not all mlps are created equal - cfra research cfra hannink mlp... · not all mlps are created...

TRANSCRIPT

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 1

Not All MLPs are Created Equal A discussion on energy master limited partnerships + identifying related accounting risks

Julie Hilt Hannink, CFA Energy Sector Lead | +1 616.517.2462 [email protected] AUGUST 22, 2013

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 2

Why MLP accounting matters

General Partner and management

discretion over Distributable Cash

Flow (DCF) calculation and the

resulting Distribution Coverage

calculation means there is the

potential for MLPs to use various

adjustments and tricks to overstate

their ability to sustain and grow

distribution, the key MLP

fundamental.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 3

Expect SEC focus

A reshuffling at the Securities & Exchange Commission (SEC) enforcement division is expected to increase the focus on accounting fraud.

Non-GAAP metrics are expected to be front and center as part of the SEC’s potential crack-down on fraud and financial disclosure concerns.

The SEC’s Accounting Quality Model searches the filings of more than 9,000 companies, with one search point being big differences between net income and actual cash outflows available to investors.

The non-GAAP DCF figures can allow large cash distributions even if reported GAAP income and cash flow from operations (CFFO) results are weak.

The Linn Energy (LINE) SEC informal inquiry includes derivative accounting, non-GAAP metrics and the Berry Petroleum (BRY) merger.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 4

MLPs decade of growth

National Association of Publicly Traded Partnerships reports a universe of more than 100 MLPs with a total market capitalization in excess of $450 billion.

Growth drivers:

Not all MLPs will make it and you can bet given so much management discretion there will be some stumbles. CFRA can help identify them before they fall.

• Universe size • Unit price performance • Asset classes

• Alternatives • MLP mutual funds • Exchange-traded funds • I-units

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 5

MLPs defined

Partnerships are typically two-tiered structures with the operating MLP owned

2% by the GP and 98% publicly held by LP unit holders.

Owners of these pass-through entities must treat part of the distribution as current taxable income and the rest as a return of capital.

GPs are typically owned by a sponsoring corporation that is can be publicly traded but there are some GPs owned directly by the public or are privately held.

Unlike other pass-through entities, royalty trusts or REITs, MLPs do not have statutory minimum distributions

Most MLPs are engaged in energy and natural resource operations with midstream businesses (gathering, transport, storage and processing of oil, natural gas and natural gas liquids) being the most common.

MLP operations are now more aggressively expanding into other areas including upstream energy, fertilizer manufacture, oil services and carbon dioxide operations.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 6

Why MLPs are attractive to investors

High yields – current average is around 6%

Current tax shelter

Unit price appreciation

Midstream MLPs tend to have the most stable yields given:

• infrastructure nature

• stable cash flows

• fee-oriented revenue streams

• high barriers to entry

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 7

Why MLPs are attractive to sponsors

Attractive “sales” price since MLPs have a lower cost of capital so can pay more for contributed assets

Ability to redeploy cash

Retention of ownership interest

Incentive distributions for growing distribution rate

Reimbursement of certain costs

Payment of management fees

Limited fiduciary responsibilities to unitholders

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 8

Energy Investment supporting MLP growth

Projected US infrastructure spending needs at $50-$300 billion+ ... MLP structure is a key investment vehicle for this growth.

CFRA’s caveat is that the market can change relatively quickly – the attached map from 2011 that shows the US LNG inflows – those terminals were thought to be imperative for US energy security just 7 years ago but today are being relicensed as export facilities.

Source: INGAA

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 9

Energy Investment Needed, Supporting MLP Growth

Source: Geology.com

Although rails will remain an important transport option, additional oil shale pipelines needed

Half of all oil coming out of the Bakken is transported by rail vs. a third by pipe.

The train that crashed in Lac-Megantic, Quebec was carrying Bakken crude.

Offset to increased pipeline is that rails are more flexible.

Source: EIA

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 10

Shales Driving Growth: EIA Processing Plants 2009

Source: EIA

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 11

Non-traditional Energy MLPs Commodity-oriented asset classes:

E&P

Fertilizer

Refining

Oil Services

Variable rate distributions

CVR Partners LP (UAN) – Nitrogen fertilizer from petroleum coke

CVR Refining LP (CVRR) – Refining & logistics

Alon USA Partners, LP (ALDW)-- Refining

Northern Tier Energy LP (NTI) – Refining & Fuel Distribution

Terra Nitrogen Company, LP (TNH) – Nitrogen fertilizer from natural gas

Dorchester Minerals LP (DMLP) – Royalty Interests

Rentech Nitrogen Partners , LP (RNF) – Nitrogen fertilizer

PetroLogistics LP (PDH) – Processes propane in propylene

Numerous 2012 IRS private letter rulings expanded qualifying income

Renewables potential with introduction of Master Limited Partner Parity Act

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 12

Along with Growth Potential Comes Risk

Economic Higher interest rates create competition

Higher interest rates increase cost structure

Regulatory Fracking/EPA/Environmental

Focus on renewables

Tax status

Industry Technology

Geology

Geopolitics/Fiscal Regimes

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 13

MLPs within CFRA’s Accounting Lens

MLPs are no different than any other sector, industry, or geography.

