ontwerp/layout: i.d. graphics - hakrinbank€¦ · business of the bank 29 nationale trust- en...

TRANSCRIPT

Ontwerp/layout: I.D. GraphicsFoto’s: Hubert Hermelijn, I.D. GraphicsCTP en druk: Leo Victor N.V.

MISSION

Hakrinbank is a dynamic, innovative bank that provides its clientswith a comprehensive range of high-quality, customised financial services.

Our highly skilled employees work together as a teamto maximise client satisfaction.

ANNUAL REPORT 2006

HAKRINBANK N.V.

The staff party held in Hotel Torarica to celebrate the 70th anniversary of Hakrinbank.

On 28 June 2006 it was exactly 70 years sinceHakrinbank started providing services to the community of Suriname. The bank began as a family business under the name of O.R.G.VervuurtsBanking Corporation and grew steadily over thesubsequent years. In 1943, it amended its Articles ofAssociation and changed its name to Vervuurts-bank N.V.

The bank’s healthy growth over the years meant thatthe original head office on Keizerstraat had becometoo small by 1971. It was consequently decided tomove the head office to Dr. Sophie Redmondstraat11-13. This office building, which is majestic by thestandards of Suriname, is still the highest inParamaribo. In the same year, the bank decided torestructure. This restructuring included a number ofwell-known foreign banks and the government ofSuriname acquiring shares in the bank, as well as thebank’s name being changed to Handels- Krediet- enIndustriebank N.V. or Hakrinbank for short. At thesame time, the bank installed its first computer and was at that time the only bank in the country tohave an automated administration system.

In the first half of the 1980s, all the bank’s sharesonce again came into Surinamese ownership.Thanks to the efforts of all its employees, both nowand in the past, and the support and trust of all itsclients and relationships, Hakrinbank has been ableto establish a solid and lasting place for itself in oursociety. The services we provide as a leading bankinginstitution comprise a wide range of financial products.We are rightly proud of the prominent rolewe play in product innovation, as witnessed, for example, by the fact that we were the first bank, inearly 2004, to introduce internet banking toSuriname.

It is now 2007 and our bank is facing a series ofmajor challenges as a result of the rapid and far-reaching changes in both the national and international arenas. These changes include theincreasing competition resulting from develop-ments in the Surinamese banking market and thecountry’s continuing economic integration intoCaricom and other economic alliances, as well astighter regulations and the increasing compliancerequirements. Clients are also becoming more critical and expect high-quality services and modern banking products. These developments aremaking it increasingly difficult for smaller banks tofund the rising level of hardware and softwareinvestments that are needed. Such banks are conse-quently increasingly seeking to merge or acquireother organisations in order to achieve the requiredcritical mass. The efforts and commitment of ouremployees will ensure that we respond effectively tothese challenges and continue providing services tothe community of Suriname so that our bank develops and flourishes, our employees’ welfareremains assured and we achieve a return for ourshareholders and thus also help to promote the further development of Suriname.

We are proud that Hakrinbank has been able to celebrate its seventieth anniversary in such good economic health, with various growth and profitability records being achieved in this anniversary year.

The celebrations of this anniversary are very much adominant theme of this annual report. Our headoffice in illuminations can be seen on the frontcover, while various aerial photographs of the celebrations can also be found on the inside pages.Hakrinbank owes a great debt of gratitude to allthose who have helped and supported it over theyears.

28 JUNE 1936 28 JUNE 2006

70 YEARS OF HAKRINBANK N.V.

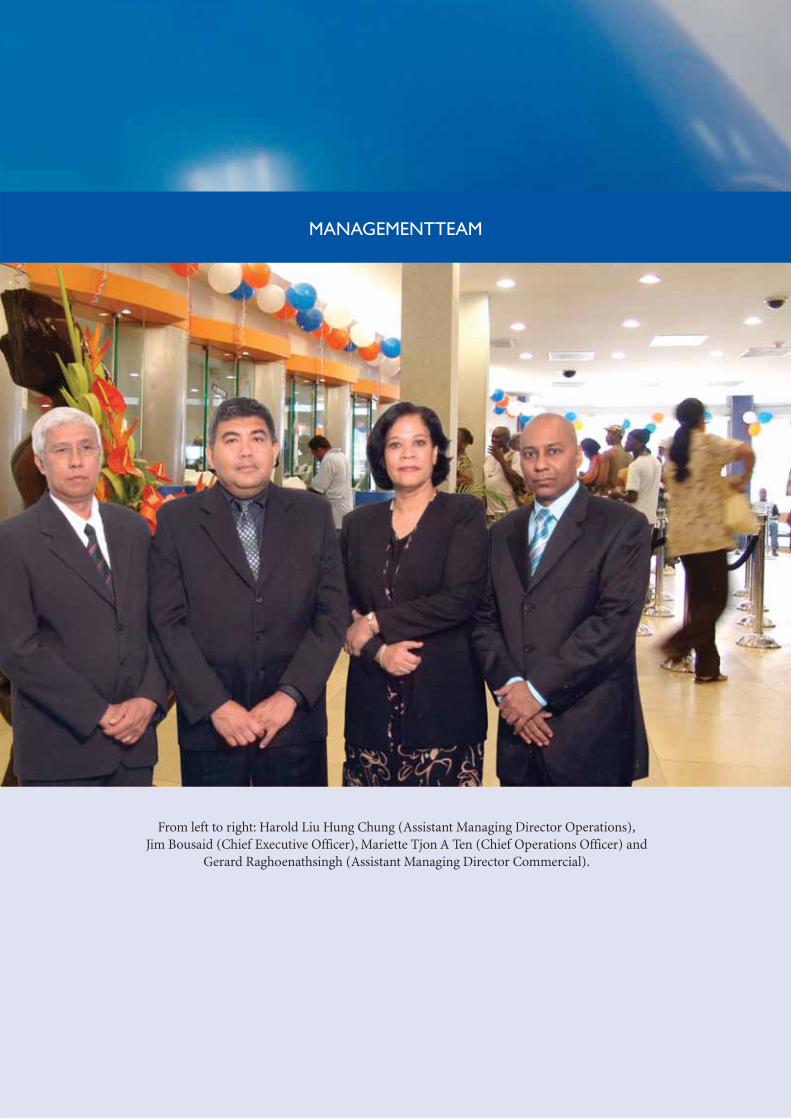

MANAGEMENTTEAM

From left to right: Harold Liu Hung Chung (Assistant Managing Director Operations),Jim Bousaid (Chief Executive Officer), Mariette Tjon A Ten (Chief Operations Officer) and

Gerard Raghoenathsingh (Assistant Managing Director Commercial).

5

CONTENTS

Mission 1

Hakrinbank N.V. - 70 years in action 3

Organogram 6

Key consolidated figures 2002 – 2006 8

Report of the Supervisory Board 10

Report of the Executive Board 13

Looking back at the year under review 13Economic developments in 2006 15Business of the bank 29Nationale Trust- en Financierings Maatschappij N.V. 41Financial developments of the bank 42

Auditors’ report 49

Financial statements 2006 51

Consolidated balance sheet 52Consolidated profit and loss account 53Company balance sheet 54Company profit and loss account 55Notes to the financial statements 56

Other information 62

Curricula vitae and details of ancillary positions of members of the Supervisory Board and Executive Board of Hakrinbank 62Addresses 65Appendix I: Suriname: Key macro-economic data 66

Cash

Human Resources &General Affairs

Insurance

Credit Administration

Foreign Transfers

Compliance & Legal

C.E.O.

C.O.O.

6

Organogram as at 31 December 2006

Information &Communication

Technology

Domestic

Affiliates (Operations)

Maintenance& Technical Support

Internal Audit

Administration& Management

Information(Accounting)

Administration& Management

Information (FinancialControlling)

Treasury & Securities

Risk Management

Credits

Nationale Trust &Financierings Mij. N.V.

Affiliates (Credits)

Assistant ManagingDirector Commercial

Assistant ManagingDirector Operations

As at 31 December 2006

7

Ms M.M. Tjon A Ten

Human Resources &General Affairs

M. Naarendorp, Head of DepartmentN. Samoedj

InsuranceR. Tjon A Kon, Head of Department

Credit AdministrationI. Loenersloot, Head of Department

Compliance & LegalM. Schaap

Maintenance & TechnicalSupport

R. Tjokro, Head of Department

Foreign TransfersM. Lie A Njoek, Head of Department

(until 31-12-2006)A. Hagens, Interim Head of Department

(from 1-1-2007)L. Karg, Deputy Head of Department

Information & CommunicationTechnology

T. Sanches, Head of DepartmentR. MahabierA. Semoedi

T. Csaba

DomesticM. Tjon, Head of Department

J. Legiman

CashA. Budel-Samiran, Head of Department

AffiliatesBranchmanagers

- TourtonneV. Ramtahalsing- Nieuwe Haven

N. Elshot-Chelius- Latour

R. Wimpel- Flora

R. Mohamatsaid

J.D. Bousaid

CreditsAccount ManagersC. Halfhide-Chou

S. Kisoensingh-JhauwS. Jadoenathmisier

L. VenlooP. QuintiusE. Frangie

Treasury & SecuritiesP. Tjon Kiem Sang, Head of Department

R. Amirkhan

Nationale Trust &Financierings Mij. N.V.

