power sector review of bangladesh - ebl securities october 29, 2017 ebl securities limited research...

TRANSCRIPT

Power Sector Review of Bangladesh

Present Scenario

111

No. of Power Plants Grid Capacity (MW)

15,821

Per Capita Generation (KWh)

433

Access to Electricity (%)

80%

Installed Capacity of

BPDB Power Plants

Gas 62.6%

HFO 20.5%

HSD 8.5%

Coal 1.8%

Hydro 1.7%

F.Oil 0.0%

Imported 4.8%

De-Rated Capacity*Without Captive

12,922 MW

Maximum Generation*as on 18 Oct 2017

9,507 MW

Forecast

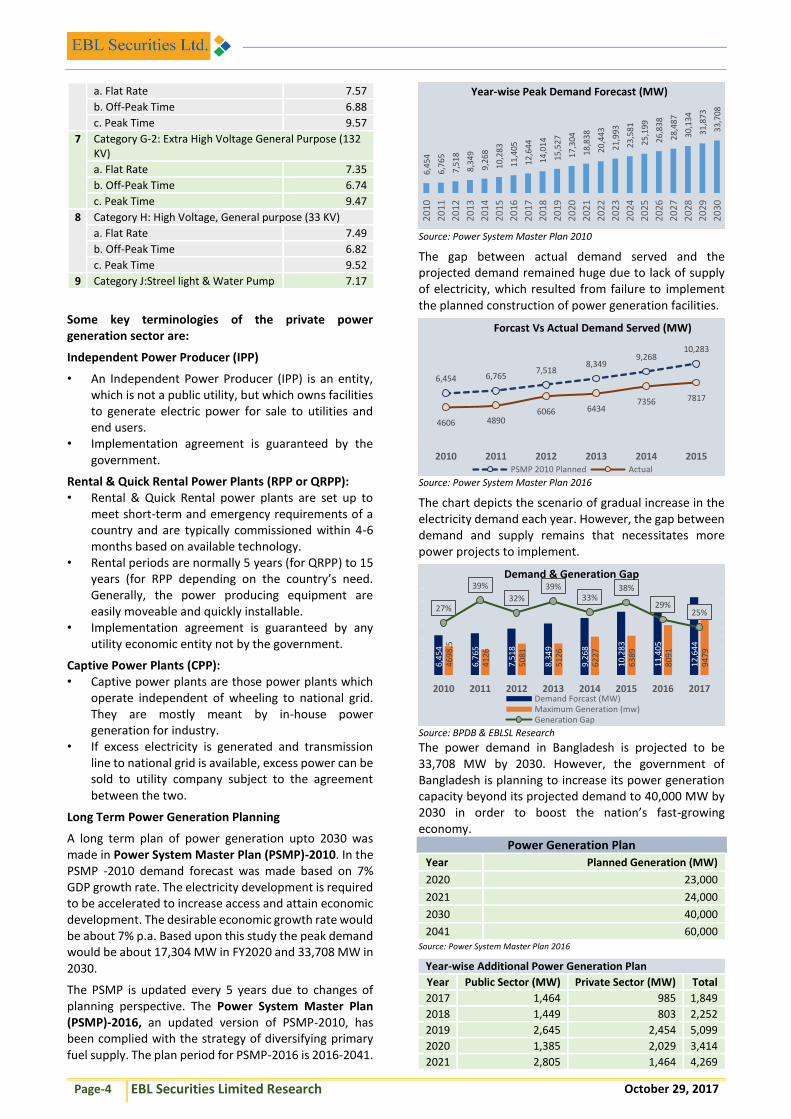

Year-wise Peak Demand Forecast (MW)2017 2020 2022 2025 2030

12,644 17,304 20,443 25,199 33,708

2020 2021 2030 2040

23,000

24,000

40,000

60,000

Power Generation Plan (MW)

Keeping pace with the growth of economy

Page-1 October 29, 2017

EBL Securities Limited Research

Power Sector Review of Bangladesh

Incessant supply of power and energy is the prerequisite for the progress of an economy. The importance of energy is even more supplementary in the context of Bangladesh, an emerging economy that has been experiencing rapid economic growth but also has been experiencing prolonged period of energy crisis. Electricity is the main form of energy that is tapped on both private and commercial scales in Bangladesh. However, the country is still at a very low level of electrification.

The government of Bangladesh (GOB) recognizes that the pace of power development has to be accelerated in order to achieve overall economic development targets of the country and avoid looming power shortages. To meet the increasing demand for Power, the government of Bangladesh has undertaken massive steps towards increasing the power supply in the short span of time by encouraging private sector power production as well as import of power from native countries. The government of Bangladesh has set a target to bring the whole country under electricity coverage by 2021.

The report contains major highlight on ongoing state of power supply in Bangladesh, major steps and new approvals of power supply as well as financial highlights of some listed power producing companies.

Present Structure of Power Sector in Bangladesh:

Apex Institution: Power Division, Ministry of Power, Energy & Mineral Resources (MPEMR)

Regulator: Bangladesh Energy Regulatory Commission (BERC)

Generation:

Bangladesh Power Development Board (BPDB)

Ashuganj Power Station Company Ltd. (APSCL)

Electricity Generation Company of Bangladesh (EGCB)

North West Power Generation Company Ltd. (NWPGCL)

Independent Power Producers (IPPs)

Transmission:

Power Grid Company of Bangladesh Ltd (PGCB)

Distribution

Bangladesh Power Development Board (BPDB)

Dhaka Power Distribution Company (DPDC)

Dhaka Electric Supply Company Ltd (DESCO)

West Zone Power Distribution Company (WZPDC)

North-West Zone Power Distribution Co. (NWZPDC)

Rural Electrification Board (REB) through Rural Co-operatives

Present Scenario of Power Generation in Bangladesh:

Power Generation Situation in Bangladesh

Installed Capacity (Excluding Captive) 13,621 MW

De-Rated Capacity 12,922 MW

Less: Maintenance and Shut Down 415 MW

Gas Shortage 1,415 MW

Low Water Level in Kaptai 0 MW

Net Generation Capacity 11,092 MW

Captive Power Generation Capacity 2,200 MW

Maximum Generation (18 Oct 2017) 9,507 MW

Source: Bangladesh Power Development Board (BPDB) website

Bangladesh Power Sector at a Glance 2009 2017 8 Years’ Addition

Power Plants (No) 27.0 111.0 84.0

Expired Plants 0.0 3.0 3.0

Grid Capacity (MW) 4,942.0 15,821 (Including Captive) 10,879.0

Highest Generation (MW) 3,268 (6 Jan 2009) 9,507 (18 Oct 2017) 6,239.0

Power Import (MW) 0.0 660.0 660.0

Total Consumers (million) 10.8 26.7 15.9

Transmission Line (Ckt Km) 8,000.0 10,436.0 2,436.0

Distribution Line (Km) 260,000.0 412,000.0 152,000.0

Grid sub-station capacity (MVA) 15,870.0 30,993.0 15,123.0

Access to Electricity (%) 47.0 80.0 33.0

Per Capita Generation (KWh) 220.0 433 (Inc. captive) (30 June 2017) 213.0

ADP allocation (BDT in bn) 26.8 225.8 199.0

System Loss (%) 16.9 12.2 -4.7 Source: http://www.powerdivision.gov.bd (19 September 2017)

Ministry of Power, Energy and Mineral Resources

Power Division Energy & Mineral Resources Division BERC

Power Cell

CEI BPDB REB DPDC DESCO

PGCB APSCL EGCB WZPDCL NWPGCL

IPPs

Page-2 October 29, 2017

EBL Securities Limited Research

Break down of Installed Generation Capacity (MW)

Public sector accounts for highest power generation of the country while the contribution from private sector is also on the rise driven by the government policy toward increasing power producing capacity at the earliest by encouraging more private investment in this sector. Out of the total 15,821 MW power generation capacity of the country as on 30 September 2017, public sectors capacity stands at 7,476 MW, which is 47% of the total power generation capacity including captive power plants (55% of total excluding captive power projects) and private sector capacity stands at 6145 MW (including 660 MW power import), which is 39% of the total power generation capacity of the country (45% of total excluding captive power projects). Besides, power generation capacity of the captive power projects now stands at 2,200 MW (14% of total capacity).