CFRA screens and analyzes MLP financial reports and disclosures to determine if the choices made by the MLP conceal the underlying position of the entity.

For MLPs our reviews seek to determine if distribution rates can be maintained and grow as promised by management.

IDR Relinquishment – similar to distribution cut

CFRA wants to determine if the MLP’s GAAP and non-GAAP metrics properly reflect its financial position.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 14

CFRA MLP Research

Educational/Industry

10 Questions to Ask MLP Managements – June 12, 2013

E&P: Alternatives to Raising Capital- July 24, 2013

Accounting Notebooks

Enterprise Products Partners LP (EPD) -7/24/13

Linn Energy LLC (LINE) -7/24/13

Kinder Morgan Energy Partners (KMP) – 7/18/13

Accounting Lens

Kinder Morgan Energy Partners (KMP) – 11/26/07

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 15

MLPs that Fall Within CFRA Market Cap Screens

T icker C o mpany N ame Secto r

ACM P Access M idstream Partners LP M idstream

ATLS Atlas Energy L.P. M idstream

APL Atlas Pipeline Partners L.P. M idstream

BWP Boardwalk P ipeline Partners L.P. M idstream

BPL Buckeye Partners L.P. M idstream

CQP Cheniere Energy Partners L.P. M idstream

CM LP Crestwood M idstream Partners LP M idstream

DPM DCP M idstream Partners L.P. M idstream

EROC Eagle Rock Energy Partners L.P. M idstream

EPB El Paso Pipeline Partners L.P. M idstream

EEP Enbridge Energy Partners L.P. Cl A M idstream

ETE Energy Transfer Equity L.P. M idstream

ETP Energy Transfer Partners L.P. M idstream

EPD Enterprise Products Partners L.P. M idstream

GEL Genesis Energy L.P. M idstream

HEP Holly Energy Partners L.P. M idstream

NRGY Inergy L.P. M idstream

KM P Kinder M organ Energy Partners L.P. M idstream

M M P M agellan M idstream Partners L.P. M idstream

M WE M arkWest Energy Partners L.P. M idstream

M M LP M artin M idstream Partners L.P. M idstream

M PLX M PLX LP M idstream

NGL NGL Energy Partners LP M idstream

OKS ONEOK Partners L.P. M idstream

PNG PAA Natural Gas Storage L.P. M idstream

PAA Plains All American Pipeline L.P. M idstream

PVR PVR Partners L.P. M idstream

RGP Regency Energy Partners L.P. M idstream

SEP Spectra Energy Partners L.P. M idstream

SXL Sunoco Logistics Partners L.P. M idstream

NGLS Targa Resources Partners L.P. M idstream

TCLP TC PipeLines L.P. M idstream

TLLP Tesoro Logistics LP M idstream

WGP Western Gas Equity Partners LP M idstream

WES Western Gas Partners LP M idstream

WPZ Williams Partners L.P. M idstream

T icker C o mpany N ame Secto r

ARLP Alliance Resource Partners L.P. Coal & Consumable Fuels

NRP Natural Resource Partners L.P. Coal & Consumable Fuels

EXLP Exterran Partners L.P. Oil & Gas Equipment & Services

USAC USA Compression Partners LP Oil & Gas Equipment & Services

ARP Atlas Resource Partners LP Oil & Gas Exploration & Production

BBEP BreitBurn Energy Partners L.P. Oil & Gas Exploration & Production

EVEP EV Energy Partners L.P. Oil & Gas Exploration & Production

LGCY Legacy Reserves L.P. Oil & Gas Exploration & Production

LINE Linn Energy LLC Oil & Gas Exploration & Production

M EM P M emorial Production Partners L.P. Oil & Gas Exploration & Production

QRE QR Energy L.P. Oil & Gas Exploration & Production

ALDW Alon USA Partners L.P. Oil & Gas Refining & M arketing

CLM T Calumet Specialty Products Partners L.P. Oil & Gas Refining & M arketing

XTEX Crosstex Energy L.P. Oil & Gas Refining & M arketing

CVRR CVR Refining LP Oil & Gas Refining & M arketing

NTI Northern Tier Energy LP Cl A Oil & Gas Refining & M arketing

NS NuSTAR Energy L.P. Oil & Gas Refining & M arketing

GM LP Golar LNG Partners LP LNG Floating Platforms

TGP Teekay LNG Partners L.P. LNG & Crude Carriers

TOO Teekay Offshore Partners L. P. Shuttle Tankers

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 16

MLPs & Screening

Accounting and financial reporting techniques that may mislead investors about a company’s financial performance or economic health:

Earnings: Adjusting accrual-based performance numbers by managing reported revenue and expenses

GAAP earnings pale in comparison to cash flow due to MLPs main purpose of distributing cash to unit holders

Cash Flow: Employing techniques to report misleadingly high operating cash flow and free cash flow

MLPs focus on cash available for distribution (CAD) or distributable cash flow (DCF) vs. cash flow from operations (CFFO) or GAAP free cash flow (FCF); however, need to access capital markets means CFFO is a key screening tool.

Key Metrics: Misusing accepted non-GAAP metrics or creating misleading ones to overstate performance or distort economic health.

