nomura - india strategy - the rural juggernaut rolls on

TRANSCRIPT

27 January 2011 Nomura 1

Any authors named on this report are research analysts unless otherwise indicated. See the important disclosures and analyst certifications on pages 27 to 31.

Strategy | I N D I A

Prabhat Awasthi +91 22 4037 4180 [email protected]

Nipun Prem +91 22 4037 5030 [email protected]

Action The rural bandwagon continues to roll. Supportive government policies, greatly

improved farm economics, improved availability of financing and benevolent wealth effects of sharp land price appreciation are driving significant changes in rural consumption habits and lifestyle. We remain bullish on the rural consumption story.

Anchor themes The rural story conforms to our bullish view on domestic consumption. It is also, in part, responsible for elevated aggregate demand, which in a supply-constrained economy is causing high inflation; a key reason for our cautious stance on the market, in addition to slowing growth momentum and a sluggish investment cycle.

How to play the rural theme? Buy mechanisation, buy low penetration and buy aspiration. The following stocks screen well on these criteria — Mahindra, Bajaj Auto, ITC, Dish TV, and Jain Irrigation.

The rural juggernaut rolls on Straight from the heartland

Seven analysts from our research team travelled to rural regions across the country to better understand the rural story. They spoke to farmers, shop keepers, auto dealers, farm labourers and general rural folk. What follows are key takeaways from the sampled regions. We have tried to be as true as we could to the sentiment expressed by those we interviewed and have not tried to overlay them with our personal views or couch them in economic statistics.

The rural economy — rising incomes, growing consumerism

Rural India is reaping the benefits of supportive government policies and favourable farm economics. Crop prices have multiplied and benevolent wealth effects of sharply rising land prices are underpinning rural incomes and propensity to consume. Positive spill-over effects of strong economy-wide growth are providing more opportunities to trade. Higher incomes are providing the seed capital to diversify into ancillary farming and other non-farm sources of income.

With income and wealth effects both in the bag, rural consumption is on a roll. We reckon that rural consumption is still in early stages of its evolution. Even as incomes have increased dramatically, the propensity to spend will change only slowly as the multiplier works its way over time.

Buy mechanisation, low-penetration and aspiration

The rural story is not easy to play. Rural India thus far has had only a marginal share in the consumption of higher-end goods. Except for FMCG, telecom and a few auto companies, the focus of corporate India has only recently shifted to the rural story. Dearer and scarcer farm labour should lead to increasing substitution of man with machine. Rising consumerism is fast underpinning rural consumption.

Top rural plays

We recommend the following stocks in our coverage universe as top rural plays — Mahindra & Mahindra, Bajaj Auto, Dish TV, ITC and Jain Irrigation.

TOP DOWN

N O M U R A F I N A N C I A L A D V I S O R Y A N D S E C U R I T I E S ( I N D I A ) P R I V A T E L I M I T E D

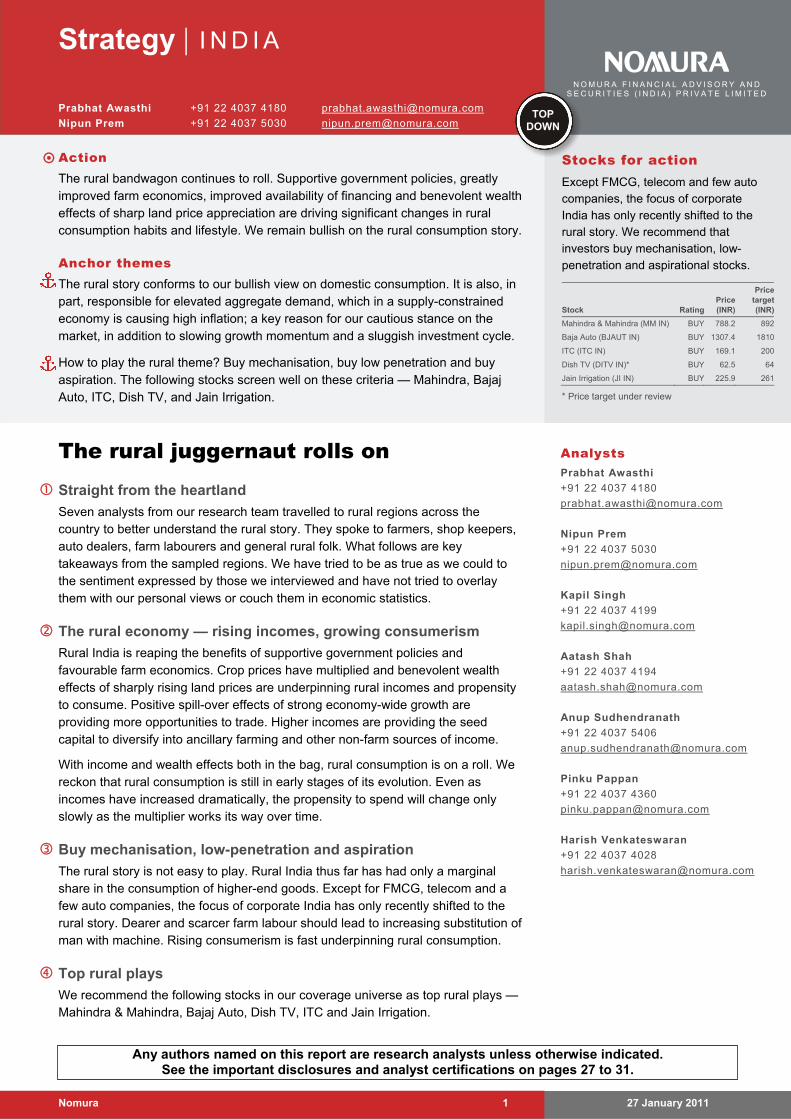

Stocks for action Except FMCG, telecom and few auto companies, the focus of corporate India has only recently shifted to the rural story. We recommend that investors buy mechanisation, low-penetration and aspirational stocks.

Stock RatingPrice (INR)

Price target (INR)

Mahindra & Mahindra (MM IN) BUY 788.2 892

Baja Auto (BJAUT IN) BUY 1307.4 1810

ITC (ITC IN) BUY 169.1 200

Dish TV (DITV IN)* BUY 62.5 64

Jain Irrigation (JI IN) BUY 225.9 261

* Price target under review

Analysts Prabhat Awasthi

+91 22 4037 4180

Nipun Prem

+91 22 4037 5030

Kapil Singh

+91 22 4037 4199

Aatash Shah

+91 22 4037 4194

Anup Sudhendranath

+91 22 4037 5406

Pinku Pappan

+91 22 4037 4360

Harish Venkateswaran

+91 22 4037 4028

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 2

Contents

The rural story continues to unfold 3 Incomes have multiplied, consumerism is fast catching on 3 How to play the rural theme? Buy mechanisation, buy low-penetration and buy aspiration 4 Top rural plays 5

The rural juggernaut 7 I. The regions visited: An overview 7 II. Farming economics 10 III. Impact of government schemes 15 IV. Availability of finance 17 V. Change in consumption habits 20 VI. Impact of information 23 VII. Other feedback from conversations with farmers 24 Valuation methodology and investment risks 26

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 3

Conclusions & stock picks

The rural story continues to unfold The rural bandwagon continues to roll: The great Indian rural story is on a roll. It is not new and has been much talked about. We think it has much longer to go. We believe that the structural changes brought about in India’s rural economy are massive and have significant investment implications.

A first-hand glimpse: The purpose of this report is not to contextualise the rural growth story in a macroeconomic framework. It has been done before, and often. Rather, we wanted to get a first-hand sense of the forces of growth chiselling away at the economic landscape in rural India and shaping the future trajectory of growth for the wider economy.

Seven analysts from our research team travelled to rural regions across the country to better understand the rural story. They spoke to farmers, shop keepers, auto dealers, farm labourers and general rural folk. What follows are key takeaways from the sampled regions. We have tried to be as true as we could to the sentiment expressed by the people we interviewed and have not tried to overlay them with our personal views or couch them in economic statistics.

Incomes have multiplied, consumerism is fast catching on Universal rise in incomes: The over-arching feedback from our field trips was the impressive rise in rural incomes across the country. Incomes have risen anywhere between 2-4x times (even higher in some cases) over the past four years. Several factors are at play here.

