organise - insage

TRANSCRIPT

OrganiseJan – June 07

RestructureSept – Dec 06

AdvanceJuly – Dec 07

ROAR Ahead2008

001 Introduction to the ROAR Strategy002 Performance 2007003 CMS at a Glance004 Corporate Information005 Group Corporate Structure006 Letter to Shareholders008 Looking Back on 2007011 Operations Review020 Management Viewpoints021 Human Capital022 CMS Doing Good (Corporate Social Responsibility)024 Board Of Directors028 Senior Management029 Statement of Corporate Governance

037 Statement of Internal Control039 Group Audit Committee Report042 Additional Compliance Information044 Statement of Directors' Responsibility045 Financial Calendar 2007046 Five-Year Financial Highlights047 Financial Statements129 Analysis of Shareholdings131 List of Properties134 Group Directory136 Notice of Annual General Meeting137 Statement Accompanying Notice

of Annual General MeetingForm of Proxy

Contents

Overall Objective of the ROAR Strategy:Align our CMS businessesin terms of

1.Strategy2.Structure3.Systems4.Skills5.Culture

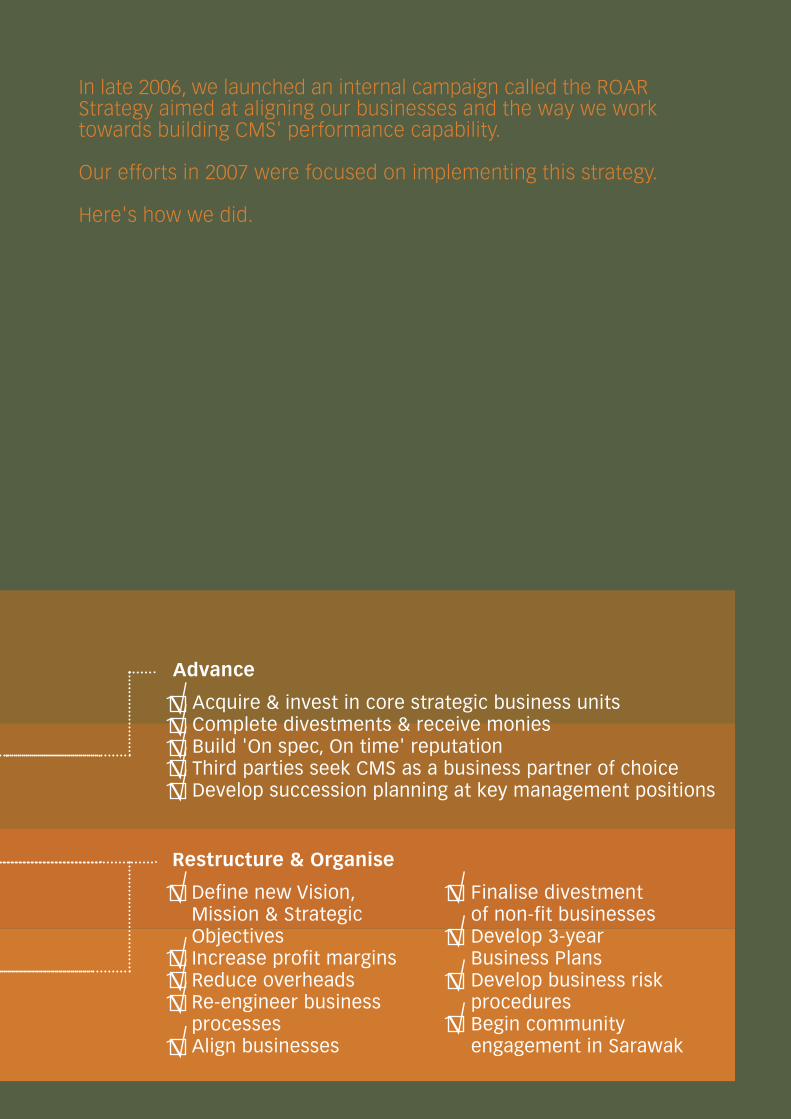

Restructure & Organise

Define new Vision,Mission & StrategicObjectivesIncrease profit marginsReduce overheadsRe-engineer businessprocessesAlign businesses

Finalise divestmentof non-fit businessesDevelop 3-yearBusiness PlansDevelop business riskproceduresBegin communityengagement in Sarawak

Advance

Acquire & invest in core strategic business unitsComplete divestments & receive moniesBuild 'On spec, On time' reputationThird parties seek CMS as a business partner of choiceDevelop succession planning at key management positions

√

In late 2006, we launched an internal campaign called the ROARStrategy aimed at aligning our businesses and the way we worktowards building CMS' performance capability.

Our efforts in 2007 were focused on implementing this strategy.

Here's how we did.

√√√√

√ √√√√

√√√√

Cahya Mata Sarawak Berhad

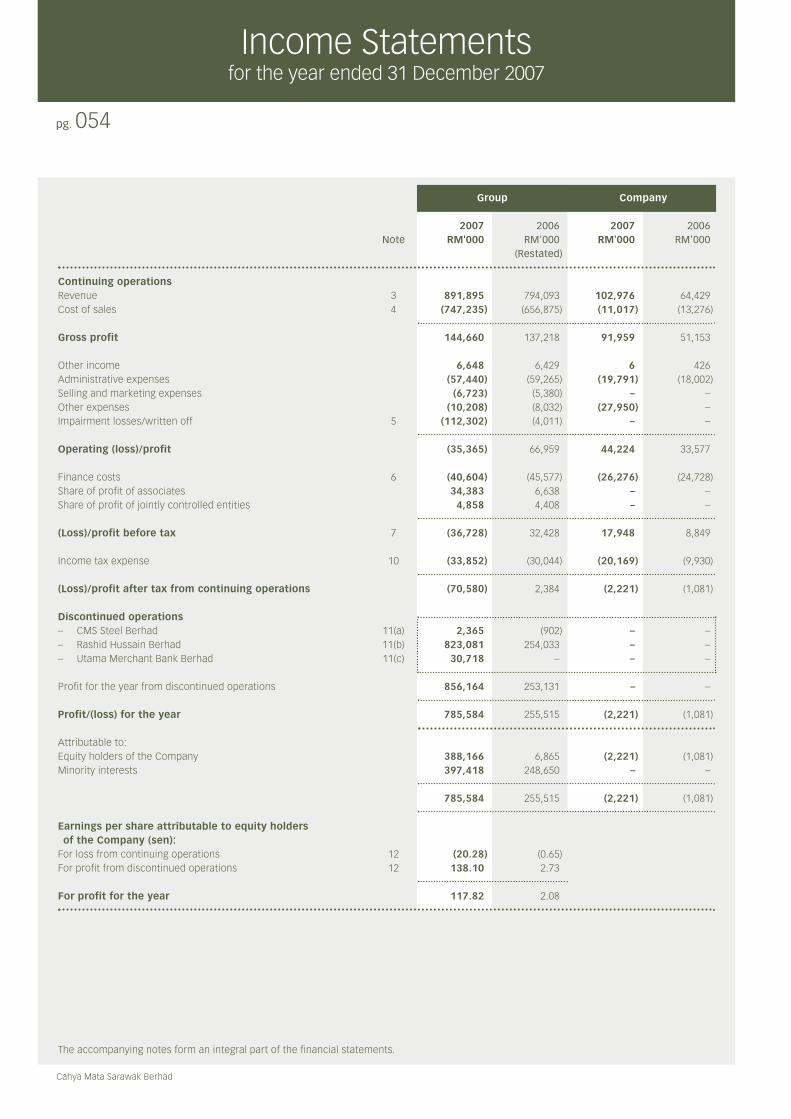

• Revenue:RM 2.55 billion

• Profit before tax:RM 887.44 million

• Net profit attributable toequity holders of the Company:RM 388.17 million

• Basic earnings per share:117.82 sen

• Gross dividends per share:15 sen

Key Products& Services

Cement ManufacturingCMS Cement, Sarawak's sole cement manufacturer,produces high quality Ordinary Portland cementat 2 plants – Kuching and Bintulu.With anannual production capacity of 1.75 million metrictonnes, the company meets customer demandfrom throughout the state of Sarawak with anestablished distribution network.

Clinker ManufacturingClinker, the main raw material of cement,is manufactured by CMS Clinker. Productioncapacity of CMS Clinker, East Malaysia's soleclinker producer, stands at 800,000 metric tonnesper annum.

Stone Aggregates (granite,microtonalite, limestone)CMS Quarries & CMS Penkuari together arethe largest aggregate producers in Sarawak,supplying 30% of the market.

PremixCMS Premix & CMS Premix (Miri) are Sarawak'sleading premix producers supplying high qualityasphalt for construction of highways, flyovers &airport runways. The Group owns & operates itsown bitumen emulsion plants.

Concrete BeamsPre-formed concrete products (square piles,bridge beams, culverts, cement sand bricks,kerbs) are produced by CMS ConcreteProducts & PPES Concrete Product in Kuching.

Steel WiresDrawn steel wires & wire mesh areproduced by CMS Wires in Kuching.

CMS GroupPerformancein 2007

Cahya Mata Sarawak Berhad

CMS at a GlanceCahya Mata Sarawak (CMS) is a leading

conglomerate listed on the Main Board ofthe Malaysian stock exchange, Bursa

Malaysia. With most of its operations basedin Sarawak, CMS is the biggest private sector

player in the largest state in Malaysia.From humble beginnings as a manufacturer

of a single product, CMS' portfolio todayspans construction materials, trading,

construction, road maintenance, propertydevelopment, financial services,

technology and education.

Our VisionTo Be the Pride of Sarawak

Our Mission• Driven by profit• Proactive & synergised in business• On spec & on time• Integrity & respect

Our Stakeholders• Shareholders• Employees• Customers• The Community

TradingCMS Infra Trading is a leading supplierof water treatment chemicals, pipes &fittings, vehicle & equipment spare parts,construction materials, petroleum products& safety equipment for roads.

ConstructionPPES Works (Sarawak) undertakes civilengineering, building & utilities work, roadsconstruction & maintenance, bridges &water-related projects. PPES Works is 51%owned by CMS & 49% owned by Governmentagency, Sarawak Economic DevelopmentCorporation (SEDC).

Road MaintenanceCMS Roads maintains over 4,000 kmof roads throughout Sarawak usingan internationally recognised roadmanagement & maintenance system.

Pavement RehabilitationCMS Pavement Tech is a specialist providerof construction, maintenance & rehabilitationtechnology for road pavements using cementstabilisation, pavement profiling & recyclingof existing pavements.

Property DevelopmentProjek Bandar Samariang, a joint-venturebetween CMS & the Employees ProvidentFund Board (EPF), is owner & developer ofBandar Baru Samariang, a 5,200 acre newriverine township in Kuching. The Isthmus,Kuching, located to the east of Kuching citycentre, is another 240 acre land bank beingdeveloped by CMS.

Technology SolutionsCMS I-Systems developes technologysolutions for the insurance & healthcaresectors. Its flagship product is the awardwinning, InsureConnect. Its current list ofclientele includes companies in Malaysia,the ASEAN region & India.

EducationCMS Education owns & operates Tunku PutraSchool in Kuching which provides kindergarten,primary & secondary level classes for both thenational & international streams.

Unit Trust FundsCMS Trust Management currently manages9 funds catering to the various risk appetitesof investors. Of all, its equity based CMSPremier Fund has been consistently ratedas a top performer for its rates of returns.

Asset ManagementCMS Asset Management provides assetmanagement expertise as well as customisedinvestment solutions. Among its clients is CMSTrust Management, for which it has beeninstrumental in generating the attractivelong term returns for these funds.

Private EquityCMS Opus Private Equity provides analternative financing platform to bridgeinvestors in Peninsular Malaysia withunder capitalised but potentially profitablecompanies connected to Sarawak.