CAD/DCF and Distribution Coverage are the central non-GAAP key metrics for MLPs

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 17

MLPs within CFRA’s Accounting Lens

When analyzing these partnerships it is crucial to:

Review GAAP items due to continued need to access capital markets to fund growth

Analyze non-GAAP items due to the need to maintain and/or grow LP distribution rates

Key non-GAAP metrics:

Distributable Cash Flow (DCF)/ Cash Available for Distribution (CAD)

Maintenance/Sustaining Capital Spending (Capex)

Distribution Coverage

A High Level of Management Discretion:

DCF/CAD and Maintenance Capex are either defined in the operating or partnership agreement

Limited fiduciary responsibilities of GP to LP unitholders.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 18

Distributions Could be at Risk if an MLP . . .

Operational

Is unable to maintain or attain planned growth benchmarks

Needs access to debt markets as interest rate spikes

Issues excessive LP units

Accounting

Changes how DCF/CAD is calculated.

Has difficulty maintaining a coverage ratio above 100%.

Maintains a 100% or more coverage ratio by lowering indicated maintenance capex levels.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 19

10 Questions to Ask MLP Management – an Update

1. What is the definition of

DCF/CAD?.

2. What is the Distribution

Coverage ratio?

3. What is the break-out of Fee

vs. Commodity exposure?

4. How is the

Sustaining/Maintenance Capex

determined?

5. How many distributions do

current cash balances cover?

6. What is the ownership

structure?

7. How are service costs and

reimbursements allocated

between related parties?

8. How has the MLP grown?

9. How has growth been funded

and is there a target level of

debt?

10.What are the governance

policies?

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 20

1. Definition of DCF/CAD?

Not always easy to find

Many companies provide the adjustment to Adjusted EBITDA and then

adjust this Non-GAAP figure to arrive at DCF/CAD.

The problem – many of the adjustments are not decipherable from

looking at the either the press release or the SEC filings.

Complicating matters are things such as:

Incentive Distribution Rights (IDRs)

Relinquishment of IDRS

GP income

Traditional DCF = Net Income + (DD&A – Maintenance Capex)

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 21

1. Definition of DCF/CAD?

6/30/13 6/30/12 6/30/13 6/30/12

Net income before certain items $ 627

$ 467

$ 1,282

$ 1,001

Less: Noncontrolling Interest before certain items (7 ) (5 ) (14 ) (11 )

Net income attributable to KMP before certain items 620

462

1,268

990

Less: General Partner’s interest in net income before certain items

(13) (418 ) (337 ) (819 ) (658 )

Limited Partners’ net income before certain items 202

125

449

332

Depreciation, depletion and amortization (14) 379

292

717

582

Book (cash) taxes - net —

(2 ) 12

7

Express & Endeavor contribution (6 ) 3

(5 ) 3

Sustaining capital expenditures (15) (70 ) (52 ) (118 ) (96 )

DCF before certain items $ 505

$ 366

$ 1,055

$ 828

Net income / unit before certain items $ 0.49

$ 0.37

$ 1.14

$ 0.98

DCF / unit before certain items $ 1.22

$ 1.07

$ 2.67

$ 2.44

Weighted average units outstanding 413

342

395

340

Three months Ended

Six Months Ended

For some MLPs, clear disclosure and easy to follow the adjustments. A good example is Kinder Morgan Energy Partners (KMP) as shown by this excerpt from its 2Q13 Press Release.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 22

1. Definition of DCF/CAD? In contrast to the clear KMP disclosure, here is a summary of the Energy Transfer Partners (ETP), DCF disclosure. Beginning in 1Q13, ETP simplified its calculation but a significant portion of the DCF is tied to its subsidiaries so they need to be analyzed as well. ETP also changed how it calculated DCF in 4Q12.

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Net Income/ Adjusted EBITDA Beg 1Q12 247.2 156.6 76.1 217.3 494.0 642.0 660.0 948.0 956.0 1,069.0

Amort. Finance Cost in Int Exp 2.3 2.4 2.5 2.7 0.0 0.0 0.0 0.0 0.0 0.0

Deferred Income Tax 1.6 (0.0) 0.4 2.1 0.0 0.0 0.0 0.0 0.0 0.0

Depreciation 89.5 98.5 106.4 110.3 0.0 0.0 0.0 0.0 0.0 0.0

Loss on Debt Extinguishment 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Non-Cash Compensation 10.2 10.6 10.4 6.3 0.0 0.0 0.0 0.0 0.0 0.0

Gain on Asset Sales/Deconsolid. 1.7 0.5 1.0 (0.0) 0.0 0.0 0.0 0.0 0.0 0.0

Unrealized deriv (gains) Losses - Inter (1.0) (7.5) 79.0 12.7 0.0 0.0 0.0 0.0 0.0 0.0

AFUD 1.1 (1.2) (0.6) (0.3) 0.0 0.0 0.0 0.0 0.0 0.0

Unrealized deriv (gains) Losses - Comm (7.1) (0.6) 6.4 12.6 0.0 0.0 0.0 0.0 0.0 0.0

Impairments 0.0 0.0 5.4 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Distribution (<) > Earnings Unconsold 4.7 (2.8) 16.0 6.9 0.0 0.0 0.0 0.0 0.0 0.0

