pricewaterhousecoopers perspectives on trends in banking* 12 october 2006 *connectedthinking...

TRANSCRIPT

PricewaterhouseCoopers

Perspectives on Trends in Banking*12 October 2006

*connectedthinking

Presentation to the Third Bankseta International

Conference

by

Tom Winterboer

PricewaterhouseCoopers

Perspectives on Trends in Banking

Agenda/Contents

1. Introduction

2. The global banking market

3. Global Market Trends

4. So why and how are things changing?

5. Areas of strategic focus

6. And the risks – Banana Skins 2006

7. Conclusion – five action points for management

Slide 3Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

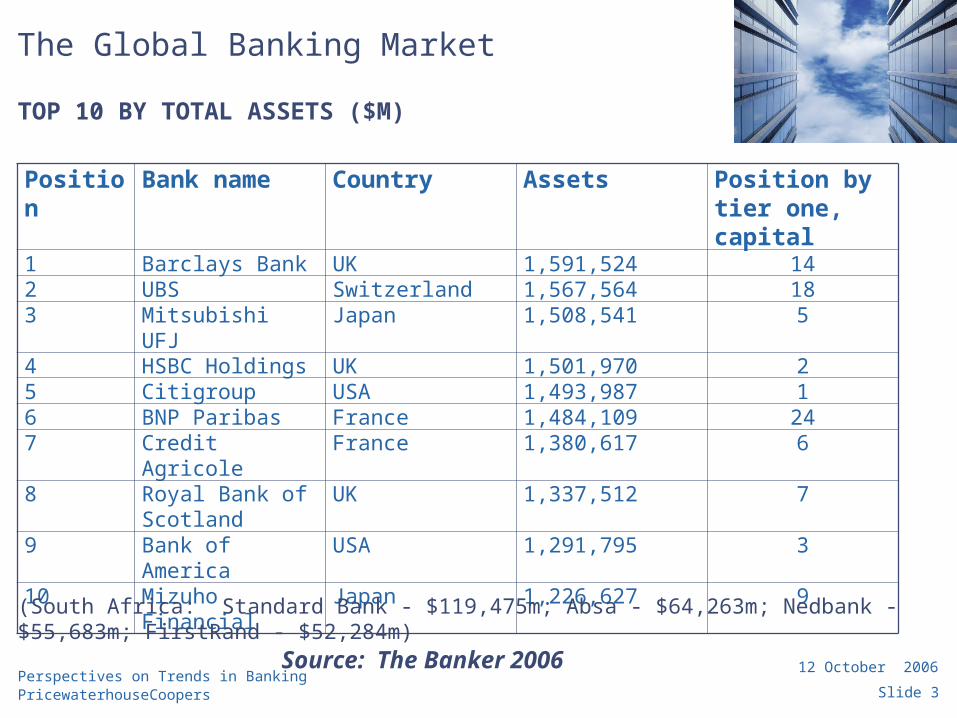

Position Bank name Country Assets Position by tier one, capital

1 Barclays Bank UK 1,591,524 142 UBS Switzerland 1,567,564 183 Mitsubishi UFJ Japan 1,508,541 5

4 HSBC Holdings UK 1,501,970 25 Citigroup USA 1,493,987 16 BNP Paribas France 1,484,109 247 Credit Agricole France 1,380,617 6

8 Royal Bank of Scotland

UK 1,337,512 7

9 Bank of America USA 1,291,795 3

10 Mizuho Financial Japan 1,226,627 9

TOP 10 BY TOTAL ASSETS ($M)

Source: The Banker 2006

The Global Banking Market

(South Africa: Standard Bank - $119,475m; Absa - $64,263m; Nedbank - $55,683m; FirstRand - $52,284m)

PricewaterhouseCoopers

Global Market Trends

• Retail and Commercial Banking Trends

• Capital Markets Trends

• Wealth Management Trends

• Insurance Trends

Slide 5Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Retail and Commercial Banking Trends

• Market maturity and slowing growth are driving an acceleration in inter-regional and cross-border consolidation among US and European players.

• Consumer borrowing in developed nations has reached historically high levels, encouraging banks to seek growth in alternative or emerging markets;

• Corporate borrowing continues to grow at strong rates, but credit risk trends remain benign at this point in the lending cycle.

Market Trends

Slide 6Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Capital Markets Trends

• Fixed income business has grown rapidly in an environment of low real interest rates, and innovation in derivatives is pushing activity to ever greater levels.

• Exceptional liquidity levels are also driving rapid developments in alternative asset classes such as commodities and private equity;

• Potential conflicts of interest and the growing importance of new types of customers like hedge funds and private equity groups are among the factors encouraging investment banks to fundamentally alter their business models.

