pc100nw ifrs scope case2

DESCRIPTION

SAP Financial AnalyticsTRANSCRIPT

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 1/11

What are the regulation requirements?

The loss of control of a subsidiary is a transaction or another event in which a

parent company sells its controlling interest in a subsidiary to another party. This

case study will focus on a loss of control where the parent doesn’t retain any

interest in the subsidiary.

When a parent company loses its controlling interest on a subsidiary:

It derecognizes the assets (including goodwill), liabilities and non-

controlling interests of the former subsidiary

It recognizes the fair value of consideration received, any distribution of

shares to owners,

It reclassifies to profit and loss any amounts previously recognized in OCI

(i.e. fair value reserve, hedging reserve and foreign currency translation

reserve)

It recognizes the resulting difference in its profit or loss, as calculated

hereafter:

Individual statement level Consolidated statement level

Sale proceeds

Cost of investment

Parent's gain or loss on sale ofinvestment at individual statement level

Sale proceeds

Carrying value of NCI

Net goodwill at the date of disposal

Acqui ree recycling of OCI (hedging, fairvalue for AFS, CTA)

Parent's gain or loss on sale ofinvestment at consolidated statement

Net assets derecognized

Consolidation Practical

Guide

N°2

July, 2011

Summary:

What are the regulation

requirements?

Presentation of the Business

Case

How to handle a loss of

control with IFRS Starter Kit?

How does the loss of control

affect financial statements?

To know more

What are SAP® BusinessObjectsTM

IFRS

Starter Kits?

Preconfigured contents on top of

SAP® BusinessObjectsTM

Planning and

Consolidation and FinancialConsolidation

with all reports, controls and rules for

performing, validating and publishing

a statutory consolidation in

accordance with IFRS standards

Based on dynamic configuration easy

to customize to specific

requirements

Delivered on SAP Service Market

Place

Provided with documentations

posted on SAP Help

How to handle the loss of control of a subsidiary

with SAP®BusinessObjectsTM Planning and Consolidation 10.0, Version for SAP

Netweaver Starter Kit for IFRS?

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 2/11

How to handle the loss of control of a subsidiary

with SAP® BusinessObjects™ IFRS Starter Kits

Consolidation Practical Guide N 2 – July, 2011

- 2 -

Presentation of the Business Case

Presentation of the Business Case

Year 2013

The 1st

of January, parent company P2 (USD) acquires 100% interest of

subsidiary PS2 (EUR) for USD 95 000 in cash. PS2 net value of the identifiable

assets and liabilities is EUR 87 500

Goodwill calculation = EUR 7 500 (x rate: 1 USD = 1 EUR)

PS2 profit for the year = EUR 10 000 (average rate for 2013: 1 USD =0,80 EUR)

On December 31st , the exchange rate is 1 USD =0,85 EUR

Year 2014

PS2 goodwill impairment = EUR 4 000

PS2 profit for the year = EUR 15 000

The 1st

of December P2 sells its 100% controlling interests in PS2 for

USD 100 000. The average rate from January 1st

to December 1st

is

1 USD = 0,75 EUR. The spot rate on December 1st is 1 USD = 0,80 EUR

Note: For a matter of simplification, the case study is displayed on two years

even if it is not fully relevant from an IFRS perspective (e.g. IFRS5)

PS2 net assets at the disposal date is EUR 112 500 (87 500 + 10 000 + 15 000).

PS2 individual accounts converted in USD and including goodwill are as follows:

12/31/2013 12/01/2014

(before sale)

Goodwill 8 824 4 375

Cash 114 706 140 625

--------------------------------- ------------- ----------

Total assets 123 529 145 000

Retained earnings 107 500 122 167Currency translation adjustment 16 029 22 833

-------------------------------- -------------- -----------

Total Equity & liabilities 123 529 145 000

Y 2013 Y 2014

Parent P2 Parent P2

Subsidiary PS2

100%

This business case is included inthe set of data provided with the

IFRS starter kit. It can be retrieved

using the following settings:

Category: ACTUAL

Time: 2014.DEC

Consolidation Currency: USD

Consoscope: CASE2

Entity: P2, PS2

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 3/11

How to handle the loss of control of a subsidiary

with SAP® BusinessObjects™ IFRS Starter Kits

Consolidation Practical Guide N 2 – July, 2011

- 3 -

Reminder

The amounts stored in the database are identified thanks to a set of elements called dimensions.

