private equity gp and employee co-investment credit

TRANSCRIPT

Private Equity GP and Employee Co-Investment

Credit Facilities, Management Lines of CreditDue Diligence, Structuring and Documentation; Role of Sponsor, Administrative Issues

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

WEDNESDAY, JUNE 10, 2020

Presenting a live 90-minute webinar with interactive Q&A

Alexander T. Grishman, Partner, Haynes and Boone, New York

Deborah P. Low, Partner, Haynes and Boone, New York

Ellen Gibson McGinnis, Partner, Haynes and Boone, Washington, D.C.

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-877-447-0294 and enter your Conference ID and PIN when prompted.

Otherwise, please send us a chat or e-mail [email protected] immediately

so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the ‘Full Screen’ symbol located on the bottom

right of the slides. To exit full screen, press the Esc button.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the link to the PDF of the slides for today’s program, which is located

to the right of the slides, just above the Q&A box.

• The PDF will open a separate tab/window. Print the slides by clicking on the

printer icon.

FOR LIVE EVENT ONLY

Private Equity GP and Employee

Co-Investment Credit Facilities,

Management Lines of CreditDue Diligence, Structuring and Documentation

Role of Sponsor and Administrative Issues

June 10, 2020

© 2020 Haynes and Boone, LLP

6

A rapid expansion in the subscription facility market has led to a desire

to leverage additional fund assets, giving rise to an increase in additional

working capital facilities:

• Management Fee Facilities secured by the payment of

Management Fees that are due to a management company

• Employee Co-Investment Lines of Credit made to employees

of a fund to finance their investment into the fund

• General Partner Lines of Credit, issued to a general partner or

a principal for the purpose of financing the general partner capital

contributions into a fund

© 2020 Haynes and Boone, LLP

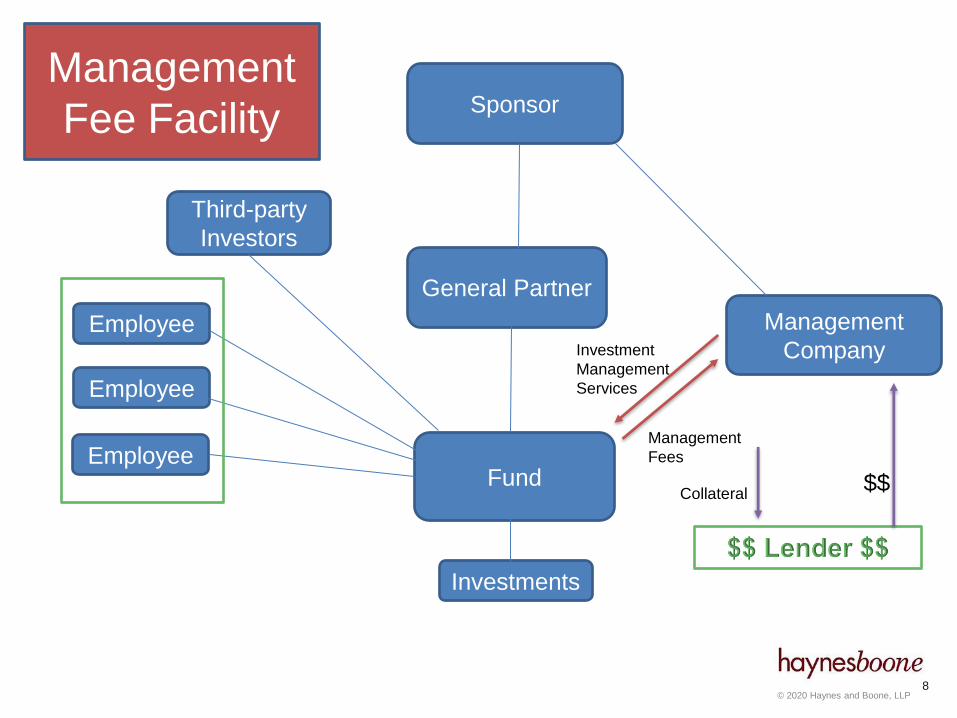

Fund

General Partner

Management

Company

Sponsor

Employee

Employee

Employee

Third-party

Investors

Investments

Subscription

Facility

$$

Collateral

Collateral (hybrid)

