polish renewable energy investment landscape ´2015 - the on-going and new legal framework -...

TRANSCRIPT

Grzegorz Wiśniewski [email protected]

Institute for Renewable Energy

Warsaw, Poland www.ieo.pl

Polish renewable energy

investment landscape ´2015 - the on-going and new legal framework

REFIP Forum 4.0 „Renewable Energy Finance in Practise”

7-8 May, 2015, Vienna

The growth rate of installed capacity in the Polish Power System in years1960-2013

(source: PSE Operator)

www.ieo.pl

Hard coal public power stations

Autoproducer power stations

Public thermal power plants

Lignite public power stations

Public hydro plants

Country total

Gas public power stations

Wind and other RES

[Years]

Directive 2009/28/EC of The European Parlilament and The Council of 23 April

2009 on the promotion of the use of energy from renewable sources and

amending and subsequently repealing Directives 2001/77/EC and

2003/30/EC

1. The Energy Law Act of 10 April 1997 (Journal of Laws 2012 No. 1059, as

amended); the „prosumer’s amendment” of July 2013

2. The Regulation (decree) of the Minister of Economy of 4 May 2007 on

detailed conditions for electricity system functioning (Journal of Laws No. 93,

item 623, as amended)

3. The Renewable Energy Act of 20 February 2015 (Journal of Laws item 478) (adopted by the Parliament on 20 February 2015 and signed by the President on 11

March 2015)

www.ieo.pl

The current support system for RES generation in

Poland – the general rule

Obliged entities – traders supplying electricity to end-users

Green certificates (certificates of origin) issued by Energy Regulatory Authority (URE) for concessioner RES owners

The trading system for green certificates managed by Polish Power Exchange (TGE).

∑≈ € 95/MWh

The quota obligation for trading Utilities and fulfillment of the obligation

Note – RES-E generation including unsolved cases of TGC issuing, mostly concerning biomass;

according to up-to-date experience these TGC are finally issued and affecting the market

RES-E installed capacity in Poland, status 31/03/2015 (MW)

www.ieo.pl

RES-E generation in Poland

~30% of RES electricity from biomass co-firing; until 2011 it was 50%

The oversupply of green certificates

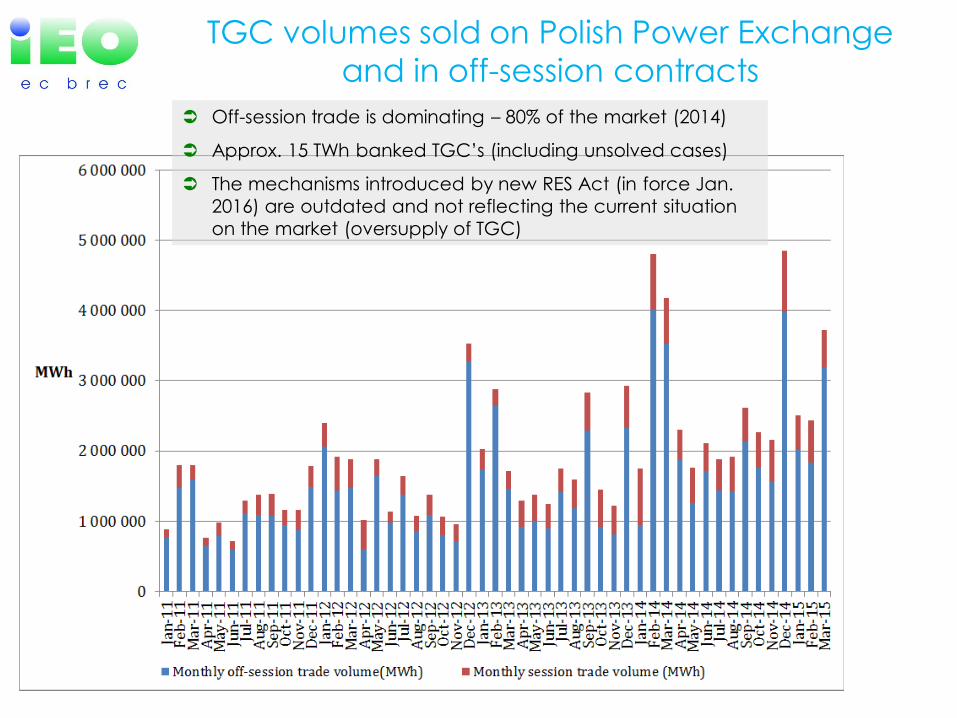

TGC volumes sold on Polish Power Exchange

and in off-session contracts

Off-session trade is dominating – 80% of the market (2014)

Approx. 15 TWh banked TGC’s (including unsolved cases)

The mechanisms introduced by new RES Act (in force Jan.