The main dimensions are listed below:

The account dimension indicates which item of the balance sheet or P&L is impacted.

The flow dimension is used to identify and analyze the changes between the opening (flow F00)

and closing (flow F99) balances.

The audit ID dimension identifies the origin of the data for input data, local adjustments, manualand automatic journal entries.

How to handle a loss of control in the IFRS starter kit?

In the following pages, we will focus on consolidation of Y2014.

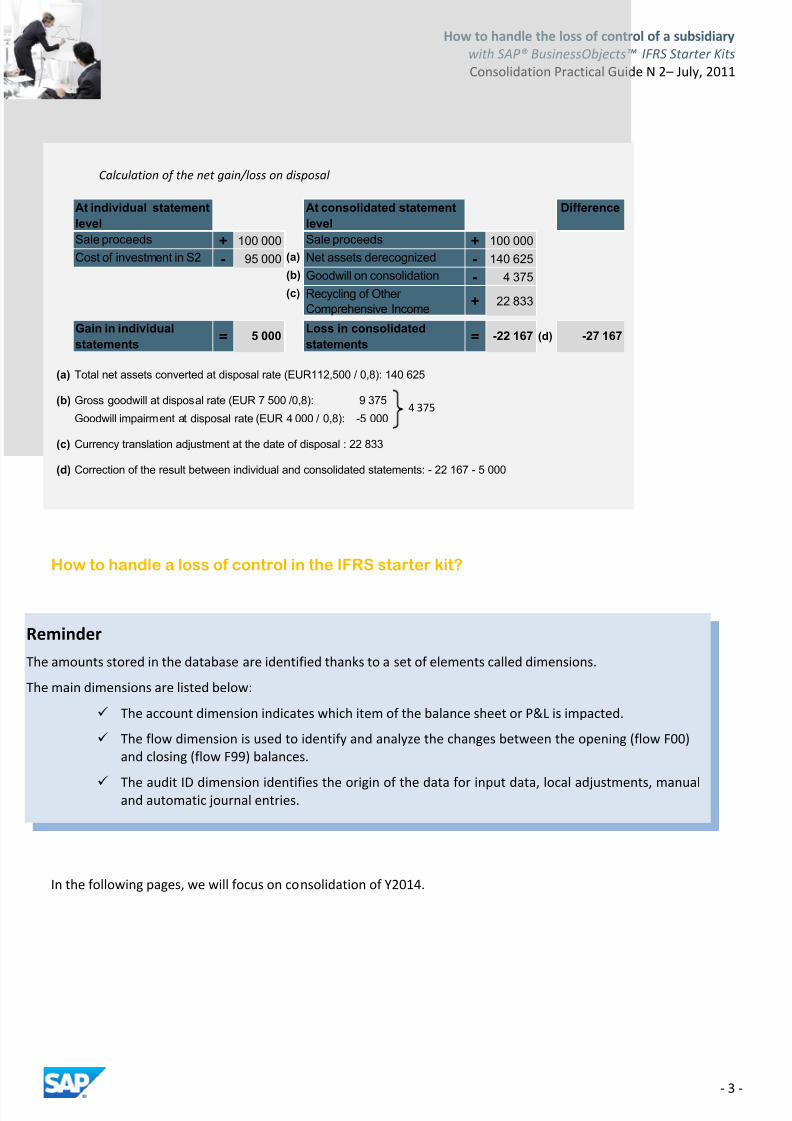

Calculation of the net gain/loss on disposal

At individual statement

level

At consolidated statement

level

Difference

Sale proceeds + 100 000 Sale proceeds + 100 000

Cost of investment in S2 - 95 000 (a) Net assets derecognized - 140 625

(b) Goodwill on consolidation - 4 375

(c) Recycling of Other

Comprehensive Income+ 22 833

Gain in individual

statements= 5 000

Loss in consolidated

statements= -22 167 (d) -27 167

(a) Total net assets converted at disposal rate (EUR112,500 / 0,8): 140 625

(b) Gross goodwill at disposal rate (EUR 7 500 /0,8): 9 375

Goodwill impairment at disposal rate (EUR 4 000 / 0,8): -5 000

(c) Currency translation adjustment at the date of disposal : 22 833

(d) Correction of the result between individual and consolidated statements: - 22 167 - 5 000

