powertrain - kgp

TRANSCRIPT

Powertrain Global Commercial Vehicle Powertrain ForecastAnnual Report 2020

ContentsGlobal Commercial Vehicle Powertrain Update, Quarter 1 2020

Commercial Powertrain Intelligence Page 1/81

Contents2 Introduction

3 Top 10 Hot Topics of 2019

4 Hot Topics Q120

5 Global Economy

6 Corona Virus Impact

7 Geographic Scope

8 Regional Outlook

9 Regional Outlook - Quarterly

10 Segment Outlook

11 EU & EFTA

12 North America

13 China

14 India

15 Japan

16 South America

17 Australia & ASEAN

18 OEM Outlook

19 Engine OEM Outlook

20 Legislative Overview

21 Carbon Dioxide Legislation

22 Noxious Emissions Legislation

23 Future Diesel Technology

24 Legislative Outlook

25 Aftertreatment Outlook

26 Technology Highlight

27 Alternative Fuels Outlook

28 Transmissions Outlook

29 Transmissions Outlook

30 Ashok Leyland Production

31 Ashok Leyland Alternative Fuels

32 Ashok Leyland Engines

33 CNH Industrial Production

34 CNH Industrial Alternative Fuels

35 CNH Industrial Engines

36 CNHTC Production

37 CNHTC Alternative Fuels

38 CNHTC Engines

39 Daimler Production

40 Daimler Alternative Fuels

41 Daimler Engines

42 Dongfeng Production

43 Dongfeng Alternative Fuels

44 Dongfeng Engines

45 FAW Production

46 FAW Alternative Fuels

47 FAW Engines

48 Ford Production

49 Ford Alternative Fuels

50 Ford Engines

51 Foton Production

52 Foton Alternative Fuels

53 Foton Engines

54 Hino Production

55 Hino Alternative Fuels

56 Hino Engines

57 Isuzu Production

58 Isuzu Alternative Fuels

59 Isuzu Engines

60 Navistar Production

61 Navistar Alternative Fuels

62 Navistar Engines

63 PACCAR Production

64 PACCAR Alternative Fuels

65 PACCAR Engines

66 Tata Motors Production

67 Tata Motors Alternative Fuels

68 Tata Motors Engines

69 TRATON Production

70 TRATON Alternative Fuels

71 TRATON Engines

72 Volvo Production

73 Volvo Altnerative Fuels

74 Volvo Engines

75 Weichai Production

76 Weichai Alternative Fuels

77 Weichai Engine Production

78 Weichai Engines

79 Cummins Engine Production

80 Cummins Alternative Fuels

81 Cummins Engines

IntroductionGlobal Commercial Vehicle Powertrain Update, Quarter 1 2020

Commercial Powertrain Intelligence Page 2/81

KGP BackgroundKGP provides insight and analysis that no other consultancy can provide, by focussing on niche segments in the industry. Founded in 1988 KGP has built 30 years’ experience and relationships to support the various stakeholders. In each segment and sub-segment of the industry we consider a number of factors in our forecasts, including, but not limited to:

▪ Emissions, fuel economy and other legislation

▪ OEM supply chain relationships

▪ OEM financial performance

▪ Vehicle, engine and component strategies

▪ Engine sourcing, development and production

▪ Engine, component and & aftertreatment developments

▪ Transmission and driveline trends

▪ Customer buying trends and TCO

The Commercial Vehicle Powertrain Service from Knibb, Gormezano and Part-ners (KGP), and its Strategic Partner, LMC Automotive, provides detailed insight and forecasts of the global Commercial Vehicle market focussed on the power-train: - engine and transmission, and increasingly electrification and alternative fuels.

LMC Automotive provides the base data for KGP’s Global Commercial Vehicle Powertrain Forecast (GCVPTF) including both global production and sales fore-casts.

The service, built on detailed databases and forecasts, complemented by ex-pert analysis, helps our customers understand an increasingly complex market. Supporting both data and analysis KGP has started producing quarterly special-ised reports examining the economic, social, political, legislative, technological

and environmental drivers that are affecting individual markets and how this, in turn, will affect the global marketplace and its stakeholders.

KGP Commercial Vehicle Executive Summary Report ▪ This product, the Commercial Vehicle Executive Summary Report, sum-

maries the data from the quarterly update to the GCVPTF and outlines any significant changes.

▪ The report covers important news items, legislative changes, technology updates and other market impacts.

▪ Although this report concentrates on engines, alternative fuels are dis-cussed. However, KGP offers a specific database and report for electric, hybrid and alternative fuelled powertrains.

KGP Other Items ▪ In Q2 2019, several new fields were added to the GCVPTF Database:

Transmissions, Voltage System, Motor Power, Motor Position and Advanced Energy Storage. KGP will include a slide discussing each addition in the Quarterly Executive Summary over the course of the year.

▪ KGP’s website ‘Commercial Powertrain Portal’ continues to be updated with the latest industry news, analysis and data regarding CV and NRMM markets.

▪ KGP’s Commercial Vehicle xEV Scenarios will be updated in April 2020 containing market penetration for alternative fuelled powertrains, in-cluding natural gas, biofuels, hybrid, electric and fuel cell, by region and segment.

▪ KGP continues to strengthen its global capabilities. Rhein Associates, our partner since 2005, will take a broader and deeper role in supporting both CV and NRMM forecasts in North America. New partner Carcon, LMC’s existing partner in South America, will mutually support each other on powertrain related topics in that market.

Top 10 Hot Topics of 2019

Commercial Powertrain Intelligence Page 3/81

01 - EPA propose new NOx rule ▪ EPA have launched the Cleaner Trucks Initiative which will reduce the

existing NOx emission standards, A proposal for the rule is expected to be published in 2022 with implementation around the 2027 timeframe. CARB will look to set standards for 2024.