DCF for non-controlling 0.0 (10.1) (11.9) (13.3) 0.0 0.0 0.0 0.0 0.0 0.0

Adjusted EBITDA Unconsolidated Subs (99.0) (97.0) (106.0) (178.0) (165.0) (158.0)

Distributions Unconsolidated Subs 42.0 67.0 81.0 72.0 95.0 102.0

Interest Expense Net of capitalized (141.0) (191.0) (147.0) (186.0) (211.0) (211.0)

Income Tax (2.0) (7.0) (27.0) (27.0) (3.0) (89.0)

Maintance Capex (19.6) (29.5) (31.4) (53.6) (24.0) (77.0) (69.0) (143.0) (51.0) (121.0)

Other 6.5 6.5 6.5 6.7 1.0 0.0 0.0 2.0 1.0 1.0

DCF 337.1 223.3 266.1 310.4 271.0 337.0 392.0 488.0 622.0 593.0

DCF attributable to SXL 0.0 0.0 0.0 0.0 0.0 0.0 0.0 (165.0) (195.0) (184.0)

Distributions from SXL 0.0 0.0 0.0 0.0 0.0 0.0 0.0 41.0 45.0 49.0

Distributions to ETE respect to LoneStar 0.0 0.0 0.0 0.0 0.0 0.0 0.0 (75.0) (50.0) 0.0

Distributions to RGP respect to LoneStar 0.0 0.0 0.0 0.0 (11.0) (21.0) (14.0) (17.0) (23.0) (16.0)

DCF attributable to ETP Partners 337.1 223.3 266.1 310.4 260.0 316.0 378.0 272.0 399.0 442.0

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 23

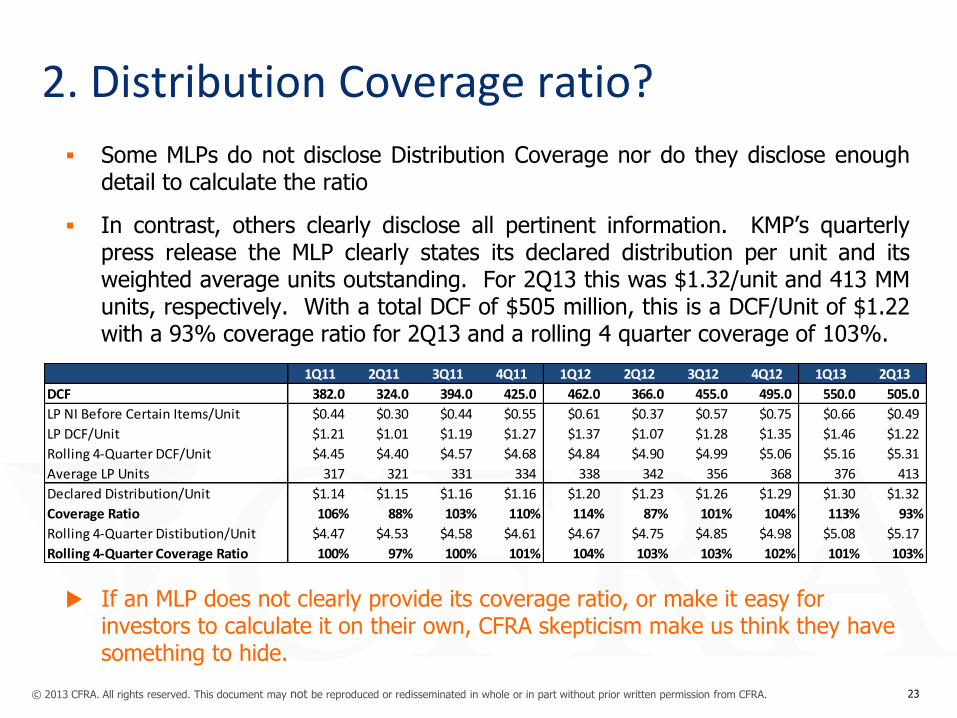

2. Distribution Coverage ratio?

Some MLPs do not disclose Distribution Coverage nor do they disclose enough detail to calculate the ratio

In contrast, others clearly disclose all pertinent information. KMP’s quarterly press release the MLP clearly states its declared distribution per unit and its weighted average units outstanding. For 2Q13 this was $1.32/unit and 413 MM units, respectively. With a total DCF of $505 million, this is a DCF/Unit of $1.22 with a 93% coverage ratio for 2Q13 and a rolling 4 quarter coverage of 103%.

If an MLP does not clearly provide its coverage ratio, or make it easy for investors to calculate it on their own, CFRA skepticism make us think they have something to hide.

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

DCF 382.0 324.0 394.0 425.0 462.0 366.0 455.0 495.0 550.0 505.0

LP NI Before Certain Items/Unit $0.44 $0.30 $0.44 $0.55 $0.61 $0.37 $0.57 $0.75 $0.66 $0.49

LP DCF/Unit $1.21 $1.01 $1.19 $1.27 $1.37 $1.07 $1.28 $1.35 $1.46 $1.22

Rolling 4-Quarter DCF/Unit $4.45 $4.40 $4.57 $4.68 $4.84 $4.90 $4.99 $5.06 $5.16 $5.31

Average LP Units 317 321 331 334 338 342 356 368 376 413

Declared Distribution/Unit $1.14 $1.15 $1.16 $1.16 $1.20 $1.23 $1.26 $1.29 $1.30 $1.32

Coverage Ratio 106% 88% 103% 110% 114% 87% 101% 104% 113% 93%

Rolling 4-Quarter Distibution/Unit $4.47 $4.53 $4.58 $4.61 $4.67 $4.75 $4.85 $4.98 $5.08 $5.17

Rolling 4-Quarter Coverage Ratio 100% 97% 100% 101% 104% 103% 103% 102% 101% 103%

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 24

3. Break-out of Fee vs. Commodity Exposure? Investors need to understand what they are buying and it is not always easy to ascertain without management disclosure.

