nigeria inter-bank settlement system (nibss) plc. december 04, 2012 financial derivatives company...

TRANSCRIPT

NIGERIA INTER-BANK SETTLEMENT SYSTEM (NIBSS)

PLC.

December 04, 2012

Financial Derivatives Company Limited

PROJECT REPORT

LAGOS PoS ADOPTION SURVEY for

Conducted by:

Commissioned by:

1

Outline

Executive Summary Background Methodology Survey Findings Summary and Conclusion Recommendations and Next Steps

2

Executive Summary

3

Executive Summary

NIBSS commissioned FDC in October 2012 to conduct a PoS adoption survey in Lagos (Project NIBSS)

The project goal is to ascertain the level of adoption and/or inhibitions to the widespread adoption of PoS terminals in Lagos

The project scope entails a market survey of both merchants and end-users (cardholders) of PoS terminals in Lagos

Market survey conducted via administration of questionnaires in four categories of market areas across Lagos

4

PoS Adoption Rate In Context

Deductions from available data on total number of PoS terminals deployed and volume of transactions conducted indicates that PoS terminals deployed recorded an average of 46 transactions and a maximum of 56 transactions per PoS terminal monthly over the period under consideration

5

Source: NIBSS

Research ObjectivesActive profiles

Understand the profiles of merchants and end-users

Service attractiveness Investigate the attractiveness of the PoS

Terminals Compare with other means of payment

Service weakness Identify perceived obstacles with the use of the

PoS Terminals Identify solutions that will enhance the adoption,

subscription and effective utilisation of the card payment system

Geographical Dynamics Understanding the dynamics and challenges in the

use of PoS Terminals, geographically6

Results and Findings

7

Merchants with PoS

8

Merchants with PoS TerminalsAccording to the survey

results, of the 3,562 merchants with PoS terminals47% are general merchants22.4% operate

supermarkets10.9% are pharmaceutical

stores/hospitals 7.3% are

restaurants/eateries12.4% are other forms of

businessesThese business types are

mostly located in open markets (39.5%)Neighborhood shops

constitute 29.5% 29.5% are in shopping

malls and 1.5% are kiosk locations

Business Location

9

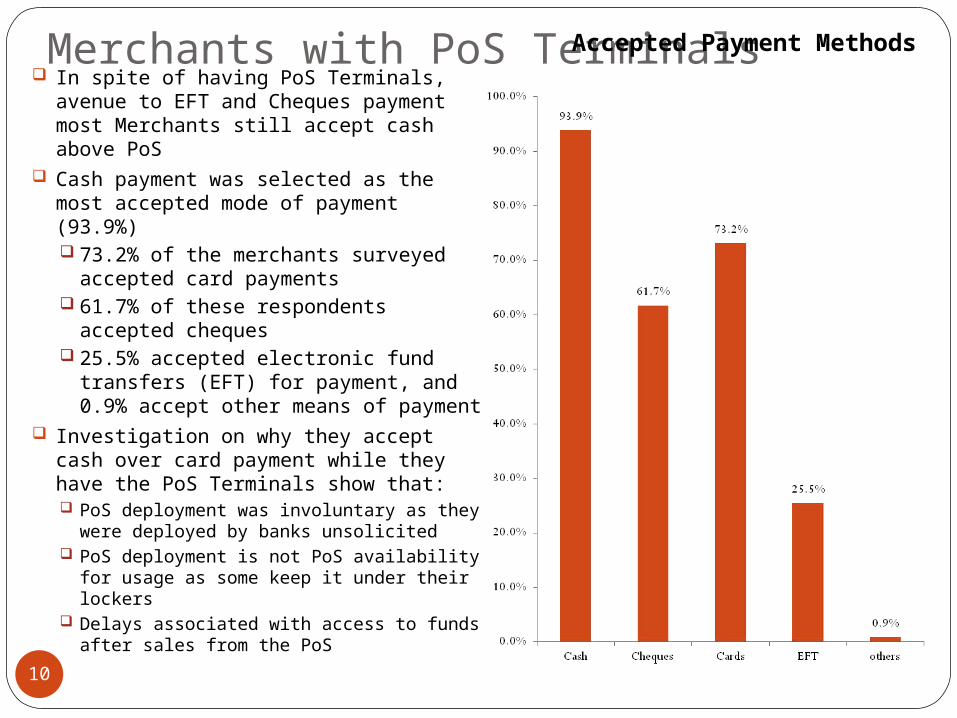

Merchants with PoS Terminals In spite of having PoS Terminals, avenue

to EFT and Cheques payment most Merchants still accept cash above PoS

Cash payment was selected as the most accepted mode of payment (93.9%) 73.2% of the merchants surveyed

accepted card payments 61.7% of these respondents accepted

cheques 25.5% accepted electronic fund

transfers (EFT) for payment, and 0.9% accept other means of payment

Investigation on why they accept cash over card payment while they have the PoS Terminals show that: PoS deployment was involuntary as they

were deployed by banks unsolicited PoS deployment is not PoS availability for

usage as some keep it under their lockers Delays associated with access to funds

after sales from the PoS

Accepted Payment Methods

10

Merchants with PoS Terminals By preference

75.5% of merchants prefer cash as the method of payment

9.1% rating for cheques 11.5% for cards 2.5% for EFTs 1.3% for other means of

payments

Accepted Payment Methods

11

For the non-cash options, 47% of merchants

prefer the card payment scheme to other payment schemes.

On the available card types40.7% of merchants

prefer the Master CardVISA is the next

preferred card payment type with 31.9% of the responses followed by Verve with 27.4% of the responses.

Merchants with PoS Terminals

12

A total of 24.4% of merchants indicated that the success rate of cards is less than 25%

29.8% of merchants believe the success rate to be between 25% and 55%.

29.6% claimed that success rate was between 55% and 75%

16.2% of the merchants indicated that the success rate of card payment was above 75%

Merchants with PoS Terminals

13

Recommendation – Merchants With PoS Terminals

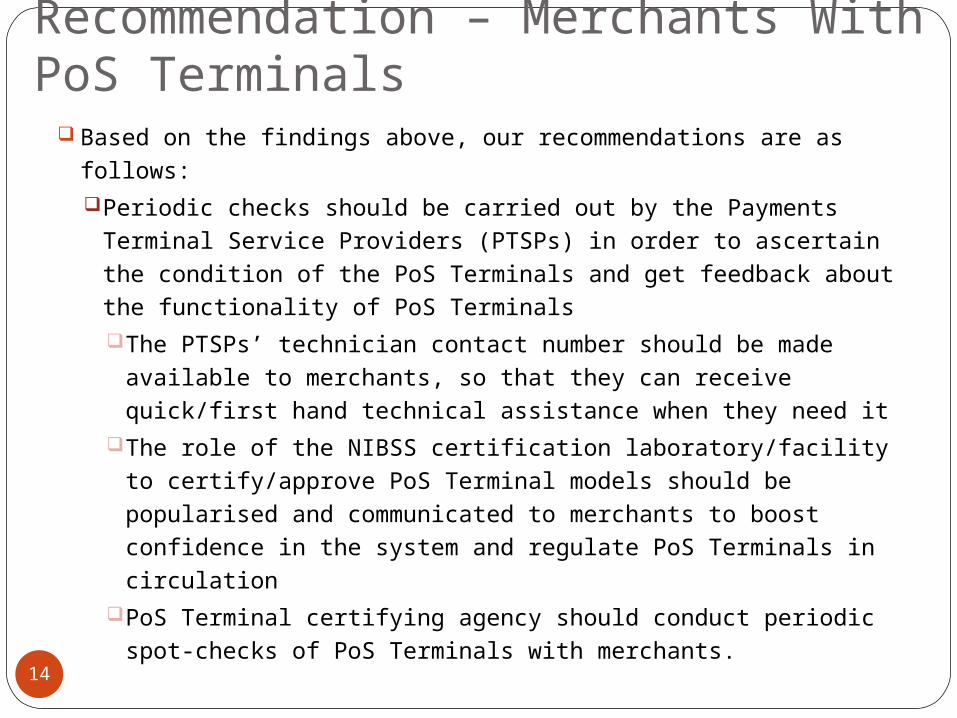

Based on the findings above, our recommendations are as follows:Periodic checks should be carried out by the Payments Terminal

Service Providers (PTSPs) in order to ascertain the condition of the PoS Terminals and get feedback about the functionality of PoS TerminalsThe PTSPs’ technician contact number should be made

available to merchants, so that they can receive quick/first hand technical assistance when they need it

The role of the NIBSS certification laboratory/facility to certify/approve PoS Terminal models should be popularised and communicated to merchants to boost confidence in the system and regulate PoS Terminals in circulation

PoS Terminal certifying agency should conduct periodic spot-checks of PoS Terminals with merchants.

14

Recommendation – Merchants With PoS Terminals

There should be partnership among banks, mobile payments operators, all other existing payment schemes and other support service providers to foster high availability and adoption of PoS Terminals, with the goals of:

Mitigating current network connectivity problemsDelays in accessing proceed of sales

A fair transaction charge should be agreed upon among banks, which should be communicated to the merchants, as:

Some merchants in certain locations are price-sensitive15

Merchants Without PoS

16

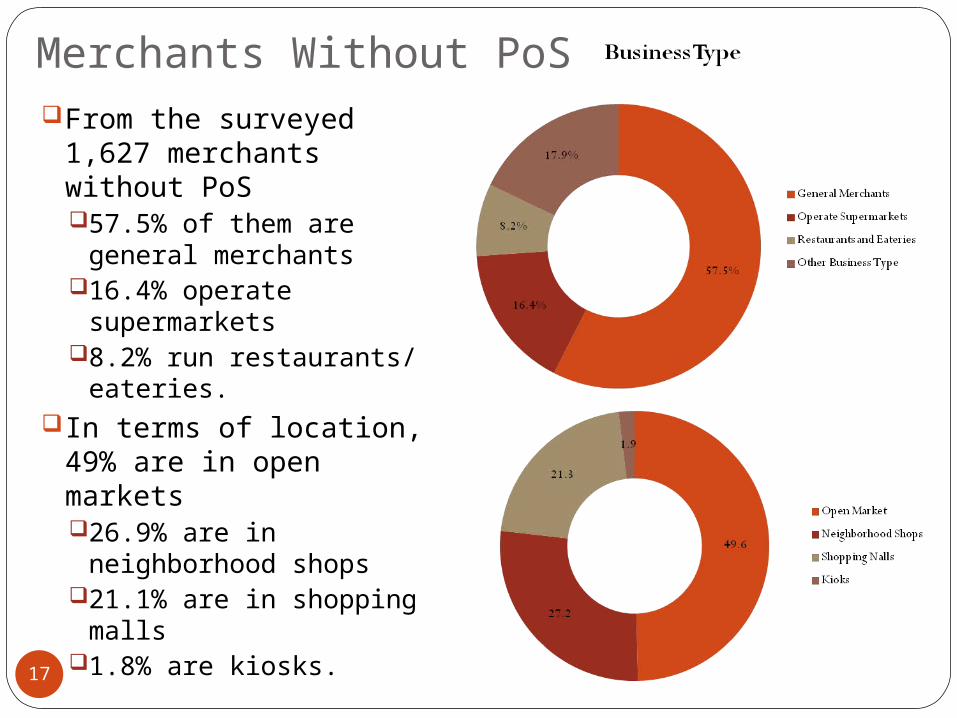

Merchants Without PoSFrom the surveyed 1,627

merchants without PoS57.5% of them are

general merchants16.4% operate

supermarkets 8.2% run restaurants/

eateries. In terms of location, 49%

are in open markets 26.9% are in

neighborhood shops21.1% are in shopping

malls1.8% are kiosks.