Source: BPDB & EBLSL research (as on 30 September, 2017)

Since the country’s overall economic progress relies significantly on uninterrupted supply of power, the sectors has always received special attention from the government. However, the country’s power capacity increased significantly since the present ruling party took charge of the government in 2009 and last nine years’ CAGR of the power sector capacity was 10.6% (excluding captive power capacity).

Source: BPDB annual report and website

Primary Fuel Supply Scenario

Up until 2016, the major consideration of energy source for power generation was Natural gas, which is now being shifted to Coal and LNG, as the deposited amount of natural gas remains uncertain. Due to no significant gas discovery in recent years, the country is facing shortage of gas supply that ultimately discouraging gas based power supply; therefore the government is now looking for big power plants to be run on Coal or other types of Energy in the near future.

Import of LNG by 2018 and implementation of LNG based power project may mitigate the ongoing crisis and can be an alternative low cost fuel for producing electricity. The government have taken initiatives to supply 1000 MMCFD of Regasified LNG into the Gas Grid using 2 Floating Storage and Regasification Units (FSRU), off the coast of Maheshkhali.

Furnace Oil, HFO and Diesel based plants are the best available alternatives for producing electricity. However, Oil based power plants are highly expensive compared to Gas based plants. So, Oil based plants are only short term solution to mitigate the supply shortage of power within the shortest period of time.

Coal is next available alternative. It can be a near term option and can be indigenous or imported. However, Coal based power projects are highly debated as they might be harmful for environment. The government is encouraging coal based projects for mitigating looming electricity shortage and to reduce dependency on gas based expensive fuel oil based plants.

Nuclear power is the safe technology; no pollution; expected to be future Base Load option (power stations which can economically generate the electrical power needed to satisfy this minimum demand) but no significant improvement has been observed to generate nuclear based power in Bangladesh.

Capacity of BPDB Power Plants as on September 2017

Fuel Type

Installed Capacity

(MW) Total (%)

Derated Capacity

(MW)

Total (%)

Coal 250.00 1.84 % 170.00 1.32 %

F.Oil 0.00 0.00 % 0.00 0.00 %

Gas 8529.00 62.62 % 7936.00 61.41 %

HFO 2794.00 20.51 % 2792.00 21.61 %

HSD 1158.00 8.54 % 1134.00 8.78 %

Hydro 230.00 1.69 % 230.00 1.78 %

Imported 660.00 4.85 % 660.00 5.11 %

Total 13621.00 100.00 % 12922.00 100.00 %

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

200

0-0

1

200

1-0

2

200

2-0

3

200

3-0

4

200

4-0

5

200

5-0

6

200

6-0

7

200

7-0

8

200

8-0

9

200

9-1

0

201

0-1

1

201

1-1

2

201

2-1

3

201

3-1

4

201

4-1

5

201

5-1

6

201

6-1

7

Power Generation Capacity (Year-wise)

Installed Capacity (MW) Derated Capcity (MW)Maximum Generation (MW)

Typ

es o

f P

ow

er

Pla

nt

Bas

ed

on

Fu

el U

se Natural Gas Based

Furnace Oil Based

Heavy Fuel Oil Based

High Speed Diesel Based

Coal Fired

Hydro-Based

Page-3 October 29, 2017

EBL Securities Limited Research

Source: BPDB website & EBLSL Research

Business Opportunities for Private Sector in Electricity Generation

To encourage private sector for investment in the power sector of the country, the government of Bangladesh adopted several policies namely Private Sector Power Generation Policy of Bangladesh, 1996 (revised 2004) and Policy Guideline for Enhancement of Private Participation in the Power Sector, 2008. The government also took a pragmatic step to revise the Electricity Act 1910, which has been renamed as Electricity Act 2016, where adequate provisions has been kept to facilitate private companies to participate in developing the country’s power sector.

Tariff for Bulk Purchase of Power at Busbar

The power produced by the Independent Power Producer (IPP) is purchased (as per Power Purchase Agreement) by BPDB/DESA/REB or any large consumer EPZs. The Power Cell as the GOB agent indicates which organization will be the power purchaser at the time of issuance of Request for Proposal (RFP). Electricity generation technology, cost structure and tariff varies based on the types of fuel used. The tariff structure consists of two parts:

1. Capacity Payment: This covers debt service, return on equity, fixed operation and maintenance cost, insurance and other fixed costs. The capacity payment is further divided into an escalating and non-escalating portions. The capacity payment is linked to a certain level of availability of the power plant which is made known to the bidders at the time of issuance of RFP. The companies will be entitled to capacity payments even if the government doesn’t buy electricity from them.

2. Energy Payment: This covers the variable costs of operation and maintenance, including fuel. The payment are further divided into fuel component which are a pass-through and a non-fuel component which escalates. In case of pass-through energy payment agreements- respective company procures required fuel oil for its plants on their own and bills to BPDB for liquid fuel payment. It is mentionable here that, there is no impact of price fluctuation in international oil market on the profitability of private power generation companies as its costs are structured as a pass through item.

In the solicited bids, the bidders offer bulk power tariff based on the capacity payment and energy payment and also provide the equivalent levelized tariff over the

contract period, based on discount rate, tariff profile restriction and plant factor to be specified during the solicitation of bids. The evaluation will be based on the criteria to be provided in the RFP.

The sponsors of private power project are required to provide year wise tariff profile over the contract period in a manner that matches their annual debt service requirements.

Present Tariff Structure in the Electricity Generation Sector: Three types of tariffs are in operation in Bangladesh:

(i) Bulk or wholesale tariff---the rate at which BPDB purchases power from the generating entities;

(ii) Wheeling charges paid to PGCB; and

(iii) Retail Tariff---the rate at which the distribution companies sell to consumers

The Bulk or wholesale tariff varies based on the power plant types and fuel used.

Sponsor Fuel Tariff Range

(per KWH)

IPP/ Rental HFO 5.5-9.0

SIPP/Quick Rental HFO 14-20.5

IPP/SIPP/ Rental/ Quick Rental HSD 21.5-29.8

IPP/SIPP/ Rental/ Quick Rental Gas 1.45-5.1

Public Gas 1.6-3.35

Public HSD 15.8-27.9

BPDB Hydro 1.1

BPDB Wind 41.43

BPDB Gas 0.94-2.56

BPDB Coal 8.93

BPDB HFO 17.5-22.2

BPDB Diesel 33.3-261.5 Source: BPDB annual report and EBLSL estimates

Retail Tarif: Present retail tariff in power sector is as presented below:

Consumer Category Energy Charges (BDT/KWh)

1

Category -A: Residential

Life Line: 1-50 Units 3.33

a. First step : from 00 to 75 units 3.80

b. Second Step: From 76 to 200 units 5.14

c. Third Step: From 201 to 300 units 5.36

d. Fourth Step: 301 to 400 units 5.63

e. Fifth Step: From 401 to 600 units 8.70

6. Sixth Step: From 601 to above 9.98

2 Category -B: Agricultural pumping 3.82

3

Category C: Small Industries

a. Flat Rate 7.66

b. Off-Peak Time 6.90

c. Peak Time 9.24

4 Category D: Non-residential (Light & power)

5.22

5

Category E: Commercial & Office

a. Flat Rate 9.80

b. Off-Peak Time 8.45

c. Peak Time 11.98

6

Category F: Medium Voltage, Generation Purpose (11 KV)

Coal1.8%

F.Oil0.0%

Gas62.6%

HFO20.5%

HSD8.5%

Hydro1.7%

Imported4.8%

I n s t a l l e d C a p a c i t y o f B P D B P o w e r P l a n t s

Coal F.Oil Gas HFO HSD Hydro Imported

Page-4 October 29, 2017

EBL Securities Limited Research

a. Flat Rate 7.57

b. Off-Peak Time 6.88

c. Peak Time 9.57

7

Category G-2: Extra High Voltage General Purpose (132 KV)

a. Flat Rate 7.35

b. Off-Peak Time 6.74

c. Peak Time 9.47

8

Category H: High Voltage, General purpose (33 KV)

a. Flat Rate 7.49

b. Off-Peak Time 6.82

c. Peak Time 9.52

9 Category J:Streel light & Water Pump 7.17

Some key terminologies of the private power generation sector are:

Independent Power Producer (IPP)

• An Independent Power Producer (IPP) is an entity, which is not a public utility, but which owns facilities to generate electric power for sale to utilities and end users.

