presentation slides - full year 2011 financial results

TRANSCRIPT

PRESENTATION SLIDES - FULL YEAR 2011 FINANCIAL RESULTS * FINANCIAL STATEMENT AND RELATED

ANNOUNCEMENT

Like 0 0

* Asterisks denote mandatory information

Name of Announcer * CAPITAMALL TRUST

Company Registration No. N.A.

Announcement submitted on

behalf of CAPITAMALL TRUST ("CMT")

Announcement is submitted with

respect to *CAPITAMALL TRUST

Announcement is submitted by * Kannan Malini

Designation * Company Secretary, CapitaMall Trust Management Limited (CMTML) (as manager of

CMT)

Date & Time of Broadcast 18-Jan-2012 07:09:15

Announcement No. 00009

>> ANNOUNCEMENT DETAILS

The details of the announcement start here ...

For the Financial Period Ended * 31-12-2011

Description The attached presentation materials issued by CMTML on the above matter is for

information.

Attachments

Total size = 2614K

(2048K size limit recommended) Total attachment size has exceeded the recommended value

CMT_PresentationSlides_FY2011Results_Annexes.pdf

CMT_PresentationSlides_FY2011Results.pdf

CAPITAMALL TRUST Singapore’s First & Largest REIT

Full Year 2011 Financial Results 18 January 2012

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

This presentation may contain forward-looking statements that involve assumptions, risks and uncertainties. Actual

future performance, outcomes and results may differ materially from those expressed in forward-looking statements as a

result of a number of risks, uncertainties and assumptions. Representative examples of these factors include (without

limitation) general industry and economic conditions, interest rate trends, cost of capital and capital availability,

competition from other developments or companies, shifts in expected levels of occupancy rate, property rental income,

charge out collections, changes in operating expenses (including employee wages, benefits and training costs),

governmental and public policy changes and the continued availability of financing in the amounts and the terms

necessary to support future business. You are cautioned not to place undue reliance on these forward-looking

statements, which are based on the current view of management on future events.

The information contained in this presentation has not been independently verified. No representation or warranty

expressed or implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or

correctness of the information or opinions contained in this presentation. Neither CapitaMall Trust Management Limited

(the “Manager”) or any of its affiliates, advisers or representatives shall have any liability whatsoever (in negligence or

otherwise) for any loss howsoever arising, whether directly or indirectly, from any use, reliance or distribution of this

presentation or its contents or otherwise arising in connection with this presentation.

The past performance of CapitaMall Trust (“CMT”) is not indicative of the future performance of CMT. Similarly, the past

performance of the Manager is not indicative of the future performance of the Manager.

The value of units in CMT (“Units”) and the income derived from them may fall as well as rise. Units are not obligations

of, deposits in, or guaranteed by, the Manager or any of its affiliates. An investment in Units is subject to investment

risks, including the possible loss of the principal amount invested.

Investors have no right to request that the Manager redeem or purchase their Units while the Units are listed. It is

intended that holders of Units (Unitholders) may only deal in their Units through trading on Singapore Exchange

Securities Trading Limited (the “SGX-ST”). Listing of the Units on the SGX-ST does not guarantee a liquid market for the

Units.

This presentation is for information only and does not constitute an invitation or offer to acquire, purchase or subscribe

for Units.

Disclaimer

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Contents

3

Year in Review

Key Financial Highlights

Portfolio Updates

Asset Enhancements

Greenfield Development

Looking Forward

CapitaMall Trust Full Year 2011 Financial Results *January 2012* Year in Review Iluma

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Year in Review

• Strong operational performance despite economic uncertainty

– Tenant sales up by 6.3%

– 503 new leases/renewals achieved with 6.4% positive rental reversion

– Healthy consumer spending and record tourist arrivals of about 13 million

• Asset enhancements

– JCube more than 90.0% committed

– Commenced AEIs(1) at Atrium@Orchard and Iluma

• Acquisition of Iluma and first foray in greenfield development

– Acquired Iluma in April 2011; potential synergies with Bugis Junction

– First greenfield project, Westgate, in Singapore‟s largest regional centre

• Proactive capital management

– Raised approximately S$1.3 billion through debt market and private placement

Set up S$2.5 billion retail bond programme and first S-REIT to launch 2-year retail bonds

Issued US$645.0 million CMBS(2) through RCS Trust

(1) AEIs: Asset Enhancement Initiatives

(2) CMBS: Commercial mortgage backed security

5

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 6 Key Financial Highlights

Bugis Junction

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 7

Distribution Per Unit for 10 Nov – 31 Dec 2011

(1) 4Q 2011 distribution income includes release of S$4.4 million of taxable income retained in 1Q 2011 and approximately S$2.2 million of net capital

distribution income from CapitaRetail China Trust (“CRCT”), after interest expense of S$0.4 million, being the balance of the S$5.2 million received

from CRCT retained in 3Q 2011.

(2) In 4Q 2010, distribution income included release of S$3.5 million, being the balance of the S$4.5 million taxable income retained in 1Q 2010.

(3) Advanced distribution income included S$1.0 million taxable income (part of the S$4.4 million taxable income retained in 1Q 2011) and S$1.0 million of

net capital distribution income after interest expense and other borrowing costs (part of the S$2.6 million from CRCT retained in 3Q 2011). The

advanced distribution was paid following the issuance of the 139,665,000 new Units via a private placement exercise completed on 10 November

2011.

(4) DPU in the table above is computed on the basis that as at the books closure date, none of the outstanding S$256.25 million (after the repurchase of

S$306.0 million in FY 2010 and FY 2011 as well as the redemption of S$87.75 million on 4 July 2011 upon the exercise of put option by the

bondholders) in principal amount of the S$650.0 million 1.0% convertible bonds due 2013 (“Convertible Bonds due 2013”) and the S$350.0 million

2.125% convertible bonds due 2014 ( “Convertible Bonds due 2014”) has been converted into Units. Accordingly, the actual quantum of DPU may

differ from the table above if any of the Convertible Bonds is converted into Units before the books closure date.

(5) Distribution for the period included release of S$3.4 million (being the balance of the S$4.4 million taxable income retained in 1Q 2011) and S$1.2

million of net capital distribution income after interest expense and other borrowing costs (being the balance of the S$2.6 million received from CRCT

retained in 3Q 2011). Distribution for 10 November 2011 to 31 December 2011 was based on enlarged unit base due to the private placement.

Distributable income for the period

10 Nov 2011 to 31 Dec 2011

4Q 2011 Distributable income

Annualised distribution/unit (DPU)

Annualised distribution yield (Based on unit price of S$1.75 on 17 Jan 2012)

S$42.9m(5)

(S$32.6m)(3)

5.22%

1.28¢(4),(5)

9.13¢(1),(4)

4Q 2011

Actual DPU

Advanced distribution for 1 Oct 2011

to 9 Nov 2011, paid on 6 Jan 2012

S$75.5m(1) 2.30¢(1)

(1.02¢)(3)

2.36¢(2)

9.36¢

DPU

S$75.4m(2)

4Q 2010

Actual

Less:

N.A. N.A.

N.A. N.A.

N.A. – Not Applicable

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(1) FY 2011 distribution income includes release of S$8.8 million of net tax-exempt and capital distribution income (after

interest expense and other borrowing costs) from CRCT retained in FY 2010. In addition, CMT has received capital

distribution income from CRCT of S$5.1 million and S$5.2 million respectively in 1Q 2011 and 3Q 2011, of which S$5.1

million is retained for future distribution.

(2) DPU in the table above is computed on the basis that none of the Convertible Bonds due 2013 and due 2014 is

converted into Units before the books closure date. Accordingly, the actual quantum of DPU may differ from the table

above if any of the Convertible Bonds is converted into Units before the books closure date.

