nordic outlook - seb filenordic outlook - november 2003 2 seb economic research important: this...

TRANSCRIPT

Nordic Outlook

Economic ResearchImportant your attention is drawn to the statement on the next page of this report which affects your rights.

OsloStockholm

Helsinki

Tallinn

Riga

Copenhagen Vilnius

November 2003 English edition

IMBALA

NCED REC

OVERY

Nordic Outlook - November 2003

2

SEB Economic Research

Important: This statement affects your rights

This report is produced for institutional investors (being, in the United Kingdom, persons who fall within Article 9 (3) of the Financial Services Act 1986 (Invest-ment Advertisements) (Exemptions) Order 1988 or other persons to whom this document may lawfully be issued or passed on). This report is produced for privateinformation of recipients and neither Skandinaviska Enskilda Banken AB (publ) (the Bank) nor any identified third party data supplier (“Data Supplier(s)”) aresoliciting any action based upon it. Opinions contained in this research report represent the Bank’s present opinion only and are subject to change without notice.All information contained in this report has been compiled in good faith from sources believed to be reliable. However, no representation or warranty, express orimplied, is made with respect to the completeness or accuracy of the contents by the Bank or any Data Supplier and it is not to be relied upon as authoritative.Recipients are urged to base their investment decisions upon such investigations as they deem necessary. The Bank does not provide legal or tax advice, and whilethe Bank believes the information contained herein to be reliable, it is not intended to be and should not be construed as a legal or tax advice. To the extent permittedby applicable law, no liability whatsoever is accepted by the Bank) or any Data Supplier for any direct or consequential loss arising from use of this document or itscontents. Your attention is drawn to the fact that a member of, or any entity associated with, the Bank or its affiliates, officers, directors, employees or shareholdersof such members may from time to time have a long or short position in, or otherwise participate in the markets for, the securities and the currencies of countriesmentioned herein.

Skandinaviska Enskilda Banken AB (publ) is incorporated in Stockholm Sweden with limited liability and is a member of the Stockholm Stock Exchange.

Skandinaviska Enskilda Banken AB (publ) which is registered in England and Wales No. BR000979 is regulated by The Securities and Futures Authority and is amember of the London Stock Exchange.

Transactions involving debt securities will be executed by or with the Bank unless you are informed otherwise at the time of dealing.

Confidentiality Notice

This report is confidential and may not be reproduced or redistributed to any person other than its recipient from the Bank.

Skandinaviska Enskilda Banken AB (publ), 2003. All rights reserved.

Klas Eklund, Chief Economist +46 8 763 [email protected]

Håkan Frisén, Head of Economic Research [email protected]

Bo Enegren, Economist [email protected]

Ann Enshagen Lavebrink, Research Assistant [email protected]

Ingela Georgii-Hemming, EU Coordinator [email protected]

Olle Holmgren, Economist [email protected]

Kerstin Jendhammar, Research Assistent/Secretary [email protected]

Mikael Johansson, Economist [email protected]

Fax no. +46 8 763 9300

Contributions to the sections on Germany and Norway in this report have been made by Thomas Köbel fromSEB Frankfurt/M and Tharald Stray Laastad from Trading Strategy, Merchant Banking.

SEB, Economic Research, K A3, SE-106 40 STOCKHOLM

This report was published on November 18, 2003.Cut-off date for calculations and forecasts was November 12, 2003.

SummaryNordic Outlook – November 2003

3

The International Economy▪ The American economy is in the midst of a powerful upswing, which will carry over a bit into

next year. Growth in 2004 will be 3.7 per cent but will cool in the course of the year as thestimulus from tax cuts and mortgage refinancing fades. During 2005, growth will drop to 2.8 percent and fiscal policy consolidation will begin.

▪ Japan’s economy has offered upside surprises this year. The cyclical upswing will also last into2004 but gradually cool. Growth will be 1.9 per cent next year and 1.2 per cent in 2005.

▪ The euro zone is recovering slowly, as consumer optimism returns, exports bounce back andcertain taxes are cut. However, growth will not exceed 1.7 per cent in 2004 and 2.3 per cent in2005. The Stability Pact is increasingly being undermined.

▪ The Fed will wait until autumn 2004 before hiking its funds rate. By year-end, the rate will be1.5 per cent and by late 2005, 3.0 per cent. The ECB will also wait until after summer beforeraising its refi rate. Bond yields will stay below 5 per cent both in the US and the euro zone.

Sweden▪ The Swedish economy is finding it hard to gather steam. Private consumption growth is strong,

due to solid balance sheets in the household sector, but local government financial woes hamperthe economic recovery. GDP will grow by 2.1 per cent in 2004 and 2.3 per cent in 2005.

▪ Underlying inflation will stay below 2 per cent both in 2004 and 2005, but the Riksbank willchoose to employ a core inflation measure that excludes energy prices and will abstain from low-ering its repo rate. The first rate hike will come after the summer of 2004. The repo rate will standat 3.25 per cent in December 2004 and 3.75 per cent a year later.

▪ The krona will appreciate to TCW 120. The manufacturing sector will lose some of its com-petitiveness, but due to good productivity growth the current account surplus will persist.

▪ The government budget is being squeezed. More cutbacks are needed to stay below the expen-diture ceiling next year. Local governments will boost income taxes both in 2004 and 2005.

▪ The ongoing “growth talks” will not lead to revolutionary results. Wealth tax will be lowered,but only in exchange for increases in other taxes. The business sector will avoid financing thethird week of employee sick pay but will have to pay a larger share of overall sickness benefit.

Other Nordic countries▪ In Norway, monetary policy shock therapy is yielding results. Growth will recover to almost

2½ per cent both in 2004 and 2005. Inflation will fall below the 2.5 per cent target in both years,but Norges Bank has stopped slashing interest rates.

▪ The Danish economy will recover slowly to GDP growth of 1.7 and 2.3 per cent in 2004 and2005, respectively. Inflation is in phase with that of the euro zone, and the central bank is shad-owing the ECB. A referendum on the euro may be held during 2005.

▪ The Finnish economy is also recovering and will achieve GDP growth of 2.5 per cent in 2004and 2.9 per cent in 2005. Inflation will drop below 1 per cent next year, partly due to tax cuts.

4

Nordic Outlook - November 2003

Contents

Summary 3

International overview 5

The US 6

Japan 9

The euro zone 10

The United Kingdom 13

Emerging markets 14

Central and Eastern Europe 15

International financial markets 16

Sweden 19

Denmark 29

Norway 30

Finland 32

Nordic key economic data 33

International key economic data 35

Boxes

US: The growth profile and the labour market 6

US: The presidential election and the effects of fiscal policy 7

The euro zone: Stability Pact under threat 12

Slow, controlled revaluation of yuan 14

Delayed enlargement of the euro zone 15

The US current account deficit and the dollar 18

Sweden: Why so little drama in the forecasts? 19

Sweden: Will new CPI measurement methods lead to a new target variable? 24

Sweden: Two per cent norm sensitive to choice of inflation measure 25

Sweden: What is happening to growth policy? 28

Sweden: Local governments raising taxes 27

International overviewNordic Outlook – November 2003

5

An imbalanced recovery▪ Signs of strength dominant

▪ But the US will lose tempo

▪ Tighter fiscal policies ahead

The American economy is currently growing at arapid pace. In Japan, the cyclical upswing has beenunexpectedly strong. China and India are expandingvigorously. The world economy is thus on the roadto recovery after its slump in recent years. Consensusforecasts for 2004 have shifted upward significantly inrecent months; in this Nordic Outlook, we too haveraised our growth figures for the US and Japan.

However, our forecast for the American economy is –once again – more cautious than the consensus. Thisautumn’s rapid growth is partly a result of massiveeconomic policy stimulus. A continued rapid build-upof household debt, galloping budget deficits and largeimbalances in foreign trade indicate that this trend isnot sustainable. We believe that growth will cool asthe effects of the stimulus policy fade in the course of2004 and are followed by fiscal tightening in 2005.Next year, growth in Gross Domestic Product will be3.7 per cent, somewhat above potential level – butpartly as a consequence of a statistical overhang fromthe autumn upswing. In 2005, GDP growth will onceagain drop below potential.

USD bn, annual rateUS: Public finance and current account

Federal surplus/deficit Current account

Source: EcoWin

92 93 94 95 96 97 98 99 00 01 02 03

-600

-500

-400

-300

-200

-100

0

100

200

300

-600

-500

-400

-300

-200

-100

0

100

200

300

The latter part of our forecast period will thus be char-acterised by economic policy consolidation and mod-est growth. This can be described as a final necessaryphase of the adjustment process after the burst bub-ble. Once it is completed, the preconditions exist forhigher, more sustainable growth. The productivityincrease in the American economy has been

maintained at a high level. This is an important plat-form for such expansion. Even if our relatively cau-tious growth scenario is realised, the final judgementwill still be that it has proved possible to limit the realconsequences of the burst bubble in a way that mustbe regarded as an economic policy success.

Owing to the adjustment process in the United States,global growth will be modest both in 2004 and 2005.The Japanese economy will slow towards its potentialgrowth level again, and recovery in Europe will berelatively lethargic. The euro zone, where the StabilityPact is being watered down, will also shift towardstighter fiscal policy.