• Implementation agreement is guaranteed by the government.

Rental & Quick Rental Power Plants (RPP or QRPP): • Rental & Quick Rental power plants are set up to

meet short-term and emergency requirements of a country and are typically commissioned within 4-6 months based on available technology.

• Rental periods are normally 5 years (for QRPP) to 15 years (for RPP depending on the country’s need. Generally, the power producing equipment are easily moveable and quickly installable.

• Implementation agreement is guaranteed by any utility economic entity not by the government.

Captive Power Plants (CPP): • Captive power plants are those power plants which

operate independent of wheeling to national grid. They are mostly meant by in-house power generation for industry.

• If excess electricity is generated and transmission line to national grid is available, excess power can be sold to utility company subject to the agreement between the two.

Long Term Power Generation Planning

A long term plan of power generation upto 2030 was made in Power System Master Plan (PSMP)-2010. In the PSMP -2010 demand forecast was made based on 7% GDP growth rate. The electricity development is required to be accelerated to increase access and attain economic development. The desirable economic growth rate would be about 7% p.a. Based upon this study the peak demand would be about 17,304 MW in FY2020 and 33,708 MW in 2030.

The PSMP is updated every 5 years due to changes of planning perspective. The Power System Master Plan (PSMP)-2016, an updated version of PSMP-2010, has been complied with the strategy of diversifying primary fuel supply. The plan period for PSMP-2016 is 2016-2041.

Source: Power System Master Plan 2010

The gap between actual demand served and the projected demand remained huge due to lack of supply of electricity, which resulted from failure to implement the planned construction of power generation facilities.

Source: Power System Master Plan 2016

The chart depicts the scenario of gradual increase in the electricity demand each year. However, the gap between demand and supply remains that necessitates more power projects to implement.

Source: BPDB & EBLSL Research

The power demand in Bangladesh is projected to be 33,708 MW by 2030. However, the government of Bangladesh is planning to increase its power generation capacity beyond its projected demand to 40,000 MW by 2030 in order to boost the nation’s fast-growing economy.

Power Generation Plan

Year Planned Generation (MW)

2020 23,000

2021 24,000

2030 40,000

2041 60,000 Source: Power System Master Plan 2016

Year-wise Additional Power Generation Plan

Year Public Sector (MW) Private Sector (MW) Total

2017 1,464 985 1,849

2018 1,449 803 2,252

2019 2,645 2,454 5,099

2020 1,385 2,029 3,414

2021 2,805 1,464 4,269

6,4

54

6,7

65

7,5

18

8,3

49

9,2

68

10

,28

3

11

,40

5

12

,64

4

14

,01

4

15

,52

7

17

,30

4

18

,83

8

20

,44

3

21

,99

3

23

,58

1

25

,19

9

26

,83

8

28

,48

7

30

,13

4

31,8

73

33

,70

8

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

Year-wise Peak Demand Forecast (MW)

6,454 6,7657,518

8,3499,268

10,283

4606 48906066 6434

7356 7817

2010 2011 2012 2013 2014 2015

Forcast Vs Actual Demand Served (MW)

PSMP 2010 Planned Actual

6,45

4

6,76

5

7,51

8

8,34

9

9,26

8

10,2

83

11,4

05

12,6

44

4698

.5

4126

5081

5126

6227

6389

8091

9479

27%

39%

32%

39%33%

38%

29%25%

0.0 0%

5.0 0%

10. 00%

15. 00%

20. 00%

25. 00%

30. 00%

35. 00%

40. 00%

45. 00%

2010 2011 2012 2013 2014 2015 2016 2017

0

2,0 00

4,0 00

6,0 00

8,0 00

10, 000

12, 000

14, 000

Demand & Generation Gap

Demand Forcast (MW)Maximum Generation (mw)Generation Gap

Page-5 October 29, 2017

EBL Securities Limited Research

Tender in Progress

Sector # of Power Plant Installed Capacity (MW)

Public 6 866

Private 38 6,738

Total 44 7,604

Contact Sign (New Power Plant)

Project Type

No of Power Plant

Capacity Already Commissioned

Government 42 11,124 3,917 (27)

Rental 20 1,653 1,653 (20)

IPP 38 6,947 2,005 (19)

Total 100 19,724 7,557 (66)

Under-Construction Power Plant

# of Power Plant Installed Capacity (MW)

Public 15 7,151

Private 19 4,710

Total 34 12,061

Source: http://www.powercell.gov.bd

Present Scenario of Power Sector Capacity Expansion Projects: Short Term Projects: The government of Bangladesh has been prioritizing on the capacity enhancement of the country’s electricity generation on immediate basis (but at high cost), for which it is perusing for some rental or quick rental basis power projects on private ownership basis as a short term solution. Moreover, to reduce the legislative delay, the government is also permitting some of the private sponsors on unsolicited bid, under special act, to set up power generation stations within the stipulated timeframe.

Under-construction Private Power Plants: A number of local and multination sponsors received permission for setting up power plants for which the construction work are on progress.

Some Upcoming Private Power Projects Plant Location Sponsor Fuel MW LOI Issued date Tenure Rate (BDT)

1. Meghnaghat, N.ganj Consortium of Summit Corp. Ltd. & GE

HFO/Diesel/ Gas

530-590

25 October 2017 22 Years 2.9546 (Gas); 5.478 (HFO),

12.6051 (Diesel)

2. Ashuganj, B.Baria* Midland Power Ltd. (SPCL) Diesel 150 09 August 2017 15 Years 8.2593

3. Keraniganj, Dhaka* APR Energy Ltd. Diesel 300 09 August 2017 05 Years 19.993

4. Keraniganj, Dhaka* Agrico International Project Ltd. Diesel (IPP) 200 09 August 2017 05 Years 19.6680

5. Jaluda, CTG* Acorn Infrastructure Service Ltd. HFO 100 09 August 2017 15 Years 8.2593

6. Noapara, Jessore* Bangla Trac Ltd. Diesel (IPP) 100 09 August 2017 05 Years 19.9930

7. Daudkandi, Comilla* Bangla Trac Ltd. Diesel (IPP) 200 09 August 2017 05 Years 19.9930

8. Bagura* Confidence Power Ltd. HFO (IPP) 113 09 August 2017 15 Years 8.3379

9. Chandpur* Desh energy Ltd. HFO (IPP) 200 09 August 2017 15 Years 8.3379

10. Laban Chora, Khulna*

Orion Power Rupsha Ltd. HFO (IPP) 105 09 August 2017 15 Years 8.3379

11 Kodda, Gazipur* Consortium of Summit Corporation Ltd. and Summit Power ltd.

HFO (IPP) 300 09 August 2017 15 Years 8.3379

12. Kodda, Gazipur Summit Technopolis Ltd, Dual Fuel (HFO & GAS)

149 08 September 2016 Purchase of plant

7.15 (HFO 2.80 (Gas)