FY 2011 Distribution Per Unit Up 1.4% Y-o-Y

Distributable income

Estimated distribution/unit (DPU)

Annualised distribution yield (Based on unit price of S$1.75 on 17 Jan 2012)

S$301.6m(1)

9.37¢(2)

5.35%

S$294.8m

9.24¢

2.3%

1.4%

FY 2011

Actual Chg FY 2010

Actual

CMT Remains Committed to Distribute 100% of its Taxable Income

8

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

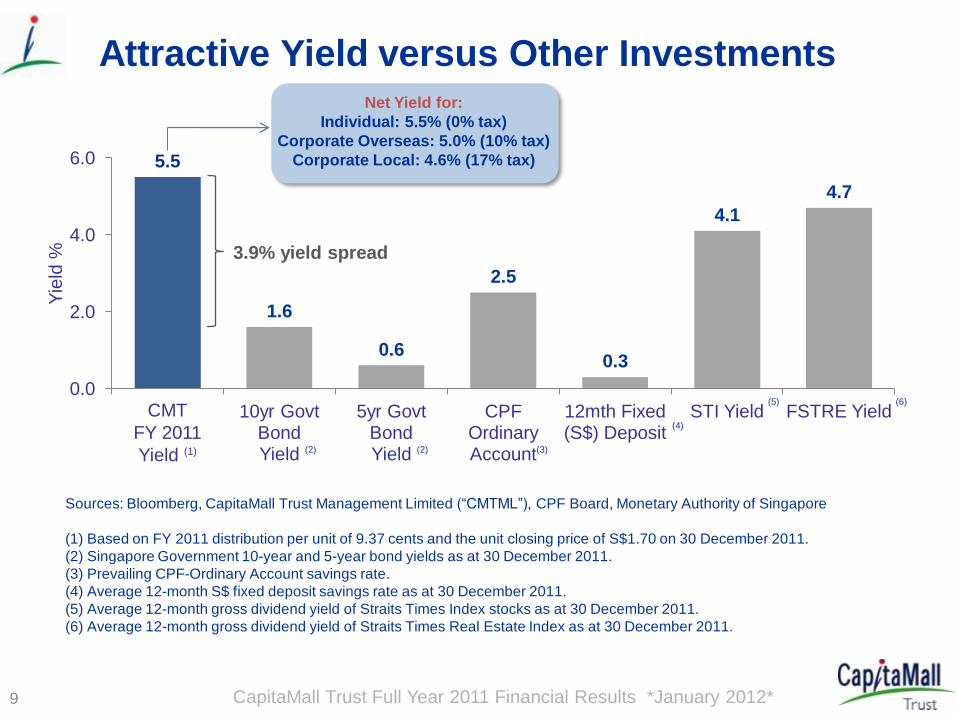

Attractive Yield versus Other Investments

Sources: Bloomberg, CapitaMall Trust Management Limited (“CMTML”), CPF Board, Monetary Authority of Singapore

(1) Based on FY 2011 distribution per unit of 9.37 cents and the unit closing price of S$1.70 on 30 December 2011.

(2) Singapore Government 10-year and 5-year bond yields as at 30 December 2011.

(3) Prevailing CPF-Ordinary Account savings rate.

(4) Average 12-month S$ fixed deposit savings rate as at 30 December 2011.

(5) Average 12-month gross dividend yield of Straits Times Index stocks as at 30 December 2011.

(6) Average 12-month gross dividend yield of Straits Times Real Estate Index as at 30 December 2011.

5.5

1.6

0.6

2.5

0.3

4.1

4.7

0.0

2.0

4.0

6.0

CMT FY 2011 Yield

10yr Govt Bond Yield

5yr Govt Bond Yield

CPF Ordinary Account

12mth Fixed (S$) Deposit

STI Yield FSTRE Yield

Yie

ld %

(1) (2) (2) (3)

(4)

(5) (6)

Net Yield for:

Individual: 5.5% (0% tax)

Corporate Overseas: 5.0% (10% tax)

Corporate Local: 4.6% (17% tax)

3.9% yield spread

9

CMT

FY 2011

Yield (1)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

64.9

98.1

126.8

169.4

211.2

238.4

282.0294.8 301.6

60

140

220

300

2003 2004 2005 2006 2007 2008 2009 2010 2011

S$ million

Steady Distributable Income Growth

10

(1) Based on compounded annual growth rate (“CAGR”).

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

4Q 2011

S$‟000

4Q 2010

S$‟000

Chg

(%)

Gross revenue 157,886 151,347 4.3

Less property operating expenses (59,094) (49,866) 18.5

Net property income 98,792 101,481 (2.6)

Interest and other income 634 539 17.6

Administrative expenses (11,201) (10,452) 7.2

Interest expenses (31,520) (30,731) 2.6

Net income before tax and share of profit of associate 56,705 60,837 (6.8)

Adjustments:

Net effect of non-tax deductible items 11,200 10,922 2.5

Net loss/(profit) from joint ventures/subsidiaries 914 184 396.7

Amount available for distribution to Unitholders 68,819 71,943 (4.3)

Distributable income 75,483(1) 75,443 0.1

Less:

Advanced distribution for the period 1 Oct 2011 to 9 Nov 2011 paid on 6 Jan 2012 (32,564) N.A. N.A.

Distributable income for the period 10 Nov 2011 to 31 Dec 2011 42,919 N.A. N.A.

Distribution Statement (4Q 2011 vs 4Q 2010)

(1) Distribution income for 4Q 2011 includes release of S$4.4 million of taxable income retained in 1Q 2011 and approximately

S$2.2 million of net capital distribution income from CRCT, after interest expense of S$0.4 million, being the balance of the

S$5.2 million received from CRCT retained in 3Q 2011.

11 N.A. – Not Applicable

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(1) Distribution income for FY 2011 includes release of S$8.8 million of net tax-exempt and capital distribution income (after

interest expense and other borrowing costs) from CRCT retained in FY 2010. In addition, CMT has received capital

distribution from CRCT of S$5.1 million and S$5.2 million respectively in 1Q 2011 and 3Q 2011, of which S$5.1 million is

retained for future distribution.

(2) For FY 2010, CMT retained a total of S$10.1 million of tax-exempt and capital distribution income from CRCT.

Distribution Statement (FY 2011 vs FY 2010) FY 2011

S$‟000

FY 2010

S$‟000

Chg

(%)

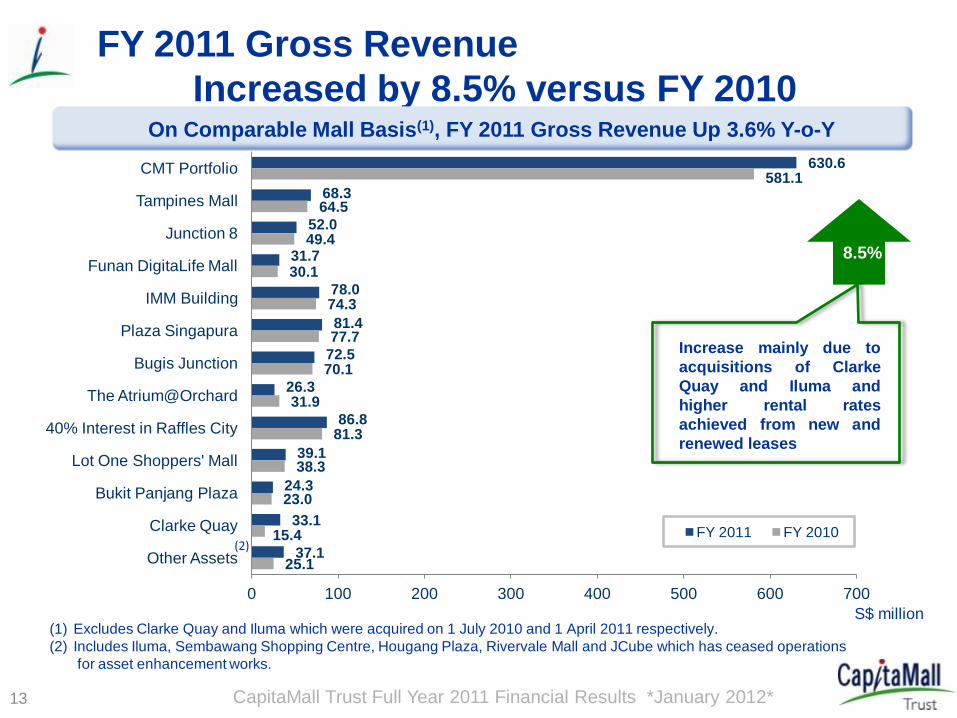

Gross revenue 630,573 581,120 8.5

Less property operating expenses (212,333) (181,973) 16.7

Net property income 418,240 399,147 4.8

Interest and other income 2,332 2,022 15.3

Administrative expenses (43,222) (39,448) 9.6

Interest expenses (134,956) (118,458) 13.9

Net income before tax and share of profit of associate 242,394 243,263 (0.4)

Adjustments:

Net effect of non-tax deductible items 44,883 50,978 (12.0)

Rollover Adjustment - 564 N.M.

