philippine savings bank - psbank | home · philippine savings bank ... board or board of directors...

TRANSCRIPT

PHILIPPINE SAVINGS BANK (A banking corporation organized and existing under Philippine Laws)

P3,000,000,000 Unsecured Subordinated Notes Qualifying as Tier 2 Capital Due 2022

Callable in 2017 Issue Price 100%

Philippine Savings Bank (“PSB” or the “Bank” or the “Issuer”) is offering P3,000,000,000 worth of Unsecured Subordinated Notes eligible as Tier 2 Capital due 2022, callable in 2017 (the “Notes”) pursuant to the authority granted by the Bangko Sentral ng Pilipinas (“BSP”) to the Bank on 1 February 2012 and Subsections X116.1 and X119.1 of the Manual of Regulations for Banks, BSP Circular No. 709 (series of 2011), and other applicable regulations and issuances of the BSP, each as amended from time to time. The Notes will bear interest at the rate of 5.75% per annum from and including 20 February 2012 to but excluding 20 February 2022. Unless the Notes are earlier redeemed upon at least 30 days’ notice prior to 21 February 2017 (the “Call Option Date”), the interest shall be payable quarterly in arrears at the end of each Interest Period on 20 May, 20 August, 20 November and 20 February, commencing on 20 February 2012 until the Maturity Date.

Unless previously redeemed, the Notes will be redeemed at their principal amount on Maturity Date or 20 February 2022. Subject to the satisfaction of certain regulatory approval requirements, the Bank may redeem the Notes in whole and not only in part at a redemption price equal to 100% of the principal amount together with accrued and unpaid interest upon at least 30 days’ notice prior to the Call Option Date. (See Terms and Conditions of the Notes – Call Option Date.) The Notes will constitute direct, unconditional, and unsecured obligations of the Bank. The Notes will be subordinated in right of payment of principal and interest to all depositors and other creditors of the Issuer and will rank pari passu and without any preference among themselves, but in priority to the rights and claims of holders of all classes of equity securities of the Bank, including holders of preferred shares, if any. (See Terms and Conditions of the Notes – Status of Notes.) THE NOTES ARE NOT DEPOSITS AND ARE NOT INSURED BY THE PHILIPPINE DEPOSIT INSURANCE CORPORATION. THE NOTES ARE SUBORDINATED TO THE CLAIMS OF DEPOSITORS AND ORDINARY CREDITORS. THE LOANS ARE UNSECURED AND NOT COVERED BY THE GUARANTY OF THE ISSUER NOR OF ITS SUBSIDIARIES AND AFFILIATES. THE NOTES ARE INELIGIBLE AS COLLATERAL FOR A LOAN GRANTED BY THE ISSUER, ITS SUBSIDIARIES AND AFFILIATES. The Notes will be issued in scripless form and in minimum denominations of P500,000.00 and integral multiples of P100,000.00 thereafter and will be registered and lodged with the Registry in the name of the Holders. The Notes will be represented by a Master Note deposited with the Trustee (with copy to the Registry). The Electronic Registry Book (the “Registry Book”) shall serve as the best evidence of ownership with respect to the Notes. However, a written advice will be issued by the Registry to the Holders to confirm the registration of Notes in their name in the Registry Book, in accordance with the regulations of the BSP (“Registry Confirmations”). Once registered and lodged, the Notes will be eligible for transfer or assignment through a Market Maker by electronic book-entry transfers in the Registry Book, and any sale, transfer, or conveyance of the Notes shall be coursed through a Market Maker. In the event that the Notes are listed in a fixed income exchange, the services of the Market Maker shall cease and secondary trading on the Notes would henceforth be conducted in such fixed income exchange in accordance with the rules and regulations of such fixed income exchange. The Notes have been given a PRS Aaa rating by PhilRatings. A rating is not a recommendation to buy sell or hold securities and may be subject to revision, suspension or withdrawal at any time by the rating agency concerned. INVESTING IN THE NOTES INVOLVES CERTAIN RISKS. (SEE “INVESTMENT CONSIDERATIONS” FOR A DISCUSSION OF FACTORS TO BE CONSIDERED IN CONNECTION WITH AN INVESTMENT IN THE NOTES).

Lead Manager and Selling Agent

Selling Agent and Market Maker

Limited Selling Agents

Offering Circular 15 February 2012

i

The date of this Final Offering Circular is 15 February 2012. The BSP on 29 December 2011 approved the issuance and sale of the Notes. The Bank confirms that this Offering Circular contains all information with respect to the Bank and the Notes which are material in the context of the issue and offering of the Notes, that the information contained herein are true and accurate in all material respects, are not misleading, that the opinions and intentions expressed herein are honestly held and have been reached after considering all relevant circumstances and are based on reasonable assumptions, that there are no other facts, the omission of which would, in the context of the issue and offering of the Notes, make this document as a whole or any of such information or the expression of any such opinions or intentions misleading in any material respect and that all reasonable inquiries have been made by the Bank to verify the accuracy of such information. The Bank accepts responsibility accordingly. In making an investment decision, the recipient of this document must rely on his own examination of the Bank and the terms of the offering of the Notes, including the merits and risks involved. By receiving this Offering Circular, the recipient acknowledges that (i) he has not relied on ING Bank N.V., Manila Branch (‘‘ING Bank’’ or the ‘‘Lead Manager’’), Multinational Investment Bancorporation (‘‘MIB’’)(collectively the “Selling Agents”) or any person affiliated with the Lead Manager or the Selling Agents in connection with his investigation of the accuracy of any information in this Offering Circular or his investment decision, and (ii) no person has been authorized to give any information or to make any representation concerning the Bank, or the Notes other than as contained in this Offering Circular and, if given or made, such information or representation should not be relied upon as having been made or authorized by the Bank or the Lead Manager. This Offering Circular contains forward looking statements that include, among others, statements concerning the Bank’s plans relating to (i) the expansion of its business and operations; (ii) the growth in its customer base and loan portfolio; (iii) the implementation of new information and other technologies; (iv) the ability to provide new products and services; and (v) the increase in its operational efficiencies, and other statements of expectation, belief, future plans and strategies, anticipated developments and other matters that are not historical facts and which may involve predictions of future circumstances. Investors are cautioned that these forward looking statements are subject to risks and uncertainties that could cause actual events or results to differ from those expressed or implied by the statements contained herein and no assurance can be given that the future results will be achieved. Actual events or results may differ materially as a result of the risks and uncertainties the Bank faces. Such risks and uncertainties include, but are not limited to (i) actions taken by the BSP, who is the regulator of the banking industry in the Philippines, and by the Government of the Republic of the Philippines; (ii) actions taken by the Bank’s competitors; and (iii) general economic and political conditions in the Philippines. No representation or warranty, express or implied, is made by the Lead Manager or the Selling Agents as to the accuracy or completeness of the information contained in this Offering Circular. Neither the delivery of this Offering Circular nor the offer of Notes shall, under any circumstances, constitute a representation or create any implication that there has been no change, material or otherwise, in the condition, operations, or affairs of the Bank since the date of this Offering Circular or that any information contained herein is correct as of any date subsequent to the date hereof. None of the Bank, the Lead Manager or the Selling Agents, or any of their respective affiliates or representatives makes any representation to any purchaser of the Notes regarding the legality of an investment by such purchaser under any applicable laws. In addition, the recipient should not construe the contents of this Offering Circular as legal, business, tax, or investment advice. The recipient should be aware that he may be required to bear for an indefinite period the risks, financial, tax, or otherwise of an investment in the Notes. The recipient is encouraged to consult with his own advisers as to the legal, tax, business, financial, and other related aspects of a purchase of the Notes. This document does not constitute an offer or solicitation by anyone in any jurisdiction in which such offer or solicitation is not authorized or to any person to whom it is unlawful to make any such offer or solicitation. Each investor in the Notes must comply with all applicable laws and regulations in force in the jurisdiction in which it purchases or offers to purchase such Notes, and must obtain the necessary consent, approval, or permission for its purchase, or offer to purchase such Notes under the laws and regulations in force in any jurisdiction to which it is subject or in which it makes such purchase or offer, and neither the Bank nor the Lead Manager shall have any responsibility thereof. Interested investors should inform themselves as to the applicable legal requirements under the laws and regulations of the countries of their nationality, residence, or domicile and as to any relevant tax or foreign exchange control laws and regulations that may affect them.