1. Higher crop prices: Crop prices are up on account of government-administered minimum support prices, rising prices of cash crops and export items (such as grapes) and ever rising demand for food in a high-growth economy. While input costs have also risen, the increase in incomes has been much stronger.

2. Government schemes: Government schemes have affected rural incomes in two ways. First, the national rural employment guarantee (NREGA) scheme has increased the bargaining power of marginal farmers and landless labourers leading to a surge in wages and a shortage of rural labour in general. Second, the general push by the government in rural infrastructure has resulted in better roads, wider connectivity and greater availability of electricity. We note that the primary driver of rural prosperity is increasing farm product prices, and NREGA and government spending have been icing on the cake.

3. Availability of financing: Availability of financing has improved, partly because of the push by the government and partly because of better penetration of banks and other rural financing companies. Competition among NBFCs is heating up and lending terms and conditions have become easier for farmers.

4. Wealth effect from rising land prices: As owners of a highly inelastic factor of production like land, farmers have benefited immensely from benevolent wealth effects of sharp recent increases in land prices across the country. Land (and gold) is the preferred instrument of savings for most in rural India. Land prices get a further leg up as farmers plough their savings back into land. Also, the inflow of remittances from Indians living abroad is chasing land prices higher, especially in Punjab and southern states of the country.

5. Spill-over effects of nationwide economic growth: Positive externalities from years of strong nation-wide growth are paying off for rural India. Better and more roads have increased trade with neighbouring villages, cities and states. Widening reach of media, cable TV and mobile phones has spurred aspirational demand and consumerism while mitigating business risk through timely dissemination of information (about crop prices and weather patterns, for example). Broad

Countryside starting to participate in the economic boom

This is boots-on-the-ground analysis …

… anecdotal — but people count as much as statistics

Rising rural incomes the key theme

Farmers like real wealth — land and gold

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 4

economic growth in the country and rising aggregate demand are providing fast-expanding markets for food products and putting upward pressure on farm output prices. Improving terms of trade for farmers imply rising incomes and consumption.

6. Farmers turning into entrepreneurs: Higher economic activity on an overall basis, rising incomes and benevolent wealth effects from the manifold increase in land prices are providing seed capital to supplement farm incomes and diversify into ancillary activities like dairy, retail, infrastructure (supplying sand, for example) and transportation (renting tippers and tractors, for example). Rising incomes mean that consumption in rural India is moving up the value chain, providing fresh opportunities for new business expansion (eg, retailing).

7. Susceptibility to droughts is falling: The other important takeaway from our rural trips is that monsoons are no longer a key driving force as farmers, in general, are significantly wealthier and their wealth in land significantly higher. Moreover, the shortage of labour created by government policies and a general tilting of terms of trade in the favour of the rural economy means that both landless labourers and land-owning farmers are less susceptible to the risk of a monsoon failures. We also note that non-agricultural activities are rising in rural areas and this is reducing the level of dependence on pure agriculture as the predominant source of income.

How to play the rural theme? Buy mechanisation, buy low-penetration and buy aspiration We think that the following are the key ways to benefit from rising rural affluence:

1. Buy mechanisation

A common theme that emerged across the regions we visited was the strength of wages paid to daily farm labourers. Rising costs of living and labour shortages have been mainly responsible for the sharp appreciation of the price of farm labour. We think that this combination of dearer and scarcer farm labour will lead to increasing substitution of man with machine and mechanisation will continue to rise at a quick pace in rural areas. Moreover, rising farming income and supplemental income from non-farming ancillary activities have imparted farmers with the ability to invest in the mechanisation of their farms. Consistent feedback from tractor dealers was that there has been a significant rise in cash sales over the past one year.

2. Buy low penetration

For all the progress and increase in wealth and incomes in the past few years, rural India still remains vastly underpenetrated. Rural India thus far has had only a marginal share in the consumption of higher-end goods. Except for FMCG, telecom and a few auto companies, the focus of corporate India has only recently shifted to the rural story.

3. Buy aspiration

Barring regional differences in tastes, preferences, and consumption habits, we found the following common threads that ran across the regions we visited: 1) an increasing willingness to experiment and explore new products; 2) need to keep up appearances and purchase goods thought of as status symbols; 3) rising consumerism and purchase of consumer durables; 4) amenability to up-trade, and; 5) rising brand awareness.

Rising incomes provide more opportunities

Richer farmers can invest in better equipment — tractor makers look good here

The countryside is also a wide-open market

And very broadly, a whole class of consumers is being created

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 5

Top rural plays 1. Mahindra & Mahindra (MM IN, BUY, CP INR788.2, PT INR892, Kapil Singh)

Tractors key beneficiaries of increased mechanization…: Mahindra & Mahindra’s tractor segment will be a key beneficiary of the labour shortages being created by the NREGA scheme, in our view. With nearly 40mn households being employed under the NREGA scheme, there is a shortage of rural labour being created.

…and higher labour costs: In addition, the government also plans to increase rural wages by 25% this year. This will lead to a sharp increase in cost of rural labour, leading to further mechanisation at farms.

Increasing non-farm usage of tractors: The rural development policies are also leading to alternative use of tractors in non farming activities. This is leading to increased viability of smaller farmers owing a tractor. The company is the leading tractor player in India with 40% market share in the tractor market and will be a big beneficiary from this, in our view. We value the company at INR 892/share based on Sum-of-the-Parts methodology.

2. Bajaj Auto (BJAUT IN, BUY, CP INR1307.4, PT INR1810, Kapil Singh)

Strong two-wheeler play: Bajaj Auto is the second-largest two wheeler company in India with 27% domestic market share. The company has had an urban-focused portfolio with 50% market share in the premium segment but only 20% in the executive segment which forms 65% of the market.

Increasing rural focus: The company is now targeting increasing dealerships by 25% to increase focus on the rural segment. They are also looking to have more products focused on the rural market. We are building in 15% growth in Bajaj Auto’s volumes in FY12F. We value the company at INR1,810, based on DCF-methodology.

3. ITC (ITC IN, BUY, CP INR169.1, PT INR200, Manish Jain / Anup Sudhendranath)

Top pick in FMCG space: In line with our broad theme of having a positive bias on aspiration and low-penetration ideas across rural India, we have ITC as one of the top picks in the FMCG space.

Up-trading to cigarettes: We believe that with farm incomes rising, rural consumers getting more affluent, and aspiration levels rising, one of the key beneficiaries would be ITC’s cigarette business. Remember, a large section of consumers still smoke local hand-rolled ‘bidis’ and we see this section of consumers increasingly moving away from bidis to cigarettes over the medium- to longer-term. ITC would be a key beneficiary of consumer up-trading in cigarettes.

Foods business under-penetrated: ITC’s foray into other FMCG businesses should also benefit from improving macro trends across rural India. Segments such as biscuits, salted snacks and the like are still largely under-penetrated and with the company offering these at price points which vastly improve affordability for the rural consumer, the food segment could also see strong traction over the short-to medium-term.

4. Dish TV (DITV IN, BUY, CP INR62.5, PT INR64, Jamil Ansari)

Biggest DTH player: Dish TV is the largest direct-to-home (DTH) player in India currently, with 9.4mn subscribers in the country’s 30mn strong DTH market. We believe growth in the DTH platform will continue unabated for the next few years and might actually accelerate in the medium-term, eventually making DTH the most dominant distribution system in the Indian television market.

Labour shortage also favours machines

Cigarettes an affordable luxury; this is an ‘aspirational’ good

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 6

Upside to rural subscriber base: In our opinion, the DTH subscriber base can potentially double in the next three years with bulk of the new subscribers coming from the rural / semi-urban regions. Currently almost 45% of Dish TV's subscriber base comes from rural India and this number can potentially go up to 60% in the next three years. As the first player in this industry, we believe Dish TV is best-placed to capitalise on the industry’s potential high-growth outlook. We have a BUY rating on the stock with a DCF-based PT of INR64.

5. Jain Irrigation (JI IN, BUY, CP INR225.9, TP INR261, Aatash Shah)

Increased policy focus on micro irrigation: With current high food inflation in India, the government will have to urgently look for solutions to increase farm yields while conserving water. Implementation of micro irrigation systems can help do this very effectively. We believe that there will be increased focus by the central government on micro-irrigation. As part of the national mission status for micro irrigation there already exists a significantly higher spending outlay on micro irrigation, expansion of the subsidy beyond horticulture and better systems to ensure quicker subsidy disbursements.