Stock BrokingCMS Capital is the single largest shareholderin financial services holding company, K&NKenanga Holdings Berhad, whose principalsubsidiaries include Kenanga InvestmentBank Berhad.

pg. 004

Cahya Mata Sarawak Berhad

Corporate Information

DirectorsY A M Tan Sri Dato' Seri Syed Anwar Jamalullail

Tuan Haji Mahmud Abu Bekir Taib

YB Dato Sri Sulaiman Abdul Rahman Taib

Y Bhg Dato' Richard Alexander John Curtis

Tuan Syed Ahmad Alwee Alsree

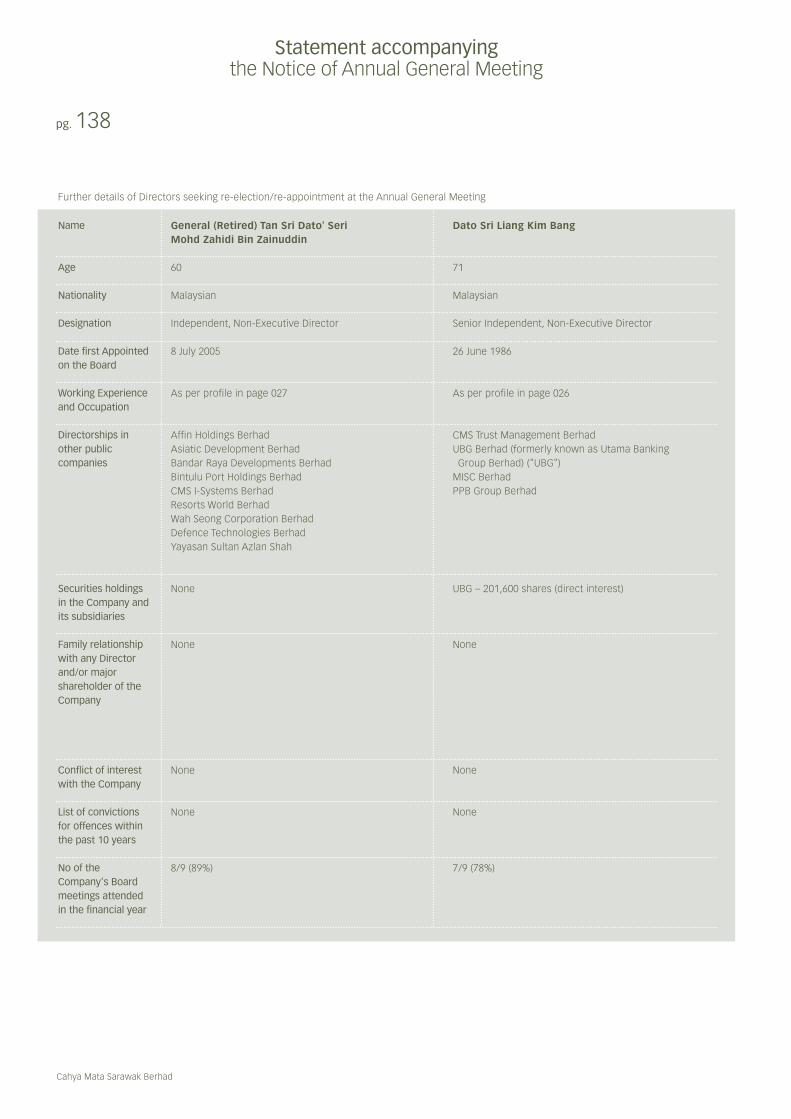

Y Bhg Dato Sri Liang Kim Bang

Y Bhg General (Retired) Tan Sri Dato' SeriMohd Zahidi bin Haji Zainuddin

YB Datuk Haji Talib bin Zulpilip

Y Bhg Datuk Wan Ali Tuanku Yubi

Y Bhg Datu Michael Ting Kuok Ngie@ Ting Kok Ngie

Kevin How Kow

Company SecretaryDenise Koo Swee Pheng

Registered OfficeLevel 6, Wisma MahmudJalan Sungai Sarawak93100 KuchingSarawakMalaysiaT +60 82 238 888F +60 82 333 828

Websitewww.cmsb.com.my

RegistrarSymphony Share Registrars Sdn BhdLevel 26, Menara Multi PurposeCapital SquareNo 8 Jalan Munshi Abdullah50100 Kuala LumpurMalaysiaT +60 3 2721 2222F +60 3 2721 2530

AuditorsErnst & Young

Principal BankersRHB Bank BerhadCIMB Bank BerhadEON Bank BerhadCitibank BerhadBank Muamalat Malaysia BerhadPublic Bank BerhadOCBC Bank (Malaysia) Berhad

Stock Exchange ListingMain Board, Bursa Malaysia Securities BerhadStock code: CMSBStock number: 2852

Cahya Mata Sarawak Berhad

pg. 005

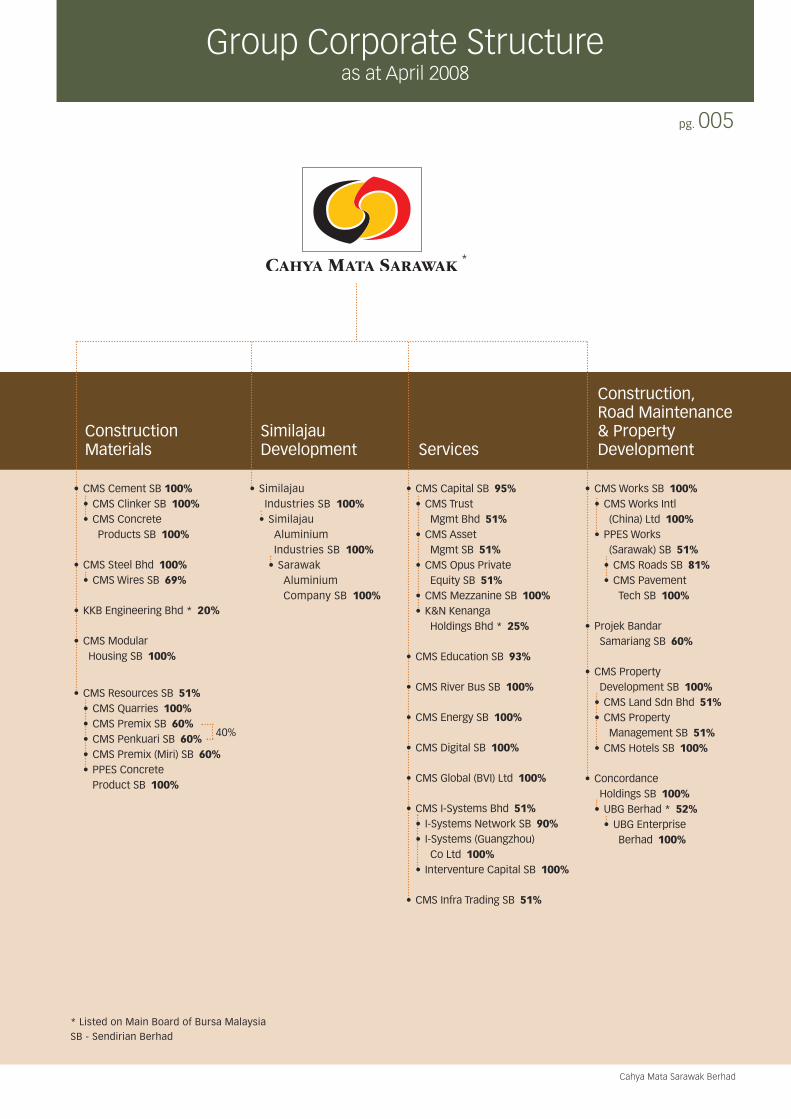

*

* Listed on Main Board of Bursa MalaysiaSB - Sendirian Berhad

ConstructionMaterials

SimilajauDevelopment Services

Construction,Road Maintenance& PropertyDevelopment

Group Corporate Structureas at April 2008

• SimilajauIndustries SB 100%

• SimilajauAluminiumIndustries SB 100%

• SarawakAluminiumCompany SB 100%

• CMS Cement SB 100%• CMS Clinker SB 100%• CMS Concrete

Products SB 100%

• CMS Steel Bhd 100%• CMS Wires SB 69%

• KKB Engineering Bhd * 20%

• CMS ModularHousing SB 100%

• CMS Resources SB 51%• CMS Quarries 100%• CMS Premix SB 60%• CMS Penkuari SB 60%

40%

• CMS Premix (Miri) SB 60%• PPES Concrete

Product SB 100%

• CMS Capital SB 95%• CMS Trust

Mgmt Bhd 51%• CMS Asset

Mgmt SB 51%• CMS Opus Private

Equity SB 51%• CMS Mezzanine SB 100%• K&N Kenanga

Holdings Bhd * 25%

• CMS Education SB 93%

• CMS River Bus SB 100%

• CMS Energy SB 100%

• CMS Digital SB 100%

• CMS Global (BVI) Ltd 100%

• CMS I-Systems Bhd 51%• I-Systems Network SB 90%• I-Systems (Guangzhou)

Co Ltd 100%• Interventure Capital SB 100%

• CMS Infra Trading SB 51%

• CMS Works SB 100%• CMS Works Intl

(China) Ltd 100%• PPES Works

(Sarawak) SB 51%• CMS Roads SB 81%• CMS Pavement

Tech SB 100%

• Projek BandarSamariang SB 60%

• CMS PropertyDevelopment SB 100%

• CMS Land Sdn Bhd 51%• CMS Property

Management SB 51%• CMS Hotels SB 100%

• ConcordanceHoldings SB 100%

• UBG Berhad * 52%• UBG Enterprise

Berhad 100%

pg. 006

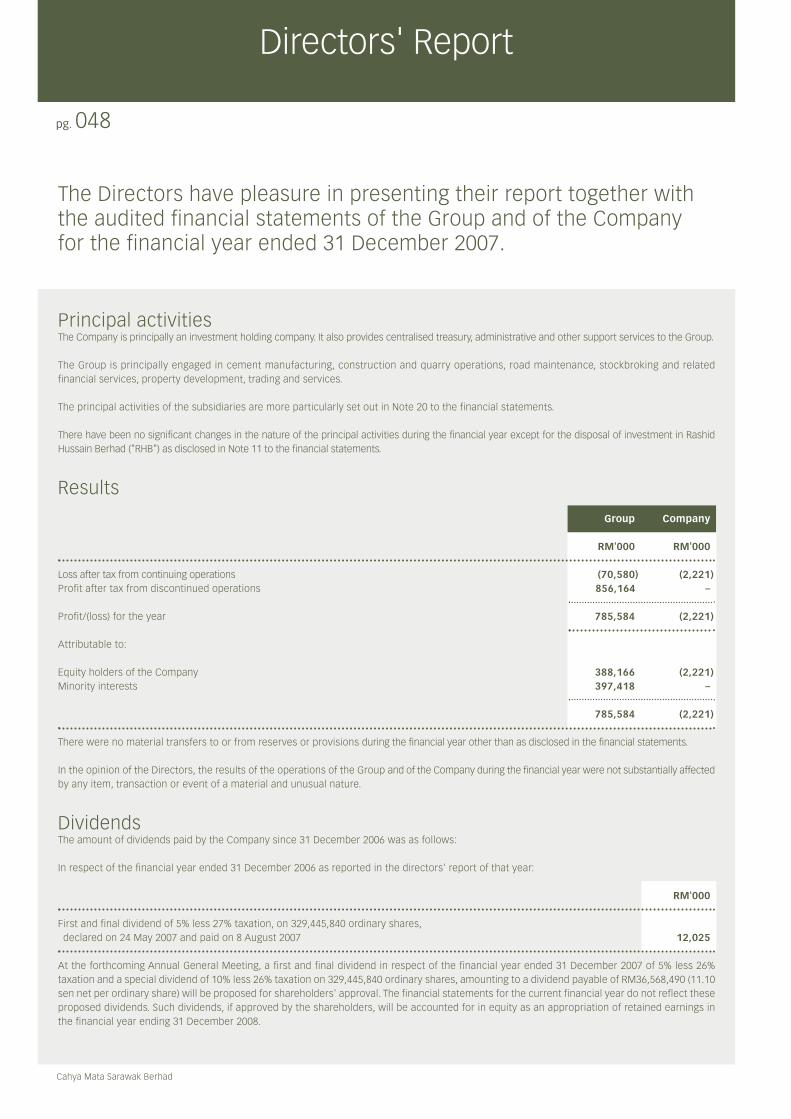

Letter to Shareholdersby Group Chairman

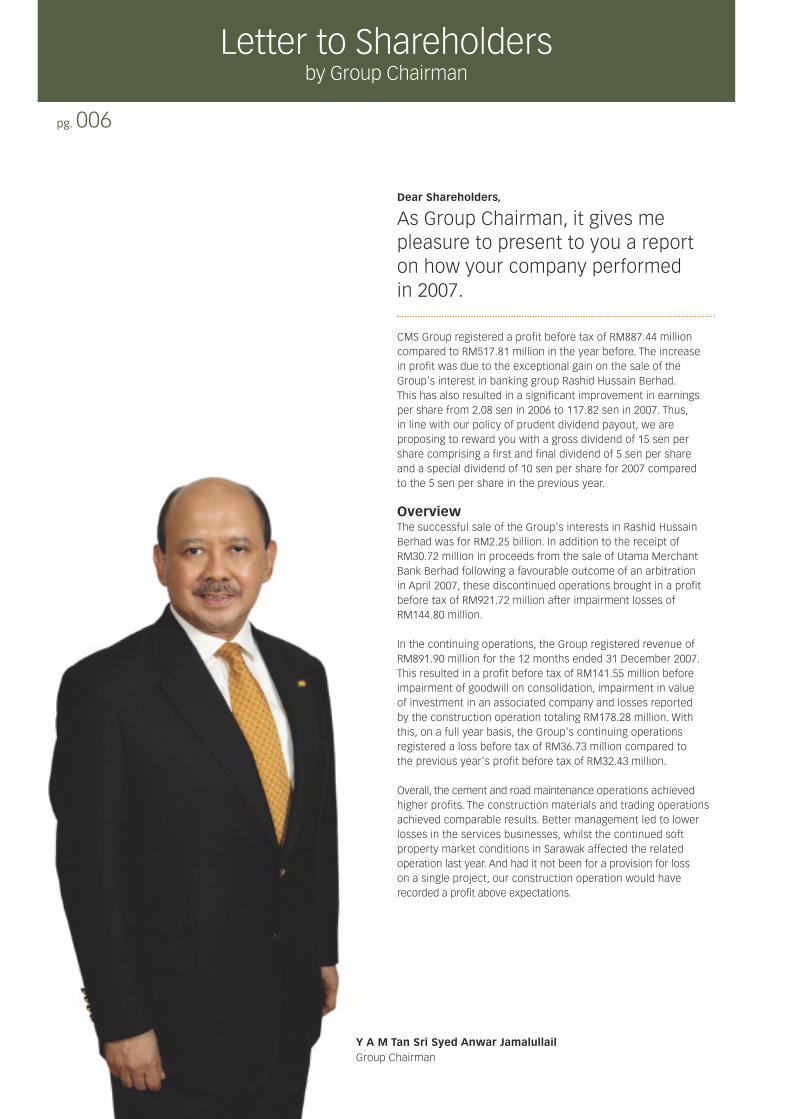

Dear Shareholders,

As Group Chairman, it gives mepleasure to present to you a reporton how your company performedin 2007.

