presented by: osburn & associates, llccreditcongress.nacm.org/pdfs/handouts/27042 - advanced...

TRANSCRIPT

ADVANCED COLLECTION TOOLS

Presented by: Osburn & Associates, LLC

2

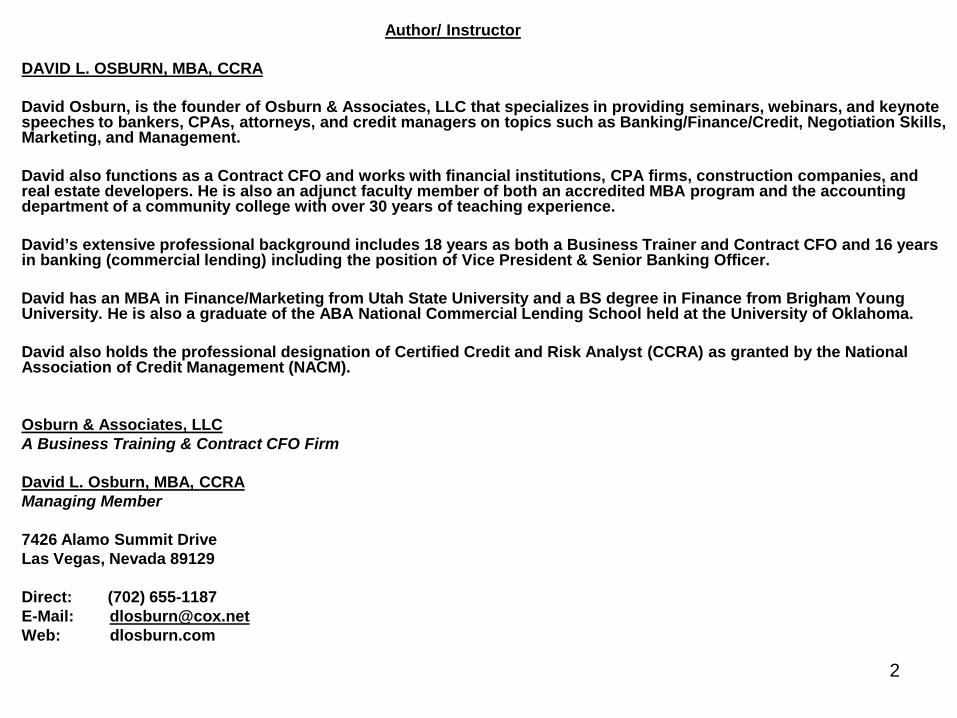

Author/ Instructor DAVID L. OSBURN, MBA, CCRA

David Osburn, is the founder of Osburn & Associates, LLC that specializes in providing seminars, webinars, and keynote speeches to bankers, CPAs, attorneys, and credit managers on topics such as Banking/Finance/Credit, Negotiation Skills, Marketing, and Management.

David also functions as a Contract CFO and works with financial institutions, CPA firms, construction companies, and real estate developers. He is also an adjunct faculty member of both an accredited MBA program and the accounting department of a community college with over 30 years of teaching experience.

David’s extensive professional background includes 18 years as both a Business Trainer and Contract CFO and 16 years in banking (commercial lending) including the position of Vice President & Senior Banking Officer.

David has an MBA in Finance/Marketing from Utah State University and a BS degree in Finance from Brigham Young University. He is also a graduate of the ABA National Commercial Lending School held at the University of Oklahoma.

David also holds the professional designation of Certified Credit and Risk Analyst (CCRA) as granted by the National

Association of Credit Management (NACM).

