patriot act compliance for finance and commercial … act compliance for finance and commercial loan...

TRANSCRIPT

Patriot Act compliance for Finance Patriot Act compliance for Finance and Commercial Loan Organizations and Commercial Loan Organizations

©Experian 2003. All rights reserved. Confidential and proprietary.

Patriot Act CompliancePatriot Act Compliance

Charles Charles KlingmanKlingman, US Treasury Dept. , US Treasury Dept. –– Present Present proposed regulations for Finance and proposed regulations for Finance and Commercial Loan CompaniesCommercial Loan Companies

Debra Ponce de Leon, Bank of America Capital Debra Ponce de Leon, Bank of America Capital ––Provide an overview of how a bank leasing Provide an overview of how a bank leasing subsidiary has interpreted and implemented subsidiary has interpreted and implemented compliancecompliance

Kim Cartwright, Experian Kim Cartwright, Experian –– Present compliance Present compliance solutions solutions

©Experian 2003. All rights reserved. Confidential and proprietary.

US Treasury RegulationsUS Treasury Regulations

On October 26, 2001, the President signed into On October 26, 2001, the President signed into law the USA PATRIOT Act law the USA PATRIOT Act

Initial compliance required for banks, savings Initial compliance required for banks, savings associations, and credit unions; securities associations, and credit unions; securities brokers and dealers; mutual funds; futures brokers and dealers; mutual funds; futures commission merchants and introducing brokers; commission merchants and introducing brokers; and credit unions. and credit unions.

Finance and Loan companies are required to Finance and Loan companies are required to comply by Summer of 2005comply by Summer of 2005

©Experian 2003. All rights reserved. Confidential and proprietary.

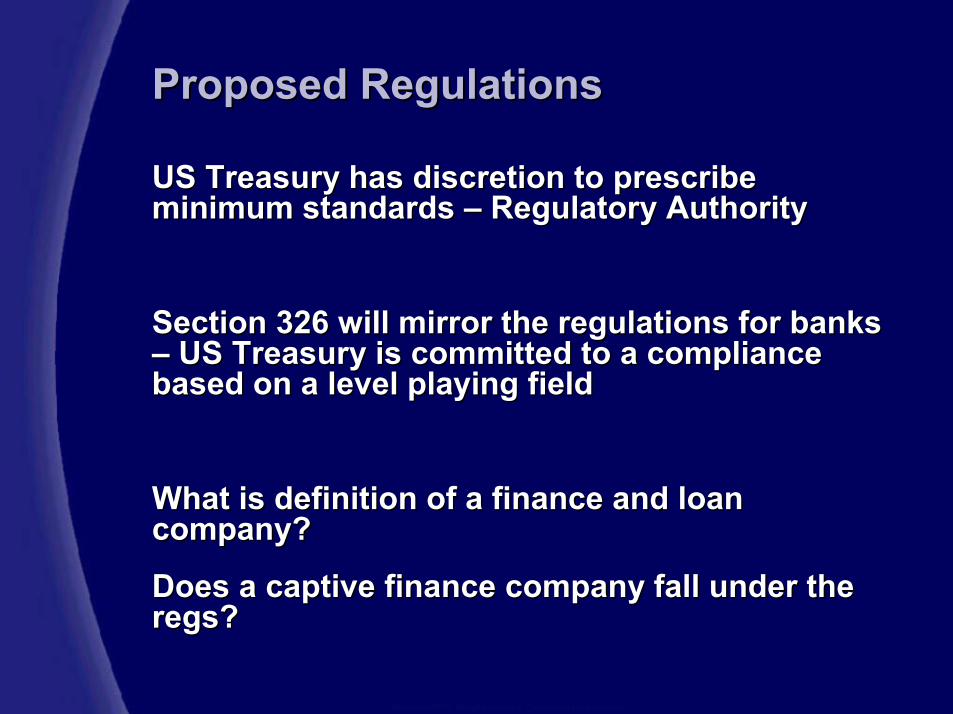

Proposed RegulationsProposed Regulations

US Treasury has discretion to prescribe US Treasury has discretion to prescribe minimum standards minimum standards –– Regulatory AuthorityRegulatory Authority

Section 326 will mirror the regulations for banks Section 326 will mirror the regulations for banks –– US Treasury is committed to a compliance US Treasury is committed to a compliance based on a level playing fieldbased on a level playing field

What is definition of a finance and loan What is definition of a finance and loan company? company?

