powerpoint presentation storage/document… · ppt file · web view · 2015-07-02nearly every...

TRANSCRIPT

Executive remuneration trends

SARA, Cape Town24 June 2015

www.pwc.com

Presented by:Martin Hopkins

Trends update 2015PwC 2

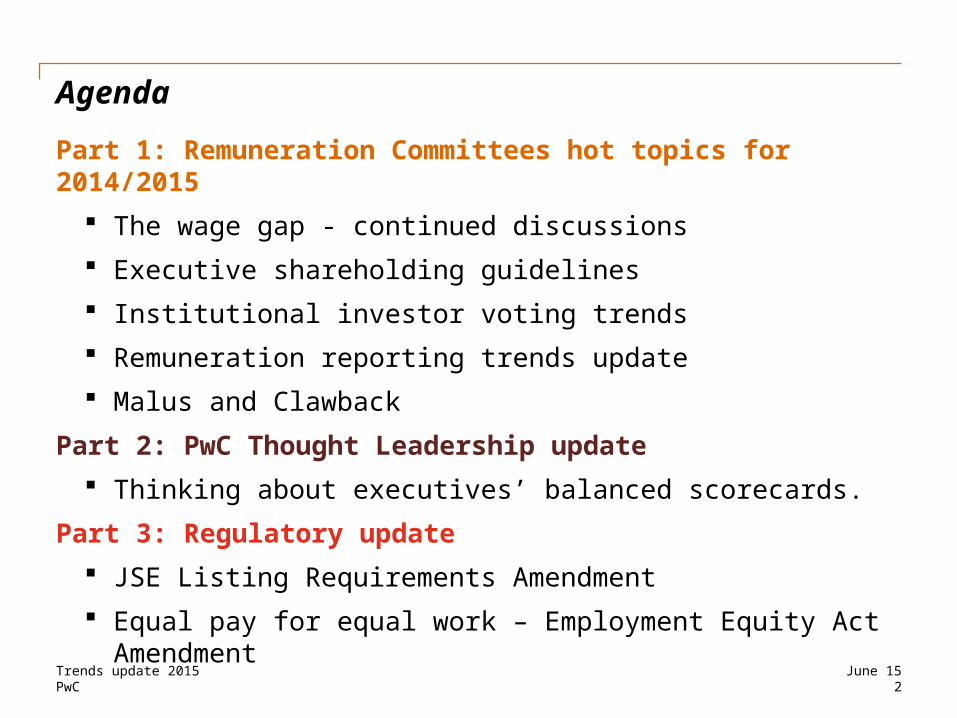

AgendaPart 1: Remuneration Committees hot topics for 2014/2015

The wage gap - continued discussions Executive shareholding guidelines Institutional investor voting trends Remuneration reporting trends update Malus and Clawback

Part 2: PwC Thought Leadership update Thinking about executives’ balanced scorecards.

Part 3: Regulatory update JSE Listing Requirements Amendment Equal pay for equal work – Employment Equity Act

AmendmentJune 15

Trends update 20153PwC

Remco hot topics

1What have Remcos been spending their time discussing in 2014, and what will be the hot topics for 2015?

June 15

Trends update 2015PwC 4

Hot topics – remuneration committees

1. Focusing on the wage gap

2. Executive shareholding guidelines

3. Pay for performance

4. Pay for risk and compliance staff (financial services)

5. Remuneration disclosure

6. Pressures from investors and shareholders

7. Malus and clawbackJune 15

Trends update 20155PwC

The wage gap – continued discussionsManaging shareholder sentiment

With continued focus in the media, particularly at present with Davos 2015, the need for positive communication with stakeholders surrounding the wage gap is increasing. Shareholder sentiment can be managed by numerous methods, including the calculation of an organisation’s Gini coefficient to illustrate that the inequality within the organisation is more favourable than the stated national.

June 15

Remco topic 1

Trends update 20156PwC

The wage gap - continued discussionsRemco topic 1

Worker payFocus on establishing a “living wage” for entry level workers which is sufficient to cover the cost of living in a frugal but dignified manner.