ii

TABLE OF CONTENTS

GLOSSARY OF TERMS iii

SUMMARY OF THE OFFERING 1

SUMMARY FINANCIAL INFORMATION 8

MANAGEMENT DISCUSSION AND ANALYSIS 11

INVESTMENT CONSIDERATIONS 14

USE OF PROCEEDS 23

CAPITALIZATION OF THE BANK 24

TERMS AND CONDITIONS OF THE NOTES 25

DESCRIPTION OF THE BANK 46

MANAGEMENT, EMPLOYEES, AND SHAREHOLDERS 63

PHILIPPINE BANKING SECTOR 69

BANKING REGULATIONS AND SUPERVISION 72

TAXATION 79

OFFER PROCEDURE 82

SUMMARY OF REGISTRY FEES 84

INDEX TO THE FINANCIAL STATEMENTS 85

iii

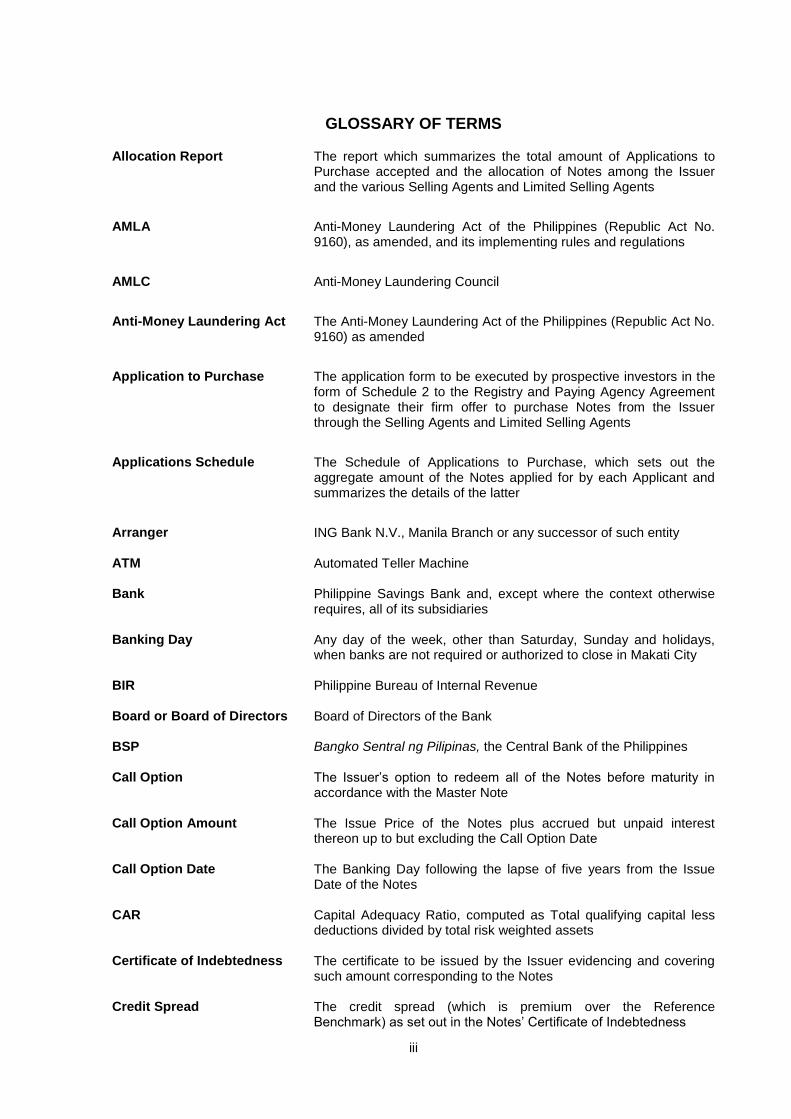

GLOSSARY OF TERMS

Allocation Report The report which summarizes the total amount of Applications to Purchase accepted and the allocation of Notes among the Issuer and the various Selling Agents and Limited Selling Agents

AMLA Anti-Money Laundering Act of the Philippines (Republic Act No.

9160), as amended, and its implementing rules and regulations

AMLC Anti-Money Laundering Council

Anti-Money Laundering Act The Anti-Money Laundering Act of the Philippines (Republic Act No.

9160) as amended

Application to Purchase The application form to be executed by prospective investors in the

form of Schedule 2 to the Registry and Paying Agency Agreement to designate their firm offer to purchase Notes from the Issuer through the Selling Agents and Limited Selling Agents

Applications Schedule The Schedule of Applications to Purchase, which sets out the

aggregate amount of the Notes applied for by each Applicant and summarizes the details of the latter

Arranger ING Bank N.V., Manila Branch or any successor of such entity

ATM Automated Teller Machine

Bank Philippine Savings Bank and, except where the context otherwise

requires, all of its subsidiaries

Banking Day Any day of the week, other than Saturday, Sunday and holidays, when banks are not required or authorized to close in Makati City

BIR Philippine Bureau of Internal Revenue

Board or Board of Directors Board of Directors of the Bank

BSP Bangko Sentral ng Pilipinas, the Central Bank of the Philippines

Call Option The Issuer’s option to redeem all of the Notes before maturity in accordance with the Master Note

Call Option Amount The Issue Price of the Notes plus accrued but unpaid interest thereon up to but excluding the Call Option Date

Call Option Date The Banking Day following the lapse of five years from the Issue Date of the Notes

CAR Capital Adequacy Ratio, computed as Total qualifying capital less deductions divided by total risk weighted assets

Certificate of Indebtedness The certificate to be issued by the Issuer evidencing and covering such amount corresponding to the Notes

Credit Spread The credit spread (which is premium over the Reference Benchmark) as set out in the Notes’ Certificate of Indebtedness

iv

Director A Director of the Bank

DOSRI Directors, Officers, Shareholders and Related Interests

Eligible Holders All prospective purchasers of the Notes other than those identified

as Prohibited Holders

FCDU Foreign Currency Deposit Unit

GAAP Generally Accepted Accounting Principles

General Banking Law General Banking Law of 2000 (Republic Act No. 8791)

GOCCs Government Owned and Controlled Corporations

Holders Eligible Holders who, at any relevant time, appear in the Registry Book as the registered owners of the Notes

Interest Payment Date The last day of each Interest Period; provided, that if such day is not a Banking Day, the Interest Payment Date shall be the immediately succeeding Banking Day, unless such succeeding Banking Day falls into the next calendar month, in which case, the Interest Payment Date shall be the immediately preceding Banking Day

Interest Period Each successive three-month period commencing on the last day of the immediately preceding Interest Period and ending on (but excluding) the first day of the immediately succeeding Interest Period. Each Interest Period shall end on the numerically corresponding day of each third month after the Issue Date (or if there is no day so corresponding in such month, such Interest Period shall end on the last day of such month); provided, that (i) if any Interest Period would otherwise end on a day which is not a Banking Day, such Interest Period shall be extended to the next succeeding day which is a Banking Day, unless the result of such extension would be to carry such Interest Period over into another calendar month, in which event such Interest Period shall end on the immediately preceding Banking Day; and (ii) the last Interest Period shall end on, but exclude, the Maturity Date or Call Option Date (as the case may be)

Interest Rate

The interest rate per annum as specified in the Certificate of Indebtedness as the interest rate corresponding to the Notes. The Interest Rate for the Notes shall be the sum of the Reference Benchmark and the applicable Credit Spread

Issue Date The date on which such the Notes was issued, as specified in the corresponding Certificate of Indebtedness

Issue Management and Placement Agreement

The Issue Management and Placement Agreement dated 3 February 2012 by and among the Issuer and the Arranger

Issue Price An amount equal to one hundred percent (100%) of the face value of the Notes thereof

Issuer Philippine Savings Bank

LGUs Local Government Units

v

Limited Selling Agents The Issuer, First Metro Investment Corporation or any other related entity appointed by the Issuer as agreed with the Arranger to sell and distribute the Notes to prospective Eligible Holders

Majority Holders At any time, the Holder or Holders who hold, represent or account for more than fifty percent (50.0%) of the aggregate outstanding principal amount of the Notes

Market Maker Agreement The Market Maker Agreement dated 3 February 2012 by and among the Issuer and the Market Makers

Market Makers Multinational Investment Bancorporation and thereafter, the institution appointed by the Issuer to perform the role of market maker required under the relevant USD Rules or such fixed-income exchange authorized by the Securities and Exchange Commission on which the Notes may be listed after the Issue Date

Master Note The Master Note issued by the Issuer to evidence its obligations under the Notes and includes the Terms and Conditions of the Note

Maturity Date The date specified as the maturity date in the corresponding Certificate of Indebtedness of the Notes, which is up to 10 years from Issue Date, subject to any exercise of the call option

Maturity Value The amount of the face value of the Notes plus unpaid accrued applicable interest on the Notes up to but excluding the Maturity Date

Metrobank Metropolitan Bank and Trust Company

Metrobank Group Companies and individual shareholders affiliated/associated with Metrobank

Monetary Board Monetary Board of the BSP

MSMEs

Micro, Small and Medium-sized Enterprises

National Government The Government of the Republic of the Philippines

Net Tier 1 Capital

Total Tier 1 capital less deductions, such as deferred income tax, goodwill and unsecured credit accommodations to DOSRI

New Central Bank Act New Central Bank Act of 1993 (Republic Act No. 7653)

NGAs National Government Agencies

Note Agreements Means the Issue Management and Placement Agreement, the Selling Agency Agreement, the Registry and Paying Agency Agreement, the Trust Agreement, and the Market Maker Agreement

Notes Means the Notes with a maximum aggregate principal amount of Three Billion Pesos (P3,000,000,000) to be issued by the Issuer on the terms and conditions set out in the Master Note and the corresponding Certificate of Indebtedness

NPAs Non-Performing Assets

NPLs Non-Performing Loans

Offer An offer for the sale and distribution of the Notes to Eligible Holders

vi

Offering Circular The preliminary offering circular dated 27 January 2012 and the final offering circular dated 15 February 2012 prepared by the Arranger in connection with the offering of the Notes to the public

Offer Period The period when the Notes are offered for sale by the Issuer through the Selling Agents and the Limited Selling Agents to prospective Eligible Holders, as determined by the Issuer and the Arranger. The Offer Period for the Notes shall commence at the start of business hours of 3 February 2012 and end at the close of business hours of 9 February 2012 or such other day as may be determined by the Issuer and the Arranger

OFWs Overseas Filipino Workers

Option Notes The Notes in respect of which the Issuer exercises the Call Option

Option Notice The notice issued by the Bank indicating its intention to exercise its call option

PA Schedule The schedule of Purchase Advice which summarizes the allocations made among the various applicants

Parent Company Refers to Philippine Savings Bank only, excluding its subsidiaries

Paying Agent Standard Chartered Bank or such successor or substitute paying agent to be appointed by the Issuer upon prior approval of the BSP

Payment Account The account to be opened and maintained by the Issuer with the Registry and Paying Agent, into which the Issuer shall timely deposit the amount of interest and/or principal payments due, to be used exclusively for the payment of the interest on and principal due on the outstanding Notes on the relevant Payment Date, and to be managed solely and exclusively by the Registry and Paying Agent

Payment Date An Interest Payment Date, the Maturity Date, the Call Option Date, and any other date on which principal, interest on and/or any other amounts on the Notes are due and payable to the Holders

PCD Philippine Central Depository, a corporation established to improve operations in securities transactions and provide a fast, safe and highly efficient system for securities settlement in the Philippines

PCD Nominee PCD Nominee Corporation, a corporation wholly-owned by PCD which acts as trustee-nominee for all shares lodged in the PCD

PDIC Philippine Deposit Insurance Corporation

PDST-F

Philippine Dealing System Treasury Fixing

PFRS Philippine Financial Reporting Standards

PhilRatings Philippine Rating Services Corporation

Prohibited Holders (i) The Issuer, its subsidiaries and affiliates, and wholly- or majority-owned or -controlled entities of such subsidiaries and affiliates, and (ii) common trust funds managed by the trust department of the Issuer, its subsidiaries and affiliates, and wholly- or majority-owned or -controlled entities of such subsidiaries and affiliates, provided, that other funds being managed by the trust department of the Issuer may purchase or invest in the Notes subject to the conditions that (x) the fund owners give prior authority/instructions to the trust

vii

department to purchase or invest in the Notes, and (y) the authority/instructions of the fund owners and their understanding of the risk involved in purchasing the Notes are fully documented. For purposes of this definition, an “affiliate” of the Issuer is an entity at least twenty percent (20.0%) but not more than fifty percent (50.0%) of the outstanding voting stock of which is owned by the Issuer

