payday lending in london - community-based …€¦ · · 2014-02-06this project was funded by...

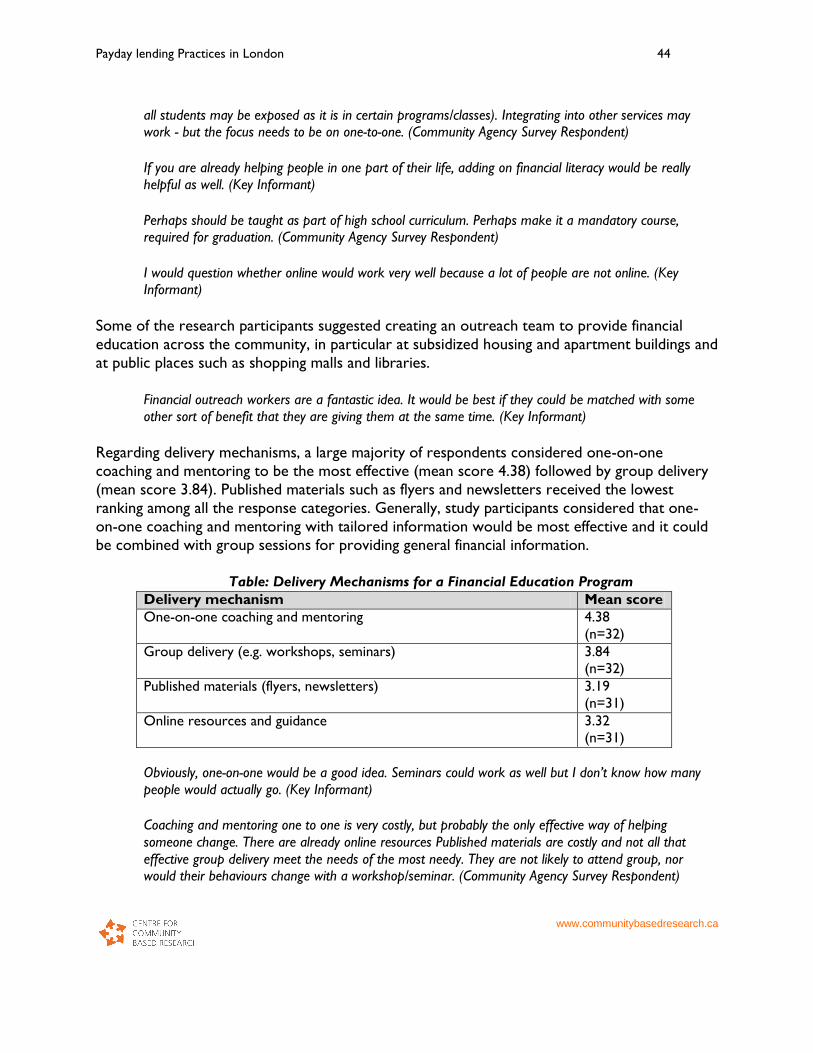

TRANSCRIPT

PAYDAY LENDING IN LO NDON

RESEARCH REPORT

April 2012

Prepared BY:

Commissioned by:

73 King Street West, Suite 300 Kitchener, Ontario N2G 1A7

Phone: (519) 741-1318 Fax: (519) 741-8262 E-mail: [email protected]

www.communitybasedresearch.ca

409 King Street London, Ontario N6B 1S5

Phone: (519) 438-1723 Fax: (519) 438-9938 www.uwlondon.on.ca

Payday lending Practices in London 2

www.communitybasedresearch.ca

United Way Staff and Volunteers

Research Team

Yasir Dildar, Team Leader Liliana Araujo, Team Member Sarah Marsh, Team Member

Research Lead Organization

Centre for Community Based Research (CCBR) 73 King Street West, Suite 300 Kitchener, Ontario N2G 1A7

Acknowledgements

The following students/volunteers helped in different tasks to complete this research study. Ayesha umme-jihad Elvis Lee Sara Naz

This project was funded by the United Way London-Middlesex. The views and opinions

expressed in the report do not necessarily reflect those of the United Way.

Payday lending Practices in London 3

www.communitybasedresearch.ca

TABLE OF CONTENTS

EXECUTIVE SUMMARY .................................................................................................. 4

1. Introduction ................................................................................................................... 6

1.1 Payday lending......................................................................................................................................... 6 1.1.1 Payday lending in Canada and Ontario ..................................................................................................................... 6

1.2 Overview of the study .......................................................................................................................... 7 1.2.1 Research purpose and quesions .................................................................................................................................. 7

1.2.2 Research methods ............................................................................................................................................................. 8

1.2.3 Data analysis ................................................................................................................................................................... 13

2. Payday lending practices ............................................................................................. 14

2.1 Payday lenders in London ................................................................................................................. 14 2.1.1 Perception about payday loan and payday lenders .............................................................................................. 14

2.1.2 Relationship of payday lenders with other financial institutions ....................................................................... 15

2.1.3 Profits of payday lenders in London .......................................................................................................................... 16

2.2 Payday loan borrowers in London .................................................................................................. 16 2.2.1 Borrowers’ experience with banking system .......................................................................................................... 17

2.2.2 Source of information and frequency of borrowing payday loans .................................................................... 21

2.2.3 Reasons for borrowing payday loans ........................................................................................................................ 23

2.2.4 Satisfaction with payday lenders ................................................................................................................................ 26

2.2.5 Impact of borrowing payday loans ............................................................................................................................ 30

3. Financial education program ...................................................................................... 35

4.1 Knowledge about existing financial education programs ........................................................... 37

4.2 Need for a financial education program ........................................................................................ 39

4. Suggestions for a financial education program ........................................................ 43

4.1 Preferred settings and delivery mechanisms ................................................................................ 43

4.2 Financial education program promotion ....................................................................................... 45

4.3 Key locations and target population ............................................................................................... 45

4.4 Implementing partners ....................................................................................................................... 46

5. Conclusion .................................................................................................................... 50

Appendices ....................................................................................................................... 51

Payday lending Practices in London 4

www.communitybasedresearch.ca

EXECUTIVE SUMMARY

This is the research report of payday lending practices in London. This study was commissioned

by the United Way of London and Middlesex and conducted by the Centre for Community Based Research (CCBR).

The purpose of this study was to explore payday lending practices in London with focus on

gathering information in three main areas. First, this study sought information about payday

lenders. Second, this research explored information about payday loan borrowers such as who

they are, why they borrow from payday lenders and how satisfied they are with payday lenders

as well as the impact that borrowing from payday lenders has on their lives. Lastly, this research

study also gathered information on financial education in London.

Multiple methods were used in this study. Main methods included: literature review; borrower

survey (face-to-face n=20; online n=53); an online survey for community agencies (n=39); key

informant interviews (n=5) and case studies which included interviews with borrowers and a

person they identified as knowing about their payday lending use (n=3).

The following are main findings of the study:

Payday lenders

There are many payday lending outlets in London and their number is rising.

Payday lenders are catering to individuals who are in need of money when unexpected

emergencies arise.

Payday lenders provide a convenient and quick access to money.

Generally, payday lenders were perceived as predatory. Those representing the

Canadian Payday Lending Association expressed that the payday lending industry is

regulated and often misperceived.

Payday loan borrowers

Payday loan borrowers in London were described as low income individuals; dependent

on Ontario Disability Support Program (ODSP), Ontario Works (OW) or social

assistance; as well as those who have a bad credit history, thus, not having access to a

loan through a bank. Some study participants said that borrowers belong to all income groups and are not

limited to the characteristics mentioned above.

The majority of borrowers who completed the survey had interacted with a bank (i.e.

had some kind of a bank account)

Most often, borrowers heard of payday lenders through family or friends or sign boards.

The most common reasons borrowers gave for making the switch to payday lending

were: having a bad credit history and the lack of small loans from banks. Lack of

awareness of the banking system was also a reason why payday loans are used rather

than banks.

Payday lending Practices in London 5

www.communitybasedresearch.ca

Borrowers identified having used multiple services at payday lending stores, including

cheque cashing, pre-paid credit cards and money transfers.

The majority of borrower survey respondents did not rollover on a loan.

The most common reasons for borrowing money from payday lenders were: to meet

basic needs, pay bills and rent.

The majority of borrowers received a contract when they obtained their loan and

reported that the loan was helpful and good for emergencies. However, they did not

like the high interest rates and fees associated with payday loans.

Most reported being charged 20-25% interest over two weeks, while some reported

being charged more. Additional services offered by payday lenders were also seen as

being very expensive.

Mostly negative impacts were identified by borrowers as a result of borrowing from

payday lenders; including: falling into a debt trap; dropping monthly income; and high

amounts of stress.

Financial Education

A vast majority of study participants identified the need for a payday loan alternative.

Providing a loan with a low interest rate and fees and clear information were the most

important elements to consider while developing a payday alternative.

Respondents suggested that there is a need for a community-wide financial education

program in London, believing that it would benefit the community.

Respondents rated integrating financial literacy into other existing programs as the most

effective delivery setting. The least preferred delivery setting was via the internet.

The most preferred delivery mechanism was one-on-one counselling with the least

preferred being via the internet again.

Providing the program close to where people live as well as providing incentives (e.g.

food, childcare, transportation costs, etc.) were identified as the best promotion

strategies.

In terms of location, low income neighbourhoods should be considered, but there is

need across the city and in rural areas as well.

For youth, delivery in schools was suggested and for individuals on ODSP or OW,

information about the program could be included with their cheques.

Suggested organizations and agencies to lead such a program include the municipal

government, OW/ODSP, and community agencies that serve people living in poverty,

including the United Way of London & Middlesex. Other community agencies and

stakeholders such as, banks, credit unions and payday lenders should be involved in

implementing a community-wide financial education program.

Payday lending Practices in London 6

www.communitybasedresearch.ca

1. INTRODUCTION

This report addresses the findings of a research study conducted by the Centre for

Community-Based Research (CCBR) on behalf of United Way of London. The United Way of London aims to try to understand the effects of payday lending on people who use payday loan.