Executive pay Should be aligned to the market and linked to performance metrics which are of importance to shareholders

Squeezing the wage gap

June 15

Trends update 20157PwC

The wage gap - continued discussionsThere are three generally accepted methods of calculating the wage gap:

June 15

CEO vs. average of entry level employees

CEO vs. average of all employee pay excluding the executive committee

Gini coefficient considered to be the most scientifically accurate

Remco topic 1

1

2

3

Trends update 20158PwC

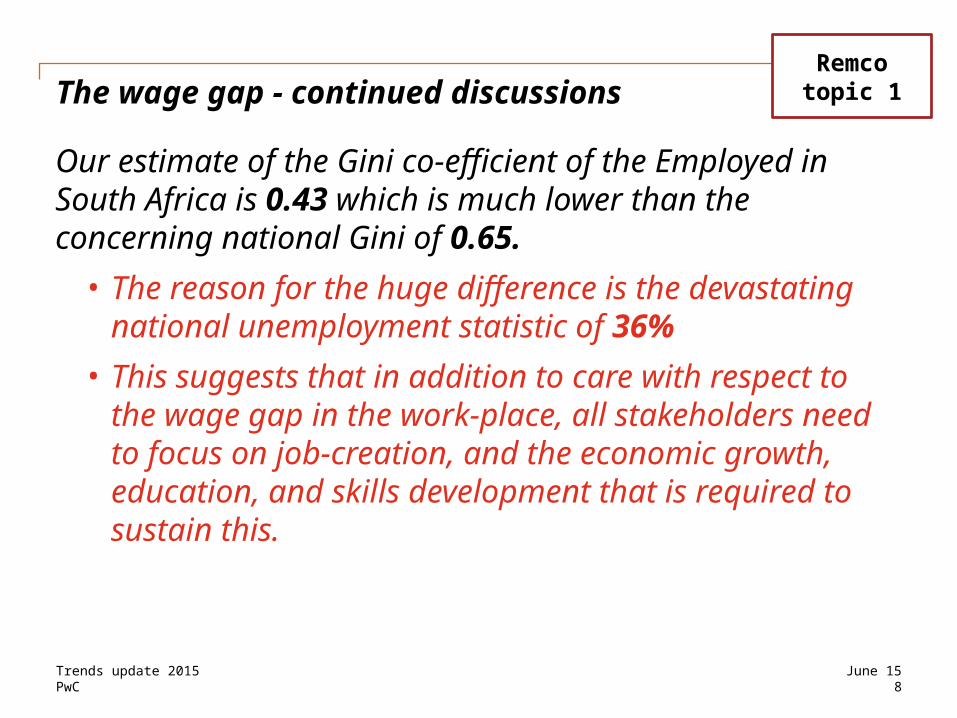

The wage gap - continued discussions

Our estimate of the Gini co-efficient of the Employed in South Africa is 0.43 which is much lower than the concerning national Gini of 0.65.

• The reason for the huge difference is the devastating national unemployment statistic of 36%

• This suggests that in addition to care with respect to the wage gap in the work-place, all stakeholders need to focus on job-creation, and the economic growth, education, and skills development that is required to sustain this.

Remco topic 1

June 15

Trends update 20159PwC

The wage gap - continued discussions

The reduction of inequality should remain a top priority, with focus on a living wage for entry-level workers.However, managing the wage gap could also include:

• investigations into innovative ways in which a company may be able to assist workers in addressing their most pressing basic financial concerns; and

• the creation of jobs to address the problem of unemployment within the country.

Remco topic 1

June 15

Trends update 201510PwC

The pay ratio provision in the Dodd-Frank ActUSA Section 953(b) of the Dodd-Frank Consumer Protection and Wall Street Reform Act (Dodd-Frank Act), known as the “pay ratio provision,” requires the Securities and Exchange Commission (SEC) to write rules to implement a requirement that

public companies disclose the ratio between the total compensation of a company’s CEO and the median compensation of all other employees.

According to the proposals released by the SEC, a firm will be able to choose its own methodology to calculate worker median pay, including statistical sampling.

