now inc. (dnow) second quarter 2016 review & key takeaways

TRANSCRIPT

We Distribute Products That Deliver Energy to the World®

NOW Inc., Third Quarter 2016 Review &Key Takeaways

Statements made in the course of this presentation that state the Company's or

management's intentions, hopes, beliefs, expectations or predictions of the future are

forward-looking statements. It is important to note that the Company's actual results

could differ materially from those projected in such forward-looking statements.

Additional information concerning factors that could cause actual results to differ

materially from those in the forward-looking statements is contained from time-to-time

in the Company's filings with the U.S. Securities and Exchange Commission. Any decision

regarding the Company or its securities should be made upon careful consideration of not

only the information here presented, but also other available information, including the

information filed by the Company with the SEC. Copies of these filings may be obtained

by contacting the Company or the SEC.

3rd Quarter 2016 Earnings2

Forward Looking Statements

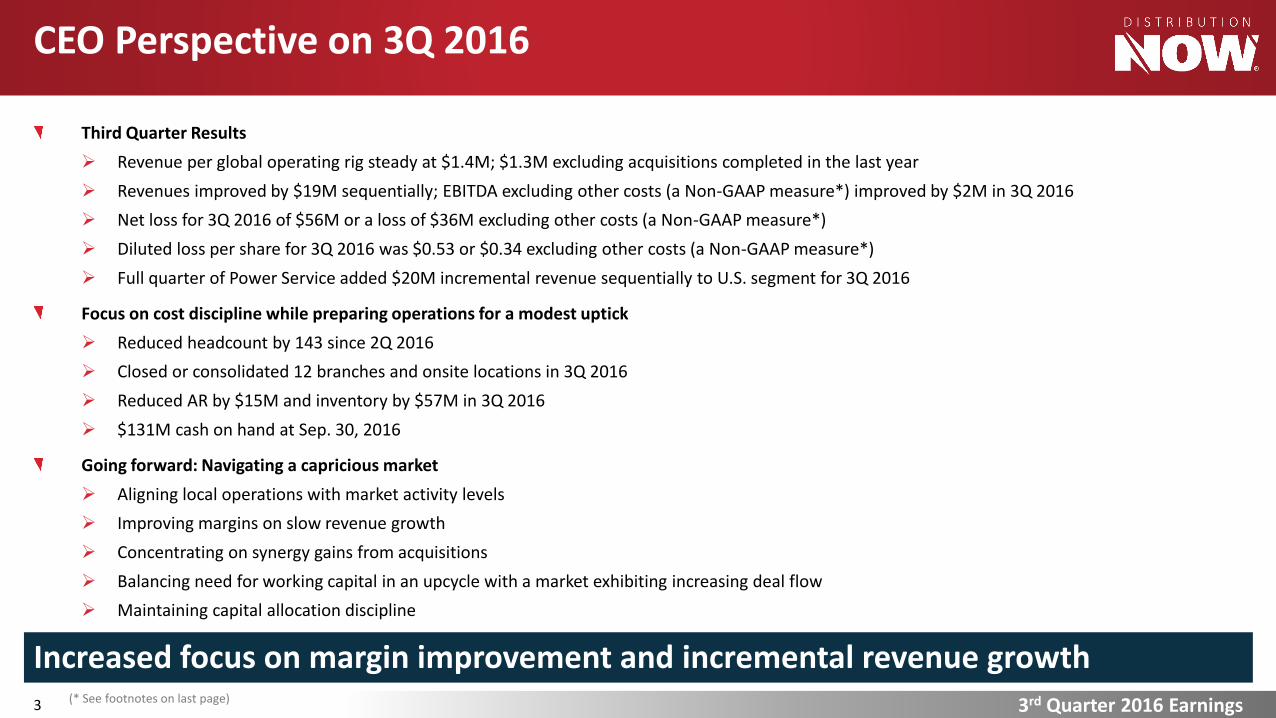

Third Quarter Results

Revenue per global operating rig steady at $1.4M; $1.3M excluding acquisitions completed in the last year

Revenues improved by $19M sequentially; EBITDA excluding other costs (a Non-GAAP measure*) improved by $2M in 3Q 2016

Net loss for 3Q 2016 of $56M or a loss of $36M excluding other costs (a Non-GAAP measure*)

Diluted loss per share for 3Q 2016 was $0.53 or $0.34 excluding other costs (a Non-GAAP measure*)

Full quarter of Power Service added $20M incremental revenue sequentially to U.S. segment for 3Q 2016

Focus on cost discipline while preparing operations for a modest uptick

Reduced headcount by 143 since 2Q 2016

Closed or consolidated 12 branches and onsite locations in 3Q 2016

Reduced AR by $15M and inventory by $57M in 3Q 2016

$131M cash on hand at Sep. 30, 2016

Going forward: Navigating a capricious market

Aligning local operations with market activity levels

Improving margins on slow revenue growth

Concentrating on synergy gains from acquisitions

Balancing need for working capital in an upcycle with a market exhibiting increasing deal flow

Maintaining capital allocation discipline

3rd Quarter 2016 Earnings3

CEO Perspective on 3Q 2016

Increased focus on margin improvement and incremental revenue growth(* See footnotes on last page)