H. Vijzelman, Head of DepartmentR. Sitaram, Deputy Head of Department

G. Jong

Administration & ManagementInformation

R. Liesdek, AccountingR. Sheorajpanday, Financial controlling

Internal AuditB. Jewbali, Head of Department

Risk ManagementS. Shair-Ali, Head of Department

AffiliatesBranchmanagers

- NickerieR. Mangala, Head of Department

A. Anandbahadoer, Deputy Head ofDepartment

- TamanredjoS. Resomardono

Assets & Liabilities ManagementCommittee

SUPERVISORY BOARD

A.K.R. Shyamnarain - ChairmanR.A. Mac Donald - Deputy ChairmanH.B. AbrahamsMs G. Lie Sem-NawikromoH.R. RamdhaniM.M. Sandvliet J.J.F. Tjang-A-Sjin

EXECUTIVE BOARD

J.D. Bousaid - Chief Executive Officer Ms M.M. Tjon A Ten - Chief Operations Officer

DEPUTY DIRECTORS

H.S.K. Liu Hung Chung - Assistant Managing Director Operations

G.M. Raghoenathsingh - Assistant Managing Director Commercial

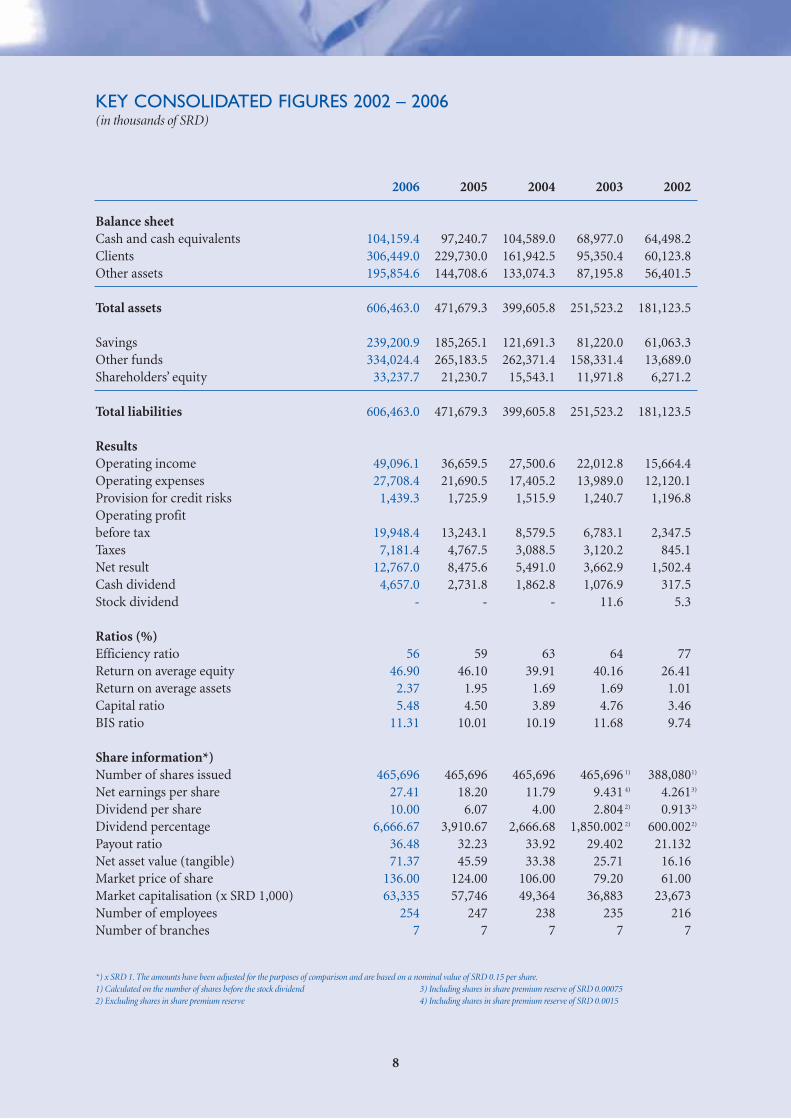

KEY CONSOLIDATED FIGURES 2002 – 2006 (in thousands of SRD)

2006 2005 2004 2003 2002

Balance sheet Cash and cash equivalents 104,159.4 97,240.7 104,589.0 68,977.0 64,498.2Clients 306,449.0 229,730.0 161,942.5 95,350.4 60,123.8Other assets 195,854.6 144,708.6 133,074.3 87,195.8 56,401.5

Total assets 606,463.0 471,679.3 399,605.8 251,523.2 181,123.5

Savings 239,200.9 185,265.1 121,691.3 81,220.0 61,063.3Other funds 334,024.4 265,183.5 262,371.4 158,331.4 13,689.0Shareholders’ equity 33,237.7 21,230.7 15,543.1 11,971.8 6,271.2

Total liabilities 606,463.0 471,679.3 399,605.8 251,523.2 181,123.5

ResultsOperating income 49,096.1 36,659.5 27,500.6 22,012.8 15,664.4Operating expenses 27,708.4 21,690.5 17,405.2 13,989.0 12,120.1Provision for credit risks 1,439.3 1,725.9 1,515.9 1,240.7 1,196.8Operating profitbefore tax 19,948.4 13,243.1 8,579.5 6,783.1 2,347.5Taxes 7,181.4 4,767.5 3,088.5 3,120.2 845.1Net result 12,767.0 8,475.6 5,491.0 3,662.9 1,502.4Cash dividend 4,657.0 2,731.8 1,862.8 1,076.9 317.5Stock dividend - - - 11.6 5.3

Ratios (%)Efficiency ratio 56 59 63 64 77Return on average equity 46.90 46.10 39.91 40.16 26.41Return on average assets 2.37 1.95 1.69 1.69 1.01Capital ratio 5.48 4.50 3.89 4.76 3.46BIS ratio 11.31 10.01 10.19 11.68 9.74

Share information*)Number of shares issued 465,696 465,696 465,696 465,696 388,080Net earnings per share 27.41 18.20 11.79 9.431 4.261Dividend per share 10.00 6.07 4.00 2.804 0.913Dividend percentage 6,666.67 3,910.67 2,666.68 1,850.002 600.002Payout ratio 36.48 32.23 33.92 29.402 21.132Net asset value (tangible) 71.37 45.59 33.38 25.71 16.16Market price of share 136.00 124.00 106.00 79.20 61.00Market capitalisation (x SRD 1,000) 63,335 57,746 49,364 36,883 23,673Number of employees 254 247 238 235 216Number of branches 7 7 7 7 7

*) x SRD 1. The amounts have been adjusted for the purposes of comparison and are based on a nominal value of SRD 0.15 per share.1) Calculated on the number of shares before the stock dividend 3) Including shares in share premium reserve of SRD 0.000752) Excluding shares in share premium reserve 4) Including shares in share premium reserve of SRD 0.0015

8

1)

4)

2)

2)

1)

3)

2)

2)

SUPERVISORY BOARD

From left to right: Harold Ramdhani, Roy Shyamnarain (Chairman), Johan Tjang-A-Sjin, Milton Sandvliet,Ghamie Lie Sem-Nawikromo, Richard Mac Donald (Deputy Chairman) and Enrico Abrahams.

9

To the shareholders

General We are pleased to present our report on our activities in the 2006 financial year, in which the celebrations of the bank’s seventieth anniversaryplayed an important part. In this report we also dis-cuss the activities of the Audit Committee and theRemuneration and Nomination Committee. Wehave also included our recommendation that thefinancial statements for the year and the proposedappropriation of profit be adopted.

Activities of the Supervisory BoardThe Supervisory Board held eleven ordinary meetings and fifteen extraordinary meetings during2006. Ordinary meetings are held monthly in thepresence of the Executive Board, while extra-ordinary meetings depend on the subjects to be discussed and are normally attended only by members of the Supervisory Board. Our super-vision focused primarily on the company’s resultsand strategy, and included regular discussions of thefigures showing the results achieved to date, as presented by the Executive Board, and approval ofthe 2007 Policy Memorandum, together with theaccompanying Operational and Investment Budgetfor 2007. Other subjects on the meeting agendasincluded corporate governance, risk management,the possibility of introducing a system ofperformance management for the Executive Board,adopting a new pension scheme for the ExecutiveBoard, a proposal to amend the pension scheme forsome former members of the Executive Board,details of the working relationship between theAudit Committee and key officers in the bank’sinternal control organisation, devising a proposal forreviewing the remuneration of members of theSupervisory Board and various other subjects. Someof these issues are discussed in greater detail below.

Corporate governanceIn June 2006, the chairman of the board and those ofthe Audit Committee attended the launch and in-augural meeting of the Caribbean Association ofAudit Committee Members (CAACM) on behalf ofthe Supervisory Board. This Committee was set upby the Caribbean Association of Indigenous Banks

(CAIB), an alliance of regional banks of which ourChief Executive Officer, Jim Bousaid, is a Boardmember. Being a member of CAACM enables us toshare in the knowledge and experience gained byother regional banks in the area of corporate gover-nance and in devising strategies benefiting the workof our Audit Committee. The Supervisory Boardintends to play an active role in the activities of bothCAIB and CAACM wherever it considers suchinvolvement to be necessary and effective. The chair-man of the Supervisory Board and the ExecutiveBoard consequently attended CAIB’s annual meetingin Port of Spain in November 2006, at which variousissues relating to corporate governance, risk manage-ment and the implementation of the Basel II guide-lines for banks in the region were discussed.

