of prime lending rate of different exim banks under export ... · “analysis of prime lending rate...

TRANSCRIPT

Page | i

Summer Internship Report

on

“ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS

UNDER EXPORT CREDIT AND PREPARATION OF FINANCIAL MODEL FOR 1MW

SOLAR PV PLANT FINANCED FROM DIFFERENT COUNTRIES”

VISWA SURYA ENERGY SOLUTIONS, Andhra Pradesh

Under the Guidance of

Mr. Alladi Raghavendra

Managing Partner

Viswa Surya Energy Solutions

Submitted by : Eshan Singh

MBA (Power Management)

Roll No. : 30

(Under the Ministry of Power, Govt. of India)

Affiliated to

MAHARSHI DAYANAND UNIVERSITY, ROHTAK

September- 2013

Page | ii

DECLARATION

I, Eshan Singh, Roll No 30/ Semester III/ Class of 2012-14 student of MBA (POWER

MANAGEMENT) at National Power Training Institute, Faridabad hereby declare that the

Summer Training Report entitled – “ANALYSIS OF PRIME LENDING RATE OF

DIFFERENT EXIM BANKS UNDER EXPORT CREDIT” is an original work and the same

has not been submitted to any other Institute for the award of any other degree.

A Seminar presentation of the Training Report was made on _______________

_____________________ and the suggestions as approved by the faculty were duly

incorporated.

Presentation In charge Signature of the Candidate

(Faculty)

Countersigned

Director/Principal of the Institute

Page | iii

ACKNOWLEDGMENT

At the outset, I am highly obliged to Mr. S.K Chaudhary, Principal Director (CAMPS)

NPTI, Mrs. Manju Mam, Director NPTI, and Mrs. Indu Maheshwari, Deputy

Director NPTI, who gave me the opportunity to do summer internship in an rapidly growing

company like Viswa Surya Energy Solutions. I would again like to thank my internal Guide

Dr. Rohit Verma, for helping me and guiding me throughout my project.

I thank my Project Convener Mr. Alladi Raghavendra, Managing Partner, Viswa Surya

Energy Solutions, for giving me the opportunity to work on such an insightful project.

I would like to extend my thanks to my Project Guide, Mr. Ankit Singh, Associate Consultant

(Finance), Viswa Surya Energy Solutions for their continuous and keen guidance, which paved

the way for successful completion of this project.

I would also thank Mr. Rakesh Kumar, Associate Consultant (Business Development) for

constantly guiding and solving all my queries throughout this project.

I am grateful to my friends who gave me the moral support in my times of difficulties. Last but

not the least I would like to express my special thanks to my family for their

continuous motivation, encouragement and support.

Eshan Singh

Page | iv

CERTIFICATE

Page | v

EXECUTIVE SUMMARY

Today the major problem solar developers are facing is the high cost of generation. The

tariff bids have reached at the level of Rs 8 and below. To compete with such low tariff bids cost

of generation should be minimised. Major part of project cost is covered by the Solar panel cost,

if this cost can be minimised then total project cost can be minimised.

Since the availability of sun is uncontrollable so improving the generation is quite

difficult and expensive. If we decrease the annual expense instead of increasing the generation

then also tariff can be brought down significantly.

Major constituents of cost of generations are depreciation and interest if we can reduce

interest payable on debt amount then the cost of generation can be reduced to a significant and

competitive level.

Foreign Solar panels are cheaper than those produced in India. Also if we are importing

goods from some country then we can apply for EXPORT CREDIT FINANCING which is

cheaper than the finance available through Indian financial institutes.

Prime Lending Rates in India are near about 13%. Interest paid on debt is a cash outflow and is

included in cost of generation. Such high cost of debt elevates the Levellised Tariff of Solar PV

Plant.

Finance from Foreign institutes such as ExIm Bank’s reduces the interest rate of debt and

hence decreases the total outflow of cash resulting in low cost of generation.

This project is the study of Financial Terms and Conditions for Export Credit Loan and

comparative financial analysis of 1MW SOLAR PV PLANT model financed from China,

Finland, Germany, Japan, Singapore, Taiwan, Thailand and United States of America.

Page | vi

LIST OF ABBREVATIONS

AD Authorised Dealer

BTSF Better Than Sovereign Factor

CEF Credit Enhancement Factor

CIRR Commercial Interest Reference rate

DGFT Director General of Foreign Trade

ECB External Commercial Borrowing

EU European Union

ExIm Export Import

FoR Forum of Regulator

GNI Gross National Income

HOR Horizon of Risk

INR Indian Rupee

IRR Internal Rate of Return

JBIC Japan Bank of International Cooperation

LCF Local Currency Factor

LoC Letter of Comfort

LoU Letter of Undertaking

MoP Ministry of Power

MPR Minimum Premium Rate

Page | vii

OECD Organization for Economic Cooperation and Development

PCC Percentage Cover of Commercial Risk

PCF Percentage of Cover Factor

PCP Percentage Cover of Political Risk

PV Photovoltaic

USA United States of America

Page | viii

LIST OF TABLES

FIGURE 1.1 TYPES OF FOREIGN INVESTMENT ............................................................................................................ 1

FIGURE 1.2 BUYER’S CREDIT DIRECT LOAN ........................................................................................................... 11

FIGURE 1.3 BANK-TO-BANK DIRECT LOAN ............................................................................................................ 12

TABLE 2.1 RISK COEFFICIENT ................................................................................................................................ 27

TABLE 2.2 COMBINATION OF BUYER’S & COUNTRY RISK CATEGORY .................................................................... 28

TABLE 2.3 BUYER’S RISK COEFFICIENT ................................................................................................................. 29

TABLE 2.4 QUALITY PRODUCT FACTOR ................................................................................................................. 30

TABLE 2.5 PERCENTAGE COVER FACTOR ............................................................................................................... 31

TABLE2.1 MPR FOR INDIA .................................................................................................................................... 31

TABLE 3.1 FINANCIAL ASSUMPTIONS ..................................................................................................................... 32

TABLE 3.2 PROJECT COST ................................................................................................................................. 33

TABLE 3-3 INTEREST RATE ............................................................................................................................... 34

TABLE 3-4 ANALYSIS SHEET ............................................................................................................................ 34

Page | ix

LIST OF FIGURES

FIGURE 1.1 TYPES OF FOREIGN INVESTMENT ............................................................................................................ 1

FIGURE 1.2 BUYER’S CREDIT DIRECT LOAN ........................................................................................................... 11

FIGURE 1.3 BANK-TO-BANK DIRECT LOAN ............................................................................................................ 12

Page | x

Table of Contents

DECLARATION ................................................................................................................................................. II

ACKNOWLEDGMENT ................................................................................................................................... III

CERTIFICATE .................................................................................................................................................. IV

EXECUTIVE SUMMARY .................................................................................................................................. V

LIST OF ABBREVATIONS .............................................................................................................................. VI

LIST OF TABLES........................................................................................................................................... VIII

LIST OF FIGURES ............................................................................................................................................ IX

TABLE OF CONTENTS .................................................................................................................................... X

CHAPTER 1: ........................................................................................................................................................ 1

1. INTRODUCTION ....................................................................................................................................... 1

1.1 BACKDROP OF SOURCES OF FOREIGN FINANCE ........................................................................... 1

1.1.1. METHODS OF FOREIGN INVESTMENT .................................................................................................. 1

1.1.1.1. Foreign Direct Investment ........................................................................................................ 2

1.1.1.2. External Commercial Borrowings (ECB) ................................................................................. 2

1.1.2 TYPES OF FOREIGN LOANS FOR IMPORT ........................................................................................... 11

1.1.2.1 Direct Loan to Foreign Buyer’s (Buyer’s Credit Loan, B/C) ................................................. 11

1.1.2.2 Direct Loan to Foreign Financial Institute (Bank-to-Bank Loan, B/L) ................................. 11

1.1.3. RBI GUIDELINES FOR TRADE CREDIT FOR IMPORTS IN INDIA............................................ 12

1.1.3.1. TRADE CREDITS FOR IMPORTS INTO INDIA ..................................................................... 12

1.2 PROBLEM STATEMENT ...................................................................................................................... 16

1.3 OBJECTIVE ............................................................................................................................................. 17

1.4. ORGANIZATIONAL PROFILE ......................................................................................................... 17

MISSION .......................................................................................................................................................... 18

VISION ............................................................................................................................................................ 19

CHAPTER 2: ...................................................................................................................................................... 20

2.1 FINANCIAL TERMS AND CONDITIONS FOR EXPORT CREDITS ................................................. 20

2.1.1. DOWN PAYMENT, MAXIMUM OFFICIAL SUPPORT AND LOCAL COSTS .......................... 20

2.1.2. CLASSIFICATION OF COUNTRIES FOR MAXIMUM REPAYMENT TERMS ...................... 21

2.1.3. MAXIMUM REPAYMENT TERMS .............................................................................................. 22

