marianne kah conocophillips chief economist i bohai phase ii yuzhno khylchuyu libya suban ii...

TRANSCRIPT

2/27/06 – Slide 1

Marianne KahConocoPhillips Chief Economist

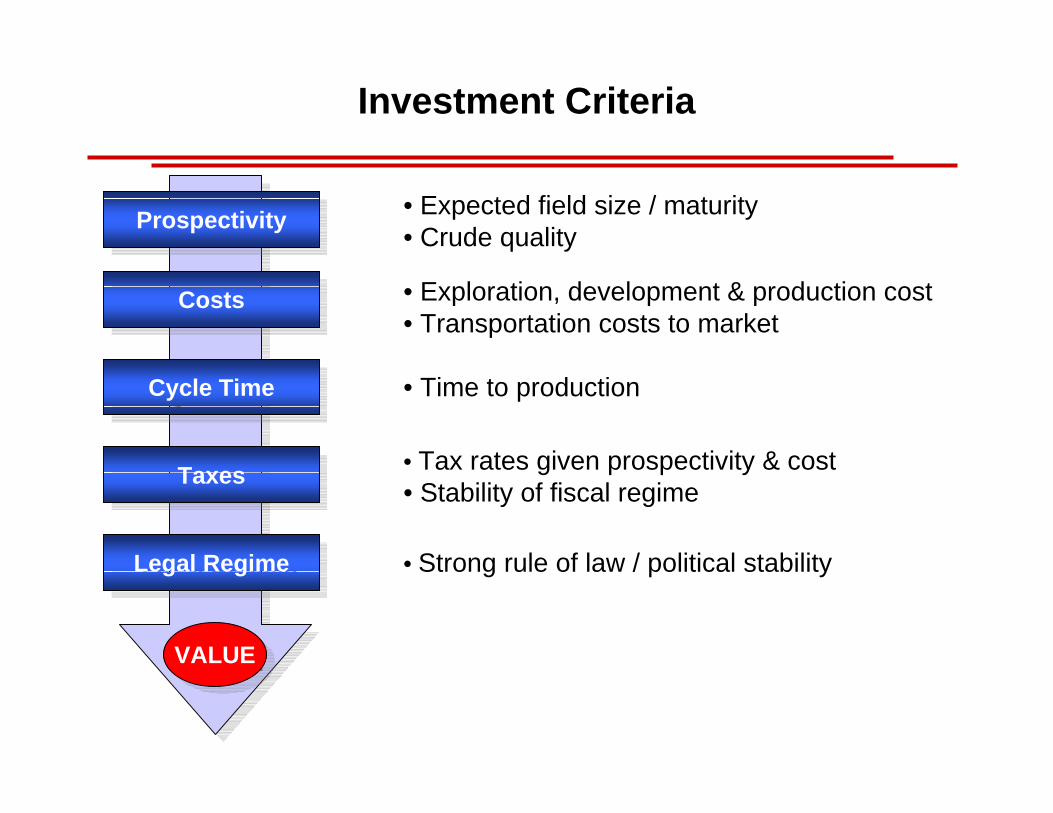

Investment Criteria

ProspectivityProspectivity • Expected field size / maturity• Crude quality

• Exploration, development & production cost• Transportation costs to market

• Tax rates given prospectivity & cost• Stability of fiscal regime

• Strong rule of law / political stability

CostsCosts

TaxesTaxes

Legal RegimeLegal Regime

Cycle TimeCycle Time • Time to production

VALUEVALUE

• Small expected field size• Lower value heavy & high sulfur crude

Investment Criteria - Alaska Rating

• High explor., develop. & production cost• High transportation costs to market

• High tax rates given prospectivity & cost• Recent concern about stability of fiscal regime

• Strong rule of law / political stability• Concern about changing tax rate withoutgrandfathering recent investment

