olympic entertainment group

TRANSCRIPT

Olympic Entertainment Group Investor update

October 2009

2

Presenting the CompanyArmin Karu, Chairman of Board of Olympic Entertainment Group (OEG) Founder and Chief Executive Officer since 1993 Bachelor’s and MBA degree from Haaga Institute in Finland Indirectly owns 47,39% of the Company

Indrek Jürgenson, Member of Management Board of OEG Joined OEG in 2003 as Chief Information Officer, Member of Management Board since 2009,

resposible for the day-to-day management of OEG Bachelor’s degree from Tallinn University in Physics Previous work experience in Estonian Telephone Company in 1996-2001 (administrator, product

manager, project manager, head of GIS sector), Eurofone – London in 2001-2003 (branch manager)

Kristi Ojakäär, Member of Management Board of OEG Joined OEG in 2005, CFO since 2007, Member of Management Board since 2009 Bachelor’s degree from Tallinn University of Technology Previous work experience in real estate and investment companies

2

3

Table of Contents• Introduction of Olympic Entertainment Group• Business Model• Operations by Markets• OEG Operations in 2004-2008• Main directions in 2009• Future plans

3

4

Introduction of Olympic Entertainment Group

5

Company History

1993 Company founded by current Chairman of the Supervisory Board Armin Karu

1997 Re-opening of flagship Reval Park Casino in Tallinn, the biggest casino in Estonia

1998 Estonian operations ISO certified

2002 First casino opened in Lithuania; acquisition of Casino Daugava, a Latvian operator

2004 Continuous expansion in Baltics, operations launched in Ukraine

2005 Acquisition of Baltic Gaming A/S, the second largest casino operator in Latvia

2006 Expansion to Belarus; Polish market entry pending regulatory approval

Opening of flagship Olympic Voodoo Casino in Riga, the biggest casino in Baltics

2007 Expansion to Poland and Romania through the acquisition of local operators

Opening of the flagship casino in Poland - Olympic Casino Sunrise in Warsaw Hilton

Acquisitions in Estonia and Ukraine

2008 Gaming activity license was obtained in Slovakia; casino opened June 19th, 2008, new casinos in other countries

2009 Opening of the flagship casino Bora-Bora in Bucharest, launch of the new casino lounge concept

5

6

OEG in Brief• Fastest growing gaming operator in Central and Eastern Europe

– Currently operating in seven countries

– OEG is the market leader in Estonia and Lithuania, currently 2nd in Latvia

– In 2007 OEG entered the markets of Poland, Romania and Slovakia

– Target markets have combined population of over 100m

• Publicly listed company

– Listed on the Tallinn Stock Exchange since October 2006

– Listed on the Warsaw Stock Exchange since September 2007

• Leading role in consolidation of current markets

– Acquisitions throughout CEE

• Expansion to new markets

– In 2007 we acquired local operators in Poland and Romania

– The subsidiary founded in Slovakia opened first casino in June 2008

6

7

Key Figures2008

• Revenue EUR 179.3m (2007: EUR 160.9m)• EBIT EUR -12.4 m (2007: EUR 27.6m)• Net profit EUR -29.1m (2007: 24.3m)• Operations in the Baltic States, Ukraine, Belarus,

Poland, Romania, Slovakia• Operating venues: 133 (2007: 122)• Total 218 tables (2007: 202) and 5301 slot

machines (2007: 4690)• Personnel: 3,924 (2007: 4,004)

• Revenue growth 08-07 11,5%• EBIT growth 08-07 -145%• Net profit growth 08-07 -219,4%

2009 H1 (continued operations)

• Revenue EUR 55.2m (2008 H1: EUR 79.5m)• EBIT EUR -9.0m (2008 H1: EUR 6.7m)• Net profit EUR -9.0m (2008 H1: EUR 6.4m)• Operations in Baltic States, Belarus, Poland,

Romania, andSlovakia• Operating venues: 86 (30.06.2008:130)• Total 209 tables and 3 037 slot machines • Personnel: 2 689

7

Business Model

9

• Differentiation from competitors through quality

– High standards (Baltic operations ISO 9001:2000 certified)

– Extensive investment in personnel training

– Advanced IT-systems (EZ-Pay system – reduces cash operations, EndX – table games management and

customer bonus programme, CasinoLink – slots management, jackpots, customer bonus programme)

