paytech trends 2016

TRANSCRIPT

Challenges and Opportunities in PayTech

Proprietary & Confidential 2014-15

• Anand Ramakrishnan, President and CEO

• Deborah Baxley, Practice Leader, Domain Specialist

Federal Reserve Bank of Atlanta / PeachPay

June 14, 2016

OPUS CONSULTING SOLUTIONS − A SNAPSHOT

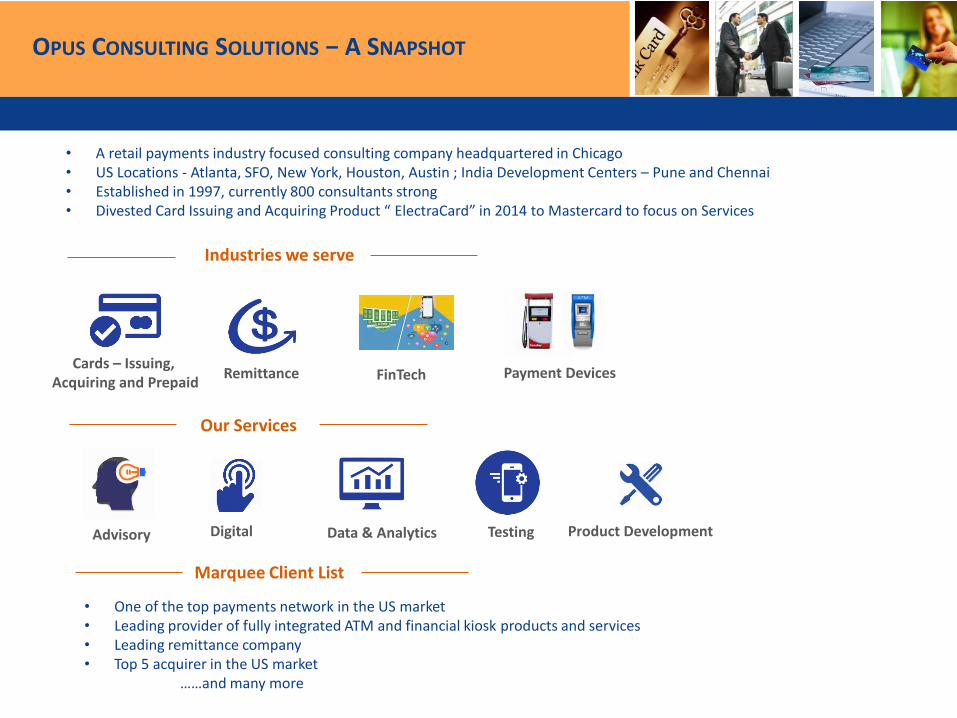

• A retail payments industry focused consulting company headquartered in Chicago• US Locations - Atlanta, SFO, New York, Houston, Austin ; India Development Centers – Pune and Chennai• Established in 1997, currently 800 consultants strong• Divested Card Issuing and Acquiring Product “ ElectraCard” in 2014 to Mastercard to focus on Services

Marquee Client List

Cards – Issuing, Acquiring and Prepaid

Remittance

Industries we serve

FinTech

Our Services

Advisory Digital Data & Analytics Testing Product Development

Payment Devices

• One of the top payments network in the US market• Leading provider of fully integrated ATM and financial kiosk products and services• Leading remittance company • Top 5 acquirer in the US market

……and many more

• The FinTech sector is dominated by PayTech, which promises to change the industry

• Both PayTech and traditional industry face challenges in cooperation, regulation and innovation

• The PayTech landscape comprises invisible payments, financial inclusion, modern payment rails, risk and FinTech banks

– Frictionless payments transform the customer experience, while mPOS disrupts traditional POS solutions across all retail segments

– P2P and prepaid innovations serve underserved, high-fee markets and white spaces

– New payment rails are faster, with much lower operational costs

– Space aged innovations around identity, fraud and risk secure the payments system

– Pure play FinTech banks provide access to the financial service ecosystem

• Industry transformation provides hidden opportunities for payment providers

PayTech leads the FinTech revolution, posing threats and opportunities in mobile, P2P, faster payments and risk management