3rd Quarter 2016 Earnings4

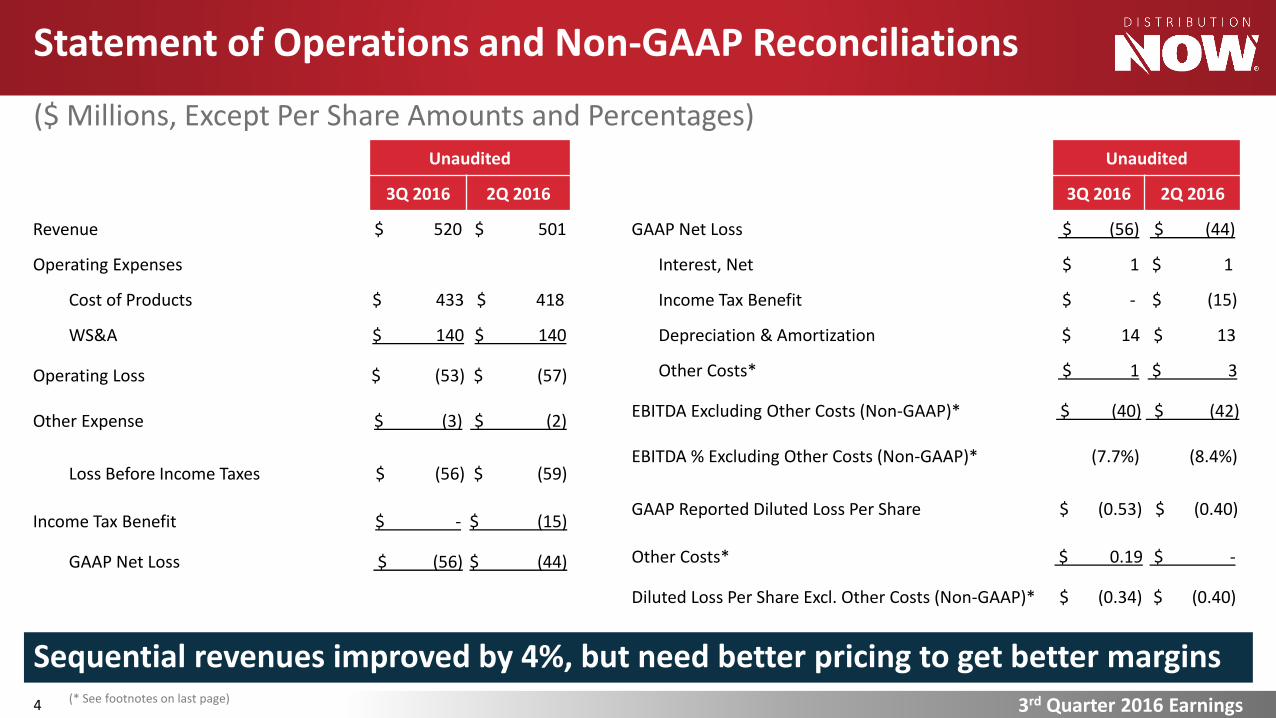

Statement of Operations and Non-GAAP Reconciliations

($ Millions, Except Per Share Amounts and Percentages)Unaudited

3Q 2016 2Q 2016

Revenue $ 520 $ 501

Operating Expenses

Cost of Products $ 433 $ 418

WS&A $ 140 $ 140

Operating Loss $ (53) $ (57)

Other Expense $ (3) $ (2)

Loss Before Income Taxes $ (56) $ (59)

Income Tax Benefit $ - $ (15)

GAAP Net Loss $ (56) $ (44)

Sequential revenues improved by 4%, but need better pricing to get better margins

Unaudited

3Q 2016 2Q 2016

GAAP Net Loss $ (56) $ (44)

Interest, Net $ 1 $ 1

Income Tax Benefit $ - $ (15)

Depreciation & Amortization $ 14 $ 13

Other Costs* $ 1 $ 3

EBITDA Excluding Other Costs (Non-GAAP)* $ (40) $ (42)

EBITDA % Excluding Other Costs (Non-GAAP)* (7.7%) (8.4%)

GAAP Reported Diluted Loss Per Share $ (0.53) $ (0.40)

Other Costs* $ 0.19 $ -

Diluted Loss Per Share Excl. Other Costs (Non-GAAP)* $ (0.34) $ (0.40)

(* See footnotes on last page)