4 375

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 4/11

How to handle the loss of control of a subsidiary

with SAP® BusinessObjects™ IFRS Starter Kits

Consolidation Practical Guide N 2 – July, 2011

- 4 -

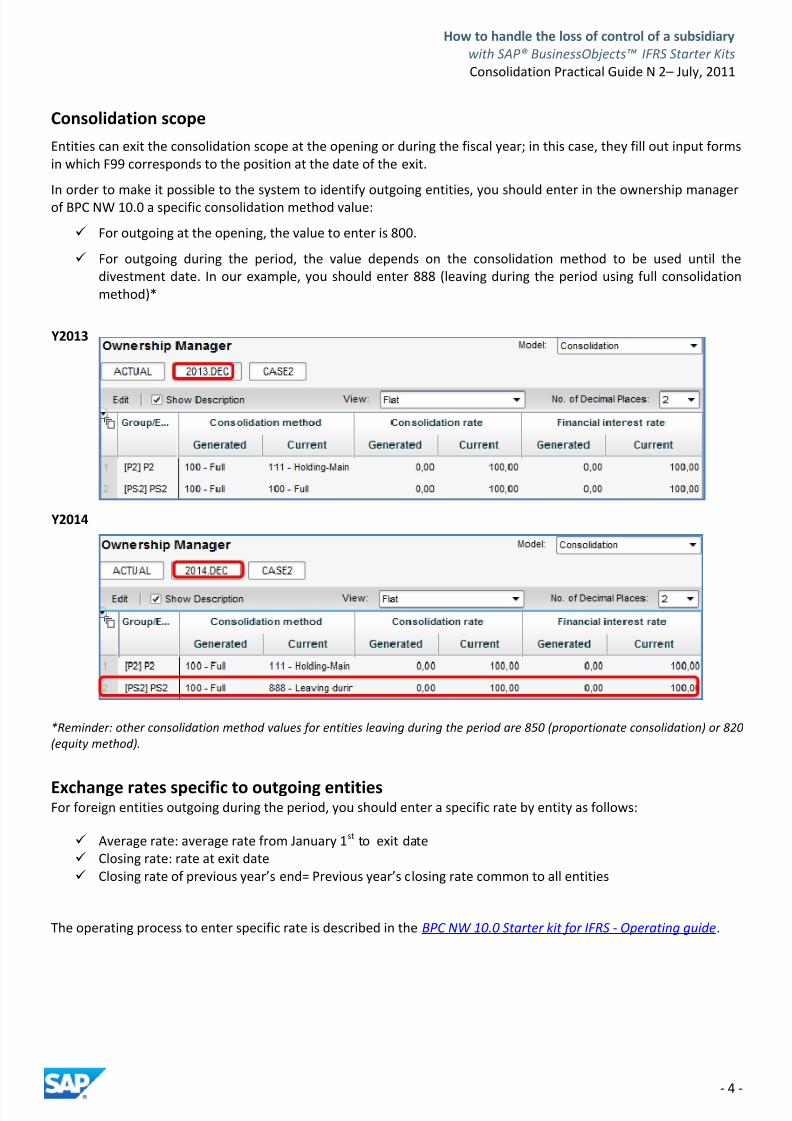

Consolidation scope

Entities can exit the consolidation scope at the opening or during the fiscal year; in this case, they fill out input forms

in which F99 corresponds to the position at the date of the exit.

In order to make it possible to the system to identify outgoing entities, you should enter in the ownership managerof BPC NW 10.0 a specific consolidation method value:

For outgoing at the opening, the value to enter is 800.

For outgoing during the period, the value depends on the consolidation method to be used until the

divestment date. In our example, you should enter 888 (leaving during the period using full consolidation

method)*

*Reminder: other consolidation method values for entities leaving during the period are 850 (proportionate consolidation) or 820

(equity method).