CMS Group registered a profit before tax of RM887.44 millioncompared to RM517.81 million in the year before. The increasein profit was due to the exceptional gain on the sale of theGroup's interest in banking group Rashid Hussain Berhad.This has also resulted in a significant improvement in earningsper share from 2.08 sen in 2006 to 117.82 sen in 2007. Thus,in line with our policy of prudent dividend payout, we areproposing to reward you with a gross dividend of 15 sen pershare comprising a first and final dividend of 5 sen per shareand a special dividend of 10 sen per share for 2007 comparedto the 5 sen per share in the previous year.

OverviewThe successful sale of the Group's interests in Rashid HussainBerhad was for RM2.25 billion. In addition to the receipt ofRM30.72 million in proceeds from the sale of Utama MerchantBank Berhad following a favourable outcome of an arbitrationin April 2007, these discontinued operations brought in a profitbefore tax of RM921.72 million after impairment losses ofRM144.80 million.

In the continuing operations, the Group registered revenue ofRM891.90 million for the 12 months ended 31 December 2007.This resulted in a profit before tax of RM141.55 million beforeimpairment of goodwill on consolidation, impairment in valueof investment in an associated company and losses reportedby the construction operation totaling RM178.28 million. Withthis, on a full year basis, the Group's continuing operationsregistered a loss before tax of RM36.73 million compared tothe previous year's profit before tax of RM32.43 million.

Overall, the cement and road maintenance operations achievedhigher profits. The construction materials and trading operationsachieved comparable results. Better management led to lowerlosses in the services businesses, whilst the continued softproperty market conditions in Sarawak affected the relatedoperation last year. And had it not been for a provision for losson a single project, our construction operation would haverecorded a profit above expectations.

Y A M Tan Sri Syed Anwar JamalullailGroup Chairman

Cahya Mata Sarawak Berhad

pg. 007

Apart from improving the Group's bottom-line, we also enhanced our corporategovernance. It is my firm belief that goodgovernance means good business. Andin 2007, we implemented a number ofnew processes and reporting measuresto better manage our operations forfuture growth.

Outlook & ProspectsThe Malaysian economy grew at 6.3% in2007, the strongest showing since 2004.The growth prospects are expected toremain favourable in 2008 on the back ofcontinued expansion of domestic demand,especially with the implementation ofprojects under the 9th Malaysia Plan.Similar positive expectations apply forSarawak's economy which will benefitfrom the recently launched SarawakCorridor of Renewable Energy (SCORE).There is much potential for CMS to play arole in SCORE, both directly and indirectly.

With the developments happening inSarawak and nationally, we look forwardto an exciting but challenging year aheadespecially with the external uncertainties.All the same, the CMS team is mindful thatthe operating environment continues toremain competitive and ever-changing.We are confident that the prudent andstrong measures taken in the recentpast to align and strengthen our Groupwill position us for sustainable growthin the future.

AppreciationLadies and Gentlemen, the Grouphandled change management well in2007, demonstrating resilience andtenacity to stay the course for success,both in good and bad times. For this, Iwould like to thank all 2,000 plus CMSemployees, members of the Managementteams and Boards, at the Group andsubsidiary levels, for their commitmentand fine efforts. Thank you also for thesupport from various external partiesthat CMS works with – Governmentdepartments, agencies, vendors,suppliers and business partners.

On behalf of the Board, I would also liketo express our appreciation to our Director,YB Dato Sri Sulaiman Abdul Rahman Taib,who has decided not to seek re-election.In total, YB Dato Sri Sulaiman had been onthe Board of CMS for more than 13 years,serving in various capacities including asGroup Chairman. YB Dato Sri Sulaiman isnow a member of the Federal Cabinet,and we wish him every success in hisfuture undertakings.

And last but not least, special thanks goto our shareholders who believe in us andour future. With your continued support,guidance and confidence, let us togethertransform CMS into a respected andpreferred Malaysian company.

Y A M Tan Sri Syed Anwar JamalullailGroup Chairmanon behalf of the Board of Directors7 April 2008

pg. 008

Cahya Mata Sarawak Berhad

Looking Back on 2007

January

23/01 – CMS I-SystemsBerhad inked a deal with prominentIndonesian insurance underwriter, PT.Citra International Underwriters,for the implementation of its GeneralInsurance Management System.

25/01 – Tunku Putra School receivedacademic accolades for its excellentresults in the 2006 IGCSE ʹOʹ levelexaminations. Students achieved 100%pass rate in all papers with outstandingresults in Mathematics and Science.

February

12/02 – CMS Premier Fund wasnamed "Best Equity Malaysia Fund"in the 10-year category for theperiod ended 31 December 2006at The Edge-Lipper Malaysia FundAwards 2007.

14/02 – CMS Trust Managementgarners more wins! CMS PremierFund was announced "Winner of theEquity Malaysia (10 Year) Category"whilst CMS Islamic Fund clinched the"Winner of the Sector – Islamic Syariah(1 Year) Category" award at the Standard& Poor's 2007 Malaysia Fund Awards.

April

04/04 – Utama Banking Group Berhad("UBG") entered into a conditional Sale& Purchase Agreement with EPF forthe disposal of UBG's 32.8% equityin Rashid Hussain Berhad ("RHB") forRM2.25 billion.

25/04 – Projek Bandar Samarianglaunched a new design double-storeyterrace house at Taman Indah, BandarBaru Samariang.

29/04 – CMS Infra Trading kick-startedthe CMS "Doing Good" CSR programmeby taking part in the Open Day sales ofwork of PERKATA (School of IntellectuallyDisabled Children) Sarawak 2007.

May

14/05 – CMS Cement does itsbit for the community by organisingan educational Recycling Campaign,Exhibition & Competition for 200secondary school students at SMKBandar Kuching No. 2. CMS Cementcollected 800 kg of recyclable materialsand raised awareness of recyclingamong students.

16/05 – Utama Banking Group Berhadshareholders voted "Yes" to dispose off itsentire investment in RHB to the EPF andapproved a proposed capital repaymentscheme of RM1.365 billion on the basis ofRM2.00 for every one (1) existing ordinaryshare of RM1.00 each in UBG.

24/05 – Shareholders attended CMS'32nd Annual General Meeting in Kuching.

June

27/06 – Utama Banking GroupBerhad changed its name to UBGBerhad. A new logo was also unveiled.

July

02/07 – CMS employee volunteersraised RM5,065 for the SarawakChildren's Cancer Society at thecharity's Open Day sales of work.

17/07 – The Chief Minister ofSarawak officially declared openTunku Putra School's new campus inPetra Jaya, Kuching. The purpose-builtcampus showcases the best in holistic,learning-centred infrastructure withchild-safety building designs andarchitecture. Facilities include singlestorey classrooms, science labs, alibrary, dedicated rooms and workshopsfor computer, music, art and drama, aswell as playgrounds and a multipurposerecreational hall.

Cahya Mata Sarawak Berhad

pg. 009

27/07 – Projek Bandar Samariangsigned a block sale agreement withKoperasi Perumahan Angkatan TenteraBhd to develop 1,000 units of singlestorey terrace houses at Bandar BaruSamariang.

30/07 – CMS and KKB EngineeringBhd ("KKB") signed a Memorandum ofUnderstanding to negotiate the sale ofCMS Steel's land and plant. The deal alsopaves the way for a strategic alliance forsteel fabrication activities in the oil & gas,shipping and marine sectors.

August

06/08 – Bandar Baru Samariangmay soon add a Chinese primaryschool to its township facilities. Anagreement for the land sale was signedbetween Projek Bandar Samariang andthe Chung Hua Primary SchoolsManagement Committee.

07/08 – CMS signed a Heads ofAgreement with leading aluminiumproducer, Rio Tinto Alcan, to beginstudies for the proposed developmentof a world-class aluminium smelter inSimilajau, Sarawak. The 550,000 metrictonnes per annum smelter will beoperated by the Sarawak AluminiumCompany ("SALCO").

18/08 – Over 200 CMS "Doing Good"employee volunteers from PPES Works,CMS Roads and CMS Pavement Techspent their Saturday to do a masscommunity clean-Up at Kampung SinarBaru, an ex-leprosy resettlement villagelocated 14 km from Kuching city.

30/08 – CMS Trust announced aninterim net income distribution of 3.5 senfor the CMS Premier Fund and CMSIslamic Fund following the fundsʹ strongfinancial performance in 2006 and 2007.

September

03/09 – CMS Cement announcedplans to acquire Sarawak Clinker, thesole clinker producer in East Malaysia,from Mirzan Mahathir and MaybachInvestment Co.

08/09 – Tunku Putra School's"Celebration of Learning" Open Dayreceived 1,500 visitors at the School'snew campus in Petra Jaya and raisedRM30,000 through food fair sales andraffle proceeds. Part of this wasdonated to charity.

16/09 – The symbolic crowningof the new Dewan Undangan NegeriSarawak building under constructionby a consortium including PPES Works,took place in a topping-up ceremonygraced by the Chief Minister of Sarawak.

17/09 – The SALCO smeltercommenced its Detailed EnvironmentalImpact Assessment ("DEIA") study. TheDEIA will take 18 months and will includeair quality, noise, flora and fauna, landuse and social impact studies along withwaste management, transport, surfacewater and groundwater impact.

24/09 – The SALCO smelter began itsprogramme of community engagementwith a dialogue in Bintulu attended by across-section of the local community –associations and the business community,local community heads and governmentdepartments.

October

09/10 – The SALCO smelter projectgained further momentum with theallocation of a parcel of State-ownedland by the Sarawak Government atSimilajau. SALCO also announced theappointment of prominent internationalengineering consultant, Bechtel, toundertake an engineering study forthe smelter.

30/10 – CMS I-Systems announcedthat it had penetrated the India marketby securing the supply of its flagshipproduct, InsureConnect, to its firstmajor customer in India, insurer FutureGenerali. Weeks later, the companyannounced its second Indian client, theReliance group. CMS I–Systems alsomade headway into the Islamic Takafulinsurance sector by securing a contractwith Hong Leong Tokio Marine Berhadin Malaysia.

November

07/11 – CMS and KKB sealedits future growth and new businessopportunities in ship-building andsteel fabrication in the region's oil & gassector by finalising the Sale & PurchaseAgreement. Under the Agreement, KKBwill acquire CMS Steel's 17.6 acre land,in exchange for 16 million new ordinaryshares in KKB valued at RM32 million.

14/11 – CMS Trust brought 3 newfunds to the market – the CMS MalaysianInc Fund, the CMS Money Market Fundand the CMS Islamic Money Market Fund.The new funds expanded the company'sproduct suite to nine funds, and totalfund capacity from 3 billion units to 3.8billion units overall – a potential increaseof RM400 million worth of new assets.

16/11 – For the fourth consecutiveyear, Tunku Putra School achieved 100%pass rate amongst its students who satfor the Ujian Penilaian Sekolah Rendah(UPSR) examinations in September.

30/11 – CMS Cement became theowner of East Malaysia's sole clinkerproducer, Sarawak Clinker Sdn Bhd.The acquisition was valued at RM131.7million. The company's name wassubsequently changed to CMS ClinkerSdn Bhd in January 2008.

December

03/12 – 07/12 – CMS held itsannual staff town-hall meetings andannual dinners through a nationwideseries of "Group Managing Director'sAddress" sessions in Kuching, Sibu,Bintulu, Miri and Kuala Lumpur.