3rd Quarter 2016 Earnings5

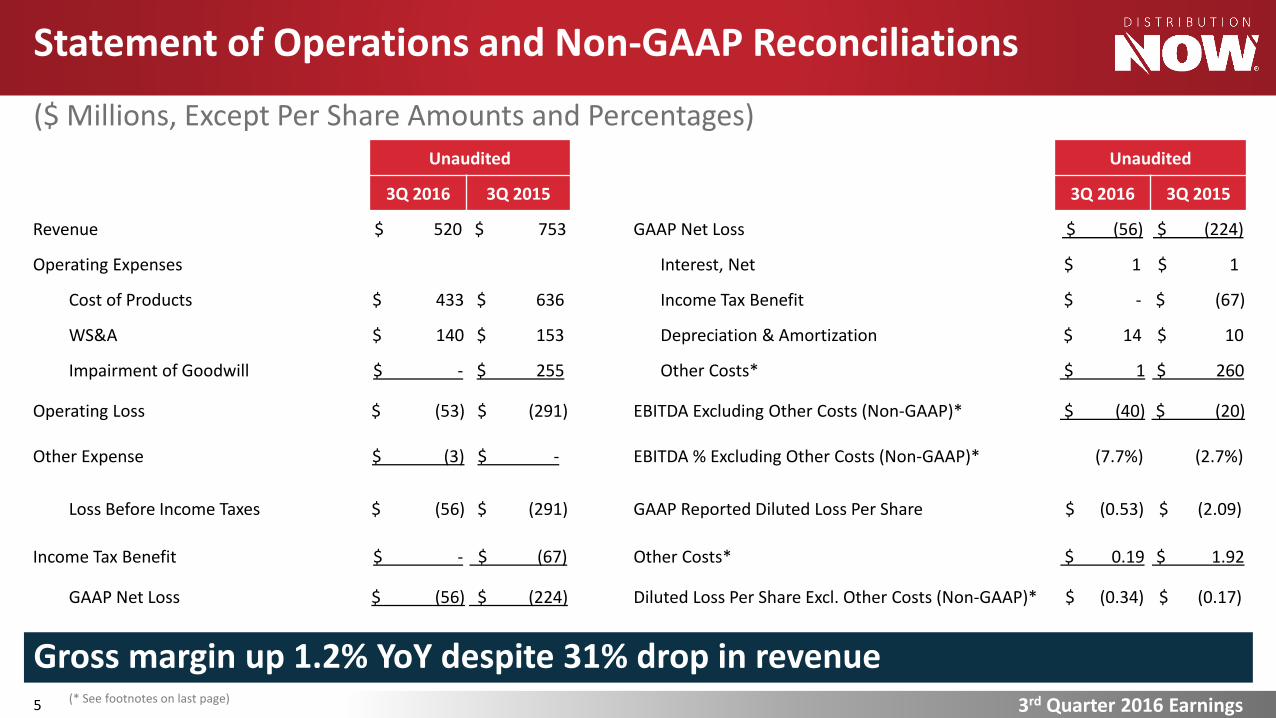

Statement of Operations and Non-GAAP Reconciliations

($ Millions, Except Per Share Amounts and Percentages)Unaudited

3Q 2016 3Q 2015

Revenue $ 520 $ 753

Operating Expenses

Cost of Products $ 433 $ 636

WS&A $ 140 $ 153

Impairment of Goodwill $ - $ 255

Operating Loss $ (53) $ (291)

Other Expense $ (3) $ -

Loss Before Income Taxes $ (56) $ (291)

Income Tax Benefit $ - $ (67)

GAAP Net Loss $ (56) $ (224)

Gross margin up 1.2% YoY despite 31% drop in revenue

Unaudited

3Q 2016 3Q 2015

GAAP Net Loss $ (56) $ (224)

Interest, Net $ 1 $ 1

Income Tax Benefit $ - $ (67)

Depreciation & Amortization $ 14 $ 10

Other Costs* $ 1 $ 260

EBITDA Excluding Other Costs (Non-GAAP)* $ (40) $ (20)

EBITDA % Excluding Other Costs (Non-GAAP)* (7.7%) (2.7%)

GAAP Reported Diluted Loss Per Share $ (0.53) $ (2.09)

Other Costs* $ 0.19 $ 1.92

Diluted Loss Per Share Excl. Other Costs (Non-GAAP)* $ (0.34) $ (0.17)

(* See footnotes on last page)

3rd Quarter 2016 Earnings6

Revenues Per Global Operating Rig

Rig Count Source: Baker Hughes, Inc.

($ Millions - QTR - Annualized)

Revenues per rig, steady as she goes

0%

5%

10%

15%

20%

25%

$-

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

1Q13 2Q 3Q 4Q 1Q14 2Q 3Q 4Q 1Q15 2Q 3Q 4Q 1Q16 2Q 3Q

Annualized Revenues Per Rig GM%

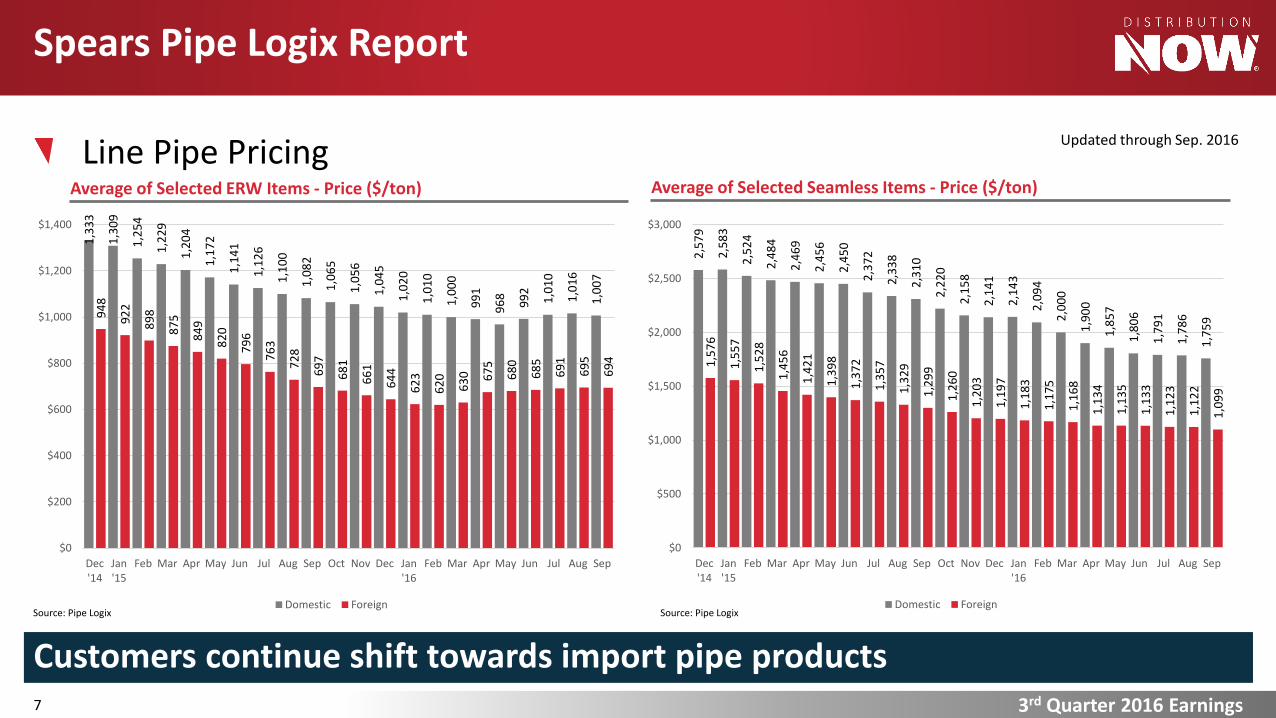

Line Pipe Pricing

3rd Quarter 2016 Earnings7

Spears Pipe Logix Report

Customers continue shift towards import pipe products

Average of Selected ERW Items - Price ($/ton) Average of Selected Seamless Items - Price ($/ton)

