outlook for the european banking sector - axiom

TRANSCRIPT

This document is not legally nor contractually binding and is intended for strictly personal use. Although the information presented hereby comes from

reliable sources it cannot be guaranteed. The judgement formulated hereby reflect our opinion as of the date of publication and may be subject to change.

. AXIOM ALTERNATIVE INVESTMENTS - 1 Conduit Street – 4th floor London W1S 2XA

| Phone: +44 203 80 70 862 |[email protected]

March 12, 2020 – Outlook for the European banking sector

Outlook for the European banking sector

Summary

The world economy and the financial sector are facing a dual threat: a global pandemic triggered by the Covid-19 virus and an oil price war between Saudi Arabia and Russia.

In this note we assess the impact of very strict stress scenarios on the European banking sector.

• The shock on the energy sector looks like déjà vu (2016). This risk is mainly borne by US banks and remains very manageable for European banks.

• The impact of the virus, and its short-term consequences on sectors such as aviation, shipping or tourism, could eliminate a significant share of banks' 2020 profits, but does not, in our opinion, represent a significant risk to banks’ capital.

• Finally, the impact of a recession (assuming that the virus spreads and quarantine measures are extended to all European countries) shows that only a limited number of banks would face a coupon risk on their hybrid bonds.

In order to mitigate these risks, the ECB’s measures can be summarized as follows: a huge disappointment for sovereign bonds but a massive package designed to support banks.

Since the 2008 crisis, regulators have forced banks to build up very large capital buffers. They are very well capitalized to face stress periods.

In practice, in our view, banks are almost assured of not coming under significant pressure from the supervisory authorities if they were to face a stress scenario that would affect their capital.

YTD March 10th,2020 Since February 21st, 2020

Indices

Stoxx 600 Bank Net Return index in EUR -28.56% -29.09%

Euro Stoxx 50 Index in EUR -22.30% -23.43%

Coco Index (Solactive AXIOM CoCo EUR Hedged) -3.76% -6.17%

Axiom funds

Axiom Optimal Fix (Unit C EUR) -1.14% -1.38%

Groupama Axiom Legacy 21 (Unit P EUR) -1.27% -3.56%

Axiom Obligataire (Unit C EUR) -1.51% -3.42%

Axiom Contingent Capital (Unit C EUR) -3.47% -5.54%

Axiom Equity (Unit C EUR) -31.26% -30.80%

Source : Bloomberg, Axiom

2

This document is not legally nor contractually binding and is intended for strictly personal use. Although the information presented hereby comes from

reliable sources it cannot be guaranteed. The judgement formulated hereby reflect our opinion as of the date of publication and may be subject to change.

. AXIOM ALTERNATIVE INVESTMENTS - 1 Conduit Street – 4th floor London W1S 2XA

| Phone: +44 203 80 70 862 |[email protected]

A. The crisis

The world economy and the financial sector are facing a dual threat: a global pandemic triggered by

the Covid-19 virus and an oil price war between Saudi Arabia and Russia. While the former should be

a short-term shock – possibly with dramatic consequences – the latter could last longer as it is rooted

in deep geopolitical dissensions. This is illustrated by the two very important market moves below: the

price drop on oil was the largest since the first gulf war and the rise in the European investment grade

CDS index was a 23.5 standard deviation event!

The impact of the coronavirus has been extensively debated and we will not go into the details.

However, it is our belief that unfortunately the effects of the virus on most G7 countries will only differ

by a time lag – effectively, they could all see the same effects as Italy with a one to two weeks lag.

3

This document is not legally nor contractually binding and is intended for strictly personal use. Although the information presented hereby comes from

reliable sources it cannot be guaranteed. The judgement formulated hereby reflect our opinion as of the date of publication and may be subject to change.

. AXIOM ALTERNATIVE INVESTMENTS - 1 Conduit Street – 4th floor London W1S 2XA

| Phone: +44 203 80 70 862 |[email protected]

Focusing on the EU banking sector, what are the threats? We see three main risks.

