philippines - international university of japan profile 2000 philippines this country profile is a...

TRANSCRIPT

COUNTRY PROFILE 2000

PhilippinesThis Country Profile is a reference tool, which providesanalysis of historical political, infrastructural and economictrends. It is revised and updated annually. The EIU’s CountryReports analyse current trends and provide a two-yearforecast

The full publishing schedule for Country Profiles is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through our digital portfolio, where our latest analysis isupdated daily; through printed subscription products ranging from newsletters to annual referenceworks; through research reports; and by organising conferences and roundtables. The firm is a memberof The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1000Fax: (44.20) 7499 9767E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

Hong KongThe Economist Intelligence Unit25/F, Dah Sing Financial Centre108 Gloucester RoadWanchaiHong KongTel: (852) 2802 7288Fax: (852) 2802 7638E-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryThis publication can be viewed by subscribing online at http://store.eiu.com/brdes.html

Reports are also available in various other electronic formats, such as CD-ROM, Lotus Notes, onlinedatabases and as direct feeds to corporate intranets. For further information, please contact your nearestEconomist Intelligence Unit office

London: Jan Frost Tel: (44.20) 7830 1183 Fax: (44.20) 7830 1023New York: Alexander Bateman Tel: (1.212) 554 0643 Fax: (1.212) 586 1181Hong Kong: Amy Ha Tel: (852) 2802 7288/2585 3888 Fax: (852) 2802 7720/7638

Copyright© 2000 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-5979

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Comparative economic indicators, 1999

1

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Contents

3 Basic data

4 Political background4 Historical background9 Political forces

12 Constitution and institutions13 International relations and defence

14 Resources and infrastructure14 Population16 Health16 Education16 Natural resources and the environment18 Transport and communications19 Energy provision

20 The economy20 Economic structure21 Economic policy25 Economic performance27 Regional trends

28 Economic sectors28 Agriculture, forestry and fishing30 Mining and semi-processing31 Manufacturing32 Construction33 Financial services34 Other services

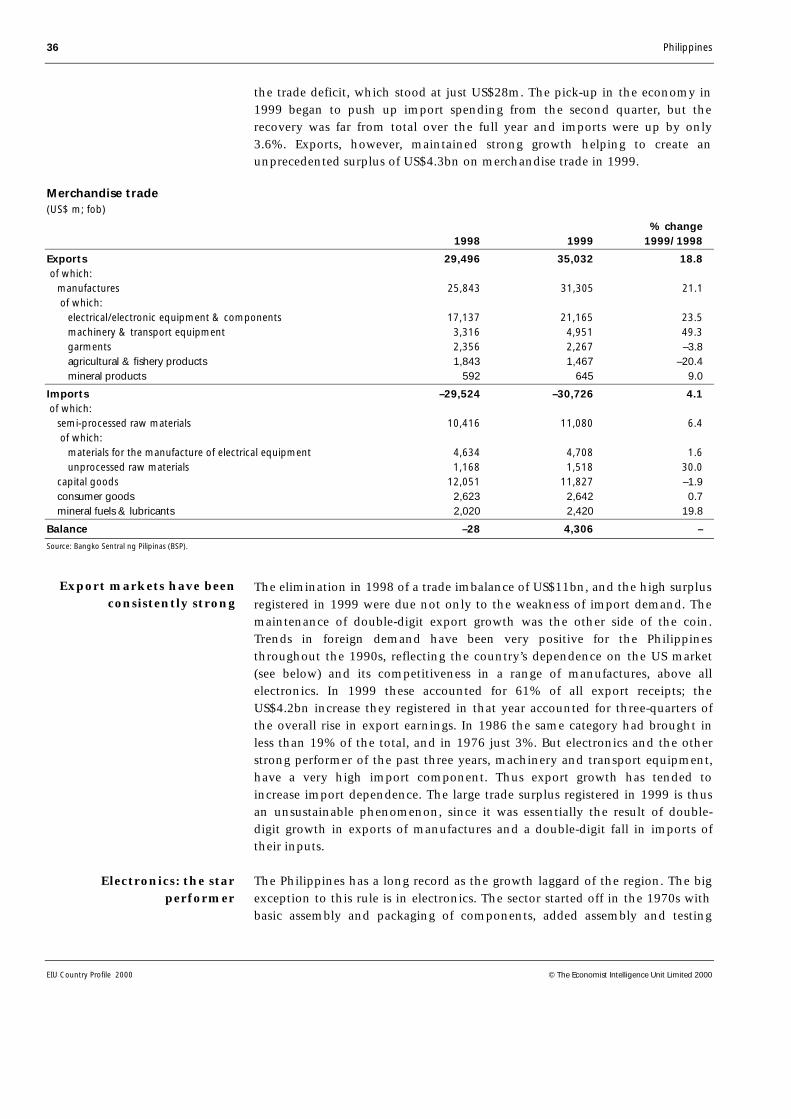

35 The external sector35 Trade in goods38 Invisibles and the current account40 Capital flows and foreign debt42 Foreign reserves and the exchange rate

44 Appendices44 Sources of information45 Reference tables45 Population45 Labour force45 Structure of employment46 Transport statistics46 Energy consumption by source47 Trend of government revenue and expenditure47 Outstanding internal public debt47 Money supply and credit48 Interest rates48 Gross domestic product48 Gross domestic product by expenditure49 Gross domestic product by sector

August 1st 2000

2

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

49 Prices and earnings50 Production of major crops50 Meat production50 Output of wood products50 Fishing production51 Minerals production51 Manufacturing production52 Structure of manufacturing industry, 199552 Private construction53 Assets of financial system53 Philippines Stock Exchange indicators53 Visitor arrivals by country of residence54 Exports54 Imports55 Key commodity exports55 Main trading partners56 Direction and composition of trade, 199857 Balance of payments, IMF estimates57 Balance of payments, national estimates58 Foreign equity investment inflows by major country of origin and by sector59 External debt60 Net official development assistance60 Foreign reserves60 Exchange rates

Philippines 3

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

Philippines

Basic data

300,176 sq km, of which 53% is classified as forest (although only 21% isunder forest cover) and 34% is under agricultural cultivation

76.37m (average for first half of 1999: official estimate)

Population in ‘000, 1995

Metropolitan Manila Davao 1,007(National Capital Region) 9,454 Cebu 662 of which: Zamboanga 511Manila (capital) 1,655 Cagayan de Oro 428Quezon City 1,989 Las Pinas 413Kalookan 1,023 Bacolod 402Makati 484 Pasay 368Pasig 471 Iloilo 335Valenzuela 437

Tropical

Hottest month, May, 24-34°C; coldest month, January, 21-30°C (average dailyminimum and maximum); driest month, February, 13 mm average rainfall;wettest month, July, 432 mm average rainfall

Tagalog, English and Spanish; many local dialects

Metric system; also some local units including the picul (63 kg) for sugar andfibres, and the cavan (75 litres) for cereals

Peso (P)=100 centavos. Average exchange rate in 1999: P39.09:US$1. Exchangerate on August 1st 2000: P44.80:US$1

8 hours ahead of GMT

January-December

January 1st; February 25th (Freedom Day); Maundy Thursday; Good Friday;May 1st (Labour Day); May 6th (Araw ng Kagitingan); June 12th(Independence Day); August 27th (National Heroes’ Day); September 11th(Barangay Day); September 21st (National Thanksgiving Day); November 1st(All Saints’ Day); November 30th (Bonifacio Day); December 25th, 30th, 31st

Land area

Population

Main towns

Climate

Languages

Weights and measures

Currency

Time

Fiscal year

Public holidays

Weather in Manila(altitude 14 metres)

4 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Political background

The Philippines is a pluralist democracy modelled on that of the US, with anexecutive presidency, a bicameral Congress and a Supreme Court that can ruleon the constitutionality of government actions. Joseph Estrada was electedpresident in May 1998 for a single six-year term. A pro-administration coalitionhas an overall majority in both the Senate and the House of Representatives.

Historical background

A Spanish expedition led by Ferdinand Magellan first reached the Philippinearchipelago in 1521. European settlement did not begin until more than 40years later, at Cebu (in the central Philippines), but within ten years Spanishcontrol had extended over most of the Visayas and central Luzon, encounteringlittle effective resistance from the indigenous Malay population, which lackedany unified political authority. The principal motivation for Spanish colonialsettlement was religious conversion, and little effort was made to exploit theislands’ economic resources. Only at the beginning of the 19th century wereother Europeans permitted to engage in economic activity. Sugar, coconuts,abaca and tobacco were developed as export crops and became the foundationsof the economy, while a Chinese entrepreneurial class evolved, marrying intothe indigenous population and providing an elite based on land ownership.

Members of the elite took over leadership of a popular rebellion against Spanishrule that broke out in 1896. The struggle continued into early 1898, when theUS intervened. In December 1898 Spain ceded the Philippines to the US.

The new republic inaugurated a month later expected Washington to grantindependence, and when this failed to happen open conflict broke out betweenthe new republic’s army and the occupying forces. A year of fierce resistance bythe Filipinos came to an end in April 1901. Under US colonial rule democraticinstitutions were introduced, Filipinos increasingly took over all political andbureaucratic positions, and English-language education was extended through-out the country. However, the social and economic structure was little changed.In 1934 the Philippines was made an internally self-governing commonwealth,with full independence scheduled for July 4th 1946.

This transition was interrupted by the Japanese invasion in December 1941.The Japanese occupation and the battle for liberation destroyed much of thecountry’s physical infrastructure—Manila was devastated—and left a bitterresidue of charges and countercharges of collaboration. The country resumedits path to full independence, which was achieved on schedule in 1946.