We think that the growth rate of the company’s MIS business can exceed 30% over the next four to five years, much longer than earlier envisaged. With the establishment of state level bodies over the next year to allocate central government funds rather than the current district level model, the subsidy disbursements should be faster and help reduce working capital requirements for Jain and improve cashflows.

Rising mechanisation: With increasing shortage of labour, farmers will have to look towards mechanising their irrigation practices with MIS as the best alternative available, in our view. The constraint in terms of high capital cost will get eased out as farmers’ incomes are increasing substantially while subsidies in the range of 50-70% are available from the government. In our estimate, MIS systems have a payback period of one-two years through increased yields, water and power saving and hence are a very cost effective investment.

Re-rating potential: We believe that the earnings CAGR of Jain irrigation will be 40% between FY11-13F and ROEs will improve from 20.5% in FY11F to 25.3% in FY12F (provided there is no equity raising). In such a situation, we believe, the earnings multiple for the stock can re-rate. Since April 2006, the stock has traded at an average multiple of 22x one year rolling forward earnings. We apply a multiple of 20x to our one-year rolling forward EPS to arrive at our 12-month price target of INR261/share.

Mechanisation pays for itself quite quickly

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 7

Drilling down

The rural juggernaut I. The regions visited: An overview Seven analysts from our research team travelled to rural regions across the country to better understand the rural story. They spoke to farmers, shop keepers, dealers, farm labourers and general rural folk. What follows are key takeaways from the sampled regions.

Exhibit 1. Rural regions visited by our analysts

Navsari, Gujarat (Aatash Shah)

Rai Bareilly/Barabanki, UP(Kapil Singh)

Amritsar, Punjab (Nipun Prem)

Barasat, West Bengal (Anup Sudhendranath)

Maddur, Karnataka (Anup Sudhendranath)

Cochin, Kerala (Pinku Pappan)

Nagercoil, Kerala (Harish Venkateswaran)

Nasik, Maharashtra (Prabhat Awasthi)

Source: Nomura research

1. Amritsar, Punjab, Northern India (Nipun Prem)

Punjab is a key agricultural state of India and led the Green Revolution in the country in the 1960s. Paddy is the main summer crop and wheat is the main winter crop in the region visited. Farmers augment their incomes following the paddy harvest by planting vegetables with short two-month life-cycles such as peas, radish, cauliflower and carrots. Even though Punjab is better irrigated compared to other states in India, tube-wells are an important source of water for most farmers. Average land holdings in the region are about 5-7 acres, though much higher for richer farmers. Farmers have benefited from higher economic activity and growth which have provided them with opportunities to supplement their incomes with ancillary activities like dairy, supplying sand (spot selling of sand is used in construction, which has seen significant growth in rural areas) and transportation.

Another important factor driving the rural theme in the region is the wealth effect from rising land prices and remittances from abroad. Agricultural surpluses have

Our analysts have not been content to merely parse data

Farmers have been able to diversify income

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 8

also been used to consolidate land holdings rather that being invested in other investment avenues like equities. Bank deposits are mainly used for working capital needs. Status is a function of size of land holdings.

2. Rai Bareilly and Barabanki, Uttar Pradesh, North central India (Kapil Singh)

The principal crops in the area are rice, wheat, pulses and cash crops like sugarcane, vegetables and Eucalyptus. Over the past few years farmers have reaped rich dividends from increased minimum support prices (MSPs) for crops. They have also benefited from improved road connectivity to Lucknow city, which has led to sharp appreciation in land prices. With incomes growing from farming as well as non-farming activities, the people we met indicated to prospects of another prosperous year.

3. Barasat and Kolkata, West Bengal, Eastern India (Anup Sudhendranath)

Paddy, vegetables, jute and potato are the main crops grown close to the area. Typically farmers are able to grow paddy crops twice a year and use some part of the land to grow vegetables. Other crops in the area include jute and potatoes. Land is fertile and crop has been good for the most part of the last three years.

Use of farm equipment seems limited, as paddy crop has traditionally relied on rain water. As far as sprinklers are concerned, most farmers seemed to be using equipment from local manufacturers. Average size of land holding is about three-four acres in the area. There are only a few farmers who own eight-10 acres or more, and they are leasing out the land to smaller farmers. Size of the land holdings has been getting smaller over the years due to its division among the family.

4. Navsari, Gujarat, Western India (Aatash Shah)

Navsari is located in southern Gujarat which has historically been a rich rural belt with good water availability and fertile soil along with proximity to large industrial centres. The main crops in the area are sugarcane, rice, mango, sapodilla and vegetables. Navsari has benefited due to its proximity to Surat and also from the fact that a large number of people have migrated abroad over the past several decades and are remitting their earnings. Farmers have benefited a lot from increased prices of sugarcane and also by appreciation in prices of their land holdings. The increasing farming income and/or the one-time increase in prosperity from sale of land has led to increased consumerism and a movement towards semi-urbanisation.

5. Nashik, Maharashtra, Western India (Prabhat Awasthi)

Nashik, a city about four hours drive from Mumbai is both an industrial and agricultural hub. The crops in the area include onions and tomatoes, grapes, cotton, rice and sugarcane. We met with two farmers (including a visit courtesy Jain irrigation), visited a tractor and UV+car dealer and spent time with people at Mahindra Finance branch at Nashik.

6. Maddur and Mandya, Karnataka, Southern India (Anup Sudhendranath)

Paddy and sugarcane are the main crops grown in the area. Typically, farmers are able to grow paddy crops twice a year and sugarcane once a year. Land is fertile and there is a constant source of water supply from the nearby KRS dam in Mysore. This meant that the drought last year did not effect the production much, as water supply from the dam was sufficient.

7. Cochin, Kerala, Southern India (Pinku Pappan)

Farming is not a major driver of the economy in Kerala, and has progressively declined over the past several years due to government apathy and labour issues. Paddy and banana are the major crops cultivated, although not on a very large

Rising MSPs, greater availability of finance and improved infrastructure and information

Remittances from abroad are fuelling land price appreciation

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 9

scale. Spices and tea cultivation happens on a larger scale, albeit with corporate participation.

Overall incomes are increasing, which is visible in consumption of discretionary items like cars and white goods. Kerala, because of its highly literate population, is a test-bed for new product testing and feedback. Brand awareness is quite high and people are willing to try out new products and brands.

8. Mathias Nagar, Nagercoil, Trivandrum, Southern India (Harish Venkateswaran)

The economy is primarily agrarian with principal crops being rubber, plantain, paddy and coconut. Most families have some land holding, big or small. We met farmers, car dealers, vehicle financiers in the region. Based on interactions with locals we inferred that standards of living and disposable incomes have increased significantly in the last two-three years. Literacy levels have also gone much higher in the last few years, with several educational institutions sprouting up in the area. People in the area were optimistic of further growth in the economy in the coming years.

High literacy levels can cause further labour shortages

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 10

II. Farming economics 1. Cochin, Kerala, Southern India

Higher output prices: Farming has become profitable more because of price increase in PDS (Public Distribution System) and less because of improvements in output yields. Rains have been good recently and have contributed to increased output.

Higher land prices and shortages: However, many farmers are surrendering land to real estate companies due to the sharp run-up in land prices and non-availability of labour. Kerala’s high population density has resulted in scarcity of land, so much so that the state government has restricted farm land from being used for other non-agricultural purposes. Famers complain that incentives for farming have come down as farm workers have emigrated in search of stable salaried jobs. Moreover, highly literacy levels in the state have added to farm labour shortages.

Labour shortages: The general feedback was that shortage of labour is the biggest problem for farming today. The younger generation and children of farmers are not interested in farming. The shortage of farm labour has in turn resulted in the existing workforce demanding higher wages. Many of them want fixed pay instead of daily wages. Cheaper labour from north India is now substituting local labour. However, as the labour required for farms is skilled in nature, it is still difficult to replace.

2. Maddur and Mandya, Karnataka, Southern India

Income from crops: The paddy crop in the area sells for about INR1500 per quintal on average with the range being INR1200 to INR1800. One acre produces about 25 quintals of paddy and farmers are able to produce two crops in a year which comes to about 50 quintals per acre. The cost of production including the seeds, fertilizers, etc is about INR20,000 per acre, which means profit of some INR50,000 (US$1,094) per acre. Most farmers have about four acres of land, which means profit of INR200,000 per year.