17

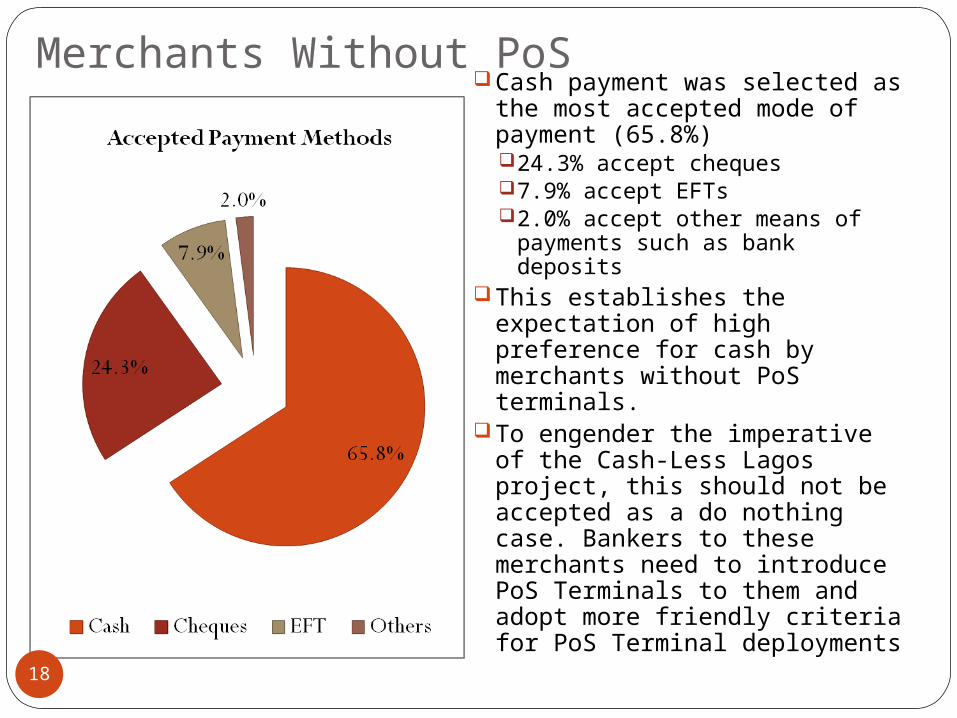

Merchants Without PoSCash payment was selected as

the most accepted mode of payment (65.8%) 24.3% accept cheques7.9% accept EFTs2.0% accept other means of

payments such as bank deposits

This establishes the expectation of high preference for cash by merchants without PoS terminals.

To engender the imperative of the Cash-Less Lagos project, this should not be accepted as a do nothing case. Bankers to these merchants need to introduce PoS Terminals to them and adopt more friendly criteria for PoS Terminal deployments18

Reasons alluded for not having PoS Terminals in descending order are:Fear of default and

fraud - 30.2%Easy access to cash –

27.7%Bank refusal to deploy

– 26.6%Customer’s insistence

to use cash – 25.7%Technical

malfunctioning – 21.6%

PoS Deployment/Transaction fee – 20.0%

Connectivity – 18.1%

Merchants Without PoS

19

70.0% of the merchants expressed willingness to accept PoS Terminal mode of payments.

Merchants Without PoS

20

We make the following suggestions based on our finding above: Banks need to revise the criteria for PoS Terminal

deployment in such a way as to encourage Merchants without PoS Terminals

A massive awareness program should be undertaken to publicize the purpose and benefits of the PoS system and allay fears of default/fraud in the following ways:Publicity through radio and direct contact

Focus on high and medium density areas (e.g. Oke-Arin, Nnamdi Azikiwe markets) because less sophisticated merchants are located in this areas.

Publicity in more sophisticated areas (e.g. Ikoyi, Victoria Island) should emphasize direct contact with the merchants and/or formal letters of introduction.

Other publicity means to be explored like bill boards, fliers, social media and TV adverts

Recommendation – Merchants Without PoS Terminals

21

PTSPs to be encouraged to accept frontal roles in PoS deployment in line with approved guidelines

Training on the usage of PoS Terminals immediately after

deployments PTSPs should check on the merchants after a few days of

training in order to ensure that merchants understand how

to use the PoS Terminals and are using them appropriatelyThe same procedures mentioned under the ‘merchants

with PoS’ section should be followed in order to ensure network problems and technical faults are addressed promptly

The fear of frauds would be resolved once the PoS Terminals are functioning properly because trust in the PoS system would have been built

Recommendation – Merchants Without PoS Terminals

22

Consumers/End-Users

23

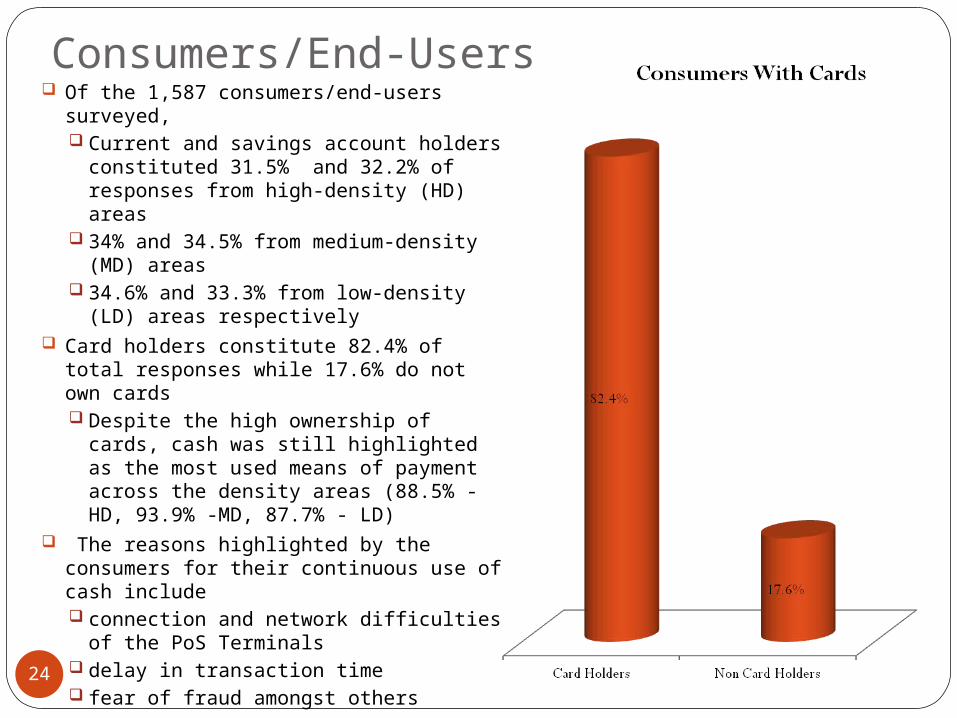

Consumers/End-Users Of the 1,587 consumers/end-users

surveyed, Current and savings account holders

constituted 31.5% and 32.2% of responses from high-density (HD) areas

34% and 34.5% from medium-density (MD) areas

34.6% and 33.3% from low-density (LD) areas respectively

Card holders constitute 82.4% of total responses while 17.6% do not own cards Despite the high ownership of cards,

cash was still highlighted as the most used means of payment across the density areas (88.5% - HD, 93.9% -MD, 87.7% - LD)

The reasons highlighted by the consumers for their continuous use of cash include connection and network difficulties of

the PoS Terminals delay in transaction time fear of fraud amongst others

24

Consumers/End-Users We also identified the closeness

of banks and ATMs’ to both merchants and consumers as a major inhibition to PoS Terminal adoption

Despite the inhibitors, the respondents indicated that they feel most comfortable using the PoS and card payment systems where available and secure. This explains comfort to use cards in supermarkets than in the open marketsSupermarkets (24.8%), malls

(17.0%), general merchants’ stores (15.0%), pharmaceutical stores and hospitals (11.5%), others (17.8%)

73% of consumers indicated they would encourage others to use the PoS and card payment systems based on their experience with the payment systems so far25

Recommendations – Consumers/End-UsersBased on our findings above, our suggestions are as

follows:A massive awareness program to publicize the purpose

and benefits of the PoS system (similar to that recommended for merchants without PoS)Publicity through radio, bill boards, fliers, social media and TV

advertsTown storms and road shows are recommended to fast track

end-users adoption Ensure transparency in the PoS system process

All transaction costs and other issues associated with PoS Terminal usage should be made known to consumers during the publicity program

Necessary steps to ensure that the PoS Terminals are working as expected should be publicized to build trust

26

Recommendations – CONSUMERS/END-USERSCarrying cash by consumers should be made

less attractive through policy formulationThe cash withdrawal limit by individuals should be

revised downward with more stringent charges for withdrawals above specified limits

The cash deposit limits for corporate account holders should be reduced and the penalty for large deposits should be increased

27

ConclusionThe potential for growth of the usage of PoS Terminal

in Lagos metropolis remains strong.With a population of over 16 million people, there

are presently approximately 8 million card holders in Lagos State

Based on the aggregated data from the 6,776 survey sample, the study found out the following:

Challenges / Perceived Obstacles to usage of PoS TerminalsTwo out of the three categories of respondents (i.e.

Merchants with PoS and Merchants without PoS Terminals) identify basically the same challenges and perceived obstacles to the smooth operation of the PoS Terminals

28

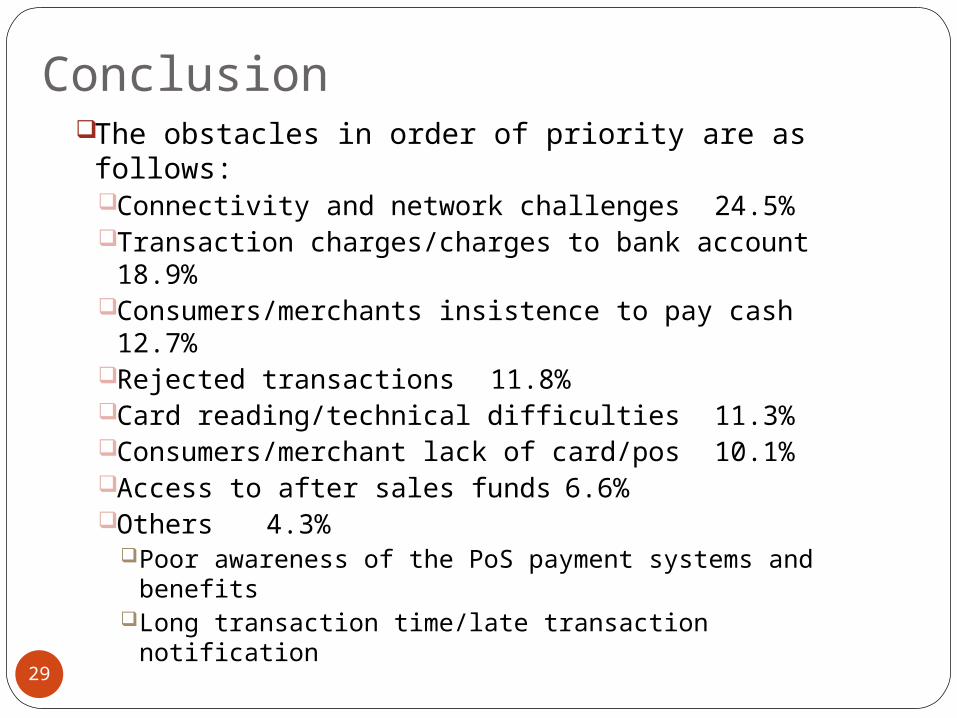

ConclusionThe obstacles in order of priority are as follows:

Connectivity and network challenges24.5%

Transaction charges/charges to bank account18.9%

Consumers/merchants insistence to pay cash12.7%

Rejected transactions 11.8%Card reading/technical difficulties

11.3%Consumers/merchant lack of card/pos 10.1%Access to after sales funds 6.6%Others 4.3%