Market Trends

Slide 7Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Wealth Management Trends

• Asset gathering is accelerating rapidly in developing markets, generating growth in offshore funds. In contrast, onshore wealth managers in the US and Europe are gaining ground from traditional private banks;

• Investment management inflows are increasingly polarised between quantitative strategies and alternative products;

• Consolidation of the investment management industry is accelerating as the growing costs of research, innovation and compliance encourage players to seek economies of scale.

Market Trends

Slide 8Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Insurance Trends

• The non-life insurance industry is showing improved profitability compared to historic norms, helped by better controls and improved pricing discipline. The balance sheet impact of 2005’s catastrophes has been repaired with support from capital markets;

• Life insurers are looking to participate in savings market growth. Now that solvency issues have receded the focus is on how best to use capital in order to maximise growth.

• Product mix is changing and products are evolving as life insurers pursue capital efficiency, respond to new performance measures and compete with asset managers.

Market Trends

Slide 9Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Piecing the Jigsaw - The Future of Financial Services

In June 2005 PwC produced this study considering the drivers, risks and opportunities facing the financial services industry and the impact and responses for existing and potential players in the market.

In compiling this document PwC has drawn out the principle areas of commonality across different regions and territories.

So why and how are things changing?

Position for graphic or image

PricewaterhouseCoopers

So why and how are things changing?

• Piecing the Jigsaw – the Future of Financial Services

• Drivers

Slide 11Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

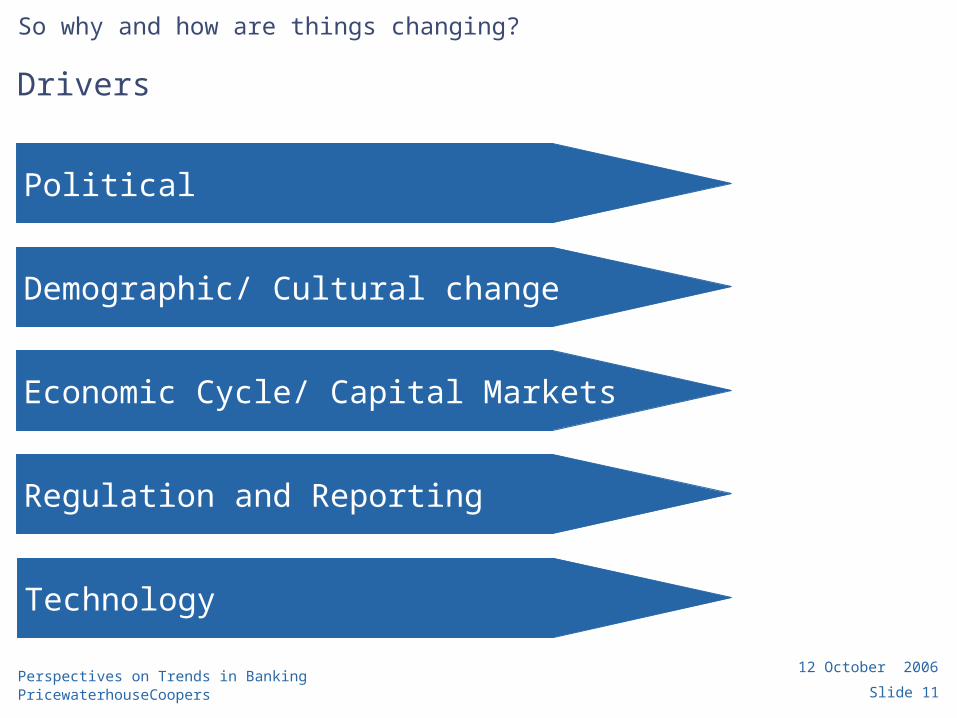

Drivers

So why and how are things changing?

Political

Demographic/ Cultural change

Economic Cycle/ Capital Markets

Regulation and Reporting

Technology

Slide 12Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Political

So why and how are things changing?

Drivers

• Access• Consumer

protection• Enhanced ethical

standards/ expectations

• Stability

Risks

• Agendas• Enhanced ethical

standards / expectations

• Instability• Terrorism

Opportunities

• Globalisation• Government debt• Single market

Slide 13Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Demographic/ Cultural change

So why and how are things changing?

Drivers

• Population (developed markets – greying) (developing markets – emerging middle class)

• Evolving client needs

• High performance culture

• Trust

Risks

• Consumer expectations

• Distribution• Health• High

performance culture

• Pensions

Opportunities

• Health• Population• Products• Regional

differentiation

Slide 14Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Economic Cycle/ Capital Markets

So why and how are things changing?