Land holdings: Average size of land holding is about three-four acres in the area. There are only a few farmers who own eight-10 acres or more, and they are leasing out land to smaller farmers. Size of the land holdings has been getting smaller over the years due to its division among the family.

3. Rai Bareilly and Barabanki, Uttar Pradesh, North central India

Farm incomes: Farming land yields returns of 10-12% on average. One acre of farming land in the area typically costs INR500,000-INR600,000. Typical income per acre is INR78,000 and the expenses are around INR18,000/acre, thus yielding a net income of INR60,000 per acre per year.

Higher crop and land prices: Sugarcane price has gone up from INR40-50 per quintal in 2006 to INR200 per quintal in 2010. The price of land has gone up much faster for land close to roads that are well connected to the city.

Agricultural implements: Agricultural implements such as cultivators and Rotavators can be bought for INR12,000 to INR85,000. Most do not buy these implements from dealers as company products are expensive compared to those in the unorganised segment. Dealers face quality issues with customers if they sell unorganised-segment implements, which is the reason that they do not stock them.

Increasing tractor usage: People now prefer to use tractors as bullocks are difficult to maintain and the time available to till the land this way can be wanting. Tractors have become much more viable for smaller farmers now. A tractor can be rented at INR200/hr for some 10 hours per day. It costs INR80/hr to run the tractor. Other expenses including drivers’ salary and food cost of some INR200/day

Higher crop prices, labour shortages and rising land prices

Farming economics has vastly improved

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 11

yielding a profit of nearly 1,000/day. Thus if the tractor can be rented for 20 days in a month, a farmer can earn 10,000 per month even after paying EMI of some INR10,000 per month. Tractor usage in non-farm applications is as high as 50% compared to 20% two years back.

Irrigation: Irrigation is done largely by canals and rain. Most farmers are not aware of micro irrigation. They buy pipes by weight and lay them in the fields. Farmers are not aware of any brands of urea or pesticide. They use whatever is available.

4. Mathias Nagar, Nagercoil, Trivandrum, Kerala, Southern India

Significant rise in crop prices: The principal crops in the region are rubber, plantain, paddy and coconut. Farming economics have considerably improved in the last couple of years. This is on account of a significant increase in crop prices in recent years. Prices of key crops have increased two to three times in the past two years, according to local farmers. For example, rubber prices are now at INR180/kg vs around INR60/kg at the peak of the economic slowdown. According to farmers, the breakeven price of rubber in the region is close to INR60/kg. Hence the disposable incomes of farmers have increased considerably. Revenue from one acre is around INR35,000/month. Cost of maintenance is around INR10,000/month leaving a profit of close to INR20,000-25,000 per acre per month.

Fishermen are also seeing increasing prosperity. They are earning handsomely as the price of catch has also gone up substantially in recent years.

Land price appreciation: The increase in crop prices has translated into a rise in land prices as well. The demand for agricultural land has far outstripped the supply. For example, one acre of rubber plantation costs around INR2mn now vs around INR1mn, two years back.

Labour shortages: Inadequate availability of labour is the key issue in farming. There are not enough labour hands to help in farming. Hence daily wages for the labourers has shot up to INR300/day from about INR100/day two-three years ago. According to farmers, labour shortage is mainly due to people moving to urban areas or abroad for employment.

5. Navsari, Gujarat, Western India

Farm incomes: Sugarcane price has gone up from INR900 per tonne in 2006 to INR2,500 per tonne in 2010. The yield is about 100 tonnes/acre on average resulting in average revenue of INR250,000/acre from one cycle of sugarcane. The investment for the farmer is about INR90,000/acre for sugarcane and hence his profits would be in the region of INR160,000/acre from one cycle of sugarcane. The average land holding in Navsari is close to four acres per farmer though the farmers we met had higher land holdings of eight acres and 20 acres. Farming costs are moving up by 10% every year.

Higher land prices: Price of land closer to the highway and the town is about INR10-15mn/acre while price of land in the interiors ranges from INR2.5-5mn/acre. Land prices have moved up about 3-4x over the past five years.

The yield on buying land today and growing sugarcane on it, in the best case would be about 6%. Farmers, though, did not seem very eager to sell their land and did so only because they either needed the cash or did not have descendants interested in farming. Some farmers are selling their land closer to town and highway and buying larger land parcels in the interior while saving some money. Some farmers are turning entrepreneurs with the money they collect from the land sale.

Labour shortages and mechanization: Farm labour is in short supply though the reason is diversion towards industries rather than NREGA. Labour costs about

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 12

INR50/day, up from INR30/day two-three years back but the labourers only work 4-5 hours in the day. This has resulted in increased mechanisation in the form of tractor and harvester usage along with drip irrigation in spite of enough water availability. People now prefer to use tractors as bullocks are difficult to maintain and can not plough very quickly, which is sometimes needed.

Non-agricultural use of tractors: Tractors are being bought not just for usage in farming but also to rent out for haulage purposes. There are a number of quarries in the area which require these tractors to transport the stone while infrastructure projects in the region also require these tractors. A farmer renting out his tractor for such purposes stands to make INR15,000/month after costs, making a tractor purchase much more viable. At the same time, there have been issues in terms of the farmers getting their payments on time. Some 60% of farmers are using tractors currently.

Irrigation: Irrigation is done by canal and ground water. There is high awareness of drip irrigation but not widespread usage given enough water availability.

6. Amritsar, Punjab, Northern India

Crops and harvest cycle: The summer crop (paddy) is sown in June, a little before the onset of the monsoons, and harvested in October. The winter crop (wheat) is sown in the beginning of November and harvested in April. The farmers augment their incomes following the paddy harvest by planting vegetables with short two-month life-cycles such as peas, radish, cauliflower and carrots. The government has disallowed sowing of paddy in the two months following the wheat harvest in April because of concerns about declining water table levels.

Crop economics: Based on feedback from a paddy farmer, the following are the expenses from sowing to harvesting associated with one acre of normal paddy:

Exhibit 2. Income from one acre of paddy crop

Amount (INR)

Diesel: 30 litres @ INR38/litre INR1140

Urea: 3 bags @ INR285/bag INR855

Fertilizer INR500

Insecticide INR700

Growth hormone INR165

Labour (during sowing) INR1200

Harvesting (using combines) INR1000

Total expenses INR5,180

Total income INR19,440

Source: Nomura research

Based on feedback from a wheat farmer, the following are the expenses from sowing to harvesting associated with one acre of wheat:

Exhibit 3. Income from one acre of wheat crop

Amount (INR)

Diesel: 20 litres @ INR38/litre INR760

Seeds INR400

Fertilizer INR500

Insecticide INR600

Growth hormone INR500

Labour (fertilizer) INR400

Harvesting (using combines) INR1200

Total expenses INR4,360

Total output = 15-20 quintals per acre @ INR1100/quintal INR16,500-22,000

Total income INR15,000 avg

Source: Nomura research

Tractors are also used to truck heavy materials

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 13

The average land holding per farmer depends upon the region, but based on our discussions we can assume an average holding of 5-7 acres. So pure farming income for a typical farmer from the two crops (kharif and rabi) would be about INR210,000 (US$4,595) per year, not including income from growing vegetables and other supplemental non-farm income

Incomes have multiplied in pace with revenue and costs, providing seed capital for expansion into non-agri activities: The general feedback from farmers was that although crop prices have risen recently on the back of higher MSPs (minimum support prices, set by the government), margins have remained the same because input cost (labour, seeds, fertilizer, etc), inflation has kept up with output prices. However, this means that income from farming activity has increased at the same rate as output prices and input costs. This increase in incomes has provided farmers with seed capital to expand into supplemental farm activities like dairy and non-farm activities like construction and transportation.

Higher labour costs, but little impact from NREGA: The general feedback on labour costs was that labour rates have risen commensurately with the increase in cost of living. Most farmers we spoke to were not aware of NREGA. We suspect that this is because NREGA wage rates are not binding at current levels as the daily wage rates for farm labour exceeds NREGA wages, with temporary labour wages at INR200/day. Temporary migrant labour (mostly from UP and Bihar) and local (Punjab) daily wage rates have converged recently to INR200 (US$4.37)/day from INR80/day five years ago, a 20% CAGR increase. Permanent labour salaries have increased from INR10,000-15,000 five years ago to INR20,000-25,000 now, about 10-15% CAGR. Development taking place in UP and Bihar along with NREGA is putting pressure on availability of migrant labour, although the farmers we spoke to did not feel that availability was a serious issue.

