

0.79%

0.79%

0.79%

0.80%

Ratio of net investment loss to average net assets

(0.29)%

(0.31)%

(0.35)%

(0.32)%

(0.41)%

Portfolio turnover rate

38.8%

42.0%

34.1%

39.9%

35.3%

Net assets, end of period

(in millions)

$ 18,344

$ 14,740

$ 14,880

$ 15,356

$ 15,844

(1) Per share amounts calculated using average shares outstanding method. (2) Total return reflects the rate that an investor would have earned on an investment in the

fund during each period, assuming reinvestment of all distributions.

Proof #4

23

T. Rowe Price New Horizons Fund

Financial Highlights For a share outstanding throughout each period

The accompanying notes are an integral part of these financial statements.

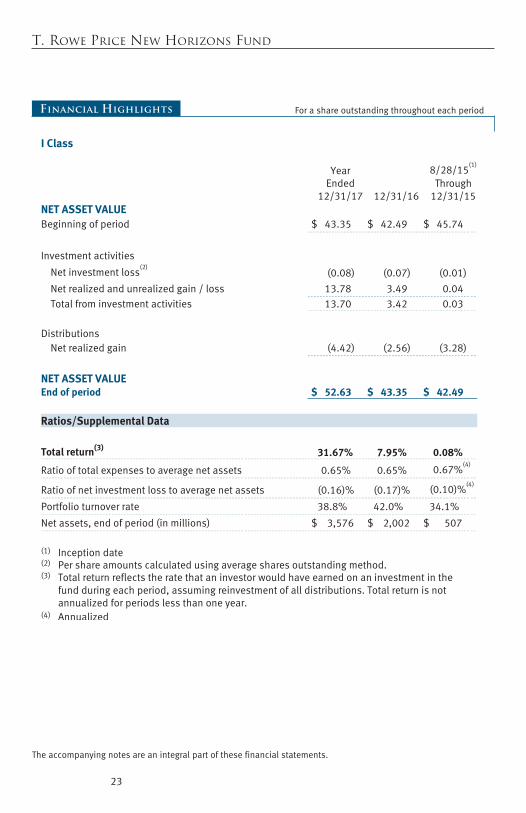

I Class

Year Ended

12/31/17

12/31/16

8/28/15(1)

Through 12/31/15

NET ASSET VALUE

Beginning of period

$ 43.35

$ 42.49

$ 45.74

Investment activities

Net investment loss(2)

(0.08)

(0.07)

(0.01)

Net realized and unrealized gain / loss

13.78

3.49

0.04

Total from investment activities

13.70

3.42

0.03

Distributions

Net realized gain

(4.42)

(2.56)

(3.28)

NET ASSET VALUE

End of period $ 52.63 $ 43.35 $ 42.49

Ratios/Supplemental Data Total return(3) 31.67% 7.95% 0.08%

Ratio of total expenses to average net assets

0.65%

0.65%

0.67%(4)

Ratio of net investment loss to average net assets

(0.16)%

(0.17)%

(0.10)%(4)

Portfolio turnover rate

38.8%

42.0%

34.1%

Net assets, end of period (in millions)

$ 3,576

$ 2,002

$ 507

(1) Inception date (2) Per share amounts calculated using average shares outstanding method. (3) Total return reflects the rate that an investor would have earned on an investment in the

fund during each period, assuming reinvestment of all distributions. Total return is not annualized for periods less than one year.

(4) Annualized

Proof #4

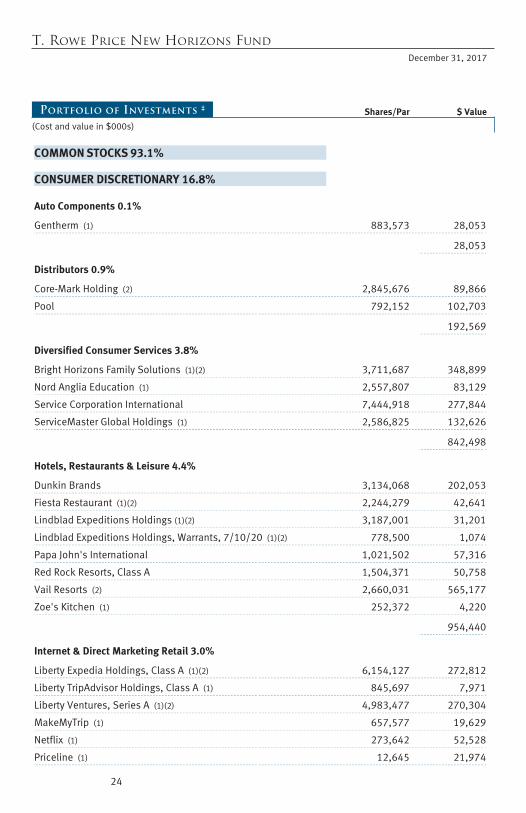

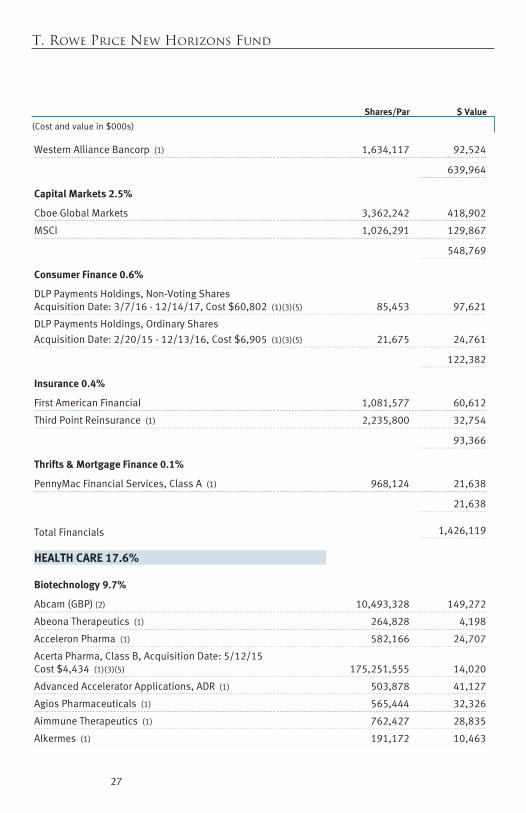

T. Rowe Price New Horizons Fund December 31, 2017

Portfolio of Investments ‡ Shares/Par $ Value

(Cost and value in $000s)

24

First Page Footer

COMMON STOCKS 93.1%

CONSUMER DISCRETIONARY 16.8%

Auto Components 0.1%

Gentherm (1) 883,573 28,053

28,053

Distributors 0.9%

Core-Mark Holding (2) 2,845,676 89,866

Pool 792,152 102,703

192,569

Diversified Consumer Services 3.8%

Bright Horizons Family Solutions (1)(2) 3,711,687 348,899

Nord Anglia Education (1) 2,557,807 83,129

Service Corporation International 7,444,918 277,844

ServiceMaster Global Holdings (1) 2,586,825 132,626

842,498

Hotels, Restaurants & Leisure 4.4%

Dunkin Brands 3,134,068 202,053

Fiesta Restaurant (1)(2) 2,244,279 42,641

Lindblad Expeditions Holdings (1)(2) 3,187,001 31,201

Lindblad Expeditions Holdings, Warrants, 7/10/20 (1)(2) 778,500 1,074

Papa John's International 1,021,502 57,316

Red Rock Resorts, Class A 1,504,371 50,758

Vail Resorts (2) 2,660,031 565,177

Zoe's Kitchen (1) 252,372 4,220

954,440

Internet & Direct Marketing Retail 3.0%

Liberty Expedia Holdings, Class A (1)(2) 6,154,127 272,812

Liberty TripAdvisor Holdings, Class A (1) 845,697 7,971

Liberty Ventures, Series A (1)(2) 4,983,477 270,304

MakeMyTrip (1) 657,577 19,629

Netflix (1) 273,642 52,528

Priceline (1) 12,645 21,974

Proof #4

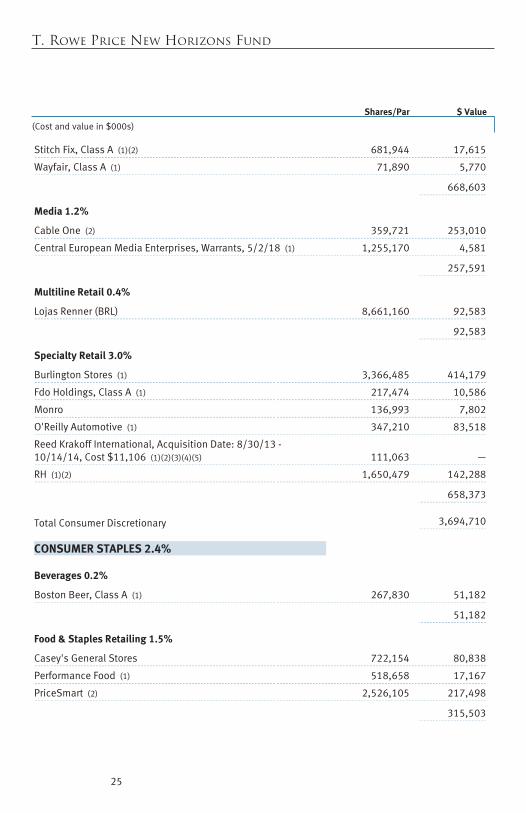

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

25

Stitch Fix, Class A (1)(2) 681,944 17,615

Wayfair, Class A (1) 71,890 5,770

668,603

Media 1.2%

Cable One (2) 359,721 253,010

Central European Media Enterprises, Warrants, 5/2/18 (1) 1,255,170 4,581

257,591

Multiline Retail 0.4%

Lojas Renner (BRL) 8,661,160 92,583

92,583

Specialty Retail 3.0%

Burlington Stores (1) 3,366,485 414,179

Fdo Holdings, Class A (1) 217,474 10,586

Monro 136,993 7,802

O'Reilly Automotive (1) 347,210 83,518

Reed Krakoff International, Acquisition Date: 8/30/13 - 10/14/14, Cost $11,106 (1)(2)(3)(4)(5) 111,063 —

