pinto valley mine - s2.q4cdn.coms2.q4cdn.com/231101920/files/doc_presentations/pinto-valley... ·...

TRANSCRIPT

1

Pinto Valley Mine Analyst & Investor Tour - April 2014

2 2

This presentation, and the documents incorporated by reference herein, may contain “forward-looking information” within the meaning of Canadian securities legislation and “forward-looking

statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 (collectively, “forward-looking statements”). These forward-looking statements are made as of

the date of this document and Capstone does not intend, and does not assume any obligation, to update these forward-looking statements, except as required under applicable securities

legislation.

Forward-looking statements relate to future events or future performance and reflect our expectations or beliefs regarding future events. Forward-looking statements include, but are not limited

to, statements with respect to the estimation of Mineral Resources and Mineral Reserves, the realization of Mineral Reserve Estimates, the timing and amount of estimated future production,

costs of production and capital expenditures, the success of our mining operations, environmental risks, unanticipated reclamation expenses and title disputes. In certain cases, forward-looking

statements can be identified by the use of words such as “plans”, “expects”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates”, “believes” or variations of such words and

phrases, or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” or the negative of these terms or comparable

terminology. By their very nature, forward-looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements

to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Such factors include, among others, risks related to:

inherent hazards associated with mining operations; future prices of copper and other metals; counterparty risks associated with sales of our metals; our ability to raise capital; foreign currency

exchange rate fluctuations; accuracy of Mineral resource and Mineral Reserve Estimates; changes in general economic conditions; increased operating and capital costs; challenges to title to our

mineral properties; operating in foreign jurisdictions with risk of changes to governmental regulation; compliance with governmental regulations; dependence on key management personnel;

compliance with environmental laws and regulations; reliance on approvals, licenses and permits from governmental authorities; impact of climatic conditions on our Pinto Valley operation;

potential conflicts of interest involving our directors and officers; aboriginal title claims and rights to consultation and accommodation; limitations inherent in our insurance coverage; land

reclamation and mine closure obligations; labour relations; increasing energy prices; competition in the mining industry; risks associated with joint venture partners; and our ability to integrate

new acquisitions into our operations.

Although we have attempted to identify important factors that could cause our actual results, performance or achievements to differ materially from those described in our forward-looking

statements, there may be other factors that cause our results, performance or achievements not to be as anticipated, estimated or intended. There can be no assurance that our forward-looking

statements will prove to be accurate, as our actual results, performance or achievements could differ materially from those anticipated in such statements. Accordingly, readers should not place

undue reliance on our forward-looking statements.

Alternative Performance Measures “C1 Cash Cost”, “Cash Cost” and “Adjusted Net Earnings” are Alternative Performance Measures. Alternative performance measures are furnished to provide additional information. These

performance measures are used by management to monitor performance, to plan and to assess the overall effectiveness and efficiency of mining operations. These performance measures may

not be comparable to similar data presented by other mining companies. These performance measures should not be considered in isolation as a substitute for measures of performance included

in the Company’s unaudited condensed interim consolidated financial statements prepared in accordance with IFRS.

Currency All amounts are in US$ unless otherwise specified.

Cautionary Note Forward Looking Information

3 3

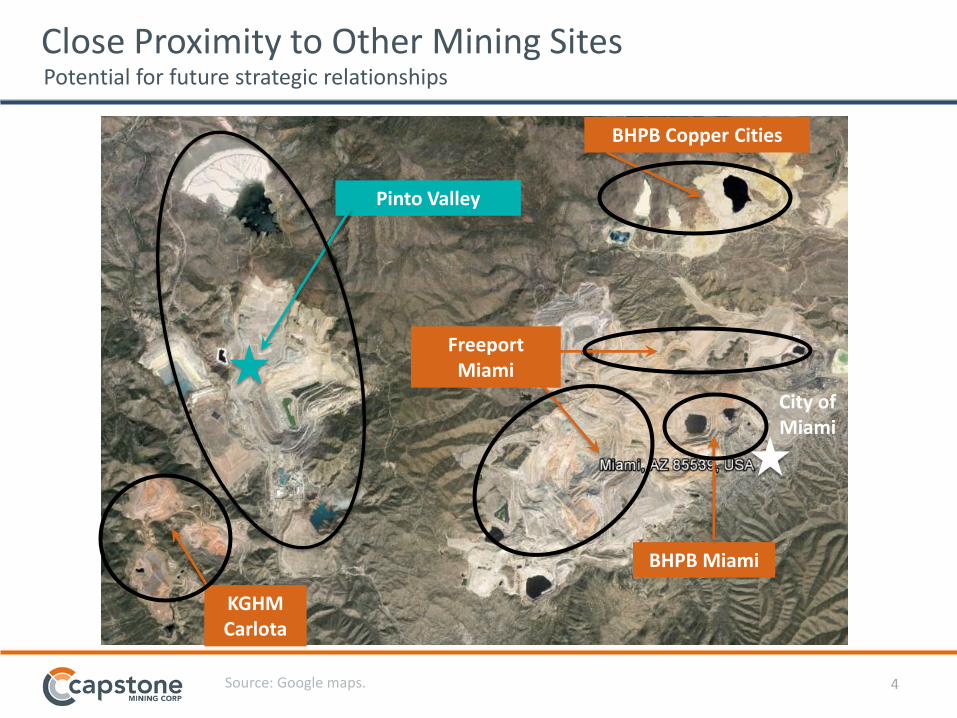

Located ~10 km west of the town of Miami in Gila, County, Arizona

129 km from Phoenix to Pinto Valley via US Highway 60

Close proximity to other copper mining operations

Fully permitted with established infrastructure and skilled workforce

Location: Historical Mining District

The Globe-Miami historical mining district is one of the world’s most favorable jurisdictions for tax, regulation and labour

4

Close Proximity to Other Mining Sites

Source: Google maps.

City of Miami

Pinto Valley

Freeport Miami

KGHM Carlota

BHPB Copper Cities

BHPB Miami

Potential for future strategic relationships

5 5

Summary of Pinto Valley’s community involvement over the past five months. Donations

Education & Training

Community Support/Capacity Building

Health

Sports & Recreation

Arts

Employee Involvement United Fund of Globe-Miami – Employees donated over $20k for 2014

Pinto Valley Road Cleanup – Two events to clean up the Pinto Valley entrance road

March of Dimes – Pinto Valley team participated and raised over $2k

Adopt-a-Senior – Employees adopted 26 local senior citizens for Christmas

Adopt-a-Family – Departments adopted six families from Globe, Miami and San Manuel

Community Relations

6 6

Geology

7 7

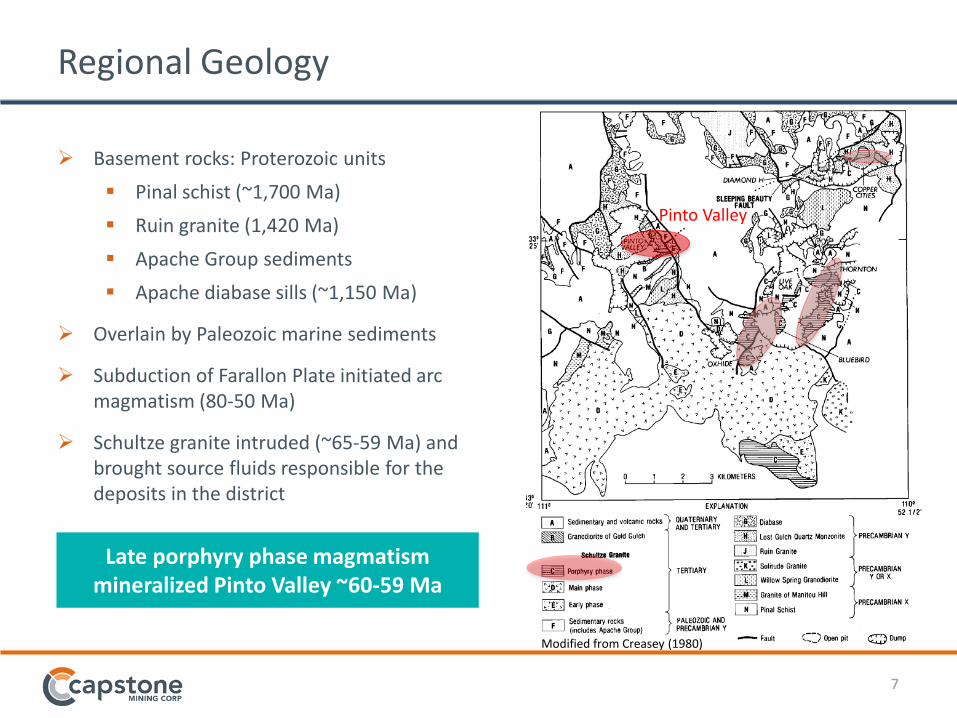

Regional Geology

Basement rocks: Proterozoic units

Pinal schist (~1,700 Ma)

Ruin granite (1,420 Ma)

Apache Group sediments

Apache diabase sills (~1,150 Ma)

Overlain by Paleozoic marine sediments

Subduction of Farallon Plate initiated arc magmatism (80-50 Ma)

Schultze granite intruded (~65-59 Ma) and brought source fluids responsible for the deposits in the district s

Pinto Valley

Modified from Creasey (1980)

Late porphyry phase magmatism mineralized Pinto Valley ~60-59 Ma

8 8

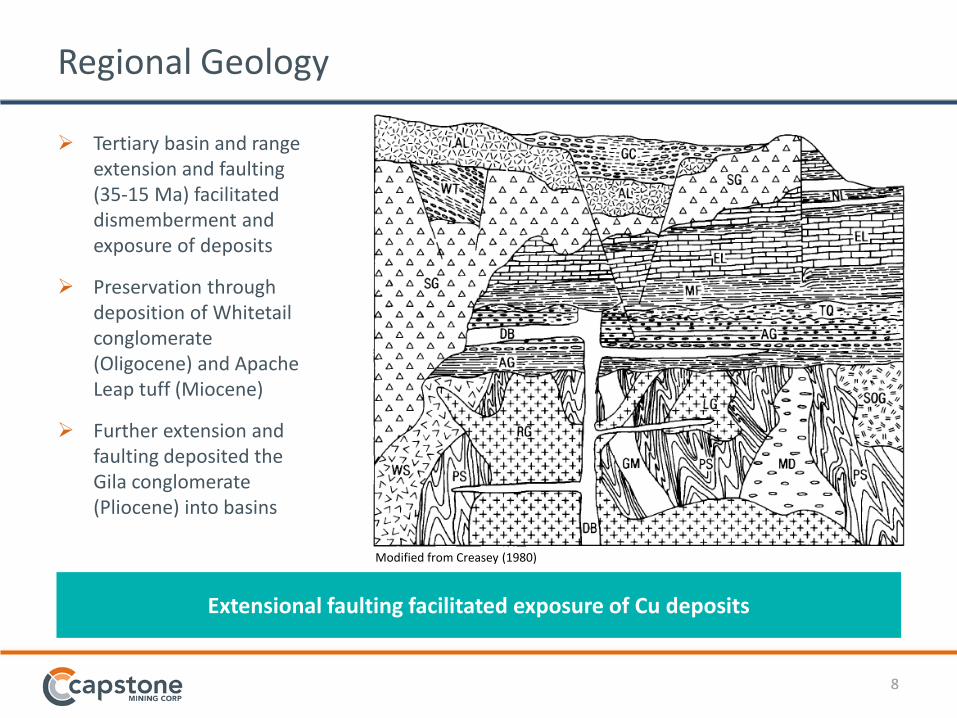

Regional Geology

Extensional faulting facilitated exposure of Cu deposits

Tertiary basin and range extension and faulting (35-15 Ma) facilitated dismemberment and exposure of deposits