13. GongaChora, Rangpur

Intraco Solar Power Ltd. Solar Power 30 16 March 2016 n/a 12.80

14. Mymensingh* United Enterprise and Company HFO 200 20 September, 2017

15 Years 8.4166

15. Jamalpur United Enterprise HFO 115 30 August 2017 15 Years 8.73

16. Ghorashal China Energy Engineering Group and Guangdong Power

Fuel Oil 210 re-powering

17. Anwara United Enterprise & Company Fuel Oil 300 16 March 2016 15 Years 14.70

18. Julda Acorn Fuel Oil 100 16 March 2016 15 Years 14.70

19. Patia Precision Energy Fuel Oil 100 16 March 2016 15 Years 14.70

20. Bhola India's Shapoorji Pallonji Infrastructure Capital Company

Dual Fuel 225 16 March 2016 n/a 3.98 cents/kWh

21. Gaibandha Beximco Power Limited and Xinjiang TBEA Sunoasis Co Ltd

Solar Power 200 03 August 2016 20 Years 12.0

22. Goainghat., Sylhet Sun Solar Power Plant Ltd Bangladesh and Japanese Iki Shoji Company Limited

Solar Power 05 03 August 2016 n/a 11.12

23. Khulna Harbin Electric International Co Ltd and Jiangsu Etern Company Limited, China

n/a 200-300

03 August 2016 n/a

24. Meghnaghat, N.ganj Reliance Power LNG 750 n/a

25. Shikalbaha, Ctg. Kaqrnaphuli Power Company HFO 110 05 July 2017 15 Years 8.2933

26. Panchaghar 8minutenergy Singapore Holdings 2 Pte Ltd

Solar Power 50 05 July 2017 20 10.66

Page-6 October 29, 2017

EBL Securities Limited Research

27. Chandpur Doreen Power HFO 115 15 May 2017 15 Years

28. Rangpur Confidence Cement and Confidence Steel

HFO 113 05 April 2017 15 Years 8.21

29. Bogra Confidence Cement and Confidence Steel

HFO 113 05 April 2017 15 Years 8.25

30. Thakurgaon EnergyPac Bangladesh HFO 115 05 April 2017

31. Meghnaghat Power Association HFO 104 05 April 2017

32. Chowmuhani Energy Prima Limited HFO 113 05 April 2017

33. Feni Lakdhanavi Ltd ., Sri Lanka HFO 114 05 April 2017 *Marked represent Fast track projects.

First Track Project of the Ministry of Power and Energy: The Power Division awarded contracts for the generation of 1,968 MW of fuel-based power to 12 unsolicited power projects to meet the country’s electricity demands next summer. The projects include the production of 800MW of diesel-based electricity at a high cost.

As per the government’s condition, the furnace-oil based IPPs would have to commence generation with nine

months (before May 9, 2018) and the diesel-based power plants will have to start generation within six months (February 16, 2018) from the date of receiving Letter of Intent (LOI). However, according to a report of local daily, most of the First Track Projects are not progressing satisfactorily to generate power before stipulated timeframe and the worst scenario is with the international companies.

Intermediate & Long Term Projects:

Renewable Energy: Presently Bangladesh generates 233MW of electricity from Renewable energy sources. The government plans to meet 10% of the total electricity generation from Renewable Energy sources by 2020. For instance, some of the solar projects include a 500 MW Solar Power energy project in Feni, 100MW Solar Photo Voltaic based Grid-Connected Power Generation Plant which is also in Feni, 200 MW Solar Park in Tekhnaf, 200MW Grid-tied Solar PV Power Plant in Latshal, 60MW and 30MW windmill energy project in Cox’s Bazar and a 1 MW garbage based power plant in Keraniganj and other areas.

Currently, there are several other renewable energy development projects running in Bangladesh. If all the projects progress in accordance with their plan, there will

be a total of 2,651 MW of electricity generation from the expansion into renewable energy.

Planned Electricity Generation for Renewable Energy

Source 2017 2018 2019 2020 2021 2022

Solar 421 237 195 203 208 1,264

Wind 250 350 350 200 200 1,350

Biomass 6 6 6 6 6 30

Biogas 1 1 1 1 1 5

Hydro 2 0 0 0 0 2

Total 680 594 552 410 415 2,651

Coal Based Mega Projects: The coal has been considered as the prime source of power generation for the long term option in PSMP. As a way of low-cost sustainable power generation option, the government is planning to increase Coal fired power projects in coming years. Government plans to set up 25 coal-fired power plants by 2022, to generate 23,692 MW, in order to meet rising

Progress of the First Track Projects

Source: News extracted from the Independent (BD) on 26 October 2017 and graphical representation by EBLSL Research Team

Page-7 October 29, 2017

EBL Securities Limited Research

electricity demand. Of the total, 16 will be built by the public sector and 9 by the private sector. The government plans to increase share of coal based power from only

1.3% to 21% by 2020 (end of the Seventh Plan) and subsequently to 50% by FY2030.

Some Upcoming Coal Based Power Projects

Name Capacity Executing Agency Expected Commencement

Moittri Super Thermal Power Project 1320 MW Bangladesh -India JV June,2019

Matarbari Coal Based Power Pant 1200 MW CPGCBL June, 2022

Paira Coal Based Power Plant 1320 MW NWPGCL-China JV December, 2019

G to G Coal Based Power Plant 1320 MW Bangladesh –S. Korea JV June, 2023

Moheshkhali Coal Based Power Plant 1200 MW BPDB June,2024

Moheshkhali Coal Based Power Plant 1320 MW Bangladesh –Malaysia JV June, 2022

Ashuganj 2x660 MW Power Plant 1320 MW APSCL

1,320 MW Coal Based Power Plant 1320 MW BPDB –CHDHK, China JV June, 2021

Banshkhali Coal Power Plant 1320 MW SS Power-1 Ltd and SS Power-2 Ltd. June, 2020

Boropukuria 275 MW PP (3rd Unit) 274 MW BPDB June, 2018

Bangladesh-India Friendship Power Co. Ltd. 1320 MW BPDB & NTPC March, 2021

Mawa, Munshiganj 522MW Coal Power Plant 630 MW IPP June, 2021

Dhaka 635MW Coal Power Plant 635 MW Orion Power Unit-2 December, 2021

Nuclear Energy Projects: As a part of the long term energy generation plan, the government plans to generate 4,000 MW electricity from Nuclear Energy Source.

Financing & Investment in Power Projects:

To achieve the government’s target to cover the whole country under electricity by 2021, the country requires multibillion dollar investments in the power sector. As a result, the government is increasingly diversifying the sources of investment.

Small power projects are attracting private sector investment while the government is seeking innovative financing through joint venture and the ECA (Export Credit Agency) backed financing for large power projects.

The Asian Development Bank (ADB) will also provide a USD616 million (BDT 50 billion) loan to Bangladesh to help the country meet its goal of providing 100% access

to electricity to its citizens by 2021. The government has also made large financing deal with Indian and Chinese government for financing big power projects of the country.

Besides, along with the loan and borrowing from local banks private sector power plant promoters are also pursuing for concessional rate loans from various foreign banks and other foreign sources.