2.1.4. REPAYMENT OF PRINCIPAL AND PAYMENT OF INTEREST ............................................... 22

2.1.5. INTEREST RATES, PREMIUM RATES AND OTHER FEES ...................................................... 24

2.1.6. VALIDITY PERIOD FOR EXPORT CREDITS ............................................................................. 24

2.1.7. ACTION TO AVOID OR MINIMISE LOSSES .............................................................................. 24

2.1.8. MATCHING .................................................................................................................................... 25

2.1.9. MINIMUM FIXED INTEREST RATES UNDER OFFICIAL FINANCING SUPPORT............... 25

2.1.10. PREMIUM FOR CREDIT RISK ................................................................................................ 25

2.1.11. MINIMUM PREMIUM RATES FOR CREDIT RISK ............................................................... 26

Page | xi

2.2 CALCULATION OF THE MINIMUM PREMIUM RATES .................................................................. 26

2.2.1. MPR Formula .............................................................................................................................. 26

2.2.2. Applicable Country Risk Classification ...................................................................................... 27

2.2.3. Selection of the Appropriate Buyer Risk Category ..................................................................... 27

2.2.4. Horizon of Risk (HOR) ................................................................................................................ 29

2.2.5. Buyer Risk Credit Enhancements ............................................................................................... 30

2.2.6. Quality of Product Factor (QPF)................................................................................................. 30

2.2.7. Percentage of Cover Factor (PCF) .............................................................................................. 30

2.2.8. Better than Sovereign Factor (BTSF) .......................................................................................... 31

2.2.9. Local Currency Factor (LCF) ..................................................................................................... 31

2.3 MPR FOR INDIAN IMPORTER ............................................................................................................. 31

CHAPTER 3: ...................................................................................................................................................... 32

3.1 FINANCIAL ANALYSIS AND MODELLING........................................................................................ 32

3.1.1. FINANCIAL ASSUMPTIONS......................................................................................................... 32

3.1.2. PROJECT COST CALCULATION ................................................................................................ 33

3.1.3. EXCHANGE RATE ......................................................................................................................... 33

3.1.4. INTEREST RATE ............................................................................................................................ 33

3.2 PROJECT ANALYSIS ............................................................................................................................. 34

CHAPTER 4: ...................................................................................................................................................... 35

4.1 CONCLUSION & RECOMMENDATION .............................................................................................. 35

BIBLIOGRAPHY .............................................................................................................................................. 36

ANNEXURE 1 .................................................................................................................................................... 37

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 1

Chapter 1:

1. INTRODUCTION

1.1 BACKDROP OF SOURCES OF FOREIGN FINANCE

1.1.1. Methods of Foreign Investment

Figure 1.1 Types of Foreign Investment

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 2

1.1.1.1. Foreign Direct Investment

FDI benefits the domestic industry as well as the Indian consumer by providing opportunities for

technological up gradation, access to global managerial skills and practices, optimal utilization of

human and natural resources, making Indian industry internationally competitive, opening up

export markets, providing backward and forward linkages and access to international quality

goods & services.

FDI is Permitted Through two routes:

A. FIPB Route (or Government Route)

under this route, prior approval from Foreign Investment Promotion Board (FIPB),

Government of India is required for foreign investment.

B. Automatic Route of Reserve Bank of India

Under this route no prior approval for foreign investment is required. Investment by a person

resident outside India in shares or convertible debentures of an Indian company.

1.1.1.2. External Commercial Borrowings (ECB)

The Government of India has further liberalized ECB approvals. The Government have vided

Press Release F.No. 4(32)-2000-ECB dated September 1, 2000, has decided to operationalise the

automatic route for fresh ECB approvals up to USD 50 million and for refinancing of an existing

ECB. .

Accordingly, under the automatic route arrangement any legal entity registered under the

Companies Act, Societies Registration Act, Co-operative Societies Act, including proprietorship/

partnership concerns will henceforth be eligible to enter into loan agreements with overseas

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 3

lender(s) for raising fresh ECB with average maturity of not less than 3 years for an amount up to

USD 50 million and for refinancing an existing ECB provided it is in compliance with both,

ECB guidelines framed by the Ministry of Finance, Government of India and the regulations/

directions/ circulars issued by Reserve Bank in this regard. No prior approval is now required

from the Ministry of Finance/Reserve Bank of India for raising ECB up to USD 50 million and

for refinancing of an existing ECB.

The borrower shall ensure that ECB is raised from an internationally acceptable and/or

recognized lender, such as export credit agencies, suppliers of equipments, foreign collaborators,

foreign equity holders, international capital markets, reputed international banks and financial

institutions, etc. The lenders should be recognized and registered in the host countries for the

purpose of extending international finance.

Further, the loan should be organized through a reputed merchant banker registered with the

regulatory authorities of the host country, such as, USA, Japan, EU countries, Singapore, and

such other countries as may be notified from time to time by the Government of India.

The borrower shall submit through an authorized dealer of its choice, three copies of the loan

agreement (along with Form ECB and Form 83, in duplicate) to the concerned Regional Office

of the Reserve Bank after signing the same with the lender. The Regional Office of the Reserve

Bank would acknowledge receipt of the copies of the agreement and allot a loan identification

number to such an agreement.

The primary responsibility to ensure that ECB raised is in conformity with the ECB guidelines

and the Reserve Bank regulations/directions/circulars will be that of the concerned borrower. If,

however, at a later stage, any violation is found, appropriate action will be taken by Reserve

Bank under the Foreign Exchange Management Act, 1999.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 4

Necessary draw - downs by the borrower will also be permitted under the automatic route

without prior permission of Reserve Bank. The borrower will, however, be required to file

quarterly returns in Form ECB-2 through the authorized dealer showing the details of drawls,

utilization and repayments made. This is to be submitted within 10 days of the close of the

calendar quarter to which it pertains.

The withholding tax exemptions would continue to be granted by the Ministry of Finance

(Department of Revenue/Department of Economic Affairs), Government of India.

For prepayment of outstanding ECBs (viz., 10% of the outstanding amount during the life of the

loan or ECBs with residual maturity up to one year), prior permission from Reserve Bank of

India, ECB Division, Exchange Control Department, Central Office, Mumbai will have to be

obtained by the borrower for which application will have to be submitted, duly forwarded by the

authorized dealer.

Opening of foreign currency account for parking ECB proceeds temporarily, pending utilization,

will require prior approval of the concerned Regional Office of Reserve Bank.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 5

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 6

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 7

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 8

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 9

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 10

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 11

1.1.2 Types of Foreign Loans for Import

1.1.2.1 Direct Loan to Foreign Buyer’s (Buyer’s Credit Loan, B/C)

A buyer's credits (B/C) are direct loans provided by a foreign financial institute for financing the

import of their machinery and equipment or the utilization of their technical services. A direct

loan to an importer is called buyer's credit.

Figure 1.2 Buyer’s Credit Direct Loan

1.1.2.2 Direct Loan to Foreign Financial Institute (Bank-to-Bank Loan, B/L)

A bank-to-bank loan (B/L) are direct loans provided by a foreign financial institution to local

Financial Institution for financing the import of foreign machinery and equipment or the

utilization of foreign technical services. A direct loan to a financial institution is called a bank-to-

bank loan.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 12

Figure 1.3 Bank-to-Bank Direct Loan

1.1.3. RBI GUIDELINES FOR TRADE CREDIT FOR IMPORTS IN INDIA

1.1.3.1. TRADE CREDITS FOR IMPORTS INTO INDIA

Trade Credits (TC) refer to credits extended for imports directly by the overseas supplier,

bank and financial institution for maturity of less than three years. Depending on the source of

finance, such trade credits include suppliers’ credit or buyers’ credit. Suppliers’ credit relates to

credit for imports into India extended by the overseas supplier, while buyers’ credit refers to

loans for payment of imports into India arranged by the importer from a bank or financial

institution outside India for maturity of less than three years. It may be noted that buyers’

credit and suppliers’ credit for three years and above come under the category of External

Commercial Borrowings (ECB) which are governed by ECB guidelines.

a. Amount and Maturity

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 13

AD banks are permitted to approve trade credits for imports into India up to USD 20

million per import transaction for imports permissible under the current Foreign

Trade Policy of the DGFT with a maturity period up to one year (from the date of

shipment). For import of capital goods as classified by DGFT, AD banks may approve

trade credits up to USD 20 million per import transaction with a maturity period of

more than one year and less than three years (from the date of shipment). No roll-

over/extension will be permitted beyond the permissible period.

