practical innovation using cutting-edge technology · practical innovation using cutting-edge...

TRANSCRIPT

Pract ica l innovat ion us ing cutt ing-edge technology

Lipis Advisors

Researched and written by

Practical innovation using cutting-edge technology

Introduction to white paper seriesThe payments industry is undergoing rapid change. Advances in technology have worked to transform end-user expectations related to speed and transparency and have enabled new players to enter the payments space, which was formerly the dominion of banks and large payments processors. In 2015, fintechs received almost $14 billion in funding, more than double the previous year’s total. This funding is not exclusive to venture capital firms either; global banks such as Citigroup have been active in investing in fintechs and new emerging technologies such as blockchain.

As more and more countries develop real-time payment infrastructures and the use of cryptotechnologies such as blockchain enters the mainstream, banks can either modernize to keep up with the pace of change or be left behind. Banks should capitalize on their own strengths, as issues such as regulatory compliance and risk management remain paramount, particularly as payments get faster and more inclusive. Fintechs and banks both bring strengths to the payments space, and combining these strengths is absolutely essential to practical innovation.

This white paper series will explore strategies for how banks can modernize to incorporate new technology and use cases into their product offerings and how new players such as fintechs can bridge the gap between new technology and regulatory compliance. By working together with established systems integrators and solution providers that have experience with traditional banking and new technologies, banks and fintechs can collaborate to meet customer expectations while ensuring security and transparency in payments.

2

To someone who spends their Sunday night ordering in from Seamless while watching Netflix on a TV purchased from Amazon, the fact that an electronic payment can take days to process in 2016 seems unbelievable. They can tweet their incredulity to thousands of people around the world in seconds, but they still have to wait until Monday morning for their paycheck to clear. The speed of payments is less surprising to businesses, which can spend an inordinate amount of time planning and forecasting payables and receivables, as well as wrangling with the often-complicated reconciliation process. In other business scenarios however, speed can be an issue, such as paying insurance claims or payroll, or receiving ecommerce payments at low cost.

An increasing number of countries have developed real-time payment systems in recent years to help meet changing end-user expectations. Today, nearly 20 countries on five continents have developed real-time payment systems, with at least a half dozen more countries actively developing or looking into developing real-time infrastructures over the next five years. The development of real-time payments has even reached major markets such as the United States, where The Clearing House is currently developing and testing a system, and the European Union, where the development of scheme rules for instant payments has already begun.

Whether driven by regulators or based on a commercial business case, the move to real-time payments is inevitable. This move presents challenges to banks, which have to deal with legacy IT and business processes based on bulk payments, while continuing to ensure regulatory compliance and risk management. With all of this change happening in an environment where financial institutions face economic pressure to lower costs, partnering with systems integrators, solution providers and fintechs to meet these diverse needs will be vital to retaining customers and expanding business.

As banks look to supplement legacy systems to thrive in a real-time environment, some are looking into the use of cryptotechnologies such as distributed ledger/blockchain to help meet the needs of their customers and offer new revenue opportunities. Indeed, leading global banks are already looking into how to implement cryptotechnologies such as blockchain in core business areas. JPMorgan Chase has tested how to use distributed ledgers to send US dollar payments internationally; Bank of America has filed dozens of patents related to blockchain aimed at transaction banking and risk management; and Santander has co-sponsored startup challenges focused on blockchain and has collaborated with winning teams on how to adapt these technologies for use within the bank.

3

Introduction

Investment in cryptotechnologies and fintech is not limited to a few pioneering banks either. 8 of the world’s 10 largest banks have either developed their own fintech/innovation labs (including JPMorgan Chase, HSBC, Agricultural Bank of China, and Wells Fargo) or have collaborated on innovation challenges aimed at fintech and distributed ledger technologies. The largest banks in Europe, the United States, and Canada have all either invested in their own innovation centers (e.g. Citigroup, Wells Fargo, Deutsche Bank, Barclays) or collaborated with fintechs and other startups in hackathons and innovation challenges (such as Bank of America and Royal Bank of Scotland). Increasingly, major banks are investing in blockchain and other cryptotechnologies. Royal Bank of Canada has developed proof of concepts for the use of blockchain for specific business areas such as payments and customer loyalty programs.