Land prices have shot up: Remittances from NRIs (Non-resident Indians) abroad and increasing pace of residential and commercial construction activity in the region are putting significant upward pressure on land prices. A wealthy farmer —land holdings of 45 acres, in addition to running a transportation business on the side — we spoke to informed us that his land is attracting a large premium amount of INR15mn/acre. His own threshold price should he sell was INR20mn/acre. This compares with a price of INR0.5-0.7mn/acre about five years ago. The enormous appreciation in the price of this particular tract of land, we were told, was because of a residential colony coming up adjacently. Also, large inflows of NRI money are also fuelling the runaway appreciation of land holdings in the region and state.

Irrigation and drought: Even though Punjab is better irrigated compared to other states in India, tube-wells are the main source of water for most farmers (80% tube-wells, 20% canals) in the region. During drought, canals dry up because water is rationed from upstream. Also, hydro power is a main source of power in the state and electricity generation suffers in a rain-deficit year, impeding the use of pump sets and forcing farmers to use diesel-based generators to draw water. This raises expenses in a year in which revenue has already been hit because of low agricultural yield. The farmers we spoke to were not aware of drip irrigation.

7. Nashik, Maharashtra, Western India

Farm incomes have multiplied: We met with two farmers and a tractor dealer. The general feedback was that farm incomes have accelerated significantly over the past three-four years. Farmers who have succeeded in tapping export markets end up making as much as INR0.4mn/acre (realisation per acre of approximately INR0.6mn and costs of approximately INR0.2mn/acre). In the domestic markets, returns are stacked up according to the risks associated with a crop. Grapes fetch a profit of INR0.2mn/acre, vegetables INR0.15mn/acre and sugarcane INR0.1mn/acre. All these numbers have possibly more than tripled over the past four-five years.

The more money in farming, the more room to branch out

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 14

So have land prices: Land prices are up 4x in the past three-four years in general and have shot up even more closer to the city, led primarily by the real estate sector. Land prices have largely followed improved farm economics and therefore may not come down. Closer to the city, farmers sell their land, reap a profit and move inwards to buy land at cheaper prices. The combined impact is a massive wealth effect through major profit increase and quadrupling of land prices.

Machine trumps beast: An interesting conversation with a tractor dealer was on the economics of owning a tractor vs bullocks. The table below shows this in some detail:

Exhibit 4. Tractor vs Bullock

Comparison point Tractor Bullock cart

Capital cost Rs210,000 for a 15 HP tractor Rs75,000-90,000

Running cost Rs.400/8 hr Rs300/day

Maintenance Rs650/250 hrs Replacement after useful life

Productivity 2.5 acres/8 hrs 0.25 acres/8 hr

Source: Nomura research

Clearly, considering the much higher productivity of tractors, they make better economic sense. It was also pointed out that bullocks need feeding even if they are not being used. Tractors are also used 30-40% of the time in haulage work which is available more frequently on account of public works. While tractors vs bullocks looks like no contest, the buying decision does depend on capital availability and land holdings. Given that cashflows have seen a significant jump, the capital cost bridge has become easy to cross. According to the tractor dealer, 35% of tractors are being bought for cash against 10% earlier.

Labour shortages: The other interesting commentary was about labour shortages. Grapes, which require manual labour due to the nature of work in the crop, face labour shortage more than other crops do. Typically, labour is required for five months in the whole year (for two crops). According to the farmer we met, he pays INR50,000/labourer for these five months to ensure availability of labour. On a per-month basis this works out to INR10,000/month, significantly higher than NREGA wages and comparable (even higher) than the cost of manual labour in urban areas.

Exhibit 5. Combine at work near Amritsar, Punjab

Source: Nomura research

Exhibit 6. Tractors hauling sand in Amritsar, Punjab

Source: Nomura research

Unlike bullocks, tractors can be a cash cow

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 15

III. Impact of government schemes 1. Cochin, Kerala, Southern India

No NREGA impact: We found no impact from NREGA as the daily labour rate for farming is much higher than NREGA wages. NREGA is seen as more of a side income by labourers and is mainly for low skilled jobs.

Subsidies and crop loans: Subsidies on farm equipment like tractors are available, though it takes time and is a lengthy process. However, most famers opt for subsidies.

Most farmers have only small fields so they are disadvantaged when it comes to crop loans which are limited to the value of land. Most of the time, farmers do not avail themselves of these loans due to the lengthy process involved and the meagre loans they can tap.

Farm waivers: There has been negligible impact from farm waivers. Most farmers who could get their loans waived had already paid back most of their loans and were hence ineligible. Farm loan waivers have mostly benefitted only the large scale farmers with political connections.

2. Rai Bareilly and Barabanki, Uttar Pradesh, North central India

NREGA and labour shortages: Government schemes like NREGA have created a shortage of farm labour. Farm labour that was available for as low as INR60/day two years earlier now costs at least INR100/day; labour is not available in many cases even at those prices. Labour can be as expensive as INR150/day in Rai Bareilly to INR180/day in Lucknow.

MSP increases: The hikes in MSPs (Minimum Support Price) have had a big impact on incomes. Farmers especially benefited from high sugarcane prices last year, which sold for as much as INR200/tonne in FY10.

Subsidy on tractors: There is a subsidy on buying tractors for INR50,000 from UP Agro. But the process is difficult and people are not aware of the subsidy. It also takes six months to get approval and hence is not very prevalent.

Public works: Rural infrastructure development activity has led to job creation and opportunity for smaller farmers to rent out their tractors.

3. Mathias Nagar, Nagercoil, Trivandrum, Kerala, Southern India

Government support for farmers is basically in the form of subsidies for seeds, fertilizers, pesticides and the like. The place receives abundant rainfall as it gets monsoons which hit both Kerala and Tamil Nadu. The place has not been affected by droughts in recent years.

Limited NREGA impact: NREGA has not had a big effect on labour availability or wages. This is because the wages under the scheme are only around INR 100/day. Any healthy labourer can get 3-4x that and hence would not opt for the scheme. So only the older labourers who have difficulty working have signed up for this.

4. Navsari, Gujarat, Western India

No NREGA impact: Neither the farmers nor others we spoke to attributed any impact to their work due to NREGA. According to the farmers, NREGA has not led to any labour shortage.

MSP increases: There are no MSPs for the crops grown here except for rice and the farmers directly negotiate the price with the sugar mills or in the markets.

Subsidy on tractors: There is a subsidy of INR45,000 for buying tractors from the government on tractors below 35HP but these tractors are not large sellers. The approval process is time-consuming.

NREGA wage rates are not always binding

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 16

Kisan credit card: Kisan (farmer) credit cards have been given to few farmers which has helped them purchase inputs through short-term credit.

5. Mathias Nagar, Nagercoil, Trivandrum, Kerala, Southern India

Farm loan waivers: The government extends farm loan waivers to farmers but the need for it was minimal. Some farmers got small amounts of loans waived off under this category. According to the farmers, they were in a position to easily repay the amounts.

6. Amritsar, Punjab, Northern India

Farm loan waiver: The farmer we spoke to had INR25,000 worth of loans waived as part of the farm loan waiver scheme of the government.

Government schemes: NBFCs do not offer government incentive schemes. The general feedback was that PSU banks take much longer in approving loans. They pledge land when giving out loans to farmers. In contrast, NBFCs are much quicker; they do not pledge land but require proof of residence in the form of ration card, voter card, driver’s license, electricity bill or passport.

Minimal NREGA impact: Most farmers we spoke to were not aware of NREGA; others said it was not an issue. We suspect that this is because NREGA wage rates are not binding at current levels as the daily wage rates for farm labour exceeds NREGA wages, with temporary labour wages at about INR200/day.

7. Nashik, Maharashtra, Western India

Higher procurement prices: Clearly, rising procurement prices have been the primary drivers of the rural economy in the region. Additionally, rural roads and other programmes under NREGA etc, have raised the level of work available in rural areas.