PSE Philippine Stock Exchange

Purchase Advice The written advice to be issued by a Selling Agent, Limited Selling Agent or the Market Maker, as the case may be, to the Holder and to the Registry, confirming the fact, details, and terms and conditions of the purchase of the Notes by a Holder

Reference Benchmark The interest rate for 10-year Fixed Rate Treasury Notes, as

published on the PDST-F section of the PDEx Market Page under

the heading “Bid Yield” at approximately 11:15 a.m., Manila time, as

of such date mutually agreed upon by Issuer and the Arranger

Registry Standard Chartered Bank or such successor or substitute registry to be appointed by the Issuer upon prior approval of the BSP

Registry and Paying Agency Agreement

The Registry and Paying Agency Agreement dated 3 February 2012 by and between the Issuer and the Registry and Paying Agent

Registry Book The electronic records maintained by the Registry containing the official information on the names of the Holders and the number of Notes they respectively hold, including records of all transfers of the Notes

Registry Confirmation The written advice to be sent by the Registry to the relevant Holder to confirm the number and terms and conditions of Notes registered in the Registry Book in the name of the Holder at any relevant time

Risk Weighted Assets

Consist of on-balance sheet and off-balance sheet assets with applicable credit risk, market risk and operational risk weights

ROPA Real and Other Properties Acquired

RTGS The Philippines Payment System via Real Time Gross Settlement that would allow banks to continually effect electronic payment transfers which are interfaced directly to the automated accounting and settlement systems of the BSP

SEC Philippine Securities and Exchange Commission

Selling Agency Agreement

The Selling Agency Agreement dated 3 February 2012 by and between the Issuer and the Selling Agents

Selling Agents ING Bank N.V., Manila Branch and Multinational Investment Bancorporation or any other entity appointed by the Issuer as agreed with the Arranger to sell and distribute the Notes to prospective Eligible Holders

SGV & Co. SyCip Gorres Velayo & Co., a member firm of Ernst & Young Global Limited

SMEs Small and Medium-sized Enterprises

SPV Act The Special Purpose Vehicle Act of 2002 (Republic Act No. 9182)

viii

SPVs Special Purpose Vehicle companies

Terms and Conditions The terms and conditions of the Notes, as set out in, and as qualified by, the section “Terms and Conditions of the Notes” of this Offering Circular

Tier 1 Capital

Consists of common stock, additional paid-in capital, retained earnings, undivided profits and cumulative translation adjustment

Total Qualifying Capital

The sum of Net Tier 1 Capital and Net Tier 2 Capital

Trust Agreement The Trust Agreement dated 3 February 2012 by and between the Issuer and the Trustee, setting out the terms and conditions upon which the Trustee shall act as trustee of the Notes for the benefit of the Holders

Trustee Development Bank of the Philippines

USD Rules Means the General Banking Law of 2000 (Republic Act No. 8791), Subsections X116.1 and X119.1 of the Manual of Regulations for Banks, BSP Circular No. 709 (series of 2011), BSP Circular No. 538 (series of 2006), and BSP Memorandum dated 17 February 2003 (as amended by BSP Memorandum dated 5 August 2004 and BSP Memorandum dated 23 March 2006), and other related circulars and issuances, in each case, as amended to date and as may be further amended from time to time

1

SUMMARY OF THE OFFERING

This summary highlights information contained elsewhere in this Offering Circular. This summary is

qualified in its entirety by more detailed information and financial statements, including notes thereto,

appearing elsewhere in this Offering Circular. For a discussion of certain matters that should be

considered in evaluating an investment in the Notes, see “Investment Considerations.” Investors are

advised to read this entire Offering Circular carefully, including the Bank’s consolidated financial

statements and related notes contained herein.

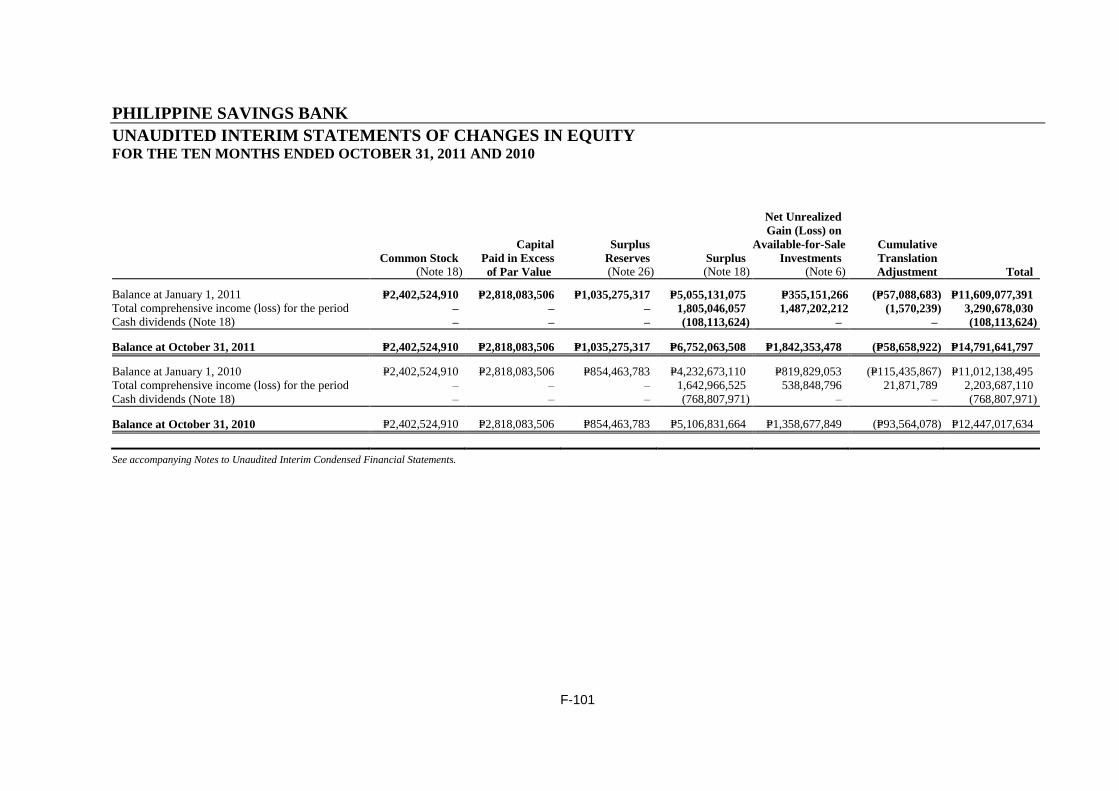

Principal Products, Markets and Distribution Philippine Savings Bank (the “Bank”) was established on 30 June 1959 primarily to engage in savings and mortgage banking. The Bank has outpaced some of its key competitors and is, today, the country's second largest thrift bank in terms of assets. The Bank is the country's first publicly listed thrift bank. The Bank caters mainly to the retail and consumer markets and offers a wide range of products and services such as deposits, loans, treasury, and trust. As of 31 October 2011, it has 196 branches. The Bank's total assets stood at P114.83 billion and P104.15 billion as of 31 October 2011 and 31 December 2010, respectively. Its total equity were at P14.79 billion and P11.61 billion as of 31 October 2011 and 31 December 2010, respectively As of 31 October 2011, the Bank is 75.98%-owned by Metrobank, a universal bank that provides a full range of banking and other financial services through its local and international branches. Metrobank is the country's second largest domestic bank with assets of P916.08 billion and has an extensive distribution network of over 585 branches nationwide as of 31 October 2011.

Competitive Strengths Majority owned by the Metrobank Group. PSBank is 75.98%-owned by the Metrobank Group, which is the second largest Philippine commercial bank in terms of assets and deposits. Metrobank is one of the leading expanded commercial banks in the country with more than 800 local and international offices and subsidiaries. Metrobank and PSBank serve distinct core markets and coordinate on market segmentation and branch location. Focused on the consumer market. Its focus is on retail deposit taking and consumer lending to upper- and middle-income classes. Through its 196 branches, it has been able to accumulate P97.04 billion deposit liabilities as of October 2011. Over the years, it has sought to develop products that address the needs of its target market. Consistent customer service and training. PSBank emphasizes Customer Service which is considered a major part of all performance evaluation reviews for both front-line and back-end support personnel. In an industry where homogenous products and services are being offered, PSBank aims to set itself apart through a unique customer-driven experience. Investments in Information Technology. PSBank has been investing in information technology for greater automation and integration of processes. This has resulted in improved efficiency through faster turn-around time for credit decisions, more uniform compliance with credit policies and better profit monitoring for its loan portfolio. PSBank offers one of the fastest turn-around times for mortgage and auto loan applications in the industry. It has a one day turn-around time for Auto Loans, five days for Home Loans and three days for Flexi/Personal Loans.

Strategy The Bank's vision is to be the country's consumer and retail bank of choice. It also aims to become the country's largest and most profitable thrift bank. The Bank will do this by maintaining a strategic management discipline that focuses on the consumer market. It will continue to harness inherent synergies with Metrobank and, at the same time, differentiate itself through its unmatched service, speed and quality. As part of the Metrobank Group, PSBank is able to easily expand its branch network and have access to customer data infrastructure and credit card operations by way of Metro Card Corporation. To grow the business, PSBank will rely on increasing visibility and customer

2

convenience by establishing more branches throughout the country. This will be complemented by the Bank’s continued improvements in customer profiling through its unique customer information system. The objective is to stay ahead of the profitability curve and build a competitive advantage by having a focus on its target market. This will be supported by having a customer-centric performance oriented culture within the Bank and an organizational structure which encourages employees to be flexible and motivated contributors. The Bank continues to be fueled and inspired by its mission and mandate to deliver Simple Lang, Maasahan (Simple and Reliable) service at all times. See Description of the Bank — Strategy of the Bank.

Risks of Investing Prospective investors should consider the current and immediate political and economic factors in the Philippines as a principal risk for investing. Political instability and threats to local and regional currencies may also influence the operations, growth, and profitability of the Bank. Of equal importance are the investment considerations regarding the Bank's operations. See Investment Considerations.