The newly independent republic initially maintained preferential economicrelations with the US. Goods from the Philippines (subject to quota) had duty-free access to the US until 1954, followed by a gradual move to full tariffs by1974. US citizens had parity with Filipinos in the exploitation of the country’snatural resources until 1974. In 1947 the US was granted a 99-year lease on23 bases, including the two major bases at Clark Field and Subic Bay in Luzon.

The colonial andcommonwealth period

An independent republicclosely tied to the US

Philippines 5

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

The new republic had a constitution modelled on that of the US and, as inWashington, power tended to alternate between two parties, the Nacionalistasand the Liberals. The fairly peaceful alternation in power within the politicalelite was interrupted in September 1972 as the president, Ferdinand Marcos,neared the end of his second term. Citing the threat from “subversive forces”,the president imposed martial law.

For the next 13 years, until 1986, the Philippines experienced “constitutionalauthoritarianism”. In a series of elections the president and the party he hadcreated, the New Society Movement (Kilusan Bagong Lipunan, KBL), con-sistently recorded overwhelming popular support, whether or not theopposition participated in the exercise. This owed something to the virtualmonopoly of the media by the president and his close associates, but more tomanipulation and outright cheating at the polls. Opposition, which was neverabsent, was growing throughout Mr Marcos’s rule, but with many of its leadersin detention or voluntary exile the moderate opposition seemed unable tomobilise feeling against the administration and its abuses. The most effectiveopposition came from the communist New People’s Army (NPA), which wasactive in rural areas, and from the southern areas, where a secessionist Muslimmovement had been active since before the beginning of martial law.

The situation changed radically in August 1983, when Benigno Aquino, theopposition leader regarded as the most credible alternative to Mr Marcos, wasassassinated minutes after his return from exile and while under military escort.A series of massive demonstrations followed in which the disenchantment ofthe urban middle class, and notably the business community, was expressed forthe first time. This disenchantment owed much to the “crony” system: thegranting of massive privileges (such as monopoly control of coconut and sugarmarketing) to individuals whose main qualifications were their closeness anddevotion to the interests of the Marcos family.

To reassert his own supremacy, Mr Marcos called an early presidential electionfor February 1986. In a close-run contest he was narrowly defeated by thecandidate of a temporarily united opposition, Corazon Aquino, Mr Aquino’swidow. Mr Marcos’s attempt to hold on to power set off a coup attempt in themilitary, backed by the deputy chief-of-staff, Fidel Ramos, and the defenceminister. This received critically important backing from Mrs Aquino’s People’sPower movement and the local Catholic Church. Under pressure from the US,Mr Marcos went into voluntary exile in Hawaii, where he died in 1989.

Under the new regime civil liberties were restored, political prisoners werereleased and an attempt was made to negotiate with the NPA. A new con-stitution, drawn up by a convention appointed by Mrs Aquino, largely restoredthe set-up abolished by President Marcos in 1972 but with new controls on thepresidency based on the experience of the Marcos years.

The newly restored democracy had a difficult initial period. President Aquinohad been brought to power by a coalition of forces—People’s Power and themilitary—in which deep tensions were inherent. Moreover, Mr Marcos persistedin using his still substantial reserves of money and personal loyalty to destabilise

The Marcos autocracy

The return to a freedemocracy

6 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

the regime. From July 1986 there was a series of attempted coups and rumoursof coups, more or less credible, in which elements of the military were involved.In all cases the loyalty of the then chief-of-staff, Mr Ramos, was critical.

Meanwhile, the reform hopes of the early days faded. The much-vaunted landreform was stalled by bureaucratic delay and landlord opposition, widespreadcorruption continued (although the president was not touched by allegationsof misconduct herself), and the government was perceived as ineffectual.

However, the Aquino presidency did achieve a fundamental objective: thetransfer of presidential power at the end of the constitutional term, bydemocratic means and in a comparatively peaceful manner (for thePhilippines). Moreover, the election of Mr Ramos in May 1992 ensured thecontinuation of the political and economic policies of the Aquino admin-istration and was well received by the country’s main foreign creditors and thelocal business community. Within months of coming to office Mr Ramos hadbuilt up a large pro-government majority in Congress, secured a cessation ofhostilities by dissident military groups and begun the process of peacenegotiations with both communist and Muslim secessionist rebels. A ceasefirewas agreed with the Muslim rebels in late 1993, while the communistinsurgency began to weaken, as fissures in the leadership emerged and activemembership fell. Although deep-rooted economic and social problemsremained largely unresolved, the resumption of economic growth and theprospect of its maintenance at more robust levels enhanced the president’spopularity. An electoral pact between the president’s party, Lakas, and the pro-government party of the Aquino period, the Laban ng Demokratikong Pilipino(Laban), delivered a strong majority for the president in the mid-termcongressional election in May 1995.

Important recent events

September 1996: Peace agreement signed with the main Muslim secessionistmovement in Mindanao.

November 1996: Congress approves the most controversial component ofthe comprehensive tax reform package, on excise taxation.

November 1997: Congress approves income tax reform.

May 1998: The anti-administration candidate, Joseph Estrada, comfortablywins the presidency out of a field of ten.

August 1998: Eduardo Cojuangco, the Marcos “super-crony” and founder ofthe main party backing Mr Estrada, regains control of the country’s leadingfood conglomerate.

September-October 1999: Lucio Tan, reputedly the biggest financial backerof the Estrada candidacy, gains a 48% stake in a leading commercial bank,largely through buying up the government’s share option.

April 2000: Breakdown of peace negotiations with the main remaining activesecessionist movement in Mindanao.

Political stability

Philippines 7

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

With his dominance in Congress thus reconfirmed, the president came underincreasing pressure from some of his supporters to stand for a second term in1998. However, this would have required a revision of the 1987 constitution (seeConstitution and institutions), and was strongly opposed by the CatholicChurch, opposition politicians and some prominent members of the businesscommunity, all of whom were alive to the dangers of another president abusingthe spirit of the constitution as Mr Marcos had done. The persistent speculationabout the president’s intentions (he had consistently stated that he planned tostep down in 1998) was finally put to rest when he endorsed Jose de Venecia, thesecretary-general of Lakas, as his nominee in November 1997.

Despite the inherent advantage of being the administration’s candidate, Mr deVenecia was beaten by a wide margin by the very popular vice-president andformer film star, Mr Estrada. Mr Estrada, who was backed by an alliance of thetwo opposition parties, the Nationalist People’s Coalition (NPC) and Laban(which had broken away from its pact with Lakas), won 40% of the votecompared with 16% for Mr de Venecia. The Lakas candidate for the vice-presidency, Gloria Macapagal Arroyo, won even more resoundingly, with 50%support. The coalition backing Mr Estrada won only around 60 of the 208directly elected seats in the House of Representatives, but as the party of thepresidential incumbent, renamed Laban ng Masang Pilipino (LAMP), it attractedenough defections from Lakas to build a majority in the lower house by the endof 1998.

The worst fears of a lurch towards populist policies were not borne out in thefirst 18 months of the Estrada administration as it maintained the macro-economic targets and liberalising stance of its predecessor (see Economic policy).But there have been adverse developments. Policy formulation andimplementation are often incoherent and unco-ordinated, as Mr Estrada’shands-off style gives scope for competition between members of his innercircle—including people with no formal responsibility in government.Cronyism has shown signs of revival (see box on page 8). Unease wascompounded by the president’s proposal that the constitution be amended,exclusively—he claimed—to change those clauses that restrict the scope forforeign investment. There was a widespread suspicion that the president—or hisallies—would use the opportunity to change the political clauses that set termlimits on elective office. These factors, plus the inevitable disappointment afterthe very high expectations raised by an avowedly pro-poor president, caused asharp fall in the president’s popularity in the second half of 1999. Whereas hisapproval rating was 78% in June in one respected poll, by December this wasdown to 44%: those expressing dissatisfaction had risen from only 12% in Juneto 38% in December. In a bid to halt this slide, in January 2000 the presidentshelved his proposal to amend the constitution. To improve the consistency ofpolicy formulation, an Economic Coordinating Council was set up, headed byMr Estrada and including the governor of the Bangko Sentral ng Pilipinas (BSP,the central bank) and leading economic ministers and presidential advisers.

President Ramos stepsdown

The new president wins thepopular mandate

His position slips by late1999

8 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Cronyism: a spectre returns

The patronage system pervades the Philippine political, economic and socialstructure; a favour granted merits a favour in return. At a moderate level thiscan be a benign feature, preserving social stability. But in the recent past thePhilippines has experienced a very extreme case, in the form of the cronycapitalism exercised by the president, Ferdinand Marcos, over a period of morethan 20 years. Ownership and control of the economy were concentrated in thehands of the president’s family and a coterie of cronies. Government mono-polies were exercised by a few friends of the president. Subsidies andpreferential access to bank credit and government guarantees were extended tocompanies controlled by crony interests.

This structure was dismantled when Corazon Aquino took power in February1986, but the system was never eliminated and the Philippines retained itsplace high up in the international league table of corruption. But since JosephEstrada took office in July 1998 there have been clear signs that cronycapitalism is coming back—in complete opposition to the trend in a number ofother countries in the region.

A number of very wealthy individuals—some of them former Marcos cronies—are doing extremely well out of their financial backing for Mr Estrada’s campaignfor the presidency. Eduardo Cojuangco was allowed to exercise the voting rightsof shares sequestrated by the government and so regain control of the country’sleading food conglomerate, the San Miguel Corporation. He is now trying tosecure the title to assets acquired by a fund drawn from a levy on coconut farmersduring the Marcos administration. The tax authorities have effectively aban-doned a multibillion peso tax evasion suit against another prominent backer ofMr Estrada, Lucio Tan. Mr Tan’s attempts to restore the fortunes of PhilippineAirlines (PAL), of which he is the majority owner, are aided by the government’srevocation of its air agreement with Taiwan, whose airlines have been cuttinginto PAL’s market share. New cronies have also emerged. Mark Jimenez, abusinessman who fled the US after he was indicted on charges of making illegalcampaign contributions, tax evasion and fraud, has been acting as adviser toPresident Estrada while brokering very large business deals (out of which hereportedly did very well) and being “consulted” by a state pension fund.