ProspectivityProspectivity

CostsCosts

TaxesTaxes

Legal RegimeLegal Regime

Cycle TimeCycle Time

VALUEVALUE

• Long lead times

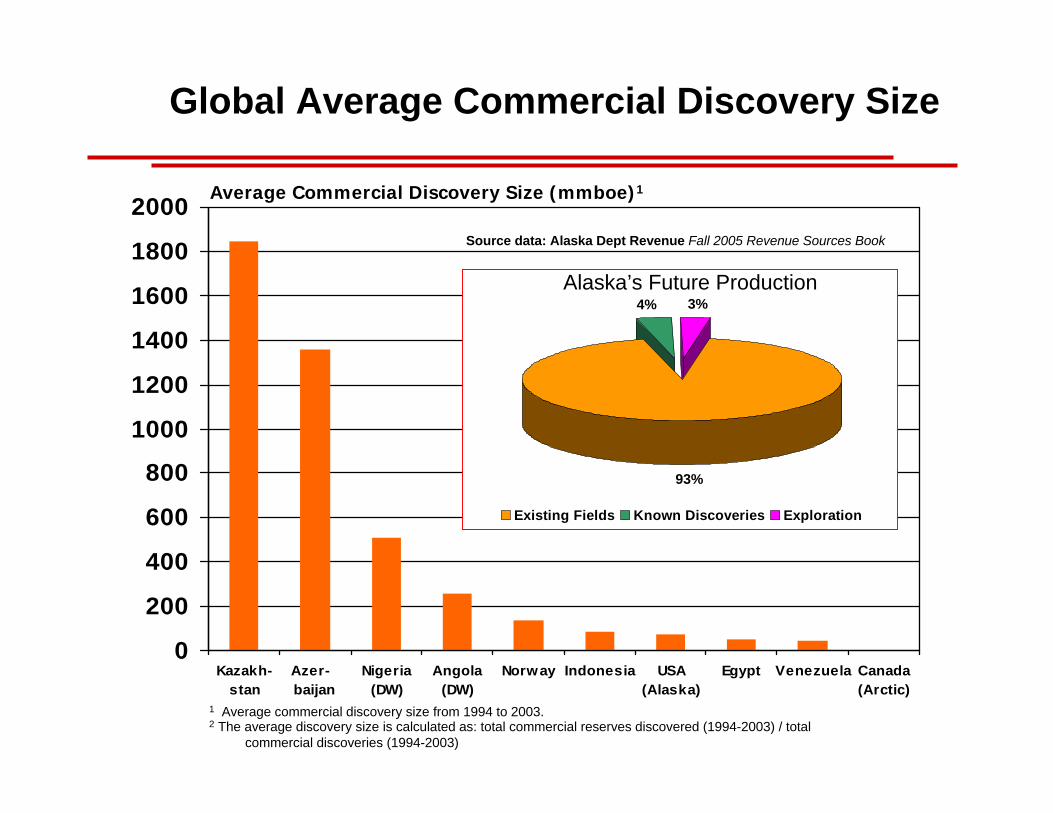

Global Average Commercial Discovery Size

1 Average commercial discovery size from 1994 to 2003.2 The average discovery size is calculated as: total commercial reserves discovered (1994-2003) / total

commercial discoveries (1994-2003)

Average Commercial Discovery Size (mmboe)1

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Kazakh-stan

Azer- baijan

Nigeria(DW)

Angola(DW)

Norway Indonesia USA(Alaska)

Egypt Venezuela Canada(Arctic)

93%

4% 3%

Existing Fields Known Discoveries Exploration

Source data: Alaska Dept Revenue Fall 2005 Revenue Sources Book

Alaska’s Future Production

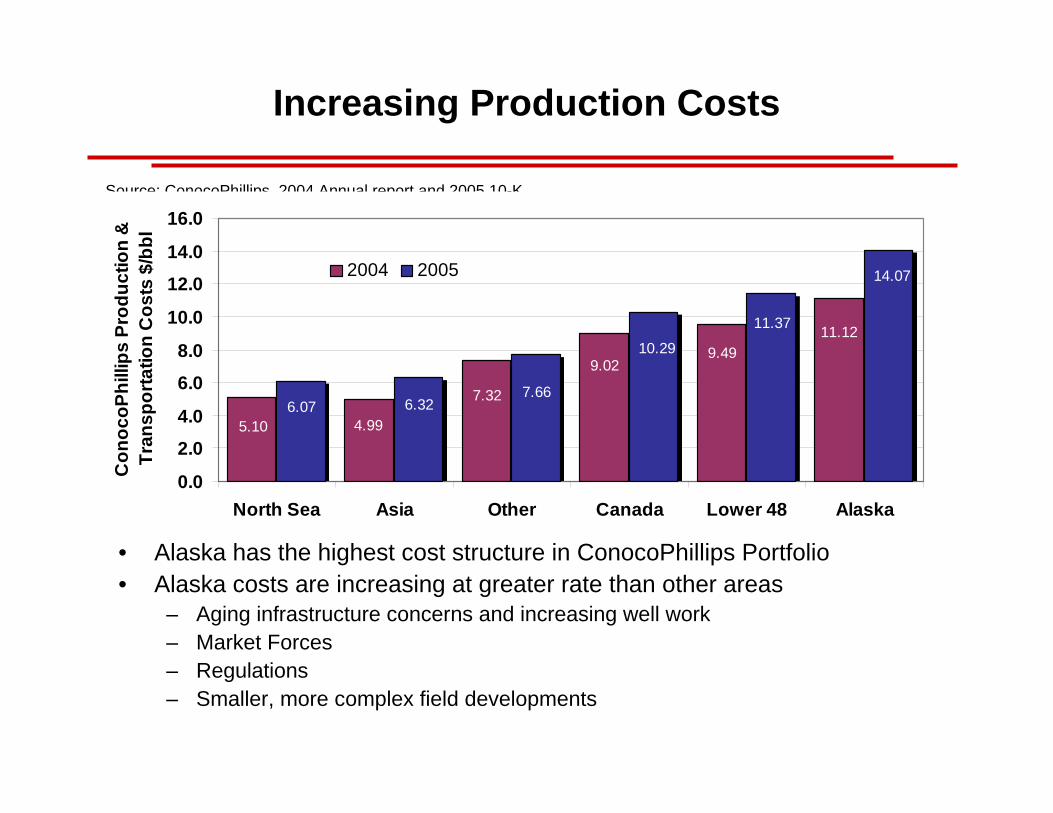

Increasing Production Costs

• Alaska has the highest cost structure in ConocoPhillips Portfolio• Alaska costs are increasing at greater rate than other areas

