pension plan returns and the firm’s cost of debt€¦2 pension plan returns and the firm’s cost...

TRANSCRIPT

Pension Plan Returns and the Firm’s Cost of Debt

Mahendra Gujarathi

1

Atul Gupta2

Kartik Raman3

Bentley University

January 2010

1 Department of Accountancy, Bentley University, 175 Forest Street, Waltham, MA 02452. Phone: 781-891-3408;

Fax: 781-891-2896; Email: [email protected] 2 Department of Finance, Bentley University, 175 Forest Street, Waltham, MA 02452. Phone: 781-891-2772; Fax:

781-891-2896; Email: [email protected] 3 Department of Finance, Bentley University, 175 Forest Street, Waltham, MA 02452. Phone: 781-891-2781; Fax:

781-891-2896; Email: [email protected]

We thank Rani Hoitash, Jay Thibodeau, and workshop participants at the Bentley University Accounting workshop

for helpful comments and suggestions. We gratefully acknowledge Yan Wu, Li Li and Shubin Liang for providing

excellent research assistance.

1

Pension Plan Returns and the Firm’s Cost of Debt

Abstract

We examine firms with defined benefit pension plans and find a positive and statistically

significant relation between assumed rates of return on pension assets and stock return volatility,

the probability of default, and particularly the firm‟s cost of debt. In contrast, the actual return on

pension assets is only weakly related to the cost of debt. The findings are generally stronger for

firms with underfunded pension plans, and indicate that a one percent increase in the assumed

rate of return is associated with a 32 basis point higher cost of debt. Evaluated at the mean, our

findings suggest that every dollar increase in reported earnings achieved by assuming a higher

rate of return on pension assets is associated with an additional $1.87 in the cost of debt, thereby

highlighting an important economic consequence of off-balance-sheet activities.

Keywords: Defined benefit pension plan, assumed rate of return, actual return, cost of capital,

bond yield, default risk.

JEL Classification: G32

2

Pension Plan Returns and the Firm’s Cost of Debt

1. Introduction

“Companies may be forced to follow the lead of Detroit-based General Motors Corp., which in

2003 sold $13.5 billion of bonds to help close its pension deficit. To entice buyers, the world's

largest automaker offered yields about half a percentage point more than those on existing

debt……..Among the issues that have driven down GM's bonds and its credit ratings since the

2003 bond sale are concerns about GM's obligations to its retirees”

- Bloomberg.com, May 16, 2006.

Off-balance sheet assets play a crucial role in corporate risk-taking. Of particular interest

are the assets and liabilities of defined benefit pension plans, which constitute one of the largest

types of off-balance sheet items (Jin, Merton, and Bodie, 2006; Rauh, 2006, 2009; Shivdasani

and Stefanescu, 2009). Not surprisingly, pension plans have been instrumental in affecting the

financial health of prominent companies.4 Although the liabilities of such plans (net of plan

assets) are liabilities of the firm (Petersen, 1994), there is scant evidence on how rates of return

on pension plan assets affect the rates of return required by the firm‟s debt holders. Our study

attempts to fill this gap in the literature by examining the relation between pension plan returns

and the firm‟s cost of debt.

Under existing pension accounting rules, the reported income from pension assets is

derived from an assumed return on pension assets rather than the actual return on such assets.

The assumed return is under the discretion of corporate management and is oftentimes used as an

earnings management tool. Bergstresser, Desai and Rauh (2006) provide evidence that firms use

4 Scores of companies including Caterpillar, Goodyear, Kroger, Lockheed Martin, NCR, Nortel Networks, have

alluded to the adverse effect of pensions in their 2008 earnings reports. According to Credit Suisse, 128 of the S&P

500 companies could face a pension-related hit to earnings in 2009 (Wall Street Journal, 12/14/2008). Numerous

articles in the business press (Katz 2009, for instance) have noted the effect of pension deficits on jobs elimination,

salary cuts, loan covenant violation, slashing of capital expenditures and possible bankruptcy. For instance, General

Motors had to spend most of the $3.5 billion in cash generated in its auto business to fund its severely underfunded

pension plan. Furthermore, GM issued additional debt and convertible securities to raise $13.5 billion needed to

make up for the pension funding deficit, thereby compounding the likelihood of financial distress (Muller, 2003). In

a recent survey, about twenty five percent of senior finance executives interviewed agreed that “pension plans might

make it difficult to meet cash requirements, raise capital, or fund strategic investments” (CFO Publishing, 2007).

3

the assumed return on pension assets to opportunistically manage earnings, particularly in

periods preceding acquisitions, option exercises, and when they are near critical earnings

thresholds. While a higher assumed return boosts reported earnings, it can also have negative

implications for the firm‟s financial health, with associated higher costs of debt.

The expectation of a positive relation between the assumed return on pension assets and

the firm‟s cost of debt follows from the link between cash flow uncertainty, default risk, and the

cost of debt (Merton, 1974). A higher assumed return signals an increase in the risk of the

pension portfolio, and thereby raises the risk of large pension deficits. As firms are mandated to

cover such deficits with additional contributions, the assumed return on plan assets impacts the

likelihood that internal funds will be diverted to cover pension shortfalls, particularly when plans

are underfunded.5 Thus, pension plans aiming for higher returns are likely to face higher costs of

debt as riskier investments required to attain the high assumed returns increase the uncertainty of

cash flows available to pay creditors.6 Using a large sample of firms with defined benefit

pension plans between 1991 and 2006, we find empirical support for our hypotheses.

Our key findings are as follows. First, we find a positive and significant relation between

the assumed rate of return and stock return volatility during the year, confirming that higher

assumed rates of return on pension assets are associated with greater uncertainty about expected

future cash flows. Second, we find a significant positive relation between assumed rates of

return and the probability of default. The estimates suggest that all else equal, the probability of

default increases by 2.43 percent for every one percent increase in the assumed rate of return.

This result is more pronounced for firms with underfunded plans. Given that the unconditional

5 A plan is said to be underfunded if the amount of pension liabilities exceeds the amount of plan assets.

6 Bergstresser, Desai and Rauh (2006) provide evidence of a positive relation between the assumed return on

pension assets and portfolio risk; they find that a 25 basis point increase in the assumed return on pension assets is

associated with a 5 percent increase in equity allocations. See also Amir and Benartzi, 1998.

4

probability of default in our sample is 10.95 percent, pension plan returns appear to play a

substantial role in predicting the incremental probability of default.

Third, as shown in Figure 1, we find a strong positive relation between the assumed rate

of return on pension assets and the cost of debt; controlling for other factors, a one percent

increase in the assumed rate of return is associated with a 32 basis point increase in the cost of

debt. This result is significant in a sub-sample of firms with underfunded pension plans, but not

for firms whose plans are not underfunded. These findings are consistent with Carroll and

Niehaus (1998), in that underfunded pension plans are found to impact a firm‟s potential

liabilities more than overfunded plans affect the firm‟s assets.

Fourth, we examine whether the cost of debt reflects actual returns on pension assets

(disclosed in footnotes to the financial statements), or the assumed rate of return (which reduces

pension costs reported in the income statement but does not represent the actual performance of

pension assets). Using a smaller sample of S&P 500 firms (4,000 firm-year observations) with

hand-collected data on the actual return on pension assets, we find that the coefficient on lagged

actual return (with cost of debt as the dependent variable) is positive and significant at

conventional levels.7 However, the economic strength of this relation is weak. Firms reporting a

one percent higher (lagged) actual return are associated with only a 0.7 basis point incremental

increase in the cost of debt.

These findings suggest that although investors do not ignore cash flow relevant

information in the actual return, they appear to place less weight on such information. Overall,

the results are consistent with the view that debt holders demand a premium from firms with

higher assumed returns on pension assets, as these returns reflect higher levels of risk, higher

7 We use the lagged (rather than contemporaneous) actual return because the actual return in a given fiscal year may

not be known for a few months after the fiscal year ends. Our inferences regarding the effects of actual return and

the assumed rate of return are unchanged if we use contemporaneous instead of lagged actual return.

5

cash flow volatility, a greater likelihood of pension deficits and a higher likelihood of the firm

having to divert future cash flows to cover pension deficits.

The results are robust to a number of diagnostic checks. We examine whether annual

changes in the cost of debt are related to annual changes in the assumed rate of return, and find

that our conclusions are robust with respect to this specification. We also examine a sample of

new debt issues and find a significant positive relation between the assumed rate of return and

the yield to maturity at the new issue. Our findings indicate that firms with a one percent higher

assumed rate of return offer yields that are 28 basis points higher.

Furthermore, we examine the robustness of our results to the inclusion of variables that

control for differences in governance across firms and years by including board characteristics.

We also include a measure of accounting quality to control for the impact of earnings

management (through working capital accruals) on the cost of debt. The coefficient on the

assumed rate of return is positive and significant in each of these alternative specifications.

Finally, we verify that the results are similar using both cross-sectional regressions as well as the

Fama and Macbeth (1973) regression approach.

Our study contributes to the literature on several dimensions. First, market efficiency in

the context of pension-related issues has been almost exclusively focused on equity markets

(e.g., Barth, 1991; Barth et al., 1992; Brown, 2002; Coronado and Sharpe, 2003; Picconi, 2006;

Jin, Merton, and Bodie, 2006). In particular, some prior studies suggest that stock market

participants may not incorporate pension accounting information into earnings forecasts and

stock prices (e.g., Coronado and Sharpe, 2003; Picconi, 2006; Franzoni and Marin, 2006). Our

study provides evidence from a bond market perspective and finds that investors in the bond

6

market appear to price the information contained in pension plan returns.8 A potential

explanation for our findings is that trading in the corporate bond market is predominated by

large, institutional investors (Edwards, Harris, and Piwowar, 2006; Biais and Green, 2007), and,

securities owned and traded by institutional investors generally tend to exhibit greater

informational efficiency than other securities (Boehmer and Kelley, 2009). Moreover, as

bondholders receive fixed claims, the detrimental effect of uncertain future cash flows on bond

prices makes the cost of debt particularly sensitive to assumed rates of return on pension assets.