Poor awareness of the PoS payment systems and benefits

Long transaction time/late transaction notification29

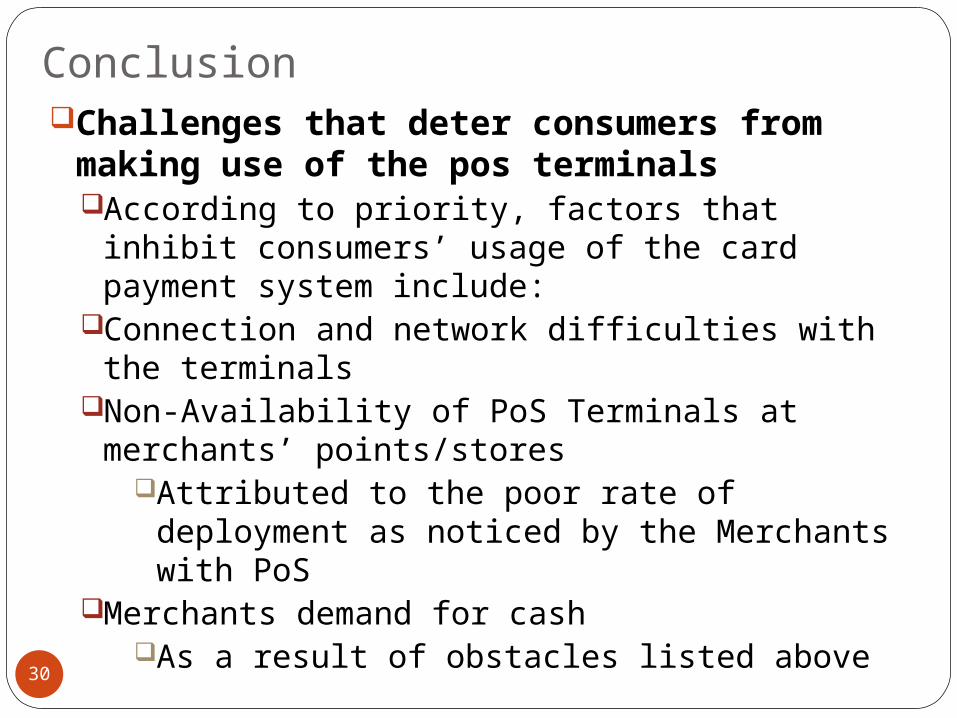

ConclusionChallenges that deter consumers from

making use of the pos terminalsAccording to priority, factors that inhibit

consumers’ usage of the card payment system include:

Connection and network difficulties with the terminals

Non-Availability of PoS Terminals at merchants’ points/stores

Attributed to the poor rate of deployment as noticed by the Merchants with PoS

Merchants demand for cash As a result of obstacles listed above

30

Conclusion

Long/delayed transaction timeFear of fraud

Some consumers gave personal experiences on being debited twice

In some cases the terminals reject the transaction, however the consumer receives a debit alert some hours after the unsuccessful transaction

31

Next Steps

32

Next StepsWe suggest a follow-up integration survey in Lagos

State most importantly in the areas not covered by this surveyThis will help to further identify other cultural and

fundamental barriers to the adoption of the PoS Terminals

Popularisation of NIBSS role as PoS Terminal certification agency and regular spot checks of PoS Terminals in use at merchant points

There is need for a pilot survey in other key cities where the Cash-less policy will be introduced before implementation This will help to identify the necessary pre-

implementation steps to be taken; identify the trend and compare results with the Lagos density areas

This will help underscore the model to be adopted for each of the new locations

33

Background & Methodology

34

Background and Methodology

The “Project NIBSS” entails a market survey of both merchants and end-users (cardholders) of PoS terminals in Lagos

Market survey conducted via administration of questionnaires in four categories of market areas across Lagos

Stratification of sample area (Lagos State) intoLagosYaba IkejaBadagry

Further stratification into high, medium and low density areas

35

Background and Methodology

Spot Check on enumerators during enumerationBy both FDC and NIBSS team

Project update presented during the course of the surveyFeedback from update incorporated

36

Scope of Survey

37

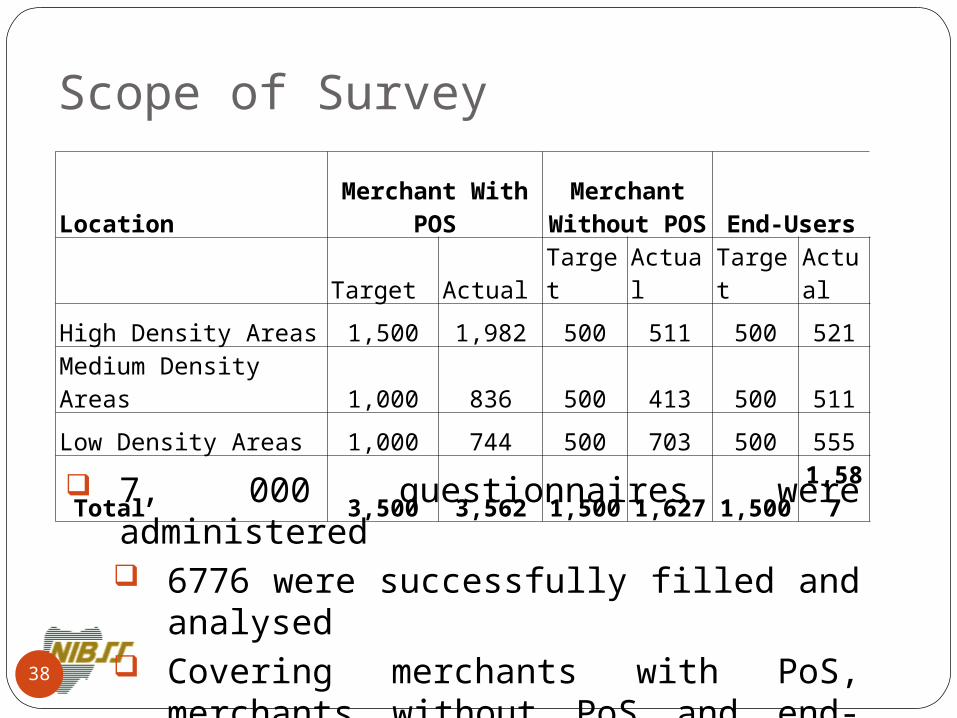

Scope of Survey

Location Merchant With POSMerchant

Without POS End-Users

Target Actual Target Actual Target Actual

High Density Areas 1,500 1,982 500 511 500 521

Medium Density Areas 1,000 836 500 413 500 511

Low Density Areas 1,000 744 500 703 500 555

Total 3,500 3,562 1,500 1,627 1,500 1,587

7, 000 questionnaires were administered 6776 were successfully filled and

analysed Covering merchants with PoS,

merchants without PoS and end-users ( Card and Non-card holders)

38

Drawbacks Drawbacks included

Several duplication of addresses of merchants with PoS

Incorrect addresses of merchants with PoS Difficulty in meeting owners and managers

where sales personnel's/other staff insist they cannot fill the questionnaires

Some questionnaires administered were not returned as a result of merchants insistence on enumerators picking them up later

Respondents fear of confidentiality Angry respondents (basically as a result of

their bad experiences with PoS terminal)39

Merchants with PoS

Survey Findings -Quantitative

40

Respondents Status in Relation to Business

41

Responses from Survey shows More business owners (45.43% - Yaba) responded to the

questionnaires 20.8% - Ikeja, 16.5% in Badagry and 11.6% in Lagos

21.1% in Ikeja were by managers 20.7% were by secretaries and personal assistants in Badagry 40.5% were other staff and workers in the various outlets

Respondents Status in Relation to Business

42

Equal number (25%) of respondents from the Ikeja, Badagry and Lagos zones are Owners, Managers, Partners and Sales representatives

However, a majority (38.5%) of the respondents in the Yaba medium density area were Owners

A greater proportion of the respondents in Yaba (46.7%) and Ikeja (24.0%) are Owners

Majority of the respondents in Badagry (24.0%) and Lagos (61.7%) zones are Managers

Sales representatives were 30% in the Lagos area

43

Respondent Status in Relation to Business

Nature of Business

44

35.6% (the majority) of the respondents in the Yaba high density areas were General merchants (traders)

Most respondents in Lagos (37.7%) own supermarkets

In the Badagry and Ikeja zones 20.2% and 20% own restaurants.

Most of the respondents in the Lagos (31.8%) and Yaba (43.9%) medium density areas were general merchants

In the Ikeja zone, 32.1% were owners of other kind of businesses

20% of respondents in the Badagry area were general merchants, own restaurants, supermarkets, pharmaceutical stores and hairdressing salons each

45

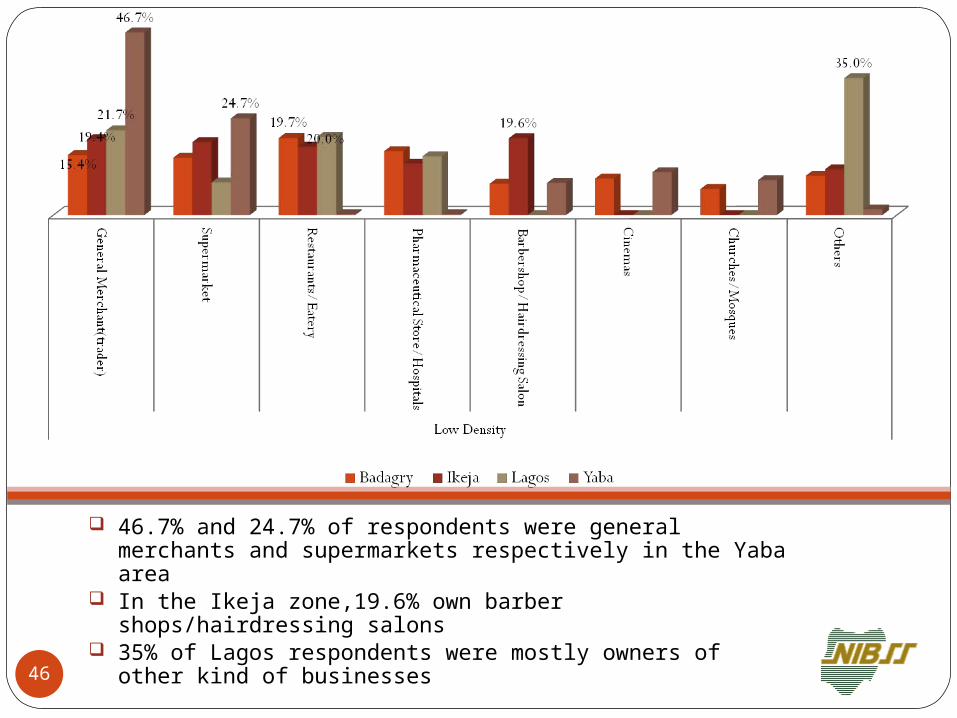

46.7% and 24.7% of respondents were general merchants and supermarkets respectively in the Yaba area

In the Ikeja zone,19.6% own barber shops/hairdressing salons

35% of Lagos respondents were mostly owners of other kind of businesses

46

Nature of Business and Business Location

47

General merchant stores (18.1%), supermarkets (7.2%), and restaurants (5.7%) were located in the open market, shopping malls, and kiosks respectively.

However, a majority of pharmaceutical stores (3.4%) and hair dressing salons (2.4%) were located in neighborhood shops.

General merchant stores (14.4%) and pharmaceutical stores (2.6%) were located in the open market

Supermarkets (7.1%), restaurants (3.7%) and hair dressing salons (1.3%) were located in kiosks, shopping malls and neighborhood shops respectively.48

Like other density areas, a majority (13.5%) of general merchants were located in open markets

Supermarkets (6.1%) and pharmaceutical stores (3.1%) were located in shopping malls

Majority of restaurants (4.1%) and hair dressing salons (2.4%) were located in neighborhood shops.