2016) are outdated and not reflecting the current situation

on the market (oversupply of TGC)

www.ieo.pl

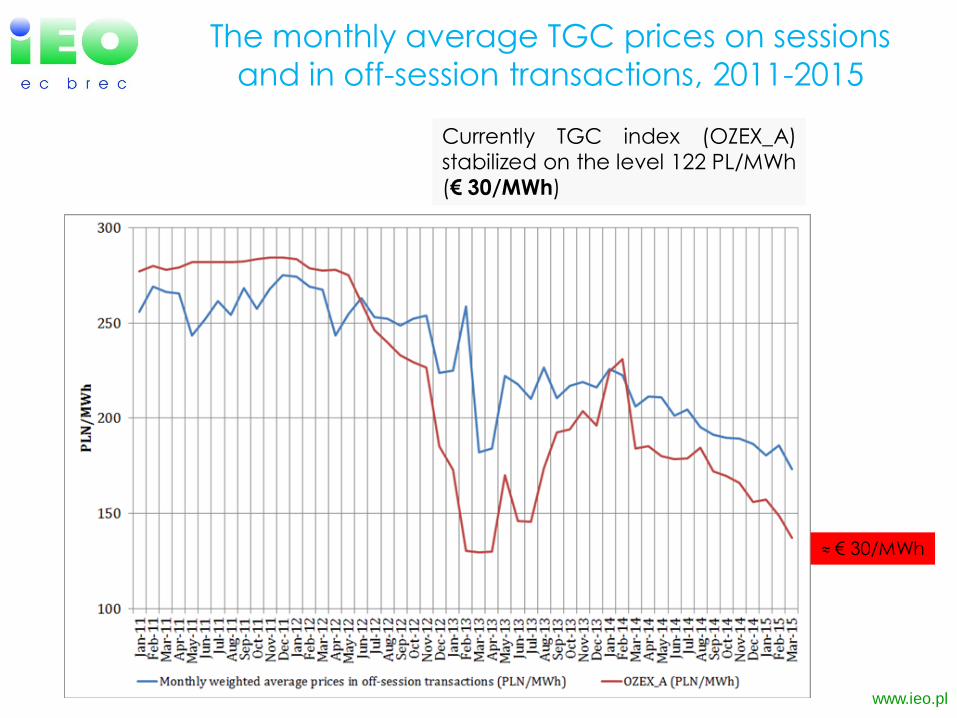

The monthly average TGC prices on sessions

and in off-session transactions, 2011-2015

Currently TGC index (OZEX_A) stabilized on the level 122 PL/MWh (€ 30/MWh)

≈ € 30/MWh

The average electricity prices and substitute fees

in Poland source: source: TGE, URE, IEO

www.ieo.pl

Growing cost

∑ electricity price+ fee = income for RES-E producer

www.ieo.pl

Electricity prices: Comparison of energy markets in Poland

and Germany (EEX)

January 2014

Own study based on TGE, EEX, Agora Energiewende

Lipiec 2014

Opracowanie własne na podstawie TGE, EEX, Agora Energiewende

Electricity prices Comparison of energy markets in Poland

and Germany (EEX)

Own study based on TGE, EEX, Agora Energiewende

The impact of RES support system and energy mix

on RES-E costs and the Germany (FiT, high RES share) and Poland (TGC, low RES share)

Sources: TGE, EEX (Phelix)

January 2014 July 2014

New RES Act = new support schemes

in force since 1 January 2016, up 2020

Different support schemes Comment: just on time, too late or too early?

too late OK too early

Biomass

co-firing ×

large scale (retrofit) ×

large scale (greenfield) ×Biogas landfill ×

sewage plants ×

agricultural ×Wind onshore ×

offshore ×

small scale ×Hydro paid off

new large scale ×

new small scale ×PV large scale PV ×

small scale PV ×

The assessment of support scheme

selection on current stage of RES

market development Support in RES Act

Type of

RESRES technology

Auctioning system

(baskets <1 MW and >1

MW)