15/12 – CMS employee volunteersassisted Habitat for Humanity tocomplete construction of two homesfor impoverished families in Desa Wiraand Mambong, Kuching.

pg. 010

Cahya Mata Sarawak Berhad

Looking Back on 2007

pg. 011

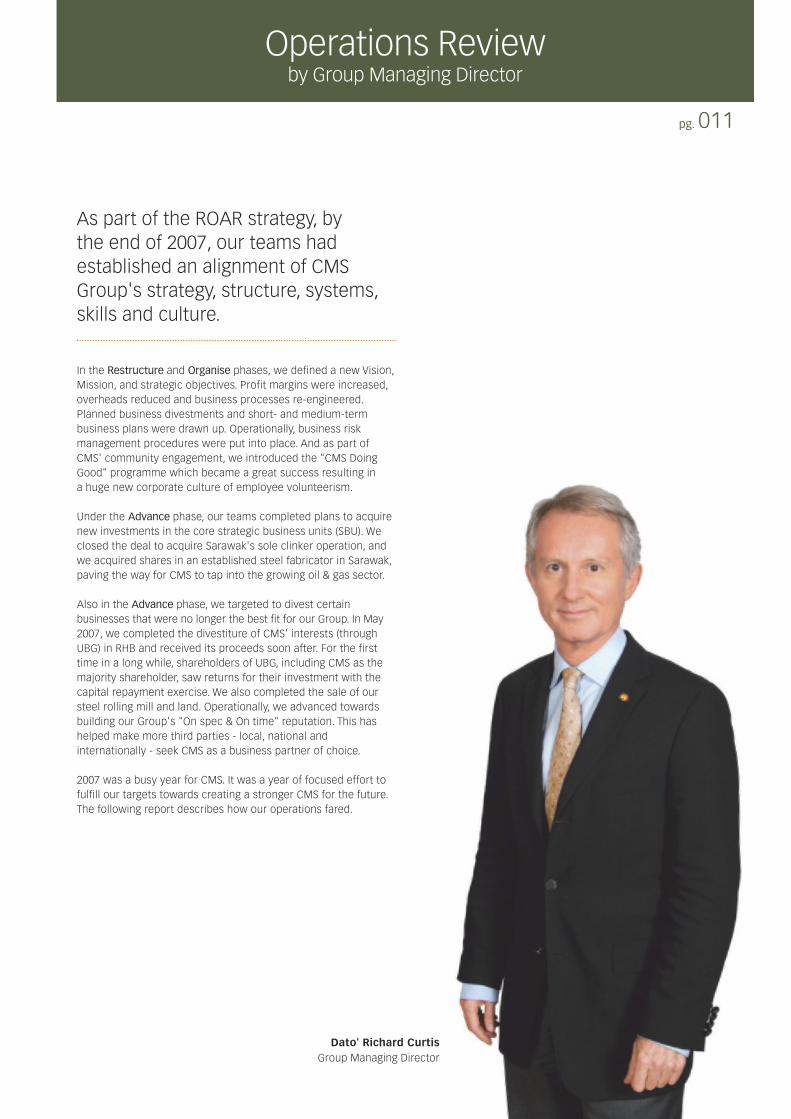

As part of the ROAR strategy, bythe end of 2007, our teams hadestablished an alignment of CMSGroup's strategy, structure, systems,skills and culture.

In the Restructure and Organise phases, we defined a new Vision,Mission, and strategic objectives. Profit margins were increased,overheads reduced and business processes re-engineered.Planned business divestments and short- and medium-termbusiness plans were drawn up. Operationally, business riskmanagement procedures were put into place. And as part ofCMS' community engagement, we introduced the "CMS DoingGood" programme which became a great success resulting ina huge new corporate culture of employee volunteerism.

Under the Advance phase, our teams completed plans to acquirenew investments in the core strategic business units (SBU). Weclosed the deal to acquire Sarawak's sole clinker operation, andwe acquired shares in an established steel fabricator in Sarawak,paving the way for CMS to tap into the growing oil & gas sector.

Also in the Advance phase, we targeted to divest certainbusinesses that were no longer the best fit for our Group. In May2007, we completed the divestiture of CMS' interests (throughUBG) in RHB and received its proceeds soon after. For the firsttime in a long while, shareholders of UBG, including CMS as themajority shareholder, saw returns for their investment with thecapital repayment exercise. We also completed the sale of oursteel rolling mill and land. Operationally, we advanced towardsbuilding our Group's "On spec & On time" reputation. This hashelped make more third parties - local, national andinternationally - seek CMS as a business partner of choice.

2007 was a busy year for CMS. It was a year of focused effort tofulfill our targets towards creating a stronger CMS for the future.The following report describes how our operations fared.

Operations Reviewby Group Managing Director

Dato' Richard CurtisGroup Managing Director

Cement

CMS Cement Sdn Bhd continued tobe the highest profit contributor in theGroup and in 2007, generated a 22%increase in profit before tax to RM72.5million. The performance reflected anationwide upward revision in the priceof cement in January 2007 by the Ministryof Domestic Trade and Consumer Affairs.CMS Cement's performance was alsoboosted by successful cost-reductionmeasures, improved efficiency inlogistics, and a favourable exchangerate that reduced the cost of importedraw materials.

The big news for our cement operationis that we have finally secured thelong-term supply of its main raw material,clinker. Managing the supply of qualityclinker is crucial. In November 2007,CMS Cement became the new owner ofEast Malaysia's sole clinker manufacturer,CMS Clinker Sdn Bhd (formerly known asSarawak Clinker Sdn Bhd). The strategic

acquisition will enable CMS Clinker'scurrent production capacity, which at800,000 metric tonnes (MT) per annumis still short of the demand from CMSCement, to be expanded.

CMS Concrete Products Sdn Bhdspecialises in pre-formed concreteproducts such as RC square piles,bridge beams, culverts, kerbs andcement sand bricks. The companyreported a lower profit before taxin 2007 despite higher sales volumeand revenue as sales were mainlyfor products with lower profit margins.

pg. 012

Cahya Mata Sarawak Berhad

Operations Reviewby Group Managing Director

Cement –22% Increasein ProfitBefore Tax

Cahya Mata Sarawak Berhad

pg. 013

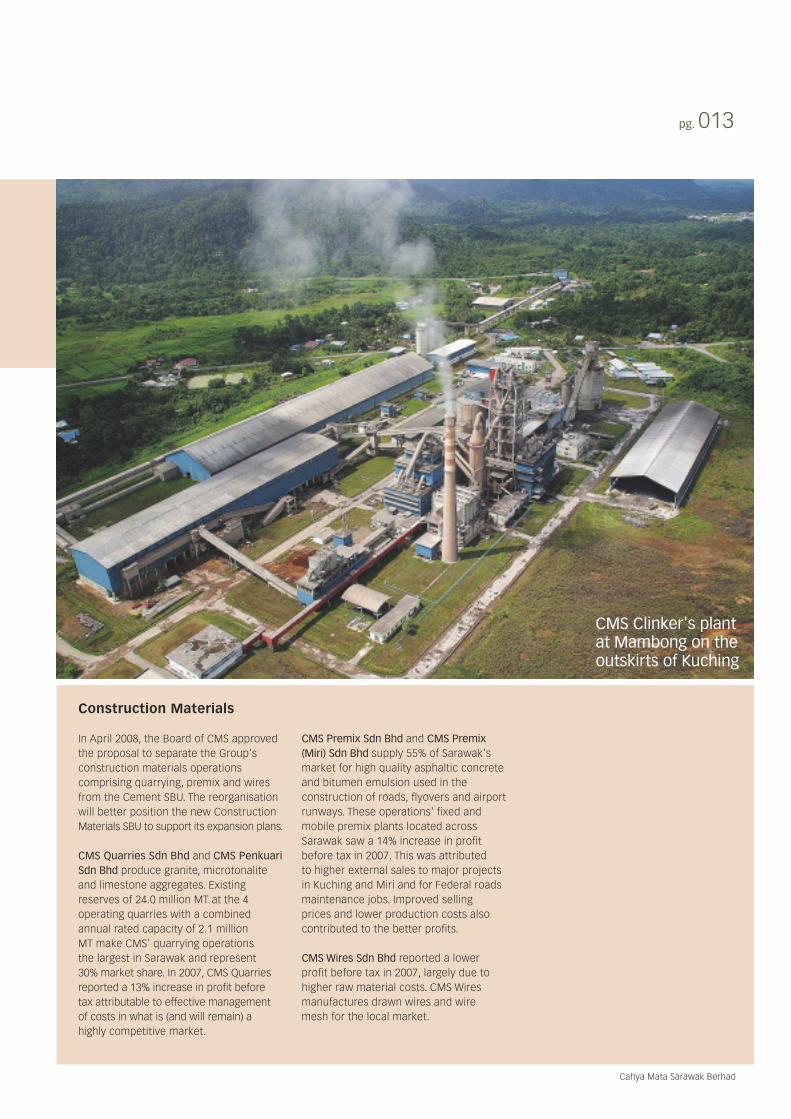

Construction Materials

In April 2008, the Board of CMS approvedthe proposal to separate the Group'sconstruction materials operationscomprising quarrying, premix and wiresfrom the Cement SBU. The reorganisationwill better position the new ConstructionMaterials SBU to support its expansion plans.

CMS Quarries Sdn Bhd and CMS PenkuariSdn Bhd produce granite, microtonaliteand limestone aggregates. Existingreserves of 24.0 million MT at the 4operating quarries with a combinedannual rated capacity of 2.1 millionMT make CMS' quarrying operationsthe largest in Sarawak and represent30% market share. In 2007, CMS Quarriesreported a 13% increase in profit beforetax attributable to effective managementof costs in what is (and will remain) ahighly competitive market.

CMS Premix Sdn Bhd and CMS Premix(Miri) Sdn Bhd supply 55% of Sarawak'smarket for high quality asphaltic concreteand bitumen emulsion used in theconstruction of roads, flyovers and airportrunways. These operations' fixed andmobile premix plants located acrossSarawak saw a 14% increase in profitbefore tax in 2007. This was attributedto higher external sales to major projectsin Kuching and Miri and for Federal roadsmaintenance jobs. Improved sellingprices and lower production costs alsocontributed to the better profits.

CMS Wires Sdn Bhd reported a lowerprofit before tax in 2007, largely due tohigher raw material costs. CMS Wiresmanufactures drawn wires and wiremesh for the local market.

CMS Clinker's plantat Mambong on theoutskirts of Kuching

pg. 014

Cahya Mata Sarawak Berhad

Operations Reviewby Group Managing Director

Similajau Development

The newest addition to the Group isa focus on potential developments atSimilajau, an area located 60 km northof Bintulu town in central Sarawak. Aspart of the Sarawak Corridor of RenewableEnergy (SCORE), there are many excitingplans for the Similajau area. SCOREcovers an area of 70,709 sq km fromTanjung Manis up to Similajau. It is acomprehensive masterplan to bringgreater development to Sarawak bythe year 2030 based on the area's largereserves of coal, oil & gas, and potentialto generate hydro power energy.Investments totaling RM334 billionare expected to pour into SCORE, bothfrom the Government and private sector,including foreign direct investments.

A major initiative by CMS is thedevelopment of an aluminium smelterat Similajau. A joint-venture betweenCMS and leading aluminium producer,Rio Tinto Alcan, will operate SarawakAluminium Company Sdn Bhd (SALCO).

Its production capacity will be a minimum550,000 MT per annum in its initial phase,with further capability to be expanded to1.5 million MT per annum. Estimated tocost over RM7 billion, the SALCO smelterwill be a major economic driver forSarawak and Malaysia. Based on currentrates, it will have the potential to generateover RM2 billion per year in sales revenuefor the local economy, and provide 1,500direct and 5,700 indirect jobs. It will alsoattract other downstream industries aswell as convert Malaysia from analuminium importer into a significantexporter of this industrially importantraw material.

A Heads of Agreement between CMSand Rio Tinto Alcan was signed in August2007. This marked the start of the project'sfeasibility studies as well as a detailedenvironmental impact assessment. Aparcel of land has also been allocatedby the State Government for the proposedaluminium smelter.

With its various businesses, CMS iswell-positioned to participate directlyand indirectly in other plans for theSimilajau area. These include supplyof cement and other constructionmaterials, development of a deep-seaport, housing and infrastructure at thenew township and industrial precinct,as well as in synergistic manufacturingand services.

1,500 Direct Jobs5,700 Indirect Jobs

Cahya Mata Sarawak Berhad

pg. 015

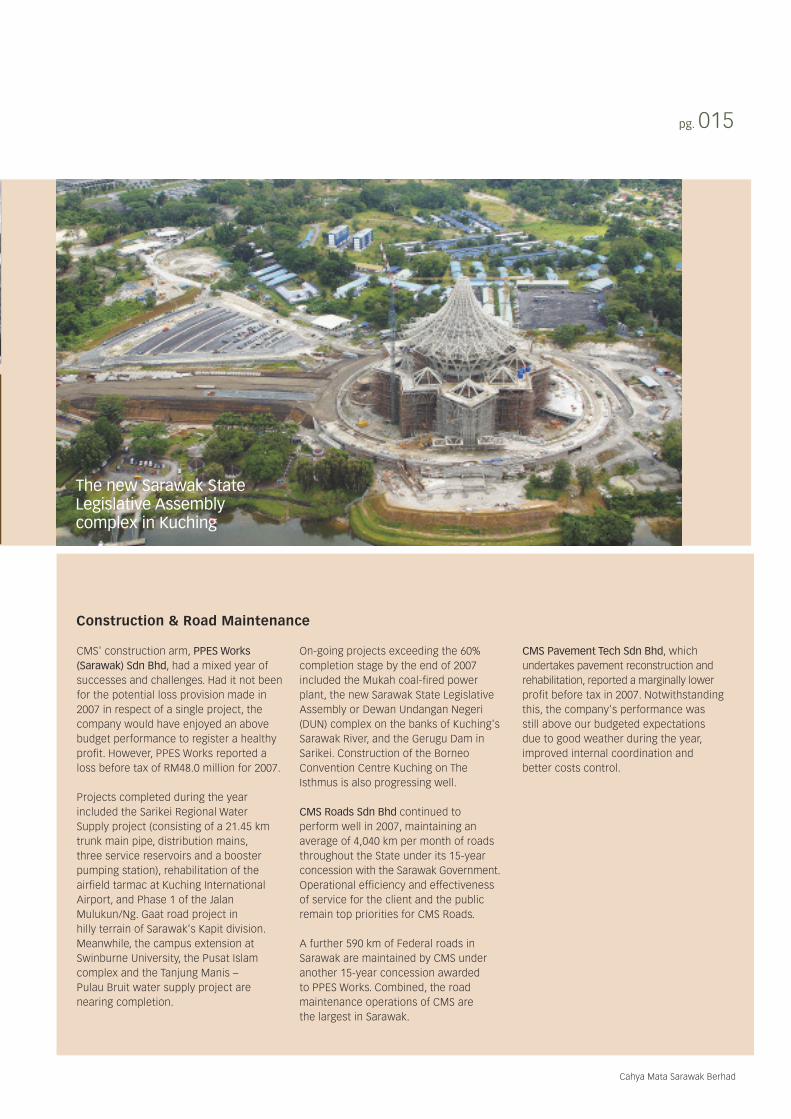

Construction & Road Maintenance

CMS' construction arm, PPES Works(Sarawak) Sdn Bhd, had a mixed year ofsuccesses and challenges. Had it not beenfor the potential loss provision made in2007 in respect of a single project, thecompany would have enjoyed an abovebudget performance to register a healthyprofit. However, PPES Works reported aloss before tax of RM48.0 million for 2007.