Preservation through deposition of Whitetail conglomerate (Oligocene) and Apache Leap tuff (Miocene)

Further extension and faulting deposited the Gila conglomerate (Pliocene) into basins

Modified from Creasey (1980)

9 9

Local Geology

Schultze granite represented at PV by granodiorite and granite porphyry intrusions along South Hill fault

Ruin granite and Apache diabase host mineralization (chalcopyrite, pyrite, magnetite, molybdenite)

Development of oxide cap and supergene blanket, since mined out; sulphide ore mineralogy remain

Approximate PV pit outline

Modified from Peterson (1962)

Long lived fault systems provided structural conduits for mineralizing fluids

10 10

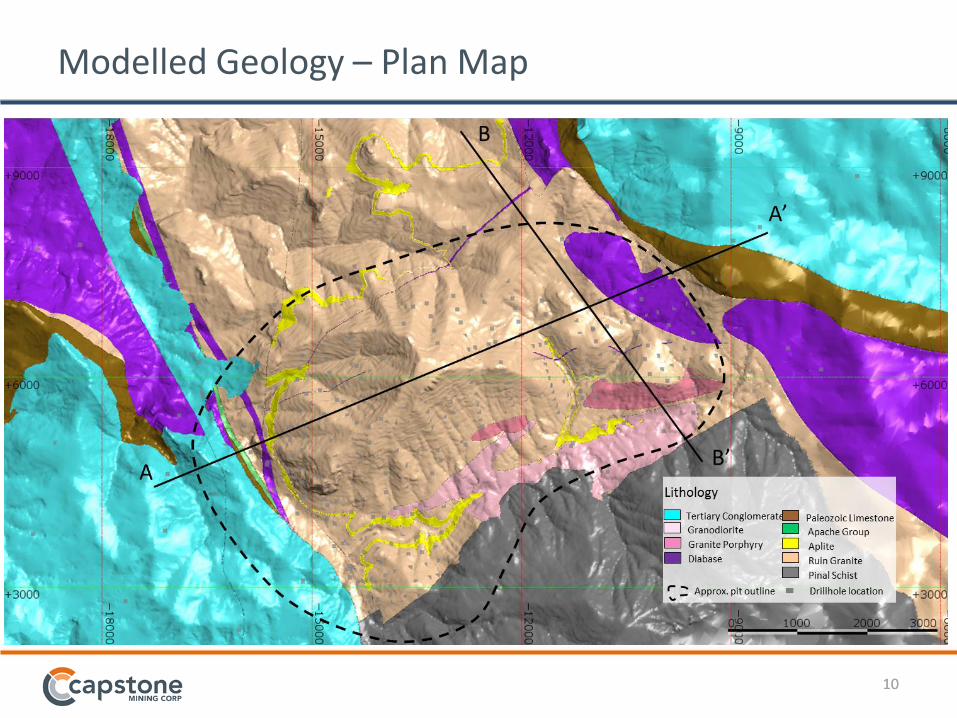

Modelled Geology – Plan Map

11 11

Modelled Geology – Long Section Looking NNW

12 12

Modelled Geology – Cross Section Looking ENE

13

Notes: 1. At a 0.18% cutoff grade. The March 2014 Mineral Resource was estimated by Kirkham Geosystems Inc. The updated resource statement, based on additional drill hole information not included in the previous resource statement, increased the resource by 75.0 million tonnes from the last mineral resource estimate completed in December 2013. The resource estimate includes the mineral reserve. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. Mineral Resource estimates do not account for mineability, selectivity, mining loss and dilution. These Mineral Resource estimates include inferred Mineral Resources that are normally considered too speculative geologically to have economic considerations applied to them that would enable them to be categorized as Mineral Reserves. There is also no certainty that these Inferred Mineral Resources will be converted to Measured and Indicated categories through further drilling, or into Mineral Reserves, once economic considerations are applied. Totals may not add due to rounding.

Metric Tonnes

(M)

Copper (%)

Molybdenum (%)

Contained Copper (M lbs)

Contained Molybdenum

(M lbs)

Measured (M) 660.4 0.34 0.008 5,014.3 119.4

Indicated (I) 902.5 0.28 0.006 5,491.8 123.4

Total M&I 1,563.0 0.30 0.007 10,506.1 242.8

Inferred 58.2 0.23 0.005 298.5 6.8

Pinto Valley Mineral Resource Estimate1

Estimated Mineral Resources as of March 2014, at a 0.18% Cu cut-off grade

The contained copper in the Mineral Resource increased by 40% at 0.18% cut-off grade

14 14

Operations

15 15

History of Pinto Valley Mine

Pinto Valley Historical Production / Copper Prices

Source: BHP Copper

16 16

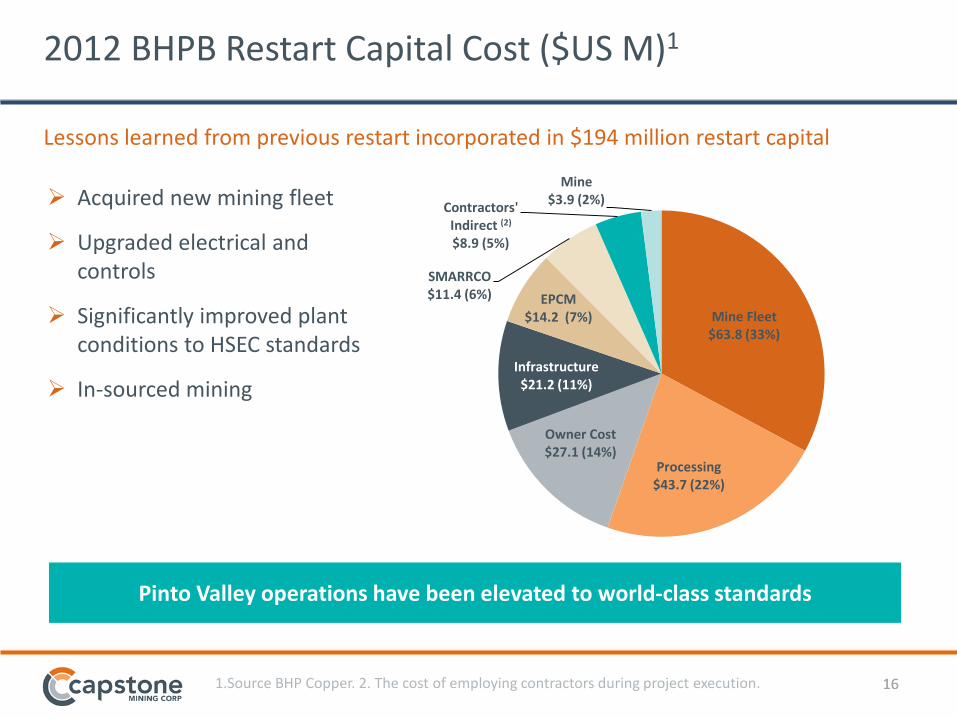

2012 BHPB Restart Capital Cost ($US M)1

Mine Fleet $63.8 (33%)

Processing $43.7 (22%)

Owner Cost $27.1 (14%)

Infrastructure $21.2 (11%)

EPCM $14.2 (7%)

SMARRCO $11.4 (6%)

Contractors' Indirect (2) $8.9 (5%)

Mine $3.9 (2%)

1.Source BHP Copper. 2. The cost of employing contractors during project execution.

Lessons learned from previous restart incorporated in $194 million restart capital

Acquired new mining fleet

Upgraded electrical and controls

Significantly improved plant conditions to HSEC standards

In-sourced mining

Pinto Valley operations have been elevated to world-class standards

17 17

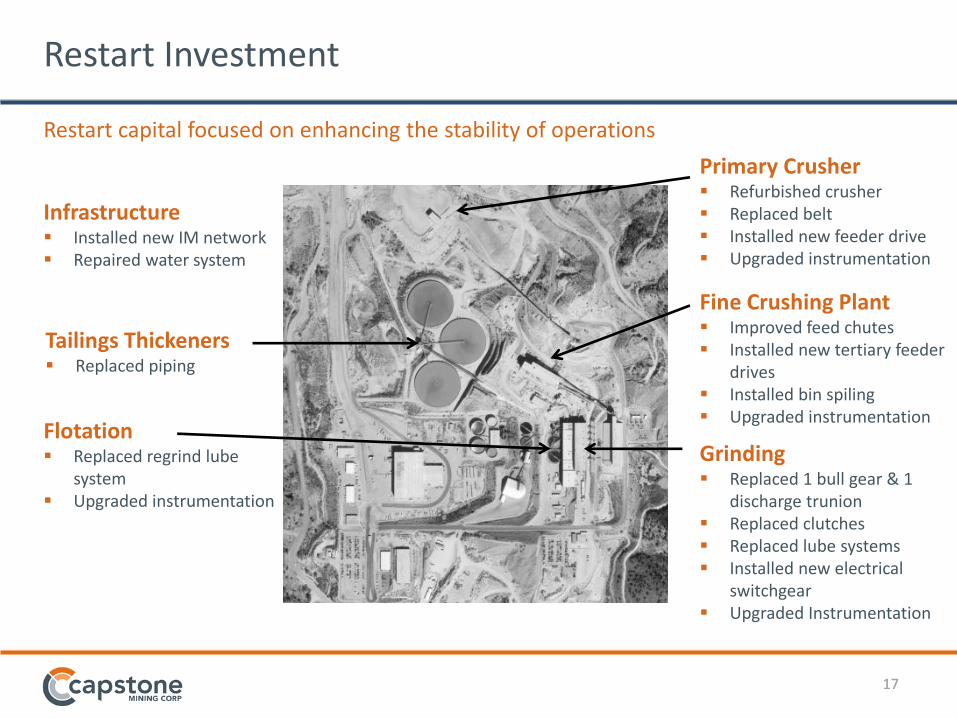

Restart Investment

Restart capital focused on enhancing the stability of operations

Infrastructure Installed new IM network Repaired water system

Tailings Thickeners Replaced piping

Flotation Replaced regrind lube

system Upgraded instrumentation

Primary Crusher Refurbished crusher Replaced belt Installed new feeder drive Upgraded instrumentation

Fine Crushing Plant Improved feed chutes Installed new tertiary feeder

drives Installed bin spiling Upgraded instrumentation

Grinding Replaced 1 bull gear & 1

discharge trunion Replaced clutches Replaced lube systems Installed new electrical

switchgear Upgraded Instrumentation

18 18

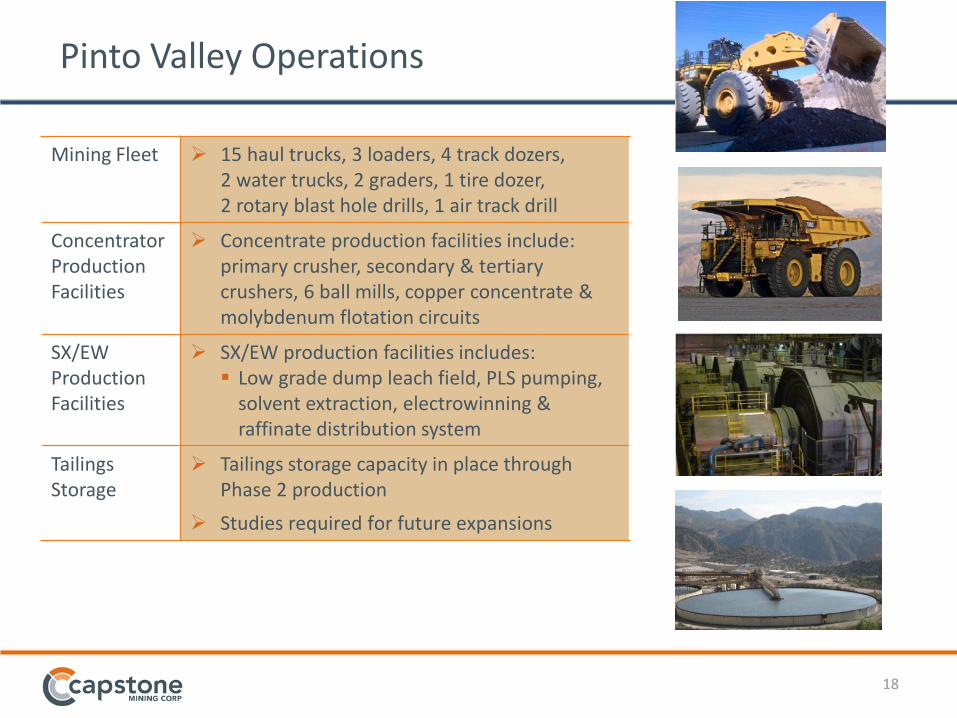

Mining Fleet 15 haul trucks, 3 loaders, 4 track dozers, 2 water trucks, 2 graders, 1 tire dozer, 2 rotary blast hole drills, 1 air track drill

