poised for digital growth - ub.unibas.ch

TRANSCRIPT

Poised for digital growthPreserving profitability in today’s digital world

Media & Entertainment

Global Media & Entertainment Centerii

About this report

Poised for digital growth: Preserving profi tability in today’s digital world iii

Seventy-fi ve media and entertainment company CFOs share their points of view on the digital landscape and how changing business models are shaping the future of the industry.

The CFOs we interviewed represent leading global

companies with combined annual revenues of

approximately US $300 billion. They broadly span the

media and entertainment industry in sector, size and

geography.

To augment our interview findings, we have used

secondary research and Ernst & Young analyses to

provide depth and context.

We promote an environment of openness and candor

during the interview process. As such, none of the

comments or quotes made by respondents and used

in this report have been attributed. We would like to

take a moment to thank all participants for the time

and the insights they generously provided. They were

instrumental in the creation of this report.

Global Media & Entertainment Centeriv

Thomas S. Summer

CFO

Advance Publications

Nick Priday

CFO

Aegis Group plc

Craig Ramsey

EVP and CFO

AMC Entertainment, Inc.

Kenneth J. Dale

SVP and CFO

The Associated Press

Claude Gagnon

SVP and CFO

Astral Media Inc.

Lothar Lanz

CFO

Axel Springer AG

Anthony Staffi eri

SVP Finance

Bell Canada

R. Shankar Narayan

CFO

Bennett Coleman & Co. Ltd.

Jim Hedges

EVP and CFO

ABC Television Network & Studios

Gord Nelson

CFO

Cineplex Entertainment LP

John H. Bell

CFO

Cinram International Inc.

Name withheld

Cogeco Cable, Inc.

Tom Peddie

CFO

Corus Entertainment Inc.

Michael Huseby

EVP and CFO

Cablevision Systems Corporation

Participating CFOs and executives

vPoised for digital growth: Preserving profi tability in today’s digital world

Mark F. Bowser

EVP and CFO

Cox Communications, Inc.

John Gossling

FCA, CFO

CTVglobemedia Inc.

P.G. Mishra

Group CFO

DB Corp Ltd.

Michael Gunter

EVP and CFO

Deluxe Entertainment Services Group Inc.

Bradley Singer

SEVP and CFO

Discovery Communications, Inc.

Lewis Coleman

President and CFO

DreamWorks Animation SKG, Inc.

Giles Willits

CFO

E1 Entertainment

David Ebersman

CFO

Facebook, Inc.

Brian Cassell

CFO

Fairfax Media Limited

Peter Tonagh

CFO

Foxtel Management Pty Limited

Piyush Gupta

CFO

HT Media Ltd.

Tom Fuelling

SVP and CFO

Hulu, LLC

Patrick T. Doyle

EVP and CFO

DirecTV

Frank Mergenthaler

EVP and CFO

Interpublic Group of Companies

Ian Griffi ths

Finance Director

ITV plc

Gérard Degonse

Chief Financial and Administrative Offi cer

JC Decaux SA

Peter Ingram

CFO

Keystone Entertainment

Bernie Dvorak

Co-CFO and Chief Accounting Offi cer

Liberty Global, Inc.

Christopher Shean

SVP and Controller

Liberty Media Corporation

Jim Keegan

CFO

Lions Gate Entertainment Corp.

Kathy Willard

EVP and CFO

Live Nation, Inc.

Global Media & Entertainment Centervi

Gordon Dyer

CFO

McGraw-Hill Ryerson Limited

Bedi A. Singh

President Finance and Administration, CFO, Offi ce of CEO

Metro-Goldwyn-Mayer Studios, Inc.

Clare Battellino

CFO

Photon Group Limited

Fabio Belli

Planning and Control Director

RAI Radiotelevisione Italiana SpA

Bryant Pike

CFO

Rainmaker Entertainment Inc.

MH Armour

CFO

Reed Elsevier Group plc

Shibasish Sarkar

CFO

Reliance Big Pictures

Shannon Valliant

VP Financial Operations

Rogers Media Inc.

Maureen O’Connell

EVP, Chief Administrative Offi cer and CFO

Scholastic Corporation

Thomas Hearne

CFO

Score Media Inc.

Silvio Santostefano

CFO

Sensis

Peter Lewis

CFO

Seven Network Limited

Kevin Kelleher

EVP and CFO

Sony Music Entertainment

David C. Hendler

SEVP and CFO

Sony Pictures Entertainment

Craig Harnett

SEVP and CFO

National Hockey League

R.D.S. Bawa

Group CFO

Network 18 Media & Investments Ltd.

James Follo

SVP and CFO

The New York Times Company

John P. Nallen

EVP and Deputy CFO

News Corporation

Stephen Rue

CFO

News Limited

Shad L. Burke

CFO

Outdoor Channel Holdings, Inc.

Pat O’Sullivan

CFO

PBL Media P/L

Robin Freestone

CFO

Pearson plc

Luke Littlefi eld

COO

Mitchell Communication Group

Jonathan Mariner

EVP and CFO

Major League Baseball

Participating CFOs and executivescontinued

viiPoised for digital growth: Preserving profi tability in today’s digital world

John Martin

CFO

Time Warner Inc.

David Holland

President and CEO (former CFO)

Torstar Corporation

Sean R. Gamble

EVP and CFO

Universal Studios

Andrew Hobson

CFO

Univision Communications Inc.

Norman McKeown

Group Finance Director

UTV Media plc

Rajeev Wagle

CFO

UTV Software Communications Limited

Thomas E. Dooley

SEVP, Chief Administrative Offi cer and CFO

Viacom Inc.

Julie Raffe

CFO

Village Roadshow Limited

Steven Macri

EVP and CFO

Warner Music Group

Hitesh Vakil

Director Finance

Zee Entertainment Enterprises Limited

Laurent Boissel

Group CFO

Zodiak Entertainment

Mark Vranesh

CFO

Zynga Game Network, Inc.

Tim Zahavich

CFO

St. Joseph Corporation

Kin-Man Lee

CFO

Sun Media Corporation

Lainie Goldstein

CFO

Take-Two Interactive Software, Inc.

Atul Bansal

CFO

Tata Sky Ltd.

Global Media & Entertainment Centerviii

The methodology

As part of the interview process, we asked CFOs to provide and rank their top

three responses to 11 questions. These questions focused on the industry as a

whole, as well as specific areas within each CFO’s organization.

We asked them to rank their answers in order of importance. Responses to each

question have been quantified and reflected in the bar charts that appear in this

report. For each response, the rankings are indicated by color and the combined

percentage for each response is provided. Responses that received less than a 20%

response rate from CFOs have been omitted from the charts.

1Poised for digital growth: Preserving profi tability in today’s digital world

Table of contents

2 Overview

5 Keeping pace with the digital imperative

New technology adoption has increased at a pace not known before in media

industries. Much of this growth is driven by the robust nature of broadband and

mobile platforms and consumers’ enthusiastic embrace of them.

11 Anticipating shifts in consumer demand

Shifting consumer patterns have the majority of CFOs worried; they are

influencing how their companies protect their market position and ensure the

continued viability of their business.

