norway sweden finland denmar k the digital … · source: mckinsey global payments map. norway is...

TRANSCRIPT

DENMAR

K FINLAND SWEDEN NORWAY

THE DIGITAL REVOLUTION – HOW NEW TECHNOLOGY AND MOBILE SOLUTIONS TOTALLY CHANGES THE WAY OF CUSTOMERS ENGAGEMENT • The impact on bank operations and networks • The competitive landscape and how new players (fintech etc) could impact the market • Impact of PSD 2 and TPP’s access to accounts • Including examples from DNB Bank and Norway Global Back Office & Operational Efficiency Summit in Frankfurt, 17th&18th November 2016 Dag-Inge Flatraaker, DNB Bank

724503

1166330

1243278

1403856

1553994

1759316

2333729

2893242

NetherlandsSpain

RussiaNordic region

BrasilItaly

FranceGreat britain

The nordic region

5,1 9,8

5,5

5,3

A region with 25,7 million inhabitants A region with GDP larger than Spain and Russia

Source: The Economist 2016

Source: McKinsey

Leaders in Internet penetration and online banking

"Multi-channel"

"Self first"

3-5 years

"Brick & mortar"

0

10

20

30

40

50

60

70

80

90

100

90 80 75 5 45 85 70 65 0 60 55 50 100 95 10 40 35 30 25 20

Czech Rep.

Poland Slovenia Spain Slovakia

Ireland Malta

Lithuania Austria Germany

Iceland Finland

Netherlands

Norway

Online banking usage1 Percentage, 2014

Russia

Internet usage1

Percentage, 2014

Sweden

Hungary Italy

Portugal

Latvia France

UK Belgium

Luxembourg Estonia Denmark

Romania Bulgaria Turkey Greece

Cyprus

10-15 years 7-10

years

"Online adaptors"

15

Sources: Euromonitor, ECB, National Banks and Banking Associations, First Annapolis market observations

Soon cashless

Source: McKinsey Global Payments Map

Norway is today leading in electronic payments, but the enviroment is now changing rapidly

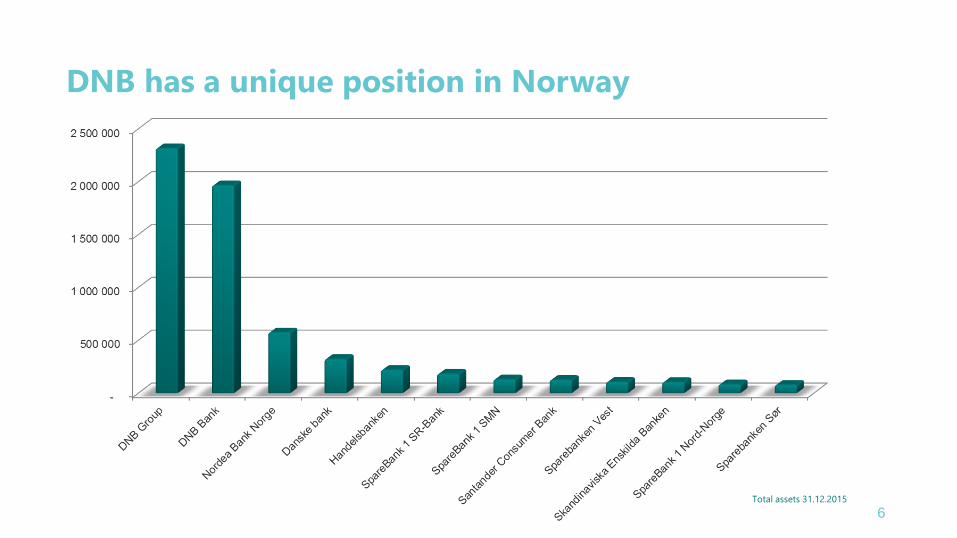

DNB has a unique position in Norway

6 Total assets 31.12.2015

DNB strategy Domestic strategy • 80% of DNB’s business is in Norway • Approx. 50% corporate and 50% retail customers International strategy • Serving Norwegian clients abroad • International clients in areas of global strategic importance:

Shipping Energy Seafood

7

DNB – With a broad global presence supporting our strategy

8

Source: DNB

Re-engineering Banking Becoming the cash-less digital bank

FAST MOVING ON MOBILE VALUE PROPOSITIONS

REAL TIME NORWAY

FASTER GLOBAL PAYMENTS

NEW TECHNOLOGIES

E.G BLOCKCHAIN

REAL TIME SEPA

DNB customers are digital and are moving to mobile first

Source: Fact Book Q2 2014 Danske Bank, Get Swish AB press release

Fast market uptake on mobile P2P

2013

2014

2015

Source: DNB

In June 2015, after 5 months of development, DNB launches

• Mobile payments P2P, P2B, In store, e&m-commerce, In app

• Onboarded 50 % of the Norwegian population as customers in roughly 1 year

• The fastest subscriber growth ever

Main drivers behind a digitised region Fast technological adoption and high education

