phillips carbon black limited phillips carbon black - at a glance largest cb capacity of 4,72,000 mt...

TRANSCRIPT

Phillips Carbon Black Limited

Power(ful) Growthwww.pcblltd.com May 2014

1

2

RP- Sanjiv Goenka Group

Power & Natural

Resources Carbon Black Retail

Media & Entertainment

InfrastructureIT &

Education

Power & NaturalResources

Retail

Carbon Black

Infratructure

Media & Entertainment

IT & Education

CESC - 4th largest Private Power Utility

Noida Power *- Private Discom in Noida

Integrated Coal Mining * - Pioneer in private sector Coal Mining

Harrisons Malayalam – Largest Plantation company in South India

Spencer`s Retail *- Pioneer in organized food retailing in India

Phillips Carbon Black - Largest in India & 8th largest in world

CESC Properties*- Showcasing East India’s 1st Specialty Mall

Saregama India - Biggest collection of Indian Music

Open* – Weekly current affairs magazine

Firstsource Solutions - Among the top 3 pure play BPO companies in India

Business Sectors Companies

RevenueRs. 140 billion+

* unlisted

RP- Sanjiv Goenka Group – Business Sectors

3

Power & Natural Reources

51%

Media & Entertainment

1%

Carbon Black19%

IT & Education19%

Retail10%

(Rs. bn )

*market cap as on 31st December 2013

Gross

Revenues

(FY`13)

EBIDTA

(FY`13)

Net Profit

(FY`13)

Current

Market cap*

Promoter

Holding

Institutional

Holding

CESC 53.20 14.20 6.18 58.20 52% 35%

Firstsource Solutions 28.20 2.80 1.47 14.51 57% 22%

Phillips Carbon Black 22.80 1.10 (0.20) 2.13 52% 21%

Spencer`s Retail 13.50 (0.78) (2.10) - 100% -

Noida Power Company 8.00 2.73 1.33 - 73% -

Saregama India 1.75 0.28 0.11 1.44 55% 24%

Harrisons Malayalam 3.47 0.25 0.02 0.93 50% 5%

Integrated Coal Mining 3.70 0.36 0.22 - 100% -

Crescent Power 1.24 0.62 0.20 - 100% -

Financials of RP- Sanjiv Goenka Group companies

4

5

Phillips Carbon Black - at a Glance

Largest CB Capacity of 4,72,000 MT p.a. across four locations in India Co –Generation Green Power Plant at each location

Capacity

Largest producer of Carbon Black in India and 7th largest in the World Second fastest growing CB company in the world

Business

Leading tyre companies around the globeCustomers

Exports to 20 countriesExports

Stock Listed on BSE (Code – 506590); NSE (PHILIPCARB)

Rs. 1.9 bn

CB – Overseas (Ba Ria Vung Tau Province in Vietnam) CPP – 8 MW in Mundra Carbo Chemicals Plant in Orissa

Expansion Plans

Cochin unit has been awarded Best Environment Management Co. by

Kerala state Government in 2011 PCBL received “Top Exports” awards for 2011-12

Awards

CRISIL Equities has assigned a valuation grade of 3/5 & fundamental

grade of 3/5 as on Feb’14Ratings

Market Cap As on Mar’14

6

PCBL receives “Top Exports” awards for 2011-12

7

Business Profile

Market Leadership

– Largest producer of CB in India for many

years

- Ranks 7th globally

High quality of R&D setup

- Manufactures all grades for tyre

industry, all four soft grades for plastic

industry

Value creating business model

– Power plants based on tail gas

- Now going for backward integration and

extension to Carbo Chemical business

Being a market leader, PCBL enjoys economies

of scale

Domestic Market Share in FY13

Sl.No Location CB (MT) CPP (MW)

1 Durgapur, W.Bengal 1,52,000 30.00

2 Palej, Gujarat 90,000 12.00

3 Mundra, Gujarat 140,000 24.00

4 Kochi, Kerala 90,000 10.00

Total 4,72,000 76.00

Current installed capacity for CB & CPP

PCBL38%Hi-Tech

38%

Others24%

8

High quality investors in the Company

Business Profile..contd

Shareholding Pattern as on Mar’13

Leading institutional investors include:

National WestMinster Bank PLC

Reliance Capital Trustee Co. Ltd

ACACIA

Birla Sun Life Trustee Company Pvt Ltd

Jupiter South Asia Investment Company Ltd

Max New York Life Insurance Co. Ltd

ICICI Prudential Emerging Star

The Dai – Ichi Life Insurance Company Limited

India Optima Fund

Promoter, 52%

Domestic institutions,

19%

Public, 19%

FII, 10%

9

Business Profile..contd

CB Revenue Split : FY14

Exports – 34%

Domestic – 66%

Increasing Power revenues and export of Carbon Black is improving PCBL’s business model