Activities relating to the Executive BoardThe Supervisory Board asked an external consultantfor advice in 2006 on devising and implementing asystem of performance management for theExecutive Board and on an accompanying bonusscheme for the individual members of the Board.Wehave since received the consultants’ advice and areconsidering how best to implement the proposedperformance management system. By introducing arelated bonus system, the Supervisory Board is seeking to establish an effective and efficient linkbetween the appraisal of performance and remuneration of the individual Executive Boardmembers. Our primary goal in this respect is toencourage and inspire the Executive Board to makeeven more efforts to achieve the organisation’sobjectives.

The Supervisory Board also gave further considera-tion to the existing pension arrangements for theExecutive Board and concluded that these arrange-ments needed to be amended in order to bring theminto line with the changed circumstances in the market. We have since adopted a new pensionscheme, following advice from external specialists.

We reported last year that the Executive Boardwould be expanded to include a Finance Director(Chief Financial Officer) within the foreseeablefuture. We duly started the appointment process inthis respect on January 1st, 2007.

10

REPORT OF THE SUPERVISORY BOARD

Activities of the Audit CommitteeIn June 2006, the chairman of the Supervisory Boardtogether with the chairman of the Audit Committeeattended the launch and inaugural meeting of theCAACM. More information on this meeting can befound in the section on corporate governance above.In October 2006, the Audit Committee held a plenary meeting with all key officers in the bank’sinternal control organisation. The meeting includeddetailed discussions of existing relationships atwork, relationships with the Executive Board, jobdescriptions and authorisations and staffing. Ameeting, which was also attended by the ExecutiveBoard, was held in November 2006 with the externalauditors to discuss the management letter for 2005.Agreements were reached for more intensive contactbetween the Executive Board, the Audit Committeeand the internal and external auditors to discussissues such as the management letters, the auditedannual figures and other relevant financial reporting.

In February 2007, the external auditors discussedways of managing the risk of fraud with the AuditCommittee, the Executive Board and the relevantbank officers. The Audit Committee reported on itsactivities at the ordinary meetings of the Super-visory Board throughout the year.

Activities of the Remuneration and Nomination Committee The Remuneration and Nomination Committeefocused in 2006 on formulating proposals foramending the pension schemes of the ExecutiveBoard and certain former members of the ExecutiveBoard. After advice on this subject had beenobtained from external specialists, proposals weresubmitted to the Supervisory Board and have sincebeen approved.

The Committee was also advised by external consultants on proposals for introducing a system ofperformance management for the Executive Boardand a linked bonus scheme. More information onthis can be found in ‘Activities relating to theExecutive Board’ above.

The Committee also contributed to the discussionswithin the Board on finalising the position of theCFO. More information on this is also provided above.

The Committee reported on its activities at the ordinary meetings of the Supervisory Boardthroughout the year.

Independence and composition of theSupervisory BoardThe Supervisory Board believes that all its memberscomply with the requirements for independence asreferred to in the Hakrinbank N.V. corporate governance code. Information on the individualBoard members and their ancillary positions can befound elsewhere in this report.

There were no changes in the Supervisory Boardduring the year under review, and the Board continues to have seven members. Mr. J.J.F. Tjang-A-Sjin and Mr. H.B. Abrahams are the next super-visory board members scheduled to resign by rotation. Both have confirmed that they wish to beconsidered for reappointment, and we recommendthat they be reappointed.

Remuneration of Supervisory Board membersThe Supervisory Board has for some time been considering how best to formulate a proposal forreviewing the remuneration paid to members of theSupervisory Board. The general principle in thesediscussions has been that members of the Boardshould be properly remunerated for their work.Account also has to be taken of the bank’s corporategovernance policy as proper performance of theBoard’s supervisory activities requires individualmembers of the Board to be closely involved in theseactivities of the bank. This inherently requires themembers’ responsibility for their work to be moreclearly defined.And this in turn will ultimately resultin a higher quality of supervision. The efforts to establish an appropriate level of remuneration takeaccount in the first instance of the individual member’s relevant expertise and the amount of timerequired to perform the activities pertaining to hisor her position on the Board. The fees set shouldalso take account of any representative tasks performed and any logistic and support facilitiesprovided.

Financial statements and proposed appropriationof profitThe Supervisory Board is pleased to present thebank’s financial statements for the 2006 financialyear. These financial statements comprise the |company balance sheet as at 31 December, the company profit and loss account, the consolidatedbalance sheet as at 31 December, the consolidatedprofit and loss account and the accompanying notes.The financial statements have been audited by theexternal auditors, as provided for in the bank’s

11

Articles of Association. This report includes theauditors’ report and unqualified approval of thefinancial statements.

The operating result is essentially the outcome of therealization of the policy objectives defined in the2006 Policy Memorandum which were conscien-tiously implemented by the Executive Board. Thisyear, too, the operating result was boosted to somedegree by the continuing positive developments inSuriname’s macro-economic environment. Prudentfinancial management by the government, togetherwith the favourable prices on the world market forcommodities such as oil, gold and alumina, has alsoundoubtedly played a role in this. It is interesting tonote in this respect that much of 2006 was dominatedby public discussions of whether we as a country areearning enough from our natural resources, whichare largely owned by foreign multinationals. Thesediscussions high-lighted the community’s deepsense of involvement in and commitment to thissubject and the need for the government’s policy ondeveloping our natural resources, to be transparent.This transparency is particularly important inrespect of the revenues that we as a community generate from our natural resources and the way inwhich these revenues are used. There also seems tobe public consensus on the need for reviewing theway in which we as a country have to date dealt withour natural resources. This may provide support forthe government in its forthcoming negotiations onthe bauxite operations in Western Suriname and thegoldmining activities in the Nassau mountain area.

Profit before tax amounted to SRD 19.95 million,with a net profit after tax of SRD 12.77 million.We propose appropriating SRD 4.66 million ofthis for dividend pay-out to the shareholders and transferring SRD 8.11 million to the general reserve.This means a dividend of SRD 10 per share ofSRD 0.15 nominal value in our anniversary year of2006. This dividend will be paid in cash. An amountof SRD 1.40 per share was previously distributed asan interim dividend in October 2006, which means afinal dividend of SRD 8.60 per share of SRD 0.15nominal value.

We recommend that you, our shareholders, adoptthese financial statements and thus ratify theExecutive Board’s management and the SupervisoryBoard’s supervision of the bank in the year underreview. We also recommend that you approve theproposed distribution of the profit for the year.

Vote of thanks for the good resultsThe Supervisory Board would like to express itsgratitude for the way in which the Executive Boardrepresented the company’s interests during the yearunder review and specifically its efforts and thestrategic choices that produced the good operatingresult for the year. We would also like to thank themanagement and other employees for the way in which they have individually contributed to a successful year for the bank and to express ourrecognition of the vital role that they have played inachieving the objectives set. We would also like tothank our clients and all the other parties whodemonstrated their trust and confidence in Hakrin-bank N.V. during the year and provided such a goodbasis for a mutually beneficial relationship. Last but not least, we would like to thank you, our share-holders, for the support that you provide us in ourwork. This inspires us as an organisation to continuestriving for excellence in everything we do.

Paramaribo, 10 April 2007

Supervisory Board

A.K.R. Shyamnarain - ChairmanR.A. Mac Donald - Deputy ChairmanH.B. AbrahamsMs G. Lie Sem-NawikromoH.R. RamdhaniM.M. SandvlietJ.J.F. Tjang-A-Sjin

12

Looking back at the year under review

Our bank recorded an excellent performance in2006, the year in which it also celebrated its seventieth anniversary. Total assets in the consolidated balance sheet rose by almost 29% toSRD 606.5 million, while the profit before taxincreased by over 50% to close to SRD 20 million.Allthe key performance ratios improved, with thereturn on assets rising from 1.95% to 2.37% and thereturn on equity increasing from 46.1% to 46.9%.The efficiency ratio improved from 59% to 56%,while the non-performing loans ratio decreasedfrom 3% to 2%.

The healthy development in the bank’s operations isthe result of a combination of factors, including thebenefits that have accrued from the favourablemacro-economic environment of low inflation,stable exchange rates and higher levels of economicgrowth. This also meant a good level of lending,with total lending increased with 33.4% which washigher than budgeted. An element of saturation wasseen in the consumer credit market, while the foreign currency market was calm as a result ofsupply and demand essentially being in equilibriumat the prevailing exchange rates.

The Minister of Finance stated in his FinancialMemorandum for 2007 that the favourable economic developments were primarily a result ofthe “strict and disciplined implementation of thebudgetary policy, underpinned by the favourableinternational economy and prudent monetary policies.” Government finances improved considerably, with a small cash budget surplus beingachieved for the first time in years. The budget policy and consistently strict monetary policy pursued by the Central Bank of Suriname resulted inthe rate of inflation falling, while the Surinamesedollar remained stable against the US dollar, ourmost important trading currency.

The favourable prices on the world markets for ourmineral exports had a positive effect on the govern-ment’s finances, the balance of payments and themonetary reserve. For the first time in years, therewas a surplus on the current account, while the

monetary reserve rose substantially to reach aninternationally acceptable level of import coverageof close to three months.

Positive trends were also seen in the mining sector,as well as in the building and construction sector, thebanana industry, aquaculture and the dairy and thewater and soft drinks industries. Significant developments were also seen in the services sector,specifically in tourism and telecommunications.Suriname’s National Planning Office is forecastingreal growth of 5.8% in the country’s GDP, and weregard this as realistic.

The national debt also decreased during the year.The improved management of state debt andimproved international debt servicing were two ofthe main reasons why the international ratingagency Standard and Poor’s decided towards the endof the year to increase Suriname’s sovereign creditrating by one notch. This is the first upgrade in thecountry’s rating since Suriname started workingwith the renowned rating agencies in 1999. The rating outlook also changed for the better, from stable to positive and this is often a precursor ofan upgrade. Suriname is seeking to achieve aninvestment-grade rating in the medium term, andwe also regard this as feasible.