The companies in the infrastructure sector, where “infrastructure” is as defined

under the extant guidelines on External Commercial Borrowings (ECB) have been

allowed to avail of trade credit up to a maximum period of five years for import of

capital goods as classified by DGFT subject to conditions that the trade credit must be

abinitio contracted for a period not less than fifteen months and should not be in the

nature of short-term roll overs. However, the condition of 'abinitio' buyers'credit

would be for 6 (six) months only for trade credits availed of on or before December

14, 2012. AD banks shall not approve trade credit exceeding USD 20 million per

import transaction.

b. All-in-cost Ceilings

The existing all-in-cost ceilings are as under

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 14

Maturity period All-in-cost ceilings over 6 months LIBOR*

Up to one year

350 basis points More than one year and upto three years

More than three years and upto five years

* For the respective currency of credit or applicable benchmark

The all-in-cost ceilings include arranger fee, upfront fee, management fee, handling/

processing charges, out of pocket and legal expenses, if any.

c. Guarantee

AD banks are permitted to issue Letters of Credit/guarantees/Letter of Undertaking (LoU)

/Letter of Comfort (LoC) in favour of overseas supplier, bank and financial institution, up to USD

20 million per transaction for a period up to one year for import of all non-capital goods

permissible under Foreign Trade Policy (except gold, palladium, platinum, Rodium, silver etc.)

and up to three years for import of capital goods, subject to prudential guidelines issued by

Reserve Bank from time to time. The period of such Letters of credit / guarantees / LoU / LoC

has to be co-terminus with the period of credit, reckoned from the date of shipment.

In respect of companies in the infrastructure sector as mentioned at para (a) (ii) above, AD

banks are not permitted to issue Letters of Credit/guarantees/Letter of Undertaking (LoU)

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 15

/Letter of Comfort (LoC) in favour of overseas supplier, bank and financial institution for the

extended period beyond three years. (as amended vide AP DIR Circular No.28 dated 11.9.2012)

d. Reporting Arrangements

AD banks are required to furnish details of approvals, drawl, utilisation, and repayment of

trade credit granted by all its branches, in a consolidated statement, during the month, in form

TC (format in Annex IV) from April 2004 onwards to the Director, Division of International

Finance, Department of Economic Policy and Research, Reserve Bank of India, Central Office

Building, 8th floor, Fort, Mumbai – 400 001 (and in MS-Excel file through email) so as to reach

not later than 10th of the following month. Each trade credit may be given a unique

identification number by the AD bank.

AD banks are required to furnish data on issuance of LCs / Guarantees / LoU / LoC by all its

branches, in a consolidated statement, at quarterly intervals (format in Annex V) to the Chief

General Manager-in-Charge, Foreign Exchange Department, ECB Division, Reserve Bank of

India, Central Office Building, 11th floor, Fort, Mumbai – 400 001 (and in MS-Excel file through

email) from December 2004 onwards so as to reach the Department not later than 10th of the

following month. TRADE CREDITS FOR IMPORTS INTO INDIA

Trade Credits (TC) refer to credits extended for imports directly by the overseas supplier,

bank and financial institution for maturity of less than three years. Depending on the source of

finance, such trade credits include suppliers’ credit or buyers’ credit. Suppliers’ credit relates to

credit for imports into India extended by the overseas supplier, while buyers’ credit refers to

loans for payment of imports into India arranged by the importer from a bank or financial

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 16

institution outside India for maturity of less than three years. It may be noted that buyers’

credit and suppliers’ credit for three years and above come under the category of External

Commercial Borrowings (ECB) which are governed by ECB guidelines.

1.2 PROBLEM STATEMENT

Today the major problem solar developers are facing is the high cost of generation. The tariff

bids have reached at the level of Rs 8 and below. To compete with such low tariff bids cost of

generation should be minimised. Major part of project cost is covered by the Solar panel cost, if

this cost can be minimised then total project cost can be minimised.

Since the availability of sun is uncontrollable so improving the generation is quite

difficult and expensive. If we decrease the annual expense instead of increasing the generation

then also tariff can be brought down significantly.

Major constituents of cost of generations are depreciation and interest if we can reduce

interest payable on debt amount then the cost of generation can be reduced to a significant and

competitive level.

Foreign Solar panels are cheaper than those produced in India. Also if we are importing

goods from some country then we can apply for EXPORT CREDIT FINANCING which is

cheaper than the finance available through Indian financial institutes.

Prime Lending Rates in India are near about 13%. Interest paid on debt is a cash outflow and is

included in cost of generation. Such high cost of debt elevates the Levellised Tariff of Solar PV

Plant.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 17

Finance from Foreign institutes such as ExIm Bank’s reduces the interest rate of debt and

hence decreases the total outflow of cash resulting in low cost of generation.

This project is the study of Financial Terms and Conditions for Export Credit Loan and

comparative financial analysis of 1MW SOLAR PV PLANT model financed from China,

Finland, Germany, Japan, Singapore, Taiwan, Thailand and United States of America.

1.3 OBJECTIVE

1. To study the methods of foreign investment.

2. To find the prime lending rate of EXIM Bank’s of different countries.

3. To calculate the project cost when Solar panels are imported from other country.

4. To prepare the Financial Model for 1MW Solar PV plant financed from different countries.

5. To suggest the method to minimize the project cost and hence minimizing the cost of

generation.

1.4. ORGANIZATIONAL PROFILE

Solar energy is renewable, non-polluting and highly cost-effective, requires little maintenance

and lasts a lifetime. It goes without saying that the future belongs to those countries which take

an initiative in tapping into solar energy solutions. India is one among the early entrants. The

support given by the government has seen the emergence of quite a few vibrant organizations

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 18

dedicated to the mission of solar energy with societal objectives taking precedence over

commerce. VSES is proud to be one such initiative.

Equipped with state-of art technology, intellect far ahead of the game and a team with

managerial and technical acumen, they endeavour to be a global leader in renewable energy

solutions.

VSES was founded in Visakhapatnam, Andhra Pradesh in the year 2012 with the objective of

providing cost-effective and indigenous solutions to the fledgling solar industry and thereby

contributing to national development. VSES has a distinction of being the tasted company in

India to offer indigenous solutions within a very short span of one year; the company has

acquired an impressive bevy of clients and is well in line with its vision of becoming a

technology leader in renewable energy.

The design and development of low cost solar solutions, especially solar wind hybrid systems

and solar hydel hybrids systems which is our forte demands an expertise across a gamut of

verticals. Backed by a team of professionals with years of experience in the above sectors that is

complemented beautifully by our support staff with administrative and business acumen and our

business model and integrity have gained us an early reputation as a quality player in this niche

market.

Mission

To enter the market as a technology and service provider of renewable energy projects and

become a world class player in the upcoming few years through the use of innovative

technologies, cost effective solutions and indigenous models.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 19

Vision

To create self-sustainable societies through the use of renewable energy. And establish a basis

for technology, service and design in the market for others to follow and to completely reduce

the dependence on the non-renewable energy sources.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 20

Chapter 2:

2.1 FINANCIAL TERMS AND CONDITIONS FOR EXPORT CREDITS

The Arrangement sets out limitations on terms and conditions that may be officially supported.

The Participants recognize that more restrictive financial terms and conditions than those

provided for by the Arrangement traditionally apply to certain trade or industrial sectors. The

Participants shall continue to respect such customary financial terms and conditions, in particular

the principle by which repayment terms do not exceed the useful life of the goods.

2.1.1. DOWN PAYMENT, MAXIMUM OFFICIAL SUPPORT AND

LOCAL COSTS

a. The Participants shall require purchasers of goods and services which are the subject of

official support to make down payments of a minimum of 15% of the export contract

value at or before the starting point of credit. For the assessment of down payments, the

export contract value may be reduced proportionally if the transaction includes goods and

services from a third country which are not officially supported. Financing/insurance of

100% of the premium is permissible. Premium may or may not be included in the export

contract value. Retention payments made after the starting point of credit are not regarded

as down payment in this context.

b. Official support for such down payments shall only take the form of insurance or

guarantee against the usual pre-credit risks.

c. Except as provided for in paragraphs b) and d), the Participants shall not provide official

support in excess of 85% of the export contract value, including third country supply but

excluding local costs.

d. The Participants may provide official support for local costs, provided that:

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 21

Official support provided for local costs shall not exceed 30% of the export

contract value.

It shall not be provided on terms more favourable/less restrictive than those

agreed for the related exports.

Where official support for local cost exceeds 15% of the export contract value,

such official support shall be subject to prior notification, pursuant to Article 48,

specifying the nature of the local costs being supported.

2.1.2. CLASSIFICATION OF COUNTRIES FOR MAXIMUM

REPAYMENT TERMS

a. Category I countries are High Income OECD countries. All other countries are in

Category II.

b. The following operational criteria and procedures apply when classifying countries:

Classification for Arrangement purposes is determined by per capita GNI as

calculated by the World Bank for the purposes of the World Bank classification of

borrowing countries.

