part i jan 2010 - can airlines power ancillary revenue with digital media and better wifi platforms?

TRANSCRIPT

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

1

What can digital entertainment, WiFi,

and mobile mean for airlines?

Part I - January 2010 Alford Strategic Development

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Introduction

2

• Airline WiFi will serve 400 - 500 million annual US airline passengers by 2012

• 300% - 400% larger than COMBINED projected iPad, Kindle, Xbox, Wii, PS3, and Netflix user bases

• US airlines could drive $3-5 Billion via revshare and customer acquisition partnerships with digital media firms

• …but charging travelers for WiFi cuts the head off the market

• “The 60-hour Cycle” - use knowledge of the itinerary to deliver impulse-buy content, entertainment, and

location-based services via mobile device, laptop, or IFE screen – from door-to-door roundtrip

• “Think Outside the Flight” - Mobile enables ~25 touchpoints – each way

Convergence of mobile technology and airline WiFi installations with digital entertainment’s fast growth could mean

significant ancillary revenue opportunity for airlines and WiFi providers…

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Airline WiFi and digital entertainment growth

3

Airline WiFi installations are growing quickly…

• 400M – 500M WiFi-enabled passengers by 2012 is on

scale of top websites’ traffic

0.5 1.1 2.2 4.27.3

10.916.4

2.6 3.03.8

4.9

5.9

7.0

8.6

0.1 0.31.0

2.1

3.3

4.6

6.3

0.71.9

4.2

4.6

4.8

5.0

8.8

$3.9B$6.3B

$11.1B

$15.8B

$21.3B

$27.5B

$40.1B

2008 2009 2010 2011 2012 2013 2014

US digital content sales - $US bn

Movie / Video Music eBooks Games

Digital entertainment markets could reach $40 Billion by 2014

• travelers are high impulse book, movie, and music consumers

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Alignment of forces

4

Mobile technology and adoption

create large opportunity next 3 yrs

Netflix, Amazon, Apple, Google battle

each other, publishers and studios Airlines need new revenue channels

Huge WiFi investment, but fee-

based model shrinks the market

• 2009 = $11 B loss; 2010 ~ $3 B loss

• Baggage and other fees make money,

but passengers don’t like them

• $100,000+ install cost per plane

• Travelers don’t want to pay WiFi fees

~ 500 million passengers

drive $1B to $5B digital

entertainment revenue

• Fierce competition for “living room”

share and market power

• Customer acquisition is critical focus

• Mobile growth and device convergence

• Location-based marketing extends

merchandising around flight

Even 6 months ago, this market did not exist…

…now forces are aligning to enable airlines to capitalize on fierce competition in digital entertainment

Digital media partners can

win captive market

competitors cannot access

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Who will own the content platform?

5

Content, merchandising,

and marketing platform

Airline-built?

Aircell?

Row 44?

Netflix?

Amazon?

YouTube?

Apple?

In-flight WiFi

service

Studios

and

publishers

Aircell and Row44 are strong WiFi technology partners…

…but airlines need world-class digital media and web / mobile merchandising partners to own the content, merchandising

and marketing platforms…

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

“Think outside the flight” to drive revenue and engagement

6

The 60-hour Cycle

Think outside the flight…travelers are high impulse-buy targets for roughly 30 hours each way

• Mobile enables 25 round-trip touchpoints:

• Market actively to drive revenue, don’t wait until passengers are in their seats

• Defray in-flight data costs by driving travelers to download content before boarding