Capital

Contributions

7

© 2020 Haynes and Boone, LLP

Fund

General Partner

Management

Company

Sponsor

Employee

Employee

Employee

Third-party

Investors

Investments

Management

Fee Facility

Investment

Management

Services

Management

Fees

$$Collateral

8

© 2020 Haynes and Boone, LLP

Fund

General Partner

Management

Company

Sponsor

Employee

Employee

Employee

Third-party

Investors

Investments

Employee

Co-Invest

Facility

$$

Capital

Contributions

LP Interests

Collateral

9

© 2020 Haynes and Boone, LLP

Fund

General Partner

Management

Company

Sponsor

Employee

Employee

Employee

Third-party

Investors

Investments

GP Facility

$$

Collateral

GP Interests

GP Capital

Contributions

10

© 2020 Haynes and Boone, LLP

Management Fee

Lines of Credit

11

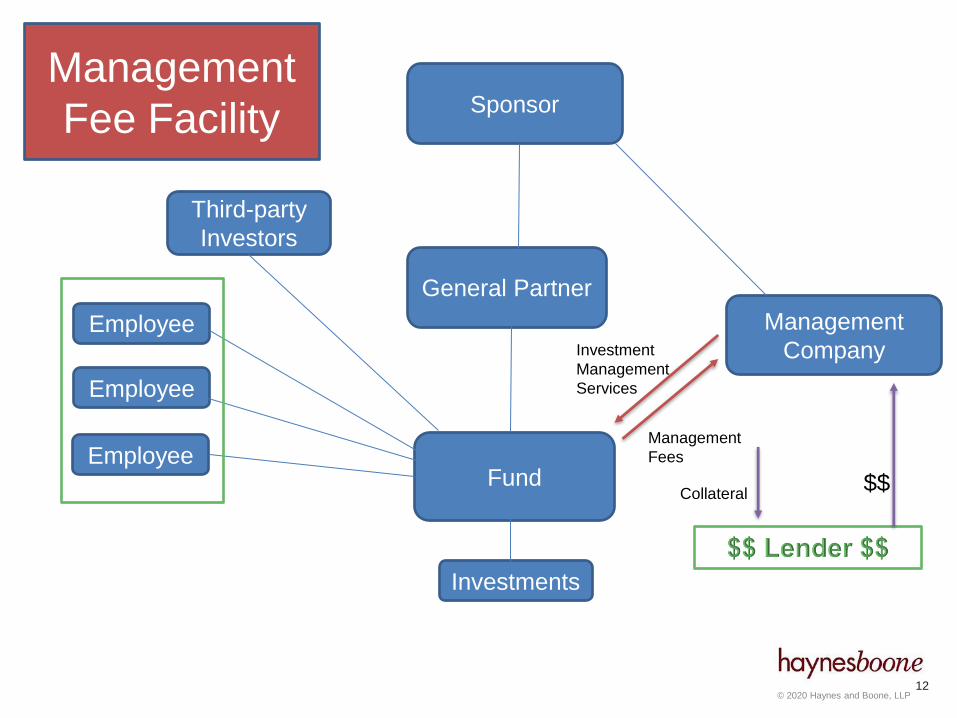

© 2020 Haynes and Boone, LLP

Fund

General Partner

Management

Company

Sponsor

Employee

Employee

Employee

Third-party

Investors

Investments

Management

Fee Facility

Investment

Management

Services

Management

Fees

$$Collateral

12

© 2020 Haynes and Boone, LLP

13

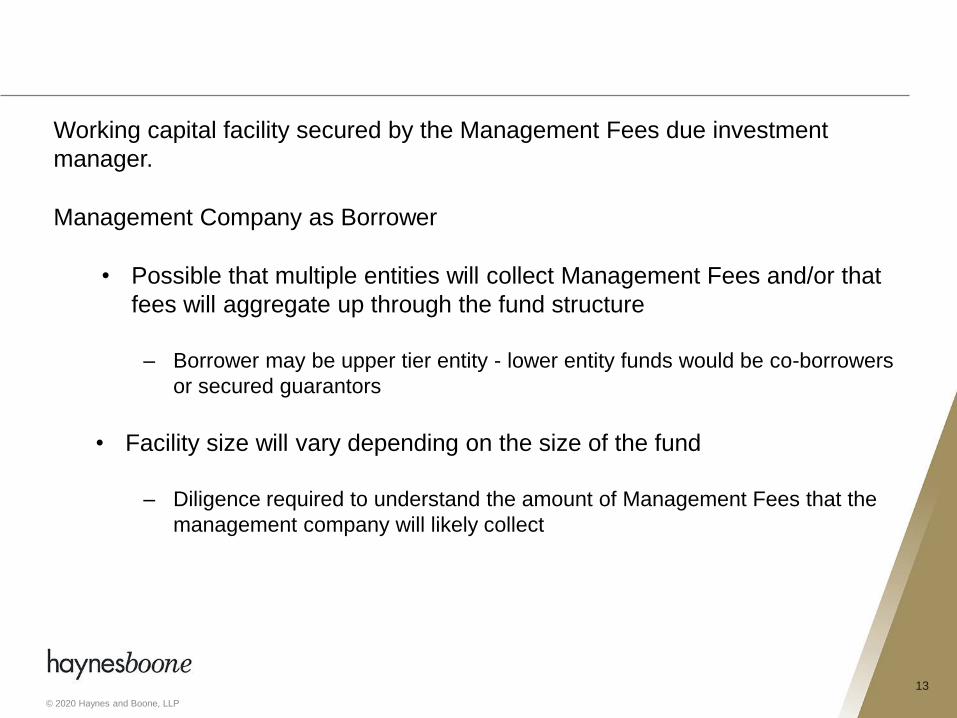

Working capital facility secured by the Management Fees due investment

manager.

Management Company as Borrower

• Possible that multiple entities will collect Management Fees and/or that

fees will aggregate up through the fund structure

– Borrower may be upper tier entity - lower entity funds would be co-borrowers

or secured guarantors

• Facility size will vary depending on the size of the fund

– Diligence required to understand the amount of Management Fees that the

management company will likely collect

© 2020 Haynes and Boone, LLP

14

For the Management Company:

• Liquidity in between payments of Management Fees

For the Lender:

• Interest and fees generally higher than those charged on traditional

subscription facilities

• Deepens relationships with sponsors and their principals

• Offering alternative financing can make the lender a more attractive

source of portfolio-level financing and traditional subscription financing

© 2020 Haynes and Boone, LLP

15

The right to receive Management Fees is typically evidenced by a Management