Recent Developments On 7 February 2012, the Impeachment Court issued a subpoena to PSBank requiring it to bring before the Senate “original and certified true copies of the account opening form / documents” for ten specified accounts allegedly owned by Chief Justice Renato C. Corona, as well as documents showing the balances of said accounts as of December 31 for the years 2007, 2008, 2009 and 2010. In compliance with the subpoena, the Bank submitted documents and account balances for five Philippine Peso accounts. With respect to other accounts appearing to be foreign currency deposits, PSBank President Pascual M. Garcia III informed the Impeachment Court that the Bank was unable to comply with the subpoena in view of Republic Act No. 6426 or the Foreign Currency Deposit Act of the Philippines. Moreover, Mr. Garcia informed the Impeachment Court that the Bank instructed its attorneys to file a Petition with the Supreme Court (SC) to effectively seek guidance on whether the Bank and its officers would be legally justified in complying with the subpoena of the Impeachment Court without violating RA 6426 and Section 87 of the Manual of Regulations on Foreign Exchange Transactions. The SC issued a Temporary Restraining Order (TRO) restraining the Impeachment Court from requiring the Bank to comply with the subpoena relating to Foreign Currency Deposits on 9 February 2012. On 13 February 2012, the Senate Impeachment Court upheld the TRO granted by the Supreme Court

with a vote from the senator-judges of 13-10 in favor of abiding by the SC decision.

3

Summary of the Terms and Conditions Issuer…………………………. Philippine Savings Bank

Notes ................................................ P3,000,000,000 aggregate principal amount of Fixed Rate Unsecured

Subordinated Notes qualifying as Tier 2 Capital issued by the Issuer under these Terms and Conditions.

Issue Price .......................................

100% of the face value of each Note.

Denomination ...................................

The Notes will be offered in minimum denominations of P500,000.00 each and increments of P100,000.00 beyond the minimum. The Notes will be represented by a Master Note which will be deposited with the Public Trustee.

Offer Period ......................................

The period when the Notes shall be offered for sale by the Issuer through the Issuer’s branches and the Selling Agents to prospective Holders, with the Offer Period commencing at 9:00 a.m. of 3 February 2012 and ending at 5:00 p.m. on 9 February 2012 or such other days as may be determined by the Arranger and Selling Agents, in consultation with the Issuer.

Issue Date ........................................

The date when the Notes are issued by the Issuer to the Holders or on 20 February 2012.

Maturity Date ....................................

Up to ten years from the Issue Date at which date the Notes will be redeemed at their Maturity Value; Provided, that if such date is declared to be a non-Business Day, the Maturity Date shall be the next succeeding Business Day. Recognition of the Notes in regulatory capital in the remaining five (5) years before maturity will be amortized on a straight line basis.

Benchmark Rate ..............................

Prevailing Philippine Dealing System Treasury Fixing (“PDST-F”) 10-year treasury securities benchmark rate displayed under the heading “Bid Yield” as published on the PDEx Page (or such successor page) of Bloomberg (or such successor electronic service provider) at approximately 11:30 a.m., Manila time on the Pricing Date.

Interest Rate .....................................

5.75% per annum.

Interest Payment Dates ...................

On the 20th of May; 20th of August; 20th of November and 20th of February of each year until Final Maturity Date. If the Interest Payment Date is not a Business Day, interest will be paid on the next succeeding Business Day, without adjustment to the amount of interest to be paid.

Redemption ...................................... Unless previously redeemed pursuant to the exercise of the Issuer’s Call Option, the Notes will be redeemed on Maturity Date at the Maturity Value. The Notes may not be redeemed at the option of the Holders.

Call Option ....................................... The Issuer may, but is not obliged to, redeem the Notes, in whole but not in part, at the Call Option Amount, on the Call Option Date, subject to the prior approval of the BSP and the compliance by the Issuer with the Regulations and prevailing requirements for the granting by the BSP of its consent therefor, including (i) the capital adequacy ratio of the Issuer is well above the required minimum ratio after redemption; or (ii) the Note is simultaneously replaced, on or prior to the Call Option Date, with issues of new capital which is of the same or of better quality and is done under conditions which are

4

sustainable for the income capacity of the Issuer; and (iii) a 30 Banking Day prior written notice to the then Holder on record. Any tax due on interest income already earned by the Holders on the Notes shall be for the account of the Issuer. The notice for the Call Option shall be sent by the Issuer to the Public Trustee (with copy to the Registrar and Paying Agent) and to each of the registered Holders nor less than thirty (30) Business Days or more than forty five (45) Business Days prior to the Call Option Date. The Issuer shall likewise publish the notice of the Call Option in two (2) newspapers of general circulation in Metro Manila once a week for two (2) consecutive weeks at any time prior to the Call Option Date. Such notice shall state the Call Option Date, the Call Option Amount and the manner in which the call will be effected. Nothing herein shall be construed as an indication that the Issuer will exercise its Call Option and the Holders should not expect that such Call Option will be exercised.

Call Option Date ............................... The Banking Day immediately following the fifth (5th) anniversary of

the Issue Date of the Notes.

Call Option Amount ..........................

The principal amount of the Note plus accrued interest covering the accrued and unpaid interest as of but excluding the Call Option Date.

Secondary Trading ........................... All secondary trading of the Notes shall be coursed through the Market Maker referred to in the same Regulations, subject to the payment by the Holder of the proper fees to the Market Maker and the Registrar. In case of a transfer or assignment deemed by the Issuer as a pre-termination, solely for withholding tax purposes, the transferor Holder shall be liable for the resulting tax due on the entire interest income earned on the Notes (if any), based on the holding period of such Notes by the transferor Holder and the amount equal to the final withholding tax, if any, will be deducted from the purchase price due to it. Thereafter, the interest income of a transferee Holder who is an individual shall not be treated as income from long-term deposit or investment certificates, unless the Notes has a remaining maturity of at least 5 years. Transfers or assignments deemed by the Issuer as pre-termination for withholding tax purposes means any transfer or assignment which: (a) is made by a Holder who is a citizen, resident individual, non-resident individual engaged in trade or business in the Philippines, or a trust (subject to certain conditions); (b) under the Regulations, is not considered a pre-termination of the Notes; and (c) under relevant tax laws or revenue regulations, will result in the interest income on the Notes being subject to the graduated tax rates imposed on long-term deposit or investment certificates on the basis of the holding period of the investment instrument. No transfer or assignment of the Notes shall be recorded in the Registry unless the Issuer (or its duly authorized agent) has certified that the amount representing the tax due or arising from any such transfer or assignment has been paid.

Status and Subordination ................. The Issuer, for itself, its successors and assigns, has in the Trust Agreement covenanted and agreed, and each Holder by accepting a Note irrevocably agrees and acknowledges, that:

5

(a) the indebtedness evidenced by the Notes constitutes direct, unconditional unsecured and subordinated obligations of the Issuer, and, upon any distribution to creditors of the Issuer in a Winding Up of the Issuer (as defined below), the claims of the Holders in respect of the Notes shall be subordinated in right of payment, to the extent and in the manner provided hereunder, to the prior payment in full of all liabilities (whether actual or contingent, present or future) of the Issuer, including claims of depositors, except those subordinated liabilities which by their terms rank equally in right of payment with or junior to the Notes;

(b) the Notes are not deposits and are not insured by the Philippine

Deposit Insurance Corporation;

(c) The Notes are unsecured and are not covered by a guarantee of the Issuer or Arranger or any other related party of the Issuer or Arranger. Neither are the Notes covered by any other arrangement that legally or economically enhances the priority of the claim of the Holders as against depositors and other creditors of the Issuer;

(d) Claims in respect of the Notes will rank pari passu without

preference among themselves, in priority to the rights and claims of holders of all classes of equity securities of the Issuer, including holders of preference shares, if any;

(e) Upon the distribution to creditors or any assets of the Issuer in

the event of any insolvency or liquidation of the Issuer, the claims of Holders for principal and interest in respect of the Notes shall be subordinated in right of payment to claims (whether actual or contingent, present or future) of all depositors and creditors of the Issuer, except those creditors that are expressly ranked equally with or junior to the Holders in right of payment;

(f) and the Notes may not be used as collateral for any loan made

by the Issuer or any of its subsidiaries or affiliates;

(g) Holders or their transferees shall not be allowed, and hereby waive their right, to set off any amount they owe to the Issuer against the Notes.

(h) Except in the case of bankruptcy and liquidation of the Issuer, no

holder shall have the right to require the Issuer to redeem and repay any or all of the Notes before the Maturity Date.

(i) The recognition of the Notes as regulatory capital in the

remaining five years before maturity shall be amortized on a straight-line basis or in accordance with prevailing regulations at that time.

Holder/s…………………….. Any person who, at any relevant time from the Issue Date, appears in the Registry as the registered owner of the Notes,

Prohibited Holders............................

The following persons and entities shall be prohibited from purchasing and/or holding any Notes of the Issuer: (1) subsidiaries and affiliates of the Issuer, including the subsidiaries and affiliates of the Issuer's subsidiaries and affiliates; or (2) common trust funds managed by the Trust Department of the Issuer, its subsidiaries, and affiliates, or other related entities; or (3) other funds being managed by the Trust Department of the Issuer, its subsidiaries and affiliates or

6

other related entities where (a) the fund owners have not given prior authority or instruction to the Trust Department to purchase or invest in the Notes or (b) the authority or and instruction of the fund owner and his understanding of the risk involved in purchasing or investing in the Notes are not fully documented. For purposes hereof, a “subsidiary” means, at any particular time, a company which is then directly or indirectly controlled, or more than fifty percent (50%) of whose issued voting equity share capital (or equivalent) is then beneficially owned, by the Issuer and/or one or more of its subsidiaries or affiliates and an “affiliate” refers to a related entity at least 20.0% to not more than 50.0% of the outstanding voting stock of which is owned by the Issuer.