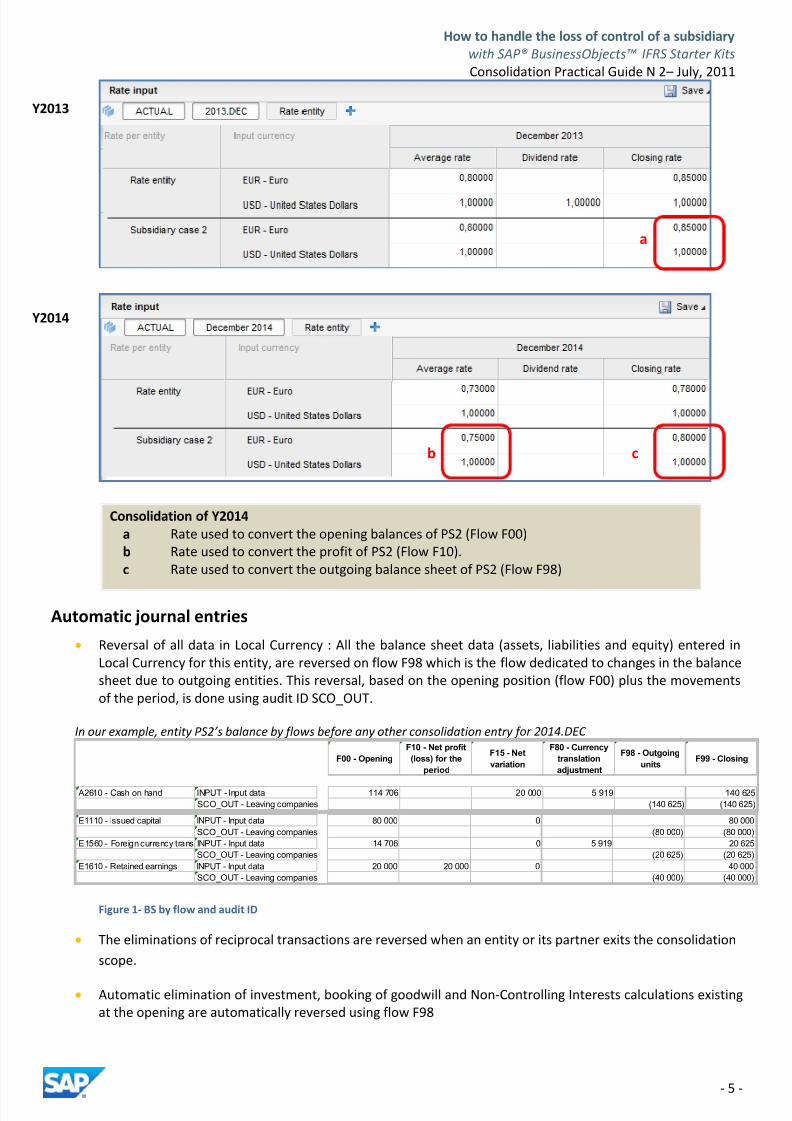

Exchange rates specific to outgoing entitiesFor foreign entities outgoing during the period, you should enter a specific rate by entity as follows:

Average rate: average rate from January 1st

to exit date

Closing rate: rate at exit date

Closing rate of previous year’s end= Previous year’s closing rate common to all entities

The operating process to enter specific rate is described in the BPC NW 10.0 Starter kit for IFRS - Operating guide.

Y2013

Y2014

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 5/11

How to handle the loss of control of a subsidiary

with SAP® BusinessObjects™ IFRS Starter Kits

Consolidation Practical Guide N 2 – July, 2011

- 5 -

Automatic journal entries

Reversal of all data in Local Currency : All the balance sheet data (assets, liabilities and equity) entered in

Local Currency for this entity, are reversed on flow F98 which is the flow dedicated to changes in the balance

sheet due to outgoing entities. This reversal, based on the opening position (flow F00) plus the movements

of the period, is done using audit ID SCO_OUT.

In our example, entity PS2’s balance by flows before any other consolidation entry for 2014.DEC

Figure 1- BS by flow and audit ID

The eliminations of reciprocal transactions are reversed when an entity or its partner exits the consolidation

scope.