Agreement

• Verify the funds that are obligated to make payment of Management

Fees

• No restrictions on transfer of economic rights to receive payment of

Management Fees (this may be included as a specific carve-out to

assignment of the contract)

• How will the performance of the underlying fund impact the amount of

fees due to the management company (are fees fixed or incentive

based)?

• Are there any circumstances under which a fund can withhold or cease

paying Management Fees?

• Frequency of Management Fee payments

© 2020 Haynes and Boone, LLP

16

Sponsor and Fund diligence

• Amount of Management Fees payable to the Management Company is

often tied assets under management which is in part based on the to

performance of the underlying fund

• Lender will need to be comfortable that the Management Company will

be able to maintain AUM through performance as it is relying on payment

of future Management Fees to repay facility

• Industry track-record

• Quality of third-party investors

• Fund strategy

© 2020 Haynes and Boone, LLP

17

Borrowing Base

• Typically advance rate percentage of anticipated Management Fees (or

the lesser of anticipated Management Fees and Management Fees

collected over the prior period)

• Projected Management Fees may be removed from the Borrowing Base

if payment of Management Fees is disrupted for any reason, including

the insolvency of the underlying fund

• Prohibitions on early redemptions and amendments to management fee

agreement

© 2020 Haynes and Boone, LLP

18

Mandatory prepayments

• Timing and calculations can vary

• Lender may require the Borrower apply a percentage of Management

Fees received in each period to the repayment of the Loan

• The actual Management Fees collected are less than the projected

Management Fees in the Borrowing Base

• Following an Event of Default or at any time the loan amount exceeds the

Borrowing Base, Borrower will be required to apply 100% of Management

Fees received to repayment of the Facility

© 2020 Haynes and Boone, LLP

19

Covenants

• Minimum Management Fees

• Minimum Assets Under Management

• Compliance Reporting (delivered shortly after payment of Management

Fees for any relevant payment)