Taxation ........................................... In the event that the Holder is either (i) a Filipino citizen, (ii) an alien residing in the Philippines, (iii) a non-resident alien engaged in trade or business in the Philippines, (iv) subject to the clause on Prohibited Holders, a long-term trust account or long-term management account (including common trust funds of banks other than the Issuer) exclusively for Filipino citizens, aliens residing in the Philippines, and non-resident aliens engaged in trade or business in the Philippines; (v) a BIR-tax-qualified employee trust fund established by corporations; or (vi) any other tax-exempt institution (upon presentation of acceptable proof of tax exemption), all payments for principal and interest shall be made free and clear of any deductions or withholding for or on account of any present or future taxes or duties imposed by or on behalf of the Republic of the Philippines, including interest and penalties, unless such withholding or deduction is required by law. In the event there is a change in the tax status of the Notes because of new, or changes in tax laws (and not merely a change in the interpretation of present tax laws and regulations) as a result of which, any payments of principal and/or interest under the Notes shall be subject to deductions or withholdings for or on account of any taxes, duties, assessments or governmental charges of whatever nature imposed, levied, collected, withheld, or assessed by or within the Philippines or any authority therein or thereof having power to tax, including but not limited to stamp, issue, registration, documentary, value-added or similar tax, or other taxes, duties, assessments, or government charges, including interest, surcharges, and penalties thereon (the "New Taxes"), then all payments of principal and interest in respect of the Notes shall be made free and clear of, and without withholding or deduction for, any such new taxes. In that event, the Issuer shall pay to the Holders concerned such additional amount as will result in the receipt by the Holders of such amounts as would have been received by them had no such withholding or deduction for new taxes been required. For the avoidance of doubt, such taxes and duties imposed shall be for the account of the Holder and the Issuer shall make the necessary withholding or deduction for the account of the Holder concerned; In any case, however, the Issuer shall not be liable for:

(a) the twenty percent (20.0%) or such other final withholding tax applicable on interest earned on the Notes prescribed under the National Internal Revenue Code (“NIRC”) of 1997, as amended;

(b) Gross Receipts Tax under Section 121 of the NIRC; (c) taxes on overall income of any securities dealer or any

Holder, whether or not subject to withholding; and (d) Value Added Tax (“VAT”) under Sections 106 to 108 of

7

the NIRC, as amended by Republic Act No. 9337. As required by law, the abovementioned 20.0% final withholding tax on interest income shall be withheld by the Issuer as withholding agent. The Issuer shall, upon request of the relevant Holder, provide the necessary proof of such withholding and corresponding payment to the Philippine revenue authorities. In case of transfers and assignments deemed by the Issuer as a pre-termination for tax purposes, the transferor Holder shall be liable for the resulting tax due on the entire interest income earned on the Notes (if any), based on the holding period of such Notes:

(1) Four (4) years to less than five (5) years: 5.00%; (2) Three (3) years to less than four (4) years: 12.00%; and (3) Less than three (3) years: 20.00%. Documentary stamp tax for the primary issuance of the Notes and the execution of the agreements pursuant thereto, if any, shall be for the Issuer’s account.

Arranger……………………… ING Bank N.V., Manila Branch

Selling Agents……………… ING Bank N.V., Manila Branch, and Multinational Investment

Bancorporation

Limited Selling Agents…….. Philippine Savings Bank (“PSBank”) and First Metro Investment Corporation (“FMIC”) PSBank and FMIC, acting as Limited Selling Agents, shall: (i) distribute no more than fifty percent (50.0%) of the total issuance of the Notes, (ii) enforce adequate client suitability procedures, and (iii) perform the other functions and responsibilities of a Selling Agent.

Registrar and Paying Agent….

Standard Chartered Bank

Market Maker ................................... Multinational Investment Bancorporation

Public Trustee .................................. Development Bank of the Philippines

8

SUMMARY FINANCIAL INFORMATION

The following tables provide selected financial information of the Bank which has been derived from its audited financial statements as of and for the years ended 31 December 2010, 2009, and 2008, including the notes thereto, included elsewhere in the document, and for the unaudited interim condensed financial statements of the Bank as of 31 October 2011 and for the ten-month period ended 31 October 2011. The unaudited interim financial statements are provided for reference purposes only and should not be relied upon by investors to provide the quality of information associated with an audit of the Bank. Neither the Bank nor the Underwriter makes any representation regarding the sufficiency of the unaudited interim financial statements for an assessment of the statements of condition, income, and cashflows of the Bank. Statements of Income Data

Unaudited For the ten months ended 31

October

Audited For the year ended 31 December

(In P) 2011 2010 2010 2009 2008

Interest Income 7,433,317,146 6,515,218,981 7,913,097,318 7,529,532,086 6,129,607,034

Interest Expense 2,687,299,931 2,371,107,868 2,900,694,510 2,696,054,957 2,420,109,373

Net interest income 4,746,017,215 4,144,111,113 5,012,402,808 4,833,477,129 3,709,497,661

Net Service Fees and Commission Income

608,966,249 561,741,617 691,681,482 596,241,357 534,365,260

Other Operating Income

821,188,191 2,025,554,370 2,532,453,557 841,618,744 693,595,578

Other Expenses 4,490,881,667 4,344,839,459 5,624,905,692 4,942,951,461 3,843,526,649

Income before Share in Net Income of an Associate and a Joint Venture and Income Tax

1,685,289,988 2,386,567,641 2,611,632,155 1,328,385,769 1,093,931,850

Share in Net Income of an Associate and a Joint Venture

25,095,851 38,465,553 41,563,418 45,129,698 46,820,603

Income before Income Tax

1,710,385,839 2,425,033,194 2,653,195,573 1,373,515,467 1,140,752,453

Provision for (Benefit from) Income Tax

(94,660,218) 782,066,669 845,080,234 133,501,051 200,600,860

Net income 1,805,046,057 1,642,966,525 1,808,115,339 1,240,014,416 940,151,593

9

Statements of Condition Data

Unaudited

As of 31 October

Audited As of 31 December

(In P) 2011 2010 2010 2009 2008

Assets

Cash and Other Cash Items

3,231,094,357 2,463,040,552 3,163,939,540 2,632,884,729 1,436,264,455

Due from Bangko Sentral ng Pilipinas

4,425,024,940 2,547,704,393 2,899,592,073 4,937,990,387 3,228,768,914

Due from Other Banks

3,056,716,899 852,833,477 7,520,836,053 1,528,847,687 1,276,768,278

Interbank Loans Receivable and Securities Purchased Under Resale Agreements

3,510,000,000 4,374,580,491 3,586,560,000 5,900,000,000 750,000,000

Fair Value through Profit or Loss Investments

701,886,015 3,376,982,251 868,316,442 248,043,099 1,081,772,381

Available for Sale Investments

20,978,187,045 24,047,673,868 16,200,339,057 18,261,371,820 16,813,786,476

Held-to-Maturity Investments

12,251,096,621 9,175,132,826 9,162,584,959 4,772,851,076 1,610,283,750

Loans and Receivables

58,106,752,194 53,120,182,373 53,207,635,160 47,308,237,957 41,603,346,112

Investment in an Associate and a Joint Venture

1,254,969,606 826,775,890 829,873,755 788,310,337 369,951,789

Property and Equipment

2,374,474,820 2,066,974,373 2,107,316,622 1,985,474,732 1,765,934,385

Investment Properties

2,764,003,768 2,765,678,633 2,772,308,932 2,582,767,705 2,776,144,811

Deferred Tax Assets 1,139,998,870 705,361,218 705,361,217 1,256,530,049 1,110,811,220

Goodwill and Intangible Assets

263,864,696 222,889,617 240,684,552 197,472,852 158,516,420

Other Assets 774,679,147 929,648,872 884,120,899 687,047,211 654,400,472

Total Assets 114,832,748,978 107,475,458,834 104,149,469,261 93,087,829,641 74,636,749,463

Liabilities

Deposit Liabilities

Demand 9,419,906,818 8,018,078,583 7,170,221,822 8,188,088,242 6,393,728,469

Savings 10,676,446,587 9,943,321,042 10,147,794,079 9,403,399,256 8,607,973,024

Time 76,948,499,840 72,127,579,521 70,200,793,366 59,798,723,788 46,676,781,428

Subordinated Notes - 1,976,818,081 1,977,141,032 1,973,881,534 2,208,541,621

Treasurer's, Cashier's and Manager's Checks

465,908,800 571,148,979 649,433,599 505,738,363 339,901,057

Accrued Taxes, Interest and Other Expenses

1,260,431,552 1,042,342,602 1,132,129,341 895,023,135 904,943,414

Income Tax Payable - - - 17,425,906 14,073,344

Other Liabilities 1,269,913,584 1,349,152,393 1,262,878,631 1,293,410,922 1,018,052,404

Total Liabilities 100,041,107,181 95,028,441,201 92,540,391,870 82,075,691,146 66,163,994,761

10

Selected Financial Ratios

(1) Net income divided by average total assets for the period indicated. Net income for the ten months ended 31 October 2011

is annualized. Average total assets is based on the two-point average considering outstanding balance as of 31 October 2011 and 31 December 2010, and for the years ended 31 December 2010, 2009, 2008, and 2007.

(2) Net income divided by average total equity for the period indicated. Net income for the ten months ended 31 October 2011 is annualized. Average total equity is based on the two-point average considering outstanding balance as of 31 October 2011 and 31 December 2010, and for the years ended 31 December 2010, 2009, 2008, and 2007.

(3) Net interest income divided by average interest-earning assets. Net income for the ten months ended 31 October 2011. (4) Net Tier 1 capital divided by total risk weighted assets. (5) Total qualifying capital less deductions divided by total risk weighted assets. (6) Annualized net income divided by weighted average number of outstanding common share.