– Aging infrastructure concerns and increasing well work– Market Forces– Regulations– Smaller, more complex field developments

Source: ConocoPhillips 2004 Annual report and 2005 10-K

11.129.49

7.32

4.99

9.02

5.10

14.07

11.37

10.29

7.666.326.07

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

North Sea Asia Other Canada Lower 48 Alaska

Con

ocoP

hilli

ps P

rodu

ctio

n &

Tr

ansp

orta

tion

Cos

ts $

/bbl

2004 2005

Argentina

Australia (offshore)

Bangladesh

Bolivia

Canada (East Coast)

Italy

Malaysia-Thailand JDA

Netherlands (offshore)Netherlands (onshore)

New Zealand

Peru

UK (shelf)UK (Southern Gas Basin)

USA (GoM deepwater)

Trinidad & TobagoAngola (shelf)

Brazil (shelf)

Canada (Arctic)

Denmark

Ecuador

Egypt

GabonNigeria (deepwater)

Alaska ELF

Nigeria (shelf)

Norway

Oman

QatarSyria Yemen

30%

40%

50%

60%

70%

80%

90%

100%

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0

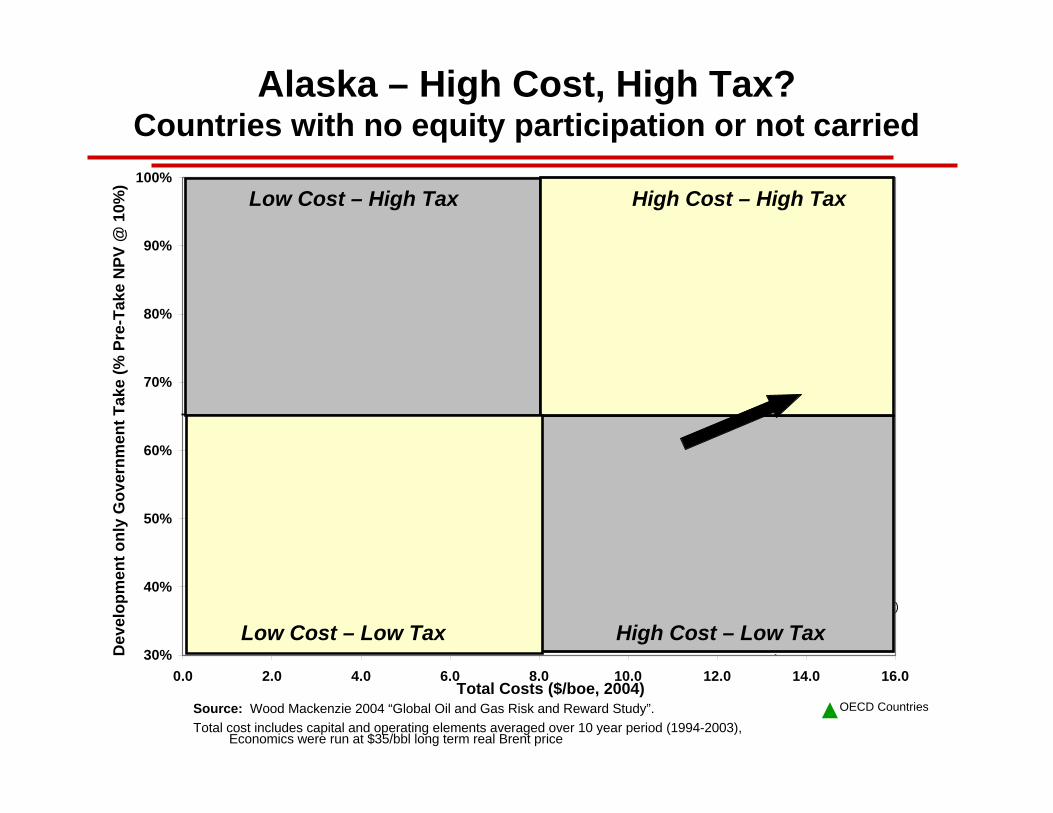

Alaska – High Cost, High Tax?Countries with no equity participation or not carried

Source: Wood Mackenzie 2004 “Global Oil and Gas Risk and Reward Study”.Total cost includes capital and operating elements averaged over 10 year period (1994-2003),

Economics were run at $35/bbl long term real Brent price

High Cost – High TaxLow Cost – High Tax

High Cost – Low TaxLow Cost – Low Tax

Dev

elop

men

t onl

y G

over

nmen

t Tak

e (%

Pre

-Tak

e N

PV @

10%

)

Total Costs ($/boe, 2004)OECD Countries

Syria

Qatar

Oman

Norway

USA (Alaska)

Nigeria (deepwater)

Egypt

Denmark

Canada (Arctic)

Trinidad & Tobago

USA (GoM deepwater)

UK (Southern Gas Basin) UK (shelf)

New ZealandNetherlands (onshore)

Netherlands (offshore)

Malaysia-Thailand JDA

Italy

Canada (East Coast)

Bolivia

Bangladesh

Australia (offshore)