Cryptotechnologies are still in their infancy, and questions remain about how they can be implemented into existing IT and business practices. But the potential benefits of cryptotechnologies – speed, transparency, security, cost savings, and richness of data – are enticing enough that many banks and solution providers are actively looking into use cases for cryptotechnologies in areas such as payments, securities, and trade finance.

But unlocking the benefits of cryptotechnologies is not possible without partners with knowledge of both legacy processes as well as the innovation being developed by fintechs. Understanding established bank processes and regulatory requirements and how best to incorporate innovative new products and services into legacy systems is key to bringing innovation to banks and making fintech products more practical while retaining their benefits. As the technology matures and industry players work together to explore practical uses for this cutting-edge technology, cryptotechnologies may be a tool that helps bridge the gap between legacy technology and future-oriented payments architecture.

4

Bank investments in fintech and cryptotechnology

A bank wishing to offer real-time payments to its customers cannot just flip a switch.

Future-proofing for innovationA bank wishing to offer real-time payments to its customers cannot just flip a switch. It must first identify the requirements for offering real-time (either as a closed-loop service or as part of a shared interbank infrastructure), and then determine the gap between these requirements and its current capabilities. Most banks looking to modernize their payment products and services must deal with legacy IT platforms and business processes that require major updates or overhauls to become compatible with modern payment needs. Legacy issues that contribute to this include systems based on batch processing instead of message-based processing, legacy data standards that do not feature the richness of modern standards like ISO 20022 (particularly relevant for businesses that often require additional remittance data with payment messages), and the fact that bank acquisitions rarely involve a harmonization of IT systems, resulting in complex, patchwork systems cobbled together between two or more banks’ legacy systems.

Banks are well aware of these issues. The biggest hurdle to overcoming them lies in the expense and operational risk inherent in any major IT overhaul. These costs can often be prohibitive, which leads many banks to restrict investments to operational necessity or regulatory mandate. It is extremely unlikely that European banks would have made the IT and business changes required by the SEPA rules if European regulators had not pushed for a harmonized European payments market. At the same time, banks are also well aware of the need to modernize IT systems to meet consumer and business expectations and “future-proof” themselves so they can adapt to changes in the market going forward. As the pressure to modernize becomes more acute from regulatory, operational, and commercial perspectives, banks face the challenge of how they can position themselves strategically to ensure that they fully realize the benefits of faster payments instead of merely playing catch-up with regulators, risk managers, and other banks and fintechs.

Protecting investment through partnershipMost banks opt to work with proven solution providers that offer platforms and services that provide modern payments functionality without the need for a full-scale overhaul of back-office IT and business processes. In addition to enabling banks to offer new products and services, these solutions can help banks protect legacy investment, break down internal siloes (e.g. between different payment instruments), improve customer service, and reduce costs. Along with established solution providers that have a proven track record developing proprietary payment products, an increasing number of smaller firms have emerged as another potential partner (or competitor) for banks in the payments space.

5

As licensed financial institutions, security and regulatory compliance are paramount issues for all banks. With technology evolving at an ever-expanding rate, banks may simply be unable to keep up with the pace of change. In the fintech world, new products and services can be developed, tested, and launched within a few months, whereas banks often need 18-24 months to release new products. A bank’s development cycle is too long when smaller players can release products in a matter of weeks. But this does not mean that banks are unable to use cutting-edge technology to enable practical innovation. On the contrary, banks can and should partner with technology solution providers and fintechs and offer their partners the benefit of risk management, regulatory compliance, and a large customer base. In turn, banks will have access to more flexible and modern products and platforms that can help them meet customer expectations and avoid disintermediation in payments.

