part i -general principle define tax

TRANSCRIPT

PART I -GENERAL PRINCIPLE Define Tax Mathew v Chicory Marketing Board – Latham CJ of HC, Australia Characteristics of Tax

1. Compulsion 2. No Quid pro quo 3. Tax is payable in money 4. Public Purpose

Cannons of Taxation 1. Equality and Ability – Adam smith- every state, Equals should be alike 2. Certainty 3. Convenience 4. Economy- expenditure in collecting < Tax

Distinction Between Tax and Fees S T Swamiar v Commissioner H R & C E – Levy is fees not tax M/s Krishna lal Lakashmi Chand v State of Haryana- quid pro quo is an ess element of fees P Kanadasa v State of Tamil Nadu – quid pro quo is irrelevant case of regulatory fees State of UP v Sitapur packing Wood Suppliers –SC, levy or fee quid pro quo is necessary By virtue of 96 - List I – Parliament enact Fees By virtue of 66- List II – parliament enact Fees By Virtue of 47 of List II – Concurrent List- Both can enact Fees

By Virtue of 82 to 92 B – List I schedule VII to constitution -Parliament By Virtue of 46 to 63 – List II Schedule VII - State Direct Tax and Indirect Tax Direct Tax- Income from Salary Indirect tax- Sales Tax- Intermediary collected Methods of Taxation

1. Propositional 2. Progressive 3. Regressive 4. Degressive

Constitutional Basis of taxation Art 265- No Tax shall be levied or collected expect by authority of law Art 246 (1) – List I ( Union List) 7th Schedule – 82 to 92 B of List I the parliament can Art 246 (3) – List II ( State List) 7th Schedule- 46 to 63 of List II the State legislature can Immunity of Instrumentalities – 285 to 289- restriction of taxing Power

1. Union property exempted from State Tax 2. State shall not tax, Sale or Purchase of good outside the state 3. State cannot Tax for using electricity and its sale by Govt of India 4. No State law to tax railway for operation of electricity 5. Property of Income of State exempted from union

Taxation Laws and Fundamental Rights Article 14 – Right to equality

Venkateswara Theatre v State of Andhra Pradesh – levy, based on person admitted earlier, now gross total collected, not violation of art 14. Western India theatre v cantonment board – seating capacity, not violation Indian Express Newspaper v Union of India – based on circulation, small, medium, big- not violation of article 14

Page 1 of 10 Tax law- Semester 4 Kerala University - 2017-2020

Read Anil K Nair Book, Before Reading This Short Note ullaskrishnan.com/llb

PART II -INCOME TAX ACT 1961 Assessment Year ( 2020-2021) comes after FY – Income Taxed Financial Year ( 2019-2020) which you earn income 1st April to 31st march (Previous Year)

Exceptions – Discontinued business, leaving India long term, income of NRI shipping company no representative in India, income of person alienate his asset

Assessee 1. Individuals 2. HUF 3. Company 4. Firm 5. Association of person or body of individuals whether incorporated or not 6. Local Authority 7. Every Artificial / Judicial Person

Surcharge on taxable income- 10% - 50 lac or more up to 1 crore, 15% more than 1 crore, Edu cess- 3% Local Authority / Partnership Firm – 30% , 12%surcharge if Taxable income above 1 crore, 3% Edu Cess Companies

• Domestic – 25% turn over below 50 crores, 30% if above, Sur 7% above on taxable income, above 10 crore then 12% and Edu cess 3%

• Foreign companies- Royalty -50% of taxable income, Fees for technical -50%,other earned income -40%, Sur 2% exceeds 1 crore, 3% exceeds 10 crore, 3% edu cess

Cooperative society

Sur- 12% if more than crore, Edu cess- 3% NRI, HUF, AJP, BOI, AOP

Sur 10% more than 50 lac to 1 crore15% more than 1 crore Edu cess :3%

Page 2 of 10 Tax law- Semester 4 Kerala University - 2017-2020

Read Anil K Nair Book, Before Reading This Short Note ullaskrishnan.com/llb

Definition of Income- S 2(24) IT act 1961 CIT v Shawallace Co- income is periodically monitory , return coming for regularity