19 Driving growth and dealing with revenue declines

As the economy continues its recovery, CFOs are seeking to galvanize digital

growth opportunities that are relevant for their business sectors. At the same

time, they are searching for the digital business models that slow declining

digital per-unit prices and product unbundling.

27 Staying lean in a recovering economy

With declines in per-unit revenue and the global economic downturn, companies

have cut costs across the organization more deeply than ever before. Areas

once immune to cost-cutting measures — including creative business units — have

come under scrutiny.

31 Defining success

As CFOs assess the landscape, they know they face some tough challenges.

They believe that their key to success will come from balance — between digital

and traditional media, consumer demands and company offerings, investing

money in new growth opportunities, and saving money through cost cutting and

operational efficiencies.

Their focus was on the digital revolution,

which was transforming how consumers

accessed information and entertainment,

and forcing them to reexamine their

traditional media models.

The global economic downturn placed

additional pressure on media and

entertainment companies. While

companies reacted quickly with cost

initiatives, most remained focused on

investing in digital as a key strategic area

of growth.

It is now 2010 and many believe

that the worst of the recession has

passed. For this study — our fourth in

a series focused on senior media and

entertainment executives — we turn to

the CFOs of 75 leading global media and

entertainment organizations to ask them

for insights into their approaches to the

present and preparations for the future.

As they consistently share with us, their

focus is on the changing digital world and

how those changes are impacting their

customers’ media consumption habits

and their own companies’ operations.

Ultimately, as CFOs survey the

landscape, they see an equitable

balance of focus shared across investing

in digital growth, managing costs,

recruiting and retaining talent, and

achieving financial goals as key to their

company’s financial success.

When Ernst & Young last interviewed media and entertainment CEOs in 2008, few had anticipated the events that would unfold in the months that followed.

Global Media & Entertainment Center2

Overview

Digital is now. New technology — broadband and mobile in particular — is having a

powerful influence on how consumers experience information and entertainment.

The shift to digital is challenging old business models and increasingly driving

C-Suite investment decisions.

CFOs are worried about shifts in consumer patterns. Consumers’ migration to

digital is influencing how companies determine where they need to invest their

money — to protect their market position and ensure the continued viability of

their business.

Anticipating changing consumer demand means having timely and relevant

trend data. CFOs want to improve their understanding of how their customers and

their competition are navigating the current landscape, and how they can better

anticipate future developments.

CFOs are trying to manage a balance between digital growth and declining

traditional media revenue. CFOs say they are finally seeing meaningful growth in

digital revenues, but price deflation and product unbundling, combined with the

global economic downturn, are placing increasing pressure on traditional media

revenues. As a result, total industry revenues and “per unit spend” on items of

media content are stagnant.

Interactive media companies are best positioned to thrive in the next two to

three years. CFOs are not losing sight of their traditional roots. Digital earnings

are on the rise, but they are doing so at lower price points and are still small in

relation to traditional media revenue streams.

Bolt-on acquisitions will serve as a key driver of growth. In the next year or

two, CFOs are seeking to take the path of least resistance regarding growth. They

see bolt-on acquisitions as having the highest probabilities of success.

Nothing is off limits when it comes to cost savings. Areas once immune to

cost-cutting measures — including creative business units — have come under

scrutiny. They continue to reorganize for increased efficiency, and they are

exploring new opportunities for savings — opportunities that may include

outsourcing and co-sourcing.

Summary of key points

3Poised for digital growth: Preserving profi tability in today’s digital world

Global Media & Entertainment Center4

On to the report!

5Poised for digital growth: Preserving profi tability in today’s digital world

Keeping pace with the digital imperative

Technology has always been an enabler for media change. But the accelerated speed at which new technologies are being introduced and adopted by consumers is making it challenging for media and entertainment companies to keep up.

In the first 65 years of the 20th century, three significant technological advances

had an impact on the industry — radio in 1920, television in 1950 and cable in 1965.

In the late 1970s and 1980s the pace of new technology picked up speed with the

introduction of VCRs, video games, wireless devices, the personal computer, the

internet and DVD players.

Since 1998, the acceleration of new technology has reached warp speed. MP3 players,

broadband, video on demand (VOD), satellite radio, social networking, digital media

adapters, HDTV, Blu-Ray and online gaming have exploded into the marketplace.

And the technologies that were introduced in the 1980s — cellular phones, PCs and

the internet — have taken on new significance since they were launched. Once niche

market products for advanced technological wizards, they are now seen, especially in

developed world markets, as must-haves that even the most technophobic consumer

cannot live without. We no longer have cell phones, we have smart phones. PCs range

from desktop to laptop to tablet. And the internet has gone from an obscure form of

communication to a global information and entertainment phenomenon that covers any

topic in any category anywhere in the world.

New technology hits warp speed

“The degree of change in the last five years is unprecedented…As new technology

emerges it will be an interesting time for a lot of big players. Who knows what the

industry will look like in five years’ time.” – survey respondent

6 Global Media & Entertainment Center

1 Source: “Communications Industry Forecast,” Veronis Suhler Stevenson, 2003, 2005, 2007 and 2009; “Population: Households, Families, Group Quarters ,” US Census

Bureau website, www.census.gov/compendia/statab/cats/population/households_families_group_quarters.html, accessed 2 October 2009; “Statistical Abstract

of the United States,” US Census Bureau, 1996, 2003, 2006; “Falling Through the Net II: New Data on the Digital Divide,” US Department of Commerce, National

Telecommunications & Information Administration, 1998; “Worldwide Broadband Services 2005-2009,” IDC, 2005; “Worldwide Mobile Phone Forecast & Analysis,” IDC,

2003; “Worldwide Mobile Phone 2005-2009 Forecast Update,” IDC, 2005; “US Home Networking 2004-2008 Forecast,” IDC, 2005; “Worldwide and US DVR 2004-2008

Forecast,” IDC, 2004; “Worldwide & US DVR 2005-2009 Forecast,” IDC, 2005; “TV Basics: Television Households,” TV Bureau of Advertising website, citing Nielsen Media

Research, www.tvb.org/rcentral/mediatrendstrack/tvbasics/02_TVHouseholds.asp, accessed 1 September 2008; “TV, DVD and VCR Household Penetration in the US,”

eMarketer, 1 September 2005, citing data from Veronis Suhler Stevenson; “Mobile Users and Usage,” eMarketer, August 2009; “US Video Game Console Household

Penetration, 1995-2008,” eMarketer, October 2008, citing data from Odyssey LP; “Consumer Electronics Primer,” J.P. Morgan, May 2009; “Money For Nothing,” Wedbush

Securities, July 2009; “Connected Consumers, Connected Devices: 2009 Forecast,” Yankee Group, May 2009; “Basic Video Customers,” NCTA website, www.ncta.com/Stats/

BasicCableSubscribers.aspx, accessed 2 October 2009; “Survey: US tops 150 million Internet users,” Portland Business Journal, 24 October 2003, via Dow Jones Factiva;

“Entrée new,” American Demographics, 1 December 2003, via Dow Jones Factiva, © 2003 by Media Central Inc., A PRIMEDIA Company; “Social Network Marketing: Ad