– Effective marketing

– Outstanding reputation

– Long-term supplier relations

• Experienced and well-motivated management team

– Proven track record in international expansion

– Combines centralised Group-level resources and local executive teams

– Chairman of the Board is the largest shareholder

• Customer prospects

– Safe venues in prime locations

– A variety of entertainment events (non-gaming events, poker rooms etc.)– High-quality service, up-to-date games – Well-developed support functions (e.g. bars)– Well-functioning customer loyalty programme

9

Key Success Factors

10

Group Structure (September 2009)

10

OÜ Hansa Assets (47,39%) OÜ Hendaya Invest (19,93%) Free float (32,68%)

Olympic Entertainment Group AS

Olympic Casino Eesti AS (95%)

Olympic Casino Latvia SIA

Olympic Casino Baltija UAB

Olympic Casino Bel IP (Belarus)

Silber Investments & Baina Investments (Poland)

Casino-Polonia Wroclaw Sp.Z.o.o. (80%)

Olympic Casino Bucharest S.r.l.

Olympic Entertainment Slovakia S.r.o

Kungla Investeeringu AS

(Hotel/bar services in Estonia)

Ahti SIA

(Bar services in Latvia)

Mecom Grupp UAB

(Bar services in Lithuania)

Muntenia Food Beverage S.r.l

(Bar services in Romania)

Holding and dormant companies or companies to be liquidated or sold:

Nordic Gaming AS, OÜ Kasiino.ee Fortuna Travel OÜ

OLympic F&B S.r.o

(Bar services in Slovakia)

Kesklinna Hotelli OÜ (97.5%) (Hotel services )

Olympic Exchange S.r.l. (currency exchange in Romania)

Operations by Markets

Overall Trends• Central and Eastern European gaming markets are in the process of consolidation

– Several current players are unable or uninterested to develop operations in terms of quantity and quality

– Favourable ground for rapid expansion by takeovers

– Economic pressures evident in most of the markets

• Legislation is being streamlined in several countries

– Quality of OEG casinos complies with all new requirements everywhere

– Activities of operators become more transparent, which is useful for sector reputation

– Due to presence in many countries, changes in one specific market do not have a major impact on

operations of OEG

12

Estonian Gaming Market

• GGR of Estonian gaming market 2003-2009 H1

• EUR, m 2003 2004 2005 2006 2007 2008 2009 H1

• GGR 63.8 62.5 74.3 106.1 121.6 101.1 24.4

• Annual change % -3.8% -2.0% 18.9% 42.8% 14.6% -16.9% -55.5%

• 11 operators active on Estonian gaming market operating a total of 80 gaming establishments with ca 50 gaming tables and ca 2,000 slots

• Stricter regulation and increasing standards of living contribute to the success of the best equipped and positioned casinos. This shift towards higher quality of gaming services is expected to continue

• About 90% of all gaming revenues stem from slot machines, ca 10% from table games• New gambling legislation (2009) may contribute to further market consolidation• New gambling legislation (2009) also regulates remote gaming principles• Regulatory environment

– Minimum mandatory share capital EEK 15,65m (EUR 1m) (latest 01.01.2015 or earlier, if operating licence expires before this date)

– Legislation changed in 2009

13

Competitive Situation in Estonia

• OEG clear market leader (47% of revenues, 2009 H1)- 23 casinos - 19 gaming tables- 674 slot machines

• Spring 2007: acquisition of Kristiine Kasiino that controlled 7% of the market- Transaction amount: 16 million EUR- Current status: Kristiine Kasiino has been integrated into the operations of OEG

• Closest competitor Grand Prix (IMG Kasiinod) has 9% market share. Combined market share of 4

biggest competitors is ca 30%

• OEG operates the largest casino in Estonia – Reval Park Hotel & Casino, offering slot and table

games and poker events

• Many competitors have focused on number of venues instead of location quality, resulting in poorer image and profitability

14

Latvian Gaming Market

• GGR of Latvian gaming market 2003-2008

• EUR, m 2003 2004 2005 2006 2007 2008 2009 H1

• GGR 73.0 98.7 139.5 204.5 279.7 172.7 57.5

• Annual growth % 29.4% 35.2% 41.3% 46.6% 36.8% -38.3% -34.6%

• 19 operators active on Latvian gaming market operating a total of 381 gaming establishments with ca 114 gaming tables and ca 9,587 slots

• Market characterized by relatively wide range of legalized gaming services incl. sports betting, bingo, telephone games, lotteries and online games of chance