Projects completed during the yearincluded the Sarikei Regional WaterSupply project (consisting of a 21.45 kmtrunk main pipe, distribution mains,three service reservoirs and a boosterpumping station), rehabilitation of theairfield tarmac at Kuching InternationalAirport, and Phase 1 of the JalanMulukun/Ng. Gaat road project inhilly terrain of Sarawak's Kapit division.Meanwhile, the campus extension atSwinburne University, the Pusat Islamcomplex and the Tanjung Manis –Pulau Bruit water supply project arenearing completion.

On-going projects exceeding the 60%completion stage by the end of 2007included the Mukah coal-fired powerplant, the new Sarawak State LegislativeAssembly or Dewan Undangan Negeri(DUN) complex on the banks of Kuching'sSarawak River, and the Gerugu Dam inSarikei. Construction of the BorneoConvention Centre Kuching on TheIsthmus is also progressing well.

CMS Roads Sdn Bhd continued toperform well in 2007, maintaining anaverage of 4,040 km per month of roadsthroughout the State under its 15-yearconcession with the Sarawak Government.Operational efficiency and effectivenessof service for the client and the publicremain top priorities for CMS Roads.

A further 590 km of Federal roads inSarawak are maintained by CMS underanother 15-year concession awardedto PPES Works. Combined, the roadmaintenance operations of CMS arethe largest in Sarawak.

CMS Pavement Tech Sdn Bhd, whichundertakes pavement reconstruction andrehabilitation, reported a marginally lowerprofit before tax in 2007. Notwithstandingthis, the company's performance wasstill above our budgeted expectationsdue to good weather during the year,improved internal coordination andbetter costs control.

The new Sarawak StateLegislative Assemblycomplex in Kuching

pg. 016

Cahya Mata Sarawak Berhad

Operations Reviewby Group Managing Director

Property Development

CMS Group owns a large land bank; thebiggest being 5,200 acres located northof Kuching city. The area is today the siteof a new riverine township developmentcalled Bandar Baru Samariang ("BBS")managed by Projek Bandar SamariangSdn Bhd, a joint-venture between CMSand the Employees' Provident Fund Board.

Sarawak experienced continued softproperty market conditions in 2007. Giventhis scenario, our property team adjustedits strategy to focus on securing sales ofcompleted properties at BBS and delayingnew launches until the market picks up.Heightened marketing efforts throughoutthe year resulted in a 171% increase intotal sales in 2007 compared to theprevious year, reducing the stock ofbuilt homes by 62%.

In August, we signed an Agreementto develop 1,000 single-storey terracehouses in BBS for Koperasi PerumahanAngkatan Tentera. Also in the same month,we signed a Sale & Purchase Agreementwith the Committee of Management ofChung Hua Primary Schools to develop aChinese-medium school at BBS. Thisschool will be one of only a few Chinese-medium schools in the Kuching Northarea which is predominantly populatedby Malay and Bumiputera communities.

Exciting developments are taking placeat The Isthmus, CMS' 240-acre landbank to the east of Kuching city centre.Construction of the 5,000 delegatecapacity Borneo Convention CentreKuching and a multi-storey hotel madeprogress in 2007. Both are part of thecomprehensive masterplan beingdeveloped with the Government tocreate a new city within Kuching city.

UBG Berhad

UBG Berhad (formerly known as UtamaBanking Group Berhad) is evolving.From being a financial services group,UBG is presently undergoing a majortransformation after divestment of itsshareholding in RHB. A subsequent namechange and new logo were unveiled inJune 2007. After much deliberation by itsBoard, the decision has been made, aspart of a series of moves to acquire newcore businesses, to buy into successfulniche construction companies. Thisdecision would transform UBG into acompany with strategic exposure in2 growth sectors – construction andproperty development, as well aswater infrastructure.

In February 2008, UBG announced itsproposed acquisition of controllinginterests in water infrastructure specialistLoh & Loh Corporation Berhad and nicheconstruction specialist Putrajaya PerdanaBerhad, which it hopes to finalise by thethird quarter of 2008. Managed by a teamof industry experts, the prospective newinvestments hold promise for UBG to steerthese companies towards new businessesand opportunities, both local and

Sale of RHBBrings in

Net Gain ofRM1.23 Billion

Cahya Mata Sarawak Berhad

pg. 017

international. A direct investment intoUBG by Middle-Eastern consortium, theAbu Dhabi-Kuwait-Malaysia InvestmentCorp, has the potential to open doors forconstruction and infrastructure jobs inthe Middle East. UBG will strengthen itsinfrastructure capabilities by finalisingthe acquisition of CMS Roads Sdn Bhdand CMS Pavement Tech Sdn Bhd duringthis year.

UBG boosted CMS Group's overall financialposition in 2007 with the successful sale ofits interest in RHB for RM2.25 billion. Thisresulted in a net gain of RM1.23 billion. Thefavourable outcome of an arbitration casealso brought in proceeds of RM30.72million. Combined, these discontinuedoperations brought in a profit before tax ofRM921.72 million to CMS for the full yearof 2007. CMS received RM707 million inproceeds from the capital reductionexercise at UBG in October 2007.

Services

CMS Trust Management Berhad recorded a12% increase in funds under managementin 2007. Sales were up 58% following moreaggressive marketing efforts. Revenuefrom management and service fees werealso higher. Having re-branded itself withthe "CMS Trust – Wealth Intelligence"tagline, the company launched three fundsin 2007, bringing its total funds to nine.CMS Trust continued to demonstrate itsobjective to provide investors with long-term returns when its CMS Premier Fundwas named "Best Equity Malaysia Fund" inthe 10-year category of 2007 by The Edge-Lipper. This was the second consecutivewin in this category for CMS Premier Fund.

CMS Asset Management Sdn Bhd saw totalassets under management (AUM) grow50% from RM1.4 billion in 2006 to RM2.1billion in 2007 following the launch ofthree new funds and fresh capital injectionfrom existing and new clients. CMS AssetManagement is the fund manager of CMSTrust Management's funds.

Going forward, we are looking to mergethe operations of CMS Trust Managementand CMS Asset Management. Apart fromgreater efficiency, the merged entity willunlock value to enable it to ventureinto wider markets and new products.Announcements on these developmentswill be made in due course.

The Group's technology solutionsoperation, CMS I-Systems Berhad,achieved a profit turnaround in 2007and expanded its reach to new markets.As a developer of solutions for the healthand insurance sectors, CMS I-Systemsdid the seemingly impossible by makinginroads into the domestic Indian softwaremarket. During the year, the companysecured contracts to supply technologysolutions to 2 major insurance companiesin India, namely Future Generali and theReliance groups. It further went on tosecure a deal to customise its award-winning flagship product, InsureConnect,to the Syariah-based Takaful insurancesector in Malaysia.

3 NewFundsLaunched

pg. 018

Cahya Mata Sarawak Berhad

CMS Opus Private Equity Sdn Bhd ("COPE")recorded a three-fold increase in profitbefore tax in 2007 against budget. Thisfavourable variance was attributed to acautious approach towards operatingexpenditure. During the year, COPEsuccessfully closed a deal with a localoil and chemical tankers' operator. Thecompany owns and operates off-shorevessels serving the oil & gas industryregionally, as well as provides technicalmanagement and marine consultancyservices. With another deal being finalisedin 2008, COPE expects to maintain itsfocus to capitalise on the booming oil& gas industry.

CMS Infra Trading Sdn Bhd registereda marginally lower profit before tax in2007 due to its products mix. In termsof revenue, higher sales of water-treatment chemicals, DI pipes and fittings,cement and steel bars were off-set bylower sales from HDPE and steel pipes.

CMS' associate company, K&N KenangaHoldings Berhad, a financial servicesholding company, recorded an improvementof 197% over the previous year's profitbefore tax, resulting in RM35.1 millioncontribution back to CMS Group. The maincontributor to K&N's revenue was fromgross brokerage fees of its subsidiary,Kenanga Investment Bank Berhad, whichrose from RM109.7 million to RM242.7million in the last financial year.

Of favorable mention is the performanceof subsidiary Kenanga Deutsche Futureswhich maintained its position as theleading futures broker in Malaysia.In 2007, it won the "Top Overall FuturesBroker" award by Bursa MalaysiaDerivatives Berhad for the fifthconsecutive year as well as the "TopEquities Futures Broker" recognition.

K&N Kenanga Holdings Berhad has nowventured into investment opportunitiesin the Middle East and the Asian region,having developed joint-ventures in theKingdom of Saudi Arabia, Dubai, Sri Lankaand Vietnam. These are for securities andinvestment banking-related activities.Strategic alliances are also being formedin South Korea and Indonesia. Theseefforts are expected to contribute to theearnings of K&N in the coming years.

CMS Capital Sdn Bhd reported a lossbefore tax of RM66.9 million in 2007mainly due to recognition of animpairment loss of RM67 million in thevalue of investment of our associatecompany, K&N Kenanga Holdings Berhad.

2007 was an excellent year for TunkuPutra School. It moved to a new, largerand better equipped, purpose-builtcampus in Petra Jaya, Kuching. Studentenrolment continues to rise by leaps andbounds. It added the Cambridge 'A' Levelsto its list of curriculum offerings. In termsof teaching faculty, the School now boastsa larger and more impressive team led bya highly experienced Principal and DeputyPrincipal. These factors have contributedto the excellent results by its studentsin both national and internationalexaminations. Such positive showingsare indeed rewarding for CMS whichcontinues to support the School'soperation financially.

Operations Reviewby Group Managing Director

Cahya Mata Sarawak Berhad

pg. 019

Dato' Richard CurtisGroup Managing Director7 April 2008

Our efforts in 2008 will be focusedon completing the final phase of ourROAR strategy which is the Roar Aheadphase. We will do this by firing up our4 business groupings known as'Engines of Growth' with theiridentified business boosters.

To translate our 'Engines of Growth' strategies into sustainablerevenue and profits growth, our Management and employees needto complete the mindset change that the ROAR strategy is bringingabout within CMS and its stakeholders.

We all need to be in a mindset that understands we share a commonpurpose in our Vision, Mission and strategies. This mindset mustwillingly embrace change and challenges, whether due to externalfactors or otherwise, seeing these as opportunities and not threats.Within this mindset, we need to stay on course with our commonpurpose and seek to realise it due to focus, hard work and passion.

I am confident that we are now moving conclusively towards seeing our'Engines of Growth' fired up for progress in future years.

pg. 020

Cahya Mata Sarawak Berhad

Management Viewpoints

"We are transforming from apredominately Malaysia-basedcompany to one that is forward-looking and getting a presencein the Gulf Corporation Council(GCC) countries. The injection of ahigh-powered management teamand the emergence of new majorshareholders and institutionalinvestors are critical elements for

the sustainable long-term economicdevelopment of UBG. It is ourintention to build this pool ofprofessionals to take UBG to evengreater heights of achievementsand excellence."

Tuan Syed Ahmad Alwee AlsreeDeputy Group Managing Director/UBG Berhad Deputy Chairman

"The acquisition of CMS Clinkerenables CMS Cement to controlthe OPC production cost andreliability of consistent qualitysupply. 95% of raw materials usedfor the production of OPC is clinker.This is produced by CMS Clinkerwhich sources all raw materialslocally. We now directly control

our own production costs, reliabilityand eventually our destiny".