• General recession risk. Banks are levered to their local economy. Recessions feed into their

P&L via increased provisions, lower loan volumes, etc. Even (very) temporary recessions have

hysteresis effects as bankruptcies cannot be unwound. This recession risk is not limited to

affected sectors: a rise in unemployment, for example, can increase losses on mortgages. We

believe the OECD and the ECB’s macroeconomic forecasts are slightly too optimistic.

• Lending to sectors at risk. Both the coronavirus and the oil shock will disproportionately affect

some sectors (tourism, energy, airlines, etc.) and will inevitably increase loan loss provisions

and risk exposure, for example via an increase of the drawing of committed facilities.

• Procyclical regulatory effects. Increased credit risk will feed into bank capital ratios via two

effects: higher probabilities of default will increase Risked Weighted Assets (RWA), and thus

lower capital ratios, and the new IFRS9 accounting rules will force banks to perform credit risk

assessments via economic models and possibly transfer exposures from Stage 1 to Stage 2,

which means switching from a 1-year expected credit loss to a lifetime expected credit loss

(effectively multiplying provisions by a 5 to 10 factor, depending on the type of lending.)

We do not see any genuine liquidity risk for EU banks: the ECB remains extremely accommodative (see

below), LCR are high and the ECB liquidity stress tests have shown the resilience of the sector.

B. Who is at risk

1. Energy risk

The 2016 oil crisis gave us very useful insights on the banks’ exposure to the North American energy

market and, since then, banks continue to update the markets on their exposures. Global banks’

funded and unfunded exposures to the sector are given below (it is crucial to also consider unfunded

exposures).

4

This document is not legally nor contractually binding and is intended for strictly personal use. Although the information presented hereby comes from

reliable sources it cannot be guaranteed. The judgement formulated hereby reflect our opinion as of the date of publication and may be subject to change.

. AXIOM ALTERNATIVE INVESTMENTS - 1 Conduit Street – 4th floor London W1S 2XA

| Phone: +44 203 80 70 862 |[email protected]