02 - EU CO2 HDV Standards Finalised ▪ On the 19th February 2019, the EU approved the very first CO2 emission

standards for heavy-duty vehicles. The European Council and the European Commission (EC) approved the proposal to set CO2 emission performance standards for new heavy-duty vehicles (HDV). Although back in November MEP backed the tightening of CO2 reducing targets, the approved tar-gets retreat to the original proposal, setting a target of 15% for 2025 and 30%, unless changed in a 2022 review, by 2030.

03 - Mexico Postpones Clean Diesel Rule ▪ Mexico has postponed the rule for clean diesel due to a lack of production

of ultra-low sulphur diesel (USLD) for five years. EPA 10/Euro VI, which was to be implemented from 2019-2021, is likely to be postponed as manufac-turers delay investments. Mexico City will continue its implementation as originally planned but other regions remain uncertain.

04 - Cummins’ and Isuzu’s partnership ▪ Following Cummins and Isuzu signing a letter of intent to evaluate global

opportunities, in October 2018, both companies has now entered the Isuzu Cummins Powertrain Partnership agreement. The agreement is the basis to jointly develop new powertrains, with a focus on diesel.

05 - Volvo sells UD Truck to Isuzu ▪ Volvo will partner with Isuzu to share costs on advanced technologies and

will also sell its Japanese truck brand UD Trucks to Isuzu for $2.3 billion.

It is uncertain in the details of the partnership with Isuzu also tied up with Cummins. KGP initial thoughts are Cummins will supply engines over 9L to Isuzu while Volvo will source MD5 and MD8.

06 - CNHi joint venture with Nikola Motors ▪ Just three months after announcing a $250m investment by CNH Industrial

in Nikola the pair announced production of the Nikola Tre as part of their co-operation. Both battery electric (BEV) and fuel cell electric (FCEV) will be produced as part of the deal.

07 - CNHi to split on and off-highway businesses ▪ As part of CNHi’s 5 year reorganisation plan, Transform 2 win, its two

main business will be separated into different segments, on-highway and off-highway, due to diverging requirements for both industries.

08 - Hyundai and Cummins partner for fuel cells ▪ Hyundai and Cummins gave entered a memorandum of understanding

(MOU) to evaluate opportunities to jointly develop electric and fuel cell powertrains. The initial focus will be on North America’s commercial vehicle market with powertrains to use Hyundai’s fuel cell technologies combined with Cummins’ electric, battery and control technologies.

09 - TRATON IPO ▪ TRATON’s IPO, although originally set for April, began in June with VW

floating 11.5% of TRATON shares with the share price set at 27 Euros each. From the IPO TRATON raised 1.55 billion Euros.

10 - Hino opens North American plant ▪ Hino held an opening ceremony for its new plant in West Virginia. The first

medium-duty trucks were produced in June this year with annual plant capacity at 24,000 units.

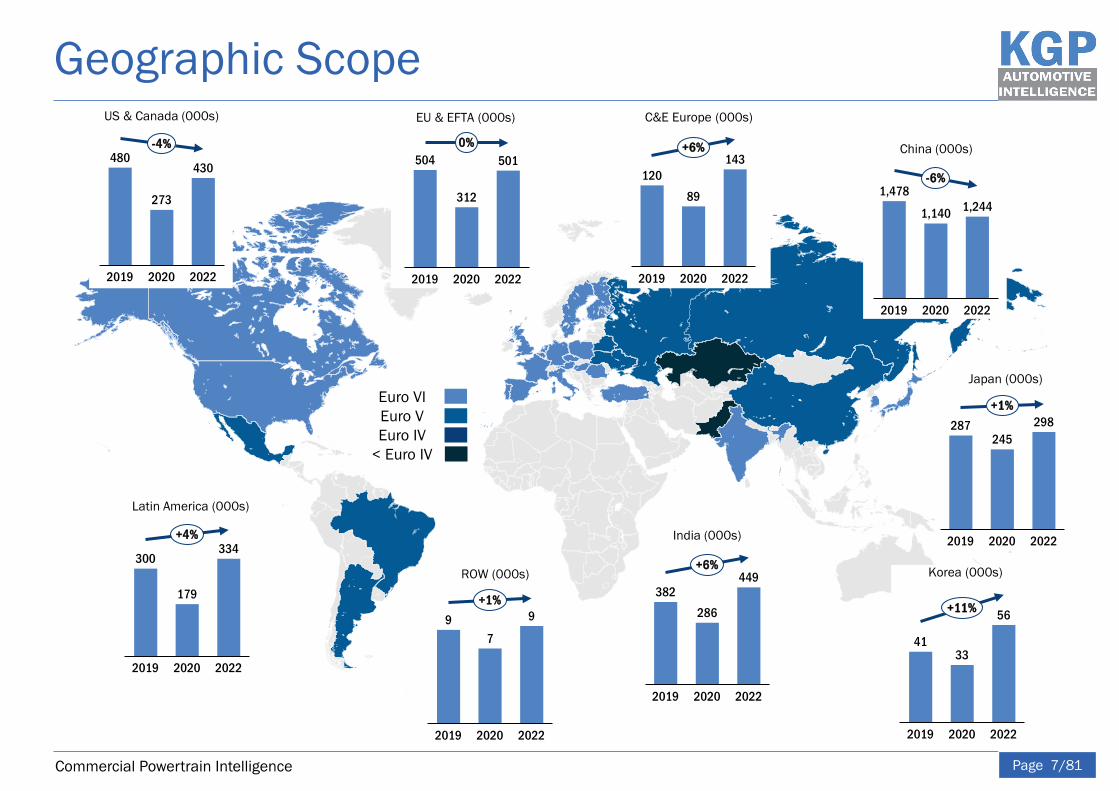

Geographic Scope

Commercial Powertrain Intelligence Page 7/81

Korea (000s)

2020

56

2019 2022

4133

++1111%%

China (000s)

1,244

20222019 2020

1,140

1,478--66%%

India (000s)

202220202019

382286

449++66%%

Japan (000s)

2019

298245

2020 2022

287++11%%

US & Canada (000s)

273

202220202019

480430

--44%%

2019

504

2020 2022

312

50100%%

Latin America (000s)

