north america’s energy infrastructure renaissance/media/enb/documents/investor relations... ·...

TRANSCRIPT

Al MonacoPresident & Chief Executive OfficerAl MonacoPresident & Chief Executive Officer

North America’s Energy Infrastructure RenaissanceCIBC Whistler Institutional Investor Conference

January 23, 2014

North America’s Energy Infrastructure RenaissanceCIBC Whistler Institutional Investor Conference

January 23, 2014

Legal Notice

This presentation includes certain forward looking information (FLI) to provide Enbridge shareholdersand potential investors with information about Enbridge and management’s assessment of its futureplans and operations, which may not be appropriate for other purposes. FLI is typically identified bywords such as “anticipate”, “expect”, “project”, “estimate”, “forecast”, “plan”, “intend”, “target”, “believe”and similar words suggesting future outcomes or statements regarding an outlook. Although we believethat our FLI is reasonable based on the information available today and processes used to prepare it,such statements are not guarantees of future performance and you are cautioned against placing unduereliance on FLI. By its nature, FLI involves a variety of assumptions, risks, uncertainties and otherfactors which may cause actual results, levels of activity and achievements to differ materially from thoseexpressed or implied in our FLI. Material assumptions include assumptions about: the expected supplyand demand for crude oil, natural gas and natural gas liquids; prices of crude oil, natural gas and naturalgas liquids; expected exchange rates; inflation; interest rates; the availability and price of labour andpipeline construction materials; operational reliability; anticipated in-service dates and weather.

Our FLI is subject to risks and uncertainties pertaining to operating performance, regulatory parameters,weather, economic conditions, exchange rates, interest rates and commodity prices, including but notlimited to those discussed more extensively in our filings with Canadian and US securities regulators.The impact of any one risk, uncertainty or factor on any particular FLI is not determinable with certaintyas these are interdependent and our future course of action depends on management’s assessment ofall information available at the relevant time. Except to the extent required by law, we assume noobligation to publicly update or revise any FLI, whether as a result of new information, future events orotherwise. All FLI in this presentation is expressly qualified in its entirety by these cautionary statements.

This presentation will make reference to certain financial measures, such as adjusted net income, whichare not recognized under GAAP. Reconciliations to the most closely related GAAP measures areincluded in the earnings release and also in the Management Discussion and Analysis posted to thewebsite.