PayTech Overview

Agenda

• Executive Summary

Overview

– Regional Landscape for PayTech

– SWOT Analysis

• PayTech Landscape

• Effects of PayTech on Financial Services Industry

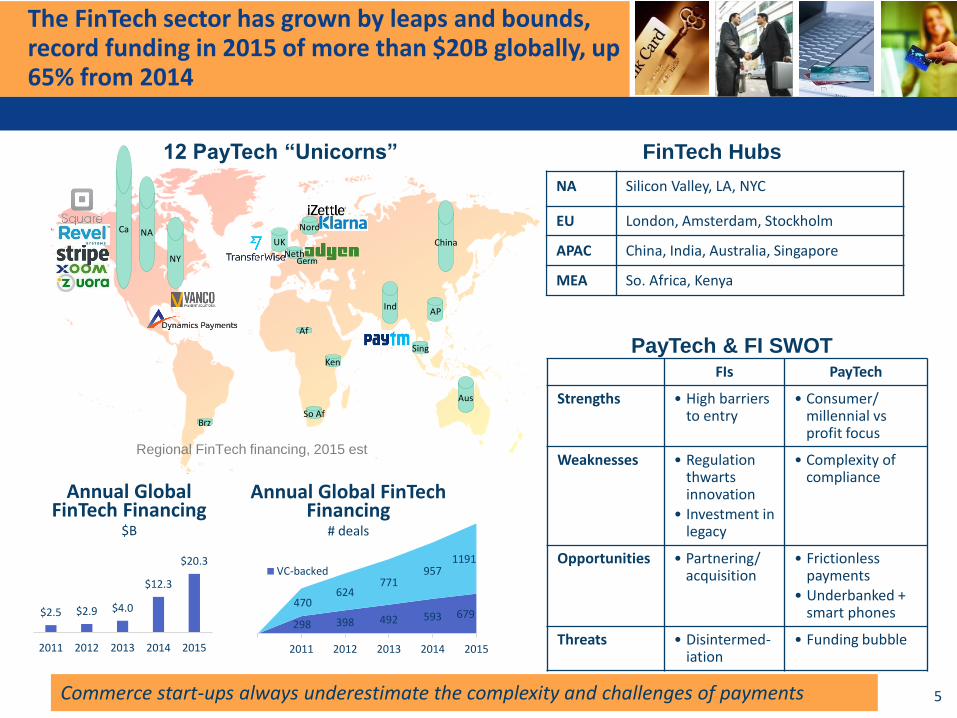

The FinTech sector has grown by leaps and bounds, record funding in 2015 of more than $20B globally, up 65% from 2014

5

NA Silicon Valley, LA, NYC

EU London, Amsterdam, Stockholm

APAC China, India, Australia, Singapore

MEA So. Africa, Kenya

FinTech Hubs

$2.5 $2.9 $4.0

$12.3

$20.3

2011 2012 2013 2014 2015

Annual Global FinTech Financing

$B

298 398 492 593 679470

624771

9571191

2011 2012 2013 2014 2015

Annual Global FinTech Financing

# deals

VC-backed

PayTech & FI SWOTFIs PayTech

Strengths • High barriers to entry

• Consumer/ millennial vs profit focus

Weaknesses • Regulation thwarts innovation

• Investment in legacy

• Complexity of compliance

Opportunities • Partnering/ acquisition

• Frictionless payments

• Underbanked + smart phones

Threats • Disintermed-iation

• Funding bubble

Commerce start-ups always underestimate the complexity and challenges of payments