Concentrator Production Facilities

Concentrate production facilities include: primary crusher, secondary & tertiary crushers, 6 ball mills, copper concentrate & molybdenum flotation circuits

SX/EW Production Facilities

SX/EW production facilities includes: Low grade dump leach field, PLS pumping,

solvent extraction, electrowinning & raffinate distribution system

Tailings Storage

Tailings storage capacity in place through Phase 2 production

Studies required for future expansions

Pinto Valley Operations

19 19

Processing

20 20

Pinto Valley Mine: Process Flow Sheet

21 21

Crushing Circuit

Under size Under size

Over size

ROM ORE

PRIMARY

CRUSHER

SECONDARY

CONE

CRUSHER (3)

FINE ORE

STORAGE

TERTIARY

SCREEN (6)

TERTIARY

SURGEBIN

COARSE ORE

RECLAIM (3)

SECONDARY

SCREENS

(3)

TERTIARY

CRUSHERS

(6)

22

Process Mill Circuit

PRIMARY

CYCLONE (6 BANKS)

FINE ORE

RECLAIMS}

FEEDERS (6)

FINE ORE

STORAGE

Under size

ROUGHER

FLOTATION

DISTRIBUTOR (3)

PRIMARY

BALL MILL (6)

23

FROM MILL

CIRCUIT

ROUGHER

FLOTATION

3 (LINES)

ROUGHER

CONCENTRATE

COLLECTION TRASH

SCREENS (2)

COLUMN CELL

DISTRIBUTOR

REGRIND MILL (2)

TAILINGS

THICKENERS (3) TAILINGS DISPOSAL

Process Rougher Flotation

24

Process Flotation Circuit

TO COPPER

FILTRATION

COPPER

CONC.

COPPER

THICKENER

FROM

ROUGHER

FLOTATION

SCAVENGER

FLOTATION

MOLY FLOTATION

CONDITIONERS (2)

MOLY ROUGHER FLOTATION

(4 BANKS)

MOLY COLUMN

FLOTATION

MOLY

RECLEANER

FLOTATION CELLS

MOLY FLOTATION

DISTRIBUTOR

COPPER/MOLY

THICKENER (2)

COLUMN

FLOTATION

CELLS (4)

TO ROUGHER

CONCENTRATE

COLLECTION

TO FINAL

TAIL

THICKENER

MOLY CLEANER

FLOTATION CELLS

TO MOLY

THICKENER

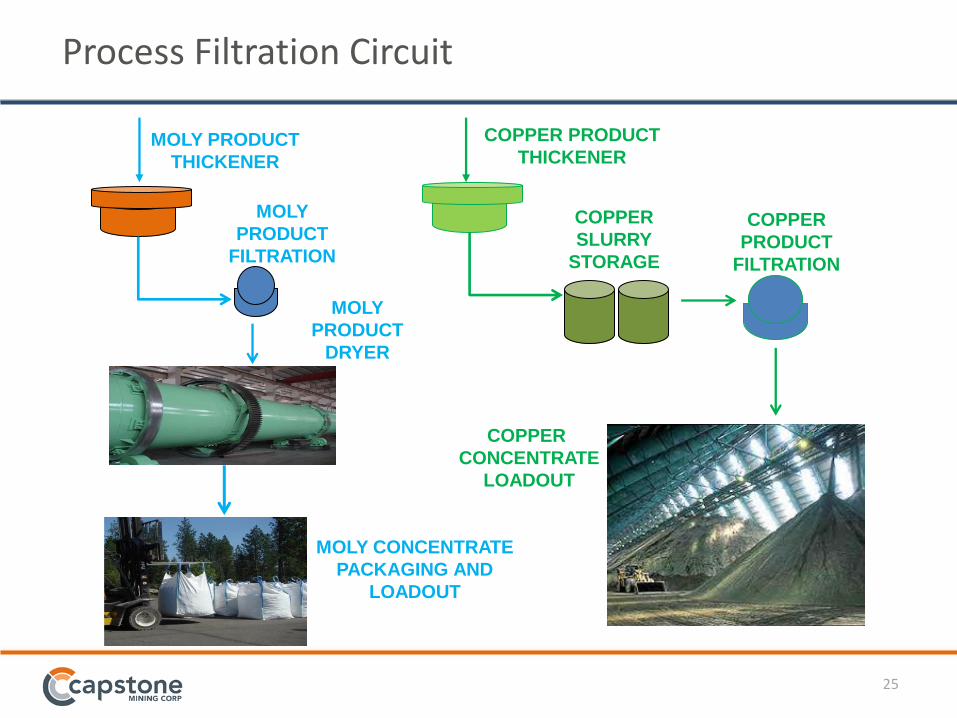

25

MOLY CONCENTRATE

PACKAGING AND

LOADOUT

COPPER PRODUCT

THICKENER

COPPER

PRODUCT

FILTRATION

COPPER

SLURRY

STORAGE

MOLY PRODUCT

THICKENER

MOLY

PRODUCT

FILTRATION

MOLY

PRODUCT

DRYER

COPPER

CONCENTRATE

LOADOUT

Process Filtration Circuit

26 26

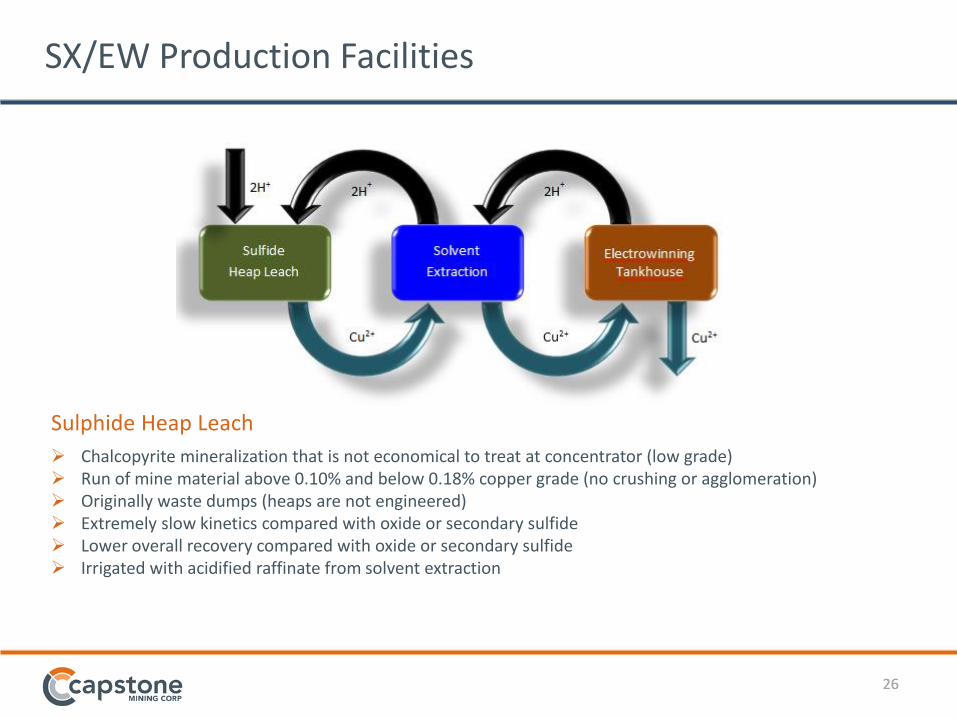

SX/EW Production Facilities

Sulphide Heap Leach

Chalcopyrite mineralization that is not economical to treat at concentrator (low grade) Run of mine material above 0.10% and below 0.18% copper grade (no crushing or agglomeration) Originally waste dumps (heaps are not engineered) Extremely slow kinetics compared with oxide or secondary sulfide Lower overall recovery compared with oxide or secondary sulfide Irrigated with acidified raffinate from solvent extraction

27 27

SX/EW Production Facilities – Sulphide Dump Leach

Electrowinning

Copper is plated onto starter sheets (Cu2+→Cu0) Starter sheets are plated on stainless steel blanks Water dissociates to oxygen gas and acid at anode

(hydrolysis – H2O→2H++½O2) Anodes are lead alloy Production currently averages 9-10 tonnes per day 5N copper LME grade Tank house capacity maximum 27M lbs/year Current density 120A/m2

Solvent Extraction

Pregnant leach solution (PLS) is mixed with organic Copper is selectively extracted into organic Transfer of copper is driven by pH (exchange

of 2H+ for Cu2+) PV PLS is extremely clean Copper is stripped from organic into a low pH electrolyte Solution flow rate capacity 7,000 gpm