The IMF’s Article IV consultation mission, whichconducted its annual examination in early 2007,commented very favourably on the Surinamese policymakers’ performance, which exceeded expectations. It was disappointing on the other handto see the limited extent of progress achieved inPublic Sector Reform, which is of such importancefor the sustainable and balanced development of thecountry. The current favourable developments in themacro-economy mean this PSR programme can,however, succeed. The benefits of the economicgrowth are also not yet sufficiently visible in societyas a whole.

Our bank has benefited from the favourable eco-nomic environment of the year under review. Thecompany policies pursued by the Executive Boardhave also proved successful and translated into goodresults for the year. The main business objectives in

13

REPORT OF THE EXECUTIVE BOARD

2006 were to achieve sustainable growth, improveour profitability and balance sheet, increase our efficiency and reinforce our risk management policies and customer relationships. Other objec-tives included increasing the level of job satisfactionand social corporate citizenship. These objectiveswere largely achieved.

A multi-disciplinary working group was set up during the year to develop a Balanced Score Card(BSC) for the bank as a whole. This card will also beextended in due course to departmental and individual levels, and will be an important tool formonitoring our operational performance.

The Hakrinbank corporate governance code wasintroduced during the year under review and willserve as a basis for the bank’s activities. The Super-visory Board also decided to set up an AuditCommittee and a Remuneration and NominationCommittee during the year. In order to improve corporate governance, we established an independent Risk Management department during2006. The primary aim of this department is to assessand manage risks within the limits set by the bankmanagement and to optimise the balance betweenrisk and return.

Our subsidiary, Nationale Trust- en FinancieringsMaatschappij N.V., also had a reasonable financialyear. Its total assets increased by 28%, while its profit rose by 16%. These growth rates were slightly below budget as a result of a certain element of

saturation in some categories of the consumer credit market and also the increased levels ofcompetition.

The price of Hakrinbank N.V. shares rose by 10% toreach SRD 136 at the 2006 year-end. The cash dividend proposed for the 2006 financial yearamounts to SRD 10 per share of SRD 0.15 nominalvalue. This comprises the normal dividend of SRD 9per share mark the bank’s seventieth anniversary.An interim plus an additional amount of SRD 1 pershare to dividend of SRD 1.40 per share was previously paid in October 2006, which means afinal dividend of SRD 8.60 per share. This corresponds to a dividend percentage of 6,667% anda dividend pay-out ratio of 36.5%. In our view, thisrepresents an attractive return for shareholders andtranslates into a favourable price/earnings ratio.

More information on the economic developments inthe year under review that are relevant to our bank’sperformance can be found elsewhere in this report.This report is more detailed than is customary in thebanking sector because we decided that the limitedavailability of and access to up-to-date statisticalinformation for large parts of the society justifiedour devoting extra attention to these aspects in ourreport. We also discuss various developments withinHakrinbank and Nationale Trust- en FinancieringsMaatschappij in this report, as well as the bank’s financial development and the proposedappropriation of profit.

14

Economic developments in 2006

This section of the annual report discusses variouseconomic developments in 2006 and includes adescription and analysis of the government’sfinances, the national debt, monetary and exchangerate policies, the balance of payments and the monetary reserve, as well as information on developments in the real sector.

Government financesThe National Assembly approved the amended draftgovernment budget for the financial year inSeptember 2006. This was later than originallyplanned because the government, which took officein September 2005, first had to complete the handlingof its Multi-Annual Development Programme, ofwhich the budget of 2006 forms a part. The budgetapproved for the year was as follows:

Expenditure on the current account totalled SRD 1,342.8 million, which was SRD 48.2 million, or3.5%, lower than initially budgeted. This was primarily the result of lower spending on goods andservices.

Actual current expenditure was as follows (in millions of SRD):

Wages and salaries 652.9Goods and services 280.3Subsidies/Government grants 307.9Interest on state debt 101.7

Total current expenditure 1,342.8

Budget for 2006 financial year (in millions of SRD)*

Description Expenditure Income Difference As % of GDP

Current account 1,391.0 1,283.5 (107.5) (2)Capital account 445.9 221.2 (224.7) (4)

Total current and capital account 1,836.9 1,504.7 (332.2) (6)

* Source: Financial Memorandum 2007

15

As the Flash Report for 2006 shows, the actual figures on a cash basis were – as in the previous threeyears – significantly better than initially budgeted.Thanks primarily to higher than forecast direct taxrevenues and dividend payments by state-ownedcompanies (mainly State Oil Company), togetherwith lower than budgeted capital expenditure, thecountry actually recorded a small surplus ofSRD 49.2 million. This can be regarded as quite anachievement.

Income on the current account totalled SRD 1,523million, which was SRD 239.5 million, or 18.7%,higher than budgeted. The total amount can be broken down as follows (in millions of SRD):Direct taxes 563.5Indirect taxes 610.8Non-tax revenues 348.7

Total income 1,523.0

Wages and salaries in 2006 rose by around 30%,which was higher than budgeted. Expenditure onpurchases of goods and services fell from the peakseen around the time of the parliamentary electionsin 2005, while interest payments and subsidies roseby around 5%. Capital expenditure came out substantially lower than budgeted at around SRD 160 million because of the limited capacityavailable for the execution of projects. The deficit onthe capital account totalled SRD 131 million.

Net unforeseen income and expenditure resulted inan overall budget surplus of SRD 49.2 millioninstead of the deficit of SRD 332.2 million that hadbeen budgeted. This surplus was used to repay foreign loans and some of the advances granted bythe Central Bank of Suriname. Previous annualreports consistently referred to the weak structure ofthe government’s finances and the threat that thisrepresented for monetary and financial stability and,

therefore, for the economy as a whole. Calls weremade for a properly planned Public Sector ReformProgramme. It is regrettable therefore that, despitethe good intentions expressed in this respect, nomeaningful steps have yet been taken. And this in anenvironment in which the conditions for success arecertainly present. In other words, the economy is growing and the outlook is favourable. The government’s financial position has clearlyimproved, and there is consequently more scope forfunding restructuring programmes. More attentionneeds therefore to be devoted to programmes of thisnature, which are of such importance for the sustainable development of Suriname.

Developments in state debtThe extent and nature of Suriname’s domestic andforeign state debt are shown below. It should benoted that the definition of state debt used in theState Debt Act differs from the definition widelyused in international circles. According to theSurinamese definition, state debt includes undrawnamounts under committed loan facilities and alsostate guarantees that have not been called, whereasthe international markets do not normally includethese items. It would be sensible, therefore, to consider revising the definition used in the StateDebt Act. Consideration should also be given as towhether the statutory debt ceiling of 60% of GDP is perhaps rather high, given the government’srepayment capacity.

16

Type of lender 31 Dec. 2006*) 31 Dec. 2005 31 Dec. 2004

Domestic debt by lender (x SRD 1000)Owed to the Central Bank of Suriname 326,007 412,760 324,962Owed to banks 206,395 198,710 158,009Owed to private individuals 118,366 82,823 56,219

Total domestic debt 650,768 694,293 539,190

State guarantees 19,540 18,379 16,549Committed loans and guarantees 63,551 89,943 120,411

Total domestic debt including committed loans and guarantees 733,859 802,615 676,150

Foreign debt by lender (x USD 1000)Multilateral lenders 63,672 54,768 55,629Bilateral lenders 319,804 317,052 313,348Commercial lenders 5,077 15,744 13,077

Total foreign debt 388,553 387,564 382,054

State guarantees 922 3,208 9,601Committed loans 101,934 96,557 125,268

Total foreign debt including committed loans 491,409 487,329 516,923

* Provisional figuresSource: Government Debt Management Office

The state debt developed well in 2006, with domestic debt falling by slightly over 6% to SRD 650.8 million, while foreign debt remainedessentially unchanged. The rise in the value of theeuro resulted in an increase in euro-denominateddebt when converted into US dollars.

The foreign debt ratio (i.e. foreign debt as a percentage of GDP) decreased to around 20%,which compares very well to other countries in theregion. The reduction in domestic debt is the resultof repayments of floating-rate loans provided by theCentral Bank of Suriname. There was little change inthe amounts owed to banks because no new treasurypaper was issued. Some of this short-term paper isexpected to be repaid in 2007 because of the state’simproved financial position.

In recent years Suriname has generally compliedwith its repayments commitments to multilateraland commercial lending institutions, and this wasalso the case in 2006. During the year, the bilateralloans from Japan, Germany and Italy were eitherrepaid in full or restructured. Some repayments ofamounts owed to Brazil and the United States are,however, overdue, and these loans need to berestructured as soon as possible. There are someindications that Suriname will be able to count on anelement of debt-forgiveness.

The improved management of state debt and the country’s improved compliance with its international debt repayment commitments weretwo of the main reasons why the international ratingagency Standard and Poor’s decided to increaseSuriname’s creditworthiness by one notch to ‘B’ forinternational creditworthiness and ‘B+’ for domesticloans. Another important aspect is the “positive out-look” in the rating as this is often a precursor of arating upgrade. Assuming the current policies continue, we expect to see a further improvement inSuriname’s credit rating during 2007.

