oecd data and statistics on r&d tax incentives · · 2016-03-29oecd science, technology and...

TRANSCRIPT

OECD SCIENCE, TECHNOLOGY AND INDUSTRY SCOREBOARD 2015

OECD Data and Statistics on R&D Tax Incentives

Governments worldwide adopt various support instruments to promote business R&D. In

addition to providing grants and buying R&D services (“direct” support), many also provide fiscal

incentives. Tax incentives for business R&D expenditures include allowances and credits, as

well as other forms of advantageous tax treatment such as allowing for the accelerated

depreciation of R&D capital expenditures.

On a purchasing power parity basis, gross domestic expenditure on R&D (GERD) in the OECD

area amounted to USD 1.13 trillion in 2013, the equivalent of 2.4% of total OECD GDP.

Business R&D accounts for approximately 68% of total R&D performed in the OECD area.

In 2015, 28 of the 34 OECD countries and a number of non-OECD economies gave preferential

tax treatment to business R&D expenditures. This figure has been steadily rising over time. As

of 2013, approximately 6.9% of business R&D was directly funded by governments. R&D tax

incentives account for the equivalent of an additional 5.2% of public funding of business R&D.

Reliance on R&D tax incentives has generally increased relative to various forms of direct

support. A comparison of public support provided in 2013 and 2006 shows an increase in the

relative importance of tax incentives among 16 out of 28 countries for which data are available.

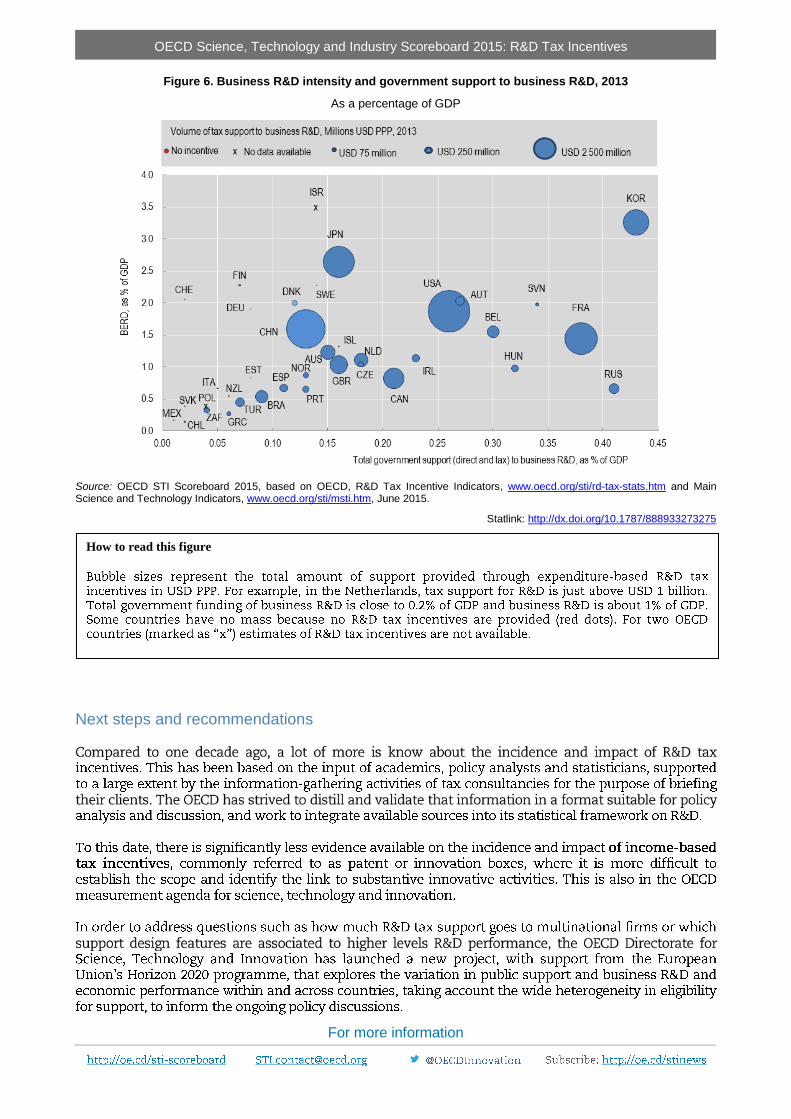

Korea, the Russian Federation and France provided the most combined support for business

R&D as a percentage of GDP in 2013, while the United States, France and China provided the

largest volumes of tax support. In relative terms, the largest amount of R&D tax support was

provided by the Netherlands – 87% as percentage of total government support – and Australia

and Canada with approximately 85%.