The purpose of this research was to gather information about the nature and location of

existing payday lending services in London; the nature and experiences of payday loan

borrowers in London; education that is available for these borrowers; as well as alternatives

and policy implications within London.

1.1 PAYDAY LENDING

Payday loans are short-term loans provided against a client's evidenced income. Borrowers take

out small loans of up to 50% of their next paycheque during situations in which they require

money before their next paycheque is due. Normally, the borrower has to pay back the loan

within the following two weeks as well as pay any additional fees, charges, and/or interest they

incurred. Besides loan interest, there are numerous other fees that payday lenders can charge

borrowers, including: set-up fees, administration fees, broker’s fees, collection fees, early

repayment fees, loan repayment fees, non-sufficient fund charges, roll-over or loan renewal

fees. Lenders typically require borrowers to provide proof of regular income, a permanent

address, an active bank account, and in some cases, post-dated cheques for the date on which

the loan should be paid in full. Many payday lenders also provide other services such as

telephone card, money transfer, pre-paid credit card, gift card, buy gold and post box services.

1.1.1 PAYDAY LENDING IN CANADA AND ONTARIO

Starting in the 1990s, payday loans became increasingly popular in Canada. Approximately 1,635

stores operate in Canada, with over 750 in Ontario (Ontario Payday Lending Industry, 2009)1.

The average loan amount is $280 borrowed for a period of 10 days (Canadian Payday Loan

Association, 2009) and the total payday loan volume in Canada is widely estimated to be

approximately $2 billion per annum (Ontario Payday Lending Industry, 2009).

Payday lenders in Canada and Ontario operate within a legislative framework. In the spring of

2007, the Canadian government amended the anti-usury section of the Criminal Code of

Canada, section 347, to exempt payday lenders from the maximum 60 % Annual Percentage

Rate and to give provinces and territories the authority to implement regulations independently

1 Established in 2004, the CPLA represents 630 businesses providing payday loans and/or cheque cashing services across Canada. With approximately 1,635 retail stores in Canada, 630 are members of the CPLA. The CPLA’s mandate is to work

with the federal and provincial government with the aim of developing a national regulatory framework that allows industry

viability and consumer protection.

Payday lending Practices in London 7

www.communitybasedresearch.ca

(Ministry of Government Services, 2009). In 2008, Ontario’s Payday Loans Act was passed and

most elements were implemented during 2009 (Ministry of Consumer Services, 2010).

The main elements of this Act are as follows:

Payday lenders and loan brokers are required to be licensed.

Roll-over loans are prohibited.

Payday loan borrowers have a two-day "cooling off" period to cancel a loan with no

reason without incurring a penalty.

An Ontario Payday Lending Education Fund will be established and paid for by licensees.

Maximum total cost for borrowing a payday loan in Ontario is $21 per $100 borrowed.

Proponents of payday lending, such as the Canadian Payday Loan Association, argue that payday

loan stores provide a product for consumers who have a short-term financial crunch, and

without this product many of these consumers would have had no option aside from turning to

underground money lenders. They also establish that banks fail to meet the financial needs of low-income Canadians and the likelihood of a bank refusing to open an account is 1.5 to 2

times higher for people with lower income, education, and age – the target market for payday

lenders. (Buckland et al., 2007)

However, the critics, including the Public Interest Advocacy Centre, term this practice as

exploitative, taking advantage of people's financial hardships. Critics claim that the payday

lending industry depends heavily on repeat business and that low-income borrowers are more

likely to be trapped in a 'debt cycle' because the short pay-back period makes it difficult to

repay the entire amount owing.

1.2 OVERVIEW OF THE STUDY

The Centre for Community Based Research (CCBR) was contracted to carry out the payday

lending research study. CCBR is an independent, not-for-profit organization established in

1982 (www.communitybasedresearch.ca). Located in Kitchener, Ontario, CCBR is committed

to social change and the development of communities and human services that are responsive

and supportive, especially for people with limited access to power and opportunity.

1.2.1 RESEARCH PURPOSE AND QUESTIONS

The overall purpose of the research was to look at the existing payday lending practices in

London by gathering information about payday lenders, payday loan borrowers, as well as information about financial education available within the community. The research study used

multiple methods to answer the following main questions:

Information about payday lenders

Where are the payday lenders located in London?

Payday lending Practices in London 8

www.communitybasedresearch.ca

What are the profits of payday lenders in London?

What are the payday lenders’ relationships with other financial institutions (e.g. banks)?

Information about payday loan borrowers

Who are the payday loans borrowers in London?

What are the main reasons that motivate the payday loan borrowers to borrow for the first time?

o Why do the payday loans borrowers continue borrowing from payday lenders?

To what extent are the payday loans borrowers satisfied with payday loans/lenders?

What is the impact of borrowing from payday lenders on payday loan borrowers?

Financial education

What are the existing financial education programs in London?

To what extent are the existing financial education programs meeting the needs of London community?

To what extent is there a need for a community-wide financial education program?

o If there is a need for a community-wide financial education program, what should

be its key components?

1.2.2 RESEARCH METHODS

The project utilized several ways of gathering information involving different stakeholder

perspectives. Use of a series of methods enhances triangulation of research results and

increases the rigour of the findings. Main methods included:

LITERATURE REVIEW

The research team conducted a review of available literature on payday lending in Ontario,

Canada and beyond. The literature review, in particular, helped in developing data collection

tools that were used to gather information from payday loan borrowers, community agencies

and key informants.

PAYDAY LOAN BORROWER SURVEY

A survey of payday loan borrowers was conducted. The quantitative survey (with a few

qualitative questions) consisted of closed, categorical, and scale-based questions. The survey

was conducted to explore the diverse motivations or reasons for using payday loans. Payday

loan borrowers also provided feedback about their level of satisfaction with payday lenders and

impact of using payday loans. Participants for the face-to-face interviews and online survey were

recruited with the help of the United Way of London and Middlesex and its member agencies.

A total of 73 surveys were completed (n=20 face-to-face and n=53 online). The majority of

respondents were in the age range of 31-40 years. More females (61%) than males (39%)

completed the survey. Three-fourths of survey respondents (75%) have completed a secondary

Payday lending Practices in London 9

www.communitybasedresearch.ca

school diploma and/or a diploma or certificate from a college or technical school. Only two

survey respondents reported completing Master’s degrees.

In terms of income sources, more than half of the survey respondents were receiving support

from Ontario Works (OW) or the Ontario Disability Support Program (ODSP). Less than one-

third (29%) were working full-time and one-tenth of respondents were working part-time.

Sixty-three per cent of survey respondents reported their income to be less than $20,000 per

annum. Only 14% earned more than $40,000 a year.

3%

13%

41%

28%

15%

20 years or younger

21-30 31-40 41-50 51-60

Borrower Survey Distribution of respondents according to their

age (n=68)

39%

61%

Male Female

Borrower Survey Distribution of respondents according to their

gender (n=69)

25 26

7

2

8

Completed diploma from secondary school (high

school)

Completed diploma or certificate from college

or technical school

Completed university undergraduate degree

(e.g. BA)

Completed university graduate or professional

degree (MA)

Other

Borrower Survey Distribution of respondents according to their formal education (n=68)

Payday lending Practices in London 10

www.communitybasedresearch.ca

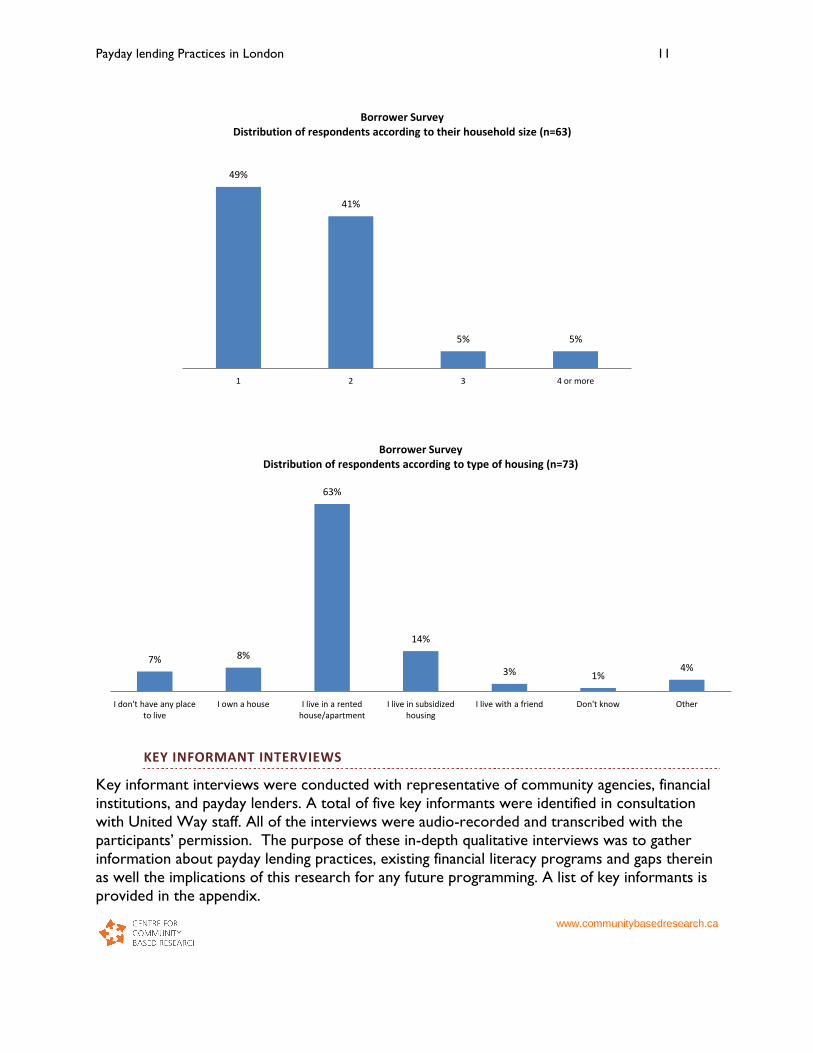

Nearly half (49%) of survey respondents were living alone, 41% with another adult and the

remaining 10% were living with more than 3 adults in the household. Most of the respondents

(63%) were living in a rented house/apartment; 14% in subsidized housing; 7% had no place to

live and only 8% reported owning their house.