Distributable income from associate 10,344 10,148 1.9

Net loss/(profit) from joint ventures/subsidiaries 217 (9) N.M.

Amount available for distribution to Unitholders 297,838 304,944 (2.3)

Distributable income 301,570(1) 294,796(2) 2.3

12

N.M. – Not Meaningful

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

630.6

68.3

52.0

31.7

78.0

81.4

72.5

26.3

86.8

39.1

24.3

33.1

37.1

581.1

64.5

49.4

30.1

74.3

77.7

70.1

31.9

81.3

38.3

23.0

15.4

25.1

0 100 200 300 400 500 600 700

CMT Portfolio

Tampines Mall

Junction 8

Funan DigitaLife Mall

IMM Building

Plaza Singapura

Bugis Junction

The Atrium@Orchard

40% Interest in Raffles City

Lot One Shoppers' Mall

Bukit Panjang Plaza

Clarke Quay

Other Assets

FY 2011 FY 2010

FY 2011 Gross Revenue

Increased by 8.5% versus FY 2010

(2)

S$ million (1) Excludes Clarke Quay and Iluma which were acquired on 1 July 2010 and 1 April 2011 respectively.

(2) Includes Iluma, Sembawang Shopping Centre, Hougang Plaza, Rivervale Mall and JCube which has ceased operations

for asset enhancement works.

8.5%

Increase mainly due to

acquisitions of Clarke

Quay and Iluma and

higher rental rates

achieved from new and

renewed leases

On Comparable Mall Basis(1), FY 2011 Gross Revenue Up 3.6% Y-o-Y

13

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

212.4

19.2

16.0

11.5

27.5

22.2

22.4

10.6

23.3

12.7

8.9

14.4

23.7

182.0

17.7

15.0

10.5

25.2

20.3

22.2

9.7

22.7

12.3

8.2

6.8

11.4

0 50 100 150 200 250

CMT Portfolio

Tampines Mall

Junction 8

Funan DigitaLife Mall

IMM Building

Plaza Singapura

Bugis Junction

The Atrium@Orchard

40% Interest in Raffles City

Lot One Shoppers' Mall

Bukit Panjang Plaza

Clarke Quay

Other Assets

FY 2011 FY 2010

14

FY 2011 Operating Expenses

Increased by 16.7% versus FY 2010

(2)

S$ million (1) Excludes Clarke Quay and Iluma which were acquired on 1 July 2010 and 1 April 2011 respectively.

(2) Includes Iluma, Sembawang Shopping Centre, Hougang Plaza, Rivervale Mall and JCube which has ceased operations

for asset enhancement works.

Increase mainly due to

acquisitions of Clarke

Quay and Iluma

16.7%

On Comparable Mall Basis(1), FY 2011 OPEX Up 7.9% Y-o-Y

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

418.2

49.1

36.0

20.2

50.5

59.2

50.1

15.7

63.5

26.4

15.4

18.7

13.4

399.1

46.8

34.3

19.6

49.0

57.4

47.9

22.1

58.6

26.0

14.8

8.6

14.0

0 50 100 150 200 250 300 350 400 450

CMT Portfolio

Tampines Mall

Junction 8

Funan DigitaLife Mall

IMM Building

Plaza Singapura

Bugis Junction

The Atrium@Orchard

40% Interest in Raffles City

Lot One Shoppers' Mall

Bukit Panjang Plaza

Clarke Quay

Other Assets

FY 2011 FY 2010

FY 2011 Net Property Income

Increased by 4.8% versus FY 2010

(2)

S$ million

4.8%

(1) Excludes Clarke Quay and Iluma which were acquired on 1 July 2010 and 1 April 2011 respectively.

(2) Includes Iluma, Sembawang Shopping Centre, Hougang Plaza, Rivervale Mall and JCube which has ceased operations

for asset enhancement works.

On Comparable Mall Basis(1), FY 2011 NPI Up 1.7% Y-o-Y

15

Increase mainly due to

acquisitions of Clarke

Quay and Iluma

Debt Maturity Profile as at 31 December 2011

Notes:

(1) Secured S$256.25 million 1.0% CBs due 2013 with conversion price of S$3.39 redeemable on 2 July 2013 at 109.31% of the

principal amount.

(2) CBs due 2014 at fixed rate of 2.125% p.a. with initial conversion price of S$2.2692.

(3) US$500.0m 4.321% fixed rate notes were swapped to S$699.5m at a fixed interest rate of 3.794% p.a. in April 2010.

(4) Drawdown of S$650.0 million by Infinity Trusts (CMT‟s 30.0% share thereof is S$195.0 million) from the S$820.0 million

secured banking facility on 30 November 2011.

(5) S$200.0 million 5-year term loan under Silver Oak (CMT‟s 40.0% share thereof is S$80.0 million).

(6) On 21 June 2011, Silver Oak issued US$645.0 million in principal amount of Class A Secured Floating Rate Notes with

expected maturity on 21 June 2016 (the “Series 002 Notes”). The Series 002 Notes are issued pursuant to the S$10.0 billion

Multicurrency Secured Medium Term Note Programme established by Silver Oak and are secured by its rights to Raffles City

Singapore. The proceeds have been swapped into S$800.0 million (CMT‟s share thereof is S$320.0 million).

Debts with secured assets Silver Maple: Silver Maple Investment Corporation Ltd

Silver Oak: Silver Oak Ltd

CBs: Convertible bonds

CMBS: Commercial mortgage backed securities

16

0

100

200

300

400

500

600

700

800

900

2012 2013 2014 2015 2016 2017

Secured Banking Facilities Secured Fixed Rate Term Loan from Silver Maple under CMBS

CBs due 2013 and 2014 Retail Bonds at fixed interest rate of 2.0% p.a.

Fixed Rate Notes issued under S$ Medium Term Note ("MTN") Programme Fixed Rate Notes issued under US$ Euro-Medium Term Note ("EMTN") Programme

Secured term loan from Silver Oak - 40.0% interest in RCS Trust Secured CMBS from Silver Oak - 40.0% interest in RCS Trust

799.5

580.1

S$ m

illi

on

250.0

500.0

150.0300.0

100.0

783.0 280.1(1)699.5(3)

320.0(6)

80.0(5)350.0(2)

595.0

195.0(4)

250.0

0

100

200

300

400

500

600

700

800

900

2012 2013 2014 2015 2016 2017

Secured Banking Facilities Secured Fixed Rate Term Loan from Silver Maple under CMBS

CBs due 2013 and 2014 Retail Bonds at fixed interest rate of 2.0% p.a.

