nobles fin5 ppt_10

TRANSCRIPT

Chapter 10Investments

Learning Objectives

1. Identify why companies invest in debt and equity securities and classify investments

2. Account for investments in debt securities

3. Account for investments in equity securities

10-2

Learning Objectives

4. Describe and illustrate how debt and equity securities are reported

5. Use the rate of return on total assets to evaluate business performance

10-3

Learning Objective 1

Identify why companies invest in debt and equity securities and classify investments

10-4

Why Do Companies Invest?

10-5

• Businesses invest in a variety of companies’ stocks and bonds.

• An investor is the owner of a bond or share of stock.

• The investee issues the bond or stock to the investor.

• A security is a share or interest representing financial value. There are two types of securities:– Debt securities– Equity securities

Reasons to Invest

• Why would a company invest in debt or equity securities? There are two common reasons: • To invest excess cash in order to generate

investment income• To invest in a debt or equity security of other

companies as a business strategy, such as enhancing a business relationship

10-6

Classification and Reporting of Investments

10-7

• Investments are classified as short-term investments or long-term investments.

• Types of investments:– Trading investments– Held-to-maturity investments (HTM)– Available-for-sale investments (AFS)– Significant interest investments– Controlling interest investments

10-8

Classification and Reporting of Investments

Learning Objective 2

Account for investments in debt securities

10-9

How Are Investments in Debt Securities Accounted For?

• Companies record the investment in debt securities by first recording the purchase of the investment.

• Companies record interest revenue. • At the date of maturity, companies record

the disposition of the investment.

10-10

Purchase of Debt Securities

• Smart Touch Learning has excess cash to invest and pays $100,000 to buy $100,000 face value, 9%, five-year Neon Company bonds on July 1, 2016. Smart Touch Learning plans to hold the bonds until maturity.

10-11

Interest Revenue

• On December 31, 2016, Smart Touch Learning receives the first interest payment on the bond investment.

10-12

Disposition at Maturity

• When Smart Touch Learning disposes of the bonds at maturity on June 30, 2021, it will receive the face value of the bond. Assuming the last interest payment has been recorded, the entry is:

10-13

Learning Objective 3

Account for investments in equity securities

10-14

How Are Investments in Equity Securities Accounted For?

• The accounting for equity securities is based on the percentage of ownership:– Cost method for ownership less than 20%– Equity method for ownership between 20% and

50%– Consolidations for ownership greater than 50%

10-15

Equity Securities with Less Than 20% Ownership (Cost Method)

• Accounted for as either:– Trading securities– Available-for-sale securities

• Recognize dividend revenue• Adjust for changes in market value• Recognize gain or loss on disposition

10-16

Purchase of Equity Securities

• On March 1, 2016, Smart Touch Learning acquires 1,000 shares of stock in Yellow Corporation for $26.16 per share. Smart Touch Learning owns less than 20% of Yellow’s voting stock. Treat as available-for-sale investment.

10-17

Dividend Revenue

• Yellow Corporation declares and pays a cash dividend of $0.16 per share on June 9, 2016.