27%

29% 29%

10%

4%

1%

Ontario Works ODSP Full-time work Part-time work Unemployed Pension (retired)

Borrower Survey Distribution of respondents according to their source of income (n=69)

26%

37%

10% 13%

10%

4%

0----less than 10,000 10,000----20,000 21,000---30,000 31,000----40,000 41,000----50,000 More than 50,000

Borrower Survey Distribution of respondents according to their income (n=68)

Payday lending Practices in London 11

www.communitybasedresearch.ca

KEY INFORMANT INTERVIEWS

Key informant interviews were conducted with representative of community agencies, financial

institutions, and payday lenders. A total of five key informants were identified in consultation

with United Way staff. All of the interviews were audio-recorded and transcribed with the

participants’ permission. The purpose of these in-depth qualitative interviews was to gather

information about payday lending practices, existing financial literacy programs and gaps therein

as well the implications of this research for any future programming. A list of key informants is

provided in the appendix.

49%

41%

5% 5%

1 2 3 4 or more

Borrower Survey Distribution of respondents according to their household size (n=63)

7% 8%

63%

14%

3% 1% 4%

I don't have any place to live

I own a house I live in a rented house/apartment

I live in subsidized housing

I live with a friend Don't know Other

Borrower Survey Distribution of respondents according to type of housing (n=73)

Payday lending Practices in London 12

www.communitybasedresearch.ca

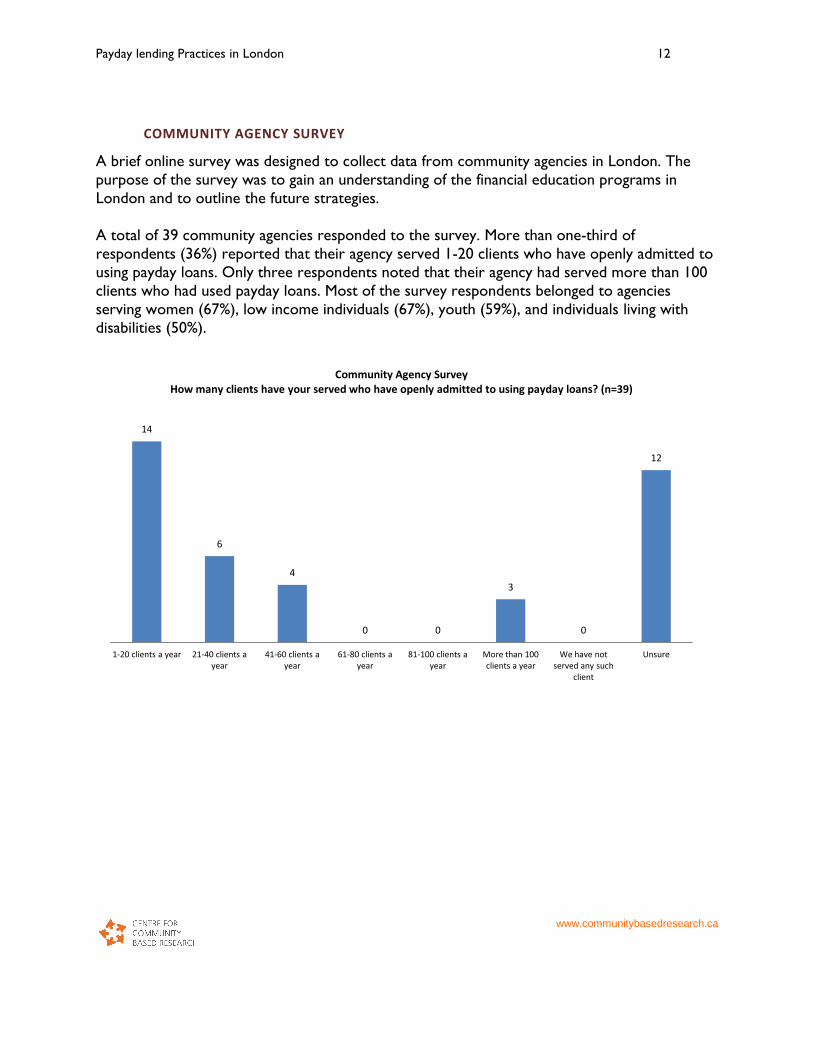

COMMUNITY AGENCY SURVEY

A brief online survey was designed to collect data from community agencies in London. The

purpose of the survey was to gain an understanding of the financial education programs in

London and to outline the future strategies.

A total of 39 community agencies responded to the survey. More than one-third of

respondents (36%) reported that their agency served 1-20 clients who have openly admitted to

using payday loans. Only three respondents noted that their agency had served more than 100

clients who had used payday loans. Most of the survey respondents belonged to agencies

serving women (67%), low income individuals (67%), youth (59%), and individuals living with

disabilities (50%).

14

6

4

0 0

3

0

12

1-20 clients a year 21-40 clients a year

41-60 clients a year

61-80 clients a year

81-100 clients a year

More than 100 clients a year

We have not served any such

client

Unsure

Community Agency Survey How many clients have your served who have openly admitted to using payday loans? (n=39)

Payday lending Practices in London 13

www.communitybasedresearch.ca

CASE STUDY

Three case studies of payday loan borrowers were conducted. Each case study involved an in-depth interview with a payday loan borrower and one other person who was aware of his/her

payday loan borrowing experience.

1.2.3 DATA ANALYSIS

Data analysis was carried out collaboratively by the research team to ensure that study themes

were identified and confirmed by multiple team members. The web survey data was entered

and analyzed using SPSS and MS Excel while the qualitative data from key informant interviews,

case study, and literature review was analyzed using content analysis.

59%

67% 67%

47%

38% 41%

32%

23%

50%

Youth Women Low income individuals

Children Aboriginal Newcomers Seniors LGBTQ Individuals living with disabilities

Community Agency Survey What population group does your agency primarily serve? (n=34)

Payday lending Practices in London 14

www.communitybasedresearch.ca

2. PAYDAY LENDING PRACTICES

This main section of the report provides multiple perspectives of payday lending practices in

London and provides information about payday lenders as well as payday loan borrowers.

2.1 PAYDAY LENDERS IN LONDON

According to the 2011 Census, the population of London, Ontario is around 366,151. There

are many payday loan outlets in London. We have compiled a list of 35 such payday loan outlets

in London and area. See Appendix for list of payday loan outlets and their location in London.

This list by no means is an exhaustive list of all payday lenders as there may be pawnshops and

other outlets that provide similar loans.

2.1.1 PERCEPTION ABOUT PAYDAY LOAN AND PAYDAY LENDERS

All the research participants agreed that payday lenders cater to individuals who need money in

times of emergencies and who cannot or do not access other financial institutions because of

eligibility criteria. Study participants also noted that payday lenders provide fast, friendly and

convenient service to their customers.

They make it really easy for people to get money. Especially people who are living in survival mode, it’s

quick and easy access to cash. (Key Informant)

Most of the study participants perceived that payday lending practices are predatory, expensive

and costly for borrowers. Key informants indicated that payday lenders are not meeting the

need but exploiting the situation of needy people. They term payday loans as notorious for high

interest rates and penalties. A few study participants called payday loans as ‘legitimized loan

shark service’. For many research participants, payday loans are the last option for most people

because payday lenders charge a very high interest rate (due to high risk nature of the loans).

Payday lenders, in their opinion, target low income individuals and exploit their situation.

Research participants believed that although there are certain regulations (i.e. explicit display of

interest rate/cost, cap on interest rate, etc), many payday lenders do not seem to observe those regulations. Study participants noted that despite provincial regulations, the payday loan

industry charges excessive fees for loans and cheque cashing.

It’s predatory; they are really hitting the lowest of the lower people that are in desperate situations. (Key

Informant)

They prey on individuals that have these strains or stresses in their lives. They can say that they’re

providing a service that is needed and sure... so is a drug dealer, I guess. But that doesn’t make it right.

(Key Informant)

Payday lending Practices in London 15

www.communitybasedresearch.ca

Loans provided at exorbitant interest rates to individuals who do not have the credit capacity to obtain

loans through institutional lenders. (Community Agency Survey Respondent)

Key informants representing payday lending association noted that there is a misperception

about payday lenders and payday loans. They noted that payday lending is a regulated industry

that provides much needed help to individuals requiring money in emergencies. They said that

payday lenders provide a lot of financial educational resources to its customers, both in print

and online. Payday lenders, in particular members of the CPLA, provide free services to their

customers to better manage their finances.

Payday lending is a regulated industry. If a payday lender wasn’t available for individuals to borrow that

$200 or $300, where would they turn? Misinformation about the industry does no service to individuals

who are in need of this product. (Key Informant)

About the interest rate and hidden fee, it was pointed out that with new provincial regulations

introduced in 2010, all the payday lenders are required to display the inclusive cost of loan

explicitly. The combined fee and interest should be no more than 21%. CPLA representatives

welcomed any effort that would ensure adherence to the new regulation and deal with payday

lenders who do not follow the interest/cost cap regulation.

2.1.2 RELATIONSHIP OF PAYDAY LENDERS WITH OTHER FINANCIAL INSTITUTIONS

Study participants provided their perceptions about the payday lenders’ relationships with other financial institutions such as banks. For a few community agency survey respondents, payday

lenders borrow money from banks to provide payday loans to low income individuals at a very

high interest rate. One respondent noted that banks actually operate payday lending stores

because they cannot provide service to individuals who have credit issues. Most of the key

informants reported that there is only a business/operational relationship between payday

lenders and banks. Generally, borrowers need to have a bank account that provides a

guarantee for repayment to payday lenders (usually with a post-dated cheque or pre-authorized

debit).