Second, by documenting a link between pension plan returns and the cost of debt, our

study adds to a growing body of research on defined benefit pension plans and their influence on

the firm‟s financial policies (e.g., Petersen, 1994; Rauh, 2006, 2009; Jin, Merton, and Bodie,

2006; Shivdasani and Stefanescu, 2009; Franzoni, 2009). In particular, Rauh (2006) suggests

that the negative relation between mandatory pension contributions and firms‟ capital

expenditures is primarily driven by the “inability of firms to raise funds for desired investments.”

Our finding that firms with higher assumed returns face higher costs of debt (particularly when

pension plans are underfunded), extends the work of Rauh (2006) and Franzoni (2009) by

suggesting that a higher cost of debt could be a potential reason why capital expenditures decline

for firms with mandatory pension contributions.

Third, prior research suggests that managers use the assumed return on pension assets to

boost reported earnings (Bergstresser, Desai, and Rauh, 2006), and that firms with higher

assumed returns are generally associated with riskier pension assets (Amir and Benartzi, 1998).

Our findings extend this line of work and support the theory in Kedia and Phillipon (2009) by

confirming that firms with higher assumed returns are associated with more uncertain future cash

8 The conceptual frameworks of both FASB and IASB state that financial reporting should provide information that

is decision-useful not only to equity investors, but also to creditors.

7

flows (arising from risky investments needed to justify the higher reported earnings), and thereby

incur a higher cost of debt. Indeed, our findings indicate that for every $1 increase in earnings

arising from the use of the assumed rate of return, firms incur additional debt costs of $1.87.

Thus, our study adds to the growing literature on economic consequences of earnings

management. In a broader vein, our study highlights how off-balance sheet activities influence a

firm‟s cost of capital.

Our findings also have implications for accounting standard-setters concerned about

whether investors are well served by firms reporting the assumed rate of return (rather than the

actual return) as it could mask information about the firm‟s net future liabilities arising from the

performance of pension plans. In particular, advocates of SFAS 87 (modified by SFAS 158)

argue that the actual return on pension assets includes transitory items in the form of unrealized

gains and losses and can exacerbate the volatility of reported earnings. Critics of SFAS 87 and

SFAS 158 however, are concerned that using the assumed rate of return to determine pension

costs has the effect of masking information about the true economic condition of pension assets.9

Our analysis contributes to this debate by providing evidence that from a credit market

perspective, investors appear to incorporate information contained in the assumed rate of return

into the firm‟s cost of debt. In addition, our finding that the actual return is only weakly related

to the cost of debt complements the evidence in Hann, Heflin, and Subramanyam (2007) who

find that fair-value pension accounting may impair the relevance of financial statements to the

market‟s assessment of firms‟ credit risk.

9 For example, prominent investors, practitioners, and members of congress have been vocal in their opposition to

the use of the assumed rate of return particularly because fair value accounting could result in the firm experiencing

a decline in the fair value of its net pension assets while at the same time reporting pension income from those assets

(see, e.g., Loomis, 2001; Barlas, 2005; Ryan and Fabozzi, 2002; and comment letters to the FASB from members of

congress at www.fasb.org).

8

The rest of the paper proceeds as follows. In the next section, we discuss the hypotheses

and related literature. The sample formation and description are presented in Section 3. We

discuss empirical results and robustness tests in Section 4, and conclude the paper in Section 5.

2. Hypotheses and related literature

In this section, we discuss factors affecting the relation between the firm‟s cost of debt

and the returns on defined-benefit pension plans. Companies use an assumed rate of return on

pension assets to compute periodic net pension costs, which impact their reported earnings. As

the assumed rate of return is supposed to reflect long-term expectations of the return on pension

assets rather than the true performance of such assets, the assumed return is likely to differ from

the actual return during any given period.

Bergstresser, Desai, and Rauh (2006) argue that one motive for the use of high assumed

rates of return is to lower the net pension cost, and thereby boost the reported earnings per

share.10

However, theory suggests that in order to credibly justify higher earnings arising from

the high assumed rates of return, firms would have to allocate pension assets into riskier

investments (e.g., Kedia and Phillipon, 2009). As a result, higher assumed rates of return on

pension assets are generally associated with riskier pension allocations such as LBOs, venture

capital and private placements (Amir and Benartzi, 1998; Bergstresser, Desai and Rauh, 2006).

The use of high assumed rates of return has potentially adverse consequences for the

firm‟s debtholders. First, riskier pension allocations increase the likelihood that firms would

have to rely on operating cash flow to cover pension shortfalls. This possibility arises because

10

A second, and mutually exclusive, motivation for using high assumed rates of return is to engage in risk-shifting,

i.e., transfer of wealth from employees and debt holders to shareholders. However, Rauh (2009) finds that risk-

shifting is not a primary motive for firms allocating assets in defined-benefit plans.

9

poor pension plan performance and pension deficits are more likely to occur when pension assets

are invested in risky securities (Rauh, 2006).11

As a result, the uncertainty about future cash

flows available for payments to creditors is expected to increase as the assumed rate of return

increases.12

Second, if high assumed rates of return increase the uncertainty about cash flows,

the risk of financial distress also increases.13

Thus, we hypothesize that:

H1: Firms with high assumed rates of return on pension assets are associated with more

volatile expected future cash flows.

H2: Firms with high assumed rates of return on pension assets are associated with a

higher probability of default.

It follows from the above arguments that bondholders would require higher premiums from firms

with high assumed returns because the claims of existing bondholders are diluted if high

assumed rates of return make cash flows more volatile than that implied by the terms of the

original bond contract (Fama and Miller, 1972; Jensen and Meckling, 1976; Smith and Warner,

1979). Moreover, the possibility of future debt issues with the same (or higher) level of seniority

increases the risk of claims dilution for existing bondholders, and thereby increases borrowing

11 When a defined-benefit pension plan is underfunded, the Employee Retirement Income Security Act (ERISA) of

1974, and more recently, the Pension Protection Act of 2006, mandate the sponsoring firm to make additional

contributions with the aim of restoring the pension plan to a fully funded status.

12

This view is corroborated by practitioners. In the context of pension shortfalls, Jonathan Nus, a director in S&P's

financial disclosure group notes that ``to the extent a company will have to contribute greater levels of cash flow it

will put increased pressure on the company's cash flow and liquidity'' (Richard, 2006).

13

For evidence on the link between cash flow volatility and distress risk, see e.g., Minton and Schrand, 1999;

Damodaran, 2002; Molina, 2005.

10

costs (Collin-Dufresne and Goldstein, 2001; Muller, 2003; Richard, 2006).14

Thus, firms with

high assumed rates of return on pension assets are expected to face higher borrowing costs.15

Collectively, the above arguments lead to our third hypothesis:

H3: Firms with high assumed rates of return on pension assets are associated with

higher costs of debt.

3. Sample and descriptive statistics

In this section, we describe the types of samples used in this study and the criteria used to

construct each sample. We also describe the key statistics associated with the variables used in

the study.

3.1 Sample formation

We examine three types of samples. First, we examine all Compustat firms with defined

benefit pension plans (hereafter referred to as the full sample). As our hypotheses examine the

relation between pension plan returns and the cost of debt, we require that sample firms have

non-missing data on pension assets and on the assumed rate of return on pension assets. This full

sample consists of 30,077 firm-year observations (represented by 4,194 firms) between 1991 and

2006. The sample period begins in 1991 because this is the first year with Compustat data

14

Brick and Fisher (1987) find that before 1950, most bond indentures prevented firms from issuing additional debt

of the same or higher seniority. However, such covenants were rare after 1976. See also, Malitz, 1994.

15

For instance, when GM issued additional debt in 2003 to cover its pension deficit, the company was forced to

offer yields that were 50 basis points higher than those of its existing debt (Richard, 2006).

11

available on the assumed rate of return on pension plans; prior research examining pension cost

issues also uses sample periods beginning in 1991 (e.g., Shivdasani and Stefanescu, 2009). 16

An advantage of using Compustat is that it enables us to draw inferences based on large

samples and makes replication easy. However, a drawback of this approach is that it does not

permit examination of the relation between actual returns and cost of debt. The actual return on

pension assets is miscoded in Compustat from 1997 onwards.17

Therefore, to examine the

relative importance of the assumed return versus the actual return on pension assets, we examine

a second (smaller) sample using hand-collected data on the actual return on pension assets from

10-K reports for the period beginning 1991 and ending 2006 for a sample of firms belonging to

the S&P 500 Index (hereafter referred to as the S&P sample). The S&P sample includes 4,000

firm-year observations.18

The third sample comprises of new debt issues between 1991 and 2006 made by firms

with defined benefit pension plans (hereafter referred to as the new issues sample). In this

sample we relate the assumed rate of return on the pension plan in the fiscal year preceding the

announcement of the new debt issue to the yield-to-maturity offered at the issue. For firms with

16

Prior studies such as Shivdasani and Stefanescu (2009) exclude financial companies because the interest expense

for such firms includes interest on deposits. In our study, we use two distinct types of samples. One sample is based

on pooled data, using the interest expense as a proxy for the cost of debt. The other sample is based on new debt

issues, where the cost of debt is measured as the yield to maturity for new debt offerings. As there is no reason to

exclude financials from the new debt issue sample, we include financials in both samples, rather than including them

in one sample and excluding them from the other. However, we verify and find that the exclusion of financials from

the pooled sample does not alter our conclusions.

17

Disclosure of actual return on pension plan assets was not required until SFAS 132 (applicable for fiscal years

ending after December 15, 1997) came into effect. As a result, actual returns are available only from 1997 for

almost all (2,584 out of 2,591) the observations.