Carbon Black, 94%

Power,6%

Revenue Split : FY14

Strategic plant locations nearer to customers

Chennai

Apollo, JK, Michelin, MRF

JK

Bridgestone

MRF

Birla

Ceat

Mundra140,000 MT +24 MW

Palej90,000 MT +12 MW

Kochi90,000 MT + 10 MW

Durgapur1,52,000 MT + 30 MW

Head Office,Kolkata

JV for CB Plant in Vietnam

10

Vietnam

Under Execution210,000 MT

Orissa ( Carbo Chemicals)

MRF

Apollo

JK

Ceat

New TyreCapacities

Our CB Plants

Our CarboChemical

Plants

11

Exports to 20 Countries

IRAN

VIETNAM

JAPAN

S. KOREA

TAIWAN

PHILIPPINES

CHINA

AUSTRALIA

NEW ZEALAND

INDONESIA

MALAYSIA

TURKEY

UAE

KENYA

SPAIN

ISRAEL

SRILANKA

BANGLADESH

SINGAPORE

USA

12

Forward Integration - Green Power Generation

Waste gases from plants being used

to produce electricity, Surplus power

sold to grid

CPP at Palej is registered as a CDM

Project with UNFCCC

Waste Gas generated at

the CB Plant

Waste Gas Electricity

Internal plant

requirement

Surplus power

sold to grid

Incineration

Waste Gas Co-

generation plant

earlier

now

Sl.No Location CPP (MW) Year of

Commission

1 Palej, Gujarat 12.00 Mar’05

2 Durgapur, W.Bengal 30.00 Apr’08

3 Mundra, Gujarat 16.00 Dec’09

4 Kochi, Kerala 10.00 Apr’11

5 Mundra, Gujarat 08.00 Jun’12

Total 76.00

Key Milestones

PCBL’s strength lies in both Greenfield & Brownfield expansion

13

Capacity increase:

Mundra : 50,000 MT and 8MW CPP

Durgapur : 12,000 MT

1960 - 2004

Aggressive Growth : Total CB Capacity is 4,72,000 MT and 76 MW CPP

2005 2007 2008 2009 2010 2011 2012 2013

30 MW

CPP at

Durgapur

Golden

Jubilee

Year

MOU for Plant in

Vietnam90,000 MT at

Mundra

16 MW CPP

at Mundra

10 MW CPP

at Kochi

12 MW CPP

at Palej

• Started with Phillips Petroleum Co, USA at Durgapur with 14,000 MT.

• Collaboration with Columbian Chemical; Total Capacity was 78,000 MT

• Acquisition of CB division of Gujarat Carbon Ltd, 25,000 MT; Total Capacity was 1,03,000 MT

• Amalgamation with Carbon & Chemicals, Ltd , Kochi, 40,000 MT; Total Capacity increased to 143,000 MT

Total Capacity by 2004 was 270,000 MT

Capacity Increase:

Cochin: 50,000 MT

14

Tyre capacities coming up in Asia incl. India

High earnings stability due to Backward &

Forward integration, different geographies &

customers

Cost advantages in Asia – CB capacities

shifting to emerging markets

Capacity Consolidation – Smaller players

shutting down plants

Entrepreneurial management team with 50

years experience

High Crude and CBFS prices

Dumping by China and Korea,

At times difficult to pass on 100% price

increase of raw materials to customers

Fluctuation in power prices

Exchange Fluctuations

Growth Drivers Key Risks

Growth Drivers & Risks

15

Tyre Capacity Expansion

Company Location Investment [` bn] Completion by

Apollo Tyres Limited

Tamilnadu and Gujarat

21

Mar-12

Chennai, Tamil Nadu

Vadodara, Gujarat

Balkrishna Industries LimitedBhuj, Gujarat 12 Jun-12

Rajasthan & Maharashtra 2 Sep-11

Bridgestone India P Limited

Chakan, Pune 26 Jan-13

3 Aug-13

Pithampur 1

3 Sep-11

Ceat Limited Halol 7 Jun-11

Ambarnath, Maharashtra 3 Dec-12

Dunlop India Limited Guwahati, Assam 5 Dec-11

Falcon Tyres Limited Haridwar, Uttarakhand 6 Mar-12

JK Tyre & Industries LimitedMysore, Karnataka 3 Aug-11

Sriperumbudur, Tamil Nadu 15 Oct-12

Kesoram Industries Limited

Haridwar, Uttarakhand 10 Dec-12

Haridwar, Uttarakhand 4 Sep-11

Balasore, Orissa 5 Sep-11

MRF Limited

Ankampaly, Andhra Pradesh

38

Sep-11

Trichy Sep-11

Pondicherry Dec-12

Michelin 40 Mar-12

Total 202Source: CMIE, Company

16

Global Carbon Black Demand Break-Up

2010 Forecast (‘000 tonnes)

-

2,000

4,000

6,000

8,000

10,000 Non Tires

Tires

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2015 Forecast (‘000 tonnes)

17

Carbon Black-Grades & Uses

The hard grades are used in the tyre surface, which

comes in contact with the road and are subject to

higher friction.

The soft grades are used for the side wall of tyres &

also for plastic industry

Tyre, 65%

Rubber,15%

Belts & Hoses,

10%

Printing Ink & Other

Speciality, 10%

Utilization of carbon black (Sector-wise)

18

Key Investment Highlights

2

1

5

3

4

Forward integration with Green Power generation - improving

value chain for investors

Global leadership in Technological Innovation

Strong customer relationship

Efficient cost management and rationalization process in place

Backward integration with Carbo Chemicals Project

19

Power Generation mitigates commodity risk ₹ mn

9,881 10,182 11,478 11,780

16,141

22,675 21,921 22,122 106 149

155 545

760

894 886

652

-

3,000

6,000

9,000

12,000

15,000

18,000

21,000

24,000

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Carbon Black Power

20

Efficient Cost Management & Rationalization

Contribution Trend

EBITDA & PAT Margin Trend

( ₹ Bln) FY09 FY10 FY11 FY12 FY13 FY14

Sales Volume (MT) 210,553 255,777 308,605 314,348 293,309 287,838

Revenue - CB 10.60 11.78 16.14 22.68 21.92 22.12

Revenue - Power 0.16 0.54 0.76 0.89 0.89 0.65

Contribution 1.00 2.69 2.94 3.87 2.13 2.40

Contribution (₹ /MT) 4,751 10,531 9,541 9,633 7,248 8,352

-10%

-5%

0%

5%

10%

15%

20%

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

EBITDA (%) PAT(%)

Strong Customer Relationship

Domestic Customers International Customers

21

22

Financial Overview

₹ mn FY09 FY10 FY11 FY12 FY13 FY14

Profit & Loss Statement

Net Sales 11,633 12,350 16,901 21,867 22,849 22,775

EBITDA 245 1,907 2,345 2,339 1,097 461

Depreciation 196 312 386 486 508 537.4

Interest 294 289 316 582 721 802.3

PBT -973 1,310 1,643 1034 (400) -879.1

Tax -325 79 481 160 (194) -13.1

PAT -648 1,230 1,163 874 (206) -866

Balance Sheet

Sources of Funds

Net Worth 2,182 3,244 5,223 5,223 5,891 5,025

Debt 4,256 5,555 5,014 5,081 8,767 6,671

Deferred Tax 17 96 569 520 527 299

Capital Employed 6,455 8,895 10,806 10,824 14,656 11,995

Application of Funds

Net Block 2,280 5,932 5,783 5,783 7,528 8,576

CWIP 3,828 923 2,058 2,059 1,590 674

Investments 378 378 576 582 724 724

Net Working Capital -38 1,662 2,389 2,400 (2,646) 2,022

Miscellaneous Expenditure 7 0 0 0 0 0

Total Assets 6,455 8,895 10,806 10,824 23,025 11,995

Debt/Equity 1.95 1.71 0.96 1.16 1.48 1.328

23

Return to the ShareholdersEPS (Rs) ROCE (%)

Debt – Equity Ratio Debt – EBITDA Ratio

35.37

-24.12

43.43

35.43

25.82

-5.99-25.12-30.00

-10.00

10.00

30.00

50.00

70.00

FY08 FY09 FY10 FY11 FY12 FY13 FY14

1.20

1.95

1.70

0.96

1.16

1.48

1.33

0.50

1.00

1.50

2.00

FY08 FY09 FY10 FY11 FY12 FY13 FY14

1.91

-8.40

2.91 2.14 2.39

13.1614.48

-9

-6

-3

0

3

6

9

12

15

FY08 FY09 FY10 FY11 FY12 FY13 FY14

26%

-12%

21% 20%22%

-3% -0.64%-20%

-10%

0%

10%

20%

30%

FY08 FY09 FY10 FY11 FY12 FY13 FY14

24

Performance Summary

Particulars Q4FY14 Q3FY14 %Change (QoQ) Q4FY13 %Change

(YoY)

