playing in extra time - robeco outlook 2018 lukas daalder · lukas daalder @ldaalder for...

TRANSCRIPT

For professional investors only @ldaalderLUKAS DAALDERC I O R O B E C O I N V E S T M E N T S O L U T I O N S

OUTLOOK 2018

PLAYING IN EXTRA TIME

TERUGBLIK OP VORIG JAAR

Brexit, Amerikaanse en Franse verkiezingen

POPULISMEuitgewerkt?

QUANTITATIVE EASINGen onzekerheid

SOMBERHEID

VORIG JAAR

WAT IS ER VERANDERD?IMF World Economic Outlook

Tijd

Opt

imis

me

‘Too slow for too long’

‘Uncertainty aftermath U.K. Referendum’

‘Gaining Momentum?’

‘A Firming Recovery’

‘Seeking Sustainable Growth’

July ‘16 April ‘17 July ‘17 Oktober ‘172016 2017

?

April ‘16source: IMF, World Economic Outlook

18,8%

1 YR 3 YR 5 YR

1 YR 3 YR 5 YR

Fixed Income EMD Hard Currency (unh. in EUR) German Government Bonds EMD Local Currency (unh. in EUR) Japan Government Bonds Global Government Bonds US Government Bonds Italy Government Bonds France Government Bonds Spain Government Bonds Investment Grade Europe Global Investment Grade Bonds Global High Yield Investment Grade US

Global real estate Oil Index Gold Emerging Markets (in EUR) Global Equities (local)

6,1%

hoog risico

AANDELEN & CREDITS

MARKT IN LIJN MET OPTIMISME

source: Bloomberg, Robeco

17,9%

6,4%

3,7%

2,6%

1 YR 3 YR 5 YR

1 YR 3 YR 5 YR

Fixed Income EMD Hard Currency (unh. in EUR) German Government Bonds EMD Local Currency (unh. in EUR) Japan Government Bonds Global Government Bonds US Government Bonds Italy Government Bonds France Government Bonds Spain Government Bonds Investment Grade Europe Global Investment Grade Bonds Global High Yield Investment Grade US

Global real estate Oil Index Gold Emerging Markets (in EUR) Global Equities (local)

MARKT IN LIJN MET OPTIMISME

hoog risico

AANDELEN & CREDITS

de daling lijkt eindelijk ten einde

OBLIGATIEMARKTEN

1,4%

1,2%

1,1%

0,7%

0,7%

0,0%

-0,9%

source: Bloomberg, Robeco

2018HET NIEUWE JAAR

OVERWAARDERING

RISICO IN DE MARKT

RISICO 1: OVERWAARDERINGS&P 500240

220

200

180

160

140

120

100

802011 2012 2013 2014 2015 2016

source: Bloomberg, Robeco

S&P 500 earningsS&P 500

RISICO 1: OVERWAARDERINGCAPE45

40

35

30

25

20

15

10

5

01885 1890 1895 1900 1905 1910 1915 1920 1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

1901:Panic of 1901

1921:Depression of 1921

1929:Black Tuesday

1966:Crash of 1966

1981:Early 1980’s recession

2000:Dotcom Bubble

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

source: Shiller database

Pric

e Ea

rnin

g Ra

tio (

CAPE

, P/E

10)

RISICO 1: OVERWAARDERINGCAPE

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

45

40

35

30

25

20

15

10

5

0

1.6

1.4

1.2

1.0

0.8

0.6

0.4

0.2

Shiller CAPE

Q Ratio (RH)

Buffett Indicator (RH)

source: Shiller database

RISICO 1: OVERWAARDERINGEuropese obligaties markt nog steeds overgewaardeerd

14

-2

0

2

4

6

8

10

12

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

German 10Y bond yield (actual)10Y fair value estimate

source: Thomson Reuters Datastream, Robeco

Draghi: “whatever it takes”