Source: Power Division, cited by The Daily Star

27.0

8.2

3.1

15.0

7.3

3.8

2022-30(Planned)

2017-21(Planned)

2009-16(Actual)

Planned Investment in Power Pjoects (USD billion)

Public Private

Page-8 October 29, 2017

EBL Securities Limited Research

Fiscal Incentives: Facilities & incentives for foreign investors: Exemption of corporate income tax for a period of 15

years

Allowed to import plant and equipment and spare parts up to a maximum of 10% of the original value of total plant and equipment within a period of twelve (12) years of commercial operation without payment of custom duties, VAT and any other surcharges as well as import permit fee except for indigenously produced equipment manufactured according to international standards

Repatriation of equity along with dividends allowed freely

Exemption from income tax for foreign lenders to such companies

The foreign investors will be free to enter into joint ventures but this is optional and not mandatory

Tax exemption on royalties, technical know-how and technical assistance for their repatriation

Tax exemption on interest on foreign loans

Tax exemption on capital gains from transfer of shares by the investing company

Avoidance of double taxation case of foreign investors on the basis of bilateral agreements

Exemption of income tax for up to three years for the expatriate personnel employed under the approved industry

Remittance of up to 50% of salary of the foreigners employed in Bangladesh and facilities for repatriation of their savings and retirement benefits at the time of their return

No restrictions on issuance of work permits to project related foreign nationals and employees

Facilities for repatriation of invested capital, profits and dividends

Presence of Private Power Generation Companies in Bangladesh Capital MarketCurrently seven companies under private power sector have active presence in Bangladesh Capital Market. Besides, few other listed Companies from different other sectors also have investment in the private power generation sector of Bangladesh.

Review of Private Power Producers in Bangladesh Capital market:

Baraka Power Limited: Baraka Power Limited is a joint collaboration of local and a group of Non Resident Bangladeshi (NRB) entrepreneurs. The company was incorporated in Bangladesh on 26 June 2007 as a Private Limited Company. On 25 September 2008 the Company was converted to Public Limited Company under the Companies Act 1994. Currently the company has a 51 MW capacity Gas based power plant which started commercial operation on October 2009 for a tenure of 15 years. The company has a subsidiary named Baraka Patenga Ltd. - a 50MW IPP HFO based power plant at Patenga, Chittagong. The plant started its operation in 2014 for a tenure of 15 years.

Khulna Power Company Ltd.: Khulna Power Company Ltd. (KPCL) is one of the first Independent Power Producer (IPP) in the country, incorporated in October 1997 and commenced commercial operation in October 1998. The formation of KPCL Project was initially sponsored by Summit Group and United Group along with their foreign partner El Paso Corporation (El Paso), USA, one of the world’s largest and most diversified natural gas exploration and pipeline companies and Wärtsilä Corporation (Wärtsilä), Finland, a leading power plant manufacturer of the world. In 2008, El Paso, as part of its global repositioning strategy disposed of its shares in KPCL to Summit Group and United Group. Later in 2009 Wärtsilä’s share was also acquired by Summit and United.

Currently the company has three power plants in its portfolio having a total installed capacity of 265 MW. The initial contractual tenure of KPCL Unit-II and Unit-III expired in 2016 and the power supply agreements have been extended for another 5 years since then. The company became listed with DSE and CSE on April 2010.

*Including Contribution from Subsidiary & Associates

Doreen Power Generations and Systems Limited: Doreen Power Generations and Systems Limited (DPGSL) was incorporated in 2007 as a private limited company and converted into public limited company in 2011 and became listed with the DSE and CSE in 2016. DPGSL has three power plants for generating and supplying 66 MW of electricity to BPDB and REB under three PPAs (22 MW each) for a tenure of 15 years.

It has two subsidiaries namely, Dhaka Southern Power Generations Ltd. (99.14% owned) and Dhaka Northern Power Generation Ltd. (98.52% owned). The Commercial Operation (COD) of those two HFO fired plants having 55MW capacity each started in in 2016.

BARAKAPOWER, 76.5

GBBPOWER, 22.8

KPCL, 265.0

SPCL, 111.0

SUMITPOWER, 544.6

UPGDCL, 160.0

DOREENPWR, 174.7

ORIONPHARM, 162.0

SHASHADNIM, 55.0

Ownership-wise power generation capacity* of listed Companies

Page-9 October 29, 2017

EBL Securities Limited Research

TICKER Plant Name Ownership Capacity (MW)

Capacity Utilization

Fuel Used

Major Customer

Contract Tenure

Contact Expiration

BARAKAPOWER BARAKA POWER 100% 51.00 77.22% Gas BPDB 15 Years 2024

BARAKA-PATENGA 51% 50.00 68.84% HFO BPDB 15 Years 2029

GBBPOWER GBBPOWER 100% 22.80 100.00% Gas BPDB 15 Years 2023

KPCL

KPCL-I 100% 110.00 54.66% HFO BPDB 15 Years 2018

KPCL-ll 100% 115.00 62.26% HFO BPDB 5 Years 2021

KPCL-lll 100% 40.00 55.74% HFO BPDB 5 Years 2021

SPCL SPCL 100% 86.00 74.00% Gas BPDB 15 Years 2024

Midland Power Co. 49% 51.00 n/a Gas BPDB 15 Years 2028

SUMITPOWER

Ashulia-Savar-1 100% 11.00 70.00% Gas BREB 15 Years 2018

Ashulia-Savar-II 100% 33.75 67.00% Gas BREB 15 Years 2022

Madhabdi-I 100% 11.00 66.00% Gas BREB 15 Years 2018

Madhabdi-II 100% 24.30 63.00% Gas BREB 15 Years 2021

Chandina-I 100% 11.00 68.00% Gas BREB 15 Years 2018

Chandina-II 100% 13.50 72.00% Gas BREB 15 Years 2021

Rupganj- N.ganj 100% 33.00 79.00% Gas BREB 15 Years 2024

Jangalia-Comilla 100% 33.00 81.00% Gas BPDB 15 Years 2024

Maona-Gazipur 100% 33.00 86.00% Gas BREB 15 Years 2024

Ullapara 100% 11.00 80.00% Gas BREB 15 Years 2014

SNPL 100% 102.00 65.00% HFO BPDB 5 Years 2021

SNPL II 49% 55.00 n/a HFO BPDB n/a n/a

SBPL-Rupatoli 49% 110.00 n/a HFO BPDB n/a n/a

KPCL-Khulna 17.64% 265.00 n/a HFO BPDB n/a n/a

SMPCL 30% 335.00 n/a Diesel BPDB n/a n/a

UPGDCL DEPZ Plant 100% 88.00 73.00% Gas DEPZ 30 Years 2038

CEPZ Plant 100% 72.00 80.00% Gas CEPZ 30 Years 2039

DOREENPWR

Tangail Plant 100% 22.00 65.00% Gas BPDB 15 Years 2023

Narsingdi Plant 100% 22.00 67.00% Gas BPDB 15 Years 2023

Feni Power Plant 100% 22.00 77.00% Gas REB 15 Years 2024

DSPGL 99.14% 55.00 n/a HFO BPDB 15 Years 2031

DNPGL 98.52% 55.00 n/a HFO BPDB 15 Years 2031

ORIONPHARM OPML 95.00% 100.00 55.00% HFO BPDB 5 Years n/a

DBPAL 67% 100.00 55.00% HFO BPDB 5 Years 2021

SHASHADNIM EPCL 99.97% 55.00 n/a n/a BPDB 5 Years 2019 *n/a= information not available

Summit Power Limited: Summit Power Limited is a concern of Summit Group, one of the leading private sector conglomerates of Bangladesh, comprising more than twenty business units ranging from power to shipping to communications and currently generating 1,423 MW of electricity. Summit Power Limited owns and operates 11 (eleven) power plants at different locations across the country having a total capacity of 316.75 MW from its fully owned plants.

Summit sells electricity to the Bangladesh Power Development Board (BPDB) and Bangladesh Rural Electrification Board (BREB) only. The company has 4 (four) associates companies which are: Summit Barisal Power Limited, a 110 MW HFO fired plant , Summit Narayanganj Power Unit II Limited, a 55 MW HFO fired plant, Summit Meghnaghat Power Company Limited (SMPCL), a 335 MW HFO fired plant and Summit Chittagong Power Limited (proposed), where Summit power holds 49%, 49%, 30% and 49% ownership respectively.

