preparing a strategic business plan -...

TRANSCRIPT

A P P E N D I X�� �

Preparing a strategicbusiness plan

A very practical issue faced by organisations and their strategic analysts is ‘How do we

write a strategic business plan?’ The strategic business plan is the link between strategic

thinking and analysis—the strategy formulation—and the action or implementation that

will be necessary to carry out the strategy. The strategic business plan summarises and

documents the strategic analysis and the implementation plans.

Few strategy texts discuss the strategic business plan, yet it is a major outcome of the

strategic planning process and it is in widespread practical use.1 We believe this is because

strategic analysts and academics are excited by the strategic analytical process and can’t

be bothered with the mechanical documentation of the conclusions they have reached. Yet,

for the business strategy to be implemented, documentation is important so that the

strategy can be widely communicated, understood and accepted within an organisation.

Documentation of the strategic business plan also provides a control for comparison of

actual performance during the planning period.

Thus, the strategic business plan is the vital formal documenting of the analysis and the

proposed plan of implementation. In this sense, the strategic business plan contains no new

concepts or techniques. But, properly implemented, it is very important to an organisation,

because of its communication role and because it provides the practical control mechanism

for evaluating whether or not the strategy is being implemented. In this appendix, we

consider the advantages of having a formal strategic business plan, the contents of the

plan, the process for preparing the plan, and issues that make for successful and unsuc-

cessful strategic business plans.

Advantages of having a formal strategic business plan

A formal, written strategic business plan is an important strategic tool, which all organisa-

tions should have for the following reasons:

�A clear and unambiguous direction is laid out for the organisation. Without a formal

plan, there will inevitably be subsequent disagreement about what the organisation is

trying to do and what was actually agreed in the strategic planning process. Writing it

down makes it objectively clear exactly what the organisation is trying to achieve.

�Key assumptions for the organisation are explicitly recognised. Having a formal plan

makes it clear what assumptions have been used in preparing the plan. For instance,

assumptions about economic growth rates, sales growth rates, margins and inflation

rates can clearly be seen, either from the words in the plan or from analysis of the

numbers in the plan.

�Everyone in the organisation is able to act in a manner consistent with the goals

specified. While the strategic thinking and analysis processes may have been confined

to a small number of people in the organisation, making the plan explicit and

communicating it widely enables everyone in the organisation to see how all the

planned actions, activities and units fit together to implement the plan.

�All actions can be assessed against the stated business and functional strategies. The

plan provides a control against which actual performance can be measured. This is a

fundamental issue for assessing performance in any area of activity. Failure to have

a formal plan means this basic control tool does not exist.

Strategic planning is not the same as strategic thinking. Mintzberg argued that

‘strategic planning’ is really ‘strategic programming’—that is, the articulation and

elaboration of strategies or visions that already exist. Strategic planners supply some of the

strategic businessplan

Summarises anddocuments the

strategic analysisand the

implementationplans.

A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N �446

information, the formal analyses act as catalysts to encourage strategic thinking and

program the strategy, but the strategic plan is not strategic thinking.2

The use of strategic plans is widespread. Several studies suggest around half of organ-

isations undertake a strategic plan, with others undertaking one-year plans that might be

consistent with a longer-term strategic plan.3

Contents of the strategic business plan

The first strategic business plan���

Morkel noted that there is a first strategic business plan for every organisation.4 This is

often the hardest plan to construct, because there is no precedent to follow. He suggested

that a ‘quick and dirty’ approach be taken in the first plan and that refinements should be

added gradually, rather than trying to produce the perfect plan on the first attempt. While

we agree that the first plan will not be perfect, it does act as an important guide for future

plans. Therefore, deficiencies in the first plan, particularly in its structure, may become

institutionalised and difficult to remove. Consequently, we believe that it is worth taking

some time over this first plan, rather than simply rushing to create a plan for the sake of it.

Plan contents���

A strategic business plan should contain discussion of all the analytical elements discussed

in this book, together with details of the proposed actions to be taken to implement the

analysis. It should also include a quantitative plan, which shows the actions and results

expected.

The elements of a typical strategic business plan are shown in Figure 1. In practice,

each organisation has quite different ways of presenting the information, and a variety of

different terminology is used. Also, the exact order of items varies from plan to plan, due

to individual preferences and organisational histories. Plans should be done separately for

each identifiable separate organisational unit, being summarised at the organisation level.