Source: Pipe Logix Source: Pipe Logix

Updated through Sep. 2016

1,3

33

1,3

09

1,2

54

1,2

29

1,2

04

1,1

72

1,1

41

1,1

26

1,1

00

1,0

82

1,0

65

1,0

56

1,0

45

1,0

20

1,0

10

1,0

00

99

1

96

8

99

2

1,0

10

1,0

16

1,0

07

94

8

92

2

89

8

87

5

84

9

82

0

79

6

76

3

72

8

69

7

68

1

66

1

64

4

62

3

62

0

63

0

67

5

68

0

68

5

69

1

69

5

69

4

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

Dec'14

Jan'15

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan'16

Feb Mar Apr May Jun Jul Aug Sep

Domestic Foreign

2,5

79

2,5

83

2,5

24

2,4

84

2,4

69

2,4

56

2,4

50

2,3

72

2,3

38

2,3

10

2,2

20

2,1

58

2,1

41

2,1

43

2,0

94

2,0

00

1,9

00

1,8

57

1,8

06

1,7

91

1,7

86

1,7

59

1,5

76

1,5

57

1,5

28

1,4

56

1,4

21

1,3

98

1,3

72

1,3

57

1,3

29

1,2

99

1,2

60

1,2

03

1,1

97

1,1

83

1,1

75

1,1

68

1,1

34

1,1

35

1,1

33

1,1

23

1,1

22

1,0

99

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

Dec'14

Jan'15

Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan'16

Feb Mar Apr May Jun Jul Aug Sep

Domestic Foreign

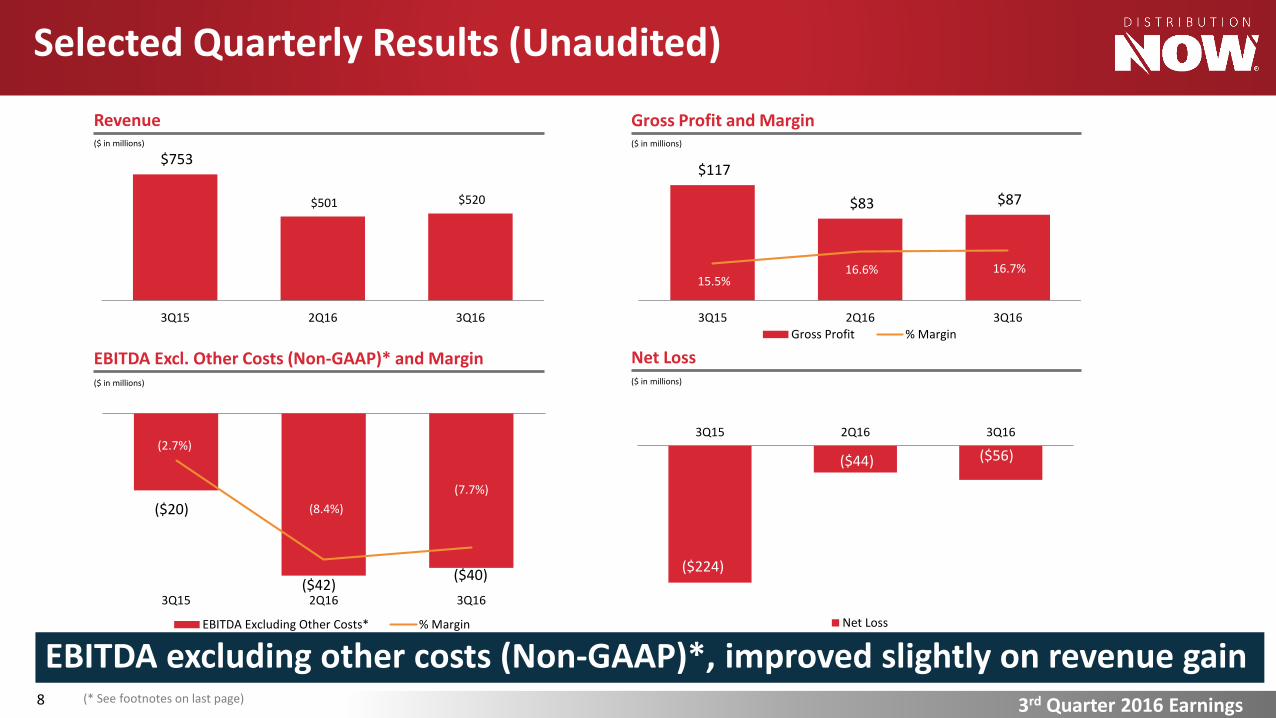

Selected Quarterly Results (Unaudited)

8

Revenue

$753

$501 $520

3Q15 2Q16 3Q16

($ in millions)

Gross Profit and Margin

$117

$83 $87

15.5% 16.6% 16.7%

3Q15 2Q16 3Q16

Gross Profit % Margin

($ in millions)

EBITDA Excl. Other Costs (Non-GAAP)* and Margin($ in millions)

Net Loss($ in millions)

($224)

($44) ($56)

3Q15 2Q16 3Q16

Net Loss

EBITDA excluding other costs (Non-GAAP)*, improved slightly on revenue gain3rd Quarter 2016 Earnings(* See footnotes on last page)

($20)

($42) ($40)

(2.7%)

(8.4%)

(7.7%)