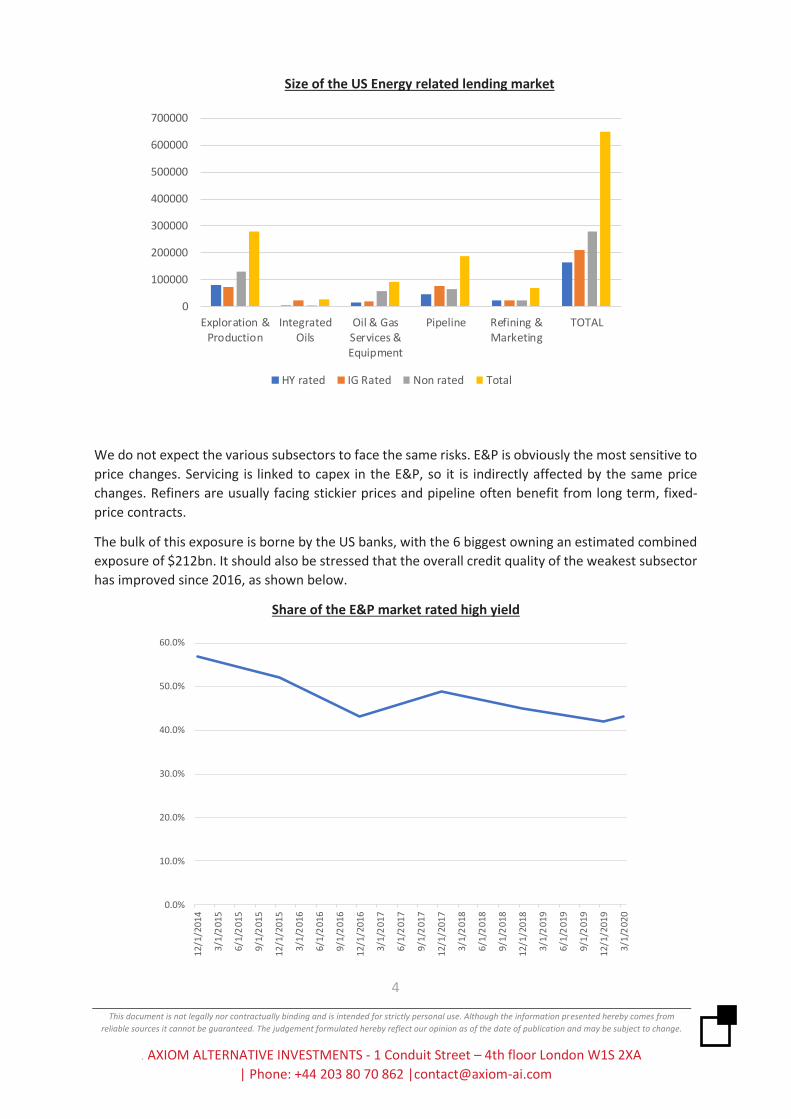

Size of the US Energy related lending market

We do not expect the various subsectors to face the same risks. E&P is obviously the most sensitive to

price changes. Servicing is linked to capex in the E&P, so it is indirectly affected by the same price

changes. Refiners are usually facing stickier prices and pipeline often benefit from long term, fixed-

price contracts.

The bulk of this exposure is borne by the US banks, with the 6 biggest owning an estimated combined

exposure of $212bn. It should also be stressed that the overall credit quality of the weakest subsector

has improved since 2016, as shown below.

Share of the E&P market rated high yield

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

12

/1/2

01

4

3/1

/20

15

6/1

/20

15

9/1

/20

15

12

/1/2

01

5

3/1

/20

16

6/1

/20

16

9/1

/20

16

12

/1/2

01

6

3/1

/20

17

6/1

/20

17

9/1

/20

17

12

/1/2

01

7

3/1

/20

18

6/1

/20

18

9/1

/20

18

12

/1/2

01

8

3/1

/20

19

6/1

/20

19

9/1

/20

19

12

/1/2

01

9

3/1

/20

20

0

100000

200000

300000

400000

500000

600000

700000

Exploration &Production

IntegratedOils

Oil & GasServices &Equipment

Pipeline Refining &Marketing

TOTAL

HY rated IG Rated Non rated Total

5

This document is not legally nor contractually binding and is intended for strictly personal use. Although the information presented hereby comes from

reliable sources it cannot be guaranteed. The judgement formulated hereby reflect our opinion as of the date of publication and may be subject to change.

. AXIOM ALTERNATIVE INVESTMENTS - 1 Conduit Street – 4th floor London W1S 2XA

| Phone: +44 203 80 70 862 |[email protected]

We are not HY Energy analysts, but specialized firms have published loss scenarios that range from 4%

in a base case approach to 8% in a severe stress approach. Those are the numbers that we use to assess

the risks European banks are facing, bearing in mind that European banks usually have lower risk

exposures (lending to high quality corporates, collateral trade finance, etc.) The 2016 crisis also

provides a useful benchmark to assess the provisions banks are facing. The banks most exposed are

well known and have not really changed since 2016, as shown below.

Energy exposures as a % of tangible book value

2. Virus risk and total exposure risk

Using EBA and company data, we can estimate the exposures banks have on selected sectors at risk:

transportation (with a focus on aviation), shipping and tourism / hospitality. We can also estimate the

SME exposure. Using S&P data, we are able to perform a stress test on those sectors by using a very

severe 2.5 standard deviations shock over the long-term default rates that were observed on those

sectors. Those numbers carry a very important health warning: the analysis does not reflect the quality

of each bank’s book, how much it is capitalized, etc. In particular, we think that banks that have

outsized exposures in some sectors usually have a very conservative risk appetite in those sectors and

the technical expertise to manage the risks. The numbers should only be used to provide orders of

magnitude.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

6

This document is not legally nor contractually binding and is intended for strictly personal use. Although the information presented hereby comes from

reliable sources it cannot be guaranteed. The judgement formulated hereby reflect our opinion as of the date of publication and may be subject to change.