Monetary developmentsThe Central Bank of Suriname relaxed its tight monetary policy to some extent in 2006. At the startof the year, for example, the cash reserve require-ment that has to be held in Surinamese dollars wasreduced from 30% to 27% of the reserve base. Thelatter comprise all the balances held by third partiesin SRD at the country’s banks. This was one of thereasons prompting the commercial banks to cuttheir lending rates by an average of two percentagepoints. The percentage of the compulsory cashreserve that may be used for long-term, low-interesthousing loans was increased from 8% to 9% of thereserve base.

17

2006*) 2005 2004

1. Liquidity created for the state (31.5) 25.4 103.32. Lending to the private sector 58.8 71.5 23.23. Other liquidity created (88.2) (59.9) (64.5)

Total domestic liquidity created (60.9) 37.0 62.0

4. Liquidity from abroad 262.7 57.4 109.5

Total increase in M2 201.8 94.4 171.5

Liquidity ratio (M2 : Nominal GNP market prices) 21.1 18.8 20.1

*) Provisional figures 1) Own estimatesSource: Central Bank of Suriname

1)

The following table shows the changes in the money supply in the Surinamese economy (M2, in millions of SRD):

2.70Jan

Buying

Selling

2.746

2.800

2.750

2.805

2.746

2.800

2.742

2.800

2.747

2.800

2.747

2.800

2.747

2.800

2.747

2.800

2.753

2.800

2.753

2.800

2.750

2.800

2.753

2.800

Feb Mar Apr May June July Aug Sept Okt Nov Dec

2.72

2.74

2.76

2.78

2.80

2.82

USD buying and selling rates in 2006

Domestic M2 liquidity, which is an important measure of the effects of monetary policy, rose in2006 by SRD 201,8 million to SRD 1,082 million.This increase of 22.9% was wholly attributable toinflows from abroad as the net effect of variousdomestic factors was a reduction in the money supply. Gross lending to the real sector added SRD 58.8 million to the money supply, while the government cash surplus reduced it by SRD 31.5 million.

The growth in the money supply resulted in a rise inthe liquidity ratio, which is the domestic M2 measure of liquidity as a percentage of GNP. Thismeasure currently remains just below the long-termaverage of around 25%, which suggests that themonetary and real sectors of the economy are reasonably in equilibrium. It should, however, benoted that the ratio takes no account of the effect ofthe dollarisation of the economy.

The reserve requirements for foreign currenciesremained unchanged in 2006 at 33.3% of the relevant reserve base. Banks are permitted to holdpart of their compulsory cash reserves in high-quality, liquid assets that are likely to generate a reasonable return on investment.

On 2 January 2007, the domestic currency reserverequirement was further reduced from 27% to 25%of the reserve base. This was a responsible move,given the stable macro-economic and monetary

environment. The percentage of the reserve baseallowed to be used for low-interest housing loanswas increased at the same time from 9% to 10%.

The reduction in the SRD cash reserve was one ofthe reasons why the commercial banks were able toreduce their SRD annual lending rates further toaround 12% - 13%. Rates have fallen considerably inrecent years as a result of the falling inflation rate. On1 January 2007, the interest on 6-month Republic ofSuriname treasury paper was also reduced furtherfrom 10% to 8% a year, while the rate charged onadvances by the Central Bank fell to 10% a year.

The monetary policy pursued in 2006 is expected tocontinue in 2007. We are once again, however,forecasting fairly substantial inflows from abroad,and it is important to ensure that these do not resultin inflationary pressure within the country’s domestic economy.

Exchange rateIt was calm on the exchange rate front throughout2006 thanks to the prudent budgetary and monetarypolicies pursued. The inflows of foreign currency(primarily from the mining sector) also contributedto this calmness. Supply and demand on the currency market were clearly in equilibrium at theprevailing pricing levels.

The following chart shows the movements in the US dollar in 2006.

18

As the chart shows, the average USD selling rate in2006 was SRD 2.80, which was less than 1% abovethe Central Bank of Suriname’s target rate and with-in the agreed bands. On 3 April 2006, the CentralBank increased its USD selling rate from SRD 2.77to SRD 2.78.

The euro strengthened significantly against the US dollar during the year in response to variousinternational economic and political developments.Given that the SRD is linked to the USD and consequently floats against the euro, the latter cur-rency became considerably more expensive duringthe year. The Central Bank of Suriname’s selling raterose from SRD 3,298 to the euro at the 2005 year-end to SRD 3,672 at the end of 2006. In other words,an increase of almost 12%.

In view of the policies that the monetary authoritieswill continue to apply and the continuing favorabledevelopments on relevant international markets, weexpect the exchange rate to remain stable in 2007.

Balance of payments The favorable prices in the world markets for ourmost important mineral exports in 2006 resulted ina significant increase of 28% to USD 931.1 million inthe value of our exports. The completion of variouslarge projects in 2005 meant that the mining sectorrequired lower levels of imports in the year underreview, and overall imports consequently rose lessrapidly. This in turn resulted in a trade surplus ofUSD 140.7 million.

The deficit on the services account was substantiallylower than in 2005. The various developmentsreferred to above had a beneficial impact on the current account, with a positive balance ofUSD 94.3 million being achieved for the first time inyears. The movements on the various sub-accountsthat make up the balance of payments resulted in themonetary reserve increasing to USD 258.9 million.The outlook for 2007 is good, which means that thetrend seen in 2006 can be expected to continue.

19

2006*) 2005*) 2004

Goods 140.7 (91.2) 40.5Services (30.7) (147.7) (129.7)Primary incomes (51.6) (40.4) (62.9)Income transfers 35.9 22.1 13.7

Current account 94.3 (257.2) (138.4)Capital account (239.9) 42.3 (13.1)Items still to be classified

1)232.3 231.8 188.6

Net non-monetary sectors 86.7 16.9 37.1

* Provisional figures1) Movements in residents’ foreign currency accounts.Source: Central Bank of Suriname

Balance of payments on cash basis (in millions ofUS dollars)

One of the winners of the colouring competition arrangedto mark the launch of the Anansi savings account comesto collect her prize.

Monetary reserveNet foreign currency assets rose in 2006 by USD 96.3million, or 59.2%, to USD 258.9 million. This translates into around 2.8 months’ coverage ofimports of goods and services.

Despite the significant increase, the monetaryreserve is still slightly below the internationallyaccepted standard of at least three months’ importcoverage. It is also, therefore, below the more conservative norm that includes foreign currencyliabilities repayable within one year. It should,however, be noted that the mining companies operating in Suriname do not use our currency

reserves for their imports. In recent years, importershave also been looking to the exchange bureau inSuriname to meet their needs for foreign currency.The monetary reserve is expected to continue growing in 2007, and this will help reinforce publicconfidence in the external value of the Surinamesedollar.

Year-end

Description 2006*) 2005*) 2004

1. Monetary authoritiesa. Gold reserves 23.0 16.0 8.9b. IMF special drawing rights 1.3 2.0 2.1c. IMF reserve position 9.2 8.8 9.5d. Foreign exchange receivables 235.5 138.4 118.0e. Foreign exchange owed to residents (28.8) (22.5) (22.1)f. Secured foreign exchange obligations (0.6) (0.6) (1.2)

Total 1 239.6 142.1 115.2

2. Currency banksa. Foreign exchange receivables 303.5 242.9 202.5b. Foreign exchange owed to residents (253.7) (211.2) (165.7)c. Foreign exchange owed to non-residents (24.3) (5.3) (4.2)

Total 2 25.5 26.4 32.6

Total 1 +2 265.1 168.5 147.8

3. Amounts owed in SRD to non-residents (6.2) (5.9) (5.6)

Net foreign exchange assets 258.9 162.6 142.2

* Provisional figuresSource: Central Bank of Suriname

Development of the monetary reserve (in millions of USD)

20

Surinamese Stock Exchange

For the Surinamese Stock Exchange, the year 2006was another year of considerable growth, with effective turnover increasing by over 114% to SRD 1.77 million. The highest trading volumes were in Assuria, VSH-United and ConsolidatedIndustries Corporation (C.I.C.) shares, whichaccounted for 42.4%, 22.7% and 11.5% respectivelyof the total equities turnover on the exchange. TheTorarica Hotel’s rights issue also contributed significantly to overall turnover levels, with most ofthis trading resulting from the government’s decision not to exercise its rights.

The most active brokers were DSB Bank, AssuriaBeleggingsmaatschappij and Hakrinbank.

The stock exchange index rose in the year underreview by 296.9 points to 1,480.6. In other words, anincrease of 25%. This rise was well above the rate of

inflation for 2006, which means that the averageinvestment in shares generated a good return in realterms during the year.

Various companies, including Assuria andHakrinbank, converted their shares during the yearand set a new nominal value for them in Surinamesedollars. This exercise resulted in changes in the shareprices.

On 1 January 2006, VSH-United Holding Co. waslaunched on the stock exchange and opened at aninitial price of SRD 21.00 per share of SRD 0.01nominal value.

Fatum Investments was officially admitted to theexchange as a broker in 2006, but did not pursue anyactivities during the year.