The strategic business plan should cover more than just the current year. Most strategic

business plans now cover a three-year period, with one year of fine detail and two years of

major line item detail. (The current year should be the budget for the year, so that the

strategic business plan and the budget are aligned.) The actual period covered will depend

on the sophistication of the planning process within the organisation, the degree of change

occurring within the industry, the importance of capital investment, the time scale of

capital investment, and the willingness of the top management team to project beyond the

current period.

The plan often begins with a summary of the organisation’s current position. This

should include:

�a brief description of the organisation

� the current statement of business strategy

�a summary of the balanced scorecard performance in the current year, together with

comparisons to current year targets and recent prior years (at least the last two prior

years, so that there is at least three years of history to consider)

�a discussion of the overall performance of the organisation against the current strategy

and performance goals that exist

�a discussion of the reasons why the overall and functional performance has or has not

met the goals specified.5

� A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N 447

This section sets out the background situation for the strategies and plans that are being

proposed. It enables the reader to understand who the organisation is, what it is trying to

achieve, the extent to which the strategies have been or are being achieved, and why

this has occurred. Chapter 5 provides information on how to measure organisational

performance for this assessment.

The plan should contain a summary of the external environment. This section covers

the analysis that an organisation would undertake, based on concepts in Chapter 3. It

should include:

�coverage of key macro-environment factors that will affect the organisation over the

period of the strategic business plan

�an industry analysis covering the current position and future trends in buyer and

supplier relationships, the potential for new entrants and the power of substitutes

�an analysis of major competitors, including expected trends

�an identification of key stakeholders and their expectations

A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N �448

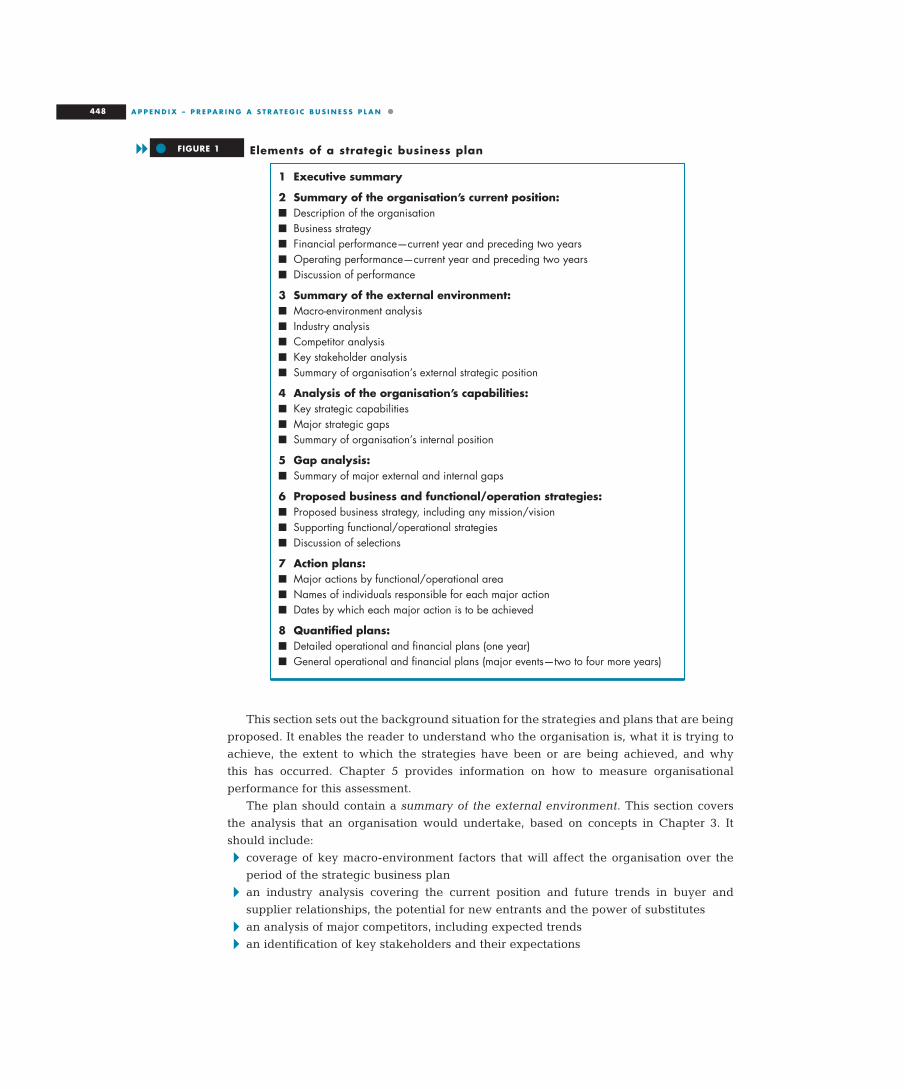

1 Executive summary

2 Summary of the organisation’s current position:n Description of the organisationn Business strategyn Financial performance—current year and preceding two yearsn Operating performance—current year and preceding two yearsn Discussion of performance