I imagine the payday lenders borrow money from banks and in turn borrow the money to others. (Community Agency Survey Respondent)

They are run by banks that do not otherwise want to provide services to people with credit issues. (Community Agency Survey Respondent)

For payday loans you have to have a “normal” bank account because you need to prove that your

paycheque or ODSP or CPP payment is going in somewhere – in order for them [payday lenders] to be

sure that they are going to get their money back. (Key Informant)

Some payday loan companies of course deal with the banks because the deposits have to be made by

the consumer borrowing payday loan product. Access has to be made to customer’s account, the

Payday lending Practices in London 16

www.communitybasedresearch.ca

customer decides if they want their account debited for the repayment of the loan. (Key Informant)

2.1.3 PROFITS OF PAYDAY LENDERS IN LONDON

There are no statistics available about the exact profits/costs of payday lenders. For many key informants and community agency survey respondents, payday lenders charge very high interest

rate and fees to provide small, short-term loans and, as a result, earn very good money. They

cited that rapid growth of payday lenders in many neighbourhoods speaks to the profitability of

the payday loan business.

Key informants representing CPLA as well as our review of a few research studies indicate that

payday lending is a risky business and cost of providing payday loans is very high. Payday lenders

have to incur a number of costs such as operating costs (e.g. staff salaries, computer systems,

rent), loan capital cost, and the cost of bad debts; the latter is considered to be the largest cost of all. According to a study conducted by Deloitte in 2008, the cost of providing a $100 payday

loan in Ontario was $20.63 According to CPLA representatives, the volume of payday loan

transactions creates profitability for payday lenders as opposed to interest/fee of providing

individual loans.

Money Mart for example is owned by the Dollar Financial Group which has created payday loan stores

in the US, Canada, England, Poland, Finland, all over the world - and their profitability in a particular

community, I wouldn’t even hazard to guess. (Key Informant)

Anecdotally, they are making very good money because these places are everywhere. They opened up a

payday loan place in a closed Blockbuster store. These places are everywhere. If they figure a certain

percentage of people don’t pay them back. It’s the $20 fees that they charge time and time again that

gives them money. (Key Informant)

I don’t know what sort of revenue they make. Suffice to say there are a number of them in London so

the revenue must be pretty decent. But they are still taking on some risk themselves, albeit very small, I

think. (Key Informant)

There’s a high cost to providing this product [payday loan] and there’s a high risk. Operating expenses

are huge so when you roll all that together it is not that profitable. (Key Informant)

2.2 PAYDAY LOAN BORROWERS IN LONDON

A study of consumer aspects of payday lending (2007) found that Canadian payday loan

consumers are more likely to have lower family incomes than non-consumers; are more likely

to be fully employed but have lower education levels; and, are more likely to live in larger

families with children. In addition to having lower income, these consumers are less likely to

have other sources of borrowing such as credit cards or financial reserves.

Payday lending Practices in London 17

www.communitybasedresearch.ca

There are no statistics available about the payday loan borrowers in London. Research

participants, however, provided broad demographic characteristics of individuals who typically

borrow from payday lenders in London. These characteristics confirm findings from other

studies conducted in Canada and elsewhere. Generally, study participants believe that payday

loan borrowers are individuals (more men than women) with low income, dependent on

ODSP/OW or social assistance, and those who do not have access to banking loan because of

their bad credit history. With little income and no other option available to get money, low

income individuals tend to borrow from payday lenders. Following are some of the excerpts

from community agency survey responses and key informant interviews explaining ‘who are the

payday loan borrowers in London’.

A lot of customers I would assume are on low income wages or government assistance. (Community

Agency Survey Respondent)

Individuals receiving OW can get their cheques cashed before the date. So, the OW cheques come out

and they are not cashable right away but they can cash them at the payday lending stores. (Key

Informant)

The poor, people with mental health issues who seek immediate gratification. (Community Agency

Survey Respondent)

People with minimal paying jobs, have additions, drug, alcohol or gambling. (Community Agency Survey

Respondent)

People who are generally on fixed incomes and have either maxed out or do not have access to more

traditional loans such as line of credits, overdraft or credit cards. (Community Agency Survey

Respondent)

Those who cannot obtain loans at a bank, trust company or credit union. Those who may not be able to

access credit cards. (Community Agency Survey Respondent)

Only a few study participants considered that payday loan borrowers belong to all income

groups and they are usually the individuals who have low financial literacy and do not know how

to manage their finances.

Moderate to higher income persons who lack the ability to manage finances. (Community Agency Survey

Respondent)

They typically are not good fiscal managers. Typically they’re not good at managing their existing money.

(Key Informant)

2.2.1 BORROWERS’ EXPERIENCE WITH BANKING SYSTEM

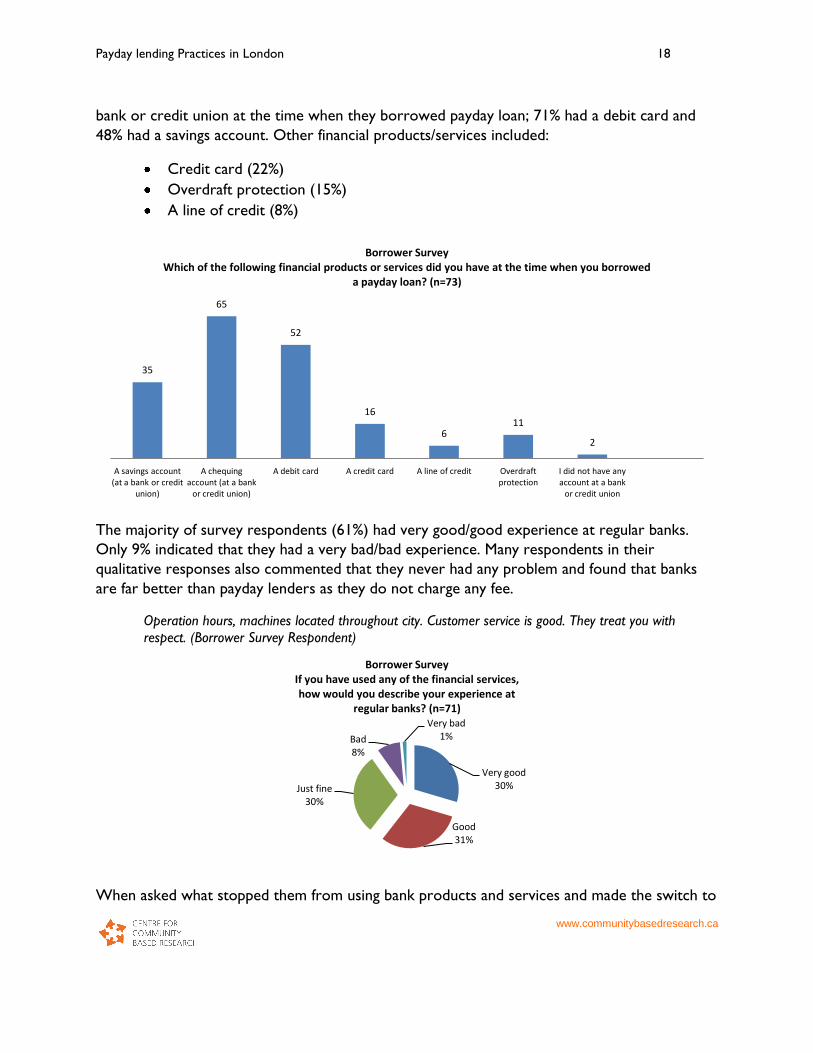

Except for two respondents, all others had some experience with the banking system (i.e. had

some kind of bank account). A large majority (89%) reported having a chequing account at a

Payday lending Practices in London 18

www.communitybasedresearch.ca

bank or credit union at the time when they borrowed payday loan; 71% had a debit card and

48% had a savings account. Other financial products/services included:

Credit card (22%)

Overdraft protection (15%)

A line of credit (8%)

The majority of survey respondents (61%) had very good/good experience at regular banks.

Only 9% indicated that they had a very bad/bad experience. Many respondents in their

qualitative responses also commented that they never had any problem and found that banks

are far better than payday lenders as they do not charge any fee.

Operation hours, machines located throughout city. Customer service is good. They treat you with

respect. (Borrower Survey Respondent)

When asked what stopped them from using bank products and services and made the switch to

35

65

52

16

6 11

2

A savings account (at a bank or credit

union)

A chequing account (at a bank

or credit union)

A debit card A credit card A line of credit Overdraft protection

I did not have any account at a bank

or credit union

Borrower Survey Which of the following financial products or services did you have at the time when you borrowed

a payday loan? (n=73)

Very good 30%

Good 31%

Just fine 30%

Bad 8%

Very bad 1%

Borrower Survey If you have used any of the financial services, how would you describe your experience at

regular banks? (n=71)

Payday lending Practices in London 19

www.communitybasedresearch.ca

payday loans, majority (55%) reported bad credit history as the main reason followed by non-

availability of small loans at banks (45%). Fourteen per cent of respondents did not even know

that they could borrow money from a bank. “Thought I have to have land (possessions) to

borrow”, commented one survey respondent. Thirteen per cent respondents indicated that too

much paper work is required using services at banks. Other reasons included:

Unfriendly staff (11%)

Location of banks (8%)

Hours of operation (7%)

Not having an ID (6%)

A few survey respondents commented that banks do not treat low income individuals with

respect and dignity. Moreover, they noted that banking services are more supportive and

accessible to those belonging to higher income levels. In their view, banks are not willing to

support and help those living in the margins of society.

Banks treat people with little money like they are less of a person. You have to meet certain income

levels to access services, instead of adjusting services based on income levels. (Borrower Survey

Respondent)

You need an income of over $40,000 a year to borrow from most banks and it cannot be social

assistance or child tax. (Borrower Survey Respondent)

A large number community agency survey respondents and key informants noted that people

borrow from payday lenders and not from banks or credit unions because of their poor credit

history or because they do not meet the eligibility criteria (e.g. lack of ID) for bank loans.