Text-offer movie

for the flight

Deliver eBook

coupon before

customer buys at

Hudson News

Flight delay? Offer

free movie at $1

cost vs. $200

flight voucher

Enjoy The Economist

free on-board. Offer trial

subscription on landing

Scan 2D code for

exclusive offers

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

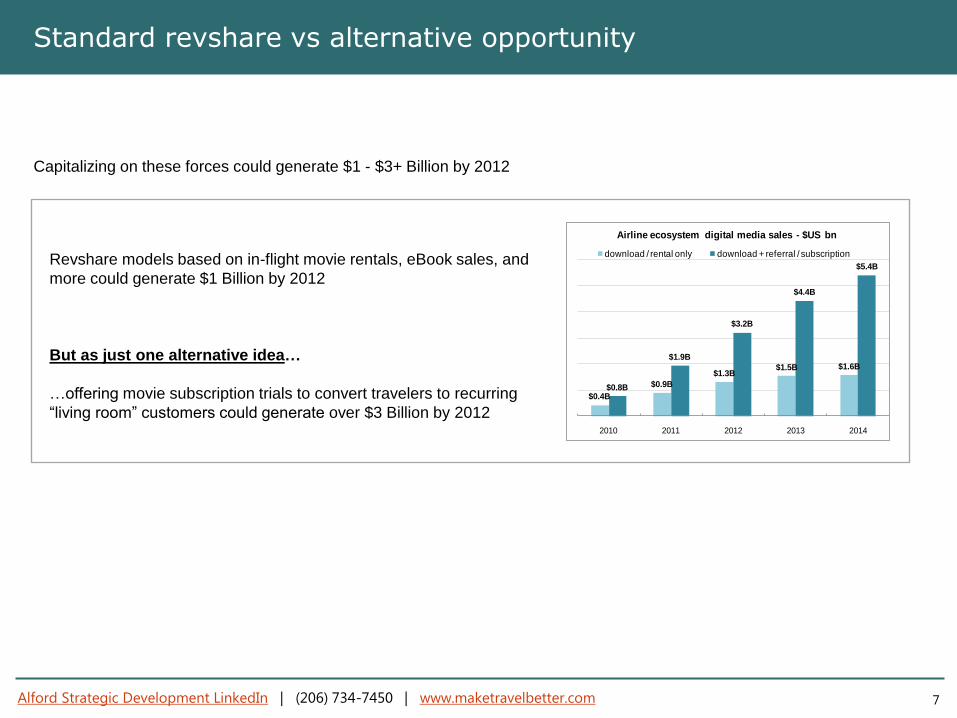

Standard revshare vs alternative opportunity

7

Revshare models based on in-flight movie rentals, eBook sales, and

more could generate $1 Billion by 2012

But as just one alternative idea…

…offering movie subscription trials to convert travelers to recurring

“living room” customers could generate over $3 Billion by 2012 $0.4B

$0.9B

$1.3B$1.5B $1.6B

$0.8B

$1.9B

$3.2B

$4.4B

$5.4B

2010 2011 2012 2013 2014

Airline ecosystem digital media sales - $US bn

download / rental only download + referral / subscription

Capitalizing on these forces could generate $1 - $3+ Billion by 2012

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

8

A conventional revenue share or affiliate model for movie, eBook and music download rentals can be profitable…

…but studio licensing and publisher royalties will take most of the income from airlines

Conventional revenue share approach

Traveler rents $5 movie

on one flight

Airline income $1

Partner income $1

Studio income $3

“GoGo Video-to-Go” Digital Entertainment Content

Ecosystem service

or

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

9

A customer acquisition model could deliver much more revenue to airlines, partners, and studios than a one-time in-flight

rental…don’t just settle for a conventional in-flight rental revenue share model

Customer acquisition / Referral approach

Traveler gets free movie by

choosing free trial

Airline income $12 - $16 referral

Partner income $120 annual subscription

Studio income $18 annual licensing fees

• As just one example, offer a free movie if traveler takes a free trial subscription for Netflix, registers for Amazon, etc

• Anecdotally, ~70-80% of travelers asked prefer the free movie / free trial option over paying for a rental

Digital Entertainment Content

cloud-based distribution or

…note for digital partners - lock competitors out…airline contracts with WiFi providers are 10-year terms

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

10

The fierce digital media battle for “living room share” is driven by customer acquisition…

Compare ~400 million WiFi passengers in 2012 to:

• iPad and Kindle install base of 20-27 million units

• Netflix subscriber base of 17-20 million

• Xbox, Wii and PS3 install bases of ~40+ million households

19M 28M 35M 39M 41M 41M 41M10M12M

15M 17M 19M 22M 24M

1M3M

7M11M 16M 20M 26M

0M0M

2M7M

11M15M

21M

0M16M

154M

320M

403M

463M 476M

2008 2009 2010 2011 2012 2013 2014

Millions

Annual WiFi pax vs hardware / subscriber bases

Game console Netflix subs Kindle iPad WiFi pax

Customer acquisition / Referral approach

…and airlines can offer a tremendous customer base and potential customer acquisition channel…

Netflix aggressively cornered game

console and television streaming market

Amazon wants to be

relevant beyond eBooks Apple using iPhone and iPad to drive digital

video and eBooks after dominating music

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Why now?