Ca

Aus

NY

Af

UKNeth

Nord

China

Ind

Sing

Ken

So Af

NA

AP

Brz

Germ

12 PayTech “Unicorns”

Regional FinTech financing, 2015 est

Agenda

• Executive Summary

• Overview

PayTech Landscape

– Invisible Payments

– Modern Faster Payment Rails

– Financial Inclusion

– Risk

– FinTech Banks

• Effects of PayTech on Financial Services Industry

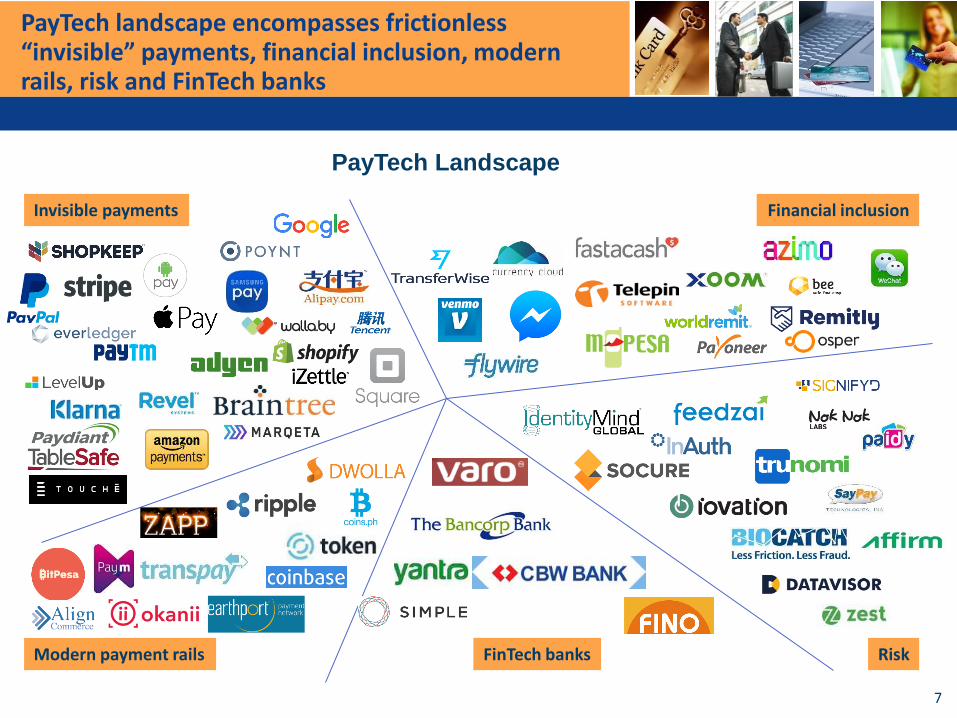

PayTech landscape encompasses frictionless “invisible” payments, financial inclusion, modern rails, risk and FinTech banks

PayTech Landscape

7

Invisible payments

Modern payment rails

Financial inclusion

RiskFinTech banks

Frictionless “invisible” payments streamline the consumer experience, transforming payments to digital

In-app payments • mCommerce in-app payments ease checkout and eliminate friction

• Amazon, AliPay and PayPal leveraging their substantial presence to expand into in-app

• Adyen global payment rails 250 payment methods 187 currencies incl. phone bill, bar coded cards, supporting AirBnB

• Klarna offer M-commerce one-click checkout for apps like Uber, assumes payment risk for delivery use cases

• Paytm is India’s largest mobile commerce platform

Mobile wallet • ApplePay, AndroidPay & SamsungPay realize the security & convenience promise of NFC technology

• Merchant issued wallets such as Starbucks & Dunkin Donuts integrate loyalty and couponing

• Wallaby recommends which card to use to optimize reward points

APIs • Open issuer processing payments APIs let developers integrate payments within their website or apps

• Users sign up within applications, get instant approval, merchants process transaction

IoT • “TOS” operate on smart TVs & smartwatches, & enables mobile payments

• Brillo for low-power IoT devices like lightbulbs & cameras

• Visa prototyping “connected car” to pay for fuel, parking, drive-through, tolls