Source: PSBank

Unaudited

As of 31 October

Audited As of 31 December

(In P) 2011 2010 2010 2009 2008

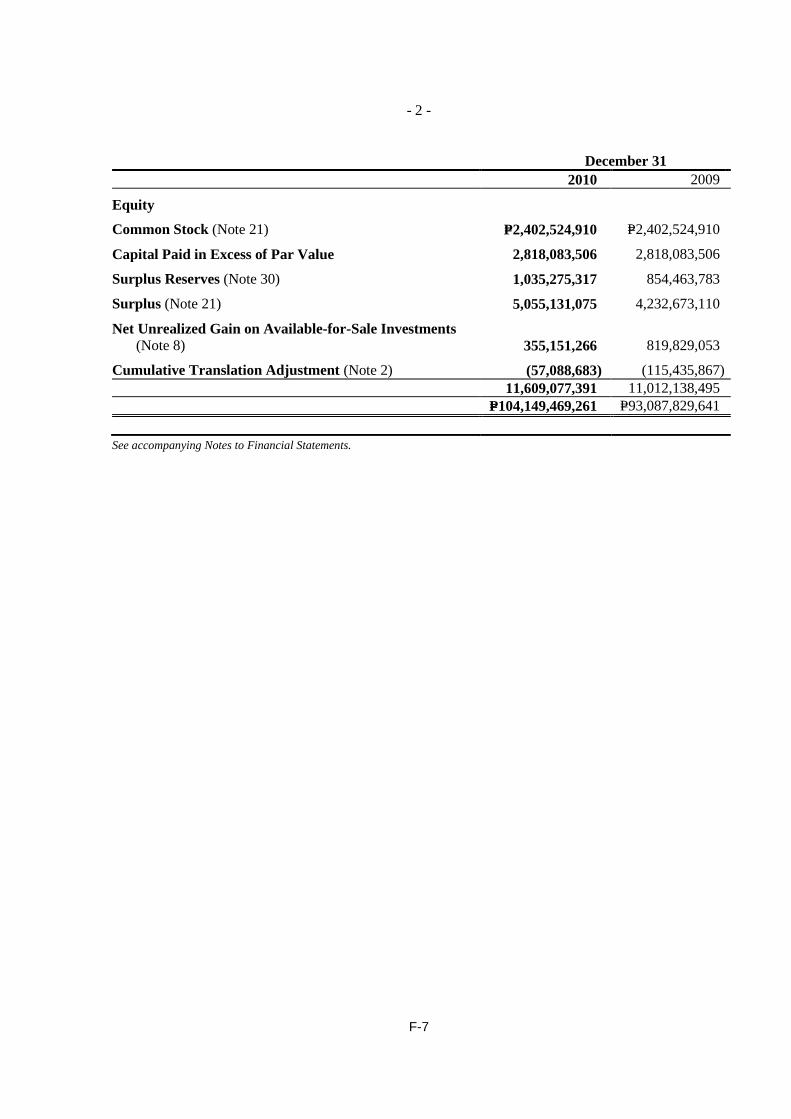

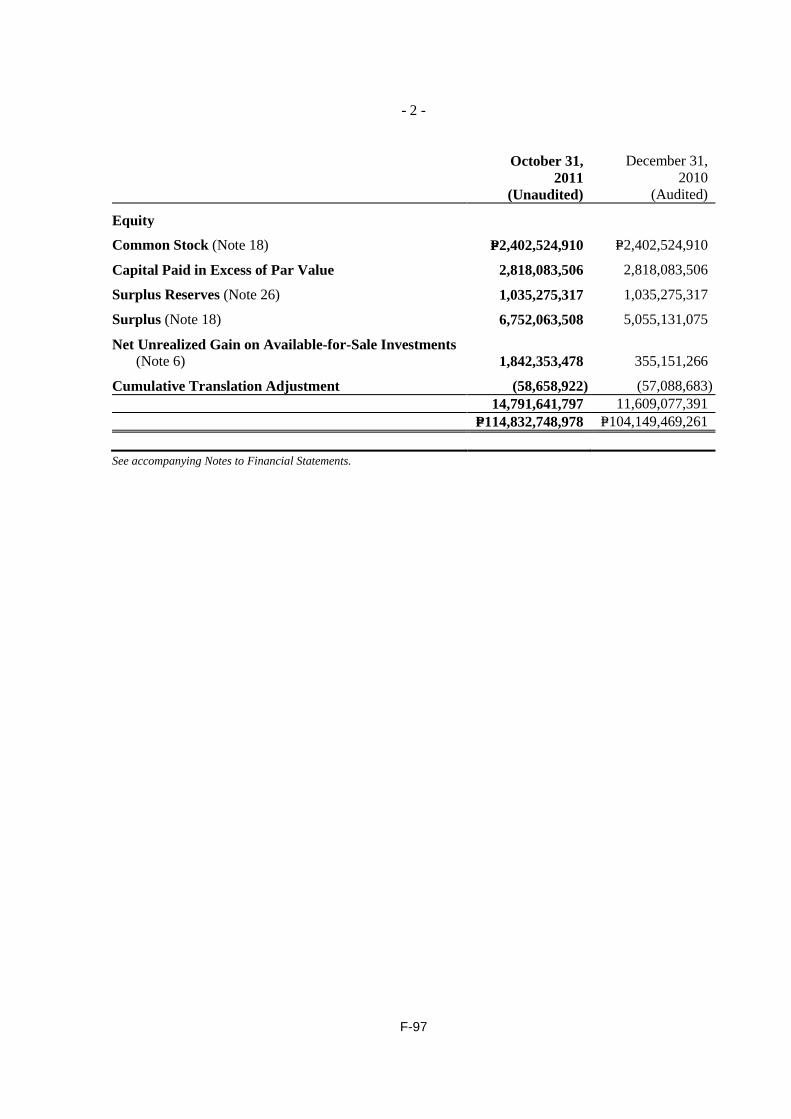

Equity

Common Stock 2,402,524,910 2,402,524,910 2,402,524,910 2,402,524,910 2,402,524,910

Capital Paid in Excess of Par Value

2,818,083,506 2,818,083,506 2,818,083,506 2,818,083,506 2,818,083,506

Surplus Reserves 1,035,275,317 854,463,783 1,035,275,317 854,463,783 730,462,341

Surplus 6,752,063,508 5,106,831,664 5,055,131,075 4,232,673,110 3,296,849,504

Net Unrealized Gain on Available-for-Sale Investments

1,842,353,478 1,358,677,849 355,151,266 819,829,053 (677,288,505)

Cumulative Translation Adjustment

(58,658,922) (93,564,079) (57,088,683) (115,435,867) (97,907,054)

Total Equity 14,791,641,797 12,447,017,633 11,609,077,391 11,012,138,495 8,472,724,702

Unaudited As of 31 October

Audited As of 31 December

2011 2010 2010 2009 2008

Return on Average Assets (1) 2.03% 1.97% 1.83% 1.48% 1.31%

Return on Average Equity (2) 16.78% 16.81% 15.99% 12.73% 12.47%

Net Interest Margin on Average Earning Assets (3) 4.68% 4.53% 5.57% 6.43% 5.75%

Tier 1 Capital Adequacy Ratio (4) 13.65% 12.38% 12.35% 11.34% 13.10%

Capital Adequacy Ratio (5) 13.65% 15.51% 15.37% 14.44% 17.42%

Earnings per share (P) (6) 7.51 6.84 7.53 5.16 3.98

11

MANAGEMENT DISCUSSION AND ANALYSIS

Balance Sheet Assets

The Bank’s Total Assets as of 31 October 2011 grew by 6.9% or P7.36 billion to P114.83 billion

compared to 31 October 2010 level of P107.48 billion as the Bank continued to expand its loan and

investment portfolios.

Cash and Cash Equivalents

Interbank Loans Receivable and Securities Purchased under Resale Agreements decreased by

19.8% or P864.58 million to P3.51 billion in 31 October 2011 versus P4.37 billion during the same

period last year. Likewise, Due from Other Banks was higher by P2.20 billion to P3.06 billion as of 31

October 2011 from P852.83 million recorded last year.

On the other hand, Due from Bangko Sentral ng Pilipinas increased by 73.7% or P1.88 billion to P4.43

billion versus the P2.55 billion recorded the previous year due to a 2.0% increase in the statutory/legal

reserve requirements for peso deposit liabilities and deposit substitutes. On 24 June 2011, a 1.0%

increase in statutory requirements for thrift banks took effect, as issued by BSP under Circular No.

726. Further, an additional 1.0% increase was issued effective 5 August 2011, under BSP Circular

No. 732. As a result, the Bank now maintains an 8% reserve requirement from a 6.0% reserve

requirement last year.

Cash and Other Cash Items increased by 31.2% or P768.05 million to P3.23 billion as of 31 October

2011 from P2.46 billion in 31 October 2010.

Loans and Receivables

Gross Loans and Receivables posted a steady growth of 9.8% to P62.88 billion versus the P57.28

billion recorded the previous year. There was a 16.2% increase in Auto Loans in October 2011,

followed by Mortgage Loans with 7.6% and Personal Loans by 5.9%. Commercial loans including

SME portfolio rose by 5.7% to P10.66 billion in October 2011. Net of Allowances, Loans and

Receivables grew by 9.4% to P58.11 billion versus the P53.12 billion recorded in the same period last

year.

Securities and Investments

Held-to-Maturity Investments climbed by 33.5% or P3.08 billion to P12.25 billion as of 31 October

2011 compared to year-ago level of P9.18 billion as the Bank accumulated long-term portfolio

investment in government securities and ROP bonds. On the other hand, Available-for-Sale

Investments was lower by 12.8% or P3.07 billion to P20.98 billion while Fair Value through Profit or

Loss Investments (“FVPL”) was lower by 79.2% or P2.68 billion at P701.89 million.

There was a 51.8% increase in Investments in an Associate and Joint Venture to P1.25 billion, due to

the P400.00 million additional investment in Sumisho Motor Finance Corporation (“SMFC”) last August

2011. This represents the Bank’s 25.0% stake in Toyota Financial Services Philippines Corporation

(“TFSPC”) and 40.0% interest in SMFC.

Meanwhile, Property and Equipment increased by 14.9% or P307.50 million to P2.37 billion due to the

expansion of the Bank’s ATM network, new branches, and renovation. Goodwill and Intangible Assets

increased by 18.4% or P40.98 million to P263.86 million as of 31 October 2011 from P222.89 million

as of 31 October 2010. On the other hand, Other Assets decreased by 16.7% or P154.97 million to

P774.68 million as of 31 October 2011 from P929.65 million the previous year.

12

Equity

Equity ended at P14.79 billion as of 31 October 2011, P2.34 billion or 18.8% higher versus the same

period last year as the Bank benefitted from higher net income for the period. The Bank declared

quarterly dividends amounting to P0.15 per quarter, consistent with its dividend policy.

Net Unrealized Gain on Available-for-Sale Investments was recorded at P1.84 billion as of 31 October

2011 compared to P1.36 billion in 31 October 2010. As of 31 October 2011 and 2010, the Bank

recorded a Cumulative translation adjustment under equity amounting to P58.66 million and P93.56

million, respectively.

Deferred Tax

Deferred Tax Asset increased by 61.6% or P434.63 million to P1.14 billion compared to year-ago level

of P705.36 million due to the recognition of deferred income tax on provision for credit and impairment

losses recorded for the period.