18 We use membership in the S&P 500 Index as a criterion to form the smaller sample because over two-thirds of

these large firms have defined-benefit plans. Moreover, roughly 90 percent of these firms had underfunded pension

plans (with an aggregate of about $1.1 trillion in assets and $1.4 trillion in projected pension obligations (present

value) at the end of 2008 (Graves, 2009)

12

multiple debt issues in a given year, we retain the largest debt issue in that year. This sample

includes of 2,120 announcements of new debt issues by firms with defined benefit pension plans.

3.2 Descriptive statistics

The distribution of observations by year, reported in Panel A of Table 1, indicates that the

observations are distributed fairly evenly throughout the sample period, ranging from 5.65

percent to 7 percent in any given year. Panel B of Table 1 presents descriptive statistics for the

full sample. The variables are defined in the Appendix, and the reported statistics and results are

based on winsorizing all variables at the one and ninety-nine percent levels.

Following Francis, LaFond, Olsson, and Schipper (2005), we estimate the cost of debt as

the interest expense during the year scaled by the average total debt over the last two years; the

average cost of debt for firms in our sample is 8.37 percent, with a median of 7.60 percent. The

assumed rate of return is reasonably well distributed, with a mean of 8.44 percent and a median

of 8.50 percent. Pension assets are 14.18 percent of the firm‟s total assets on average, which is

similar to the mean value of 16.4 percent reported by Shivdasani and Stefanescu, 2009.

Moreover, about 63 percent of the firm-year observations are associated with underfunded

pension plans. The relatively high percentage of underfunded pension plans in our sample

reflects the low interest rate environment for much of the sample period, and is consistent with

anecdotal evidence suggesting that large percentages of S&P 500 firms had underfunded plans

over this time period.19

The sample firms are large, with total assets of about $12 billion on average, although the

median is much smaller at $1.2 billion. The mean leverage is 30.82 percent of assets, and the

19

For example, Kwan (2003) notes that about 90 percent of S&P 500 firms with defined benefit plans had

underfunded pension plans as of 2002. See also Graves, 2009.

13

sample firms are relatively profitable with a mean ROA of 2.37 percent. In addition, the mean

interest coverage ratio indicates that the operating income for firms in the sample is 13 times the

interest expense, on average, and the volatility of annual earnings during the prior ten years

(divided by average total assets during the same period) is around 4 percent, on average.

About 51 percent of the firm-year observations have debt ratings, and the volatility of

daily stock returns is about 2.51 percent on average. The average book-to-market ratio is 0.58.

Consistent with the sample firms having relatively low levels of uncertainty, the average beta for

the sample firms during a given fiscal year is 0.71. Furthermore, the probability of default (over

the next five years) for the average firm in our sample is around 10.95 percent and the mean

value of our measure of distance to default is 4.45. Interestingly, the characteristics of firms are

similar across sub-samples categorized by the funding status of the pension plan. The results in

the last two columns in Panel B of Table 1 suggest that firms with underfunded plans appear to

be slightly smaller, have pension assets that are a smaller proportion of total assets, are less

profitable on average and have slightly higher betas compared to firms without underfunded

plans. Finally, our proxy for the term structure, estimated as the difference between the 10-year

and the six-month Treasury yield, is 1.46 percent on average.

Panel C of Table 1 presents key characteristics of firms without defined benefit plans

(and hence not in our sample). A comparison of these characteristics with those of the sample

firms in Panel A indicates that firms with defined benefit pension plans are larger, more

profitable, have less uncertainty, higher interest coverage ratios and a lower cost of debt. This

pattern of results for defined benefit plan sponsors and non-sponsors is largely similar to those

reported by Shivdasani and Stefanescu (2009) for their sample period of 1991 to 2003.

14

4. Empirical results

In this section, we describe findings from multivariate regressions exploring the relation

between pension plan returns and the volatility of stock returns, the likelihood of default, and the

firm‟s cost of debt. As our sample comprises of panel data on variables (such as cost of debt and

the assumed rate of return on pension assets) that are likely to be correlated across time for a

given firm, or across firms each year, we follow Petersen (2009) and include firm and year fixed

effects to minimize the bias in the coefficient estimates and in the significance levels.20

Moreover, the firm fixed effects specification helps mitigate the endogeneity bias in the

coefficient estimates due to the omission of potentially correlated variables. Following Petersen

(2009), the t-statistics reported in the study are based on standard errors that are robust with

respect to heteroskedasticity and adjusted for firm-level clustering.

4.1. Assumed rate of return and stock return volatility

A higher level of cash flow uncertainty implies more volatile stock returns. Thus, if

higher assumed returns increase cash flow uncertainty by increasing the uncertainty about

pension shortfalls, we should expect a positive relation between assumed rates of return and

stock return volatility. In this section, we examine the relation between stock return volatility

and assumed rates of return using the following regression specification:

𝑆𝑡𝑎𝑛𝑑𝑎𝑟𝑑 𝑑𝑒𝑣𝑖𝑎𝑡𝑖𝑜𝑛 𝑜𝑓 𝑟𝑒𝑡𝑢𝑟𝑛𝑠𝑖 ,𝑡 =

∝ + 𝛽1 𝐴𝑠𝑠𝑢𝑚𝑒𝑑 𝑟𝑎𝑡𝑒 𝑜𝑓 𝑟𝑒𝑡𝑢𝑟𝑛 𝑖,𝑡 + 𝛽2 𝐿𝑜𝑔 𝑡𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠 𝑖 ,𝑡

+ 𝛽3 𝐿𝑒𝑣𝑒𝑟𝑎𝑔𝑒 𝑖 ,𝑡 + 𝛽4 𝑅𝑂𝐴 𝑖 ,𝑡 + 𝛽5 𝐼𝑛𝑐𝑜𝑚𝑒 𝑣𝑜𝑙𝑎𝑡𝑖𝑙𝑖𝑡𝑦 𝑖,𝑡 + 𝛽6 𝑅𝑎𝑡𝑒𝑑 𝑖,𝑡

+ 𝛽7 𝐵𝑒𝑡𝑎 𝑖 ,𝑡 + 𝛽8 𝐵𝑜𝑜𝑘 𝑡𝑜 𝑚𝑎𝑟𝑘𝑒𝑡 𝑖 ,𝑡 + ∈𝑖 ,𝑡 (1)

20

We verify the robustness of our findings using alternative regression specifications including cross-sectional

regressions and the Fama-Macbeth specification. Findings from these additional tests are presented and discussed in

section 4.8 of the paper.

15

The rationale for our choice of explanatory variables is as follows. We include firm size

as small firms are likely to be associated with greater information asymmetries and hence, higher

stock return volatility. We also include leverage as firms with higher leverage are likely to face

more volatile stock returns. In addition, we control for measures of firm profitability and income

volatility as we expect less profitable firms and those with more volatile earnings to be

associated with higher stock return volatility. We also expect firms with higher betas and firms

that are not rated to be associated with more volatile stock returns. Additionally, we include the

book to market equity ratio as an independent variable to control for the possibility that firms

with high ratios may be distressed (and hence, associated with higher stock return volatility), or

that firms with low ratios may be characterized by growth options (leading to more uncertainty

about future cash flows, and hence, greater stock return volatility).

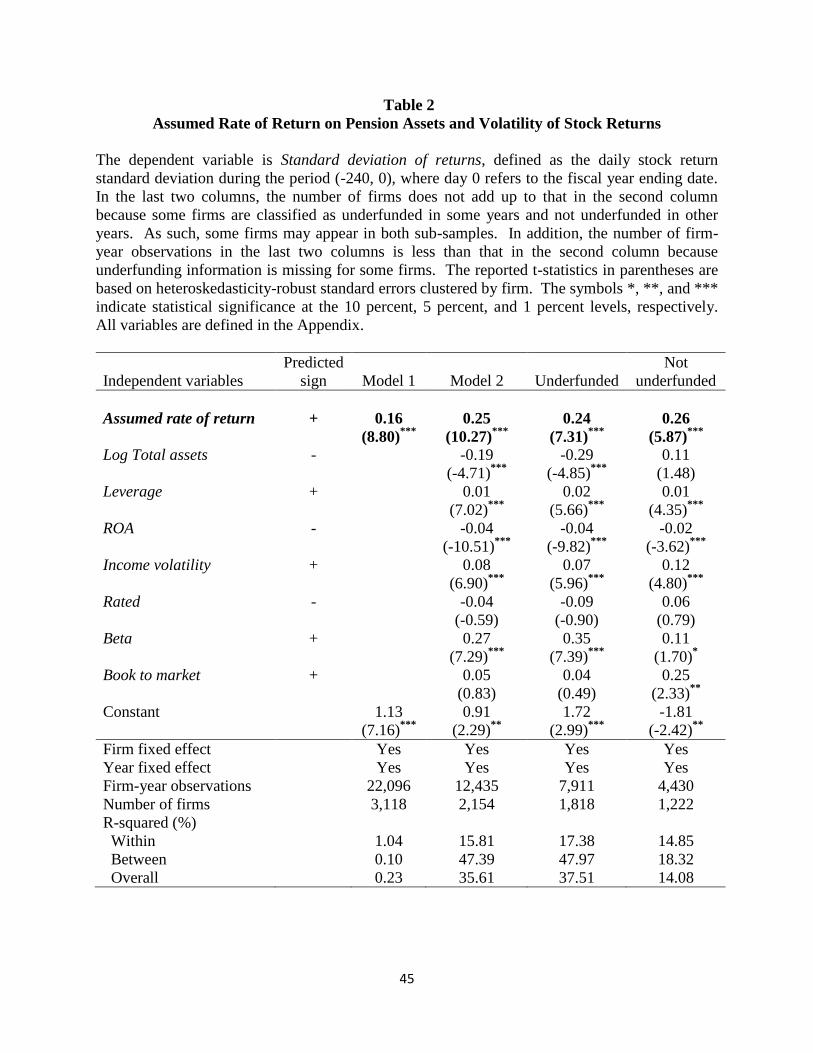

Findings from this regression are reported in Table 2. In Model 1 of Table 2, with no

control variables, the coefficient on Assumed rate of return is 0.16 with a t-statistic of 8.80,

confirming the presence of a significant positive relation between assumed rates of return and

stock return volatility. Including the entire set of explanatory variables yields the findings

reported in Model 2; in this specification the coefficient on Assumed rate of return is 0.25 with a

t-statistic of 10.27. These results suggest that firms reporting a one percent higher assumed rate

of return are associated with a 25 basis point higher volatility in daily stock returns. This finding

indicates that pension returns have an economically significant impact on return volatility,

considering that the mean daily stock return volatility for the sample is 2.55 percent.