As early as July 1999 a survey of 104 leading business executives citedcorruption and influence peddling as the most negative feature of the Estradaadministration. The situation has deteriorated since.

In September-October 1999 Mr Tan acquired the government’s share option ina leading commercial bank, Philippine National Bank (PNB), giving him a near-50% stake, which put him in pole position to acquire the residual governmentstake that is due to be sold off in April 2000. Both the World Bank, which haslinked the release of funding for structural banking reform to the privatisationof PNB, and the IMF have demanded transparency in the disposal process. Thejustice minister who insisted on pursuing the tax suit against Mr Tan andrecommended meeting the US request for Mr Jimenez’s extradition wasremoved in the cabinet change in January 2000. Most damaging of all,President Estrada has intervened in a recent investigation by the US Securities

Philippines 9

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

& Exchange Commission (SEC) of alleged insider trading and sharemanipulation by another close friend and campaign financier, Dante Tan.According to the head of the SEC, the president contacted him on fouroccasions urging him to clear Mr Tan. This episode sends out extremelynegative signals to potential investors, domestic and foreign, when thePhilippines is lagging behind the recovery in other economies in the region.

Political forces

Political parties in the Philippines are based on personalities rather thanideologies. All those represented in Congress support the existing political andsocial structures, espouse a market economy (until it threatens sectoralinterests), and are nationalistic, to varying degrees. There are thus constantshifts of allegiance. The president tends to attract a greater following inCongress than the election results would indicate, at least in the early years ofthe term. In the final years of a presidential term of office the parties tend tosplinter as presidential hopefuls emerge and the president has only limitedpatronage to offer.

As of mid-2000 there was one dominant, pro-administration party in Congress(based on two established parties) and the remnants of older parties, includingthe pro-administration party under the previous presidency.

Laban ng Masang Pilipino (LAMP) is the pro-administration coalitionformally created in August 1998 out of the parties which backed Mr Estrada’scandidacy. LAMP candidates won 60 seats in the election, but its membership inthe lower house had reached a reported 195 by the end of 1998. As of early 2000its following there was put at around 170, while in the Senate (where partylabels are of little significance) LAMP had 12 supporters and no cohesiveopposition. The two parties that form the core of LAMP are the following.

The Nationalist People’s Coalition (NPC), originally formed to support thepresidential candidacy of Mr Cojuangco in 1992. The NPC initially teamed upwith Lakas in support of President Ramos, but became the official oppositionafter Laban agreed an electoral pact with the pro-administration party, Lakas,in 1994. It backed Mr Estrada’s presidential candidacy and its former leader inthe lower house, Ronaldo Zamora, was given the key post of executivesecretary in the new administration.

Laban ng Demokratikong Pilipino (Laban), formed in 1988 to back theAquino presidency. After the 1992 elections its position as the largest party inthe House of Representatives soon collapsed owing to defections to the newadministration party, Lakas. The May 1995 poll left it with only 27 members inthe lower house, while its majority in the Senate split into pro-government andopposition blocs. In December 1997 the party gave its support to Mr Estradaafter its leader, Edgardo Angara, abandoned his own presidential ambitions torun as the vice-presidential candidate of the opposition. Mr Angara did verybadly, and Laban did not recover ground in the lower house. It has nowvirtually lost its separate identity in LAMP.

10 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Now the opposition, Lakas ng Edsa-National Union of ChristianDemocrats (Lakas) was formed in 1992 to support the candidacy ofMr Ramos. Its strength in the House of Representatives rose from 50 membersin the May 1992 congressional elections to a peak of 155 by late 1997. Itsfollowing in the House eroded very rapidly after the May 1998 elections, fallingfrom 112 members following the vote to fewer than 20 by the end of the year.In the Senate, where it had always been in a minority, its representation in late1999 was down to three.

Outside the mainstream of congressional politics are political forces for whichideology is the determining factor.

The National Democratic Front (NDF) is the umbrella organisation for theMaoist Communist Party and its military wing, the New People’s Army(NPA). The Philippines has a long tradition of rural rebellion, and the NPA,founded in 1969, took up the fight waged by the Hukbalahap rebel movementin Luzon in the mid-1950s. The NPA expanded rapidly under martial law, thenumber of its regulars rising to an estimated 25,000 by mid-1985. It was thenthought to control one-fifth of the country’s villages and to be active in 60 ofthe 75 provinces, as well as in the Manila region. Its attachment to the Maoistdogma that revolution must come from the countryside meant that it playedno role, as an organisation, in the overthrow of Mr Marcos. The post-Marcosregimes eroded its popular base by offering amnesties, legalisation of theCommunist party (in late 1992), and land and jobs to surrendered rebels, whilemaintaining an active military campaign. In mid-1999 its numbers wereestimated at some 8,000. The movement is now riven by disputes on strategyand tactics, but its roots are likely to remain strong as long as income and landdistribution are so grossly uneven.

Another, more heavily armed but less cohesive, rebel movement is the Muslimsecessionist rebellion in Mindanao. The main group is the Moro NationalLiberation Front (MNLF), which was estimated by military sources to have17,000 active members in late 1995. Vying with it for primacy is the MoroIslamic Liberation Front (MILF), which has a religious appeal and isthought to have a smaller following (of 6,000-10,000), more widely dispersedthroughout the region. Unlike the NPA, the Muslim rebels have receivedsupport from foreign sources. The secessionist movement has a historystretching back several centuries. There is no easy solution since immigrationfrom Luzon and the Visayas in the 1950s and 1960s has created a Christianmajority—or near parity—in a number of Mindanao’s provinces. Thus a pro-posal to grant regional autonomy to Mindanao found favour in a referendumin 1989 in only four of the 13 provinces.

One of the major achievements of the Ramos administration was the peacesettlement agreed with the MNLF in September 1996. It provides for atransition to an autonomous entity within an integral Philippines, setting upan administrative body, the Southern Philippines Council for Peace andDevelopment (SPCPD), covering the whole of Mindanao and advised by a con-sultative assembly of local officials and representatives of non-governmentalorganisations. After the SPCPD had operated for three years (until September1999), the whole region was due to vote on whether the council should

Philippines 11

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

become its autonomous government. This poll has been postponed, at theurging of the MNLF leader, governor of the four autonomous provinces andhead of the SPCPD, Nur Misuari, because peace has not yet delivered the eco-nomic benefits that might induce the other provinces to opt for autonomyunder his aegis. The situation is complicated, moreover, by the refusal of theMILF to recognise the validity of the 1996 peace settlement and its continuingdemand for an independent Islamic state. Technical-level discussions betweenthe government and the MILF started in late 1998 against the background of ade facto, though frequently breached, ceasefire. This ceasefire seemed to havebroken down definitively in April 2000 after government forces sought toremove MILF checkpoints on a stretch of highway leading to the rebels’ mainbase at Camp Abubakar in Maguindanao. The MILF called off the negotiationsthat were due to resume in mid-May. The situation was complicated by asimultaneous upsurge in activity by a much smaller, more extremist, group,Abu Sayyaf, involving two sets of kidnappings: one of a group from a localschool and the other of foreign tourists from a Malaysian resort, whose purposeseems to be to win both publicity and ransom money.

Another important political force is that represented by the Catholic Church. Itplayed an active part in the civilian opposition to the Marcos regime andhelped the military rebellion to victory by bringing the population out on tothe streets of Manila in its support. Although it was compromised when itshead in the Philippines, Cardinal Jaime Sin, overtly supported an unsuccessfulcandidate in the 1992 presidential election, the Catholic Church was asignificant force in opposition to any extension of President Ramos’s term inoffice. It avoided endorsing any specific candidate in 1998, although itsdistaste for Mr Estrada was evident, and it took the lead in opposition to hisproposal for constitutional change.

Main political figures

Joseph Estrada: President, elected in May 1998 for a six-year term, withstrong popular backing that was sharply eroded over the second half of 1999.

Gloria Macapagal Arroyo: Vice-president, elected with more than 50% ofthe vote as the candidate of the previous administration. Appointed to thesecond-rank portfolio of social welfare, she has maintained a studiously loyalstance, while tacitly distancing herself from the defects of the Estrada regime.She is seen to have strong potential in the next presidential election.

Ronaldo Zamora: Executive secretary to the president, former head of theNationalist People’s Coalition (NPC) in the House of Representatives andbrother of the president’s campaign manager in 1998. One of the main playersin an administration marked by a lack of presidential direction. Member of theEconomic Coordinating Council (ECC).

Rafael Buenaventura: Governor of the Bangko Sentral ng Pilipinas (BSP, thecentral bank), who has assumed a high-profile role in economic policy sincetaking up the post in July 1999. He clashed with the finance minister of thetime, Edgardo Espiritu, on interest rate policy. Member of the ECC.

12 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Jose Pardo: Former trade minister, who replaced Mr Espiritu in a cabinetreshuffle in January 2000, and is thought to be closer in thinking to the centralbank governor. Now ex officio deputy head of the ECC.

Edgardo Angara: Unsuccessful running mate to Mr Estrada and former headof Laban, with a strong background in economic policy formulation. Aftercompleting one year out of governmental office, in May 1999 he wasappointed agricultural secretary. Member of the ECC.

Eduardo Cojuangco: Extremely wealthy former crony of Ferdinand Marcos,founder of the NPC as his vehicle for a presidential bid in 1992 and a criticallyimportant political and financial backer of Mr Estrada’s presidential campaignin 1998.

Lucio Tan: Another former Marcos crony and Estrada campaign backer, whohas seen a tax evasion case effectively abandoned and his corporate interestsflourish under the present administration.