The combined value of this support in 2013, across the OECD and major economies (Brazil,

China, the Russian Federation and South Africa), was close to USD 50 billion, and amounted to

approximately USD 40 billion in the OECD area alone.

The design of R&D tax incentives influences the "expected" generosity of tax relief per

additional unit of R&D investment. Across OECD and partner economies providing tax relief,

there is a significant variation in tax subsidy rates for firms of different size and profitability. The

OECD median tax subsidy rate is estimated at 0.19 for profitable and of 0.13 for loss-making

SMEs, above the OECD median of 0.13 for large profitable firms and of 0.10 for large loss-

making enterprises. This result is attributable to the preferential tax treatment that currently only

12 out of OECD countries provide for SMEs or young firms vis-à-vis large firms.

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives

Key features of R&D tax incentives and rationale

Features of expenditure-based R&D tax incentives

Box 1. Tax incentives for business R&D – expenditure and income based provisions

Tax incentives for business R&D

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives

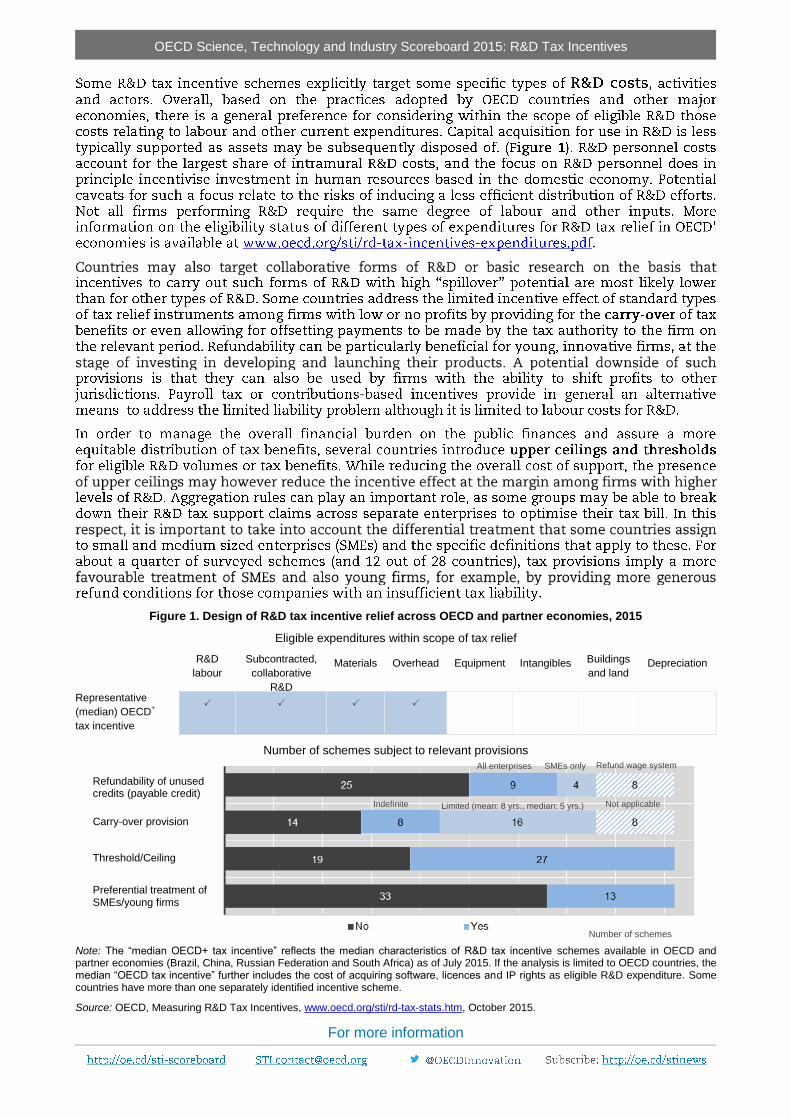

Figure 1. Design of R&D tax incentive relief across OECD and partner economies, 2015