2

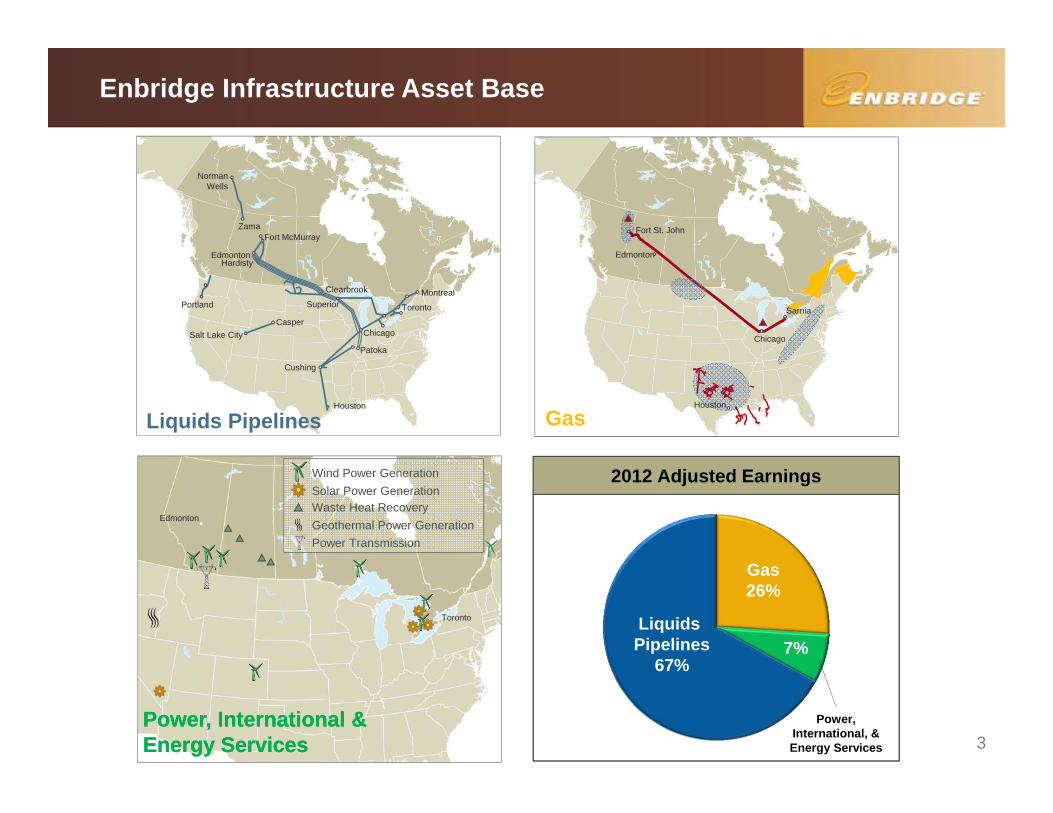

Enbridge Infrastructure Asset Base

Norman Wells

ZamaFort McMurray

Portland

Casper

Montreal

Salt Lake City

Patoka

Cushing

Houston

Superior

Clearbrook

EdmontonHardisty

Toronto

Chicago

Liquids Pipelines

Edmonton

Fort St. John

Houston

Chicago

15%

Gas

Sarnia

2012 Adjusted Earnings

Liquids Pipelines

67%

Power, International, & Energy Services

7%

Gas26%

Toronto

Edmonton

Wind Power Generation

Waste Heat RecoverySolar Power Generation

Geothermal Power GenerationPower Transmission

Power, International & Energy ServicesPower, International & Energy Services 3

North American Regional Pricing Disparities

4

Asia

$86

$89

$111

AlbertaLight

WCS

Bakken Light

Brent

Maya

Pricing Based on Q4 2013 - Daily Average(USD per barrel)

$83$107

$101

LLS

$98

WTI

$117

Light Crude

Heavy Crude

*Brent price is a landed price on US East Coast/ US Gulf Coast. Assumed tanker freight cost of US$2.00 per bbl.