3Q15 2Q16 3Q16

EBITDA Excluding Other Costs* % Margin

3rd Quarter 2016 Earnings

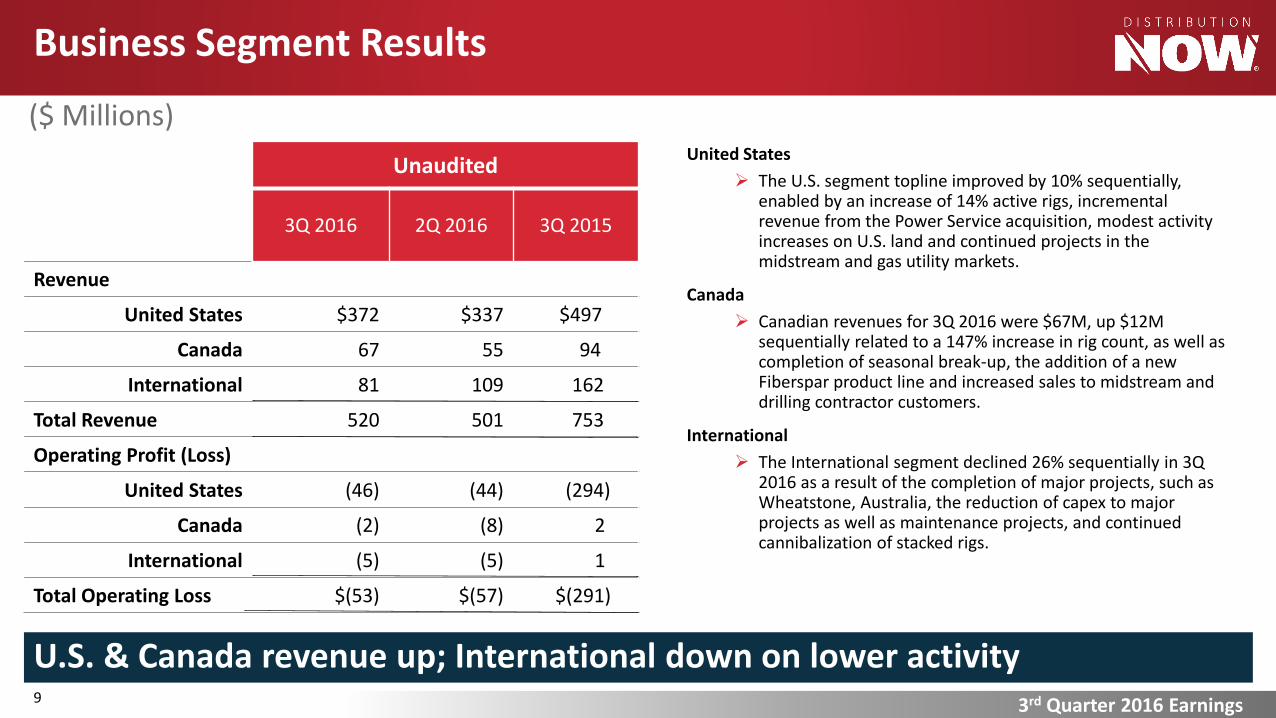

Business Segment Results

($ Millions)

Unaudited

3Q 2016 2Q 2016 3Q 2015

Revenue

United States $372 $337 $497

Canada 67 55 94

International 81 109 162

Total Revenue 520 501 753

Operating Profit (Loss)

United States (46) (44) (294)

Canada (2) (8) 2

International (5) (5) 1

Total Operating Loss $(53) $(57) $(291)

United States

The U.S. segment topline improved by 10% sequentially, enabled by an increase of 14% active rigs, incremental revenue from the Power Service acquisition, modest activity increases on U.S. land and continued projects in the midstream and gas utility markets.

Canada

Canadian revenues for 3Q 2016 were $67M, up $12M sequentially related to a 147% increase in rig count, as well as completion of seasonal break-up, the addition of a new Fiberspar product line and increased sales to midstream and drilling contractor customers.

International

The International segment declined 26% sequentially in 3Q 2016 as a result of the completion of major projects, such as Wheatstone, Australia, the reduction of capex to major projects as well as maintenance projects, and continued cannibalization of stacked rigs.

U.S. & Canada revenue up; International down on lower activity9

3rd Quarter 2016 Earnings10

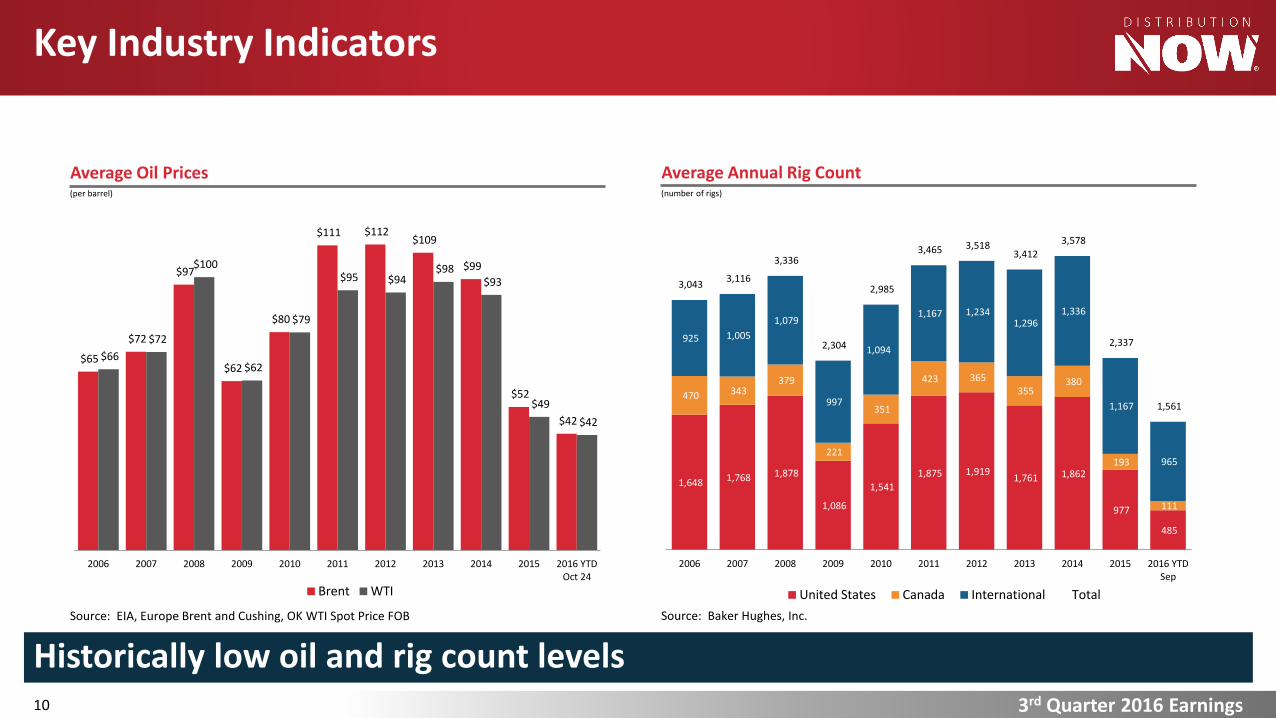

Key Industry Indicators

Average Annual Rig Count

Source: Baker Hughes, Inc.