Tractor sales have received a boost: Tractor sales are a key beneficiary of benevolent government schemes as: 1) there is a benefit of using tractors in construction works, and; 2) labour shortages created on account of the government programmes also drive up tractor usage. The government has also pushed higher the usage of internet and has schemes for sending SMSs on “mandi” prices on a monthly subscription basis. Easy loan availability is another by-product of government policies.

Exhibit 7. Unorganised sand mining in Mandia, Karnataka

Source: Nomura research

Exhibit 8. Dish TV antenna on tiled roof in Maddur, Karnataka

Source: Nomura research

Rural public works can add to labour shortages

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 17

IV. Availability of finance 1. Cochin, Kerala, Southern India

Loans – NBFCs preferred to PSU banks: For housing loans, the general feedback here was that people in rural areas lean on NBFCs as the lack of regular income and documentation make them ineligible for state bank loans. Also the speedy processing attracts several customers towards NBFCs. In the rural housing loans segment, Dewan Housing Finance limited is competition for Mahindra Finance. For auto financing, other NBFCs like Muthoot Group is biggest competition for Mahindra Finance.

Tractor sales have increased about 30% y-y in 2010, although dealers say they expect it to come down this year with the change in government. PDS price increase and thrust by current government on farming has led to the surge in tractor sales.

Cash purchases as percentage of sales: Auto dealers say that about 15-20% of sales are paid out fully in cash. They also add that many customers opt for auto loans, even though they have the resources to pay cash in full, in order to avoid income tax scrutiny. For tractors sales, the percentage of full cash sales is negligible.

2. Maddur and Mandya, Karnataka, Southern India

Loans – NBFCs preferred to PSU banks: Mahindra Finance units in Bangalore and Mysore put together do about 1000-1100 disbursements per month – Bangalore 800, Mysore (includes Maddur and Mandya) 200 and Kolar (northern Bangalore) 100. In Mysore, this relates mainly to tractors, but in Bangalore they also do passenger car financing and have tie ups with Hyundai, Maruti, CAT, JCB etc. Of the overall portfolio, tractors are about 40%, 3 wheelers and pickups are about 30%, small cars about 25% and 2 wheelers about 5%.

The typical approval time for loans is about 2-3 days vs banks which take about 3-4 weeks or so. Feedback received elsewhere seemed to suggest that this is one of the main reasons that customers prefer NBFCs to banks.

Competition is rising: Shriram Finance is a well established player, but competition from Kotak and L&T finance has been rising over the past two years.

Availability not an issue: Tractor availability did not appear to be a problem. Feedback suggested waiting time of 2-3 weeks.

3. Barasat and Kolkata, West Bengal, Eastern India

NBFCs preferred to PSU banks: Mahindra Finance units at Barasat do about 45-50 disbursements per month. This relates mainly to commercial vehicles and some passenger vehicles as well. The typical approval time is about 2-3 days vs. banks which take about 3-4 weeks or so. Feedback received elsewhere seemed to suggest, this is one of the reason that customers go to NBFCs vs. banks. About 30% of all Mahindra vehicles sold in the area are financed by Mahindra Finance.

Competition is heating up: Shriram Finance is a well established player, but competition from Kotak and L&T finance has been increasing. L&T Finance seems to be building a sizeable presence in the area with focus on growing the loan book.

Availability is limited by tight supply constraints: Feedback suggested that availability of vehicles is a significant issue across the three dealers in the region. Most popular models where demand has consistently been strong over the last 6 months are Bolero, Scorpio, Xylo and Logan. Maximo and pickup trucks are the popular commercial vehicles. Feedback suggested that demand for these vehicles put together was about 20-25 units per month, but severe supply constraints have meant that delivery is limited to only 6-7 per month. This situation has been there for 3 months now and dealers seemed to be concerned that this has not corrected

Auto sales are hitting supply constraints

NBFCs are often preferred to PSU banks because of quicker loan approvals, lesser documentation and convenience

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 18

itself. Dealers sounded confident of selling at least 20 a month if availability were not an issue.

4. Rai Bareilly and Barabanki, Uttar Pradesh, North central India

Cash sales rising: People in rural areas in general are now cash rich and require fewer loans to finance purchases of vehicles. Hence, the proportion of cash sales has gone up. Some dealers reported as much as 40% of auto sales without organised financing.

Loan rates: Banks are offering crop loans at 6-7%. The amount of loans given is INR20,000 per acre. Some times people divert these funds for other uses. The IRR on tractor loans is about 22% and that for cars ranges between 14-16%.

Revenue split: For loans disbursed by Mahindra Finance, tractors form 13% of revenue, UVs 50%, non-Mahindra autos 24%, CVs 11% and the rest 2%.

5. Mathias Nagar, Nagercoil, Trivandrum, Kerala, Southern India

Farmers prefer NBFCs to PSU banks: There is not much support from the government for farm-related financing. Farmers take loans from banks/NBFCs to finance farming equipment. There are society loans (government-backed) for agriculture at much lower rates but these are very difficult to obtain as they require a lot of documentation. On the other hand, NBFCs provide financing quickly with minimal documentation. They also have doorstep collection of payments every month which saves the farmers trouble of travelling to the branches to pay their EMIs. Hence, farmers prefer financing from NBFCs.

6. Navsari, Gujarat, Western India

Lack of proper documentation makes PSU bank finance difficult: Financing for the purchase of tractors, consumer goods and automobiles is available to farmers from both banks and NBFCs. Many farmers do not have appropriate documentation and hence banks are reluctant to lend to them whereas NBFCs take that risk. NBFCs IRRs are between 11-22% while banks lend at 12% and below.

Cash sales increasing: As per the Mahindra Finance branch head and the auto dealers we spoke to, people in Navsari no longer require financing to buy two wheelers. Some 20% of all vehicles sold in Navsari are through full equity. Loans are for a period of 5 years and lower.

Loan rates: Crop loans are available from banks and farmers who avail of these often use them for purposes other than farming. Crop loan amounts are INR20,000/acre at 6%. IRRs on tractor loans are 22% and for cars ranges between

14-16%. SBI, BoB and Kotak are the most aggressive lenders in this segment.

7. Amritsar, Punjab, Northern India

Based on our conversations with representatives of a leading NBFC we learnt the following:

Loan portfolio: The composition of their loan portfolio: 90% autos, 10% non-autos. Within autos: 40% cars, 20% tractors, 20% UVs, 20% CVs.

Loan rates: Interest rates (minimum loan amount INR50,000) across their product portfolio: Tractors: 24% floating, 16.6% flat; prime customers pay lower rate. Autos: rates have increased from the bottom; 16.5%; 14% (Special urban scheme); 10% (1 lakh loan for 1 year). The 0% interest rate scheme is offered only to a few select customers. The company earns servicing fees and subventions and hence has an incentive to push 0% interest rate loans onto customers who would otherwise have paid full cash down. No loans are given for farming activities (combines,

fertilizers, seeds, reapers etc). The company discourages financing of high-end luxury

cars because of low resale value.

Full cash down purchases are rising along with incomes

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 19

NBFC edge over PSU banks: PSU banks require much stricter documentation and also pledge land, something NBFCs don’t do. NBFCs don’t extend government schemes, something PSU banks do. NBFCs approve loans within 2 days, PSU banks take at least one month in disbursing the loan.

Competition getting hotter: The competitive landscape is getting tougher for NBFCs operating in the area and customers have good bargaining power. Mahindra Finance, Chola Mandalam, Magma, Sri Ram finance and HDFC are some of the leading NFBCs in the region.

Cash as % of sales: On an overall basis, 40% of sales are full cash payment, 60% is financed. Of the ones who get financed, company policy is an 85% LTV ratio.

Use of tractors: 75% for farming (ploughing), 25% non-farming (moving bricks, sand, cattle)

Waiting period at dealers’ end: Maruti Swift diesel/Dezire: 2 months, UV (Bolero SLX): 1 month, Tractors: no waiting, CVs: 1 month.

8. Nashik, Maharashtra, Western India

Government push and greater NBFC involvement: There has been a massive improvement in access to financing because of the following factors: 1) while the schemes for credit always existed, the push by the government has led to higher disbursement and easier access to credit, and; 2) private NBFCs have become very active in the last few years. Even though the cost of loans from private NBFCs tends to be higher, flexibility in terms of getting a loan is equally high.