10-18

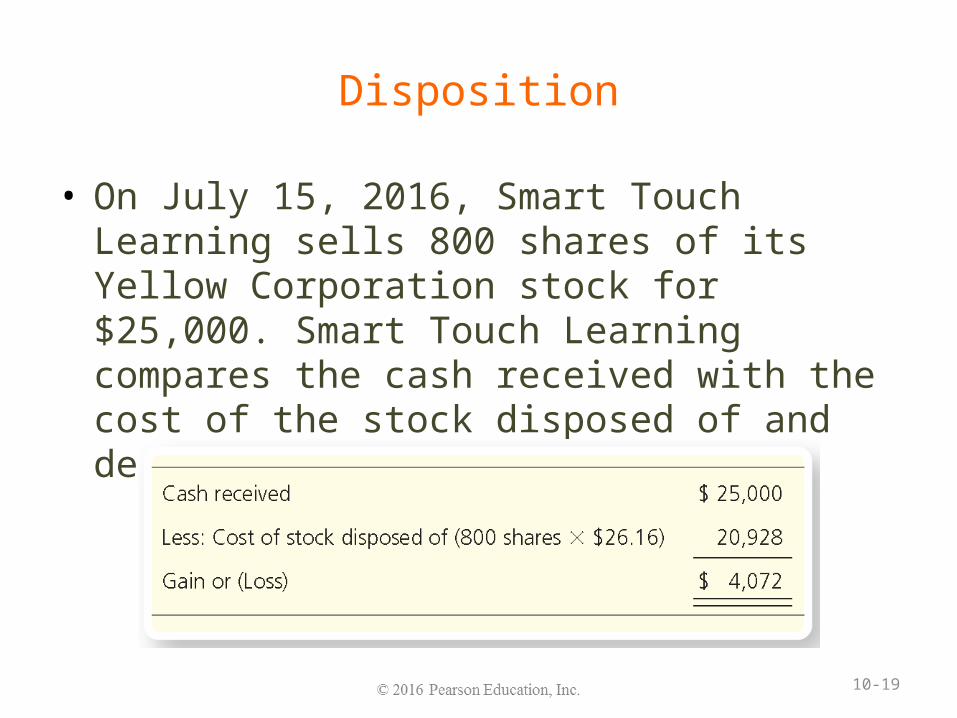

Disposition

• On July 15, 2016, Smart Touch Learning sells 800 shares of its Yellow Corporation stock for $25,000. Smart Touch Learning compares the cash received with the cost of the stock disposed of and determines the gain as follows:

10-19

Disposition

• Smart Touch Learning will record the following entry for the disposition of the Yellow Stock:

10-20

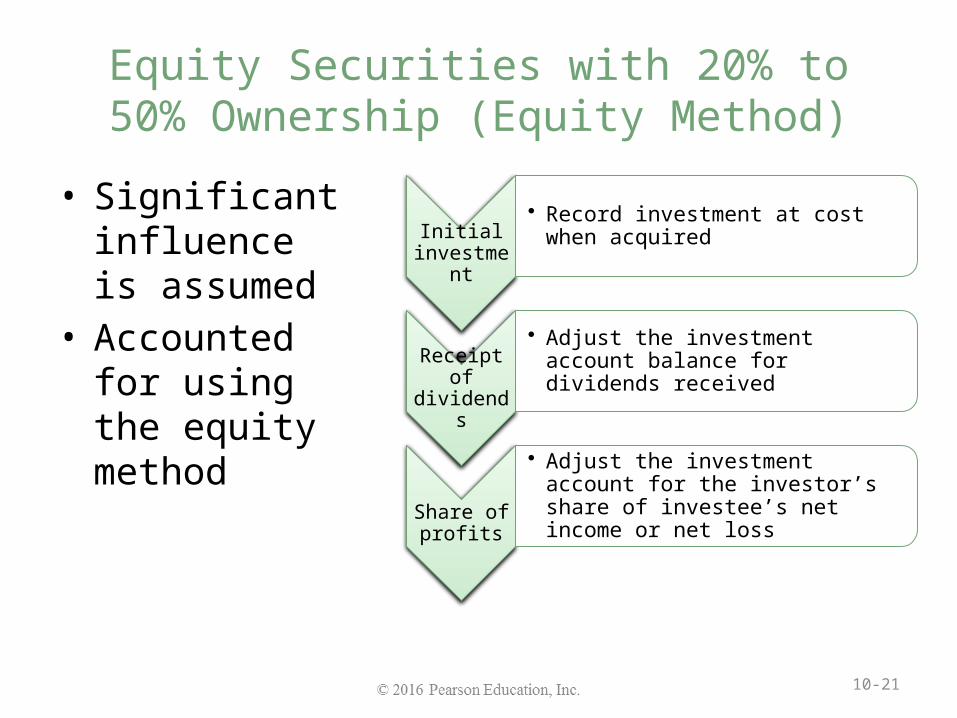

Equity Securities with 20% to 50% Ownership (Equity Method)

• Significant influence is assumed

• Accounted for using the equity method

10-21

Initial

investmen

t

• Record investment at cost when acquired

Receipt of dividends

• Adjust the investment account balance for dividends received

Share of profi

ts

• Adjust the investment account for the investor’s share of investee’s net income or net loss