Osburn & Associates, LLC A Business Training & Contract CFO Firm

David L. Osburn, MBA, CCRA Managing Member

7426 Alamo Summit Drive Las Vegas, Nevada 89129

Direct: (702) 655-1187 E-Mail: [email protected] Web: dlosburn.com

3

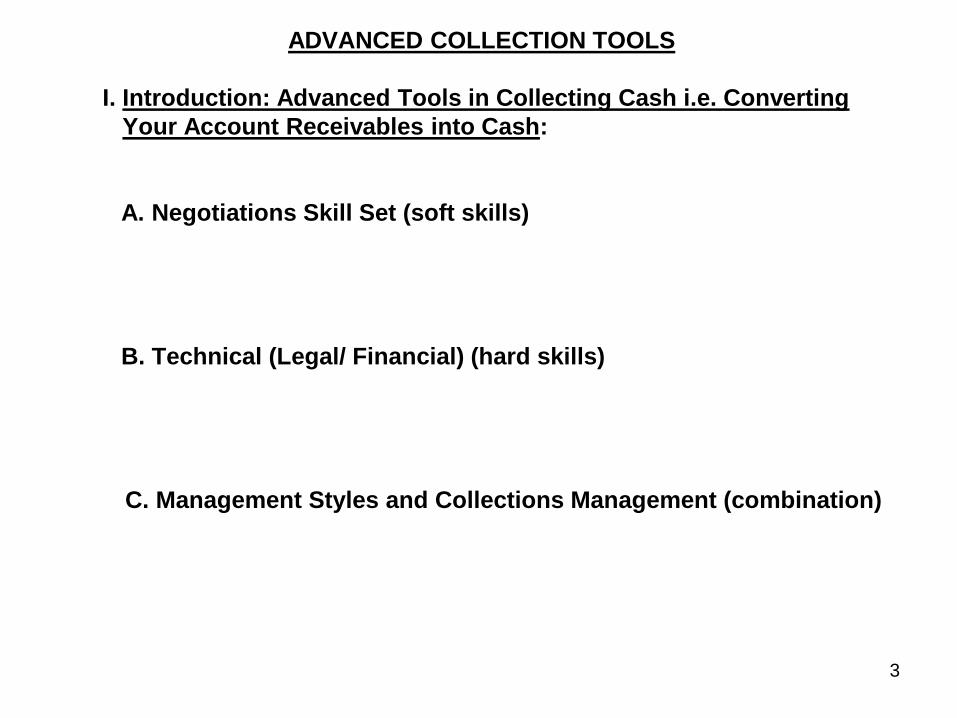

ADVANCED COLLECTION TOOLS

I. Introduction: Advanced Tools in Collecting Cash i.e. Converting Your Account Receivables into Cash: A. Negotiations Skill Set (soft skills) B. Technical (Legal/ Financial) (hard skills) C. Management Styles and Collections Management (combination)

4

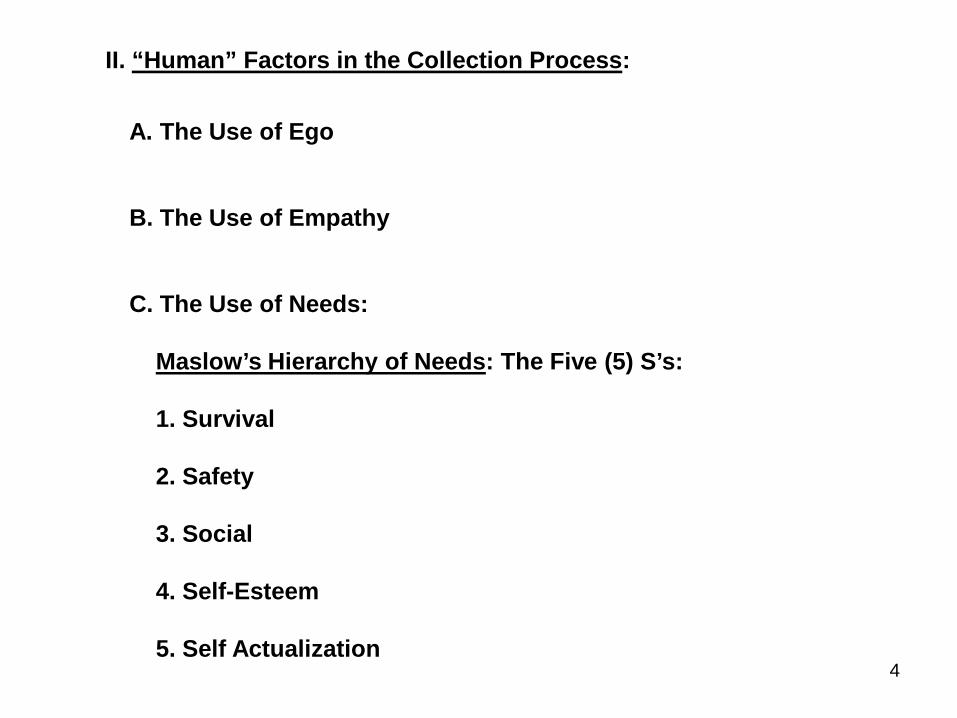

II. “Human” Factors in the Collection Process:

A. The Use of Ego B. The Use of Empathy C. The Use of Needs: Maslow’s Hierarchy of Needs: The Five (5) S’s: 1. Survival 2. Safety 3. Social 4. Self-Esteem 5. Self Actualization