GDP growthYear-on-year percentage change

2002 2003 2004 2005US 2.4 2.9 3.7 2.8Japan 0.2 2.4 1.9 1.2Euro zone 0.9 0.5 1.7 2.3OECD 1.8 1.9 2.7 2.6World economy 2.5 2.7 3.5 3.4Sources: OECD, SEB

As a result of American imbalances, the dollar willweaken against both the euro and Asian currencies.The Chinese yuan’s fixed dollar exchange rate will bereplaced during our forecast period by a slow, con-trolled appreciation against the dollar.

Looking ahead, stock and bond markets will be char-acterised by tension between the healing process afterthe bubble, on the one hand, and disappointments inrelation to overly optimistic forecasts, on the otherhand. We expect stock markets to move sidewaysduring 2004, while bond more or less stay unchanged.

Central banks will keep their key interest rates atlow levels. Given modest growth, low inflation pres-sure and tighter fiscal policies, economies will needcontinued propping up. Only well into next year will anormalisation of key interest rates begin. In the US,the Federal Reserve will raise its funds rate to 1.5 percent during the autumn. By the end of 2005 it will be3.0 per cent. The European Central Bank will raise itsrefi rate to 2.25 per cent by the end of 2004 and 3.25per cent by the end of 2005.

The USNordic Outlook – November 2003

6

Growth will culminate early▪ Growth already peaking – will slow

▪ Fed key rate on hold until next autumn

▪ Tighter fiscal policy after presidential election

Since this past summer, the American economy hasbeen characterised by mounting optimism. Businessconfidence has climbed and companies seem to beregaining a desire for capital spending. Despite signsof concern about the weak labour market, householdshave used their tax cuts and lower interest rates –which have enabled them to refinance their homemortgages and thereby slash their housing costs – forincreased consumption. In financial markets, a grow-ing risk appetite has been manifested in rising shareprices and narrowing credit spreads, while long-termyields have climbed. The strong GDP figure for thethird quarter of 2003, with annualised growth topping

7 per cent, confirms the picture of significantly accel-erating economic activity.

In light of this, we are revising our US growth fore-cast upward to 2.9 per cent this year and to 3.7 percent in 2004.

Is the US entering a positive spiral?Hopes of an imminent, lasting recovery are relativelywidespread. The crucial question is whether the cur-rent surge in growth can lead the economy into a posi-tive spiral. Such a scenario presupposes that the la-bour market will bounce back clearly during thecoming six months. If so, rising employment can sus-tain household purchasing power, even when stimulifrom tax cuts and widespread mortgage refinancinghave lost their punch. Capital spending will then alsoachieve new vigour, even though capacity utilisationremains low. Continued rapid productivity growth andrising share prices are important elements of such apositive spiral.

The growth profile and the labour marketOur forecast underscores the differences in the waygrowth is measured in Europe and the United States.The customary American way of calculating growth,where every quarterly change (growth between onequarter and the next) is individually recalculated atan annual rate (“annualised”), enlarges GDPchanges compared to the method generally used inEurope. Measured as annualised growth, GDPgrowth has already culminated with the high thirdquarter 2003 figure.If we instead measure growth in the way that is cus-tomary in Europe – “year-on-year” change between aquarter in one year and the corresponding quarter ofthe preceding year – growth will peak during thefirst and second quarters of 2004.It took a long time before employment started to rise.This is partly a consequence of strong productivitygrowth; due to streamlining, companies have beenable to boost production without having to add new

jobs. Since production hikes affect job creation aftera certain time lag, “slower” year-on-year growth(GDP growth measured in the “European” way) is abetter indicator of labour market trends than annual-ised GDP growth.

During the third quarter of 2003, this year-on-yeargrowth amounted to 3.3 per cent. The pace of growthis thus around its long-term potential level. What weare currently seeing is thus growth that should not beexpected to generate rapidly rising employment.Employment will instead be at its most expansivein mid- and late 2004, one or two quarters after thepeak of the year-on-year growth profile. This looksalmost pre-meditated: The sharpest upswing in USjob creation will thus coincide exactly with the periodwhen the presidential election will be decided. During2005, the labour market will again weaken some-what.

200420032002200120001999

8

6

4

2

0

-2

8

6

4

2

0

-2

Sources: EcoWin, SEB

US: Gross domestic productAnnualised change

SEB

Per centPer cent

forecast

200420032002200120001999

8

6

4

2

0

-2

8

6

4

2

0

-2

Sources: EcoWin, SEB

US: Gross domestic productYear-on-year change

SEB

Per centPer cent

forecast

The USNordic Outlook – November 2003

7

This is quite possible. The dynamic of a recovery isoften characterised by such positive spirals, where“success breeds success” in a way that is not initiallyapparent.

Our main forecast – in spite of this – is that the path tosustainable recovery is not so straight. Today’s rapidgrowth is partly a consequence of an extremely ex-pansive economic policy. During the first half of2003, home mortgage refinancing alone bolstered thepurchasing power of American households. But thisgrowth is occurring at the expense of worse imbal-ances in the financial position of households, as wellas deficits in the country’s current account and publicsector budgets.

The forces of deceleration will therefore graduallymake themselves felt. Today the above-mentionedstimulus to the finances of households is already be-ginning to ebb. Public sector consumption is levellingoff after a rapid increase in recent years. Austeritymeasures will not materialise immediately, however.Not until the second half of 2004 will the FederalReserve gently begin normalising interest rates. Fiscalconsolidation will come only in 2005, when a newterm of office begins after the November 2004 presi-dential election. The result will be a relatively pro-longed period of growth somewhat below potential.In 2005, GDP growth will cool to 2.8 per cent.

Although our forecast is below consensus, our finalassessment is that the real consequences of the burstbubble will be limited. The Fed’s ambition of using

an extremely low funds rate to smooth and postponethe adjustment thus seems likely to succeed. Sustainedproductivity growth in the economy will serve as astable platform for faster future growth, once the ad-justment has made some progress.

Larger public deficits in the short termThe runaway deterioration in public sector finances iscontinuing. Large tax cuts and rising defence expen-ditures have driven up deficits, while the economy hasbeen too weak to provide any cyclical help. In theshort term, deficits will continue to climb. Next year,the overall public sector deficit will be 6-7 per cent ofGDP, almost on par with Japan. This implies thatpublic savings will have deteriorated by nearly 10 percent of GDP in just four years.

However, public sector debt remains relatively low inan international perspective, currently at about 40 percent of GDP. Fortunately, this means that there isroom to carry out the necessary consolidation at arelatively modest pace during the second half of thedecade. States and cities are nevertheless legally re-quired to balance their budgets, which will demandfaster steps. Our forecast is based on the assumptionthat fiscal tightening during 2005 will be in the rangeof ½-1 per cent of GDP.

The US economy would thereby pass through the foursequences that are common after a period of majorover-heating: Crisis, early recovery, economic policyconsolidation and – after some time – a sustainableupturn.

The presidential election and the effectsof fiscal policyPresident George W Bush has a strong position. TheRepublicans enjoy a majority both in the US Senateand House of Representatives. However, due tovarious independent-minded legislators, the presi-dent cannot be certain that White House proposalswill get through Congress untouched. The November2004 election is about both presidential power and alarge proportion of Congress. Various power-sharingcombinations between the president, Senate andHouse are thus conceivable.For a long time, the president’s position seemed in-vulnerable. However, US difficulties in Iraq along withdomestic labour market and budget problems haveenabled various Democratic challengers to gainground in the opinion polls.It is nevertheless more likely that Bush will be re-elected. Our forecast is therefore based on this. We

also assume that the Republicans will largely main-tain their position of strength in Congress and thatfiscal tightening will start in 2005, in order to bring thebudget deficit under control. Most austerity measureswill probably occur on the expenditure side. Suchdecisions, however, normally take time to pushthrough Congress, so the effects in 2005 will not belarge. Should the Democrats win the election, we ex-pect tax hikes, the impact of which will come quicker.Effects of fiscal policyPer cent of GDP2003:1 2003:2 2004:1 2004:2 2005:1 2005:2 0.4 1.2 0.6 -0.3 -0.5 -0.7

The USNordic Outlook – November 2003

8

Changing forces of growthOur forecast implies that the driving forces in theeconomy will shift. In recent years, consumption –both private and public – has been totally dominant. Agradually tighter economic policy will decrease thecontribution of consumption to growth. Public sectorconsumption is already stagnating, while householdconsumption is decelerating to growth of around 2½per cent. In the short term, inventory build-up willprop up growth. Fixed investments will then graduallybecome the dominant engine of the economy, thoughit will still take some time before this expansiongenuinely takes off. Due to a weaker dollar, the con-tributions from foreign trade will accelerate. However,weak demand from other countries and continuedcompetitive problems for American companies willkeep the change small.

0504030201009998

7.0

6.0

5.0

4.0

3.0

3.0

2.5

2.0

1.5

1.0

0.5

0.0

Sources: EcoWin, SEB

US: Inflation and unemploymentPer cent Per cent

SEB forecast

Unemployment (LHS)Core inflation, year-on-year change (RHS)

Fed will start hiking rates next autumnDespite the rapid growth that we are seeing right now,the Fed will stick to its pledge to keep the funds ratevery low. The likely scenario is that the Fed will nowgradually signal greater confidence about the labourmarket outlook, but will continue to express concernat the risks of undesirably low inflation. Given ourforecast, it will not be difficult for the Fed to keep itskey rate at low levels. The output gap will remainlarge and inflationary pressure will be low. Unem-ployment will fall somewhat next year, but after that itwill again show an upward trend.