Fixed Rate Notes issued under S$ Medium Term Note ("MTN") Programme Fixed Rate Notes issued under US$ Euro-Medium Term Note ("EMTN") Programme

Secured term loan from Silver Oak - 40.0% interest in RCS Trust Secured CMBS from Silver Oak - 40.0% interest in RCS Trust

0

100

200

300

400

500

600

700

800

900

2012 2013 2014 2015 2016 2017

Secured Banking Facilities Secured Fixed Rate Term Loan from Silver Maple under CMBS

CBs due 2013 and 2014 Retail Bonds at fixed interest rate of 2.0% p.a.

Fixed Rate Notes issued under S$ Medium Term Note ("MTN") Programme Fixed Rate Notes issued under US$ Euro-Medium Term Note ("EMTN") Programme

Secured term loan from Silver Oak - 40.0% interest in RCS Trust Secured CMBS from Silver Oak - 40.0% interest in RCS Trust

0

100

200

300

400

500

600

700

800

900

2012 2013 2014 2015 2016 2017

Secured Banking Facilities Secured Fixed Rate Term Loan from Silver Maple under CMBS

CBs due 2013 and 2014 Retail Bonds at fixed interest rate of 2.0% p.a.

Fixed Rate Notes issued under S$ Medium Term Note ("MTN") Programme Fixed Rate Notes issued under US$ Euro-Medium Term Note ("EMTN") Programme

Secured term loan from Silver Oak - 40.0% interest in RCS Trust Secured CMBS from Silver Oak - 40.0% interest in RCS Trust

0

100

200

300

400

500

600

700

800

900

2012 2013 2014 2015 2016 2017

Secured Banking Facilities Secured Fixed Rate Term Loan from Silver Maple under CMBS

CBs due 2013 and 2014 Retail Bonds at fixed interest rate of 2.0% p.a.

Fixed Rate Notes issued under S$ Medium Term Note ("MTN") Programme Fixed Rate Notes issued under US$ Euro-Medium Term Note ("EMTN") Programme

Secured term loan from Silver Oak - 40.0% interest in RCS Trust Secured CMBS from Silver Oak - 40.0% interest in RCS Trust

595.0

Programme Programme

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Key Financial Indicators

(1) Total Assets exclude non-eliminated portion of CMT‟s loan to Infinity Trusts arising from proportionate accounting.

(2) Ratio of borrowings (including 40.0% share of borrowings of S$400.0 million at RCS Trust level and 30.0% share of

borrowings of S$195.0 million at Infinity Trusts level), over total deposited properties for CMT Group (exclude non-

eliminated portion of CMT‟s loan to Infinity Trusts arising from proportionate accounting).

(3) Net Debt comprises Gross Debt less temporary cash intended for acquisition and refinancing and EBITDA refers

to earnings before interest, tax, depreciation and amortisation.

(4) Ratio of net investment income at CMT Group before interest and tax over interest expense for FY 2011. (In

computing the ratio, cost of raising debt is excluded from interest expense).

(5) Ratio of interest expenses over weighted average borrowings.

(6) Moody‟s has affirmed a corporate family rating of “A2” with a stable outlook to CMT in February 2011.

As at 31 December 2011

As at 30 September 2011

Unencumbered Assets as % of Total Assets(1) 37.9% 38.7%

Gearing Ratio(2) 38.4% 38.4%

Net Debt / EBITDA(3) 7.4 x 7.6 x

Interest Coverage Ratio(4) 3.3 x 3.4 x

Average Term to Maturity (years) 2.7 2.8

Average Cost of Debt(5) 3.5% 3.6%

CMT‟s Corporate Rating(6) “A2”

17

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Valuations and Valuation Cap Rates

(1) Reflects valuation of the property in its entirety.

(2) Comprising Hougang Plaza, JCube, Sembawang Shopping Centre, Rivervale Mall and Iluma which was acquired on 1 April 2011.

(3) Iluma‟s valuation was dated 21 February 2011.

(4) Valuation per sq ft excludes JCube which has been closed for asset enhancement works.

(5) Total valuation exlcudes the Jurong Gateway site which is currently under development.

(6) Not meaningful because Raffles City Singapore comprises retail units, office units, hotels and convention centre.

(7) Valuation per sq ft excludes JCube and Raffles City Singapore.

(8) Valuation of the land as at 1 November 2011.

Valuation as

at 31 Dec 11

S$ million

Valuation as

at 30 Jun 11

S$ million

Variance

S$ million

Valuation as at

31 Dec 11

S$ per sq ft NLA

Valuation Cap

Rate

as at 31 Dec 11

Valuation Cap

Rate

as at 30 Jun 11

Cap rate

Variance

(bps)

Tampines Mall 800.0 794.0 6.0 2,431 5.50% 5.65% (15)

Junction 8 597.0 580.0 17.0 2,363 5.50% 5.65% (15)

Funan DigitaLife Mall 347.0 338.0 9.0 1,161 5.65% 5.80% (15)

IMM Building 606.0 659.0 (53.0) 642(1)

Retail: 6.50% Office: 6.75%

Warehse: 7.75%

Retail: 6.60% Office: 6.85%

Warehse: 7.85%

(10) (10) (10)

Plaza Singapura 1,080.0 1,047.0 33.0 2,168 5.25% 5.40% (15)

Bugis Junction 864.0 854.0 10.0 2,057 5.50% 5.65% (15)

Lot One Shoppers‟ Mall 454.0 445.0 9.0 2,070 5.50% 5.65% (15)

Bukit Panjang Plaza 259.0 255.0 4.0 1,697 5.60% 5.75% (15)

Clarke Quay 293.0 285.0 8.0 994 5.65% 5.80% (15)

Others(2) 793.0 757.8(3) 35.2 1,078 (4) 5.85 – 6.00% 5.70 – 5.85% N.A.

Total CMT Portfolio excluding Raffles City Singapore, The Atrium@Orchard and Jurong Gateway Site(5)

6,093.0 6,014.8 78.2 1,565(4) - - -

Raffles City Singapore (40.0%) 1,133.2 1,093.6 39.6 N.M.(6)

Retail: 5.40% Office: 4.50% Hotel: 5.75%

Retail: 5.50% Office: 4.50% Hotel: 5.75%

(10) - -

The Atrium@Orchard 623.0 595.0 28.0 1,643(1) Retail: 5.50% Office: 4.15%

Retail: 5.65% Office: 4.25%

(15) (10)

Total CMT Portfolio(5) 7,849.2 7,703.4 145.8 1,565(7) - - -

Less additions during the period (109.9)

Net increase in valuations 35.9

Jurong Gateway Site (30.0%) (8) 290.7 - N.M. N.M. N.M. - N.M.

CMT Portfolio as at 31 Dec 2011

18 N.M. – Not Meaningful

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

As at 31 December 2011

S$‟000

Healthy Balance Sheet

Non-current Assets 8,384,559

Current Assets 787,617

Total Assets 9,172,176

Current Liabilities 1,038,842

Non-current Liabilities 2,887,312

Total Liabilities 3,926,154

Net Assets 5,246,022

Unitholders‟ Funds 5,246,022

Units in Issue („000 units) 3,328,417

Net Asset Value/Unit (as at 31 December 2011)

S$1.58

Adjusted Net Asset Value/Unit (excluding distributable income)

S$1.56

19

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Distribution Details

(1) Estimated DPU is computed on the basis that as at the books closure date, none of the outstanding

Convertible Bonds has been converted into Units. Accordingly, the actual quantum of DPU may differ from

the table above if any of the Convertible Bonds is converted into Units before the books closure date.