. AXIOM ALTERNATIVE INVESTMENTS - 1 Conduit Street – 4th floor London W1S 2XA

| Phone: +44 203 80 70 862 |[email protected]

Losses on weak sectors as a % of pretax profits and % of book value

This chart has two key implications:

• Except for a tiny sample of banks, the shock is a profitability shock that could erase a significant

part of this year’s profits – especially if IFRS 9 provisions force banks to book a majority of losses

coming from the next few years. As an example, previous stress tests showed that IFRS 9 leadd to

an upfront booking of a large majority (up to 60%) of 3-year losses in the first year.

• However, in all cases, we believe capital is not significantly at risk from direct exposure to those

sectors.

3. Capital and recession risk.

We tried to combine this sectoral analysis with a general, macro-based analysis. For this, we rely on the latest EBA bank-by-bank disclosure and on the outcome of the previous stress tests.

Our base case scenario assumes a broader contagion and an extension of quarantine measures to all European countries. The key macroeconomic drivers will be the duration and severity of containment measures as well as the willingness of public institutions to socialize losses and boost investment. Given that retail trade, transport and hospitality directly account for over 15% of EU GDP, with tourism alone contributing close to 5%, we believe that the latest OECD interim forecasts, which assume deviations of respectively -0.5% and -1.6% in the base and pessimistic scenarios, should be adjusted downwards. We would expect containment measures on the continent to last between 1 and 2

0%

1%

2%

3%

4%

5%

6%

0%

20%

40%

60%

80%

100%

120%

140%

160%P

ira

eu

s

Co

mm

erz

Ban

kia

Sab

adel

l

NB

G

Deu

tsch

e

Alp

ha

Nat

ixis

Cre

d A

g

ING

RB

S

BB

VA

Euro

bank

Soc

Gen

AB

N

Caix

aBan

k

Inte

sa

Un

icre

dit

Stan

Char

t

DN

B

BN

P

Bar

cla

ys

Dan

ske

Ban

k

AIB

Rai

ffe

ise

n

SEB

Ers

te G

rou

p

BC

P

HS

BC

San

tan

de

r

No

rdea

Ha

nd

els

ban

ken

Swed

ban

k

Cre

dit

Su

isse

Ban

k o

f Ir

ela

nd

KB

C

BA

WA

G

UBS

Losses as a percentage of pretax profits (lhs) Loss as a percentage of TBV (rhs)

7

This document is not legally nor contractually binding and is intended for strictly personal use. Although the information presented hereby comes from

reliable sources it cannot be guaranteed. The judgement formulated hereby reflect our opinion as of the date of publication and may be subject to change.

. AXIOM ALTERNATIVE INVESTMENTS - 1 Conduit Street – 4th floor London W1S 2XA

| Phone: +44 203 80 70 862 |[email protected]

months, leading to a deviation from baseline projections of over 2%, i.e. a contraction in EU GDP of around -1%/-1.5% in 2020, which compares to the -3.5% stress test contraction in the adverse scenario.

Banks will feel the impact of the recessionary environment through higher provisions, lower loan growth, and possibly lower rates, impacting profitability, capital and asset quality. This is all considered in the stress testing methodology. As we focus mostly on fixed income instruments, we calculate the likely resulting CET1 ratios (assuming no management actions) to estimate the MDA risks – i.e. the risks that coupons could be suspended. We assume 0 countercyclical buffer – see below for a description of the actual, much more effective, supervisory package

MDA buffers post stress scenarios

This shows that only a small number of banks face a coupon risk on their hybrid bonds. We believe even those banks would be able to manage the risk with management actions – not to mention the fact that supervisory actions just announced would probably effectively lower the MDA threshold and erase the stress test impact.