RISICO 1: OVERWAARDERINGGlobal Credit Spread

0

1

2

3

4

6

5

2000 2002 2004 2006 2008 2010 2012 2014 2016

lang termijn gemiddelde

source: Bloomberg, Robeco

RISICO 1: OVERWAARDERINGGlobal High Yield Spread

0

4

8

12

16

20

2000 2002 2004 2006 2008 2010 2012 2014 2016

lang termijn gemiddelde

source: Bloomberg, Robeco

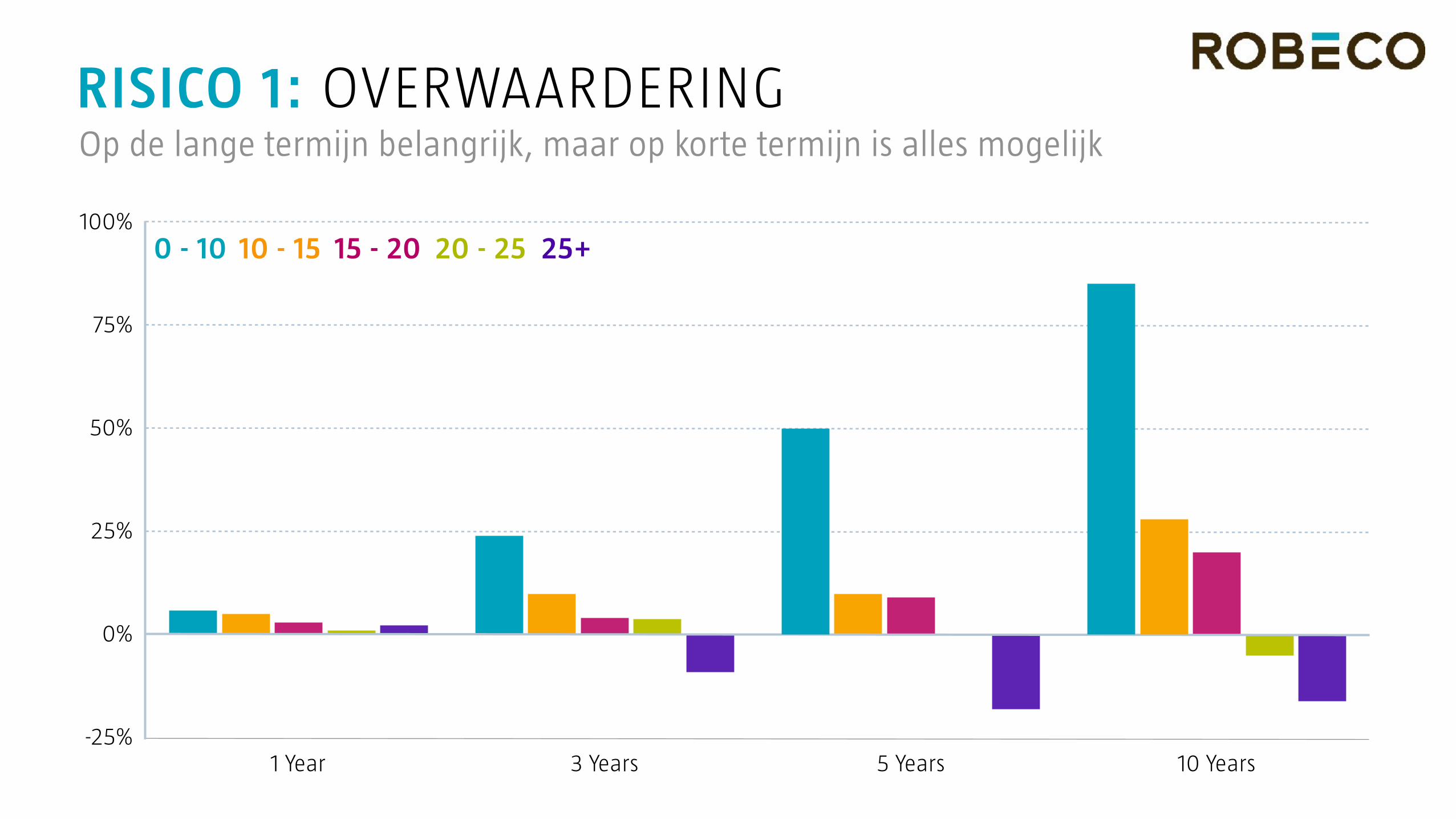

RISICO 1: OVERWAARDERINGOp de lange termijn belangrijk, maar op korte termijn is alles mogelijk

100%

75%

50%

0%

25%

-25%1 Year 3 Years 5 Years 10 Years

0 - 10 10 - 15 15 - 20 20 - 25 25+

OVERWAARDERING LATE CYCLE

RISICO IN DE MARKT

RISICO 2: LATE CYCLE FOR CREDIT CYCLEVerslechterde kredietkwaliteit

20%Improving but ignored

20%Attractive, but no takers

60%Exhaustion, disbelief and

demorilization

30%Solid underlying performance

50%Abundant bargains

20%Doubt, reflection and conversion

40%Sweet summer of growth

30%Willingness to pay up

30%Faith, hope and charity

20%Optimistic, long-

duration projections

20%Revised models justify stretching

60%Euphoria, greed

and extrapolation

30%Over-awareness of

deteriorating conditions

20%Shocked recognition of outlandish prices paid

50%Fear, panic and

loathing

Fundamentals

Valuation

Psychology, Technical and Liquidity

Market Phase Bottom Early Stage Recovery Mid Stage Bull Market Peak of Bull Market Bear Market

EMERGING CREDITS

INVESTMENT GRADE

EUROPEAN HIGH Y IELD

GLOBAL HIGH Y IELD

source: Robeco, Morgan Stanley, June 2017

RISICO 2: VERSLECHTERDE KREDIETKWALITEITLate cycle for credit cycle2.40

5.40

4.90

4.40

3.90

3.40

2.90

2011 201720162015201420132012

BBa Caa/Ca

source: Moody’s

OVERWAARDERING LATE CYCLE CHINESE SCHULD

RISICO IN DE MARKT

Start of the euro crisis

Start of the Asian crisis

RISICO 3: CHINESE SCHULD NADERT DRAAIPUNTDe eeuwige belofte van a crash waiting to happen

??