5

III. Business Law Basics including Contract Law and Lender Liability: A. Contract Law (Promissory Note): Components of a Contract: 1. Genuine mutual assent (Offer & Acceptance) 2. Legal contractual capacity a. Minors b. Drunken/drugged individuals c. Insane persons 3. Consideration (of value) 4. Must be legal 5. Must be in writing (sale of land, guarantee other’s debts, more than one year, over $500)

6

B. Lender Liability:

Lender Liability Defined:

Lender's exposure to financial compensation claims relating directly or indirectly to actions taken by the lender. Lender liability

is a complex topic and can include the following: 1. Conflicts of Interest

2. Misrepresentations

3. Inappropriate Control

4. Failure to Fund Commitment

5. Inappropriate Behavior by Lender

7

6. Technical Aspects of Lender Liability:

a. Every word you say may be used against you in a court of law, in a deposition, etc.

b. Referrals vs. Endorsements

c. File Maintenance: Too much, too little!

d. Technical Abilities?

e. Memory: Fuzzy or Clear?

8

IV. How to Avoid Having a “Bad” Account Receivable i.e. Avoiding the “Collection Process”:

A. Understanding your “Borrower’s” Business Structure:

1. C Corporation

2. S Corporation

3. LLC

B. Underwriting the Borrower:

1. Financial Statement Analysis

2. Credit Reports (direct, indirect credit checks)

3. Five Cs of Credit (Capacity, Capital, Collateral, Conditions, Character)

9

C. Proper Structure of the Receivable:

1. Terms

2. Conditions

D. Receivable Support:

1. Collateral (UCC-1 Filing)

2. Guaranties (General & Continuing)

10

VII. What Happens When a “Good” Receivable Turns into a “Bad” Receivable?

A. The Scenario:

1. The Market Turns Down

2. Your Customer’s Customers “Dry Up”

3. The Payments are Delinquent

B. Initial Assessment i.e. Where Are We At?

How Delinquent are the Payments?

30, 60, 90 days

11

C. What is the Condition of Our Borrower & Collateral?

1. Borrower: Financial Update (Financial Statements, Credit Reports, etc.)

2. Collateral:

a. Liquidity

b. Marketability

c. Dependability of Value

d. Controllability

12

D. What is the Condition of Our File?

1. Complete (documentation, etc.)?

2. Too Complete?

13

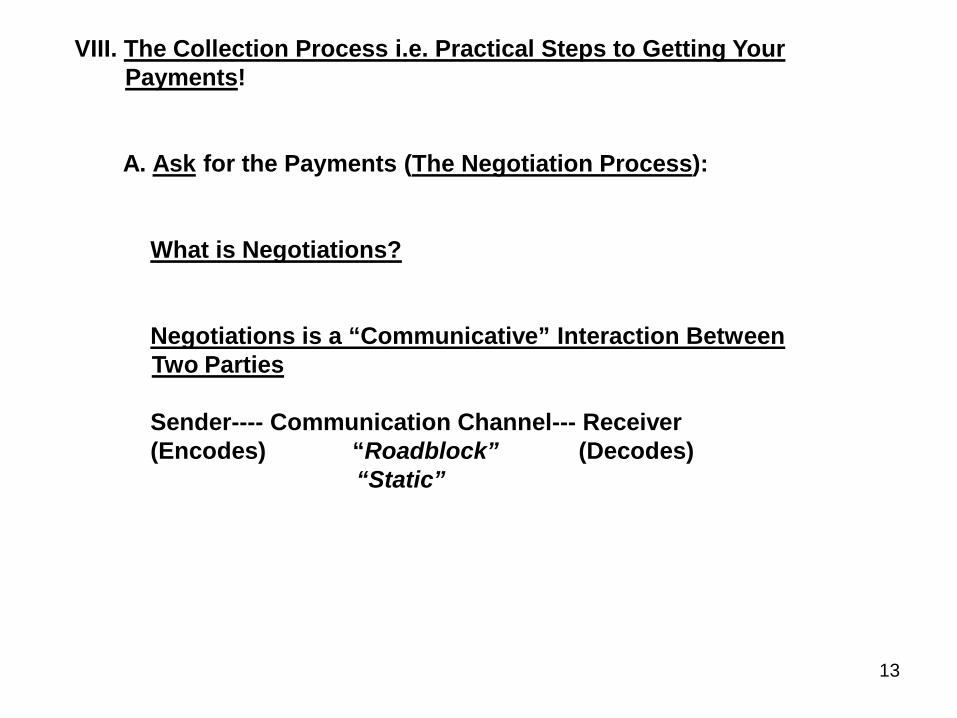

VIII. The Collection Process i.e. Practical Steps to Getting Your Payments!

A. Ask for the Payments (The Negotiation Process):

What is Negotiations?