Argentina

Libya

Papua New Guinea

Kazakhstan

IndonesiaVietnam

VenezuelaMalaysia

Colombia

Brunei

Azerbaijan

Angola (deepwater)

Algeria

Pakistan

Cote d'IvoireIndia

Congo (Brazzaville)

China (offshore)

30%

40%

50%

60%

70%

80%

90%

100%

0.0 2.0 4.0 6.0 8.0 10.0 12.0 14.0 16.0

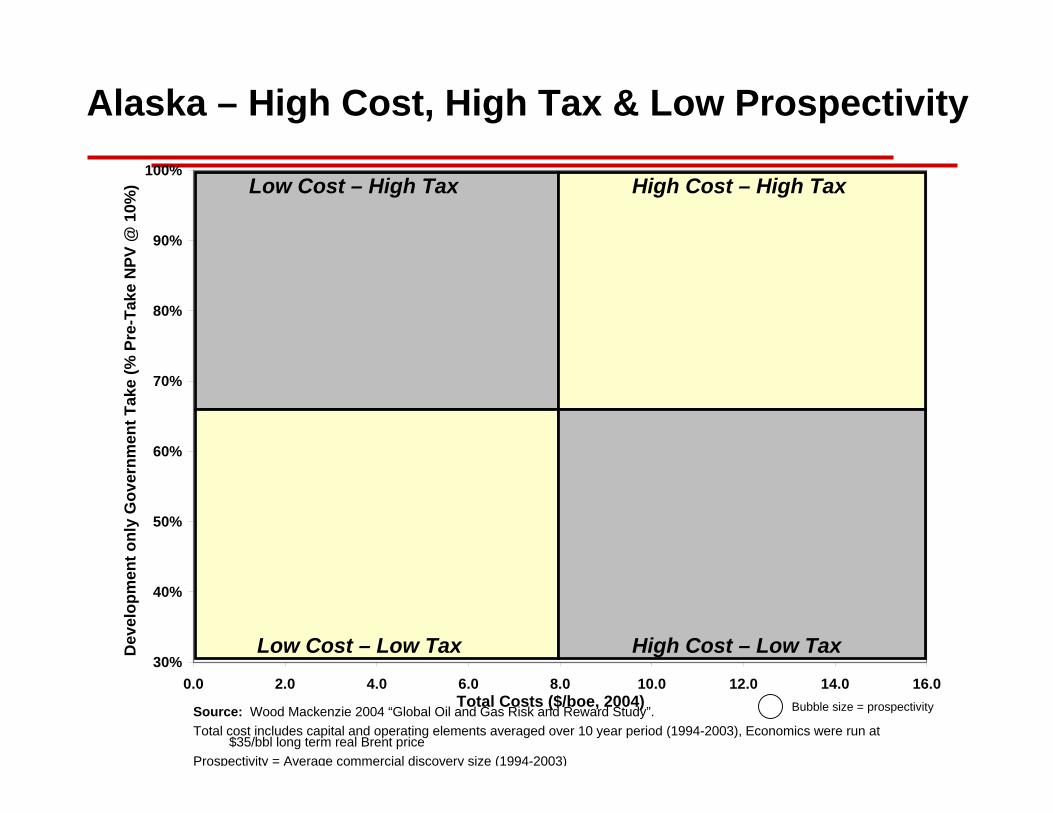

Alaska – High Cost, High Tax & Low Prospectivity

Source: Wood Mackenzie 2004 “Global Oil and Gas Risk and Reward Study”.Total cost includes capital and operating elements averaged over 10 year period (1994-2003), Economics were run at

$35/bbl long term real Brent priceProspectivity = Average commercial discovery size (1994-2003)

High Cost – High TaxLow Cost – High Tax

High Cost – Low TaxLow Cost – Low TaxDev

elop

men

t onl

y G

over

nmen

t Tak

e (%

Pre

-Tak

e N

PV @

10%

)