3 Summary of the external environment:n Macro-environment analysisn Industry analysisn Competitor analysisn Key stakeholder analysisn Summary of organisation’s external strategic position

4 Analysis of the organisation’s capabilities:n Key strategic capabilitiesn Major strategic gapsn Summary of organisation’s internal position

5 Gap analysis:n Summary of major external and internal gaps

6 Proposed business and functional/operation strategies:n Proposed business strategy, including any mission/visionn Supporting functional/operational strategiesn Discussion of selections

7 Action plans:n Major actions by functional/operational arean Names of individuals responsible for each major actionn Dates by which each major action is to be achieved

8 Quantified plans:n Detailed operational and financial plans (one year)n General operational and financial plans (major events—two to four more years)

Elements of a strategic business planFIGURE 1��

�a summary of the strategic position of the organisation relative to the current and

expected future demands of the environment.

The plan should also include an analysis of the organisation’s capabilities. This section

covers the analysis that the organisation should undertake based on concepts discussed in

Chapter 4. It should include:

�an identification of strategic capabilities

�an identification of major strategic gaps6

�a summary of the strategic position of the organisation relative to the demands of, and

trends in, the industry and the expectations of the current strategy.

A gap analysis should draw together the external and internal analyses of the organi-

sation. Chapter 6 covers gap analysis. It should cover both the external opportunities and

threats and the internal capabilities and gaps, bringing together the internal and external

position of the organisation, in order to explain rationally the subsequent choice of business

and operational strategies for the future.

This should then lead to the proposed strategies for the organisation. This section

should include:

�a reaffirmation of the existing business strategy, including any related mission or vision

statement(s), or any change that is being made and the reasons for the change

� the supporting functional/operational strategies needed to achieve the business

strategy

� reasoning for the selection of both the business and functional/operational strategies,

whether or not they involve change.

For the plan to be implemented, the changes proposed at the business and functional

strategy level must be turned into action plans by functions, by projects and by individuals.

The action plans will be the largest part of the strategic business plan, in terms of volume,

as the detail required to implement the business strategy extends to all parts of the organ-

isation. For each function or operation, this section should include:

� the specific functional/operational strategies to be pursued, preferably with some

explanation of how they will assist the business strategy to be implemented

�how, by whom and when each functional/operational strategy is going to be achieved.

Where there is no change (e.g. the marketing strategy remains unaltered), the strategy

should still be specified, with the notation that no particular change action is required,

so that a complete set of strategies is specified in the total plan.

Each action plan should be assigned to an individual and given a date by which the

action plan is to be achieved. This is a very important decision. Assignment to an

individual, rather than a group, enforces personal responsibility, a factor that was found to

be very important in winning organisational behaviour.7 It is easy for groups to agree what

should be done, but to disagree on just who is responsible for actually doing it. If this step

is not followed, the plan runs a very real risk of not being implemented because no one was

assigned the responsibility to carry out the important change tasks.

The date is similarly important. It acts as a control mechanism for follow-up. Without a

date, an individual can say the task is ‘in hand’, ‘in progress’ or ‘under way’, with the

organisation having no real control over just when the task will be completed. Individuals

will always disagree about their recollections of responsibilities and times unless they are

clearly documented. Table 1 gives an example of action plans. Treating the implementa-

tion plans for the business strategy as a project management task, with intermediate dates

at which certain tasks have to be achieved, is a valuable way of reinforcing the importance

action plansThe set of specificactions which, takentogether, areexpected to result inthe achievement ofthe proposedstrategy.

� A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N 449

of and management of the individual actions. Chapters 12–14 consider issues of imple-

mentation that lead to the development of operational-level strategies.