During the winter and spring, the Fed will begin pre-paring the market for a normalisation of interest rates.But its cautious interest-raising cycle will not beginuntil autumn, by which time a 0.5 per cent hike willoccur. In December 2005 the federal funds rate willstand at 3.0 per cent.

The market is currently pricing in a first Fed hike asearly as before summer. The reason for us predicitinga later raise is our weaker-than-consensus growthforecast. The Fed will still hike rates during next yeareven in our conservative forecast. The reason is thatthe Fed’s risk picture will gradually shift. House-hold debts will continue rising at a rapid pace. Thefurther this process continues, the more sensitive theeconomy will be to interest rate hikes once they in-evitably must come.

At present, the Fed has no alternative to continuing itsstimulation of borrowing, since demand is too weak inother parts of the economy. As the corporate sectorstrengthens its balance sheets and capacity utilisationrises, capital spending will climb. With the Americaneconomy beginning to stand on more solid ground, itis likely that the Fed will prefer to accept a certaincooling of growth, instead of continuing to inflate thedebt bubble in the household sector.

USD bn, quarterly data, annualisedUS: Lending to households

Source: EcoWin

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02030

100

200

300

400

500

600

700

800

900

1000

1100

0

100

200

300

400

500

600

700

800

900

1000

1100

JapanNordic Outlook – November 2003

9

Heating up▪ Strong cyclical upswing

▪ Deflationary pressure easing

▪ Reform mandate for Koizumi

The Japanese recovery that began late in 2002 hasbecome stronger than expected. There is consequentlyreason to raise our growth forecast for this yearonce again, this time to 2.4 per cent.

The upturn is occurring on a broad front. Exports haverecovered strongly. Capital spending has reboundedand confidence has climbed in industry – for the firsttime in over three years, today more companies areoptimistic about the future than foresee a downturn.Bond yields have moved up from previously de-pressed levels, resulting in a significant steepening ofthe yield curve. The Tokyo Stock Exchange climbedsharply during the first three quarters of 2003. Finan-cial markets are thus indicating a continued cyclicalupturn and diminishing deflationary expectations. Lastbut not least, rising optimism among households hascontributed to a decline in the savings ratio and con-sumption has risen faster than expected.

We anticipate that the price level will fall by 0.2 percent in 2003, but that next year there will be inflationof 0.1 per cent. Deflation is slowly relaxing its grip.

Growth in 2004 will not be as strong as this year. Tosome extent, the cyclical upswing will lose its vigour.A stronger yen and tighter fiscal policy will also con-tribute to slower growth. GDP will rise by 1.9 percent in 2004.

Since our last forecast, the yen has strengthened morethan expected. This is due to greater strength in theJapanese economy as well as American pressures for amore market-based determination of the value of thedollar against Asian currencies.

Our forecast assumes a marginal strengthening of theyen against the dollar during the coming year. We donot expect the movement of the yen to have majoreffects, however. The Japanese economy is not espe-cially sensitive to exchange rate fluctuations (mer-chandise exports comprise only 10 per cent of GDP),and the export sector is accustomed to external pres-sure for change due to a strong currency.

The domestic economy is being sustained by an ex-pansive monetary policy; the stronger the yen, thelonger the Bank of Japan will keep its key rate at to-day’s extremely low level. We anticipate that the zero

interest rate policy will last until late 2004. Sincethe deflationary danger will gradually ease and theeconomy will regain its footing, during the comingyear the BoJ must prepare the markets for a higherfuture key interest rate.

Second wind for reform policyWhat we are now seeing is mainly a cyclical upswing.The crucial question is whether Japan can now end thelong-term stagnation that has characterised its econ-omy since the big bubble burst 13 years ago.

There are hopeful signs. Over the past six months, co-operation between the BoJ and the Finance Ministry –previously characterised by turf wars and conflictingstrategies – has clearly improved. The new BoJ lead-ership has proved more inclined to satisfy the gov-ernment’s desire for expansion, including the use of“unconventional” methods.

Prime Minister Junichiro Koizumi has strengthenedhis position by being re-elected Chairman of the rul-ing LDP and by winning the recent parliamentaryelection. The LDP’s position did weaken a bit, but theparty has become more dependent on Mr Koizumi asa vote-catcher. As a result, the old “traditionalists”within the LDP have been losing strength. Our per-ception is that the Prime Minister wants to speed thepace of reform efforts. We anticipate that new stepswill be taken in plans to privatise portions of thepostal bank and that there will be increased pressureon the banking sector to restructure.

However, it will take time before reform efforts yieldlasting results. Demography – an old and ageingpopulation – is another obstacle to growth. In ourjudgement, GDP will climb by 1.2 per cent in 2005(close to potential) and inflation will be 0.2 percent.

0504030201009998979695

4

3

2

1

0

-1

-2

-3

4

3

2

1

0

-1

-2

-3

Sources: EcoWin, SEB

Japan: GDP and inflationYear-on-year changePer cent Per cent

GDP

CPI

SEB forecast

The euro zoneNordic Outlook – November 2003

10

Slow recovery has begun▪ Mounting optimism, but modest growth

▪ Stronger euro delaying interest rate hike

▪ Continued watering-down of Stability Pact

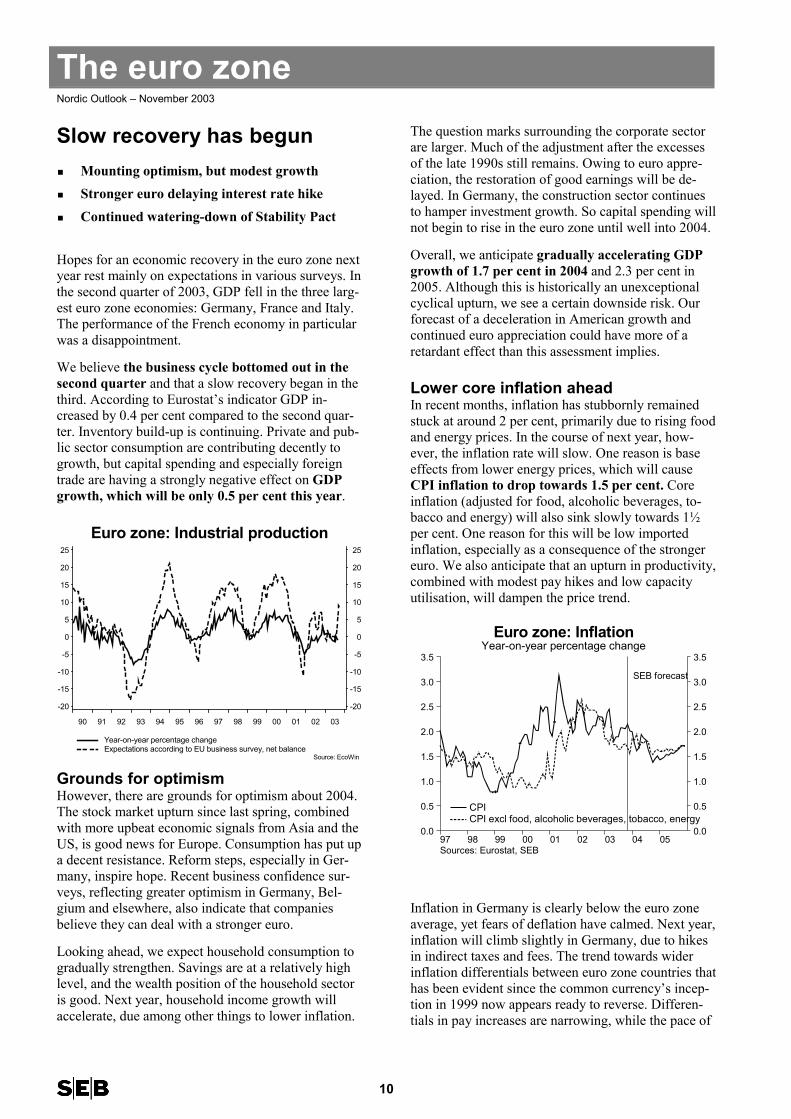

Hopes for an economic recovery in the euro zone nextyear rest mainly on expectations in various surveys. Inthe second quarter of 2003, GDP fell in the three larg-est euro zone economies: Germany, France and Italy.The performance of the French economy in particularwas a disappointment.

We believe the business cycle bottomed out in thesecond quarter and that a slow recovery began in thethird. According to Eurostat’s indicator GDP in-creased by 0.4 per cent compared to the second quar-ter. Inventory build-up is continuing. Private and pub-lic sector consumption are contributing decently togrowth, but capital spending and especially foreigntrade are having a strongly negative effect on GDPgrowth, which will be only 0.5 per cent this year.

Euro zone: Industrial production

Year-on-year percentage change Expectations according to EU business survey, net balance

Source: EcoWin

90 91 92 93 94 95 96 97 98 99 00 01 02 03

-20

-15

-10

-5

0

5

10

15

20

25

-20

-15

-10

-5

0

5

10

15

20

25

Grounds for optimismHowever, there are grounds for optimism about 2004.The stock market upturn since last spring, combinedwith more upbeat economic signals from Asia and theUS, is good news for Europe. Consumption has put upa decent resistance. Reform steps, especially in Ger-many, inspire hope. Recent business confidence sur-veys, reflecting greater optimism in Germany, Bel-gium and elsewhere, also indicate that companiesbelieve they can deal with a stronger euro.