Trends update 2015 May 7, 2023June 15

Trends update 201511PwC

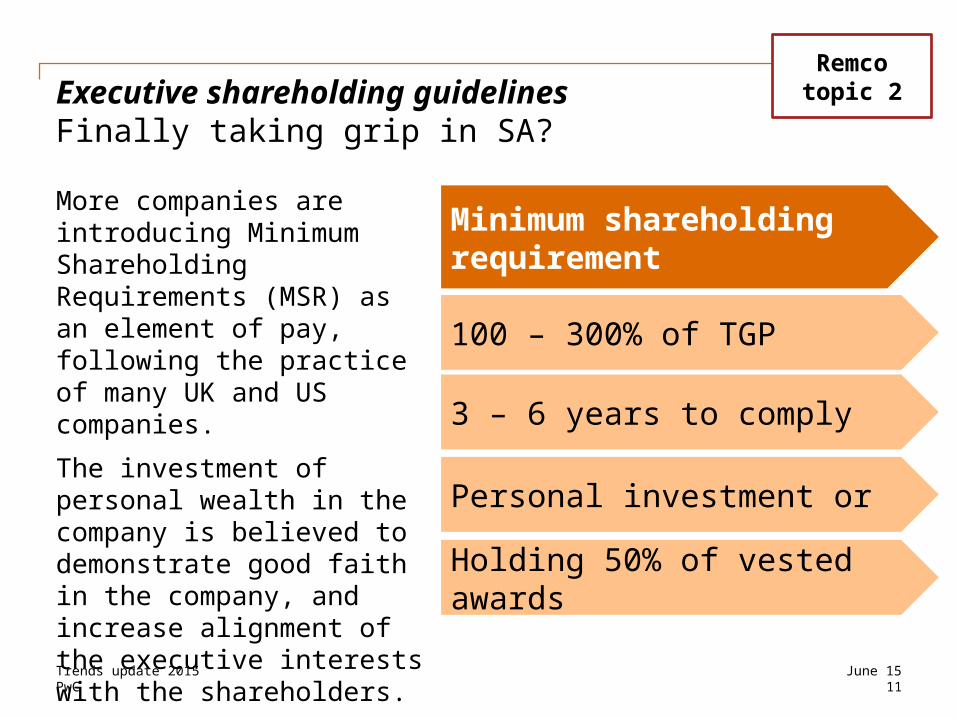

More companies are introducing Minimum Shareholding Requirements (MSR) as an element of pay, following the practice of many UK and US companies.The investment of personal wealth in the company is believed to demonstrate good faith in the company, and increase alignment of the executive interests with the shareholders.

Minimum shareholding requirement

100 – 300% of TGP

3 – 6 years to comply

Personal investment or

Holding 50% of vested awards

June 15

Executive shareholding guidelines Finally taking grip in SA?

Remco topic 2

Trends update 201512PwC

Pay plan supportThere was a season-over-season increase in the number of pay plans that failed to receive majority shareholder support.

“Say-on-pay”Overall, shareholders continued to support “say-on-pay” proposals at high levels.8 in 10 directors surveyed agree that there has been an increase in the influence of proxy advisory firms.

Shareholder dialogueNearly three-quarters of directors agree that “say-on-pay” has prompted directors to change the way they communicate about compensation.

Two thirds of directors don’t believe that “say-on-pay” has effected a “right-sizing” of CEO compensation.