In cases where the World Bank does not have enough information to publish per

capita GNI data, the World Bank shall be asked to estimate whether the country in

question has per capita GNI above or below the current threshold. The country

shall be classified according to the estimate unless the Participants decide to act

otherwise.

If a country is reclassified, the reclassification will take effect two weeks after the

conclusions drawn from the above-mentioned data from the World Bank have

been communicated to all Participants by the Secretariat.

In cases where the World Bank revises figures, such revisions shall be

disregarded in relation to the Arrangement. Nevertheless, the classification of a

country may be changed by way of a Common Line and Participants would

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 22

favourably consider a change due to errors and omissions in the figures

subsequently recognised in the same calendar year in which the figures were first

distributed by the Secretariat.

c. A country will change category only after its World Bank category has remained

unchanged for two consecutive years.

2.1.3. MAXIMUM REPAYMENT TERMS

The maximum repayment term varies according to the classification of the country of

destination.

a. For Category I countries, the maximum repayment term is five years, with the possibility

of agreeing up to eight-and-a-half years when the procedures for prior notification are

followed.

b. For Category II countries, the maximum repayment term is ten years.

c. In the event of a contract involving more than one country of destination the Participants

should seek to establish a Common Line to reach agreement on appropriate terms defined

by the World Bank on an annual basis according to per capita GNI.

2.1.4. REPAYMENT OF PRINCIPAL AND PAYMENT OF INTEREST

a. The principal sum of an export credit shall be repaid in equal instalments.

b. Principal shall be repaid and interest shall be paid no less frequently than every six

months and the first instalment of principal and interest shall be made no later than six

months after the starting point of credit.

c. For export credits provided in support of lease transactions, equal repayments of principal

and interest combined may be applied in lieu of equal repayments of principal as set out

in paragraph a).

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 23

d. On an exceptional and duly justified basis, export credits may be provided on terms other

than those set out in a) through c) above. The provision of such support shall be

explained by an imbalance in the timing of the funds available to the obligor and the debt

service profile available under an equal, semi-annual repayment schedule, and shall

comply with the following criteria:

No single repayment of principal or series of principal payments within a six-

month period shall exceed 25% of the principal sum of the credit.

Principal shall be repaid no less frequently than every 12 months. The first

repayment of principal shall be made no later than 12 months after the starting

point of credit and no less than 2% of the principal sum of the credit shall have

been repaid 12 months after the starting point of credit.

Interest shall be paid no less frequently than every 12 months and the first interest

payment shall be made no later than six months after the starting point of credit.

The maximum weighted average life of the repayment period shall not exceed:

- For transactions with sovereign buyers (or with a sovereign repayment

guarantee), four-and-a-half years for transactions in Category I Countries and

five-and-a-quarter years for Category II Countries.

- For transactions with non-sovereign buyers (and with no sovereign repayment

guarantee), five years for Category I Countries and six years for Category II

Countries.

- Notwithstanding the provisions set out in the two previous tirets, for

transactions involving support for non-nuclear power plants six-and-a-quarter

years.

The Participant shall give prior notification that explains the reason for not

providing support according to paragraphs a) through c).

e. Interest due after the starting point of credit shall not be capitalised.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 24

2.1.5. INTEREST RATES, PREMIUM RATES AND OTHER FEES

a. Interest excludes:

Any payment by way of premium or other charge for insuring or guaranteeing

supplier credits or financial credits;

Any payment by way of banking fees or commissions relating to the export credit

other than annual or semi-annual bank charges that are payable throughout the

repayment period; and

Withholding taxes imposed by the importing country.

b. Where official support is provided by means of direct credits/financing or refinancing,

the premium either may be added to the face value of the interest rate or may be a

separate charge; both components are to be specified separately to the Participants.

2.1.6. VALIDITY PERIOD FOR EXPORT CREDITS

Financial terms and conditions for an individual export credit or line of credit, other than the

validity period for the Commercial Interest Reference Rates (CIRRs), shall not be fixed for a

period exceeding six months prior to final commitment.

2.1.7. ACTION TO AVOID OR MINIMISE LOSSES

The Arrangement does not prevent export credit authorities or financing institutions from

agreeing to less restrictive financial terms and conditions than those provided for by the

Arrangement, if such action is taken after the contract award (when the export credit agreement

and ancillary documents have already become effective) and is intended solely to avoid or

minimise losses from events which could give rise to non-payment or claims.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 25

2.1.8. MATCHING

Taking into account a Participant’s international obligations and consistent with the purpose of

the Arrangement, a Participant may match, financial terms and conditions offered by a

Participant or a non-Participant.

2.1.9. MINIMUM FIXED INTEREST RATES UNDER OFFICIAL

FINANCING SUPPORT

a. The Participants providing official financing support for fixed rate loans shall apply the

relevant CIRRs as minimum interest rates. CIRRs are interest rates established according

to the following principles:

CIRRs should represent final commercial lending interest rates in the domestic

market of the currency concerned;

CIRRs should closely correspond to the rate for first class domestic borrowers;

CIRRs should be based on the funding cost of fixed interest rate finance;

CIRRs should not distort domestic competitive conditions; and

CIRRs should closely correspond to a rate available to first class foreign

borrowers.

b. The provision of official financing support shall not offset or compensate, in part or in

full, for the appropriate credit risk premium to be charged for the risk of non-repayment.

2.1.10. PREMIUM FOR CREDIT RISK

The Participants shall charge premium, in addition to interest charges, to cover the risk of non-

repayment of export credits. The premium rates charged by the Participants shall be risk-based,

shall converge and shall not be inadequate to cover long-term operating costs and losses.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 26

2.1.11. MINIMUM PREMIUM RATES FOR CREDIT RISK

The Participants shall charge no less than the applicable Minimum Premium Rate (MPR) for

Credit Risk.

a. The applicable MPR is determined according to the following factors:

The applicable country risk classification;

The time at risk ( i.e. the Horizon of Risk or HOR);

The selected buyer risk category of the obligor;

The percentage of political and commercial risk cover and quality of official

export credit product provided;

Any country risk mitigation technique applied; and

Any buyer risk credit enhancements that have been applied.

b. MPRs are expressed in percentages of the principal value of the credit as if premium

were collected in full at the date of the first drawdown of the credit.

c. There are no MPRs for transactions involving obligors in Category 0 countries, High

Income OECD Countries and High Income Euro Area Countries. The premium rates

charged by Participants for transactions in such countries shall be determined on a case-

by-case basis.

2.2 CALCULATION OF THE MINIMUM PREMIUM RATES

2.2.1. MPR Formula

The formula for calculating the applicable MPR for an export credit involving an

obligor/guarantor in a country classified in Country Risk Categories 1-7 is:

MPR = { [ (ai* HOR + bi) * max (PCC, PCP) / 0.95 ] * (1-LCF) + [cin * PCC / 0.95 *

HOR * (1-CEF) ] }* QPFi * PCFi *BTSF

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 27

Where:

ai = country risk coefficient in country risk category i (i = 1-7)

cin = buyer risk coefficient for buyer category n ( n = SOV+, SOV/CCO, CC1-

CC5) in country risk category i (i = 1-7)

bi = constant for country category risk category i (i = 1-7)

HOR = horizon of risk

PCC = commercial (buyer) risk percentage of cover

PCP = political (country) risk percentage of cover

CEF = credit enhancements factor

QPF i = quality of product factor in country risk category i ( i = 1-7)

PCF = percentage of cover factor in country risk category i ( i = 1-7)

BTSF = better than sovereign factor

LCF = local currency factor

2.2.2. Applicable Country Risk Classification

The applicable country risk classification determines the country risk coefficient (ai) and

constant (bi) that are obtained from the following table:

1 2 3 4 5 6 7

(a) 0.090 0.200 0.350 0.550 0.740 0.900 1.100

(b) 0.350 0.350 0.350 0.350 0.750 1.200 1.800

Table 2.1 Risk Coefficient

2.2.3. Selection of the Appropriate Buyer Risk Category

The appropriate buyer risk category is selected from the following table, which provides

the combinations of country and buyer risk categories that have been established and the

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 28

agreed concordance between buyer risk categories CC1-CC5 and the classifications of

accredited CRAs.

Qualitative descriptions of each buyer risk category (SOV+ to CC5) have been

established to facilitate the classification of obligors (and guarantors).

Table 2.2 Combination of Buyer’s & Country Risk Category

The selected buyer risk category, in combination with the applicable country risk

category determines the buyer risk coefficient (cin) that is obtained from the following

table:

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 29

Table 2.3 Buyer’s Risk Coefficient

2.2.4. Horizon of Risk (HOR)

The Horizon of Risk (HOR) is calculated as follows:

For standard repayment profiles (i.e. equal semi-annual repayments of principal):

HOR = (length of the disbursement period * 0.5) + the length of the repayment

period

For non-standard repayment profiles:

HOR = (length of the disbursement period * 0.5) + (weighted average life of the

repayment period - 0.25) / 0.5

In the above formulas, the unit of measurement for time is years.