Analysis of sub-samples reveals that the association between assumed rate of return and

stock return volatility is stable across firms with underfunded plans as well as those with plans

that are not underfunded. The coefficients for the assumed rate of return in both sub-samples are

16

similar to those for the full sample, suggesting that the incremental increase in stock return

volatility that is attributable to the assumed rate of return on pension assets is independent of the

funding status of the pension plan.

The control variables have signs that are intuitive and consistent with expectations. We

find that firms that are smaller, more levered, less profitable, having more volatile income, and

higher betas are associated with higher levels of stock return volatility. Overall, the results in

this section are consistent with hypothesis H1, indicating that investors attach higher levels of

uncertainty to firms with higher assumed returns, regardless of whether or not the pension plan is

underfunded.

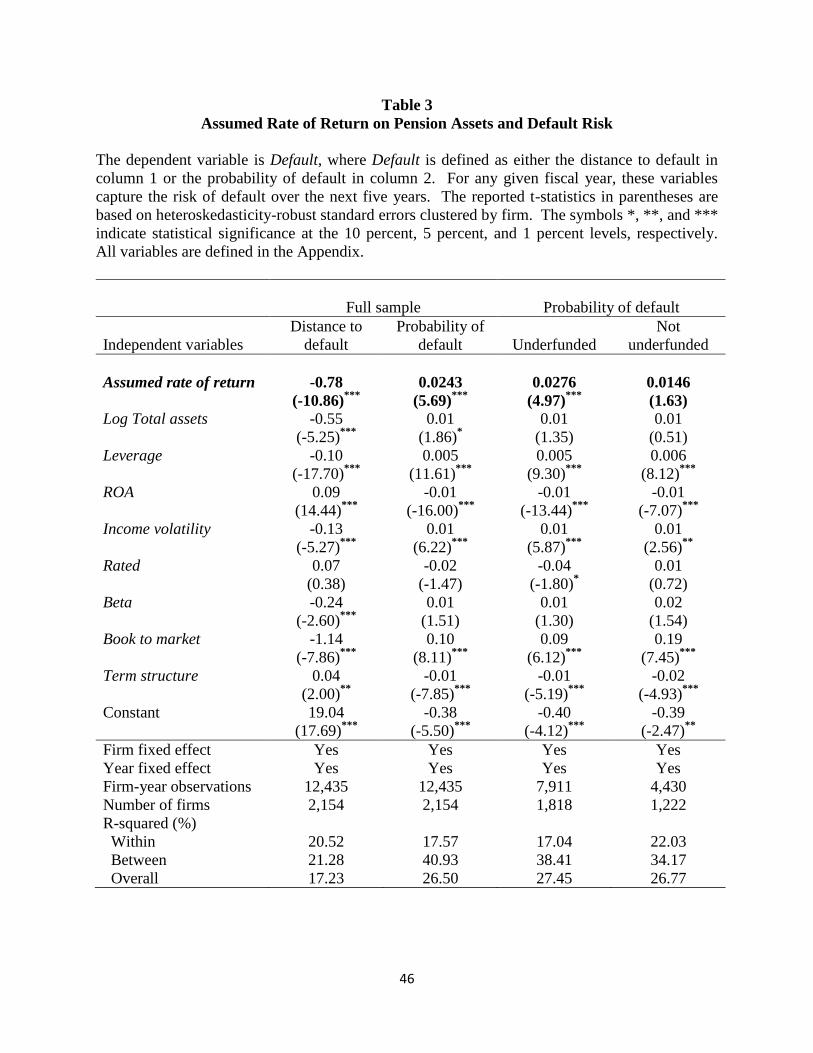

4.2. Assumed rate of return and default risk

Given the importance of default risk to the cost of debt, we examine whether investors

expect higher probabilities of default for firms reporting higher assumed rates of return.

4.2.1. Choice of model and measure of default risk

One challenge in the estimation of default probabilities is the choice of an appropriate

model. As noted by Vassalou and Xing (2004), accounting based models of default risk rely on

financial statement information, which is inherently backward looking and hence less suited to

estimating the future probability of default. Moreover, although the volatility of asset values is

an important indicator of default risk (Merton, 1974), accounting based models do not take into

account the impact of asset volatilities on the probability of default.

Following prior research such as Vassalou and Xing (2004) and Bharath and Shumway

(2008), we use the option pricing framework, which incorporates forward-looking information

17

about investors‟ expectations of future firm performance into the estimates of default

probabilities.21

According to the option pricing framework used in Merton (1974), the value of a

firm‟s equity at time t can be viewed as a call option on the firm‟s assets, with the value of

liabilities as the strike price. We follow the KMV-Merton approach suggested in Duffie and

Singleton (2003) and estimate distance to default as:

𝐷𝐷𝑡 = 𝑙𝑛

𝑉𝑎 ,𝑡

𝑋𝑡 + 𝜇 −

12𝜎𝑎

2 𝑇

𝜎𝑎 𝑇 (2)

where, DD refers to the distance to default, taV , is the value of the underlying assets, tX is the

value of the firm‟s liabilities, represents the expected asset returns, a is the volatility of the

firm‟s assets, and T represents the time remaining until expiration of the call option. Given that

the effects of pension plan returns on pension deficits and the firm‟s liabilities are unlikely to

manifest in the short term (within a year), we use five years as the time till expiration and assess

the likelihood of default over the next five years.

Intuitively, given that default occurs if the ratio of the value of assets to debt is less than

one (or log of this ratio is negative), the distance to default indicates approximately by how many

standard deviations the log of this ratio has to deviate from its mean for default to occur. Thus,

our first measure of default risk is the distance to default. Based on our hypothesis H2, we

expect firms reporting higher assumed rates of return on pension assets to be associated with a

smaller distance to default, reflecting greater credit risk.

Our second measure of default risk is the probability of default, which is based on the

distance to default. The probability of default is estimated as:

21

In addition, this framework incorporates the volatility of assets into the estimation of default probabilities. As a

result, even if firms have similar levels of equity and debt, their default probabilities could differ if their asset

volatilities are different.

18

𝑃𝑟𝑜𝑏𝑎𝑏𝑖𝑙𝑖𝑡𝑦 𝑜𝑓 𝑑𝑒𝑓𝑎𝑢𝑙𝑡 = 𝜑 −𝐷𝐷𝑡 (3)

where 𝜑() represents the cumulative normal distribution function. As it is unclear how much of

the long-term debt should be used to estimate default risk over the next five years, we follow the

approach used in prior research (e.g., Crosbie, 1999; Vassalou and Xing, 2004; Das and

Hanouna, 2009) and include one half the long-term debt in our calculation of total debt.22

We

estimate the market value of the firm‟s assets as the market value of common equity plus book

value of total assets minus the book value of common equity. Further, we estimate expected

asset returns as the average daily stock return during the 240 days preceding the fiscal year end,

and the volatility of the firm‟s asset values as the daily stock return standard deviation during the

240 days preceding the fiscal year end, both measures annualized using 240 trading days.

4.2.2. Assumed rate of return and default risk: Empirical results

We examine the relation between pension returns and the probability of default using the

following multivariate regression specification.

𝐷𝑒𝑓𝑎𝑢𝑙𝑡 𝑟𝑖𝑠𝑘𝑖,𝑡 =

∝ + 𝛽1 𝐴𝑠𝑠𝑢𝑚𝑒𝑑 𝑟𝑎𝑡𝑒 𝑜𝑓 𝑟𝑒𝑡𝑢𝑟𝑛 𝑖,𝑡 + 𝛽2 𝐿𝑜𝑔 𝑡𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠 𝑖 ,𝑡

+ 𝛽3 𝐿𝑒𝑣𝑒𝑟𝑎𝑔𝑒 𝑖 ,𝑡 + 𝛽4 𝑅𝑂𝐴 𝑖 ,𝑡 + 𝛽5 𝐼𝑛𝑐𝑜𝑚𝑒 𝑣𝑜𝑙𝑎𝑡𝑖𝑙𝑖𝑡𝑦 𝑖,𝑡 + 𝛽6 𝑅𝑎𝑡𝑒𝑑 𝑖,𝑡

+ 𝛽7 𝐵𝑒𝑡𝑎 𝑖 ,𝑡 + 𝛽8 𝐵𝑜𝑜𝑘 𝑡𝑜 𝑚𝑎𝑟𝑘𝑒𝑡 𝑖 ,𝑡 + 𝛽9 𝑇𝑒𝑟𝑚 𝑠𝑡𝑟𝑢𝑐𝑡𝑢𝑟𝑒 𝑖 ,𝑡

+ ∈𝑖 ,𝑡 (4)

We model default risk using variables that are likely to affect the likelihood of financial

distress. In addition to the control variables in Table 2, we include the term structure of Treasury

22

We verify and find that including all the long-term debt as part of the firm‟s total debt does not change our

conclusions with regard to the relation between assumed rate of return on pension assets, distance to default and the

probability of default.

19

yields as an independent variable to control for the effects of macroeconomic factors on distress

risk. Table 3 presents results from the above regression. In the first column of Table 3, the

dependent variable, Default risk, is measured using Distance to default. The coefficient on

Assumed rate of return is -0.78 and is highly significant with a t-statistic of -10.86, indicating

that firms reporting higher assumed returns are closer to default than other firms.