2014123 plans 8 in 10

directors agree say-on-pay has changed their view on compensation disclosures

June 15

2013104 plans

¾ of directors agree that say-on-pay has increased shareholder dialogue

Remco topic 3Institutional investor voting trends

Proxy Pulse* – USA voting trends

Remco topics 3,5,6

Trends update 201513PwC

June 15

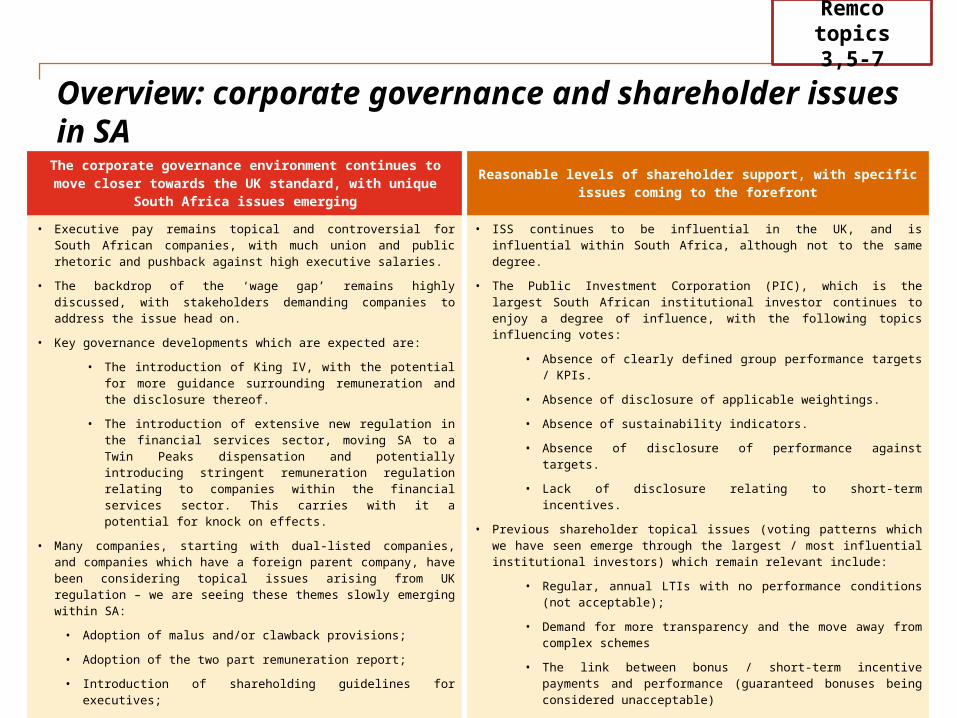

Overview: corporate governance and shareholder issues in SA

Remco topics 3,5-7

The corporate governance environment continues to move closer towards the UK standard, with unique

South Africa issues emergingReasonable levels of shareholder support, with specific

issues coming to the forefront

• Executive pay remains topical and controversial for South African companies, with much union and public rhetoric and pushback against high executive salaries.

• The backdrop of the ‘wage gap’ remains highly discussed, with stakeholders demanding companies to address the issue head on.

• Key governance developments which are expected are:

• The introduction of King IV, with the potential for more guidance surrounding remuneration and the disclosure thereof.

• The introduction of extensive new regulation in the financial services sector, moving SA to a Twin Peaks dispensation and potentially introducing stringent remuneration regulation relating to companies within the financial services sector. This carries with it a potential for knock on effects.

• Many companies, starting with dual-listed companies, and companies which have a foreign parent company, have been considering topical issues arising from UK regulation – we are seeing these themes slowly emerging within SA:

• Adoption of malus and/or clawback provisions;

• Adoption of the two part remuneration report;

• Introduction of shareholding guidelines for executives;

• Quality of disclosure of pay versus performance.

• ISS continues to be influential in the UK, and is influential within South Africa, although not to the same degree.

• The Public Investment Corporation (PIC), which is the largest South African institutional investor continues to enjoy a degree of influence, with the following topics influencing votes:

• Absence of clearly defined group performance targets / KPIs.

• Absence of disclosure of applicable weightings.

• Absence of sustainability indicators.

• Absence of disclosure of performance against targets.

• Lack of disclosure relating to short-term incentives.

• Previous shareholder topical issues (voting patterns which we have seen emerge through the largest / most influential institutional investors) which remain relevant include:

• Regular, annual LTIs with no performance conditions (not acceptable);

• Demand for more transparency and the move away from complex schemes

• The link between bonus / short-term incentive payments and performance (guaranteed bonuses being considered unacceptable)

• It should be noted that in some instances proxy voting within South Africa is approached in a formulaic manner, and for structures which South African shareholders may be unfamiliar with, extensive shareholder engagement is vital to help them understand the rationale for the approach taken and to avoid principle-based ‘no’ votes by shareholders who do not fully understand principles applied.

Trends update 2015PwC 14

Investor activism - from the mouths of proxy votersWhat are shareholder activists looking for?• They want to see the potential value a proposal could

unlock• They want to know what precedent exists for it – how has

it worked at companies which are in similar situations?• They want constructive meetings with company reps –

sometimes egos can prevent reasonable solutions and result in a lack of support Also, they expect the representative to have intimate knowledge of the subject matter (CEO vs. Chair of Remco)

• They expect boards to regularly look at their company as they think an activist would. “If they see a good idea, they should do it. If they see a bad idea, they should document their reasons. Then they should tell these things to their investors.”