2019 2020

179

300

2022

334++44%%

C&E Europe (000s)

143

89

2019 2020 2022

120

++66%%

ROW (000s)

9

2019 2020 2022

79

++11%%

EU & EFTA (000s)

Euro VIEuro VEuro IV

< Euro IV

Korea (000s)

2020

56

2019 2022

4133

++1111%%

China (000s)

1,244

20222019 2020

1,140

1,478--66%%

India (000s)

202220202019

382286

449++66%%

Japan (000s)

2019

298245

2020 2022

287++11%%

US & Canada (000s)

273

202220202019

480430

--44%%

2019

504

2020 2022

312

50100%%

Latin America (000s)

2019 2020

179

300

2022

334++44%%

C&E Europe (000s)

143

89

2019 2020 2022

120

++66%%

ROW (000s)

9

2019 2020 2022

79

++11%%

EU & EFTA (000s)

Euro VIEuro VEuro IV

< Euro IV

Korea (000s)

2020

56

2019 2022

4133

++1111%%

China (000s)

1,244

20222019 2020

1,140

1,478--66%%

India (000s)

202220202019

382286

449++66%%

Japan (000s)

2019

298245

2020 2022

287++11%%

US & Canada (000s)

273

202220202019

480430

--44%%

2019

504

2020 2022

312

50100%%

Latin America (000s)

2019 2020

179

300

2022

334++44%%

C&E Europe (000s)

143

89

2019 2020 2022

120

++66%%

ROW (000s)

9

2019 2020 2022

79

++11%%

EU & EFTA (000s)

Euro VIEuro VEuro IV

< Euro IV

Korea (000s)

2020

56

2019 2022

4133

++1111%%

China (000s)

1,244

20222019 2020

1,140

1,478--66%%

India (000s)

202220202019

382286

449++66%%

Japan (000s)

2019

298245

2020 2022

287++11%%

US & Canada (000s)

273

202220202019

480430

--44%%

2019

504

2020 2022

312

50100%%

Latin America (000s)

2019 2020

179

300

2022

334++44%%

C&E Europe (000s)

143

89

2019 2020 2022

120

++66%%

ROW (000s)

9

2019 2020 2022

79

++11%%

EU & EFTA (000s)

Euro VIEuro VEuro IV

< Euro IV

Korea (000s)

2020

56

2019 2022

4133

++1111%%

China (000s)

1,244

20222019 2020

1,140

1,478--66%%

India (000s)

202220202019

382286

449++66%%

Japan (000s)

2019

298245

2020 2022

287++11%%

US & Canada (000s)

273

202220202019

480430

--44%%

2019

504

2020 2022

312

50100%%

Latin America (000s)

2019 2020

179

300

2022

334++44%%

C&E Europe (000s)

143

89

2019 2020 2022

120

++66%%

ROW (000s)

9

2019 2020 2022

79

++11%%

EU & EFTA (000s)

Euro VIEuro VEuro IV

< Euro IV

Korea (000s)

2020

56

2019 2022

4133

++1111%%

China (000s)

1,244

20222019 2020

1,140

1,478--66%%

India (000s)

202220202019

382286

449++66%%

Japan (000s)

2019

298245

2020 2022

287++11%%

US & Canada (000s)

273

202220202019

480430

--44%%

2019

504

2020 2022

312

50100%%

Latin America (000s)

2019 2020

179

300

2022

334++44%%

C&E Europe (000s)

143

89

2019 2020 2022

120

++66%%

ROW (000s)

9

2019 2020 2022

79

++11%%

EU & EFTA (000s)

Euro VIEuro VEuro IV

< Euro IV

Korea (000s)

2020

56

2019 2022

4133

++1111%%

China (000s)

1,244

20222019 2020

1,140

1,478--66%%

India (000s)

202220202019

382286

449++66%%

Japan (000s)

2019

298245

2020 2022

287++11%%

US & Canada (000s)

273

202220202019

480430

--44%%

2019

504

2020 2022

312

50100%%

Latin America (000s)

2019 2020

179

300

2022

334++44%%

C&E Europe (000s)

143

89

2019 2020 2022

120

++66%%

ROW (000s)

9

2019 2020 2022

79

++11%%

EU & EFTA (000s)

Euro VIEuro VEuro IV

< Euro IV

Korea (000s)

2020

56

2019 2022

4133

++1111%%

China (000s)

1,244

20222019 2020

1,140

1,478--66%%

India (000s)

202220202019

382286

449++66%%

Japan (000s)

2019

298245

2020 2022

287++11%%

US & Canada (000s)

273

202220202019

480430

--44%%

2019

504

2020 2022

312

50100%%

Latin America (000s)

2019 2020

179

300

2022

334++44%%

C&E Europe (000s)

143

89

2019 2020 2022

120

++66%%

ROW (000s)

9

2019 2020 2022

79

++11%%

EU & EFTA (000s)

Euro VIEuro VEuro IV

< Euro IV

Korea (000s)

2020

56

2019 2022

4133

++1111%%

China (000s)

1,244

20222019 2020

1,140

1,478--66%%

India (000s)

202220202019

382286

449++66%%

Japan (000s)

2019

298245

2020 2022

287++11%%

US & Canada (000s)

273

202220202019

480430

--44%%

2019

504

2020 2022

312

50100%%

Latin America (000s)

2019 2020

179

300

2022

334++44%%

C&E Europe (000s)

143

89

2019 2020 2022

120

++66%%

ROW (000s)

9

2019 2020 2022

79

++11%%

EU & EFTA (000s)

Euro VIEuro VEuro IV

< Euro IV

Korea (000s)

2020

56

2019 2022

4133

++1111%%

China (000s)

1,244

20222019 2020

1,140

1,478--66%%

India (000s)

202220202019

382286

449++66%%

Japan (000s)

2019

298245

2020 2022

287++11%%

US & Canada (000s)

273

202220202019

480430

--44%%

2019

504

2020 2022

312

50100%%

Latin America (000s)