In the second column of Table 3, with Default risk measured as the probability of default

over the next five years, we find that the coefficient on Assumed rate of return is positive and

significant at conventional levels. The coefficient implies that every one percent increase in the

assumed rate of return is associated with a 2.43 percent increase in the probability of default.

This finding appears to be economically significant, given that the unconditional probability of

default for the full sample is 10.95 percent.

In the last two columns, we report the regression coefficients for probability of default by

categorizing the sample based on pension funding status. The results indicate that the link

between the assumed rate of return on pension assets and the probability of default is more

pronounced in the sub-sample of firms with underfunded plans. The probability of default

associated with a one percent increase in the assumed rate of return is 2.76 percent in the

underfunded sub-sample, compared to the statistically insignificant coefficient in the sub-sample

of firms without underfunded pension plans. These findings complement the evidence on stock

return volatility, and suggest that investors in debt markets appear to incorporate the information

in pension returns into their assessment of default risk.

The control variables in Table 3 yield coefficients that are largely consistent with

expectations. For instance, the probability of default increases with leverage and the book-to-

market ratio. Furthermore, firms with lower profitability (ROA) and greater variability in

20

profitability (income volatility) are associated with higher probabilities of default. These

findings are consistent with the results in prior research (e.g., Bharath and Shumway, 2008).23

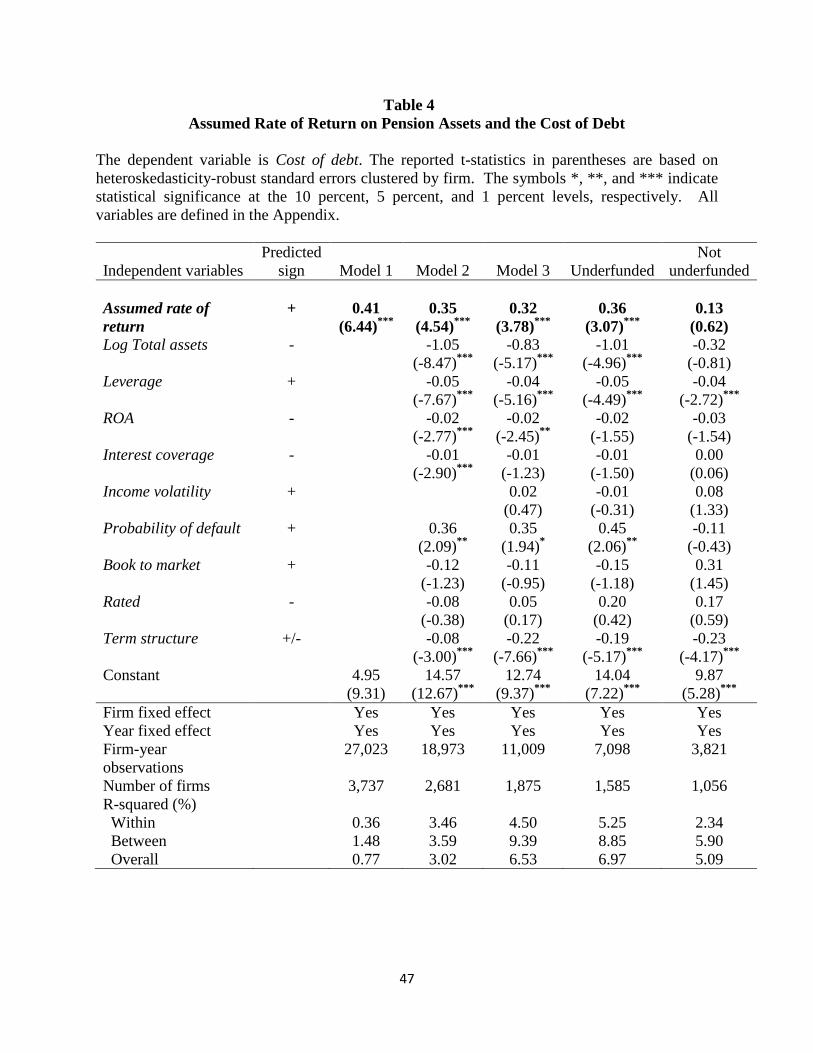

4.3. Assumed rate of return and the cost of debt

To test hypothesis H3 pertaining to the firm‟s cost of debt, we examine the following

regression specification:

𝐶𝑜𝑠𝑡 𝑜𝑓 𝑑𝑒𝑏𝑡𝑖 ,𝑡 =

∝ + 𝛽1 𝐴𝑠𝑠𝑢𝑚𝑒𝑑 𝑟𝑎𝑡𝑒 𝑜𝑓 𝑟𝑒𝑡𝑢𝑟𝑛 𝑖 ,𝑡 + 𝛽2 𝐿𝑜𝑔 𝑡𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠 𝑖 ,𝑡

+ 𝛽3 𝐿𝑒𝑣𝑒𝑟𝑎𝑔𝑒 𝑖,𝑡 + 𝛽4 𝑅𝑂𝐴 𝑖,𝑡 + 𝛽5 𝐼𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑐𝑜𝑣𝑒𝑟𝑎𝑔𝑒 𝑖 ,𝑡

+ 𝛽6 𝐼𝑛𝑐𝑜𝑚𝑒 𝑣𝑜𝑙𝑎𝑡𝑖𝑙𝑖𝑡𝑦 𝑖,𝑡 + 𝛽7 𝑃𝑟𝑜𝑏𝑎𝑏𝑖𝑙𝑖𝑡𝑦 𝑜𝑓 𝑑𝑒𝑓𝑎𝑢𝑙𝑡 𝑖 ,𝑡

+ 𝛽8 𝐵𝑜𝑜𝑘 𝑡𝑜 𝑚𝑎𝑟𝑘𝑒𝑡 𝑖,𝑡 + 𝛽9 𝑅𝑎𝑡𝑒𝑑 𝑖,𝑡 + 𝛽10 𝑇𝑒𝑟𝑚 𝑠𝑡𝑟𝑢𝑐𝑡𝑢𝑟𝑒 𝑖 ,𝑡

+ ∈𝑖 ,𝑡 (5)

Following Francis, LaFond, Olsson, and Schipper (2005), the dependent variable in the

regression is a measure of the aggregate amount of interest payments made by firms in a given

fiscal year. In section 4.8, we describe the robustness of our findings using the at-issue yield to

maturity for a sample of new debt issues as an alternative measure of the cost of debt. Following

prior research (e.g., Francis, et al., 2005), we include firm characteristics that are likely to affect

the firm‟s cost of debt. In addition, we control for the term structure of Treasury yields to

account for interest rate conditions in the market. These variables are defined in the Appendix.

Table 4 presents findings from the above regression specification. Based on hypothesis

H3, we expect the coefficient on Assumed rate of return to be positive. In Model 1 of Table 4,

23

We do not include the interest coverage ratio in this regression because interest coverage and firm profitability

(ROA) largely capture the same construct. We verify that the coefficient on the assumed rate of return is not

sensitive to the inclusion of interest coverage ratio. In addition, the coefficient on the assumed rate of return is

positive and significant even if ROA is replaced by interest coverage ratio in the regression. The results are also

similar to those reported when both ROA and interest coverage are excluded.

21

with only the fixed effects indicators included in the regression, the coefficient on Assumed rate

of return is 0.41 with a t-statistic of 6.44. In Model 2, controlling for other factors affecting the

cost of debt, the coefficient on Assumed rate of return is 0.35 with a t-statistic of 4.54, indicating

that the positive relation between the cost of debt and the assumed rate of return is highly

significant. The coefficient on the assumed rate of return in Model 3 (including income volatility

as an additional control variable) indicates that a one percent increase in the assumed rate of

return is associated with a 32 basis point increase in the cost of debt.

Given that the average cost of debt for the sample firms is 8.37 percent, a 32 basis point

increase in cost of debt represents a 3.82 percent increase at the mean. Moreover, comparing

Model 1 and Model 3, the goodness of fit in Model 1, with only the assumed rate of return as the

independent variable, is 0.77 percent whereas the corresponding number in Model 3 is 6.53,

suggesting that about 12 percent of the explanatory power in Model 3 is attributable to the

assumed rate of return.

The last two columns in Table 4 present results categorized by firm-years with

underfunded pension plans versus plans that are not underfunded. If pension plan returns reflect

the potential risk of future pension deficits, and hence, the possibility that future cash flow could

be channeled to cover such deficits, then the pension funding status should influence the relation

between assumed rate of return and the cost of debt. Consistent with this intuition, the results in

the last two columns indicate that the coefficient on the assumed rate of return is positive and

significant among firms with underfunded pension plans, but statistically insignificant among

firms whose plans are not underfunded. Thus, the statistically significant association between

the assumed rate of return and the cost of debt is driven primarily by the sub-sample of firms

where creditors are concerned about the funding status of the pension plans.

22

With the exception of leverage, the coefficients for control variables have the expected

signs and indicate that the cost of debt is declining in firm size, interest coverage and

profitability, and is lower for rated firms.24

Our findings imply that a one percent increase in the

assumed rate of return is associated with a 32 basis point increase in the cost of debt. In dollar

terms, a one percent increase in the assumed rate of return implies an increase of $6.78 million in

income (1 percent X mean pension assets of $677.65 million). In comparison, a 32 basis point

increase in the cost of debt translates into an increase of $12.70 million in debt payments.25

Thus, for every dollar increase in net income attributable to a percent increase in the assumed

rate of return, the firm incurs a $1.87 increase in debt payments ($12.70 million / $6.78 million).

These findings suggest that by reporting higher assumed rates of return, firms incur an

economically significant indirect cost in the form of a higher cost of debt.