Shahjibazar Power Co. Ltd.: Shahjibazar Power Co. Ltd., was incorporated as a public limited company in 2007

and started its operation in January 2009. It is situated at Fatehpur, Shahjibazar, Hobigonj. The company signed power supply agreement with BPDB in 2008 for a tenure of 15 years with an 86MW gas fired power plant that started commercial operation in 2009.

The company has a 90% owned subsidiary company namely Petromax Refinery Limited. The principal activity of this company is production and supply of petroleum products like liquid petroleum gas, special boiling point solvent, mineral turpentine, high speed diesel, octane, kerosene and fuel gas to Bangladesh Petroleum Corporation. The Company has started its commercial operation on 25 October, 2013. The company also has an Associates Company namely “Midland Power Co. Ltd” (51 MW Gas based power Plant) where it holds 49% shares. This company has started its commercial operation on 7 December, 2013.

GBB Power Ltd: GBB Power Ltd. is an Independent Power Producer (IPP) in Bangladesh that was incorporated on 2006 as a private limited company and subsequently converted into a public limited company on 2008. In 2007 the company signed an agreement with BPDB to

Page-10 October 29, 2017

EBL Securities Limited Research

supply upto 22MW of electricity with its Gas based power plant for a tenure of 15 years. The company became listed with DSE and CSE in 2012.

United Power Generation & Distribution Co. Ltd.: United Power Generation & Distribution Co. Ltd. (UPGDCL) generates power and deliver to the industries housed within Export Processing Zone (DEPZ & CEPZ). At the

initiation, it was known as Malancha Holdings Ltd. The installed capacity of DEPZ plant is 86 MW and installed capacity of CEPZ is 72 MW. Both plant are gas fired. The Company has 30 year’s agreement with BEPZA and to cope with increased load growth the company is increasing its capacity in both DEPZ and CEPZ to 100 MW each and the expansion projects are expected to complete within this year.

Performance of Power Generation Companies Listed in Bangladesh Capital Market Sponsors hold majority of the shareholding in most of the private power generation companies in Bangladesh, excluding BARKAPOWER and GBBPOWER, where general public holds majority of the shares. Currently, SUMITPOWER holds highest paid up capital among the

listed power producing companies. The company has 11 fully owned power plants and 3 more plants in its portfolio. Earnings of the DOREENPWR increased significantly due to commencement of two new HFO fired power plants a having capacity of 55 MW each.

TICKER Close Price EPS EPS EPS NVPS Shareholding Structure Paid-up

24-Oct-17 Ann. Audited growth Sponsor Govt. Institution Foreign Public (BDT mn)

BARKAPOWER 39.2 3.2 2.65 21% 19.9 19.91% 0.00% 19.56% 0.00% 60.53% 1,740

SUMITPOWER 37.7 3.76* 4.37 -14% 29.0 56.60% 0.00% 25.15% 3.65% 14.60% 10,679

DOREENPWR 123.0 7.57* 0.64 1085% 36.0 75.00% 0.00% 7.89% 0.00% 17.14% 960

GBBPOWER 19.9 1.21 0.85 43% 20.8 30.01% 0.00% 12.02% 0.00% 57.97% 970

KPCL 63.9 5.21 5.96 -13% 25.0 70.59% 0.00% 16.26% 0.90% 12.25% 3,613

UPGDCL 170.5 11.8 10.38 14% 38.6 92.02% 0.00% 3.69% 0.00% 4.29% 3,629

SPCL 133.3 7.4 5.14 44% 33.8 68.03% 0.00% 12.58% 0.00% 18.90% 1,412

DESCO 43.9 1.25 1.12 12% 37.5 0.00% 67.63% 20.25% 0.56% 11.56% 3,976

POWERGRID 54.8 3.2 2.66 20% 83.3 0.00% 76.25% 18.78% 0.39% 4.58% 4,609 *based on 2016-17 year-end declaration

A Comparative Financial Review Company Fundamentals DOREENPWR SUMITPOWER UPGDCL SPCL KPCL BARKAPOWER GBBPOWER

Market Cap (BDT mn) 11,808.0 40,259.0 61,882.1 18,828.1 23,086.1 6,819.3 1,929.4

Market Weight 0.29% 0.99% 1.52% 0.46% 0.57% 0.17% 0.05%

Free-float (Public + Inst.) 25.0% 43.4% 8.0% 32% 29.41% 80.1% 68.0%

No of shares (mn) 96.0 1067.9 362.9 141.25 361.28 173.96 96.96

52-week Low 99.0 33.0 139.3 131.3 57.4 27.5 14.2

52-week High 158.0 46.7 195.4 162.8 69.8 53.4 26.3

Last Declared Dividend 10%C & 10%B 30%C(18M) 125%C(18 M) 30%C &3%B 75%C (18 M) 15%C & 5%B 15%C (18M)

Financial Information (BDT mn): DOREENPWR

9M,An. SUMITPOWER

9M,An. UPGDCL 9M,An.

SPCL 9M,An.

KPCL 9M,An.

BARKAPOWER 9M,An.

GBBPOWER 9M,An.

Sales 4,724.6 6,113.0 5,714.6 8,798.7 8,846.5 3,686.2 521.2

Gross Profit 1,428.8 3,201.3 4,145.0 1,910.0 2,250.9 1,230.7 172.2

Operating Profit 1,244.6 2,857.2 4,285.0 1,756.3 2,148.5 1,105.5 110.0

Profit After Tax 738.7 3,930.4 4,282.7 1,116.7 1,885.8 741.4 118.1

Total Assets 12,872.0 32,246.7 14,109.0 10,197.6 14,767.3 8,536.5 2,178.0

Total Debt (LTD+STD) 7,425.3 - - 4,297.5 4,167.3 3,626.3 57.3

Equity 3,287.0 31,526.8 13,998.0 5,017.9 9,048.1 4,324.4 2,019.4

Retained Earnings 1,199.2 10,965.8 8,322.6 1,775.0 5,109.6 749.9 183.3

Cash 3.9 2,977.4 472.9 488.8 2,076.1 154.0 478.0

Margin:

Gross Profit 30.2% 52.4% 72.5% 21.7% 25.4% 33.4% 33.0%

Operating Profit 26.3% 46.7% 75.0% 20.0% 24.3% 30.0% 21.1%

Pre Tax Profit 15.6% 64.3% 74.9% 15.5% 23.2% 21.8% 23.6%

Net Profit 15.6% 64.3% 74.9% 12.7% 21.3% 20.1% 22.7%

Growth:

Sales 345.6% -2.1% 8.2% 9.5% -11.5% 18.5% 0.6%

Gross Profit 219.3% -12.1% 13.8% 30.5% -23.4% -0.1% -1.3%

Operating Profit 361.8% -5.4% 12.8% 33.1% -16.6% 7.9% -2.6%*

Net Profit 1619.1% 0.8% 11.9% 64.0% -10.9% 7.7% -3.0%*

Profitability:

ROA 11.5% 24.4% 60.7% 21.9% 25.5% 17.4% 10.8%

ROE 44.9% 24.9% 61.2% 44.5% 41.7% 34.3% 11.7%

Leverage:

Page-11 October 29, 2017

EBL Securities Limited Research

Debt Ratio 57.7% 0.0% 0.0% 42.1% 28.2% 42.5% 2.6%

Debt-Equity 225.9% 0.0% 0.0% 85.6% 46.1% 83.9% 2.8%

Altman Z Score 3.1 2.1 4.2 4.6 3.1 2.8 1.6

Valuation:

Price/Earnings 17.0 10.3 14.8 18.4 12.3 12.4 16.6

Price/BV 3.8 1.3 4.5 3.8 2.6 1.6 1.0

Price/ Sales 2.5 6.6 10.8 2.1 2.6 1.8 3.7

EV/EBITDA 15.6 9.6 14.3 13.0 11.6 10.2 12.3

EV/Sales 4.1 6.1 10.7 2.6 2.8 3.0 2.9 *GBBPOWER had written off BDT51.7 million in FY2015-16 as liquidated damage which was arisen by reduced payment of electricity bill by BPDB due to short supply of electricity. As the amount are no longer recoverable, the company wrote-off the amount. However, to compute YoY earnings growth, we ignored this one-off event and made comparison based on continued operation.