• No adverse amendments to Management Agreements

• Notice of key events affecting underlying fund

• Agreement to cause Management Fees to be paid directly into a deposit

account pledged by Borrower

© 2020 Haynes and Boone, LLP

20

Events of Default

• If the Borrowing Base is comprised of only one or two funds, any

disruption in payment Management Fees may give rise to an Event of

Default

• Actual Management Fee collections exceed a variation threshold from

projected Management Fees

• Regulatory Events

© 2020 Haynes and Boone, LLP

21

Assignment of Rights to Receive Payment of Management Fees

• Rights to receive payment of Management Fees is a general intangible

under the UCC and the security interest is perfected by filing a UCC-1

Assignment of a security interest in the deposit account where Management

Fees are paid

• Lender and Borrower will need to enter into a deposit account control

agreement with the bank where the deposit account is maintained, to

perfect the Lender’s security interest in the account by “control”

• In an enforcement scenario, Lender will need to exercise exclusive

control over the account to capture payment of any Management Fees

that are made into the deposit account

© 2020 Haynes and Boone, LLP

22

Acknowledgment and Consent of the underlying funds paying Management Fees

• Acknowledgment of the pledge of the right to receive payment of

Management Fees

• Agreement to pay Management Fees directly into the pledged deposit

account

• Agreement to comply with Lender’s instructions regarding payment of

fees into a different account post Event-of-Default

© 2020 Haynes and Boone, LLP

23

Standard loan deliverables:

• Opinion

• Organizational documents and Management Agreements

• Resolutions

• Incumbency

• UCCs and lien searches

© 2020 Haynes and Boone, LLP

24

• If the underlying fund has a subscription facility or other credit facility in

place, such facility might prohibit the payment of Management Fees

during an Event of Default

• Creditors of the underlying fund are unlikely to waive the prohibition

• In a subscription facility a minor default might be remedied fairly quickly

and cause little to no disruption in payment of Management Fees

• For other kinds of facilities, including NAV or hybrid, if the lender

forecloses on and/or forces a sale of collateral there may be a longer

disruption

• In either circumstance, the underlying fund might be left with fewer assets

with which to pay accrued but unpaid Management Fees

© 2020 Haynes and Boone, LLP

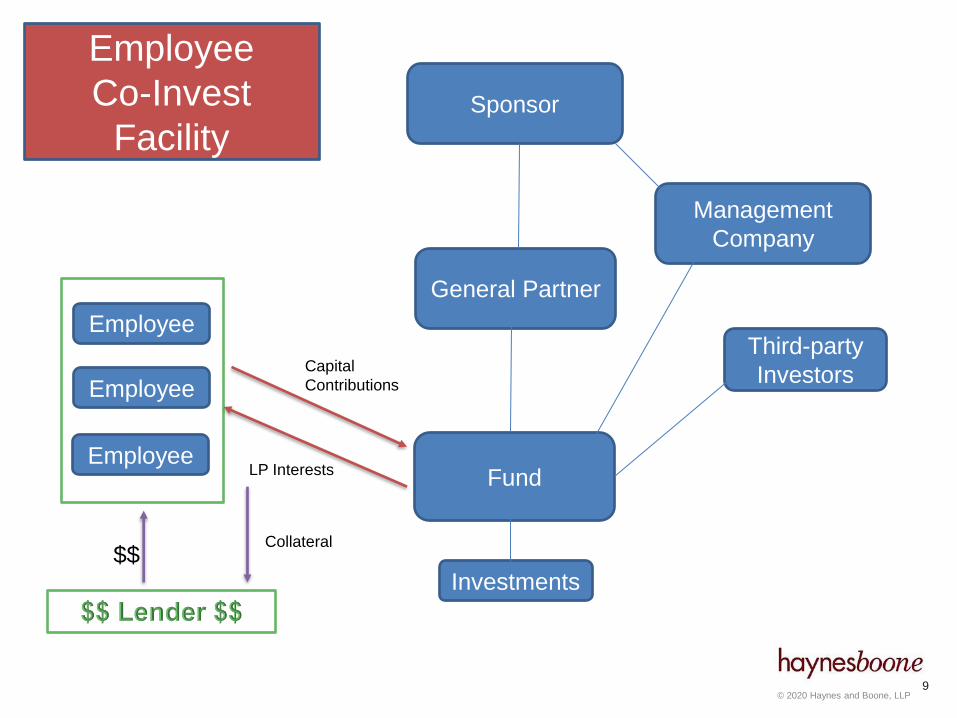

Employee Co-Invest

Lines of Credit

25

© 2020 Haynes and Boone, LLP

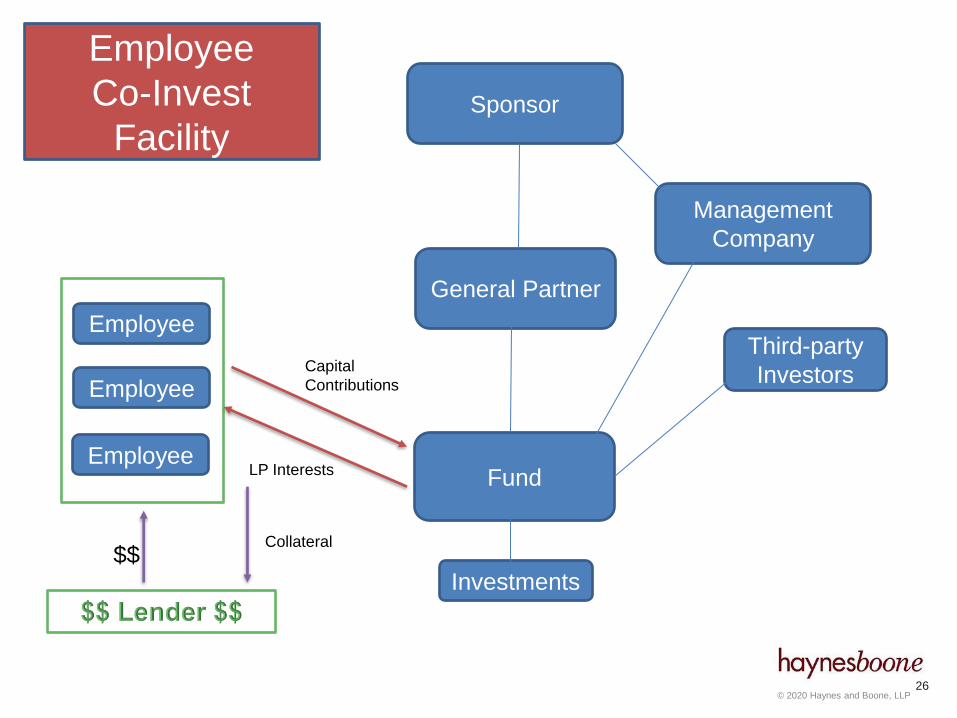

Fund

General Partner

Management

Company

Sponsor

Employee

Employee

Employee

Third-party

Investors

Investments

Employee

Co-Invest

Facility

$$

Capital

Contributions

LP Interests

Collateral

26

© 2020 Haynes and Boone, LLP

27

• Advanced to employees of a fund to finance their investment into the fund

• Secured by the limited partnership interests acquired by the employees in

the subject fund

• Who are the parties?