• Industry is concentrated in the larger towns of Latvia, especially in capital Riga• About 90% of all gaming revenues stem from slot machines, 10% from table games • The recent considerable increase in Latvian GGR may partly be attributed to increased transparency in the

industry. It may be assumed that most of the overall gaming revenues are now properly accounted for, thus GGR growth is expected to normalize

• Minimum share capital requirement LVL 1m (ca EUR 1.4m) (from 2007) • License is also required for each casino, which requires the consent of local municipality

15

Competitive Situation in Latvia• OEG has 2nd position on the market (14% of revenues, 2009 H1)

- 26 casinos- 25 gaming tables- 740 slot machines

• Majority of gaming operators are held by private individuals and lack the administrative and financial resources to expand their business

• Majority of gaming operators prioritize the number of venues over the quality of service

• OEG operates the largest casino in Latvia (and Baltics) – Olympic Voodoo Casino in Reval Hotel Latvija

16

Lithuanian Gaming Market• GGR of Lithuanian gaming market 2003-2009 H1

• EUR, m 2003 2004 2005 2006 2007 2008 2009 H1

• GGR (A-kat) 11.4 20.7 29.5 40.8 52.5 46.2 15.4

• Annual growth % 199.6% 81.2% 42.4% 42.4% 28.7% -12% -38%

• 8 operators active on Lithuanian gaming market operating a total of 26 gaming establishments with ca 184 gaming tables and ca 1090 slots (A-kat). 6 operators active on Lithuanian gaming market from 2009 Q3, total of 21 gaming establishments with ca 132 gaming tables and ca 774 slots (A-kat).

• Gaming legislation is often ambiguous resulting in the regulator frequently referring cases to the judicial system. Legislation is expected to become more consistent and precise over the coming years, which is believed to benefit operators offering a higher quality of gaming services

• GGR growth is eventually likely to slow down as the market matures. However, Lithuanian GGR per capita of EUR 8.2 (2005) is significantly lower than that of Estonia (EUR 55.0) and Latvia (EUR 61.2)

• Minimum share capital requirement LTL 4m (ca EUR 1.1m) • Casino operators must retain certain minimum amounts, which secure disbursement of winnings • Management is personally responsible for administrative compliance• Strict legislation constitutes an effective entry barrier for new competitors• Taxes increased since 01.01.2009 (incl.: Gaming taxes : A slots + 33%; B slots +50%; tables +50%; VAT +1%,

additional VAT from September 2009 +2%) etc.

17

Competitive Situation in Lithuania• OEG clear market leader (60.1 % of revenues, 2009 H1)

- 15 casinos (10 A cat & 5B cat)- 74 gaming tables- 547 slot machines

• OEG entered the B category market in 2007 (slot machines with limited bets and winnings)

• Strict legislation constitutes an effective entry barrier for new competitors

• OEG operates the largest casino in Lithuania in Reval Hotel Lietuva

18

Belarus Gaming Market• Significantly underdeveloped market with excellent growth potential

• Vast majority of operators are single-venue companies. The quality of gaming services offered by existing casinos is mostly sub-standard

• Market is under-regulated when compared to the Baltic States and most gaming activities are permitted with little or no restrictions. No reliable information on the actual volume of the Belarusian gaming market is currently available

• High political and business risk associated with Belarus has so far inhibited growth in all sectors of economy, including gaming services. Belarusian gaming market is heavily influenced by legislative uncertainty and inefficient administration

– License can be obtained only after the casino is fully equipped and ready for business– No requirements for minimum number of gaming devices per casino

19

Competitive Situation in Belarus• Significant growth in revenues 2009 H1 (60% up on a year ago)

• Oprerates today 5 casinos

• OEG operates a total of 261 slot machines

• Biggest operators like Princess, Admiral and Kolumbus operate maximum 4 casinos, majority of them slots only, ca 15 casinos in Minsk

• Many competitors focus on a small segment of high-end customers (high entrance fees)

• OEG intends to introduce high standards of service while targeting a clientele with average and above-average income

• Olympic Casino has been awarded the best casino enterprise in Belarus

22

Polish Gaming Market• Highly regulated market with limited access

• Because of limited access, underdeveloped market with weak competition

• Highest taxation rate in the current markets of OEG: 45% of gross gaming revenue

• Growth potential: high

• Casino market in Poland is regulated by licence system

• The number of licences in the given city is restricted and determined in accordance to the number of inhabitants (for example, in Warsaw 7 casinos can be licensed, while in Krakow max.3)

• The licence determines the number of tables and slot machines in each casino

21

Competitive Situation in Poland• Successful entry to the market in the first half of 2007