C. The ECB’s response

After the BOE’s bold measures announced on March 11th, markets were eagerly expecting the ECB’s decisions. The stock market continued to fall after the news, for three reasons, in our view:

• There was no rate cut: unlike the Fed and the BOE, the ECB did not change its policy rate. We believe the market was disappointed by this, but we think the decision made sense. Empirical research has shown that at their current levels, a new rate cut could actually be harmful for the economy and the banks.

• There was no announcement on a change to the allocation of the public QE (issuer limit, capital

key.) Mrs. Lagarde was asked at least three times about this and kept answering “we will use the full flexibility of the program”, which suggests temporary deviations to the key but no bold

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

8

This document is not legally nor contractually binding and is intended for strictly personal use. Although the information presented hereby comes from

reliable sources it cannot be guaranteed. The judgement formulated hereby reflect our opinion as of the date of publication and may be subject to change.

. AXIOM ALTERNATIVE INVESTMENTS - 1 Conduit Street – 4th floor London W1S 2XA

| Phone: +44 203 80 70 862 |[email protected]

decision. Moreover, Mrs. Lagarde made a rather clumsy statement when she said that the ECB’s role is “not to close spreads”.

This might be true, but it was not the best moment to say it. It triggered the biggest 1-day move ever on the 10Y BTP yield.

• The positive news (see below) are extremely complex and we believe there was no clear explanation of their very substantial benefits. Algorithms are unlikely to have picked up on them.

On the positive side, there was an additional QE (€120bn), mainly targeted at the private sector (IG corporate bonds) but, much more significantly, a coordinated set of measures announced by the ECB, the SSM and the EBA.

• The first decision relates to the TLTRO and is extremely important as it introduces dual rates for the first time. Banks will be able to borrow at -75bps and still be able to deposit cash at -50bps. Banks with enough lending, will effectively be able to get a free 25bps return! Moreover, the borrowing allowance will be raised to 50% of eligible loans and the lending performance threshold is now 0%, so no growth required. This is effectively a large subsidy to the sector. The new rules will allow banks to borrow up to approximately €2.3tn. In order to ensure that banks can fully benefit from this facility, the ECB will also relax collateral rules, which should allay any liquidity fears.

• The second decision is about capital buffers: banks will be temporarily allowed to operate below the conservation capital buffer (2.5%) and the Pillar 2 Guidance (1.5% approximately on

9

This document is not legally nor contractually binding and is intended for strictly personal use. Although the information presented hereby comes from

reliable sources it cannot be guaranteed. The judgement formulated hereby reflect our opinion as of the date of publication and may be subject to change.

. AXIOM ALTERNATIVE INVESTMENTS - 1 Conduit Street – 4th floor London W1S 2XA

| Phone: +44 203 80 70 862 |[email protected]

average). The countercyclical buffers are also expected to be removed by national authorities. With an estimated 14tn RWA in the sector, this is effectively a lowering of the capital requirement close to 550bn€! A huge relief for banks that will have to bear the bulk of the effort to support the economy affected by the virus.

• The new allocation of the Pillar 2 Requirement (56% CET1, the rest with subordinated debt) that was scheduled for 2021 is implemented immediately.

• Crucially, the SSM and the EBA confirmed that they expect supervisors to apply the guidelines on non-performing loans in a flexible way. In practice, it means that banks will be able to use grace period or interest holidays on affected businesses without risking the transfer of the loan to the non-performing exposure category. It could also mean that a prudential filter is used to offset the transfer of some exposure to Stage 2 under IFRS 9 rules.

• The ECB will also adjust, on bank by bank basis, any remedial actions currently discussed. This is likely to include, at least partially, the very large TRIM impacts. The 2020 EBA EU-wide stress tests have been postponed to 2021.

We can summarize the ECB’s policy response as follows: a huge disappointment on sovereign bonds, a massive package designed to support banks. In practice, this means that banks are almost assured to face no supervisory pressure should they be hit by a stress scenario that would jeopardize their current capital requirements.