2019 2020

179

300

2022

334++44%%

C&E Europe (000s)

143

89

2019 2020 2022

120

++66%%

ROW (000s)

9

2019 2020 2022

79

++11%%

EU & EFTA (000s)

Euro VIEuro VEuro IV

< Euro IV

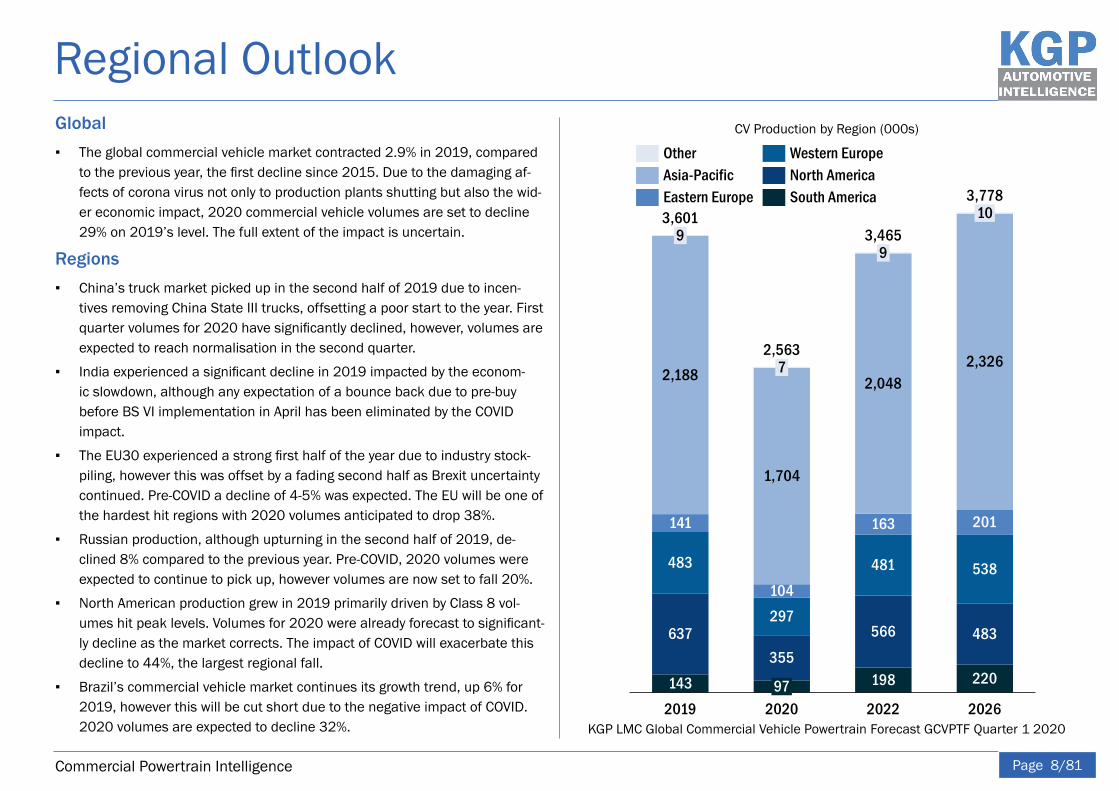

Regional Outlook

Commercial Powertrain Intelligence Page 8/81

Global ▪ The global commercial vehicle market contracted 2.9% in 2019, compared

to the previous year, the first decline since 2015. Due to the damaging af-fects of corona virus not only to production plants shutting but also the wid-er economic impact, 2020 commercial vehicle volumes are set to decline 29% on 2019’s level. The full extent of the impact is uncertain.

Regions ▪ China’s truck market picked up in the second half of 2019 due to incen-

tives removing China State III trucks, offsetting a poor start to the year. First quarter volumes for 2020 have significantly declined, however, volumes are expected to reach normalisation in the second quarter.

▪ India experienced a significant decline in 2019 impacted by the econom-ic slowdown, although any expectation of a bounce back due to pre-buy before BS VI implementation in April has been eliminated by the COVID impact.

▪ The EU30 experienced a strong first half of the year due to industry stock-piling, however this was offset by a fading second half as Brexit uncertainty continued. Pre-COVID a decline of 4-5% was expected. The EU will be one of the hardest hit regions with 2020 volumes anticipated to drop 38%.

▪ Russian production, although upturning in the second half of 2019, de-clined 8% compared to the previous year. Pre-COVID, 2020 volumes were expected to continue to pick up, however volumes are now set to fall 20%.

▪ North American production grew in 2019 primarily driven by Class 8 vol-umes hit peak levels. Volumes for 2020 were already forecast to significant-ly decline as the market corrects. The impact of COVID will exacerbate this decline to 44%, the largest regional fall.

▪ Brazil’s commercial vehicle market continues its growth trend, up 6% for 2019, however this will be cut short due to the negative impact of COVID. 2020 volumes are expected to decline 32%. KGP LMC Global Commercial Vehicle Powertrain Forecast GCVPTF Quarter 1 2020

CV Production by Region (000s)