Eligible expenditures within scope of tax relief

R&D

labour

Subcontracted,

collaborative

R&D

Materials Overhead Equipment Intangibles Buildings

and land Depreciation

Representative

(median) OECD+

tax incentive

Number of schemes subject to relevant provisions

Note: The “median OECD+ tax incentive” reflects the median characteristics of R&D tax incentive schemes available in OECD and partner economies (Brazil, China, Russian Federation and South Africa) as of July 2015. If the analysis is limited to OECD countries, the median “OECD tax incentive” further includes the cost of acquiring software, licences and IP rights as eligible R&D expenditure. Some countries have more than one separately identified incentive scheme.

Source: OECD, Measuring R&D Tax Incentives, www.oecd.org/sti/rd-tax-stats.htm, October 2015.

Number of schemes

Refundability of unused credits (payable credit)

Carry-over provision

Threshold/Ceiling

Preferential treatment of SMEs/young firms

Limited (mean: 8 yrs., median: 5 yrs.) Indefinite Not applicable

All enterprises SMEs only Refund wage system

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives

Box 2. R&D tax incentives and R&D statistics

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives

Table 1. Main features of R&D tax incentives provisions in selected OECD and non OECD countries, 2015

Expenditure-based R&D tax incentives

Corporate income tax

Social security/payroll

withholding tax R&D tax credit

R&D tax allowance Volume Incremental/hybrid

Taxable: Australia, Canada, Chile,

United Kingdom (large companies)

Non-taxable: Austria, Belgium

(incompatible with allowance),

Denmark (deficit only), France,

Iceland, Ireland, New Zealand

(deficit only), Norway, Hungary

Taxable: United States

(credit on fixed, indexed

base and incremental for

simplified credit)

Non-taxable: Italy (Legge

di Stabilità 2015), Japan,

Korea, Portugal, Spain

Non-taxable: Belgium, Brazil,

China, Czech Republic (hybrid),

Greece, Hungary, Netherlands,

Poland (R&D Centres), Russian

Federation, Slovenia, Slovak

Republic (hybrid and volume-

based), South Africa, Turkey

(hybrid), United Kingdom

Taxable: Belgium, France,

Netherlands, Hungary,

Russian Federation, Spain,

Sweden, Turkey

Treatment of excess claims

Refund

Australia (SMEs), Austria, Belgium

(after five years), Canada (SMEs),

Denmark, France (SMEs), Iceland,

Ireland, New Zealand, Norway,

United Kingdom (large companies)

Spain (reduced, payable

credit optional) United Kingdom (SMEs)

Automatic refund through

wage system

Carry-forward

Australia, Belgium, Canada, Chile,

France, Ireland

Korea, Portugal, Spain

(unreduced, non-payable

credit), United States

Belgium, China, Czech

Republic, Greece, Poland,

Netherlands, Russian

Federation, Slovenia, Slovak

republic, South Africa, Turkey,

United Kingdom

Not applicable

Enhanced tax credit/allowance rates or more favourable terms

SMEs

Australia, Canada, France, Norway

Italy (innovative start-ups),

Japan, Korea, Portugal

(start-ups)

United Kingdom

Belgium (young innovative

firms), France (JEI/JEU),

Netherlands (start-ups),

Spain (innovative SMEs)

Collaboration

France Italy, Iceland, Japan Hungary Belgium

Limitation of benefits

Threshold-dependent credit rates

Canada (SMEs), France Netherlands, Russian

Federation

Ceilings on amount of eligible R&D expenditure or value of R&D tax relief

R&D expenditure: Australia (floor

and cap), Canada (SMEs), Chile,

Denmark, Iceland, Norway

R&D tax relief: Hungary, New

Zealand (deficit only)