Total Costs ($/boe, 2004) Bubble size = prospectivity

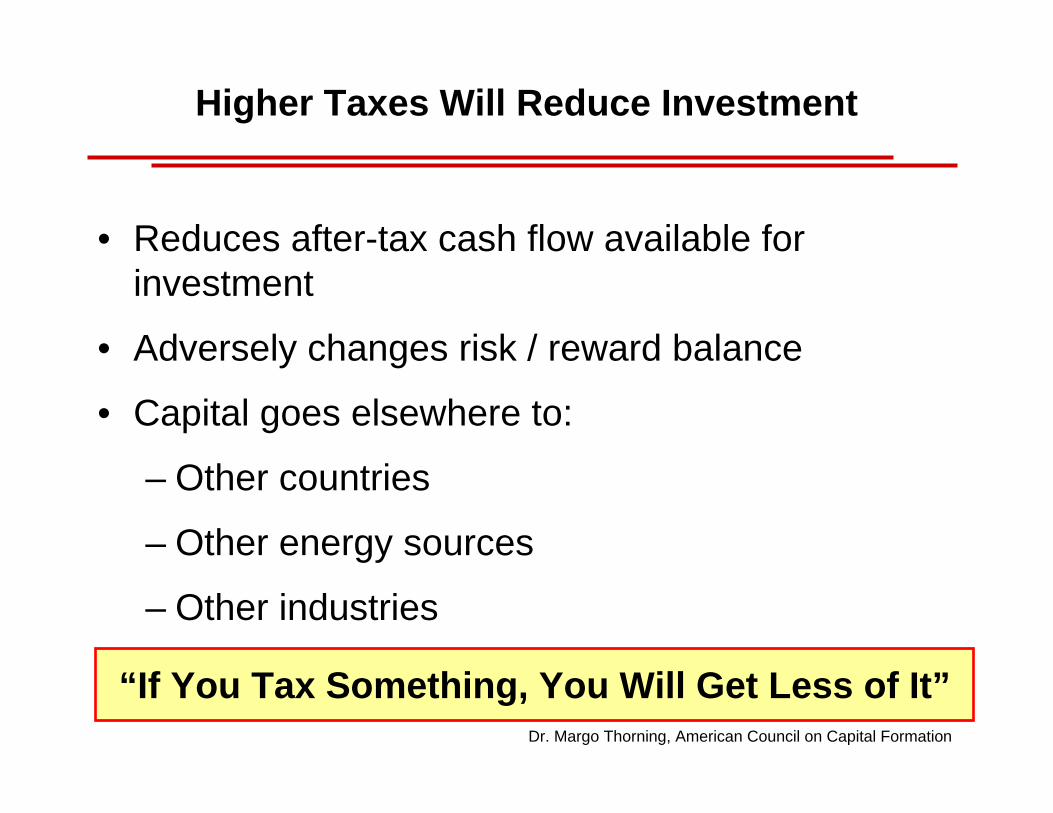

Higher Taxes Will Reduce Investment

• Reduces after-tax cash flow available for investment

• Adversely changes risk / reward balance

• Capital goes elsewhere to:

– Other countries

– Other energy sources

– Other industries

Dr. Margo Thorning, American Council on Capital Formation

“If You Tax Something, You Will Get Less of It”

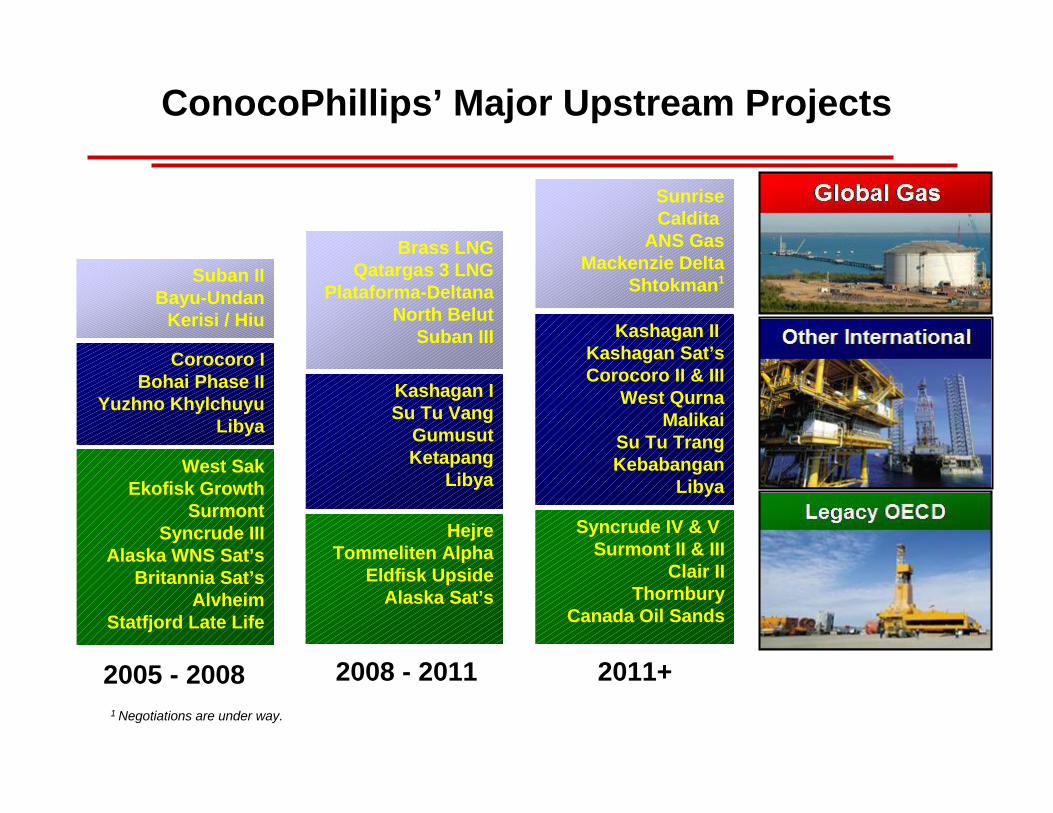

ConocoPhillips’ Major Upstream Projects

West SakEkofisk Growth

SurmontSyncrude III

Alaska WNS Sat’sBritannia Sat’s

AlvheimStatfjord Late Life

Corocoro IBohai Phase II

Yuzhno KhylchuyuLibya

Suban IIBayu-Undan

Kerisi / Hiu

HejreTommeliten Alpha

Eldfisk UpsideAlaska Sat’s

Kashagan ISu Tu Vang

GumusutKetapang

Libya

Brass LNGQatargas 3 LNG

Plataforma-DeltanaNorth Belut

Suban III

Syncrude IV & V Surmont II & III

Clair IIThornbury

Canada Oil Sands

Kashagan II Kashagan Sat’sCorocoro II & III

West QurnaMalikai

Su Tu TrangKebabangan

Libya

SunriseCaldita

ANS GasMackenzie Delta

Shtokman1

2008 - 2011 2011+2005 - 20081 Negotiations are under way.