4.4. Does the actual return on pension assets matter for the cost of debt?

Although the assumed rate of return reflects information about the firm‟s expectations of

the long-term rate of return on pension assets, and hence, the perceived level of risk associated

with pension assets (Amir and Benartzi, 1998; Bergstresser, Desai and Rauh, 2006), it does not

reflect the actual performance of pension assets. An alternative measure of pension plan returns

that is more representative of the true performance of the pension assets is the actual return on

24

The negative coefficient on leverage is due to a mechanical relation between the definitions of cost of debt

(interest cost divided by average total debt) and leverage (total debt divided by assets). The result is similar when

we use market leverage instead of book leverage. In addition, we find similar results if leverage is defined by

including pension liabilities and assets, as in Shivdasani and Stefanescu (2009). Moreover, the reported negative

relation between leverage and cost of debt is similar to that reported by Francis et al. (2005). However, excluding

leverage from the regression does not alter our conclusions. In addition, we show later in the analyses of new debt

issues, that the coefficient on leverage is positive and highly significant in regressions with at-issue yield to maturity

as the dependent variable. Thus, our conclusions are unaffected by the definition of cost of debt or leverage.

25

The average total debt (short-term plus long-term debt) for our sample is $3,969.55 million. Hence, a 32 basis

point increase in the cost of debt translates into additional debt payments of $12.70 million (0.32% X 3,969.55

million).

23

pension assets. In this section, we examine the relative importance of the assumed rate of return

and the actual return on pension assets for the firm‟s cost of debt.

4.4.1. Actual return on pension assets and the cost of debt: Hypotheses

The relation between the actual returns on pension assets and the firm‟s cost of debt is

ambiguous for several reasons. On the one hand, actual returns on pension assets affect pension

funding levels by either enhancing or eroding the value of pension assets. As such, actual returns

could influence the expected level of cash required for future contributions to the pension plan as

firms are required to make additional contributions depending on the extent to which the plans

are underfunded.26

Prior research suggests that creditors may incorporate pension accounting

footnote information into their assessments of the firm‟s credit worthiness (Martin and

Henderson, 1983; Maher, 1987; Carroll and Niehaus, 1998). In addition, Jin, Merton, and Bodie

(2006) find that equity risk (measured by the CAPM beta) reflects the risk of the firm‟s pension

plans, despite the practical difficulties of deciphering corporate pension accounts.

Furthermore, advocates of fair value accounting standards often argue that the actual

return on pension assets is less affected by earnings management, and hence, should be more

informative. For instance, prominent analysts, investors, and lawmakers have argued in favor of

the use of the actual return rather than the assumed rate of return in their push for greater

transparency in firms‟ pension disclosures (e.g., Loomis, 2001; UBS, 2003; Barlas, 2005;

PAAinE, 2008). These arguments suggest that all else equal, higher actual returns may be

relevant for bond investors and could be viewed favorably by bond market participants because

higher actual returns reduce the extent of pension plan underfunding; alternately, if higher actual

26

Goldman Sachs estimates that companies will be forced to boost their pension contributions to $40 billion in

2009, from about $18 billion in 2008 as a result of decimated stock prices during the recent credit crisis.

24

returns reflect the riskiness of pension plans, debt holders may view high actual returns

adversely.

On the other hand, advocates of SFAS 87 or IAS 19 (favoring the use of the assumed rate

of return) argue that the actual return on pension assets reflects transitory gains and losses, and

hence adds to the volatility of pension costs and the firm‟s reported earnings27

. Recent empirical

evidence suggests that fair value pension accounting (including the use of the actual return on

pension assets) impairs the relevance of financial statements to the market‟s assessment of firms‟

credit risk (Hann, Heflin, and Subramanyam, 2007). Furthermore, the evidence in some studies

suggests that market participants do not appear to incorporate pension accounting footnote

information into earnings forecasts and equity prices (e.g., Coronado and Sharpe, 2003; Picconi,

2006; Franzoni and Marin, 2006). Moreover, even if market participants pay attention to such

information, the actual return on pension assets may simply be less informative about the risk

and return of pension assets as it is subject to fluctuations in capital markets that are beyond the

control of the firm. Thus, the actual rate of return may be unrelated to the cost of debt.

Collectively, the above arguments suggest that the relation between the firm‟s cost of

debt and the actual return on pension assets is an empirical issue that can shed light on whether

investors in the bond market assign more weight to information that reflects actual pension plan

returns or to information that reflects expected long-term pension plan returns.

4.4.2. Actual return on pension assets and the cost of debt: Empirical results

The results of regressions explaining the cost of debt are presented in Table 5. The key

independent variables of interest are the lagged actual return (scaled by lagged pension assets)

27

SFAS 87 permits an additional smoothing mechanism by which the expected rate of return may be multiplied by

either the fair value of plan assets or by a „smoothed fair value‟, i.e. a moving average of the fair values of pension

assets.

25

and the assumed rate of return on pension assets. In Model 1 of Table 5, the results indicate a

positive and significant coefficient (t-statistic of 3.76) on Lagged actual return. Controlling for

other factors affecting the cost of debt, in Model 2 and Model 3, we find that while Assumed rate

of return has positive and significant coefficients, the coefficient on Lagged actual return is

insignificant in Model 2 and significant in Model 3.

Notably, we find a sharp contrast in the magnitude of the coefficients on the assumed rate

of return versus those on the actual return. For instance, in Models 2 and 3, the coefficients on

Assumed rate of return are 0.36, whereas the coefficients on Lagged actual return are 0.005 and

0.007 respectively.28

These coefficients on the actual return imply that every one percent higher

actual return reported by firms is associated with a 0.7 basis point increase in the cost of debt; in

comparison, in the same model (Model 3), the coefficient on the assumed rate of return implies

that the impact of one percent increase in the assumed rate on the cost of debt is 36 basis points.

The last two columns present the regression results for sub-samples categorized by the

funding status of pension plans. Consistent with the results for the full sample, the coefficient on

the assumed rate of return is positive and significant in the sub-sample of firms with underfunded

pension plans. In contrast, the coefficient on the actual return is insignificant for firms with

underfunded plans, but positive and significant for firms whose plans are not underfunded.

These findings suggest that the empirical relation between the firm‟s cost of debt and the

actual return appears to be weak, and importantly, the economic significance of this relation is

very small. Thus, our results do not support the hypothesis that the actual return on pension

assets affects the cost of debt. Rather, the findings are consistent with the evidence in Hann, et

28

If the lagged actual return is replaced with the contemporaneous actual return on pension assets, the coefficient on

actual return is statistically insignificant in all the models (Model 1, Model 2 and Model 3). However, the

coefficient on the assumed rate of return in Model 2 and Model 3, with the inclusion of the contemporaneous actual

return, continues to be statistically significant and is stable with values of 0.34 and 0.35 respectively.

26

al. (2007) that fair value pension accounting information (including actual return on pension

assets) impairs the relevance of financial statement information for credit markets.

These findings have implications for accounting standard setters contemplating the pros

and cons of having firms disclose a smoothed measure of pension plan performance versus a

measure that more closely represents the true economic value of pension assets. Our findings

suggest that the debt market appears to incorporate information in the smoothed measure of

pension plan performance rather than the actual return on pension assets.29

4.5. Change in variables specification

Given that the assumed rate of return is at the discretion of managers, it is arguably a

choice that is likely to be endogenously determined. In this section, following the suggestion in

Weber (2006), we attempt to address this concern by estimating the cost of debt regression using

a change in variables specification. Thus, we examine the following regression specification:

∆𝐶𝑜𝑠𝑡 𝑜𝑓 𝑑𝑒𝑏𝑡𝑖 ,𝑡 =

∝ + 𝛽1 ∆𝐴𝑠𝑠𝑢𝑚𝑒𝑑 𝑟𝑎𝑡𝑒 𝑜𝑓 𝑟𝑒𝑡𝑢𝑟𝑛 𝑖,𝑡 + 𝛽2 ∆𝐿𝑜𝑔 𝑡𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠 𝑖 ,𝑡

+ 𝛽3 ∆𝐿𝑒𝑣𝑒𝑟𝑎𝑔𝑒 𝑖 ,𝑡 + 𝛽4 ∆𝑅𝑂𝐴 𝑖,𝑡 + 𝛽5 ∆𝐼𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑐𝑜𝑣𝑒𝑟𝑎𝑔𝑒 𝑖,𝑡

+ 𝛽6 ∆𝐼𝑛𝑐𝑜𝑚𝑒 𝑣𝑜𝑙𝑎𝑡𝑖𝑙𝑖𝑡𝑦 𝑖,𝑡 + 𝛽7 ∆𝑃𝑟𝑜𝑏𝑎𝑏𝑖𝑙𝑖𝑡𝑦 𝑜𝑓 𝑑𝑒𝑓𝑎𝑢𝑙𝑡 𝑖,𝑡

+ 𝛽8 ∆𝐵𝑜𝑜𝑘 𝑡𝑜 𝑚𝑎𝑟𝑘𝑒𝑡 𝑖 ,𝑡 + 𝛽9 ∆𝑅𝑎𝑡𝑒𝑑 𝑖,𝑡 + 𝛽10 ∆𝑇𝑒𝑟𝑚 𝑠𝑡𝑟𝑢𝑐𝑡𝑢𝑟𝑒 𝑖 ,𝑡

+ ∈𝑖 ,𝑡 (6)

29

As an additional robustness check, we define an indicator variable which takes the value of one if the lagged

actual return on pension assets is either in the lowest quartile or the highest quartile. The lowest quartile of actual

returns captures the risks of pension deficits arising from lower values of pension assets, whereas the highest

quartile of actual returns captures the riskiness of pension plan investments. As both these factors adversely affect

credit risk, we expect the coefficient on this indicator variable to be positive in a regression with cost of debt as the

dependent variable. However, we find that the coefficient of this indicator variable is statistically insignificant.