This model of partnership between banks and third parties also reflects the current reality of innovation in technology and other fields. No longer do a few monolithic giants control entire industries. Even the world’s largest banks cannot do everything on their own. In today’s world, the bazaar has replaced the cathedral, and mindsets must change accordingly. The democratization of finance and technology is perhaps best evidenced by the latest innovation that has the potential to transform banking over the coming years: the use of cryptotechnologies.

Security and speed through distributed ledgersCryptotechnologies use shared uniform ledgers that are replicated among all participants over a network of interconnected computers to exchange information and value over the Internet. A key aspect of many cryptotechnologies (often referred to as distributed ledgers or blockchain) is decentralized control of the shared ledger, with security and accuracy assured through the use of cryptography. This decentralized control is typically guaranteed via one of two methods: proof-of-work and consensus.

Proof-of-work is a method whereby individual members of a network seek to independently solve a mathematical operation in order to update the shared ledger. Any other member of the network that wishes to check the work done to update the ledger can verify it via a “hash” that is included in each new group of transactions (typically referred to as “blocks” of transactions that link to each other to form a ledger, hence the term “blockchain”). This process is often referred to as “mining,” and is used in the Bitcoin protocol to verify the ledger and create new Bitcoins. The fact that the process of verifying a new ledger is open to all network participants makes this an “unpermissioned” ledger. “Permissioned” ledgers are those where verifying transactions is not open to all members of the network. Instead, the network relies on trusted parties to verify transactions and update the shared ledger that is visible to all participants in the network. These ledgers are often verified using the consensus method. This method involves a consensus algorithm that is applied by all trusted parties (“nodes”) in regular time intervals (often every few seconds). Consensus is reached when a supermajority of nodes agree on the state of the ledger, at which point the ledger is “closed” and the new ledger is open until consensus is reached on the next ledger.

A bank’s development cycle is too long when smaller players can release products in a matter of weeks.

6

As opposed to linking blocks of transactions like Bitcoin, consensus ledgers are continuous records of transactions, not blocks of transactions interlinked with previous blocks. The Ripple protocol uses a consensus algorithm to update its shared ledger every few seconds. The trusted actors who verify the ledger via consensus tend to be large banks and other financial institutions that are geographically dispersed so as to avoid collusion and thereby decrease trust in the network. Ripple continuously updates a list of recommended nodes for participants to use for consensus verification, although individual users can appoint their own nodes to complete the consensus algorithm if they wish.

While cryptotechnologies generally share the common elements of a decentralized shared ledger replicated among all participants using cryptography to ensure security and accuracy, not all cryptotechnologies target the same end users or use cases. To understand the full potential that distributed ledger technology can bring to finance, it is important to explore the full spectrum of cryptotechnology platforms being developed today.

Bringing cutting edge technology into financeMost of the attention given to cryptotechnologies over the past few years has been about Bitcoin, a decentralized cryptocurrency that has been both praised for its technological innovation, speed, and efficiency and criticized for being perceived as a tool for speculation and money laundering. Bitcoin is the first cryptocurrency to gain a sizable amount of users, as well as a whole host of Bitcoin-related businesses that offer services such as Bitcoin gateways, F/X services, merchant acquiring services, and more. Bitcoin has helped bring cryptotechnologies into the mainstream, but it is important to draw a distinction between Bitcoin and the wide range of cryptotechnologies being developed today.

In its May 2015 publication, the Euro Banking Association’s (EBA) Working Group on Electronic and Alternative Payments identified four categories of cryptotechnologies: currencies, asset registries, application stacks, and asset-centric technologies1. Bitcoin, along with similar products such as Dogecoin and Litecoin, fall under the currency category, which deals with the creation and exchange of value via distributed ledgers. Asset registries such as Counterparty on the other hand focus on registering existing assets such as stocks, buildings, and domain names via public distributed ledgers without the need for a central counterparty.