Percentage of Cover for Commercial (Buyer) Risk (PCC) and Political (Country) Risk

(PCP)

The Percentages of Cover (PCC and PCP) expressed as a decimal value ( i.e. 95% is

expressed as 0.95) in the MPR formula.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 30

2.2.5. Buyer Risk Credit Enhancements

The value of the credit enhancement factor (CEF) is 0 for any transaction that is not

subject to any buyer risk credit enhancements. The value of the CEF for transactions that

are subject to buyer risk credit enhancements is determined and may not exceed 0.35.

2.2.6. Quality of Product Factor (QPF)

The QPF is obtained from the following table:

Table 2.4 Quality Product Factor

2.2.7. Percentage of Cover Factor (PCF)

The PCF is determined as follows:

For ( max(PCC, PCP) ≤ 0.95, PCF = 1)

For ( max(PCC, PCP) > 0.95, PCF = 1 + ( ( max(PCC, PCP) - 0.95) / 0.05 ) *

(Percentage of cover coefficient)

The percentage of cover coefficient is obtained from the following table:

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 31

Table 2.5 Percentage Cover Factor

2.2.8. Better than Sovereign Factor (BTSF)

When an obligor is classified in the “better than sovereign” (SOV+) buyer risk category,

BTSF = 0.9,

Otherwise BTSF = 1.

2.2.9. Local Currency Factor (LCF)

For transaction making use of local currency country risk mitigation, the value of the

LCF may not exceed 0.2. The value of the LCF for all other transactions is 0.

2.3 MPR FOR INDIAN IMPORTER

ai bi HOR PCC PCP LCF Cin CEF QPFi PCFi BTSF MPR

0.35 0.35 12.04167 0.00489 0.95 0.2 0.495 0.35 1 1 1 3.67%

Table2.6 MPR for India

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 32

Chapter 3:

3.1 FINANCIAL ANALYSIS AND MODELLING

3.1.1. FINANCIAL ASSUMPTIONS

Table 3.7 Financial Assumptions

Particular No. Units

Capital Cost 6.56 Crs/MW

Plant Life 25 years

Tariff Period* 25 years

Debt 70.00%

Equity 30.00%

Debt Employed 459.2862482 lakhs/MW

Equity employed 196.8369635 lakhs/MW

Discoutn Rate 10.95% p.a.

Loan Teneure 12 years

Capcity Utilization

Factor (CUF)19.00%

Interest Rate

Depreciation 90.00%

Salvage Value 10.00%

5.83% p.a.

1.54% p.a.

20.00% p.a.

24.00% p.a.

Interest On

Working Capital

(10% + 3.5%) =

13.5%p.a.

Normative O&M

expenses11.63 Lakhs/MW

O&M escalation

Rate5.72% p.a.

2.00%

1.00%

Late Payment OF

surcharge1.25% per Month

Tax rate(30%+5%+3%) =

32.445%p.a.

Rebate

Return on Equity

(RoE)

Depreciation Rate

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 33

3.1.2. PROJECT COST CALCULATION

Capital Costs Units Input Value In Rs

Panel Cost $/Watt dc $ 0.59 Rs. 40.00

1MW $ 5,90,000.00 Rs. 4,00,02,000.00

Export cost

$ - Rs. -

Import cost

$ 1,02,733.35 Rs. 69,65,321.18

Appx. Local charges (transportation

and installation $ 1,25,000.00 Rs. 84,75,000.00

Ancillary Services & Products

$ 1,50,000.00 Rs. 1,01,70,000.00

Total Project Cost

$ 9,67,733.35 Rs. 6,56,12,321.18

Table 3.2 PROJECT COST

3.1.3. EXCHANGE RATE

1 USD = 67.8 INR

3.1.4. INTEREST RATE

Country Interest Rate

PLR PLR+ MPR

China 6% 9.67%

Finland 3.21% 6.88%

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 34

Germany 3.71% 7.38%

Japan 3.31% 6.98%

Singapore 5.38% 9.05%

Taiwan 2.88% 6.55%

Thailand 6.88% 10.55%

United States of America 2.71% 6.38%

Table 3-3 INTEREST RATE

3.2 PROJECT ANALYSIS

Country Interest

Rate

Assumed Project

Cost ( in Lakhs)

Cost of

Generation

Interest Paid (in

Lakhs) Project IRR

China 10% Rs. 656.12 Rs. 6.95 Rs. 268.37 20.05%

Finland 6.88% Rs. 656.12 Rs. 6.60 Rs. 190.95 19.79%

Germany 7.38% Rs. 656.12 Rs. 6.66 Rs. 204.83 19.83%

Japan 6.98% Rs. 656.12 Rs. 6.61 Rs. 193.73 19.80%

Singapore 9.05% Rs. 656.12 Rs. 6.87 Rs. 251.17 19.99%

Taiwan 6.55% Rs. 656.12 Rs. 6.55 Rs. 181.80 19.76%

Thailand 10.55% Rs. 656.12 Rs. 7.07 Rs. 292.65 20.13%

USA 6.38% Rs. 656.12 Rs. 6.53 Rs. 177.08 19.74%

Table 3-4 ANALYSIS SHEET

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 35

Chapter 4:

4.1 CONCLUSION & RECOMMENDATION

Due to current economic conditions i.e. current INR to USD exchange rate, the import

cost of solar panels has increased by about 30%. This increased cost is adversely affecting the

benefits of importing of solar panel and also the financing from other countries.

Even with such high exchange rate, the average cost of generation achieved is about

Rs.6.75 which is still competable in market.

After analysing the financial terms and conditions and also the trade agreements with

above mentioned countries, I recommend JAPAN as the most suitable country to get finance for

Viswa Surya Energy Solutions.

Reasons for recommending JAPAN:

ZERO Export Duty on Solar PV

Low Interest Rates

Japan Bank of International Cooperation (Formerly known as Japan’s ExIm Bank) has

been a prime investor in many Indian Solar projects such as for 25MW Solar Plat in

ANTA.

India and Japan has signed a bilateral trade agreement which promotes both trade and

investment, hence financing from Japan will be easier.

VSES is already importing their Solar Panel from Japan.

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 36

Bibliography Arrangement of Officially Supported Export Credit, retrieved from www.oec.org

Bilateral Trade Agreement 2010,with Japan, retrieved from www.commerce.nic.in

Export Loans from Japan, studied from www.jbic.go.jp

Export credit terms of USA, studied from www.exim.gov

Export Credit terms of Germany, studied from www.kfw.de

Concepts of foreign trade, studied from www.eximguru.com

AGREEMENT ON ECONOMIC COOPERATION BETWEEN THE GOVERNMENT

OF THE REPUBLIC OF INDIA AND THE GOVERNMENT OF THE REPUBLIC OF

FINLAND, studied from www.eximguru.com

Annual Report 2012-13 of China ExIm Bank, retrieved from www.eximbank.gov.cn

Financial Management- I.M Pandey

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 37

Annexure 1

Financial Model for 1MW Solar PV Plant Financed From Japan.

Assumption Sheet:

1000 KW Parameters JAPAN Financed

S. No. Sub Head Unit Assumption Value

1

Capacity KW 1000

% 19.00%

Lakhs KWh 16.644

% 0.00%

Lakhs KWh 16.644

% 0.00%

Years 25

2

Capital cost/MW Rs Lacs/MW 656.12

Annual Net Generation

Annual Deration

Useful Life

Project Cost

Power Plant Cost

Auxiliary Consumption

Assumption For Solar PV power Project

Assumption Head Sub Head (2)