Stocks Nom. value Turnover Effective Opening Closing per share (number of turnover price price

shares) Jan. 2006 Dec. 2006

Assuria 0.10 151,604 404,760.40 6.25 11.60C.I.C. 0.01 16,575 110,467.00 6.10 6.80De Surinaamsche Bank 0.025 11,845 99,498.00 7.68 9.00Elgawa 0.01 - - 1.60 1.80Hakrinbank 0.15 3,995 76,409.65 124.00 136.00Margarine & Vettenfabriek 0.01 - - 5.20 5.20Self Reliance 0.01 1,574 13,625.90 9.30 8.60Surinaamse Brouwerij 5.00 - - 51.00 73.00Torarica 0.10 862 33,187.00 27.00 39.00Varossieau 0.10 100 950.00 9.00 9.00VSH-United 0.01 10,333 217,793.00 21.00 21.50

Total shares 196,888 958,690.95

Torarica rights issue 272,856 811,275.50

Total general 469,744 1,769,966.45

Stock market index as at 31 December 2006: 1,480.6Source: Securities Trading Association of Suriname

The following table provides an overview of trade on the Surinamese Stock Exchange in 2006

21

Banking sector in SurinameThe Surinamese banking sector had a good year in2006. This can be seen in the following table,which provides information on various recent developments in the country’s commercial banking sector. Total consolidated assets rose by 26%, while

lending increased by around 23%. Funds availablefor lending were 29% higher than in 2005, whichmeant an increase in the credit availability. The capital ratio I fell slightly, while the capital ratio IIimproved.

22

Year-end 2006*) 2005 2004

Total assets 2,871.0 2,276.6 2,004.5

Funds available for lending and cash/cash equivalentsFunds on current accounts 539.7 443.4 412.4(Compulsory cash reserve) (179.4)6 (179.0)4 171.62

360.3 264.4 240.8

Savings 311.8 252.3 207.8Term deposits 126.5 94.3 76.5Capital and reserves 157.3 131.0 105.7

Total funds available for lending and cash/cash equivalents 955.9 742.0 630.8

Lending and investments 765.55 661.33 496.11

Key ratiosCapital ratio I(capital and reserves as % of total assets) 5.48 5.75 5.27Capital ratio II(capital and reserves as % of lending) 20.55 19.81 21.31

1. Excluding provision for bad and doubtful debts of SRD 25.7 million.2. Excluding cash reserve of SRD 21.5 million for housing loans.3. Excluding provision for bad and doubtful debts of SRD 26.5 million.4. Excluding cash reserve of SRD 51.3 million for housing loans.5. Excluding provisions for bad and doubtful debts of SRD 36.1 million.6. Excluding cash reserve of SRD 76.8 million for housing loans.* Provisional figuresSource: Central Bank of Suriname

Key figures of the general banking sector in Suriname (in millions of SRD)

6) 4) 2)

5) 3) 1)

Previous annual reports discussed the increasing US dollarisation of bank balance sheets and the implications of this in detail. The Central Bank ofSuriname and the commercial banks’ executiveboards have pursued policies aimed at reversing thistrend. The following chart shows the development ofUS dollarisation within the banking sector and thefact that this increased during 2006.

As the chart shows, the share of total depositsdenominated in foreign currencies increased onlymarginally, while the extent to which lending was indollars rose substantially. This development isremarkable, given that the difference between interest rates in SRD and those in foreign currenciesactually decreased during the year under review.Low inflation and the stable exchange rate may,however, have prompted clients to opt for loans inforeign currencies that had lower rates of interest inabsolute terms. In early 2007, the SRD lending ratesfell further, and this could result in the extent ofdollarisation slowing down.

During its Article IV consultation mission in early2007, the IMF concluded that “bank soundness indicators improved in 2006, but non-performingloans and financial (US) dollarisation remain high.”

Consumer price index The following table shows the inflation figures for2002 - 2006 compiled by the General Office ofStatistics. These reflect the changes in the price of afixed, representative basket of 240 consumer goodsand services.

Year Average Year-endinflation (%) inflation (%)

2002 15.5 28.42003 23.0 13.12004 9.1 9.12005 9.5 15.82006 11.3 4.7

1) Extrapolated from figures for January – June 20032) Estimated on the basis of figures for March – December 20043) Provisional figures

As the above table shows, consumer prices rose by an average of 11.3% in 2006, while inflation calculated using the year-end method (i.e. 31 Decem-ber 2006 compared with 31 December 2005) was4.7%. Price changes are recognised more quickly inthe latter method, which means that the rate ofinflation has slowed down. In 2005, it was the rises inenergy and oil prices that pushed inflation up. In2006, however, inflation was driven more by ‘costpush’ (i.e. increases in costs) than ‘demand pull’ (i.e.increases in spending), given the reasonable degreeof equilibrium in the government’s finances and the limited extent of monetary financing. It is

23

US dollarisation in 1996 – 2006 as a percentage of total deposits and lending

1)

3)

2)

0

10

20

30

40

50

60

Foreign currency deposits as % of total deposits held by commercial banks

Foreign currency lending as % of total lending by commercial banks to the private sector

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

interesting to note that inflation has had no effect onthe external value of the Surinamese dollar in recentyears. It consequently remains important to keepcontrol of macro-economic spending and to ensurethat wage and salary increases remain moderate. Wetherefore fully support the public appeal by theGovernor of the Central Bank of Suriname for thetrade unions to adopt a moderate stance on theirwage negotiations so as not to endanger the country’s economic stability.

Under the current system of payroll and income tax,inflation has an impact on tax revenues. In an en-vironment in which the value of money is decliningand with a resultant rise in the nominal tax base,progressive rates of tax lead to an unintentionalincrease in the tax burden. This in turn has implications for the purchasing power of salariedemployees and in results in businesses being subjected to taxes on illusory profits. These consequences can fully justify corrective measuresby the legislator.

Average inflation is expected to fall in 2007, whileyear-end inflation will be slightly lower.

Developments in important production sectorsThe vast majority of developments in the real sectorof the economy in 2006 were positive, specificallythe stable macro-economic environment and thefavourable international climate, which boostedboth production and exports. According to estimates by the National Planning Office, the country achieved real GNP growth of 5.8%, much ofwhich was attributable to the mining, building andconstruction and trading sectors.

The world market prices for our main exports (i.e.alumina, oil and gold) rose substantially during theyear, just as they did in the previous three years.Prices are expected to continue developingfavourably in the near future. These sectors areattracting the interest of investors, particularly fromabroad. And this in turn means we can expect significant levels of investment in the near future.

Substantial investments were also made in other sectors, which means that economic growth can beexpected to remain at a good level in the future.

The bilateral investment protection agreementbetween Suriname and the Netherlands came intoforce in early September 2006. This agreement,

which was signed on 31 March 2005, provides forforeign investors to be treated as national investorsand for investment-related payment transfersabroad to be made in a freely convertible currency,while also giving investors protection against illegalexpropriations of property and allowing disputes tobe submitted to international arbitration. Neither ofthe countries is permitted to amend the agreementunilaterally.

Various important developments in Suriname’smain production and export sectors are discussed indetail below.

Bauxite sectorThe bauxite sector had a significantly better year in2006 than in 2005, when both alumina productionand exports fell by 4%. This was despite the increasein alumina refining capacity to 2.2 million tons ayear. Alumina production in the year under reviewtotalled 2,132,800 metric tons, representing anincrease of 10% on the total for 2005. Exports werealso higher, with an increase of 9.3% to 2,127,200metric tons. The refinery had a very good capacityutilisation rate of almost 97%.

The total value of these exports amounted to USD 642.5 million, representing an increase ofalmost 44%. The price per metric ton rose in 2006 by31.6% to USD 302. Some USD 234.4 million of thetotal exports accrued to Suriname in the form oflocal payments for oil product sales (including theamounts paid to State Oil Company). This was USD 37 million, or 18.7%, higher than in 2005.A total of USD 144.2 million was transferred to StateOil Company, while USD 44.6 million was paid intaxes (approximately USD 2 million less than in2005). Investments in 2006 totalled around USD 150 million. We expect alumina prices to be maintainedin 2007 because of the continuing high levels of demand in the world market and various evelopments on the supply side of the market.

Negotiations are due to start shortly between thegovernment of Suriname and the bauxite companiesBHP-Billiton and Alcoa/Suralco on the oppor-tunities for bauxite mining in the Bakhuys area ofWestern Suriname. The companies have expressedtheir interest in mining bauxite and processing itinto alumina in the Paranam refinery. Surinamewould like to see an integrated bauxite industry inthe west of the country, providing this is technicallyand economically feasible. These negotiations are

24

particularly important for the country, and themomentum to achieve results is excellent. It is crucial, therefore, to ensure a highly competent teamis appointed to conduct the negotiations. It wouldalso seem sensible to consider a range of business models, including some non-traditional ones, inorder to ensure that Suriname’s interests are properly safeguarded.

Oil sectorOur State Oil Company had another year of excel-lent operating results, with record sales and profits.These were primarily due to the rise in world marketprices and the increased levels of production. Grosssales in 2006 came out at USD 263.5 million, whichrepresented an increase of USD 62.2 million, or31%, on the figure for 2005. The average price ofSaramacca crude oil rose from USD 38.57 per barrelin 2005 to USD 46.43 in 2006. Profit before taxtotalled USD 153.1 million and was, therefore, 46%higher than in 2005. A total of USD 106.9 millionwas contributed to the Treasury in the form of taxesand dividends, while the balance of payments wasboosted to the tune of USD 114.7 million.

Total crude oil production for the year amounted to4.8 million barrels, which was around 10% higherthan in 2005. Much of this increase is attributable toimproved results from existing wells, while a total of98 new wells also became operational during theyear.

The oil refinery was able to achieve a high capacityutilisation rate and processed a total of 2.5 millionbarrels of oil into heavy vacuum gas oil, diesel andheating oil and asphalt (bitumen). Most of the production was sold to Suralco.

Over the coming years, State Oil Company will startfocusing also on generating electricity. Its 15 MWelectricity power station at Tout Lui Faut becameoperational in July 2006.