(number of rigs)

1,648 1,768 1,878

1,086

1,541

1,875 1,919 1,761 1,862

977

485

470 343 379

221

351

423 365

355 380

193

111

925 1,005

1,079

997

1,094

1,167 1,234 1,296

1,336

1,167

965

3,043 3,116

3,336

2,304

2,985

3,465 3,518 3,412

3,578

2,337

1,561

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 YTDSep

United States Canada International Total

Average Oil Prices

Source: EIA, Europe Brent and Cushing, OK WTI Spot Price FOB

(per barrel)

$65

$72

$97

$62

$80

$111 $112 $109

$99

$52

$42

$66

$72

$100

$62

$79

$95 $94 $98

$93

$49

$42

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 YTDOct 24

Brent WTI

Historically low oil and rig count levels

3rd Quarter 2016 Earnings11

Key Industry Indicators

Recent Canada Rig Count Trends

Source: Baker Hughes, Inc., gray bars indicate 4th QTD rig count averages through Oct. 28

Recent U.S. Rig Count Trends

866

755

555

421480

543

0

100

200

300

400

500

600

700

800

900

1000

3Q15 4Q 1Q16 2Q 3Q 4QTD16

191174

164

49

121

157

0

50

100

150

200

250

3Q15 4Q 1Q16 2Q 3Q 4QTD16

Strengthening U.S. and Canada rig count trends

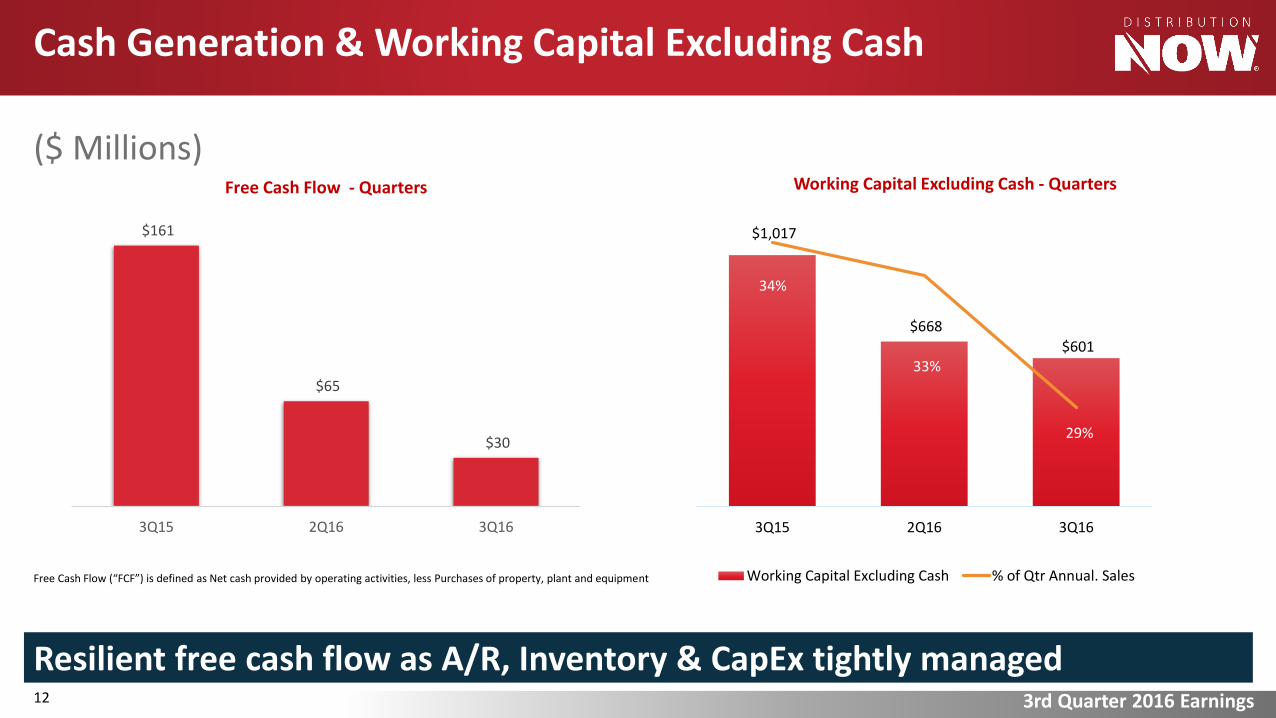

($ Millions)

Cash Generation & Working Capital Excluding Cash

Resilient free cash flow as A/R, Inventory & CapEx tightly managed

$1,017

$668

$601

34%

33%

29%

3Q15 2Q16 3Q16

Working Capital Excluding Cash % of Qtr Annual. SalesFree Cash Flow (“FCF”) is defined as Net cash provided by operating activities, less Purchases of property, plant and equipment