Looking ahead, we expect household consumption togradually strengthen. Savings are at a relatively highlevel, and the wealth position of the household sectoris good. Next year, household income growth willaccelerate, due among other things to lower inflation.

The question marks surrounding the corporate sectorare larger. Much of the adjustment after the excessesof the late 1990s still remains. Owing to euro appre-ciation, the restoration of good earnings will be de-layed. In Germany, the construction sector continuesto hamper investment growth. So capital spending willnot begin to rise in the euro zone until well into 2004.

Overall, we anticipate gradually accelerating GDPgrowth of 1.7 per cent in 2004 and 2.3 per cent in2005. Although this is historically an unexceptionalcyclical upturn, we see a certain downside risk. Ourforecast of a deceleration in American growth andcontinued euro appreciation could have more of aretardant effect than this assessment implies.

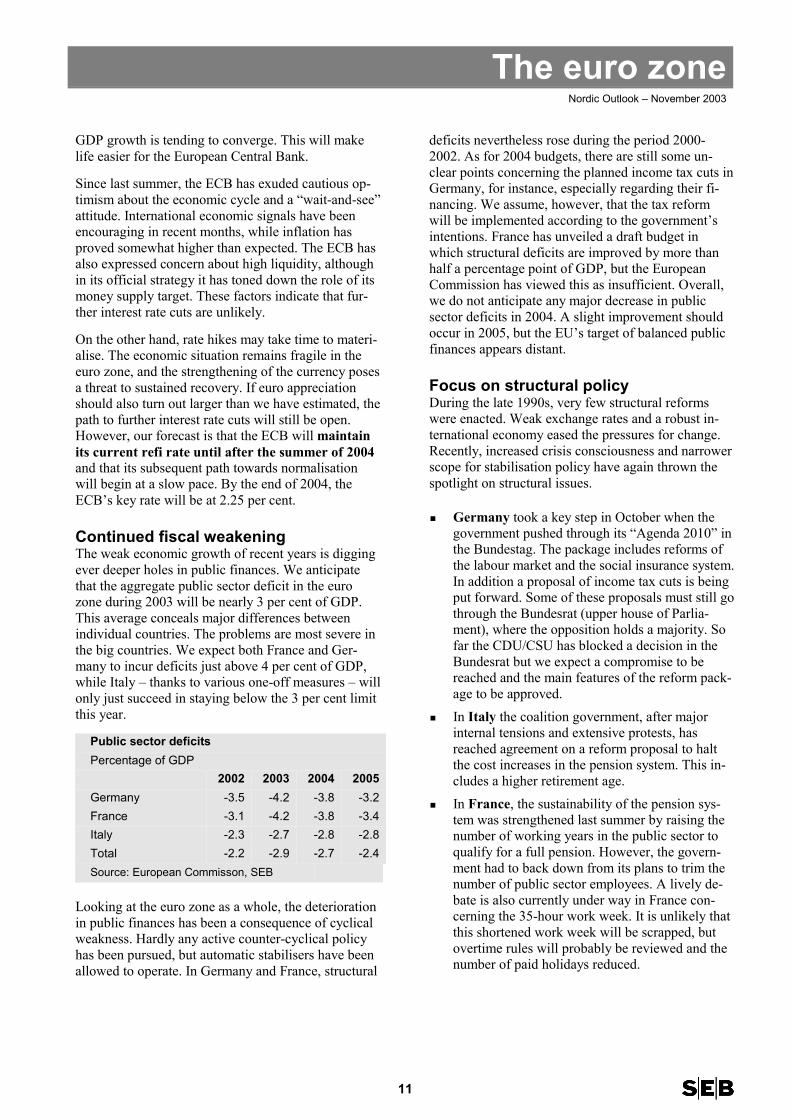

Lower core inflation aheadIn recent months, inflation has stubbornly remainedstuck at around 2 per cent, primarily due to rising foodand energy prices. In the course of next year, how-ever, the inflation rate will slow. One reason is baseeffects from lower energy prices, which will causeCPI inflation to drop towards 1.5 per cent. Coreinflation (adjusted for food, alcoholic beverages, to-bacco and energy) will also sink slowly towards 1½per cent. One reason for this will be low importedinflation, especially as a consequence of the strongereuro. We also anticipate that an upturn in productivity,combined with modest pay hikes and low capacityutilisation, will dampen the price trend.

050403020100999897

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

3.5

3.0

2.5

2.0

1.5

1.0

0.5

0.0

Sources: Eurostat, SEB

Euro zone: InflationYear-on-year percentage change

SEB forecast

CPICPI excl food, alcoholic beverages, tobacco, energy

Inflation in Germany is clearly below the euro zoneaverage, yet fears of deflation have calmed. Next year,inflation will climb slightly in Germany, due to hikesin indirect taxes and fees. The trend towards widerinflation differentials between euro zone countries thathas been evident since the common currency’s incep-tion in 1999 now appears ready to reverse. Differen-tials in pay increases are narrowing, while the pace of

The euro zoneNordic Outlook – November 2003

11

GDP growth is tending to converge. This will makelife easier for the European Central Bank.

Since last summer, the ECB has exuded cautious op-timism about the economic cycle and a “wait-and-see”attitude. International economic signals have beenencouraging in recent months, while inflation hasproved somewhat higher than expected. The ECB hasalso expressed concern about high liquidity, althoughin its official strategy it has toned down the role of itsmoney supply target. These factors indicate that fur-ther interest rate cuts are unlikely.

On the other hand, rate hikes may take time to materi-alise. The economic situation remains fragile in theeuro zone, and the strengthening of the currency posesa threat to sustained recovery. If euro appreciationshould also turn out larger than we have estimated, thepath to further interest rate cuts will still be open.However, our forecast is that the ECB will maintainits current refi rate until after the summer of 2004and that its subsequent path towards normalisationwill begin at a slow pace. By the end of 2004, theECB’s key rate will be at 2.25 per cent.

Continued fiscal weakeningThe weak economic growth of recent years is diggingever deeper holes in public finances. We anticipatethat the aggregate public sector deficit in the eurozone during 2003 will be nearly 3 per cent of GDP.This average conceals major differences betweenindividual countries. The problems are most severe inthe big countries. We expect both France and Ger-many to incur deficits just above 4 per cent of GDP,while Italy – thanks to various one-off measures – willonly just succeed in staying below the 3 per cent limitthis year.

Public sector deficitsPercentage of GDP

2002 2003 2004 2005Germany -3.5 -4.2 -3.8 -3.2France -3.1 -4.2 -3.8 -3.4Italy -2.3 -2.7 -2.8 -2.8Total -2.2 -2.9 -2.7 -2.4Source: European Commisson, SEB

Looking at the euro zone as a whole, the deteriorationin public finances has been a consequence of cyclicalweakness. Hardly any active counter-cyclical policyhas been pursued, but automatic stabilisers have beenallowed to operate. In Germany and France, structural

deficits nevertheless rose during the period 2000-2002. As for 2004 budgets, there are still some un-clear points concerning the planned income tax cuts inGermany, for instance, especially regarding their fi-nancing. We assume, however, that the tax reformwill be implemented according to the government’sintentions. France has unveiled a draft budget inwhich structural deficits are improved by more thanhalf a percentage point of GDP, but the EuropeanCommission has viewed this as insufficient. Overall,we do not anticipate any major decrease in publicsector deficits in 2004. A slight improvement shouldoccur in 2005, but the EU’s target of balanced publicfinances appears distant.

Focus on structural policyDuring the late 1990s, very few structural reformswere enacted. Weak exchange rates and a robust in-ternational economy eased the pressures for change.Recently, increased crisis consciousness and narrowerscope for stabilisation policy have again thrown thespotlight on structural issues.

▪ Germany took a key step in October when thegovernment pushed through its “Agenda 2010” inthe Bundestag. The package includes reforms ofthe labour market and the social insurance system.In addition a proposal of income tax cuts is beingput forward. Some of these proposals must still gothrough the Bundesrat (upper house of Parlia-ment), where the opposition holds a majority. Sofar the CDU/CSU has blocked a decision in theBundesrat but we expect a compromise to bereached and the main features of the reform pack-age to be approved.

▪ In Italy the coalition government, after majorinternal tensions and extensive protests, hasreached agreement on a reform proposal to haltthe cost increases in the pension system. This in-cludes a higher retirement age.

▪ In France, the sustainability of the pension sys-tem was strengthened last summer by raising thenumber of working years in the public sector toqualify for a full pension. However, the govern-ment had to back down from its plans to trim thenumber of public sector employees. A lively de-bate is also currently under way in France con-cerning the 35-hour work week. It is unlikely thatthis shortened work week will be scrapped, butovertime rules will probably be reviewed and thenumber of paid holidays reduced.

The euro zoneNordic Outlook – November 2003

12

Stability Pact under threatThe Stability Pact is under severe strain. When thePact was written in 1997, it was a compromise be-tween two approaches to fiscal policy:

� According to one approach, each member countryin the currency union should pursue an independ-ent fiscal policy. Since euro zone monetary policycan only be pursued at union level, it is necessaryfor individual countries to be able to stabilise theireconomies via fiscal policy if they are hit by a na-tional disruption.