RH (1)(2) 1,650,479 142,288

658,373

Total Consumer Discretionary 3,694,710

CONSUMER STAPLES 2.4%

Beverages 0.2%

Boston Beer, Class A (1) 267,830 51,182

51,182

Food & Staples Retailing 1.5%

Casey's General Stores 722,154 80,838

Performance Food (1) 518,658 17,167

PriceSmart (2) 2,526,105 217,498

315,503

Proof #4

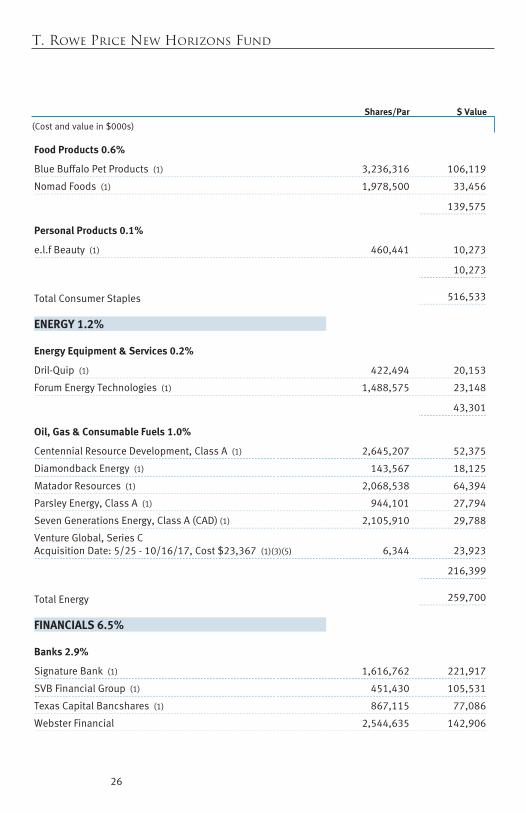

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

26

Food Products 0.6%

Blue Buffalo Pet Products (1) 3,236,316 106,119

Nomad Foods (1) 1,978,500 33,456

139,575

Personal Products 0.1%

e.l.f Beauty (1) 460,441 10,273

10,273

Total Consumer Staples 516,533

ENERGY 1.2%

Energy Equipment & Services 0.2%

Dril-Quip (1) 422,494 20,153

Forum Energy Technologies (1) 1,488,575 23,148

43,301

Oil, Gas & Consumable Fuels 1.0%

Centennial Resource Development, Class A (1) 2,645,207 52,375

Diamondback Energy (1) 143,567 18,125

Matador Resources (1) 2,068,538 64,394

Parsley Energy, Class A (1) 944,101 27,794

Seven Generations Energy, Class A (CAD) (1) 2,105,910 29,788

Venture Global, Series C Acquisition Date: 5/25 - 10/16/17, Cost $23,367 (1)(3)(5) 6,344 23,923

216,399

Total Energy 259,700

FINANCIALS 6.5%

Banks 2.9%

Signature Bank (1) 1,616,762 221,917

SVB Financial Group (1) 451,430 105,531

Texas Capital Bancshares (1) 867,115 77,086

Webster Financial 2,544,635 142,906

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

27

Western Alliance Bancorp (1) 1,634,117 92,524

639,964

Capital Markets 2.5%

Cboe Global Markets 3,362,242 418,902

MSCI 1,026,291 129,867

548,769

Consumer Finance 0.6%

DLP Payments Holdings, Non-Voting Shares Acquisition Date: 3/7/16 - 12/14/17, Cost $60,802 (1)(3)(5) 85,453 97,621

DLP Payments Holdings, Ordinary Shares Acquisition Date: 2/20/15 - 12/13/16, Cost $6,905 (1)(3)(5) 21,675 24,761

122,382

Insurance 0.4%

First American Financial 1,081,577 60,612

Third Point Reinsurance (1) 2,235,800 32,754

93,366

Thrifts & Mortgage Finance 0.1%

PennyMac Financial Services, Class A (1) 968,124 21,638

21,638

Total Financials 1,426,119

HEALTH CARE 17.6%

Biotechnology 9.7%

Abcam (GBP) (2) 10,493,328 149,272

Abeona Therapeutics (1) 264,828 4,198

Acceleron Pharma (1) 582,166 24,707

Acerta Pharma, Class B, Acquisition Date: 5/12/15 Cost $4,434 (1)(3)(5) 175,251,555 14,020