Does a captive finance company fall under the Does a captive finance company fall under the regsregs??

©Experian 2003. All rights reserved. Confidential and proprietary.

Regulations 326 and 352 will apply to Regulations 326 and 352 will apply to Finance and Loan companiesFinance and Loan companiesSection 326 directs the Department of the Section 326 directs the Department of the Treasury and the federal functional regulators to Treasury and the federal functional regulators to jointly issue regulations requiring financial jointly issue regulations requiring financial institutions to establish minimum procedures for institutions to establish minimum procedures for the identification and verification of customers the identification and verification of customers who open new accounts.who open new accounts.

Section 352 requires the development of internal policies, procedures, and controls; the designation of a compliance officer; an ongoing employee training program and an independent audit function to test programs

This presentation will focus on Section 326This presentation will focus on Section 326

©Experian 2003. All rights reserved. Confidential and proprietary.

The Practitioner’s Point of ViewThe Practitioner’s Point of ViewDebra Ponce de LeonDebra Ponce de Leon

©Experian 2003. All rights reserved. Confidential and proprietary.

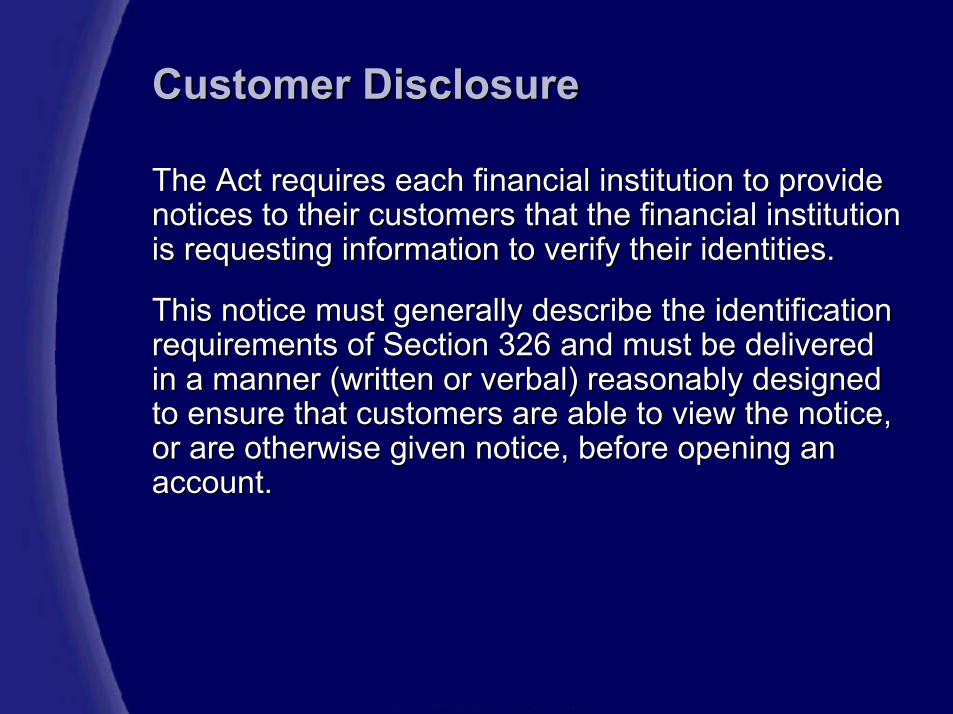

Customer DisclosureCustomer Disclosure

The Act requires each financial institution to provide The Act requires each financial institution to provide notices to their customers that the financial institution notices to their customers that the financial institution is requesting information to verify their identities. is requesting information to verify their identities.

This notice must generally describe the identification This notice must generally describe the identification requirements of Section 326 and must be delivered requirements of Section 326 and must be delivered in a manner (written or verbal) reasonably designed in a manner (written or verbal) reasonably designed to ensure that customers are able to view the notice, to ensure that customers are able to view the notice, or are otherwise given notice, before opening an or are otherwise given notice, before opening an account.account.