Subordinated Notes

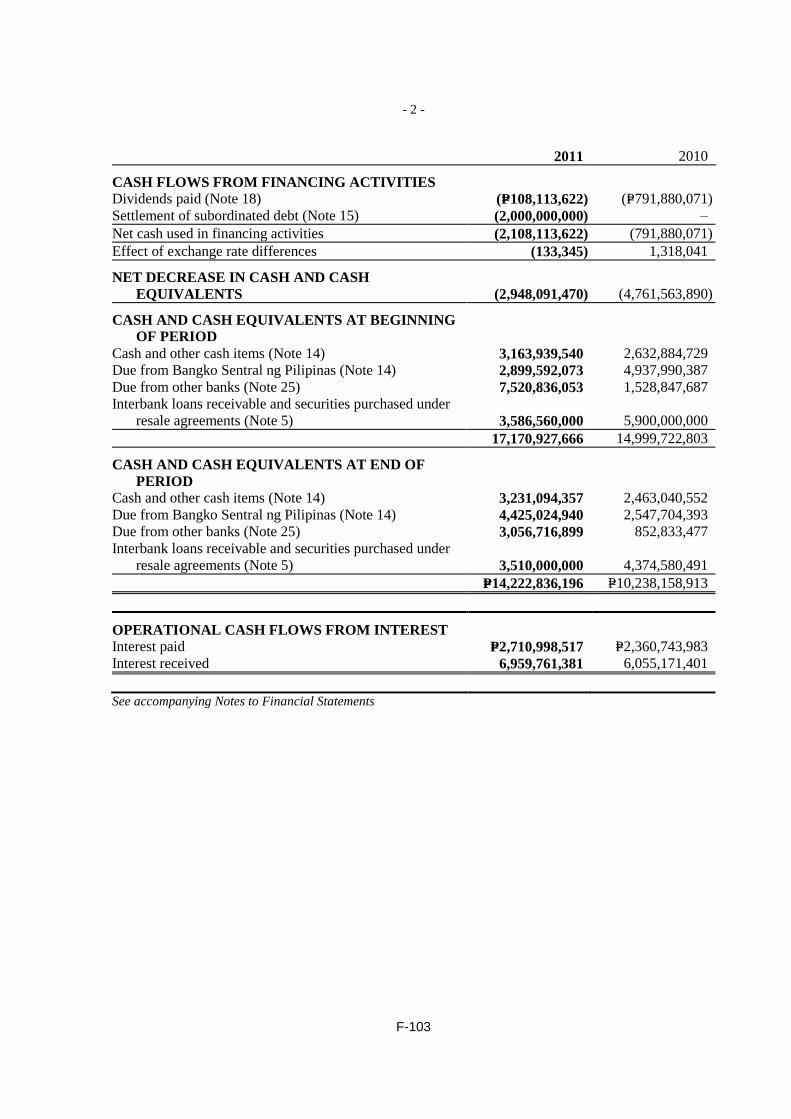

Last January 28, 2011, the Bank exercised the call option on its P2.00 billion Unsecured Subordinated

Notes (Tier 2) which was rated PRS Aaa by Philippine Rating Services Corporation (PhilRatings). PRS

Aaa indicates that the Notes are of the highest quality with minimal credit risk and that the Bank’s

capacity to meet its financial commitment is extremely strong.

Deposit Liabilities

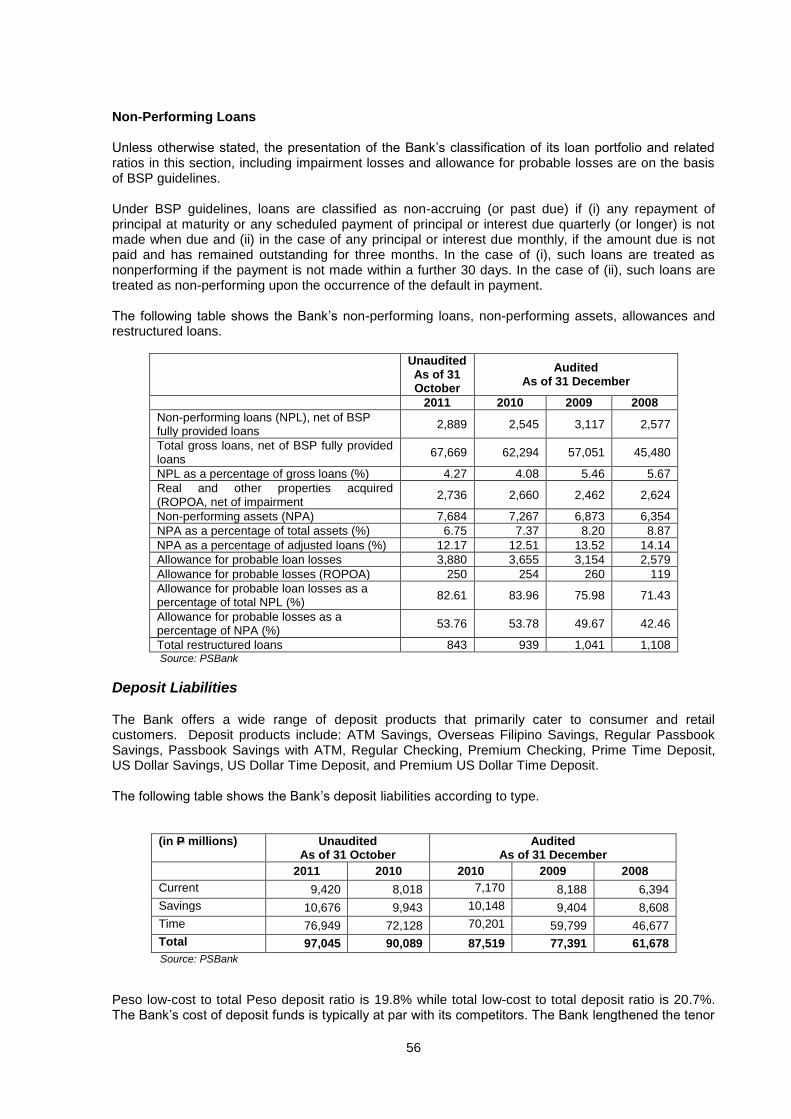

The Bank’s deposit liabilities level improved by 7.7% or P6.96 billion to P97.04 billion as of 31 October

2011 from P90.09 billion as of 31 October 2010 as it continued to benefit from various deposit

generation campaigns and expanded branch and ATM network. Time Deposits posted a growth of

6.7% or P4.82 billion while Demand Deposits also edged up by 17.5% or P1.40 billion from P8.02

billion. Likewise, Savings Deposits grew by 7.4% or P733.13 million as of 31 October 2011 from

P9.94 billion during the same period last year.

Income Statement

Net Income

The Bank recorded an after tax net income of P1.80 billion for the first ten months of 2011, 9.9%

higher versus the same period last year.

Interest Income

The Bank posted an increase in total interest income of 14.1% to P7.43 billion for the first ten months

of 2011, better than the P6.52 billion recorded in the same period last year. Interest income from

loans grew 10.6% to P5.38 billion with the expansion of the Bank’s total loan portfolio. Interest income

from investment securities also grew by 36.7% to P1.85 billion in October 2011.

Interest income from Due from Other Banks and Due from Bangko Sentral ng Pilipinas was at P59.11

million in October 2011, 61.0% lower than the P151.46 million previously realized in October 2010.

There was also a slight decrease in interest income from Interbank Loans Receivables and Securities

Purchased under Resale Agreements by 0.9% to P144.53 million.

Interest Expense was higher by 13.3% or P316.20 million, reaching P2.69 billion in October 2011

versus the same period last year as a result of growth in deposit liabilities.

Net Interest Income reached P4.75 billion in October 2011 from P4.14 billion last year or a 14.5%

increase.

13

Non-Interest Income

The Bank’s Other Operating Income in October 2011 posted at P821.19 million, 59.5% less than the

P2.03 billion recorded in October 2010 due to lower trading gains for the period. There was a decline

in Income from trading activities by 68.1% to P560.89 million from P1.76 billion. Foreign exchange

gains were recorded at P5.72 million while net Service Fees and Commission were higher at P608.97

million versus P561.74 million from the same period last year.

The Bank reflected a decline on gain on foreclosures of investment properties and chattel to P88.63

million, which was 58.2% lower than the P211.85 million reflected in October 2010. The Bank incurred

gains on the sale of investment properties and chattel including properties and equipment at P16.56

million.

The Bank’s other expenses for the period ended October 2011 were moderate at P4.49 billion from

the year-ago level of P4.34 billion. The Bank set aside a total of P396.42 million provisions for credit

and impairment losses for the ten months ended October 2011 compared to the P547.15 million

provisions in the same period last year.

Occupancy and equipment-related costs increased by 14.5% to P396.45 million due to branch and

ATM expansion during the period. As of October 2011, the Bank had 196 branches and 492 ATMs.

14

INVESTMENT CONSIDERATIONS

An investment in the Notes involves a number of investment considerations. You should carefully

consider all the information contained in this Offering Circular including the investment considerations

described below, before any decision is made to invest in the Notes. The Bank's business, financial

condition and results of operations could be adversely affected materially by any of these investment

considerations. The market price of the Notes could decline due to any one of these risks, and all or

part of an investment in the Notes could be lost.

Considerations Relating to the Bank

Significant Shareholding by Metrobank

As of 31 October 2011, a significant portion of the equity of the Bank, or 75.98%, is owned by Metrobank. The next largest shareholder is the Dolor Family, which owns 8.42% of the Bank. There is no assurance that the interests of Metrobank will necessarily coincide with the interests of the Noteholders. Concentration of Loan Portfolio

As of 31 October 2011, the Bank’s top 10 largest exposures account for 12.1% of the Bank’s total loan portfolio. There can be no assurance that these exposures would continue to perform their obligations to the Bank. As of 31 October 2011, 77.58% or P60.14 billion of the Bank’s Gross Loans is concentrated in three major economic activities. These include Real Estate (at P18.79 billion or 31.2%), Wholesale and Retail Trade (at P14.49 billion or 24.1%), and Other Community, Social, and Personal Activities (at P3.38 billion or 22.3%). High Level of Regulation

The Bank, being subject to the supervision and regulation of the BSP, is periodically audited by the BSP through the appropriate Supervision and Examination Sector for compliance with banking rules and regulations. While the Bank believes that as of 31 October 2011, it is fully compliant with all applicable rules and regulations and has effectively and efficiently implemented all corrective actions required, if any, to the satisfaction of the BSP, there can be no assurance that the Bank will at all times be compliant or that the BSP will find the operations or corrective measures taken by the Bank to be proper, acceptable or sufficient. In such cases, the Bank could be reprimanded, fined, or in extreme cases, have its banking license revoked, but at all times after due notice and hearing. Level of Non-Performing Loans

As of 31 October 2011, the Bank’s NPL ratio was at 4.27%. Through the implementation of stringent credit policies, the Bank expects its NPLs to further taper off. Ongoing volatile economic conditions in the Philippines may adversely affect the ability of the Bank’s borrowers to service their indebtedness and as a consequence the Bank may experience an increase in NPLs and provisions for probable losses. Although the Bank monitors closely current and future credit risk exposures, no assurance can be given that the amount of NPLs will not increase and will not have a material effect on the Bank’s capital adequacy ratio, its operations, and financial condition. Credit Risk

Credit risk is the risk that obligations will not be repaid on time and in full as contracted, resulting in a financial loss. It is the broadest category of risk in the Bank and is closely linked with other risk categories. Exposure to credit risk arises primarily from its lending activities.