Cardinal Jaime Sin: Head of the Catholic Church in the Philippines. Caninfluence, but not direct, the vote of the 85% of the population who areCatholic.

Organised labour has little power. Only around one in five workers was in atrade union in the late 1990s, although the rate is significantly higher in multi-national firms, where around one in three was unionised. A tiny proportion(only 4% of the 11.8m salaried workers in the mid-1990s) has collectivebargaining agreements. This reflects the weak bargaining position of workers ina labour surplus economy.

Constitution and institutions

The constitution introduced in 1987 provides for a single six-year presidentialterm. The president is chief executive, head of state and commander-in-chief.The legislature is bicameral, with a Senate of 24 members elected “at large” (ona nationwide ballot) and a House of Representatives composed of 208 membersdirectly elected by district and up to 52 members chosen by party list. Senatorshave six-year terms and representatives three-year terms. The president mayimpose martial law for no longer than 60 days, and the decree proclaiming itcan be revoked by Congress. The president may not abolish Congress and hisveto can be overridden by a two-thirds majority in the legislature. Thejudiciary, which is independent of the executive, rules on the constitutionalityof presidential decrees. A permanent, independent commission oversees com-pliance with a bill of rights contained in the constitution.

The president selects the members of the cabinet but, in line with the separationof powers, they must be outside Congress. All cabinet appointments require con-gressional approval, but, once approved, the incumbent can be removed only bythe president. Areas of policy that straddle departmental responsibility tend to betreated in cabinet committee; privatisation and infrastructure projects areleading examples. This does not, however, eliminate interdepartmental conflictsof interest, such as that between the Department of Finance and the Department

Philippines 13

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

of Trade and Industry on the issue of tax incentives for investment or thatbetween the environment and energy departments on the siting of power plants.The National Economic Development Authority (NEDA), headed ex officio by theplanning secretary, is intended to co-ordinate policy and decisions in all areasrelevant to the economic development plan. The planning secretary also sits onthe Economic Coordinating Council (ECC), set up in January 2000, withresponsibility in “urgent matters relating to the country’s economic recovery”and power to overrule decisions in any other government agency.

Traditionally, government in the Philippines has been highly centralised.However, the 1987 constitution made provision for the establishment ofautonomous regions in two areas with distinctive historical and culturalheritages—the Cordillera region of northern Luzon and Mindanao—if the localpopulation voted by referendum for this status. Both autonomous regions havenow been established, although the autonomous region in Mindanao islimited to the four, out of 13, provinces that voted for it. The autonomousauthorities have powers in the areas of personal and property relations,regional and urban planning, education, and economic and social develop-ment. The Local Government Code of 1991 also devolved some fiscal powers,in the form of the oversight and control of government spending, to localgovernments.

International relations and defence

A continuing foreign policy priority has been the strengthening of relationswith fellow members of the Association of South-East Asian Nations (ASEAN).Membership of this organisation gives the Philippines an Asia-Pacific identityindependent of the US umbrella.

Another priority for the Philippine government is participation in a regionalforce to counterbalance China, which is seen as a threat, most recently in thedispute over the Spratly Islands in the South China Sea. Relations with the USadministration retain a special character and significance, even as thePhilippines seeks to diversify its relations, notably with Europe.

The US has retained a special relationship, both political and economic, withthe Philippines since independence. The US administration has on a numberof occasions played a pivotal role in domestic political affairs in recent years,inducing Mr Marcos to leave the country in February 1986 and backing theAquino administration against coup attempts (on one occasion with militaryaircraft). The Philippines was home to two of the US’s most important militarybases outside US territory, the naval facility at Subic Bay and the nearby airbase at Clark Field. The non-renewal of the lease on the military bases when itexpired in 1991 was the most open sign of the Philippines’ emerging “Asian”identity. Nevertheless, the US remains a leading source of private investment inthe Philippines, reflecting links forged during the colonial period and the earlydecades of independence; it has by far the largest Filipino community outsidethe Philippines; and its culture remains dominant. A special militaryrelationship remains in place by virtue of the Mutual Defence Treaty, under

Relations with the US

14 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

which the US administration pledges to defend the territorial integrity of thePhilippines; and military equipment is almost wholly of US origin, althoughthis may change.

Although the support of the military was one of the pillars of the Marcosregime, and its discontent helped to foster serious instability under hissuccessor, the defence forces have traditionally accounted for a small share ofgovernment budget spending. Their numbers are fairly small compared withthose of other countries in the region. Their equipment is outdated andinappropriate to the country’s real needs. In 1995 the Ramos administrationinitiated a programme of modernisation and re-equipment, shifting the focusof the security forces from counter-insurgency—which has tended to be a low-technology, high-manpower activity—to external defence. The first five yearsof the P332bn (US$12.9bn at the 1995 exchange rate of P25.71:US$1) 15-yearprogramme envisaged buying a fighter squadron, naval patrol boats and anindependent nationwide radar system, and reducing military personnel fromaround 110,000 to 100,000. However, the depreciation of the peso since mid-1997 has raised the local cost of a programme initially expected to absorbP50bn in its first five years, and the deterioration in the fiscal balance in 1998has brought both the targets and the schedule into question. As of late 1999only P9.1bn had been allocated to this programme.

Armed forces and paramilitary, 1999

Armed forces 110,000 Army 73,000 Navy (incl 8,500 marines) 20,500 Air force 16,500

Paramilitary 104,000 Philippine National Police (PNP) 40,500 Coast guard 3,500 Civil Armed Force Geographical Units (CAFGU): part-time units 60,000

Source: International Institute for Strategic Studies, The Military Balance, 1999/2000.

Resources and infrastructure

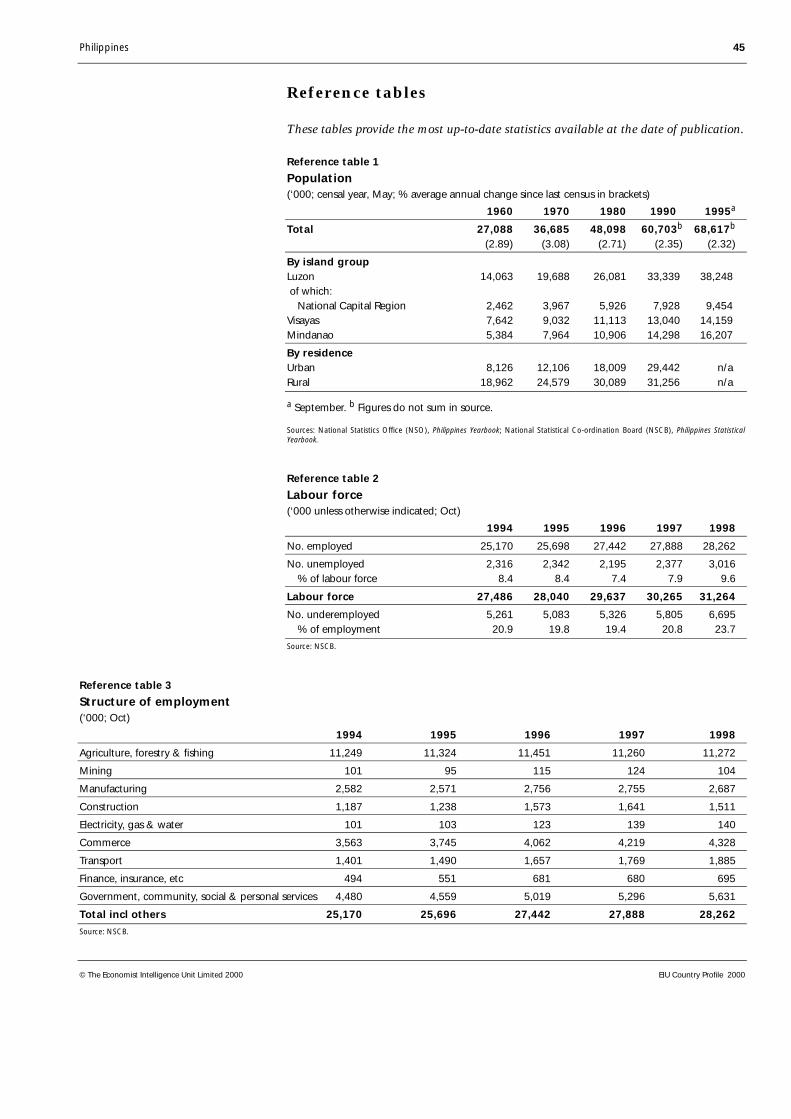

Population

The rate of population growth has been slowing in recent decades (accordingto national sources), from an average of 3.08% in the 1970s to 2.35% in the1980s and just over 2% by the end of the 1990s (see Reference table 1 forpopulation data). This reflects two trends: a fall in the birth rate and a fall inthe death rate as infant mortality rates have declined. Thus the crude birth ratefell from 46 per 1,000 in 1960 to 32 in 1992, as family planning became morewidely accepted. The government gave its backing to birth control, and thepercentage of married women of reproductive age practising contraceptionrose, reaching 40% in 1988-93. Meanwhile, life expectancy at birth rose from53 years in 1960 to 66 years in 1995 as the infant mortality rate fell from 72deaths in the first year of life per 1,000 live births in 1965 to 40 in 1992. The

Philippines 15

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

comparatively high rate of population growth means that the Philippines has ayoung population, 51% being under the age of 20 in 1990.

Population density is high in metropolitan Manila and neighbouring areas ofcentral Luzon, whereas Mindanao, Negros and the other southern islands aresparsely populated. There have been two significant trends in populationmovement in the past 30 years. First, the proportion of the population livingin rural areas has decreased, from 70% in 1960 to 56% in 1992, while theurban population has grown by just under 4% per year on average during theperiod. The second trend is the migration to the agricultural frontier areas inMindanao, despite the unrest in that region. Competition from migrants forland has significantly contributed to the unrest.