Negotiations is a “Communicative” Interaction Between Two Parties

Sender---- Communication Channel--- Receiver (Encodes) “Roadblock” (Decodes) “Static”

14

B. Demand the Payments: Collections (How Hard Can You Push?): Fair Debt Collections Practices Act 1. Postcard 2. Represented by an attorney 3. Time: 8am-9pm 4. Place of Employment 5. Not communicate with other parties 6. Refuses to pay, cease to communicate 7. No harassment

15

IX. The Restructure Process (when “regular” payments cannot

be made)

A. Terms:

B. “Good Faith” Payments:

C. Collateral:

D. Additional Support:

16

IX. The Restructure Process (Continued): E. Credit Policy: Does it allow flexibility in “restructuring” the debt? F. Company Management: How flexible is management in “working out a deal”?

17

X. The Company’s Strategy When Negotiations, Collections, and Restructuring Fails A. What is the company’s strategy? B. Is our strategy realistic in today’s market? C. Will the law assist or hurt us? D. What are the political ramifications (within the industry and/or community)?

18

XI. The Company’s Strategy to Protect Its Collateral? A. Repossession of “Personal Property” Ex. A/Rs, Inventory 1. Logistics (including timing) 2. Legal Rights 3. Costs 4. Marketability

19

B. File a Lawsuit to Obtain a Judgment i.e. The Judicial Process Stages of the Litigation Process 1. Pre-litigation concerns 2. Pleadings stage 3. Pretrial activities (Judgment Obtained) 4. Trial procedures 5. Post-judgment concerns 6. Appellate process

20

C. The “Judgment”

1. Obtaining the judgment (first lawsuit)

2. Perfecting the judgment (second lawsuit)

3. What does the judgment really do for your company?

D. Forcing the Customer into Bankruptcy (Who wins?)

1. Chapter 7

2. Chapter 9

3. Chapter 11

4. Chapter 12

5. Chapter 13

21

E. Alternatives to Litigation

1. Arbitration

2. Mediation (Business Marriage Counseling)

F. Walking Away?

22

XIII. The X, Y, and Z Management Styles and Collections Management:

A. Management Styles:

1. Theory X (Authoritative)

2. Theory Y (Delegation)

3. Theory Z (Team Approach)

23

XIII. The X, Y, and Z Management Styles and Collections Management (Continued): B. Collections Management: 1. “People” Skills 2. Listening Skills 3. Communication Skills 4. Time Management Skills