• Acquisition of Casino Polonia, the third largest operator- Transaction amount 9m EUR

• OEG operates today 9 casinos- 67 gaming tables- 415 slot machines- ca 23% of OEG gaming revenues

• In June 2007 OEG opened Poland’s largest casino in Warsaw in the newly-opened Hilton Hotel• In 2008, OEG has opened 2 new casinos – casino in Kielce and Janki. • In 2009 2 new casinos were opened (instead of 2 old ones) – Wroclaw Polonia & Gorzow Mostowa.• 3 main competitors : Casinos Poland with 7 casinos and 1 slot hall, Orbis Casino with 9 casinos and 4 slot halls,

ZPR with 4 casinos and 125 slot halls.

22

Competitive Situation in Romania• Unregulated market

• Large number of small operators

• Overall quality level is low

• Growth potential: high

• Acquisition of a local operator Empire International Game World in April 2007– Gateway to market– Transaction amount 3,85 m EUR– 8 slot casinos operated by OEG at end of June– New exclusive Casino Bora Bora opened in May 2009

• There are 900 locations with slot and almost 23 000 machines in Bucharest

• 7 bigger competitors : Grand Casino ( 4 locations), Platinum Casino, Queen Casino ( 2 locations), Casino Bucharest International, Casino Mirage, Casino Palace, Princess Casino ( 4 locations).

23

Slovakian Gaming Market• GGR of Slovakian gaming market 2005-2007

EUR, m 2005 2006 2007 2008 2009 H1

GGR 263 302 331 410 174Annual growth % 20.2% 9.6% 23.9% -15.0%

• Strict legislation constitutes an effective entry barrier for new competitors

• In addition to OEG, 2 operators active on Slovakian gaming market operating a total of 48 gaming tables and ca 80 slot machines

• Minimum share capital requirement SKK 50m (EUR 1.5m)

• Security deposit for each casino operation SKK 15m (EUR 0.45m)

• No limitations on Jackpots, maximum bets or maximum winnings

• 1st Olympic Casino opened June 19th, 2008

– Largest casino in Slovakia

– Radisson SAS Carlton in Bratislava

– 1000m2, 12 gaming tables, 61 slot machines

– Total investment EUR 5m

• 2nd Olympic Casino (Trnava) opened in 2009 Q1

– Shopping Park Arkadia

– 650m2, 8 gaming tables, 34 slot machines

24

Situation in Ukraine• Ukrainian parliament issued an “Ukrainian gaming activities suspension” law on May 15th 2009, which entered

into force since the moment of publication on June 25th

• The law cancelled all licenses issued to casino operators and terminated all casino activities in Ukraine for unknown period of time

• OEG’s Ukrainain subsidiaries Olympic casino Ukraine TOV, Ukraine Leisure Company and Eldorado leisure Company have submitted a bunkruptcy petition as a step of the liquidation process of OEG’s activities in Ukraine

• OEG has demanded investment compensation from the Ukrainian state based on investments propitation and mutual protection agreement signed between Estonian and Ukrainan governments

25

OEG Operations 2004-2009 H1

Rapid Growth Factors 2007 and 2008• Acquisitions 2007

– Kristiine Kasiino (Estonia) 16.0 mEUR– Empire International Game World (Romania) 3.85mEUR– Casino Polonia (Poland) 9.0 mEUR– Eldorado (Ukraine) 9.3 mEUR– Based on the results of the financial due diligence OEG decided on 18 January 2008 not to acquire AS

Admirāļu Klubs under the terms and conditions provided in the preliminary agreement

• Investments in opening new casinos and upgrading of existing casinos in 2007 and 2008– 18 new casinos opened in 2007 and 21 new casinos during 2008– 23 rebranded/renovated (incl 2 relocated casinos) in 2007 and 15 rebranded in 2008– Total investments 2007 ~ 92 mEUR– Total investments in 2008 ~ 51 mEUR

27

Investments 2004 – 2009 H1 (M EUR)