Population by region

Annual average1995 % change

(‘000) 1990-95

LuzonNational Capital Region 9,454 3.52Cordillera Administrative Region 1,255 –2.00Ilocos 3,804 1.38Cagayan Valley 2,536 1.60Central Luzon 6,933 2.24South Tagalog 9,941 3.69Bicol 4,325 2.02

VisayasWestern Visayas 5,777 1.38Central Visayas 5,015 1.76Eastern Visayas 3,367 1.94

MindanaoWestern Mindanao 2,795 2.55Northern Mindanao 2,483 2.45Southern Mindanao 4,604 2.78Central Mindanao 2,360 3.28Autonomous Region of Muslim Mindanao 2,021 1.91Caraga 1,942 1.92

Total 68,612 2.32

Source: Census reports.

There has also been significant migration out of the country—both permanentand temporary (in the form of overseas employment under contract), whichhas held down both the population resident in the Philippines and the rate ofunemployment (see Reference tables 2 and 3 for data on employment). Thismovement has been made feasible by the population’s familiarity with Englishand the comparatively high standard of education. Registered emigration hasbeen running at around 63,000 per year since 1990, with the US by far theleading destination, accounting for around two-thirds of the number. Overseasemployment represents an important outlet for the excess labour force and is amajor source of income for Philippine households. The number of contractworkers deployed each year fluctuates with conditions in host countries, butthe annual average was some 644,000 in the decade of 1989-98, or ten timesthe number emigrating each year. The great majority of placements (74% of

16 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

the total of 755,684 in 1998) are for land-based employment. The Middle Eastwas traditionally the leading destination by a wide margin, with openings inboth construction work and private services. From the beginning of the 1990s,however, Asia grew in significance as a destination, and in 1997 it briefly edgedahead of the Middle East, with 42% of land-based placements compared with39.5%. The contraction in regional economies brought Asia’s share back tosecond place in 1998.

Health

Overall healthcare provision is inadequate for the needs of the country, andWorld Bank data indicate a deterioration since the mid-1980s in terms of thenumbers of doctors and nurses per 10,000 of the population (to 1.5 and 3.6respectively in 1989-90). To some extent, as in the case of education, thisreflects budgetary constraints. Spending on public health in the Philippinesaveraged only 1.3% of GDP in 1990-95, a smaller proportion than in most othercountries in the region. But the situation is worsened by the skewed distributionof health facilities throughout the country. About half of all doctors are in theNational Capital Region (NCR), where each health centre covers an average of14,200 people, compared with 21,000-44,000 in other regions. Moreover, thepoor road infrastructure in the rural areas of the poorer provinces limits theaccess of large numbers of the population to such facilities as exist.

Education

Education standards are fairly high. Of the population aged over 15, 90% areliterate. In 1990 some 99% of children of the relevant age were enrolled inprimary and 73% in secondary schools. There is a fairly high level of tertiaryeducation: 27% of the relevant group were enrolled in 1990.

However, the situation is not as good as these figures indicate. About one-fifthof the adult population is thought to be functionally illiterate (they cannot reador write with any fluency) because, although there has been universal enrol-ment at the primary level for over two decades now, nearly one-third of primaryschool pupils do not complete their education. This national figure alsoconceals the familiar disparity between Manila and the poorer provinces: in theformer nearly 100% complete their primary education, in the latter only around30% do so. This reflects factors including general underinvestment in educationas this sector has fallen victim to the squeeze on government spending. Inaddition, the state’s percentage contribution to primary education costs hasfallen in recent years whereas its contribution to tertiary education has risen.

Natural resources and the environment

The Philippines is one of the largest island groups in the world, numberingmore than 7,100 islands and extending 1,851 km north to south and 1,107 kmeast to west. The topography is very varied and includes two mountain rangesin Luzon and several volcanoes, 21 of them active, throughout the country.

Philippines 17

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

The climate is tropical, with some variation in the extent and duration of thedry season. In the western parts of Luzon, Mindoro, Negros and Palawan (thewestern rim) there are two pronounced seasons: dry from November to Apriland wet for the rest of the year. Other regions have rainfall more or less evenlydistributed throughout the year. All are exposed to typhoons, which occurmost frequently across the middle latitudes of the country. Southern Mindanaois almost typhoon-free.

The area under crops expanded markedly in the 1970s and reached 12.25m hain 1979/80, mainly as a result of the clearing of virgin forest, particularly inMindanao, which has more than half the commercial acreage. Since 1979/80the area under crops has stabilised at about 13m ha and land availability isnow a serious constraint in Luzon and some parts of the Visayas.

Forests were in the past one of the Philippines’ main resources. An area of some15.88m ha was classified as forest land in 1996, of which around half was inproductive use. But these forest resources have been rapidly depleted, mainlyowing to shifting cultivation, illegal cutting and inadequate reforestation. The1987-92 and 1993-98 development plans had a reforestation target of100,000 ha per year, but the rate averaged only 70,800 ha per year, whereas thetarget should in fact be 120,000 ha per year merely to balance deforestation.Only 5.5m ha was forested in 1998, with just 700,000 ha virgin forest. There isa real possibility that forests could be virtually eliminated before the end of thisdecade. Logging in virgin forest has been banned since 1991 (although suchprohibitions are notoriously difficult to enforce) and the number of timberlicences had been cut to 30 by the beginning of 1996, down from around 100in the early 1990s.

The country has extensive fishing resources, both marine and inland, with thelargest area of developed estuarine fishponds in South-east Asia and anexclusive fishing zone of 1.89m sq km. While neither freshwater fishponds normost of the marine waters have been fully developed, the productivity of someresources has been deteriorating as rising demand and the use of destructivemethods of exploitation have resulted in overfishing.

Mineral resources are widely scattered throughout the islands, but around one-quarter of the land area has not been surveyed. At the end of 1996 there wereestimated reserves of copper of 4.79m tonnes, nickel of 1.09m tonnes,chromite of 36,667 tonnes, gold of 226,852 tonnes and iron of 484,696 tonnes.The picture is mixed for energy resources. There are large deposits of coal andlignite, with proven reserves of 369m tonnes, of which close to 40% are onSemirara Island, and potential reserves estimated at 1.59bn tonnes. Commer-cial deposits of oil off Palawan Island are very small (estimated at 16.3m barrelsin 1985) and have proved technically difficult to exploit and operate. Reservesof gas in the same region are substantial, estimated at 2.8trn-3.5trn cu ft (othergas reserves are estimated at 1.82trn cu ft). The offshore deposits are to bedeveloped to fuel three power plants with a total installed capacity of 2,700mw and possibly also to serve as the basis for petrochemicals industries.Geothermal resources are large and not yet fully developed.

18 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

Transport and communications

The transport and communications infrastructure is inadequate for thecountry’s requirements, having suffered decades of underinvestment. Now,however, in the liberalised investment environment, some of the most seriousshortcomings are being or are due to be tackled.

The transport system is essentially bimodal, roads carrying 60% of freight and80% of passenger traffic, and water 40% of freight and 10% of passenger traffic.Air transport is oriented towards carrying passengers on long-distance inter-island travel. The rail network (see below) is limited. (See Reference table 4 fortransport statistics.)

The road network covers some 161,000 km. More than 26,000 km of roads areclassified as national and more than 28,000 km as provincial (mainlysecondary roads); the rest are feeder and village roads. Although average roaddensity is comparatively high, at 2.35 km per 1,000 people, there is a very widedisparity between regions, the NCR having the highest density and parts ofMindanao the lowest. Moreover, less than half the network is all-weather, avery important consideration in view of the country’s climate, and only 17% ofall roads are paved with concrete or asphalt. The condition of the feeder roadsis generally very poor, the result of substandard construction, inadequatemaintenance and use by overloaded vehicles. Bridges are often weak, if notaltogether absent, and some remote areas have very few access roads. Currentprojects provide for the improvement of roads in Luzon, including the con-struction of an elevated expressway in Manila and the rehabilitation andmodernisation of the North Luzon highway and its extension to the SubicSpecial Economic Zone. Both are under build-operate-transfer (BOT) terms,bringing in private capital and expertise.

The railway system is limited to 740 km of single-line track in the Bicol-Manila-La Union corridor in Luzon. It is in urgent need of rehabilitation, since onlyone-fifth of the track is in operation. In addition, there is a modern, elevatedrail system in Manila, which is currently being expanded within the metro-politan area. In 1997 this system registered 134m passenger journeys.

Given the country’s geography, shipping services and port facilities are ofcritical importance. In all there are more than 400 ports in operation, but six—Manila, Cebu, Iloilo, Cagayan de Oro, Zamboanga and Davao—handle over80% of public port traffic. The inter-island fleet is old, safety regulations arepoor and maritime navigational aids, in particular lighthouses, are inadequate.However, more operators have entered the port and shipping sector as a resultof liberalisation by the Ramos administration, and the domestic fleet has grownrapidly, generating a 30% rise in passenger traffic between 1992 and 1995.

There are 89 national airports, of which three—Manila, Cebu and GeneralSantos—are international. The provision of domestic services has beenimproving as the aviation sector has been liberalised. One result has been thatthe privatised national carrier, Philippine Airlines (PAL), has started to operatein competition with new airlines. However, a financial crisis at PAL resulted in

Transport

Philippines 19

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

a sharp cutback in services (both domestic and international) in mid-1998, andthe airline’s future remained problematic at the beginning of 2000.

The telecommunications system used to be inadequate and unreliable, andtelephone density was only 1.02 per 100 persons in the mid-1980s. Thederegulation of the sector in 1993 has transformed the situation. Presidentialdecrees mandated interconnections between networks and required that inter-national gateway operators and cellular telephone companies install telephonesystems in urban and rural areas. The changes ended the monopoly enjoyed bythe Philippines Long Distance Telephone Company (PLDT).