Advanced Accelerator Applications, ADR (1) 503,878 41,127

Agios Pharmaceuticals (1) 565,444 32,326

Aimmune Therapeutics (1) 762,427 28,835

Alkermes (1) 191,172 10,463

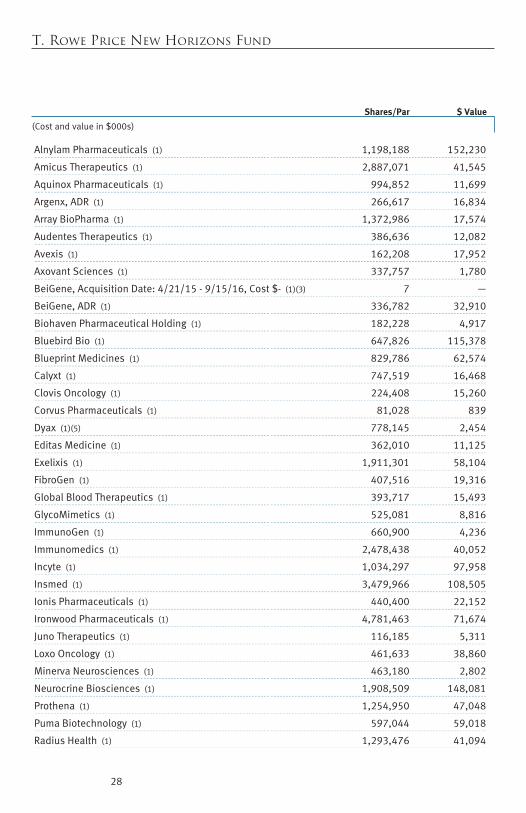

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

28

Alnylam Pharmaceuticals (1) 1,198,188 152,230

Amicus Therapeutics (1) 2,887,071 41,545

Aquinox Pharmaceuticals (1) 994,852 11,699

Argenx, ADR (1) 266,617 16,834

Array BioPharma (1) 1,372,986 17,574

Audentes Therapeutics (1) 386,636 12,082

Avexis (1) 162,208 17,952

Axovant Sciences (1) 337,757 1,780

BeiGene, Acquisition Date: 4/21/15 - 9/15/16, Cost $- (1)(3) 7 —

BeiGene, ADR (1) 336,782 32,910

Biohaven Pharmaceutical Holding (1) 182,228 4,917

Bluebird Bio (1) 647,826 115,378

Blueprint Medicines (1) 829,786 62,574

Calyxt (1) 747,519 16,468

Clovis Oncology (1) 224,408 15,260

Corvus Pharmaceuticals (1) 81,028 839

Dyax (1)(5) 778,145 2,454

Editas Medicine (1) 362,010 11,125

Exelixis (1) 1,911,301 58,104

FibroGen (1) 407,516 19,316

Global Blood Therapeutics (1) 393,717 15,493

GlycoMimetics (1) 525,081 8,816

ImmunoGen (1) 660,900 4,236

Immunomedics (1) 2,478,438 40,052

Incyte (1) 1,034,297 97,958

Insmed (1) 3,479,966 108,505

Ionis Pharmaceuticals (1) 440,400 22,152

Ironwood Pharmaceuticals (1) 4,781,463 71,674

Juno Therapeutics (1) 116,185 5,311

Loxo Oncology (1) 461,633 38,860

Minerva Neurosciences (1) 463,180 2,802

Neurocrine Biosciences (1) 1,908,509 148,081

Prothena (1) 1,254,950 47,048

Puma Biotechnology (1) 597,044 59,018

Radius Health (1) 1,293,476 41,094

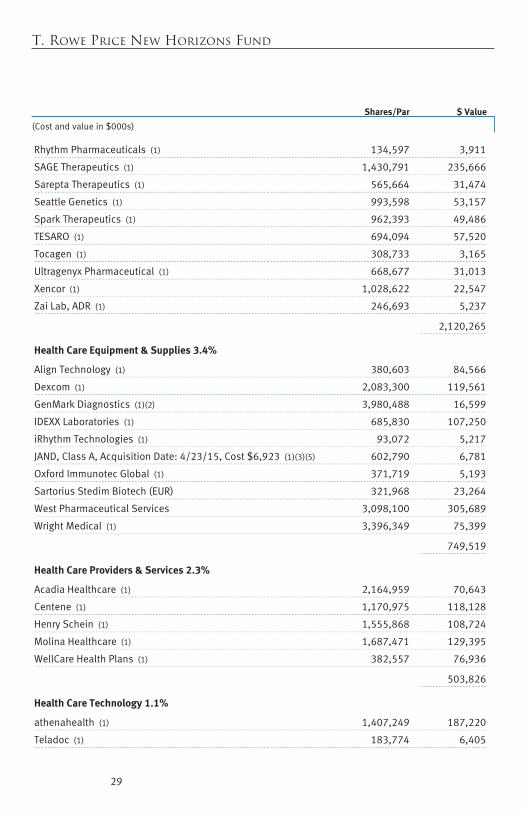

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

29

Rhythm Pharmaceuticals (1) 134,597 3,911

SAGE Therapeutics (1) 1,430,791 235,666

Sarepta Therapeutics (1) 565,664 31,474

Seattle Genetics (1) 993,598 53,157

Spark Therapeutics (1) 962,393 49,486

TESARO (1) 694,094 57,520

Tocagen (1) 308,733 3,165

Ultragenyx Pharmaceutical (1) 668,677 31,013

Xencor (1) 1,028,622 22,547

Zai Lab, ADR (1) 246,693 5,237

2,120,265

Health Care Equipment & Supplies 3.4%

Align Technology (1) 380,603 84,566

Dexcom (1) 2,083,300 119,561

GenMark Diagnostics (1)(2) 3,980,488 16,599

IDEXX Laboratories (1) 685,830 107,250

iRhythm Technologies (1) 93,072 5,217

JAND, Class A, Acquisition Date: 4/23/15, Cost $6,923 (1)(3)(5) 602,790 6,781

Oxford Immunotec Global (1) 371,719 5,193

Sartorius Stedim Biotech (EUR) 321,968 23,264

West Pharmaceutical Services 3,098,100 305,689

Wright Medical (1) 3,396,349 75,399

749,519

Health Care Providers & Services 2.3%

Acadia Healthcare (1) 2,164,959 70,643

Centene (1) 1,170,975 118,128

Henry Schein (1) 1,555,868 108,724

Molina Healthcare (1) 1,687,471 129,395

WellCare Health Plans (1) 382,557 76,936

503,826

Health Care Technology 1.1%

athenahealth (1) 1,407,249 187,220

Teladoc (1) 183,774 6,405

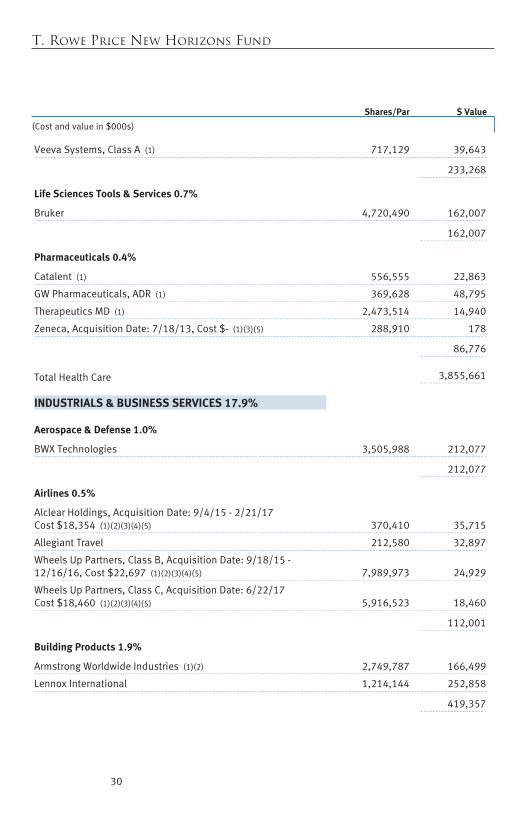

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

30

Veeva Systems, Class A (1) 717,129 39,643

233,268

Life Sciences Tools & Services 0.7%

Bruker 4,720,490 162,007

162,007

Pharmaceuticals 0.4%

Catalent (1) 556,555 22,863

GW Pharmaceuticals, ADR (1) 369,628 48,795

Therapeutics MD (1) 2,473,514 14,940

Zeneca, Acquisition Date: 7/18/13, Cost $- (1)(3)(5) 288,910 178

86,776

Total Health Care 3,855,661

INDUSTRIALS & BUSINESS SERVICES 17.9%

Aerospace & Defense 1.0%

BWX Technologies 3,505,988 212,077

212,077

Airlines 0.5%

Alclear Holdings, Acquisition Date: 9/4/15 - 2/21/17 Cost $18,354 (1)(2)(3)(4)(5) 370,410 35,715

Allegiant Travel 212,580 32,897

Wheels Up Partners, Class B, Acquisition Date: 9/18/15 - 12/16/16, Cost $22,697 (1)(2)(3)(4)(5) 7,989,973 24,929

Wheels Up Partners, Class C, Acquisition Date: 6/22/17 Cost $18,460 (1)(2)(3)(4)(5) 5,916,523 18,460