49

Nature of Business and Proximity to Banks and ATMs

50

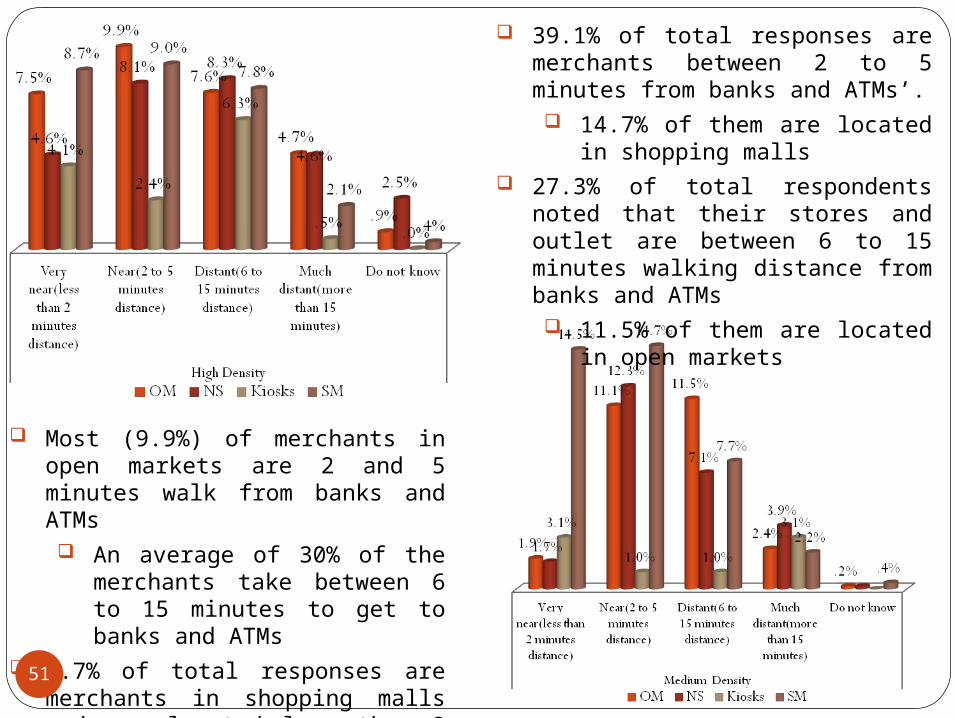

Most (9.9%) of merchants in open markets are 2 and 5 minutes walk from banks and ATMs An average of 30% of the

merchants take between 6 to 15 minutes to get to banks and ATMs

8.7% of total responses are merchants in shopping malls and are located less than 2 minutes away from banks and ATMs (24.9% - less than 2 minutes)

39.1% of total responses are merchants between 2 to 5 minutes from banks and ATMs’. 14.7% of them are located in

shopping malls 27.3% of total respondents noted

that their stores and outlet are between 6 to 15 minutes walking distance from banks and ATMs 11.5% of them are located in

open markets

51

36.9% of the responses take between 6 to 15minutes, while 36.4% of merchants take 2 to 5 minutes to get to banks and ATMs 12.8% of those with 6

to 15minutes are located in Kiosk

12.% of those with 2 to 5minutes are located in open markets

18.7% noted that their stores and outlet are less than 2 minutes walking distance from banks and ATMs 6.2% of them are

located in open markets

52

Accepted Means of Payment

53

54

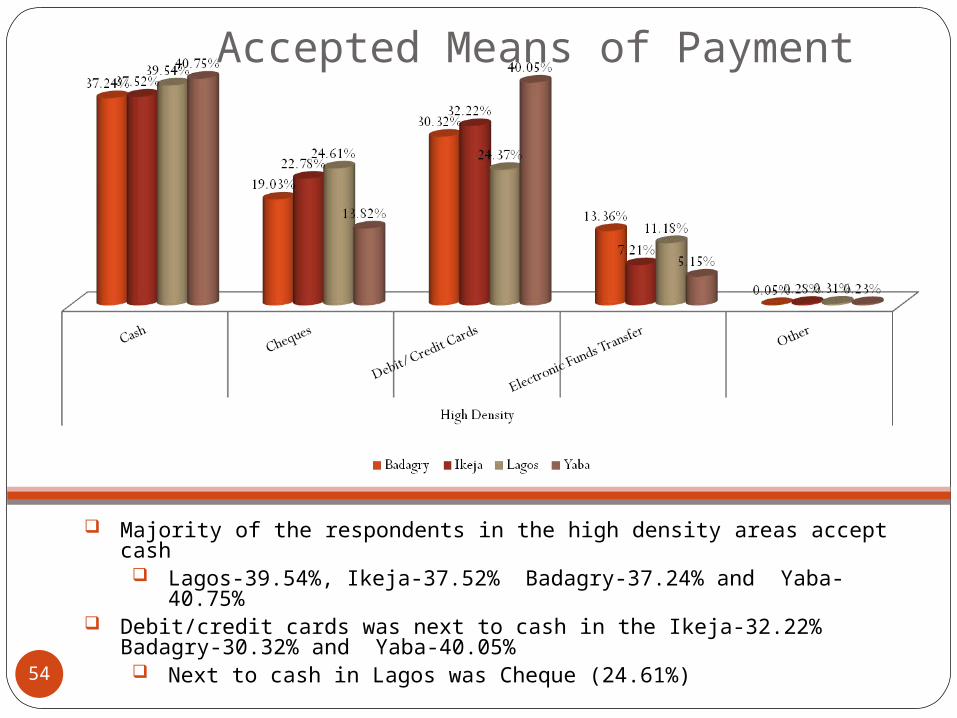

Majority of the respondents in the high density areas accept cash Lagos-39.54%, Ikeja-37.52% Badagry-37.24% and Yaba-40.75%

Debit/credit cards was next to cash in the Ikeja-32.22% Badagry-30.32% and Yaba-40.05% Next to cash in Lagos was Cheque (24.61%)

Accepted Means of Payment

Respondents in the Lagos (38.89%) and Yaba (32.47%) medium density areas accept cash.

In Ikeja (37.04%) preferred debit/credit cards Equal number (40.28%) of respondents in the Badagry area accept cash and

debit/credit cards55

Accepted Means of Payment

In the low density areas, majority of the respondents accept cash (Ikeja-38.06%, Badagry- 35.31%, and Yaba- 30.81%)

Equal number (37.65%) of respondents in the Lagos zone accept cash and debit/credit cards.

56

Accepted Means of Payment

Frequency of Usage

57

In all the high density areas, cash is used many times a day

Lagos- 85.1% Ikeja- 90% Badagry- 92.9% Yaba- 95.4%

EFT was never used Lagos- 35.8%Ikeja- 38.6%Badagry- 31.2% Yaba - 59.9%

58

Like the high density areas, cash was used many times a day in the medium density areas

Lagos- 65.2%, Ikeja-80% Badagry-89.7% Yaba-96.5%

Electronic funds transfer was never used

Lagos- 34.8% Ikeja - 68.9% Badagry (80%) Yaba- 34.2%

Many times per day

59

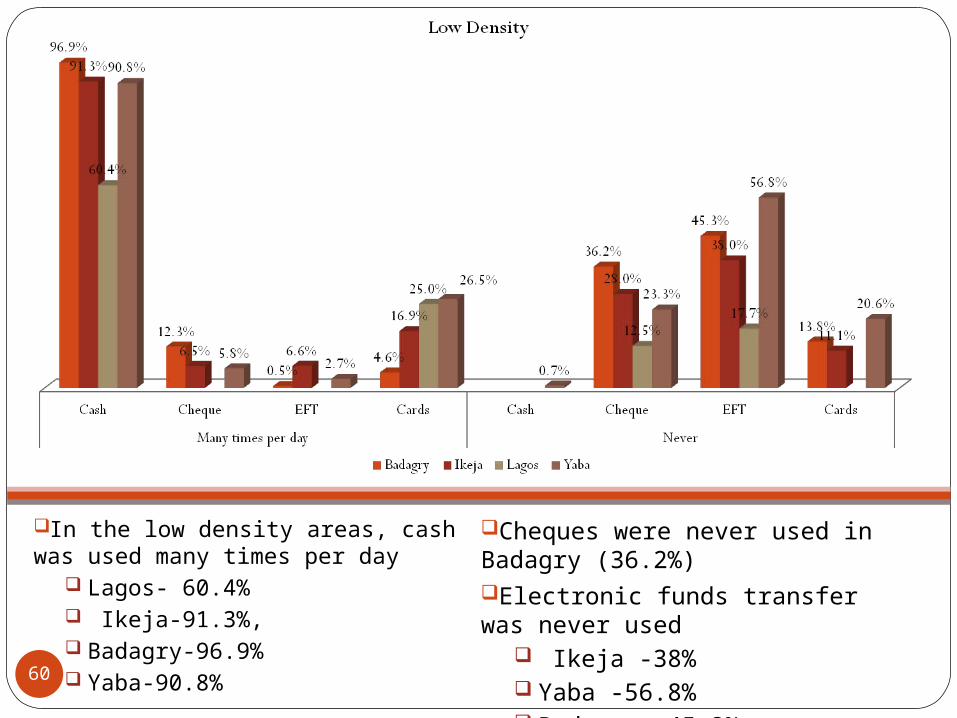

In the low density areas, cash was used many times per day

Lagos- 60.4% Ikeja-91.3%, Badagry-96.9% Yaba-90.8%

Cheques were never used in Badagry (36.2%) Electronic funds transfer was never used

Ikeja -38% Yaba -56.8% Badagry -45.3%

60

Preferred Card Scheme

61

Majority of the respondents in the Badagry (38.1%), Ikeja (30.6%) and Yaba (29.4%) high density areas preferred the MasterCard

VISA card was preferred in Lagos (22.2%) The second choice in the Badagry (30%) and Ikeja (23.7%) zones was the VISA card

MasterCard and Verve were the second best in the Lagos (20.9%) and Yaba (17.8%) zones respectively

62

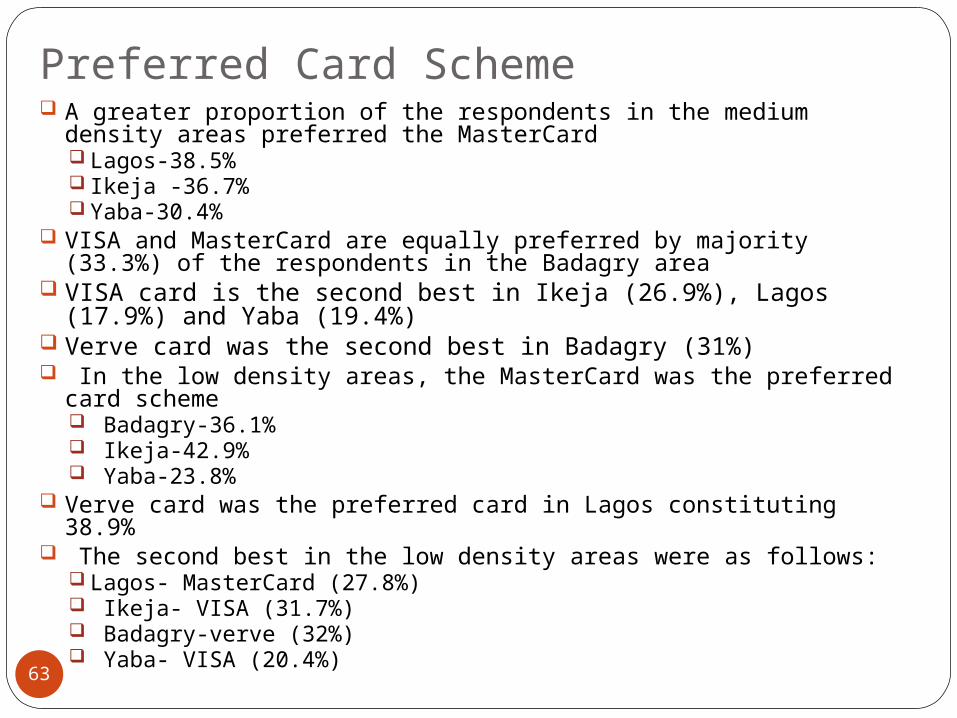

Preferred Card Scheme A greater proportion of the respondents in the medium density

areas preferred the MasterCard Lagos-38.5% Ikeja -36.7% Yaba-30.4%

VISA and MasterCard are equally preferred by majority (33.3%) of the respondents in the Badagry area

VISA card is the second best in Ikeja (26.9%), Lagos (17.9%) and Yaba (19.4%)

Verve card was the second best in Badagry (31%) In the low density areas, the MasterCard was the preferred card

scheme Badagry-36.1% Ikeja-42.9% Yaba-23.8%

Verve card was the preferred card in Lagos constituting 38.9% The second best in the low density areas were as follows:

Lagos- MasterCard (27.8%) Ikeja- VISA (31.7%) Badagry-verve (32%) Yaba- VISA (20.4%)63

PoS Usage Motivation

64

Majority of the respondents in the Ikeja (16.06%) and Yaba (14.55%) zones acknowledged that the main motivation for adopting the PoS was the simplicity of its usage.