9

2019

2,188

483

2020

297

7

143

637

1,704

104

2,563

10

355

97

141

2,048

3,601

163

481

483566

198

2022

2,326

201

538

220

2026

3,778

3,4659

OtherNorth AmericaWestern Europe

Asia-PacificEastern Europe South America

Australia & ASEAN

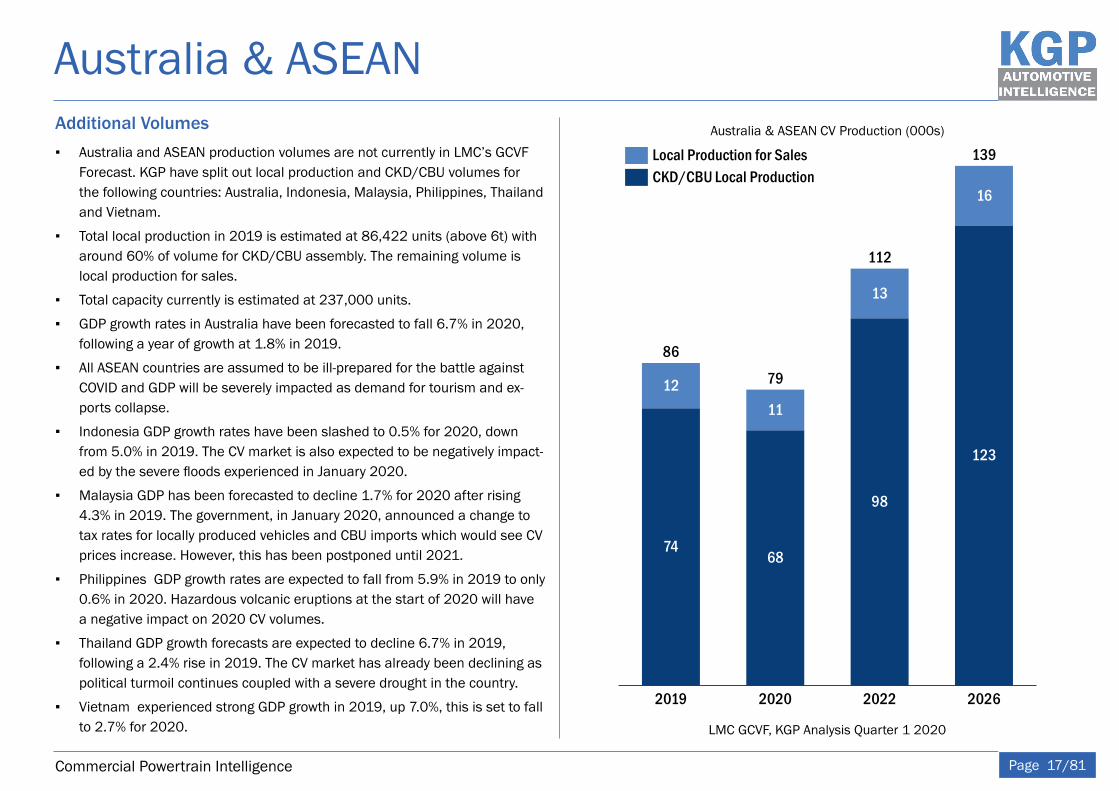

Commercial Powertrain Intelligence Page 17/81

Additional Volumes ▪ Australia and ASEAN production volumes are not currently in LMC’s GCVF

Forecast. KGP have split out local production and CKD/CBU volumes for the following countries: Australia, Indonesia, Malaysia, Philippines, Thailand and Vietnam.

▪ Total local production in 2019 is estimated at 86,422 units (above 6t) with around 60% of volume for CKD/CBU assembly. The remaining volume is local production for sales.

▪ Total capacity currently is estimated at 237,000 units.

▪ GDP growth rates in Australia have been forecasted to fall 6.7% in 2020, following a year of growth at 1.8% in 2019.

▪ All ASEAN countries are assumed to be ill-prepared for the battle against COVID and GDP will be severely impacted as demand for tourism and ex-ports collapse.

▪ Indonesia GDP growth rates have been slashed to 0.5% for 2020, down from 5.0% in 2019. The CV market is also expected to be negatively impact-ed by the severe floods experienced in January 2020.

▪ Malaysia GDP has been forecasted to decline 1.7% for 2020 after rising 4.3% in 2019. The government, in January 2020, announced a change to tax rates for locally produced vehicles and CBU imports which would see CV prices increase. However, this has been postponed until 2021.

▪ Philippines GDP growth rates are expected to fall from 5.9% in 2019 to only 0.6% in 2020. Hazardous volcanic eruptions at the start of 2020 will have a negative impact on 2020 CV volumes.

▪ Thailand GDP growth forecasts are expected to decline 6.7% in 2019, following a 2.4% rise in 2019. The CV market has already been declining as political turmoil continues coupled with a severe drought in the country.

▪ Vietnam experienced strong GDP growth in 2019, up 7.0%, this is set to fall to 2.7% for 2020. LMC GCVF, KGP Analysis Quarter 1 2020

Australia & ASEAN CV Production (000s)