Spending and Usage,” eMarketer, December 2007; “US Online Overview,” eMarketer, October 2007; “Social Networks: Five Consumer Trends for 2009,” eMarketer, February

2009; “Internet & new media - internet usage survey: focus on search,” SG Cowen, 23 May 2005; “The Digital Home: Emerging Trends in TV/PC Viewership,” eMarketer,

November 2009; “US Household Penetration of Select Media, 2001, 2006 & 2011,” eMarketer, 7 August 2007, citing data from PQ Media; “High-Definition (HD) Household

Penetration in the US,” eMarketer, 22 Sept 2006, citing data from Kagan Research; “US Broadband and Dial-Up Households and Penetration, 2000-2012,” eMarketer, 10

September 2008, citing data from FCC, MAGNA and US Census Bureau; “US Broadband and Dial-Up Households and Penetration, 2002-2014,” eMarketer, 23 September

2009, citing data from FCC, MAGNA and US Census Bureau; “US Internet Households, by Access Technology, 2009-2014,” eMarketer, 11 November 2009, citing data

from Forrester Research; “Computer use in 2003,” US Census Bureau, 2004; “MP3 Player Penetration in the US, 2002-2006,” eMarketer, 29 June 2006, citing data from

Ipsos Insight; “XM Satellite Radio Holdings Inc.,” Citi Corp., 26 October 2004; “Sirius XM Radio,” Stanford Group Company, 17 February 2009; “Digital Media And Electronic

Equipment,” SG Cowen, September 2001; “PC Household Penetration in Select Countries, 2001-2007,” eMarketer, 1 March 2008, citing data from Organisation for Economic

Co-operation and Development; “Echostar Communications Corp.,” Credit Suisse, 15 July 2004; “This Defense Not the Best Offense,” Morgan Stanley, January 2009.

2 Ibid

Perc

ent o

f hou

seho

lds

or p

opul

atio

n in

yea

rPe

rcen

t of h

ouse

hold

s or

pop

ulat

ion

in y

ear

Video games

Personal computer

Internet access

Radio

Television

Cable TV

VCR

Wireless devices

DBS

DVD player

MP3 players

Video on demand

Broadband

Satellite radio

DVRs

Social networking users

Digital media adapters

Blu-Ray

HDTV

100%

80%

60%

40%

20%

0%1920 1930 1940 1950 1960 1970 1980 2000 20101990

100%

80%

60%

40%

20%

0%1998 2000 2002 2004 2006 2008 2009

Figure 1

EY index of US media technology innovation frequency (1920-2009e1)

EY index of US media technology innovation frequency (1998-2009e2)

Poised for digital growth: Preserving profi tability in today’s digital world 7

So, when we asked CFOs what trends they thought would have the greatest impact

on their industry in the next two to three years, their answers were not surprising.

Seventy-eight percent of respondents rank new technology-enabled competitive

offerings among the top three drivers of change in the industry. The consequences of

these new technology-enabled competitive offerings, such as disruptive new business

models and shifts in consumer spending, are also cited as key drivers of change.

Notably, all of these drivers are technology-enabled and relate back to the rapid pace

of new technology adoption, which has so changed the media landscape.

Figure 2

Over the next two to three years, what trends will have the greatest impact on the

media and entertainment industry

Tech

nolo

gy c

hang

e

New technology enabled competitive offerings

Disruptive new business models

Shifting consumer spending

Global economic conditions

Reduction in marketing and advertising budgets

78%

10%0% 20% 30% 40% 50% 60% 70% 80%

Percent of total respondents (three responses provided)

Ranked #1 Ranked #2 Ranked #3

66%

53%

51%

30%

“The youth of the world are going to drive

new opportunities for new technology

and new media formats. New cost-

effective business models will gain

strength in the industry — video on

demand (VOD), internet-based and other

products will mature and new business

models will emerge.” – survey respondent

8 Global Media & Entertainment Center

The engine of change

For new technology adoption to accelerate at its current pace, it has needed a robust

platform — or two. Broadband and mobile networks are proving to have the strength

and capacity to enable the rocket-like speed of application development.

To provide a wider comparison, the Ernst & Young Digital Media Platform Saturation

(MPS) index indicates that although the global number of households has not yet

reached a 50% penetration mark, it will do so by next year. By 2013, two-thirds of

the world’s population will be connected and ready for multiplatform consumption.

Penetration rates vary by region, but overall, global penetration rates have seen a six-

fold increase in the last five years.

In 2010, we expect that 82% of US households will report having either broadband, 3G

or both mobile devices — penetration rates that have more than quadrupled in the last

five years.

Figure 3

Ernst & Young digital media platform saturation index

US and worldwide3

Index is based on the household penetration rates of broadband and 3G mobile devices. Index of 1.00 means all households have both technologies

20062005 2007 2008 2009 2010e 2011e 2012e 2013e

Dig

ital m

edia

pla

tfor

m s

atur

atio

n in

dex

0.10

0.20

0

0.30

0.40

0.50

0.60

0.70

0.80

0.90

0.200.24

0.49

0.64

0.810.82 0.83 0.83 0.84

0.07

0.130.17

0.23

0.31

0.41

0.52

0.63 0.66

US Digital Media Platform Saturation Index

Worldwide Digital Media Platform Saturation Index

In 2010, it is estimated that 27% of worldwide households will have

broadband and 55% will have 3G mobile devices.

Index = (27% + 55%) / 200% = 0.41

Penetration rates for 3G mobile devices were capped at 100% when the number of 3G mobile devices

equaled the number of households.

Survey respondents say:

“The way that consumers enjoy media

is going to change dramatically with

technological advancements in devices.”

“Technology is enabling a profound

new relationship to be established with

the customer. This is taking place at

lightning speed and the big old elephants

are having trouble keeping up.”

“Technology is driving change in how

people consume media. This raises

difficult questions in terms of how you

deliver your content and whether your

content is exclusive or not (e.g., paid

content versus ad funded).”

Peri Shamsai, Ernst & Young LLP:

“Penetration, particularly of mobile

devices is enabling the repurposing

of media brands and content in

the forms of games and snack-size

videos targeted at young consumers

resulting in new and lucrative

revenue streams.”

3 Source: “Wireless Equipment,” SG Cowen, 28 March 2006; “Mobile regional and country forecast pack,”

Ovum, December 2009; “Topline Data Forecast,” Yankee Group, October 2009; “Broadband forecast pack,”

Ovum, October 2009; “Broadband Worldwide: 2005-2011,” eMarketer, 1 March 2007; “US Broadband and

Dial-Up Households and Penetration, 2003-2015,” eMarketer, 14 January 2010, citing data from Federal

Communications Commission, MAGNA, US Census Bureau; “Paying 3G Subscribers in the US, by Company,”

eMarketer, 17 October 2005, citing data from Morgan Stanley.

Poised for digital growth: Preserving profi tability in today’s digital world 9

Broadband, cable modem and DSL speeds are increasing, while wireless

broadband is extending coverage to wider areas. In the mobile arena, the

use of smart phones is growing. These new phones combine extensive

communication, video, text and music capabilities. The result is that while

the MPS Index is growing, so too is the functionality of the devices being

measured in the Index.