©Experian 2003. All rights reserved. Confidential and proprietary.

Collecting InformationCollecting Information

As part of any CIP, financial institutions must collect, at a As part of any CIP, financial institutions must collect, at a minimum, the following information from customers prior minimum, the following information from customers prior to opening an account:to opening an account:••customer’s legal name; customer’s legal name; ••customer’s address;customer’s address;••date of birth (for individuals and sole proprietors date of birth (for individuals and sole proprietors onlyonly); ); andand••taxpayer identification number or a social security number taxpayer identification number or a social security number (for a U.S. person or entity, as applicable), (for a U.S. person or entity, as applicable), oror••passport number (and country of issuance), taxpayer passport number (and country of issuance), taxpayer identification number, or number (and country of issuance) identification number, or number (and country of issuance) from any other governmentfrom any other government--issued document that shows issued document that shows nationality and includes a photograph or similar safeguard nationality and includes a photograph or similar safeguard (for a non(for a non--U.S. person or entityU.S. person or entity

©Experian 2003. All rights reserved. Confidential and proprietary.

Verifying Identity:Verifying Identity:

As part of any CIP, financial institutions must verify the As part of any CIP, financial institutions must verify the identity of the customer. Verification can be accomplished identity of the customer. Verification can be accomplished using documents, nonusing documents, non--documentary methods, or a documentary methods, or a combination of both, and must enable financial institutions combination of both, and must enable financial institutions to form a reasonable belief that it knows the true identity of to form a reasonable belief that it knows the true identity of the customer. the customer.

The verification procedure must be based on each financial The verification procedure must be based on each financial institution’s assessment of the relevant risks, including institution’s assessment of the relevant risks, including those presented by the various types of accounts those presented by the various types of accounts maintained by the financial institution, the various methods maintained by the financial institution, the various methods of opening accounts provided by the financial institution, of opening accounts provided by the financial institution, the various types of identifying information available, and the various types of identifying information available, and the financial institution’s size, location, and customer base. the financial institution’s size, location, and customer base.

©Experian 2003. All rights reserved. Confidential and proprietary.

Checking terrorist lists:Checking terrorist lists:

Financial institutions must determine whether a Financial institutions must determine whether a customer appears on any list of known or customer appears on any list of known or suspected terrorists or terrorist organizations suspected terrorists or terrorist organizations issued by a Federal government agency and issued by a Federal government agency and designated as such by Treasury and Federal designated as such by Treasury and Federal regulators. regulators.

©Experian 2003. All rights reserved. Confidential and proprietary.

Maintaining records:Maintaining records:

Institutions must maintain a record of all information obtained Institutions must maintain a record of all information obtained under a under a CIP. CIP.

At a minimum, this record must include the following:At a minimum, this record must include the following:•• All identifying information obtained about a customer (i.e., namAll identifying information obtained about a customer (i.e., name, DOB, e, DOB,

address, and TIN or other ID number);address, and TIN or other ID number);•• A description of any document relied on in verifying the identitA description of any document relied on in verifying the identity of the y of the

customer, including the type of document, identification number customer, including the type of document, identification number contained in the document, the place of issuance and, if any, thcontained in the document, the place of issuance and, if any, the date of e date of issuance and expiration date;issuance and expiration date;

•• A description of the methods and the results of any nonA description of the methods and the results of any non--documentary documentary or supplemental measures undertaken to verify the identity of thor supplemental measures undertaken to verify the identity of the e customer; andcustomer; and

•• A description of the resolution of any substantive discrepancy A description of the resolution of any substantive discrepancy discovered when verifying the information obtained.discovered when verifying the information obtained.

Information must be retained for the duration of the relationshiInformation must be retained for the duration of the relationship, and for a p, and for a period of (a) with respect to the information listed under bulleperiod of (a) with respect to the information listed under bullet 1 above, t 1 above, five (5) years after the account is closed, and (b) with respectfive (5) years after the account is closed, and (b) with respect to the to the information listed under bullets 2information listed under bullets 2--4 above, five (5) years after the record 4 above, five (5) years after the record is made.is made.

©Experian 2003. All rights reserved. Confidential and proprietary.