Automatic elimination of investment, booking of goodwill and Non-Controlling Interests calculations existing

at the opening are automatically reversed using flow F98

F00 - Opening

F10 - Net profit

(loss) for the

period

F15 - Net

variation

F80 - Currency

translation

adjustment

F98 - Outgoing

unitsF99 - Closing

A2610 - Cash on hand INPUT - Input data 114 706 20 000 5 919 140 625

SCO_OUT - Leaving companies (140 625) (140 625)

E1110 - Issued capital INPUT - Input data 80 000 0 80 000

SCO_OUT - Leaving companies (80 000) (80 000)

E1560 - Foreign currency trans INPUT - Input data 14 706 0 5 919 20 625

SCO_OUT - Leaving companies (20 625) (20 625)

E1610 - Retained earnings INPUT - Input data 20 000 20 000 0 40 000

SCO_OUT - Leaving companies (40 000) (40 000)

a

Y2013

Y2014

a Rate used to convert the opening balances of PS2 (Flow F00)

b Rate used to convert the profit of PS2 (Flow F10).

c Rate used to convert the outgoing balance sheet of PS2 (Flow F98)

b c

Consolidation of Y2014

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 6/11

How to handle the loss of control of a subsidiary

with SAP® BusinessObjects™ IFRS Starter Kits

Consolidation Practical Guide N 2 – July, 2011

- 6 -

Manual journal entries

A first manual journal entry (MJE) has been posted to declare on a technical account the depreciation of goodwill of

the year.

A second manual journal entry has been posted to adjust the difference between the net gain booked in the

individual accounts of its owner company and the net loss to account for in the consolidated statements using a

dedicated audit ID INV31- Adjust. on gain/loss on disposal of a subs., JV or associate (Local currency) (see calculation

of the net gain/loss on disposal on page 3)

If there was any manual journal entry entered in consolidation currency (= all MJE with an audit ID different from

ADJ91, GW01, FVA11 and INPUT91) in the consolidated opening balance, it should be reversed manually using the

flow F98. In the case of an elimination of the gain/loss on internal transfer of assets (DIS11), the manual journal

entry existing at the partner should also be reversed

a The entry is posted at the owner, in

local currency (i.e in the reporting

currency of P2),

b Using the audit ID INV31,

c the flow F98 (outgoing unit), on

account E1610 Retained earnings

d the flow PL99 (P&L period to date) on

account P1615 Gains or losses on sale

of shares in subsidiary

a b

c

d

a The entry is posted at the subsidiary, in

local currency (i.e in the reporting

currency of PS2)

b using the audit ID GW01 – Disclosure

of goodwill and bargain purchase

c on account XA1312 for the goodwill

depreciation attributable to the group,

with an INTERCO detail by owner

company. This amount will trigger an

automatic journal entry on audit ID

GW10.