– Sponsor / Fund / GP

– Lender

– Employees

© 2020 Haynes and Boone, LLP

28

• Facility size will vary depending on the number of participating employees

• Each individual employee loan is typically in the range of $50,000-

$250,000

• Facility may be comprised of revolving loans or multi-draw term loans

© 2020 Haynes and Boone, LLP

29

Employees:

• Negotiated on their behalf by the Sponsor

• Enhanced bargaining capacity when aggregated with other employee

investment

• Frees up personal capital and assets

• Attractive employee benefit

© 2020 Haynes and Boone, LLP

30

Sponsor:

• Satisfies investor requirements for the Sponsor to have more “skin in the

game”

• Permits leveraging of future distributions

• Attractive employee benefit

• Enhances commitment of sponsor to valuable employees

• Reduces administrative burdens

© 2020 Haynes and Boone, LLP

31

Lender:

• Payment of interest and fees that are generally higher than those

charged on traditional subscription facilities

• Deepens relationships with Sponsors and their principals

– This makes the Lender a more attractive source of portfolio-level financing

and traditional subscription financing

© 2020 Haynes and Boone, LLP

32

Significant diligence will be performed on employees which may be seen as a

barrier to completing the facility

• Personal financial reporting requirements

– May be seen as invasive by the employee

– Time consuming for employees to compile

– Time consuming for Lenders to underwrite

© 2020 Haynes and Boone, LLP

33

• Sponsor and Fund diligence

– Industry track-record

– Quality of third-party investors

– Fund strategy

• Facility size vs documentation and diligence requirements

© 2020 Haynes and Boone, LLP

34

• Highly customizable facilities

• Sponsor Involvement

– Sponsor backing can be a contentious point when determining the structure

– Lender will want employee loans to be backed by a guaranty of the Sponsor,

or conversely, to have the Sponsor as the primary obligor

– The more senior the employees, the less likely the Sponsor’s credit is needed

and vice versa

• Flexible documentation to cover multiple employees and multiple

investment vehicles

© 2020 Haynes and Boone, LLP

35

Borrowing Base

• Typically calculated based on an advance rate percentage of the lesser

of (i) net asset value of the employee’s equity interest in a fund and (ii)

actual capital contributions paid by the employee to into the fund or co-

investment vehicle

• Equity interests may be removed from the Borrowing Base if net asset

value is impaired for any reason, including the insolvency of the

underlying fund

• No ability to increase Borrowing Base above capital contributions made

• Calculation of net asset value to be determined using an objective

standard that is agreeable to Lender (typically calculated by the third

party administrator of the underlying fund)

© 2020 Haynes and Boone, LLP

36

Borrowing mechanics

• Borrowers permitted to borrow to make capital calls coming due (or to

reimburse the borrower for capital calls made)

• Amount of loan will correspond to the advance rate percentage of the

relevant capital call

• Borrowers will have to evidence or certify to the existence of the relevant

capital call

© 2020 Haynes and Boone, LLP

37

Use of Proceeds

• Availability is limited to amounts needed to pay capital calls

(up to a loan limit)