Finally, the plan needs quantified plans to show the expected effects of implementing

the action plans. While these quantified plans will certainly include financial measures and

outcomes, they should also include other quantified measures relevant for particular

functional/operational strategy assessment. For instance, measures of market share,

productivity, numbers of suggestions for improvements, absenteeism, on-time delivery,

percentage of returns, etc. should be included, if they are important measures in the

strategic control system.

The extent of quantification may vary. While quantification of the first year of the plan

should be detailed—it should be the same as the operating plans and budgets for the

year—detailed quantification of subsequent years is of limited value, as our ability to

forecast the future accurately is quite limited. The day of the quantified five-year strategic

business plan is over. Nevertheless, some quantification for a two- to three-year period can

be very useful for modelling purposes. To the extent that strategic actions undertaken in

this year will not have an effect until following years, it is important to show the expected

effects of such actions. For instance, the decision to open a new production facility in two

years, which requires building commencement now, is expected to have an effect on sales

volumes and costs in two years’ time. It should be possible to make reasonable estimates

from the capital expenditure proposals for the project, or from other information used to

make this decision.

Confidentiality of strategic business plans���

Many organisations are afraid that some aspects of their plans are too confidential to be

documented—for instance, the planned closure of a plant, the takeover of a competitor, the

introduction of a new product range. Not to include these aspects, or to include their

planned results but not recognise the causes of the sharp changes in the planned results,

means the plans themselves will be deficient documents. However, the leaking of

information (e.g. to employees that a plant is to be closed) may also have negative conse-

quences for the organisation.

Our belief is that much so-called confidential information tends to leak out anyway. The

strategic business plan merely documents decisions that have already been agreed in

principle. If the strategic business plan is a confidential document, including this type of

information in it should not greatly increase the chances of leakage. Further, inclusion of

the information may enable these issues to be considered more rationally than when the

A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N �450

An example of some action plansTABLE 1��

Who is When to beProblem Action responsible completed

We don’t really Undertake market Marketing manager July 200Xunderstand what research with keycustomers think customers

Too many quality Get team to analyse past Operations manager Stage 1 January 200Xdefects defects by cause; focus on Stage 2 December 200Y

solving key causes

information is given only to an exclusive few. For instance, the knowledge that a plant is

expected to be closed within 12 months often acts as a spur to employees to consider how

to improve performance so that the decision can be reversed. Positive outcomes are

possible here, whereas if the closure decision is announced unilaterally and with a short

time scale, negative results (e.g. low productivity, low morale, sabotage) are quite likely.

Organisations that are obsessed with secrecy are likely to create uncertainty, suspicion

and a lack of trust among their employees, due to the shortage of information. Without

information, employees will assume the worst. The more accurate and widely distributed

and discussed the plan is, the more likelihood there is that it will be accepted and

understood. This is a critical issue for implementation, as we have demonstrated in

Chapter 14. For this reason, we do not believe that the details of the strategic business plan

should be kept confidential from employees in normal circumstances.

The strategic business planning process

In a conventional top-down approach, the top management team meets for a two- or three-

day period once a year to consider all the analytical elements and to produce the essence

of the business strategy and the broad-scale operational strategies for the planning period

(see Strategy @ work 1). The operational expression of that (i.e. the strategic business plan,

including the specific required operational plans) is prepared subsequently. The whole

detailed process is then brought together, reviewed and approved at a series of meetings

(strategic planning committee, top management team, board of directors, corporation),

before the outcome is finally communicated to the organisation.

Another approach—often used by public sector organisations—is to gather information

from outside the organisation and from various stakeholder groups within the organisation

and to bring this material together gradually from the bottom to the top of the organisation.

� A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N 451

Most organisations have a two- to three-daystrategic planning workshop to set the strategicdirections for the year. Many of these areregarded as unsuccessful by participants. Howcan they be made most valuable?�Set the agenda clearly, allocate times and

objectives to each section, and stick to it.�Only invite those who can really make a

difference (generally ten or fewer people).�Minimise pre-reading to essentials, but make

sure it is read beforehand.�Allow everyone to have their say, but recog-

nise that some opinions are more valuablethan others.

�Pay attention to the quality of the conversation.�Ensure that discussions are brought to a close

and momentum is maintained.

�Consider using a facilitator so that the CEOcan take part in the conversation withoutdominating it.

�Develop a manageable number of clearactions.

�Ensure the executive team is unified andaligned at the end of the workshop.

�Ensure action plans are formulated, responsi-bilities allocated and the results of theworkshop communicated.

�Have subsequent half- or one-day follow-upsessions to reinforce and work on theoutcomes.