a b

c

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 7/11

How to handle the loss of control of a subsidiary

with SAP® BusinessObjects™ IFRS Starter Kits

Consolidation Practical Guide N 2 – July, 2011

- 7 -

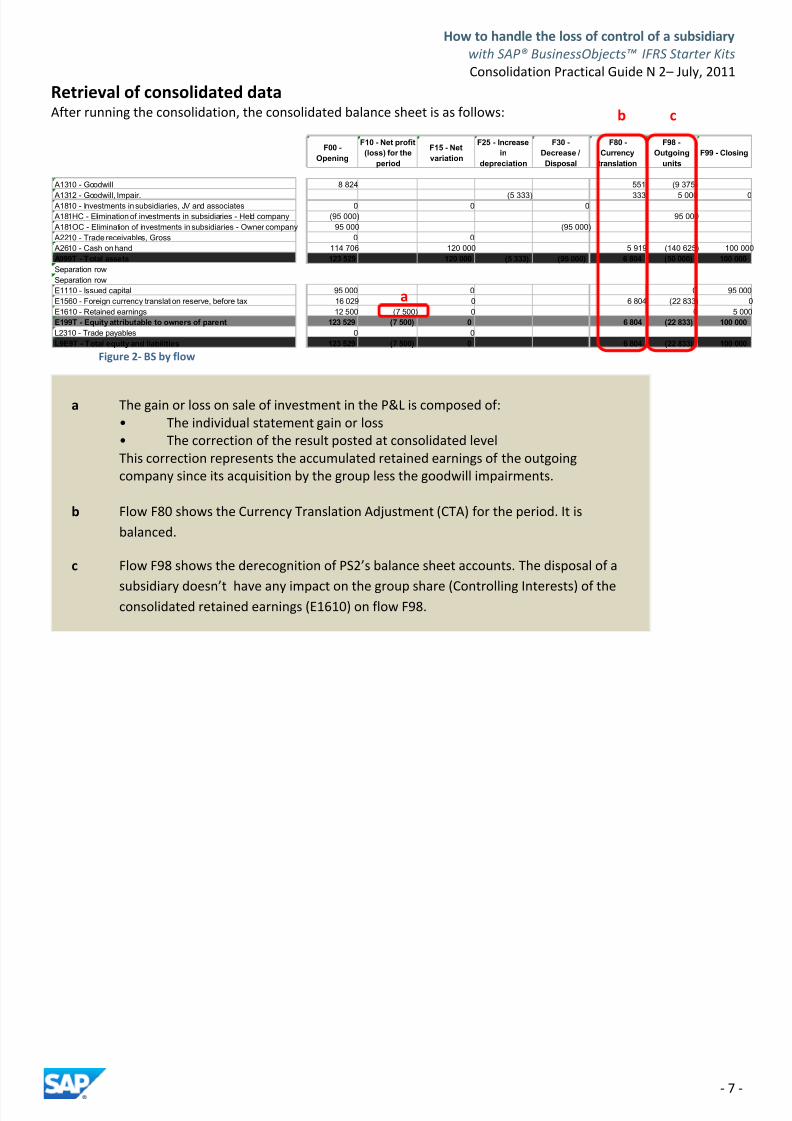

Retrieval of consolidated dataAfter running the consolidation, the consolidated balance sheet is as follows:

Figure 2- BS by flow

F00 -

Opening

F10 - Net profit

(loss) for the

period

F15 - Net

variation

F25 - Increase

in

depreciation

F30 -

Decrease /

Disposal

F80 -

Currency

translation

F98 -

Outgoing

units

F99 - Closing

A1310 - Goodwill 8 824 551 (9 375)

A1312 - Goodwill, Impair. (5 333) 333 5 000 0 A1810 - Investments in subsidiaries, JV and associates 0 0 0

A181HC - Elimination of investments in subsidiaries - Held company (95 000) 95 000

A181OC - Elimination of investments in subsidiaries - Owner company 95 000 (95 000)

A2210 - Trade receivables, Gross 0 0

A2610 - Cash on hand 114 706 120 000 5 919 (140 625) 100 000

A999T - Total assets 123 529 120 000 (5 333) (95 000) 6 804 (50 000) 100 000

Separation row

Separation row

E1110 - Issued capital 95 000 0 0 95 000

E1560 - Foreign currency translation reserve, before tax 16 029 0 6 804 (22 833) 0

E1610 - Retained earnings 12 500 (7 500) 0 0 5 000

E199T - Equity attributable to owners of parent 123 529 (7 500) 0 6 804 (22 833) 100 000

L2310 - Trade payables 0 0

L9E9T - Total equity and liabilities 123 529 (7 500) 0 6 804 (22 833) 100 000

c

e

a The gain or loss on sale of investment in the P&L is composed of:

• The individual statement gain or loss

• The correction of the result posted at consolidated level

This correction represents the accumulated retained earnings of the outgoing

company since its acquisition by the group less the goodwill impairments.

b Flow F80 shows the Currency Translation Adjustment (CTA) for the period. It is

balanced.

c Flow F98 shows the derecognition of PS2’s balance sheet accounts. The disposal of a

subsidiary doesn’t have any impact on the group share (Controlling Interests) of theconsolidated retained earnings (E1610) on flow F98.

a

b

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 8/11

How to handle the loss of control of a subsidiary

with SAP® BusinessObjects™ IFRS Starter Kits

Consolidation Practical Guide N 2 – July, 2011

- 8 -

The equity movements are explained below:

Figure 3- BS by flow and audit ID

F00 -

Opening

F10 - Net

profit (loss)

for the

F80 -

Currency

translation

F98 -

Outgoing

units

F99 -

Closing

E1110 - Issued capital INPUT - Input data 175 000 175 000

SCO_OUT - Leaving companies (80 000) (80 000)

CONS10 - Elim. of subsidiaries' capital (80 000) 80 000

Total Issued capital 95 000 0 0 0 95 000

INPUT - Input data 14 706 5 919 20 625

SCO_OUT - Leaving companies (20 625) (20 625)

GW20 - Currency translation adjust. on 1 324 885 (2 208)