Majority in the Lagos (15.46%) zone adopted the PoS due to high costs of cash management Badagry (15.57%) zone adopted the PoS based on other reasons 65

A greater proportion of the respondents in the medium density areas adopted the PoS due to faster payment processing time, image of the outlet, and high costs of cash management respectively

Yaba (16.1%), Lagos (15.9%) and Ikeja (15.7%)

66

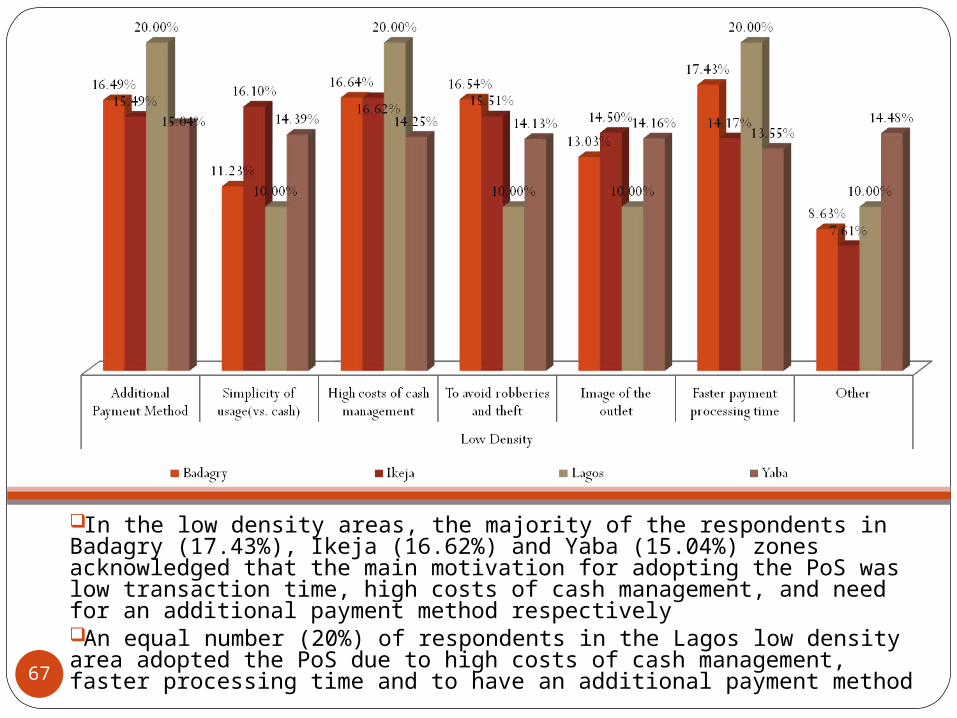

In the low density areas, the majority of the respondents in Badagry (17.43%), Ikeja (16.62%) and Yaba (15.04%) zones acknowledged that the main motivation for adopting the PoS was low transaction time, high costs of cash management, and need for an additional payment method respectivelyAn equal number (20%) of respondents in the Lagos low density area adopted the PoS due to high costs of cash management, faster processing time and to have an additional payment method

67

Perceived Inhibitions to PoS Usage

68

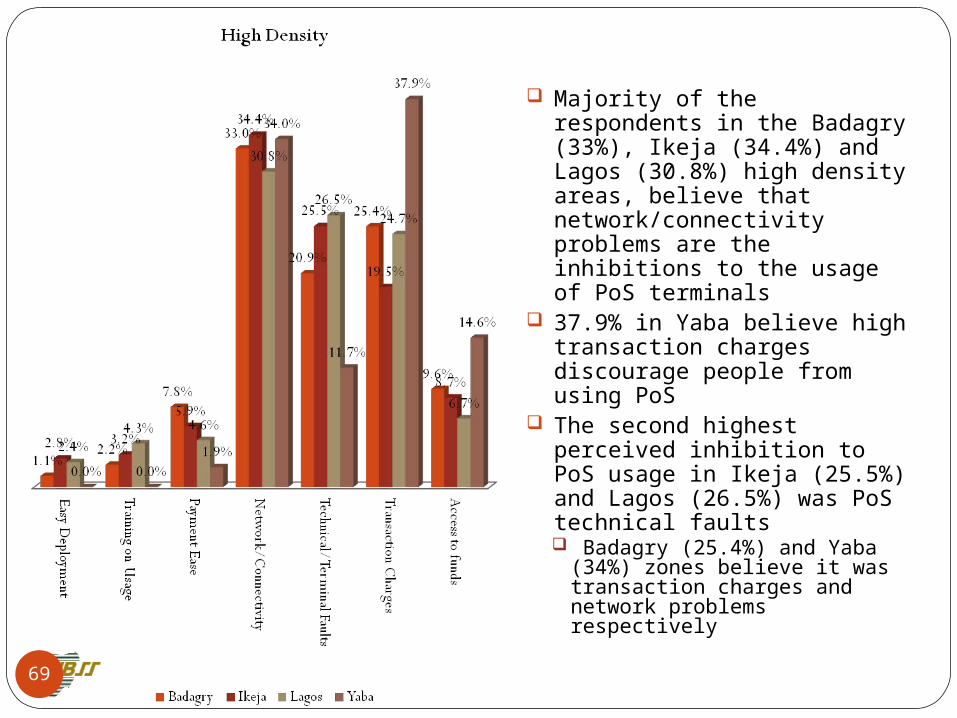

Majority of the respondents in the Badagry (33%), Ikeja (34.4%) and Lagos (30.8%) high density areas, believe that network/connectivity problems are the inhibitions to the usage of PoS terminals

37.9% in Yaba believe high transaction charges discourage people from using PoS

The second highest perceived inhibition to PoS usage in Ikeja (25.5%) and Lagos (26.5%) was PoS technical faults Badagry (25.4%) and Yaba

(34%) zones believe it was transaction charges and network problems respectively

69

Like the high density areas, 75% of the respondents Badagry, 30.6% in Lagos and 35.3% in Ikeja medium density areas believe that network/connectivity problems may prevent people from using the PoS

35.1% in Yaba believed that transaction charges was the main problem.

The second highest perceived inhibition to PoS usage in Ikeja (27.7%) and Badagry (25%) is PoS technical faults In Yaba (18.6%), delay in

access to funds is the second highest.

An equal number (27.4%) of respondents in the Lagos believe that the second highest inhibition to PoS usage was the high transaction charges and technical faults70

In all the low density areas, network/connectivity problems discouraged their usage of PoS terminals Lagos-66.7%, Ikeja-

29.9%, Badagry-38.2% and Yaba-35.6%

Technical faults are perceived to be the second highest inhibition to PoS usage in all the zones Lagos-25%, Ikeja-

24.8%, Badagry-28.7% and Yaba-28.2%71

Inhibitions to PoS Usage Based on Experience

72

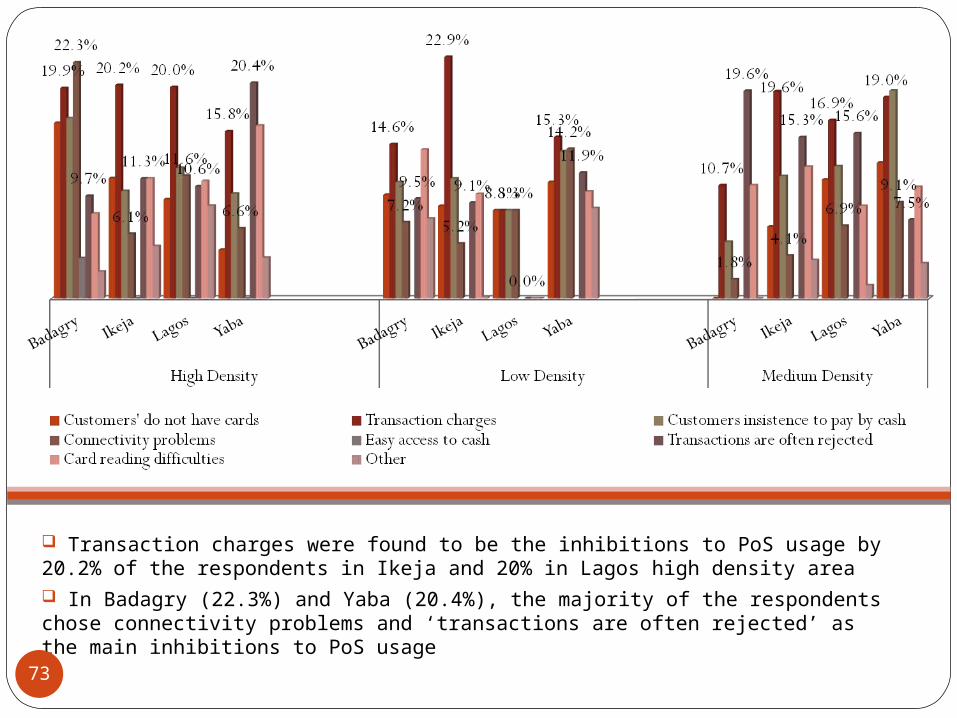

Transaction charges were found to be the inhibitions to PoS usage by 20.2% of the respondents in Ikeja and 20% in Lagos high density area In Badagry (22.3%) and Yaba (20.4%), the majority of the respondents chose connectivity problems and ‘transactions are often rejected’ as the main inhibitions to PoS usage

73

A greater proportion of the respondents in the Ikeja (19.6%) and Lagos (16.9%) medium density areas chose transaction charges as the inhibition to PoS usage

19.7% in Yaba and 19.6% in Badagry zones chose ‘customers insist to pay by cash’ and ‘transactions are often rejected’

In the Badagry (14.6%), Ikeja (22.9%) and Yaba (15.3%) low density areas, transaction charges were the main inhibitions to PoS usage

Equal percentage (8.3%) of respondents in Lagos chose connectivity problems, customer’s insistence to pay by cash, and transaction charges respectively as obstacles to PoS usage

74

Merchants without PoS

Survey Findings -Quantitative

75

Respondents Status in Relation to Business

76

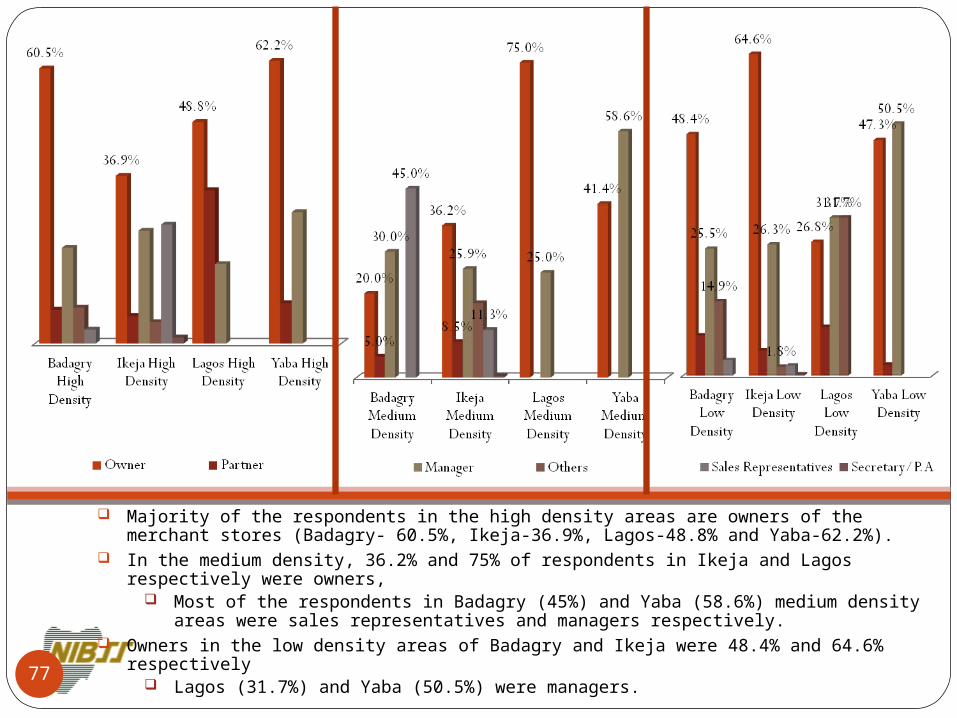

Majority of the respondents in the high density areas are owners of the merchant stores (Badagry- 60.5%, Ikeja-36.9%, Lagos-48.8% and Yaba-62.2%).