Application stacks using distributed ledger/blockchain are being developed by organizations such as NXT and Ethereum in order to enable the development of applications such as smart contracts via decentralized networks using cryptotechnology. The fourth category identified by the EBA is that of asset-centric technologies, which involve the exchange of digital representations of real-life assets (currencies, stocks, property, etc.) as opposed to merely registering these assets on the blockchain. Examples of asset-centric technologies include Ripple, Stellar, and Namecoin. These asset-centric cryptotechnologies are identified by the EBA as having the most potential for use by financial institutions due to regulatory and technical issues being a stronger obstacle in the currency, asset registry, and application stack cryptotechnologies.

7

It is clear that cryptotechnologies will play a role in payments and trade finance going forward.

1 https://www.abe-eba.eu/downloads/knowledge-and-research/ EBA_20150511_EBA_Cryptotechnologies_a_major_IT_innovation_v1_0.pdf

It is clear that the development of cryptotechnologies is growing rapidly and that it is not focus on cryptocurrencies such as Bitcoin. It remains unclear which categories or use cases will provide the most potential in the short- to medium-term, but it is clear that cryptotechnologies will play a role in payments and trade finance going forward. But before a bank, fintech, or solution provider can implement or utilize cryptotechnologies in their business, it is important to first understand the benefits these technologies can bring, the challenges to implementing them, and strategies for overcoming these challenges and reaping the rewards cryptotechnologies can bring to banks, fintechs, and end users.

How cryptotechnologies increase agility and customer satisfactionWhile cryptotechnologies possess a number of features that make them attractive for smaller players such as fintechs and challenger banks, they also promise benefits for banks and other large financial institutions. Chief among these benefits are speed and transparency, which are key to meeting customer expectations in a modern payments environment. Cryptotechnologies also offer security and the chance for banks to lower costs and become more flexible in an environment of changing regulations and customer expectations.

The most immediate benefit cryptotechnologies provide is speed, namely the ability to send and receive assets over the blockchain within minutes or even seconds. The lack of a central authority to oversee each transaction removes the possibility of a bottleneck, particularly when high volumes are being exchanged. The use of encryption over the Internet can increase the velocity of payments and other related information compared to legacy payment systems or interbank networks. On distributed ledgers, two banks can directly exchange information without relying on third parties or correspondent banks, even if the payment is being made internationally.

Distributed ledgers also enable a level of transparency that currently does not exist in legacy payment systems, particularly for international payments. While consumers may have full visibility of where a package is when they order something off of the Internet, bank customers rarely if ever have the same level of transparency when it comes to payments. With cryptotechnologies, banks can give end users full visibility of payments and other information in real-time, thereby improving the quality of their products and customer service.

Security is the backbone of cryptotechnologies, which can help protect customer data and ensure the integrity of information. Cryptotechnology platforms have security hard-coded into their DNA, with all exchanged information encrypted. This information can only be unlocked with the use of security key (public-private key encryption), enabling participants to both “lock” data as it is exchanged and provide others with keys to “unlock” data in order to verify that the information came from the party that claims to have sent it. In an environment where data is fast becoming more valuable than oil, the need to send and receive secure data in an instant will be paramount.

8

Cryptotechnologies offer speed, transparency, security and cost savings.

Cryptotechnologies can also reduce costs related to the processing of payments. This is particularly relevant for international payments, which often require banks to send payments via one or more correspondents, each of which charges a processing fee for the service. But even domestic payments could see cost savings compared to legacy payment systems and back-office processes, many of which run on older, less efficient technology platforms that have been patched or partially updated over the years. Incorporating cryptotechnology functionality into back office systems can allow a bank to rationalize processing costs by using platforms that automatically incorporate updates as technology evolves. The reduction in both internal and external processing costs could also result in smaller transaction values being exchanged, which would benefit corporate clients in particular. This also has the effect of lowering barriers to entry in payments, thereby allowing smaller banks, third parties, or even individuals to directly participate in systems that would otherwise require partnering with (and paying fees to) larger players.