Gopal Saran Singh v CIT – anything properly described income as taxable under act , unless expressly exempted

CIT v G R Karthikeyan – Motor car prize income tax Definition of Agriculture Income – 2(1)(A)

CIT v raja Benoy Kumar S roy – prior to germination essential, sowing seed, watering by planting by assessee , subsequent operations weeding, pruning alone not constitute CIT v J K Chaudary – spontaneous harvesting not agriculture CIT v Bacha F Gusdar – dividend by company in agriculture field is not agriculture income State farming Corporation v CIT – sugarcane cultivation , tender sale is not agriculture income RM Chidhambhara pillai v CIT – Salary and interest for capital and share profit from firm engaged in agriculture, is agriculture income Rent received by land lord for agriculture purpose is agri income Enhance product in to selling market – enhanced income is agriculture income Maharaja of Kapurthala v CIT – sale of forest and trees is not agri income Chellaiah Pillai v CIT- lease fo land for grazing of cattle required for agriculture pursuit is agriculture income

Computation

Page 3 of 10 Tax law- Semester 4 Kerala University - 2017-2020

Read Anil K Nair Book, Before Reading This Short Note ullaskrishnan.com/llb

Capital Income and Revenue Income & Capital Expenditure and Revenue Expenditure Capital Income/ Receipts and Revenue Income

Decided cases

Sharajudeen v CIT – compensation from one partner – capital receipt Shamseher printing press v CIT- suspension of export license ,capital receipt MB Tyres v CIT – government acquire building, compensation capital receipt Raja Giri Rubber and Produce v CIT- subsidy from board is capital receipt ( earlier it was receipt Malayalam Manorama plantation v CIT)

Travancore Rubber and tata Tea company v CIT – advance, old rubber tree sale, capital receipt

Capital Expenditure and Revenue Expenditure Capital expenditure is not deductible from the gross income

Bikaner Gypsum v CIT – land mining, railway station moved , revenue expenditure Hindusthan Commercial bank v CIT – Cost of advertisement is revenue expenditure Ambika mills v CIT – new machinery installation , expense, capital Sitalpur Sugar works v CIT – shifting machinery , office, capital expenditure CIT v karandura Development – refitting of plant new premise, revenue expenditure CIT v Aluminium Corporation – foreign technician , revenue expenditure Residential Status – sec 6 to 9

1. Taxable entities a. Individual b. HUF c. A firm or association of person d. Joint Stock companies e. Every other person

2. An individual and Hindu undivided family either be a. Resident and ordinarily resident b. Resident and not ordinarily c. NRI

Page 4 of 10 Tax law- Semester 4 Kerala University - 2017-2020

Read Anil K Nair Book, Before Reading This Short Note ullaskrishnan.com/llb

3. All other Assesses a. RI b. NRI

4. Residential Status of assess is determined from respective previous year Resident and Ordinarily Resident in India

1. Basic condition ( any one) a. In India previous 182 days or more b. In India for period of 60 days or more during the previous or 365 days or more

for the 4 preceding previous year 2. Resident and ordinarily resident in India (both conditions should satisfy)

a. He has been India for at least 2 /10 previous year preceding the relevant previous year

b. He has been India for total of 730 days or more for 7 years preceding the relevant previous year

Income exempted from Tax – sec 10, 10A,10B, 11 to 13 and 13A

Sections Particulars Exemption limit

Sec 10(1) Agricultural Income (from agricultural land, farm house, or sapling seedling grown in nursery) for self employed

Fully exempt from tax

Sec 10(2) Income received from HUF (Hindu-undivided family) by a tax payer in his capacity as a member of HUF

Fully exempt from tax

Sec 10(10C) Compensation received at the time of voluntary retirement for salaried employees

Exempt from tax up to a certain limit of compensation amount Rs. 5,00,000

Sec 10(10D) Amount received under life insurance policy including policy bonus

Fully exempt from tax

Sec 10(11)(12)