Source: Based on Frisch, B. & Chandler, L. 2006, ‘Off-sites thatwork’, Harvard Business Review, June:117–26.

THE STRATEGIC PLANNING WORKSHOP: MAKING IT WORKSTRATEGY @ WORK 1

�

�

This process involves many more people, and captures many more ideas, than the top-down

process. It has the big advantages that many perspectives are considered and that

individuals who are involved in the process are more likely to be committed to any

subsequent strategic business plan that emerges. However, it takes longer and is subject to

problems and conflicts over different perspectives, different assumptions, and the natural

desire of individual groups to want to enhance their own position during the process.

A hybrid approach is to gather information from many areas inside and outside the

organisation, and to summarise and discuss it at the top, with the top management team

deciding on the strategy through incorporating that widespread information. This is

perhaps the best approach, as it ensures that many viewpoints are available, while limiting

the decision-making process to a feasible number of people to get a clear strategy. It does

depend, of course, on the ability of the top team to understand the information and for them

to effectively incorporate it and sell the decisions made to the various stakeholder groups

subsequently.

The use of mid-period or ongoing reviews provides the opportunity to ensure that the

feedback during the period is incorporated and any necessary adjustments are made,

which is particularly important if errors of judgment have been made by the top group or

as aspects of implementation proceed differently, and more slowly, than expected. It also

demonstrates that strategy is a process, not a once-a-year meeting unrelated to the actual

business operations.

The process itself���

Responsibility for the planning process and its conduct rests with the CEO. The CEO and

the top management team determine the process and timing. In some cases, a facilitator is

brought in to assist. This enables the CEO and the top management team or other groups

to share their views equally, without an insider with a vested interest (such as the CEO)

taking a controlling position in the process and vetoing ideas that are not acceptable to

their personal interests or values. In some cases, an ad hoc or permanent planning group

is given the task of conducting the process. Where the planning group is closely related to

the accounting unit, as it often is in order to link the process to the budgeting process, the

process tends to be heavily financially oriented, rather than strategically oriented.

However the process is conducted, it is clear that operational managers have responsi-

bility for carrying out the actions agreed in the plan. Failure of those operational managers

to carry out the activities in the plan will mean that the plan will not be achieved, so it is

essential that the process contains ways to gain the commitment of operational managers

and all employees. Chapter 14 covers the processes available for achieving this.

Writing the plan���

Two alternatives are usually considered to decide who should be responsible for actually

writing the plan that has been agreed. The first approach is to give the task to a central

specialist individual or group. It then becomes their responsibility to draw the required

detailed information from the various functional/operational groups to match the broad

ideas agreed in the strategic planning workshop and to put the integrated plan together.

This approach is based on the following assumptions:

�The specialist and the functions are equally familiar with the proposals for the plan.

�The functions are under severe time constraints, so that the specialist will get the task

done more quickly.

A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N �452

�The specialist will write and integrate the plan better than if a series of individual

functional personnel do their own parts of the plan.

�The task is only one of documentation, as the decisions have been agreed by those

responsible for their implementation.

A variation on the approach is to employ an outside consultant, either to utilise profes-

sional expertise, or to alleviate management time pressures. While this approach will

almost certainly produce an expertly written and beautifully presented document within a

limited time frame, a lack of commitment to the document by those responsible for its

implementation often results in the plan failing to be implemented.

The second approach is to ask each part of the organisation to write its own part of the

plan. The assumptions of this approach are:

�By being involved in and committed to decisions which affect them, individuals will

take responsibility.

�Specialists cannot understand the intricacies of the function/operation, so they cannot

resolve any planning conflicts that occur between functions, or in technical aspects

within a function.

�Whether or not the plan looks ‘nice’ is not really important. What matters is whether or

not it actually works.

Some organisations use responsibility for writing the plan as an educational experience

for managers by sharing the task around, thereby awakening managers to the necessary

interconnections between major functions. This approach also ensures that there is a fresh

view every year or so on the writing task.

Each approach can work, provided its assumptions are valid. The key issue is to ensure

that the plan is agreed, understood and feasible, and that individuals are committed to its

achievements.