For the first time in the country’s history, Repsol YPFand its partners conducted a three-dimensionalseismic survey of the oil reserves along Suriname’scoastline in 2006. As a result of this survey, the companies decided to drill two exploratory wells.These will be drilled in the first quarter of 2008. TheUSD 100 million contract for this drilling workwas signed with the US company Trans Ocean inOctober 2006. Maersk Oil and Occidental PetroleumInc. also continued their own two-dimensional

seismic survey along the Surinamese coast duringthe year. The international tender round for blocks15, 36 and 37 resulted in a tender being submittedfor each block.

Paradise Oil Company N.V., a wholly owned subsidiary of State Oil Company was established inearly 2006. The intention is to use this subsidiary as a vehicle for participating in joint ventures with third parties and conducting exploratory programmes. The first activity will be to performon-shore explorations in Uitkijk and Coronie in collaboration with the Irish company Tullow Oil.The outlook for our oil industry is very promising.

Gold sectorSuriname’s gold sector continued to develop well in2006, largely thanks to developments in the worldmarket. Investments in explorations were higherthan in 2005, while the trend of rising gold prices onthe world market, which started back in mid-1999,continued throughout the year. The rise between 10March and 12 May 2006 was particularly striking,with an increase from USD 535 to USD 725 per troyounce (= 31.1035 grams). The average gold price onthe London Metal Exchange in the year underreview was USD 603.46 per troy ounce, which was35.7% higher than in 2005.

This rise was primarily the result of the growingpolitical and financial uncertainty in the world andthe concerns about the value of the US dollar in particular, which were prompted by the twinAmerican budget and trade deficit. Investments ingold have traditionally provided a safe haven formoney in times of uncertainty. Demand for gold inemerging economies such as China and India is alsorising sharply in response to the increased scope forindustrial applications and the growth in the countries’ prosperity. These developments will continue to put upward pressure on prices in thenear future.

The largest goldmining company in Suriname,Rosebel Goldmines N.V., which is a subsidiary of theCanadian mining company Cambior Inc., recordedanother set of excellent operating results in 2006,with production of around 300,000 troy ounces(9,400 kg). A detailed exploratory survey resulted inproven reserves rising by 19% to over 3.8 milliontroy ounces (approximately 118,000 kg). This inturn resulted in the Rosebel mine’s remaining economic life being extended by two years to around

25

twelve years. A total of around USD 5.5 million willbe invested in more detailed explorations in 2007.

In November 2006, Cambior Inc. was taken over byIAMGOLD, a listed Canadian company. The acquisition price of almost USD 1.2 billion was over30% above Cambior’s stock market value. Followingthis acquisition, IAMGOLD is now the tenth largestgoldmining company in the world, with annual production of over one million troy ounces fromeight mines in Africa and the Americas.

According to a rough estimate, the gold productionof the many small-scale producers, most of whomare individual pork nokkers, fell to around 10,000kg, with a total value of around USD 180 million.This decrease is primarily attributable to the exhaustion of the richer mining areas, the lowernumbers of new finds and the sharp rise in operating costs.

The largest Surinamese goldmining company,Sarakreek Resource Corporation, also achievedgood operating results, and there are plans toexpand its activities.

The total area of rice fields under cultivation fellslightly during the year. The volumes sown by thelarger growers have been on the low side for someyears, primarily because of the decision by ricegrowers on the left bank of the Nickerie river andStichting Machinale Landbouw (SML) to stop cultivating.A slight increase in sowing was, however,seen among the smaller growers in 2006.

The joint venture partners Alcoa/Suralco LLC andNewmont Mining Corporation, which is the world’s largest goldmining company, continued their intensive explorations near the Nassau mountain inMarowijne district in 2006. The survey has to dateproduced promising results, and these have furtherincreased the chances of mining activities in the area. The company has since announced that it islooking to sign a Memorandum of Understandingwith the Surinamese government on the possibilityof mining these gold deposits.

Agricultural sector

RiceThe developments in the rice sector are very important for the economy, particularly the economy of Nickerie. Farmers and rice-processorshave for many years been facing a wide range ofproblems, mainly of a structural nature, and thesehave had an adverse impact on production. Nothingessentially changed in this respect in 2006.

Various key figures showing the developments in thesector over the past five years can be seen in the following table.

The increase in the average overall production perhectare from 3.6 to 4.5 metric tons of wet paddy wasa positive factor during the year. As a result of thesefactors, paddy production rose by 16% to over198,000 metric tons. Export volumes were 8% higher than in 2005, partly because of the exports ofrice harvested at the end of 2005. Export prices wereslightly higher because of developments on both thesupply and demand sides of the world market.

26

2006*) 2005 2004 2003 2002

Under cultivation (hectares) 44,266 45,563 49,020 54,425 40,050Production of dry paddy (Mt) 198,162 163,955 174,490 193,685 157,105Average production per hectare (Mt) 4.48 3.59 3.56 3.69 3.92Export volumes (USD 1,000) 38,617 35,877 51,830 41,949 71,812Export value (USD 1,000) 10,690 8,913 11,891 9,097 14,175Export price of cargo rice (USD/mt ton) 236 220 190 191 191Export price of white rice (USD/mt ton) 297 301 268 273 286

Source: Ministry of Agriculture, Animal Husbandry and Fisheries* Provisional figures

In both the spring and autumn growing seasons ricefarmers received refunds of diesel duty paid, andthis refund of SRD 112.50 per hectare under cultivation helped to improve the sector’s profitability.

The agreement signed in 2003 between theEuropean Commission and the Cariforum in support of the rice sectors in the Cariforum countries resulted in € 9,255,000 being made available for Suriname’s rice sector. This will be usedas follows:

1. Technical assistance € 1,815,0002. Training € 140,0003. Restructuring of water facilities € 3,800,0004. Lending facilities € 3,500,000

The lending facilities will be made available viaLandbouwbank N.V.

A programme has been established to improve thesector’s quality and reduce the cost price. This programme, which will run until 2010, started beingimplemented in early 2007. The aim of this and various other restructuring programmes, which arestill to be arranged, is to return the whole rice sectorto the strong position it enjoyed in the past.

Banana industryThe European Union’s trade policy on bananaimports improved significantly in 2006, thanks inpart to the relevant authorities’ willingness to listento Suriname. The principle of ‘First Come, FirstServed’ applied to 81% of the EU’s import quota of 775,000 tons for the ACP countries in 2006,which meant in effect that Suriname had to purchaselicences for or pay import duties on 19% ofits exports. This cost the country a total of around3 million. The outlook for further improvements in2007 and subsequent years is good. A total of 46,368tons of bananas, with an FOB value of USD 14 mil-lion, were exported in 2006, compared with 39,472tons and an FOB value of USD 12 million in 2005.

At the end of the year under review, SBBS had a totalof 1,925 employees and also indirectly providedwork to many other companies on the supply side inthe sector.

Preparations to privatise Surland N.V. started inJanuary 2003, while the process itself started in 2005in the form of an open international bidding round.

This involved drawing up a short list of investors,identified through market research. Unfortunatelythe uncertainties surrounding the European Union’spolicy for this market meant that none of thesepotential investors submitted a bid. Since then,however, a cooperation agreement has been signedwith the French Agrisol/Katope group, and it hasbeen decided to restart the privatisation process in 2008.

Palm oil productionAfter a long period of preparations, the ChineseChina Zhong Heng Tai consortium provided theSurinamese government with the required bankguarantee of USD 16 million in mid-2006, and thismeant that the large-scale production of palm oil atPatamacca in the Marowijne district could begin.

The business plan assumes that a total area of400 km2 will in due course be cultivated, with ultimate production of 700,000 tons of palm oil ayear. The total investments over a 10-year period will be around USD 116 million. The start ofproduction has unfortunately been delayed as aresult of concerns among the local population aboutthe possible effects on their surroundings. They areworried about an inflow of Chinese workers working for low wages and also about the impactthat the plantations may have on the local population’s land rights. We hope that the problemswill be able to be resolved through dialogue sincethis project is very important for the development ofEastern Suriname, now that the bauxite industrythere will soon come to an end.

AquacultureIn mid-2006 Suraq N.V. started creating a modernshrimp-farming business in Nickerie. The land hasnow been cleared and the issue of drainageaddressed. Cultivation ponds started being constructed in early 2007, while the rest of the workwill be completed in the second half of the year. Thebusiness will involve total investments of aroundUSD 17 million and will be farming black tigerprawns, all of which will be for export. This nvestment is very important for the development ofthe Nickerie economy.

Outlook for 2007The macro-economic outlook for 2007 is promising.The IMF concluded during its country review inearly 2007 that “the macro-economic outlook for2007 is broadly favourable. Confidence is expected

27

to remain strong, aided by continued favourable external conditions and the commitment to a stableexchange rate and low inflation. Against this back-ground, real GDP is projected to expand by 5 - 51/2

per cent, driven mainly by the non-mining sector, while inflation would stay in the range of3 - 6 per cent. The external current account surpluscould fall to about 2 percent of GDP.”

The government will need to ensure a balancedbudget if it is to achieve these objectives. In thelonger term, a successful Public Sector Reform(PSR) programme must be executed to maintainand increase financial stability and to promoteeconomic growth.We believe that the favourable outlook provides theright conditions for a successful PSR programme. Itis also important in this respect to improve themacro economic monitoring of the country’s economy and to strengthen key institutions so as toimprove the overall quality of public governance.

Important negotiations will be held with variousmultinationals in 2007 on using our naturalresources. The challenge is to devise a businessmodel that will be acceptable to all stakeholders andwill benefit the country as a whole. We will need toensure that sufficient amounts are invested in ournegotiating position.