Amount withdrawn from Provident fund by salaried employees

Fully exempt from tax

Sec 10(10BC)

Compensation received in case of any disaster from central government

Fully exempt from tax

Sec 10(13A) House rent allowance (HRA) to salaried employees (rent paid by the employees to stay in a rented house)

Fully exempt from tax and 50% of salary amount if residential house is in metro cities otherwise 40% in non-metro

Sec 10(14) Children education allowance (salaried employees can claim a pre defined allowance for two children)

Exemption up to Rs. 100 per month per child

Sec 10(14) Special compensatory allowance for hilly areas or climate allowance or high altitude allowance to salaried employees

Exemption up to Rs. 7,000 per month

Sec 10(14) rule 2BB

Border area allowance or remote area or any disturbed area allowance to salaried employees

Exemption up to Rs. 1,300 per month

Sec 10(14) Tribal area allowance in: Madhya Pradesh, Tamilnadu, Assam, UP, Karnataka, West Bengal, Bihar, Orissa and Tripura to salaried employees

Exemption up to Rs. 200 per month

Sec 10(14) Compensatory field area allowance available in various areas of AP, Manipur, Sikkim, Nagaland, HP, UP and J&K to salaried employees

Exemption up to Rs. 2,600 per month

Sec 10(14) Transport allowance granted to employee for the purpose of commuting from home to office salaried employees

Exemption up to Rs. 1,600 (Rs. 3,200 for blind, deaf and dumb) per month

Page 5 of 10 Tax law- Semester 4 Kerala University - 2017-2020

Read Anil K Nair Book, Before Reading This Short Note ullaskrishnan.com/llb

Sec 10(15) Income from tax free securities to all assesses (Income received as interest from securities, bonds, deposits notified by government)

Fully exempt from tax

Sec 10(23D) Income from mutual fund (Any income earned from mutual funds registered under SEBI or set-up by any PSU or authorized by RBI)

Fully exempt from tax

Sec 10(34) Income from dividends (Tax paid by the company over the profits is considered as the final payment of tax no further credit to be claimed as dividends)

Fully exempt from tax

Sec 10(38) Long term capital gains on transfer of shares and securities

Fully exempt from tax

Sec 10(43) Reverse Mortgage (Any amount received by the individual as loan in lump-sum or in installments in transaction of reverse mortgage)

Fully exempt from tax

Sec 10(44) New Pension System exemption (Any income received by any person on the behalf of New pension system)

Fully exempt from tax

Sec 10(49) Income of National financial holdings company Fully exempt from tax

Tax Free Income

1. Agricultural Income 2. Gift Tax Exemption 3. LTA Exemption 4. Saving Bank Interest Exemption 5. Interest on PPF and PF 6. Tax on Dividend Income 7. Tax Free Bonds & Certificates 8. Leave Encashment on Retirement

Income tax exemption 1. House rent allowance - HRA tax exemption 2. Leave Travel Assistance - LTA tax exemption

Define Salaries Sec 14 – divide salaries in to five heads

1. Salaries = sec 15-17 2. Income from House r property – 22 to 27 3. Profit and Gain from Business or Professions – 28 to 44B 4. Capital Gains – 45 to 55

a. Short term capital assets b. Long term capital assets

5. Income under other sources = 56 to 59 Sec 27 Deemed Owner

Page 6 of 10 Tax law- Semester 4 Kerala University - 2017-2020

Read Anil K Nair Book, Before Reading This Short Note ullaskrishnan.com/llb

Income under Head Profit and Gains – sec 28 to 44B Deductions expressly allowed = 30 to 37

1. [Section-30] : Rent, Rates, Taxes, Repairs and Insurance of Building used for the purpose of the business.