Drivers

• Competition• Performance• Profitability

Risks

• Competitive pressure

• Performance

Opportunities

• Access to capital• Consumer

demands• Structural

change

Slide 15Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Regulation and Reporting

So why and how are things changing?

Drivers

• Capital requirements

• Governance• Level & intensity• Reporting

Risks

• Compliance• Product offerings• Reporting• Tax• Transparency

Opportunities

• Expansion• Inclusion• Stability• Strategic

alignment• Transparency

Slide 16Perspectives on Trends in BankingPricewaterhouseCoopers

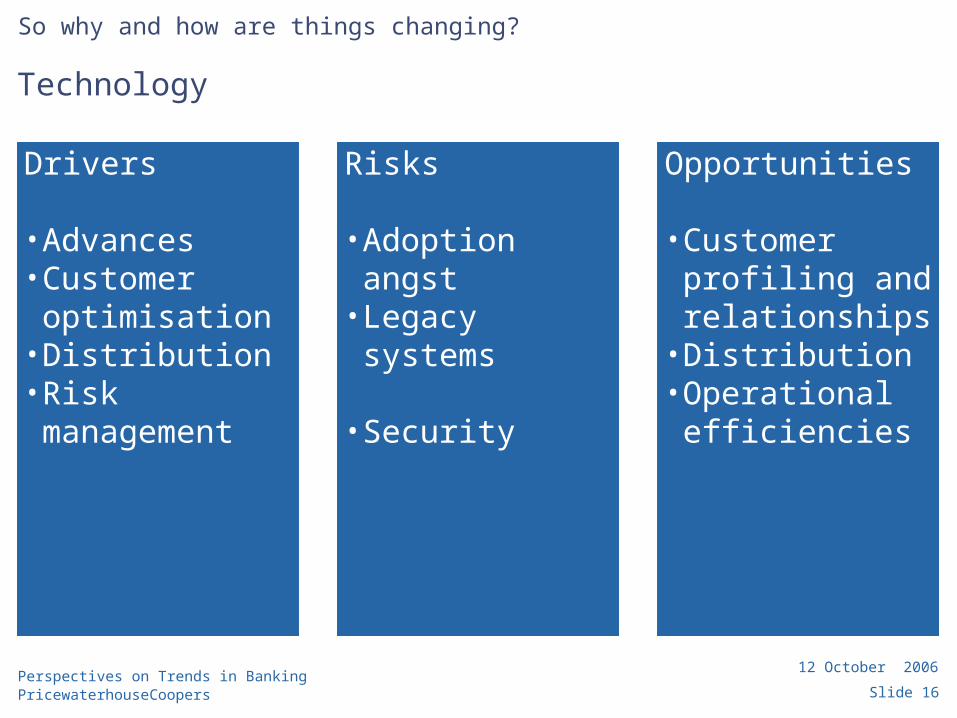

12 October 2006

Technology

So why and how are things changing?

Drivers

• Advances • Customer

optimisation • Distribution• Risk

management

Risks

• Adoption angst • Legacy systems

• Security

Opportunities

• Customer profiling and relationships

• Distribution• Operational

efficiencies

PricewaterhouseCoopers

What are the areas of Strategic Focus?