Reliance on other financial institutions:Reliance on other financial institutions:

The final rule also contains a provision that The final rule also contains a provision that permits, under certain limited circumstances, a permits, under certain limited circumstances, a financial institution to rely on another regulated financial institution to rely on another regulated U.S. financial institution to perform any part of U.S. financial institution to perform any part of the financial institution’s CIP. the financial institution’s CIP.

For example, in the securities industry it is For example, in the securities industry it is common to have an introducing broker common to have an introducing broker –– who has who has opened an account for a customer opened an account for a customer –– conduct conduct securities trades on behalf of the customer securities trades on behalf of the customer through a clearing broker. Under this regulation, through a clearing broker. Under this regulation, the introducing broker is required to identify and the introducing broker is required to identify and verify the identity of their customers and the verify the identity of their customers and the clearing broker can rely on that information clearing broker can rely on that information without having to conduct a second redundant without having to conduct a second redundant verification, provided certain criteria are met.verification, provided certain criteria are met.

©Experian 2003. All rights reserved. Confidential and proprietary.Experian and the Experian marks herein are service marks or registered trademarks of Experian

Customer Information ProgramCustomer Information ProgramSolutionsSolutions

Kim CartwrightKim Cartwright

ExperianExperian

©Experian 2003. All rights reserved. Confidential and proprietary.

AgendaAgenda

�� Review of Patriot ActReview of Patriot Act

�� How vendor How vendor solutions can help solutions can help

�� QuestionsQuestions

©Experian 2003. All rights reserved. Confidential and proprietary.

�� Three provisions of Act affect financial Three provisions of Act affect financial institutionsinstitutions

�� Found in Title III, the ‘International Money Found in Title III, the ‘International Money Laundering Abatement and AntiLaundering Abatement and Anti--terrorist terrorist Financing Act of 2001’Financing Act of 2001’

�� Section 314: Cooperative efforts to deter Section 314: Cooperative efforts to deter money launderingmoney laundering

�� Section 326: Verification Section 326: Verification of identificationof identification

�� Section 352: AntiSection 352: Anti--moneymoney--laundering programslaundering programs

U.S. Patriot ActU.S. Patriot Act

©Experian 2003. All rights reserved. Confidential and proprietary.

Section 326Section 326

What is it?What is it?

�� Requirement for Requirement for financial institutions financial institutions to establish a Customer to establish a Customer Identification Program Identification Program (CIP)(CIP)

�� Document the CIPDocument the CIP

�� Have CIP approved by Have CIP approved by boardboard

�� Incorporate CIP into Incorporate CIP into BSA programBSA program

Who does it apply to?

� Banks, savings associations, credit unions

� Securities broker-dealers

� Investment companies

� Futures merchants

� Insurance companies

©Experian 2003. All rights reserved. Confidential and proprietary.

Customer Identification ProgramCustomer Identification Program

Maintain records of Maintain records of information used to verify information used to verify a customera customer

Establish procedures to verify identity of persons seeking to open an account

Determine whether person Determine whether person appears on any lists of appears on any lists of known or suspected known or suspected terrorists issued by terrorists issued by federal governmentfederal government

Use risk-based procedures for verification

Develop procedures for Develop procedures for determining when not to determining when not to open an account or close an open an account or close an existing account as a result existing account as a result of inability to verify identityof inability to verify identity

Verify name, address, taxpayer ID, date of birth at a minimum

©Experian 2003. All rights reserved. Confidential and proprietary.

VerificationVerification

�� DocumentaryDocumentary

�� Unexpired governmentUnexpired government--issued identificationissued identification

�� NonNon--documentarydocumentary

�� Encouraged even when documentary Encouraged even when documentary verification is providedverification is provided

�� Contact customer after account Contact customer after account is openedis opened

�� Check references with other Check references with other financial institutionsfinancial institutions

�� Negative verificationNegative verification

�� Positive verificationPositive verification

�� Logical verificationLogical verification

©Experian 2003. All rights reserved. Confidential and proprietary.Experian and the Experian marks herein are service marks or registered trademarks of Experian

NonNon--documentary solutions documentary solutions --logical and positive verificationlogical and positive verification

©Experian 2003. All rights reserved. Confidential and proprietary.