Source: European Commission

Main drivers behind a digitised region High costs

Source: Eurostat

0

10

20

30

40

50

60EU

-28

Euro

are

a (E

A-1

9)N

orw

ayD

enm

ark

Bel

gium

Swed

enLu

xem

bour

gFr

ance

Net

herla

nds

Finl

and

Aus

tria

Ger

man

yIre

land

Italy

Uni

ted

Kin

gdom

Spai

nC

ypru

sSl

oven

iaG

reec

ePo

rtug

alM

alta

Esto

nia

Slov

akia

Cze

ch R

epub

licC

roat

iaPo

land

Hun

gary

Latv

iaLi

thua

nia

Rom

ania

Bul

garia

Other labour costs

Wages and salaries

Digital Interaction between the Norwegian Financial- and Public sector

INHABITANTS

PUBLIC SECTOR

FINANCIAL INDUSTRY

PUBLIC SECTOR

INHABITANTS FINANCIAL INDUSTRY

PUBLIC SECTOR

INHABITANTS FINANCIAL INDUSTRY

CONSENT BASED LOAN APPLICATIONS 6 BNOK / 10 YEARS

BANKRUPTCY PROCEEDINGS ~1 BNOK / 10 YEARS

INTELLIGENCE ~1 BNOK / 10 YEARS

External changes – Regulatory and Market Creates Compliance requirements and Adaptation cost

16

AML FATF

SEPA Migration End date

Feb 14th 2012

EU ‘Payments Package’

(PAD, PSD2, IF-regulation)

Global Competition

Globalisation of Business

Global Standardisation

ISO 20022

Innovations Mobility/Digital Fintech, Blockchain etc

CPSS-IOSCO

A «Tsunami» of new EU regulations

17

• 2002 : EU introduces «price regulation» - SEPA

Vision and ”kind of” selfregulation created

• 2008 : 8000 banks in Europe agreed • «SEPA Rulebooks»

• 2009 : New legal basis – Payment Service

Directive

• 2012 : SEPA End date • Legal requirements and mandatory use of SEPA Standards • Removal of national formats in the eurosone

• 2014/16 : «Payments package» (PSD2, PAD og MIF-reguleringen

• Euro Retail Payments Board (ERPB)

ERPB’s agenda: - “SEPA post migration”, improve todays SEPA-solutions (SCT, SDD, e-mandates ++) - Card standardisation (for the time being leverage Card Stakeholder Group (CSG) - e-identity & e-invoicing related to payments - pan-european e-commerce - Mobile Payments (pan-european solutions for proximity contactless and P2P payments) - SEPA “Faster Payments” (24/7) 18

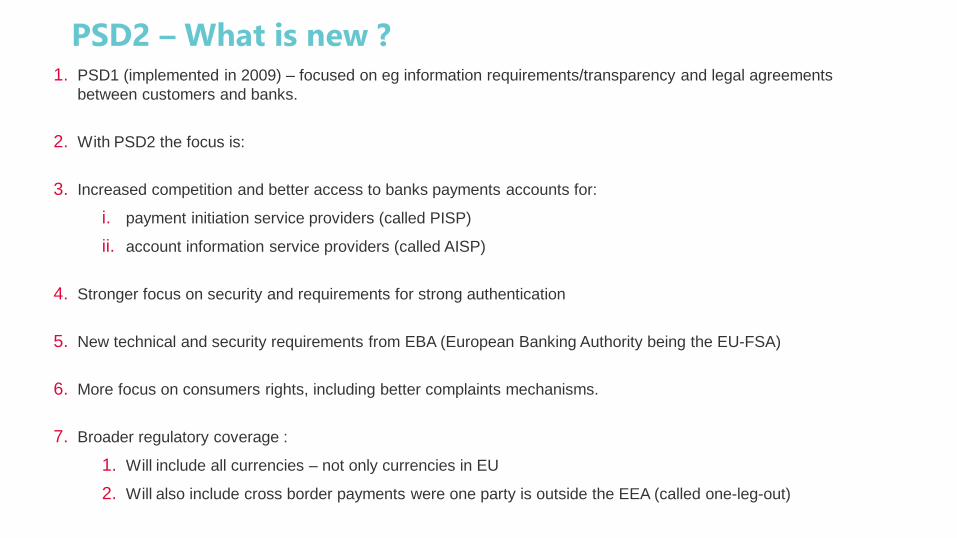

PSD2 – What is new ? 1. PSD1 (implemented in 2009) – focused on eg information requirements/transparency and legal agreements

between customers and banks.

2. With PSD2 the focus is:

3. Increased competition and better access to banks payments accounts for:

i. payment initiation service providers (called PISP)

ii. account information service providers (called AISP)

4. Stronger focus on security and requirements for strong authentication

5. New technical and security requirements from EBA (European Banking Authority being the EU-FSA)

6. More focus on consumers rights, including better complaints mechanisms.

7. Broader regulatory coverage :

1. Will include all currencies – not only currencies in EU

2. Will also include cross border payments were one party is outside the EEA (called one-leg-out)

PSD2 – Why ?

Why? EU Commission wants to build a common digital internal payments market for cards, mobile and internett based bill payments

Timeline ○ Published december 2015 ○ January 2016: The Directive enter into force in

EU ○ Januar 2018: Must be implemented

Background ○ Single European Payment Area (SEPA) ○ Payments Service Directive 2009 ○ New technology and new entrants to the

market

Fintech, nye players, new technology, faster market changes

Customers are changing habits faster than before, fast growth in ecommerce, but also more exposure to fraud, potential lossesetc

More changes will most probably be needed to ensure/preserve safety and trust,

SAMFUNNSANSVAR OG NÆRINGSPOLITIKK

Many details are still unclear EBA have got the responsibility to draft Regulatory

Technical Guidelines for: requirements of the strong customer authentication;

exemptions from the application of these requirements;

requirements to protect the user's security credentials;

common and secure open standards of communication;

security measures between the various types of providers in the payments sector.

Discussion Paper with high level discussion of issues published and sent for consultation early 2016 and then draft RTS requirement with consultation ending early october.

Final RTS requirements for strongs customer authentication and communicationare expected early 2017.

21

European Banking Authority (EBA) www.eba.europa.eu

Strategic choices

WHAT WILL THE FUTURE BRING?