00.250.5

0.751

1.251.5

1.752

Alaska

1

Alaska

2

Alaska

3Downstre

am 1Alte

rnati

ve E

nergy 1

Upstream

1

Upstream

2

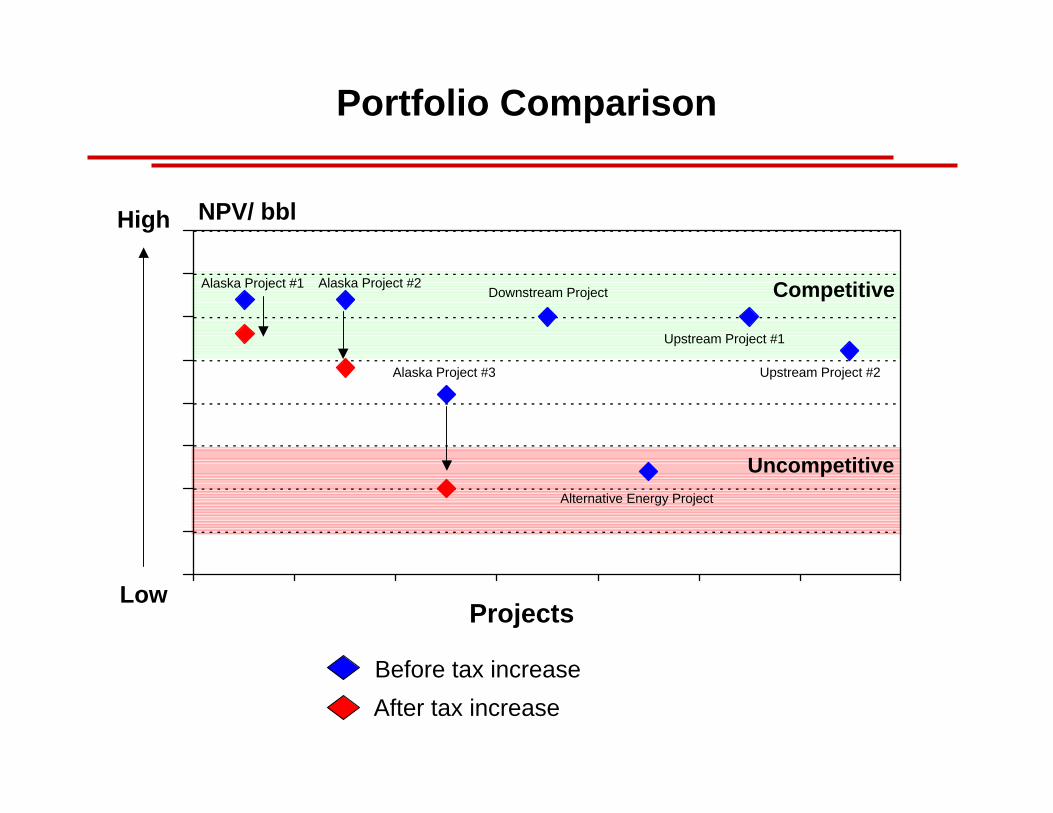

Portfolio Comparison

Alaska Project #1 Alaska Project #2

Alaska Project #3

Downstream Project

Upstream Project #1

Upstream Project #2

Alternative Energy Project

High

Low

NPV/ bbl

Competitive

Uncompetitive

Before tax increaseAfter tax increase

Projects

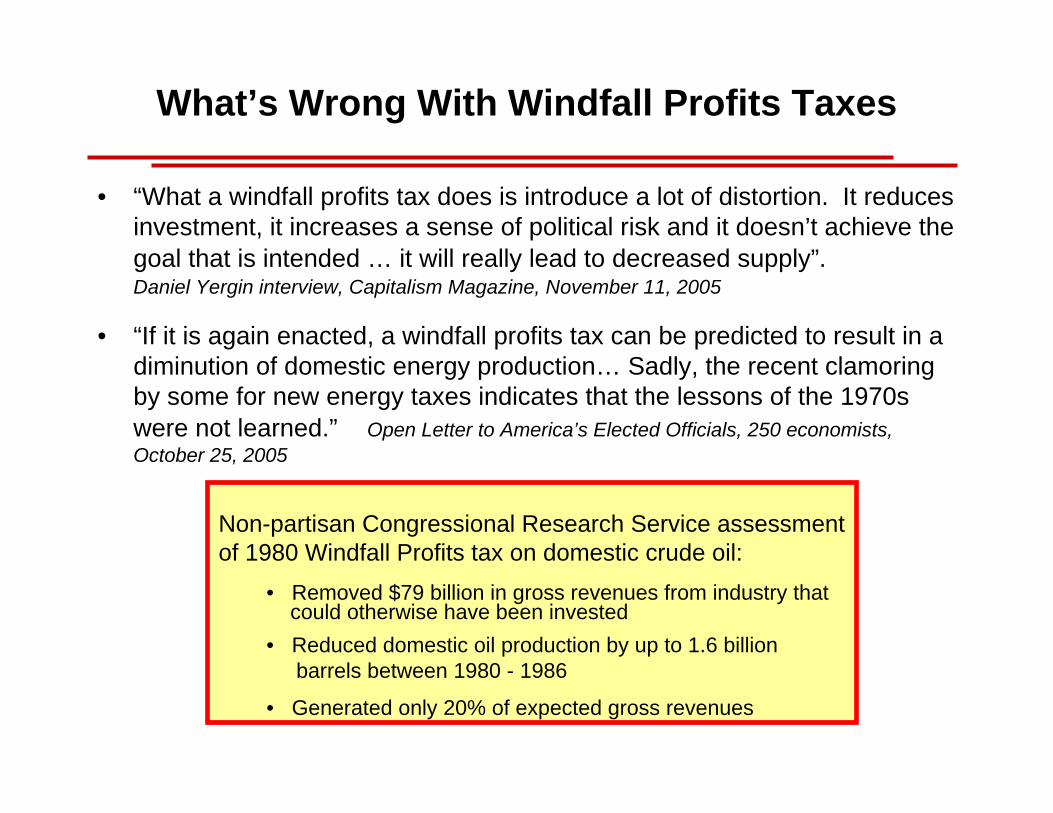

What’s Wrong With Windfall Profits Taxes

• “What a windfall profits tax does is introduce a lot of distortion. It reduces investment, it increases a sense of political risk and it doesn’t achieve the goal that is intended … it will really lead to decreased supply”.Daniel Yergin interview, Capitalism Magazine, November 11, 2005

• “If it is again enacted, a windfall profits tax can be predicted to result in a diminution of domestic energy production… Sadly, the recent clamoring