Verification typesVerification types

Type Method Sources

Positive

LogicalLogical

Compare information provided with a trusted third party source

Analyze logical Analyze logical consistency between consistency between information providedinformation provided

Consumer reporting agency

Commercial verification Commercial verification productsproducts

Negative Negative Check information Check information provided for association provided for association with known incidents of with known incidents of fraudulent behaviorfraudulent behavior

Compare against known Compare against known fraud or bad check fraud or bad check databasesdatabases

©Experian 2003. All rights reserved. Confidential and proprietary.

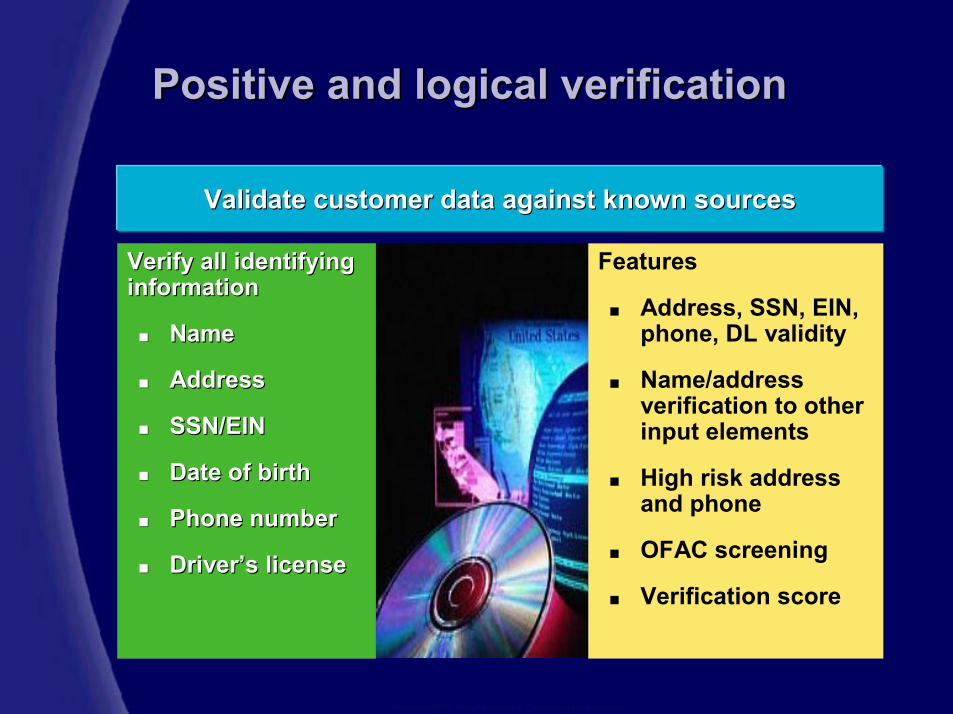

Positive and logical verificationPositive and logical verification

Verify all identifying Verify all identifying informationinformation

�� NameName

�� AddressAddress

�� SSN/EINSSN/EIN

�� Date of birthDate of birth

�� Phone numberPhone number

�� Driver’s licenseDriver’s license

Features

� Address, SSN, EIN, phone, DL validity

� Name/address verification to other input elements

� High risk address and phone

� OFAC screening

� Verification score

Validate customer data against known sourcesValidate customer data against known sources

©Experian 2003. All rights reserved. Confidential and proprietary.

Data ElementsData Elements

Telephone data, area code filesTelephone data, Telephone data, area code filesarea code files

OFAC SDN listOFAC SDN listOFAC SDN listSocial Security AdministrationSocial Security Social Security AdministrationAdministration

Address data -standardization, residential, deliverable address, change of address

Address data Address data --standardization, residential, standardization, residential, deliverable address, deliverable address, change of addresschange of address

Credit header -includes SSN and DOB data

Credit header Credit header --includes SSN includes SSN and DOB dataand DOB data

Business data -address, phoneBusiness data Business data --address, phoneaddress, phone

High risk address, phoneHigh risk High risk address, phoneaddress, phone

verification databaseverification database

Driver’s license dataDriver’s Driver’s license datalicense data

©Experian 2003. All rights reserved. Confidential and proprietary.