Invisible Payments

8Frequent payments are moving from cash, to contactless, to invisible

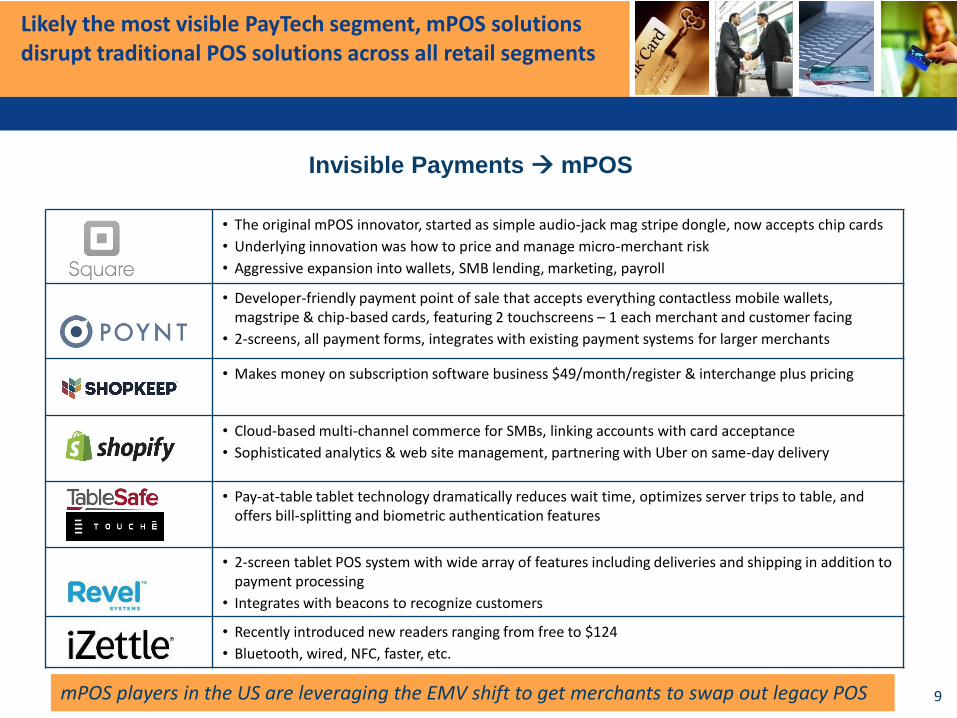

Likely the most visible PayTech segment, mPOS solutions disrupt traditional POS solutions across all retail segments

• The original mPOS innovator, started as simple audio-jack mag stripe dongle, now accepts chip cards

• Underlying innovation was how to price and manage micro-merchant risk

• Aggressive expansion into wallets, SMB lending, marketing, payroll

• Developer-friendly payment point of sale that accepts everything contactless mobile wallets, magstripe & chip-based cards, featuring 2 touchscreens – 1 each merchant and customer facing

• 2-screens, all payment forms, integrates with existing payment systems for larger merchants

• Makes money on subscription software business $49/month/register & interchange plus pricing

• Cloud-based multi-channel commerce for SMBs, linking accounts with card acceptance

• Sophisticated analytics & web site management, partnering with Uber on same-day delivery

• Pay-at-table tablet technology dramatically reduces wait time, optimizes server trips to table, and offers bill-splitting and biometric authentication features

• 2-screen tablet POS system with wide array of features including deliveries and shipping in addition to payment processing

• Integrates with beacons to recognize customers

• Recently introduced new readers ranging from free to $124

• Bluetooth, wired, NFC, faster, etc.

9

Invisible Payments mPOS

mPOS players in the US are leveraging the EMV shift to get merchants to swap out legacy POS

Domestic and international person-to-person and prepaid innovations promise to serve underserved and white spaces, or disrupt high-fee markets

P2P • Payment messaging service M-Pesa >13m users 40% of Kenyans, 42% GDP, no need for bank accounts

• Venmo, wildly popular with millennials, P2P app used to split bar tabs & bills, sending $1b/mo

• Telepin software powers most of the world’s mobile money deployments in emerging markets

Social • Facebook Messenger allows users to send money between debit cards right inside the chat

• Fastacash sends international transfers among social networks e.g. Facebook, WhatsApp or WeChat

• Wildly popular in China, WeChat allows 639m active users to send money or gifts over chat

Remittances • Transferwise sends money with no currency conversion charges, 8X cheaper vs banks, supporting 300 currency corridors, avoiding actual transfers by netting in each market

• Currency Cloud allows any company to offer customers access to foreign exchange through a simple API

• Xoom allows transfers to 50 countries with delivery options including cash, bill payment• Remitly is the US largest digital transfer business charging a fraction of fees compared to

legacy providers• Payoneer provides cross-border transfers, online payments, and reloadable MasterCard

Prepaid • Aims to replace check-cashing services and checking accounts, wants to be where bank branches are not as prevalent

• Prepaid debit card and mobile banking service empowering young people to manage their money responsibly by instilling good financial habits from an early age