Net metering 0-40 kW

Large scale RES

Prosumers installations

should never be supported

PV home PV ×Wind microturbines ×

micro biogas plants ×Bioliquids CHP ×

FiT 0-10 kW

Net metering 0-40 kW

Biomass

PV home PV ×Wind microturbines ×

Biomass micro biogas plants ×

FiT 0-10 kW

General rules of RES support in different for different scales of RES according to RES Act:

administrative and connection requirements

Administrative and DSO requirements

Micro RES Small scale RES Large scale RES

10 kW

40 kW

50 kW

75 kW

100 kW 200 kW

500 kW

1 MW

5 MW

10 MW

20 MW

50 MW

Administrative requirements

• Written information to DSO with installation description

• Not threaten as enterprise activity

• Concession not requested

• Registration as small scale RES energy supplier requested

• Treaten as enterprize • Concession not requested

Concession requested

Grid connection Lack of connection fee 50% connection fee Full connection fee

FiT up to 10 kW

Net metering up to 40 kW

FiT after auction – basket up to 1 MW

FiT after auctions- basket over 1 MW

Expected volumes in MW of auctions predicted

in 2015-2020 ≈ 4,2 GW

Technology

New capacity originally planet for auctions 2015 -2020 [MW]

2015 2016 2017 2018 2019 2020

Wind 500 500 500 500 500 500

Biomas 70 70 70 70 70 70

Hydro 0 0 0 0 0 80

Up to 1 MW (25% of total) 74,5 100,5 112,5 124,5 135,5 147,5

Wind 50 70 75 80 85 90

Biomas 21 27 34 41 47 54

PV ? ? ? ? ? ?

Hydro 3,5 3,5 3,5 3,5 3,5 3,5

TOTAL 644,5 670,5 682,5 694,5 705,5 797,5

Indicative/cumulated /updated

dates of auctions 1st auction

The forecast of LCOE for PV, biogas and wind energy vs. to

the wholesale electricity price (current value): Source: IEO study for Ministry of Economy, 2013, RES Act impact assessment ,2014

No official reference prices yet

www.ieo.pl

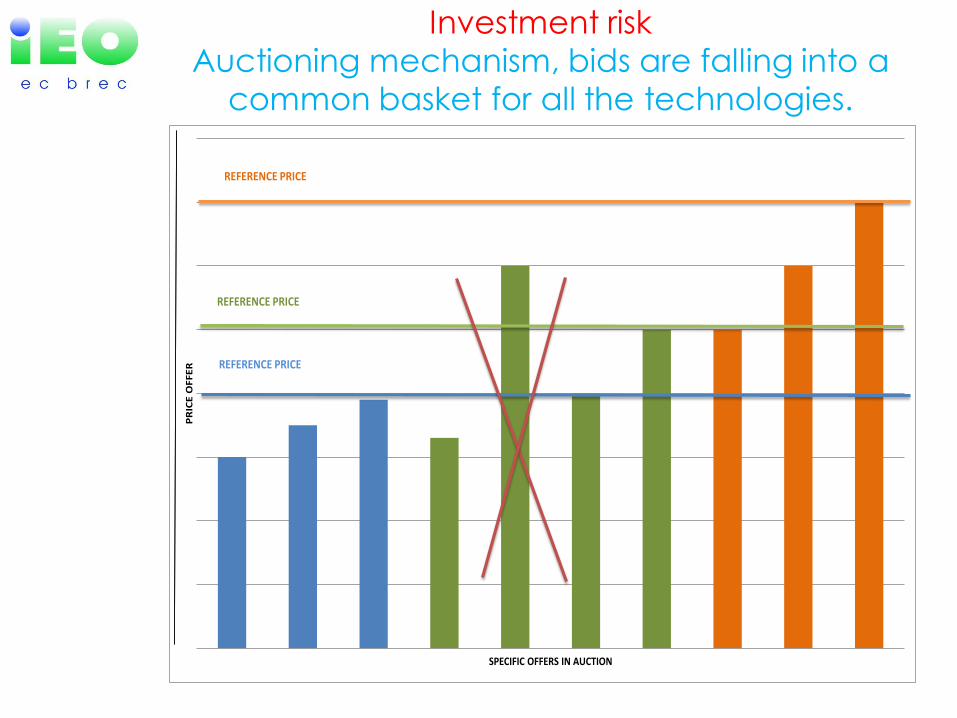

Simulation of „merit order” for RES-E technologies >1MW in

auctioning system (LCOE, PLN/MWh),, source IEO

Investment risk

Auctioning mechanism, bids are falling into a

common basket for all the technologies.