On the new strategic business focus for CMS in thearea of Similajau, north of Bintulu in Sarawak:

On the evolution of UBG from a financial services group to onewith a focus on construction, engineering and infrastructure:

On the significance of the clinker business as a powerbooster for the Construction Materials 'Engine of Growth':

Tuan Haji Othman Abdul RaniHead, Cement SBU/Executive Director, CMS Cement Sdn Bhd

"The development of Similajauis a big dream and it comeswith daunting challenges. Itis a green field site without anysupporting infrastructure andthe investment required for itsmaiden project, the aluminiumsmelter project, is the biggestsingle investment for the CMS

Group. However, it is a necessarystrategic step that the Group hasto take to secure the sustainablilityof its business for the long term."

Isaac LugunHead, Similajau Development SBU/Chief Executive Officer, Similajau IndustriesSdn Bhd

Cahya Mata Sarawak Berhad

pg. 021

Human Capital

• We completed the formation of theStrategic Human Resource Unit tobetter serve the whole Group.

• The first full-year implementationof the Key Performance Indicators(KPI) for management-level employeeswas a success.

• Succession planning and specifictraining plans for key managementpositions was implemented.

• Human capital development effortsto retain talents through careerplanning and effective supervisorymanagement skills training wereconducted in-house for non-executives,executives and managers.

• Training and development programmeswere implemented for all levels ofemployees.

• A greater focus on internalcommunications has supportedthe new energy across CMS today.Activities of 2007 included:

– The newly introduced "Koffee Talk"sessions where executive and non-executive employees have aninformal breakfast with the GroupManaging Director and DeputyGroup Managing Director.

– The annual Group ManagingDirectors' Address sessions wereheld in Kuching, Sibu, Bintulu, Miri,and Kuala Lumpur. Previously, thiscommunications session was onlyheld in Kuching.

– Improvement of content on CMS'Intranet.

– Publication of the quarterly in-housenewsletter called OurCMS.

– The organisation of in-house sportsactivities and gatherings such asannual dinners.

– Management strategic 'away-day'sessions.

– Leadership surveys were conductedtwice in 2007 to gather feedbackon Management's leadership skillsand style.

• Reviewing remuneration to ensure thatno employee is paid below the PovertyLine, in line with the Government'sefforts to eradicate poverty

• We showed we care for our employees– over and above the standard practices,CMS has included two insurance coverageschemes for employees, the provisionof festive cash gifts for every employee,and the setting-up of a dedicatedCompassionate Fund for special needs.

• Acknowledging the long service ofemployees via our Long Service Awardsfor dedicated employees serving theGroup and/or its subsidiaries for 10years and more. The quantum of rewardfor long service was increasedmarkedly in 2007.

It was a busy year for our Group's Human Resources team towards strategicallymanaging human capital development. Among the key activities of 2007 were:

Communicating the ROAR Strategy One-on-One

"It is very important to be there for our employees – to listen to them, to understand their work, to heartheir difficulties, and to support their successes. Improving communication with our employees is especiallyimportant when implementing change or selling new ideas. We have to earn their buy-in, and that begins withrespect. The new breakfast sessions called "Koffee Talk" and the annual Group Managing Director's Addresssessions were very useful for the top management of CMS to listen to the messages and feelings directly fromthe ground, with no barriers of supervisors and managers in between."

Tuan Syed Ahmad Alwee AlsreeDeputy Group Managing Director/Group General Manager – Human Resources

pg. 022

Cahya Mata Sarawak Berhad

CMS Doing Good

Doing good forthe communityThe Rise of EmployeeVolunteerism in CMSCelebrating outstanding success in 2007is CMS' new, purpose-driven EmployeeVolunteerism programme. In its inauguralyear, CMS "Doing Good" communityoutreach programmes tracked over 7,719man-hours of voluntary good deeds fordisadvantaged communities and individuals,children, the disabled and the environment.The top three activities were RebuildingCommunities (28%), Education Projects(25%) and Sustaining Charities (18%). Theresulting man-hours recorded in 2007 was3½ times the original targeted man-hoursfor the whole year.

Employees contributed their own sparetime, not company time, to help othersin the community around which CMSoperates – a reflection of the strongsense of social responsibility and highEmployee Volunteerism culture amongour 2,100 employees.

Major Employee VolunteerismActivities in 2007Building homes for hardcore poor– in and around Kuching.

Supporting children's education –Through providing English tuition to theSalvation Army's primary school-agedchildren, organising the "Back To School"donation drive for children from KampungSinar Baru, an ex-leprosy resettlementvillage, giving furniture to rural tuitioncentres, and contributing books andbook shelves to a library/learning centerestablished by a CMS employee in a poorvillage in Kuching.

Sustaining charities – Over 100employees teamed up during 2007 toset up stalls at annual charity fund-raisersof PERKATA School for Special Children,Sarawak Children's Cancer Society, ChungHua Primary School No. 6, and SarawakCheshire Home.

Bringing joy to the children – throughcollection of cash and kind.

Community clean-up – 'Gotong-royong'and minor construction jobs were carriedout by CMS employee volunteers benefitingdisadvantaged schools, villages andlonghouses. Employees from CMS Cementalso organised a recycling campaign at aschool in Kuching and collected 800 kgof recyclable materials in the process.

Aiding rural communities – Employeevolunteers raised cash and kind for firevictims, and conducted regular visits,community clean-ups, donation drivesand motivational talks at Kampung Sinar Baru.

Blood donation drives – The localblood bank benefited from the generousityof employees of CMS Cement and theConstruction & Road Maintenance SBU.

Caring CorporatePromoting Road Safety – PPES Worksjoined the State Public Works Department(JKR) to promote road safety around theclock in a 14-day Hari Raya Aidilfitri RoadSafety Campaign in October 2007.

CMS Adopt-A-Mosque Programme– Into its fifth year, CMS continued tocontribute towards the utility expenses for66 mosques and surau throughout Sarawak.

Helping future careers – In 2007,CMS' Internship Programme benefited52 students from local universities andpolytechnics.

For CMS, Corporate Social Responsibility (CSR) is simply about 'Doing Good'for our stakeholders – be they our shareholders, employees, customers orthe community around us. The year 2007 saw the Group continue to enrichits CSR practices. These efforts included:

Supporting children's education

Bringing joy to the children

Aiding rural communities

Cahya Mata Sarawak Berhad

pg. 023

Doing good forthe environmentTurning Green into Gold – Recyclingof green waste at PPES Works' projectsites continued in 2007. Now into itssecond year, PPES Works' joint-venturewith a team of young entrepreneurs toturn green waste into organic compostand fertiliser has proved to be a sustainablebusiness. The 'EcoGold' compost andfertilisers are now used in plantationsand in landscaping of gardens in Kuching,and is sold state-wide.

Doing good forthe marketplaceResponsibility to shareholders –As a public-listed entity with over 6,800shareholders, maintaining the highestcorporate governance standards is a mustfor CMS. CMS is a four time winner of theOverall Excellence Award for corporatereports by the Sarawak Chamber ofCommerce & Industry. CMS also pridesitself on compliance with the strict rulesand regulations set by the Malaysianstock exchange.

Responsibility to customers – CMSupholds the quality of its products andservices to the highest standards possible.Even within Sarawak's large land massand rough terrain, CMS manages to riseto the challenge of timely delivery andservice. CMS conducts regular customersatisfaction surveys to garner feedback asa way to constantly improve efficiency.

Fair procurement practices forvendors & suppliers – It is importantfor vendors and suppliers to know thatthey will be treated fairly when puttingin bids to supply products and services.CMS Group Procurement is continuouslyimproving its policies, processes,documentation, and quality of servicefor greater ease and simplicity. The Codeof Ethics and Business Conduct forContractors and Suppliers is publishedon the corporate web-site. In 2007,Group Procurement carried out a triale-bidding exercise to ensure transparencyand competitive bidding. On-goingimprovements to the Contractor-SupplierManagement System are expected tobe completed in 2008.

Doing good atthe workplacePromoting good health & safetypractices at the workplace – CMSis committed to protecting employeesby adhering to good practices in healthand safety. In 2007, CMS Cement wasnamed one of the top 5 winners of theSafety & Health Excellence NationalAward 2006 (Large Scale Category) bythe Ministry of Human Resources. CMSCement also conducted its annual Safety& Health Week in October to raiseawareness among employees.

PPES Works, CMS Roads and CMSPavement Tech continued to maintaintheir Integrated Management System(IMS) accreditation as well as separateinternational accreditations for quality,environmental management andoccupational health and safety.

Strengthening internal bridges –In 2007, we launched "Koffee Talk",a popular employee activity in whichthe top management of CMS Groupengage employees at executive-levelsand below over an informal breakfast.Employees also have the opportunity togive feedback and express their thoughtsat the annual Group Managing Director'sAddress sessions. In 2007, such sessionswere held in Kuching, Sibu, Bintulu, Miriand Kuala Lumpur.

Looking after our employees –We try our utmost best to look after our2,100 employees whilst they are in ouremployment and if possible, to be therefor their families if the unfortunate shouldhappen. In 2007, the Group successfullyclaimed RM687,456 in insurance forbeneficiaries of deceased employees.In addition, CMS has set up theCompassionate Fund to provide financialassistance to employees in times ofurgent need.

pg. 024

Cahya Mata Sarawak Berhad

Y A M Tan Sri Syed Anwar JamalullailGroup Chairman

Tuan Haji Mahmud Abu Bekir TaibDeputy Group Chairman

YB Dato Sri Sulaiman Abdul Rahman TaibNon-Independent, Non-Executive Director

Y Bhg. Dato' Richard Alexander John CurtisGroup Managing Director

Tuan Syed Ahmad Alwee AlsreeDeputy Group Managing Director

Y Bhg. Dato Sri Liang Kim BangSenior Independent, Non-Executive Director

Y Bhg. General (Retired) Tan Sri Dato' SeriMohd Zahidi bin Hj ZainuddinIndependent, Non-Executive Director

YB Datuk Haji Talib bin ZulpilipNon-Independent, Non-Executive Director

Y Bhg. Datuk Wan Ali Tuanku YubiIndependent, Non-Executive Director

Y Bhg Datu Michael Ting Kuok NgieIndependent, Non-Executive Director

Kevin How KowIndependent, Non-Executive Director

01

02

03

04

05

06

07

08

09

10

11

02 03

01

04

08

05

09

06

10

07

11

Board of Directors

Cahya Mata Sarawak Berhad

pg. 025

YAM Tan Sri Syed Anwar Jamalullail is theGroup Chairman of CMS, having beenappointed to the Board on 10 May 2006.He holds a Bachelor of Arts (Accounting)degree from Macquarie University, Australiaand is a Chartered Accountant and CertifiedPractising Accountant of Australia. Hebegan his career as a financial accountantwith Malaysia Airlines System Berhad in1975 and has worked for Price Waterhouse(Australia), D&C Nomura Merchant BankBerhad, Amanah Merchant Bank Berhadand Amanah Capital Partners Berhad asits Group Managing Director. Tan Sri SyedAnwar has also served as Chairman ofMalaysian Resources Corporation Berhadand Media Prima Berhad.

Apart from CMS, Tan Sri Syed Anwar iscurrently Chairman of DRB-HICOM Berhad,EON Capital Berhad, HICOM Berhad,HICOM Holdings Berhad, Uni. Asia LifeAssurance Berhad and Uni. Asia GeneralInsurance Berhad. He is a director ofNestle (M) Berhad and several othercompanies. Tan Sri Syed Anwar wasuntil recently a director of MaxisCommunications Berhad. He was alsothe former Chairman of the InvestmentPanel of Lembaga Urusan Tabung Haji.

Tan Sri Syed Anwar has no familyrelationship with any director and/ormajor shareholder of the Company.

Tuan Haji Mahmud is the Group DeputyChairman of CMS. He was appointed tothe Board of CMS as Group ExecutiveDirector on 23 January 1995. Havingpursued his tertiary education in USAand Canada, Haji Mahmud has extensiveexperience in the stock-broking andcorporate sectors. He was a foundingmember of Sarawak Securities Sdn Bhd,Sarawak's first stock-broking companywhich is now merged with K&N KenangaHoldings Berhad.

Tuan Haji Mahmud is currently Chairmanof UBG Berhad (formerly known as UtamaBanking Group Berhad) and a member ofseveral CMS subsidiaries.

Tuan Haji Mahmud is the brother of YBDato Sri Sulaiman Abdul Rahman Taib (adirector and major shareholder of CMS),Hanifah Hajar Taib and Jamilah HamidahTaib (major shareholders of CMS). He isalso a son of Lejla Taib (a major shareholderof CMS) and brother-in-law of Tuan SyedAhmad Alwee Alsree (Deputy GroupManaging Director of CMS). Tuan HajiMahmud is also a director and formermajor shareholder of Majaharta Sdn Bhd(a major shareholder of CMS). Tuan HajiMahmud is deemed interested inrecurrent related party transactionsannounced to Bursa Malaysia SecuritiesBerhad on 7 April 2008.

YB Dato Sri Sulaiman first joined the Boardof CMS on 23 January 1995 and resignedon 21 January 2008. He was reappointedas Director on 29 January 2008.

YB Dato Sri Sulaiman was Group Chairmanof CMS from May 2002 until June 2006.Prior to that, he had been Deputy GroupChairman from January to April 2002,and held the position of Acting GroupChief Executive Officer of CMS in 2001.