“If a board is doing its job, there’s no room for an activist.”

June 15

Remco topic 6

Trends update 2015PwC

15

“Remuneration policy should provide greater detail and disclosure – such as stretch/target hurdles and criteria thereof”

“Lack of disclosure of weightings, indicators and targets”

“Insufficient detail around specific short and long term executive performance targets”

“No clearly defined group performance targets”

“Link between company performance and remuneration levels is not clear”

“Mix of remuneration appears unduly weighted towards share based pay”

Institutional investor voting trendsWhy are institutional investors voting “no”?

Remco topics 3,5,6

June 15

Trends update 201516PwC

Shareholders are demanding more information around the quantum and mix of executive pay in different scenarios of company performance, i.e. • expected (on-target)

performance, • below expected

performance and • exceeding expected

(stretch) performance June 15

Minimum On-target Stretch0

2

4

6

8

10

12

CEO potential pay

ZAR

mill

ions

Remuneration reporting trends updateThe visual representation of pay linked to performance

Remco topics 3,5,6

Belo

w

expe

cted

pe

rfor

man

ce At e

xpec

ted

perf

orm

ance

Abov

e ex

pect

ed p

erfo

rman

ce

Trends update 201517PwC

June 15

Remuneration reporting trends updateWhat are the forces driving remuneration reporting within South Africa?

Remco topic 5

Belo

w

expe

cted

pe

rfor

man

ce At e

xpec

ted

perf

orm

ance

Abov

e ex

pect

ed p

erfo

rman

ce

Remuneration Reporting

within South Africa

Regulatory environment in

South Africa- Companies

Act- Banks Act

- King III

Regulatory enviornment in

influential jurisdictions

Institutional investors

(shareholder activism) both in South Africa

and other influential

jurisdictions

Public perception

Integrated Reporting movement

Trends update 201518PwC

June 15

Remuneration reporting trends updateCall to action and shareholder expectations

Remco topics 5,6

Belo

w

expe

cted

pe

rfor

man

ce At e

xpec

ted

perf

orm

ance

Abov

e ex

pect

ed p

erfo

rman

ce

• It is increasingly expected that remuneration committees get involved with the drafting of remuneration reports, and have enough understanding of the policies and processes within the company to be able to effectively translate and explain them.

• In terms of content, there is a growing expectation from shareholders for companies to provide more comprehensive disclosures with regards to STI and LTI, particularly in respect of performance conditions and targets.

• In this regard, balance can be struck between protecting what may be considered “commercially sensitive information” and providing adequate detail.

• In addition, the principles of integrating reporting should be used to contextualise the remuneration received during a financial year, in light of the organisation, it’s performance and the creation of value.

Trends update 201519PwC

The inclusion of malus and clawback conditions in incentive plans is an evolving practice both in SA and globally, with some calls from institutional shareholders to introduce clawback provisions

Unclear exactly where the market will settle in striking the right balance in protecting the interests of shareholders without undermining the effectiveness of incentive plans in motivating and rewarding key management

UK model of 2 year post-vesting holding period after the 3 year vesting period could alleviate some of these concerns Malus provisions would also apply during the vesting period

Evolving practice

Post-vesting holding

Striking a balance

June 15

Malus and clawbackWhere is the South African market?

Remco topic 7

Trends update 2015PwC 20

The malus conditions need to be clearly defined and typically cover:

Malus and clawbackWhere is the South African market?

Remco topic 7

June 15

Material misstatement of financial results for any financial

year

Material financial loss or under-

performance of a business unit that could have been

risk-managed

Error or material misstatement leading to an

overpayment of an incentive amount

Employee misconduct,

including regulatory or

other breaches

Concerns regarding an employee's

conduct, capability or performance

Actions leading to reputational

damage

Deterioration in the financial health of the

company leading to severe financial

constraint

Trends update 201521PwC

PwC Thought Leadership update

2June 15

• Environmental & Social Investing• Boards of the Future• Board Priorities and Practices• Balanced Scorecards for Executives

Trends update 201522PwC

Environmental & social investing

• United Nations’ Principles for Responsible Investment Initiative (“PRI”). Criteria considered include:- Environmental - Social- Governance