Cryptotechnologies can also increase flexibility by allowing banks and fintechs to be more agile when developing new products and services for their customers. Some cryptotechnology platforms are even going one step further and enabling businesses to build products and services on distributed ledger applications. Ethereum has developed a custom blockchain platform that allows users to run smart contracts that can be used to exchange value or represent ownership of property or other assets. This shows that cryptotechnologies not only allow banks and fintechs to focus on innovation through the use of efficient, secure, and cost effective payments processing, but it also represents potential as a platform for innovation itself.

Cryptotechnologies enable banks and fintechs to increase speed and transparency while ensuring a high degree of security. Banks in particular can benefit by reducing costs and becoming more flexible, thereby empowering them to focus on innovation and meeting customer needs. By lower the barriers to entry for payments, cryptotechnologies can also help expand the spectrum of financial services offered to consumers and businesses. These benefits can certainly help change the game in payments, but it is not about fundamentally changing business practices. Instead, it is about improving them by making them more efficient, flexible, transparent, and cost effective.

While cryptotechnologies offer a number of benefits and advantages for banks, solution providers, fintechs, and end users, there are still a number of serious challenges that could inhibit adoption. Chief among these challenges are the unclear regulatory and legal environment surrounding cryptotechnologies, issues of compliance due to a lack of understanding of end-to-end business processes, questions around scaling up as transaction volumes increase, the trouble banks face in creating a business case for implementing cryptotechnologies, and the difficulty of incorporating cryptotechnologies into legacy back-office systems.

9

The regulatory framework around distributed ledger technology remains unclear. Cryptotechnologies are still in their infancy, and their adoption by financial institutions, corporates, and individuals is still quite low. But the uncertainty that results from this lack of a regulatory framework could inhibit uptake of cryptotechnologies. Regulatory compliance is a key strength of banks, and many financial institutions may prefer to wait until there is more legal clarity on this issue before adopting distributed ledger technologies in earnest. There are some positive signs on this front: the UK Government Office for Science recently published a report2 on distributed ledger technology that included a recommendation that government consider developing regulations around distributed ledger technology. As other countries follow the UK’s lead, the regulatory environment around cryptotechnologies should become clearer.

The use of cryptotechnologies by banks is also inhibited by the fact that many cryptotechnology providers and other fintechs lack the necessary understanding of the end-to-end business process around legacy payment instruments and systems. Compliance issues such as anti-money laundering and counter-terrorism financing (AML/CTF) screening or Know Your Customer (KYC) regulations are extremely important for banks, particularly for international payments. Cryptotechnology solutions that do not account for these processes or that are difficult to integrate in IT systems based on batch processing and banking business hours will not be feasible for banks to adopt.

Distributed ledger solutions that do account for compliance and business process issues are an improvement, but it does not negate the problem of banks implementing such solutions into legacy back-office systems. No matter how well designed a cryptotechnology solution is, banks are rarely able to incorporate any “plug and play” solution into existing systems. Many banks have turned to trusted solution providers to help bridge the gap between legacy systems and modern products, so cryptotechnology providers should look to partner with these vendors and ensure that their solution can be added to their suite of products.

Currently, transaction volumes on distributed ledger platforms are very low. Even the most popular cryptotechnology solution, Bitcoin, sees far lower volumes than legacy payment systems used by banks. In order for the use of cryptotechnologies to migrate from individuals to institutions, there will need to be proof that it can scale up to handle higher volumes and values. As long as this issue remains unclear, it is difficult to envision banks utilizing distributed ledgers for anything more than niche products and services.

The last challenge lies in the difficulty banks have in developing a traditional business case for adopting cryptotechnologies at an institutional level. Part of this difficulty is directly related to uncertainty around regulations and the technology’s ability to scale up. If a bank is unsure whether or not it will even be allowed by regulators to use cryptotechnologies for areas such as payments, it cannot accurately forecast revenue or predict a return on investment. Because cryptotechnologies are still in the early adoption phase, it is unclear how many other institutions will adopt distributed ledger technology in the coming years and whether or not the use of cryptotechnologies will become widespread and therefore necessary to compete in the payments market. Projects that involve renovating or updating IT systems without a regulatory mandate are always a difficult sell within banks, and the uncertainty surrounding cryptotechnologies could compound these difficulties.