� Offsetting this is the risk that the policies of a sin-gle country may have an impact at union level. Anexpansive policy in a large country may drive upinflation in the entire union – forcing the ECB toraise interest rates for all member countries.

The rules…The Pact stipulated that fiscal policy as a whole re-mained the business of individual countries, butwould meanwhile be limited by a common set ofrules. The treaty text contains rules about balancingbudgets over a business cycle and states that overallpublic sector deficits may not exceed 3 per cent ofGDP. The treaty was supplemented by more opera-tive resolutions about time limits for excessive defi-cits and under what circumstances the deficit ceilingmay be breached: according to the rules, this mayonly occur during a deep recession.If the European Commission is of the opinion that amember country risks breaking these rules, it beginsan “excessive deficit procedure”. The Commissionwrites an opinion, after which the European Councildecides whether there is an excessive deficit and is-sues recommendations to the country in question. Ifinsufficient steps are taken, sanctions shall be im-posed. They consist of a deposit in a non-interest-bearing account. If the deficit still persists after twoyears, the deposit shall be transformed into a fine.

…and the realityWe believe that the Pact has contributed to betterbudget discipline during the recent cyclical slowdownthan would have existed without the Pact. But thisperiod of weak growth has also subjected the Pact tostrains. To date, the Commission has initiated its ex-cessive deficit procedure against three countries:Portugal (for its 2001 deficit) as well as Germanyand France (2002 deficits). Portugal was subjectedto tough discipline by the Council – but the ruleswere bent for the two larger countries.Although Germany is violating the Pact several yearsin a row, the Council has shown great tolerance.

Finance ministers have had qualms about imposingtough belt-tightening requirements on the union’slargest country.France, however, has triggered opposition by openlydeclaring that its domestic goals enjoy precedenceover the rules of the Pact. The Commission arguesthat France has not taken sufficient steps to remedythe deficits, but has still accepted a gentle interpreta-tion of the rule system. The Commission has calledfor an improvement in the structural deficit of 1.0 percent of GDP in 2004, but France has been cool eventowards this comparatively mild action.

Even more compromisesAt present, the Council is deadlocked and a decisionconcerning France has been postponed until No-vember 25. At the same meeting, the Commissionalso wants to reopen the case against Germany. Weanticipate, however, that the two big countries willgather enough votes to prevent any serious sanc-tions procedure from being set in motion. Some kindof compromises will likely be reached: France andGermany will receive a verbal warning, but theCouncil will again extend the timetable for restoringbudgetary order.The medium-term effects of such compromises arenot big. Given the forecasts we have made in this is-sue of Nordic Outlook, the deficits will graduallyshrink in the next few years. Besides, financial mar-ket confidence in the Pact is already low; anothercompromise is not likely to seem especially dramatic.However, every new round of horse-trading under-scores that the Pact is under threat. In practice, bothGermany and France are violating the existing rulesystem – and Council has de facto accepted this. Ifthe Pact is to survive unscathed, the EU must dealwith the troublesome gap between rules and real-ity.This is probably exactly what will happen. No totalrenegotiation of the Pact seems imminent; the EUdraft constitution contains no change in the Pact. It islikely, however, that the resolutions that make thetreaty operational will be modified to fit better with themilder interpretation that has evolved in practice.This concerns the circumstances under which thedeficit ceiling may be exceeded and the time limitwithin which excessive budget deficits are to be rem-edied. This will allow the EU to save face by arguingthat it is adhering to the Treaty but has neverthelessmade the Pact more flexible. In practice, however, itmeans that the Pact itself is increasingly becoming adocument written in sand.

The United KingdomNordic Outlook – November 2003

13

Modest interest rate hike▪ Unexpected economic strength

▪ Buying pressure will slowly cool

▪ Lingering risk of home price decline

The British economy began a gradual recovery duringthe summer, earlier than expected. Stronger interna-tional demand is stimulating exports and capitalspending. Meanwhile the inflation risk has increased,since already lofty home prices have continuedclimbing. In early November, the Bank of Englandthus carried out its first key interest rate hike for fouryears: from 3.50 to 3.75 per cent.

The national accounts were revised during theautumn. Growth in recent years has been somewhatstronger and more balanced than assumed earlier.Private consumption has not been quite as dominantas previously reported.

The revised figures show stronger growth during thefirst half of 2003; second-quarter GDP growth wasdoubled from 0.3 to 0.6 per cent, on a quarterly basis.This trend continued in the third quarter, when privateservices were a driving force. In light of this andpositive global economic signals, we are revising ourGDP forecasts slightly upward, to 1.9 per cent thisyear, then 2.4 and 2.6 per cent, respectively, in thenext two years.

The housing market shows no signs of cooling. Thepace of year-on-year price increases remains at around20 per cent. This is one important reason why house-holds have resumed their buying spree. Lending tohouseholds is also climbing at a high, stable year-on-year pace of 10-15 per cent. This continued build-upof debt risks escalating to unsustainable levels.

BoE cools the housing marketIn our view, these are the most important reasons whythe BoE recently raised its repo rate. The central bankhad previously hoped for an autonomous cooling indomestic demand and the housing market. But this didnot happen. This is why the BoE wants to dampenpartly credit-driven UK domestic demand and thehousing market.

The BoE will be relatively cautious about further ratehikes. Low inflation also provides room for such astrategy. The central bank will raise its key rate by0.25 percentage points in the first quarter of 2004,then by a total of 0.50 points in the second half of theyear.

This will be sufficient to slow the pace of growth inprivate consumption to just above 2 per cent annuallyin 2004-2005. Real income growth will decelerate andunemployment will climb somewhat. We also predicta certain downturn in home prices. The householdsavings ratio will rise to a historically high 10-11 percent in 2005.

Monetary policy is likely to switch to a new guidingprinciple soon. The BoE is abandoning its inflationtarget based on the retail price index (RPIX) in favourof the EU’s harmonised index of consumer prices(HICP). However, this will have no major impact oninterest rate decisions. Granted that the HICP is at alow 1.4 per cent today, well below the new 2 per centtarget. But looking ahead two years, inflation willclimb to 2 per cent as a consequence of increasedeconomic activity as well as a weakening of thepound.

In effective terms, the currency has depreciated by 7per cent in the past year. The pound will strengthensomewhat in the short term, since the BoE is the firstcentral bank to begin the rate hike cycle. But viewedover a two-year period, there will again be someweakening, partly due to growing government budgetand current account deficits.

UK: Repo rate and house prices

BoE repo rate, per cent (LHS) House prices (Halifax), index 1983 = 100 (RHS)

Source: EcoWin

95 96 97 98 99 00 01 02 03

175

200

225

250

275

300

325

350

375

400

425

450

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

Fiscal policy is expansive. Public sector consumptionwill grow by 3 per cent next year. Health care andeducational investments, combined with lower taxrevenues than expected, will lead to budget strains. In2005, the UK public sector deficit will exceed theMaastricht limit of 3 per cent of GDP.

Chancellor Gordon Brown has a reputation as aguardian of good budgetary discipline, but this is nowunder threat. There is a major risk that for the firsttime in six years, the Labour government will violateits “golden rule” that the central government shouldnot borrow more than it invests over a business cycle.

Emerging marketsNordic Outlook – November 2003

14

Chinese dragon growingfaster and faster▪ Increasing stability in Latin America

▪ Vigorous expansion in China

▪ Controlled revaluation of the yuan

The improving international outlook also applies tothe world’s emerging markets. Low interest rates andshrinking credit spreads are benefiting developingeconomies. Exports are being stimulated by the recov-ery in the US and Japan and in a number of cases alsoby the falling US dollar, since many currencies arepegged to the dollar.

The major economies in Latin America are showingsigns of stabilisation:

▪ In Argentina, the economy has begun to climbout of its depression. The peso has strengthenedby some 25 per cent in the past year, and acutecredit problems have been bridged over by meansof a large IMF loan.

▪ In Brazil, too, the currency has strengthened andinterest rates have fallen. The confidence of inter-national financial markets in the Brazilian leader-ship has increased significantly. Even thoughPresident Lula’s programme for trimming pensionexpenditures for public sector employees is en-countering strong resistance, we expect that it willpass. We do not expect any dramatic new crises inthe next few years.

In Asia, the picture is mainly bright. The big excep-tion is Hong Kong, which is still suffering from theburst real estate bubble. The dollar decline and lowAmerican interest rates have nevertheless providedsome support via the currency board system.In India, large-scale outsourcing of service activitiesby the West is generating new jobs and boosting tech-nical skills. Meanwhile, step-by-step reforms areslowly making the economy more flexible. The proc-ess has achieved such a dynamic that it will also yieldgood growth over the next few years.

China is demonstrating unparalleled growth. Thereare many indications that this year’s GDP increasewill exceed 10 per cent. This would imply 20 per centor more in the rapidly growing coastal regions.Growth is driven by a massive influx of direct invest-ments, an almost inexhaustible supply of cheap la-bour, high investment ratios and a rapid rise in pur-chasing power. China’s accession to the WTO hasopened a growing number of markets, and we antici-pate an increase in the pace of privatisation of state-owned companies.