28

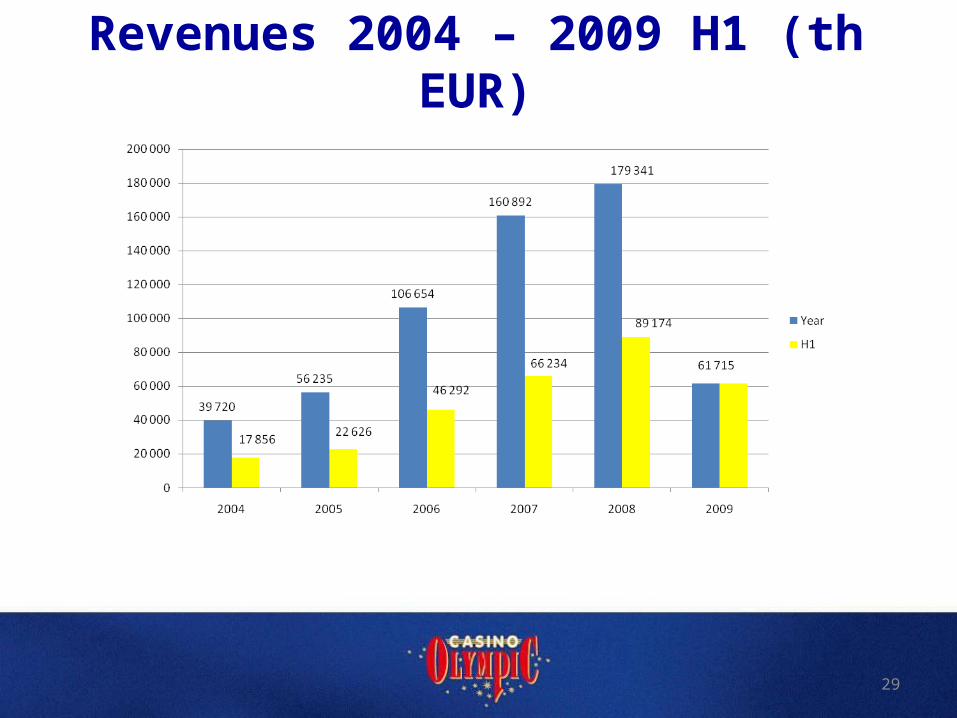

Revenues 2004 – 2009 H1 (th EUR)

29

Revenues by Markets 2004–2009 H1(M EUR)

30

25,7

3,7

10,4

29,8

7,8

16,7

2,0

42,9

32,7

24,9

6,1

0,1

55,5

44,3

30,1

12,0

0,8

17,3

1,1

47,4

41,9

26,5

21,6

2,2

35,1

2,5 2,1

12,0 12,010,1

6,5

1,3

14,4

1,93,4

0,0

10,0

20,0

30,0

40,0

50,0

60,0

Estonia Latvia Lithuania Ukraine Belarus Poland Romania Slovakia

2004

2005

2006

2007

2008

2009 H1

Key Milestones for 2009

Main directions in 2009• The objective of OEG is to continually adapt to rapidly changing market situation,

raising the market share and improving the efficiency in core activity• In spite of negative developments on markets, in the 2nd quarter of the year the level

of consolidated revenues has stabilized after significant decline during the first 2 months of 2009

• By Q2 2009 OEG launched its new concept of casino lounges to target new client groups - more space in casinos, wider possibilities to spend leisure time also for those not wanting to play casino games, a wider food and cocktail menues in casino bars

• In the light of the market situation and the aim of implementing a new concept of casino lounges OEG has reduced the number of slot machines in most of its casinos in 2009, resulting in significant decrease in fixed costs related to the gaming tax

32

Main directions in 2009 (continued)• Already during 2008 OEG implemented an extensive efficiency program in order to

adapt its operations to changing market situation. 10 casinos with negative cash flows were closed.

• In 2009, 43 more casinos have been closed (excluding 24 casinos in Ukraine). The number of employees reduced since 2008 Q1 totals 1 132 positions or ca 26% (excluding Ukraine).

• The positive influence on the cost structure of OEG since the second quarter of 2009 appeared as agreements of reducing the rental prices on average 30% have been concluded

• The total cost effect of optimisation activities implemented within the last year and first quarter of the current year is expected to be 45.1 million euros, constituting 23.7% of the year 2008 total operating expenses

33

Future activities• OEG is entering the online gaming market and will open its first online casino at the

beginning of 2010• For providing online services, OEG has signed a parntership agreement with

Playtech, the world’s leading developer of online gaming technology• OEG will start by offering online gaming on the markets where it currently has

operations• The main competitive advantages:

– Extensive experience as a casino operator

– In-depth know-how of its markets

– Possibility to create synergy between company’s regular casinos and online casinos

• The Estonian market of online gaming services will be clearly regulated from 1 January 2010 when several provisions of the Estonian Gaming Act on offering online gaming servies enter into force

34

Thank you!