Sometimes the paperwork involved in getting loan approval also deters people from seeking

bank loans. In a few cases, previous bad banking experiences may cause individuals to switch

from banks to payday lenders. Many individuals with low income do not feel that bank staff

treat them with respect.

Banks and credit unions won't lend to people who live at or below the poverty line. They also don't lend small amounts. (Community Agency Survey Respondent)

They may not be able to open bank accounts due to lack of identification or be overwhelmed by some of

the bureaucratic processes of applying for different places such as these. (Community Agency Survey Respondent)

They do not get any help from banks or credit unions. They mistrust that system and usually had a bad

experience with bank or credit union. (Community Agency Survey Respondent)

These clients don't always get respect from the bank when they try to resolve a situation or make

themselves heard. I have heard many stories of people being treated dreadfully because OW/ODSP is

Payday lending Practices in London 20

www.communitybasedresearch.ca

their source of income. (Community Agency Survey Respondent)

Lastly, lack of information about the availability of bank loans and the cost of borrowing from

payday lenders were identified as two other main reasons that many individuals switch from

banks to payday loans. Many people have misperceptions about opening a bank account, banking

fees and doing business with banks and credit unions, including, for example, overdraft

protection that banks offer.

For many of them, they are unaware of the laws that are out there that actually say that the banks are

relatively flexible on what we look for ID purposes and for opening accounts. In fact, we have to have a

low fee account to offer to customers. I think part of that is financial education – they don’t have to go

to these places to cash their ODSP cheques or whatever, they can go to any of the banks and do it that

way. (Key Informant)

There’s a perception that if you owe one bank money, the others will know about it. That’s not the truth

at all. If you only owe a couple service charges, we don’t put anything on the credit bureau or anything

like that; you can just go to bank and open an account there. (Key Informant)

One community agency survey respondent eloquently summarized the reasons for using payday loans instead of banks and credit unions. There are a number of reasons including:

past problems with banks---owe service charges such as ones for bounced checks;

garnishment issues on bank accounts;

costs of maintaining bank accounts;

poor treatment for those who viewed as poor; and

lack of educational material about the true costs of using pay day loans industry.

Payday lending Practices in London 21

www.communitybasedresearch.ca

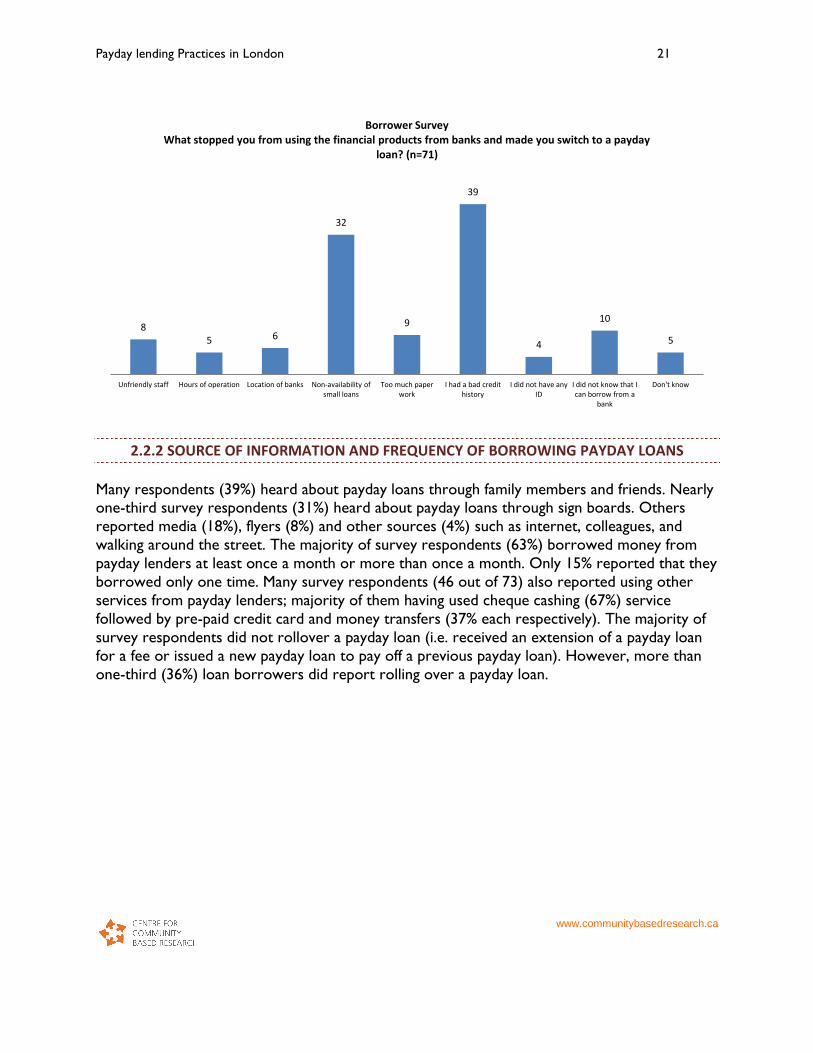

2.2.2 SOURCE OF INFORMATION AND FREQUENCY OF BORROWING PAYDAY LOANS

Many respondents (39%) heard about payday loans through family members and friends. Nearly one-third survey respondents (31%) heard about payday loans through sign boards. Others

reported media (18%), flyers (8%) and other sources (4%) such as internet, colleagues, and

walking around the street. The majority of survey respondents (63%) borrowed money from

payday lenders at least once a month or more than once a month. Only 15% reported that they

borrowed only one time. Many survey respondents (46 out of 73) also reported using other

services from payday lenders; majority of them having used cheque cashing (67%) service

followed by pre-paid credit card and money transfers (37% each respectively). The majority of

survey respondents did not rollover a payday loan (i.e. received an extension of a payday loan

for a fee or issued a new payday loan to pay off a previous payday loan). However, more than

one-third (36%) loan borrowers did report rolling over a payday loan.

8 5 6

32

9

39

4

10

5

Unfriendly staff Hours of operation Location of banks Non-availability of small loans

Too much paper work

I had a bad credit history

I did not have any ID

I did not know that I can borrow from a

bank

Don't know

Borrower Survey What stopped you from using the financial products from banks and made you switch to a payday

loan? (n=71)

Payday lending Practices in London 22

www.communitybasedresearch.ca

Friend 29%

Family member

10% Flyer 8%

Sign board 31%

TV/Radio/Newspaper

18%

Other 4%

Borrower Survey How did you first hear about payday loans?

(n=72) More than once a month

26%

Once a month

37%

One or two times per

year 22%

One time only 15%

Borrower Survey How often do/did you borrow payday loans?

(n=73)

67%

0

13%

37% 37%

19%

13%

28%

Cheque cashing Post box Telephone card Pre-paid credit card

Money transfers Gift card Sell gold Other

Borrower Survey Have you also used other services where payday loans are offered? (n=46)

Payday lending Practices in London 23

www.communitybasedresearch.ca

2.2.3 REASONS FOR BORROWING PAYDAY LOANS

Payday loans are provided to people who cannot get access to money from any informal source (e.g. family, and friends). Moreover, the payday lending industry exists because the "regular'

banking industry and other financial institutions do not provide needed services to those with a

lower income, i.e. small loans for emergencies. Borrower survey respondents identified three

most important reasons for borrowing payday loans. These reasons included meeting basic

needs (71%); bill payment (48%); and rent payment (46%). Only 10 respondents (out of 73)

indicated that they borrowed money for gambling and/or for alcohol. A large majority of

community agency survey respondents also noted that individuals use payday loans to pay for

their basic needs, including food, rent and/or utility bills. Other main reasons included meeting

expenses related to transportation, paying off loans, and to avoid bouncing a cheque. A few

community agency survey respondents also cited addiction and/or gambling as a reason for

borrowing payday loans.

Yes 36%

No 60%

Don't know

4%

Borrower Survey Have you ever rolled over a payday loan?

(n=73)

Payday lending Practices in London 24

www.communitybasedresearch.ca

Following are some of the stories that community agency survey respondents provided about their clients who openly admitted using payday loans:

One of our clients is an OW participant who was at risk of having her hydro switched off and had

already accessed funds and programs of support in the past. She felt she had no choice so accessed a

loan and ended up in double her debt.

One of our clients had a pay cheque from a casual job. He did not have a bank account. He did not

have identification to open a bank account or $20.00 to deposit in an account. He needed the money to

pay his rent.

The client is addicted to both alcohol and gambling and has a limited income. He often binges on

alcohol and gambles while under the influence of alcohol. Following the binge he often requires payday

loans to cover rent, basic living needs, food. He no longer uses a bank as they have revoked any lending

privileges due to a poor repayment history.

34

6

35

52

10

28

19 19

9 11

3

7 10

Rent payment Mortgage payment

Bill payment Other basic needs

Medical or health related

expenses

Transportation To pay for other loans or

debts

To avoid bouncing a

cheque

Car repair Recreation Gambling Alcohol/liquor Other

Borrower Survey What did you use your payday loan money for? (n=73)

Payday lending Practices in London 25

www.communitybasedresearch.ca

Case Study

Mary is a single mother in her 30s. She has a college diploma and is working fulltime in London. Mary borrowed

from payday lenders for two and a half years but does not use payday loans any longer. She began borrowing

from payday lenders to meet basic needs for herself and her young child. She used the money for rent,

groceries, bills and car insurance. She did not borrow money from a bank because she had a bad credit history

and thought that she would not be approved for a loan at her bank. During the two and a half years, she

borrowed from two different payday lenders at a time- and sometimes even three.

Mary believed that the best thing about payday lenders was the quick access to cash. She never had a bad

experience with payday lenders and customer service at the stores was quite good. The terms and conditions of

her loans were explained to her. Mary found the payday loans to be very expensive that created a ‘vicious

cycle’—she had to borrow from other payday lenders to repay the original loan.