“The mobile phone is quickly becoming the new internet and computer at

home, delivering information closer to the consumer and making it more

accessible. Having that content and information available on a mobile basis

will drive a shift in consumer desires and behavior.” – survey respondent

As consumers continue to adopt digital media around the world, CFOs

need to ensure that their companies’ media assets are available for digital

distribution. But they also need to make certain that as they wait for the

next technological explosion to occur, they are listening to their customers

and understanding their shifting demands and tastes. They need to be

able to adapt to changing desires by delivering content regardless of the

technology platform.

“It’s all about digital…people want content on their cell phones and other

handhelds.” – survey respondent

Global Media & Entertainment Center10

John Nendick, Ernst & Young LLP: “The phenomenal proliferation of

digital entertainment among consumers continues to challenge media and

entertainment companies. Revenues are dropping due to the unbundling

of media and the reduction of per unit pricing, challenging CFOs to identify

innovative ways to reach their financial objectives. However, as the demand

for digitally delivered entertainment continues to increase significantly,

CFOs feel optimistic about revenue potential.”

11Poised for digital growth: Preserving profi tability in today’s digital world

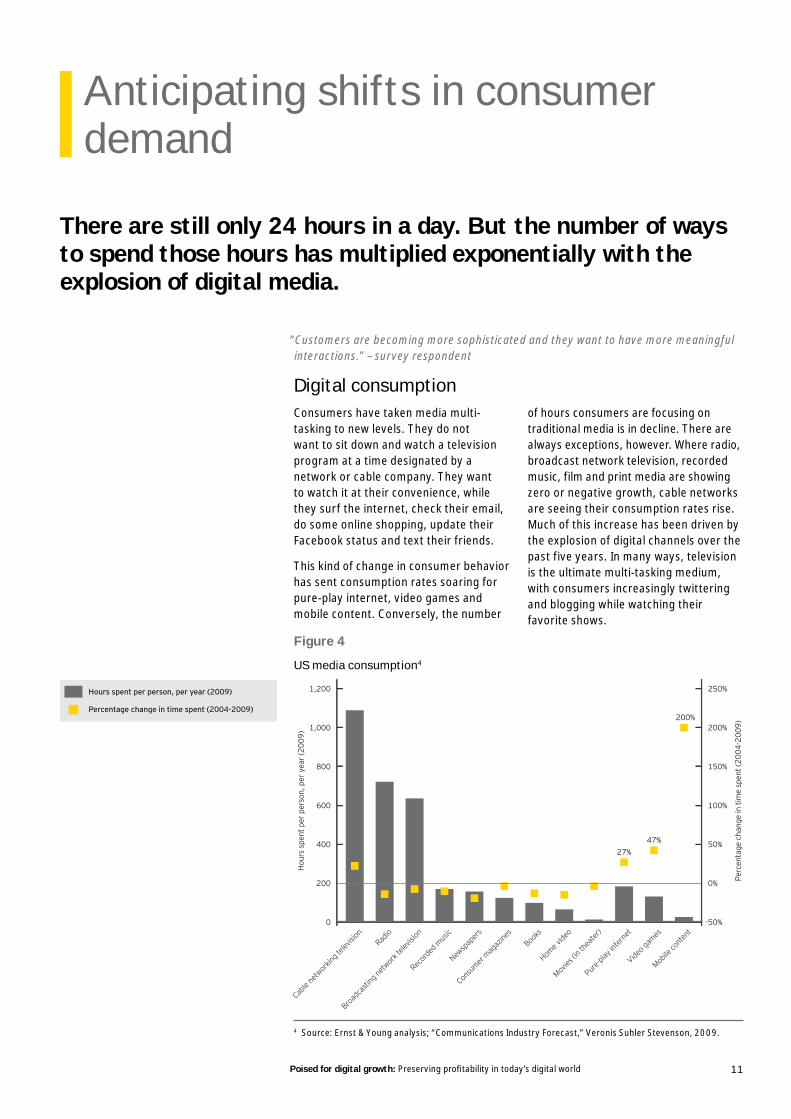

Anticipating shifts in consumer demand

There are still only 24 hours in a day. But the number of ways to spend those hours has multiplied exponentially with the explosion of digital media.

Consumers have taken media multi-

tasking to new levels. They do not

want to sit down and watch a television

program at a time designated by a

network or cable company. They want

to watch it at their convenience, while

they surf the internet, check their email,

do some online shopping, update their

Facebook status and text their friends.

This kind of change in consumer behavior

has sent consumption rates soaring for

pure-play internet, video games and

mobile content. Conversely, the number

of hours consumers are focusing on

traditional media is in decline. There are

always exceptions, however. Where radio,

broadcast network television, recorded

music, film and print media are showing

zero or negative growth, cable networks

are seeing their consumption rates rise.

Much of this increase has been driven by

the explosion of digital channels over the

past five years. In many ways, television

is the ultimate multi-tasking medium,

with consumers increasingly twittering

and blogging while watching their

favorite shows.

Digital consumption

“Customers are becoming more sophisticated and they want to have more meaningful

interactions.” – survey respondent

Figure 4

US media consumption4

Cable

netw

orkin

g tele

vision

Broadc

astin

g netw

ork t

elevis

ionRad

io

Record

ed m

usic

Newsp

apers

Consu

mer mag

azine

sBoo

ks

Home v

ideo

Movies

(in th

eater

)

Pure-pl

ay in

terne

t

Video g

ames

Mobile

conte

nt

1,200

1,000

800

600

400

200

0

250%

200%

150%

100%

50%

0%

-50%

Hou

rs s

pent

per

per

son,

per

yea

r (20

09)

Perc

enta

ge c

hang

e in

tim

e sp

ent (

2004

-200

9)

27%47%

200%

Hours spent per person, per year (2009)

Percentage change in time spent (2004-2009)

4 Source: Ernst & Young analysis; “Communications Industry Forecast,” Veronis Suhler Stevenson, 2009.

Global Media & Entertainment Center12

It is these shifts in consumer patterns, with the resulting declines in traditional media

consumption that have a large majority of CFOs worried. It is influencing how their

companies determine where they need to make investments to protect their market

position and ensure the continued viability of their business.

Protecting intellectual property

More than half of respondents cite intellectual property protection as an area of

concern. As consumption patterns change, how intellectual property rights are

protected needs to change with them.

Companies are investing in rights management systems, which enable transparency

across media asset rights and restrictions in ways not experienced in the traditional

file-cabinet approach to contract management. Companies are also enabling greater

content exploitation across their assets by coupling their rights management systems

with robust product metadata repositories and digital asset management systems,

which allow sophisticated identification, search and retrieval of content. As a result,

the digital transformation is not relegated to the consumer experience alone. It is

influencing media companies’ operating models, enabling greater exploitation of their

assets across platforms, geographies, markets and businesses.

“The brand is very powerful, so there is a need to protect, maintain and monitor it.” –

survey respondent

Figure 5

Which areas of your business are being most impacted by the evolving digital

landscape?