by some for new energy taxes indicates that the lessons of the 1970s were not learned.” Open Letter to America’s Elected Officials, 250 economists, October 25, 2005

Non-partisan Congressional Research Service assessmentof 1980 Windfall Profits tax on domestic crude oil:

• Removed $79 billion in gross revenues from industry thatcould otherwise have been invested

• Reduced domestic oil production by up to 1.6 billion barrels between 1980 - 1986

• Generated only 20% of expected gross revenues

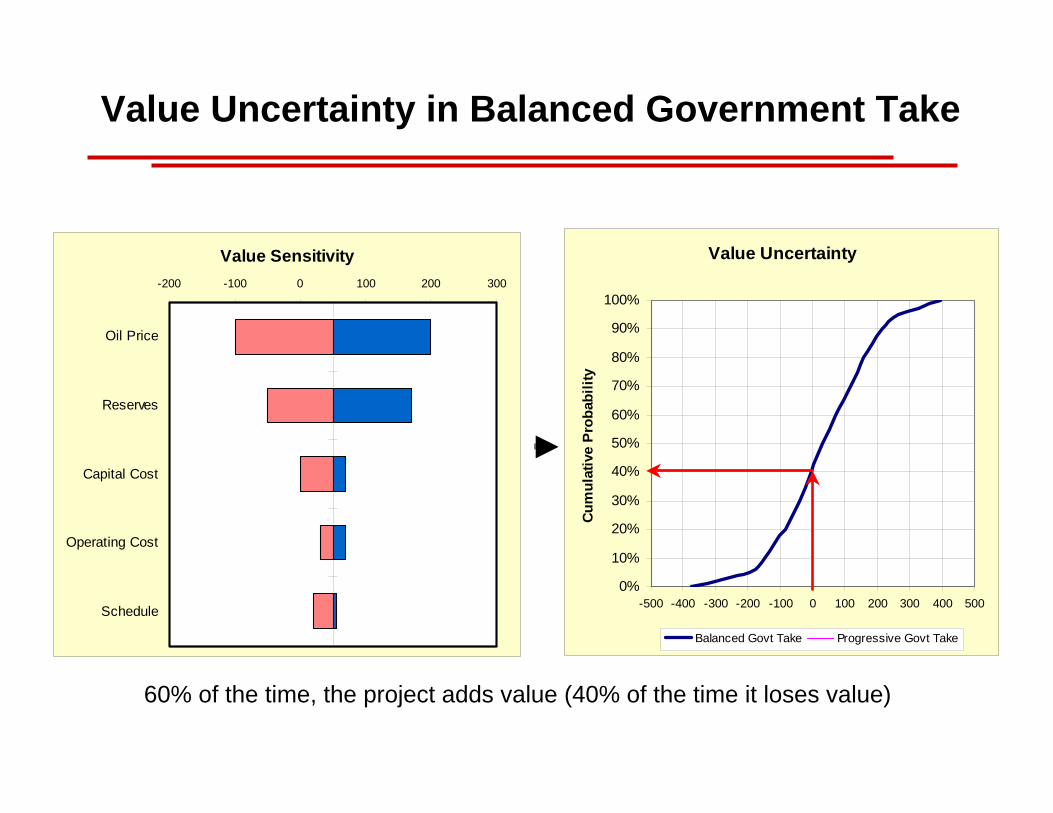

Value Uncertainty

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-500 -400 -300 -200 -100 0 100 200 300 400 500Cu

mul

ativ

e Pr

obab

ility

Balanced Govt Take Progressive Govt Take

Value Sensitivity-200 -100 0 100 200 300

Oil Price

Reserves

Capital Cost

Operating Cost

Schedule

Value Uncertainty in Balanced Government Take

60% of the time, the project adds value (40% of the time it loses value)