$161

$65

$30

3Q15 2Q16 3Q16

Free Cash Flow - Quarters Working Capital Excluding Cash - Quarters

3rd Quarter 2016 Earnings12

3rd Quarter 2016 Earnings13

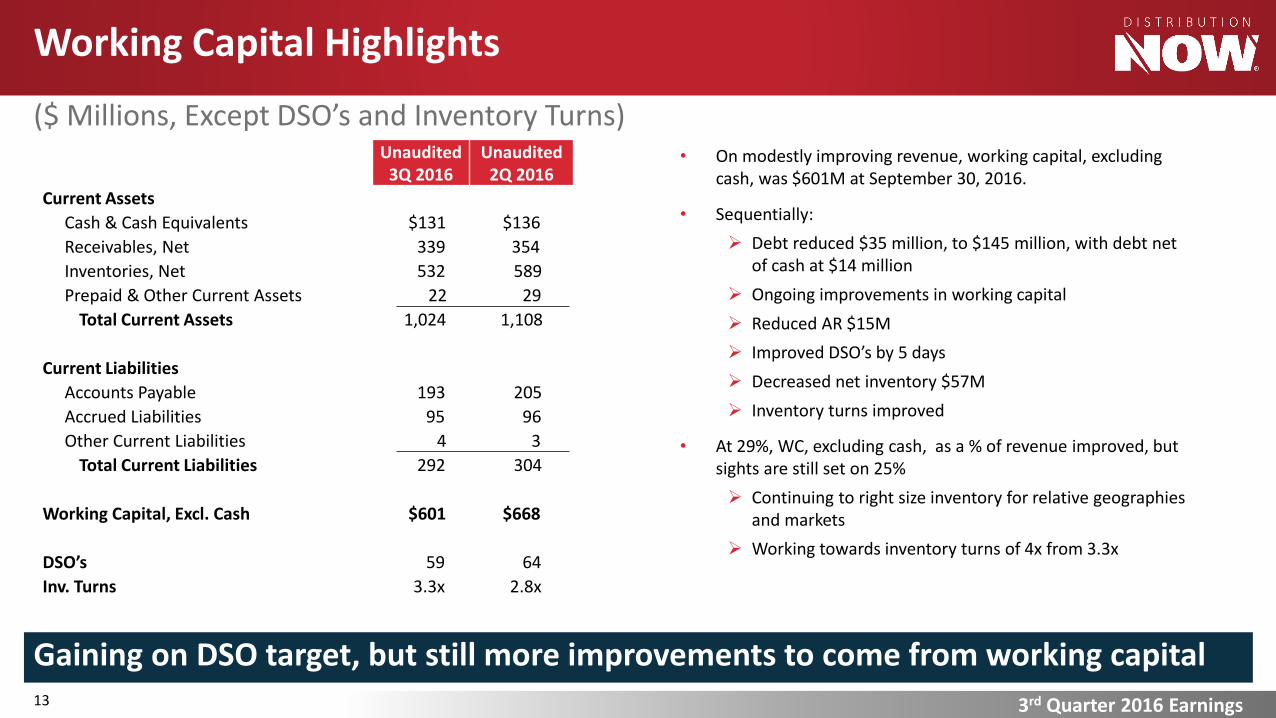

Working Capital Highlights

($ Millions, Except DSO’s and Inventory Turns)

Gaining on DSO target, but still more improvements to come from working capital

Unaudited3Q 2016

Unaudited2Q 2016

Current Assets

Cash & Cash Equivalents $131 $136

Receivables, Net 339 354

Inventories, Net 532 589

Prepaid & Other Current Assets 22 29

Total Current Assets 1,024 1,108

Current Liabilities

Accounts Payable 193 205

Accrued Liabilities 95 96

Other Current Liabilities 4 3

Total Current Liabilities 292 304

Working Capital, Excl. Cash $601 $668

DSO’s 59 64

Inv. Turns 3.3x 2.8x

• On modestly improving revenue, working capital, excluding cash, was $601M at September 30, 2016.

• Sequentially:

Debt reduced $35 million, to $145 million, with debt net of cash at $14 million

Ongoing improvements in working capital

Reduced AR $15M

Improved DSO’s by 5 days

Decreased net inventory $57M

Inventory turns improved

• At 29%, WC, excluding cash, as a % of revenue improved, but sights are still set on 25%