Becomes even more problematic once a parent MLP has multiple subsidiary MLPs.

Regency Energy Partners (RGP) provides details on its Segment Margin:

Fee-based and Hedged Commodity are not created equal.

Even fee-based can fall off : HiCrush Partners LP (HCLP) fell 30% when Baker Hughes terminated its contract.

RGP stopped reporting Haynesville JV volumes in 2012

FY 2010 FY 2011 FY 2012

FY 2013

Target

Fee-based 76% 83% 83% 70%

Hedged Commodity 21% 11% 8% 20%

Un-hedged Commodity 3% 6% 9% 10%

Fee Based + Hedged 97% 94% 91% 90%

Three Months Ended December 31, Year Ended December 31,

2011 2010 2009

2011 2010 2009

($ in thousands)

Haynesville Joint Venture

Financial data:

Segment margin $ 43,901

$ 47,450

$ 12,157

$ 183,309

$ 174,347

$ 52,051

Operating data:

Throughput (MMbtu/d)

1,054,392

1,543,570

640,166

1,321,266

1,277,881

738,654

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 25

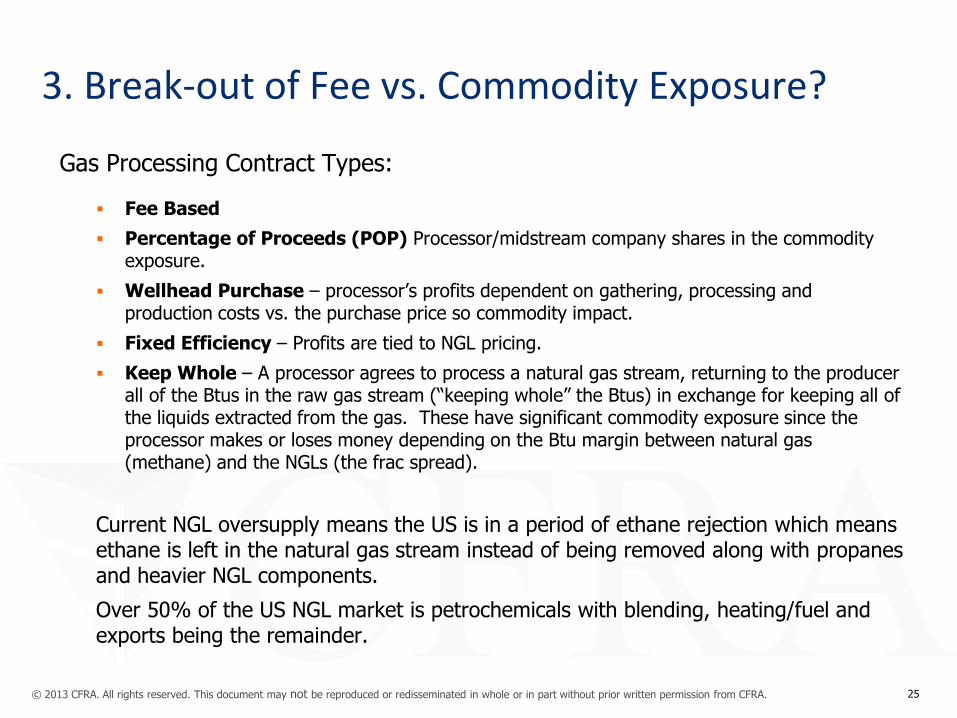

3. Break-out of Fee vs. Commodity Exposure?

Gas Processing Contract Types:

Fee Based

Percentage of Proceeds (POP) Processor/midstream company shares in the commodity exposure.

Wellhead Purchase – processor’s profits dependent on gathering, processing and production costs vs. the purchase price so commodity impact.

Fixed Efficiency – Profits are tied to NGL pricing.

Keep Whole – A processor agrees to process a natural gas stream, returning to the producer all of the Btus in the raw gas stream (“keeping whole” the Btus) in exchange for keeping all of the liquids extracted from the gas. These have significant commodity exposure since the processor makes or loses money depending on the Btu margin between natural gas (methane) and the NGLs (the frac spread).

Current NGL oversupply means the US is in a period of ethane rejection which means ethane is left in the natural gas stream instead of being removed along with propanes and heavier NGL components.