*

$66

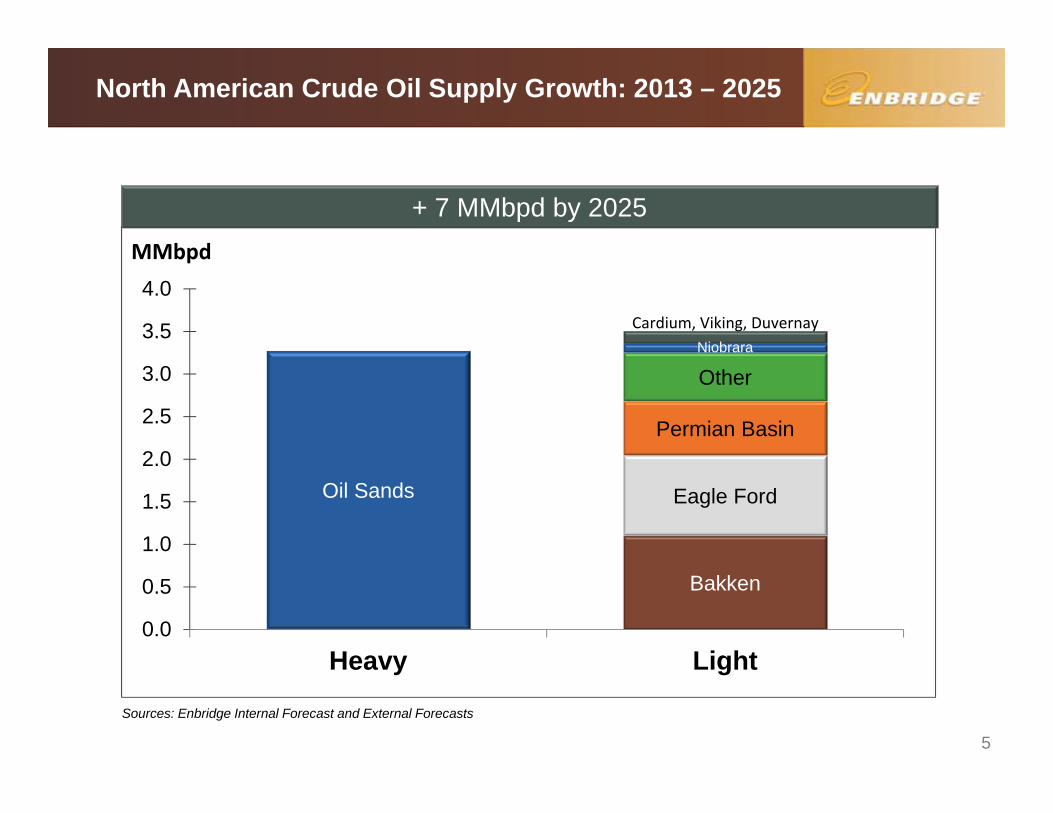

North American Crude Oil Supply Growth: 2013 – 2025

5

Bakken

Eagle Ford

Permian Basin

OtherNiobrara

Oil Sands

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Heavy Light

Cardium, Viking, Duvernay

Sources: Enbridge Internal Forecast and External Forecasts

+ 7 MMbpd by 2025MMbpd

Source: StatsCan, EIA, Enbridge Internal Forecasts

Light Markets• East Coast• Eastern PADD II• PADD III

Heavy Markets• PADD II• PADD III

North American Crude Oil Demand

6

Providing New Market Access (Heavy & Light)

7

Norman Wells

Zama

Edmonton

Fort McMurray

Portland

Seattle

Casper

Montreal

Salt Lake City

Patoka

Cushing

Superior

Chicago

Clearbrook

Regina

Flanagan

Hardisty

ToledoSarnia

Buffalo

Houston

St. James

CromerSt. John

+600 kbpd Heavy

+80 kbpd Heavy

+250 kbpd Light

+50 kbpdHeavy

+300 kbpd Light

Western USGCAccess ($6.4B)

Eastern Access ($2.7B)

Light Oil Market Access ($6.3B)

+50 kbpdLight

Incremental Market Access Volumes

+ ~1.0 MMbpd of Heavy+ ~0.7 MMbpd of Light

+50 kbpdLight

Nanticoke+250 kbpd Heavy

7

New Market Access – Under Development

8

MontrealGretna

Regina

Hardisty

Kerrobert

Toledo

Buffalo

Edmonton

Fort McMurray

Cromer

Cushing

Patoka

Clearbrook

Sarnia

Chicago/ Flanagan

WoodRiver

Asia Pacific/West Coast Refinery Markets

Eastern U.S. Gulf Coast Refinery Markets

Canadian/U.S. East Coast Refinery Markets

Houston

St. JamesPort Arthur

Regional Infrastructure – Alberta Oil Sands

NTD: Secured capital does not align with LRP (2013 – 2017)- Fort Hills and Norlite should be classified as unsecured?

Edmonton

AlbertaAlbertaCheechamTerminal

Kirby Lake Terminal

Athabasca Terminal

Cenovus(Christina Lake)

AOC(Hangingstone)

JACOS(Hangingstone)

Suncor(MacKay River) Suncor

(Firebag)

Imperial Oil(Kearl)

Norealis Terminal

Husky(Sunrise)

Hardisty

FHELP(Fort Hills)

ConocoPhillips(Surmont)

Statoil(Leismer)

Nexen(Long Lake)

Total Secured Capital = $6.0 B** Excluding ~$1B of projects that came into service in 2012

9

Wood Buffalo PipelineWaupisoo PipelineAthabasca PipelineWoodland PipelineNorealis PipelineAthabasca Twin PipelineWoodland Pipeline ExtensionWood Buffalo ExtensionNorlite Diluent PipelineSouthern Lights Pipeline

Canadian Midstream

10

• Commercially Secured: $1.1B

– Cabin Phases 1 & 2

– Peace River Arch Gathering

• Potential Opportunities: $4.5B

– Cabin expansion phases (3–6)

– Peace River Arch expansion

– Montney, Duvernay and other Deep Basin infrastructure

– Regional condensate & NGL pipelines & processing infrastructure

Horn River Montney Duvernay

U.S. Offshore Gulf Coast of Mexico

11

• Legacy Investment $0.6B

• Commercially Secured : $1.0B– Venice Expansion (Q4/13)

– Walker Ridge Gathering (Q3/14)

– Big Foot Oil Pipeline (Q4/14)

– Heidelberg Oil Lateral (2016)

• Potential Opportunities: $1.5B Offshore Earnings

($10)

$0

$10

$20

$30

$40

$50

$60

2012 2013 2014 2015 2016 2017

$ m

illio

ns

Gas Distribution

12Total Secured Capital = $0.7 B

System Reinforcement Project

Power Generation & Transmission

13

Transmission Focus Areas

0

500

1,000

2013 2017

MW

Transmission Capacity

0

1,000

2,000

3,000

2013 2017

MW

Power Generation Capacity

CDN U.S.