27

The variables used in the above regression are as defined in the Appendix, in first-

differenced form. The results, presented in Table 6, indicate that 𝛽1 is 0.19 with a t-statistic of

2.31. Furthermore, the results in the last two columns indicate that 𝛽1 is positive and significant

for firms with underfunded pension plans, but not for other firms. This finding is consistent with

the earlier results using variable levels. Overall, the results using the change specification

suggest that the relation between cost of debt and the assumed rate of return is robust with

respect to the potential endogeneity of the assumed rate of return.

4.6. Assumed rate of return and the cost of debt: Evidence on new debt issues

The above results are based on a pooled sample of observations where the cost of debt is

measured as the interest expense during the year (scaled by the average total debt during the

current year and the prior year). In this section, we examine the relation between the assumed

rate of return and the cost of debt using a sample of new debt issues. We obtain a sample of new

debt issues by publicly listed firms between 1990 and 2007 from the Securities Data Corporation

(SDC) database. This database contains data on the characteristics of the new issue, such as

maturity, issue size, offer yield to maturity, and other relevant information.

We exclude observations where the maturity date is incorrectly recorded as appearing

before the issue announcement date; if the contemporaneous yield on the Treasury security is

recorded as negative or the offer yield to maturity for the issuer is recorded as being less than the

corresponding maturity Treasury security; or if the issue proceeds information is missing or

recorded as zero. Furthermore, we retain only the largest issue by an issuer in a given year. We

merge this data with Compustat and retain observations with data available for the fiscal year

preceding the issue. Finally, we merge the data with our full sample of firms with defined

28

benefit pension plans because our objective is to examine the relation between the issuing firm‟s

offer yield to maturity and the assumed rate of return on its pension assets. The final sample of

new debt issues by firms with defined benefit pension plans comprises of 2,120 debt issues. The

sample size varies for the regressions, depending on the availability of data on the issuers.

Following prior studies, we measure the cost of debt as the yield to maturity offered by

the issuing firm at the announcement of the new debt issue (see, e.g., Sengupta, 1998; Shi, 2003;

Jiang, 2008).30

While the cost of debt measured using interest expense (as is the case above, for

the full sample and for the S&P sample) is a proxy for the aggregate amount of debt payments

during the year (assuming that debt repayments and issuance offset each other during the year),

the yield to maturity for new debt issues represents the incremental cost of debt required by

investors for the marginal amount borrowed by the firm. Thus, in any given year, the yield to

maturity captures the actual rate of return required by creditors at the time of issuance.

Following prior research (e.g., Khurana and Raman, 2003; Klock, Mansi, and Maxwell,

2005; Ortiz-Molina, 2006), the regression specification includes variables that control for both

firm characteristics as well as issue characteristics. The firm characteristics, including the

assumed rate of return, are measured as of the fiscal year-end immediately preceding the debt

issue announcement. As the dependent and independent variables can persist over time for a

given firm, and because variables such as the cost of debt could be correlated across firms in a

given year, we include firm and year fixed effects to account for the correlations among these

variables. The regression model is as follows:

30

While our regression specification controls for the corresponding maturity Treasury yield at the announcement,

we verify the robustness of our inferences using the yield spread (difference between the offer yield and the

Treasury yield) at the announcement as an alternative measure of the cost of debt. Prior studies that use the yield

spread as a measure of cost of debt include Bhojraj and Sengupta (2003), Khurana and Raman (2003), Anderson,

Mansi, and Reeb (2004), Klock, Mansi, and Maxwell (2005), and Ortiz-Molina (2006), among others. The

regression with yield spread as the dependent variable indicates that the coefficient of assumed rate of return is

positive (0.23) and highly significant (t-statistic of 4.06) in a specification with other control variables as in Model 3

of Table 7.

29

𝑂𝑓𝑓𝑒𝑟 𝑦𝑖𝑒𝑙𝑑 𝑡𝑜 𝑚𝑎𝑡𝑢𝑟𝑖𝑡𝑦𝑖 =

∝ + 𝛽1 𝐴𝑠𝑠𝑢𝑚𝑒𝑑 𝑟𝑎𝑡𝑒 𝑜𝑓 𝑟𝑒𝑡𝑢𝑟𝑛 𝑖 + 𝛽2 𝑇𝑟𝑒𝑎𝑠𝑢𝑟𝑦 𝑌𝑇𝑀 𝑖

+ 𝛽3 𝐿𝑜𝑔 𝑡𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠 𝑖 + 𝛽4 𝐿𝑒𝑣𝑒𝑟𝑎𝑔𝑒 𝑖 + 𝛽5 𝑅𝑂𝐴 𝑖

+ 𝛽6 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡 𝑔𝑟𝑎𝑑𝑒 𝑖 + 𝛽7 𝐵𝑜𝑜𝑘 𝑡𝑜 𝑚𝑎𝑟𝑘𝑒𝑡 𝑖

+ 𝛽8 𝐶𝑎𝑙𝑙 𝑝𝑟𝑜𝑡𝑒𝑐𝑡𝑖𝑜𝑛 𝑦𝑒𝑎𝑟𝑠 𝑖 + 𝛽9 𝑀𝑎𝑡𝑢𝑟𝑖𝑡𝑦 𝑖 + 𝛽10 𝐼𝑠𝑠𝑢𝑒 𝑠𝑖𝑧𝑒 𝑖

+ 𝛽11 𝑆𝑢𝑏𝑜𝑟𝑑𝑖𝑛𝑎𝑡𝑒𝑑 𝑖 + 𝛽12 𝐷𝑖𝑠𝑡𝑎𝑛𝑐𝑒 𝑡𝑜 𝑑𝑒𝑓𝑎𝑢𝑙𝑡 𝑖 + 𝛽13 𝐵𝑒𝑡𝑎 𝑖

+ 𝛽14 𝐼𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑐𝑜𝑣𝑒𝑟𝑎𝑔𝑒 𝑖 + 𝛽15 𝐼𝑛𝑐𝑜𝑚𝑒 𝑣𝑜𝑙𝑎𝑡𝑖𝑙𝑖𝑡𝑦 𝑖 + ∈𝑖 (7)

Findings from the above regression are presented in Table 7. In model 1, 𝛽1 is 0.45 with

a t-statistic of 5.64. In Model 2 of Table7, without including interest coverage and income

volatility, the value of 𝛽1 is 0.13 with a t-statistic of 3.40. In Model 3, including all control

variables, the value of 𝛽1 is 0.28, which is similar to the coefficient of 0.32 for Assumed rate of

return in Table 4 for the full sample. This result indicates that investors in the bond market

require a 28 basis point yield premium for every one percent higher assumed rate of return

reported by the issuing firms. This incremental impact of the assumed rate of return on the offer

yield to maturity represents about 4 percent of the average yield to maturity (6.80 percent)

offered by the issuing firms in the sample.

The results in the last two columns indicate that investors require a premium from issuers

for the higher assumed rate of return on pension assets, regardless of the funding status of their

pension plans. The coefficients on the assumed rate of return in these sub-samples are fairly

similar to each other. Overall, the results from the new debt issues sample are consistent with

those obtained using the full pooled sample of observations, suggesting that the relation between

the assumed rate of return and the firm‟s cost of debt is robust with respect to the specification

used to examine the hypothesis.

30

4.7. Robustness: Controlling for corporate governance and earnings management

Prior research suggests that firms with poor quality earnings are associated with a higher

cost of debt (e.g., Ashbaugh-Skaife, Collins, and LaFond, 2006; Francis, LaFond, Olsson, and

Schipper, 2005). Likewise, studies also find that firms with weak governance are associated

with higher debt financing costs (e.g., Sengupta, 1998; Bhojraj and Sengupta, 2003; Anderson,

Mansi, and Reeb, 2004; Ashbaugh-Skaife, Collins, and LaFond, 2006). In the context of our

study, if firms with weak governance and poor quality accruals are associated with higher

assumed rates of return (as shown by Bergstresser, Desai, and Rauh, 2006), the relation between

assumed rates of return and the firm‟s cost of debt may be spuriously driven by the exclusion of

these potentially correlated variables.

Thus, we examine the robustness of the relation between cost of debt and the assumed

rate of return by including variables representing governance characteristics. In particular, we

include key board characteristics such as board size, CEO duality, proportion of independent

board members, and the equity holdings of officers and directors in the company. The regression

specification is as follows.

𝐶𝑜𝑠𝑡 𝑜𝑓 𝑑𝑒𝑏𝑡𝑖,𝑡 =

∝ + 𝛽1 𝐴𝑠𝑠𝑢𝑚𝑒𝑑 𝑟𝑎𝑡𝑒 𝑜𝑓 𝑟𝑒𝑡𝑢𝑟𝑛 𝑖 ,𝑡 + 𝛽2 𝐿𝑎𝑔𝑔𝑒𝑑 𝑎𝑐𝑡𝑢𝑎𝑙 𝑟𝑒𝑡𝑢𝑟𝑛 𝑖,𝑡

+ 𝛽3 𝐿𝑜𝑔 𝑡𝑜𝑡𝑎𝑙 𝑎𝑠𝑠𝑒𝑡𝑠 𝑖 ,𝑡 + 𝛽4 𝐿𝑒𝑣𝑒𝑟𝑎𝑔𝑒 𝑖,𝑡 + 𝛽5 𝑅𝑂𝐴 𝑖,𝑡

+ 𝛽6 𝐼𝑛𝑡𝑒𝑟𝑒𝑠𝑡 𝑐𝑜𝑣𝑒𝑟𝑎𝑔𝑒 𝑖,𝑡 + 𝛽7 𝐼𝑛𝑐𝑜𝑚𝑒 𝑣𝑜𝑙𝑎𝑡𝑖𝑙𝑖𝑡𝑦 𝑖 ,𝑡 + 𝛽8 𝑅𝑎𝑡𝑒𝑑 𝑖,𝑡

+ 𝛽9 𝑇𝑒𝑟𝑚 𝑠𝑡𝑟𝑢𝑐𝑡𝑢𝑟𝑒 𝑖 ,𝑡 + 𝛽10 𝐴𝑐𝑐𝑜𝑢𝑛𝑡𝑖𝑛𝑔 𝑞𝑢𝑎𝑙𝑖𝑡𝑦 𝑖,𝑡

+ 𝛽11 𝐿𝑜𝑔 𝑏𝑜𝑎𝑟𝑑 𝑠𝑖𝑧𝑒 𝑖 ,𝑡 + 𝛽12 𝑃𝑟𝑜𝑝𝑜𝑟𝑡𝑖𝑜𝑛 𝑖𝑛𝑑𝑒𝑝𝑒𝑛𝑑𝑒𝑛𝑡 𝑖 ,𝑡

+ 𝛽13 𝐷𝑖𝑟 𝑎𝑛𝑑 𝑂𝑓𝑓 𝑜𝑙𝑑𝑖𝑛𝑔𝑠 𝑖 ,𝑡 + 𝛽14 𝐶𝐸𝑂 𝑛𝑜𝑡 𝐶𝑂𝐵 𝑖,𝑡 + ∈𝑖 ,𝑡 (8)

