pasta in europe: opportunities and … board 2014/pasta in europ… · pasta in europe:...

TRANSCRIPT

PASTA IN EUROPE: OPPORTUNITIES AND CHALLENGES FOR MANUFACTURERS

UNAFPA/SEMOULIERS AND IPO BOARD MEETING 23 MAY 2014 - LYON

ILDIKO SZALAI SENIOR ANALYST

© Euromonitor International

2

• Global provider of Strategic Market Intelligence

• 12 Regional offices - 800+ analysts in 80 countries

• Cross-country comparable data and analysis

• Consumer focused industries, countries and

consumers

• 5 - 10 year forecasts with matching trend analysis

• All retail channels covered

• Subscription services, reports and consulting

About Euromonitor International EUROMONITOR INTERNATIONAL London

Singapore

Shanghai

Dubai

Vilnius

Cape Town

San7ago

Tokyo

Sydney

Chicago

Bangalore

Sao Paulo

MARKET ENVIRONMENT

ADDING VALUE TO PASTA

LESSONS FROM BEYOND EUROPE

KEY TAKEAWAYS

© Euromonitor International

4

4.0%

2011

3.2%

2012

3.0%

2013

3.6%

2014

2014 Expected to Be Turning Point in Real GDP Growth Globally MARKET ENVIRONMENT

World: % Real GDP Growth

© Euromonitor International

5

Modest Recovery Expected in GDP Growth in Europe by 2019 MARKET ENVIRONMENT

5.4

2.9 3.3 3.7 4.6

2.4 2.0

-8

-6

-4

-2

0

2

4

6

8

Asia Pacific Australasia Eastern Europe

Latin America

Middle East and Africa

North America

Western Europe

% y

-o-y

gro

wth

% Year on Year Real GDP Growth by Region – 2009-2019

2009 2014 2019

© Euromonitor International

6

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2011-12 2012-13 2013-14

% y

-o-y

gro

wth

World: Retail Volume Sales of Packaged Food Versus Pasta 2012-2014

Packaged Food Pasta

Pasta Volume Growth Remain Slower & Lower than Overall Food MARKET ENVIRONMENT

© Euromonitor International

7

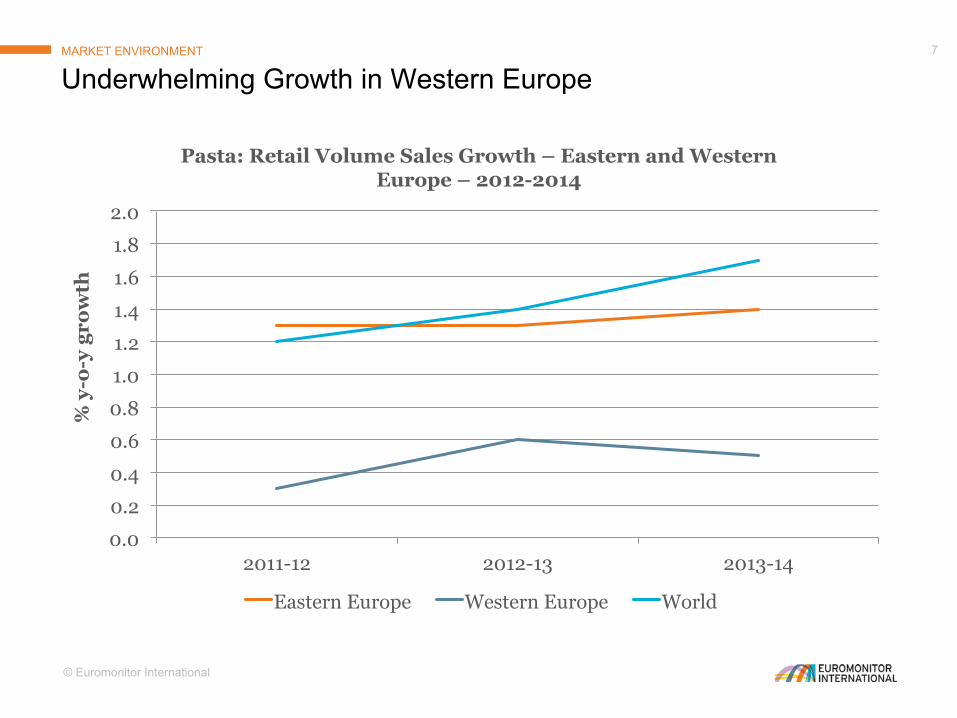

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2011-12 2012-13 2013-14

% y

-o-y

gro

wth

Pasta: Retail Volume Sales Growth – Eastern and Western Europe – 2012-2014

Eastern Europe Western Europe World

Underwhelming Growth in Western Europe MARKET ENVIRONMENT

© Euromonitor International

8

0

20

40

2010 2011 2012 2013 2014

US

$ bn

rsp

Global Pasta Market Size by Category – Value 2010-2014

Dried Pasta Chilled/Fresh Pasta Canned/Preserved Pasta

0

10,000

20,000

2010 2011 2012 2013 2014

'00

0 t

onn

es

Global Pasta Market Size by Category – Volume 2010-2014

Dried Pasta Chilled/Fresh Pasta Canned/Preserved Pasta

Value Growth Outpace Volume in Global Pasta MARKET ENVIRONMENT

1.4% CAGR

5.8% CAGR

© Euromonitor International

9

2013 Global Pasta Retail

Value: US$27.9 billion

2018 Global Pasta Retail

Value: US$31.3 billion

-500 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

Absolute Market Value Growth by Region – 2013-2018

Middle East and Africa Latin America Eastern Europe Asia Pacific North America Australasia Western Europe

Europe Contributes Little to Global Pasta Value Growth up to 2018 MARKET ENVIRONMENT