15

Market Risk

Market risk is the risk that the Bank's earnings decline, either immediately or over time, as a result of a change in market factors. The level of market risk to which the Bank is exposed varies continually as a result of changing market conditions as well as the composition of the Bank's trading and non-trading portfolios.

Operational Risk

Operational risk is the risk of loss resulting from inadequate or failed internal processes, people and systems or from external events. This risk is a function of internal controls, information systems, employee integrity and operating processes. Operations risk has a very broad category that encompasses any risk not categorized as market or credit risk. The Bank’s operations are centralized in its Head Office in Makati. Although this is intended to promote efficiency, this set-up could also be a source of operational risk. The Bank mitigates this risk through its Business Continuity Program (“BCP”). It conducts regular BCP exercises and targets different recovery times per system. The Bank’s heavy reliance on technology for its operations also presents operational risks.

Liquidity Risk

Liquidity Risk relates to the Bank’s ability to generate sufficient cash or equivalents from internal or external sources, in a timely and cost-effective manner, to meet its commitments as they fall due. Mismanagement of liquidity will have quicker and more severe repercussions than errors in managing other risks. The Bank’s objective in liquidity management is to ensure that the Bank has sufficient liquidity to meet obligations under normal and adverse circumstances and is able to take advantage of lending and investment opportunities as they arise.

Considerations Relating to the Philippine Banking Industry

The Philippine banking industry is highly competitive and increasing competition may result in

declining margins in the Bank's principal businesses

The Bank is subject to significant levels of competition from many other Philippine banks and branches of international banks, including competitors which in some instances have greater financial, capital resources, market share and brand name recognition than the Bank. The banking industry in the Philippines has, in recent years, been subject to consolidation and liberalization, including liberalization of foreign ownership regulations. According to the BSP, as of 30 June 2011, thirty eight (38) domestic and foreign universal and commercial banks operated in the Philippines. These banks comprised three (3) domestic government-owned banks, nineteen (19) private domestic banks and sixteen (16) banks that are either branches or subsidiaries of foreign banks, all of which compete with the Bank in its targeted sectors and products. In the future, the Bank may face increased competition from financial institutions offering a wider range of commercial banking products and services than the Bank and that have larger lending limits, greater financial resources and stronger balance sheets than the Bank. Increased competition may arise from: (1) Other domestic Philippine banking and financial institutions with significant presence in Metro

Manila and large country-wide branch networks; (2) Rural and thrift banks, which may successfully implement strategies targeting customers in the

MSME sector; (3) Foreign banks, due to, among other things, relaxed standards permitting foreign banks to open

branch offices; (4) Domestic banks entering into strategic alliances with foreign banks with significant financial and

management resources; and (5) Continued consolidation in the banking sector involving domestic and foreign banks, driven in part

by the gradual removal of foreign ownership restrictions. There can be no assurance that the Bank will be able to compete effectively in the face of such increased competition. Increased competition may make it difficult for the Bank to continue to increase

16

the size of its loan portfolio and deposit base, as well as cause increased pricing competition, which could have a material adverse effect on its growth plans, margins, results of operations and financial condition. Philippine banks are generally exposed to higher credit risks and greater market volatility than

banks in more developed countries

Philippine banks are subject to the credit risk that Philippine borrowers may not make timely payment of principal and interest on loans and, in particular that, upon such failure to pay, Philippine banks may not be able to enforce the security interest they may have. The credit risk of Philippine borrowers is, in many instances, higher than that of borrowers in developed countries due to: (1) The greater uncertainty associated with the Philippine regulatory, political, legal and economic

environment; (2) The vulnerability of the Philippine economy in general to a severe global downturn due to the

dependence of the Philippine economy in general on remittances and exports for economic growth;

(3) The large foreign debt of the government and corporate sector, relative to the gross domestic product of the Philippines; and

(4) The volatility of interest rates and USD/P exchange rates. Higher credit risk has a material adverse effect on the quality of loan portfolios and exposes Philippine banks, including the Bank, to more potential losses and higher risks than banks in more developed countries. In addition, higher credit risk generally increases the cost of capital for Philippine banks compared to their international counterparts. Such losses and higher capital costs arising from this higher credit risk may have a material adverse effect on the Bank's financial condition, liquidity and results of operations. The average NPL ratios, exclusive of interbank loans, in the Philippine banking system were 4.5%, 4.1%, 3.9% and 3.1% for the years ended 31 December 2008, 2009, and 2010, and 30 June 2011, respectively. Philippine banks in general have exposure to the Philippine property market through holdings

of real and other properties acquired

As with other banks in the Philippines, the Bank has exposure to the Philippine property market due to the level of its real and other properties acquired (“ROPA”) holdings. The Bank’s ROPA (net of allowances for impairment) amounted to P2.55 billion as of 31 October 2011, or approximately 2.2% of the Bank’s total assets. The Philippine property market is highly cyclical, and property prices in general have been volatile through the past decade, though an uptrend has been observed toward the end of 2010 owing in part to recent domestic economic and political developments. Property prices are affected by a number of factors, including, among other things, the supply of and demand for comparable properties, the rate of economic growth in the Philippines and political and economic developments. There can be no assurance that an extended downturn in the property market will not occur, resulting in a significant decline in property values. Thus, there can be no assurance that the Bank will be able to recover all or most of the originally anticipated value of its ROPA in an eventual sale. Furthermore, the Bank is required under PFRS to recognize impairment losses on all ROPA, by reference to the difference between the carrying amount and the fair value less cost to sell. Accordingly, any extended downturn in the Philippine property sector could increase the level of the Bank’s recognized impairment losses, reduce the Bank’s net income and consequently adversely affect the Bank’s business, financial condition and results of operations generally. The Bank is subject to additional regulations and guidelines as a result of the developments in

the international banking industry

While the Bank is regulated principally by, and has reporting obligations to, the BSP and other government agencies, the Bank is also subject to regulations and guidelines imposed by and as a result of the international banking industry. For example, the BSP requires domestic banks to maintain a minimum risk weighted capital adequacy ratio of 10.0%, primarily as a result of the Revised Framework of the International Convergence of

17

Capital Measurement and Capital Standards (“Basel II”). The Bank’s capital adequacy ratio as of 31 October 2011 was 13.65%. Pursuant to the second pillar of Basel II, the Bank has also adopted the Internal Capital Adequacy Assessment Process in assessing capital adequacy in relation to risk profiles. In December 2010, the BSP also laid down preliminary guidelines for banks’ compliance with the updated guidelines of the Basel Committee on Banking Supervision (“Basel III”), which included certain amendments to the Basel II capital adequacy framework. As a result of the Basel directives, the Bank is exposed to the risk that the BSP may increase applicable risk weights for different asset classes from time to time. Any incremental capital requirement may adversely impact the Bank’s ability to grow its business and may even require the Bank to withdraw from or curtail some of its current business operations. There can also be no assurance that the Bank will be able to raise adequate additional capital in the future on terms favorable to it. Furthermore, while the Philippines enacted the Anti-Money Laundering Act of 2001 (the Anti-Money Laundering Act) to introduce more stringent anti-money laundering regulations pursuant to updated international standards, these regulations did not initially comply with the standards set by the Financial Action Task Force (“FATF”). However, following pressure from the FATF, an amendment to the Anti-Money Laundering Act became effective on 23 March 2003. In February 2005, the Philippines was removed from the list of Non-Cooperative Countries and Territories, confirming that anti-money laundering measures to remedy deficiencies that were originally identified by the FATF are in place. Anti-money laundering systems (including strict customer identification, suspicious transaction reporting, bank examinations, and legal capacities to investigate and prosecute money laundering) were all identified to be of a satisfactory nature. There can be no assurance that the FATF will not require more stringent money laundering standards in the future, and any failure by the Bank to comply with these standards may adversely affect its profile in the international market and results of operations. Any future changes in PFRS may affect the financial reporting of the Bank

PFRS continues to evolve with the effectivity of new standards and interpretations subsequent to 31 December 2010. The BSP recently approved the guidelines on the early adoption by banks and other BSP-supervised financial institutions of Philippine Financial Reporting Standards (“PFRS”) 9 Financial Instruments under Circular No. 708 s. 2011. PFRS 9 is the local adoption of International Financial Reporting Standards (“IFRS”) 9 Financial Instruments – the first phase of the three-phased improvement project by the International Accounting Standards Board (“IASB”) to ultimately replace International Accounting Standards (“IAS”) 39 Financial Instruments: Recognition and Measurement. Phases 2 and 3 of the project deal with accounting for the impairment of financial assets and hedge accounting, respectively. Phase 1 of IFRS 9, which deals with the classification and measurement of financial assets and financial liabilities, was adopted in the Philippines by the Financial Reporting Standards Council (“FRSC”) as PFRS 9. It will be mandatory beginning 1 January 2013 but entities were permitted to early adopt beginning on or after 1 January 2010. On November 7, 2011, the International Accounting Standards Board amended the mandatory adoption date for IFRS 9 to January 1, 2015. The Securities and Exchange Commission (“SEC”) has approved its adoption as part of its rules and regulations on 6 May 2010. PFRS 9 aims to improve and simplify the classification and measurement of financial instruments. It requires entities to classify and subsequently measure financial assets at either amortized cost or fair value on the basis of both (a) the entities’ business model for managing the financial assets; and (b) the contractual cash flow characteristics of the financial assets. Among others, PFRS 9 does away with “Available-for-Sale” (“AFS”) and “Held-to-Maturity” (“HTM”) categories, together with the “tainting rule” which requires entities to reclassify HTM securities to AFS securities in the event that any instrument booked under the HTM category is sold. PFRS9 also eliminates the requirement to bifurcate embedded derivatives from financial assets host contracts. It also requires enhanced disclosures to help the users of financial statements better understand the risks and the likely cash flows from the financial assets.

18