Power Generation

Installed Power Generation Capacity

Capacity Utilization Factor

Annual Gross Generation

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 38

3

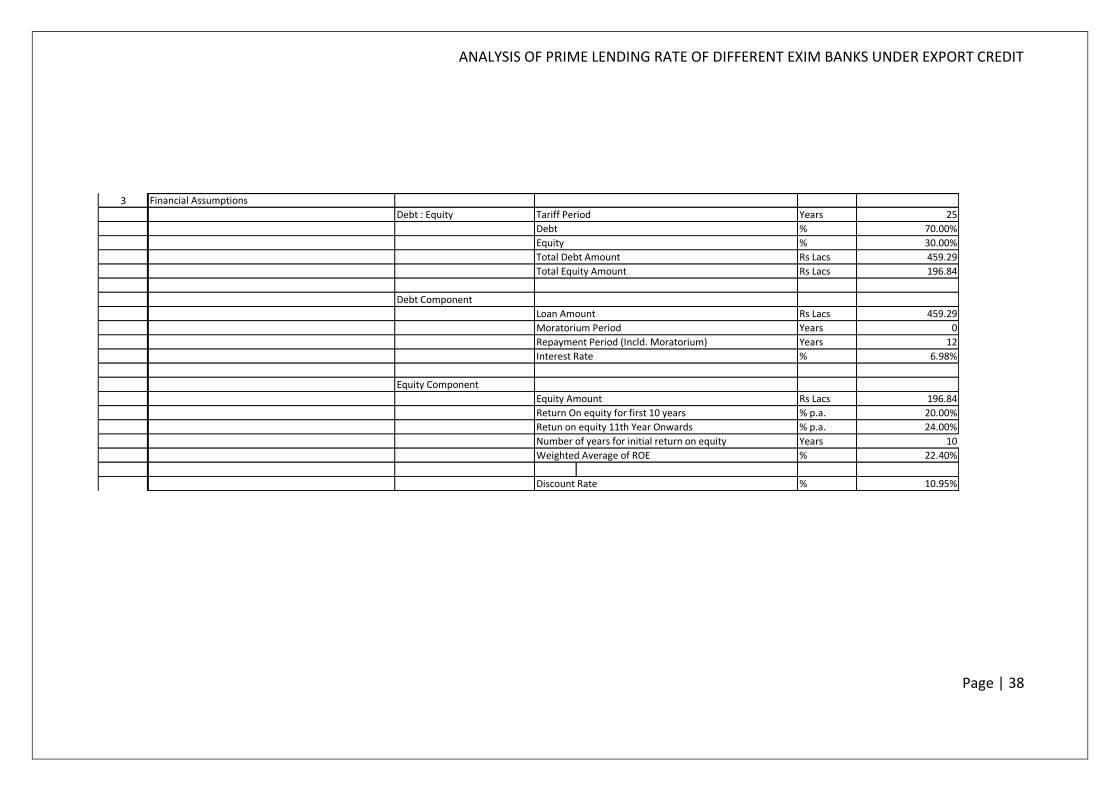

Debt : Equity Years 25

% 70.00%

% 30.00%

Rs Lacs 459.29

Rs Lacs 196.84

Debt Component

Rs Lacs 459.29

Years 0

Years 12

% 6.98%

Equity Component

Equity Amount Rs Lacs 196.84

Return On equity for first 10 years % p.a. 20.00%

Retun on equity 11th Year Onwards % p.a. 24.00%

Number of years for initial return on equity Years 10

Weighted Average of ROE % 22.40%

Discount Rate % 10.95%

Interest Rate

Loan Amount

Moratorium Period

Repayment Period (Incld. Moratorium)

Total Equity Amount

Debt

Equity

Total Debt Amount

Tariff Period

Financial Assumptions

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 39

4 Fiscal Assumptions

Assumed tariff (Iterative) Rs/kWh 10.39

Income tax % 32.45%

8.66

Depreciation

lakhs 590.5108906

lakhs 65.61232118

% 2.64%

% 5.83%

% 5.83%

% 1.54%

Years 12

% 40%

% 80%

Book depreciation first year

Book depreciation from second year

Depreciation rate for First 12 years

Depreciation rate 13th years onwards

Number of years for initial depreciation rate

Accelerated Depreciation for First Year

Accelerated Depreciation for Second Year onwards

Non Depreciable Amount (10%)

Fianancial Assumptions

Annuity Factor

Depreciable amount (90%)

5

For Fixed Charges

O&M Charges Months 1

Maintenance Spares (% of O&M expenses) % 15.00%

Recievables for Debtors Months 2

For Variable Charges

Interest on Working Capital % 13.50%

Working Capital

6

Power Plant (First Yr Of

Operation) Rs Lacs 11Total O&M Expenses

Escalation % 5.72%

Operation & Maintenance

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 40

7 Tax Corporate Tax % 32.45%

Land Lease Rate % 5.00%

MAT % 20.00%

Tax Holiday start Year Year 1

Tax holiday duration years 10

MAT Set OFF start year years 11

MAT Set OFF accumulation

allowed u/s 115JAA (3A) years 10

MAT SET OFF Duration years 11

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 41

Depreciation Sheet:

Depreciaiton Calculation For SLM Value Units

CapEx 656.12 Rs lacs

Annual Net Genration 16.644 Lakh KWhs

Annual Deration 0.00% %

Life of Plant and Machinery/Project Life 25 Years

Annual Depreciaiton for Period Of term Loan 38.25198325 Laks/Yr

Advance against Depreciation 0 Lakhs/Yr

Amount remaining to be depreciated post term loan 131.4870916 Lakhs

Book Depreciation first year 2.64% %

Book Depreciation Second year 5.83% %

Depreciable amount 590.5108906 Rs lacs

Accelerated Depreciation first year 40.00% %

Accelerated Depreciation from second year 80.00% %

Corporate Tax 32.45% %

Year>> 1 2 3 4 5 6 7 8 9 10

Book Depreciation 17.32 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25

Cumulative Book Depreciation 17.32 55.57 93.83 132.08 170.33 208.58 246.83 285.09 323.34 361.59

Accelerated Depreciation Benefit Calculations Year>> 1 2 3 4 5 6 7 8 9 10

Opening 100.00% 60.00% 12.00% 2.40% 0.48% 0.10% 0.02% 0.00% 0.00% 0.00%

Allowed During the Year 40.00% 48.00% 9.60% 1.92% 0.38% 0.08% 0.02% 0.00% 0.00% 0.00%

Closing 60.00% 12.00% 2.40% 0.48% 0.10% 0.02% 0.00% 0.00% 0.00% 0.00%

Accelerated Depreciation 262.45 314.94 62.99 12.60 2.52 0.50 0.10 0.02 0.00 0.00

Net Depreciaiton Benefit Rs. Lacs 245.13 276.69 24.74 -25.65 -35.73 -37.75 -38.15 -38.23 -38.25 -38.25

Tax Benefit Rs. Lacs 79.53 89.77 8.03 -8.32 -11.59 -12.25 -12.38 -12.40 -12.41 -12.41

Per Unit Benefit Rs./kWh 4.78 5.39 0.48 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Discounting Factor (DF) 1.000 0.904 0.817 0.739 0.668 0.603 0.545 0.493 0.446 0.403

Per Unit Benefit * DF 4.778 4.875 0.394 0.000 0.000 0.000 0.000 0.000 0.000 0.000

Discounting Factor 1.000 0.901 0.812 0.732 0.660 0.595 0.536 0.483 0.435 0.393

Levellised AD benefit Rs./kWh 1.01220857

Depreciation Calculation

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 42

Depreciaiton Calculation For SLM Value Units

CapEx 656.12 Rs lacs

Annual Net Genration 16.644 Lakh KWhs

Annual Deration 0.00% %

Life of Plant and Machinery/Project Life 25 Years

Annual Depreciaiton for Period Of term Loan 38.25198325 Laks/Yr

Advance against Depreciation 0 Lakhs/Yr

Amount remaining to be depreciated post term loan 131.4870916 Lakhs

Book Depreciation first year 2.64% %

Book Depreciation Second year 5.83% %

Depreciable amount 590.5108906 Rs lacs

Accelerated Depreciation first year 40.00% %

Accelerated Depreciation from second year 80.00% %

Corporate Tax 32.45% %

Year>> 1 2 3 4 5 6 7 8 9 10

Book Depreciation 17.32 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25

Cumulative Book Depreciation 17.32 55.57 93.83 132.08 170.33 208.58 246.83 285.09 323.34 361.59

Accelerated Depreciation Benefit Calculations Year>> 1 2 3 4 5 6 7 8 9 10

Opening 100.00% 60.00% 12.00% 2.40% 0.48% 0.10% 0.02% 0.00% 0.00% 0.00%

Allowed During the Year 40.00% 48.00% 9.60% 1.92% 0.38% 0.08% 0.02% 0.00% 0.00% 0.00%

Closing 60.00% 12.00% 2.40% 0.48% 0.10% 0.02% 0.00% 0.00% 0.00% 0.00%

Accelerated Depreciation 262.45 314.94 62.99 12.60 2.52 0.50 0.10 0.02 0.00 0.00

Net Depreciaiton Benefit Rs. Lacs 245.13 276.69 24.74 -25.65 -35.73 -37.75 -38.15 -38.23 -38.25 -38.25

Tax Benefit Rs. Lacs 79.53 89.77 8.03 -8.32 -11.59 -12.25 -12.38 -12.40 -12.41 -12.41

Per Unit Benefit Rs./kWh 4.78 5.39 0.48 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Discounting Factor (DF) 1.000 0.904 0.817 0.739 0.668 0.603 0.545 0.493 0.446 0.403

Per Unit Benefit * DF 4.778 4.875 0.394 0.000 0.000 0.000 0.000 0.000 0.000 0.000