Key Investment Insights

Positive Insights Negative Insights

UPGDCL The company is increasing its plant capacity of DEPZ and CEPZ to 100 MW each from existing 86 MW (16.3% enhancement) and 72 MW (38.9% enhancement) capacity respectively which will in operation within December of 2017. These capacity enhancement will boost the earnings of the company.

UPGDCL has 30 years of power supply agreement with BEPZA for both of its plant with provision for extension of another 30 years of tenure, whereas the agreement tenure for all other private power plants ranges from 5 to 15 years of tenure.

The company has no long term loan currently in its portfolio that resulted into higher profit margin for the company.

UPGDCL enjoys highest profit margins in the industry. Besides, ROA & ROE of the company are also significantly higher (60.7% and 61.2% respectively) than other private power producers listed in the capital market.

Both of the power generation plants of the company are gas based and recent gas price hike will adversely affect the operating cost and thus it may affect the profitability as well. Gas price for electricity generation plants has been increased to BDT 3.16 since June 2017 and was increased to BDT 2.99 in March from earlier price of BDT 2.82

The country is suffering from acute shortage of Gas and it is said that total gas reserve of the country will be depleted within next 15 years. Hence, the company might face difficulties to operate in the absence of uninterrupted supply of gas.

SUMITPOWER The Consortium of Summit Corporation Limited (SCL) and Summit Power Limited (SPL) is setting up a 300MW HFO fired power plant where Summit Power shall have 20% ownership. The project is expected to commence by June 2018

Summit Power Ltd. has successfully completed its amalgamation with its three subsidiaries, Summit Purbanchol Power Company Limited (SPPCL), Summit Uttaranchol Power Company Limited (SUPCL) and Summit Narayanganj Power Limited (SNPL) where the company earlier held 71.06%, 51.48% and 55.00% ownership. Implementation of the aforesaid amalgamation is supposed to enable the company to reduce operating costs through increased efficiency.

Summit Power Ltd. has acquired 64% shares of Ace Alliance Power Limited, a proposed 149MW Dual Fuel (HFO/Gas) Fired Power Project at Kodda, Gazipur. The facility will be implemented on Build, Own and Operate

Any policy level changes like, not extending the tenure of IPP (Independent power producer) in the future may drastically affect the Company’s ability to operate as going concern.

As 10 out of the company’s 11 power plants are gas based, increase in the price of gas will increase the power generation cost significantly.

Due to scarcity of gas in the country, there is a high risk of not extending the tenure of power supply agreement for gas based plants after expiration. In such cases, the company’s revenue as well as profitability might experience significant decline in future.

Page-12 October 29, 2017

EBL Securities Limited Research

(BOO) basis for a period of 15 years from the Commercial Operation Date (COD). The estimated cost for the project would be BDT 6,750.0 million with 70% debt and 30% Equity funding. The plant is expected to commence operation from August 2018.

Finance costs has remarkably reduced because of payoff of short term loan and timely repayment of project loan, finance leases and redeemable preference shares. Reduction in finance cost has significantly increased the net profit margin of the company.

Other income of the Company went up during the year especially due to increase in the dividend income from subsidiaries and others.

The company has invested BDT 4.9 million at Summit Chittagong Power Limited for its 49% ownership. However, the details of the project has not been disclosed yet by the company

DOREENPWR The Consortium of Doreen Power Generations and Systems Ltd. and Doreen Power House & Technologies Limited is going to set up a new 115 MW capacity HFO fired power plant at Chandpur, Bangladesh. DOREENPWR has 60% stake in the said consortium. The project is supposed to commence operation by the end of 2018. The new project will bring significant jump to the company’s consolidated earnings.

Commencement of the commercial operation of two new HFO fired power plants having 55MW capacity each has started to contribute to the consolidated financials of the company and driving the revenue and net profit growth of the company significantly. The tariff rate for these two projects are BDT 6.9898 per kwh.

The company is exposed to high leverage. Interest expense eats up significant portion of its operating profit. 40% of operating profit were paid as financial expenses during the first 9 months of the FY 2016-17.

Any disruption in gas supply may hamper productivity as the 3 of the company’s power plants summing up 66 MW generation capacity are gas based.

BARKAPOWER Karnaphuli Power Limited, a 51% owned subsidiary of the Baraka Power’s subsidiary Baraka Patenga Power Limited is setting up a 110 MW HFO based power plant on BOO basis. The project is required to start operation by the end of 2018. Besides, Baraka Power will also directly invest in 25% shares of the Karnaphuli Power Limited, meaning an aggregate holding of the company will stand at 51.01% to the new plant. The project is supposed to create significant growth in the earnings of the company, once it come into operation.

The company has acquired 51% stake of a 100% export oriented newly built Ready-Made-Garments Factory having 10-line (woven tops) production capacity by investing BDT 61.2 million. Total cost of the acquisition and modification is BDT 400.0

Baraka Power’s Fenchuganj project is gas based. Any disruption in gas supply may hamper productivity.

Dollar appreciation may increase the cost of debt as Baraka Power availed big portion of foreign debt of USD4 mn from IDCOL (Interest rate LIBOR+ 5%)3

Page-13 October 29, 2017

EBL Securities Limited Research

million, which has been financed through 70:30 debt-equity ratio.

SPCL SPCL’s 49% owned associate, Midland Power Company Limited is setting up a 150 MW HFO fired IPP plant. The project is supposed to be completed by the end of 2018. Once it comes into operation, SPCL’s income from associate will increase significantly.

The company’s associate, Midland Power Co. Ltd., will subscribe 20% equity of the 200 MW Grid Tied Solar Park Project by Southern Solar Power Limited. After implementation and start of commercial operation of the said project, there shall have prospective impact on the profitability of SPCL with around 20.9 MW contribution to the consolidated profit of SPCL.

As Petromax is allowed to import condensate from the international market at a lower price, it helps the company to reduce cost.

Petromax consumed 90% of its allocated condensate (8350 MT) and produced 7601 MT of diesel unlike many other refineries in the market that produced diesel of 12%-14% of the condensate allocated to them.

As the price of petroleum products has been revised by the Government on 24 May 2016 the gross revenue of Petromax Refinery Ltd. (PRL), a 90% owned subsidiary of SPCL, has increased significantly and will result in a robust growth in both consolidated revenue and net profit of the company in FY2016-17.

Both SPCL and Petromax Refinery Ltd. will be enjoying tax exemption on its operating income up to the year 2024 and the year 2020 respectively.

As the fuel and power sector is highly regulated, pricing and investment strategies are decided by the government. Therefore, profitability for SPCL and its subsidiary depend on the Tariffs set by the government.

The major raw material for generating SPLC’s electricity is natural gas. Any interruption of supply of fuel to the power plants will hamper the production.

SPCL has the lowest profitability margins among the listed companies in the sector. Business diversification with refinery business caused the minimized profit margins. Moreover, the debt ratio and debt equity ratio of the company are pretty higher compared to other similar companies.

KPCL The power supply agreement with BPDB has been extended for another 5 years for KPCL Unit-II (115 MW HFO based power plant) and KPCL Unit-III (40 MW HFO based power plant) with effect from June 01, 2016 and May 29, 2016 respectively. These extension of agreements ensured uninterrupted revenue generation from those two plants for another 5 years.