112,001

Building Products 1.9%

Armstrong Worldwide Industries (1)(2) 2,749,787 166,499

Lennox International 1,214,144 252,858

419,357

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

31

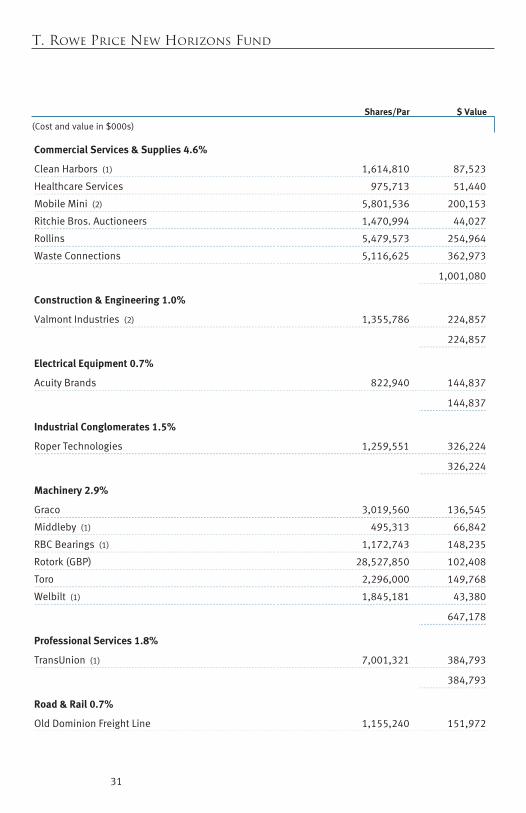

Commercial Services & Supplies 4.6%

Clean Harbors (1) 1,614,810 87,523

Healthcare Services 975,713 51,440

Mobile Mini (2) 5,801,536 200,153

Ritchie Bros. Auctioneers 1,470,994 44,027

Rollins 5,479,573 254,964

Waste Connections 5,116,625 362,973

1,001,080

Construction & Engineering 1.0%

Valmont Industries (2) 1,355,786 224,857

224,857

Electrical Equipment 0.7%

Acuity Brands 822,940 144,837

144,837

Industrial Conglomerates 1.5%

Roper Technologies 1,259,551 326,224

326,224

Machinery 2.9%

Graco 3,019,560 136,545

Middleby (1) 495,313 66,842

RBC Bearings (1) 1,172,743 148,235

Rotork (GBP) 28,527,850 102,408

Toro 2,296,000 149,768

Welbilt (1) 1,845,181 43,380

647,178

Professional Services 1.8%

TransUnion (1) 7,001,321 384,793

384,793

Road & Rail 0.7%

Old Dominion Freight Line 1,155,240 151,972

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

32

Saia (1) 182,286 12,897

164,869

Trading Companies & Distributors 1.3%

Beacon Roofing Supply (1) 689,349 43,953

Watsco 1,442,779 245,330

289,283

Total Industrials & Business Services 3,926,556

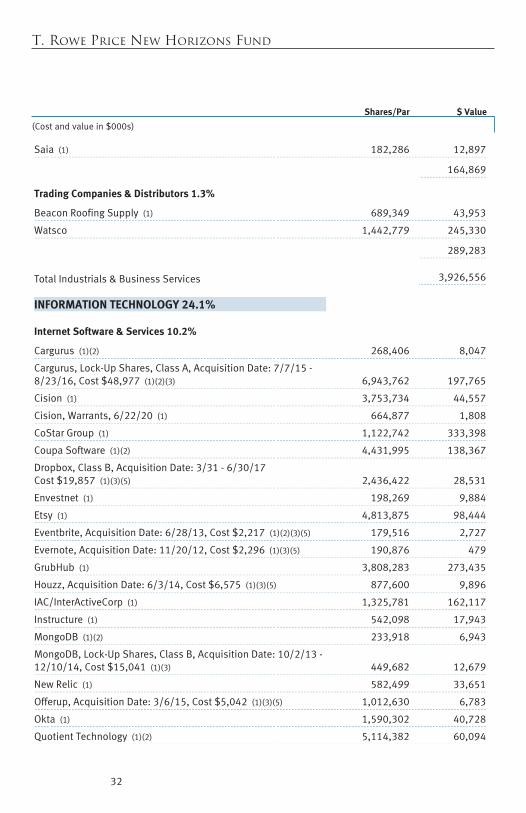

INFORMATION TECHNOLOGY 24.1%

Internet Software & Services 10.2%

Cargurus (1)(2) 268,406 8,047

Cargurus, Lock-Up Shares, Class A, Acquisition Date: 7/7/15 - 8/23/16, Cost $48,977 (1)(2)(3) 6,943,762 197,765

Cision (1) 3,753,734 44,557

Cision, Warrants, 6/22/20 (1) 664,877 1,808

CoStar Group (1) 1,122,742 333,398

Coupa Software (1)(2) 4,431,995 138,367

Dropbox, Class B, Acquisition Date: 3/31 - 6/30/17 Cost $19,857 (1)(3)(5) 2,436,422 28,531

Envestnet (1) 198,269 9,884

Etsy (1) 4,813,875 98,444

Eventbrite, Acquisition Date: 6/28/13, Cost $2,217 (1)(2)(3)(5) 179,516 2,727

Evernote, Acquisition Date: 11/20/12, Cost $2,296 (1)(3)(5) 190,876 479

GrubHub (1) 3,808,283 273,435

Houzz, Acquisition Date: 6/3/14, Cost $6,575 (1)(3)(5) 877,600 9,896

IAC/InterActiveCorp (1) 1,325,781 162,117

Instructure (1) 542,098 17,943

MongoDB (1)(2) 233,918 6,943

MongoDB, Lock-Up Shares, Class B, Acquisition Date: 10/2/13 - 12/10/14, Cost $15,041 (1)(3) 449,682 12,679

New Relic (1) 582,499 33,651

Offerup, Acquisition Date: 3/6/15, Cost $5,042 (1)(3)(5) 1,012,630 6,783

Okta (1) 1,590,302 40,728

Quotient Technology (1)(2) 5,114,382 60,094

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

33

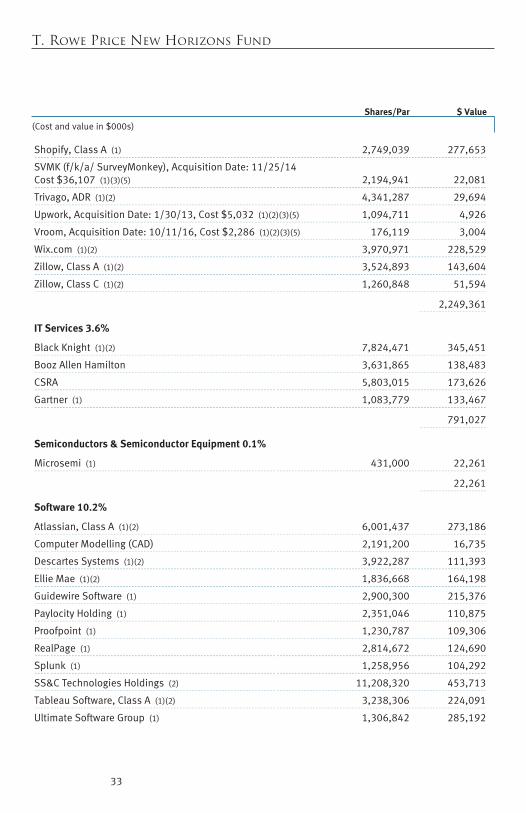

Shopify, Class A (1) 2,749,039 277,653

SVMK (f/k/a/ SurveyMonkey), Acquisition Date: 11/25/14 Cost $36,107 (1)(3)(5) 2,194,941 22,081

Trivago, ADR (1)(2) 4,341,287 29,694

Upwork, Acquisition Date: 1/30/13, Cost $5,032 (1)(2)(3)(5) 1,094,711 4,926

Vroom, Acquisition Date: 10/11/16, Cost $2,286 (1)(2)(3)(5) 176,119 3,004

Wix.com (1)(2) 3,970,971 228,529

Zillow, Class A (1)(2) 3,524,893 143,604

Zillow, Class C (1)(2) 1,260,848 51,594

2,249,361

IT Services 3.6%

Black Knight (1)(2) 7,824,471 345,451

Booz Allen Hamilton 3,631,865 138,483

CSRA 5,803,015 173,626

Gartner (1) 1,083,779 133,467

791,027

Semiconductors & Semiconductor Equipment 0.1%

Microsemi (1) 431,000 22,261

22,261

Software 10.2%

Atlassian, Class A (1)(2) 6,001,437 273,186

Computer Modelling (CAD) 2,191,200 16,735

Descartes Systems (1)(2) 3,922,287 111,393

Ellie Mae (1)(2) 1,836,668 164,198

Guidewire Software (1) 2,900,300 215,376

Paylocity Holding (1) 2,351,046 110,875

Proofpoint (1) 1,230,787 109,306

RealPage (1) 2,814,672 124,690

Splunk (1) 1,258,956 104,292

SS&C Technologies Holdings (2) 11,208,320 453,713

Tableau Software, Class A (1)(2) 3,238,306 224,091

Ultimate Software Group (1) 1,306,842 285,192

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

34

Zendesk (1) 1,042,282 35,271

2,228,318

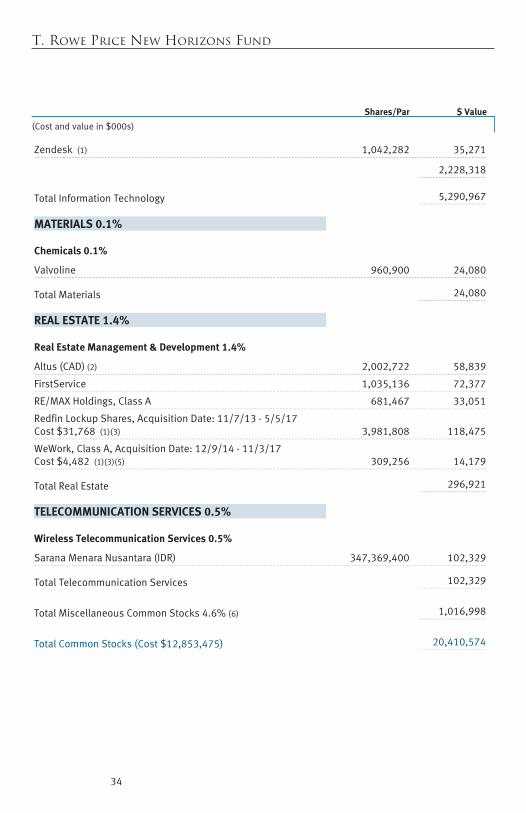

Total Information Technology 5,290,967

MATERIALS 0.1%

Chemicals 0.1%

Valvoline 960,900 24,080

Total Materials 24,080

REAL ESTATE 1.4%

Real Estate Management & Development 1.4%

Altus (CAD) (2) 2,002,722 58,839

FirstService 1,035,136 72,377

RE/MAX Holdings, Class A 681,467 33,051

Redfin Lockup Shares, Acquisition Date: 11/7/13 - 5/5/17 Cost $31,768 (1)(3) 3,981,808 118,475

WeWork, Class A, Acquisition Date: 12/9/14 - 11/3/17 Cost $4,482 (1)(3)(5) 309,256 14,179