The Caricom single market was officially launchedin January 2006, and the intention is to create a single economy by 2009. This far-reaching processof regional integration will have significant consequences for the investment climate andSuriname’s business sector, and our strategic planning will have to take this into account.

We firmly believe that Suriname is well positionedto achieve further accelerated and sustainable development, but we will have to ensure that weadopt the right stance and approach.

28

One of the events held to mark our bank’s 70th anniversarywas a bicycle trip to White Beach.

IntroductionExcellent operating results were once again recordedin the year under review. The bank continued togrow and its operating returns improved. We also continued to give priority to improving our governance structures and to ensuring that ouroperating processes are properly and effectivelymanaged. Risk management is increasingly becoming a common thread in this respect.Management is based on task-setting budgets, withobjectives being quantified wherever possible. Theseobjectives are recorded in the annual plan, which ispart of the bank’s strategic plan. It is pleasing to note that the business objectives set for 2006 werecomfortably achieved, and that the strategic objectives will consequently not need to be revised.Considerable energy will be devoted in 2007 topreparing a new strategic plan for the coming years.

Our main business objectives for 2006 were toachieve sustainable growth, to improve profitabilityand assets and liabilities management, to increase productivity and to improve risk management andcustomer relationships management. Other impor-tant objectives included achieving an increase in thelevels of employee satisfaction and demonstrating aclear commitment to the community of which weare a part by actively sponsoring various communi-ty projects.

Total consolidated assets rose by 28.6% to SRD 606.5 million in 2006, which is a higherincrease than in 2005. Consolidated lending rose by33.4%, which was over 3.4 percentage points abovethe budget. The extent of US dollarisation in thelending portfolio increased slightly, but remainedwithin the short-term target. The ratio of non-performing loans continued falling to 2%, which isalso satisfactory from an international perspective.Hakrinbank’s share of the country’s lending marketincreased slightly.

The bank’s assets and liabilities managementimproved in comparison to 2006 and also whencompared with local benchmarks. This in turn had apositive effect on operating results, with the profitbefore tax rising by 50.6% to SRD 19.95 million.

One of the bank’s main operational objectives in2006 was to improve overall productivity by achieving a better efficiency ratio. This ratioimproved from 59% to 56% during the year, and wewill strive to achieve further improvements in thefuture. In addition, the return on assets increasedfrom 1.95% to 2.37%, while the return on equityrose from 46.10% to 46.90%. During the year underreview, the bank’s corporate governance code wasapproved and is now being used as the basis for ouractivities. This code, the contents of which can beviewed on our website, sets out a series of principlesand rules for proper corporate governance. We officially presented the code to the President of theRepublic of Suriname in May 2006, when we alsotook the opportunity to call for a national corporate governance code to be compiled and implemented.

Compliance – in other words, seeking to promotethe bank’s reputation for integrity, together with thatof its management and employees, as a means ofmanaging risks and preventing damage to our reputation by adherence to strict rules of conduct –is a high priority within our bank. We also have anintegrity code, which all our employees have signed.

During the year under review we arranged Anti-Money-Laundering (AML) courses for our staff andalso worked on a compliance handbook, whichincludes a manual on anti-money-laundering.We alsoinvested in AML software, which will be installed in2007.

Almost all transactions performed by a financialinstitution involve an element of risk. Effective risk management is consequently crucial for the successof any bank, which is why we attach such a high priority to it within our organisation. The primaryobjectives of risk management is to assess and managerisks within the limits set by the bank. It is also important to ensure a balance between risk and return.

During the year under review we set up a separateRisk Management department and appointed amanager to run it. The aim in due course is to bringall the bank’s risk management activities within thescope of this department. The department’s mainactivities in 2006 involved formalising and tightening up the bank’s credit risk policy and performing credit risk assessments. In due course,responsibility for monitoring and managing otherrisks, such as market, liquidity and operational risks,will be assigned to this department.

29

Business of the bank

Managing customer relationships is of fundamentalimportance to a bank as no bank can survive with-out satisfied clients. We consequently strive to provide the highest quality of professional servicesto our customers, with their needs and wishes running as a common thread through our activities.

In the year under review we once again spent timetraining our employees in customer relations management and communication skills. We alsosimplified our procedures for dealing with customercomplaints and made the process more accessible.Our policy is to treat all complaints seriouslybecause they arise as a result of concerned but loyalclients drawing our attention to possible imperfec-tions in our services and giving us the opportunityto take corrective action.

Our preparations to establish a full-service marketing department continued in 2006. Thisdepartment will become operational in early 2007,and we will also be appointing a manager to run it.

Over the past few years we have made donations andprovided sponsoring as a way of demonstrating ourcommitment to the community of which we are a

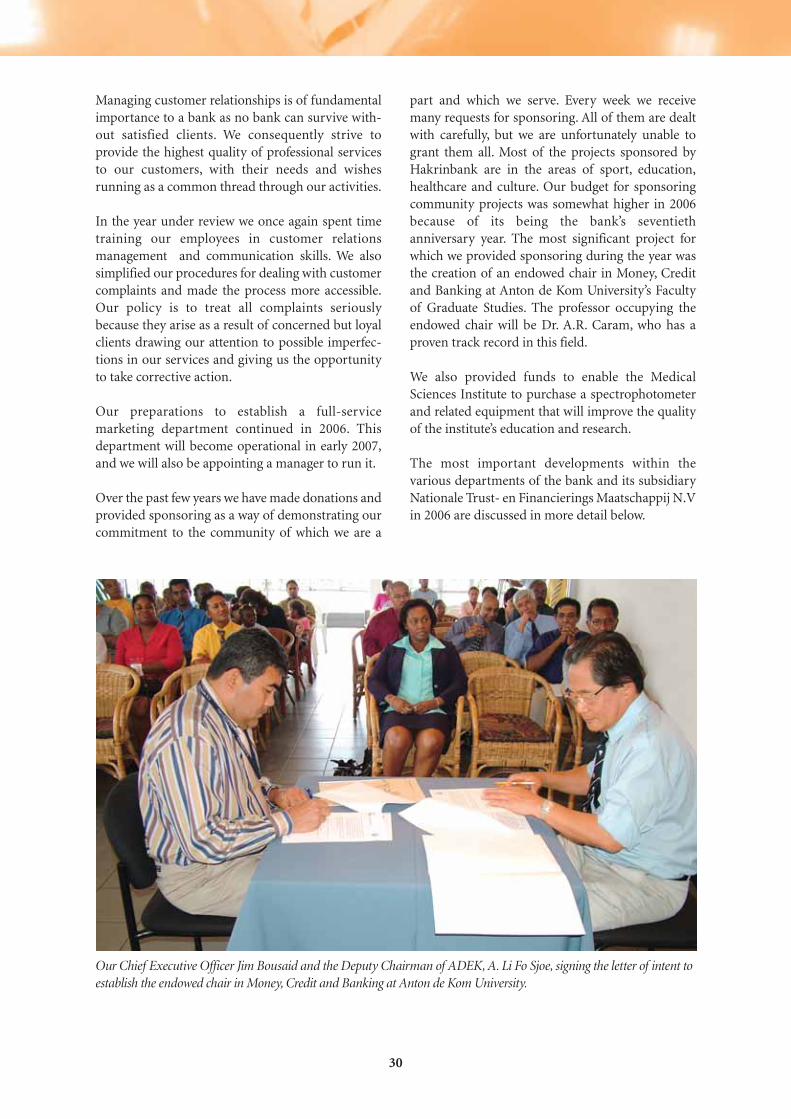

part and which we serve. Every week we receivemany requests for sponsoring. All of them are dealtwith carefully, but we are unfortunately unable togrant them all. Most of the projects sponsored byHakrinbank are in the areas of sport, education,healthcare and culture. Our budget for sponsoringcommunity projects was somewhat higher in 2006because of its being the bank’s seventieth anniversary year. The most significant project forwhich we provided sponsoring during the year wasthe creation of an endowed chair in Money, Creditand Banking at Anton de Kom University’s Facultyof Graduate Studies. The professor occupying theendowed chair will be Dr. A.R. Caram, who has aproven track record in this field.

We also provided funds to enable the MedicalSciences Institute to purchase a spectrophotometerand related equipment that will improve the qualityof the institute’s education and research.

The most important developments within the various departments of the bank and its subsidiaryNationale Trust- en Financierings Maatschappij N.Vin 2006 are discussed in more detail below.

30

Our Chief Executive Officer Jim Bousaid and the Deputy Chairman of ADEK, A. Li Fo Sjoe, signing the letter of intent toestablish the endowed chair in Money, Credit and Banking at Anton de Kom University.

Corporate GovernanceBanks were not involved in the major accountingscandals that affected various well-known listedcompanies in the United States and Europe around2002 and caused major financial losses. The fact thatthese scandals could occur is attributable to failuresof corporate governance. In other words, the way inwhich companies are managed.

Proper corporate governance is particularly important for banks, given that they play such amajor role in economic stability and development.This means that, here in particular, good checks andbalances, together with proper and effective internalcontrol of processes, are essential. Effective governance is a precondition for retaining publicconfidence. Given its importance, it is not onlyregulators, parties operating in the market and otherstakeholder organisations that are continually seeking to set new standards for ensuring propercorporate governance. Institutions themselves arealso increasingly accepting that they have a role toplay in this process. And Hakrinbank is no exception in this respect as we are continually striving to apply best practices in our corporate governance so that we improve our operating performance and increase our accountability.