Migrating consumer consumption patterns

Intellectual property protection

Pricing and packaging/bundling of new products and services

Contents management infrastructure (e.g., royalties, rights exploitation)

Technology infrastructure

67%

51%

47%

38%

30%

10%0% 20% 30% 40% 50% 60% 70%

Percent of total respondents (three responses provided)

Ranked #1 Ranked #2 Ranked #3

Michael Rudberg, Ernst & Young LLP:

“The challenge for CFOs and M&E

companies is to stay on top of the

consumer migration to these new

offerings, create value and monetize

these new digital media offerings —

which is difficult given how rapidly the

consumer moves.”

13Poised for digital growth: Preserving profi tability in today’s digital world

Pricing strategies for digital media

As consumers increasingly embrace online media, the industry

is seeking to capitalize on the trend by monetizing digital media

consumption. As illustrated in Figure 6, the number of users

creating a social network profile has increased from a modest

27% in 2006 to 63% in 2009. Similarly, the compound annual

growth rate (CAGR) of streamed videos has risen by a whopping

108% in the same time period.

But trying to create value by monetizing digital offerings is not

easy in a world where consumers are always looking for the

next new platform, “killer app” or creative content.

Access to information

Understanding that always knowing what is around the

corner is one of the biggest challenges a CFO faces in media

and entertainment, we asked them what they need to stay

competitive. CFOs point to greater insights into consumer

trends and the ability to benchmark data against their peers

and competitors.

Respondents say that getting real-time information into where

consumers are heading will help their companies be flexible in

adapting product offerings, keep pace with current trends and

anticipate future demands.

Figure 6

Percentage of worldwide internet users who have created a

social network profile5

Perc

enta

ge o

f int

erne

t use

rs

0%

10%

20%

30%

40%

50%

60%

70%

2006 2007 2008 2009

27%

36%

57%

63%

Streamed videos, by selected sites, US6

Stre

amed

vid

eos

(in b

illio

ns)

0

2

4

6

8

10

12

14

August 2006

November 2007

November 2008

November 2009

Google sites (primarily YouTube)HuluYahoo

1.5

3.3

5.6

13.6

CAGR 108%

5 Source: “Social Network Ad Spending: 2010 Outlook,” eMarketer, December 2009, citing data from Universal McCann.

Note: n=22,729; ages 16-54; daily or every other day internet access.

6 Source: “Top 10 Online Video Properties among US Internet Users, Ranked by Streams Initiated, August 2006,” eMarketer, 19 October 2006; “Top 10 Online Video

Properties Among US Internet Users, Ranked by Videos Viewed, November 2007,” eMarketer, 17 January 2008; “Top 10 Online Video Properties Among US Internet

Users, Ranked by Videos Viewed, November 2008,” eMarketer, 5 January 2009; “Top 10 Online Video Properties Among US Internet Users, Ranked by Videos

Viewed, November 2009,” eMarketer, 5 January 2010; all citing data from comScore, Inc.

14 Global Media & Entertainment Center

Survey respondents say:

“One of the challenges we have as CFOs

is how do we keep ourselves on the tips

of our toes such that when things change

we are well-positioned to respond.”

“Real-time customer data and trends are

more important than ever. We need to be

able to get data, mine data and translate

the data in order to compete in this

changing market.”

“The winners will be the ones who can

predict most accurately what the

consumption will be.”

Figure 7

What kind of information would help you to be more

effective as a CFO?

10%0% 20% 30% 40% 50% 60% 70%

Insights intoconsumer trends

Benchmarking key metrics against peers/competitors

Competitive intelligence

Real-time data and analyses

Benchmarking key metrics across industries

62%

Percent of total respondents (three responses provided)

Ranked #1 Ranked #2 Ranked #3

Operating and capital management information

60%

53%

36%

27%

21%

They also point to the need to be able to benchmark data against their peers and

their competitors. With the colossal growth rates of sites like Hulu and Google,

media and entertainment companies are finding that their competition is no

longer confined to other traditional media players. They also have to worry about

companies with new media platforms that have burst into their space from garages,

basements, grad schools and high schools around the world.

Survey respondents say:

“Because of our parent/structure we’re so inwardly focused that perhaps we lose sight

of how we’re actually performing against our peers or other industries.”

”We would be interested in understanding the pricing strategy of our competitors.”

“Benchmarking with peers and competitors is always important to substantiate how

you are performing.”

“Benchmarking across industries will allow us to gain better insights and understanding

into the industry and how to enable the transition. What are packaged goods

companies doing, or consumer products or retail?”

15Poised for digital growth: Preserving profi tability in today’s digital world

Tom Connolly, Ernst & Young LLP:

“Interactive media companies are

appealing areas for investment

because of their revenue

growth potential and leverage in

expanding margins.”

Positioning for success

For the past six years we have been asking C-Suite executives which companies they

thought were best positioned to thrive in the future. Each time their answers have

been the same: Internet and interactive media. But where it was tied with new content

creation in our 2008 CEO survey, CFOs today select it by almost a two to one margin

over all other media channels.

Figure 8

What kind of media and entertainment companies are best positioned to thrive in

the future?

10%0% 20% 30% 40% 50% 60% 70%

Internet/interactive media

Conglomerates

Cable operators

Electronic gaming

Cable networks/channels

64%

38%

38%

37%

37%

Percent of total respondents (three responses provided)

Ranked #1 Ranked #2 Ranked #3

Traditional content creation (studio) 36%

Survey respondents say:

“The best positioned companies are

those that understand that digital is …

part of a revolution.”

“Interactive media and gaming

companies are best positioned to

thrive in the future. Consumers are

more about demand, personalization

and interactivity. These companies

have the make-up to succeed and have

employees who are more innovative.”

“Younger generations, which have more

access to the internet and technologies,

will position certain companies to thrive

with internet- and interactive-based

media. These companies will benefit

from more cost effective ways to

distribute their content and have a direct

to consumer relationship — which should

result in a better business model, faster

access to content and at costs that are

much cheaper than traditional business

models today.”

Global Media & Entertainment Center16

CFOs are not using growth or revenues

as the only measures of success.

Although EBITDA — earnings before

interest, taxes, depreciation and

amortization — is not a standardized term

under generally accepted accounting

principles and may be calculated

differently from one company to

another, it nevertheless serves as a

widely available metric used by analysts,

investors and reporting companies

to look at the financial performance

of companies in the media and

entertainment industry.

Figure 9 summarizes the results of an

Ernst & Young study of approximately

95 leading global companies and

conglomerates in 11 distinct M&E

sectors that, in the aggregate, generated

over $125 billion of EBITDA in 2009.

The line graph depicts the EBITDA

margin percentage for each sector over

the period 2005 through 2009. The

data on the right reflects the compound

annual growth rate (CAGR) in EBITDA

dollars over the same period.

For the years 2005-2009, interactive

media companies posted strong EBITDA

margins that, in 2009, were growing

and second only to the EBITDA margins

of cable operators. For the same

period, interactive media companies

can also boast a 19% CAGR in EBITDA

dollars — the highest of all media and

entertainment sectors. No wonder,

CFOs ranked internet and interactive

media companies as best positioned for

future success.