Total Foreign currency translation rese 16 029 0 6 804 (22 833) 0

E1610 - Retained earnin INV31 - Adjust. on G/Lon disp. of a subs. (27 167) 27 167

INPUT - Input data 20 000 25 000 45 000

SCO_OUT - Leaving companies (40 000) (40 000)

INV10 - Elimination of investments - Aut (95 000) 95 000

GW10 - Booking of goodwill and bargain 7 500 (5 333) (2 167) 0

CONS10 - Elim. of subsidiaries' capital 80 000 (80 000)Total Retained earnings 12 500 (7 500) 0 0 5 000

E1560 - Foreign

currency translation

The movements on the equity are the following:

a P2 net income

Gain on sale of S2 at package level (INPUT): +5 000 Correction of the gain at consolidation level (INV31 MJE #5): -27 167

PS2 net income

Net income at package level (INPUT): +20 000

Goodwill impairment (GW10 MJE #4): -5 333

b Flow F80 shows PS2’s exchange differences for Y2014

CTA on the PS2’s equity (difference closing rate – historical rate for INPUT data audit ID)

CTA on goodwill (GW20)

c Flow F98 shows the outgoing of PS2. Package data on flow F00 + movement flows (stored on

INPUT audit ID) are reversed using SCO_OUT audit ID.

a

b

b

c

e

c

f

h

b

g

a

d

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 9/11

How to handle the loss of control of a subsidiary

with SAP® BusinessObjects™ IFRS Starter Kits

Consolidation Practical Guide N 2 – July, 2011

- 9 -

How does the acquisition affect financial statements?

Statement of financial position

F00 - Opening

S

e

p

F99 - Closing

A1310 - Goodwill 8 824

A1312 - Goodwill, Impair. 0

A139T - Goodwill 8 824 0

A1810 - Investments in subsidiaries, JV and associates 0

A181HC - Elimination of investments in subsidiaries - Held company (95 000)

A181OC - Elimination of investments in subsidiaries - Owner company 95 000A189T - Other non-current financial assets 0

A199T - Non-current assets 8 824 0

A2210 - Trade receivables, Gross 0

A229T - Trade and other current receivables 0

A2610 - Cash on hand 114 706 100 000

A269T - Cash and cash equivalents 114 706 100 000

A299T - Current assets other than non-current assets held for sale 114 706 100 000

A959T - Current assets 114 706 100 000

A999T - Total assets 123 529 100 000

Separation row

E1110 - Issued capital 95 000 95 000

E1560 - Foreign currency translation reserve, before tax 16 029 0

E159T - Other reserves 16 029 0

E1610 - Retained earnings 12 500 5 000

E199T - Equity attributable to owners of parent 123 529 100 000

E999T - Total equity 123 529 100 000

L2310 - Trade payables 0

L239T - Trade and other current payables 0

L299T - Current liab. other than liab. included in disp. groups 0

L959T - Current liabilities 0

L999T - Total liabilities 0

L9E9T - Total equity and liabilities 123 529 100 000

a

The loss of control impacts the following accounts:

a the goodwill

b the cash

c the equity

b

c

c

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 10/11

How to handle the loss of control of a subsidiary

with SAP® BusinessObjects™ IFRS Starter Kits

Consolidation Practical Guide N 2 – July, 2011

- 10 -

Statement of comprehensive income(Extract)

Statement of cash flows(Extract)

2014.DEC

Profit (loss) for the period -7 500

Gains (losses) on exchange differences, before tax 6 804

Tax on gains (losses) on exchange differences 0

Reclass. adj. on exchange differences, before tax -22 833

Tax on reclass. adj. on exchange differences 0

Exchange differences on translation, net of tax -16 029

Available-for-sale financial assets, net of tax 0

Cash flow hedges, net of tax 0

Gains (losses) on revaluation, net of tax 0

Gains (losses) on def. benefit plans, net of tax 0

Share of OCI of associates and JV in equity method 0 OCI related to NC assets and disposal groups classif ied as held f or sale 0