Telephone density had risen to 4.09 per 100 of the population in 1996, asPLDT implemented a programme to install 1m lines by the end of the year andother operators entered the field. Some 4.8m telephone lines were due to beinstalled in 1995-2000, of which PLDT would provide about 2.42m, to bringtelephone density to 7-8 per 100. In fact, this density was achieved by 1997.

Under the Marcos regime the mass media, with the exception of a few small-circulation and often short-lived newspapers, were controlled by interests closeto the president, and press censorship was exercised by the government. Nowthat the sector has opened up again, there is a multiplicity of newspapers andthe Philippines press is a byword for freewheeling comment and speculation.This has not been to President Joseph Estrada’s taste, and in 1999 there weresigns of some attempt to intimidate the press, for example by an orchestratedadvertising boycott of one daily newspaper.

There are some 270 broadcasting radio stations, commercial and non-commercial. There are five main television networks, 19 carrier and sevenrelay stations.

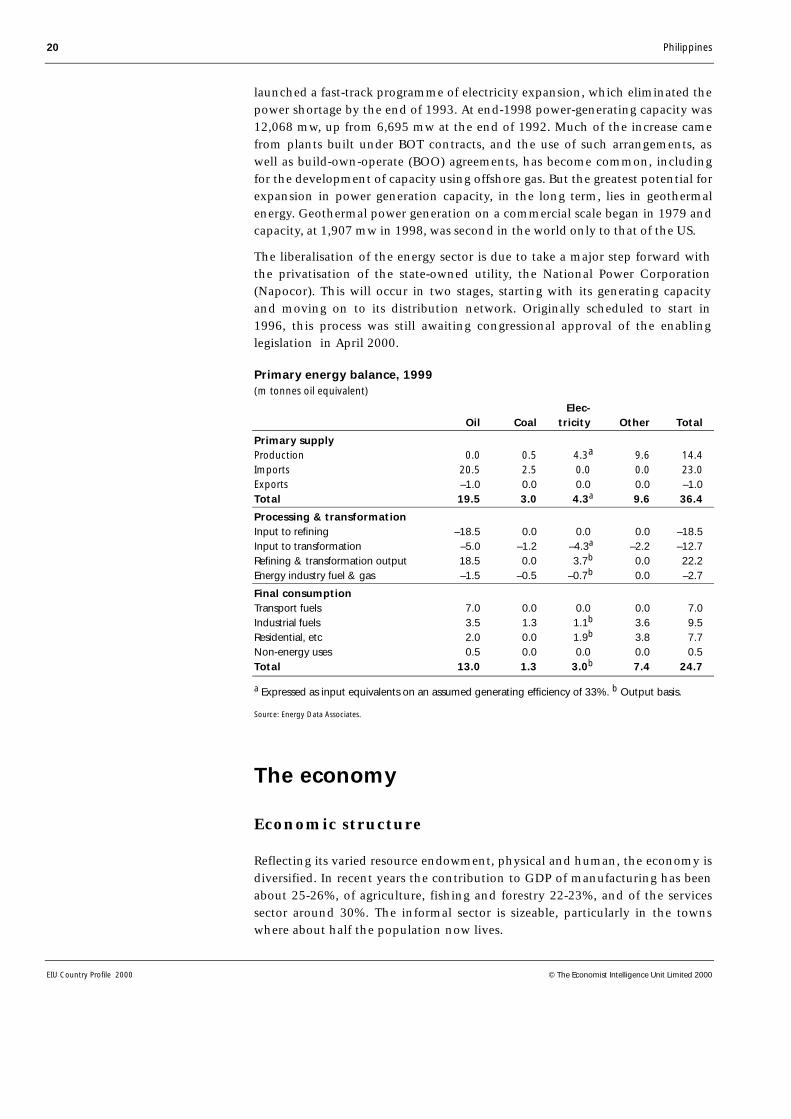

Energy provision

The Philippines depends to a fairly high degree on foreign energy, but since theoil price rises of the 1970s the government has sought to bring down the deficitin national supply. (Reference table 5 gives statistics on energy consumption bysource.) The contribution of domestic energy sources has been rising—reflectinginvestment in geothermal and hydroelectric capacity and the availability of awider range of non-conventional sources—and covered 41% of consumption in1998, but imported oil still accounted for the largest share, at 54%.

The contribution of indigenous commercial sources is due to rise markedlyonce gas production from the Malampaya reserves, offshore of Palawan, comeson stream as from October 2001 and as geothermal output rises. Domestic oil isnot at present expected to make a significant contribution, and coal will needto be supplemented by imports.

Power generation was previously a state preserve but severe shortcomings ininfrastructure have been remedied by bringing in the private sector. When FidelRamos became president in May 1992 the Luzon grid (on which Maniladepends) had a supply deficit of 1,000 mw. This was because a plan for 620 mwin nuclear capacity to come on stream in 1986 had lapsed. The new government

Communications

Energy generationand usage

20 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

launched a fast-track programme of electricity expansion, which eliminated thepower shortage by the end of 1993. At end-1998 power-generating capacity was12,068 mw, up from 6,695 mw at the end of 1992. Much of the increase camefrom plants built under BOT contracts, and the use of such arrangements, aswell as build-own-operate (BOO) agreements, has become common, includingfor the development of capacity using offshore gas. But the greatest potential forexpansion in power generation capacity, in the long term, lies in geothermalenergy. Geothermal power generation on a commercial scale began in 1979 andcapacity, at 1,907 mw in 1998, was second in the world only to that of the US.

The liberalisation of the energy sector is due to take a major step forward withthe privatisation of the state-owned utility, the National Power Corporation(Napocor). This will occur in two stages, starting with its generating capacityand moving on to its distribution network. Originally scheduled to start in1996, this process was still awaiting congressional approval of the enablinglegislation in April 2000.

Primary energy balance, 1999(m tonnes oil equivalent)

Elec- Oil Coal tricity Other Total

Primary supplyProduction 0.0 0.5 4.3a 9.6 14.4Imports 20.5 2.5 0.0 0.0 23.0Exports –1.0 0.0 0.0 0.0 –1.0Total 19.5 3.0 4.3a 9.6 36.4

Processing & transformationInput to refining –18.5 0.0 0.0 0.0 –18.5Input to transformation –5.0 –1.2 –4.3a –2.2 –12.7Refining & transformation output 18.5 0.0 3.7b 0.0 22.2Energy industry fuel & gas –1.5 –0.5 –0.7b 0.0 –2.7

Final consumptionTransport fuels 7.0 0.0 0.0 0.0 7.0Industrial fuels 3.5 1.3 1.1b 3.6 9.5Residential, etc 2.0 0.0 1.9b 3.8 7.7Non-energy uses 0.5 0.0 0.0 0.0 0.5Total 13.0 1.3 3.0b 7.4 24.7

a Expressed as input equivalents on an assumed generating efficiency of 33%. b Output basis.

Source: Energy Data Associates.

The economy

Economic structure

Reflecting its varied resource endowment, physical and human, the economy isdiversified. In recent years the contribution to GDP of manufacturing has beenabout 25-26%, of agriculture, fishing and forestry 22-23%, and of the servicessector around 30%. The informal sector is sizeable, particularly in the townswhere about half the population now lives.

Philippines 21

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

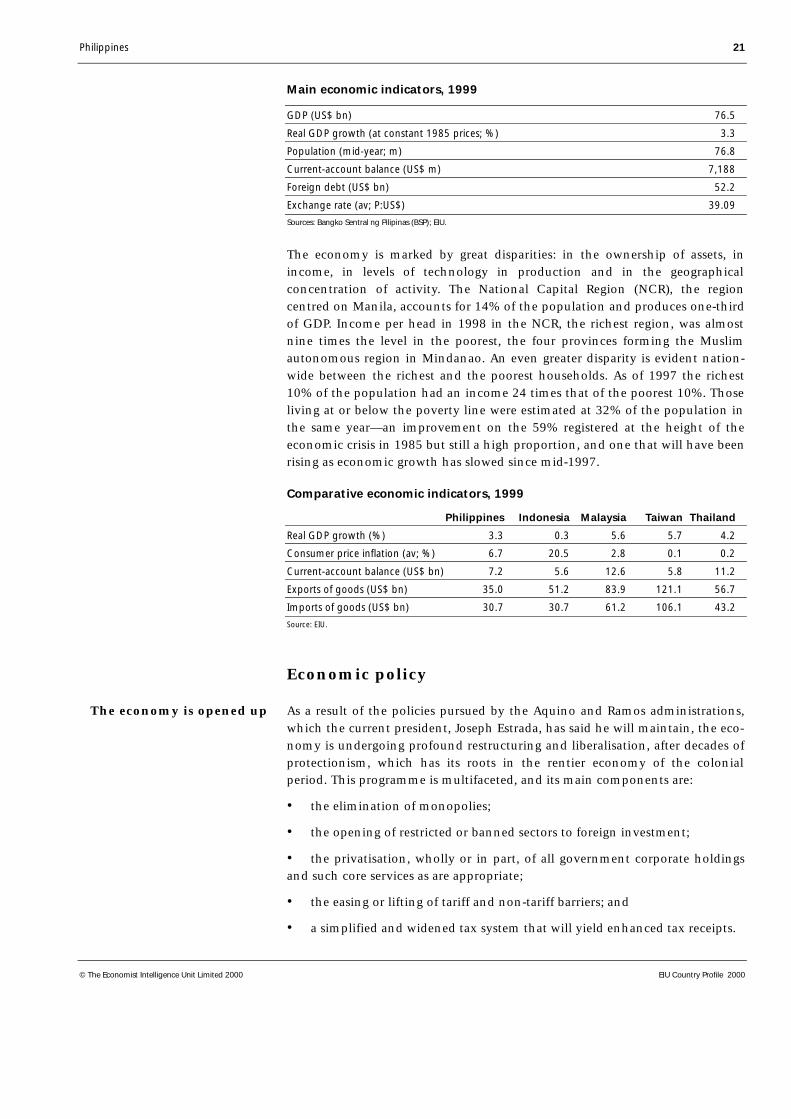

Main economic indicators, 1999

GDP (US$ bn) 76.5

Real GDP growth (at constant 1985 prices; %) 3.3

Population (mid-year; m) 76.8

Current-account balance (US$ m) 7,188

Foreign debt (US$ bn) 52.2

Exchange rate (av; P:US$) 39.09

Sources: Bangko Sentral ng Pilipinas (BSP); EIU.