2. [Section 31] : Repairs & Insurance Of Plant, Machinery & Furniture 3. [Section 32] : Depreciation

Atlas cycle Industries v CIT – Temple Scientific Engineering House Pvt Ltd v CIT- Books , drawings , designs plans etc

4. Expenditure of scientific research 5. Copy Right and Patent 6. Know How 7. Payment to Institution to carry out rural development 8. Interest on borrowed capital 9. Payment by way of bonus and commission 10. Insurance paid 11. PF 12. Gratuity 13. Revenue Expenditure 14. Bad Debts 15. Employee benefit 16. General deductions 37(1)

Income under Capital Gain – sec 45

• Long term – 20% tax rate

• Short term – 15% tax rate Sec 47 – transaction not regarded as transfer ( between share holders, Gift , Will) Sec 48- computation of Capital gain

Capital gain exempted from Tax

1. Sale of residential house 2. Sale and purchase of agriculture land 3. Compulsory acquisition of land and building part of industrial undertaking

Income from other sources sec 56 to 58 1. Dividend 2. Winning from Lotteries, etc. 3. Employees' Contribution towards Staff Welfare Scheme 4. Interest on Securities 5. Gift 6. Advance Money Received in the course of negotiations for transfer of a Capital Asset. 7. Compensation on Termination of Employment or Modification of Terms of Employment 8. Family Pension 9. Directors fees 10. Ground rent Deduction permissible under the head

1. Commission paid for realising the dividend

Page 7 of 10 Tax law- Semester 4 Kerala University - 2017-2020

Read Anil K Nair Book, Before Reading This Short Note ullaskrishnan.com/llb

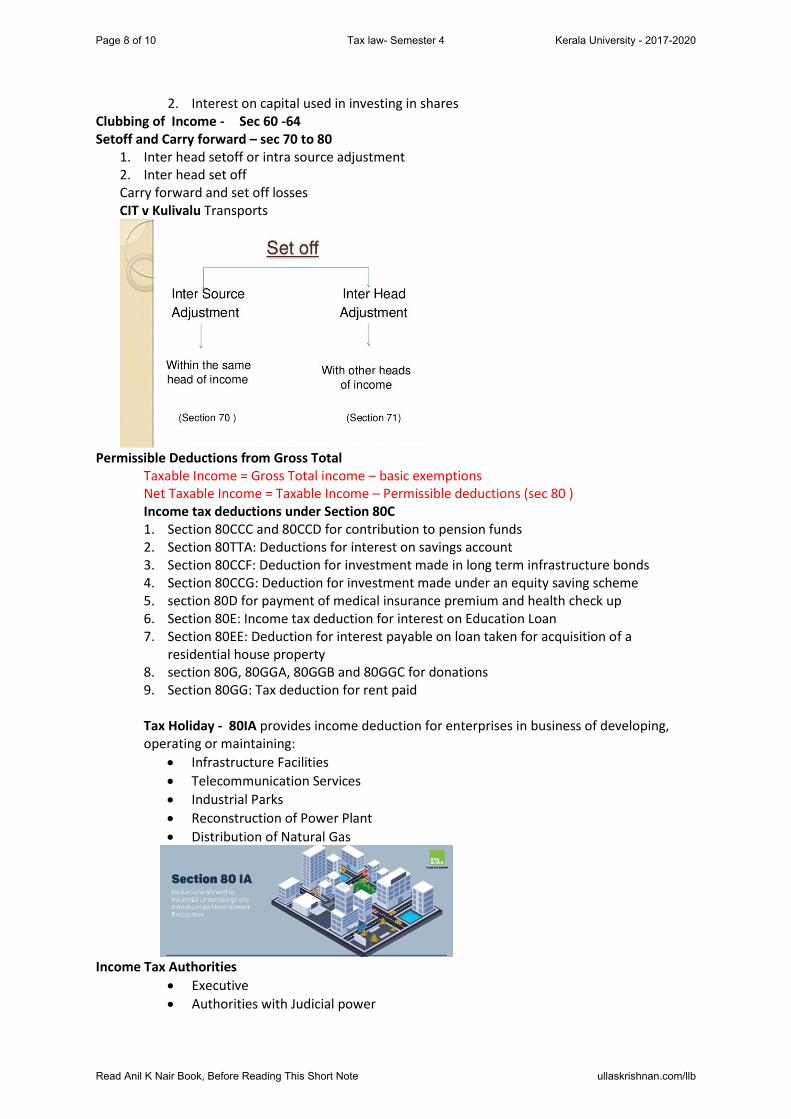

2. Interest on capital used in investing in shares Clubbing of Income - Sec 60 -64 Setoff and Carry forward – sec 70 to 80