Run of mine material above 0.10% and below 0.18% copper grade

28 28

By-Products

Molybdenum and silver by-products lower cash cost

MoS2 concentrate is produced – Molybdenum( Mo) is the payable metal

1.4 million pounds of contained Mo annually LOM

2014 recovery at 20% in start-up, PV2 PFS LOM 47%

Silver is recovered from copper concentrate

235,000 ounces of contained silver annually

29 29

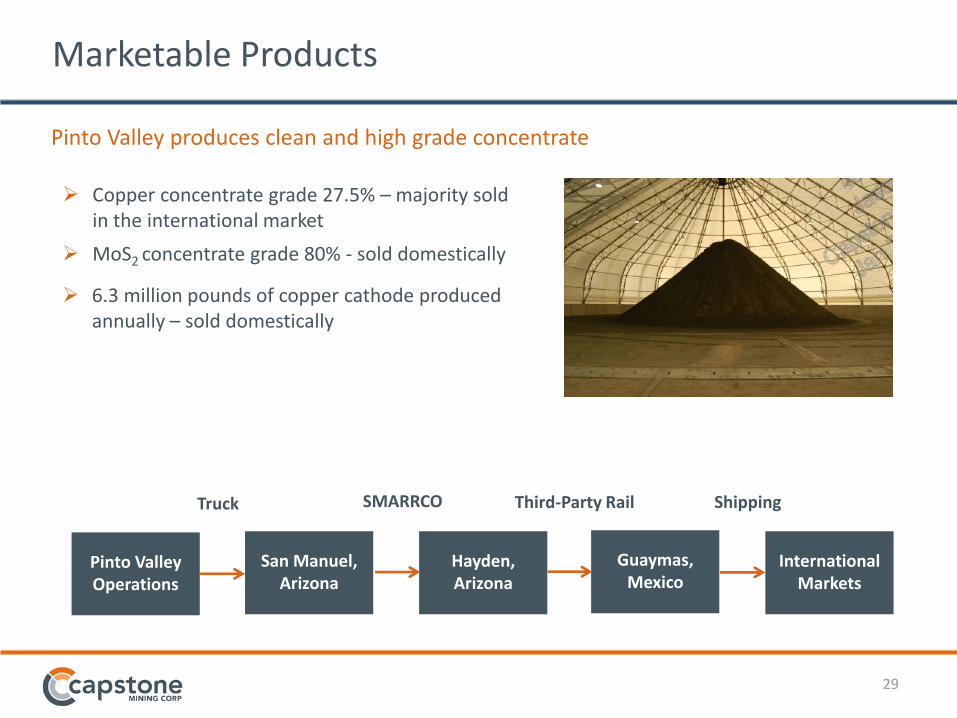

Marketable Products

Copper concentrate grade 27.5% – majority sold in the international market

MoS2 concentrate grade 80% - sold domestically

6.3 million pounds of copper cathode produced annually – sold domestically

Pinto Valley produces clean and high grade concentrate

Truck

Pinto Valley Operations

San Manuel, Arizona

Hayden, Arizona

Guaymas, Mexico

International Markets

SMARRCO Third-Party Rail Shipping

30 30

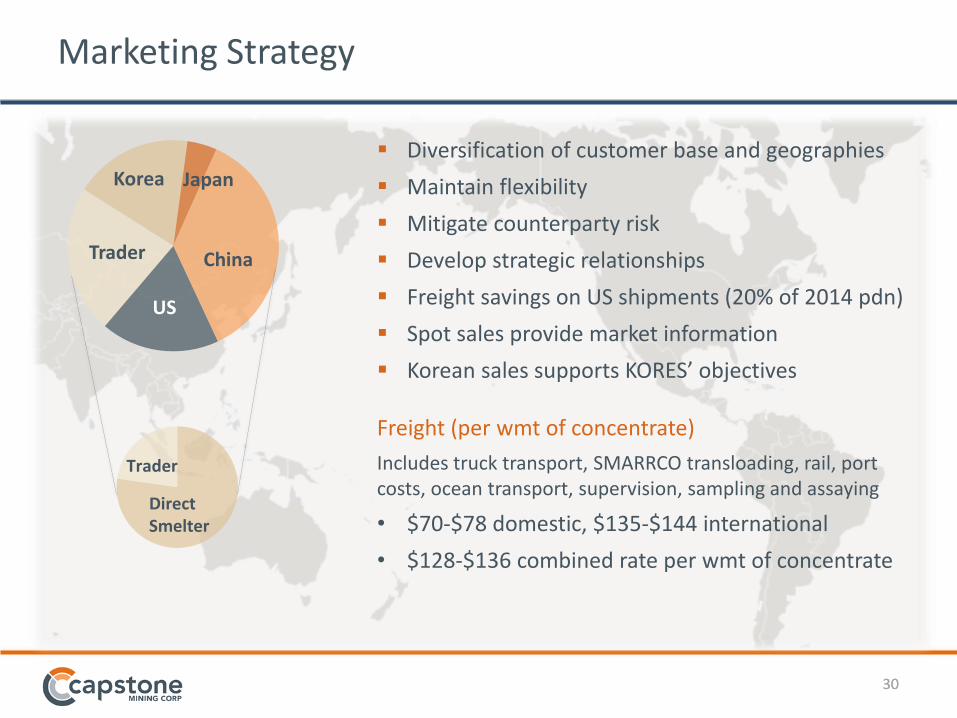

Marketing Strategy

US

Trader

Korea Japan

China

Direct Smelter

Trader

Diversification of customer base and geographies

Maintain flexibility

Mitigate counterparty risk

Develop strategic relationships

Freight savings on US shipments (20% of 2014 pdn)

Spot sales provide market information

Korean sales supports KORES’ objectives Freight (per wmt of concentrate)

Includes truck transport, SMARRCO transloading, rail, port costs, ocean transport, supervision, sampling and assaying

• $70-$78 domestic, $135-$144 international

• $128-$136 combined rate per wmt of concentrate

31 31

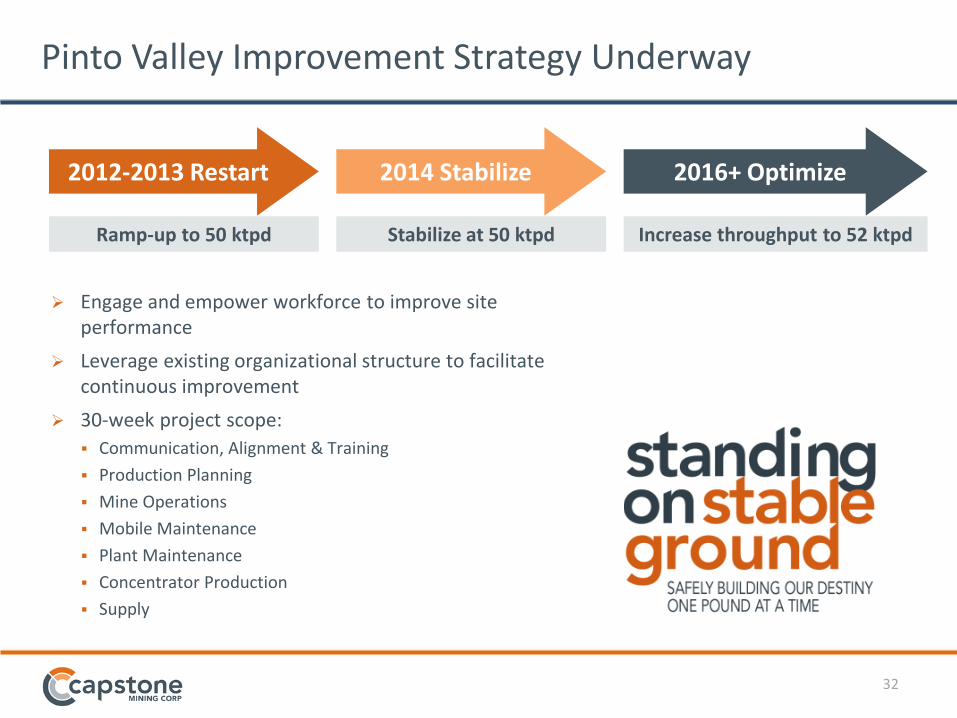

Improvement Initiative: Standing on Stable Ground

32

Ramp-up to 50 ktpd Stabilize at 50 ktpd

2012-2013 Restart 2014 Stabilize

Increase throughput to 52 ktpd

2016+ Optimize

Pinto Valley Improvement Strategy Underway

Engage and empower workforce to improve site performance

Leverage existing organizational structure to facilitate continuous improvement

30-week project scope:

Communication, Alignment & Training

Production Planning

Mine Operations

Mobile Maintenance

Plant Maintenance

Concentrator Production

Supply

33

Weekly Update – Week 17 of 30

Trending towards reliably achieving our targets

225,000

275,000

325,000

375,000

425,000

1/5/14 1/12/141/19/141/26/142/2/14 2/9/14 2/16/142/23/143/2/14 3/9/143/16/143/23/143/30/14

Tonnes

MillWeeklyTonnes

Baseline TonnesMilled

ProjectTargetMillTonnes 4WeekRollingAverageTonnesMilled

Budget

34 Notes: The only remaining active Wave 1 sourcing effort underway is Fuel

Supply: Sourcing Prioritization Matrix

35

Change Management & Improvement

Approach

Active Supervision,

Variance Management, “To Be” SFM

Effective Communication,

Management Styles, Conflict Management

Leadership, Effective

Execution, Sustainability,

Team Work

Session 1

Session 2

Session 3

Session 4

Management Skills Development Program

Session 1 understand their role in change management and tools to help identify and implement change and process improvement

Session 2 understand the positive and negative impacts of Active Supervision and proactively identify lost time and do Root Cause Analysis to prevent it

Session 3 tools and concepts to effectively communicate and manage people and situations, helping them to position themselves as leaders of the process.

Session 4 learn how effective leadership can promote teamwork and sustainability of the culture of improvement

36 36

Infrastructure

37 37

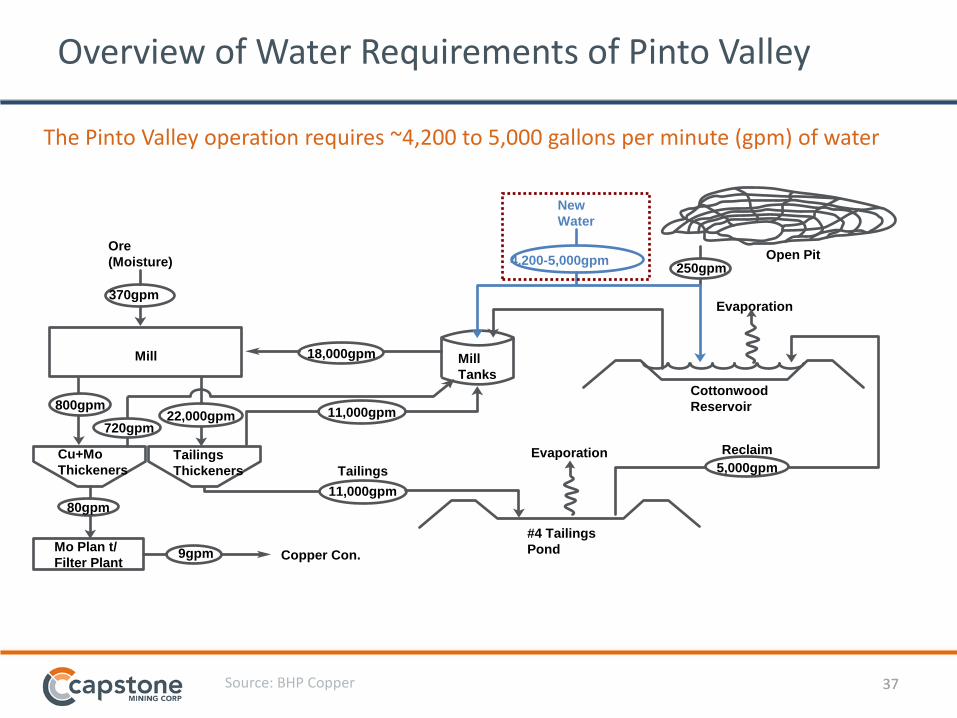

Overview of Water Requirements of Pinto Valley

The Pinto Valley operation requires ~4,200 to 5,000 gallons per minute (gpm) of water

Source: BHP Copper

Ore

(Moisture)

New

Water

370gpm

Mill

800gpm

Tailings

18,000gpm

22,000gpm

Mo Plan t/

Filter Plant Copper Con.

#4 Tailings

Pond

Evaporation

Mill

Tanks

Evaporation

250gpm Open Pit

Reclaim

370gpm

4,200-5,000gpm

Mill

800gpm

80gpm

Cu+Mo

Thickeners

11,000gpm

18,000gpm

22,000gpm

9gpm

Mill

Tanks

Cottonwood

Reservoir

250gpm

5,000gpm

11,000gpm

720gpm

Tailings

Thickeners

38 38

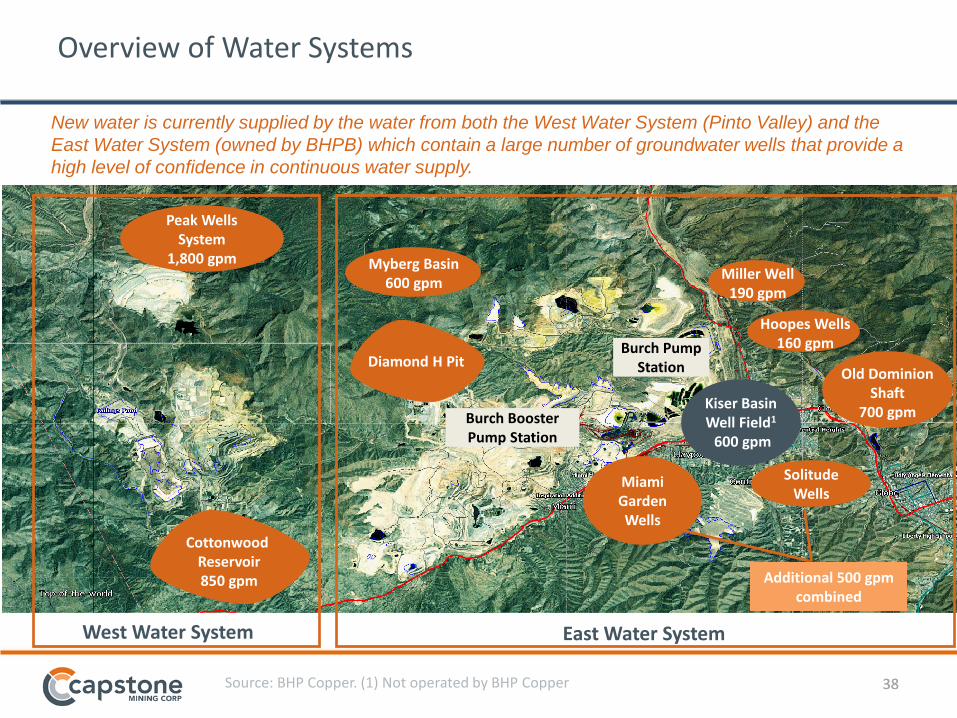

Overview of Water Systems

Burch Pump Station

Burch Booster Pump Station

New water is currently supplied by the water from both the West Water System (Pinto Valley) and the

East Water System (owned by BHPB) which contain a large number of groundwater wells that provide a

high level of confidence in continuous water supply.