Loan rates: We were told that tractor loans from private NBFCs come at rates between 14-20%, car loans at 14%, refinanced loan at 18-22%. Crop loans from PSU banks are available at 6%. These are available against land holdings with amount per acre being fixed. Farmers tend to use these loans for purposes other than farming at times given the cheap rate of financing.

Exhibit 9. Food Corporation of India grain storage facility near Amritsar, Punjab

Source: Nomura research

Exhibit 10. Drip irrigation facility in Nashik, Maharashtra

Source: Nomura research

NBFCs are more nimble

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 20

V. Change in consumption habits 1. Cochin, Kerala, Southern India

There has been an increase in discretionary spending in the state. Some of the visible trends in consumption behaviour are:

Increase in brand awareness: Customers are willing to try out new products before making the final decision. Also, novelty factor sometimes scores over practical factors, as evidenced by surge in sales of newer models of cars like Beat and Figo.

Up-trading: Many customers are opting to exchange 2-wheelers for cars. There is evidence of up-trading within cars too – exchange offers for a new car in lieu of an older one are much in demand.

Real estate: In terms of vehicles of investment, real estate is the most preferred asset class for most in the area.

2. Maddur and Mandya, Karnataka, Southern India

Thriftiness: Even though the region has many such farmers who have branched out into alternative businesses, the culture seems to be of not spending away the money too much. The typical farmer has been investing back into his own business for a long time and the only other place he invests his money is gold.

What do they spend on? Based on our conversations, the most popular FMCG brands seem to be Lux, Lifebouy, Wheel, Good day, Five Star, Johnson & Johnson baby products and Mysore sandalwood soap. The availability of these products is not a problem – there are a couple of local stores about 3kms away that sell these products. The farmers visit these stores on weekends. Most also

have a refrigerator at home with LG being the more popular brand among the 5 people

we asked. Reliance DTH has been running an offer in the area with a one year

subscription free, so most of the DTH subscribers here seemed to have a Reliance Big

TV connection. There were also many with a connection from the local cable service

provider who charges INR130 per month.

Other businesses contributing significantly: Both farmers we met said they made more money from their other businesses than they did from traditional farming. Both were committed to increasing their investments in these other businesses over the next few years. Government schemes have benefited, but many still seem to be averse to taking funding from the government as: 1) they are able to invest surplus cash themselves into the business, and; 2) there were issues with getting government funding approved.

3. Rai Bareilly and Barabanki, Uttar Pradesh, North central India

Wealth effects of land price appreciation: The manifold increase in land prices has brought significant new-found wealth in the region. Smaller landholders are

selling out as rich people invest in land, particularly land holdings that are well

connected to cities.

Consumerism on the rise: As people have become richer they are buying 4-wheelers as a status symbol. About 10% people buy products outright with cash. According to dealers, some people take loans to avoid suspicion of having too much cash with them. Retail stores like Hariyali and Vishal Megamart have set up

their shops and people are beginning to explore them. People are buying ever more

mobiles and consumer durables. However, electronic goods and Dish TV penetration is

still low as electricity availability is erratic.

Strong auto sales: Growth in categories such as tractors and automobiles has been in

excess of 30%. It is likely to continue at the same rate for many more months

according to dealers due to strong growth in incomes and good crop prospects from

this last year’s rains. New auto dealerships are also penetrating slowly and some very

Increasing willingness to experiment and explore new products

Farmers prefer land and gold as stores of value

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 21

rich people are experimenting with newer brands. By and large though they still prefer

tried and tested brands.

4. Mathias Nagar, Nagercoil, Trivandrum, Kerala, Southern India

Higher purchasing power driving auto and consumer goods sales: The increase in disposable incomes and purchasing power have resulted in a sharp increase in sales of automobiles, consumer durables etc. Car dealers have seen a 25-30% growth y-y in car sales. The target for coming months has been set a further 15-20% higher, which is in line with the peak monthly sales ever. Two-wheeler sales are also at an all-time high. All this has pushed up the waiting time for sought-after models. For example, waiting period for cars like Swift and Swift Dzire is 4-7 months, while for Wagon R it is close to 3 months at the local Maruti dealer.

Increasing cash purchases: Close to 30% of car purchases are outright with no financing. Even in cases where financing is involved, the loan is about 50% of the value. For commercial vehicles, financing is usually higher at about 80% of the value. People either take auto loans from banks/NBFCs or gold loans to finance their car purchases.

Strong brand awareness: While purchasing cars, people are very aware of brands and their relative standing in public perception. According to the vehicle dealers we met, people are buying cars more as a status symbol than anything else. People who come in to buy lower-end models like Wagon R are easily convinced to upgrade to higher-end models like Swift. Premium segment car sales have also increased substantially. Brands like Skoda, Mercedes-Benz have seen a significant uptick in sales in the last one year. Since there are no local dealers for such cars, people travel to close-by cities to buy such cars.

Land and gold preferred investment vehicles: In terms of investment, the preferred options are land and gold. Only a small part goes into bank deposits and other investments. Housing has picked up in the past 2-3 years. Most people own land and have a house right in the middle of their plot. Now with greater resources, they are expanding their present houses by building new floors, extensions etc.

5. Navsari, Gujarat, Western India

Rising consumerism: The increase in incomes from farming, remittances from NRIs and windfall gains from sale of land has increased consumerism a great deal as per the people interviewed. However, most purchases are need-based and not as status symbols. TV and mobile penetration is high and DTH was also quite

prevalent. A number of new auto dealerships have been set up in the last 2-3 years

and new brands which have set up their dealerships are Honda, Hyundai and GM.

Maruti and M&M have been the leaders to date. Mahindra Finance has financed the

same number of vehicles in 1H FY11 as it did in entire FY10 in Gujarat.

Preference for small-scale retail: Retail stores like Reliance have been set up in

the region but are not too popular with the local people who still prefer the mom-and-

pop shops because of credit availability. Also there is good amount of competition from

the local farmer co-operative shops.

6. Amritsar, Punjab, Northern India

Higher farm incomes providing seed capital to diversify into ancillary activities:

Farmers have benefitted from higher economic activity and growth which have provided them with opportunities to supplement their incomes with ancillary activities like dairy, supplying sand (spot selling of sand is used in construction, which has seen significant growth in rural areas) and transportation. This diversification into supplemental means of income has provided a big boost to consumerism in the region. A farmer we spoke to had diversified into Basmati rice (1121 variety), dairy (12 buffalos and 3 cows) and sand-supplying. He owned 5

Rising brand awareness and amenability to up-trade

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 22

acres of land and owned one tractor (Mahindra 605) and one motor cycle (Hero Honda).

Brand awareness stronger among the rich: We found that awareness of brands is a function of the size of land holdings, typically. The smaller farmers we spoke to were neither picky nor aware of brands. The richer farmers were pretty clued into latest consumer trends and owned the array of aspirational consumer durables – plasma TVs, luxury cars, washing machines, air conditioners, etc.

Wealth effect of higher land prices: Another factor driving rural consumption is the wealth effect from rising land prices. A farmer told us that the price of his land had increased from INR0.3-0.4mn five years ago to INR2mn now, more than a 40% CAGR. The price appreciation has been much higher for land close to a road or area identified for residential or commercial development. Development of rural roads has boosted trade and movement of goods between villages and cities close by. There are also positive spill-over affects of development in neighbouring states. A relatively well-off farmer, we learnt, has invested in tippers which are being used to move road construction materials for a dam being built in neighbouring state of Himachal Pradesh. Farmers with land holdings close to roads have been particular beneficiaries of rising land prices, the wealth-effect from which has spurred consumption further. There has been a large and steady inflow of NRI remittances and this money has primarily been used to bid land prices higher.

Land the primary reservoir of savings: Agricultural surpluses have also been used to consolidate land holdings rather that being invested in other investment classes like equities. Bank deposits are mainly used for working capital needs.

Housing – thatched no longer: The housing outlook, we learnt, is good. While 10 years ago most rural houses were thatched and paved and fortified with cow-dung, almost all rural houses being built these days are made of cement and are reasonably furnished with most modern amenities and white goods.