Notice of Books Closure Date 18 January 2012

Last Day of Trading on “cum” Basis 25 January 2012, 5.00 pm

Ex-Date 26 January 2012, 9.00 am

Books Closure Date 30 January 2012

Distribution Payment Date 29 February 2012

Sub-point

Distribution Period 10 November to 31 December 2011

Estimated Distribution Per Unit(1) 1.28 cents

20

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 21 Portfolio Updates

Raffles City Singapore

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

200,000

210,000

220,000

230,000

240,000

250,000

FY 2011 FY 2010

Source: CMTML, CapitaMalls Asia Limited (“CMA”)

Shopper Traffic FY 2011

Shopper

Tra

ffic

(„0

00)

FY 2011 Shopper Traffic(1) Increased by 1.1% Y-o-Y

22

(1) For comparable basis, the chart includes the entire CMT portfolio of malls, except JCube which has ceased

operations for asset enhancement works and the following for which traffic data was not available: Iluma,

Hougang Plaza and The Atrium@Orchard.

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Source: CMTML, CMA

(1) For comparable basis, the chart includes the entire CMT portfolio of malls, except JCube which

has ceased operations for asset enhancement works and the following for which data was not available: Iluma,

Hougang Plaza and The Atrium@Orchard.

Portfolio Tenant Sales for FY 2011

FY 2011 Tenant Sales(1) Increased by 6.3% Y-o-Y

23

40

45

50

55

60

65

70

75

80

85

90

FY 2011 FY 2010

Tenant S

ale

s (

$ p

sf/

mth

)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

23.4%

18.1%

12.7%

8.5% 7.0% 7.0% 6.8% 6.7% 6.4%

4.8% 4.5% 4.1% 3.9% 3.2% 1.7% 1.2%

-0.9% -1.3% -5%

5%

15%

25%

35%

Tele

com

munic

ation

Info

rmation T

echnolo

gy

Shoes &

Bags

Music

& V

ideo

Superm

ark

et

Depart

ment S

tore

Hom

e F

urn

ishin

g

Jew

ellery

& W

atc

hes

Sport

ing G

oods

Fashio

n

Leis

ure

& E

nte

rtain

ment

Ele

ctr

ical &

Ele

ctr

onic

s

Food &

Bevera

ges

Books &

Sta

tionery

Gifts

& S

ouvenir

s

Beauty

& H

ealth R

ela

ted

Toys &

Hobbie

s

Serv

ices

Source: CMTML, CMA

(1) Services include convenience stores, bridal shops, optical, film processing, florist, magazine / mamak stores, pet shops /

grooming, travel agencies, cobbler / locksmith, laundromat and clinics.

FY 2011 Tenant Sales by Trade Categories

(1)

Stronger Sales Performance for Most Trade Categories

24

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Source: Companies reports, CMTML

(1) As at 30 September 2011.

(2) Occupancy cost is defined as a ratio of gross rental (inclusive of service charge and advertising & promotional charge) to

tenant sales.

(3) Based on tenant sales figures submitted by tenants in Tampines Mall, Junction 8, Bugis Junction, Plaza Singapura, IMM

Building, Funan DigitaLife Mall, Raffles City Singapore, Lot One Shoppers‟ Mall, Bukit Panjang Plaza, Rivervale Mall,

Sembawang Shopping Centre and Clarke Quay.

Healthy Occupancy Cost

Average Occupancy Cost

18.6%

17.3%

15.5%

16.4% 16.0%

Westfield (Australia & NZ)

CFS Retail Property Trust

(Australia)

Westfield (US)

CMT (2010) CMT (2011) (1)

(1)

(1)

(2),(3) (2),(3)

25

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(1) Includes only retail leases, excluding The Atrium@Orchard and JCube which has ceased operations for asset

enhancement works.

(2) Based on compounded annual growth rate.

(3) Based on IMM Building‟s retail leases.

(4) Based on Raffles City Singapore‟s retail leases.

(5) Includes Iluma, Sembawang Shopping Centre, Hougang Plaza and Rivervale Mall.

Positive Rental Reversions From 1 January to 31 December 2011 (Excluding Newly Created and Reconfigured Units)

Property

No. of

Renewals /

New

Leases(1)

Retention

Rate

Net Lettable Area Increase in

Current Rental

Rates vs

Preceding

Rental Rates

(typically

committed 3

years ago)

Average

Growth

Rate Per

Year(2)

Area

(sq ft)

Percentage

of Mall

Tampines Mall 41 78.0% 61,322 18.6% 7.8% 2.5%

Junction 8 42 85.7% 65,882 26.0% 7.2% 2.4%

Funan DigitaLife Mall 50 72.0% 53,671 18.0% 6.4% 2.1%

IMM Building(3) 19 78.9% 13,540 3.3% 4.8% 1.6%

Plaza Singapura 66 80.3% 112,308 22.5% 8.0% 2.6%

Bugis Junction 56 73.2% 31,686 7.6% 6.2% 2.0%

Raffles City Singapore(4) 36 80.0% 59,772 14.2% 5.1% 1.7%

Lot One Shoppers‟ Mall 89 82.9% 104,947 47.8% 8.3% 2.7%

Bukit Panjang Plaza 30 86.7% 47,575 31.2% 7.8% 2.5%

Clarke Quay 16 81.3% 42,840 16.9% 9.8% 3.2%

Other assets(5) 58 72.4% 92,600 19.2% -5.3% -1.8%

CMT Portfolio 503 78.8% 686,143 18.4% 6.4% 2.1%

26

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(1) For the financial years ended 31 December 2003, 2004, 2005, 2006, 2007, 2008, 2009, 2010 and 2011, respectively.

For IMM Building and Raffles City Singapore, only retail units were included into the analysis.

(2) Based on the respective yearly financial results presentation slides available at the investor relations section of CMT‟s

website at www.capitamall.com/ir.html

(3) Based on compounded annual growth rate.

(4) Not applicable as there is no forecast for 2011.

Positive Renewals Achieved Year-on-Year

CMT Portfolio

(Year)(1)

No. of

Renewals /

New

Leases

Net Lettable Area

Increase in Current Rental Rates

vs

(typically committed 3 years ago) Average

Growth

Rate Per

Year(3) Area

(sq ft)

% of Total

NLA

Forecast Rental

Rates (2)

Preceding Rental

Rates

(typically

committed

3 years ago)

2011 503 686,143 18.4% N.A.(4) 6.4% 2.1%

2010 571 898,713 25.4% 2.2% 6.5% 2.1%

2009 614 971,191 29.8% N.A. 2.3% 0.8%

2008 421 612,379 19.0% 3.6% 9.6% 3.1%

2007 385 806,163 25.6% 5.8% 13.5% 4.3%

2006 312 511,045 16.0% 4.7% 8.3% 2.7%

2005 189 401,263 23.2% 6.8% 12.6% 4.0%

2004 248 244,408 14.2% 4.0% 7.3% 2.4%

2003 325 350,743 15.6% 6.2% 10.6% 3.4%

27

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

No. of

Leases

Net Lettable Area Gross Rental Income

sq ft ('000) % of Mall NLA(1) S$'000 % of Mall Income(2)

Tampines Mall 47 41.8 12.7% 931 18.9%

Junction 8 56 47.1 18.6% 850 22.4%

Funan DigitaLife Mall 59 93.4 31.2% 679 28.7%

IMM Building(3) 230 222.0 24.1% 2,227 37.2%

Plaza Singapura 73 173.0 34.7% 2,124 32.9%

Bugis Junction 54 84.2 20.1% 1,256 22.6%

The Atrium@Orchard(3) 1 2.6 1.3% 54 3.6%

Raffles City Singapore(3) 53 76.1 16.7% 979 23.2%

Lot One Shoppers‟ Mall 27 58.3 26.8% 630 21.9%

Bukit Panjang Plaza 12 15.8 10.4% 245 13.7%

Clarke Quay 17 100.2 34.0% 623 27.3%

Other assets(4) 87 184.1 47.2% 1,179 44.4%

Portfolio 716 1,098.6 24.8% 11,777 26.5%

2012 Portfolio Lease Expiry Profile by Property

(1) As a percentage of total net lettable area for each respective mall as at 31 December 2011.

(2) As a percentage of total gross rental income for each respective mall for the month of December 2011.