© Euromonitor International

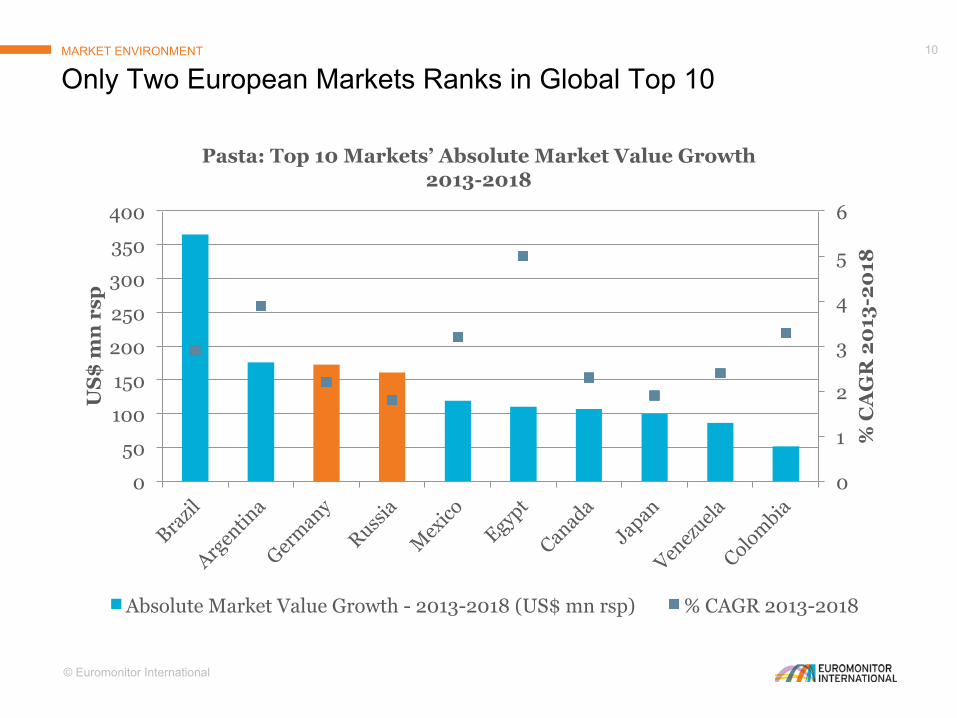

10

0

1

2

3

4

5

6

0

50

100

150

200

250

300

350

400

% C

AG

R 2

013

-20

18

US

$ m

n r

sp

Pasta: Top 10 Markets’ Absolute Market Value Growth 2013-2018

Absolute Market Value Growth - 2013-2018 (US$ mn rsp) % CAGR 2013-2018

Only Two European Markets Ranks in Global Top 10 MARKET ENVIRONMENT

© Euromonitor International

11

Top Growth Markets in Europe – 2013-2018 MARKET ENVIRONMENT

Belarus 3.9%

Ukraine 3.3%

Serbia 2.7%

Austria 3.7%

Germany 2.2%

United Kingdom

0.9%

% CAGR 2013-2018, retail value terms, 2013 fixed exchange rate, US$ million

© Euromonitor International

12

-20

0

20

40

60

80

100

120

140

160

180

200

Germany Russia UK Austria Norway Ukraine Poland Belarus Serbia Portugal

Abs

olu

te M

arke

t V

alu

e G

row

th –

20

13-2

018

- U

S$

mn

rsp

Top 10 European Pasta Markets’ Growth Prospect by Category 2013-2018

Canned/Preserved Pasta Chilled/Fresh Pasta Dried Pasta

Still Dried Pasta Generates Most of European Growth MARKET ENVIRONMENT

© Euromonitor International

13

-600.0

-500.0

-400.0

-300.0

-200.0

-100.0

0.0

Italy Spain Switzerland Romania France

US

$ m

n r

sp

Five European Markets’ Negative Growth Prospects 2013-2018

Absolute Market Value Growth - 2013-2018 (US$ mn rsp)

Market Value Contraction in European Markets MARKET ENVIRONMENT

© Euromonitor International

14

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013

Axi

s T

itle

Western Europe Pasta Competitive Landscape

2010-2013

Top 10 Companies Private Label Others

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013

Axi

s T

itle

Eastern Europe Pasta Competitive Landscape

2010-2013

Top 10 Companies Private Label Others

Moderately Consolidated but Private Label Dominated Europe MARKET ENVIRONMENT

STILL UNSTABLE MARKET ENVIRONMENT

ADDING VALUE TO PASTA

LESSONS FROM BEYOND EUROPE

KEY TAKEAWAYS

© Euromonitor International

16

Convenience

Health Credentials

“Big Night- In”

Pasta Opportunities in the Gloomy Economy ADDING VALUE TO PASTA