24

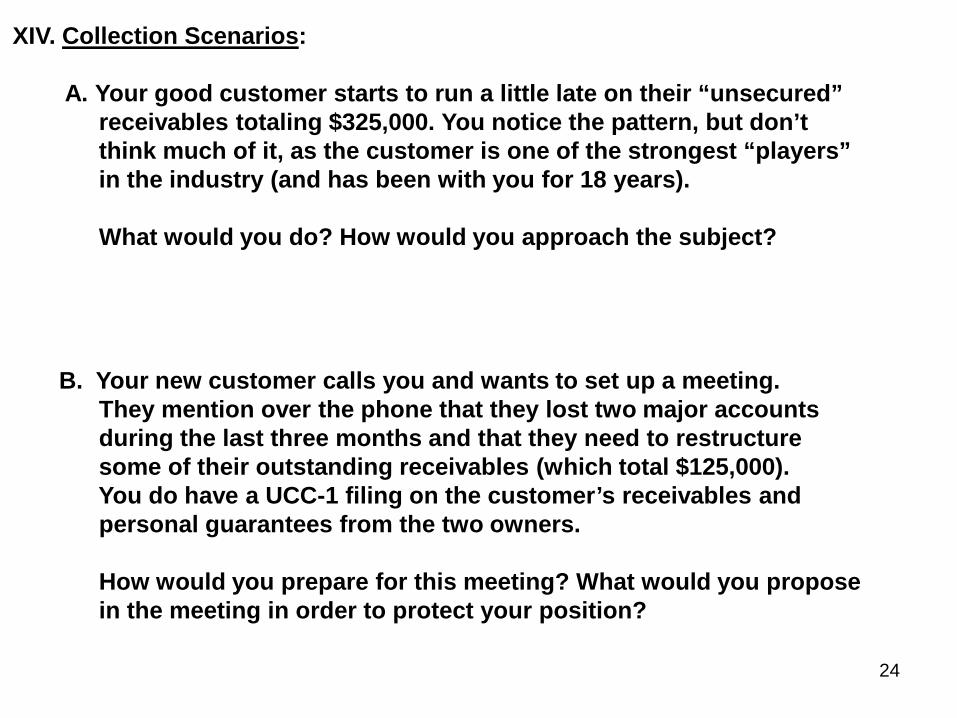

XIV. Collection Scenarios: A. Your good customer starts to run a little late on their “unsecured” receivables totaling $325,000. You notice the pattern, but don’t think much of it, as the customer is one of the strongest “players” in the industry (and has been with you for 18 years). What would you do? How would you approach the subject? B. Your new customer calls you and wants to set up a meeting. They mention over the phone that they lost two major accounts during the last three months and that they need to restructure some of their outstanding receivables (which total $125,000). You do have a UCC-1 filing on the customer’s receivables and personal guarantees from the two owners. How would you prepare for this meeting? What would you propose in the meeting in order to protect your position?

25

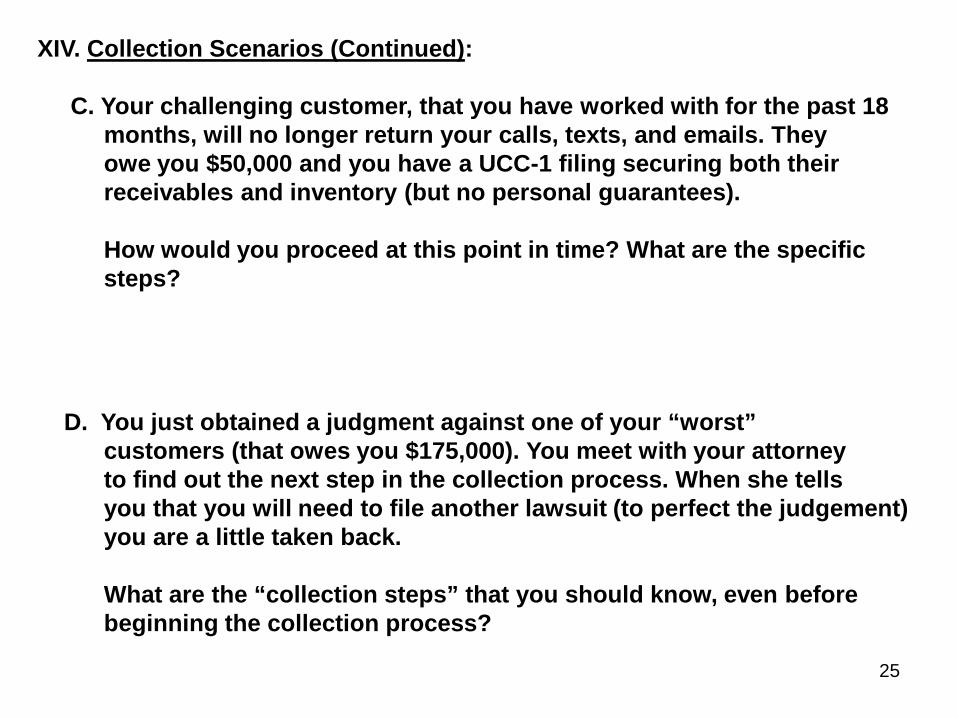

XIV. Collection Scenarios (Continued): C. Your challenging customer, that you have worked with for the past 18 months, will no longer return your calls, texts, and emails. They owe you $50,000 and you have a UCC-1 filing securing both their receivables and inventory (but no personal guarantees). How would you proceed at this point in time? What are the specific steps? D. You just obtained a judgment against one of your “worst” customers (that owes you $175,000). You meet with your attorney to find out the next step in the collection process. When she tells you that you will need to file another lawsuit (to perfect the judgement) you are a little taken back. What are the “collection steps” that you should know, even before beginning the collection process?

26

XV. Ethical Behavior and the Collection Process

Be Trustworthy and full of Integrity aka

“Your Word is Your Bond!”