7. Nashik, Maharashtra, Western India

Rise of consumer durables: The changes in consumer behaviour are more anecdotal in nature. We were told of farmers starting to buy LCD-TVs. Auto dealers talked about farmers buying Toyota Fortuner which costs close to INR2mn (US$45,000). Lifestyles are being influenced by television where access is rising on account of direct-to-home operators. One of the farmers we met told us that he has bought a Bolero for each of his sons when they turned 18.

Earnings reinvested in land: We also noted that the farmers talked about reinvesting a significant portion of their earnings back into land.

More diversified sources of income and wealth effects from rising land prices are underpinning changes in consumption habits

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 23

VI. Impact of information 1. Rai Bareilly and Barabanki, Uttar Pradesh, North central India

People are becoming more aware of brands through TV advertising, road connectivity to cities and retail stores. The younger generation with cash is more willing to experiment. With improved road connectivity and availability of transport rich people also travel more frequently to cities to buy the latest apparel and consumer goods. Retail stores are in initial stages but have been catching on as people get wealthier. People are also able to get up-to-date information on crop prices through cell phones, thus improving their ability to negotiate prices.

2. Mathias Nagar, Nagercoil, Trivandrum, Kerala, Southern India

Rural consumers are getting more tech- and brand-savvy. Almost everyone has a TV and cable connection in their house. The government had run a scheme last year to distribute free TVs to poor households. Many farmers have got TVs under this scheme. Although the middle-aged farmers and their wives are not too brand-savvy, their children, who are better-educated and are influenced by advertising, are very particular about their brand preferences. They prefer to buy brands endorsed by their favourite actors and actresses.

Mobile phones have had a significant positive impact on the daily lives of farmers and fishermen. Most farmers have 3-4 mobiles in their houses which they share with their labourers. For them, communication is vital between them and their labourers, to get information about produce prices in other regions.

3. Navsari, Gujarat, Western India

The increased penetration of TV and mobiles has led to heightened awareness about brands and increased consumerism. Mobiles have also helped the farmers regarding information on weather and product prices. As per the farmers, given that they live in joint families, somebody or the other is always watching TV in the house resulting in demand for branded items by their kids and wives. An increasing number of computers is also being sold to farmers’ children with internet connections.

4. Nashik, Maharashtra, Western India

There are couple of points here. First, cell phones have made a significant impact on the availability of rural information. Farmers can subscribe to a service at INR30/month to receive prices in wholesale markets (and can choose to take their produce to the market where prices are higher). Second, at every “Panchayat” level the government has made PC connection available. The Internet service is used extensively for price information.

Technology, infrastructure, media and mobile phones are mitigating business risks and driving consumerism

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 24

VII. Other feedback from conversations with farmers

Maddur and Mandya, Karnataka, Southern India

Feedback from farmer: We met Mr Raju, who has about 4 acres of land on which he grows paddy. However, over the years, he has diversified into other businesses. He now runs a small factory where he manufactures bricks using a JCB machine. These bricks are manufactured using sand, which is only allowed under licence along the coast. However, because of the shortage of these bricks, there are many such illegal operations running in places close to Bangalore. Mr Raju is only a sub-contractor and does not deal with the final user himself.

This is a very profitable business. One truck load is worth INR16,000 in revenues and excluding costs (INR6,000 for materials, INR4,000 for labourers, and INR4,000 as bribe to local authorities to run the operation), he makes a net profit of INR2,000 per truck load. He does about 25 truck loads in a month and has a net income of INR50,000 per month from this operation.

He has been investing back into this business over the last few years and now owns two of the JCB machines that he uses. One of them is fully paid for and he has an outstanding loan on the other machine with an EMI of INR46,000, which he is able to service using money he earns from his farm income as well as the bricks business.

Feedback from farmer: We met Mr Somanna, who has about 3.5 acres of land on which he grows paddy and ragi. He has over the years diversified into manufacture of raw silk. There is a big silk industry in the area and he supplies to the end users. He is aware of the loans that the government provides to start a silk manufacturing unit, but has opted to not take any loans because of the red tape involved in getting a government loan approved. He produces about 200kg of raw silk, which gives him a profit of INR25,000.

Also like many others in the area, this family grows most of the produce it needs. Only a few items are sourced from the market such as FMCG products.

The government provides funding of about 60% to set up a silk worm house. It costs about INR0.1mn to setup a house with the silk worms. However, he has opted to not take the government funding.

Barasat and Kolkata, West Bengal, Eastern India

Feedback from farmer: We met Mr Dashrath Sarkar, who grows vegetables and supplies them to the market in Kolkata and uses a truck on rental basis to transport the produce from the farm to the market. However, he has recently bought a Mahindra Geo to help in the transport of vegetables. He has made a down payment of INR38,000 for this vehicle and pays an EMI of INR4,200 per month. He earns an income of INR25,000 per month from this business and has about 2 acres of land. He also gets about INR2000 from selling milk and INR15,000 from selling fish. His family use HPC and FMCG products such as Lifebuoy soap and Britannia biscuits. He owns a TV and a two wheeler.

Feedback from farmer: We met with Mr Hashnu, who has a brick manufacturing set-up in Bashirhat. He has farmland of about 10 acres on which he grows paddy twice a year. He said he has benefitted from the improving farm economics in the past 5 years and the price which he gets for his produce is up significantly in the period. His biggest concern is the increasing labour cost over the next couple of years. His brick manufacturing unit earns his about INR0.1mn per month. He has spent on building a new house in the area, and owns a variety of vehicles including a Mahindra Bolero. He also owns four trucks (2 Tata, 1 Ashok Leyland and 1 Shriram), which help him transport the bricks to the end-user. He owns variety of white goods including 2 air-conditioners, a refrigerator and TV with a cable connection.

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 25

Feedback from farmer: We met with Mr Ramakant Das, who runs a variety of businesses and lives in a village which is about 80km from Barasat. He owns about 3 acres of land. He makes about INR10,000 per month from cultivating vegetables, INR10,000-15,000 per month from cultivating paddy and INR15,000 per month from renting out his vehicle (a Maruti Omni). He has recently bought an Eicher truck and has a loan amount of INR 0.7mn and an EMI of INR16,500.

He said the infrastructure in his village has improved dramatically over the last five to seven years as new roads have been built under the Pradhan Mantri Gram Sadak Yojna (centre-sponsored rural roads scheme). There are about 845 houses in the village, which have all been rebuilt or revamped over the last 5 years.

Most homes in the village have a cable connection. Lifebuoy, Lux, Parle-G, Wheel and Maggi seem to be the popular FMCG products.

Strategy | India Prabhat Awasthi

27 January 2011 Nomura 26

Valuation methodology and investment risks

Bajaj Auto (BJAUT IN)

We value Bajaj Auto based on DCF at INR1,810. This includes INR209/share of bookvalue of investments. We are building in volume growth of 38% for FY11F and 15.5% for FY12F. We are building in 20.4% margins for FY11F and 19.7% margins for FY12F. Risks include slower-than-expected volume growth; possibility of price wars breaking out that could result in downside to our margin estimates; and a global slowdown in domestic and/or export markets could present downside risks to our volume estimates.

Mahindra & Mahindra (MM IN)

Valuation: Mahindra and Mahindra is our top pick in the India Auto sector. We value Mahindra and Mahindra at INR 892/share. We value the standalone business at 13x Average EPS of FY12 and FY13 (INR 51.2) at INR666/share and subsidiaries at INR 226/share. Key Risks: Ssangyong Motors acquisition: MM is planning to acquire Ssangyong Motors in Korea (announced in August 2010). Below-normal rainfall in 2011: We have assumed a scenario of normal rainfall in 2011. Risks. If rainfall is significantly different from normal, it could have a material impact on our volume estimates. Excise duty increase: We have assumed that the excise duty will not be increased from the current 10%. If it is increased further, it could have a material negative impact on our margin estimates as the company may not be able to pass through increases in excise duty on tractor components.

ITC (ITC IN)

We value the company using a sum-of-the-parts valuation methodology. We value the core cigarettes business at INR149 per share based on a P/E multiple of 22x FY11F earnings. The other core businesses are valued at around INR44 per share. We have valued the net cash (after deducting corporate expenses) at book value. Risks: Policy directives from the union government form the biggest risk to our investment view.

Jain Irrigation (JI IN)

We value JISL based on an earnings multiple of 20x our one-year rolling forward EPS (methodology unchanged) to arrive at our target price of INR261.