In March 2008, YB Dato Sri Sulaimanwas appointed as Malaysia's DeputyMinister of Tourism. He is also theMember of Parliament for the KotaSamarahan constituency in Sarawak.YB Dato Sri Sulaiman holds a Bachelorof Science degree in BusinessAdministration from the Universityof San Francisco, USA.

YB Dato Sri Sulaiman is the brotherof Tuan Haji Mahmud Abu Bekir Taib(a director and major shareholder ofCMS), Hanifah Hajar Taib and JamilahHamidah Taib (major shareholders ofCMS). He is also a son of Lejla Taib(a major shareholder of CMS) andbrother-in-law of Tuan Syed AhmadAlwee Alsree (Deputy Group ManagingDirector of CMS). YB Dato Sri Sulaimanis also a director and former majorshareholder of Majaharta Sdn Bhd(a major shareholder of CMS). YB DatoSri Sulaiman is deemed interested inrecurrent related party transactionsannounced to Bursa Malaysia SecuritiesBerhad on 7 April 2008.

Y A M Tan Sri Syed Anwar JamalullailGroup ChairmanIndependent, Non-Executive Director

Malaysian, Age 56 years

Member – Group Audit Committee

Chairman – Nomination &Remuneration Committee

Chairman – Executive Committee

Tuan Haji Mahmud Abu Bekir TaibDeputy Group ChairmanNon-Independent,Non-Executive Director

Malaysian, Age 44 years

Member – Nomination &Remuneration Committee

Member – Executive Committee

YB Dato Sri SulaimanAbdul Rahman Taib

Non-Independent,Non-Executive Director

Malaysian, Age 39 years

Dato' Richard Curtis is the Group ManagingDirector of CMS having been appointed tothe Board on 4 September 2006.

Dato' Richard graduated with a Bachelorof Law (LL.B.) (Honours) degree fromUniversity of Bristol, UK and is a SloanFellow of the London Business School.He began his career in legal practice asa solicitor in Norton Rose (1974-1979) inLondon and then joined Jardine Matheson& Co. (1979-1983) in Hong Kong afterwhich he joined the Jardine OffshoreGroup (1983-1986) in postings toSingapore and Indonesia. Dato' Richardalso pursued his own businesses(1988-1997) in retail, consultancy andconstruction. He was Chief Executive

Officer of The Melium Group from 1997 –2000, a leading Malaysian retail companyand F&B chain operator.

Dato' Richard is a director of UBG Berhad(formerly known as Utama Banking GroupBerhad), CMS Trust Management Berhad,K&N Kenanga Holdings Berhad, KenangaInvestment Bank Berhad, and a numberof CMS subsidiaries. Dato' Richard is aTrustee of Yayasan Raja Muda Selangor.

Dato' Richard has no family relationshipwith any director and/or major shareholderof the Company.

Tuan Syed Ahmad Alwee Alsree is theDeputy Group Managing Director of CMSfollowing his appointment to the Boardon 4 September 2006.

He had earlier joined CMS in February2004 as Group General Manager – HumanResources, a portfolio which he continuesto oversee until today. Tuan Syed Ahmadgraduated with a Bachelor of Law (LL.B.)degree from the National University ofSingapore, and practised law in Singaporefor over 10 years prior to joining CMS.

Tuan Syed Ahmad is currently DeputyChairman of UBG Berhad (formerlyknown as Utama Banking Group Berhad),Chairman of CMS Trust ManagementBerhad, and director of a number ofsubsidiaries of CMS Group.

Tuan Syed Ahmad is a brother-in-law ofJamilah Hamidah Taib (a major shareholderof CMS), Tuan Haji Mahmud Abu Bekir Taiband YB Dato Sri Sulaiman Abdul RahmanTaib (directors and major shareholders ofCMS). He is also a son-in-law of Lejla Taib(a major shareholder of CMS) and thespouse of Hanifah Hajar Taib (a majorshareholder of CMS).

He is deemed interested in recurrentrelated party transactions announcedto Bursa Malaysia Securities Berhadon 7 April 2008.

Dato Sri Liang Kim Bang was appointedto the Board of CMS on 26 June 1986.

He is currently Non-Executive Chairmanof CMS Cement Sdn Bhd, CMS Clinker SdnBhd (formerly known as Sarawak ClinkerSdn Bhd), CMS Infra Trading Sdn Bhd andCMS Wires Sdn Bhd. He is also a directorof MISC Berhad, PPB Group Berhad, UBGBerhad (formerly known as Utama BankingGroup Berhad) and CMS TrustManagement Berhad.

Dato Sri Liang holds a Bachelor of Artsand Bachelor of Arts (Honours) degreesfrom the University of Malaya, Singapore(1957-1961), and attended a Post GraduateCourse in Public Administration atCambridge University, England (1962-1963).

He served in the Sarawak Civil Servicefrom 1971 until his retirement in1994. Senior positions held includePermanent Secretary of the Ministryof Communication and Works, DeputyState Financial Secretary andChairman/Director/Member of severalgovernment statutory bodies andgovernment-linked companies. DatoSri Liang was Sarawak's State FinancialSecretary from 1984 to 1994.

Dato Sri Liang has no family relationshipwith any director and/or majorshareholder of the Company.

pg. 026

Cahya Mata Sarawak Berhad

Board of Directors

Y Bhg. Dato' Richard AlexanderJohn Curtis

Group Managing Director

UK national, Malaysian PermanentResident, Age 56 years

Member – Executive Committee

Tuan Syed Ahmad Alwee AlsreeDeputy Group Managing Director

Singapore national, Age 42 years

Member – Nomination &Remuneration Committee

Member – Executive Committee

Y Bhg. Dato Sri Liang Kim BangSenior Independent,Non-Executive Director

Malaysian, Age 71 years

Cahya Mata Sarawak Berhad

pg. 027

General (R) Tan Sri Dato' Seri Mohd Zahidiwas appointed to the Board of CMS on 8July 2005.

He has 39 years experience as aprofessional military officer with his lastappointment as Chief of Defence ForcesMalaysia from January 1999 until hisretirement at the end of April 2005.

General (R) Tan Sri Zahidi is currentlyChairman of Affin Holdings Berhad andCMS I-Systems Berhad. He is a directorof Asiatic Development Berhad, BandarRaya Developments Berhad, Bintulu PortHoldings Berhad, Defence TechnologiesBerhad, Resorts World Berhad and WahSeong Corporation Berhad. In November2006, General (R) Tan Sri Zahidi waselected by DYMM Paduka Seri Sultan

Perak to be a Member of Dewan NegaraPerak, and is a director of Yayasan SultanAzlan Shah.

General (R) Tan Sri Zahidi holds a Masterof Science degree (Defence and StrategicStudies) from Quaid-I-Azam University ofIslamabad, Pakistan. He has attended theSenior Executive Programme in Nationaland International Security at HarvardUniversity, USA, and courses at theCommand and General Staff Collegein the Philippines, Joint Warfare Centrein Australia, Joint Services Staff Collegein Australia and the National DefenceCollege in Pakistan.

General (R) Tan Sri Zahidi has no familyrelationship with any director and/ormajor shareholder of the Company.

YB Datuk Haji Talib was appointed to theBoard of CMS on 13 February 1995.

He is currently Chairman of the SarawakEconomic Development Corporation, andhas been an elected Member of theSarawak State Legislative Assembly sinceSeptember 1996. YB Datuk Haji Talib hasheld senior positions in both publicservice (as Permanent Secretary in theMinistry of Industrial Development andMinistry of Infrastructure Development,Sarawak) and in the private sector (atPetronas and several other organizations).He holds a Master of Commerce andAdministration degree from VictoriaUniversity, New Zealand (1976).

Apart from CMS, YB Datuk Haji Talib is adirector of Sarawak Concrete IndustriesBerhad, a number of CMS subsidiaries,and several private limited companies.

YB Datuk Haji Talib has no familyrelationship with any director and/ormajor shareholder of the Company.

Y Bhg. General (Retired) Tan Sri Dato'Seri Mohd Zahidi bin Hj ZainuddinIndependent, Non-Executive Director

Malaysian, Age 60 years

Member – Nomination &Remuneration Committee

YB Datuk Haji Talib bin ZulpilipNon-Independent, Non-Executive Director

Malaysian, Age 56 years

Member – Group Audit Committee

Datuk Wan Ali was appointed to the Boardof CMS on 23 June 1995.

A former Sarawak State FinancialSecretary (1995-2000) and Director/ChiefExecutive Officer of Sarawak EnterpriseCorporation Berhad (December 2000 -June 2005), Datuk Wan Ali had a longcareer in public service. He also servedas Permanent Secretary in the Ministryof Land Development, Sarawak, and asGeneral Manager of Land Custody andDevelopment Authority, Sarawak. He holds

a Bachelor of Economics degree andGraduate Diploma in Education fromthe University of Malaya. He also holdsa Master of Education degree fromBirmingham University, UK.

Datuk Wan Ali has no family relationshipwith any director and/or majorshareholder of the Company.

Y Bhg. Datuk Wan Ali Tuanku YubiIndependent, Non-Executive Director

Malaysian, Age 58 years

Member – Nomination &Remuneration Committee

pg. 028

Cahya Mata Sarawak Berhad

Datu Michael Ting was appointed tothe Board of CMS on 24 March 1999.

A civil engineer by profession, DatuMichael served in the Public WorksDepartment (PWD) for 32 years. Hislast appointment was as Director of PWDprior to retiring in 1998. Datu Michaelcontinued to serve as Technical Advisorto Sarawak's State Planning Unit for afurther two years. Datu Michael holds aBachelor of Engineering (Honours) andMaster of Engineering degrees in CivilEngineering, both from the TechnicalUniversity of Nova Scotia, Canada.

Datu Michael is currently a director of UBGBerhad (formerly known as Utama BankingGroup Berhad), CMS Trust ManagementBerhad and a number of subsidiaries ofthe CMS Group.

Datu Michael has no family relationshipwith any director and/or major shareholderof the Company. He is deemed interestedin recurrent related party transactionsannounced to Bursa Malaysia SecuritiesBerhad on 7 April 2008.

Kevin How Kow was appointed to the Boardof CMS on 12 March 2004.

Kevin is a Fellow of the Institute ofChartered Accountants in England &Wales and the Institute of Certified PublicAccountants of Singapore. He is a memberof the Malaysian Institute of Accountantsand the Malaysian Institute of CertifiedPublic Accountants. He was made apartner of Ernst & Young, Malaysia in 1984and served as Partner-in-charge of itsoffices in Sabah and Sarawak. From 1996onwards, Kevin was Partner-in-chargeof the firm's practice in Sabah and Labuanuntil his retirement at the end of 2003.

Kevin's directorships in public companiesinclude UBG Berhad (formerly known asUtama Banking Group Berhad), CMS I-Systems Berhad, K&N Kenanga HoldingsBerhad, Kenanga Investment Bank Berhad,Sabah Development Bank Berhad andSaham Sabah Berhad. He is also a directorof CMS Opus Private Equity Sdn Bhd andother private limited companies.

Kevin has no family relationship withany director and/or major shareholderof the Company.

Senior Management

Ian G. SadlerGroup Chief Financial Officer

Tuan Haji Draim Abdul LatipDeputy Group General Manager,

Human Resources

Hasanah AbdullahDeputy Group General Manager,

Human Resources

Abdul Rashid Daljit AbdullahHead, Group Technology

David Ling Koah WiGroup General Counsel

Eda AhmadHead, Group Corporate

Communications

Woo Yoke MengGroup Internal Auditor

Tuan Haji Othman Abdul RaniHead, Cement SBU

Robert E. GardnerHead, Construction &

Road Maintenance SBU

Y Bhg Datuk Dr Chew Han ChingHead, Property Development SBU

Isaac LugunHead, Similajau Development SBU

Goh Chii BingHead, Construction Materials SBU

Board of Directors

Save as disclosed, none of the Directors have:• Any conflict of interest with CMS.• Any conviction for offences within the past 10 years other than traffic offences.

Y Bhg Datu Michael Ting Kuok NgieIndependent, Non-Executive Director

Malaysian, Age 67 years

Member – Group Audit Committee

Member – Nomination &Remuneration Committee

Kevin How KowIndependent, Non-Executive Director

Malaysian, Age 59 years

Chairman – Group Audit Committee

Cahya Mata Sarawak Berhad

pg. 029

Statement of Corporate Governance

Once again, the Board would like to assure shareholders ofits commitment towards maintaining the highest standardsof corporate governance and the effective application of itsprinciples and best practices throughout the Group, as set outin the Malaysian Code of Corporate Governance ("the Code").These principles include accurate financial disclosure, an opendialogue between the Board of Directors and Management,accountability to our shareholders, and utmost integrity inall our actions.

The Board will continue to enhance its role in improvinggovernance practices effectively to safeguard the interestsof shareholders and other stakeholders.

Corporate Governance PrinciplesThis Report, which has been considered and adopted by theBoard, sets out the manner in which the Company implementedand applied the Code's principles and best practices. The Boardbelieves that the Principles of the Code and the Best Practicesoutlined in the Code have, in all material respects, been compliedwith and adhered to.