• Link to executive remuneration- Financial capital (KPIs)- Natural capital (e-KPIs)

June 15

Trends update 201523PwC

Boards of the future

Require the right expertise, experience & diversity

June 15

Not very important Somewhat important Very important

0 20 40 60 80100

Humanresources expertise

International expertise

Legal expertise

Racial diversity

Gender diversity

Marketing expertise

Technology/digital media expertise

Risk management expertise

Operational expertise

Industry expertise

Financial expertise1% 6%

26%

30%

32%

46%

51%

46%

49%

56%

28%

49%

93%

72%

68%

65%

41%

35%

37%

28%

21%

45%

22%

13%

14%

17%

23%

23%

27%

29%

2%

3%

2%

Trends update 201524PwC

Boards of the future : gender diversity

June 15

Fig 2 Racial diversity Fig 3 Gender diversity

Trends update 201525PwC

IT risks

Executive compensation

Director communicatio

n

CEO succession plan

Company tax matters

Corporate social

responsibility

Board priorities and practices

June 15

Trends update 201526PwC

Thinking about executives’ balanced scorecardsPwC 18th annual CEO survey

June 15

77% of CEO’s plan to adopt a talent diversity strategy

61% of CEO’s prioritize skills and talent retention

FOCUS: Mix of talent and ability to alter the mix – driven by applying capabilities in more innovative ways

Trends update 201527PwC

Regulatory update

3June 15

• JSE Listings Requirements• Equal pay for equal work• International trends

Trends update 2015PwC 28

01

02

03

Schedule 14 explicitly states that a scheme may not purchase its securities during a prohibited period unless done so in terms of the repurchase agreement.

This is problematic for companies which are subject to extended closed periods.

Schedule 14 has been amended to introduce section 14.9(e) that allows for a repurchase agreement for the purchase of shares during a closed period to be pre-approved by the JSE.

Text to go here to go here to go here to go here to go here to

JSE Listings Requirements - Schedule 14 Amendment

June 15

29PwC

“Equal pay for equal work” – the Employment Equity Act AmendmentThe South African Department of Labour published the Code of Good Practice on Equal Pay for Work of Equal Value.

• The onus is on the employer to prove that the differentiation is fair based on factors such as qualifications, skills and or responsibilities once the employee has substantiated the income differential.

• Employers should therefore take steps to ensure that they eliminate differences in remuneration between employees who perform the same or substantially the same work of equal value.

Trends update 2015 June 15

Work of equal value is defined to include work that is the same or substantially the same

Trends update 2015PwC 30

Objective appraisals of jobs

Robust performance management system

Consistent and indiscriminate application of the remuneration policy

Ways of managing performance ratings should be defensible

01 02

03

04 Address

inequalities found without reducing remuneration of employees, to bring about equal remuneration

05

Equal Pay for Equal work – Best Practice Recommendations

June 15

Trends update 201531PwC

Regulatory update - International

European Union• CRD IV

◦ 1:1 limit on the ratio of variable to guaranteed without shareholder approval and 2:1 with shareholder approval

United Kingdom• Corporate Governance Code

◦ Inclusion of clawback and malus provisions for all elements of variable remuneration

◦ Non-executive directors should not receive share options or other performance-related pay

South Africa• Draft Code of Good Practice on Equal Pay for Work of Equal Value• FSB’s governance and risk management framework for Insurers

June 15

Questions?

“The information contained in this publication by PwC is provided for discussion purposes only and is intended to provide the reader or his/her entity with general information of interest. The information is supplied on an “as is” basis and has not been compiled to meet the reader’s or his/her entity’s individual requirements. It is the reader’s responsibility to satisfy him or her that the content meets the individual or his/ her entity’s requirements. The information should not be regarded as professional or legal advice or the official opinion of PwC. No action should be taken on the strength of the information without obtaining professional advice. Although PwC take all reasonable steps to ensure the quality and accuracy of the information, accuracy is not guaranteed. PwC, shall not be liable for any damage, loss or liability of any nature incurred directly or indirectly by whomever and resulting from any cause in connection with the information contained herein.”

© PwC Inc. [Registration number 1998/012055/21](“PwC”). All rights reserved. PwC refers to the South African member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.co.za for further details.