Over 50% of the US NGL market is petrochemicals with blending, heating/fuel and exports being the remainder.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 26

3. Break-out of Fee vs. Commodity Exposure?

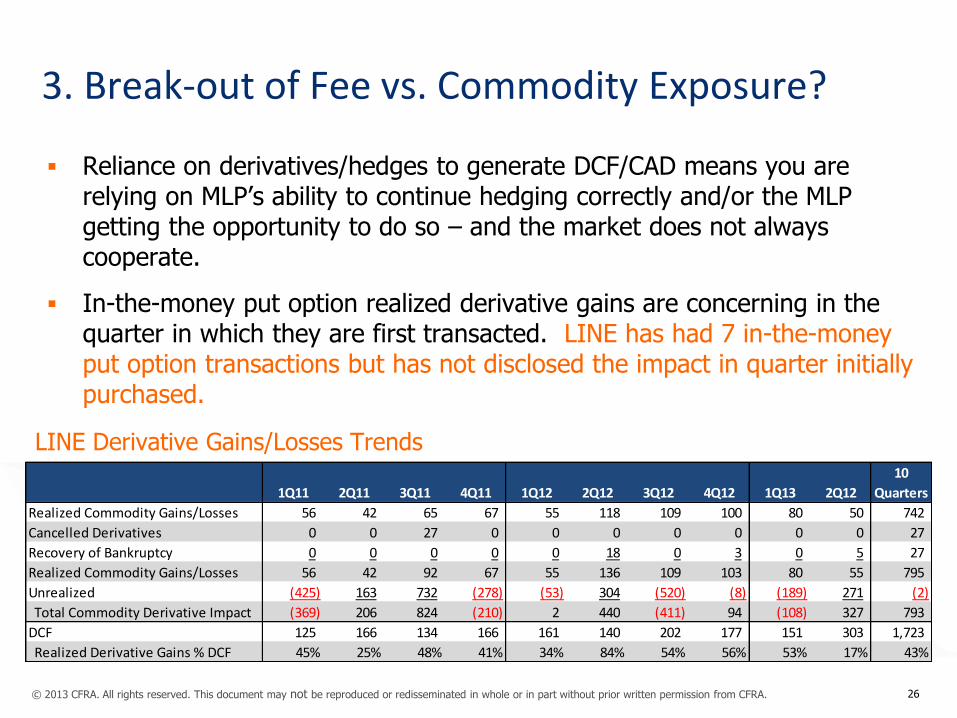

Reliance on derivatives/hedges to generate DCF/CAD means you are relying on MLP’s ability to continue hedging correctly and/or the MLP getting the opportunity to do so – and the market does not always cooperate.

In-the-money put option realized derivative gains are concerning in the quarter in which they are first transacted. LINE has had 7 in-the-money put option transactions but has not disclosed the impact in quarter initially purchased.

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q12

10

Quarters

Realized Commodity Gains/Losses 56 42 65 67 55 118 109 100 80 50 742

Cancelled Derivatives 0 0 27 0 0 0 0 0 0 0 27

Recovery of Bankruptcy 0 0 0 0 0 18 0 3 0 5 27

Realized Commodity Gains/Losses 56 42 92 67 55 136 109 103 80 55 795

Unrealized (425) 163 732 (278) (53) 304 (520) (8) (189) 271 (2)

Total Commodity Derivative Impact (369) 206 824 (210) 2 440 (411) 94 (108) 327 793

DCF 125 166 134 166 161 140 202 177 151 303 1,723

Realized Derivative Gains % DCF 45% 25% 48% 41% 34% 84% 54% 56% 53% 17% 43%

LINE Derivative Gains/Losses Trends

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 27

4. How is Sustaining/Maintenance Capex determined?

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Maintenance Capex 36 49 55 72 44 52 78 111 48 52

PP&E, net 14,696 14,824 15,344 15,596 14,916 15,130 19,326 22,330 22,584 15,130

Depreciation (281) (294) (301) (304) (321) (337) (367) (387) (401) (337)

Total Capex 265 270 302 361 353 424 496 533 552 424

Maintenance Capex % net PP&E 0.24% 0.33% 0.36% 0.46% 0.29% 0.34% 0.40% 0.50% 0.21% 0.34%

Maintenance Capex % Depreciation 12.8% 16.7% 18.3% 23.7% 13.7% 15.4% 21.3% 28.7% 12.0% 15.4%

Maintenance Capex % Total Capex 13.6% 18.1% 18.2% 19.9% 12.5% 12.3% 15.7% 20.8% 8.7% 12.3%

Rolling 4 Quarter

Maintenance Capex % net PP&E 1.14% 1.24% 1.29% 1.36% 1.47% 1.47% 1.27% 1.28% 1.28% 1.47%

Maintenance Capex % Depreciation 15.6% 16.4% 17.2% 18.0% 18.0% 17.7% 18.5% 20.2% 19.4% 17.7%

Maintenance Capex % Total Capex 15.9% 16.9% 18.5% 17.7% 17.1% 15.5% 15.1% 15.8% 14.4% 15.5%

Depreciation % net PP&E 1.91% 1.98% 1.96% 1.95% 2.15% 2.23% 1.90% 1.73% 1.78% 2.23%

What is good for a midstream assets . . .