KPCL does not require to make any provision for tax for the KPCL Unit-II and Unit-III as according to the agreement, BPDB is responsible for payment of income taxes, other taxes, VAT, duties, levies and all other charges imposed inside Bangladesh on any payments made by BPDB to the company from the start of operation.

The company has significant exposure to foreign exchange volatility risk due to its US Dollar Accounts, Working capital loan and interest for acceptance of HFO L/Cs, Service charges/Handling commission payable to fuel suppliers, Accounts payables and Accounts receivable from BPDB. During the third quarter (3 months) of FY2016-17, the company experienced BDT 25.2 mn (4.3% of operating profit) foreign exchange loss due to devaluation of BDT against USD.

The extended power supply agreement for KPCL unit-I (110 MW) with BPDB will expire on 2018. If the agreement is not renewed further the earnings of the company will fall drastically.

GBBPOWER According to the annual report of the company, the management is looking for opportunities to set up plants on alternative fuel-fired engines and/ or sourcing of

The company runs only one gas fired power plant of 22 MW. Scarcity of natural gas might remain a key concern for the company. Besides increase in Gas price will increase the cost of power generation of the company.

Page-14 October 29, 2017

EBL Securities Limited Research

renewable energy in collaboration with foreign companies.

Failure to diversify the business of the company or expand existing business with alternative fuel based technology remains a key concern.

Summary of the Forthcoming Power plants approved for companies listed in Bangladesh Capital Market

TICKER Upcoming Project Details

1. SUMITPOWER 2 (Two) new power plants having installed capacity of 149MW and 300 MW HFO fired power plants are being constructed where the company has 64% and 20% ownership respectively. Tariff rate for the plants are BDT7.5 and BDT8.3379 per unit and will be operational by the middle of 2018.

2. SPCL SPCL’s 49% owned associate, Midland Power Company Limited is setting up a 150 MW HFO/ Diesel fired IPP plant at a tariff rate of 8.2593. Besides, Midland Power will also subscribe 20% equity of the proposed 200 MW Grid Tied Solar Park Project by Southern Solar Power Limited.

3. BARKAPOWER Karnaphuli Power Limited has received LOI for implementation of an 110MW HFO fired power plant where the company will have 51% ownership. Moreover, the group is also approaching for more power plants but no further approval from the government has been received yet.

4. CONFIDCEM Three new power plants having 113 MW capacity each are being constructed by the group. Confidence cement shall have 51% ownership in two 113 MW power plants and its 25% owned associate Confidence Power Ltd. is setting up another 113MW power plant under the government’s fast track project.

5. DOREENPWR A new 115MW HFO fired power plant is being constructed on which the company shall have 60% ownership.

6. PTL The company has decided to participate in the unsolicited tender under the government’s First Track Project to develop HSD Based 2X100 MW IPP/Rental Power Plant. However, no approval from the government has been received yet.

7. ORIONPHARM The company’s 95% owned subsidiary Orion Power Meghna Ghat Ltd. has equity shares in the under-construction fast tract project of 105MW HFO fired power plant of Orion Power Rupsha Ltd. Detail shareholding information of the Orion Power Meghna Ghat Ltd. on the said power plant is not available yet.

8. BSRMSTEEL Chittagong Power Company Limited (CPCL), a sister concern of the steelmaker BSRM, will build and operate a 150-megawatt (MW) coal-fired merchant power plant at Mirersarai. However, the company is yet to get required land allocation from BEBZA for the plant. Both BSRMSTEEL and BSRMLTD shall have ownership in the plant.

9 SHASHADNIM The company’s subsidiary Energis Power Corporation Ltd. participated in tender for power plant setup. But till date the company didn't receive any formal information/ approval from the BPDB

Concluding Remark: Power is the prime mover of any economy. Any big push of the economy would need uninterrupted power supply. The provision of adequate and reliable supply of electricity at a reasonable cost is a pre-requisite to attain the goal of being a middle income country by 2021. The government is working relentlessly to increase the country’s capacity to generate required power. However, the focus of short term highly expensive power supply

based on rental and quick rental power project need to change and the government need to look for low cost sustainable projects for generation of power. Moreover, uncertainly regarding extension of power supply agreements remains a key concern for all the rental and quick rental power projects to continue as a going concern.

Page-15 October 29, 2017

EBL Securities Limited Research

DISCLAIMER

This document has been prepared by the Research Team of EBL Securities Limited (EBLSL) for information only of its clients residing both in Bangladesh and abroad, on the basis of the publicly available information in the market and own research. This document has been prepared for information purpose only and does not solicit any action based on the material contained herein and should not be taken as an offer or solicitation to buy or sell or subscribe to any security. Neither EBLSL nor any of its directors, shareholders, member of the management or employee represents or warrants expressly or impliedly that the information or data of the sources used in the documents are genuine, accurate, complete, authentic and correct. However all reasonable care has been taken to ensure the accuracy of the contents of this document. EBLSL will not take any responsibility for any decisions made by investors based on the information herein.

ANALYST DISCLAIMER The person or persons named as the author(s) of this report hereby certify that the views expressed in the research report accurately reflect their personal views about the subject matters discussed. No part of their compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in the research report. The views of the author(s) do not necessarily reflect the views of the EBL Securities Limited (EBLSL) and are subject to change without any notice. All reasonable care has been taken to ensure the accuracy of the contents of this document and the author(s) will not take any responsibility for any decisions made by investors based on the information herein.

ABOUT EBL SECURITIES LTD. EBL Securities Ltd. (EBLSL) is one of the fastest growing full-service brokerage companies in Bangladesh and a fully owned subsidiary of Eastern Bank Limited. EBLSL is also one of the top ten leading stock brokerage houses of the country. EBL Securities Limited is the TREC-holder of both exchanges of the country; DSE (TREC# 026) and CSE (TREC# 021). EBLSL takes pride in its strong commitment towards excellent client services and the development of the Bangladesh capital markets. EBLSL has developed a disciplined approach towards providing capital market services, including securities trading, margin loan facilities, depository services, online trading facilities, panel brokerage services, trading through NITA for foreign investors & NRBs etc.

EBLSL KEY MANAGEMENT

Md. Sayadur Rahman Managing Director [email protected]

Md. Humayan Kabir SVP & Chief Operating Officer (COO) [email protected]

EBLSL RESEARCH TEAM

M. Shahryar Faiz FAVP & Head of Research [email protected]

Md. Asrarul Haque Senior Officer-Research [email protected]

Mohammad Rehan Kabir Officer-Research [email protected]

Tajkera Rahman Officer-Research [email protected]

Md. Nazmus Sakib Officer-Research [email protected]

Md. Mosavvir Al Ashick Officer-Research [email protected]

Asaduzzaman Ashik Officer-Research [email protected] Farzana Hossain Laizu Assistant Officer- Research [email protected]

For any queries regarding this report: [email protected]

EBLSL BRANCHES

Head office: HO Extension-1 HO Extension-2 Dhanmondi Branch Chittagong Branch

59, Motijheel C/A (1st Floor) Dhaka-1000 +8802 7119631, 9556539 +8802 47111935; FAX: +8802 47112944 [email protected]

Modhumita Building 160 Motijheel C/A (2nd Floor) Dhaka-1000. +88 02 9569480, 9564393, +88 02 8825236 FAX: +8802 47112944 [email protected]

Bangladesh Sipping corporation (BSC) Tower 2-3, Rajuk Avenue (4th floor), Motijheel, Dhaka-1000 +880257160801-4

Sima Blossom (4th Floor) House # 390 (Old), 3 (New), Road # 27 (Old), 16 (New), Dhanmondi R/A, Dhaka-1209. +8802-9130268, +8802-9130294

Suraiya Mansion (6th Floor), Northern East Front Side & Northern West Front Side, 30, Agrabad C/A, Chittagong-4100. +031 2522041-43