The economy is marked by great disparities: in the ownership of assets, inincome, in levels of technology in production and in the geographicalconcentration of activity. The National Capital Region (NCR), the regioncentred on Manila, accounts for 14% of the population and produces one-thirdof GDP. Income per head in 1998 in the NCR, the richest region, was almostnine times the level in the poorest, the four provinces forming the Muslimautonomous region in Mindanao. An even greater disparity is evident nation-wide between the richest and the poorest households. As of 1997 the richest10% of the population had an income 24 times that of the poorest 10%. Thoseliving at or below the poverty line were estimated at 32% of the population inthe same year—an improvement on the 59% registered at the height of theeconomic crisis in 1985 but still a high proportion, and one that will have beenrising as economic growth has slowed since mid-1997.

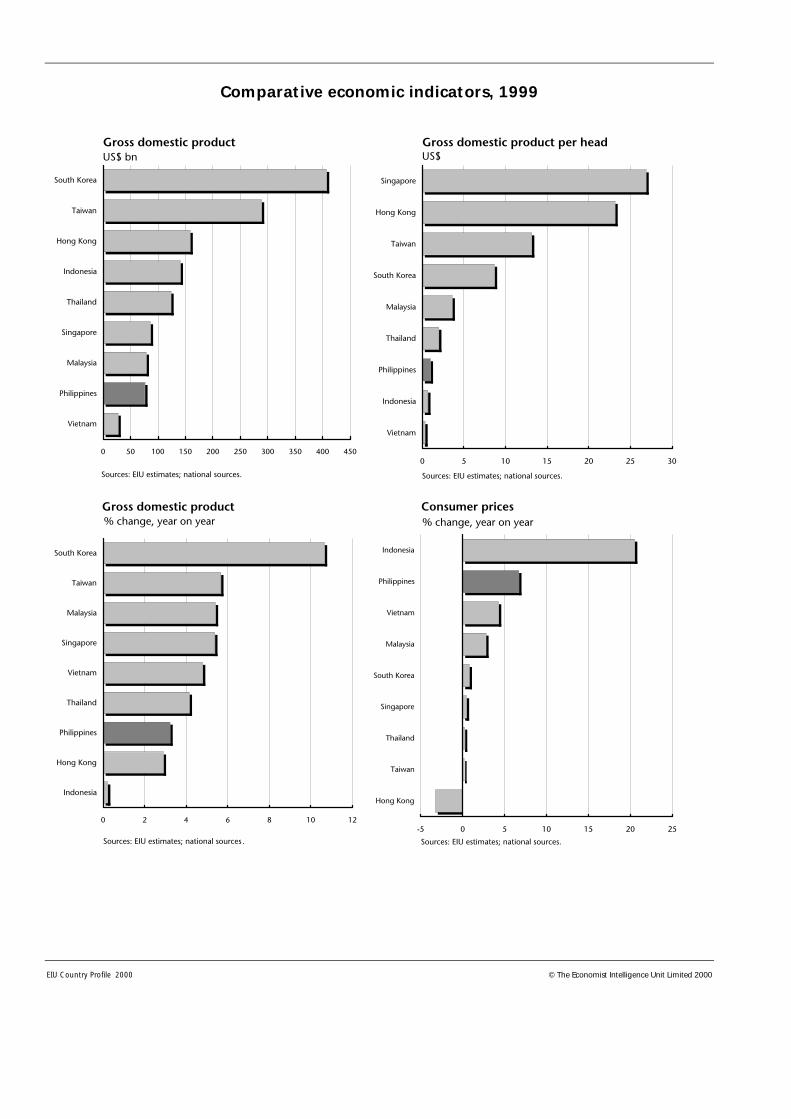

Comparative economic indicators, 1999

Philippines Indonesia Malaysia Taiwan Thailand

Real GDP growth (%) 3.3 0.3 5.6 5.7 4.2

Consumer price inflation (av; %) 6.7 20.5 2.8 0.1 0.2

Current-account balance (US$ bn) 7.2 5.6 12.6 5.8 11.2

Exports of goods (US$ bn) 35.0 51.2 83.9 121.1 56.7

Imports of goods (US$ bn) 30.7 30.7 61.2 106.1 43.2

Source: EIU.

Economic policy

As a result of the policies pursued by the Aquino and Ramos administrations,which the current president, Joseph Estrada, has said he will maintain, the eco-nomy is undergoing profound restructuring and liberalisation, after decades ofprotectionism, which has its roots in the rentier economy of the colonialperiod. This programme is multifaceted, and its main components are:

• the elimination of monopolies;

• the opening of restricted or banned sectors to foreign investment;

• the privatisation, wholly or in part, of all government corporate holdingsand such core services as are appropriate;

• the easing or lifting of tariff and non-tariff barriers; and

• a simplified and widened tax system that will yield enhanced tax receipts.

The economy is opened up

22 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

To varying degrees all these policies challenge entrenched interests, and somehave not been fully implemented because, in the existing political and eco-nomic climate, these interests find strong protection in Congress. Nevertheless,major structural reforms were introduced by the Aquino and Ramosadministrations (see box below) and despite some signs of backsliding by thepresent administration in the drive to eliminate monopolies, the agendaremains one of structural reform. As of early 2000 Congress had approved theopening of retail trade to foreign investment and was debating theprivatisation of the power utility, while the sale of the government’s residualequity in the Philippine National Bank was scheduled for April. (The date set isnow late May.) The president has deferred, but not abandoned, his proposal tolift the constitutional ban on foreign ownership of land and restrictions onforeign involvement in the media, education and utilities.

Landmarks in economic liberalisation

June 1989: Privatisation of 30% equity in the Philippine National Bank.

June 1991: Foreign Investment Act allows 100% foreign equity ownership except insectors where it is specifically restricted (to 25-40%) or banned.

August 1992: Lifting of the exchange controls on virtually all current-accounttransactions.

February 1993: Ending of telecommunications monopoly.

February-June 1994: Privatisation of 60% equity in state-owned oil refinery.

May 1994: Lifting of ban on entry of operating branches of foreign banks.

January 1995: Aviation services opened up. Extension of land-lease period forforeigners from 50 to 75 years.

February 1995: A total of 100% foreign equity allowed in mining under terms offinancial and technical agreements.

March 1996: Deletion of the negative list in the Foreign Investment Act relating tosectors where there is already adequate capacity to meet domestic demand.

January 1997: Privatisation of Manila water system through two 25-year franchises.

February 1997: Downstream Oil Industry Deregulation Law ends administered pricingof petroleum products.

February 1998: New oil deregulation law replaces previous law declaredunconstitutional by the Supreme Court in November 1997.

December 1999: Congress lifts the ban on foreign investment in retail trade.

Philippines 23

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

The underlying aim of the restructuring programme is to improve resourcemobilisation. One means of achieving this is the build-operate-transfer (BOT)type of contract, where the Philippines has been a ground-breaker. Thismechanism shifts the capital and management burden from the public to theprivate sector, and was initially employed to remedy the critical power shortagein Luzon in 1992-93. It has been extended to other forms of physicalinfrastructure (such as roads and commuter rail services) where gaps alreadyconstrain economic growth and the government’s budget resources areinsufficient.

The liberalisation programme made a significant contribution to achieving oneof the main macroeconomic targets—the elimination of the fiscal deficit. Theproceeds of the sale of government assets, both corporate and physical,enabled the budget to move into a P16.3bn (US$617m) surplus in 1994(equivalent to 1% of GDP) and remain in surplus through to 1997. A newfeature in 1996 was a small surplus before privatisation proceeds, which owedmuch to the fact that interest payments—the largest single expenditure item—had been eroded by the fall in the government’s debt stock. The public-sectordeficit (as opposed to the government’s budget balance) was nearly zero inboth 1994 and 1995, and there was even a small surplus in 1996.

At the same time, the Ramos administration, taking up the baton from theAquino presidency, made a concerted effort to strengthen the tax base. Value-added tax (VAT) was extended at the beginning of 1996, while a com-prehensive tax reform package, approved in two stages in 1996 and 1997,tackled a range of defects in the tax structure. It simplified the system ofpersonal and corporate tax, raising thresholds for the former and reducing therange of allowances in both, and rebased the excise system from ad valorem tospecific levy. The underlying aim was to reduce both the scope and theincentive for corruption and evasion, and thereby increase the tax take fromthe present inadequate 15-16% of GDP.

The financial crisis that hit the Asian region in 1997 had a immediate andsevere impact on the budget. The depreciation in the peso and the steep rise ininterest rates pushed up the cost of servicing the government’s debt, at thesame time as the downturn in economic growth hit the revenue side. The fiscalsurplus in 1997 was only around one-tenth the original target, at P1.56bn,while the slip into recession in mid-1998 ended all hope of maintainingequilibrium. The target deficit agreed with the IMF in February, under a newprecautionary stand-by agreement for US$1.37bn, had to be revised upwardstwice, with the final outturn just below the P50bn ceiling. As the economywent into recession (GDP fell year on year from the second quarter to thefourth quarter of 1998) the government adopted an expansionary budget for1999: spending was set to rise by 16% and revenue by 13%. This would haveproduced a deficit of P68.4bn. In the event the recovery in GDP growth in1999 was slower, and more fitful, than scheduled, with the result that internaltax receipts fell well below expectations. Despite some trimming on theexpenditure side, the deficit exceeded the target, at P111.7bn (latest estimate).(Reference table 6 provides data on government revenue and expenditure in

Fiscal targets were metby 1997

There was a sharpdeterioration in 1998-99

24 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

1994-98, and Reference table 7 gives figures for outstanding internal publicdebt in the same period.)