East Water System West Water System

Solitude Wells

Miami Garden Wells

Peak Wells System

1,800 gpm

Cottonwood Reservoir 850 gpm

Diamond H Pit

Myberg Basin 600 gpm

Old Dominion Shaft

700 gpm

Source: BHP Copper. (1) Not operated by BHP Copper

Kiser Basin Well Field1 600 gpm

Miller Well 190 gpm

Hoopes Wells 160 gpm

Additional 500 gpm combined

39 39

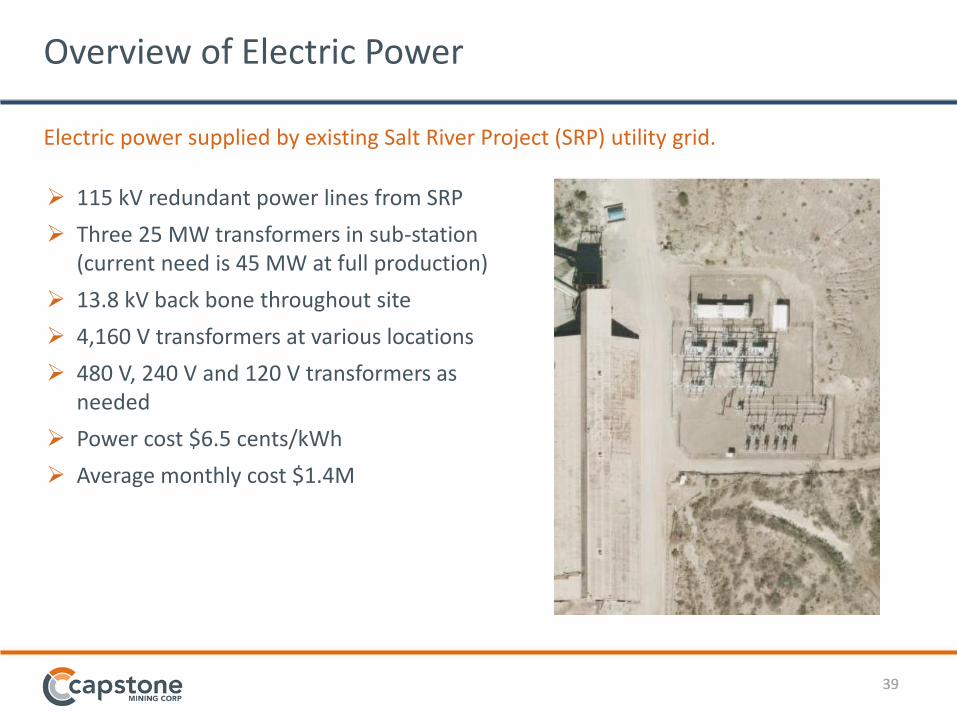

Overview of Electric Power

115 kV redundant power lines from SRP

Three 25 MW transformers in sub-station (current need is 45 MW at full production)

13.8 kV back bone throughout site

4,160 V transformers at various locations

480 V, 240 V and 120 V transformers as needed

Power cost $6.5 cents/kWh

Average monthly cost $1.4M

Electric power supplied by existing Salt River Project (SRP) utility grid.

40 40

Tailings Management

41 41

People

42 42

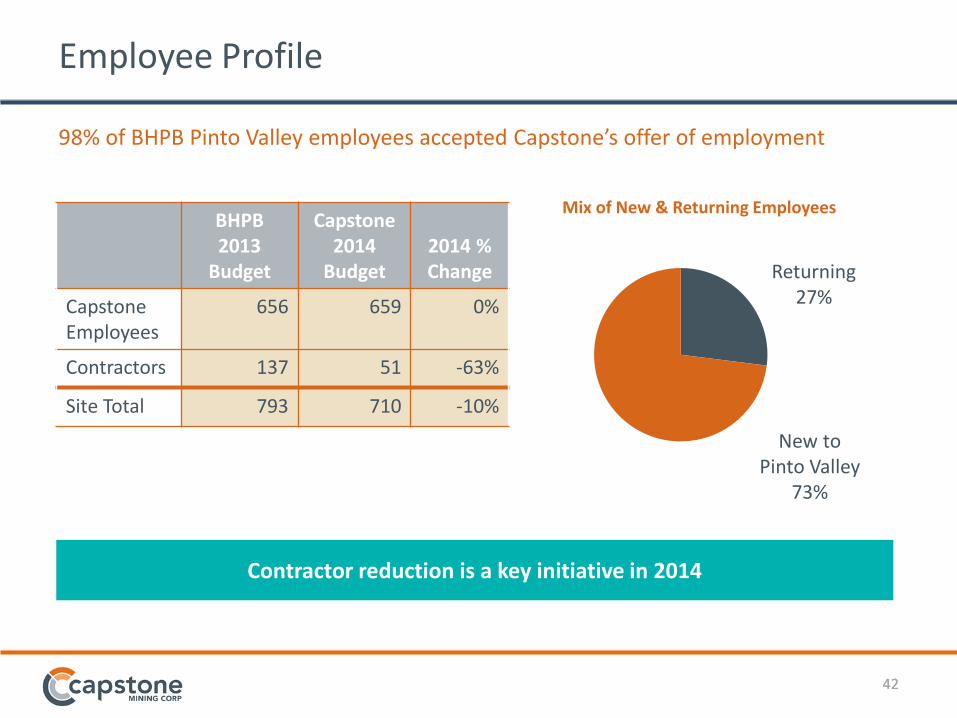

Employee Profile

BHPB 2013

Budget

Capstone 2014

Budget

2014 % Change

Capstone Employees

656 659 0%

Contractors 137 51 -63%

Site Total 793 710 -10%

Returning 27%

New to Pinto Valley

73%

Mix of New & Returning Employees

Contractor reduction is a key initiative in 2014

98% of BHPB Pinto Valley employees accepted Capstone’s offer of employment

43 43

Collective Bargaining Agreement Collective Bargaining Agreement at Pinto Valley

Contract extended for one year by BHPB on June 30, 2013 and expires June 30, 2014.

Capstone preparing for negotiations

Hourly employees represented by a joint union comprised of six constituent unions:

The United Steel, Paper and Forestry, Rubber, Manufacturing, Energy, Allied Industrial and Services Workers International Union, AFL-CIO-CLC

International Brotherhood of Teamsters, Chauffeurs, Warehousemen & Helpers of America, Local No. 104

International Union of Operating Engineers, Local No. 428, AFL-CIO

International Brotherhood of Electrical Workers, Local No. 518, AFL-CIO

International Brotherhood of Boilermakers, Iron Ship Builders, Blacksmiths, Forgers and Helpers, Local No. 627, AFL-CIO

United Association of Journeymen and Apprentices of the Plumbing and Pipefitting Industry of the United States and Canada, Local No. 469, AFL-CIO

44 44

PV2: Pre-Feasibility Study

45 45

PV2 Pre-Feasibility Summary – March 2014

Mine Life (years) 12.3

Mineral Resources 1,[email protected]%(1)

Mineral Reserves [email protected]%

Planned Throughput (ktpd) 50 - 52

Avg. Annual Production – Contained in Concentrate (M lbs)

119.5

Avg. Annual Production – Cathode (M lbs)

6.3

Est. LOM Avg. C1 Cash Costs $2.00

LOM Sustaining Capital ($ millions) $187.9

After-tax NPV, 8% ($M) $738

1. Measured and Indicated Mineral Resource Estimate, March 2014, at 0.18% Cu Cut-off Grade.

46 46

PV2 Economic Assumptions

Key Assumptions

Cu Price - Average 2014-2022 $/lb 3.15

Cu Price - long term (2023+) $/lb 2.75

Mo Price $/lb 12.50

Ag Price $/oz 20.00

Copper concentrate grade - Cu % 27.5%

Copper payable % 96.5%

Copper treatment charge $/dmt 85.00

Copper refining charge $/lb Cu 0.085

Concentrate sold internationally % 90

47

Ore (M tonnes)

Copper (%)

Molybdenum (%)

Contained Copper (M lbs)

Contained Molybdenum

(M lbs)

Proven 218.97 0.33 0.008 1,593.1 38.6

Probable 13.25 0.33 0.008 96.4 2.3

Total Proven & Probable 232.22 0.33 0.008 1,689.5 41.0

Pinto Valley Mineral Reserves1

PV2 PFS brings reserves to 12.3 years, all within patented property boundaries

1. Mineral Reserve Estimate, January 1, 2014. Economic inputs to the block model were $2.75 per pound copper, mining $2.02 per tonne moved, mill $5.50 per tonne processed, G&A $1.65 per tonne processed and an average copper recovery of 88%. Cut-off Grade – 0.18% Cu 2014 – 2022, excess ore below 0.20% Cu was stockpiled for processing in 2025 -2026. An internal cut-off grade of 0.17% Cu was applied in 2023-2025. Qualified Person is John Marek, Independent Mining Consultants Inc.