Some sectors, in particular the cable

operators and cable networks, showed

both healthy EBITDA dollar CAGR growth

(14% and 10%, respectively, for the

period 2005-2009), and high EBITDA

margins (approximately 40% and 30%,

respectively in 2009). Other sectors

enjoyed relatively high EBITDA margins

in a mature market, but declining EBITDA

dollar CAGR growth. For example,

the radio broadcast sector generated

EBITDA margins of over 40% in 2005,

declining to approximately 25% in 2009,

and suffered an EBITDA dollar CAGR of

-18% from 2005-2009.

Companies in the electronic games

sector generated relatively high margins

in 2005, but exhibited inconsistent and

declining margins in the subsequent

years. Not surprisingly, as a result of

the sector’s stronger performance in

2005, the electronic games sector

posted an EBITDA dollar CAGR of -8%

for the period. The music and publishing

sectors, not surprisingly, have shown

relatively consistent EBITDA margins

with very little EBITDA dollar CAGR

growth for the period 2005-2009.

Even as many media and entertainment

sectors appear to be positioned for

future success, their future is not without

challenge. As media and entertainment

companies experiment with new business

models to optimize their opportunities

within the digital marketplace, they need

to focus on maintaining revenues in the

areas that have been their mainstay

in decades past. CFOs cannot forsake

traditional earning in their quest for the

digital jackpot.

17

Figure 9

EBITDA margin percentage* (2005-2009)7

Poised for digital growth: Preserving profi tability in today’s digital world

7 Source: EBITDA data presented is based on publicly available company and analyst information for the years of 2005 to 2009.

* “EBITDA margin percentage“ is EBITDA dollars divided by revenue dollars.

** “2005-2009 CAGR (EBITDA $)” is the compound annual growth rate of EBITDA dollars.

30%

25%

20%

15%

10%

5%

0%

35%

40%

45%

EBIT

DA m

argi

n pe

rcen

tage

2005-2009 CAGR (EBITDA $**)

Interactive media: 19%

Satellite TV: 17%

Cable operators: 14%

Cable networks: 10%

Conglomerates: 4%

Film and TV production: 3%

Music: 3%

Publishing: 1%

TV broadcast: -4%

Electronic games: -10%

Radio broadcast: -18%

20062005 2007 2008 2009

Howard Bass, Ernst & Young LLP: “CFO’s see growth in new

distribution channels, products and services. Publishers and similar

content companies are embracing the fact there are almost 2 billion

digital media users to leverage their content and core products and

services to the web, mobile devices and electronic gaming globally.”

Global Media & Entertainment Center18

19Poised for digital growth: Preserving profi tability in today’s digital world

Driving growth and dealing with revenue declines

As the economy continues its recovery, CFOs are seeking to take the path of least resistance when it comes to growth opportunities. At the same time, they are searching for the digital business model that slows declining revenues from digital pricing and product unbundling.

“New digital distribution channels are a wonderful way to grow but monetization is the

key word.” – survey respondent

Knowing that interactive media is the place to play, when asked where they saw

the greatest opportunities for revenue growth in the next one or two years, 73% of

respondents indicated they will seek to invest in new distribution channels.

CFOs rank new products and services as their next target area for growth — with a

caveat. The opportunities they pursue will target digital channels. This is consistent

with everything we heard from CFOs throughout the study.

New geographic markets — a significant area of focus for CEOs in our last study — seem

less of a priority for CFOs today. In 2008, when we asked CEOs how large a part

emerging markets would play in their strategic growth plan over the next two to five

years, 89% saw those markets as key to their future growth. In this year’s study, new

geographic markets ranks third in importance, and some acknowledge that pushing into

new markets will play a role in their strategy.

Figure 10

Where do you see the greatest opportunities from a “go-to-market” or revenue

growth perspective over the next one to two years?

10%0% 20% 30% 40% 50% 60% 70% 80%

New distribution channels (e.g., digital)

New products and services

New geographic markets

Brand enhancements

New pricing strategies

73%

60%

53%

30%

26%

Percent of total respondents (three responses provided)

Ranked #1 Ranked #2 Ranked #3

Expanded licensing partnerships 23%

Survey respondents say:

“Distribution will become more

unconstrained by a tethered medium.

People will watch what they want,

where they want to watch it.”

“New distribution channels are critical

right now. People have to make

decisions and commitments.”

“The primary impact will be from new

business models designed around

digital distribution.”

20 Global Media & Entertainment Center

Looking for the easy deal

Not surprisingly, mergers and acquisitions

(M&A) transactions slowed for media

and entertainment companies in 2009.

Although CEOs expressed a desire in

our last study to invest in mergers that

would combine top technology with ready

access to the audience, because of the

economic downturn most companies

shelved M&A plans that could not meet

high return on investment hurdles or

increase share prices from day one. New

media companies sometimes proved an

exception, but CFOs noted that many of

the most attractive new media properties

had already been acquired.

However, even though the number of

announced transactions declined for

most subsectors of the industry, a few

high-priced deals pushed the average deal

value higher than previous years. These

included:

Comcast’s acquisition of NBC

Universal, announced at $14 billion

The Walt Disney Company’s $3.9 billion

acquisition of Marvel Entertainment

UPC Germany’s $3 billion acquisition

of Unitymedia

CPP Investment Board’s $2

billion acquisition of Macquarie

Communications

Figure 11

Global media and entertainment M&A transactions8

(Based on announced deals with disclosed transaction values)

8 Source: Ernst & Young analysis of Capital IQ data.

100

0

200

300

400

500

600

700

800

900 $250

$200

$150

$100

$50

$0

Num

ber o

f dea

ls

Ave

rage

dea

l val

ue (i

n m

illio

ns)

2006 2007 2008 2009

Broadcasting and cable TV

Digital

Publishing

Filmed entertainment

Average deal value (in millions)

$61

740

843

574

398

$194

$169$191

21Poised for digital growth: Preserving profi tability in today’s digital world

When we asked CFOs about their company’s acquisition strategy in the next year

or two, the majority indicated that M&A activity will focus primarily on bolt-on

acquisitions that could add depth to existing portfolios and improve profit margins.

They felt that these types of transactions are most likely to succeed and the easiest

ones to integrate into the existing structure of their organizations.

Figure 12

If your company were to acquire a business over the next one to two years, what

would that acquisition more likely reflect?

10%0% 20% 30% 40% 50% 60% 70% 80%

A “bolt on” to an existing operation to improve margins and depth of product

A new complementary business

An acquisition from outside your home country

An acquisition in the distressed markets (pre- or post-bankruptcy filing)

81%

55%

38%

32%

Percent of total respondents (three responses provided)

Ranked #1 Ranked #2 Ranked #3

Survey respondents say:

“Our most successful deals have been

small bolt-ons. Our larger attempts have

been unsuccessful to date, mainly as we

have smothered these businesses in our

corporate processes.”

“Bolt-on acquisitions are just easier to do;

they have fewer integration challenges.”

“We would look for an acquisition that

would take us deeper into each of our

current verticals.”