PR

ICE

OF

FE

R

SPECIFIC OFFERS IN AUCTION

REFERENCE PRICE

REFERENCE PRICE

REFERENCE PRICE

Investment risk

Merit order of the auction, assumption of equal

treatment of bidders

Investment risk

Merit order of the auction, limitation of the volume

for technologies generating <4000 MWh/MW

Feed in Tariffs (FiT) for micro installations according to the RES Act

Feed-in-Tarrifs FiT (wholesale sale of electricity, from renewable seller to retail utility) a „cap” on the clearing sale system from micro installation (the option to choose), available for everyone at specified time (2020) and specified power range (800MW).

FiT RES type RES technology Electricity rate

zł/kW

0-3 kW

Sun PV installations 0,75

Wind Micro Wind Turbines 0,75

Water Water plants 0,75

>3 – 10 kW

Sun PV installations 0,65

Wind Micro Wind Turbines 0,65

Water Water plants 0,65

Biogas

Agricultural micro-biogas plants 0,70

Landfill micro-biogas plants 0,55

Sewage micro-biogas plants 0,4

1zł=0,25 €

Feed-in-Tariffs(FiT) for micro

installations according to RES Act

-an implementation plan?

www.ieo.pl

Feed-in-Tariffs – over 200.000 installation until 2020:

• 145.000 micro installations up to 3 kW (together 300 MW)

• ≈60.000 micro installations between 3-10 kW (together 500 MW)

10 000

45 000

90 000

<3 kW

2 500

12 500

34 375

5 000

2 500 2 500

3-10 kW water

wind

PV

agricultural biogas

landfill biogas

sewage biogas

200.000 families and small enterprises – RES micro installation users – would not change the polish energy mix, however it could have changed the energy scenario

www.ieo.pl

Possible pay-back

by classical net-

metering for

bigger sources

Lack of price

defined in RES Act

(subject of

contract

negotiation)

„Net metering” up to 40 kW – economic effect for companies

www.ieo.pl

„Net metering”- an economic effect for individuals

Possible pay-back by

„gross” net-metering

for bigger sources

The solution for

idividuals in RES Act –

„net” net-metering

Doesn't pay back by sale of not used electricity

EU (subsidy) funds 2014-2020

for RES and related topics in Poland

Investment area –priority

All funds mln €*

Central (POIS) mln €*

Regional (16 RPOs) mln €*

RES only 1.200 900 300

RES & EE investment in industrial companies

400 250 150

EE in buildings 2.000 1.500 500

Intelligent grids 100 100

Low carbon (city) transport

5.000 2.200 2.800

CHP (including RES) 400 100 300

TOTAL 9.100 4.950 4.150

www.ieo.pl

1. Poland – EU partnership agreement-priority:„Transition to low carbon economy”

*rounded values

2. Other EU and Polish funds for RES:

a) Rural Ares Development Programmed (PROW 2014-2020), for farmers and rural municipalities

b) Polish Environmental funds (NFOSiGW and 16 of WFOSiGW)

EU public aid rule/RES Act : If FiT (auctions) – no investment subsidy

Conclusions

• Poland is moving from the TGC (2006-2015) system to auctioning system (2016-2020)

• Exemptions from auctions:

– Traditional biomass co-firing (app. 20 plants remain within TGC to at least 2020)

– Small scale RES (prosumer type investment) microinstallations: FiT - up to 10 kW; net metering – up to 40 kW

• The expected winners of auctioning system

– > 1 MW: biomass power (retrofits) and on-shore wind with dominant position of Polish utilities (BIG 4)

– < 1 MW: competition: biogas & biomass CHP, PV and on-shore wind (?)

• Major risks: – Unclear, not yet tested auctioning system, lack of enforcing regulations (reference

prices etc.)

– Unclear rules for grid access for PV and wind (capacity factors <4000 h/year)

• Opportunities for independent investors and power procures (IPP) – auctions up to 1 MW (25% of the total volume, excepted high prices)

– microprosumers (FiT)

– off grid/self consumptions (SMEs, farmers, municipalities) with investment support from EU and Polish environmental funds) www.ieo.pl