Discounting Factor 1.000 0.901 0.812 0.732 0.660 0.595 0.536 0.483 0.435 0.393

Levellised AD benefit Rs./kWh 1.01220857

Depreciation Calculation

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 43

Cost of Generation Sheet:

Working Capital Sheet:

Value Units656.12 Rs Lakhs

25 years

12 years

196.84 Rs Lakhs

20.00% %

24.00% %

10 years

5.83% %

1.54% %

12 years

10.95% %

5.72% %

8.66

Cost Of Generation Units Year 1 2 3 4 5 6 7 8 9 10

O&M expenses Rs Lacs 11.00 11.63 12.29 13.00 13.74 14.53 15.36 16.24 17.17 18.15

Depreciaition Rs Lacs 38.25198325 38.25198325 38.25198325 38.25198325 38.25198325 38.25198325 38.25198325 38.25198325 38.25198325 38.25198325

Cummulative Depreciaiton Rs Lacs 38.25198325 76.50396649 114.7559497 153.007933 191.2599162 229.5118995 267.7638827 306.015866 344.2678492 382.5198325

Interest on Term Loan Rs Lacs 30.84 28.17 25.50 22.82 20.15 17.48 14.81 12.14 9.46 6.79

Interest on Working Capital Rs Lacs 4.03 4.04 4.05 4.06 4.07 4.08 4.09 4.10 4.11 4.13

Return on Equity Rs Lacs 39.36739271 39.36739271 39.36739271 39.36739271 39.36739271 39.36739271 39.36739271 39.36739271 39.36739271 39.36739271

Total Cost of Generation Rs Lacs 123.49 121.46 119.46 117.50 115.58 113.71 111.88 110.09 108.36 106.68

Per Unit Cost Of Generation Rs/kWh 7.419699945 7.297446231 7.177382848 7.059635082 6.944335387 6.831623793 6.721648339 6.614565532 6.510540831 6.409749161

Discounting Factor 1 0.901306895 0.812354119 0.732180369 0.659919215 0.594789738 0.536088092 0.483179894 0.43549337 0.392513177

Levellised Tariff Rs./kWh 6.608531523

Levellised Tariff With AD benefit Rs./kWh 5.596322953

Discount rate

O&M escalation Rate

Annuity Factor (25 years)

Return on equity - Pretax (Initial Years 10 )

Return on equity - Pretax (later Years 11th Yr Onwards)

Number of years for initial return on equity

Depreciation rate for First 12 years

Depreciation rate 13th year onwards

Number of years for initial depreciation rate

Equity

InputsCapex

Life of plant and Machinery (Project life)

Number of years for initial depreciation rate

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 44

Value Units1000 kw

25 years

11 Lacs/MW

5.72% %

16.644 lakhs KWhs

10.39 Rs/kWh

15.00% of Yearly O&M cost

13.50% %

1 2 3 4 5 6 7 8 9 10

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

11.00 11.63 12.29 13.00 13.74 14.53 15.36 16.24 17.17 18.15

0.92 0.97 1.02 1.08 1.15 1.21 1.28 1.35 1.43 1.51

28.82 28.82 28.82 28.82 28.82 28.82 28.82 28.82 28.82 28.82

0.14 0.15 0.15 0.16 0.17 0.18 0.19 0.20 0.21 0.23

29.88 29.94 30.00 30.07 30.14 30.21 30.29 30.38 30.47 30.56

4.03 4.04 4.05 4.06 4.07 4.08 4.09 4.10 4.11 4.13Interest On working Capital

Annual Net Generation

Assumed tariff (Iterative)

Maintenance Spares

Interest on Working Capital

Working Capital

Fuel Cost ( 4 months Equivalent)

O&M (For One Year)

O&M expeses for 1 month

Receivables (2 months of energy charges)

Maintenance Spares

Total Working Capital

O&M Cost Escalation

InputsCapacity

Life of Plant and Machinery (Project Life)

O&M Cost

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 45

Term Loan Sheet:

Profit & Loss Sheet:

Value Units459.29 Lacs

6.98% %

196.84 Lacs

0 years

144 Months

3.19 lacs

0 1 2 3 4 5 6 7 8 9 10 11 12

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19 3.19

38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27

38.27 76.55 114.82 153.10 191.37 229.64 267.92 306.19 344.46 382.74 421.01 459.29

Installment - 8

Installment - 9

Installment - 10

Installment - 11

Installment - 12

Total Installment

Cumulative Principal Repayment

Installment - 7

No. of Installment for Principal Repayment

Monthly Principal Repayment

Term Loan Repayment Details

Installment - 1

Installment - 2

Installment - 3

Installment - 4

Installment - 5

Installment - 6

Moratorium Period

User InputLoan Amount

Interest Rate

Equity

Term Loan Calculations

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 46

Profit and Loss Calcualation

Value Units

196.837 Rs lakhs

25 Years

32.45% %

20.00% %

1 Year

10 Years

11 Year

10 Years

11 Year

10.39 Rs

1 2 3 4 5 6 7 8 9 10

16.644 16.644 16.644 16.644 16.644 16.644 16.644 16.644 16.644 16.644

10.39 10.39 10.39 10.39 10.39 10.39 10.39 10.39 10.39 10.39

172.9312 172.9312 172.9312 172.9312 172.9312 172.9312 172.9312 172.9312 172.9312 172.9312

0 0 0 0 0 0 0 0 0 0

0 0 0 0 0 0 0 0 0 0

172.9312 172.9312 172.9312 172.9312 172.9312 172.9312 172.9312 172.9312 172.9312 172.9312

0 0 0 0 0 0 0 0 0 0

11.00 11.63 12.29 13.00 13.74 14.53 15.36 16.24 17.17 18.15

161.93 161.30 160.64 159.93 159.19 158.40 157.57 156.69 155.77 154.78

17.32 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25

144.61 123.05 122.38 121.68 120.94 120.15 119.32 118.44 117.51 116.53

34.87 32.21 29.55 26.88 24.22 21.56 18.90 16.24 13.58 10.92

109.74 90.84 92.84 94.80 96.72 98.59 100.42 102.21 103.94 105.61

87.79 72.67 74.27 75.84 77.37 78.87 80.34 81.76 83.15 84.49

Corporate Tax rate

User Inputs

Equity

Life of plant and Machinery (Project Life)

Income from Carbon Market

MAT

Tax Holiday start Year

Tax holiday duration

MAT Set OFF start year

MAT Set OFF accumulation allowed u/s 115JAA (3A)

MAT SET OFF Duration

Levellised Tariff (Cost OF Generation )

Year

Net Energy Sold (lakh kWhs)

Tariff (Rs/kWh)

Income From Sale of Electricity (Lakhs)

Income from REC market

Total Income

Fuel Cost

O&M

EBDIT

Book Depreciation

EBIT

Interest on term loan and Working capital

EBT

PAT

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 47

1 2 3 4 5 6 7 8 9 10

109.74 90.84 92.84 94.80 96.72 98.59 100.42 102.21 103.94 105.61

127.06 129.09 131.09 133.05 134.97 136.84 138.68 140.46 142.19 143.87

109.74 90.84 92.84 94.80 96.72 98.59 100.42 102.21 103.94 105.61

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

109.74 90.84 92.84 94.80 96.72 98.59 100.42 102.21 103.94 105.61

1 2 3 4 5 6 7 8 9 10

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

21.95 18.17 18.57 18.96 19.34 19.72 20.08 20.44 20.79 21.12

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

21.95 18.17 18.57 18.96 19.34 19.72 20.08 20.44 20.79 21.12

87.79 72.67 74.27 75.84 77.37 78.87 80.34 81.76 83.15 84.49

44.60% 36.92% 37.73% 38.53% 39.31% 40.07% 40.81% 41.54% 42.24% 42.92%

EBT

Year

Gross Income (EBT + Book Depreciation)

Taxable Income

Loss Carried Over*

Taxable Income after loss Carried Over

Years for tax holiday

PAT

Post - Tax ROE

Income Tax

MAT

Set OFF under MAT

MAT Set OFF remaining at the end of each year*****

TAX Paid (MAT or IT)

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 48

Cash Flow Sheet:

Year

0 1 2 3 4 5 6 7 8 9 10 11 12

- 105.11 110.92 112.52 114.09 115.63 117.13 118.59 120.02 121.40 122.74 110.69 111.75

196.84 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

459.29 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

656.12 105.11 110.92 112.52 114.09 115.63 117.13 118.59 120.02 121.40 122.74 110.69 111.75

656.12 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

- 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27

656.12 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27

0.00 0.00 66.84 139.49 213.73 289.55 366.90 445.76 526.07 607.82 690.94 775.41 847.83

0.00 66.84 72.65 74.25 75.82 77.35 78.85 80.32 81.74 83.13 84.47 72.42 73.48

0.00 66.84 139.49 213.73 289.55 366.90 445.76 526.07 607.82 690.94 775.41 847.83 921.31