Slide 18Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

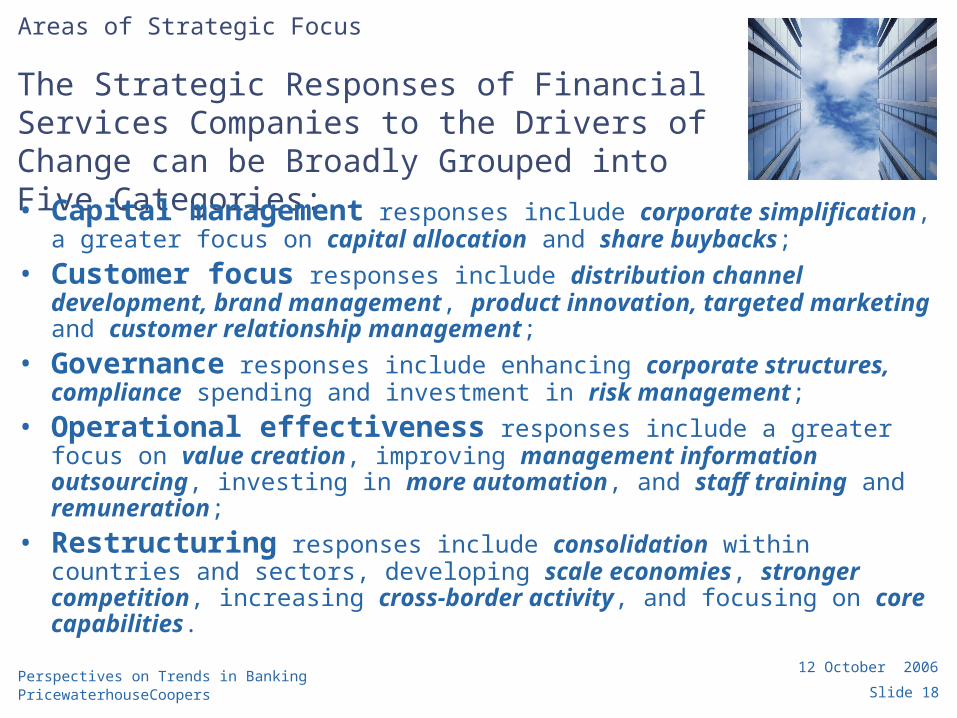

The Strategic Responses of Financial Services Companies to the Drivers of Change can be Broadly Grouped into Five Categories:

• Capital management responses include corporate simplification, a greater focus on capital allocation and share buybacks;

• Customer focus responses include distribution channel development, brand management, product innovation, targeted marketing and customer relationship management;

• Governance responses include enhancing corporate structures, compliance spending and investment in risk management;

• Operational effectiveness responses include a greater focus on value creation, improving management information outsourcing, investing in more automation, and staff training and remuneration;

• Restructuring responses include consolidation within countries and sectors, developing scale economies, stronger competition, increasing cross-border activity, and focusing on core capabilities.

Areas of Strategic Focus

Slide 19Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

About the Banana Skins Survey

Produced in July 2006

11th year, ranking banking risks by their perceived severity

Sponsored by PwC and conducted by David Lascelles of Centre for the Study of Financial Innovation (“CSFI”)

468 responses (440), 60 countries (54), 6 South African respondents

Many of the new respondents now come from emerging markets

Replies confidential

Slide 20Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Banana Skins 2006(2005 Ranking in brackets)

1. Too much regulation (1)

2. Credit risk (2)

3. Derivatives (4)

4. Commodities (14)

5. Interest rates (12)

- “where is the next banking disaster coming

from?”

“there will be one – it is the nature of the beast!”

Andrew Hilton – Director CSFI

Slide 21Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Banana Skins 2006(2005 Ranking in brackets)

6. High dependence on technology (8)

7. Hedge funds (5)

8. Corporate governance (3)

9. Emerging Markets (15)

10.Risk management techniques (9)

Slide 22Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Banana Skins 2006(2005 Ranking in brackets)

11.Fraud (6)

12.Equities (18)

13.Currencies (7)

14.Macro-economic trends (10)

15.Political shocks (22)

16. Conflicts of interest (-)

17. Banking market overcapacity (20)

18. Money laundering (13)

19. Merger mania (27)

20. Legal risk (17)

Slide 23Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Banana Skins 2006(2005 Ranking in brackets)

21.Business continuation (19)

22.Retail sales practices (23)

23. Insurance sector problems (11)

24.Back office (26)

25.Environmental risk (28)

26. Management incentives (21)

27. Rogue trader (24)

28. Competition from new entrants (29)

29. Payment systems (25)

30. Too little regulation (30)

Slide 24Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Big movers

UP:

Commodities: price volatility

Merger mania: - sharp rise in M&A emergence of “unwieldy” groups

- resulting in oligopolistic behaviour (Malaysia & Taiwan)

Emerging markets: stability concerns

Political shocks: Iraq, N. Korea, Middle East

Equities: markets looking “toppy”

Slide 25Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

BananaSkins2006The CSFI’s annual survey of the risks facing banks

CSFICentre for the Study

of Financial Innovation

And the risks?

BANANA SKINS 2006

The CSFI’s annual survey of the risks facing banks

CSFI

Centre for the Study of Financial Innovation

Slide 26Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Conclusion on Banana Skins

“Banks’ readiness to deal with Banana Skins – or at least the perception of their readiness-

has improved. Regulators increased their rating of bank

preparedness as well.”

Slide 27Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Conclusion

Five action points for Management?

There is no single, pre-determined route to success over the coming years. As the leaders of today’s

financial institutions think about the shape of tomorrow’s leading players, their strategies should

embrace five key principles:

Slide 28Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Conclusion

1. Identify and articulate what your institution does best.

A well defined corporate identity, in the minds of

customers, investors, regulators and staff, will be critical.

Whatever an institution’s core activity, it should be at the

heart of its strategy.