Total Real Estate 296,921

TELECOMMUNICATION SERVICES 0.5%

Wireless Telecommunication Services 0.5%

Sarana Menara Nusantara (IDR) 347,369,400 102,329

Total Telecommunication Services 102,329

Total Miscellaneous Common Stocks 4.6% (6) 1,016,998

Total Common Stocks (Cost $12,853,475) 20,410,574

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

35

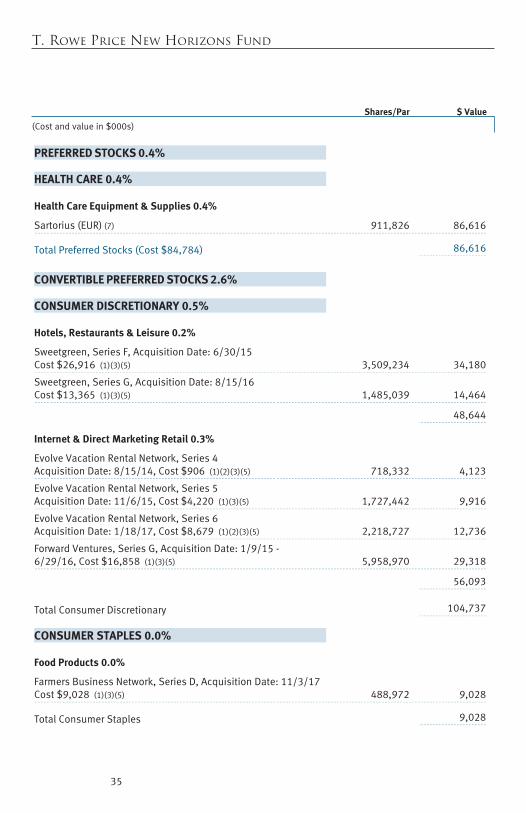

PREFERRED STOCKS 0.4%

HEALTH CARE 0.4%

Health Care Equipment & Supplies 0.4%

Sartorius (EUR) (7) 911,826 86,616

Total Preferred Stocks (Cost $84,784) 86,616

CONVERTIBLE PREFERRED STOCKS 2.6%

CONSUMER DISCRETIONARY 0.5%

Hotels, Restaurants & Leisure 0.2%

Sweetgreen, Series F, Acquisition Date: 6/30/15 Cost $26,916 (1)(3)(5) 3,509,234 34,180

Sweetgreen, Series G, Acquisition Date: 8/15/16 Cost $13,365 (1)(3)(5) 1,485,039 14,464

48,644

Internet & Direct Marketing Retail 0.3%

Evolve Vacation Rental Network, Series 4 Acquisition Date: 8/15/14, Cost $906 (1)(2)(3)(5) 718,332 4,123

Evolve Vacation Rental Network, Series 5 Acquisition Date: 11/6/15, Cost $4,220 (1)(3)(5) 1,727,442 9,916

Evolve Vacation Rental Network, Series 6 Acquisition Date: 1/18/17, Cost $8,679 (1)(2)(3)(5) 2,218,727 12,736

Forward Ventures, Series G, Acquisition Date: 1/9/15 - 6/29/16, Cost $16,858 (1)(3)(5) 5,958,970 29,318

56,093

Total Consumer Discretionary 104,737

CONSUMER STAPLES 0.0%

Food Products 0.0%

Farmers Business Network, Series D, Acquisition Date: 11/3/17 Cost $9,028 (1)(3)(5) 488,972 9,028

Total Consumer Staples 9,028

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

36

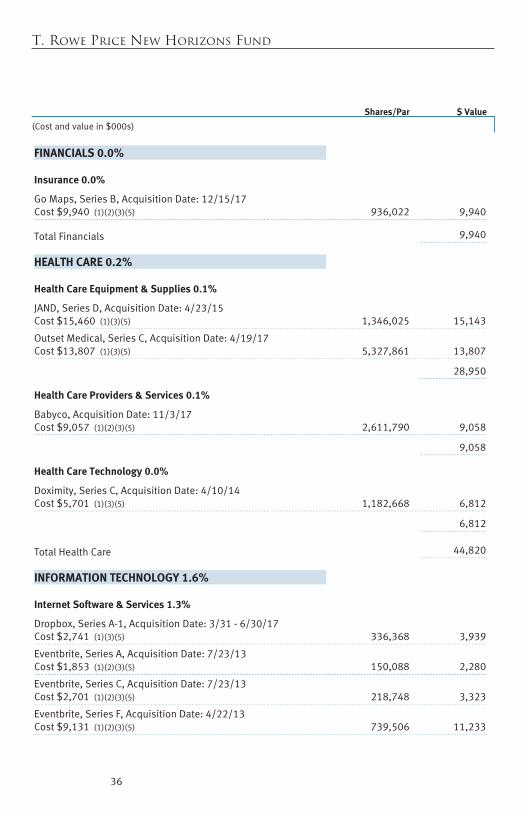

FINANCIALS 0.0%

Insurance 0.0%

Go Maps, Series B, Acquisition Date: 12/15/17 Cost $9,940 (1)(2)(3)(5) 936,022 9,940

Total Financials 9,940

HEALTH CARE 0.2%

Health Care Equipment & Supplies 0.1%

JAND, Series D, Acquisition Date: 4/23/15 Cost $15,460 (1)(3)(5) 1,346,025 15,143

Outset Medical, Series C, Acquisition Date: 4/19/17 Cost $13,807 (1)(3)(5) 5,327,861 13,807

28,950

Health Care Providers & Services 0.1%

Babyco, Acquisition Date: 11/3/17 Cost $9,057 (1)(2)(3)(5) 2,611,790 9,058

9,058

Health Care Technology 0.0%

Doximity, Series C, Acquisition Date: 4/10/14 Cost $5,701 (1)(3)(5) 1,182,668 6,812

6,812

Total Health Care 44,820

INFORMATION TECHNOLOGY 1.6%

Internet Software & Services 1.3%

Dropbox, Series A-1, Acquisition Date: 3/31 - 6/30/17 Cost $2,741 (1)(3)(5) 336,368 3,939

Eventbrite, Series A, Acquisition Date: 7/23/13 Cost $1,853 (1)(2)(3)(5) 150,088 2,280

Eventbrite, Series C, Acquisition Date: 7/23/13 Cost $2,701 (1)(2)(3)(5) 218,748 3,323

Eventbrite, Series F, Acquisition Date: 4/22/13 Cost $9,131 (1)(2)(3)(5) 739,506 11,233

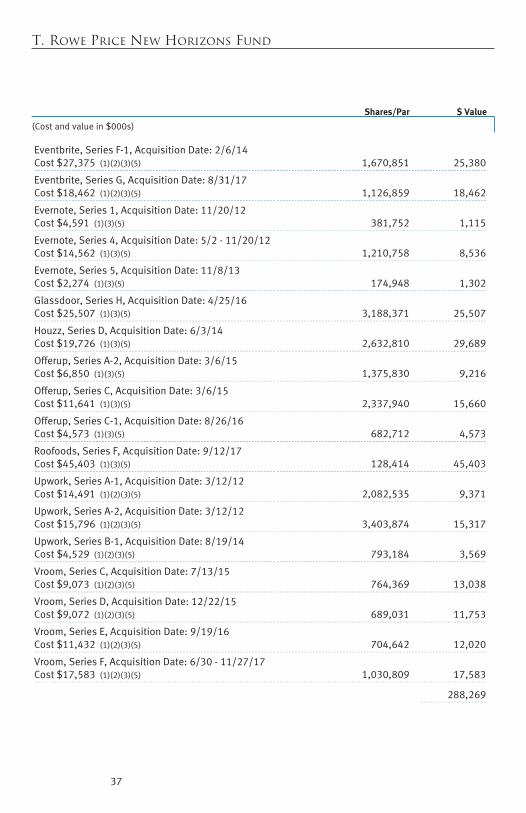

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

37

Eventbrite, Series F-1, Acquisition Date: 2/6/14 Cost $27,375 (1)(2)(3)(5) 1,670,851 25,380

Eventbrite, Series G, Acquisition Date: 8/31/17 Cost $18,462 (1)(2)(3)(5) 1,126,859 18,462

Evernote, Series 1, Acquisition Date: 11/20/12 Cost $4,591 (1)(3)(5) 381,752 1,115

Evernote, Series 4, Acquisition Date: 5/2 - 11/20/12 Cost $14,562 (1)(3)(5) 1,210,758 8,536

Evernote, Series 5, Acquisition Date: 11/8/13 Cost $2,274 (1)(3)(5) 174,948 1,302

Glassdoor, Series H, Acquisition Date: 4/25/16 Cost $25,507 (1)(3)(5) 3,188,371 25,507

Houzz, Series D, Acquisition Date: 6/3/14 Cost $19,726 (1)(3)(5) 2,632,810 29,689

Offerup, Series A-2, Acquisition Date: 3/6/15 Cost $6,850 (1)(3)(5) 1,375,830 9,216

Offerup, Series C, Acquisition Date: 3/6/15 Cost $11,641 (1)(3)(5) 2,337,940 15,660

Offerup, Series C-1, Acquisition Date: 8/26/16 Cost $4,573 (1)(3)(5) 682,712 4,573

Roofoods, Series F, Acquisition Date: 9/12/17 Cost $45,403 (1)(3)(5) 128,414 45,403

Upwork, Series A-1, Acquisition Date: 3/12/12 Cost $14,491 (1)(2)(3)(5) 2,082,535 9,371