(3) Includes office leases (for Raffles City Singapore, The Atrium@Orchard and IMM Building) and warehouse leases (for IMM Building only).

(4) Includes Iluma, Hougang Plaza, Sembawang Shopping Centre and Rivervale Mall; Excludes JCube which has ceased operations for asset enhancement works.

As at 31 December 2011

28

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(1) Based on IMM Building‟s retail leases.

(2) Includes Iluma, Hougang Plaza, Sembawang Shopping Centre and Rivervale Mall. Years 2007 and 2008 exclude Sembawang

Shopping Centre which commenced major asset enhancement works in March 2007. Years 2008 to 2011 exclude JCube which

has ceased operations for asset enhancement works.

(3) Lower occupancy rate was due to 53.3% occupancy rate at Iluma, which is undergoing asset enhancement works.

(4) Based on Raffles City Singapore‟s retail leases.

(5) Lower occupancy rate was due to asset enhancement works at Lot One Shoppers‟ Mall.

(6) Low occupancy rate was due to asset enhancement works at The Atrium@Orchard.

High Occupancy Maintained

(3.6)

As at As at As at As at As at As at As at As at As at As at

31-Dec

2002

31-Dec

2003

31-Dec

2004

31-Dec

2005

31-Dec

2006

31-Dec

2007

31-Dec

2008

31-Dec

2009

31-Dec

2010

31-Dec

2011

Tampines Mall 100.0% 99.3% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Junction 8 100.0% 100.0% 99.8% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Funan DigitaLife Mall 99.3% 99.3% 100.0% 99.4% 99.6% 99.7% 99.8% 99.3% 100.0% 100.0%

IMM Building(1) 98.5% 99.4% 99.0% 99.0% 99.9% 100.0% 99.7% 100.0% 100.0%

Plaza Singapura 100.0% 100.0% 100.0% 100.0% 99.8% 100.0% 100.0% 100.0%

Bugis Junction 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Other assets(2) 99.8% 100.0% 100.0% 100.0% 99.8% 99.8% 80.9%(3)

Raffles City Singapore(4) 99.3% 100.0% 100.0% 100.0% 99.6% 100.0%

Lot One Shoppers' Mall 92.7%(5) 99.3% 99.9% 99.6% 99.7%

Bukit Panjang Plaza 99.9% 100.0% 99.8% 100.0% 100.0%

The Atrium@Orchard 98.0% 99.1% 93.5% 65.5%(6)

Clarke Quay 100.0% 100.0%

CMT Portfolio 99.8% 99.1% 99.8% 99.7% 99.5% 99.6% 99.7% 99.8% 99.3% 94.8%

29

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 30 Asset Enhancements (AEIs)

Clarke Quay

Clarke Quay

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Proposed AEI Plans for Clarke Quay

Block D

Block A

Block B

Block C

Block E

Recovering space from

anchor tenant to optimise

the use of Block C

Optimising Rental Upside from Lease Renewals at Block C

32

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

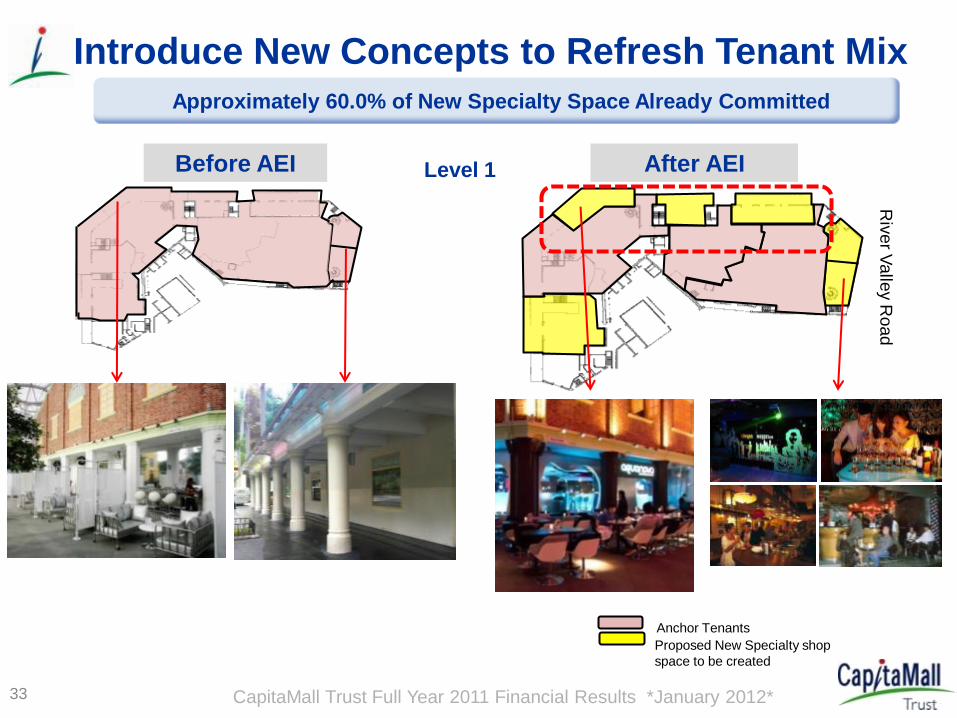

Introduce New Concepts to Refresh Tenant Mix

Level 1

Anchor Tenants

Proposed New Specialty shop

space to be created

Riv

er V

alle

y R

oad

Approximately 60.0% of New Specialty Space Already Committed

33

After AEI Before AEI

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

More Diverse Tenant Mix

Level 2

Anchor Tenants

Proposed New Specialty

shops space to be created

Riv

er V

alle

y R

oad

34

After AEI Before AEI

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Impact on Value Creation

Impact On Rental Of Affected Units at Block C

Before AEI After AEI(1) Variance

Net Lettable Area (sq ft) 77,320 75,483 (2.4%)

Average Rent per sq ft

per month (S$) 3.80 6.87 80.8%

Gross Rent per month

(S$) 293,815 518,568 76.6%

More than 80.0% Increase in Average Rent

35

(1) Based on Manager‟s estimates.

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Financials and Indicative Timeline

AEI Budget(1) (S$ mil)

Incremental Gross Revenue 2.70

Incremental Net Property Income 2.02

Capital Expenditure Required 15.56

Return on Investment 13.0%

Capital Value of AEI

(based on 5.8% capitalisation rate) 34.83

Increase in Value (net of investment costs) 19.27

Capital Expenditure Commencement Date Completion Date

S$15.56 million 2nd Quarter 2012 3rd Quarter 2012

(1) Based on Manager‟s estimates.

Return on Investment of 13.0%

36

JCube

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

JCube – Update on AEI

38

On Track for Opening in 1Q 2012 with More Than 90.0% of Space Committed

View of facade

Ice skating rink

Basement carpark

The Atrium@Orchard

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

The Atrium@Orchard – Update on AEI On Track To Complete in 4Q 2012

Facade works along Orchard Road

Works on link between

Plaza Singapura and Atrium@Orchard

40

Perspective of new facade(1)

(1) Artist‟s impression; subject to authority‟s approval.

Iluma

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Iluma – Update on AEI On Track To Complete in 2Q 2012

42

Works on levels 1 to 3

Works on level 2 link bridge

Perspective of new facade(1)

(1) Artist‟s impression; subject to authority‟s approval.

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 43 Greenfield Development

Westgate

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Westgate & Westgate Tower

44

Key Event Date

Award of tender for the site May 2011

Obtained Provisional Permission Dec 2011

Award of main construction contract Dec 2011

Groundbreaking and commencement of construction Jan 2012

Perspective of office building(1)

Perspective of mall(1)

Target to Complete Mall in 4Q 2013 Target to Complete Mall in 4Q 2013

(1) Artist‟s impression; subject to authority‟s approval.

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Westgate - Shopping Mall

45

(1) Artist‟s impression; subject to authority‟s approval.