This expansion is not without problems, however.Inflation is climbing, though still at a low level. Therisk of overheating that will have to be cooled bytough austerity is not imminent right now but maycreep up gradually. We expect that a credit tighten-ing will cool off growth somewhat during nextyear. Longer term, the new leadership of the centralgovernment and the ruling party face the challenge ofcreating a new social insurance system. The bankingsystem is fragile, and restoring it to health will take anumber of years.

Slow, controlled revaluation of yuanChina’s renminbi (“people’s currency”) and its basicunit, the yuan, are pegged to the dollar at a fixed ex-change rate of CNY 8.28. Loud American demandsfor a future Chinese currency revaluation are basedon the fact that China has large trade surpluses withthe US, and that a large influx of capital is contribut-ing to the build-up of rapidly growing Chinese foreigncurrency reserves.It is difficult to calculate an equilibrium exchange ratefor the yuan, since it is not convertible. It is probablyundervalued, but estimates of how much vary. Amodest Chinese currency appreciation would benefitthe world economy; it would make growth easier inthe US and Europe, while cooling down the rapidlygrowing Chinese economy somewhat. China is nev-ertheless unlikely to implement a large one-off re-valuation, among other things because it does notwish to stat a series of currency discuptions in Asia.China’s negotiating position is also relatively

strong, since it is sitting on large holdings of Ameri-can government securities, and since different tradeand barter agreements also may be part of a deal.Nor will any transition to a floating exchange ratetake place as long as the banking system is vulner-able.The likely compromise is that during our forecastperiod – at the earliest during H2 2004 – China willbroaden the yuan’s fluctuation band against the dol-lar and let its currency strenghten within that band. Aprobable pace of appreciation is 3-5 per cent an-nually. We foresee no difficulties for the Chinesecentral bank to steer the yuan in the desired direc-tion, since the currency will not become entirely con-vertible for many years to come. The appreciationwill not be large enough to have any measurable ef-fects on trade.

Central and Eastern EuropeNordic Outlook – November 2003

15

More balanced growth▪ Exports recovering

▪ EU accession will drive capital spending

▪ Budget deficits causing concern

Weak demand in the West has only had a marginalimpact on the relatively strong economic performanceof Central and Eastern Europe. In large economiessuch as Russia and Poland, as well as in the CzechRepublic, Latvia and Lithuania, GDP growth is ac-celerating this year. Russia has benefited from highoil prices, while Poland and other countries are expe-riencing export-driven recovery, despite weaknessesin the EU. The competitiveness of the Polish exportsector has strengthened, thanks to streamlining, lowpay increases and a sharp weakening of the currencyexchange rate.

Except for Poland, strong domestic demand hasfuelled growth in most of the region’s countries.Growing private consumption is a central drivingforce. The background is high real pay increases and,in many places, major cuts in real interest rates. Thelatter is partly a consequence of convergence tradingin the run-up to EU membership on May 1, 2004.

Consumption will continue to stimulate growth nextyear, except in Slovakia and Hungary, where eco-nomic policy is being tightened. Meanwhile, the in-crease in exports and capital spending is strengthen-ing. This will mean broader, more vigorous economicgrowth over the next couple of years.

The Baltic countries and Russia are leading the way inannual GDP increases 2004-2005, with Estonia, Lat-via and Lithuania showing growth in the 5.5-7.0 percent range and Russia about 5 per cent.

In Russia, President Vladimir Putin is in a strongposition in the run-up to the Duma election in Decem-ber and the presidential election in March 2004. TheYukos affair − including the arrest of the oil com-pany’s former head, Mikhail Khodorkovsky − isprimarily politically motivated. In spite of Moody´srevision of Russia´s credit rating to investment grade,the affair underlines sustained legal and political risksin Russia. The short-term effect of the Yukos affairwill be a slowing of foreign capital flows to Russia.However, after the elections we expect the situation tostabilise and the economic reform policies to continue.

An upswing for exports is especially welcome in theCzech Republic, Hungary and Estonia, which areshowing sizeable current account deficits – in Esto-nia’s case at an alarming level, this year more than 15per cent of GDP. We anticipate that the Estonian defi-cit will shrink to about 10 per cent in 2005. This isnevertheless well above the 6-7 per cent of GDP thatis a sustainable level. Despite the need for belt-tightening, fiscal policy will remain expansive, amongother things due to an income tax cut. This increasesthe risk of interest rate unrest in Estonia.

What may jeopardise a continued favourable eco-nomic scenario in Central and Eastern Europe is theabove-mentioned external imbalances, as well as sub-stantial budget deficits in several countries

.

Delayed enlargement of the euro zoneThe new EU countries transition to the euro will bedelayed. The reason is that several countries willhave problems meeting budget and inflation criteria.This applies especially to Poland, the Czech Repub-lic, Hungary and Slovakia, although the first two arein better shape in terms of inflation.This year, these four countries will report budgetdeficits of between 5.0 and 8.0 per cent of GDP,which is well above the Maastricht limit of 3 per cent.

� In our judgement, over the next few years thegovernments of Slovakia, the Czech Republicand Hungary will implement the necessarybudget austerity measures to reduce their eco-nomic imbalances, while maintaining levels ofconfidence in the market.

� Poland’s fragile minority government is continu-ing to pursue an expansive fiscal policy, however.This risks leading the country into a budget crisis,with threatened downgrading of its

credit rating. We nevertheless anticipate certainbudget cutbacks in 2005, but even after thesethe budget will show minus 6 per cent.

Our conclusion is that economic imbalances will de-crease in these four countries, but that their transitionto the euro will be delayed by a year or more com-pared to their original optimistic timetable.The signals from the EU side are also that there is nohurry to enlarge the euro zone eastward. We antici-pate a strict interpretation of the Maastricht criteria. Anarrow exchange rate fluctuation band would createunrest during the candidate countries’ period in theERM2.Our forecast is that the Baltic countries plus Slo-venia will make up the first wave that switches tothe euro in 2008. Next in line, in 2008-2009, will beSlovakia and Hungary. Poland and the Czech Re-public appear likely to have to wait until 2009-2010.For a detailed analysis, see Baltic Outlook, Oct 2003.

International financial marketsNordic Outlook – November 2003

16

Continued low interest rates▪ Warning against stock market overoptimism

▪ Continued steep yield curves

▪ The dollar will weaken further

During the summer and early autumn, internationalshare prices as well as bond yields climbed sharply.The main reason was that last spring’s deflation wor-ries disappeared. During the autumn, stock exchangeswere also cheered by both second and third quarterearnings reports that exceeded expectations. Mean-while, macroeconomic signals have been strong. Theconsequence has been increased risk appetite.

This financial optimism will not continue into 2004.In our scenario, stock exchanges will eventually face acalmer period and bond yields in both the US andEurope will move sideways.

Stock market upturn will slowStronger economic signals and positive companyreports, especially in the US, have driven broad stockmarket indexes upward during the summer andautumn. Cyclically sensitive industries, such as engi-neering and consumer capital goods, have climbedappreciably.

This is typical of a recovery after a cyclical downturn.It is often characterised at first by a steeper yieldcurve and by sharply climbing confidence indicators.This leads to rising risk appetite, where the first up-swing results in a strong upturn in indexes led bycyclical shares. This year, technology and growthshares have also recovered sharply.

We are now on the way into a calmer phase, whereeconomic indicators will level off and the yield curvewill no longer become steeper. After the powerfulGDP rebound of recent months in the US, sentimentindicators will gradually flatten and turn downward.This will lead to a considerably calmer stock mar-ket. For this reason, we do not anticipate that thesemovements will have any major macroeconomic ef-fect during the next year.

Bond yields will peakDuring the summer and autumn, bond yields climbedsharply, especially in the US. Their levels thus re-verted to those prevailing at the beginning of the year.American yields also pulled European ones with them.

Market interest rates will remain low. During the firsthalf of 2004, the interest rate upturn in the US willcease and bond yields will stay put. After that, therewill be a marginal upturn, bringing 10-year Treasuryyields to 5.0 per cent at the end of 2005.

We thus believe that interest levels will be lower thanreflected in market expectations. The main reason isthat our 2004 US growth forecast is below consensusand we anticipate growth below long-term potentialduring 2005. The output gap will thus remain sizeable,and inflation will be low. The tightening of fiscalpolicy that begins in 2005 will also help to hold downinterest levels.

Weekly average, per cent10-year government bond yields

US Germany

Sources: EcoWin, SEB

99 00 01 02 03 04 05

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

SEB forecast

European bond yields are following the same pattern,but at a somewhat lower level. Slow growth and lowinflation will hold down yields.

Unchanged central bank ratesThe Fed will keep its key interest rate at a very lowlevel to prevent households from cutting back theirconsumption too quickly. However, the Fed willgradually prepare the market for future rate hikes. Thefirst step toward a normalisation of the key rate levelwill be taken during the second half of 2004, whenthe federal funds rate is increased to 1.5 per cent. Itwill reach 3.0 per cent at the end of 2005 − somewhatbelow our previous forecast.

Due to low inflation and an appreciating euro, theECB will also hold off on interest rate hikes. The firstECB rate hike will come in the autumn of 2004. Atthe end of 2004, the bank’s refi rate will be 2.25 percent and at the end of 2005 it will be 3.25 per cent.