Production (MT) 73,867 71,564 3% 66,775 11%

Capacity Utilization(%) 80% 78% - 73% -

Total Sales Volume (MT) 77,298 66,842 16% 69,600 11%

Domestic (MT) 50,635 46,113 10% 48,375 5%

Export (MT) 26,663 20,729 29% 21,225 26%

Rs Crs Rs Rs Crs Rs Rs Crs

Net Sales 594 560 6% 535 11%

EBITDA (before forex) 43 44 -4% 33 27%

EBITDA% 7.2% 7.9% - 6.2% -

PBT 2 -17 - 1.5 -32%

PAT 2 -15 - 4.9 -59%

25

Performance Summary

Particulars FY14 FY13 % Change

Production (MT) 288,676 296,555 -3%

Capacity Utilization(%)78% 83%

Total Sales Volume (MT) 287,839 293,309 -2%

Domestic (MT) 199,100 208,136 -4%

Export (MT) 88,739 85,173 4%

Rs Crs Rs Crs

Net Sales 2277 2285

EBITDA (before forex) 155 119 30%

EBITDA% 6.8% 5.2%

PBT -88 -40

PAT -87 -21

Power Sales

Power Sales (KwH in lacs) Net Sales (` Crs) Net Realization

Q1FY13 792 24.39 3.08

Q2FY13 725 21.04 2.90

Q3FY13 657 19.19 2.92

Q4FY13 550 18.73 3.41

Q1FY14 488 15.54 3.18

Q2FY14 527 17.09 3.24

Q3FY14 528 17.67 3.35

Q4FY14 484 13.68 2.82

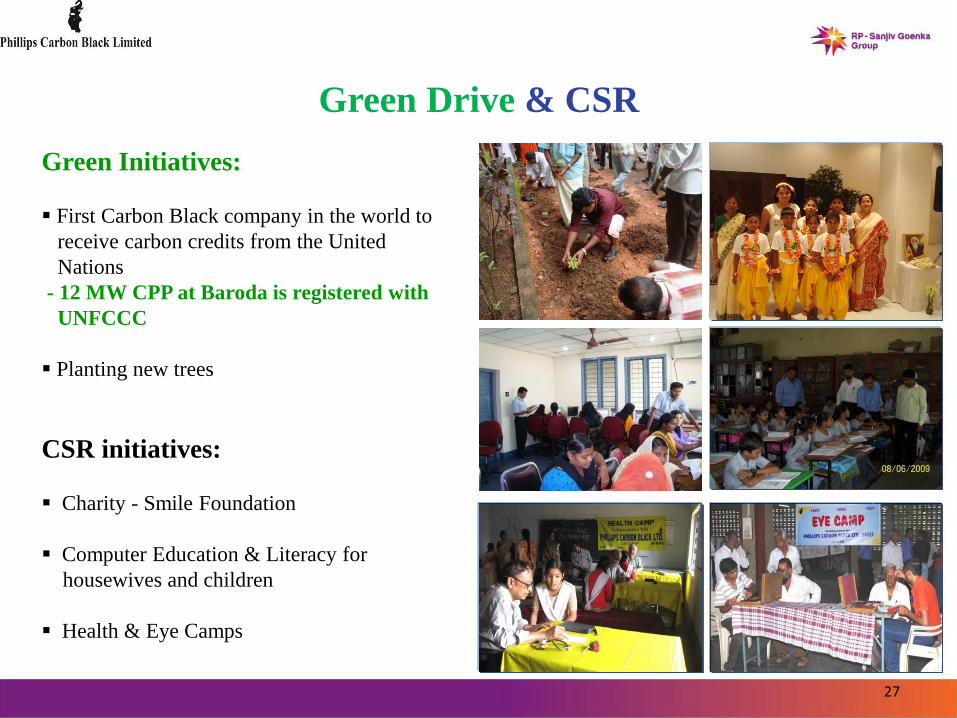

Green Drive & CSR

Green Initiatives:

First Carbon Black company in the world to

receive carbon credits from the United

Nations

- 12 MW CPP at Baroda is registered with

UNFCCC

Planting new trees

CSR initiatives:

Charity - Smile Foundation

Computer Education & Literacy for

housewives and children

Health & Eye Camps

27

28

Thank You