31

We measure Accounting quality as the standard deviation of unexpected accruals, as in

Francis, et al., 2005.31

The inclusion of board characteristics reduces the sample size

substantially. The results, presented in Table 8, indicate that the value of 𝛽1 is positive and

significant in all three models. Moreover, the coefficient on the actual return on pension assets is

statistically insignificant. Among the governance related control variables, the variable

representing CEO duality (equals one if the CEO is not also the chairman of the board) is

significant, indicating that firms with separate CEOs and board chairmen are associated with

lower debt financing costs.

Although the coefficient of Accounting quality is positive, it is statistically insignificant

in Table 8. However, as discussed below, we include this variable in alternate specifications and

find that its coefficient is positive and highly significant, consistent with the findings in Francis,

et al. (2005).32

Overall, the results in this section suggest that the relation between assumed rate

of return on pension assets and the firm‟s cost of debt is robust with respect to the inclusion of

corporate governance and earnings quality variables.

31

We follow the regression approach outlined in Francis, et al. (2005, equation (1)) to construct a measure of

accruals quality. This measure of accruals quality builds on the approach in Dechow and Dichev (2002) as modified

by McNichols (2002). Specifically, in the first step, for each year, using all firms in a given 2-digit SIC code

industry, the dependent variable in the regression is total current accruals, and the independent variables are the one-

year lagged, contemporaneous and the next year‟s cash flow from operations, the change in revenues, and the gross

value of property, plant, and equipment. Thus, we obtain firm-year residuals of total current accruals. In the next

step, for each firm in each year t, we compute the standard deviation of the firm-year residuals for the years t-4

through t and use this estimate as the measure of accounting quality. Thus, larger standard deviations of residuals

are indicators of poorer accruals quality.

32

In our sample, the mean value of Accounting quality is 0.0389, which is slightly lower than the overall average for

Compustat firms, mainly because our sample of firms with defined benefit pension plans are larger than the average

firm in Compustat, as shown in Panel B and Panel C of Table 1. The lower value for Accounting quality in our

sample reflects the inverse relation between firm size and earnings quality reported in the literature (e.g., Francis, et

al., 2005).

32

4.8. Robustness: Alternative regression specifications

The results reported above are based on pooled regressions. To the extent that the

dependent and independent variables in this study (e.g., cost of debt and assumed rate of return)

persist over time for a given firm, Petersen (2009) recommends the firm fixed effects approach to

account for the correlation between observations on the same firm in different years. However,

if the correlations exist across observations on different firms in the same year, Petersen (2009)

suggests that the Fama and Macbeth (1973) approach is better suited to minimize the bias in the

estimates and in the significance levels.

In this section, we examine the relation between the cost of debt and the assumed rate of

return using two alternative specifications: (1) a cross-sectional regression specification; and (2)

a Fama-Macbeth regression specification. The cross-sectional specification involves the use of

firm-specific time-series means, and thereby captures differences across firms. The Fama-

Macbeth regression entails the estimation of regression coefficients each year (from 1991 to

2006 in our sample) and then averaging the coefficients. The standard deviation of the yearly

coefficients is used to determine the significance level.

In Table 9, the results indicate that the coefficient of the assumed rate of return is positive

and highly significant in all three models presented. As income volatility is measured using a

minimum of five years of data, the number of observations is lower when this variable is

included in the regression. The control variables are largely consistent with expectations. In

particular, we find that the coefficient of Accounting quality is positive and significant in all

three models. Overall, the results in this section affirm our earlier findings and suggest that the

positive relation between the cost of debt and the assumed rate of return on pension assets is

robust with respect to the regression specification used to examine the relation.

33

5. Conclusions

Assets held in defined benefit pension plans are the single largest off-balance sheet item

at U.S. corporations, amounting to approximately 14 percent of the firm‟s assets on average. In

this paper we use a comprehensive sample of firms with defined benefit pension plans to

examine the extent to which debt investors see through the accounting veil, such that a firm‟s

cost of debt reflects the risk exposure of its pension assets.

Our findings indicate a positive relation between the assumed rate of return on pension

assets and the firm‟s cost of debt. This finding is robust across different specifications, is both

statistically and economically significant, and is stronger for firms with underfunded pension

plans. We find that a one percent increase in the assumed rate of return is associated with a 32

basis point increase in the firm‟s cost of debt. In contrast, the relation between actual return and

the cost of debt is weak and is not economically significant, confirming that debt holders do not

regard year to year volatility in actual returns from pension asset investments to be informative

about the longer-term prospects of the firm.

We also find positive and statistically significant relations between the assumed rate of

return and (i) the uncertainty of expected cash flows and (ii) the level of a firm‟s default risk.

Debt holders appear to understand that higher assumed returns on pension assets are likely to

reflect higher portfolio risk, with associated negative implications for the likelihood that pension

shortfalls would divert operating cash flows away from the firm‟s creditors. These results are

supportive of the informational efficiency of the market for corporate debt, and suggest that

using an assumed rate of return to determine pension returns and costs (SFAS 87) does not

mislead corporate debt holders.

34

Our findings highlight an economic consequence of off-balance-sheet activities. It has

been documented in the literature (Bergstresser, Desai, and Rauh, 2006) that firms use discretion

over the assumed rate of return on pension assets to opportunistically manage earnings,

particularly in time periods preceding acquisitions and when they are close to critical earnings

thresholds. We find that this form of opportunism comes at a significant cost, in that a one dollar

increase in reported income resulting from a higher assumed rate of return on pension assets

results in a $1.87 increase in debt payments.

35

Appendix

Variable definitions

Accounting quality standard deviation of accruals; defined in more detail in Section 4.7.

Assumed rate of return (%) data336

Beta slope estimate in the regression of daily stock return on the daily

CRSP value-weighted index return during the 240 days ending on

the fiscal year-end date.

Book to market data60/(data199*data54)

Book to market (data60/data199*data54)

Call protection years number of years of call protection / number of years to maturity

CEO not COB equals 1 if CEO is not the board chairman; and 0 otherwise. (as

reported by IRRC)

Cost of debt (%) data15/average total debt, where total debt = data9 + data34, and

average total debt is the average of total debt in the current year and

the prior year.

Dir and Off holdings percentage of shares owned by the officers and directors of the

company (as reported by IRRC)

Distance to default, 𝐷𝐷𝑡 computed as in equation (3); where, 𝑉𝑎 ,𝑡 equals

(data199*data54)+data6-data60; 𝑋𝑡 equals [data34 + (0.5*data9)];

𝜇 equals stock return during the 240 days ending on the fiscal year-

end date; 𝜎𝑎2 is the daily stock return variance, annualized using 240

days ending on the fiscal year-end date; T equals 5 years;

Income volatility (%) (standard deviation of data18 / average of data6) during years -9,0,

where year 0 is a given fiscal year. We require a minimum of 5

observations to compute income volatility.

Interest coverage data13/data15

Investment grade equals 1 if data280 is less than or equal to 9;

equals 0 if data 280 is greater than 9.

Issue size natural logarithm of issue proceeds

Lagged actual return actual return on pension assets in year t-1.

Leverage (%) (data9+data34)/data6

Log board size natural logarithm of board size (as reported by IRRC)

Log total assets natural logarithm of total assets

Maturity number of years to maturity

Offer yield to maturity yield to maturity on the new debt issue at the time of issuance, as

reported by SDC

Pension assets ($millions) prior to and including fiscal year 1997: Equals data 296 if data 287 is

missing; equals data287 if data296 is missing.

after and excluding fiscal year 1997: equals data287.

Probability of default computed as in equation (4): 𝜑 −𝐷𝐷𝑡 , where 𝜑() is the cumulative

normal distribution function.

Proportion independent number of board members classified as independent divided by

board size, (as reported by IRRC).

36

Appendix (continued)

Rated equals 1 if data280 is not missing; otherwise equals 0.

Relative pension asset size (%) equals Pension assets / data6.

ROA (%) data172/data6

Standard deviation of returns standard deviation of daily stock returns during the period (-240,0),

where day 0 represents the fiscal year-end date.

Subordinated equals 1 if the new debt issue is subordinated; 0 otherwise.

Term structure (%) 10-year Treasury yield minus 6-month Treasury yield, both

measured at fiscal year-end.

Total assets ($millions) data 6

Treasury YTM yield to maturity on a Treasury security having the same maturity as

the new debt issue at the time of issuance, as reported by SDC

Underfunded A pension plan is defined as underfunded if Pension assets is less

than Projected benefit obligation; Projected benefit obligation equals

(data286+data294) for fiscal years prior to and including 1997; and

equals data286 after and excluding fiscal year 1997.

37

References

Amir, Eli, and Shlomo Benartzi, 1998, The Expected Rate of Return on Pension Funds and Asset