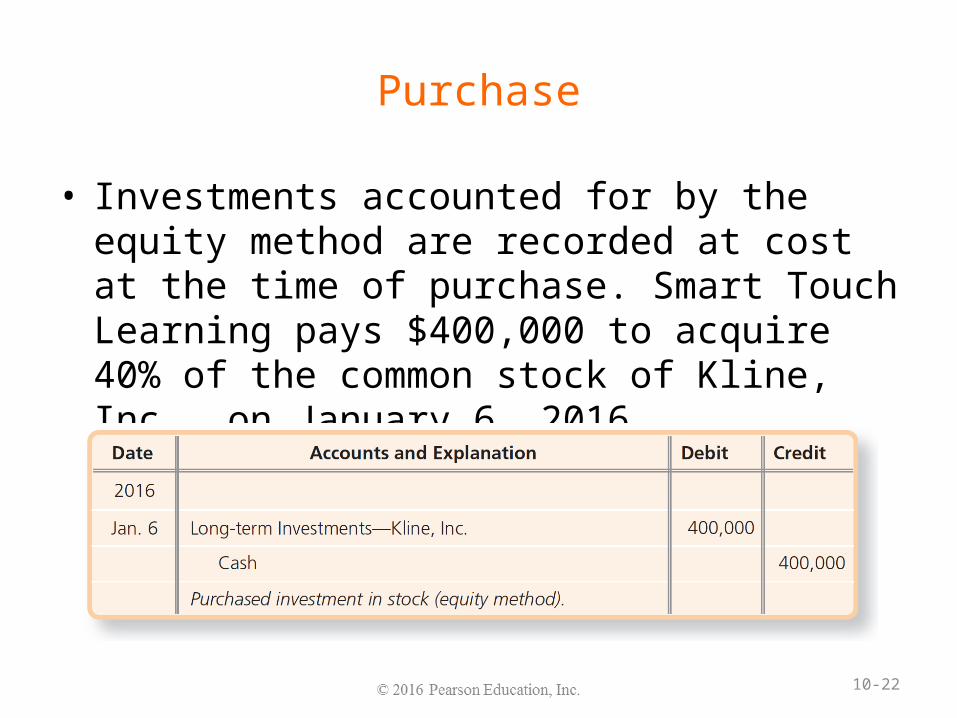

Purchase

• Investments accounted for by the equity method are recorded at cost at the time of purchase. Smart Touch Learning pays $400,000 to acquire 40% of the common stock of Kline, Inc., on January 6, 2016.