© Euromonitor International

17

Smaller outlets lose share

Supermarkets/ hypermarkets stand up to discounters

0

10

20

30

40

2008 2013

% s

ales

Eastern Europe: Pasta Distribution Channel Breakdown – 2008/2013

Supermarkets

Hypermarkets

Discounters

Independent Small Grocers

Time Scarcity Drives Need for Convenient Shopping ADDING VALUE TO PASTA

0

20

40

60

2008 2013

% s

ales

Western Europe: Pasta Distribution Channel Breakdown – 2008/2013

Supermarkets

Hypermarkets

Discounters

Independent Small Grocers

© Euromonitor International

18

Pasta Meals: Convenient Cooking - Preparation ADDING VALUE TO PASTA

Pasta dish promotions

Cooking time promoted

front of package

Single portion – on-the-go

consumption

© Euromonitor International

19

-5

0

5

10

15

20

25

30

2008-09 2009-10 2010-11 2011-12 2012-13

% y

-o-y

gro

wth

Western Europe: Pasta Growth Performance by HW Category 2009-2013

Gluten-Free Pasta NH High Fibre Pasta Organic Pasta Pasta

0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000

Western Europe: Pasta Retail Value Sales by Category - 2013

Gluten-Free Pasta NH High Fibre Pasta Organic Pasta "Standard" Pasta

Premium Price of Healthy Pasta Offers Dynamic Growth – but on Small Scale

ADDING VALUE TO PASTA

© Euromonitor International

20

215

220

225

230

235

2009 2010 2011 2012 2013 2014

US

$ bi

llio

n

Western Europe: Total Retail Value Sales through Full-Service

Restaurants 2009-2014

• Challenging economy underpins home cooking trend

• Italian cuisine grows in popularity

0

10

20

30

2008 2013

% o

f to

tal c

hil

led

rea

dy

mea

ls

% Italian Chilled Ready Meal – 2008-2013

Austria Germany

Dried Pasta Eating into Share of Foodservice ADDING VALUE TO PASTA

© Euromonitor International

21

Natural ingredients

Variety of vegetable fillings No preservatives

Chilled Formats Thrive on Quality and Price in Germany ADDING VALUE TO PASTA

0

1

2

3

Germany Austria Germany Austria

Dried Pasta Chilled/Fresh Pasta Eu

ro /

40

0 g

pac

k

Dried vs Chilled/Fresh Pasta Unit Prices through Supermarket vs Discounter - 2013