11

0M7M 9M

21M

39M47M 47M

77M82M 83M

78M

107M108M102M

86M

124M122M115M

102M

128M126M118M

105M

Q1 08

Q2 08

Q3 08

Q4 08

Q1 09

Q2 09

Q3 09

Q4 09

Q1 10

Q2 10

Q3 10

Q4 10

Q1 11

Q2 11

Q3 11

Q4 11

Q1 12

Q2 12

Q3 12

Q4 12

Q1 13

Q2 13

Q3 13

Q4 13

Q1 14

Q2 14

Q3 14

Q4 14

WiFi providers need to replace a deteriorating revenue model just as installation capital costs take off…

• As with broader trends, passengers don’t want to pay for WiFi, and charging for it shrinks the potential media market

• WiFi providers are developing partnerships, but opportunity exists to create a better consumer experience

Row 44 partners with:

• SkyMall, HSN

Aircell announces:

• Gogo Video-to-Go

Continental tests:

• LiveTV

JetBlue tests BetaBlue

(with Amazon, Yahoo)

Virgin America creates

regarded RED in-flight

entertainment

Quarterly passengers with WiFi access

0M 0M

7M9M

21M

39M

Q1 2008 Q2 2008 Q3 2008 Q4 2008 Q1 2009 Q2 2009 Q3 2009 Q4 2009 Q1 2010 Q2 2010

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Disrupt the traditional IFE content value chain

12

Movie

Studios

Ovhd or seat-

back screens

Plane IFE

server

content and

film services

content ship

and storage Airport plane

load facilities

Traditional value chain

Cost = $150 M

No revenue

Future value chain

Mobile

Ovhd or seat-

back screens

Plane IFE

server

Movie

Studios

DECE content

platform WiFi service

Cost = $5 M

revenue opp herein

A new approach leveraging cloud-based digital services could disrupt the labor-intensive in-flight entertainment value chain

• Could save the airline industry ~ $150 Million

• Rule-of-thumb costs of $75 - $80 per flight for licensing and film services

• IFE serves ~ 20% of flights and is used to drive premium fares, but not direct revenue

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Summary – General factors to consider

13

• WiFi fees are less sustainable and drop usage significantly, missing

out on potential digital entertainment revenue

• Digital merchandising is high-margin and has the Earnings value of

a much greater volume of air fares

• IFE has been a cost center, but money can be made

• Airline markets could be a key battleground in digital entertainment

• Amazon can package all digital categories and retail

capability in an on-board and mobile solution

• Netflix leads the movie category, but offers no others

• Subscription-referral model could be much more lucrative

• Netflix offering standard $16 affiliate referral

• Lifetime value of subscription is significantly greater; leverage

huge passenger base in negotiations

From an airline perspective

• Airlines likely will want a one-stop solution

• Amazon can package all digital categories and its incredible

retail capability in an on-board and mobile solution

• Aggregate passengers

• Lock competitors out; don’t get locked out

• Customer acquisition channel is potentially much larger than

Netflix’s console deals

• Sheer size of the passenger base can influence markets, studio and

publisher leverage, and M&A activity

• Netflix subscriber growth is a key driver of its 30x PE multiple

and $4 Billion market value

• Amazon, Apple and YouTube have great general customer

bases, but assuming Netflix is a subject of M&A interest:

• If Netflix drives 4 million subscribers, its valuation could

increase significantly

• If Amazon takes those 4 million customers, Netflix

acquisition pricing could be lower

From a digital media partner perspective

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Appendices

14

Appendices

Digital entertainment industry overview

• Amazon, Netflix, Apple, Google comparison

• Movies

• eBooks

• Music

• Games

• Unit sale economics

Airline WiFi service provider summary

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Appendix – Potential partner comparison

15

Four players are best-positioned, but have key differences in what they provide and how they can benefit from air markets

Amazon Netflix Apple Google

Digital Media

positioning

How they can

benefit from

Air markets

General

strengths

• Mass niche - all categories

• eBook leader with strong Kindle

hardware platform

• New movie product coming?

• “sexy” brand and design talent

• Large digital cust base via iTunes

• iPhone base

• Airline market bias – exclusive iPod

jack in new Panasonic IFE systems

• The movie rental brand

• Single focus – no distractions

• 12 M subscribers, growing fast

• Console deals lock out competitors

• Recommendation engine

• Capital base and customer base

• Precedent for strategic patience

• Cloudfront streaming service

• Recommendation engine

• Movie subscription category killer

• No hardware platform

• Direct retail streaming and

streaming distribution partner

• Mass niche - all categories

• Music dominance with strong

hardware and iTunes distribution

• New eBook platform coming?

• Scanning large eBook library but

engaged in civil actions

• Testing movie product via YouTube

• Always a threat due to capital base,

search base, and innovative culture

• Android operating system could be

used to drive mobile content

• Lock out Apple and Netflix

• Drive Kindle in competitive market

• Gain music share in mature market

• Launch pad for movie product?