1. Inter head setoff or intra source adjustment 2. Inter head set off Carry forward and set off losses CIT v Kulivalu Transports

Permissible Deductions from Gross Total Taxable Income = Gross Total income – basic exemptions Net Taxable Income = Taxable Income – Permissible deductions (sec 80 ) Income tax deductions under Section 80C

1. Section 80CCC and 80CCD for contribution to pension funds 2. Section 80TTA: Deductions for interest on savings account 3. Section 80CCF: Deduction for investment made in long term infrastructure bonds 4. Section 80CCG: Deduction for investment made under an equity saving scheme 5. section 80D for payment of medical insurance premium and health check up 6. Section 80E: Income tax deduction for interest on Education Loan 7. Section 80EE: Deduction for interest payable on loan taken for acquisition of a

residential house property 8. section 80G, 80GGA, 80GGB and 80GGC for donations 9. Section 80GG: Tax deduction for rent paid Tax Holiday - 80IA provides income deduction for enterprises in business of developing, operating or maintaining:

• Infrastructure Facilities

• Telecommunication Services

• Industrial Parks

• Reconstruction of Power Plant

• Distribution of Natural Gas

Income Tax Authorities

• Executive

• Authorities with Judicial power

Page 8 of 10 Tax law- Semester 4 Kerala University - 2017-2020

Read Anil K Nair Book, Before Reading This Short Note ullaskrishnan.com/llb

Search and Seizure- sec 132

1. Company – oct 31 2. Individual – Jul 31

Filing of Income tax return (139) and Assessment procedure ( 143,144) Sec 139(1)- mandatory and voluntary return

• Self Assessment

• Regular assessment o Assessment based on evidence o Best judgement assessment

THE KERALA AGRICULTURE INCOME TAX ACT 1991

Article 246(3) Entry 46 of VII schedule to the Constitution of India Definition of Agriculture Income – 2(1)

1. Rent or revenue derived from land in India used for agriculture purpose 2. Any income derived from land

a. By agriculture b. By agriculture performance c. By sale of produced raised by cultivator after the above said process

3. Any income owned by building used for cultivation and agriculture

Rate of Agriculture Income Tax for person

Firm – 35% Foreign company – 80% Domestic company or co-operative society

up to 25K 35%

25K to 100K 40%

1lac to 3 lac 45%

above 3 lac 50%

Deductions

• Land Revenue

• Local taxes , cess, municipal tax

• Rent paid for land

up to 40K Nil

40k to 60 K 10%

60K to100K 20%

above 100K 30%

Page 9 of 10 Tax law- Semester 4 Kerala University - 2017-2020

Read Anil K Nair Book, Before Reading This Short Note ullaskrishnan.com/llb

• Expense incurred for maintenance

• Machinery repair

• Interest paid on loan Agriculture Income Tax authorities – sec 24 Appellate Tribunal sec 73

WEALTH TAX 1957 Entry 56 of List I of the VII schedule – Discontinued from 2016 Net wealth - sec 2(m) Net wealth = ( assets + deemed assets ) –( exempted assets + debts incurred in relations to assets ) Asset – sec 2(e)(a)

V S Nayak v CWT – Title in legal case, but still liable to pay tax Deemed asset – sec 4 Assets expected from Tax – sec 5 Definition of Sale – sec 2(42) Value Added tax Act 2003 Definition of Dealer – sec 2(15) Turnover – sec2( 52)

CENTRAL EXCISE ACT 1944 Duties of Excise defined in – sec 3 Power of search and seizure- sec 12 F Power Arrest – sec 13

Page 10 of 10 Tax law- Semester 4 Kerala University - 2017-2020

Read Anil K Nair Book, Before Reading This Short Note ullaskrishnan.com/llb