Payday loan borrowing impacted Mary in two ways: financially and psychologically. Financially, she was ‘debt

trapped’ and had to borrow money from multiple lenders to keep the cycle running. She was paying a lot of

money in interest and in loan fees. Borrowing from payday lenders also had psychological and emotional

consequences on Mary’ life—it caused anxiety and stress especially when she would think that all her salary

would go into paying back loans and she would have to borrow again. Mary’s friend found her very stressed

during that two and a half year period. Looking back, Mary now realized the impact that her borrowing had on

her family. She noted that the money she was spending on borrowing payday loans could have been better spent

on her family. In her view, although payday loans serve an immediate financial need, the cost and impacts are

long-term. Mary’s friend recalled that when borrowing from payday lenders, Mary was not able to do anything

‘fun’ with her family; instead, her money was only going towards paying bills and repaying her loans.

The continued realization of how much it was costing her to borrow led Mary to stop borrowing. She shared

this realization in the following words: “I just remember working it out one time and being pretty shocked at

how much money I was giving them to just get money earlier and I just stopped.” She further explained that in

order to stop she had to pay her current loans off and be ‘pretty broke’ for a couple of weeks. Although it was a

sacrifice, Mary found this a better option than paying loans every two weeks. Mary had the support of her close

friend in creating a budget and plan so that she would not need to borrow any longer. Now that Mary was no

longer borrowing from payday lenders, Mary felt her life had improved quite a bit. She went back to school and

found a better job. About the future use of payday loans, she did not rule out it out completely because she is

the sole earner to provide for herself and for her son’s basic needs. However, payday loan would be her last

option and she would do everything she could to avoid it.

Mary was aware of a few money management resources in London. At one point, she used a debt counsellor but

did not find helpful. In her view, payday lending was a bigger issue than providing information on money

management to individuals who struggle financially: “I don’t think it’s a matter of people not always knowing how

to manage money-you can’t manage money you don’t have. The cost of living goes up and money does not [...]

it’s a lack of money and no financial literacy class is going to help with that”.

Payday lending Practices in London 26

www.communitybasedresearch.ca

2.2.4 SATISFACTION WITH PAYDAY LENDERS

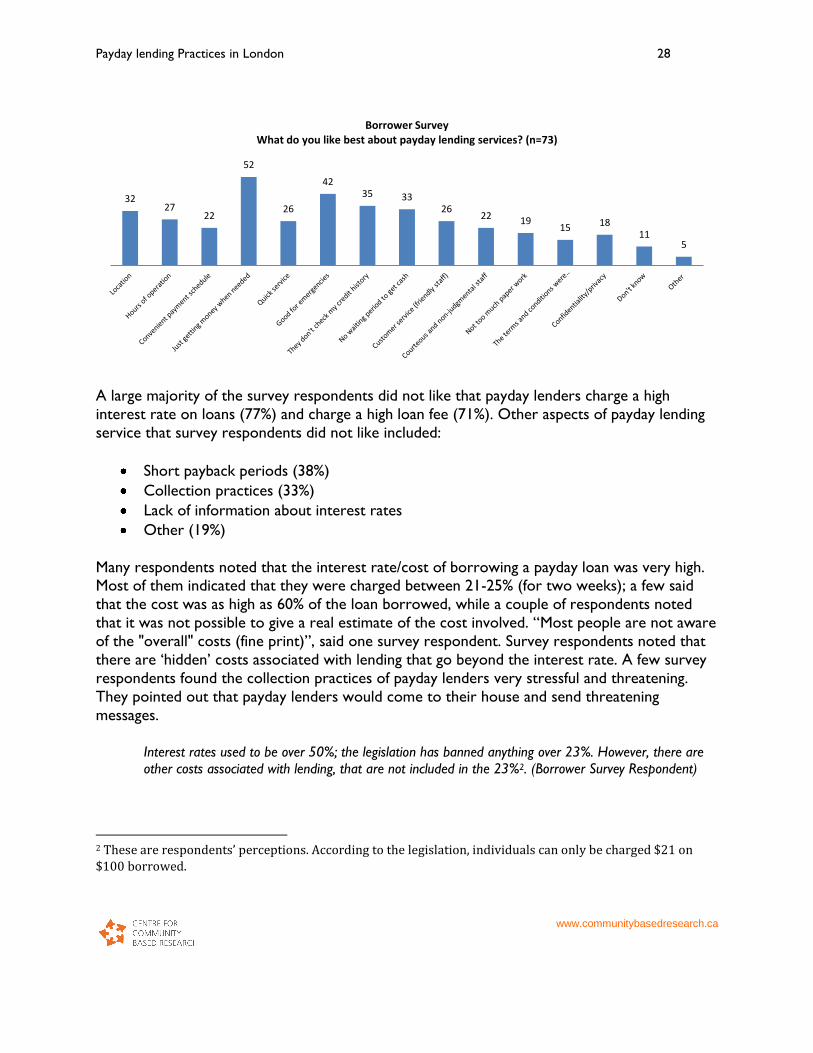

A large majority of survey respondents (85%) reported that they signed a contract when they

obtained their payday loan. More than two-thirds (71%) survey respondents liked that payday

lenders were helpful in giving them money when they needed. More than half reported (57%)

that payday loans are good for emergencies. Other aspects of payday lending that survey

respondents liked included:

They don’t check my credit history (48%)

No waiting period to get cash (45%)

Location of payday lenders (44%)

Hours of operation (37%)

Quick service (36%)

Customer service (36%)

Convenient payment schedule (30%)

Courteous and non judgemental staff (30%)

Not too much paper work (26%)

Confidentiality/privacy (25%)

The terms and conditions were explained well (20%)

Other (7%)

In their qualitative response, a number of survey respondents appreciated the simplicity,

accessibility and convenience in obtaining payday loans. They liked the fact that payday lenders

are not judgemental and do not check their credit history. They noted that payday loans helped

them in emergencies to meet their needs. “It’s an evil necessity’, is how one survey respondent

described payday loans.

If anything it helped when needed to ensure the kids had proper food. (Borrower Survey Respondent)

It allowed us to get food when we needed. (Borrower Survey Respondent)

Community agency survey respondents and key informants identified convenience, customer

service and perceived sense of anonymity when borrowing from a payday lender as the main

motivating factors.

It is fast, easy; [borrowers] think that it won't go on their financial record, it is anonymous. (Community

Agency Survey Respondent)

Customer service---when they go to these ........ places, maybe their buddies are going there. It’s really

convenient; they are open later than banks till 9 o’clock and 10 at some places. (Key Informant)

It’s the convenience factor. You walk in and in 20 minutes, you walk out with your requested sum of

money. (Key Informant)

Payday lending Practices in London 27

www.communitybasedresearch.ca

Borrowers who used other services from payday lenders (e.g. cheque cashing, selling gold,

telephone card, etc) found them useful. In particular, they appreciated the very personalized

nature of the customer service they received.

Customer service is good. Go over info quickly - more of a sales than concern about you and budget.

They know they have you because you need them. (Borrower Survey Respondent)

However, a number of survey respondents found that using additional services, in particular

cheque cashing, from payday lenders were very expensive and costly and had negative

consequences for them. “I lost my jewellery”, commented one survey respondent. They

indicated that the service is convenient and quick but the cost of using any additional service is

very high.

With the cheques cashing service, I felt as though I was being cheated of my money and paying way too

much for a simple service. It seems that these services just take advantage of people in desperate

circumstances. (Borrower Survey Respondent)

For the cheque cashing service, it was at least $15 for every $100 cashed. (Borrower Survey Respondent)

Yes 85%

No 7%

Don't know 8%

Borrower Survey Did you sign a contract when you obtained

your payday loan? (n=73)

Payday lending Practices in London 28

www.communitybasedresearch.ca

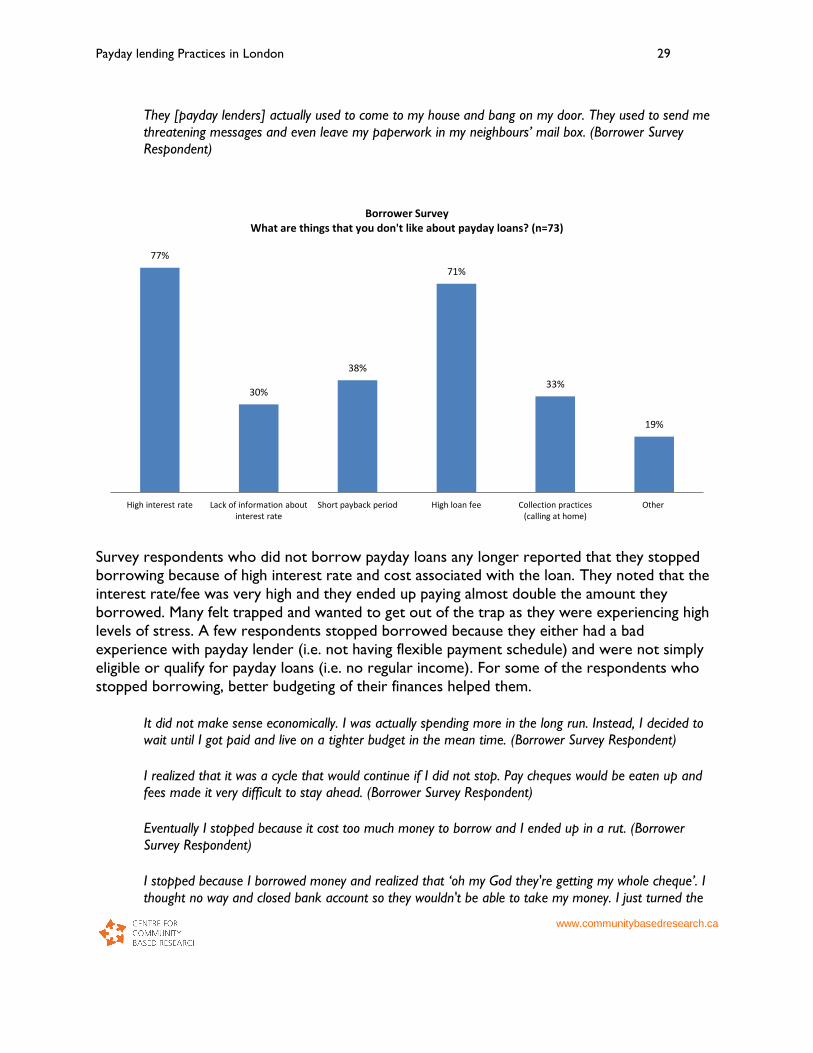

A large majority of the survey respondents did not like that payday lenders charge a high

interest rate on loans (77%) and charge a high loan fee (71%). Other aspects of payday lending

service that survey respondents did not like included:

Short payback periods (38%)

Collection practices (33%)

Lack of information about interest rates

Other (19%)

Many respondents noted that the interest rate/cost of borrowing a payday loan was very high. Most of them indicated that they were charged between 21-25% (for two weeks); a few said

that the cost was as high as 60% of the loan borrowed, while a couple of respondents noted

that it was not possible to give a real estimate of the cost involved. “Most people are not aware

of the "overall" costs (fine print)”, said one survey respondent. Survey respondents noted that

there are ‘hidden’ costs associated with lending that go beyond the interest rate. A few survey

respondents found the collection practices of payday lenders very stressful and threatening.