Communicating the strategic business plan to the organisation

The process of preparing the plan, and the actual writing of it, are far less important than

its ultimate acceptance and use within the organisation. Many strategic business plans fail

to be effectively communicated to the organisation, so operations go on regardless of the

plan. Such failure reduces the credibility of the strategic business-planning tool itself. Yet,

there is evidence that those organisations that undertake strategic business planning do

better than those that do not.8

Making the strategic business plan successful���

An organisation can maximise the chance of the strategic business plan being an important

and useful part of the strategic tools of the business by ensuring that the plan has the

following characteristics:

� It is simple but comprehensive. A turgidly written strategic business plan, full of

caveats and different scenarios, will be more confusing than helpful. So, the style of

writing and presentation of the strategic business plan is actually quite important, even

though it is primarily a task of documentation. It must be understood by those who need

to make it work. Having those who have to implement the plan as writers has many

advantages, but a well-written, consistently styled strategic business plan written by an

individual at the centre of the organisation can achieve the same ends. Keeping the

strategic business plan as short as possible, yet comprehensive, is also important, if

� A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N 453

the plan is to be absorbed by operating managers. Consulting firms and several

organisations have developed a ‘Plan-On-A-Page’ concept. This approach provides the

complete essentials of the strategic plan on a single page, which can be widely

distributed and displayed throughout the organisation.

Another approach to simplicity has been the introduction of narrative stories, which

are more engaging than dry business documents. For instance, 3M introduced the

practice of writing its divisional strategic business plans as stories, in order to make

them more understandable to employees (see Strategy @ work 2).

� It is credible and feasible. Many plans fail because operating managers simply do not

believe in them (often through lack of involvement in the process). Some plans fail

because, even though they are feasible, lower-level managers simply do not believe that

top managers will provide the resources or support to enable the plan to be achieved.

� It is widely circulated, widely understood and widely accepted. Not only do many

people in the organisation need to have access to the strategic business plan and to

understand it, but they also need to accept it (see Chapter 2). This is not an easy task

to achieve. It requires good internal communication, openness to questioning and

debate, and time for the plan to be absorbed, particularly if it is radical in its proposals

(see Chapter 14). The plan covers not only the business strategy, but also how to

achieve the business strategy. This must also be accepted if it is to actually happen.

�The budget is linked to the plan. Managers do not want to report on two conflicting

systems. If forced to do so, they will concentrate on achieving the (short-term) budget

rather than the (long-term) strategic business plan. The budget already exists when the

strategic business plan is formulated, so the budget for the new period must be adjusted

to account for any changes in strategy in the plan. Therefore, the budget must be linked

to, and integrated with, the strategic business plan, not the other way around (see

Figure 2).

�The reward system is linked to the plan. Managers and employees will do what is

necessary and achievable to maximise their personal performance under the existing

A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N �454

Diversified conglomerate manufacturer, 3M,grew dissatisfied with the bullet point strategicplans it was producing. Outsiders—and, moreimportantly, insiders who were not part of theplanning process—simply could not tell from theset of bullet points how the units perceived them-selves to be different from their competitors. Thiswas because bullet points leave critical relation-ships unspecified and critical assumptions abouthow the business works unstated. Further, suchstrategic business plans lacked a sense of excite-ment—necessary if employees were to becommitted to them.

To address these issues, 3M began to write itsplans using narratives from storytelling. First, theplan sets the stage. It defines the current situation

in an insightful, coherent manner. Next, the planintroduces dramatic conflict. What challengesdoes the organisation face? What are the criticalissues for success? Finally, the story reaches aresolution, in a satisfying, convincing manner.How will the organisation overcome thechallenges?

Requiring a plan to tell a story forces the planwriter to bring to the surface buried assumptionsabout cause and effect. It creates a richer pictureof the context. Flaws in the logic—like those in astory—are glaringly obvious and readers find itmore interesting and compelling to read.

Source: Based on Shaw, G., Brown, R. & Bromiley, P. 1998,‘Strategic stories: How 3M is rewriting strategic businessplanningÕ, Harvard Business Review, May–June:4.

3M’S STRATEGIC BUSINESS PLAN ‘STORIES ’STRATEGY @ WORK 2

�

�

reward system. For the strategic business plan to be successful, it must be consistent

with the reward system. (Or the reward system must be changed to encourage

behaviour consistent with the plan.)

� It is timely. The strategic business plan must be available before the start of the

planning period so that there is time for the actions that are required to be put into

place. In many government organisations, this simply does not occur, making the

strategic plan of little value.