Particulars

Life of plant and Machinery (Project life) 25

Cash Flow Calculations

Total Outflow

Opening Balance

Surplus/Defict

Closing balance

Cash Profit

Equity

Loan Amount

Total Inflow

Project Cost

Loan Repayment

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 49

Balance Sheet:

Life of Plant and Machinery (Project Life) 25 Years

0 1 2 3 4 5 6 7 8 9 10 11 12

656.12 638.80 600.55 562.30 524.05 485.79 447.54 409.29 371.04 332.79 294.53 256.28

17.32 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25

638.80 600.55 562.30 524.05 485.79 447.54 409.29 371.04 332.79 294.53 256.28 218.03

105.11 110.92 112.52 114.09 115.63 117.13 118.59 120.02 121.40 122.74 110.69 111.75

38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27

66.84 139.49 213.73 289.55 366.90 445.76 526.07 607.82 690.94 775.41 847.83 921.31

705.64 740.04 776.03 813.60 852.70 893.30 935.36 978.85 1023.73 1069.95 1104.12 1139.34

196.84 196.84 196.84 196.84 196.84 196.84 196.84 196.84 196.84 196.84 196.84 196.84 196.84

87.79 72.67 74.27 75.84 77.37 78.87 80.34 81.76 83.15 84.49 72.44 73.50

87.79 160.46 234.73 310.57 387.94 466.82 547.16 628.92 712.07 796.56 869.00 942.50

196.84 284.63 357.30 431.57 507.41 584.78 663.65 743.99 825.76 908.91 993.40 1065.84 1139.34

459.29 421.01 382.74 344.46 306.19 267.92 229.64 191.37 153.10 114.82 76.55 38.27 0.00

656.12 705.64 740.04 776.03 813.60 852.70 893.30 935.36 978.85 1023.73 1069.95 1104.12 1139.34

0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

Cash Flow from Operations

AssetsGross Fixed Assets

Less : Book Depreciation

Net Fixed Assests

Balance Sheet

Check

Principal Payment

Cash and Equivalent

Total Assets

LiabilitiesEquity Share Capital

PAT for the Year

Reserves and Surplus

Networth

Rupee Debt

Total Liabilities

ANALYSIS OF PRIME LENDING RATE OF DIFFERENT EXIM BANKS UNDER EXPORT CREDIT

Page | 50

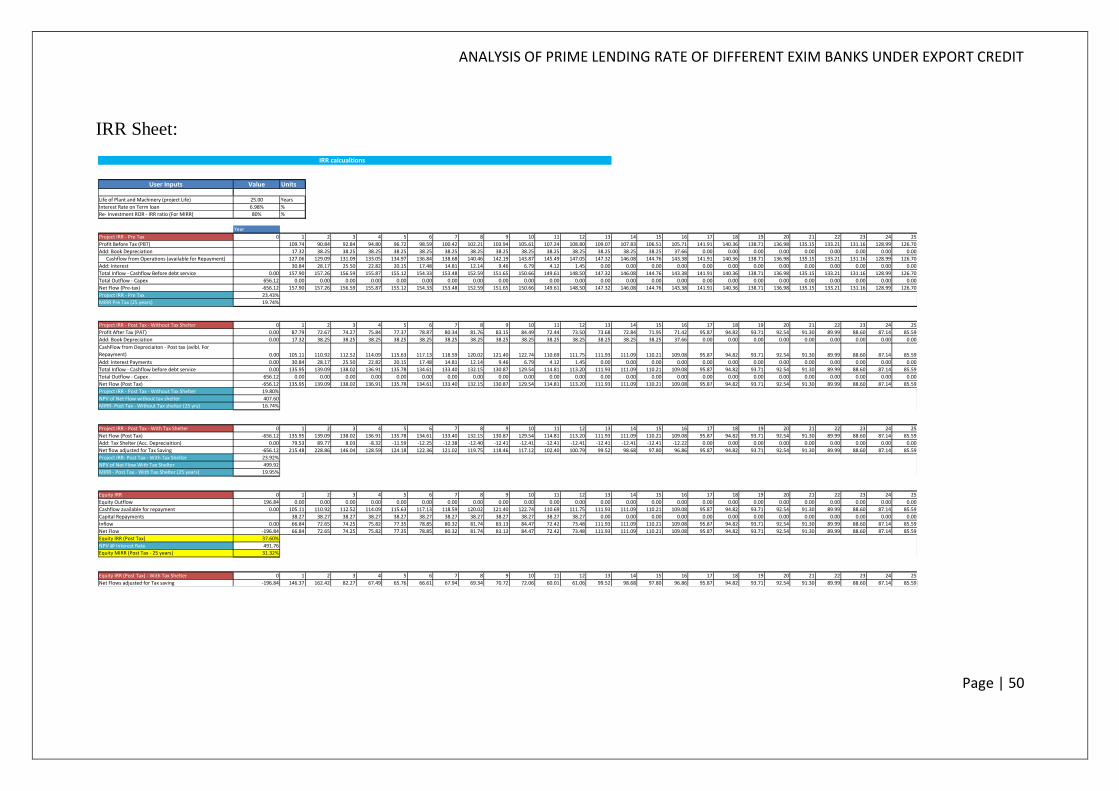

IRR Sheet:

Value Units

25.00 Years

6.98% %

80% %

Year

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

109.74 90.84 92.84 94.80 96.72 98.59 100.42 102.21 103.94 105.61 107.24 108.80 109.07 107.83 106.51 105.71 141.91 140.36 138.71 136.98 135.15 133.21 131.16 128.99 126.70

17.32 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 37.66 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

127.06 129.09 131.09 133.05 134.97 136.84 138.68 140.46 142.19 143.87 145.49 147.05 147.32 146.08 144.76 143.38 141.91 140.36 138.71 136.98 135.15 133.21 131.16 128.99 126.70

30.84 28.17 25.50 22.82 20.15 17.48 14.81 12.14 9.46 6.79 4.12 1.45 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

0.00 157.90 157.26 156.59 155.87 155.12 154.33 153.48 152.59 151.65 150.66 149.61 148.50 147.32 146.08 144.76 143.38 141.91 140.36 138.71 136.98 135.15 133.21 131.16 128.99 126.70

656.12 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

-656.12 157.90 157.26 156.59 155.87 155.12 154.33 153.48 152.59 151.65 150.66 149.61 148.50 147.32 146.08 144.76 143.38 141.91 140.36 138.71 136.98 135.15 133.21 131.16 128.99 126.70

23.43%

19.74%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

0.00 87.79 72.67 74.27 75.84 77.37 78.87 80.34 81.76 83.15 84.49 72.44 73.50 73.68 72.84 71.95 71.42 95.87 94.82 93.71 92.54 91.30 89.99 88.60 87.14 85.59

0.00 17.32 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 38.25 37.66 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

0.00 105.11 110.92 112.52 114.09 115.63 117.13 118.59 120.02 121.40 122.74 110.69 111.75 111.93 111.09 110.21 109.08 95.87 94.82 93.71 92.54 91.30 89.99 88.60 87.14 85.59

0.00 30.84 28.17 25.50 22.82 20.15 17.48 14.81 12.14 9.46 6.79 4.12 1.45 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

0.00 135.95 139.09 138.02 136.91 135.78 134.61 133.40 132.15 130.87 129.54 114.81 113.20 111.93 111.09 110.21 109.08 95.87 94.82 93.71 92.54 91.30 89.99 88.60 87.14 85.59

656.12 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

-656.12 135.95 139.09 138.02 136.91 135.78 134.61 133.40 132.15 130.87 129.54 114.81 113.20 111.93 111.09 110.21 109.08 95.87 94.82 93.71 92.54 91.30 89.99 88.60 87.14 85.59

19.80%

407.60

16.74%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

-656.12 135.95 139.09 138.02 136.91 135.78 134.61 133.40 132.15 130.87 129.54 114.81 113.20 111.93 111.09 110.21 109.08 95.87 94.82 93.71 92.54 91.30 89.99 88.60 87.14 85.59

0.00 79.53 89.77 8.03 -8.32 -11.59 -12.25 -12.38 -12.40 -12.41 -12.41 -12.41 -12.41 -12.41 -12.41 -12.41 -12.22 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

-656.12 215.48 228.86 146.04 128.59 124.18 122.36 121.02 119.75 118.46 117.12 102.40 100.79 99.52 98.68 97.80 96.86 95.87 94.82 93.71 92.54 91.30 89.99 88.60 87.14 85.59

23.92%

499.92

19.95%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

196.84 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00

0.00 105.11 110.92 112.52 114.09 115.63 117.13 118.59 120.02 121.40 122.74 110.69 111.75 111.93 111.09 110.21 109.08 95.87 94.82 93.71 92.54 91.30 89.99 88.60 87.14 85.59

38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 38.27 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00 0.00