They pointed out that payday lenders would come to their house and send threatening

messages.

Interest rates used to be over 50%; the legislation has banned anything over 23%. However, there are other costs associated with lending, that are not included in the 23%2. (Borrower Survey Respondent)

2 These are respondents’ perceptions. According to the legislation, individuals can only be charged $21 on $100 borrowed.

32 27

22

52

26

42 35 33

26 22 19

15 18 11

5

Borrower Survey What do you like best about payday lending services? (n=73)

Payday lending Practices in London 29

www.communitybasedresearch.ca

They [payday lenders] actually used to come to my house and bang on my door. They used to send me

threatening messages and even leave my paperwork in my neighbours’ mail box. (Borrower Survey

Respondent)

Survey respondents who did not borrow payday loans any longer reported that they stopped borrowing because of high interest rate and cost associated with the loan. They noted that the

interest rate/fee was very high and they ended up paying almost double the amount they

borrowed. Many felt trapped and wanted to get out of the trap as they were experiencing high

levels of stress. A few respondents stopped borrowed because they either had a bad

experience with payday lender (i.e. not having flexible payment schedule) and were not simply

eligible or qualify for payday loans (i.e. no regular income). For some of the respondents who

stopped borrowing, better budgeting of their finances helped them.

It did not make sense economically. I was actually spending more in the long run. Instead, I decided to wait until I got paid and live on a tighter budget in the mean time. (Borrower Survey Respondent)

I realized that it was a cycle that would continue if I did not stop. Pay cheques would be eaten up and fees made it very difficult to stay ahead. (Borrower Survey Respondent)

Eventually I stopped because it cost too much money to borrow and I ended up in a rut. (Borrower

Survey Respondent)

I stopped because I borrowed money and realized that ‘oh my God they're getting my whole cheque’. I

thought no way and closed bank account so they wouldn't be able to take my money. I just turned the

77%

30%

38%

71%

33%

19%

High interest rate Lack of information about interest rate

Short payback period High loan fee Collection practices (calling at home)

Other

Borrower Survey What are things that you don't like about payday loans? (n=73)

Payday lending Practices in London 30

www.communitybasedresearch.ca

other way. (Borrower Survey Respondent)

Even though the fees are supposed to be regulated they hit you with "bank fees" and lender's fees which puts up the amount that you have to pay back. (Borrower Survey Respondent)

Overall, when survey respondents were asked how likely they were to use payday lending

services in the future, the majority of them (57%) said not likely at all or a little likely to use the

payday loan service in the future. Less than one-third of survey respondents (29%), however,

reported that they would use payday loan service in the future.

Expressing his/her sentiments about borrowing from payday lenders, one survey respondent

commented: “I felt dirty, as a failure, unable to make ends meet, beggar, embarrassed, ashamed,

angry, and disgusted.”

2.2.5 IMPACT OF BORROWING PAYDAY LOANS

Survey respondents noted mostly negative impact of borrowing from payday lenders on their

life. The most significant impacts included falling into a debt trap (56%), dropping month income

(49%), and experiencing high level of stress (48%). Only 14% of respondents said that

borrowing from payday lender made them happier. Other negative impacts included:

Not able to meet needs of the family (20%)

Strained relations with family (18%)

Strained relations with friends (11%)

Becoming aggressive (9%)

Other (3%)

Losing assets (1%)

It made me happier the first time. Never thought how hard it would be to get out of it. (Borrower Survey

Respondent)

Very likely 12%

Likely 17%

Somewhat likely 14%

A little likely 13%

Not likely at all

44%

Borrower Survey How likely are you to use payday loan service

in the ftuure? (n=72)

Payday lending Practices in London 31

www.communitybasedresearch.ca

Once you borrow from them, it’s a downwards spiral. You’ve already borrowed against your next

paycheque, your paycheque comes in and it goes to the Money Mart people. You need money to eat so

you have to borrow another one. It’s a vicious cycle. (Key Informant)

A family I am working with recently shared with me they currently have 3 loans and have no idea how

they are going to pay the money back. They have described very high interests rates and are getting

themselves deeper and deeper in the hole of which they are not going to be able to get out of.

(Community Agency Survey)

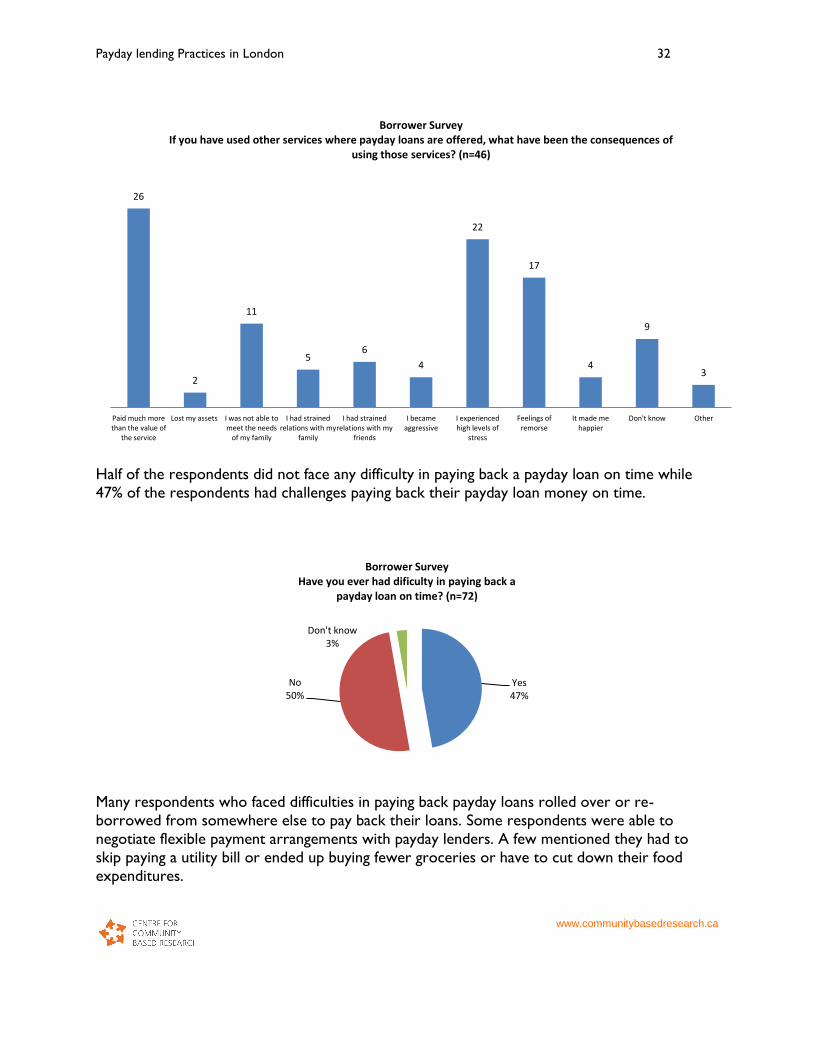

Using other services from payday lenders also had mostly negative consequences. Significant

negative consequences included paying much more than the value of the service (56%),

experiencing high level of stress (48%), and feelings of remorse (37%). Only 9% of respondents said that using other services from payday lenders made them happier. Other negative

consequences included:

Not able to meet needs of the family (24%)

Strained relations with friends (13%)

Strained relations with family (11%) Becoming aggressive (9%)

Other (6%)

Losing assets (4%)

41

1

36

15 13

8 7

35

10 11

2

Fell into a debt trap

Lost my assets My monthly income dropped

I was not able to meet the needs

of my family

I had strained relations with my

family

I had strained relations with my

friends

I became aggressive

I experienced high levels of

stress

It made me happier

Don't know Other

Borrower Survey What has been the impact of borrowing from payday lenders on your life? (n=73)

Payday lending Practices in London 32

www.communitybasedresearch.ca

Half of the respondents did not face any difficulty in paying back a payday loan on time while

47% of the respondents had challenges paying back their payday loan money on time.

Many respondents who faced difficulties in paying back payday loans rolled over or re-

borrowed from somewhere else to pay back their loans. Some respondents were able to

negotiate flexible payment arrangements with payday lenders. A few mentioned they had to

skip paying a utility bill or ended up buying fewer groceries or have to cut down their food

expenditures.