KMP Maintenance Capex Trends

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 28

4. How is Sustaining/Maintenance Capex determined?

Adjusted for Price Revisions 2006 2007 2008 2009 2010 2011 2012 5-yr Avg

Drill-bit F&D/BOE $8.31 $15.43 $8.68 $26.48 $9.45 $12.99 $41.52 $16.78

Acquisition F&D/BOE $10.34 $14.09 $9.64 $11.27 $12.13 $15.72 $9.21 $10.96

Total F&D/BOE $10.04 $14.21 $9.27 $16.44 $11.63 $14.80 $11.81 $12.13

Adjusted for Price Revisions 2010* 2011 2012 2013E

5-YR F&D - Hist Used for Maint Capex $11.15 $11.15 $11.96 $16.78

Annual Production 16 22 41 50

CFRA Estimated Maintenance Capex 180 249 491 839

LINE Reported/Proj Maint. Capex 87 167 362 440

Total Shortfall (93) (82) (128) (399)

Quarterly Shortfall (23) (21) (32) (100)

... is not what is good for E&P assets.

Why should we compare E&P maintenance capex to EBITDA?

LINE Maintenance Capex Trends

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 29

5. How many distributions do current cash balances cover?

Variable distribution MLPs should have higher coverage than traditional

MLPs.

When reviewing cash position of variable distribution MLPs also review the

reserving needed to get to that cash position.

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Cash and Cash Equivalents 178 353 271 409 491 522 532 529 736 656

Quarterly Distribution 361 369 384 387 406 421 449 475 489 545

Cash Balance Distribution Coverage 0.5 1.0 0.7 1.1 1.2 1.2 1.2 1.1 1.5 1.2

KMP Cash Balances

NTI Cash Balances 3Q12 4Q12 1Q13 2Q13

Cash and Cash Equivalents 324 273 172 99

Quarterly Distribution 136 117 113 62

Cash Balance Distribution Coverage 2.4 2.3 1.5 1.6

Reserves & Adjustments (51.7) 16.6 (10.0) 0.0

% of Quarterly Distribution -38% 14% -9% 0%

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 30

6. What is the ownership structure?

Make sure you know what they own and who owns them.

Few traditional midstream companies left that are not or do not

have an MLP.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 31

6. What is the ownership structure?

General Partner

Sponsoring

Corporation

MLP

Subsidiary Holding

Company

100% Interest

2% GP Interest

100% Interest 10% LP Interest

88% External LP Unit

Holders

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 32

6. What is the ownership structure?

Source: Energy Transfer Partners

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 33

6. What is the ownership structure?

Distribution

Schedule LP% GP%

LP Distrib Up

To

Distribution

by Tier LP Share

Total

Distribution

Total GP

Share

GP

Regular GP IDR

Tier 1 98% 2% $0-$1 $1.00 $98.00 $100.00 $2.00 $2.00 $0.00

Tier 2 85% 15% $1-$2 $1.00 $98.00 $115.29 $17.29 $2.00 $15.29

Tier 3 75% 25% $2-$3 $1.00 $98.00 $130.67 $32.67 $2.00 $30.67

Tier 4 50% 50% Over $3 $1.00 $98.00 $196.00 $98.00 $2.00 $96.00

Total 72% 28% $4.00 $392.00 $541.96 $149.96 $8.00 $141.96

1) 100 shares total with 98 LP units and the remainder GP units

2) Current distribution is $4.00/unit

GPs may also have Incentive Distribution Rights as part of their

ownership interest which could pressure it to raise overall distributions

more quickly than what can be supported by the underlying assets.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 34

6. What is the ownership structure?

Source: Energy Transfer Partners

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

ETE's Cash Distributions from ETP

GP Interest 4.9 4.9 4.9 4.9 4.9 4.9 4.9 5.0 5.0 5.0

IDR 103.2 103.4 103.7 111.6 99.5 120.9 147.3 148.0 156.0 183.0

LP Interest 44.9 44.9 44.9 44.9 46.9 44.9 44.9 45.0 45.0 89.0

Total 153.0 153.1 153.5 161.4 151.4 170.7 197.1 198.0 206.0 277.0

IDR Reliquishment Citrus & Sunoco 0.0 0.0 0.0 0.0 0.0 (13.8) (31.3) (31.0) (31.0) (55.0)

Total Cash Distribution from ETP 153.0 153.1 153.5 161.4 151.4 156.9 165.9 167.0 175.0 222.0

ETE's Cash Distributions from RGP

GP Interest 1.3 1.3 1.3 1.3 1.3 1.3 1.3 1.0 1.0 1.0

IDR 1.1 1.3 1.7 1.9 2.1 2.1 2.1 2.0 2.0 3.0

IDR Reliquishment 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 (1.0)

LP Interest 11.7 11.8 12.0 12.1 12.1 12.1 12.1 12.0 12.0 12.0

Total Cash Distribution from RGP 14.1 14.4 14.9 15.3 15.5 15.5 15.5 15.0 15.0 15.0

Total Distribution from ETP and RGP 167.0 167.6 168.4 176.8 166.8 172.4 181.4 182.0 190.0 237.0

SUG CF/Regency Adjustment 0.0 0.0 0.0 0.0 (45.7) 51.3 76.5 75.0 50.0 0.0

SG&A ex non-cash comp (1.8) (12.0) (11.6) (4.3) (31.0) (10.3) (6.3) (4.0) (6.0) (24.0)

Interest net of adjustments (40.1) (40.1) (40.0) (40.5) (42.4) (65.7) (63.9) (60.0) (58.0) (48.0)