In the medium density, 36.2% and 75% of respondents in Ikeja and Lagos respectively were owners,

Most of the respondents in Badagry (45%) and Yaba (58.6%) medium density areas were sales representatives and managers respectively.

Owners in the low density areas of Badagry and Ikeja were 48.4% and 64.6% respectively Lagos (31.7%) and Yaba (50.5%) were managers. 77

Business Nature and Location

78

Most respondents (58.6%) were general merchants (traders) and they were located in the open market

16.7% of outlets business were supermarkets

Distribution of merchants’ location vary

50% were in Open markets

27% in Neighborhood shops

21% in Shopping malls

2% in Kiosk

79

Proximity to Banks and ATMs

80

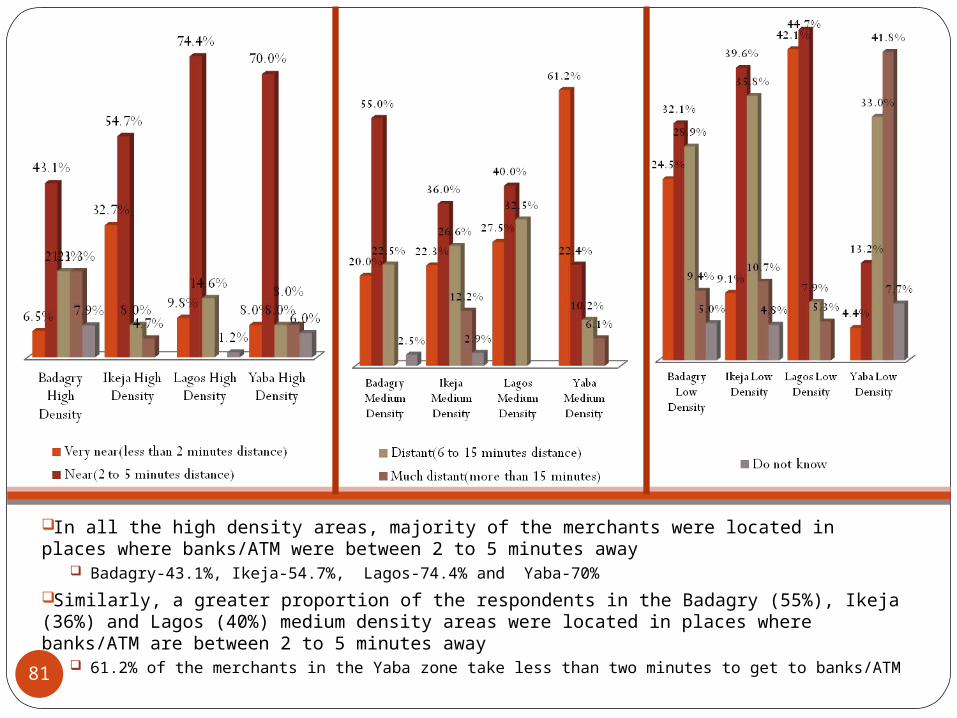

In all the high density areas, majority of the merchants were located in places where banks/ATM were between 2 to 5 minutes away

Badagry-43.1%, Ikeja-54.7%, Lagos-74.4% and Yaba-70%

Similarly, a greater proportion of the respondents in the Badagry (55%), Ikeja (36%) and Lagos (40%) medium density areas were located in places where banks/ATM are between 2 to 5 minutes away

61.2% of the merchants in the Yaba zone take less than two minutes to get to banks/ATM81

Accepted Means of Payment

82

Majority of the respondents in the high density areas accept cash

Badagry-97.4%, Ikeja-94.7%, Lagos-97.6% and Yaba-100%

Cheques were the second best accepted means of payment.

The distribution of the medium density areas was identical to the high density areas.

Majority of the respondents accept cash (Badagry-100%, Ikeja-96.8%), Lagos-100% and Yaba-98%) Cheques were the second best accepted means of payment.

In the low density areas, cash is also the favoured accepted means of payment (Badagry-96.5%, Ikeja-98.7%), Lagos-97.6% and Yaba-98.9%).

cheques were the second best in only Badagry (50.9%), Ikeja (28.1%) and Lagos (31.7%).

83

Why Merchants Discontinued Use of PoS

84

In the Yaba (66.7%), Badagry (54.2%) and Ikeja (73.1%) high density areas, the respondents discountinued use of the PoS due to;

Perceived difficulty in easy access to cash after sales customer’s insistence to use cash and technical malfunction

Equal percentage (66.7%) of respondents in the Lagos zone claimed that telecommunications and customer’s insistence to use cash were the factors that prevent them from having the PoS terminals.

85

Transaction fees and technical malfunction were the reasons most of the respondents discontinued the use of PoS terminals in the Ikeja (33.3%) and Yaba (50%) medium density areas.

In the low density areas of Ikeja and Badagry, 76.7% and 56.1% of the without PoS merchants said technical malfunction was the main impediment to the adoption of PoS terminals

In Lagos and Yaba, 40% and 77.6% chose ‘fear of fraud’ and ‘transaction fees’.

86

Cashless Policy Awareness and

Perception on PoS Usage

87

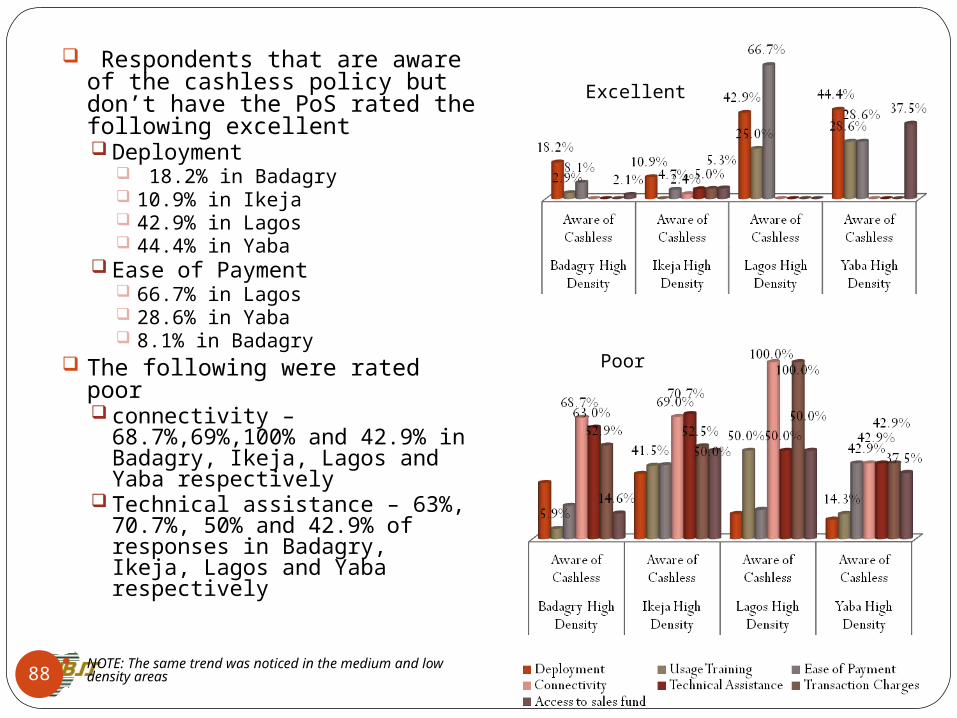

Respondents that are aware of the cashless policy but don’t have the PoS rated the following excellent Deployment

18.2% in Badagry 10.9% in Ikeja 42.9% in Lagos 44.4% in Yaba

Ease of Payment 66.7% in Lagos 28.6% in Yaba 8.1% in Badagry

The following were rated poor connectivity –

68.7%,69%,100% and 42.9% in Badagry, Ikeja, Lagos and Yaba respectively

Technical assistance – 63%, 70.7%, 50% and 42.9% of responses in Badagry, Ikeja, Lagos and Yaba respectively

NOTE: The same trend was noticed in the medium and low density areas

Excellent

Poor

88

Frequency of Usage

89

Frequency of Usage In all the high density area, cash was used many times a day

Lagos - 94.3% Ikeja - 96%Badagry- 68.3%Yaba - 88%

EFT was never used Cash was used many times a day in the medium density

areasLagos - 90.2% Ikeja - 96%Badagry - 91.3%Yaba - 97.8%Most respondents indicated that EFTs were never used by a large

percentageBadagry - 65% Ikeja - 48.1%Lagos - 47.5% %

Cheques were never used in the Yaba (54%) area Similar to the high density areas, cash was used many times

per day in the low density areas (Lagos- 60.4%, Ikeja-91.3%, Badagry-96.9%, and Yaba-90.8%) but electronic funds transfer was never used

90

End-Users

Survey Findings -Quantitative

91

Bank Proximity

92

Majority of the responses in the high density area showed that banks were within 6 to 15 minutes distance from their place of work

57.6%, 35.2%, 47.7% and 60.6% in Badagry, Ikeja, Lagos and Yaba respectively

A greater proportion of the respondents in the Lagos (60.6%) and Yaba (38.25%) medium density areas take about 6 to 15 mins to get to banks/ATMs while those in the Ikeja area take less than 5 minutes

Similar to the high density areas, banks are 6 to 15 minutes close to the respondents in the Ikeja (44.7%), Lagos (44.7%) and Yaba (48.8%) low density areasIn the Badagry it takes less than 2 minutes to get to banks/ATMs