� It is monitored and reviewed. Often the strategic business plan is prepared, filed and

forgotten, with emphasis returning to the operating budgets (which may or may not be

consistent with the strategic business plan). Unless the strategic business plan is

constantly being used to assess business performance, and unless the operating

budgets are directly linked to the strategic business plan, the plan will simply gather

dust and have little influence on organisation behaviour.

Reasons for plan failure���

There are many reasons why even brilliant strategic business plans fail. Fundamental

reasons include the inability to determine a clear strategy, or to distinguish the purpose of

the organisation from the implementation actions. Also, the planning process often fails to

produce the critical insights required to develop innovative, value-creating ideas.9 Other

reasons include:

�There is a failure to focus on implementation. Too often there is a belief that, once the

strategic plan is prepared, the job is complete. But it is not until the implementation

projects in the plan are actioned that the strategy is implemented.

� It may not be accepted by the functional/operational groups on which its

implementation relies. Fundamental functional/operational information may have been

overlooked, particularly if the plan has been prepared by central specialists, making the

plan unworkable. Alternatively, the functional/operational specialists may deliberately

ignore the plan because they were not involved in its final version and do not agree

with it. Getting functional/operational managers to sign off on the plan, either

physically or by having their names against specific task responsibilities, is one way of

increasing commitment to the plan. Knowledge that there is a follow-up process to

review performance against the plan is another way to increase commitment.

� It is so detailed and long that few people actually understand what the organisation is

trying to achieve. It is extremely difficult for most organisations to predict detailed plans

� A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N 455

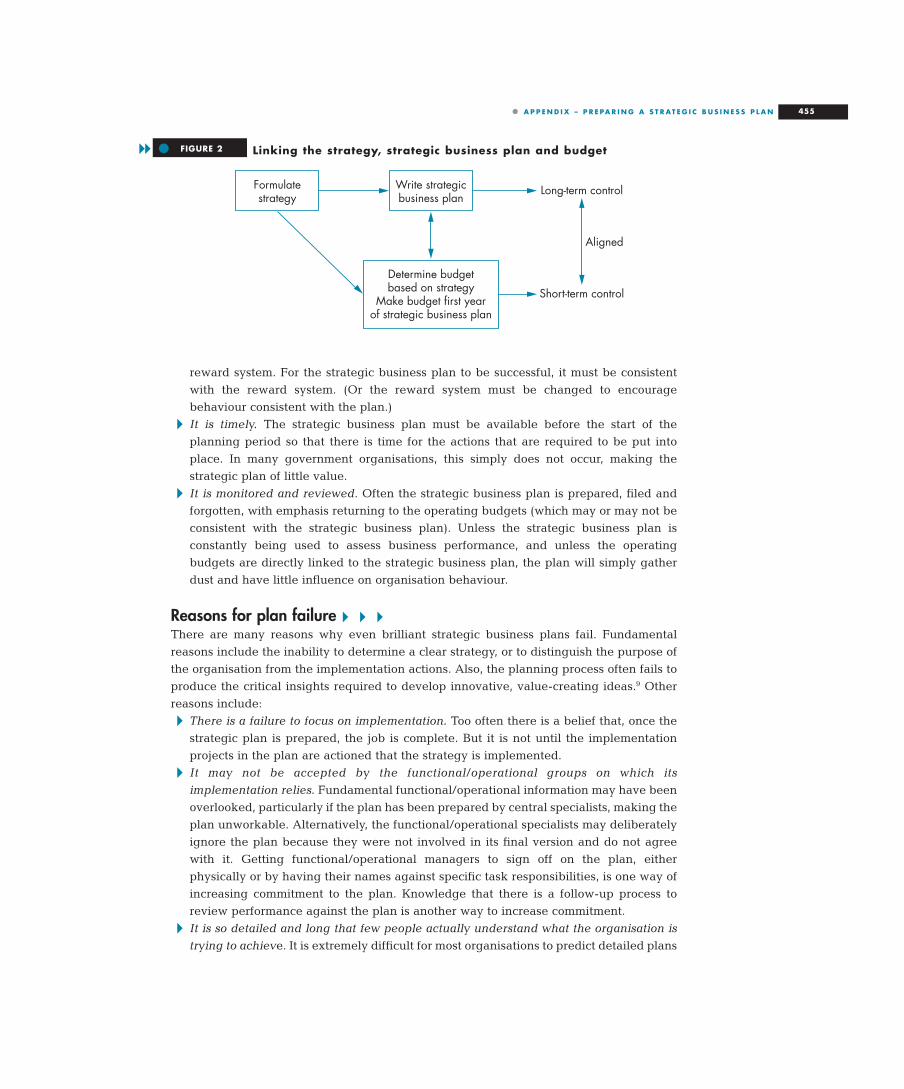

Formulatestrategy

Write strategicbusiness plan

Determine budgetbased on strategy

Make budget first yearof strategic business plan

Long-term control

Aligned

Short-term control

Linking the strategy, strategic business plan and budgetFIGURE 2��

more than a year in advance. It is quite likely that much of the detail is actually wrong.