Global Media & Entertainment Center22

As media companies move into the

digital marketplace, there is inevitably

a significant impact on key areas of

financial reporting that are top-of-mind

for CFOs. Revenue recognition is an area

of concern. With an increasing number

of channels across which media and

entertainment companies can distribute

their assets, we are seeing that revenue

recognition is changing dramatically. This

is becoming more complex with respect

to timing and allocation issues.

New products and services in the

digital market are also resulting in

highly complex revenue recognition

requirements. As the number of

channels grows, CFOs need to review

revenue recognition policies to ensure

that they properly reflect the new

revenue streams.

New digital revenue streams may be

the “long tail” for many media assets.

Digital distribution channels may enable

companies to exploit older titles or

products through new media and may

represent a hidden demand for content

that was previously inaccessible.

The move to digital may impact more

than just revenue recognition. New

revenue streams may mean companies

need to reevaluate their amortization

of content and programming costs.

They may need to revisit their risk

assessments, as digital initiatives bring

new challenges in rights management,

intellectual property protection, and

are increasingly demanding the audit of

third-parties for transparency. Among

other things, they want access to

click-through rates, costs per thousand

impressions in ad buys and details to

support royalty payments.

Addressing the complexities of revenue recognition

23Poised for digital growth: Preserving profi tability in today’s digital world

While digital and online media are

key areas of growth — areas where

consumers are spending their time

and money — most traditional media

consumption is either flat or in decline.

Between 2004 and 2009 the number of

hours spent per person using traditional

media has seen either zero or negative

growth, except for cable networks (see

Figure 4). For traditional media, those

lost hours are translating into reduced

profit margins.

The decline in consumer end-user

spending began in the late 1990s with

online piracy of music, which resulted

in a 32% fall in global revenues. That is

expected to level out in the near future

as the number of entertainment units

being consumed increases because of

digital adoption (see Figure 13). But the

music industry serves as a cautionary

tale for other media and entertainment

sectors that are poised to experience

a similar revenue squeeze. In the

publishing industry, for example, price

points for books, which had historically

been $24.99, $19.99 or $14.99 are now

appearing as eBooks for $9.99.

As shown by the yellow trend line in

Figure 13, declining price points are

having a significant impact on the

aggregate consumer spend across music

and video purchases.

Additional downward pressure on

pricing has come in the form of product

unbundling. Where consumers once

ordered from a “prix fix” menu, they

are now able to order “à la carte.” For

example, music companies went from

a $14.99 bundled package of singles to

selling a single song for $0.99. Similarly,

episodes of a television series, once

only available for purchase on DVD as

a season, are now available as a single

unit of entertainment. The Kindle, Sony

Reader and iPad may usher in a similar

pricing challenge for publishers, and

some analysts are beginning to warn

that moving broadcast television content

from the television to the personal

computer — and thus unbundling it —

may diminish the industry’s advertising

pricing power and reshuffle the notion

of a bundled cable subscription service,

once televisions are broadly connected

to the internet.

There are a multitude of factors that

depress the price of content and that is

part of what is making it so hard for media

and entertainment companies to find the

right digital business model — whether it

is advertising, subscriptions or a hybrid.

CFOs across the industry worry about

how they are going to migrate into the

digital space, at what price point and how

it will impact their business in the near

and long term.

Managing revenue declines

Global Media & Entertainment Center24

Figure 13

Units consumed, and total end-user spending, for online and physical music and

home video, US9

9 Source: Ernst & Young analysis; “Communications Industry Forecast,” Veronis Suhler Stevenson, 2009; “The

Pause Button 3-D: Studio Benefits Unclear; Lowering DVD Sales Again,” Morgan Stanley, 26 October 2009.

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Uni

ts c

onsu

med

(in

mill

ions

)

Tota

l end

-use

r spe

ndin

g (in

bill

ions

)

2009e 2010e 2011e 2012e0

$5

$10

$15

$20

$25

$30

$35

$40

$0

Digital home video downloads (purchase and rental)

Digital music downloads (singles and albums)

Physical CD shipments (singles and albums)

Physical home video (rental and purchases)

Total home video and music end-user spending (in billions)

621 514 385 257 205 178 161

$36.4

614

3,562

$34.5

852

3,545

$31.6

1,090

3,544

$29.4

1,258

3,557

$28.5

1,417

3,566

$27.6

491

3,517

1,625 1,904

$27.5

808

3,472

2006 2007 2008

25Poised for digital growth: Preserving profi tability in today’s digital world

David McGregor, Ernst & Young: “Our media and

entertainment clients across the board are actively reviewing

how they are going to migrate into the digital space and at what

price point, and what the impact will be on their core business

two, five, ten years down the road.”

Global Media & Entertainment Center26

27Poised for digital growth: Preserving profi tability in today’s digital world

Staying lean in a recovering economy

With declines in per-unit revenue and the global economic downturn, companies have cut costs across the organization more deeply than ever before. Areas once immune to cost-cutting measures — including creative business units — have come under scrutiny.

“We need to continually look at

structures and processes: shared

services for finance, IT, research, call

centers and even editorial content.” –

survey respondent

One surprising result from this study

is the speed with which media and

entertainment CFOs cut costs when

the economic crisis began. Most

CFOs state that they have already

cut the majority of fat from their

organizations. Furthermore, CFOs

express a commitment to keeping

costs down as the economy rebounds.

As we emerge from the recession,

CFOs continue to search for cost-

saving opportunities. They are

reorganizing already lean operations

to improve performance. And they

are exploring new opportunities

for savings through shared service

centers, outsourcing and off-shoring

where appropriate — all without

compromising the quality of key talent

they know is necessary to take their

companies to the next level.

Figure 14

Where do you see the greatest opportunities for cost savings over the next

one to two years?

10%0% 20% 30% 40% 50% 60%

Process improvement

Improved sourcing/outsourcing

Integration and optimization of technologies

Rethinking organizational structure

Control content and marketing costs

56%

51%

47%

45%

41%

Percent of total respondents (three responses provided)

Ranked #1 Ranked #2 Ranked #3

Increased automation 23%

28 Global Media & Entertainment Center

CFOs feel they have identified all cost efficiencies available in a business-as-usual

context. They are now looking at different ways of performing day-to-day activities that

can drive costs out of the business without taking away any of the service or delivery.

Process improvement and enhanced sourcing and outsourcing receive the largest

numbers of votes overall. But when looking at responses in the context of ranking the

number one choice in isolation, controlling content and marketing costs ranks highest

for more than 30% of CFOs.

“It’s a balancing act to control content and marketing costs. We are scrutinizing costs

but it’s hard to find the right digital business model so we don’t lose market share.” –

survey respondent

Survey respondents say:

“We have ripped our cost down to the

lowest level possible unless we make a

cultural change in the organization.”

“Moving to outsource more of the

company’s activities should provide

significant cost savings.”

“There are still a lot of costs to take out

of the back office, particularly in IT

and finance.”

“We need to step back and strategically

look at the business-heavy costs

as opposed to continuing to nibble

around the edges.”

Figure 15

Common media and entertainment outsourcing initiatives

Accounting and

Finance

Accounts payable (e.g., vendor master data management,

payables processing, disbursements processing); accounts

receivable (e.g., billing); payroll; general ledger maintenance;

financial and management reporting

Supply chain Printing and production of books, CDs and DVDs

Distribution Warehousing, picking and packing of retail products

IT Application

Development

Digital content creation, media asset management, community

networking and cross-brand programming.