Combination of air-conditioned and

open air shopping experience(1)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Westgate – Office

46

(1) Artist‟s impression; subject to authority‟s approval.

Second storey lobby

of office tower(1)

Well-designed quality office space

surrounded by greenery;

equipped with childcare, gym

and pool facilities(1)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Westgate – Groundbreaking on 12 Jan 2012

47

Groundbreaking 7 Months After Award of Tender

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 48 Looking Forward

Bugis Junction

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Looking Forward

Strong Foundations to Ride Out Potential Economic Uncertainties

• Uncertain economic outlook may affect retail consumption – Singapore government expects slower 2012 GDP growth of 1.0%-3.0%

– Consumer sentiment may soften

• Active leasing management – Leases up for renewal in 2012 were signed in 2009 during global financial crisis

– Scale, a strong retailer network and knowledge of tenant sales are strengths in

uncertain times

– Defensiveness of portfolio underpinned by predominantly necessity shopping malls

• Focus on smooth execution of AEIs and Westgate project – Rental upside from ongoing AEIs will be realised progressively over 2 years

– Construction of Westgate commenced; target completion 4Q 2013

49

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Thank You

For enquiries, please contact:

Jeanette Pang (Ms)

Investor Relations

Tel : (65)-6826 5307

Fax : (65)-6536 3884

Email: [email protected]

http://www.capitamall.com

Acknowledgements:

CapitaLand-National Geographic Channel „Building People‟ Photographic Contest

Pages 4, 6, 21 and 30 of presentation: Iluma by Thomas Phoon (Singapore), Bugis Junction by Alvin Bui (Singapore),

Raffles City Singapore by Chow Kian Yew (Singapore) and Clarke Quay by Jimmy Chan (Singapore) respectively

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Annexes

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(1) Includes CMT’s 40.0% stake in Raffles City Singapore (office and retail components) and Iluma. Excludes JCube

which has ceased operations for asset enhancement works.

Portfolio Lease Expiry Profile

as at 31 December 2011(1)

2012

2013

2014

2015 and beyond

Total

Number of Leases

716

970

643

160

2,489

Gross Rental Income

for the month of December 2011

S$’000 % of Total

11,778 26.5

14,630 32.9

11,624 26.2

6,373 14.4

44,405 100.0

2

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

23.4%

14.0%

9.2%

8.6%

6.9%

5.8%

5.2%

4.6%

3.6%

3.4%

3.3%

3.2%

3.1%2.8%2.9%

Food & Beverages

Fashion

Office

Beauty & Health

Services

Department Store

Supermarket

Gifts / Toys & Hobbies / Books / Sporting Goods

Leisure & Entertainment / Music & Video

Jewellery & Watches

Electrical & Electronics

Houseware & Furnishings

Shoes & Bags

Information Technology

Others

27.3%

13.6%

3.7%

9.0% 6.7%

5.7%

5.0%

4.6%

6.1%

3.1%

2.6%

2.8%

3.0% 2.8%

4.0%

3

Well Diversified Trade Mix Across the Portfolio(1)

By Gross Rent for the month of December 2011(2)

(1) Includes CMT’s 40.0% interest in Raffles City Singapore (only retail and office leases, excluding hotel lease) and excludes JCube.

(2) Based on committed gross rental income for the month of December 2011 and excludes tenant sales rental.

(3) Others include Education, Art Gallery, Luxury and Warehouse.

(3)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

Top 10 Tenants

10 largest tenants(1) by total gross rental contribute 20.7% of total gross rental

No one tenant contributes more than 3.0% of total gross rental

Tenant Trade

Sector

% of Gross Rental Income

RC Hotels Pte Ltd Hotel 3.0%

BHG (Singapore) Pte Ltd Department Store 2.6%

Cold Storage Singapore (1983) Pte Ltd Supermarket/ Beauty & Health /

Services/ Warehouse 2.4%

Robinson & Co (Singapore) Pte Ltd Department Store/ Beauty & Health 2.4%

NTUC Supermarket / Beauty & Health / Food

Court /Services 2.4%

Wing Tai Clothing Pte Ltd Fashion / Food & Beverage 1.8%

Kopitiam Pte Ltd Food & Beverage 1.6%

Food Junction Management Pte Ltd Food & Beverage 1.6%

Temasek Holdings Pte Ltd Office 1.5%

Golden Village Multiplex Pte Ltd Leisure & Entertainment 1.4%

(1) Includes CMT’s 40.0% interest in Raffles City Singapore and excludes JCube. Based on actual gross rental income for

the month of December 2011 and excludes tenant sales rental.

4

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

10.8%

8.3%

5.0%

12.4%

12.9% 11.5%

5.9%

6.2%

3.8%

4.2%

5.2%

13.8%

Tampines Mall

Junction 8

Funan DigitaLife Mall

IMM Building

Plaza Singapura

Bugis Junction

Others

Lot One Shoppers' Mall

Bukit Panjang Plaza

The Atrium@Orchard

Clarke Quay

40.0% interest in Raffles City

5

FY 2011 Total Gross Revenue by Property

Percentage of Portfolio(1) by FY 2011 Total Gross Revenue

(1) Excludes JCube which has ceased operations for asset enhancement works.

(2) Includes Sembawang Shopping Centre, Hougang Plaza, Rivervale Mall and Iluma.

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

6.5%

5.0%

5.9%

18.7%

9.9%

8.3%

9.6%

4.3%

3.0%

7.1%

5.8%

15.9%

Tampines Mall

Junction 8

Funan DigitaLife Mall

IMM Building

Plaza Singapura

Bugis Junction

Others

Lot One Shoppers' Mall

Bukit Panjang Plaza

The Atrium@Orchard

Clarke Quay

40.0% interest in Raffles City

6

Net Lettable Area by Property

Percentage of Portfolio(1) by Net Lettable Area as at 31 December 2011

(1) Excludes JCube which has ceased operations for asset enhancement works.

(2) Includes Sembawang Shopping Centre, Hougang Plaza, Rivervale Mall and Iluma.

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

18.2%

6.4%

9.1%

5.6%

4.1%

8.4% 8.2%

4.2%

10.1%

0.9%

3.1%

3.2%

1.4% 3.5%

13.6%

27.3%

13.6%

3.7% 9.0%

6.7%

5.7%

5.0%

4.6%

6.1%

3.1%

2.6%

2.8% 3.0%

2.8%

4.0%

7

Well Diversified Trade Mix

CMT PORTFOLIO(1)

(1) Includes CMT’s 40.0% interest in Raffles City Singapore (only retail and office leases, excluding hotel lease) and excludes JCube.

(2) Based on committed gross rental income for the month of December 2011 and excludes tenant sales rental.

(3) Others include Education, Art Gallery, Luxury and Warehouse.