Upwork, Series A-2, Acquisition Date: 3/12/12 Cost $15,796 (1)(2)(3)(5) 3,403,874 15,317

Upwork, Series B-1, Acquisition Date: 8/19/14 Cost $4,529 (1)(2)(3)(5) 793,184 3,569

Vroom, Series C, Acquisition Date: 7/13/15 Cost $9,073 (1)(2)(3)(5) 764,369 13,038

Vroom, Series D, Acquisition Date: 12/22/15 Cost $9,072 (1)(2)(3)(5) 689,031 11,753

Vroom, Series E, Acquisition Date: 9/19/16 Cost $11,432 (1)(2)(3)(5) 704,642 12,020

Vroom, Series F, Acquisition Date: 6/30 - 11/27/17 Cost $17,583 (1)(2)(3)(5) 1,030,809 17,583

288,269

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

38

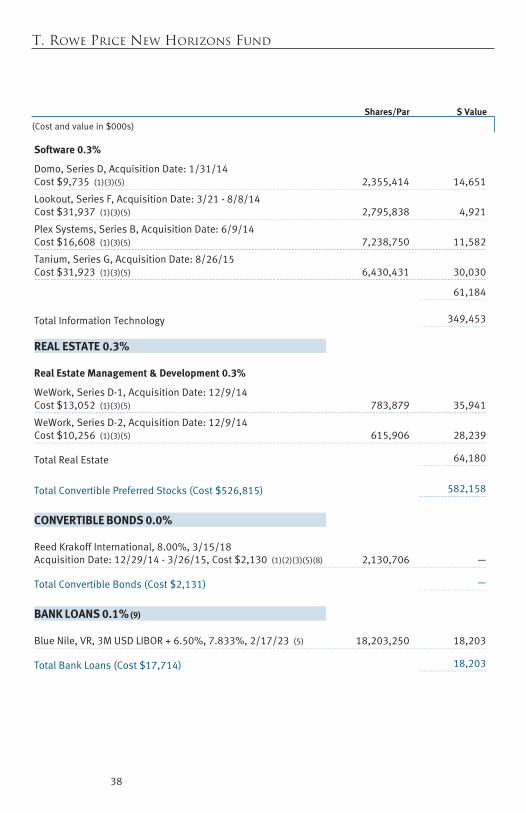

Software 0.3%

Domo, Series D, Acquisition Date: 1/31/14 Cost $9,735 (1)(3)(5) 2,355,414 14,651

Lookout, Series F, Acquisition Date: 3/21 - 8/8/14 Cost $31,937 (1)(3)(5) 2,795,838 4,921

Plex Systems, Series B, Acquisition Date: 6/9/14 Cost $16,608 (1)(3)(5) 7,238,750 11,582

Tanium, Series G, Acquisition Date: 8/26/15 Cost $31,923 (1)(3)(5) 6,430,431 30,030

61,184

Total Information Technology 349,453

REAL ESTATE 0.3%

Real Estate Management & Development 0.3%

WeWork, Series D-1, Acquisition Date: 12/9/14 Cost $13,052 (1)(3)(5) 783,879 35,941

WeWork, Series D-2, Acquisition Date: 12/9/14 Cost $10,256 (1)(3)(5) 615,906 28,239

Total Real Estate 64,180

Total Convertible Preferred Stocks (Cost $526,815) 582,158

CONVERTIBLE BONDS 0.0%

Reed Krakoff International, 8.00%, 3/15/18 Acquisition Date: 12/29/14 - 3/26/15, Cost $2,130 (1)(2)(3)(5)(8) 2,130,706 —

Total Convertible Bonds (Cost $2,131) —

BANK LOANS 0.1% (9)

Blue Nile, VR, 3M USD LIBOR + 6.50%, 7.833%, 2/17/23 (5) 18,203,250 18,203

Total Bank Loans (Cost $17,714) 18,203

Proof #4

T. Rowe Price New Horizons Fund

Shares/Par $ Value

(Cost and value in $000s)

39

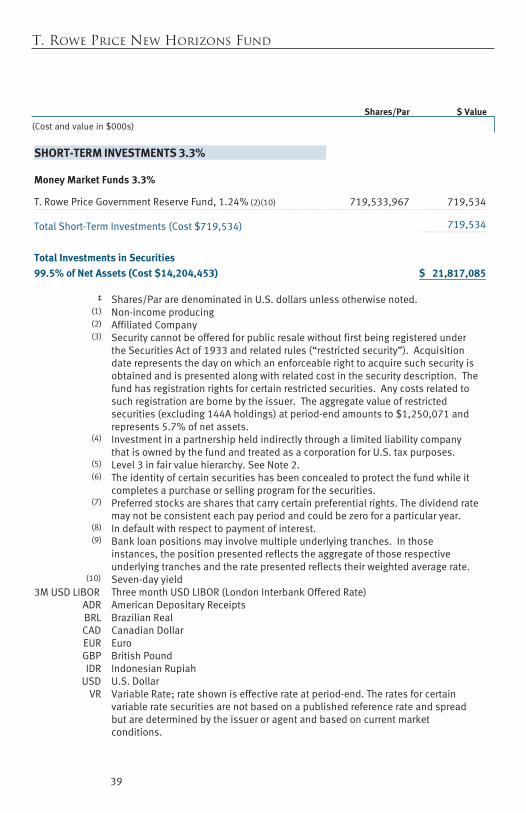

SHORT-TERM INVESTMENTS 3.3%

Money Market Funds 3.3%

T. Rowe Price Government Reserve Fund, 1.24% (2)(10) 719,533,967 719,534

Total Short-Term Investments (Cost $719,534) 719,534

Total Investments in Securities

99.5% of Net Assets (Cost $14,204,453) $ 21,817,085

‡ Shares/Par are denominated in U.S. dollars unless otherwise noted. (1) Non-income producing (2) Affiliated Company (3)

Security cannot be offered for public resale without first being registered under the Securities Act of 1933 and related rules (“restricted security”). Acquisition date represents the day on which an enforceable right to acquire such security is obtained and is presented along with related cost in the security description. The fund has registration rights for certain restricted securities. Any costs related to such registration are borne by the issuer. The aggregate value of restricted securities (excluding 144A holdings) at period-end amounts to $1,250,071 and represents 5.7% of net assets.

(4)

Investment in a partnership held indirectly through a limited liability company that is owned by the fund and treated as a corporation for U.S. tax purposes.

(5) Level 3 in fair value hierarchy. See Note 2. (6)

The identity of certain securities has been concealed to protect the fund while it completes a purchase or selling program for the securities.

(7)

Preferred stocks are shares that carry certain preferential rights. The dividend rate may not be consistent each pay period and could be zero for a particular year.

(8) In default with respect to payment of interest. (9)

Bank loan positions may involve multiple underlying tranches. In those instances, the position presented reflects the aggregate of those respective underlying tranches and the rate presented reflects their weighted average rate.

(10) Seven-day yield 3M USD LIBOR Three month USD LIBOR (London Interbank Offered Rate)

ADR American Depositary Receipts BRL Brazilian Real CAD Canadian Dollar EUR Euro GBP British Pound IDR Indonesian Rupiah

USD U.S. Dollar VR

Variable Rate; rate shown is effective rate at period-end. The rates for certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and based on current market conditions.

Proof #4

T. Rowe Price New Horizons Fund

40

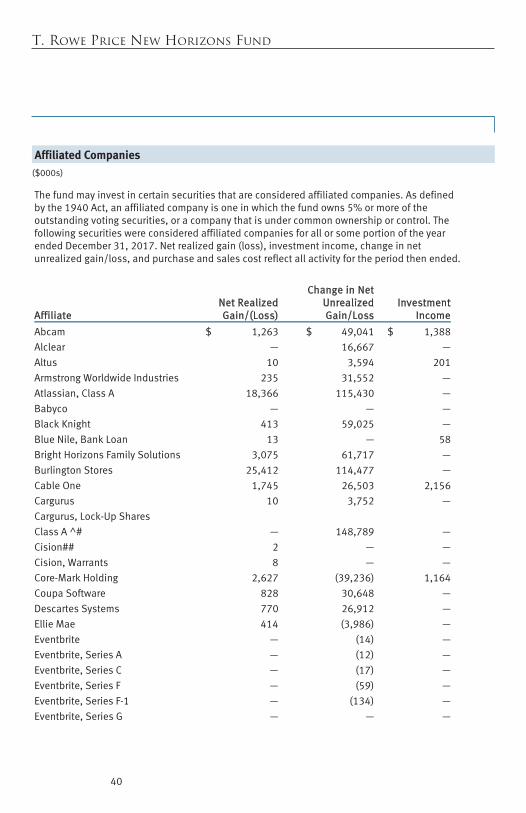

Affiliated Companies

($000s) The fund may invest in certain securities that are considered affiliated companies. As defined by the 1940 Act, an affiliated company is one in which the fund owns 5% or more of the outstanding voting securities, or a company that is under common ownership or control. The following securities were considered affiliated companies for all or some portion of the year ended December 31, 2017. Net realized gain (loss), investment income, change in net unrealized gain/loss, and purchase and sales cost reflect all activity for the period then ended.