Validating and verifying information Validating and verifying information

Phone number

Drivers license

•Residential or business•Match to full name/surname and/or address

Social Social security security numbernumber

•Area code/format•Prefix to zip•Cell phone or pager

•• FormatFormat•• Issued Issued -- includes state includes state and years of issuanceand years of issuance

•• DeceasedDeceased

•Format correct for state

•• Match to full name/surname Match to full name/surname and/or addressand/or address

•• Based on full SSN or last Based on full SSN or last fourfour

•Match to full name/surname and/or address

Address Address ••DeliverableDeliverable••StandardizedStandardized

••Residential or businessResidential or business••Match to full name/surnameMatch to full name/surname

Element Validation Verification

Date of birthDate of birth •• Match to input Match to input •• Comparison to SSN (if Comparison to SSN (if provided)provided)

••Full DOB or year onlyFull DOB or year only

©Experian 2003. All rights reserved. Confidential and proprietary.

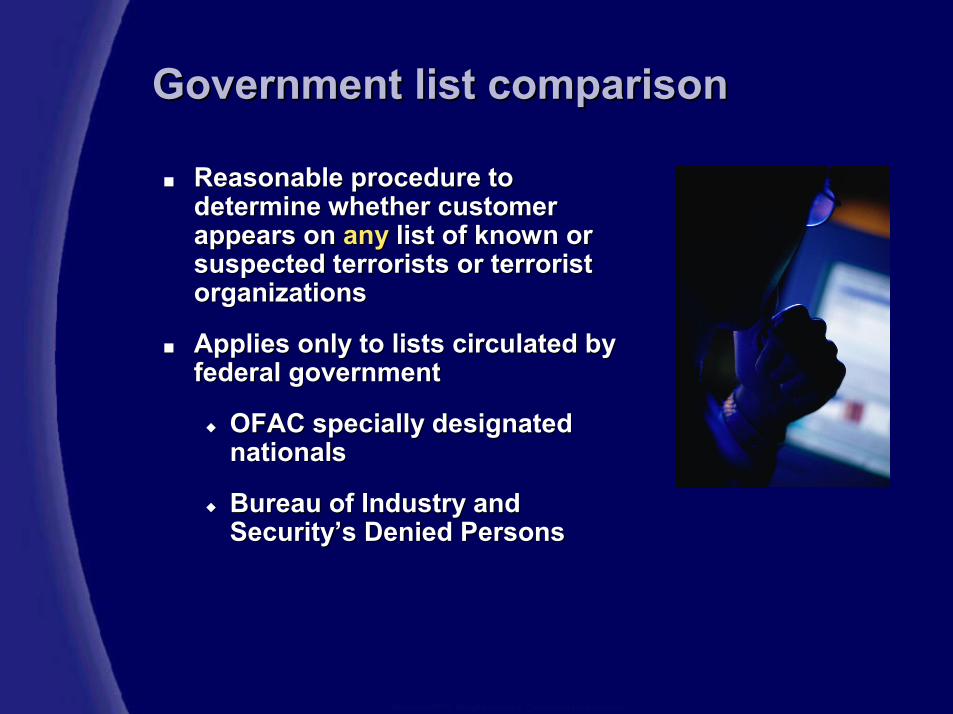

Government list comparisonGovernment list comparison

�� Reasonable procedure to Reasonable procedure to determine whether customer determine whether customer appears on appears on anyany list of known or list of known or suspected terrorists or terrorist suspected terrorists or terrorist organizationsorganizations

�� Applies only to lists circulated by Applies only to lists circulated by federal governmentfederal government

�� OFAC specially designated OFAC specially designated nationalsnationals

�� Bureau of Industry and Bureau of Industry and Security’s Denied PersonsSecurity’s Denied Persons

©Experian 2003. All rights reserved. Confidential and proprietary.

Selecting a solutionSelecting a solution

Factors to considerFactors to consider

�� Data qualityData quality

�� FunctionalityFunctionality

�� Where does solution applyWhere does solution apply

�� CostCost

�� Applicability across Applicability across organizationorganization

�� Ease of implementationEase of implementation

©Experian 2003. All rights reserved. Confidential and proprietary.Experian and the Experian marks herein are service marks or registered trademarks of Experian

QuestionsQuestions