48 48

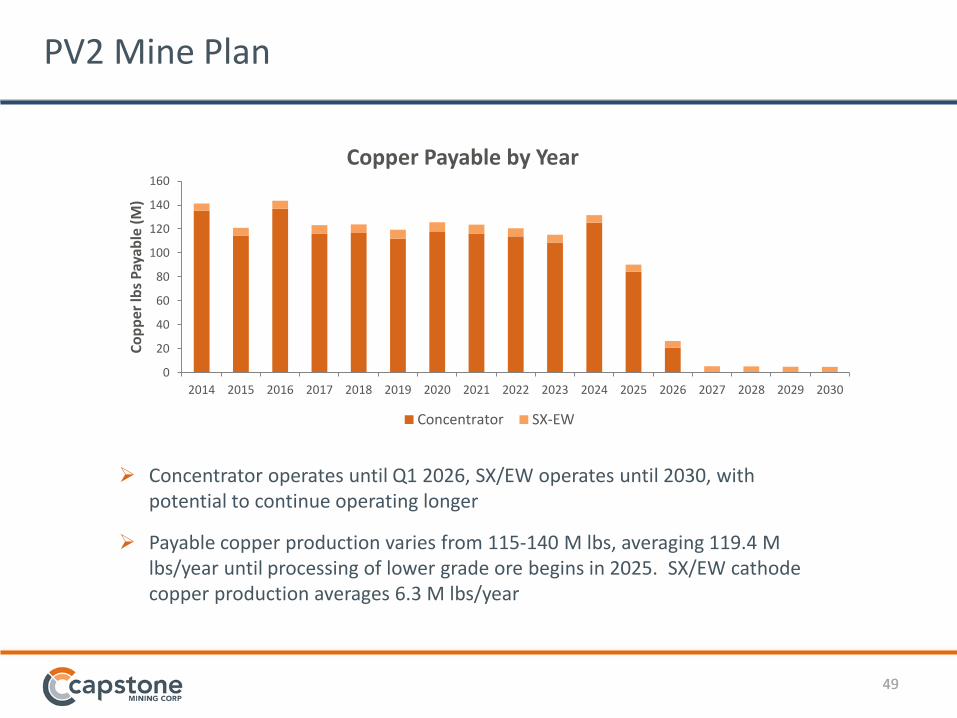

PV2 Mine Plan

PV2 extends production to 2026

Mining rate increases from 22.5 M tonnes in 2014 to 42 M tonnes in 2016 and decreases from 2020 onwards

Mine plan will add 2 hydraulic shovels and 4 haul trucks

LOM strip ratio is 0.65

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.35%

0.40%

0

5

10

15

20

25

30

35

40

45

50

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026

Co

pp

er G

rad

e %

Mat

eria

l Min

ed (

M t

/yea

r)

Total Material Moved

Ore mined to concentrator Ore mined to stockpile

Ore from stockpile to concentrator Low Grade Material mined to heap leach

Waste mined Cu Grade

49 49

PV2 Mine Plan

Concentrator operates until Q1 2026, SX/EW operates until 2030, with potential to continue operating longer

Payable copper production varies from 115-140 M lbs, averaging 119.4 M lbs/year until processing of lower grade ore begins in 2025. SX/EW cathode copper production averages 6.3 M lbs/year

0

20

40

60

80

100

120

140

160

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Co

pp

er lb

s P

ayab

le (

M)

Copper Payable by Year

Concentrator SX-EW

50 50

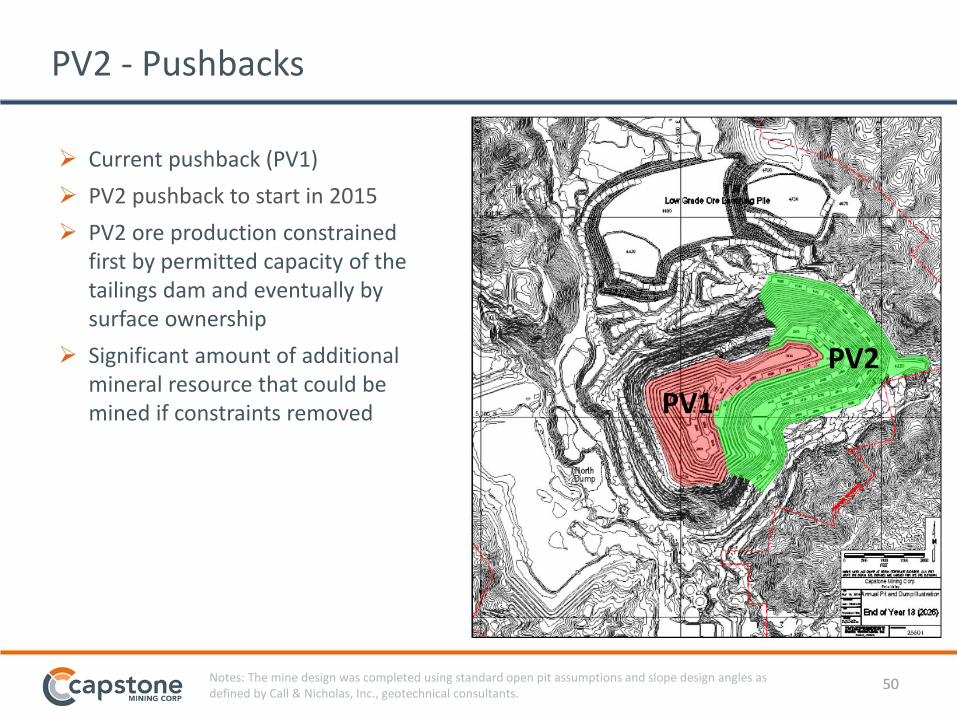

PV2 - Pushbacks

Current pushback (PV1)

PV2 pushback to start in 2015

PV2 ore production constrained first by permitted capacity of the tailings dam and eventually by surface ownership

Significant amount of additional mineral resource that could be mined if constraints removed

PV2

PV1

PV2

Notes: The mine design was completed using standard open pit assumptions and slope design angles as defined by Call & Nicholas, Inc., geotechnical consultants.

51 51

Capacity for tailings storage through PV2 production

Tailings Dam #4

Primary location for tailings placement

Permitting requirements currently under study for maximum capacity

Unpatented mining claims held on east side of Tailings Dam #4

Earthen structures can be utilized within permitted area to ensure PV2 capacity

Additional Resources

Tailings Dam #3 is the tailings backup

Recently expanded for more capacity

Pinto Valley Tailings Management

52 52

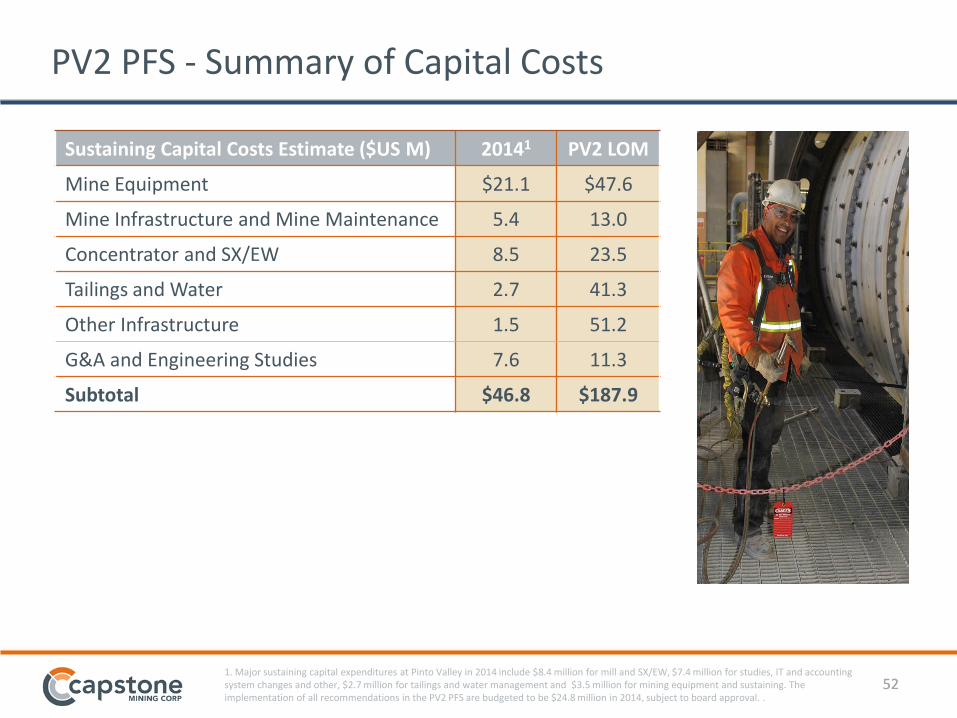

Sustaining Capital Costs Estimate ($US M) 20141 PV2 LOM

Mine Equipment $21.1 $47.6

Mine Infrastructure and Mine Maintenance 5.4 13.0

Concentrator and SX/EW 8.5 23.5

Tailings and Water 2.7 41.3

Other Infrastructure 1.5 51.2

G&A and Engineering Studies 7.6 11.3

Subtotal $46.8 $187.9

PV2 PFS - Summary of Capital Costs

1. Major sustaining capital expenditures at Pinto Valley in 2014 include $8.4 million for mill and SX/EW, $7.4 million for studies, IT and accounting system changes and other, $2.7 million for tailings and water management and $3.5 million for mining equipment and sustaining. The implementation of all recommendations in the PV2 PFS are budgeted to be $24.8 million in 2014, subject to board approval. .

53 53

PV2 PFS - Summary of Capital Costs

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

US$

Mill

ion

s

Sustaining Capital Requirements G&A and Engineering Studies

Other Infrastructure

Tailings and Water

Concentrator and SX/EW

Mine Infrastructure and Mine Maintenance

Mine Equipment

Major Expenditures in 2015

Mining Equipment (second shovel, trucks, auxiliary equipment)

New tailings line to Tailings Dam 4

Tailings Dam 4 booster station upgrades

54 54

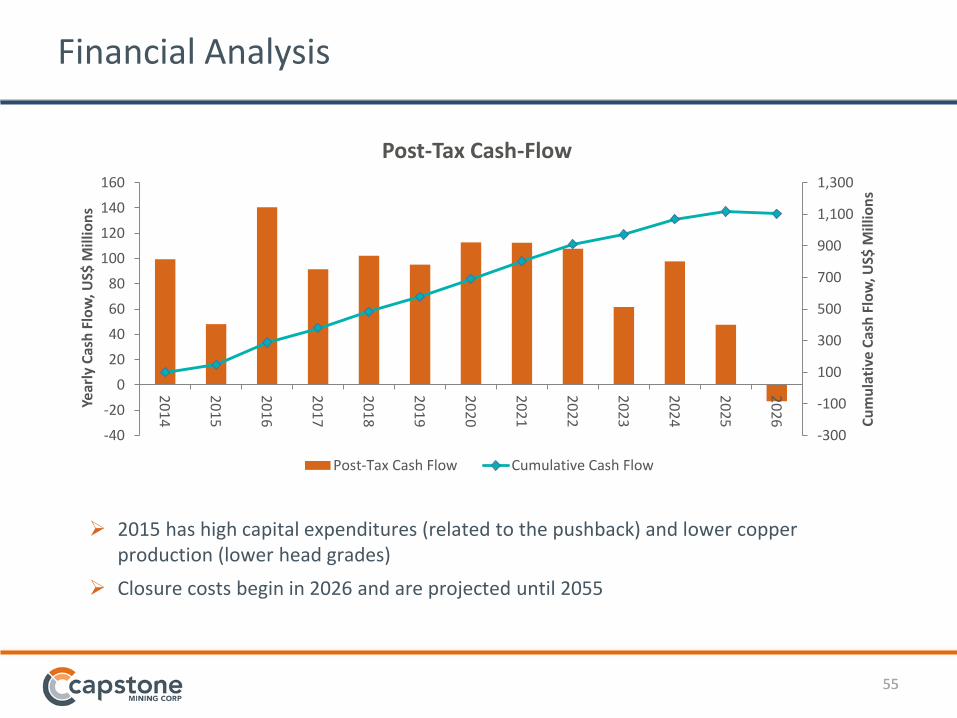

Financial Analysis

Financial Analysis $M

Copper Revenue 4,656

Moly Revenue 210

Silver Revenue 52

Total Revenue 4,918

Site Costs -2,600

Conc. Transport, TC/RCs -716

Operating Cash Flow 1,602

Sustaining Capital Costs -188

Closure Costs -129

Net Cash Flow, Pre-Tax, Undiscounted 1,285

NPV (8%) Pre-Tax 931

Taxes Payable -274

Net Cash Flow, Post-Tax, Undiscounted 1,011

NPV (8%) Post-Tax 738

55 55

Financial Analysis

-300

-100

100

300

500

700

900

1,100

1,300

-40

-20

0

20

40

60

80

100

120

140

160

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26 C

um

ula

tive

Cas

h F

low

, US$

Mill

ion

s

Yea

rly

Cas

h F

low

, US$

Mill

ion

s

Post-Tax Cash-Flow

Post-Tax Cash Flow Cumulative Cash Flow

2015 has high capital expenditures (related to the pushback) and lower copper production (lower head grades)