10

2 https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/492972/gs-16-1- distributed-ledger-technology.pdf

Cryptotechnology solutions must account for legacy compliance and business issues.

11

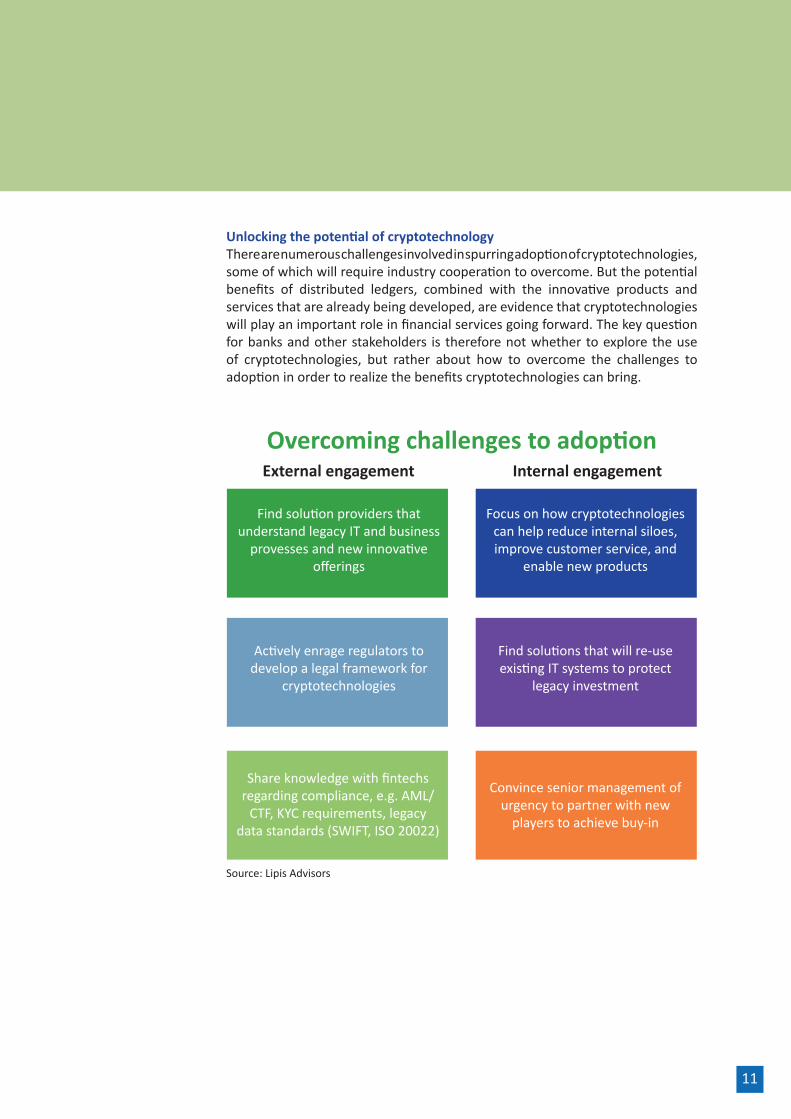

Unlocking the potential of cryptotechnologyThere are numerous challenges involved in spurring adoption of cryptotechnologies, some of which will require industry cooperation to overcome. But the potential benefits of distributed ledgers, combined with the innovative products and services that are already being developed, are evidence that cryptotechnologies will play an important role in financial services going forward. The key question for banks and other stakeholders is therefore not whether to explore the use of cryptotechnologies, but rather about how to overcome the challenges to adoption in order to realize the benefits cryptotechnologies can bring.