Bridge Financing/Other 0.0 0.0 0.0 0.0 (62.2) 0.0 0.0 0.0 0.0 0.0

DCF 125.2 115.5 116.9 132.1 (14.5) 147.8 187.7 193.0 176.0 165.0

Acquisition expenses/Other 0.6 9.0 9.5 2.8 145.2 10.5 1.4 0.0 2.0 15.0

DCF Adjusted 125.8 124.6 126.4 134.9 130.7 158.2 189.2 193.0 178.0 180.0

GPs can also relinquish IDRs for a period of time – this should only

happen if growth was not as expected and should send the same type of

signal as a LP distribution cut.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 35

7. How are service costs and reimbursements allocated between related parties?

Limited disclosure

Particularly concerning if there are numerous MLP

related parties.

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13

Total Service Fee RGP to ETE -- RGP Qs 3.9 4.2 4.2 4.3 4.3 4.3 4.3 4.3 4.3 2.0

Total Service Fee ETE to ETP -- ETE Qs 4.9 3.5 4.4 4.4 4.4 4.5 4.4 4.7 NA NA

Total Service Fee SUG to ETP -- ETP Qs 0.0 0.0 0.0 0.0 0.0 0.0 2.3 NA NA NA

Employee Reimb RGC to ETP -- RGP Qs 20.3 4.3 12.6 20.8 13.8 11.0 12.9 NA NA NA

Opex reim RGP to ETP -- RGP Qs 5.5 3.1 6.2 6.8 8.3 6.2 9.4 NA NA NA

Reimb G&A RGC to ETP-- ETP Qs 3.0 0.8 NA NA 1.8 1.8 NA NA NA NA

Source: Energy Transfer Partners. Energy Transfer Equity, Regency Energy Partners

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 36

8. How has the MLP grown?

Organic vs. Acquisitions

Dropdowns vs. Third Party Acquisitions

Funding: Debt vs. Equity

E&P MLPs largely grow by acquisitions

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 37

9. How as the growth been funded and is there a target level of debt?

Creditors still look at GAAP items

Higher commodity exposure means less willing to accept high leverage

As balance sheet leverage bumps up against target debt increased

likelihood of equity offering which will pressure unit performance.

NTI Balance Sheet Items

3Q12 4Q12 1Q13 2Q13

Cash and Cash Equivalents 324 273 172 99

Current Assets 643 600 569 498

Total Assets 1,177 1,137 1,123 1,085

Cash % Current Assets 50.3% 45.5% 30.3% 19.8%

Cash % Total Assets 27.5% 24.0% 15.3% 9.1%

Debt 269 283 282 282

Total Partners' Capital 538 484 492 443

Total Capital 806 766 774 725

Debt-to-Total Capital Ratio 33.3% 36.9% 36.5% 38.9%

Net Debt (55) 10 110 184

Total Net Capital 483 493 602 627

Net Debt to Total Capital Ratio -11.4% 1.9% 18.3% 29.3%

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 38

10. What are the governance policies?

Conflicts Committees

Cross-Board Relationships

Cannot Contract Away “Good Faith”

Understand Management Compensation

Understand IDR Status

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 39

Questions?

New York City September 9-10

Julie Hilt Hannink, CFA Energy Sector Lead 646-517-2472 [email protected]

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 40

About Julie Hilt Hannink

Julie Hilt Hannink is the head of energy sector research for CFRA and has 28 years of experience in financial and fundamental research and analysis. Before joining CFRA seven years ago, Julie was Director-Oil and Gas Equity Research at Medley Global Advisors. Prior to that, she spent nearly 15 years on the asset management side of the investment business, most recently at J.P. Morgan Asset Management where she was a Managing Director and senior North American oil & gas analyst.

Julie holds a BS in Commerce (concentration in Accounting) from the University of Virginia.

© 2013 CFRA. All rights reserved. This document may not be reproduced or redisseminated in whole or in part without prior written permission from CFRA. 41

Client Services Email

+ 1 (212) 981-1062 [email protected]

The content of this report and the opinions expressed within are those of CFRA. This analysis has not been submitted to, nor received approval

from, the United States Securities and Exchange Commission or any other regulatory body. While CFRA exercised due care in compiling this

analysis, CFRA AND ALL RELATED ENTITIES SPECIFICALLY DISCLAIM ALL WARRANTIES, EXPRESS OR IMPLIED, regarding the accuracy,

completeness or usefulness of this information. and assumes no liability with respect to the consequences of relying on this information for

investment or other purposes. In particular, the research provided is not intended to constitute an offer, solicitation or advice to buy or sell

securities.

CFRA’s financial data provider for financial companies is SNL FINANCIAL LC. CONTAINS COPYRIGHTED AND TRADE SECRET MATERIAL

DISTRIBUTED UNDER LICENSE FROM SNL. FOR RECIPIENT’S INTERNAL USE ONLY

CFRA, CFRA Accounting Lens, CFRA Legal Edge, CFRA Score, and all other CFRA product names are the trademarks, registered trademarks, or

service marks of CFRA or its affiliates in the United States and other jurisdictions. CFRA Score may be protected by U.S. Patent No. 7,974,894

and/or other patents.

If you have any comments or questions, please contact [email protected].