Closure costs begin in 2026 and are projected until 2055

56 56

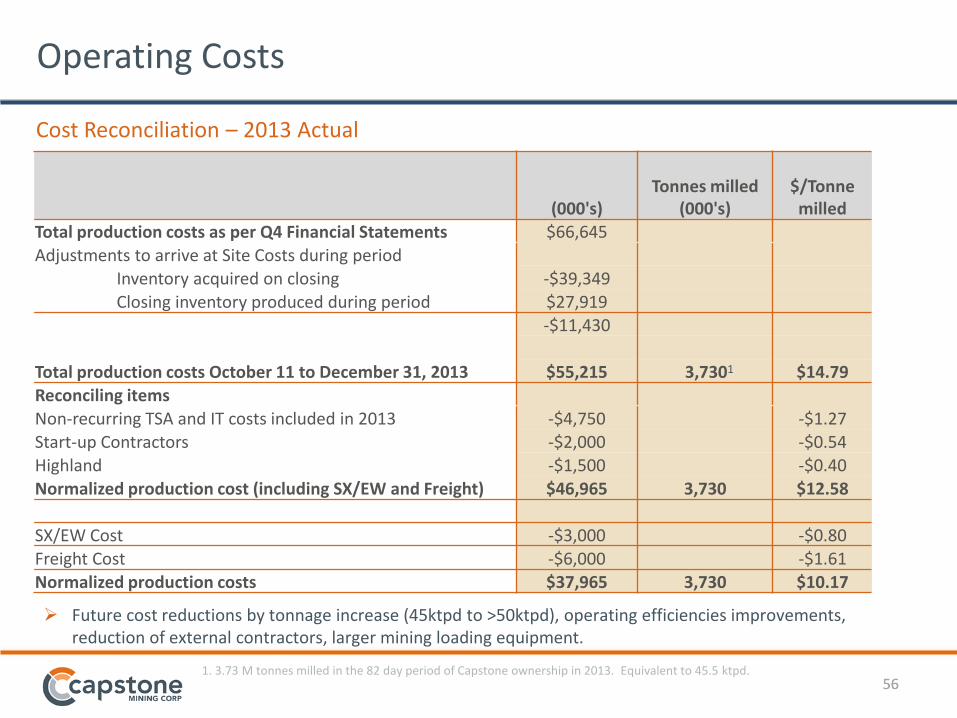

Operating Costs

(000's)

Tonnes milled (000's)

$/Tonne milled

Total production costs as per Q4 Financial Statements $66,645

Adjustments to arrive at Site Costs during period

Inventory acquired on closing -$39,349

Closing inventory produced during period $27,919

-$11,430

Total production costs October 11 to December 31, 2013 $55,215 3,7301 $14.79 Reconciling items

Non-recurring TSA and IT costs included in 2013 -$4,750 -$1.27 Start-up Contractors -$2,000 -$0.54

Highland -$1,500 -$0.40 Normalized production cost (including SX/EW and Freight) $46,965 3,730 $12.58

SX/EW Cost -$3,000 -$0.80 Freight Cost -$6,000 -$1.61

Normalized production costs $37,965 3,730 $10.17

Cost Reconciliation – 2013 Actual

Future cost reductions by tonnage increase (45ktpd to >50ktpd), operating efficiencies improvements, reduction of external contractors, larger mining loading equipment.

1. 3.73 M tonnes milled in the 82 day period of Capstone ownership in 2013. Equivalent to 45.5 ktpd.

57 57

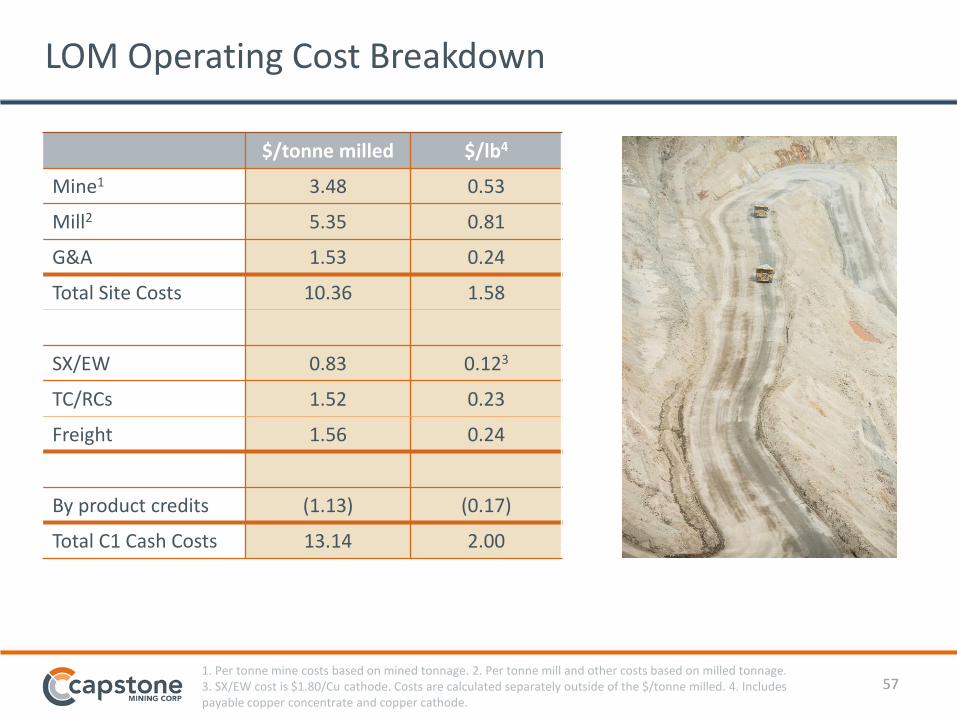

LOM Operating Cost Breakdown

1. Per tonne mine costs based on mined tonnage. 2. Per tonne mill and other costs based on milled tonnage. 3. SX/EW cost is $1.80/Cu cathode. Costs are calculated separately outside of the $/tonne milled. 4. Includes payable copper concentrate and copper cathode.

$/tonne milled $/lb4

Mine1 3.48 0.53

Mill2 5.35 0.81

G&A 1.53 0.24

Total Site Costs 10.36 1.58

SX/EW 0.83 0.123

TC/RCs 1.52 0.23

Freight 1.56 0.24

By product credits (1.13) (0.17)

Total C1 Cash Costs 13.14 2.00

58 58

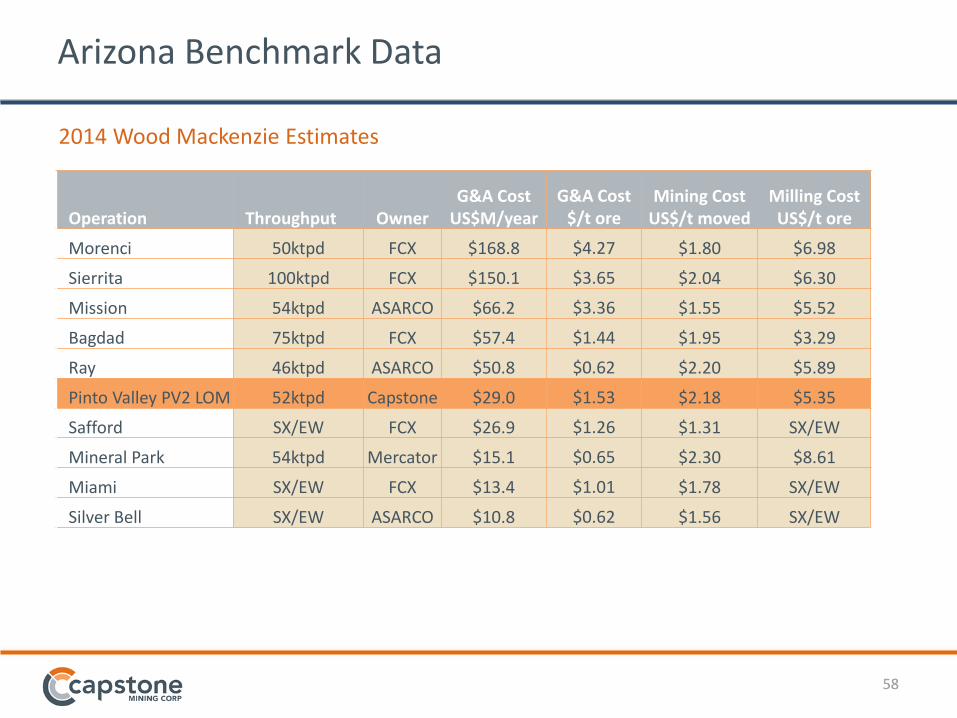

Arizona Benchmark Data

Operation Throughput Owner G&A Cost

US$M/year G&A Cost

$/t ore Mining Cost

US$/t moved Milling Cost US$/t ore

Morenci 50ktpd FCX $168.8 $4.27 $1.80 $6.98

Sierrita 100ktpd FCX $150.1 $3.65 $2.04 $6.30

Mission 54ktpd ASARCO $66.2 $3.36 $1.55 $5.52

Bagdad 75ktpd FCX $57.4 $1.44 $1.95 $3.29

Ray 46ktpd ASARCO $50.8 $0.62 $2.20 $5.89

Pinto Valley PV2 LOM 52ktpd Capstone $29.0 $1.53 $2.18 $5.35

Safford SX/EW FCX $26.9 $1.26 $1.31 SX/EW

Mineral Park 54ktpd Mercator $15.1 $0.65 $2.30 $8.61

Miami SX/EW FCX $13.4 $1.01 $1.78 SX/EW

Silver Bell SX/EW ASARCO $10.8 $0.62 $1.56 SX/EW

2014 Wood Mackenzie Estimates

59 59

PV2 Sensitivities

VARIATION

AFTER TAX NPV AFTER TAX NPV

@ 0%

($M) @ 8.0%

($M)

Copper Price

-20% 306 254

-10% 682 512

Base Case 1,011 738

10% 1,324 952

20% 1,620 1,155

Total Operating Costs

-20% 1,415 1,011

-10% 1,221 880

Base Case 1,011 738

10% 785 585

20% 537 418

60 60

2014 Guidance

61 61

2014 Guidance

Tonnes milled (millions) 18.2

Copper grade (%) 0.39

Copper recovery (%) 88.5

Production (contained in concentrates)

Copper (tonnes) 63,500

Copper cathode (tonnes) 2,800

Molybdenum (000s) 660

Silver (million ounces) 0.3

C1 cash costs/lb payable Cu net of by-product credits and selling costs1

$1.90 - $2.00

1. This is an alternative performance measure.

62 62

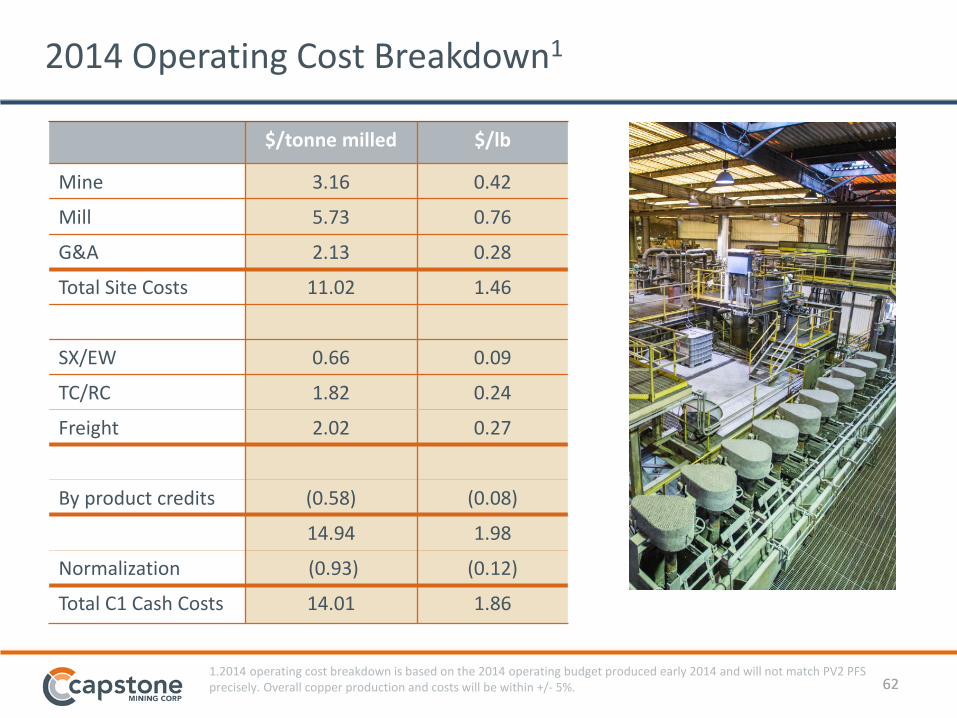

2014 Operating Cost Breakdown1

$/tonne milled $/lb

Mine 3.16 0.42

Mill 5.73 0.76

G&A 2.13 0.28

Total Site Costs 11.02 1.46

SX/EW 0.66 0.09

TC/RC 1.82 0.24

Freight 2.02 0.27

By product credits (0.58) (0.08)

14.94 1.98

Normalization (0.93) (0.12)

Total C1 Cash Costs 14.01 1.86

1.2014 operating cost breakdown is based on the 2014 operating budget produced early 2014 and will not match PV2 PFS precisely. Overall copper production and costs will be within +/- 5%.