93

Payment Frequency

94

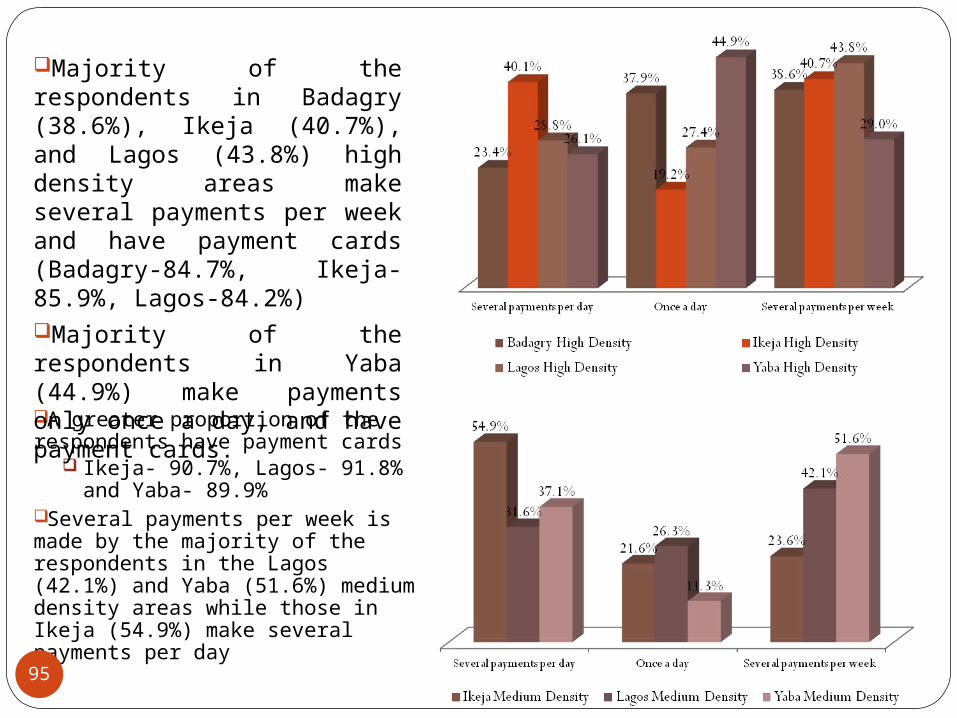

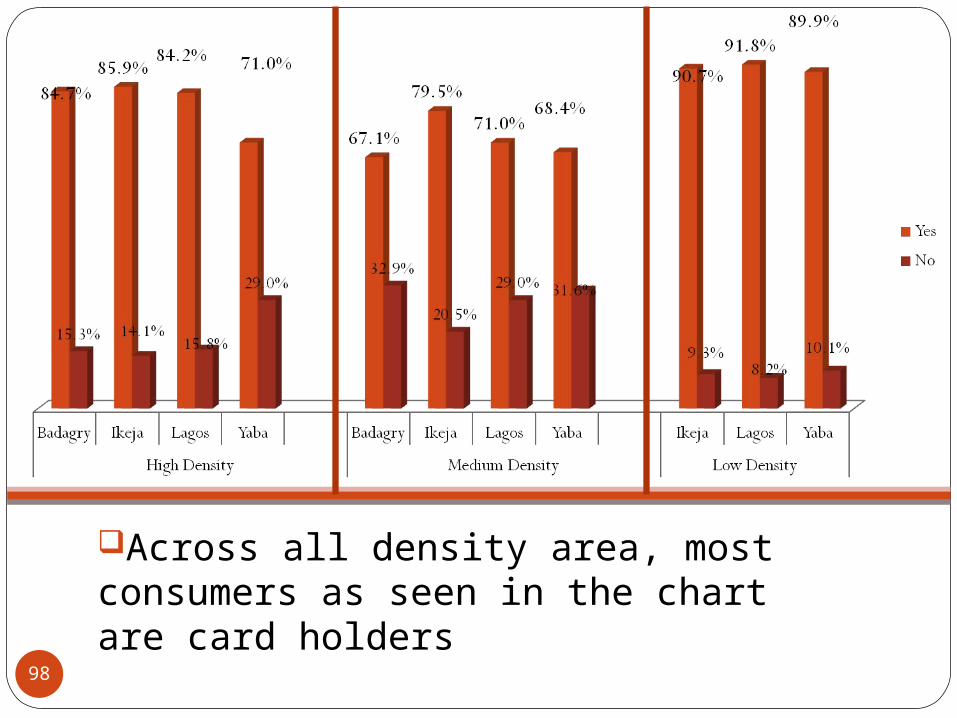

A greater proportion of the respondents have payment cards

Ikeja- 90.7%, Lagos- 91.8% and Yaba- 89.9%

Several payments per week is made by the majority of the respondents in the Lagos (42.1%) and Yaba (51.6%) medium density areas while those in Ikeja (54.9%) make several payments per day

Majority of the respondents in Badagry (38.6%), Ikeja (40.7%), and Lagos (43.8%) high density areas make several payments per week and have payment cards (Badagry-84.7%, Ikeja-85.9%, Lagos-84.2%)Majority of the respondents in Yaba (44.9%) make payments only once a day, and have payment cards.

95

In all the low density areas, most respondents make several payments per day

Badagry- 45.1% Ikeja- 51.3%Lagos- 47% Yaba- 41.3%96

Consumer with Payment Cards

97

Across all density area, most consumers as seen in the chart are card holders

98

Range of Cards Owned

99

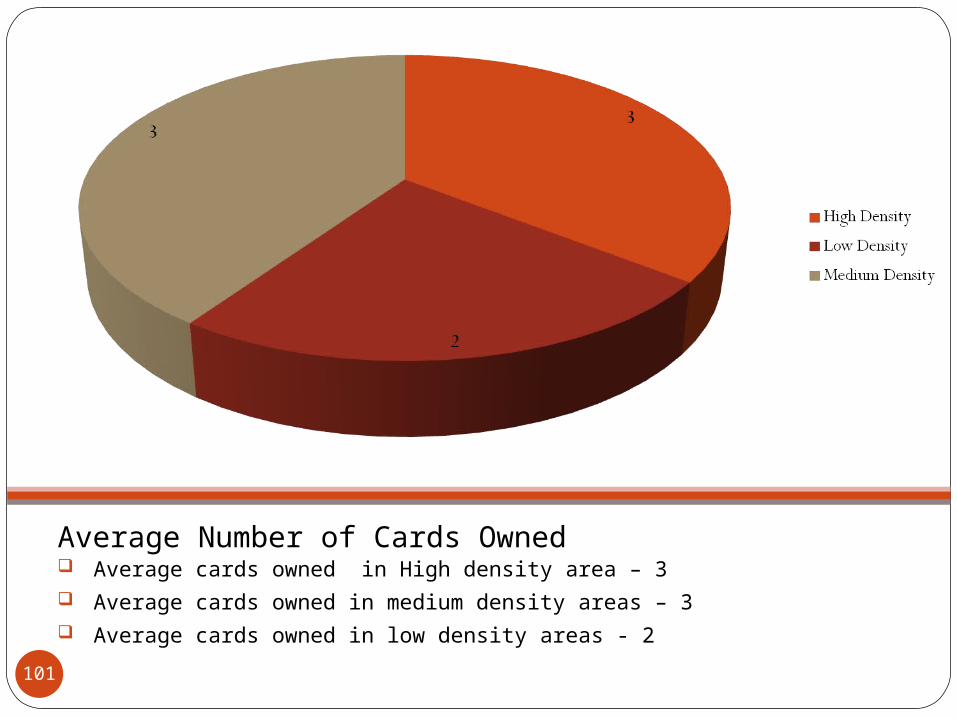

Given the range of cards owned (above) by consumers Average range of cards owned

In the high density area – 5 In medium density area – 3 In low density area – 3

100

Average Number of Cards Owned Average cards owned in High density area – 3 Average cards owned in medium density areas – 3 Average cards owned in low density areas - 2

101

Factors Likely to Encourage Consumers

102

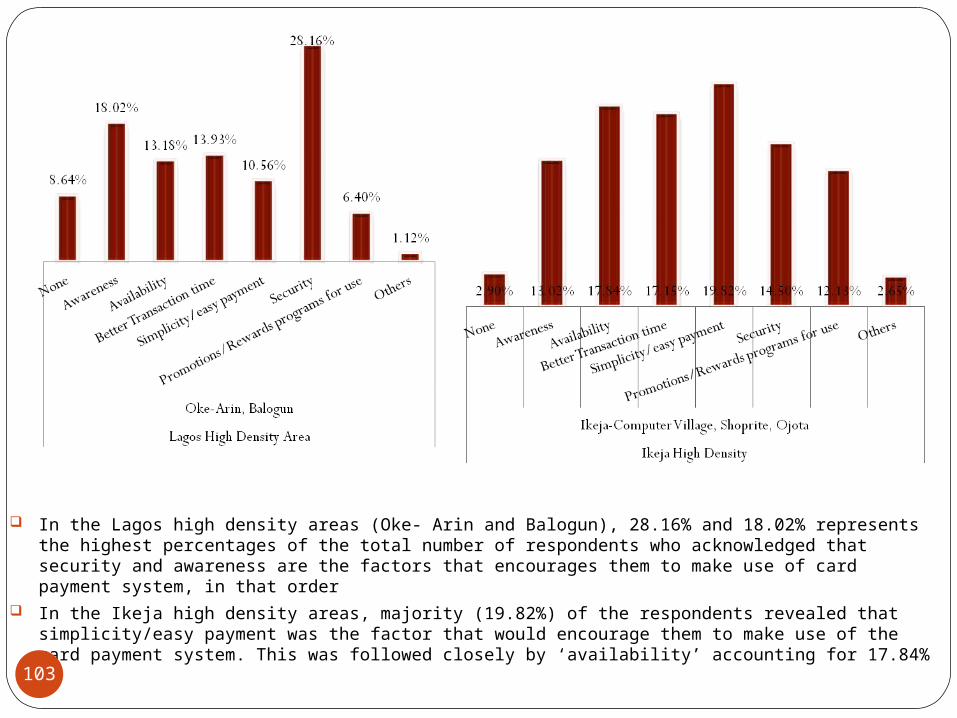

In the Lagos high density areas (Oke- Arin and Balogun), 28.16% and 18.02% represents the highest percentages of the total number of respondents who acknowledged that security and awareness are the factors that encourages them to make use of card payment system, in that order

In the Ikeja high density areas, majority (19.82%) of the respondents revealed that simplicity/easy payment was the factor that would encourage them to make use of the card payment system. This was followed closely by ‘availability’ accounting for 17.84%103

However in the Yaba high density areas, better transaction time was selected by a greater proportion (22.39%) of respondents, then availability accounts for 18.66%.

The Badagry high density area has a similar distribution to that of the Ikeja high density areas. The top two factors that encourage the use of the card payment system are simplicity/easy payment (22.28%) and availability (20.34%)104

In the Lagos medium density areas, the factors with the primary will encourage the use of the card payment system are promotions/rewards (20.57%), security (19.86%) and awareness (17.73%).

In the Ikeja areas, the distribution was as follows: security at 18.69%, and simplicity/easy payment at 18.07%.

In the Yaba area, 21.51% identified availability as the factor primary factor followed by security (20.35%), simplicity/ease of payment (19.77%) and better transaction time (18.02%).

105

In the Lagos medium density areas, the factors with the primary will encourage the use of the card payment system are promotions/rewards (20.57%), security (19.86%) and awareness (17.73%).

In the Ikeja areas, the distribution was as follows: security at 18.69%, and simplicity/easy payment at 18.07%.

In the Yaba area, 21.51% identified availability as the factor primary factor followed by security (20.35%), simplicity/ease of payment (19.77%) and better transaction time (18.02%).

106

Factors that Discourage Consumers

107

In all of the high density areas, majority of the respondents indicated that the non-connectivity of PoS terminals discourages them from using the terminalsLagos-19.39%Ikeja-23.59%Yaba-20.90%Badagry-24.22%.

The second highest selected by the various areas include: Fear of fraud- LagosDemand for cash- IkejaNon-availability of PoS at

merchant stores- Yaba PoS transaction charges-

Badagry.108

In the medium density areas, ‘terminals not connecting’ also ranks highest as the factor that discourages consumers from making use of PoS terminals Lagos-25% Ikeja-21.19% Yaba-27.81)

In the low density areas, respondents in the Lagos (25.04%) and Ikeja (22.22%) areas indicated ‘terminals not connecting’ as the factor that discourages them from using PoS terminals 38.81% of the respondents in the Badagry zone

reveal that the fear of fraud was the factor that discourages consumers from using PoS terminals