79

2019

139

20222020

86

2026

112

74

12

68

11

98

13

123

16

Local Production for SalesCKD/CBU Local Production

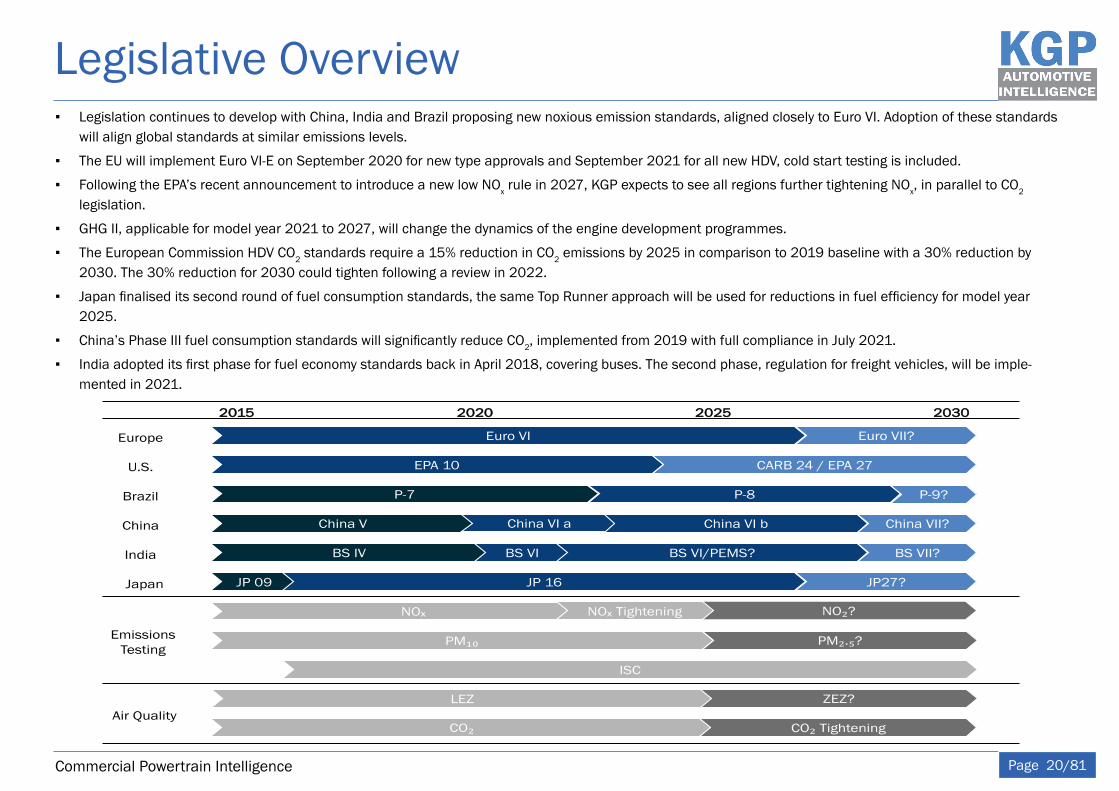

Legislative Overview

Commercial Powertrain Intelligence Page 20/81

▪ Legislation continues to develop with China, India and Brazil proposing new noxious emission standards, aligned closely to Euro VI. Adoption of these standards will align global standards at similar emissions levels.

▪ The EU will implement Euro VI-E on September 2020 for new type approvals and September 2021 for all new HDV, cold start testing is included.

▪ Following the EPA’s recent announcement to introduce a new low NOx rule in 2027, KGP expects to see all regions further tightening NOx, in parallel to CO2 legislation.

▪ GHG II, applicable for model year 2021 to 2027, will change the dynamics of the engine development programmes.

▪ The European Commission HDV CO2 standards require a 15% reduction in CO2 emissions by 2025 in comparison to 2019 baseline with a 30% reduction by 2030. The 30% reduction for 2030 could tighten following a review in 2022.

▪ Japan finalised its second round of fuel consumption standards, the same Top Runner approach will be used for reductions in fuel efficiency for model year 2025.

▪ China’s Phase III fuel consumption standards will significantly reduce CO2, implemented from 2019 with full compliance in July 2021.

▪ India adopted its first phase for fuel economy standards back in April 2018, covering buses. The second phase, regulation for freight vehicles, will be imple-mented in 2021.

Euro VI

22001155 22002200 22002255 22003300

Europe

EPA 10U.S.

P-7Brazil

China VChina

BS IVIndia

JP 09Japan

P-8

China VI a China VI b

BS VI

JP 16

Euro VII?

BS VI/PEMS?

NOₓ NO₂?

PM₁₀ PM₂.₅?

ISC

LEZ ZEZ?

NOₓ Tightening

CO₂ CO₂ Tightening

Emissions Testing

Air Quality

CARB 24 / EPA 27

P-9?

China VII?

BS VII?

JP27?

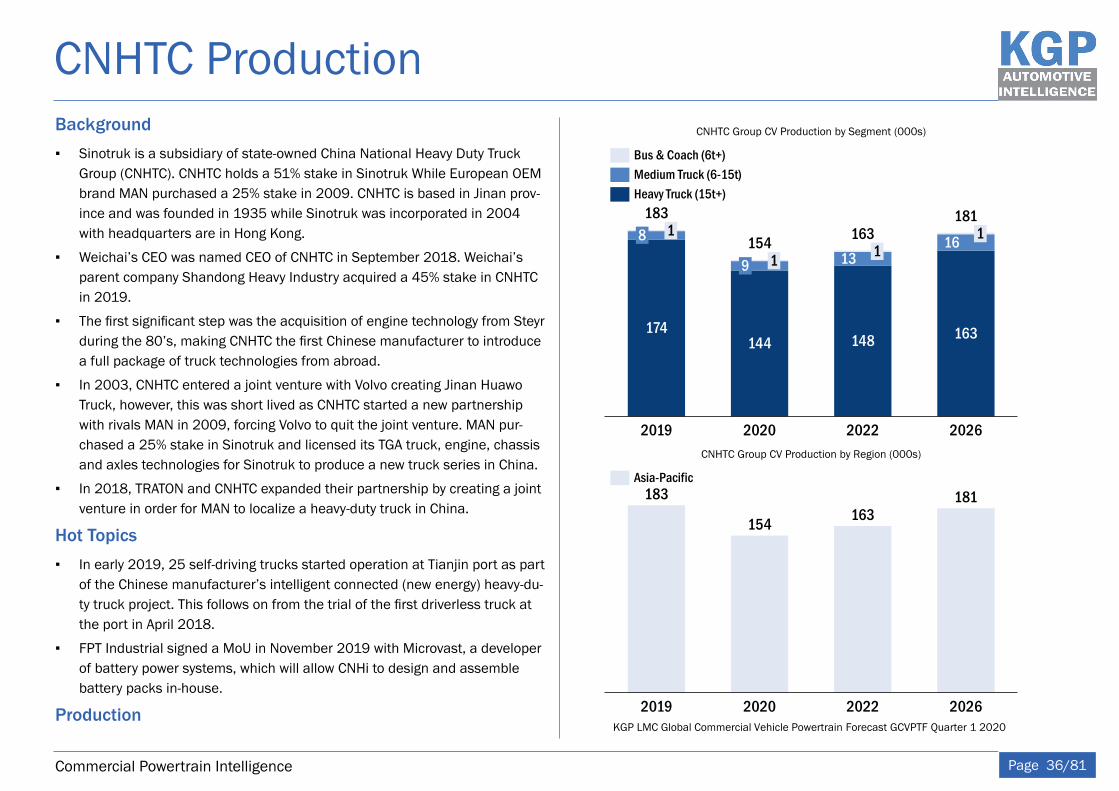

CNHTC Production

Commercial Powertrain Intelligence Page 36/81

Background ▪ Sinotruk is a subsidiary of state-owned China National Heavy Duty Truck

Group (CNHTC). CNHTC holds a 51% stake in Sinotruk While European OEM brand MAN purchased a 25% stake in 2009. CNHTC is based in Jinan prov-ince and was founded in 1935 while Sinotruk was incorporated in 2004 with headquarters are in Hong Kong.