26

2

11

5 6

4

22

17

4

9

3

Paid much more than the value of

the service

Lost my assets I was not able to meet the needs

of my family

I had strained relations with my

family

I had strained relations with my

friends

I became aggressive

I experienced high levels of

stress

Feelings of remorse

It made me happier

Don't know Other

Borrower Survey If you have used other services where payday loans are offered, what have been the consequences of

using those services? (n=46)

Yes 47%

No 50%

Don't know 3%

Borrower Survey Have you ever had dificulty in paying back a

payday loan on time? (n=72)

Payday lending Practices in London 33

www.communitybasedresearch.ca

Most people, eventually, have difficulty paying the loans back; if not immediately. Rollover loans are

illegal. However, there are different names for them that mean the same thing. A loan can be partially

paid back, with a new loan extended to the customer. (Borrower Survey Respondent)

I had to borrow money from another source to pay the money back. (Borrower Survey Respondent)

Made payment arrangements and went in once per week and paid what I could until balance was paid. (Borrower Survey Respondent)

I had to get another payday loan or skip a bill or buy fewer groceries. (Borrower Survey Respondent)

I told them I couldn’t pay it this month, and they took all my money out of the bank. My son could not eat that month. (Borrower Survey Respondent)

Payday lending Practices in London 34

www.communitybasedresearch.ca

Case Study

Sarah is in her 20s, has a college diploma, and is working fulltime. She earns around $45,000 annually and

does not borrow from payday lenders any longer. She has been living in London for the past 12 years. Sarah

started borrowing from payday lenders four years ago when her five-person household was living on a

single income. Finding it hard to make ends meet, Sarah and her spouse decided to borrow from a payday

lender and the borrowing escalated from that point on. Sarah first learned of payday lending from ‘lots of

advertising’ about their products. She read the sign outlining the cost of borrowing and thought that if she

borrowed $300, she would only be required to pay $321. She soon found out that this was not the case;

instead she paid $363. Moreover, Sarah had to pay other costs such as ‘account fees’, ‘monthly card fees’

and broker fees’. Sarah never rolled over. Her consistent borrowing from the same store allowed her to

borrow greater amounts of money. In one instance she was able to borrow $820 because they knew her by

name at the store and were able to ‘stretch the limit’ for her.

Payday loan borrowing had an impact on Sarah and her family. She suffered from depression and often

would become stressed when the time to pay back loans arrived. Borrowing also strained her relationship

with her spouse due to the financial burdens they were facing in repaying loans. Sarah also sought the

assistance of her parents who were able to provide her with some money to help alleviate her financial

situation. Having to seek her parent’s help caused additional stress because she felt that she disappointed

them by getting caught in such a ‘debt trap’. However, Sarah’s mother did not feel that there was a change

in their relationship. In her view, they just tried to help Sarah with providing some money as well as help in

budgeting. Overall, Sarah felt ashamed for having to borrow money, but also felt relief when she did

because it meant she could provide the basic necessities for her family, including food.

Although Sarah did not plan not to borrow from payday lenders in the future, she recognized that

something might come up that would lead her to borrow again-just as has happened in the past. Both Sarah

and her mother noted that with increased household income, they would need to focus on better budgeting

their finances.

Sarah noted that community resources providing financial information could help individuals who face

financial hardships. Specifically, the program should include information about ‘how to budget’ and ‘how to

make your budget work’. Sarah believed that keeping in touch with individuals [clients of programs] is a key

to making sure clients follow-through with their budgeting plan. In her opinion, both one-on-one and group

counselling are good approaches for any financial education program. In addition, she also wanted an

alternative to payday lending for those individuals who might have bad credit history and were not eligible

for bank loans.

Payday lending Practices in London 35

www.communitybasedresearch.ca

3. FINANCIAL EDUCATION PROGRAM

In this study, we asked participants about the potential need and viability of a community-wide

financial education program in London. Before providing specific comments about a community-

wide financial education program, a large majority of survey respondents and key informants

provided comments about a general need for an alternative to payday lending.

More than four-fifths of borrower survey respondents (81%) and more than three-quarters

community agency survey respondents (76%) indicated that there is a need for an alternative to

payday lending. A large majority of respondents (84% borrowers and 83% community agencies)

would like the alternative to provide loans at a lower interest rate with clear information about

the fee/interest rate (73% borrowers and 96% community agencies). Survey respondents

suggested that a bank or other small businesses similar to payday lending should provide small

emergency loans to low income individuals with lower interest rates/fees. Such a business

should provide clear information about the cost of borrowing as well as provide them with

information about how to effectively manage their finances. Other elements of an alternative

that borrower survey respondents suggested are given below in order of their preference.

Friendly service (55%)

Convenient hours (52%)

Convenient location (43%)

Providing telephone card service (25%)

Providing money transfer service (23%)

Providing post box service (12%)

Other (12%)

The same banks that people use on a daily basis need to provide micro-services for those with lower

incomes at reasonable costs to help people manage their finances especially when they only get money once a month. (Borrower Survey Respondent)

You need something in between (in between a bank and payday loan service), a small business, that

deals with low income people. Better interest rates; once they give you a loan they tell you about money

management, help you out when you pay it back and how to avoid the situation in the future. (Borrower Survey Respondent)

Something where they do the same thing [provide small loans] but minimize loaning fee/interest (e.g. $5 for $50). Keep interest rate low. (Borrower Survey Respondent)

Payday lending Practices in London 36

www.communitybasedresearch.ca

A few research participants cautioned about an alternative to payday lending. In their view, low

income individuals might continue to borrow from payday lenders even if there is an option of

obtaining a short term, low cost loan. This would make them more indebted and would worsen

their situation. They suggested holding a community dialogue around this issue.

I would like to hear community debate on this issue. For our clients, it would be problematic because

they would probably use both and get deeper into debt. (Community Agency Survey Respondent)

More than two-thirds of borrower respondents (71%) noted that there is a need for a

service that provides education about managing money and credit (i.e. financial

literacy). Some respondents thought that the real issue is effectively managing finances to avoid

getting debt trapped. In their view, launching an alternative that provides low interest loans

would be waste of resources. They suggested that awareness should be created among low

income individuals about these services in the community.

I think the only acceptable alternative is financial literacy and teaching ways to better manage money;

not another place you can borrow (waste) money. (Borrower Survey Respondent)

If I knew how to better manage my money then I don't think I would've needed a payday loan. (Borrower Survey Respondent)

Yes 81%

No 19%

Borrower Survey Is there a need for an altnernative to payday

lending? (n=69)

Yes 76%

Unsure 24%

Community Agency Survey Is there a need for an alternative to payday

lending? (n=33)

Payday lending Practices in London 37

www.communitybasedresearch.ca

4.1 KNOWLEDGE ABOUT EXISTING FINANCIAL EDUCATION PROGRAMS

Nearly two-thirds borrower survey respondents (66%) were not aware of any service in London that provides information on how to better manage their money. A large majority of

community agency survey respondents (80%) indicated that they were aware of

programs/services that provide information to community members to better manage their

money. Most of the survey respondents, borrowers as well as community agencies, who were

aware of any existing financial education service/program frequently named Family Service

40 41

31

47

24

29

7

14 13

7

Provide education about managing

money and credit

Provide clear information about

the fee/interest rate

Friendly service Lower interest rate Convenient location Convenient hours Post box service Telephone card Money transfers Other

Borrower Survey If there is a need for a payday alternative, what would be its key elements? (n=56)

28

24 22 22

16

22

Provide clear informaiton about the fee/interest

rate

Low interest rate Convenient location Convenient hours of operation

Provide other services Friendly customer service

Community Agency Survey If there is a need for an alternative, what would be key elements of an alternative? (n=29)

Payday lending Practices in London 38

www.communitybasedresearch.ca

Thames Valley Credit Counselling program. A few respondents mentioned the names of

Goodwill Industries, seminars at church, programs at the London Public Library, Junior

Achievement (for grade 7 and 8) and bulletin boards at community centres that contain

information about a number of different programs on money management. A large majority of

borrower respondents (79%) reported not using financial education service in the past. Only a

couple of respondents reported using Family Service Thames Valley credit counselling services

but noted that it was not lack of budgeting but acute shortage of financial resources to meet

their daily needs. ‘There was nothing to budget; money goes to rent and food”, commented

one borrower survey respondent.

More than three-quarters of borrower survey respondents (77%) indicated that they would

have used a community service that provides information to better manage their money if they

had known about it. Some respondents, who reported that they would not use the community

service even if they knew, provided two main reasons for their response. The most frequently

cited reason was ‘I already know but do not have enough money to manage’. Not having

enough time to avail any financial education service was another reason.

I know how to manage my money. Sometimes I just don't have enough available to make ends meet so I

Yes 34%

No 66%

Borrower Survey Are you aware of any service in

London/Middlesex that provides information on how to better manage your money? (n=70)

Yes 80%

No 20%

Community Agency Survey Are you aware of any program in that provides

information to community members on how to better manage money? (n=35)

Yes 21%

No 79%

Borrower Survey Have your ever used that service in the past?

(n=48)

Yes 77%

No 23%

Borrower Survey If you knew about the community service that provides information to better manage your

money, would you have used it? (n=64)

Payday lending Practices in London 39

www.communitybasedresearch.ca

need to borrow it. (Borrower Survey Respondent)

It’s not the management - it's simply not having enough. (Borrower Survey Respondent)

The reality is when you have little money to start out with and the cost of living (i.e. basic needs such as

food and shelter) is higher than the income you receive or earn working; you are sometimes left without

a choice. (Borrower Survey Respondent)

Almost half of the community agency survey respondents (47%) noted that existing financial

education programs are not meeting the needs of the community; only 17% indicated that the

existing financial education programs are meeting the need to ‘very much and much’ extent.

Community agency survey respondents noted that there is a lack of awareness about the

existing financial education programs and people face barriers (e.g. transportation) to attending

these programs, including long waiting lists for some of the services that provide one-on-one

counselling. A few respondents indicated that the existing financial education programs do not

provide comprehensive information about the banking rules and cost of borrowing from payday

lenders and possible alternatives.

Existing programs are not really visible, often referred by someone else but many people needing the help may not have connections in community. (Community Agency Survey Respondent)

There is a long waiting list for some of the [financial education] services; the others are crisis driven with little capacity for prevention work. (Community Agency Survey Respondent)

There is not enough information to working poor/those on social assistance about true costs of using

payday loan industry and possible alternatives. (Community Agency Survey Respondent)

4.2 NEED FOR A FINANCIAL EDUCATION PROGRAM

Identifying this as a gap, a large majority of the community agency survey respondents indicated

that there is a need for a community-wide financial education program in London—80% noted