(3)

By Gross Rent

For the month of December 2011(2)

By Net Lettable Area

as at 31 December 2011

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

29.4%

11.5%

11.0% 7.8%

5.5%

6.0%

7.0%

5.2%

6.7%

2.0%

0.5%

3.8%

1.6%

2.0%

8

Tampines Mall - Trade Mix

By Gross Rent

For the month of December 2011(1)

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

24.3%

6.2%

6.3%

4.7%

11.7%

10.8%

9.6%

12.1%

2.7%

3.3%

0.5%

2.2%

0.8%

4.8%

By Net Lettable Area

as at 31 December 2011

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

20.3%

6.9%

17.6%

5.0% 3.7%

10.5%

8.1%

6.2%

10.7%

1.0%

6.3%

0.7%

1.2%

0.8% 1.0%

9

Junction 8 - Trade Mix

By Gross Rent

For the month of December 2011(1)

31.1%

15.5%

1.7%

9.6%

6.5%

5.3%

5.4%

5.5%

6.1%

2.9%

4.6%

1.1%

2.4%

1.8% 0.5%

By Net Lettable Area

as at 31 December 2011

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 10

Funan DigitaLife Mall - Trade Mix

By Gross Rent

For the month of December 2011(1)

17.4%

1.1%

7.9%

4.8% 1.0%

5.8%

1.2%

1.9%

12.0%

1.6%

2.1%

39.8%

3.4% 13.8%

1.8%

7.9%

2.5% 1.6%

7.0%

0.8%

0.9% 11.3%

2.0% 1.1%

43.8%

5.5%

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

By Net Lettable Area

as at 31 December 2011

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

8.6%

3.5%

9.2%

2.5%

2.1%

2.4%

8.5%

2.3%

0.6%

0.5%

4.4% 7.2%

0.8%

0.9%

46.5%

21.1%

9.4%

3.9%

7.5%

6.5%

1.6%

7.1%

4.6%

1.0%

3.3%

6.6%

12.9%

1.9%

1.6%

11.0%

11

IMM Building - Trade Mix

By Gross Rent

For the month of December 2011(1)

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

By Net Lettable Area

as at 31 December 2011

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(2)

12

Plaza Singapura - Trade Mix

By Gross Rent

For the month of December 2011(1)

23.5%

13.1%

11.2% 9.3%

2.0%

7.8%

6.0%

6.6%

3.2%

1.3%

5.8%

6.0%

0.9%

3.3%

17.5%

7.4%

9.2%

5.3%

5.9%

16.4%

5.0%

13.5%

1.2%

1.3%

8.4%

3.5%

0.9%

4.5%

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

By Net Lettable Area

as at 31 December 2011

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

20.8%

11.3% 0.3%

5.8%

2.3%

41.4%

3.6%

3.2%

8.3%

1.4%

0.2% 1.1%

0.3%

13

Bugis Junction - Trade Mix

By Gross Rent

For the month of December 2011(1)

31.1%

20.9%

0.1%

8.3%

3.9%

17.5%

2.2%

3.6%

4.4%

4.4%

0.4%

2.2%

1.0%

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

By Net Lettable Area

as at 31 December 2011

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

26.0%

5.8%

8.2%

5.0% 8.9%

29.2%

5.2%

3.0%

0.6%

2.1%

0.8%

3.9%

1.3%

14

Sembawang Shopping Centre - Trade Mix

By Gross Rent

For the month of December 2011(1)

27.8%

9.9%

13.8% 9.5%

4.2%

16.2%

4.3%

2.7%

1.9%

3.7%

1.3%

3.3%

1.4%

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

By Net Lettable Area

as at 31 December 2011

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(2)

15

Hougang Plaza - Trade Mix

By Gross Rent

For the month of December 2011(1)

39.2%

5.5%

1.9%

19.1%

6.9%

10.1%

17.3% 20.3%

4.1%

0.7%

24.6%

4.2%

17.6%

28.5%

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

By Net Lettable Area

as at 31 December 2011

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(2)

23.9%

10.4%

8.5%

5.2% 5.9% 6.4%

6.2%

11.0%

1.0% 6.8%

0.5%

1.9%

0.4%

11.9%

16

Lot One Shoppers’ Mall - Trade Mix

By Gross Rent

For the month of December 2011(1)

30.2%

16.5%

13.4%

8.5%

3.5%

4.3%

5.8%

4.6%

3.3%

3.5%

0.7%

3.1%

0.6%

2.0%

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

By Net Lettable Area

as at 31 December 2011

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

28.3%

3.6%

11.5%

6.0% 6.2%

18.2%

6.3%

1.2%

1.2%

6.0%

1.1% 0.9%

9.5%

37.1%

6.1%

16.1%

10.7%

2.3%

11.0%

4.3%

0.9%

3.2% 2.6%

1.8% 1.4%

2.5%

17

Bukit Panjang Plaza - Trade Mix

By Gross Rent

For the month of December 2011(1)

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

By Net Lettable Area

as at 31 December 2011

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

(2)

19.5%

1.4%

10.1%

16.2%

15.2%

27.4%

1.2%

0.3% 0.3%

1.2%

7.2%

27.3%

2.6%

13.0%

23.0%

6.5%

17.3%

1.5%

0.8% 0.8%

1.6%

5.6%

18

Rivervale Mall - Trade Mix

By Gross Rent

For the month of December 2011(1)

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

By Net Lettable Area

as at 31 December 2011

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 19

Clarke Quay - Trade Mix

By Gross Rent

For the month of December 2011(1)

41.4%

7.3%

2.2%

1.4%

47.7%

22.6%

14.0% 3.0%

3.7%

56.7%

(1) Based on tenancy schedule as at 31 December 2011.

(2) Others include Education, Art Gallery, Luxury and Warehouse.

By Net Lettable Area

as at 31 December 2011

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012*

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2012 2013 2014 2015 and Beyond

24.8

29.7

26.1

19.4

26.5

32.9

26.2

14.4 (%)

% of total Net Lettable Area % of total Gross Rental Income

20

Lease Expiry Profile – Portfolio(1)

(1) Includes CMT’s 40.0% interest in Raffles City Singapore (only retail and office leases, excluding hotel lease) and excludes

JCube which has ceased operations for asset enhancement works.

(2) Based on committed gross rental income for the month of December 2011 and excludes tenant sales rental.

(2)

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 21

Lease Expiry Profile – Tampines Mall

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2012 2013 2014 2015 and Beyond

12.7

44.8

31.2

11.3

18.9

43.6

31.3

6.2

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 22

Lease Expiry Profile – Junction 8

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

2012 2013 2014 2015 and Beyond

18.6

37.3

41.7

2.4

22.4

37.8 36.7

3.1

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 23

Lease Expiry Profile – Funan DigitaLife Mall

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

2012 2013 2014 2015 and Beyond

31.2

45.4

17.2

6.2

28.7

39.5

23.8

8.0

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 24

Lease Expiry Profile – IMM Building

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2012 2013 2014 2015 and Beyond

24.2

36.3

27.9

11.6

37.3 38.6

16.3

7.8

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 25

Lease Expiry Profile – Plaza Singapura

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2012 2013 2014 2015 and Beyond

34.7

20.3

37.6

7.4

32.9

27.8

31.0

8.3

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 26

Lease Expiry Profile – Bugis Junction

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

2012 2013 2014 2015 and Beyond

20.1 21.5

12.0

46.4

22.6

34.0

23.2

20.2

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 27

Lease Expiry Profile – Sembawang Shopping Centre

0.0

20.0

40.0

60.0

2012 2013 2014 2015 and Beyond

55.5

8.7 10.1

25.7

47.6

11.9 12.2

28.3 (%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 28

Lease Expiry Profile – Hougang Plaza

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

2012 2013 2014 2015 and Beyond

59.7

40.3

0.0 0.0

76.9

23.1

0.0 0.0

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 29

Lease Expiry Profile – Lot One Shoppers’ Mall

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

2012 2013 2014 2015 and Beyond

26.8

9.0

40.8

23.4 21.9

15.3

49.2

13.6

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 30

Lease Expiry Profile – Bukit Panjang Plaza

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2012 2013 2014 2015 and Beyond

10.4

49.6

7.6

32.4

13.7

54.0

13.8

18.5

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 31

Lease Expiry Profile – Rivervale Mall

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2012 2013 2014 2015 and Beyond

36.7

18.9

15.0

29.4

33.6

25.9

18.4

22.1

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 32

Lease Expiry Profile – Clarke Quay

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2012 2013 2014 2015 and Beyond

34.0

27.3

29.4

9.3

27.3

30.2 31.0

11.5

(%)

% of total Net Lettable Area % of total Gross Rental Income

CapitaMall Trust Full Year 2011 Financial Results *January 2012* 33

Thank You

For enquiries, please contact:

Jeanette Pang (Ms)

Investor Relations

Tel : (65)-6826 5307

Fax : (65)-6536 3884

Email: [email protected]

http://www.capitamall.com