• If proceeds of a borrowing are not used to make a capital call, they must

be returned to the Lender

• Note that loan proceeds may not cover 100% of the required capital

contributions

© 2020 Haynes and Boone, LLP

38

Mandatory prepayments

• Timing and calculations can vary

• Lender may require the Borrower apply a percentage of distributions

received from the underlying fund in each period to the repayment of the

Loan

• Following an Event of Default or at any time the loan amount exceeds the

Borrowing Base, Borrower will be required to apply 100% of distributions

received to repayment of the Facility

• If any equity interest is disposed of, 100% of the proceeds will be

required to be used to pay down the loan

Approval of underlying investment funds

© 2020 Haynes and Boone, LLP

39

Covenants

• Minimum NAV

• Compliance with underlying fund documentation

• No adverse amendments to the limited partnership agreement of the

underlying fund

• Notice of default under underlying fund

• Notice of suspension of the investment period of underlying fund

© 2020 Haynes and Boone, LLP

40

Covenants

• Compliance reporting

– Capital account statements received from underlying fund

– Delivery of investment reports and material notices from underlying fund

– Financial statements of underlying fund

© 2020 Haynes and Boone, LLP

41

Events of Default

• If the Borrowing Base is comprised of only one or two funds, any

impairment in the value of the underlying equity interests in a fund may

give rise to an Event of Default

• Failure by the Borrower to make any capital call when due, or any other

circumstance that results in the Borrower being a defaulting partner

under the relevant LPA

• Performance declines

Remedies

• Blocking the deposit account from which distributions will be made

• Foreclosing on and disposing of limited partnership interests

© 2020 Haynes and Boone, LLP

42

• Master Agreement for the Sponsor and related entities with supplements

to be signed by employees

– Administrative ease for distribution of loan proceeds and collection of

distributions from the underlying fund

– Streamline reporting

– Maintain confidentiality of personal terms

• Note of each Borrower

• Guarantee of the Sponsor or Employees

© 2020 Haynes and Boone, LLP

43

• Security Agreement pledging the employee’s limited partnership interest

in the fund

– Perfected by filing a UCC-1

• Assignment of the deposit account where collections will be paid and

where loan proceeds will be distributed (typically in the name of Sponsor)

– Deposit account control agreement with depository bank, to perfect the

Lender’s security interest in the account by “control”

• Spousal Consents

© 2020 Haynes and Boone, LLP

44

GP consent

• The limited partnership agreement of the underlying fund likely requires

the consent of the general partner for any assignment of limited

partnership interests

• GP will also consent to the payment of distributions directly to the

pledged deposit account

• Consent to the admission of a replacement limited partner in connection

with an enforcement action

© 2020 Haynes and Boone, LLP

45

Standard loan deliverables:

• Opinion

• Organizational documents and trust documentation (including

documentation of underlying fund)

• Evidence of ownership in the underlying fund (capital account statement,

subscription agreement, etc.)

• Resolutions or Trust Consents

• Incumbency

• Lien searches

© 2020 Haynes and Boone, LLP

46

• Consents for the pledge of LP interests by creditors of the underlying fund

• Personal information on individual employees

• Notarization of loan documents may be required for individuals

© 2020 Haynes and Boone, LLP

47

Fund diligence:

• The LPA of the underlying fund may prohibit or limit the pledge of limited

partnership interests and the scope of GP consent.

• Subscription facility prohibitions or limitations:

– Restricting pledge of partnership interests or bank accounts

– Limiting the timing or payment of distributions following an Event of Default

• Can be a challenge to get information on additional debt of the underlying

fund

© 2020 Haynes and Boone, LLP

48

Changes to employment status

• Consider how this might impact ownership of the partnership interests

and any mandatory prepayment or default triggers for the Lender to

exercise

• One approach is to require the Sponsor to purchase the shares upon a

termination of employment

© 2020 Haynes and Boone, LLP

GP Lines of Credit

49

© 2020 Haynes and Boone, LLP

Fund

General Partner

Management

Company

Sponsor

Employee

Employee

Employee

Third-party

Investors

Investments

GP Facility

$$

Collateral

GP Interests

GP Capital

Contributions

50

© 2020 Haynes and Boone, LLP

51

• Advanced to general partner to finance required GP capital contributions

to the fund

• The facility can be made to the general partner directly, or to a principal of

the fund to invest in the fund through the general partner

• Facility size will vary, but many funds have a minimum capital

commitment requirement for the GP (which is often reflected as a

percentage of total capital commitments)

• Sponsor backing can be a contentious point when determining the

structure

© 2020 Haynes and Boone, LLP

52

GP:

• If a GP line provides financing for a principal of the fund, the principal

gets the benefit of a facility negotiated on their behalf by the Sponsor and

is also able to free up personal capital and assets

• For the GP, access to a credit facility can provide liquidity prior to making

any additional capital calls on its members or partners

Sponsor:

• Satisfies investor requirements for the Sponsor to have more “skin in the

game”

• Permits leveraging of future distributions

© 2020 Haynes and Boone, LLP

53

Lender:

• Payment of interest and fees that are generally higher than those

charged on traditional subscription facilities

• Deepens relationships with Sponsors and their principals

• Makes Lender a more attractive source of portfolio-level financing and

traditional subscription financing

© 2020 Haynes and Boone, LLP

54

Diligence will be performed on any principal of the fund who is obligated to fund

capital calls directly or indirectly through the general partner

• Sponsor and Fund diligence

– Industry track-record

– Quality of third-party investors

– Fund strategy

• Diligence on underlying fund

– Can a GP Interest be pledged (often just interested in economic benefit)