Overcoming challenges to adoptionExternal engagement Internal engagement

Actively enrage regulators to develop a legal framework for

cryptotechnologies

Share knowledge with fintechsregarding compliance, e.g. AML/

CTF, KYC requirements, legacydata standards (SWIFT, ISO 20022)

Find solution providers thatunderstand legacy IT and business

provesses and new innovativeofferings

Find solutions that will re-useexisting IT systems to protect

legacy investment

Convince senior management ofurgency to partner with new

players to achieve buy-in

Focus on how cryptotechnologiescan help reduce internal siloes,improve customer service, and

enable new products

Source: Lipis Advisors

12

There is often a knowledge gap between banks and fintechs that presents an obstacle to incorporating innovative products based on cryptotechnology with established systems. Banks tend to focus more on regulatory compliance and risk management than on innovation, and the sheer number of different innovative products available (particularly those based on new technologies that banks do not yet understand) makes it difficult to know which products and services are feasible for use within a bank. On the other side, many fintechs lack knowledge of end-to-end processes within banks in areas such as payments. Compliance issues such as AML/CTF screening or KYC requirements may not be taken into account, not to mention the reality of legacy systems that are not as fast or transparent as services based on cryptotechnologies. Bridging this gap requires both banks and fintechs to look to trusted partners with a proven track record of servicing banks and other financial institutions as well as knowledge of innovation currently taking place in financial services. These partners can provide advice on how to best integrate new products into legacy systems and on how products can be adjusted to optimize their use within legacy banking systems.

Collaboration and partnership between industry stakeholders will be key to unlocking the potential of cryptotechnologies in finance. This includes not only banks and fintechs, but regulators, payment associations, software providers, and non-bank financial institutions as well. Banks should actively engage regulators about developing a legal framework around cryptotechnologies. By exploring the opportunities distributed ledgers can bring internally and to their customers, banks can provide regulators with their view on these technologies and how they view them fitting into current regulatory frameworks and where uncertainty in regulation lies. By engaging regulators and other industry stakeholders, banks can contribute to new regulations regarding cryptotechnologies, which can aid internal planning. The Australian government has devised an agenda aimed at promoting fintech development, including for start-ups using cryptotechnologies.3 The plan aims to guarantee that tax, investment, and regulatory policies are aligned with the government’s goal to ensure a level playing field for fintechs and other non-bank payment providers.

Fintechs should actively look to partner with banks and solution providers in order to better understand the end-to-end processes in payments and other areas of finance that cryptotechnology solutions are targeting. This could help fintechs adapt solutions to meet regulatory and business needs of banks, including AML/CTF screening, KYC requirements, interoperability with widely-used data standards such as SWIFT MT and ISO 20022, and reporting requirements for international transactions. Fintechs should look to solution providers that already service banks and look into opportunities to integrate distributed ledger technology into product suites used by banks. By collaborating with banks and the solution providers that serve them, fintechs can improve their product offerings and enable practical innovation.

3 http://fintech.treasury.gov.au/files/2016/03/Fintech_March2016_online.pdf? utm_content=buffer35071&utm_medium=social&utm_source=twitter.com&utm_campaign=buffer

There is often a knowledge gap between banks and fintechs that presents an obstacle to incorporating innovative products with established systems.

Banks should also reach out to partners that understand innovative offerings in the market and the role cryptotechnologies can play as the payments industry evolves. Whether this means finding individual fintechs to collaborate with, fintech accelerators (either internal or external), or solution providers with knowledge of both core payments and cryptotechnologies, banks can profit from partners with both knowledge of current processes and vision about how innovative offerings can be implemented practically in order to meet customer needs and lower costs. One of the more prominent examples of this in the cryptotechnology space is R3, a consortium of 42 global banks that is actively exploring use cases and testing solutions for financial markets using distributed ledgers. Most recently, R3 banks tested five separate blockchains running smart contracts to see which solution would add the most value to these banks’ financial trading business. R3 member banks include Barclays, HSBC, TD Bank, Wells Fargo, JPMorgan Chase, Bank of America, and Citi.