The higher than expected fiscal deficit in 1999 meant that the targets forsubsequent years have had to be revised. The six-year fiscal programme drawnup at the beginning of the Estrada administration had envisaged a rapidreduction in the fiscal deficit from P40bn in 1998 to P17.9bn in 1999,stabilising in 2000, and then replaced by a marginal surplus in 2001, of P7.4bn,with a sustained and strong improvement thereafter, to P75.6bn in 2004. Thedraft budget for 2000 drawn up in mid-1999 had projected a P40bn deficit. Therevised figure in December was P62.5bn. Even this will prove overoptimisticunless the deepening in the economic recovery in 2000 is accompanied byincreased effort on the tax collection front. The government’s target forprivatisation proceeds, at P22bn-30bn, looked in early 2000 to be too high,given rather bearish investor sentiment. Even if the 2000 target is met, there isno expectation of a return to fiscal surplus until late in the president’s term, andeven then only at modest levels.

Budget results for 1999 and government proposals for 2000(P bn)

2000 20001999 Original (Jul 1999) Revised (Dec 1999)

Revenue 478 551.8 518.6

Expenditure 585 591.8 581.1

Balance –112 –40.0 –62.5

Source: Press reports.

Whereas the Philippines had achieved its fiscal and other macroeconomictargets by 1997 (money growth was broadly in line with the agreed targets andinflation, with some blips, had moved down to an average of 6% in that year),the deterioration in the fiscal position and the Supreme Court ruling against oilderegulation (one of the core policy commitments agreed with the IMF) meantthat the Philippines did not make the hoped-for graduation from its IMF pro-gramme by the end of 1997. However, the prospect of a complete break withthe IMF had become less attractive as the regional financial crisis deepened.Consequently, a “precautionary stand-by arrangement” was negotiated inMarch 1998, to follow on from the extended funding facility that expired inthat month. The facility, for up to US$1.37bn, covered a two-year period andaccompanied a set of GNP growth targets, which had to be revised downwardslater in the year as the economy moved into recession. Inflation targets—7.5-8.5% for 1998 and 4-5% in 1999—were maintained, but proved ambitious. (SeeReference table 8 for money supply data for 1995-99 and Reference table 9 forinterest-rate data for 1995-99.) Against the background of the regional financialcrisis there was a renewed focus on reform and strengthening of the bankingsector, with four broad policy objectives and promises:

• increasing banks’ capitalisation and encouraging consolidation;

• tightening provisioning requirements and strengthening regulatoryoversight;

The planned return toequilibrium is postponed

IMF tutelage is maintained

Philippines 25

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

• dealing “expeditiously” with any problem bank while safeguarding thesoundness of the system; and

• levelling the playing field between different types of institutions andinstruments.

As of early 2000 the government had not revised its economic growth targetsin the Medium-Term Philippine Development Plan for 1999-2004. Drawn up atthe beginning of the Estrada presidency, this had modest expectations for GDPand GNP growth over the period, starting from a range of 2.6-3.2% and 3-3.7%respectively in 1999 to a peak of 6.1-6.6% and 6.6-7.1% in 2003. Theperformance in the first year was just under the low end of the target (seeEconomic performance) and the government has kept its target for 2000 at thelow end—while hoping for more.

Medium-Term Philippine Development Plan(target range for % annual growth)

1999 2000 2001 2002 2003 2004

Agriculture 3.0-3.5 3.5-4.1 0.5-1.5 3.5-4.3 4.0-4.6 1.0-2.0

Industry 1.4-2.0 5.0-5.6 4.8-5.4 6.0-6.6 6.8-7.5 6.6-7.2

Services 3.5-4.0 5.3-5.8 4.7-5.3 5.6-6.0 6.4-6.7 5.8-6.4

GDP 2.6-3.2 4.8-5.4 3.9-4.6 5.8-5.9 6.1-6.6 5.2-5.9

GNP 3.0-3.7 5.3-5.9 4.6-5.1 5.9-6.4 6.6-7.1 5.7-6.4

Note. The growth dips in 2001 and 2004 flow from the assumption of a recurrence of the El Niño climatic phenomenon.

Source: National Economic & Development Agency (NEDA) as reported in press.

Economic performance

Gross domestic product(% real change at constant 1985 prices)

Annual average1999 1995-99

Private consumption 2.6 3.9

Government consumption 5.3 3.5

Fixed capital formation –2.0 2.6

Exports of goods & services 3.6 4.4

Imports of goods & services –2.8 5.0

GDP 3.3 3.7

Source: National Statistical Co-ordination Board (NSCB).

Economic growth until 1998 was based on the buoyancy of exports and theinvestment this in turn stimulated. With an initial boost from the ending ofthe power shortfall in 1993, the rate of GDP growth was rising in every year toa peak of 5.8% in 1996, before a modest deterioration in 1997, to 5.2%, as theregional crisis hit. In each year exports were rising at double-digit rates (in bothnational accounts terms and on the US dollar-denominated merchandisemeasure), while the real growth in gross fixed investment reached 12-14% peryear in 1996 and 1997.

Medium-term growthtargets are maintained

Exports and investmenttwin pillars of growth

26 Philippines

EIU Country Profile 2000 © The Economist Intelligence Unit Limited 2000

The sharp fall in fixed capital formation in 1998, of 11.2%, owing to thecombination of a steep rise in interest rates and import costs since mid-1997and slackening domestic demand, brought economic growth to a halt. GDP fellby 0.6% while GNP was stagnant. The 21% contraction in exports (nationalaccounts measure) was also significant, as the percentage rise on this side of theforeign account exceeded the fall in imports (of 14.7%), which meant that thenet foreign balance improved slightly. Meanwhile, on the supply side, agricul-tural output fell sharply owing to drought damage to the rice and corn crops.

These demand trends were broadly maintained in 1999. Figures from theNational Statistical Coordination Board (NSCB) for 1999 published in May 2000showed a modest recovery in exports, with a further—if much slower—fall inimports. Capital formation also continued to contract though at a much slackerpace. The most dynamic demand component was government consumptionspending, which recorded its fastest growth in the first quarter (7.6% year onyear) and then slackened in each successive quarter, but still registered growth of5.3% for the full year. On the supply side, agriculture made up the ground lost in1998, while industry remained in the doldrums with only 0.9% growth. (ForGDP and GNP growth in 1995-99 see Reference tables 10, 11 and 12.)

One important factor in the rate of economic growth, which is not directlyregistered in the GDP measure, is the inflow of remittances from Filipinos over-seas, both contract workers and emigrants. The World Bank has estimated thatsuch remittances were in the range of 2.2-4.5% of GDP in 1991, and thepercentage has risen substantially since then (see The external sector). Trendsin these inflows consequently have an impact on the pace of overall economicgrowth, as they represent a significant source of income for Filipino house-holds and generate demand for Filipino assets.

The recovery in economic performance after 1991 was accompanied by asteadying in the rate of consumer price inflation. An important contributingfactor until mid-1997 was the stability of the peso against the US dollar, withthe annual average fluctuating within a narrow band, of 2-7%, in 1992-96 andin the first half of 1997. The steep fall in the peso’s value in the second half of1997 added to the pressure from a much lower rice crop to push up the rate ofinflation to 10-11% in May-December 1998.

But strong deflationary pressures began to be felt in early 1999, from the eco-nomic recession, the weakness in world oil prices and—as from October 1998—the slight appreciation in the peso’s value against the US dollar. With therebound in the rice crop in the second quarter of 1999, and despite the recoveryin oil prices, the rate of consumer price inflation was falling in virtually everymonth in 1999. By January 2000 it was down to a 13-year low of 2.6%.

Over most of the 1990s real wages have tended to decline. Wages tend to lagbehind the rise in prices, with sudden catch-up increases that owe most toessentially political pressures (such as a surge in food prices or an imminentnational election). The measure used is the minimum wage, which varies withthe type of work (agricultural or non-agricultural) and the region. It is an

Until 1998

Overseas remittances play asignificant role

An inflationary blipin 1998

A slowdown in 1999

Wages tend to lagprice inflation

Philippines 27

© The Economist Intelligence Unit Limited 2000 EIU Country Profile 2000

imperfect measure for a number of reasons. Many sectors are excluded from itsoperation—the whole of the public sector, as well as export-oriented andlabour-intensive manufacturing—and many companies ignore it because of thelimited bargaining power of organised labour. (See Reference table 13 for dataon consumer and wholesale prices and the minimum wage in 1995-99.)

Inflation and the minimum wage(% change, year on year)

Annual average1999 1995-99

Consumer prices 6.7 7.9

Minimum non-agricultural wage in National Capital Region (incl allowances) 6.4 6.2

Source: Bangko Sentral ng Pilipinas.

Regional trends

The figures for overall GDP of P2.99trn and for GDP per head of P38,919(US$996) in 1999 conceal a wide disparity in wealth between different regionsof the country. The NCR accounts for one-third of the economy’s output andits GDP per head is close to three times the national average. Only two otherregions—South Tagalog and Cordillera Administrative Region—have incomeper head that is above the national average, while four register around half thatfigure and the four autonomous provinces in Mindanao only one-third. Thisreflects the concentration of manufacturing activities in the Manila area.However, growth points have been developing in other regions, whereindustrial parks have been the focus for much investment, both domestic andforeign, in recent years.

Gross domestic product by region, 1998