10-22

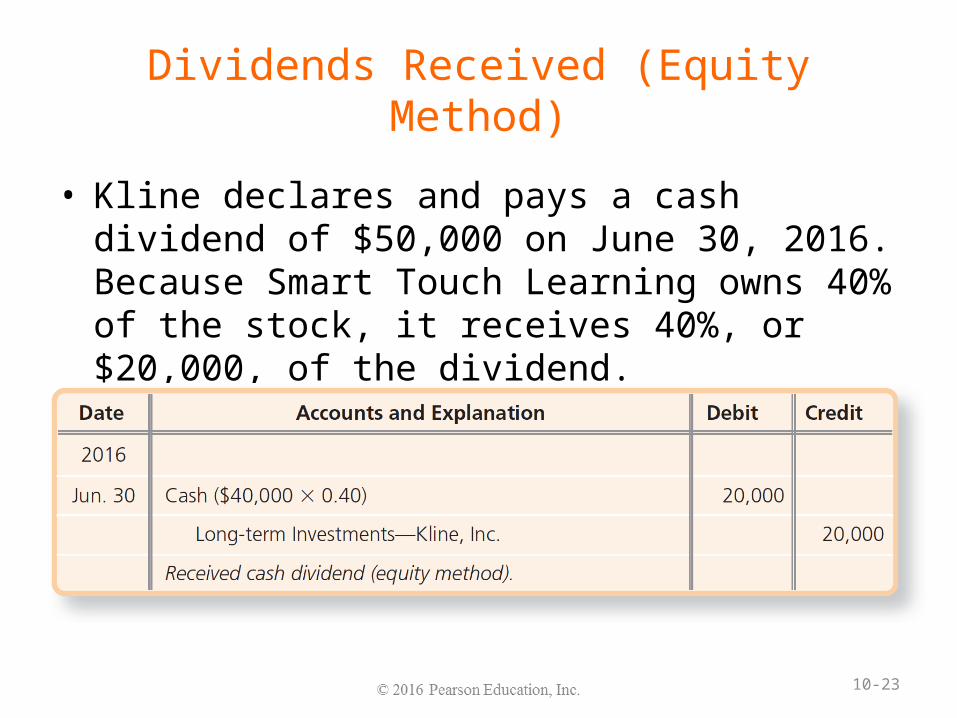

Dividends Received (Equity Method)

• Kline declares and pays a cash dividend of $50,000 on June 30, 2016. Because Smart Touch Learning owns 40% of the stock, it receives 40%, or $20,000, of the dividend.

10-23

Share of Net Income (Equity Method)

• Kline, Inc., reported net income of $125,000 for the 2016 year. Smart Touch Learning must account for 40% of Kline’s net income as an increase in the investment account.

10-24

Equity Securities with 20% to 50% Ownership (Equity Method)

• After the preceding entries are posted, Smart Touch Learning’s Long-term Investments T-account shows its equity in the net assets of Kline as follows:

10-25

Disposition

• On January 1, 2017, Smart Touch Learning sells 10% of the Kline common stock for $40,000. Smart Touch Learning will calculate the gain or loss as follows:

10-26

Disposition

• The journal entry to record the disposition of 10% of Smart Touch Learning’s interest in Kline is as follows:

10-27

Equity Securities with More Than 50% Ownership (Consolidations)

• A controlling interest exists when the investor owns more than 50% of the investee’s voting stock. • The parent company is the corporation that

controls the other company. • The subsidiary company is the company

controlled by another corporation. • The parent prepares consolidated statements

using consolidation accounting.

10-28

Learning Objective 4

Describe and illustrate how debt and equity securities are reported

10-29

How Are Debt and Equity Securities Reported?

• Trading investments• Available-for-sales (AFS) investments• Held-to-maturity investments

10-30

Trading Investments

• Record initial investment at cost.

• Adjust for changes in fair value.

• The fair value adjustment is called unrealized holding gain/loss.– Reported on the

income statement

10-31

Fair value is the price that would be

used if the company were to

sell the investments on the

market.

Trading Investments

• On December 31, 2016, Smart Touch Learning reported trading investments of $26,160. The market value of the investments is $24,000.

10-32

Available-for-Sale Investments

• Record initial investment at cost.

• Adjust for changes in fair value.

• The adjustment is called unrealized holding gain/loss.– Reported in

stockholders’ equity

10-33

The adjustment is recorded and shown in the stockholders’ equity section of the

balance sheet as part of comprehensive

income.

Available-for-Sale Investments

• On December 31, 2016, Smart Touch Learning reported AFS investments of $60,000. The market value of the investments is $64,000.

10-34

Available-for-Sale Investments

• Comprehensive income includes net income plus some specific gains and losses, such as unrealized holding gains or losses on available-for-sale investments.

10-35

Held-to-Maturity Investments

• Held-to-maturity investments are reported at amortized cost.

• The investment may be reported as a current asset or long-term asset on the balance sheet, depending on the maturity date.

• Interest revenue is reported on the income statement in the Other Revenues and (Expenses) section.

10-36

How Are Debt and Equity Securities Reported?

10-37

Learning Objective 5

Use the rate of return on total assets to evaluate business performance

10-38

How Do We Use the Rate of Return on Total Assets to Evaluate Business Performance?

• The rate of return on total assets measures a company’s success in using assets to earn a profit.

• Companies finance assets two ways:– Debt: A company borrows from creditors to

purchase assets.– Equity: A company receives cash or other

assets from stockholders.

10-39

• The rate of return on total assets is calculated by adding interest expense to net income and dividing by average total assets. For Green Mountain:

10-40

How Do We Use the Rate of Return on Total Assets to Evaluate Business Performance?

10-41