– Can the GP be removed

• Facility size vs documentation and diligence requirements

© 2020 Haynes and Boone, LLP

55

Borrowing Base:

• Typically calculated based on an advance rate percentage of the lesser

of (i) net asset value of the general partnership interest in a fund and (ii)

actual capital contributions paid by the general partner into the fund

• General partnership interests may be removed from the Borrowing Base

if net asset value is impaired for any reason, including the insolvency of

the underlying fund

Calculation of Net Asset Value to be determined using an objective standard that

is agreeable to Lender (typically calculated by the third-party administrator of the

underlying fund)

© 2020 Haynes and Boone, LLP

56

Borrowing Mechanics:

• Borrower will be permitted to borrow to make capital calls coming due (or

to reimburse the employee for capital calls made)

• Amount of loan will correspond to the advance rate percentage of the

relevant capital call

• Borrowers will have to evidence or certify to the existence of the relevant

capital call

© 2020 Haynes and Boone, LLP

57

• If proceeds of a borrowing are not used to make a capital call, they must

be returned to the Lender

• Facilities will typically be revolving up to a loan limit

• To the extent there is overcollateralization, Lenders might consider

permitting loan proceeds to be used for general working capital and

investment purposes

© 2020 Haynes and Boone, LLP

58

Mandatory Prepayments:

• Timing and calculations can vary

• Lender may require the Borrower apply a percentage of distributions

received from the underlying fund in each period to the repayment of the

Loan

• Following an Event of Default or at any time the loan amount exceeds the

Borrowing Base, Borrower will be required to apply 100% of distributions

received to repayment of the facility

• If any general partnership interest is disposed of, 100% of the proceeds

will be required to be used to pay down the loan

© 2020 Haynes and Boone, LLP

59

Covenants:

• No adverse amendment to the limited partnership agreement of the

underlying fund

• Minimum NAV

• Notice of removal by limited partners or suspension of investment period

© 2020 Haynes and Boone, LLP

60

Covenants:

• Compliance reporting

– Capital account statements received from underlying fund

– Delivery of investment reports and material notices from underlying fund

(including any notice relating to misconduct of the general partner or a notice

seeking the removal of the general partner)

– Financial statements of underlying fund

© 2020 Haynes and Boone, LLP

61

Events of Default

• If the Borrowing Base is comprised of only one or two funds, any

impairment in the value of the underlying general partnership

interests in a fund may give rise to an Event of Default

• Failure by the Borrower to make any capital call when due, or any

other circumstance that results in the Borrower being removed as

the general partner under the relevant LPA

Remedies

• Following an Event of Default a Lender might require that upon a

foreclosure of the general partnership interests they will convert to

limited partnership interests and be subject to the same rights and

benefits as other limited partners, or that Lender will only foreclose

on the economic right of such general partner interests

© 2020 Haynes and Boone, LLP

62

Security Agreement pledging the general partnership interest in the fund

• Perfected by filing a UCC-1

Assignment of the Deposit Account where distributions will be paid and where

loan proceeds will be distributed

• Deposit account control agreement with depository bank, to perfect the

Lender’s security interest in the account by “control”

Consent to pledge

• The limited partnership agreement of the underlying fund may require

consents for any assignment of general partnership interests.

© 2020 Haynes and Boone, LLP

63

Standard loan deliverables:

• Opinion

• Organizational documents and trust documentation (including for

underlying funds)

• Resolutions

• Incumbency

• Lien searches

Notarization of loan documents may be required for individuals

© 2020 Haynes and Boone, LLP

64

Fund diligence:

• The LPA of the underlying fund may prohibit or limit the pledge of general

partnership interests.

• Subscription facility prohibitions or limitations:

– Restricting pledge of general partnership interests or bank accounts

– Restricting additional debt of the general partner

– Limiting the timing or payment of distributions following an Event of Default

• Can be a challenge to get information on additional debt of the underlying

fund

• A NAV/hybrid facility would cut off access to payments of distributions

© 2019 Haynes and Boone, LLP

Ellen G. McGinnis

(202) 654-4512

Deborah Low

(212) 918-8987

Alexander Grishman

(212) 918-8965

Questions?

65