Solar 100 MW 50 MW

Wind 1,302 MW 360 MW

Geothermal ‐ 23 MW

Waste Heat 30 MW ‐

Power Generation Focus Areas

Total Secured Capital = $1.5 B

$36 Billion Growth Investment Plan

14

- Unsecured

- Commercially Secured

Enterprise Wide Growth Capital In ServiceEnterprise Wide Growth Capital In Service

Enbridge Day 2012 (2012 – 2016)

Enbridge Day 2013 (2013 – 2017)

Current

$17 B

$18 B

$36 B$10 B $7 B

$26 B$29 B

$36 B$35 B

(2013 – 2017)

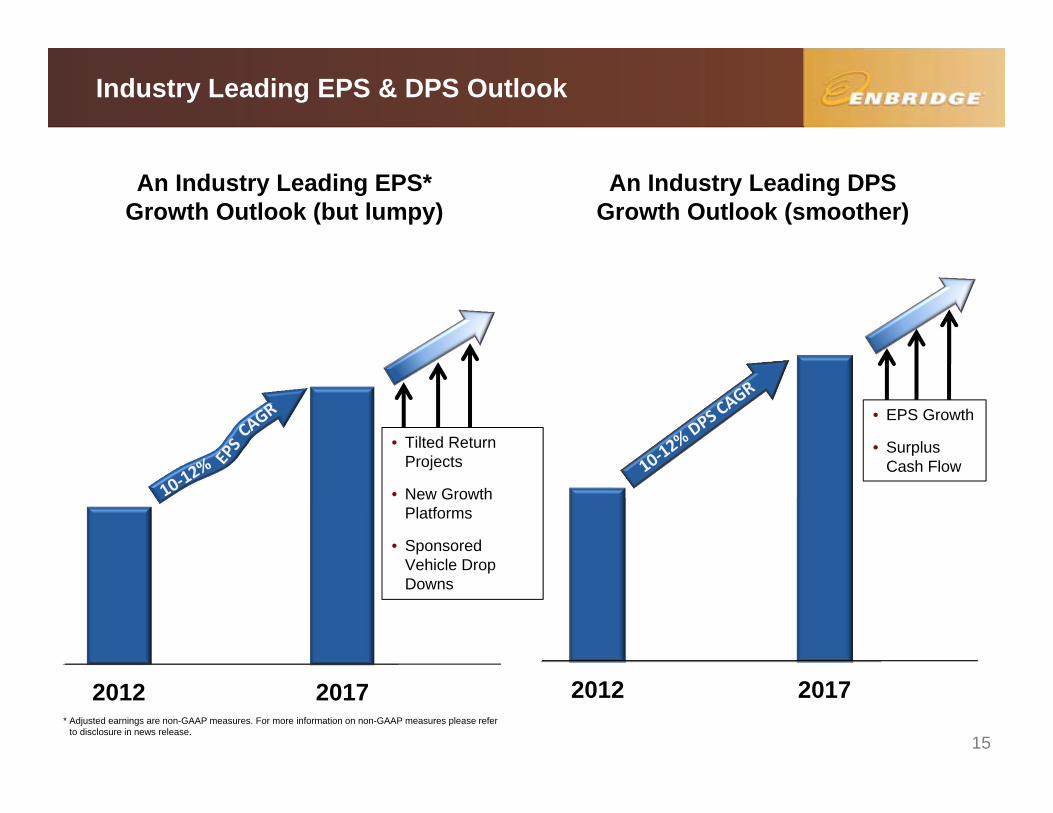

Industry Leading EPS & DPS Outlook

15

2012 2017

An Industry Leading DPSGrowth Outlook (smoother)

2012 2017

An Industry Leading EPS* Growth Outlook (but lumpy)

* Adjusted earnings are non-GAAP measures. For more information on non-GAAP measures please refer to disclosure in news release.

• Tilted Return Projects

• New Growth Platforms

• Sponsored Vehicle Drop Downs

• EPS Growth

• Surplus Cash Flow

Summary

16

• Record portfolio of attractive investment opportunities

• Commercial and financial risk tightly managed

• Access to multiple low cost funding alternatives

• Highly visible industry leading growth including significant embedded post 2017 organic growth

Attractive investments low cost of capital

Industry leading growth

Substantial Valuation Upside