▪ Weichai’s CEO was named CEO of CNHTC in September 2018. Weichai’s parent company Shandong Heavy Industry acquired a 45% stake in CNHTC in 2019.

▪ The first significant step was the acquisition of engine technology from Steyr during the 80’s, making CNHTC the first Chinese manufacturer to introduce a full package of truck technologies from abroad.

▪ In 2003, CNHTC entered a joint venture with Volvo creating Jinan Huawo Truck, however, this was short lived as CNHTC started a new partnership with rivals MAN in 2009, forcing Volvo to quit the joint venture. MAN pur-chased a 25% stake in Sinotruk and licensed its TGA truck, engine, chassis and axles technologies for Sinotruk to produce a new truck series in China.

▪ In 2018, TRATON and CNHTC expanded their partnership by creating a joint venture in order for MAN to localize a heavy-duty truck in China.

Hot Topics ▪ In early 2019, 25 self-driving trucks started operation at Tianjin port as part

of the Chinese manufacturer’s intelligent connected (new energy) heavy-du-ty truck project. This follows on from the trial of the first driverless truck at the port in April 2018.

▪ FPT Industrial signed a MoU in November 2019 with Microvast, a developer of battery power systems, which will allow CNHi to design and assemble battery packs in-house.

ProductionKGP LMC Global Commercial Vehicle Powertrain Forecast GCVPTF Quarter 1 2020

CNHTC Group CV Production by Region (000s)

181

2019 2020

163

2026

183

2022

154

Asia-Pacific

CNHTC Group CV Production by Segment (000s)

18

163144

2019

174

15419

2020

113

148

2022

116

2026

183163

181

Bus & Coach (6t+)Medium Truck (6-15t)Heavy Truck (15t+)

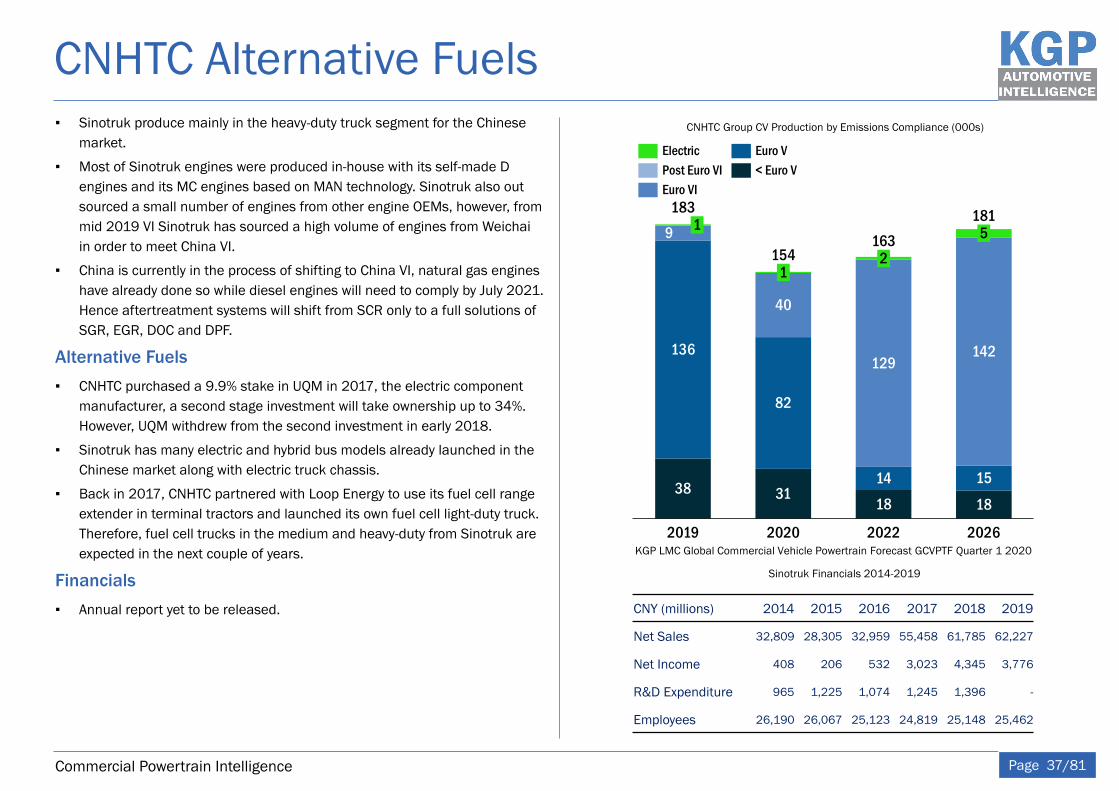

CNHTC Alternative Fuels

Commercial Powertrain Intelligence Page 37/81

▪ Sinotruk produce mainly in the heavy-duty truck segment for the Chinese market.

▪ Most of Sinotruk engines were produced in-house with its self-made D engines and its MC engines based on MAN technology. Sinotruk also out sourced a small number of engines from other engine OEMs, however, from mid 2019 VI Sinotruk has sourced a high volume of engines from Weichai in order to meet China VI.

▪ China is currently in the process of shifting to China VI, natural gas engines have already done so while diesel engines will need to comply by July 2021. Hence aftertreatment systems will shift from SCR only to a full solutions of SGR, EGR, DOC and DPF.

Alternative Fuels ▪ CNHTC purchased a 9.9% stake in UQM in 2017, the electric component

manufacturer, a second stage investment will take ownership up to 34%. However, UQM withdrew from the second investment in early 2018.