Other comprehensive income, net of tax -16 029

Comprehensive income -23 530

Comprehensive income, share of ow ners of parent -23 530

Comprehensive income, share of non-control. Inter. 0

2014.DEC

Profit (loss) -7 500 Adj. for impair. loss (reversal) recognised in P&L 5 333

Adj. for losses (gains) on disposal of NC assets 22 167

Other adj. w ith cash effects in inv.or fin. CF 0

Adjustments for reconcile profit (loss) 27 500

Interests paid 0

Income taxes (refund) paid 0

Other inflow s (outflow s) of cash 0

Net cash flow s from (used in) operating activities 20 000

CF from losing control of subsidiaries or JV -40 625

CF used in obtaining control of subsidiaries or JV 0

Other inflow s (outflow s) of cash 0

Net cash flow s from (used in) investing activities -40 625

Net cash flows from (used in) financing activities 0

Effect of exch. rate changes on cash & cash equiv. 5 919

Ne t incre as e (de cre as e) in cas h & cash e quivale nts -14 706

Cash and cash equivalents at beginning of period 114 706

Cash and cash equivalents at end of period 100 000

Difference Closing - Opening -14 706

a PS2’s net profit of the year 20 000

PS2 Goodwill impairment - 5 333

P2 Loss on PS2 sale - 22 167

-----------

- 7 500

b PS2 CTA on 1/12/2014 22 833

PS2 CTA on 12/31/2013 -16 029

---------

6 804

c PS2 cumulated CTA recycled 22 833

a

b

c

a

a PS2’s net profit of the year EUR 15 000 /0,75: USD 20 000

b Sale proceed USD +100 000

Cash of PS2 outgoing USD -140 625

__________

USD -40 625

c Effect of exchange rate on PS2’s cash:

at opening EUR 97 500/0,80 – 97 500/0,85: +7169

on movement EUR 15 000/0,80 – 15 000 /0,75: -1 250

_____

5 919

b

c

7/21/2019 Pc100nw Ifrs Scope Case2

http://slidepdf.com/reader/full/pc100nw-ifrs-scope-case2 11/11

How to handle the loss of control of a subsidiary

with SAP® BusinessObjects™ IFRS Starter Kits

Consolidation Practical Guide N 2 – July, 2011

Statement of changes in equity

To know moreYou will find further indications on how to deal with outgoing entities in the BPC NW 10.0 Starter kit for IFRS -

Operating guide.

Issued

capital

Share

premium

Treasury

shares

Other

reserves

Retained

earnings

Equity

attributable

to owners of

parent

Non-

controlling

interests

Total equity

Balance at opening 95 000 0 0 0 0 95 000 0 95 000

Changes in accounting policies 0 0 0 0 0 0 0 0

Balance at opening as restated - 2013.DEC 95 000 0 0 0 0 95 000 0 95 000

Comprehensive income 0 0 0 16 029 12 500 28 529 0 28 529

Issue of shares 0 0 0 0 0 0 0 0

Dividends paid 0 0 0 0 0 0 0 0

Transfers 0 0 0 0 0 0 0 0

Issue of convertible notes 0 0 0 0 0 0 0 0

Share-based payments 0 0 0 0 0 0 0 0

Purchase and disposal of treasury shares 0 0 0 0 0 0 0 0

Transactions w ith non-controlling interests 0 0 0 0 0 0 0 0

Other movements 0 0 0 0 0 0 0 0

Balance at closing - 2013.DEC 95 000 0 0 16 029 12 500 123 529 0 123 529

Balance at opening 95 000 0 0 16 029 12 500 123 529 0 123 529

Changes in accounting policies 0 0 0 0 0 0 0 0

Balance at opening as restated - 2014.DEC 95 000 0 0 16 029 12 500 123 529 0 123 529

Comprehensive income 0 0 0 -16 029 -7 500 -23 530 0 -23 530 Issue of shares 0 0 0 0 0 0 0 0

Dividends paid 0 0 0 0 0 0 0 0

Transfers 0 0 0 0 0 0 0 0

Issue of convertible notes 0 0 0 0 0 0 0 0

Share-based payments 0 0 0 0 0 0 0 0

Purchase and disposal of treasury shares 0 0 0 0 0 0 0 0

Transactions w ith non-controlling interests 0 0 0 0 0 0 0 0

Other movements 0 0 0 0 0 0 0 0

Balance at closing - 2014.DEC 95 000 0 0 0 5 000 100 000 0 100 000

a Net profit of the year: -7 500

b Changes in the CTA: -16 029

ab