Continuing to right size inventory for relative geographies and markets

Working towards inventory turns of 4x from 3.3x

2,0

14

1,9

76

1,9

35

1,7

82

1,5

53

1,3

20

1,1

05

99

5

91

8

89

5

93

1

98

0

1,0

09

1,0

44

1,1

07

1,1

72

1,2

67

1,3

50

1,4

19

1,4

79

1,5

13

1,5

31

1,5

73

1,6

38

1,6

55

1,6

68

1,6

83

1,7

11

1,9

30

1,9

25

1,9

25

1,8

82

1,6

83

1,3

48

1,1

10

97

6

88

9

86

1

86

6

88

3

84

8

79

1

76

0

71

4

65

4

53

2

47

8

43

7

40

8

41

7

44

9

48

1

50

9

54

3

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Pea

k

Mo

1

Mo

2

Mo

3

Mo

4

Mo

5

Mo

6

Mo

7

Mo

8

Mo

9

Mo

10

Mo

11

Mo

12

Mo

13

Mo

14

Mo

15

Mo

16

Mo

17

Mo

18

Mo

19

Mo

20

Mo

21

Mo

22

Mo

23

Mo

24

Mo

25

Mo

26

Mo

27

2008/2009/2010 - Peak Sep 2008 2014/2015/2016 - Peak Sep 2014

$1

34

$1

33

$1

17

$1

04

$7

7

$5

7

$4

1

$4

2

$3

9 $

48

$5

0 $

59

$7

0

$6

4 $7

1

$6

9 $7

6

$7

8

$7

4

$7

8

$7

6

$8

1

$8

4

$7

4

$7

5

$7

6

$7

7

$7

5 $8

2

$1

06

$1

04

$9

7

$9

3

$8

4

$7

6

$5

9

$4

7

$5

1

$4

8 $5

4

$5

9

$6

0

$5

1

$4

3

$4

5

$4

6

$4

2

$3

7

$3

2

$3

0 $3

8

$4

1 $4

7

$4

9

$4

5

$4

5

$4

5

$5

0

$-

$20

$40

$60

$80

$100

$120

$140

$160

Pea

k

Mo

1

Mo

2

Mo

3

Mo

4

Mo

5

Mo

6

Mo

7

Mo

8

Mo

9

Mo

10

Mo

11

Mo

12

Mo

13

Mo

14

Mo

15

Mo

16

Mo

17

Mo

18

Mo

19

Mo

20

Mo

21

Mo

22

Mo

23

Mo

24

Mo

25

Mo

26

Mo

27

Mo

28

2008/09/10 - Peak June 2008 2014/15/16 - Peak June 2014

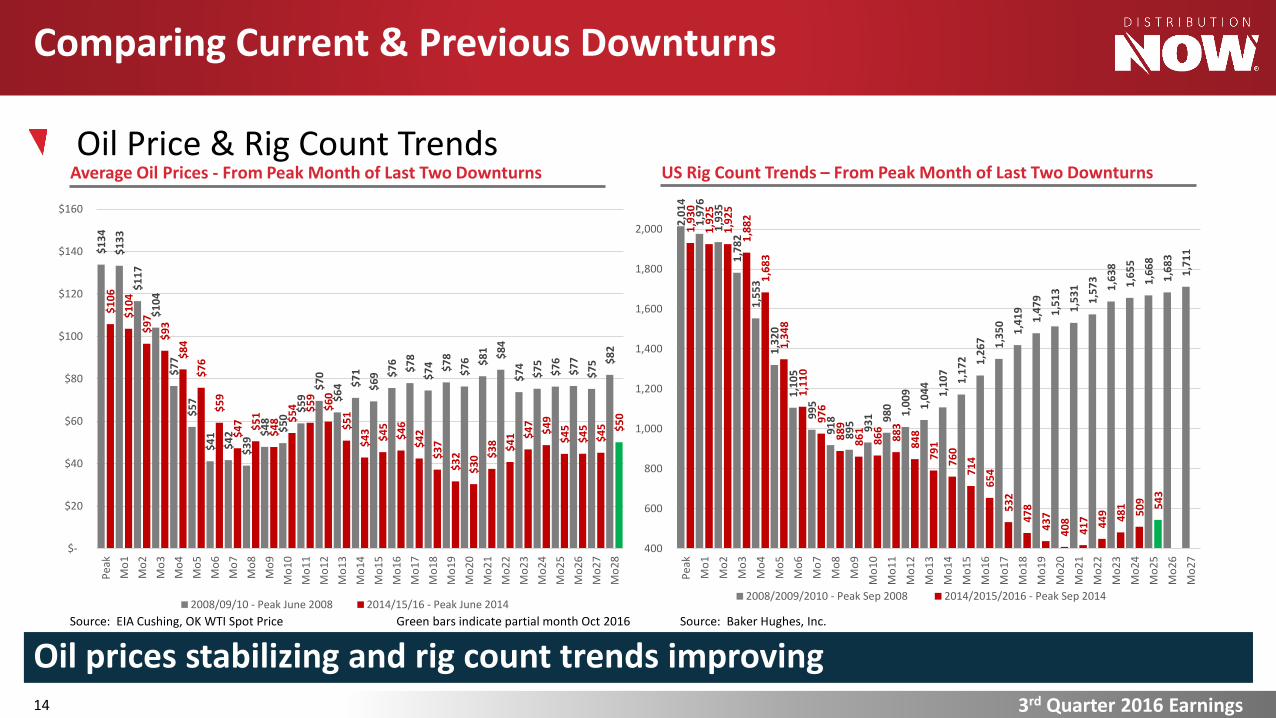

Oil Price & Rig Count Trends

3rd Quarter 2016 Earnings14

Comparing Current & Previous Downturns

US Rig Count Trends – From Peak Month of Last Two Downturns

Source: Baker Hughes, Inc.

Average Oil Prices - From Peak Month of Last Two Downturns

Source: EIA Cushing, OK WTI Spot Price

Oil prices stabilizing and rig count trends improvingGreen bars indicate partial month Oct 2016

3rd Quarter 2016 Earnings15

EBITDA, Net Income and Diluted EPS Excl. Other Costs Footnotes

* See referenced schedules on slides 3, 4, 5 & 8

(1) In an effort to provide investors with additional information regarding our results as determined by GAAP, we disclose various non-GAAP

financial measures in our quarterly earnings press releases and other public disclosures. The non-GAAP financial measures include: (i) earnings

before interest, taxes, depreciation and amortization (EBITDA) excluding other costs, (ii) net loss excluding other costs and (iii) diluted loss per

share excluding other costs. Each of these financial measures excludes the impact of certain other costs and therefore has not been calculated in

accordance with GAAP. A reconciliation of each of these non-GAAP financial measures to its most comparable GAAP financial measure is

included in the Earnings Release.

(2) For the three and nine months ended September 30, 2016, other costs primarily includes the transaction costs associated with acquisition

activity, including the cost of inventory that was stepped up to fair value during purchase accounting related to acquisitions and severance

expenses which are included in operating loss. For the three and nine months ended September 30, 2015, other costs additionally includes the

estimated goodwill impairment charge of $255 million.

(3) EBITDA % excluding other costs is defined as EBITDA excluding other costs divided by Revenue.

(4) Other costs, net of tax, for the three and nine months ended September 30, 2016 and 2015 included expenses of $19 million, $39 million, nil

and nil, after tax, respectively, for a valuation allowance recorded against the Company’s deferred tax assets; as well as, $1 million, $6 million,

$206 million and $215 million, after tax, respectively, in transaction costs associated with acquisitions, including the cost of inventory that was

stepped up to fair value during purchase accounting related to acquisitions, and severance expenses, as well as, impairment charges associated

with the fair value of goodwill, which are included in operating loss. Other costs, net of tax, for the second quarter of 2016 included $3 million, after

tax, in acquisition-related and severance charges and a net $3 million after-tax benefit related to a deferred tax asset valuation allowance release.

Other costs, net of tax, was less than $1 million, after tax, for the three months ended June 30, 2016.

(5) Per share amounts may not foot due to rounding.