Partnership has the added benefit of enabling both banks and fintechs to focus on their core business. For banks, regulatory compliance, risk management, and trust are their key differentiator with clients. Fintechs focus on using new technology to create innovative product offerings for the market. If a bank spends too much time focusing on innovation, it could take resources away from financing and risk management. Fintechs need to stay aware of regulatory requirements, but cannot let this take away from staying on the cutting edge of technology. By working together, both sides can mutually benefit from the core business of the other and create a greater whole that will benefit end users.

Most banks looking to implement cryptotechnologies will experience difficulties in gaining internal approval and funding for a project that still has so much uncertainty. Partnership with fintechs and solution providers (particularly with vendors that have already implemented distributed ledger technology into its product offerings) can help, but it may not be enough to create a traditional business case. But this does not mean that the adoption of cryptotechnologies is doomed to fail, or that all banks will wait until a critical mass of adoption of reached before exploring their own use of the technology. In an age where customer expectations and technology are changing rapidly, banks must adopt a strategic mindset to payments in order to avoid being left behind by innovation.

Banks should ask themselves not only how much revenue cryptotechnologies will bring in the next 3-5 years, but also about how distributed ledger can help reduce or eliminate internal siloes, how it can improve customer service, how it can enable new connection with banks and fintechs around the world, and how it can enable new product offerings that offer enhanced transparency, speed, and lower cost to consumers and businesses. By expanding the scope of a business case and adopting a strategic mindset to how cryptotechnologies can create long-lasting improvements to IT architecture and business processes, bankers can achieve internal buy-in and focus around the project of implementing distributed ledger technology.

13

ConclusionBridging the gap between legacy systems and processes and cutting-edge innovation is a difficult task with huge potential benefits for banks, fintechs, and end users. Cryptotechnologies have emerged as a tool for creating innovative products that meet customer expectations for speed and transparency while enabling banks to reduce costs, increase flexibility, and ensure security. While there are still obstacles to adoption of cryptotechnologies, it is vital that banks work to overcome these challenges. Failing this, they will risk being left behind in an industry where innovation is becoming quicker and more agile. The key to overcoming these challenges will be in finding partners that understand legacy bank systems as well as cutting edge innovation, and in working together with fintechs, solution providers, and regulators. By doing this, both banks and fintechs can deliver practical innovation that meets customer expectations, lowers costs, and provides flexibility for the future.

14

About CGI

Founded in 1976, CGI is a global IT and business process services provider delivering high-quality business consulting, systems integration and managed services. The company’s leadership in the payments marketplace dates to the 1970s and it has been at the forefront in key payments initiatives such as SWIFT, SEPA, UK CHAPS, and CLS.

Today, CGI’s payment solutions, based on industry best practices and standards, enable banks to efficiently manage regulatory and market changes while introducing new and tailored services across the globe. CGI’s modernization-in-place strategies minimize disruption and mitigate client risk, while creating transformative solutions which lead the industry in on-time and within budget delivery.

More than 10,000 CGI financial services professionals based in 40 countries help top banks to reduce cost, increase efficiency and improve customer service. Having implemented more than 80 payment solutions globally, CGI offers robust consulting and systems integration expertise to transform operations across the payments lifecycle. Learn more at www.cgi.com/payments.

About Lipis Advisors

Lipis Advisors is a leading strategy consultancy specializing in the payment sector. Lipis Advisors are experts on payment systems, services, and strategy, as well as the underlying technologies that support payment infrastructures. Lipis Advisors advises on all forms of payments, including ACH payments, real-time payments, card payments, cheques, mobile payments, online payments, and RTGS/wire payments. To learn more about Lipis Advisors, please visit www.lipisadvisors.com

Authors

Leo Lipis is chief executive and founder of Lipis Advisors.

Colin Adams is a senior consultant for Lipis Advisors.

Lipis Advisors