R&D expenditure: Italy

(floor), Portugal

(incremental)

R&D tax relief: Italy,

Japan, Korea (large firms),

Spain, United States

R&D tax relief: Hungary (R&D

collaboration), United Kingdom

R&D expenditure and R&D tax

relief: Slovak Republic (volume-

based tax allowance)

R&D expenditure: Hungary

R&D tax relief: France,

Sweden, Turkey (five year

limit)

Accelerated depreciation provisions for R&D capital

Belgium, Brazil, Chile, China, Denmark, France, Israel (non R&D specific), Poland, Russian Federation, Spain, United Kingdom

No expenditure-based R&D tax incentives

Estonia, Finland, Germany, Luxembourg, Mexico, Switzerland

Preferential tax treatment of income derived from R&D or other innovation activities

Belgium, China, France, Greece, Hungary, Ireland, Israel, Italy, Korea, Luxembourg, Netherlands, Portugal,

Russian Federation (Technology and Innovation Special Economic Zones), Spain, Switzerland (Canton of Nidwalden),

Turkey (Technology Development Zones), United Kingdom

Source: OECD, R&D Tax Incentives Database, www.oecd.org/sti/rd-tax-stats.htm, December 2015.

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives

How much financial support do governments provide through R&D tax incentives?

Tax subsidy rates

Figure 2. Implied tax subsidy rates on R&D expenditures, 2015

1-B-Index, by firm size and profit scenario

Source: OECD STI Scoreboard 2015, based on OECD, R&D Tax Incentive Indicators, www.oecd.org/sti/rd-tax-stats.htm and Main Science and Technology Indicators, www.oecd.org/sti/msti.htm, June 2015.

Statlink: http://dx.doi.org/10.1787/888933274335

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives

The value of R&D tax expenditures

Figure 3. Direct government funding of business R&D and tax incentives for R&D, 2013

As a percentage of GDP

Source: OECD STI Scoreboard 2015, based on OECD, R&D Tax Incentive Indicators, www.oecd.org/sti/rd-tax-stats.htm and Main Science and Technology Indicators, www.oecd.org/sti/msti.htm, June 2015.

Statlink: http://dx.doi.org/10.1787/888933274317

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives

Trends in R&D tax support volumes

Figure 4. Trends in government tax incentive and direct support for business R&D, 2000-13

Tax support as a percentage of total (direct and tax) government support for business R&D, selected countries

Source: OECD STI Scoreboard 2015, based on OECD, R&D Tax Incentive Indicators, www.oecd.org/sti/rd-tax-stats.htm and Main Science and Technology Indicators, www.oecd.org/sti/msti.htm, June 2015.

Statlink: http://dx.doi.org/10.1787/888933273262

How to measure the cost of R&D tax incentives

Frascati Manual

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives

Figure 5. Change in government support for business R&D through direct funding and tax incentives, 2006-13

As a percentage of total support, and annualised growth rates

Source: OECD STI Scoreboard 2015, based on OECD, R&D Tax Incentive Indicators, www.oecd.org/sti/rd-tax-stats.htm and Main Science and Technology Indicators, www.oecd.org/sti/msti.htm, June 2015.

Statlink: http://dx.doi.org/10.1787/888933274322

The relationship between government support for business R&D and R&D performance

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives

Figure 6. Business R&D intensity and government support to business R&D, 2013

As a percentage of GDP

Source: OECD STI Scoreboard 2015, based on OECD, R&D Tax Incentive Indicators, www.oecd.org/sti/rd-tax-stats.htm and Main Science and Technology Indicators, www.oecd.org/sti/msti.htm, June 2015.

Statlink: http://dx.doi.org/10.1787/888933273275

Next steps and recommendations

How to read this figure

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives

References

OECD general policy recommendations on the use of R&D tax incentives

For more information

OECD Science, Technology and Industry Scoreboard 2015: R&D Tax Incentives