Slide 29Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Conclusion

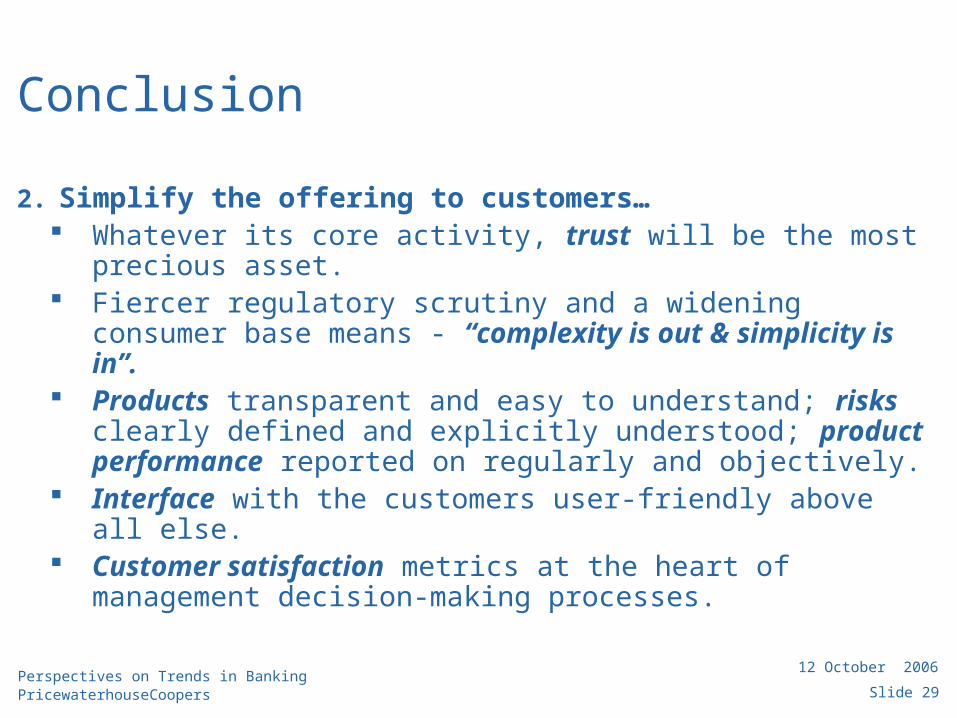

2. Simplify the offering to customers… Whatever its core activity, trust will be the most precious

asset. Fiercer regulatory scrutiny and a widening consumer base

means - “complexity is out & simplicity is in”. Products transparent and easy to understand; risks

clearly defined and explicitly understood; product performance reported on regularly and objectively.

Interface with the customers user-friendly above all else. Customer satisfaction metrics at the heart of

management decision-making processes.

Slide 30Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Conclusion

3. … and simplify the enterprise itself. As the corporate identity and product offering need to

simplify, so will the organisation itself. Technology platforms to be consolidated and integrated. Risks should be assessed and managed on an enterprise-

wide basis. Performance data a panoramic view of the institution. Cost efficiencies will arise as a result. Silos should fade and teams collaborate. Little room for hierarchies, whether based on products or

functions, in tomorrow’s leading institution.

Slide 31Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Conclusion

4. Hone market positioning in line with demographic trends. Whether seeking to take advantage of growth potential of

emergent middle class in developing markets, or target fast-expanding sub-populations through ethnic products and services, or pursuing life-cycle strategies aimed at tomorrow’s pensioners, successful institutions will put demographic trends at the heart of their business plans.

To drive growth effectively, a core of high-potential customers should be identified, and offering built accordingly.

Slide 32Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Conclusion

5. Don’t forget the most important ingredient – people.

“The industry landscape may change but the importance of people is permanent”.

Need high-quality employees at all levels of the organisation.

Next few years will see two pronounced and convergent trends in employee capabilities – towards better data analysis and enhanced customer-facing skills.

Slide 33Perspectives on Trends in BankingPricewaterhouseCoopers

12 October 2006

Further information

Piecing the jigsaw: The future of financial services - http://www.pwc.com/financialservices

Banana Skins - http://www.pwc.com/banking

SA Strategic and Emerging Issues in South African Banking – http://www.pwc.com/banking

Emerging Trends and Strategic Issues in South African Insurance 2006 – http://www.pwc.com/insurance

Strategic and Emerging Issues in the South African Insurance Broking Industry 2005 – http://www.pwc.com/insurance

© 2004 PricewaterhouseCoopers. All rights reserved. “PricewaterhouseCoopers” refers to the network of member firms of PricewaterhouseCoopers International Limited, each of which is a separate and independent legal entity. *connectedthinking is a trademark of PricewaterhouseCoopers.