International financial marketsNordic Outlook – November 2003

17

Per centKey rates

US: Fed funds Euro zone: Refi rate (Germany until 1999)

Sources EcoWin, SEB

97 98 99 00 01 02 03 04 050

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7SEBforecast

Credit spreads – the gap between corporate or emerg-ing market bonds and “safe” government bonds inlarge countries – narrowed sharply during the lowinterest period last spring. During the autumn, theyhave continued to shrink. This reflects an increasedrisk appetite and diminshed bankruptcy risks. Thespreads have squeezed together so much that we doubtthat this movement will continue. Nor do we foresee awidening of credit spreads.

Continued weakening of the dollarIn our last Nordic Outlook, the forecast was that nextyear, the American dollar would weaken to USD 1.20.However, the dollar weakened considerably fasterthan we had expected. One factor that helped triggerthis development was the G7 statement in Septemberabout the need for more “flexible” exchange rates.

The flows generated by direct investments and port-folio reallocations are now contributing to downwardpressure on the dollar. From a fundamental analyticperspective, too − based on the current account deficit− the dollar should weaken from today’s level. Weestimate that the long-term equilibrium exchange rateis USD 1.10-1.15 per EUR.

In order to significantly reduce the big US currentaccount deficit, the dollar needs to be weaker than thisfor some years ahead. We anticipate that the dollarwill reach USD 1.22 per euro during the spring,then remain in the USD 1.20-1.25 range.

The US trade deficit with China has been in the spot-light recently. As indicated above, we anticipate anappreciation of the yuan by 3-5 per cent in 2005.This is not enough to affect trade flows to any greatextent.

The Japanese yen has been traded in a managedmarket, where Japan’s Ministry of Finance has inter-vened continuously to slow any yen appreciation.However, the Ministry seems to have shifted its sightsand is now accepting a somewhat stronger yen thanpreviously. We anticipate that during the comingyear the yen will trade at around 105 per dollar.

There is an obvious risk here that the dollar may fallmore sharply, since the corrections that have occurredto date have not affected trade flows to any great ex-tent. If this occurs, though, a new kind of PlazaAgreement between the major countries is likely to beworked out, in order to counteract excessively sharpcurrency movements.

Weekly averageExchange rates EUR/USD and USD/JPY

USD/JPY (RHS) EUR/USD (LHS)

Sources: EcoWin, SEB

99 00 01 02 03 04

100

105

110

115

120

125

130

1350.80

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

SEBforecast

International financial marketsNordic Outlook – November 2003

18

The US current account deficit and the dollarThe American current account deficit is more than 5per cent of GDP. Deficits normally shrink whengrowth slows, since lower growth usually results inlower imports. In the case of the United States, thishas not occurred; today the deficit is twice as largeas it was when economic growth peaked in 1999.For a long time, it could be argued that the Americandeficit was not a problem, since it was matched by alarge capital account surplus: Other countries werewilling to buy American securities on a large scale –so large that the dollar continued to climb despite thegrowing US current account deficit.Today, however, the deficit appears more worrisome.It has reached such a high level that the US has be-come by far the world’s largest borrower. Due togrowing interest costs, the continued swelling of thedeficit is becoming harder and harder to stop. Norare private, business-driven capital flows coveringthe deficit any longer. Instead it is primarily strategicdollar purchases by Asian central banks.

An unstable situationAll this makes today’s situation unstable. IMFeconomists have emphasised that no country inmodern history has been able to maintain such largecurrent account deficits for as long a period as theUS has today; such deficits have always resulted in asizeable weakening of the currency – often by 25-30per cent – or a sharp economic deceleration (orboth), after which a gradual reduction in the deficitcould take place.Granted that the US is no ordinary country. Its cur-rency is the world’s reserve currency, which gives itsubstantial resilience. Nevertheless, the market’s in-terest in the dynamic of the current account deficithas been awakened. The G7 statement in Dubai thisautumn about the need for more “flexible” exchangerates must also be interpreted as a wish that thedollar will fall, at least against major Asian curren-cies.

Our forecast projects a decline in the dollar to USD1.22 per euro this spring and a strengthening of theyen to 105 per dollar. This is not enough to bringabout a rapid decrease in the deficit, however. Cal-culations by the IMF and others indicate that thedollar would need to fall by 35 per cent for the deficitto shrink significantly.One common view is that the economies of Japanand Europe would suffer serious damage from afurther sizeable weakening of the dollar. This risk isoften exaggerated. Movements between leading cur-rencies have previously been very large, especiallyin the 1980s, without significant consequences in thereal economy.It is also possible to identify arguments as to why aweakening of the dollar might have a positive net ef-fect on global growth:� The reaction of central banks will be asymmetri-

cal in a way that will lead to overall easing ofmonetary policy. The Fed will not be con-cerned about the weakening, while the ECB andBoJ will pursue a looser policy if their currenciesstrengthen.

� Stock markets will react positively. In the past1-2 years, a weaker dollar has been correlatedwith a stock market upturn. This trend may con-ceivably continue; an upturn in US stock ex-changes will have contagious effects, whilestock exchanges will generally react positively toa better long-term balance situation in the worldeconomy.

On the other hand, a development in which the Asiancentral banks stop their supportive purchases ofAmerican Treasury securities will lead to generalupward pressure on long-term bond yields.Our overall conclusion is that the world economycan cope with a weaker dollar – provided that ithappens in an “orderly” fashion rather than in large,destabilising jumps.

SwedenNordic Outlook – November 2003

19

Limping recovery▪ Robust productivity offsets krona appreciation

▪ Households can handle tighter policy

▪ Weak local government finances will slow re-covery

▪ Low inflation – but how to measure it?

A stronger krona and tighter fiscal policy will helpmake the Swedish recovery sluggish. GDP will riseby 2.1 per cent in 2004 and 2.3 per cent in 2005, inparity with its potential level. Growth will be drivenby household consumption and exports, while therecovery in capital spending will be delayed. Thecyclical upswing will be too weak to achieve a turn-around in the labour market. Unemployment will stayat nearly 5 per cent until 2005.

Inflation will be low in 2004, due to the strongerkrona and lower energy prices. The wage round willproceed smoothly. In 2005 too, underlying inflationwill end up below the Riksbank’s target. However, thecentral bank will abstain from interest rate cuts, sinceit will be continuing to focus on an inflation measureadjusted for energy prices and because the cyclicalupswing will be underway and lending to householdswill still be rising. The first Riksbank interest ratehike will not occur until next autumn.

The official target of a public sector budget surplustotalling 2 per cent of GDP appears increasingly dis-tant. Public sector savings will fall below 1 per cent of

GDP in both 2004 and 2005. The central governmentbudget seems likely to stay below its expenditureceiling this year, but will again end up under pressurenext year. It will be hard for Prime Minister GöranPersson to win solid support for the ambitious growthpolicy signalled in his mid-September Statement ofGovernment Policy, both among his ruling SDP andits parliamentary allies, the Left Party and GreenParty. We foresee compromises, resulting only inminor changes in the tax system during our forecastperiod.

Local governments are being squeezed by slowergrowth and small increases in central governmentgrants. Meanwhile, demand for health care and socialservice expenditures is continuing to grow. Both in2004 and 2005, local governments will boost incometaxes and fees while holding back on consumption.This will slow Sweden’s economic recovery.

Industry can tolerate stronger kronaThe krona will appreciate significantly in trade-weighted terms (see also the final section of thischapter). The Riksbank’s Total CompetitivenessWeighted or TCW index will fall to 120, a level notreached since 1998.

Most economists are arguing the krona is underval-ued. Traditional macro indicators also show that Swe-den can handle a stronger krona. The current accountsurplus is large and the competitiveness of manufac-turing industry, measured as relative unit labour cost(RULC), looks strong.

Why so little drama in the forecasts?Today’s macro forecasts for the Swedish economyare unusually tightly clustered around a gradual re-covery to GDP growth that is close to the long-termtrend. Our own forecast is slightly below consensus,mainly due to our somewhat weaker internationalscenario. But in our forecast, major risks or possibili-ties for the Swedish economy in the near future donot play any prominent role either. Why does thepicture look so undramatic?� One reason is that right now the output gap is

small. It is thus difficult to foresee any largeswings in growth − either strong cyclical re-covery or some form of collapse due to over-heating.

� Inflation is under control and the outlook for apeaceful wage round is good. No sharp realign-ment of monetary policy is likely.

� Government finances are in decent shape. Nei-ther the public sector nor households are bur-dened by imbalances that can form the startingpoint for a dramatic economic scenario.

The risks of serious contagious effects from thestock market slide on home prices have faded.

� On the other hand, there are few signs of break-through in official growth and structural policythat could initiate a period of more robustgrowth.

Obviously we can never rule out a different economiccourse of events. The international scenario includesboth upside and downside risks. Domestic factorsthat might trigger stronger growth are a more vigor-ous resurgence in the information and communica-tions technology (ICT) sector or a clearer break-through in growth policy than we expect. On thedownside is the risk that the weakening trend of pub-lic finances is more severe than in our forecast andthat austerity measures aimed at households willthus be larger.Yet our overall assessment is that various risk sce-narios both have less amplitude and are less likelythan normally.