▪ Sinotruk has many electric and hybrid bus models already launched in the Chinese market along with electric truck chassis.

▪ Back in 2017, CNHTC partnered with Loop Energy to use its fuel cell range extender in terminal tractors and launched its own fuel cell light-duty truck. Therefore, fuel cell trucks in the medium and heavy-duty from Sinotruk are expected in the next couple of years.

Financials ▪ Annual report yet to be released. CNY (millions) 2014 2015 2016 2017 2018 2019

Net Sales 32,809 28,305 32,959 55,458 61,785 62,227

Net Income 408 206 532 3,023 4,345 3,776

R&D Expenditure 965 1,225 1,074 1,245 1,396 -

Employees 26,190 26,067 25,123 24,819 25,148 25,462

Sinotruk Financials 2014-2019

40

18

1

19

2019

136

82

38 31

2020

2

129

1418

2022

5

142

15

2026

183

154163

181

Electric< Euro VPost Euro VIEuro V

Euro VI

KGP LMC Global Commercial Vehicle Powertrain Forecast GCVPTF Quarter 1 2020

CNHTC Group CV Production by Emissions Compliance (000s)

Expected 26th april

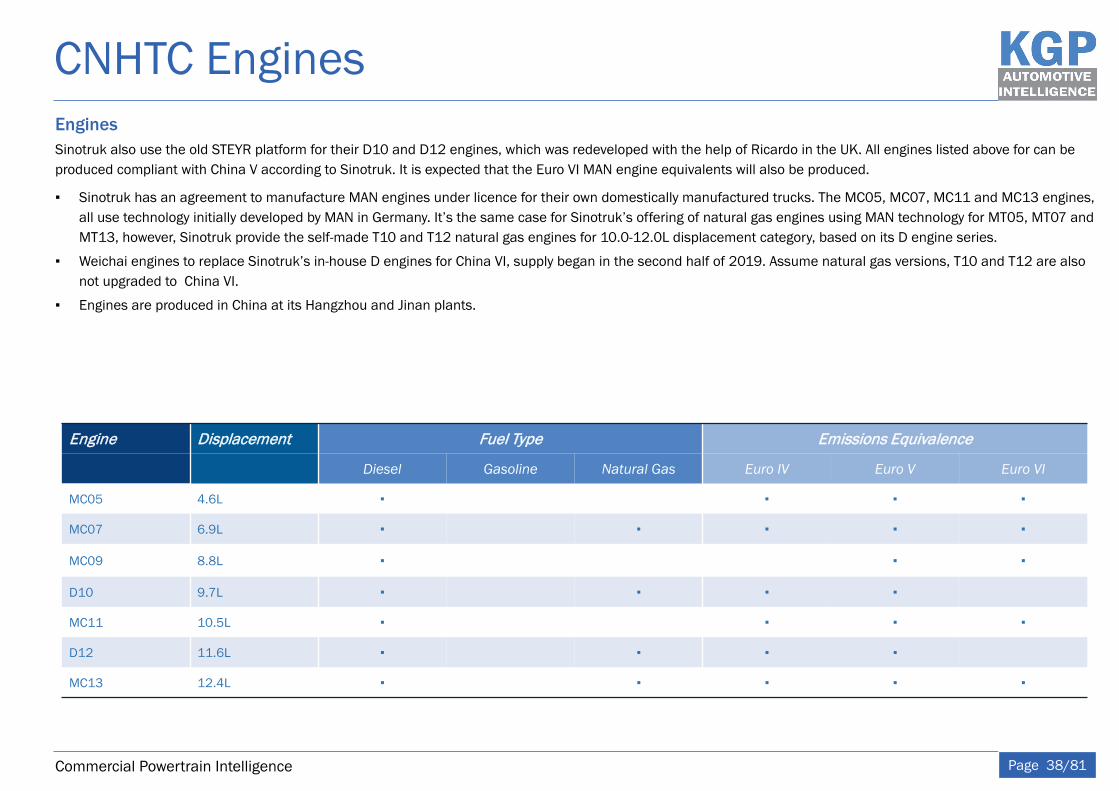

CNHTC Engines

Commercial Powertrain Intelligence Page 38/81

EnginesSinotruk also use the old STEYR platform for their D10 and D12 engines, which was redeveloped with the help of Ricardo in the UK. All engines listed above for can be produced compliant with China V according to Sinotruk. It is expected that the Euro VI MAN engine equivalents will also be produced.

▪ Sinotruk has an agreement to manufacture MAN engines under licence for their own domestically manufactured trucks. The MC05, MC07, MC11 and MC13 engines, all use technology initially developed by MAN in Germany. It’s the same case for Sinotruk’s offering of natural gas engines using MAN technology for MT05, MT07 and MT13, however, Sinotruk provide the self-made T10 and T12 natural gas engines for 10.0-12.0L displacement category, based on its D engine series.

▪ Weichai engines to replace Sinotruk’s in-house D engines for China VI, supply began in the second half of 2019. Assume natural gas versions, T10 and T12 are also not upgraded to China VI.

▪ Engines are produced in China at its Hangzhou and Jinan plants.

EEnnggiinnee DDiissppllaacceemmeenntt FFuueell TTyyppee EEmmiissssiioonnss EEqquuiivvaalleennccee

Diesel Gasoline Natural Gas Euro IV Euro V Euro VI

MC05 4.6L ▪ ▪ ▪ ▪

MC07 6.9L ▪ ▪ ▪ ▪ ▪

MC09 8.8L ▪ ▪ ▪

D10 9.7L ▪ ▪ ▪ ▪

MC11 10.5L ▪ ▪ ▪ ▪

D12 11.6L ▪ ▪ ▪ ▪

MC13 12.4L ▪ ▪ ▪ ▪ ▪

For further information please contact:

LMC [email protected] Oxford +44 1865 791737 Detroit +1 248 817-2100 Bangkok +662 264 2050 Shanghai +86 21 5283 3526

Knibb, Gormezano & [email protected] kgpauto.com UK +44 1332 856301

For experts by experts