63 63

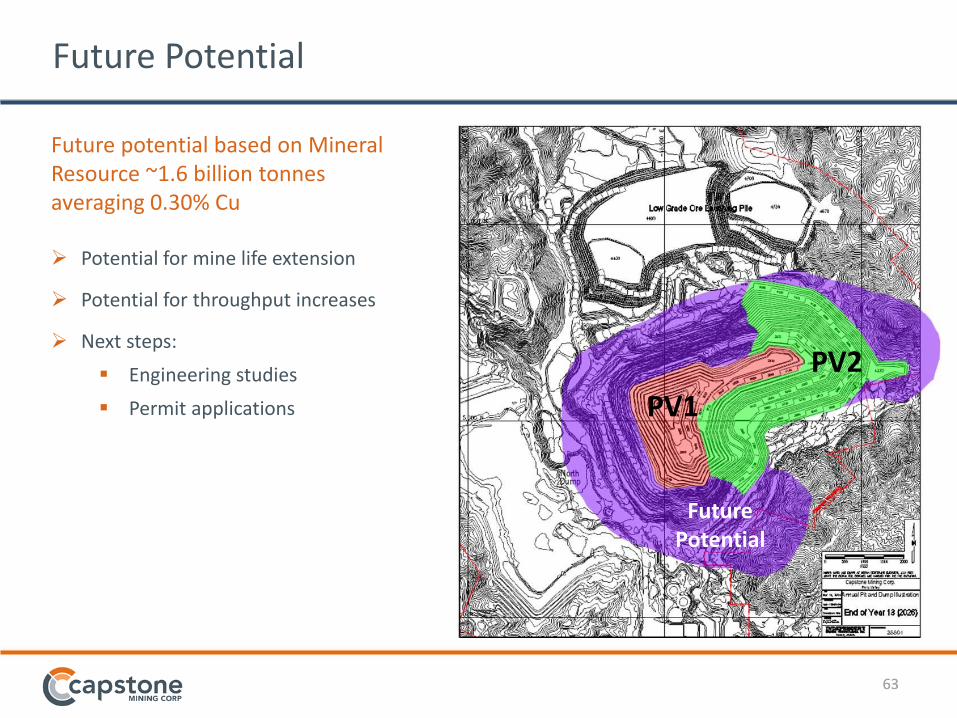

Future Potential

Future potential based on Mineral Resource ~1.6 billion tonnes averaging 0.30% Cu Potential for mine life extension

Potential for throughput increases

Next steps:

Engineering studies

Permit applications

PV1

PV2

Future Potential

64 64

HSEC and Permitting

65 65

Safety Program – Reportable Incidents

Total Reportable Incident Frequency Rate – LTM

0

2

4

6

8

10

12

March May July Sept Nov Jan

Month TRIFR Rolling 12 month MSHA National Avg.

Safety is non-negotiable; it ensures the well-being of our people and our business.

5 MSHA Reportable Incidents since Capstone assumed ownership

4 Restricted Duty

1 Lost Time Injury

Total Reportable Incident Frequency Rate

PV 12-month rolling average is 3.46

Surface metal mining average is 2.45

Objective to improve safety training and eliminate incidents

PV rolling average since assuming ownership is 1.67

Capstone assumes ownership Oct 11, 2013

66 66

Environmental Program – Non-Reportable Incidents

2014 Environmental Targets

Provide environmental awareness training to all employees

Increase the reporting for minor spills to create a non-reportable spill baseline

Close out 100% of the items identified during the December 2013 Spill, Prevention, Control & Counter measures inspection

Prior to Capstone ownership, Pinto Valley did not capture the number of minor or non-reportable spills. Using the data we collect in 2014 we will create targets for the reduction of non-reportable spills in future years.

67 67

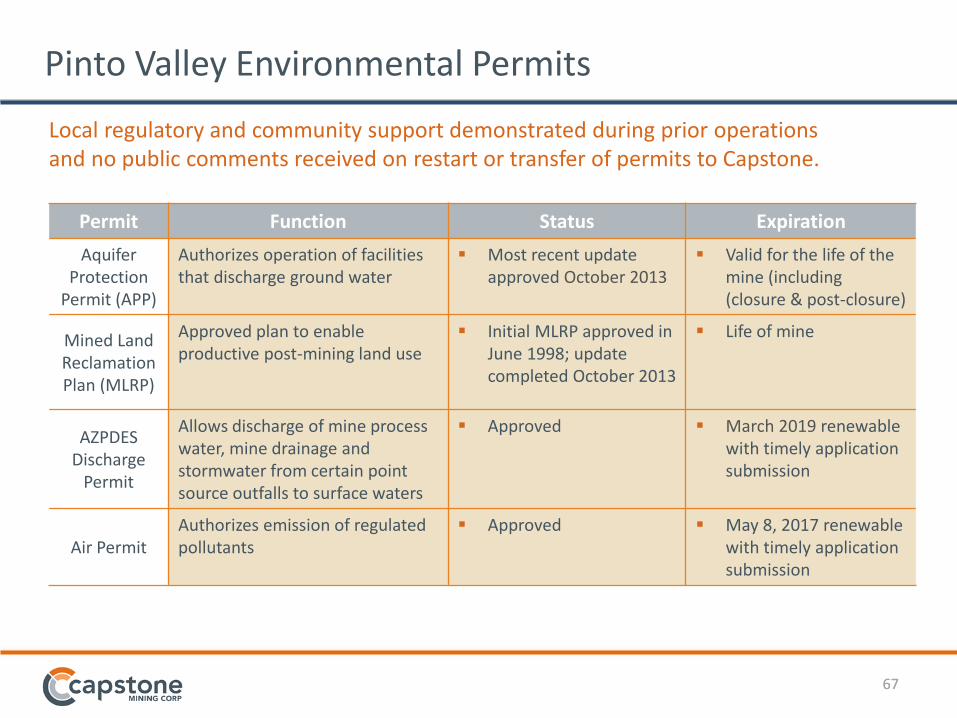

Permit Function Status Expiration

Aquifer Protection

Permit (APP)

Authorizes operation of facilities that discharge ground water

Most recent update approved October 2013

Valid for the life of the mine (including (closure & post-closure)

Mined Land Reclamation Plan (MLRP)

Approved plan to enable productive post-mining land use

Initial MLRP approved in June 1998; update completed October 2013

Life of mine

AZPDES Discharge

Permit

Allows discharge of mine process water, mine drainage and stormwater from certain point source outfalls to surface waters

Approved March 2019 renewable with timely application submission

Air Permit Authorizes emission of regulated pollutants

Approved May 8, 2017 renewable with timely application submission

Pinto Valley Environmental Permits

Local regulatory and community support demonstrated during prior operations and no public comments received on restart or transfer of permits to Capstone.

68 68

Permitting – Next Steps

Existing Capstone proponent on Plan of Operations

submitted by BHPB in September 2009

PV2

Optimized mine plan will require amendment, initial approach to regulators received positively

Key change is waste haul distance

Future Potential

Internal scoping study may be followed by PV3 PFS at which time EIS will be submitted

No new permits required for 12 years under BHPB’s mine plan. Capstone’s PV2 optimized mine plan contemplates some modifications.

69 69

Unless otherwise indicated, Capstone has prepared the technical information in this presentation (“Technical Information”) based on information contained in the

technical reports and news releases (collectively the “Disclosure Documents”) available under Capstone Mining Corp.’s company profile on SEDAR at www.sedar.com. Each

Disclosure Document was prepared by or under the supervision of a qualified person (a “Qualified Person”) as defined in National Instrument 43-101 – Standards of

Disclosure for Mineral Projects of the Canadian Securities Administrators (“NI 43-101”). For readers to fully understand the information in this presentation, they should

read the Technical Reports (available on www.sedar.com) in their entirety, including all qualifications, assumptions and exclusions that relate to the information set out in

this presentation which qualifies the Technical Information. Readers are advised that mineral resources that are not mineral reserves do not have demonstrated economic

viability. The Disclosure Documents are each intended to be read as a whole, and sections should not be read or relied upon out of context. The Technical Information is

subject to the assumptions and qualifications contained in the Disclosure Documents.

The technical information in this presentation has been prepared in accordance with Canadian regulatory requirements set out in National Instrument 43-101 Standards of

Disclosure for Mineral Projects of the Canadian Securities Administrators ("NI 43-101") and reviewed by Brad Skeeles, P.Eng. VP of North American Operations (Technical

Information related to mining and production) and Brad Mercer, P. Geol., Senior Vice President, Exploration (Technical Information related to mineral exploration

activities), and reviewed and approved by Gregg Bush, P. Eng., Senior Vice President and Chief Operating Officer for Capstone Mining, all "Qualified Persons" under NI 43-

101.

The PV2 PFS project was directed by Capstone with contributions from Kirkham Geosystems Ltd. (geology, Resource estimation), Independent Mining Consultants Inc.

(reserve, geotechnical, mine design and schedule, equipment selection), KWM Consulting Inc. (metallurgy, mill operation), AMEC Environment & Infrastructure Inc.

(tailings), Stantec (Infrastructure and PFS report compilation), SRK (US), Inc. (environmental), and Adam M Consulting Inc. (financial modelling). Personnel from each of

these companies will be signing off as a QP as defined in NI 43-101 for their specific responsibilities. The following QP’s will author the technical report: Mel Lawson, P.E. of

Stantec, Garth Kirkham, P.Geo. of Kirkham Geosystems Ltd., John Marek P.E. of Independent Mining Consultants, Inc., Ken Majors P.Eng. of KWM Consulting Inc, Tony

Freiman, P.E. of AMEC Inc., Adam Majorkiewicz, P.Eng of Adam M Consulting Inc. and Cori Hoag C.P.G. of SRK.

The March 2014 Mineral Resource estimate reported herein for the Pinto Valley property was prepared by Garth Kirkham, P. Geo, Kirkham Geosystems Ltd., an

independent QP. Based on the Mineral Resource Estimate, a standard methodology for pit limit analysis, mining sequence, and cut-off grade optimization, including

application of mining dilution, process recovery, economic criteria and physical mine and plant operating constraints, has been followed to design the Pinto Valley pit and

determine the Mineral Reserve Estimate.

Compliance with NI 43-101

70

For additional information, please visit capstonemining.com or contact us at:

Phone: +1-604-684-8894

Toll Free: 1-866-684-8894

Email: [email protected]

Last updated March 25, 2014