SwedenNordic Outlook – November 2003

20

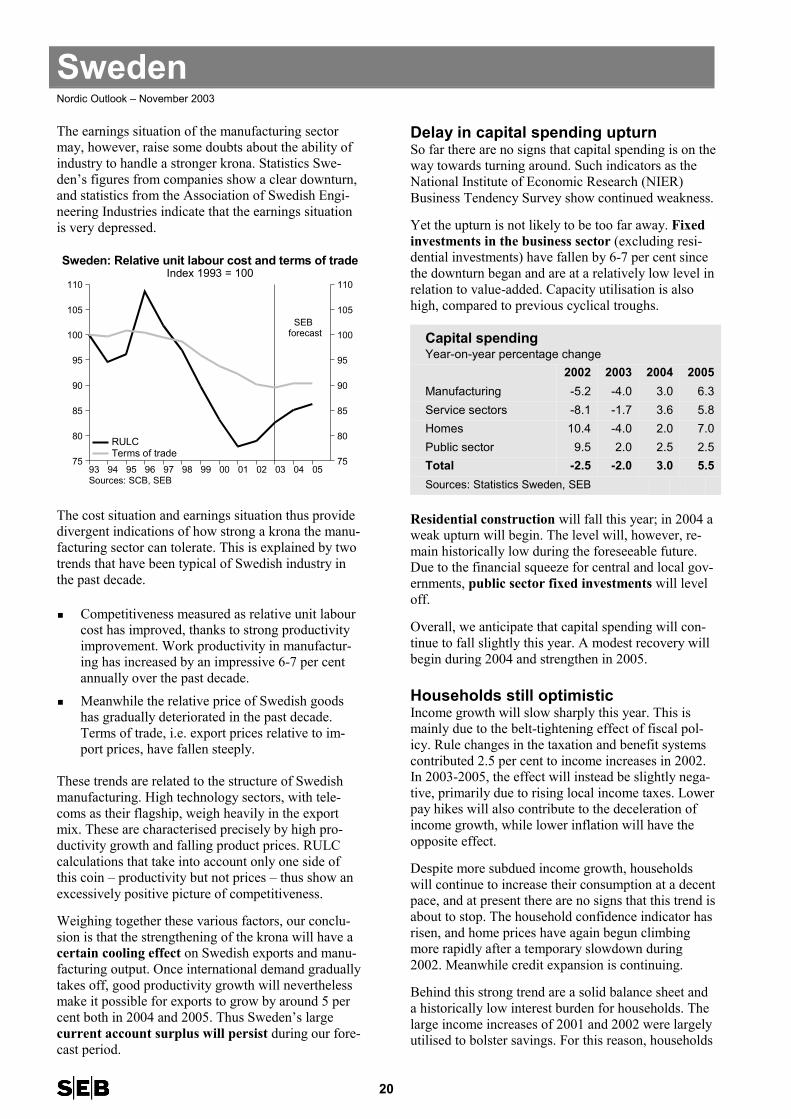

The earnings situation of the manufacturing sectormay, however, raise some doubts about the ability ofindustry to handle a stronger krona. Statistics Swe-den’s figures from companies show a clear downturn,and statistics from the Association of Swedish Engi-neering Industries indicate that the earnings situationis very depressed.

05040302010099989796959493

110

105

100

95

90

85

80

75

110

105

100

95

90

85

80

75

Sources: SCB, SEB

Sweden: Relative unit labour cost and terms of tradeIndex 1993 = 100

SEB forecast

RULCTerms of trade

The cost situation and earnings situation thus providedivergent indications of how strong a krona the manu-facturing sector can tolerate. This is explained by twotrends that have been typical of Swedish industry inthe past decade.

▪ Competitiveness measured as relative unit labourcost has improved, thanks to strong productivityimprovement. Work productivity in manufactur-ing has increased by an impressive 6-7 per centannually over the past decade.

▪ Meanwhile the relative price of Swedish goodshas gradually deteriorated in the past decade.Terms of trade, i.e. export prices relative to im-port prices, have fallen steeply.

These trends are related to the structure of Swedishmanufacturing. High technology sectors, with tele-coms as their flagship, weigh heavily in the exportmix. These are characterised precisely by high pro-ductivity growth and falling product prices. RULCcalculations that take into account only one side ofthis coin – productivity but not prices – thus show anexcessively positive picture of competitiveness.

Weighing together these various factors, our conclu-sion is that the strengthening of the krona will have acertain cooling effect on Swedish exports and manu-facturing output. Once international demand graduallytakes off, good productivity growth will neverthelessmake it possible for exports to grow by around 5 percent both in 2004 and 2005. Thus Sweden’s largecurrent account surplus will persist during our fore-cast period.

Delay in capital spending upturnSo far there are no signs that capital spending is on theway towards turning around. Such indicators as theNational Institute of Economic Research (NIER)Business Tendency Survey show continued weakness.

Yet the upturn is not likely to be too far away. Fixedinvestments in the business sector (excluding resi-dential investments) have fallen by 6-7 per cent sincethe downturn began and are at a relatively low level inrelation to value-added. Capacity utilisation is alsohigh, compared to previous cyclical troughs.

Capital spendingYear-on-year percentage change

2002 2003 2004 2005Manufacturing -5.2 -4.0 3.0 6.3Service sectors -8.1 -1.7 3.6 5.8Homes 10.4 -4.0 2.0 7.0Public sector 9.5 2.0 2.5 2.5Total -2.5 -2.0 3.0 5.5Sources: Statistics Sweden, SEB

Residential construction will fall this year; in 2004 aweak upturn will begin. The level will, however, re-main historically low during the foreseeable future.Due to the financial squeeze for central and local gov-ernments, public sector fixed investments will leveloff.

Overall, we anticipate that capital spending will con-tinue to fall slightly this year. A modest recovery willbegin during 2004 and strengthen in 2005.

Households still optimisticIncome growth will slow sharply this year. This ismainly due to the belt-tightening effect of fiscal pol-icy. Rule changes in the taxation and benefit systemscontributed 2.5 per cent to income increases in 2002.In 2003-2005, the effect will instead be slightly nega-tive, primarily due to rising local income taxes. Lowerpay hikes will also contribute to the deceleration ofincome growth, while lower inflation will have theopposite effect.

Despite more subdued income growth, householdswill continue to increase their consumption at a decentpace, and at present there are no signs that this trend isabout to stop. The household confidence indicator hasrisen, and home prices have again begun climbingmore rapidly after a temporary slowdown during2002. Meanwhile credit expansion is continuing.

Behind this strong trend are a solid balance sheet anda historically low interest burden for households. Thelarge income increases of 2001 and 2002 were largelyutilised to bolster savings. For this reason, households

SwedenNordic Outlook – November 2003

21

can maintain consumption growth today by drawingdown their savings buffer. We thus believe that con-sumption growth will gradually accelerate from 1.3per cent in 2002 to 2½ per cent in 2005.

0302010099989796

14

12

10

8

6

4

2

0

-2

14

12

10

8

6

4

2

0

-2

Sources: Statistics Sweden, The Riksbank

Sweden: Property prices and lendingYear-on-year change

Lending to householdsProperty price index, permanent one-family homes

Economic situation of householdsYear-on-year percentage change

2002 2003 2004 2005Disposable income 4.7 1.6 1.5 1.6Consumption 1.3 2.0 2.3 2.5Household savings 8.2 7.4 6.5 5.8ratio, % of disposable incomeSources: Statistics Sweden, SEB

One downside risk in our forecast is that the weaklabour market may dampen household optimism.Poorer public sector finances may also lead to a fiscalpolicy that squeezes households to a greater degreethan we have assumed.

Labour market will remain weakUnemployment has climbed by nearly 1 percentagepoint in the course of 2003. Part of this upturn is dueto a decline in the number of people in government-financed employment training or temporary jobs (“la-bour market programmes”). Meanwhile, strong pro-ductivity growth indicates that companies areresponding to increased cost pressures with effi-ciency-raising measures, which in the short termlower the demand for labour.

In recent years, continued job creation in the publicsector has lowered unemployment. This trend is nowabout to end. Due to increasingly tight public financ-es, the number of jobs in the public sector will leveloff.

Labour marketYear-on-year change

2002 2003 2004 2005Hours worked -1.2 -1.1 0.0 0.3Labour productiv-ity

3.1 2.5 2.1 2.0

Unemployment, %of labour force

4.0 4.8 5.0 4.9

Employment, % ofworking-agepopulation

78.1 77.8 77.3 77.0

Sources: Statistics Sweden, SEB

03020100999897969594

6

4

2

0

-2

-4

-6

-8

-10

6

4

2

0

-2

-4

-6

-8

-10

Source: SCB

Sweden: EmploymentYear-on-year change, rolling 6-month average

ManufacturingPublic sector

There are many indications that the higher unem-ployment we have seen will persist during our fore-cast period. The labour market normally reacts tochanges in output after a time lag, so the effects ofrecent years of economic slowdown have not yetworked their way through. The GDP growth we an-ticipate in the near future will not be sufficient toimprove the labour market situation either.

Smooth wage roundThe 2004 wage round has now begun, but the firstnegotiating proposals do not usually provide muchguidance as to how the final collective agreementswill look. These agreements will probably be con-cluded during the first quarter of 2004.

▪ We do not believe that employer organisationsand unions will have a particularly hard timereaching a settlement on average pay hike levels,since nowadays the Riksbank’s inflation target issuch an established point of departure for the ne-gotiations.

SwedenNordic Outlook – November 2003

22