Financial Inclusion

10

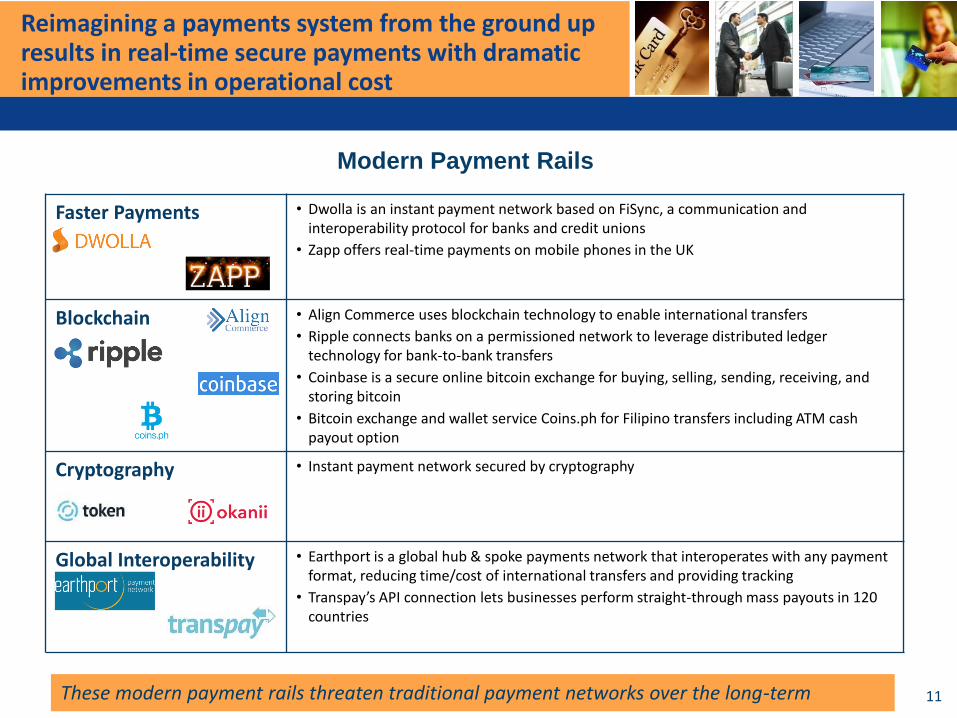

Reimagining a payments system from the ground up results in real-time secure payments with dramatic improvements in operational cost

Faster Payments • Dwolla is an instant payment network based on FiSync, a communication and interoperability protocol for banks and credit unions

• Zapp offers real-time payments on mobile phones in the UK

Blockchain • Align Commerce uses blockchain technology to enable international transfers

• Ripple connects banks on a permissioned network to leverage distributed ledger technology for bank-to-bank transfers

• Coinbase is a secure online bitcoin exchange for buying, selling, sending, receiving, and storing bitcoin

• Bitcoin exchange and wallet service Coins.ph for Filipino transfers including ATM cash payout option

Cryptography • Instant payment network secured by cryptography

Global Interoperability • Earthport is a global hub & spoke payments network that interoperates with any payment format, reducing time/cost of international transfers and providing tracking

• Transpay’s API connection lets businesses perform straight-through mass payouts in 120 countries

Modern Payment Rails

11These modern payment rails threaten traditional payment networks over the long-term