109

Locations Consumer Feel Comfortable Using Cards

110

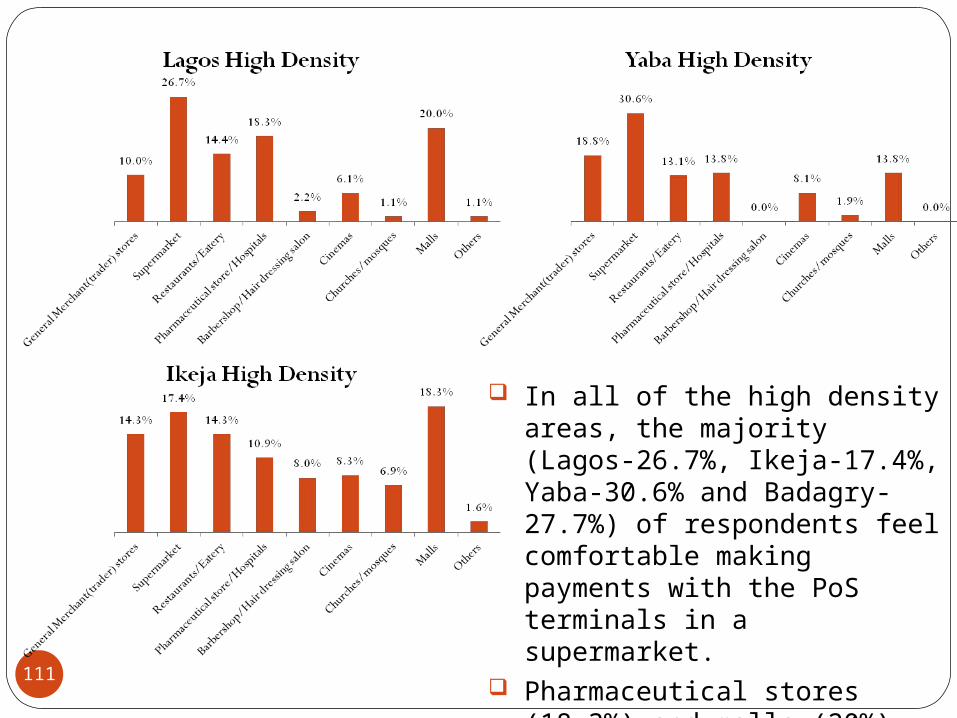

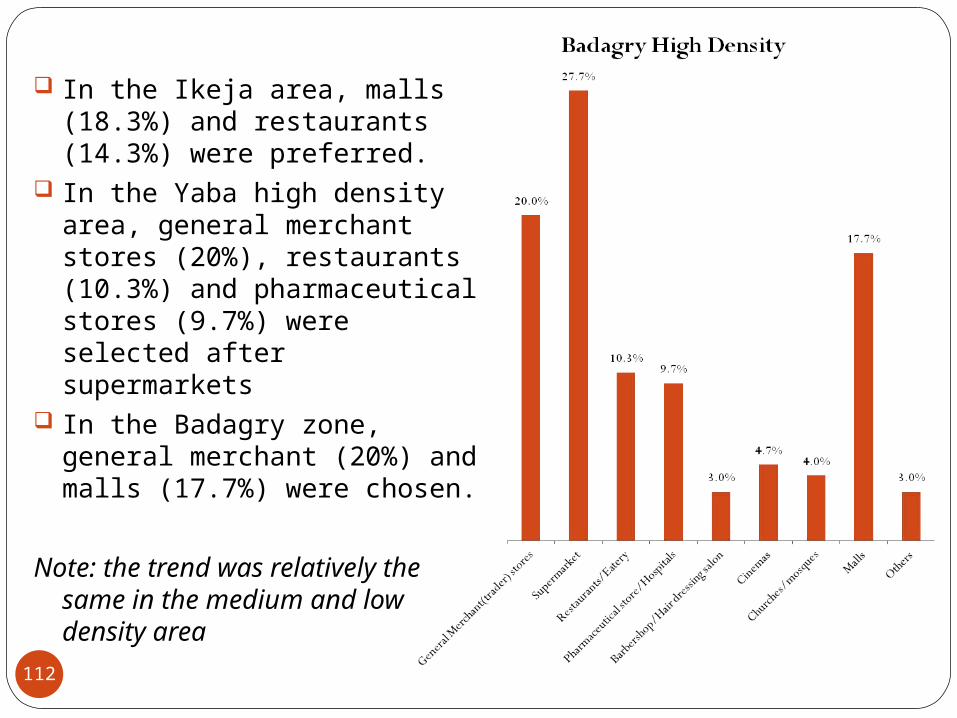

In all of the high density areas, the majority (Lagos-26.7%, Ikeja-17.4%, Yaba-30.6% and Badagry-27.7%) of respondents feel comfortable making payments with the PoS terminals in a supermarket.

Pharmaceutical stores (18.3%) and malls (20%) were preferred in the Lagos zone after supermarkets

111

In the Ikeja area, malls (18.3%) and restaurants (14.3%) were preferred.

In the Yaba high density area, general merchant stores (20%), restaurants (10.3%) and pharmaceutical stores (9.7%) were selected after supermarkets

In the Badagry zone, general merchant (20%) and malls (17.7%) were chosen.

Note: the trend was relatively the same in the medium and low density area

112

Customer’s Insistence for Card Usage And Merchant’s

Change of Position

113

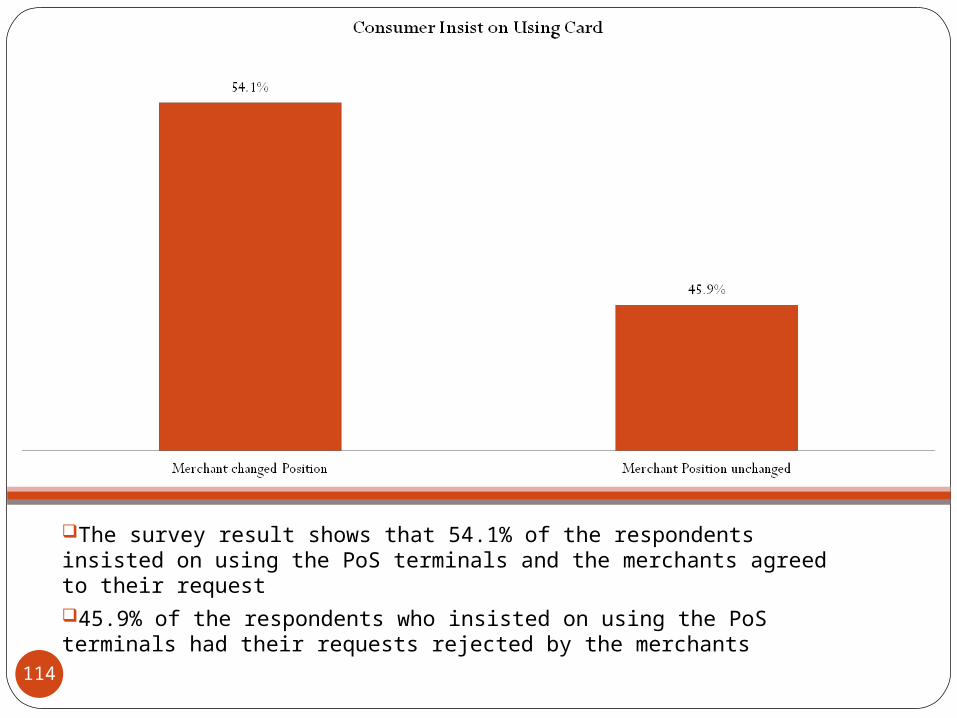

The survey result shows that 54.1% of the respondents insisted on using the PoS terminals and the merchants agreed to their request 45.9% of the respondents who insisted on using the PoS terminals had their requests rejected by the merchants

114

Conclusion

115

Conclusion

The potential for growth in the usage of PoS terminals in Lagos metropolis remains strong

With a population of over 16 million people, there are approximately 8 million card holders in Lagos state

Based on the aggregated data from the 6,776 survey sample, the study finds that:

116

ConclusionProfile of Merchants/End-Users

Most of the merchants with PoS terminals are general merchants or traders located mainly in open markets and neighborhood shops.

Over 60% of the stores and outlets are located less than 5 minutes walking distance from banks and ATMs

Though merchants accept cards and have PoS terminals for payment, the majority still prefer the cash payment method to other forms of payments (i.e. Checks, Cards and EFTs) and cash payment remains the most frequently used payment system

117

ConclusionWith regards to consumers, the majority were

fully employed and self employed Average income is between N20, 000 and

N100, 000 across the density areas (i.e. high, medium and low)

Banks and ATMs proximity to the consumer by walking is an average of 6 to 15 minutes from their place of work

Most consumers make several payments daily and weekly and prefer the cash payment option due to the challenges they often face when using PoS terminals

118

ConclusionMerchants without PoS terminals are also mostly

general merchants/traderslocated in open markets and shopping malls that

are within 2 to 5 minutes walking distance from banks and ATMs.

As expected the most preferred method of payment is cash and in some cases checks or bank drafts

Challenges / Perceived Obstacles to usage of PoS TerminalsTwo out of the three categories of respondents (i.e.

Merchants with PoS and Merchants without PoS terminals) identify basically the same challenges and perceived obstacles to the smooth operation of the PoS terminals

119

ConclusionThese obstacles are as follows according to priority:

Connectivity and network challenges24.5%

Transaction charges/charges to bank account18.9%

Consumers/merchants insistence to pay cash12.7%

Rejected transactions 11.8%Card reading/technical difficulties

11.3%Consumers/merchant lack of card/PoS 10.1%Access to after sales funds 6.6%Others 4.3%

Poor awareness of the PoS payment systems and benefitsLong transaction time/late transaction notification

120

ConclusionChallenges that deter consumers from making

use of the pos terminalsAccording to priority, factors that inhibit consumers’

usage of the card payment system include:Connection and network difficulties with the terminals Non-Availability of PoS terminals at merchants’

points/storesAttributed to the poor rate of deployment as

noticed by the merchants with PoSMerchants demand for cash

As a result of obstacles listed aboveLong transaction timeFear of fraud

Some consumers cited personal experiences of being debited twice

In some cases the terminals would reject the transaction, however the consumer receives a debit alert some hours after the unsuccessful transaction

121

RecommendationsAwareness Increased awareness of consumers will accelerate the adoption

of the PoS terminal and the card payment systemincluding the new electronic money and mobile payments

systems Collective efforts by all key stakeholders towards achieving

greater awareness via:Initial Stakeholder Road show across various key regionsPeriodic summits, workshops, seminars to enlighten and

keep targets informedMass media coverage via:

Print Media – billboards, newspapers, magazines, bulletins, publications

Digital Media – television, documentariesVoice Media – radio advertising, jingles in various local

languagesSocial Media – internet, web (facebook, twitter etc)Mobile/Vehicular Media – advertisements on mobile

vehicles122

Centralized Provider of PoS Terminals and Equipment

Maintaining a single or limited source of equipment manufacturers/type

This will simplify the deployment of PoS terminals and equipmentIt will also facilitate easy education for the

stakeholders (merchants, end-users and providers)

Recommendations

123

Improve Connectivity Our findings show that there is a low level of

coordination among banks, mobile operators, and existing payment networks

Inter-operability across provider solutions (mobile, financial institutions, networks) will be necessary to drive mass market adoption.

We suggest that NIBSS/CBN partner with mobile network operatorsCollaboration between the key regulators and mobile

network operators will bring about efficiencies in processes quick identification and resolution to network and

connectivity issues thus enhancing the merchants, end-users improved PoS

experience resulting in increased PoS adoption

Recommendations

124

Incentives In many new programs, incentives have played a major

role in attracting customersOur findings show that merchants and end-users across

the density areas are willing to adopt PoS usage irrespective of any incentive program

Despite these findings, incentives are suitable at this stage in order to encourage people and impress upon them the seriousness of implementing the cashless policy

We suggest that several promotions be put underway such as the ‘cash back’ promo as already adopted by GTBank

Suggested incentives for merchants and end-users include:Cash-Back PromotionsReward PromotionsLoyalty RewardsRaffle PromotionsCoupon/Discount Promotions

Recommendations

125

Pricing StrategyStakeholders must develop a pricing strategy

that promotes and encourages PoS adoptionCharges on provision of an electronic payment

system by a merchant should be similar and at a fair cost

The policy objectives must factor in the affordability for merchant and end-user access and adoption Some merchants in certain locations are price-

sensitive

Recommendations

126

Safety and Security of InformationMerchants and customers recognize the importance

of safety and security of information There is need for secure transaction platforms and

security of information cannot be compromisedCases of fraud or lapses in the system can have the

potential to undermine confidence in the use of the systemwhich will ultimately impact public perception.

Safeguarding transactions and client information is an imperative as a high level of security is requiredFraud prevention is required to encourage acceptance

and adoption of the electronic payment systems

Recommendations

127

Mobile Money is the Game ChangerMobile phone technology has reduced

communication costs in Nigeria to very low levelsThis transformation has increased teledensity

significantlyHowever, telco's are not allowed to lead

cashless policy implementationsThe high level of specification in roles and

responsibilities will limit innovation by banks, telco's and payment companies

Inter-operability across provider solutions (mobile, financial institutions, networks) will be necessary to drive mass market adoption

Recommendations

128

Next Steps

129

Next StepsWe suggest a follow-up integration survey in Lagos

State most importantly in the areas not covered by this surveyThis will help to further identify other cultural and

fundamental barriers to the adoption of the PoS Terminals

Popularisation of NIBSS role as PoS Terminal certification agency and regular spot checks of PoS Terminals in use at merchant points

There is need for a pilot survey in other key cities where the Cash-less policy will be introduced before implementation This will help to identify the necessary pre-

implementation steps to be taken; identify the trend and compare results with the Lagos density areas

This will help underscore the model to be adopted for each of the new locations

130

Thank You

131