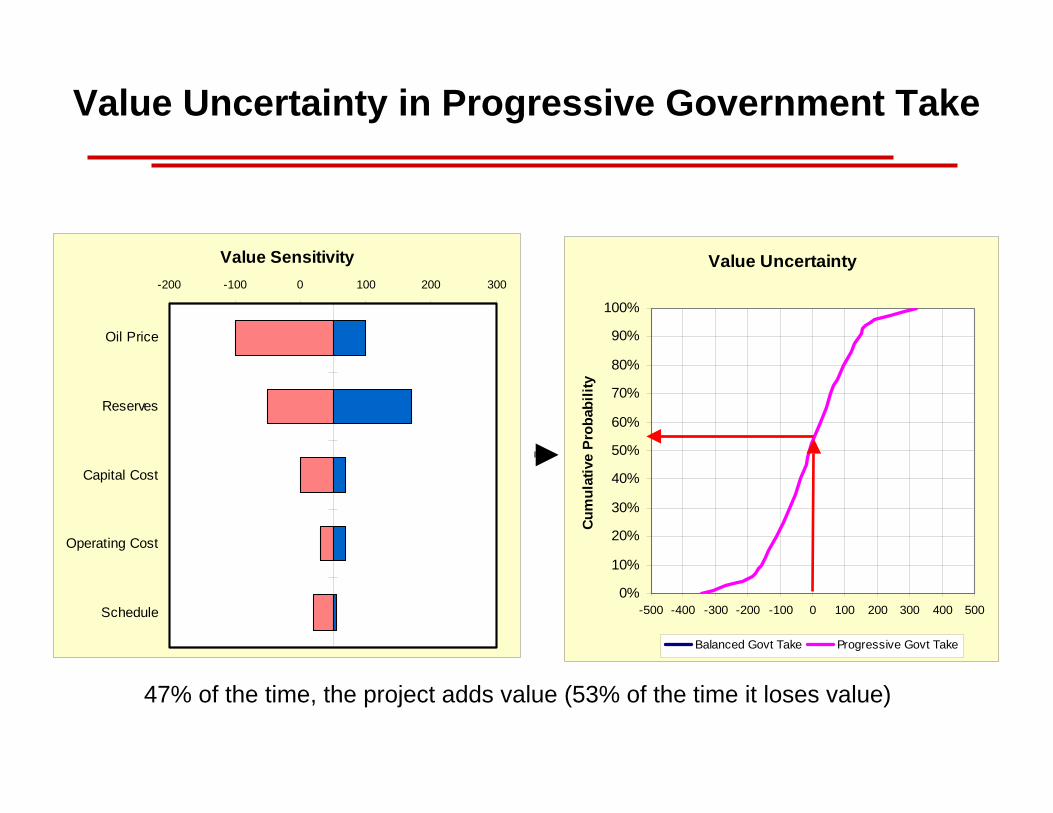

Value Sensitivity-200 -100 0 100 200 300

Oil Price

Reserves

Capital Cost

Operating Cost

Schedule

Value Uncertainty

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-500 -400 -300 -200 -100 0 100 200 300 400 500

Cum

ulat

ive

Prob

abili

ty

Balanced Govt Take Progressive Govt Take

Value Uncertainty in Progressive Government Take

47% of the time, the project adds value (53% of the time it loses value)

Value Uncertainty

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-500 -400 -300 -200 -100 0 100 200 300 400 500

Cum

ulat

ive

Pro

babi

lity

Balanced Govt Take Progressive Govt Take

53% Chance of

Losing Money

40% Chance of

Losing Money

Balanced and Progressive Value Uncertainty Comparison

In this example:

• Under a balanced government take the project would be developed

• Under the progressive government take the project would not go forward.

Finding, Development & Production Costs

$0

$4

$8

$12

$16

$20

1999 2000 2001 2002 2003 2004 2005

ProductionF&D

2006 Dollars per Barrel of Oil Equivalent

More than Doubled Since 1999

Source: J.S. Herold

Excludes all government take ($20-25/bbl), adjustment for the time value of money &

a cost of capital return

Key Messages from Corporate Perspective

• Current tax rate already uncompetitive given cost & prospectivity

• Proposed tax increases will reduce investment & production in Alaska

• U.S. federal windfall profits taxes lowered production and failed to produce expected revenues

2/27/06 – Slide 17

Jim BowlesPresident

ConocoPhillips Alaska

Summary

• Higher taxes will reduce investments– 20% strikes the right balance– Increased Tax rate and windfall profits surcharge

decreases project value

• Recognition of transition investments is fair

• Reasonable start date