Affiliate

Net RealizedGain/(Loss)

Change in NetUnrealizedGain/Loss

InvestmentIncome

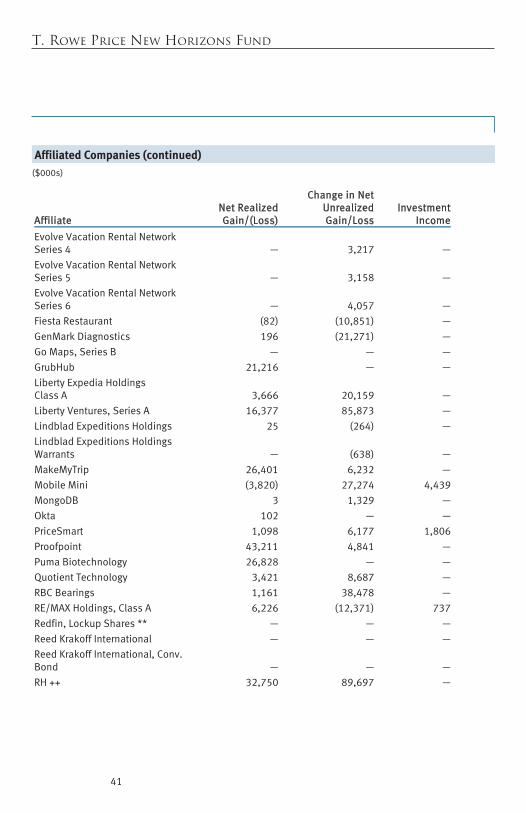

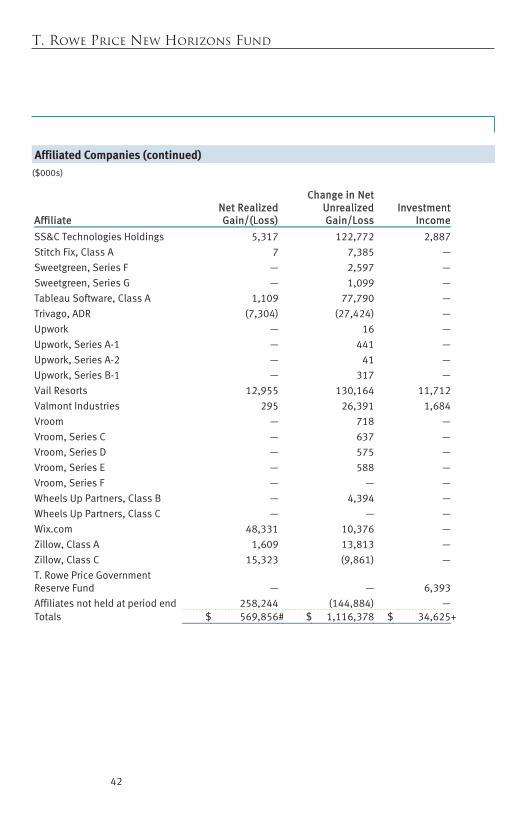

Abcam $ 1,263 $ 49,041 $ 1,388 Alclear — 16,667 — Altus 10 3,594 201 Armstrong Worldwide Industries 235 31,552 — Atlassian, Class A 18,366 115,430 — Babyco — — — Black Knight 413 59,025 — Blue Nile, Bank Loan 13 — 58 Bright Horizons Family Solutions 3,075 61,717 — Burlington Stores 25,412 114,477 — Cable One 1,745 26,503 2,156 Cargurus 10 3,752 — Cargurus, Lock-Up Shares Class A ^# — 148,789 — Cision## 2 — — Cision, Warrants 8 — — Core-Mark Holding 2,627 (39,236) 1,164 Coupa Software 828 30,648 — Descartes Systems 770 26,912 — Ellie Mae 414 (3,986) — Eventbrite — (14) — Eventbrite, Series A — (12) — Eventbrite, Series C — (17) — Eventbrite, Series F — (59) — Eventbrite, Series F-1 — (134) — Eventbrite, Series G — — —

Proof #4

T. Rowe Price New Horizons Fund

41

Affiliated Companies

($000s)

Affiliate

Net RealizedGain/(Loss)

Change in NetUnrealizedGain/Loss

InvestmentIncome

Evolve Vacation Rental Network Series 4 — 3,217 — Evolve Vacation Rental Network Series 5 — 3,158 — Evolve Vacation Rental Network Series 6 — 4,057 — Fiesta Restaurant (82) (10,851) — GenMark Diagnostics 196 (21,271) — Go Maps, Series B — — — GrubHub 21,216 — — Liberty Expedia Holdings Class A 3,666 20,159 — Liberty Ventures, Series A 16,377 85,873 — Lindblad Expeditions Holdings 25 (264) — Lindblad Expeditions Holdings Warrants — (638) — MakeMyTrip 26,401 6,232 — Mobile Mini (3,820) 27,274 4,439 MongoDB 3 1,329 — Okta 102 — — PriceSmart 1,098 6,177 1,806 Proofpoint 43,211 4,841 — Puma Biotechnology 26,828 — — Quotient Technology 3,421 8,687 — RBC Bearings 1,161 38,478 — RE/MAX Holdings, Class A 6,226 (12,371) 737 Redfin, Lockup Shares ** — — — Reed Krakoff International — — — Reed Krakoff International, Conv. Bond — — — RH ++ 32,750 89,697 —

affiliated companies (continued)

Proof #4

T. Rowe Price New Horizons Fund

42

Affiliated Companies

($000s) Affiliate

Net RealizedGain/(Loss)

Change in NetUnrealizedGain/Loss

InvestmentIncome

SS&C Technologies Holdings 5,317 122,772 2,887 Stitch Fix, Class A 7 7,385 — Sweetgreen, Series F — 2,597 — Sweetgreen, Series G — 1,099 — Tableau Software, Class A 1,109 77,790 — Trivago, ADR (7,304) (27,424) — Upwork — 16 — Upwork, Series A-1 — 441 — Upwork, Series A-2 — 41 — Upwork, Series B-1 — 317 — Vail Resorts 12,955 130,164 11,712 Valmont Industries 295 26,391 1,684 Vroom — 718 — Vroom, Series C — 637 — Vroom, Series D — 575 — Vroom, Series E — 588 — Vroom, Series F — — — Wheels Up Partners, Class B — 4,394 — Wheels Up Partners, Class C — — — Wix.com 48,331 10,376 — Zillow, Class A 1,609 13,813 — Zillow, Class C 15,323 (9,861) — T. Rowe Price Government Reserve Fund — — 6,393 Affiliates not held at period end 258,244 (144,884) — Totals $ 569,856# $ 1,116,378 $ 34,625+

affiliated companies (continued)

Proof #4

T. Rowe Price New Horizons Fund

43

Affiliated Companies

($000s)

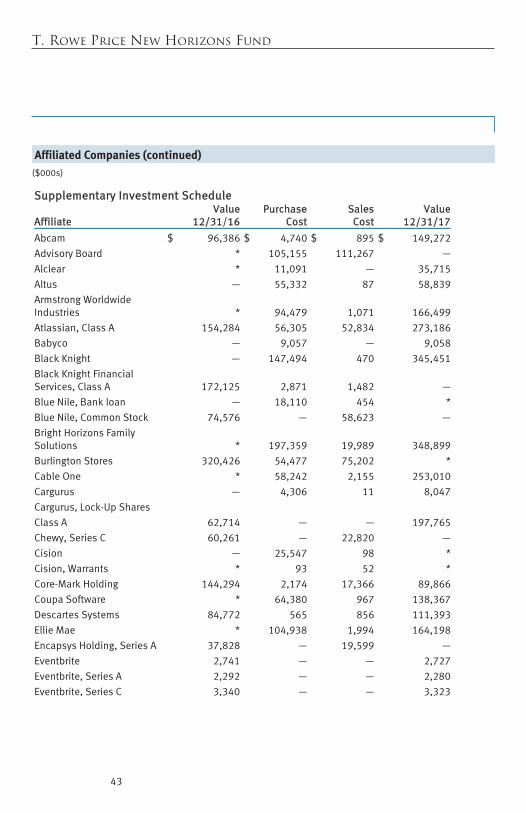

Supplementary Investment Schedule Affiliate

Value12/31/16

PurchaseCost

SalesCost

Value12/31/17

Abcam $ 96,386 $ 4,740 $ 895 $ 149,272 Advisory Board * 105,155 111,267 — Alclear * 11,091 — 35,715 Altus — 55,332 87 58,839 Armstrong Worldwide Industries * 94,479 1,071 166,499 Atlassian, Class A 154,284 56,305 52,834 273,186 Babyco — 9,057 — 9,058 Black Knight — 147,494 470 345,451 Black Knight Financial Services, Class A 172,125 2,871 1,482 — Blue Nile, Bank loan — 18,110 454 * Blue Nile, Common Stock 74,576 — 58,623 — Bright Horizons Family Solutions * 197,359 19,989 348,899 Burlington Stores 320,426 54,477 75,202 * Cable One * 58,242 2,155 253,010 Cargurus — 4,306 11 8,047 Cargurus, Lock-Up Shares Class A 62,714 — — 197,765 Chewy, Series C 60,261 — 22,820 — Cision — 25,547 98 * Cision, Warrants * 93 52 * Core-Mark Holding 144,294 2,174 17,366 89,866 Coupa Software * 64,380 967 138,367 Descartes Systems 84,772 565 856 111,393 Ellie Mae * 104,938 1,994 164,198 Encapsys Holding, Series A 37,828 — 19,599 — Eventbrite 2,741 — — 2,727 Eventbrite, Series A 2,292 — — 2,280 Eventbrite, Series C 3,340 — — 3,323