Further, there is a large time cost involved in preparing such detailed plans. Large plans

are also often communicated to few people. All these aspects multiply the chance of

failure for such a plan.

� Its circulation is limited. Many managers simply never see the strategic business plan

and so they make their own decisions in ignorance of what the organisation’s overall

plan actually is.

� It is out of date. The plan may have had a long gestation period so that, by the time the

plan is finalised, the circumstances have changed, invalidating key aspects.

Alternatively, the plan is not completed by the start of a particular financial year, so that

the operating budget and the strategic business plan—which ought to be compatible—

are not. Managers will then choose the short-term, more detailed operating budget as

their performance target rather than the less detailed, less evaluation-oriented strategic

business plan, for they will certainly be judged by performance against budget.

Mintzberg argued that the process of strategic planning has three fundamental fallacies

that significantly affect its success rate.10 First, planners overestimate their ability to predict

the future. He argued that ‘visionary’ managers actually create their strategies in intuitive

and creative ways, rather than base them on their ability to predict the future from data.

Second, he argued that plans should involve those who actually have the data, not those to

whom the data is passed, and who are often quite detached from how activities and

operations actually work. The use of only hard data denies the value of qualitative

information. Hard data is also often out of date. Third, he argued that attempts to formalise

the strategy process, through such things as planning workshops and agendas, ignored the

ongoing learning dimension involved in strategy making. He argued that planners should

be documenters of the strategic thinking, not creators of it. This is also our view.

In this appendix, we have considered the strategic business plan—that is, the documentation of thestrategic thinking of the organisation. We have outlined the advantages of having a formal strategicbusiness plan, and considered its contents and the processes for constructing it. Finally, we consideredhow to make the strategic business plan successful and why strategic business plans tend to fail. Thestrategic business plan is an important part of the complete process of strategic thinking, analysis andaction. Its role is underestimated by texts. This appendix shows how the strategic business plan fits intothe strategy process and how it can be used most successfully to help implement strategy.

1 Hubbard, G., Pocknee, G. & Taylor, G. 1996, Practical Australian Strategy, Prentice Hall, is a rare exception.This chapter draws heavily from that chapter.

2 Mintzberg, H. 1994, ‘The fall and rise of strategic planning’, Harvard Business Review, January–February:107–14.3 See Fenton-Jones, M. 2007, ‘Strategic planning delivers outperformance’, The Age, 6 February; Bonn, I. &

Christodoulou, C. 1996, ‘From strategic planning to strategic management’, Long Range Planning,

A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N �456

Summary� �

�

Endnotes� �

�

29(4):543–51; and Goodwin, D. & Hodgett, R. 1991, ‘Strategic planning in medium size companies’,Australian Accountant, March:71–5.

4 Morkel, A. 1990, Strategic Business Planning, Do It Yourself, 3rd ed., Australian Institute of CompanyDirectors.

5 ‘Functional goals’ are goals for those major areas or activities of the organisation that impact on the overallgoals. Such goals may be related to important activities or to processes, as well as to functions. Similarly, theword ‘goals’ used here may be called ‘objectives’, ‘targets’ or ‘measures’ in other organisations.

6 In many cases, capabilities and gaps are termed ‘strengths’ and ‘weaknesses’ in practical strategic businessplans. We discussed in Chapter 4 why we believe capabilities and gaps are more appropriate than thetraditional strength and weakness analysis.

7 Hubbard, G., Samuel, D., Heap, S. & Cocks, G. 2002, The First XI: Winning Organisations in Australia,Wiley.

8 Bonn & Christodoulou 1996, op. cit.9 Campbell, A. & Alexander, M. 1997, ‘What’s wrong with strategy?’, Harvard Business Review,

November–December:42–51.10 Mintzberg 1994, op. cit.

� A P P E N D I X – P R E PA R I N G A S T R AT E G I C B U S I N E S S P L A N 457