Supermarket Discounter

Variety of Retail Formats

© Euromonitor International

22

Dried Pasta

Price

Dried formats are

the “real Italian style”

Benefits from

television cooking

New shapes, even for children

Wholegrain and organic

lines tap into health trend

“Big night in” occasions

Dried pasta outperformed chilled/fresh formats in the UK ADDING VALUE TO PASTA

© Euromonitor International

23

Austrian brands dominate

Innovation targets food intolerance consumer

group

Nostalgia in packaging

Pasta for less than €1 per kg

Strongest Western European Growth for Pasta - the Austrian Way ADDING VALUE TO PASTA

© Euromonitor International

24

0

500

1,000

1,500

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

‘00

0 t

rip

s

Tourism Arrivals from Eastern Europe in Italy 2000-2014

Arrivals from Poland Arrivals from Russia

Travelling to Italy is expected to increase significantly because of safety concerns in competitor markets like Egypt and Tunisia.

Italian-travelled consumers in Eastern Europe are more receptive to pasta offerings than the rest of the population.

Increased Travel to Italy Inspires Eastern European Pasta Sales ADDING VALUE TO PASTA

© Euromonitor International

25

Russia: Pasta Dynamically Growing Source of Carbohydrate ADDING VALUE TO PASTA

-4

-3

-2

-1

0

1

2

3

4

5

6

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

Potatoes Pasta Rice

% C

AG

R 2

00

9-2

013

‘00

0 t

onn

es

Pasta Versus Rice and Potato in Russia. Retail Volume Growth – 2009-2013

Total Volume, 2013 % CAGR 2009-2013

© Euromonitor International

26

0

10

20

30

40

50

Russia Hungary Poland

% o

f p

asta

sal

es t

hro

ugh

In

dep

end

ent

Sm

all

Gro

cers

Pasta Sales Through Independent Small Grocers – 2008-2013

2008 2009 2010 2011 2012 2013

Consumers continue to be quite price sensitive and trade down to side dish staples during periods of economic duress

Low, competitive price at independent groceries is necessary

Eastern Europe: Expansion In Independent Groceries a challenge ADDING VALUE TO PASTA

© Euromonitor International

27

• Wholemeal, free-from, organic, fortified The health conscious

• Diverse distribution channel • Pasta for less than €1 per kg The price conscious

• Promote short cooking time/easy pasta recipes The time conscious

• Continuous expansion of premium fresh pasta offerings, e.g lamb-filled wine flavoured chilled pasta

The taste conscious

Europe: Producers Target Wider Consumer Range ADDING VALUE TO PASTA

STILL UNSTABLE MARKET ENVIRONMENT

ADDING VALUE TO PASTA

LESSONS FROM BEYOND EUROPE

KEY TAKEAWAYS

© Euromonitor International

29

Middle East and Africa & Latin America Drive Global Growth LESSONS FROM BEYOND EUROPE

992.3

1,825.1

72.0 482.5

Absolute Market Value Growth by Region – 2013/2018 - US$ mn rsp

Latin America

Middle East and Africa

Europe

Others

© Euromonitor International

30

Latin America Proven specially popular among less affluent consumers.

Mexico Versatility is a key driver of sales in the Mexican market.

Middle East & Africa Adoptable to a variety of traditional cuisine with sauces and fillings

Iran Diversification of products on store shelves & withdrawal of bread subsidies

Pasta Beyond Europe

Versatility and Adaptability the Key to Success LESSONS FROM BEYOND EUROPE

STILL UNSTABLE MARKET ENVIRONMENT

ADDING VALUE TO PASTA

LESSONS FROM BEYOND EUROPE

KEY TAKEAWAYS

© Euromonitor International

32

Western Europe: Largest Potential in Premium formats

Eastern Europe: Strike Balance between Quality and Price

Tailor and market offering to wide range of consumer segments

Retail Expansion is Key for Reaching New Consumers

Winning Strategies in Europe KEY TAKEAWAYS

THANK YOU FOR LISTENING Ildikó Szalai Senior Analyst Euromonitor International www.euromonitor.com [email protected] +44 (0) 20 7251 8024 EXT 2406