• Greater cust acquisition channel

than Netflix console deals

• Leverage vs studios, publishers

• Movie subscriber growth creates

M&A leverage if eyeing NFLX

• Publishers may approve “airline

window” to offer new eBooks

• Lock out Amazon and Apple

• May be greater cust acquisition

channel than console deals

• Leverage vs studios re licensing

and “day and date” schedules

• M&A pricing leverage if considering

being acquired

• Engage mobile consumer in

addition to home-based

• Lock out Amazon and Netflix

• iTunes movie / video trails Netflix

• Drive eBook business for iPad

• Leverage vs studios, publishers,

and labels

• Lock out Amazon and Apple

• Lock out Bing and Yahoo search

• Launch pad for YouTube movie

rentals

• Drive eBook business

• Mobile search and location-based

search opportunity

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Appendix – Digital Movie / Video overview

16

The market is just forming, and positioning for customer acquisition

and profitability is paramount. Expectations have increased with:

• Streaming technology advancement and cost reductions

• DECE’s common file format and Digital Rights Locker

• Increased competition and partnerships to stream to home-

networked HDTV’s, Blu-ray players, game consoles, and PCs

• Netflix’s aggressive positioning as retailer and distributor

• Apple’s aggressive iPad promotion

• Mobile video, processing and storage technology following

classic (maybe faster) advancement cycles

• Netflix overwhelmed Blockbuster and has a strong singular

focus, but not a large capital base

• It must drive customer acquisition, reduce churn and

streaming costs, and navigate studio licensing demands

• Netflix may be a necessary acquisition candidate

• Apple’s iPad launching successfully

• Amazon have significant financial muscle and content, but is

not on the radar in significant way

• YouTube has significant Google muscle and is testing movie

downloads, but continues to face revenue challenges

Competitive characteristics

$0.5 $1.1 $2.2$4.2

$7.3$10.9

$16.4

$21.7 $20.7 $19.7$17.7

$15.0$12.0

$9.0

$0B

$5B

$10B

$15B

$20B

$25B

$30B

2008 2009 2010 2011 2012 2013 2014

US movie sales & rentals - $US bn

digital movies physical format

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Appendix – Digital eBooks overview

17

The eBook market is tremendously dynamic, with Amazon, Barnes &

Noble, Apple, Sony, the Big 6 publishers, Google, and disruptive

publishing startups like Smashwords vying for influence.