84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14 160

50

100

150

200

250

Start of the ‘lost decade’

Japan Thailand Spain China

source: Expected Returns

Priv

ate

sect

or to

tal d

ept a

s %

of G

DP

OVERWAARDERING LATE CYCLE CHINESE SCHULD MONETAIR BELEID

RISICO IN DE MARKT

RISICO 4: DRAAI IN MONETAIR BELEID Van quantitive easing naar quantitive tightening

752008

95

115

135

155

175

195

215

235

255

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

S&P 500 (r)Fed balance sheet (l)

2008 = 100

75

125

175

225

275

source: Bloomberg, Robeco

OVERWAARDERING LATE CYCLE CHINESE SCHULD MONETAIR BELEID

RISICO IN DE MARKT

OVERWAARDERING LATE CYCLE CHINESE SCHULD MONETAIR BELE ID

MAAR OOK RUIMTE VOOR OPTIMISME

RISICO IN DE MARKT

OPTIMISME: GROEI De groei trekt wereldwijd verder aan

ISM (non-)manufacturing Tankan Eurozone

ISM Manufacturing35

40

45

50

55

1990 1995 2000 2005 2010 2015

60

Jul -‘17

ISM non-manufacturing

OPTIMISME: GROEI De groei trekt wereldwijd verder aan

source: Thomson Reuters Datastream

Large manufacturers actual-60

-40

-20

0

20

2000 2002 2004 2006 2008 2010 2012 2014 2016

40

ISM (non-)manufacturing Tankan Eurozone

OPTIMISME: GROEI De groei trekt wereldwijd verder aan

PMI Output Index25

30

35

40

45

50

55

60

’98

65

-6

-5

-4

-3

-2

-1

0

1

3

2

’99 ’00 ’01 ’02 ’03 ’04 ’05 ’06 ’07 ’08 ’09 ’10 ’11 ’12 ’13 ’14 ’15 ’16 ’17

Eurozone PMI Output Index, sa, 50 = no change Eurostat, 3m/3m % change

Industrial Production (excluding construction)

ISM (non-)manufacturing Tankan Eurozone

Duitse kapitaalmarkt rente

FAVORIETE UITKOMST

5

4

3

2

1

0

-12007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

source: Bloomberg, Robeco

Aandelenmarkten

FAVORIETE UITKOMST

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018source: Bloomberg, Robeco

OVERWAARDERING LATE CYCLE CHINESE SCHULD MONETAIR BELE ID

MOMENTUM STERK INFLATIE AFWEZIG CENTRALE BANKEN

RISICO’S

OPTIMISME

DISCLAIMER

DisclaimerRobeco Institutional Asset Management B.V., hereafter Robeco, has a license as manager of UCITS and AIFs from the Netherlands Authority for the Financial Markets in Amsterdam. This statement is intended for professional investors. Therefore, the information set forth herein is not addressed and must not be made available, in whole or in part, to other parties, such as retail clients. Robeco disclaims all liability arising from uses other than those specified herein. Without further explanation this presentation cannot be considered complete. It is intended to provide the professional investor with general information on Robeco’s specific capabilities, but does not constitute a recommendation or an advice to buy or sell certain securities or investment products. All rights relating to the information in this presentation are and will remain the property of Robeco. No part of this presentation may be reproduced, saved in an automated data file or published in any form or by any means, either electronically, mechanically, by photocopy, recording or in any other way, without Robeco's prior written permission. The information contained in this publication is not intended for users from other countries, such as US citizens and residents, where the offering of foreign financial services is not permitted, or where Robeco's services are not available. The prospectus and the Key Investor Information Document for the Robeco Funds can all be obtained free of charge at www.robeco.com. Investment involves risks. Before investing, please note the initial capital is not guaranteed. The value of the investments may fluctuate. Past performance is no guarantee of future results. Historical returns are provided for illustrative purposes only. The price of units may go down as well as up and the past performance is not indicative of future performance. If the currency in which the past performance is displayed differs from the currency of the country in which you reside, then you should be aware that due to exchange rate fluctuations the performance shown may increase or decrease if converted into your local currency.