Board of DirectorsPrincipal Responsibilities of the BoardThe Board of Directors is accountable to shareholders for theperformance of CMS. Without intending to limit this generalrole and its statutory duties, the Board's principal functionsand responsibilities include the following:

• Setting the Group's overall strategic direction andmonitoring progress of these strategies.

• Authorising and monitoring investments and strategiccommitments.

• Approving business plans and budgets.

• Overseeing conduct of the Company's business.

• Identifying principal risks and ensuring systemsare in place to manage these risks.

• Reviewing the adequacy of the Company's systemof internal controls.

• Succession planning, including appointing, fixing thecompensation of, and where appropriate, replacingsenior management.

• Developing investor relations programmes for the Group.

• Scrutinising and reporting to shareholders on, but notlimited to, the financial statements of the Company.

Board Balance and IndependenceThe Board currently has eleven (11) members, of whichnine (9) are non-executive Directors, including the Chairman.Six (6) of the eleven (11) Directors are independent Directors,which exceeds the one-third requirement set by BursaMalaysia Securities Berhad ("Bursa Securities").

This size and composition of the Board is considered optimum,well balanced and caters effectively at present to the scope andcomplexity of the diverse businesses of CMS Group.

Together, the Directors have a wide range of business, financial,management, technical, private sector and public serviceexperience. This enables the Board to provide effective leadershipto the Group's strategy and performance. A brief profile of eachDirector is presented on pages 025 to 028 of this Annual Report.

The independent Directors, based on their breadth of knowledgeand experience, provide unbiased and independent views, adviceand judgment to take account the interests of all stakeholdersincluding shareholders, employees, customers, suppliers andthe communities in which the Group conducts its business. Byway of their majority membership of the Audit Committee andthe Nomination and Remuneration Committee ("NRC"), theindependent Directors fulfill a self-regulating and key role incorporate accountability.

Division of Roles and Responsibilities between theChairman and the Group Managing DirectorThe role of the Chairman and the Group Managing Director isseparated and clearly defined to ensure a balance of power andauthority. The Chairman is responsible for ensuring the Board'seffectiveness and conduct, whilst the Group Managing Directorhas overall responsibility for the operating units, organisationaleffectiveness and implementation of the Board's policies anddecisions. In addition, the Group Managing Director also actsas the intermediary between the Board and Management.

Cahya Mata Sarawak's ("CMS") approach to corporate governance isdesigned to ensure that its business and affairs are effectively managedin order to deliver value to the shareholders. It is a system that the Boardhas put in place to enhance transparency and accountability, to providechecks and balances throughout the organisational structure, whilstemphasising increased business efficiency of the Group.

pg. 030

Cahya Mata Sarawak Berhad

Statement of Corporate Governance

Appointments to the BoardThe NRC recommends the appointment of new Directorsto the Board. Upon appointment, new Directors undergoa familiarisation programme to facilitate a quick andcomprehensive understanding of the Group. This includesa detailed information package comprising:

• Corporate and company organisation structures.

• Terms of Reference of the various Board committees.

• Profiles of key personnel.

• An overview of the Group's operations.

• Corporate governance guidelines which have beenapproved by the Board. The guidelines set out specificroles, duties, responsibilities and rights of the Directors.

Visits to the various operating businesses and meetings withsenior management are arranged, as appropriate.

On 21 January 2008, YB Dato Sri Sulaiman Abdul Rahman Taibresigned as a Non-Executive Director. He was subsequentlyreappointed to the Board as Non-Executive Director on 29January 2008.

Re-election of DirectorsIn accordance with the Company's Articles of Association,all Directors appointed by the Board are subject to electionby shareholders at the first Annual General Meeting aftertheir appointment. One-third of the remaining Directors arerequired to submit themselves for re-election by rotationat each Annual General Meeting. All Directors must submitthemselves for re-election at least once in every three years.Directors over seventy years of age are required to submitthemselves for re-appointment annually in accordance withSection 129(6) of the Companies Act, 1965.

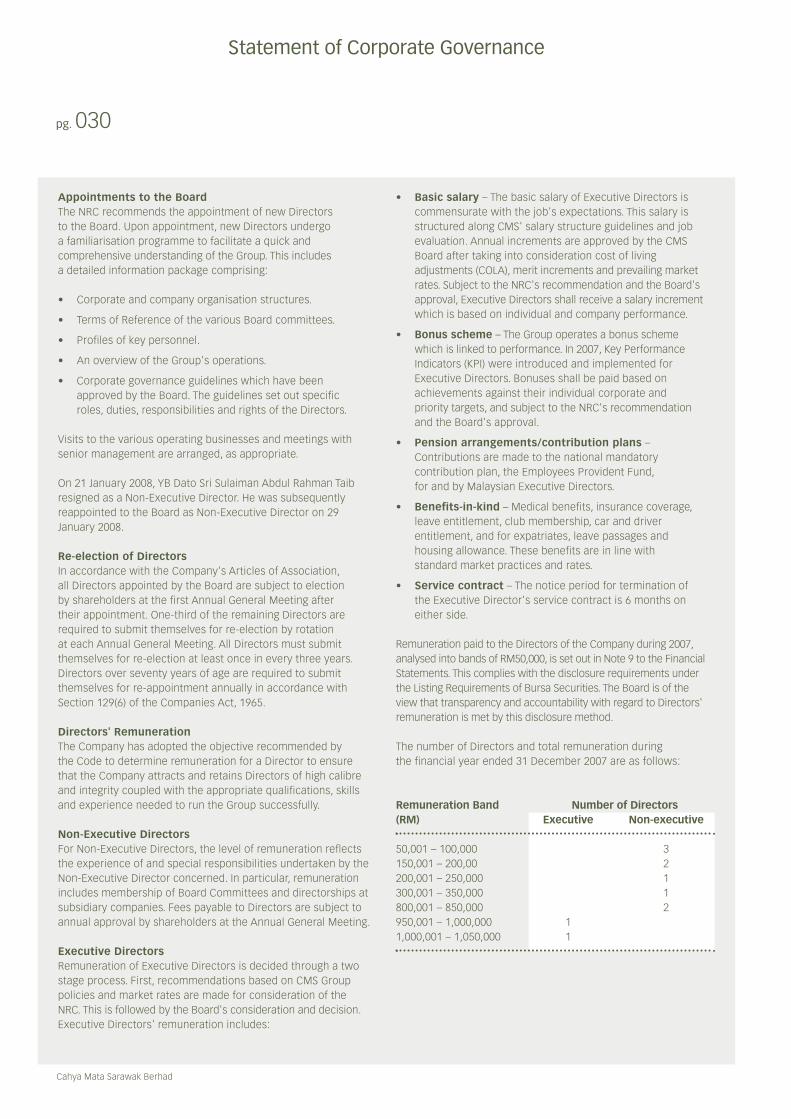

Directors' RemunerationThe Company has adopted the objective recommended bythe Code to determine remuneration for a Director to ensurethat the Company attracts and retains Directors of high calibreand integrity coupled with the appropriate qualifications, skillsand experience needed to run the Group successfully.

Non-Executive DirectorsFor Non-Executive Directors, the level of remuneration reflectsthe experience of and special responsibilities undertaken by theNon-Executive Director concerned. In particular, remunerationincludes membership of Board Committees and directorships atsubsidiary companies. Fees payable to Directors are subject toannual approval by shareholders at the Annual General Meeting.

Executive DirectorsRemuneration of Executive Directors is decided through a twostage process. First, recommendations based on CMS Grouppolicies and market rates are made for consideration of theNRC. This is followed by the Board's consideration and decision.Executive Directors' remuneration includes:

• Basic salary – The basic salary of Executive Directors iscommensurate with the job's expectations. This salary isstructured along CMS' salary structure guidelines and jobevaluation. Annual increments are approved by the CMSBoard after taking into consideration cost of livingadjustments (COLA), merit increments and prevailing marketrates. Subject to the NRC's recommendation and the Board'sapproval, Executive Directors shall receive a salary incrementwhich is based on individual and company performance.

• Bonus scheme – The Group operates a bonus schemewhich is linked to performance. In 2007, Key PerformanceIndicators (KPI) were introduced and implemented forExecutive Directors. Bonuses shall be paid based onachievements against their individual corporate andpriority targets, and subject to the NRC's recommendationand the Board's approval.

• Pension arrangements/contribution plans –Contributions are made to the national mandatorycontribution plan, the Employees Provident Fund,for and by Malaysian Executive Directors.

• Benefits-in-kind – Medical benefits, insurance coverage,leave entitlement, club membership, car and driverentitlement, and for expatriates, leave passages andhousing allowance. These benefits are in line withstandard market practices and rates.

• Service contract – The notice period for termination ofthe Executive Director's service contract is 6 months oneither side.

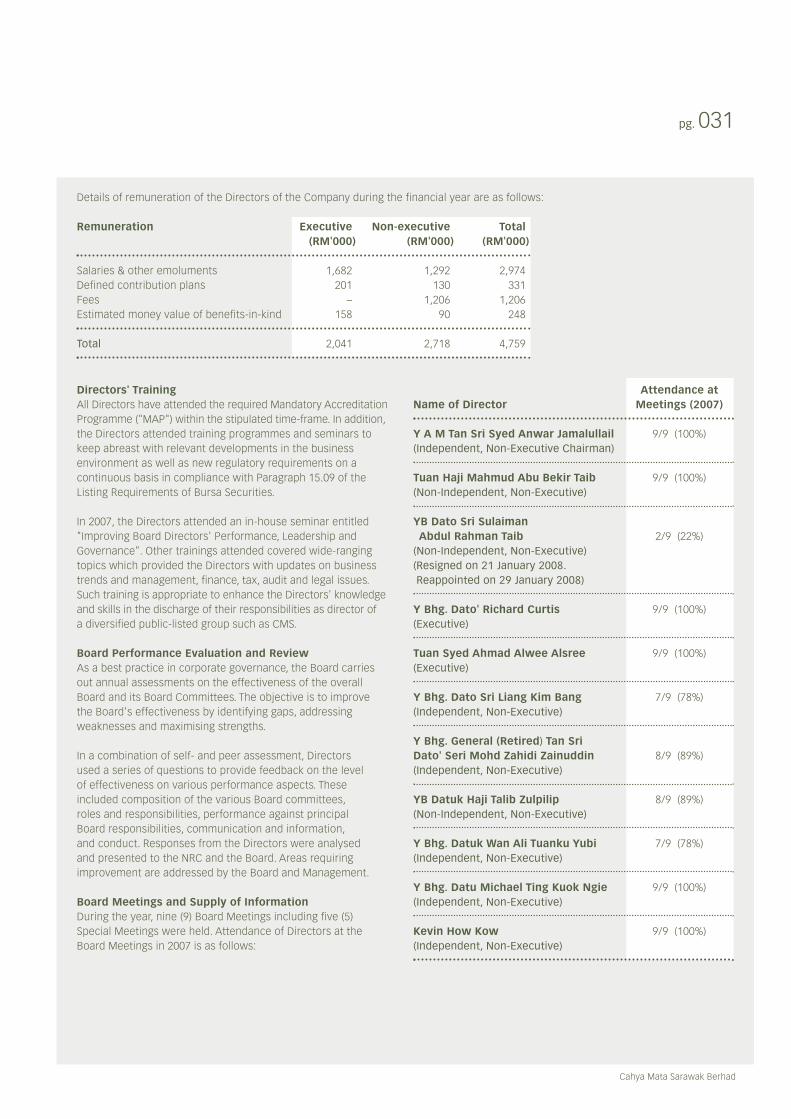

Remuneration paid to the Directors of the Company during 2007,analysed into bands of RM50,000, is set out in Note 9 to the FinancialStatements. This complies with the disclosure requirements underthe Listing Requirements of Bursa Securities. The Board is of theview that transparency and accountability with regard to Directors'remuneration is met by this disclosure method.

The number of Directors and total remuneration duringthe financial year ended 31 December 2007 are as follows:

Remuneration Band Number of Directors(RM) Executive Non-executive

50,001 – 100,000 3150,001 – 200,00 2200,001 – 250,000 1300,001 – 350,000 1800,001 – 850,000 2950,001 – 1,000,000 11,000,001 – 1,050,000 1

Cahya Mata Sarawak Berhad

pg. 031

Directors' TrainingAll Directors have attended the required Mandatory AccreditationProgramme ("MAP") within the stipulated time-frame. In addition,the Directors attended training programmes and seminars tokeep abreast with relevant developments in the businessenvironment as well as new regulatory requirements on acontinuous basis in compliance with Paragraph 15.09 of theListing Requirements of Bursa Securities.

In 2007, the Directors attended an in-house seminar entitled"Improving Board Directors' Performance, Leadership andGovernance". Other trainings attended covered wide-rangingtopics which provided the Directors with updates on businesstrends and management, finance, tax, audit and legal issues.Such training is appropriate to enhance the Directors' knowledgeand skills in the discharge of their responsibilities as director ofa diversified public-listed group such as CMS.

Board Performance Evaluation and ReviewAs a best practice in corporate governance, the Board carriesout annual assessments on the effectiveness of the overallBoard and its Board Committees. The objective is to improvethe Board's effectiveness by identifying gaps, addressingweaknesses and maximising strengths.