• Kindle is Amazon’s bestselling item, and Amazon is holding to its

disruptive pricing strategy and walled-garden approach

• Google is still engaged in anti-trust and legal licensing issues to

scan older texts and develop its online service

• It is opposed by almost everyone else in the market

• Smashwords is building a publishing service aimed at disrupting

traditional publisher economic models – Amazon followed suit

• Magazine and newspaper publishers are forging on their own, led

by Hearst’s FirstPaper, to produce eReaders and content display

Competitive characteristics

As expected, Amazon’s success continues to attract competition in both

content and eReader-oriented hardware

• Apple launched its iPad and is arranging content deals

• Barnes & Noble’s Nook platform got a lot of holiday buzz, though

results are unclear

• Traditional publishers are threatening a new “day and date” release

window, similar to movie studios, to protect hardcover margins

$0.1 $0.3 $1.0 $2.1 $3.3 $4.6 $6.3

$38.0 $36.7 $36.0 $35.2 $34.5 $33.8$33.2

$0B

$10B

$20B

$30B

$40B

2008 2009 2010 2011 2012 2013 2014

US digital and physical book sales - $US bn

digital retail physical retail

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

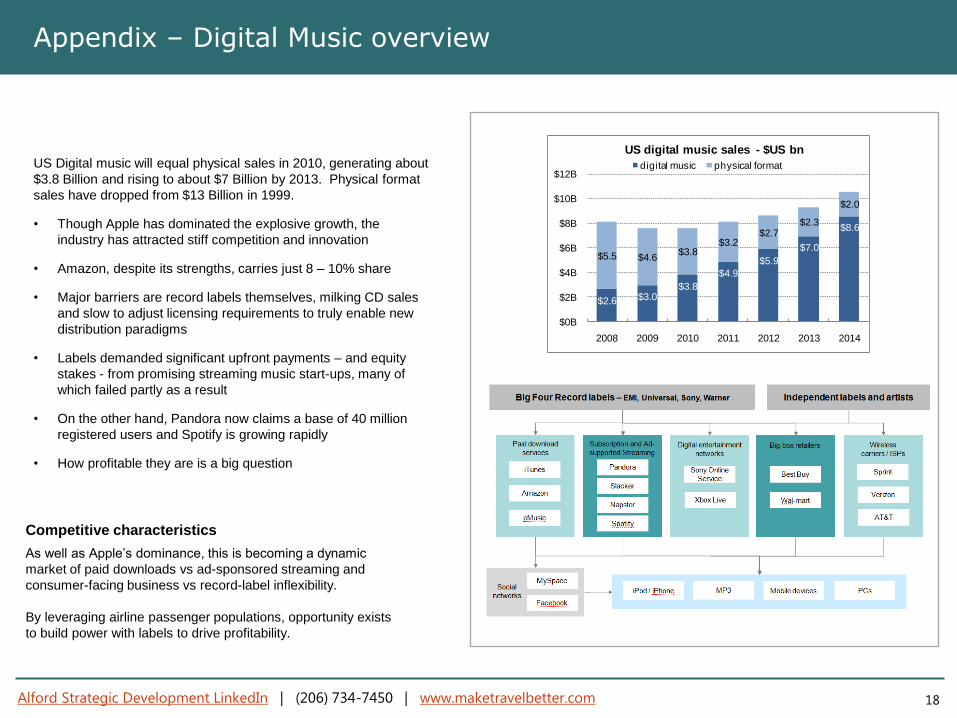

Appendix – Digital Music overview

18

US Digital music will equal physical sales in 2010, generating about

$3.8 Billion and rising to about $7 Billion by 2013. Physical format

sales have dropped from $13 Billion in 1999.

• Though Apple has dominated the explosive growth, the

industry has attracted stiff competition and innovation

• Amazon, despite its strengths, carries just 8 – 10% share

• Major barriers are record labels themselves, milking CD sales

and slow to adjust licensing requirements to truly enable new

distribution paradigms

• Labels demanded significant upfront payments – and equity

stakes - from promising streaming music start-ups, many of

which failed partly as a result

• On the other hand, Pandora now claims a base of 40 million

registered users and Spotify is growing rapidly

• How profitable they are is a big question

$2.6 $3.0$3.8

$4.9

$5.9

$7.0

$8.6

$5.5 $4.6$3.8

$3.2$2.7

$2.3

$2.0

$0B

$2B

$4B

$6B

$8B

$10B

$12B

2008 2009 2010 2011 2012 2013 2014

US digital music sales - $US bn

digital music physical format

Competitive characteristics

As well as Apple’s dominance, this is becoming a dynamic

market of paid downloads vs ad-sponsored streaming and

consumer-facing business vs record-label inflexibility.

By leveraging airline passenger populations, opportunity exists

to build power with labels to drive profitability.

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

Appendix – Digital Games overview

19

Pyramid Research claims the global casual digital gaming market

will rise to $18 billion by 2014 from $6.9 billion in 2008.

However, little data exists to verify this or determine which content

platforms or game publishers are driving the business.

Often anecdotal evidence of potential opportunity includes:

• In the US, digital game sales allegedly topped $1 Billion in

2009, and the iPhone game market may have been

accountable for $250 Million of it

• 250 million people are active social gamers, up from 100

million just several months ago in April

• VC firms have poured money into companies such as Zynga,

Playdom, which received $40 Million from Kleiner Perkins.

• EA acquired Playfish for $400 Million

• Virtual gaming goods are widespread outside the US, and may

now generate $1 billion in the US, up 100% from 2008, as

sales and gifts grow on Facebook, etc.

Competitive characteristics

The burning platform might be to use casual game distribution

as a complementary product offering to drive deals with airlines

and share in the other major categories.

$0.7$1.9

$4.2 $4.6 $4.8 $5.0

$8.8

$0B

$2B

$4B

$6B

$8B

$10B

2008 2009 2010 2011 2012 2013 2014

US digital game sales - $US bn

digital games

Alford Strategic Development LinkedIn | (206) 734-7450 | www.maketravelbetter.com

20

About Jonathan Alford

With 16+ years of experience in consumer and business travel, hospitality, and retail, Jonathan’s work centers on dual principles of driving a better traveler experience and advancing travel industry/company economic models. Recent focus includes creating visionary product and platform strategies for global corporate travel firms, leveraging new mobile/tablet platform capabilities and themes of "consumerization" to improve traveler experience, drive economic value to offset rising travel costs, and deliver enhanced duty of care to mitigate travel risks as emerging economies shift. Recognized thought leadership influencing disruption of airline industry WiFi and digital entertainment (manifested in current advancements in both in-flight and "outside the flight" experience) and promoting voice recognition technology impact in mobile travel search and itinerary management. Jonathan was awarded an Olympic Order of Excellence for executive program and Games-wide operations management at the 2002 Winter Olympics, judged best-managed Games in history. He is a graduate of The Johnson School at Cornell University and the University of Virginia.

About Alford Strategic Development