Poised for digital growth: Preserving profi tability in today’s digital world 29

Bruno Perrin, Ernst & Young et Associés: “CFOs are looking

for different ways to sustain recent cost reductions, while

maintaining the value and brand of the business. Shared

service centers, outsourcing, and off-shoring are appealing

ways to improve efficiency of back-office functions.”

Global Media & Entertainment Center30

31

Defining success

In our 2008 study, CEOs told us they saw the role of the CFO changing in response to the shifting media landscape — that they were looking for more. CEOs were demanding greater insight, analysis and planning, a more effi cient fi nance function, and more open and accurate accounting.

“The role of the CFO is no longer purely

accounting-based. He/she needs to be

updated about technological advancements,

legal issues, copyrights and other financial

aspects.” – survey respondent

Figure 16

Let’s imagine it’s two years from now and you are celebrating a wildly successful

performance as the CFO at your company. What would you think you would identify

as having been your keys to success?

Poised for digital growth: Preserving profi tability in today’s digital world

10%0% 20% 30% 40% 50% 60% 70%

Met, or exceeded, the company’s financial performance goals

Recruited, developed and retained the right talent

Successfully implemented operational efficiencies resulting in cost reductions

Established myself as a strategic partner within the company

Enabled the company to develop a successful business strategy

Successfully managed the company’s balance sheet

40%

56%

68%

27%

23%

22%

Percent of total respondents

I have...

It is interesting then to compare how CFOs view themselves today and what they

think will make them successful. When asked how they would define their keys

to success, CFOs cited implementing operational efficiencies that reduced costs,

recruiting and retaining the right talent, and achieving or surpassing financial

performance targets.

This shift in focus from the strategic to the operational directly corresponds to

the economic downturn, which forced CFOs to turn their attention to operational

efficiencies.

32 Global Media & Entertainment Center

Survey respondents say:

“The key to success will be to have

improved our cost structure through the

use of technology and process synergies.”

“We will succeed if we continue to be a

lean, not fat, organization.”

“The CFO should not be in the back office

looking at data. They need to have their

heads up looking at the future to improve

the decision-making of the business.”

“Doing what we are currently doing will

not get us there — even if we do it better.

We need to change.”

As CFOs assess the landscape, they

know they face some tough challenges.

New technology and customer

consumption patterns are evolving at

lightning speed, making it hard for the

industry to adapt. Traditional business

models that have rooted the industry for

decades are beginning to decay, while

new models have yet to gain traction.

And then there was the global economic

crisis, which placed CFOs in the position

of having to make some hard decisions

around cost savings and cost cutting.

Finding the balance

In the chaos that swirls around them,

CFOs are seeking a calm that comes

from balance — among digital and

traditional media, consumer demands

and company offerings, investing

money in new growth opportunities,

and saving money through cost-cutting

and operational efficiencies.

It is a tough balance to achieve, but

CFOs feel certain that their success

depends on it.

“Success will be finding the right balance

between growth and profitable growth.” –

survey respondent

33Poised for digital growth: Preserving profi tability in today’s digital world

Farokh Balsara, Ernst & Young Pvt. Ltd.: “Most media companies

have targeted the low-hanging fruits, cutting non-essential costs

across the board. The focus has now turned to “profitable growth”

through operational efficiencies such as process improvement,

outsourcing, shared services and alliances. These areas are more

difficult to achieve as they may require structural and cultural shifts

within the organization.”

Global Media & Entertainment Center34

Poised for digital growth: Preserving profi tability in today’s digital world 35

Contacts

Telephone Email

Global Media & Entertainment CenterJohn Nendick, Global Sector leader (Los Angeles, US) + 1 213 977 3188 [email protected]

Sylvia Ahi Vosloo, Associate Director, Marketing (Los Angeles, US) + 1 213 977 4371 [email protected]

Karen Angel, Global Implementation Director (Los Angeles, US) + 1 213 977 5809 [email protected]

Yooli Ryoo, Knowledge Manager (Los Angeles, US) + 1 213 977 4218 [email protected]

Peri Shamsai, M&E Senior Manager (New York, US) + 1 212 773 9172 [email protected]

Pam Walker, Events Coordinator (Los Angeles, US) + 1 213 977 3046 [email protected]

Global Area Leaders and Advisory Panel MembersFarokh T. Balsara (Mumbai, India) + 91 22 4035 6550 [email protected]

Mark Besca (New York, US) + 1 212 773 3423 [email protected]

Neal Clarance (Vancouver, Canada) + 1 604 648 3601 [email protected]

Noriharu Fujita (Tokyo, Japan) + 813 3503 1355 [email protected]

David McGregor (Melbourne, Australia) + 613 9288 8491 [email protected]

Gerhard Mueller (Munich, Germany) + 49 891 4331 13108 [email protected]

Bruno Perrin (Paris, France) + 33 1 46 93 6543 [email protected]

Michael Rudberg (London, England) + 44 207 951 2370 [email protected]

Global Service Line Leaders and Advisory Panel MembersMark J. Borao, Global M&E Advisory Services leader + 1 213 977 3633 [email protected]

Thomas J. Connolly, Global M&E Transaction Advisory Services leader + 1 212 773 7146 [email protected]

Alan Luchs, Global M&E Tax leader + 1 212 773 4380 alan.luchs @ey.com

Chris Pimlott, Global M&E Tax leader + 1 213 977 7721 [email protected]

Advisory Panel MembersHoward Bass + 1 212 773 4841 [email protected]

Glenn Burr + 1 213 977 3378 [email protected]

Vincent de La Bachelerie, Global Telecommunications leader + 33 1 46 93 6205 [email protected]

Pat Hyek, Global Technology leader + 1 408 947 5608 [email protected]

Bud McDonald + 1 203 674 3510 [email protected]

Ken Walker + 1 805 778 7018 [email protected]

Ernst & Young

Assurance | Tax | Transactions | Advisory

About Ernst & Young

Ernst & Young is a global leader in assurance, tax, transaction and

advisory services. Worldwide, our 144,000 people are united by

our shared values and an unwavering commitment to quality. We

make a difference by helping our people, our clients and our wider

communities achieve their potential.

Ernst & Young refers to the global organization of member firms

of Ernst & Young Global Limited, each of which is a separate

legal entity. Ernst & Young Global Limited, a UK company limited

by guarantee, does not provide services to clients. For more

information about our organization, please visit www.ey.com.

© 2010 EYGM Limited.

All Rights Reserved.

EYG No. EA0040

In line with Ernst & Young’s commitment to minimize

its impact on the environment, this document has

been printed on paper with a high recycled content.

This publication contains information in summary form and is

therefore intended for general guidance only. It is not intended to

be a substitute for detailed research or the exercise of professional

judgment. Neither EYGM Limited nor any other member of the

global Ernst & Young organization can accept any responsibility for

loss occasioned to any person acting or refraining from action as

a result of any material in this publication. On any specific matter,

reference should be made to the appropriate advisor.