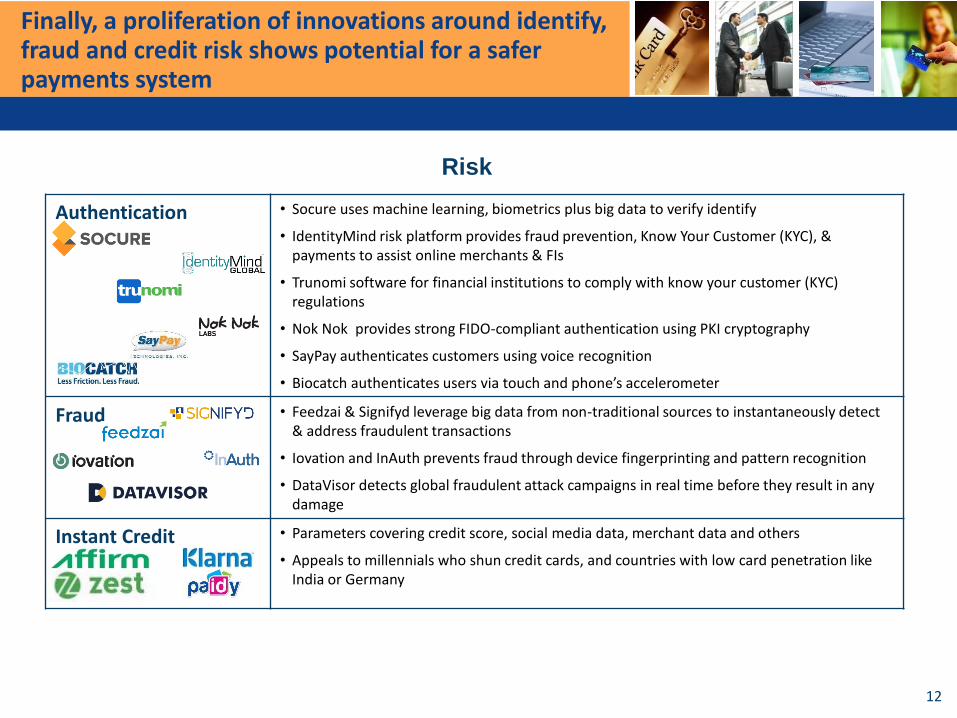

Finally, a proliferation of innovations around identify, fraud and credit risk shows potential for a safer payments system

Authentication • Socure uses machine learning, biometrics plus big data to verify identify

• IdentityMind risk platform provides fraud prevention, Know Your Customer (KYC), & payments to assist online merchants & FIs

• Trunomi software for financial institutions to comply with know your customer (KYC) regulations

• Nok Nok provides strong FIDO-compliant authentication using PKI cryptography

• SayPay authenticates customers using voice recognition

• Biocatch authenticates users via touch and phone’s accelerometer

Fraud • Feedzai & Signifyd leverage big data from non-traditional sources to instantaneously detect & address fraudulent transactions

• Iovation and InAuth prevents fraud through device fingerprinting and pattern recognition

• DataVisor detects global fraudulent attack campaigns in real time before they result in any damage

Instant Credit • Parameters covering credit score, social media data, merchant data and others

• Appeals to millennials who shun credit cards, and countries with low card penetration like India or Germany

Risk

12

As traditional banks become more risk averse, a number of pure play FinTech banks provide access for PayTech start-ups into the financial services ecosystem

White Label Banking • The Bancorp Bank offers “Banking as a Service,” supporting Simple all-digital checking account designed for mobile plus first-rate mobile banking tools

Banks Powering PayTech • CBW plus its technology arm, Yantra, aims to reinvent banking and it is the bank powering “Moven”

• Varo Money is a mobile-only banking app that offers financial advice, with the unusualstated intention of seeking a banking license

• FINO Paytech is Indian financial inclusion bank using biometric & smart card technology for micro customers especially in rural areas, now classified as a new “payments bank” by RBI

FinTech Banks

13

Agenda

• Executive Summary

• Overview

• PayTech Landscape

Effects of PayTech on Financial Services Industry

The PayTech revolution will reshape our industry by cutting costs, improving quality, and innovating around risks

15Never mind if PayTech fails to take over the world, its emergence is changing the face of payments

How will PayTech impact traditional players?

Consolidation: In-app payments push transactions to “lodged” card, whose wallet share increases -differentiators like card brand & design decline

Potential Scenarios:

Fragmentation: Digital wallets displace physical cards & optimize card usage, proliferating niche / merchant issued cards, splintering wallet share

Displacement: Customers elect POS financing, credit card usage erodes as transactional users migrate to payment seamlessly linked to bank accounts

Venture capital investment • Santander, HSBC, Sberbank, BBVA Ventures

Accelerator programs • ATDC, FinTech Innovation Lab, Barclays, Citi Ventures Plug and Play FinTech Program, Level39, Westpac Innovation Challenge

Collaboration • UBS Blockchain Innovation Lab, BNY Mellon MyIdea, RBS, Bank Leumi, ING FinTech Village

Consortium • R3

Acquisition • First Data & Clover, PayPal & Paydiant, Xoom

FI and Processor Responses

INDIA OPERATIONS: PUNE AND CHENNAI CORPORATE HQ: CHICAGO

THANK YOU