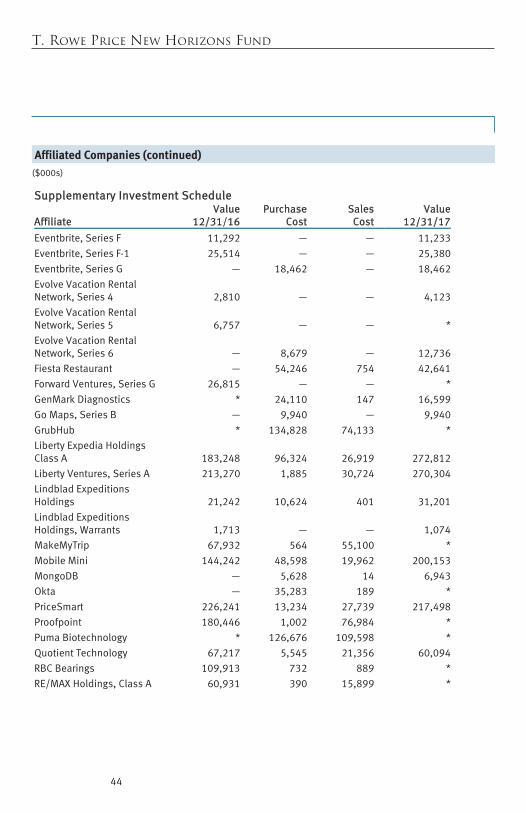

affiliated companies (continued)

Proof #4

T. Rowe Price New Horizons Fund

44

Affiliated Companies

($000s) Supplementary Investment Schedule Affiliate

Value12/31/16

PurchaseCost

SalesCost

Value12/31/17

Eventbrite, Series F 11,292 — — 11,233 Eventbrite, Series F-1 25,514 — — 25,380 Eventbrite, Series G — 18,462 — 18,462 Evolve Vacation Rental Network, Series 4 2,810 — — 4,123 Evolve Vacation Rental Network, Series 5 6,757 — — * Evolve Vacation Rental Network, Series 6 — 8,679 — 12,736 Fiesta Restaurant — 54,246 754 42,641 Forward Ventures, Series G 26,815 — — * GenMark Diagnostics * 24,110 147 16,599 Go Maps, Series B — 9,940 — 9,940 GrubHub * 134,828 74,133 * Liberty Expedia Holdings Class A 183,248 96,324 26,919 272,812 Liberty Ventures, Series A 213,270 1,885 30,724 270,304 Lindblad Expeditions Holdings 21,242 10,624 401 31,201 Lindblad Expeditions Holdings, Warrants 1,713 — — 1,074 MakeMyTrip 67,932 564 55,100 * Mobile Mini 144,242 48,598 19,962 200,153 MongoDB — 5,628 14 6,943 Okta — 35,283 189 * PriceSmart 226,241 13,234 27,739 217,498 Proofpoint 180,446 1,002 76,984 * Puma Biotechnology * 126,676 109,598 * Quotient Technology 67,217 5,545 21,356 60,094 RBC Bearings 109,913 732 889 * RE/MAX Holdings, Class A 60,931 390 15,899 *

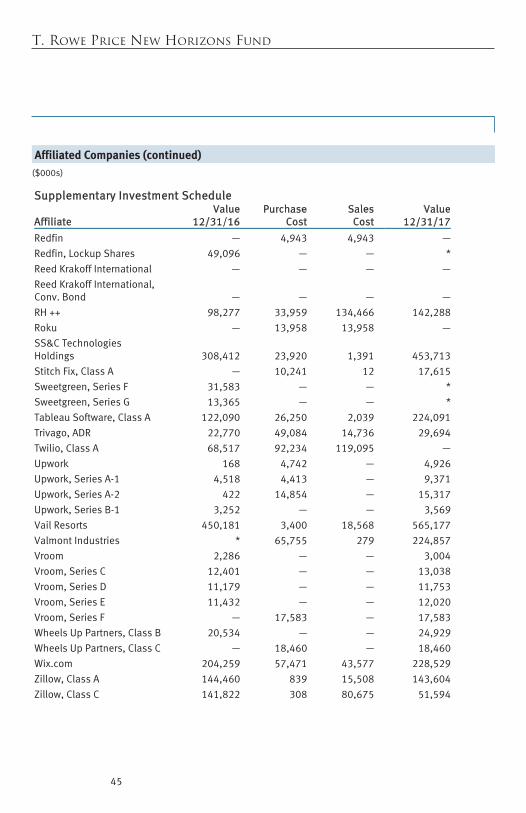

affiliated companies (continued)

Proof #4

T. Rowe Price New Horizons Fund

45

Affiliated Companies

($000s)

Supplementary Investment Schedule Affiliate

Value12/31/16

PurchaseCost

SalesCost

Value12/31/17

Redfin — 4,943 4,943 — Redfin, Lockup Shares 49,096 — — * Reed Krakoff International — — — — Reed Krakoff International, Conv. Bond — — — — RH ++ 98,277 33,959 134,466 142,288 Roku — 13,958 13,958 — SS&C Technologies Holdings 308,412 23,920 1,391 453,713 Stitch Fix, Class A — 10,241 12 17,615 Sweetgreen, Series F 31,583 — — * Sweetgreen, Series G 13,365 — — * Tableau Software, Class A 122,090 26,250 2,039 224,091 Trivago, ADR 22,770 49,084 14,736 29,694 Twilio, Class A 68,517 92,234 119,095 — Upwork 168 4,742 — 4,926 Upwork, Series A-1 4,518 4,413 — 9,371 Upwork, Series A-2 422 14,854 — 15,317 Upwork, Series B-1 3,252 — — 3,569 Vail Resorts 450,181 3,400 18,568 565,177 Valmont Industries * 65,755 279 224,857 Vroom 2,286 — — 3,004 Vroom, Series C 12,401 — — 13,038 Vroom, Series D 11,179 — — 11,753 Vroom, Series E 11,432 — — 12,020 Vroom, Series F — 17,583 — 17,583 Wheels Up Partners, Class B 20,534 — — 24,929 Wheels Up Partners, Class C — 18,460 — 18,460 Wix.com 204,259 57,471 43,577 228,529 Zillow, Class A 144,460 839 15,508 143,604 Zillow, Class C 141,822 308 80,675 51,594

affiliated companies (continued)

Proof #4

T. Rowe Price New Horizons Fund

46

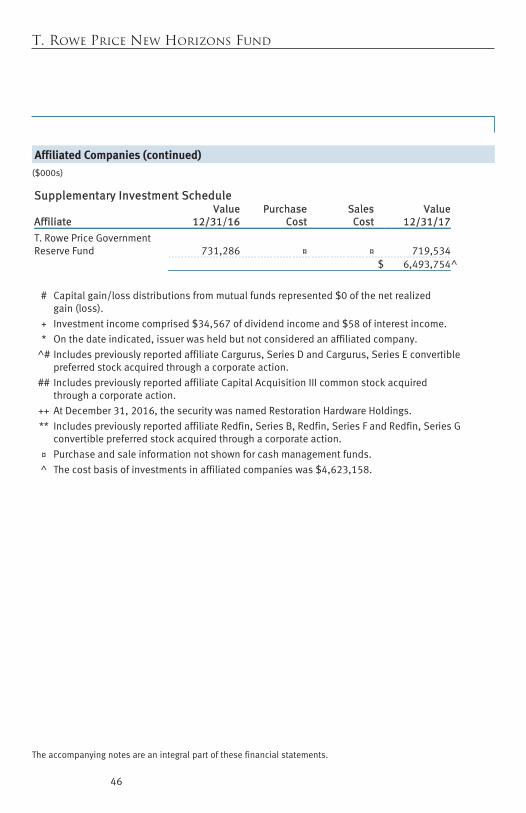

The accompanying notes are an integral part of these financial statements.

($000s)

affiliated companies (continued)

Supplementary Investment Schedule Affiliate

Value12/31/16

PurchaseCost